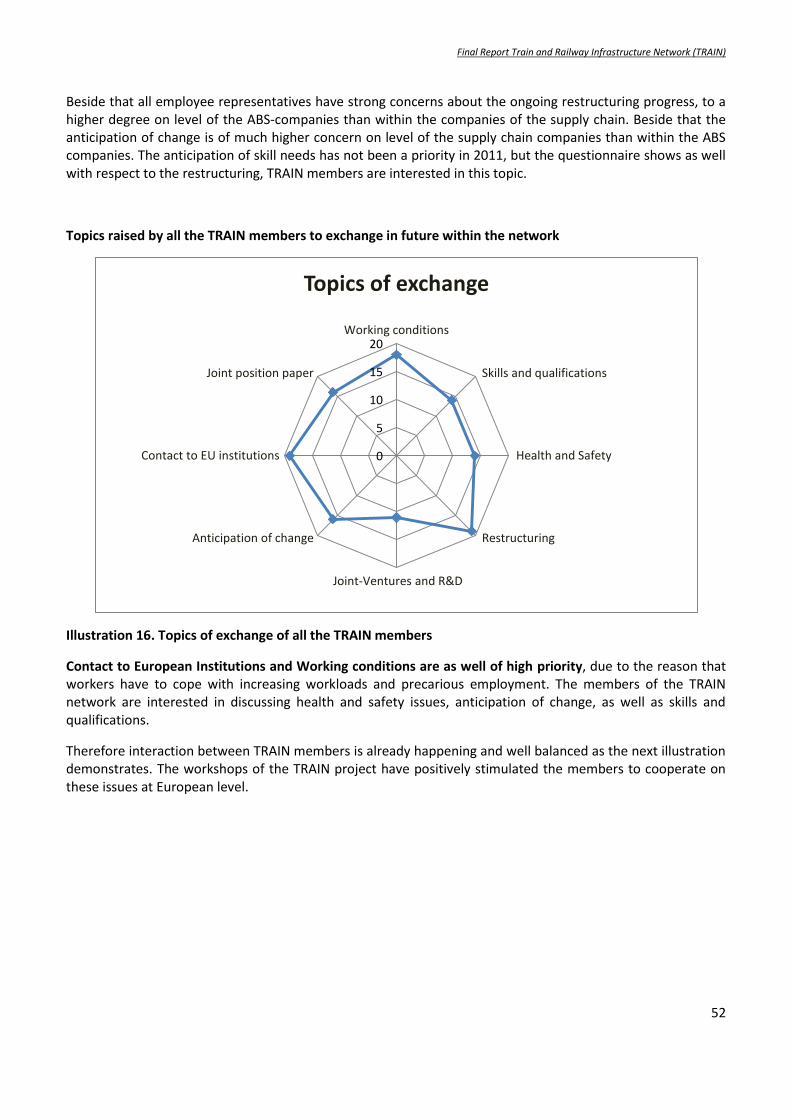

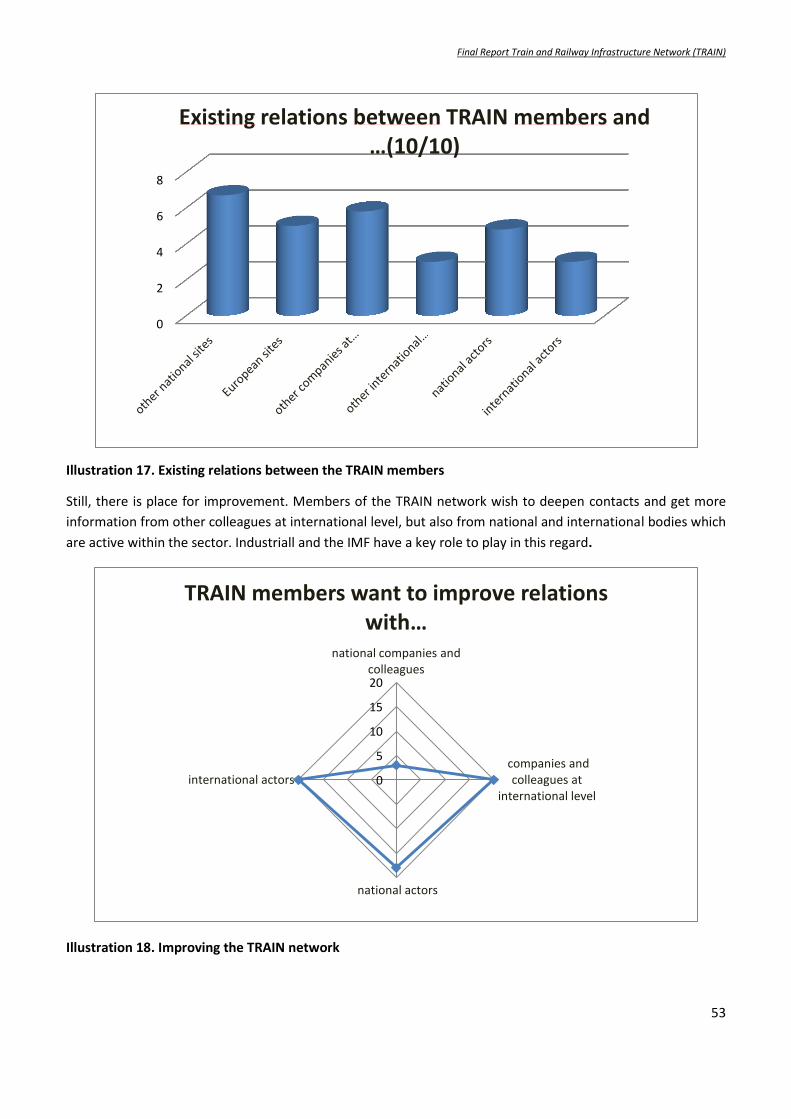

« Lesson learned? Challenges due to the transformation of the train and railway infrastructure towards a sustainable European

transport system»

Research funded under the European Budgetline

04 03 03 03

Authors:

Pierre-Yves Bour

Jean-Jacques Paris

Nicolas Rode

Winfried Wolf

This report was carried out with the financial support of the European Commission

Final Report Train and Railway Infrastructure Network (TRAIN)

2

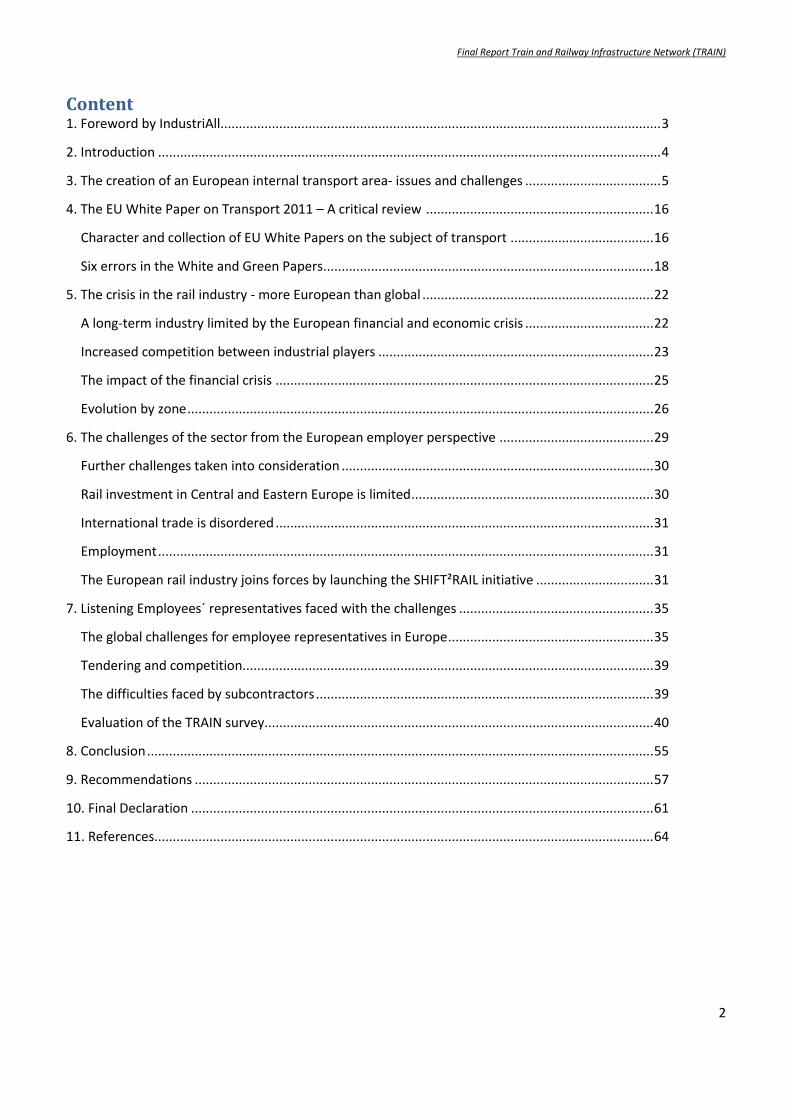

Content 1. Foreword by IndustriAll........................................................................................................................ 3

2. Introduction ......................................................................................................................................... 4

3. The creation of an European internal transport area- issues and challenges ..................................... 5

4. The EU White Paper on Transport 2011 – A critical review .............................................................. 16

Character and collection of EU White Papers on the subject of transport ....................................... 16

Six errors in the White and Green Papers .......................................................................................... 18

5. The crisis in the rail industry - more European than global ............................................................... 22

A long-term industry limited by the European financial and economic crisis ................................... 22

Increased competition between industrial players ........................................................................... 23

The impact of the financial crisis ....................................................................................................... 25

Evolution by zone ............................................................................................................................... 26

6. The challenges of the sector from the European employer perspective .......................................... 29

Further challenges taken into consideration ..................................................................................... 30

Rail investment in Central and Eastern Europe is limited .................................................................. 30

International trade is disordered ....................................................................................................... 31

Employment ....................................................................................................................................... 31

The European rail industry joins forces by launching the SHIFT²RAIL initiative ................................ 31

7. Listening Employees´ representatives faced with the challenges ..................................................... 35

The global challenges for employee representatives in Europe ........................................................ 35

Tendering and competition................................................................................................................ 39

The difficulties faced by subcontractors ............................................................................................ 39

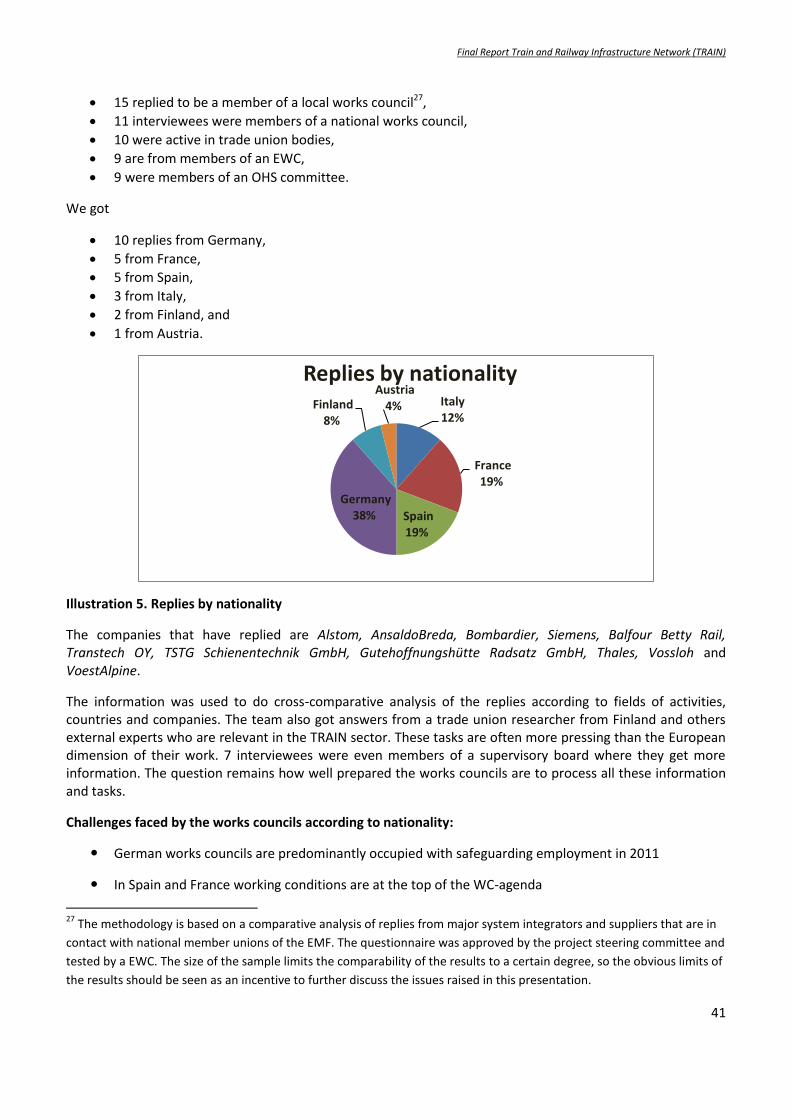

Evaluation of the TRAIN survey.......................................................................................................... 40

8. Conclusion .......................................................................................................................................... 55

9. Recommendations ............................................................................................................................. 57

10. Final Declaration .............................................................................................................................. 61

11. References........................................................................................................................................ 64

Final Report Train and Railway Infrastructure Network (TRAIN)

3

1. Foreword by IndustriAll – European Trade Union

In the series of sector projects initiated by the former EMF within the larger Mechanical Engineering sector, I now have the

pleasure to present the outcome of one year of activity in connection with the railway equipment sector.

Initiated by our previous organisation, the EMF, it is part of its heritage. Even though the railway equipment sector is very

much centred on metalworking activities, the advantages of now having one single European trade union federation covering

“all of industry” is starting to pay off.

Especially when facing our partners in Brussels - be it the industrial associations or the European institutions - there is just

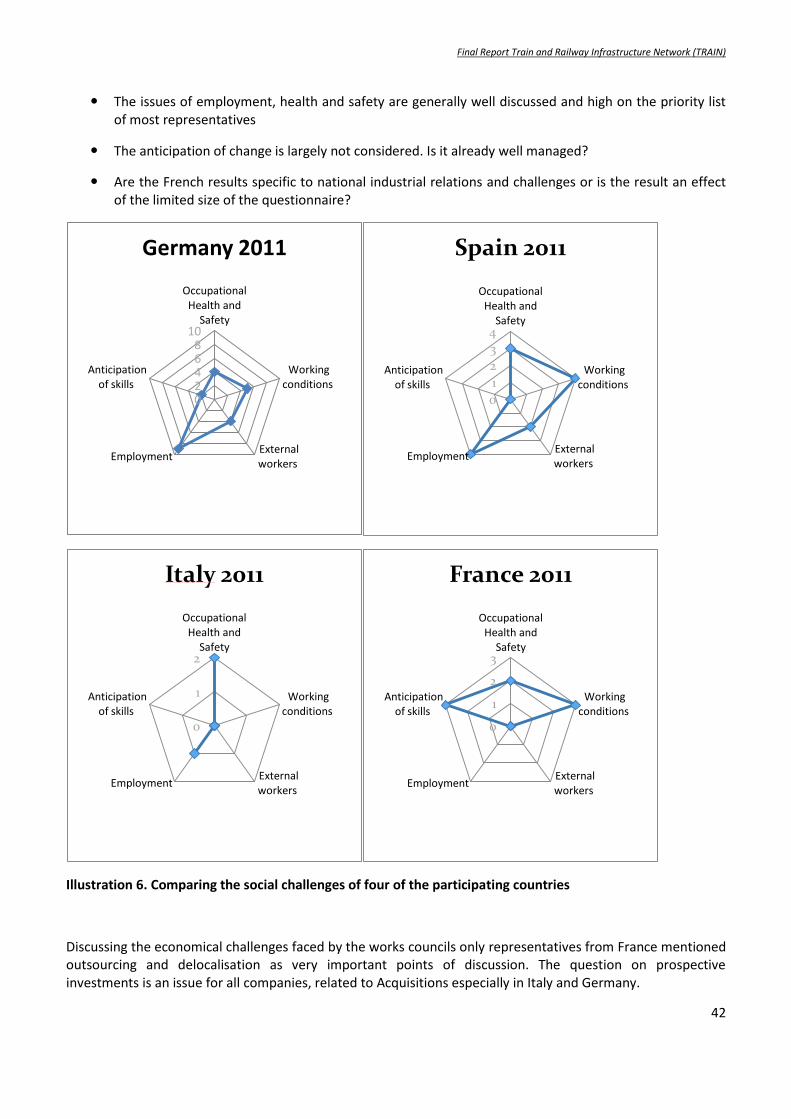

one interlocutor for manufacturing industry. This was felt in particular in relation to the debate on transport and mobility

issues. With the exception of service activities - covered by our sister organization ETF - the entire value and supply chain is

now represented by industriAll Europe.

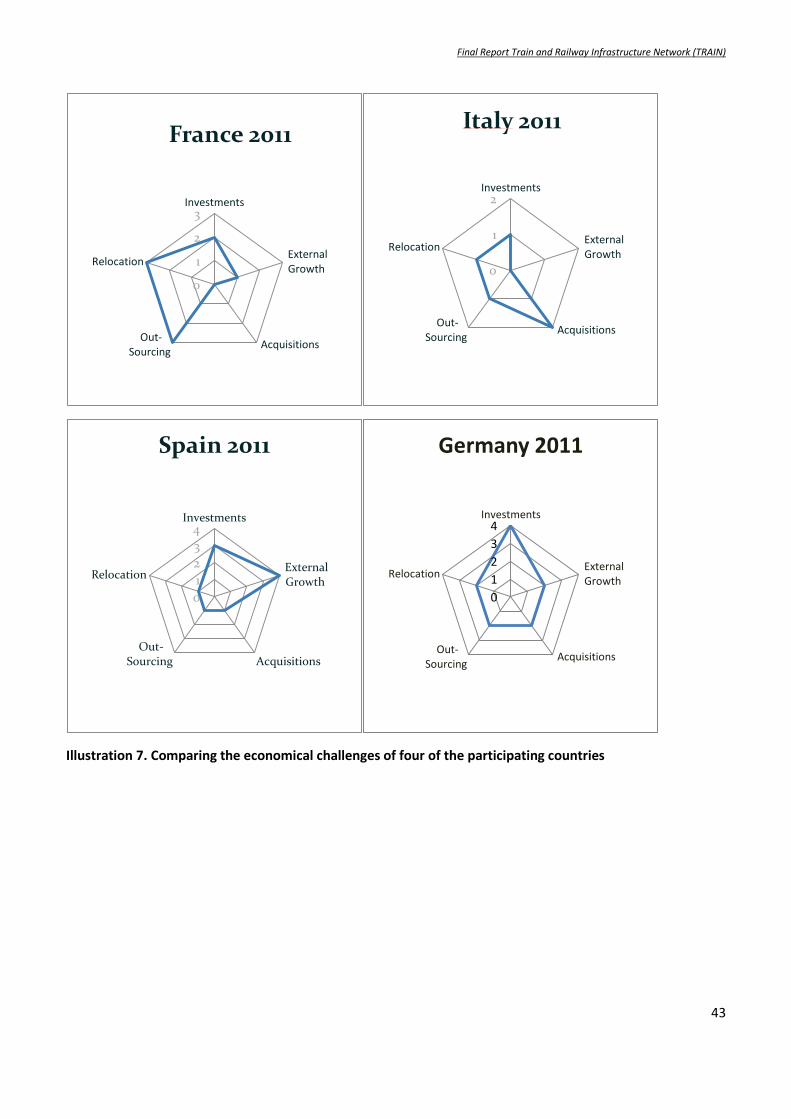

Much of the debate during this project dealt with the issues of transport and mobility policies and we in fact entered into an

intensive exchange of views and cooperation with ETF on this topic. We must not neglect the aspect of the way the material

“we” produce is actually used – which in the present sector is a rather long life-time (30 years) - but also not neglect the fact

that he railway equipment built in our sector becomes the workplace of transport workers. Therefore we need to discuss the

issues surrounding the health and safety and working conditions for service staff. We look forward to continuing this

cooperation.

The issues on mobility showed that regrouping the sectors directly involved (automotive, aerospace and shipbuilding) with

the present sector clearly demonstrated that there are some common interests but diverging views as well. As a result of the

discussions organised within the framework of this project, industriAll Europe is now holding a debate with all the sectors

concerned about a coherent approach to mobility and transport policies. We intend to feed the output back into the EU

Commission policies where manufacturing aspects are almost entirely absent in this context.

The other outcome of this project is that we need to pay more attention to public procurement questions. The lowering of

public budgets certainly does have an impact on the order books of railway equipment manufacturers in Europe. And public

calls for tender too often focus on simply the cost of purchase. This has consequences for the users of the equipment -

transport workers among others - but also on manufacturing in Europe and, in the longer term, on the image and the

attractiveness of the European railway transport offer of services.

Obviously, from a trade union perspective, one cannot limit oneself to a sectoral approach alone, but we will develop

cooperation with other European federations to make sure we cover all aspects of our members’ needs, and that we do so in

a coherent manner.

If there was any need to prove this requirement, then this project certainly delivered it very convincingly.

As a “young” European trade union federation, we are looking forward to taking part in this debate.

Ulrich Eckelmann,

General Secretary, industriAll – European Trade Union

Final Report Train and Railway Infrastructure Network (TRAIN)

4

2. Introduction

The European rail industry, where direct employment accounts for around 400.000 jobs1, is of structural importance. But it is time to discuss the issue of industrial change in the European train and railway sector for several reasons. On the one hand, train and railway production is hardly hit by the ongoing financial and economic crisis in terms of production and employment. On the other hand the sector is crucial in terms of employment (1), sustainability (2) and industrial competitiveness (3) on European level. In fact IndustriAll - the European Trade Union - argues that it represents an often underestimated key sector for the sustainable industrial development of Europe and is as well crucial to reach the important climate policy objectives in combination with the requirements on mobility of European citizens and the economy.

This report reflects on and takes into account the discussions and results of three workshops and the final conference organized by IndustriAll in 2011/2012.2 First this report deals with the ambitions of the European Commission to establish the “European Internal Transport Area” in order to set this project and report into a larger context. Second Mr. Winfried Wolf discusses critically the current EU white paper and we will analyse the impact of the crisis on the rail industry. In a third step, the perspective of the employers will be discussed and afterwards the challenges and positions of the employee representatives (being part of this project) will be analysed. Over the project period of one year the employee representatives explored their challenges within the workshops and specific country reports and within an anonymous survey consultingeuropa realized during the running time of the project.

1 According to information presented by UNIFE - This amount does not include employment within the value chain.

2 These events took place on the 30

rd of November 2011, 12

th of January 2012, 29

th of March and 5

th / 6

th November 2012 in Brussels

Final Report Train and Railway Infrastructure Network (TRAIN)

5

3. The creation of an European internal transport area- issues and challenges

Unlike many other markets the rail industry has to deal with some specifics. On the one hand, the rail industry

depends massively on public (transport) expenses, and thus of political

decisions from. Secondly, the industry has been linked with a European and national decision-making

processes. Due to the introduced and/or realized privatization and liberalization processes on the traditional

track market the whole sector is affected by an enlarged and serious competition.

Over the last years the idea to have an internal European rail market served by European operators, which

would trigger new innovation and employment, has been a main driving force. The European commission has

accelerated this process with mixed results. The history of this process is relevant for a better understanding

on the context of the current white paper and the overall perspective of the rail industry which will be

discussed in the following chapters.

Opening for competition – the different models

The liberalization of the rail way market can occur in two ways, which do not exclude each other. What is

meant by that?

The competition of the market:

The track network is completely open to competition: Several companies (the national operators and other

newcomers) have a right of access to this network (for example routes), similar to the competition in the air,

where companies have a specific time frame assigned to routes. The competition is transparent and visible to

the consumer who has to choose between different providers. This type of competition could be considered

for profitable business (international freight transport by rail – coastal sea shipping – transport of freight

national - international passenger carriage).

The competition for the market:

Competition for the market is a different model, which refers to activities that require public funding. In this

case, an announcement on competition (a tender) is published in order to contract a rail service company with

a market or a special segment of it; if the market is gained, the company operates in the services alone. This

construct refers to patterns of franchise or concession types (British model) or the delegation of public

Final Report Train and Railway Infrastructure Network (TRAIN)

6

services. The competent and decision taking authority (a state or region) is launching a tender for a specific

scope of work and searches a rail operator.

The Europeanization of the railway transport: The European Commission and the public transport policy play a large role regarding the perspective

development of the rail industry: Different approaches and levels of intervention can be identified.

The three most important intervention levels of the European Commission:

1. Creation of an «internal rail market»

The terms «Opening for competitors» and «Liberalization» refer to the same thought; the goal is to provide

free access for new players to the national rail markets in order to create a common European internal

transport area. Barely being put into words, this goal faces two limiting factors. First, each state has

implemented its own railway system over a long period of time. Second, the rail companies/providers have

inserted their own technical and operational standards in accordance with the national railway systems. Due

to these more or less historical facts, there are a multitude of different, co-existing railway systems, which all

represent an obstacle to the process of liberalization (for example with regard to interoperability). The

liberalization requires a loosening up of national rail regulation and authority, hence the regulatory

intervention at the European level.

2. Interoperability and safety

The compatibility of the infrastructure (material, signals and other systems) and the implementation of less

complex procedures for the approval of authorizations (e.g. on the rolling stock) are essential for an effective

liberalization. The European Railway Agency was set up to help create this integrated railway area. The Agency

has the task to make progress on the harmonizing of the technical standards and to improve the

«interoperability» inside Europe.

The assessment of the role of the agency, which was conducted in April 2011 on the request of the

Commission, however, shows that this role could be stronger and developed further on. Therefore the agency

should improve their strategic initiatives with regard to innovations in the key areas of expertise

(interoperability and safety)

3. The development of the infrastructures

82 billion euro of the structural and cohesion fund of the European Union (23,8 % of the total volume) are

devoted to transportation and its infrastructure (23.6 billion to transportation by rail). Neighbour countries

and aspiring EU-members can benefit from the “Instrument for Pre-accession Assistance” (IAP) and the

Final Report Train and Railway Infrastructure Network (TRAIN)

7

European Neighbourhood and Partnership instrument (ENPI) in order to extend and modernize their rail

infrastructure.

According to the European Commission, the creation of such a «financial background » should force the

competent authorities to adjust to the long-term investment strategies, by encouraging in particular the

railway companies to invest in new, secure, interoperable and environmentally friendly technologies.

Over the past 20 years the European Community has been engaged in restructuring the European rail

transport market and promoting the growth of rail transport by stimulating «Liberalization»

Several documents have been signed in order to promote the liberalization of rail way services.

1. The integration agreement - the single act of 1986-1987: does not decide the allocation between

competing actors and non-profit services, but promotes the emergence of an area of competition.

2. The foundations:

- The White Book of the 30th of July in 1996: «Strategy for revitalizing the collective rail

companies/providers», since been supplemented by

– The White Book of 2001: «The European transport policy in 2010: time to decide»

– and the one of 2011: «Strategic plan for a single European transport area - The Way towards

a competitive and resource-efficient transport system»

3. The founding text: The directive 91/440 (29th of July in 1991) sets out a framework and requirements

for railways in the EU to allow open access operations on railway lines by companies beside those one

that own the rail infrastructure. Especially its article 20 is important to notice. The Article 20 of the

directive 91/440 of the 29th of July in 1991 elaborates the principle of a «right of access to the rail

network». It is the logical consequence of the separation of rail network and operator: «The train/rail

way is like a one-lane motorway, steered by a flight controller…» The legislation was extended by

further directives to include cross border transit of freight. The subsequent directives 2001/12/EC,

2001/13/EC and 2001/14/EC which built upon the initial legislation are collectively known as the First

Railway Package. (See the next page)

First rail way package (presented in 1998, passed in 2001):

- Creating of the opening of the market of the international rail way services (step by step: 2003

opening of the Trans-European Network and 2008 opening of the whole network);

- Independence of the main functions of the administrator of the infrastructure towards the state

- Regulation of the rate making and the allocation of the railway lines (transparency, without

discrimination, etc.…)

Final Report Train and Railway Infrastructure Network (TRAIN)

8

Member States under the control of the Commission and the EU Court of Justice

1. First rail way package Different countries implemented the package to different extents and at different paces. By 2004 some

countries such as the United Kingdom had gone far beyond the original remit privatizing the entire railway

system, others such as Finland and France had created fully separate infrastructure and railway companies

from the state run enterprises, whilst others such as Germany had created separate subsidiaries for different

service providers and a subsidiaries for infrastructure and track (DB Netz), others merely separated accounting

between the two organizational sections. In general, most countries in the EU still have a state owned

infrastructure company, but many have privatized parts or all of their service providers others are still working

towards privatization.

According to the European Commission the implementation of the package was not completed. The EC started

violation procedures against 13 member states: Austria, Czech Republic, Germany, France, Hungary, Italy,

Ireland, Luxembourg, Poland, Portugal, Slovenia and Spain. The main complaints concern the lack of

Third rail way package (presented in 2004, passed in 2007):

- Creating of the opening of the market for international passenger carriage including coastal

shipping from 2010;

- Certification of engine drivers and trains, which are envisaged to carry passengers/goods;

- Elaboration of a directive towards the rights and duties of rail passengers;

- Proposal of a directive towards the quality of rail freight traffic services

Second rail way package (presented in 2002, passed in 2004):

- Safety of the rail traffic: Clarification of the responsibilities, determining of common goals,

indicators, etc.

- Replenishment of the fundamental principles of the interoperability Founding of an efficient

control tool: The European Railway Agency

- Expansion and acceleration of the opening of the international rail freight traffic throughout the

whole network in 2006 and opening for the total freight transport in 2007

Final Report Train and Railway Infrastructure Network (TRAIN)

9

independence of the functions of the infrastructure administration and the lack of an independent regulatory

authority.

2. Second rail way package

The Second Railway Package is a group of European Union legislation initiatives which promote common

standards and open access to the systems, working towards an integrated European railway area.

The second package (Regulation 881/2004) created the European Railway Agency, to coordinate safety and

interoperability efforts - seated in Valenciennes (France) - which has been given the task of harmonizing the

European networks and the European materials in technical manner. One of its most important tasks is to

enforce the safety of the rail transport and the interoperability, especially through the elaboration of common

technical standards for the interoperability (TSIs) and common safety procedures (CSIs).

3. Third package (liberalization of the passenger carriage):

Following on from the second railway package, the main act of the third railway package was to open access

for all international passenger services, including cabotage, across the railways of the EU. However, there were

also reforms to rail passengers' rights (including a minimum level of compensation for delays); this applies to

both international and domestic rail travel, but national governments can exempt some domestic services

from this in the medium term and harmonization of train driver licenses

The directive 2007/58/CE ought to be transmitted to all member states. Nevertheless the EC started violation

procedures against four member states (Luxembourg, Denmark, Lithuania and the Netherlands), which had

not transmitted the directive into national law, at the 24th of June in 2010. At the same time elements of the

directive 2007/59/CEE ought to be transmitted until the third of December in 2009. At the 24th of June 2010

the EC took actions against 19 member states (among them France, Germany, Belgium, the Netherlands and

Spain).

Taken into account the duties of public services and transport

The regulation 1370/2007, adopted by the European Parliament and the European Council on the 23th of

October in 2007, concerns public services in context of carrying passengers by train and on the street (named

«OSP regulation» - duty of public services. It provides a framework for the competition in the sector of public

transport services, which balance cannot be guaranteed without public support (so called services providing

collective economic interests)

– Duty to settle contracts of the public service for services to the travelling public

– Possibility to create more competition on notice of public service contract awards but under certain

conditions, the award of contracts on the basis of mutual agreement is authorized.

Final Report Train and Railway Infrastructure Network (TRAIN)

10

This regulation underlines that Services of General Economic Interests (SGEI) must be in accordance with the

EU Treaty. It is based on the assumption that «the creation of a regulated competition among the providers of

services leads onto more attractive, more innovative and more reasonable services».

But it also concedes, that «national departments are allowed to offer transport services themselves and to

allocate these services to an internal service provider without previous competition».

The Protocol no. 26 of the Lisbon Treaty on “Services of General Interest” clearly states the importance of such

services and underlines the essential role of the national, regional and local level to provide Services of

General Economic interest. The division between Services of General Economic Interest (SGEI) and Services of

General Interest (SGI) is a reading grid applies to all sectors. Social services are no exception. The dividing line

is not between social and non-social, but between services of general economic interest or non-economic. So

there are social services of general economic interest and social services of non-economic interest. Some are

subject to the rules of the competition, others not. The distinction requires a case-by-case basis and may leave

room for doubt, a "gray area”.

Assessment by the EU-Com remains mixed

It can be considered that the Commission does not wish to jeopardize its political offensive regarding

Liberalization. It nevertheless can be wondered about the role of the European Railway Agency (ERA), which

according to its assessment lacks up to now of strategic initiatives for innovation in these key areas of

expertise (interoperability and security). In terms of governance system, the Commission acknowledges that

the question of the management, maintenance or renewal of infrastructure remains central, the case of the

UK where the private group “Railtrack” took the responsibility for infrastructure and railways it is subjected to

critical analysis. (Based on consequences we know: A deterioration of the infrastructure, before the state

intervenes to regain control of the system)3

But evolutions are slow and still leave room for many questions regarding the financing of the railway system

and its consequences:

What is the trade-off between investment in infrastructure, price of train paths and offers? Members of the European Parliament already demanded the establishment of a multiannual scheme investment

The issue of equalization of funding between services with higher attendance and lower attendance services

Funding models (and use) of rolling stock

The entry of "low cost" Operators and consequences on employment, security etc.

Social questions remain acute

3 Railtrack Group plc was renamed by RT Group plc and was dissolved on 22 June 2010

Final Report Train and Railway Infrastructure Network (TRAIN)

11

The Commission’s views about the positive impact of liberalization and the promotion of employment in

railways does not take into account a number of social issues related to the prospective development of the

sector. Especially the European Transport Workers´ Federation (ETF) is in charge of those questions and issues

to improve the working conditions for the railway workers across Europe.4

In fact, the future of the social status of employees is at the center of concerns and up to now there already

exist ideas and initiatives, e.g. the development of a European collective agreement for workers in the rail

sector could be considered. This could strengthen the recognition of specific professions in the sector and

anticipate evolutions of jobs and skills with the aim of ensuring a strong and sustainable rail sector.

These developments, which are currently under way, necessitate solid European standards for working

conditions and closer cooperation of trade unions on cross-border working conditions and collective

bargaining issues.

Good initiatives from ETF evaluate the impact of ERTMS deployment on employment and working conditions.

ERTMS is a new train signaling and traffic management system created to gain interoperability by using a

unique signaling and communication standard throughout Europe.

4 Sabine Trier presented and discussed the initiatives on behalf of the ETF to improve the working conditions at the final

conference of the TRAIN-project.

Final Report Train and Railway Infrastructure Network (TRAIN)

12

The ETF strictly rejects any further liberalization of rail passenger transport and has developed a position paper

ETF Position Paper on rail passenger transport in Europe - Save public services

- no further liberalization (Brussels, 17 November 2010)

The ETF calls on the European Parliament, the Council of Ministers and the European Commission:

1) Immediately take appropriate action at EU level to take care that the increasing competition is

not played at the expense of workers. From the perspective of the ETF, this implies for the rail

sector:

protection against wage and social dumping through the strengthening of regulation 1370/2007 on the European level, in which the requirements of social standards and workers’ protection for the award of public transport service contracts by rail and road are made mandatory; • certification of on-board personnel / conductors in rail passenger transport; • Recording of the “ILO Convention No. 94 on Labour Clauses” in the contracts concluded by the authorities as a criterion for determining the traffic volume in the domestic or international passenger services under Directive 2007/58/EGB.

2) Strengthen public services or services of general (economic) interests at EU level as a necessary

consequence of the financial and economic crisis. From the perspective of the ETF, this mainly

means in the rail sector:

to prevent the liberalization of rail passenger traffic, which threatens the service security of people and job security for workers,

avoid a competition in rail passenger transport, which privatizes profits and socializes losses;

the requirement of strong investment in rail infrastructure under state responsibility and public service obligations, no private public partnerships or sold off;

prevent the formation of European private transport oligopolies, which can mean the loss of democratic control.

3) Give a higher priority to the concept of "sustainability" in the face of the challenges in the

transport by the threat of climate change and resource scarcity, by appropriate measures at EU

level.

Principle political reasons:

At least since the outbreak and consequences of the current financial and economic crisis, we know

that a "business as usual" means a "long wave" of further economic, ecological and social crises for

our community.

It also hit the railway sector strongly and put many jobs in danger. The under investment in the

railway sector in the rail sector continues even more severe due to the public deficits and endangers

not only work places but as well the service levels for European citizens in passenger transport. The

now following widespread austerity policies of European countries is a threat for the quantity and

quality of public services, including rail passenger transport services and for employment.

Final Report Train and Railway Infrastructure Network (TRAIN)

13

For the background of this economic crisis and its causes it is inexplicable for the ETF, how the

European Commission and the European legislators can continue pursuing a liberalization policy -

and in particular a policy without social guarantees. With such a policy they would set in danger the

service provision for European citizens and thousands of work places.

Rail passenger transport as part of public transport is a public service that guarantees mobility for

European citizens. This is valid for short distance regional and sub-urban rail passenger transport,

for people commuting to work or going to the theatre, shopping etc in the nearby centre. It is also

valid for long distance rail passenger transport for people visiting friends or relatives living in other

parts of the country. EU citizens need public transport and in particular rail transport, which still is

the most environmentally friendly form of passenger transport.

A well integrated railway system, which guarantees mobility for all citizens and not only of those

living in big cities and economic centre, is a combination of profitable and unprofitable lines. State

financing of the infrastructure and state financing of public passenger transport is therefore

indispensable for ensuring mobility for all its citizens. Hundreds of thousands of railway workers are

working in the sector in order to provide these services.

The effects of open access competition:

As already said, a good integrated rail network that provides mobility to the whole population and

not only to those who live in the big cities and economic centre, is a combination of profitable and

non-profitable lines.

Open access competition will lead automatically to a situation in which profitable lines will be

served while non-profitable lines will be closed down. A cross financing between profitable and non-

profitable lines in order to provide a larger service to the public is not possible any more in an open

access competition environment. Even more, competition on profitable lines between two or

several companies can result in total closing down of the line because, due to the high costs of rail

services, none of the competitors would make its profit any more.

In such an open access scenario, Member States have to ensure the mobility needs of people by

enlarging the services that are considered as “PSO services” and so compensated by the state. In

this case the state has to pay more “PSOs” while on the profitable lines private companies would

absorb the profit and put it in the pockets of private shareholders instead of using it for cross-

financing of un-profitable lines. This endangers the country wide supply and the traffic outside the

peak-hours.

The consequences would be either less service for the public or higher PSO compensation to be paid

by the public authorities, so in consequence by the public and the tax payers. The ETF is of the

opinion that it is not acceptable that profit is going to private interests while the public fully has to

pay to ensure mobility needs of all people.

The effects of competitive tendering of a whole national network

Final Report Train and Railway Infrastructure Network (TRAIN)

14

Usually there is one major reason why politicians are in favor of competition via competitive

tendering: They believe it is cheaper.

But there is sufficient experience available by now to show that it is an illusion to believe that

tendering, concessions or franchising of rail passenger services reduce costs for the public. It is an

illusion to believe that competition ‘for the track’ (competitive tendering) provides better and

cheaper services for rail users and customers.

There are many problems and risks for the public: Bidders that make too low offers and are not able

to provide the service as contracted. Bidders that go bankrupt and the continuation of services is in

danger. Regular demands for re-negotiation of contracts.

But first of all, bidders usually compete on the level of personnel costs in order to win contracts. This

initiates a downwards spiral on working conditions and pay on the back of railway workers and to

the detriment of good quality services. Fixed-term contracts not only reduce the motivation of

companies to invest in the skills of workers or health and safety, but they prevent in view of the

"demographic change", that working conditions can be designed in rail transport in such a way that

workers can age healthy maintain their employability in a sustainable way.

A number of experience show that for example on-board personnel will be reduced. This creates

problems for safety and personal safety (aggressions, attacks). People feel more insecure. People

with reduced mobility have more problems with using the trains, or cannot longer use them. Their

mobility is simply limited.

Today railway workers are still proud being a railway man or railway women. Railway companies

and politicians totally underestimate the strong commitment of railway workers for their profession

and their company. ETF fears that in future being a railway worker will be a precarious job like many

others.

All experiences show that competitive tendering imposed by liberalization of rail passenger

transport is to the disadvantage of workers in the various sectors. As long as there is no strong

Community instrument and guarantee that such introduced competition will not take place on the

basis of working conditions and employment, as long workers will not agree to so called regulated

competition.

The up-coming 4th Railway Package

Final Report Train and Railway Infrastructure Network (TRAIN)

15

The main objective of the 4th Railway Package is to enhance the quality and efficiency of rail services by

removing the remaining obstacles, fostering thereby the performance of the railway sector and hence,

competitiveness and growth. The adoption of the 4th Railway Package is expected till end of December 2012.5

These obstacles can be grouped into 4 categories (technical, administrative, institutional and legal barriers),

tackled by the initiatives composing this new railway package. The initiatives refer to the institutional

organisation of the rail market, to addressing legal barriers to access the domestic passenger market and the

initiatives on the European Railway Agency (ERA), interoperability and safety.

Different options are discussed and have to be evaluated form a employee´s perspective in future:

“To remedy the situation, the 4th Railway Package proposes the evaluation of options such as no legislative

changes, but continued progressive implementation of existing legislation (this being option 0), then the first

option will be open access competition for domestic services. The second option comprises the first one plus

mandatory competitive tendering of PSC for domestic rail; the third option cumulates option 2 plus introduction

of framework conditions potentially having a favorable impact on market access and quality of service e.g. full

independence of infrastructure managers, better access to facilities and stations, through ticketing, inter-

availability of tickets”, pointed out an Economic Advisor, quoted by a railway magazine. 6

The ETF Railway Section already had adopted as well a position paper on the upcoming 4th Railway Package.

The ETF rejects the liberalization of domestic passenger rail transport and insists that the EU regulation Public

Passenger Transport Services is not opened up. The ETF is against further separation of rail infrastructure

management and rail operations and expresses its favor to integrated companies.7

According to contributions by the final project conference and the ETF position paper the separation of rail

and track is evaluated critically. The ETF is convinced that the political and non-political actors that push for a

complete separation between infrastructure management and railway operations (unbundling) do not take

into account the unavoidable link that exists between rail and track. In integrated companies, this link allows

better punctuality, communication and transparency, also towards the passengers. An integrated company is

also better suited to do long-term investments and promote innovation, which can be done with converging

developments of infrastructure and rolling stock. With separate companies these synergies are lost.8

Sabine Trier, ETF Deputy General Secretary, said: “Additionally, the total destruction of integrated companies

has severe consequences on employment security and working conditions of the workers of those companies”.9

5 Due to this timeframe this report could not analyzed and discussed critically the 4

th railway package.

6 According to the magazine “Railway pro” http://www.railwaypro.com/wp/?p=9153

7 See as well the results of the PIQUE-Project - Privatization of Public Services and the Impact on Quality, Employment

and Productivity 8 http://www.itfglobal.org/etf/etf-press-area.cfm/pressdetail/7904

9 http://www.itfglobal.org/etf/etf-press-area.cfm/pressdetail/7904 - Nov. 2012

Final Report Train and Railway Infrastructure Network (TRAIN)

16

4. The EU White Paper on Transport 2011 – A critical review 10

On 28th of March 2011 the EU Commission presented the white paper “Roadmap to a Single European Transport Area – Towards a competitive and resource efficient transport system“. The title of this White Paper shows the difficult balance in two different ways:

- A “single transport area” implies harmony, social equilibrium; accessibility for all – however, a “competitive transport system“ implies the diversity and enforcement of the principle according to which the stronger one has the better chances

- A “resource efficient transport system“ is targeted towards environmental protection and low power consumption; lowering the so-called external costs of transport – a “competitive transport system“, however, is targeted towards low costs for the operator and subscribes to the principle of velocity and efficiency which is usually linked to a high consumption of resources.

The EU white paper did not arouse any enthusiasm but it certainly received praise. In a comment made by the European Transport Workers Federation (ETF) it states that „The white paper contains a number of good approaches which could strengthen the international competition for the railway.” And: “The goals are not new. However, the good thing is that they are now defined as official objectives at the highest level.”

But the targets presented in this white paper have been already developed by the EU for over one and a half decade. It is exactly these approaches for EU policy on transport which have been weakening the railways for some time and which can increase damage to the railway in the near future.

Character and collection of EU White Papers on the subject of transport

There are general – and largely non-committal – statements by the Commission. Further on the Commission publishes the so called “White Papers” which likewise demonstrate a relatively low degree of concretisation. There are thus like the “Railway Packages” and the specific EU guidelines which one, as far as implemented at a national level, are then enforced by law. Finally, there are EU programmes and financial resolutions, for

10

The text is based on two speeches held by the author on the topic of the EU White Paper 2011 on 9 November 2011 in

Bautzen for the Branch Committee for the Rail Industry of the Unions (IG Metall) and on 30 November 2011 in Brussels

for the European Metal Worker’s Federation (EMF) – 1st workshop of the EMF train project. The quotations from the

White Paper follow the German text; in the case of the White Paper on Traffic 2011 this is the EU document “COM(2011)

144 final“ (Brussels, 29 March 2011).

Final Report Train and Railway Infrastructure Network (TRAIN)

17

example in the transport sector the TEN programmes and the support of air transport through an absence of kerosene tax and promotion of regional airports which considerably define the specific policies on transport.

The analysis of these texts is worthwhile and we have to place these white papers and similarly interesting green papers 11 on the subject of transport in a larger context.

What happened till today? Since 1992 the EU commission has published two green papers on transport (1992 and 1995) and three white papers on transport (1992, 2001 and 2011). Purely in mathematical terms, there has been a similar basic declaration on EU policy on transport every four years. The new white paper is, however, the first publication of this kind in one decade.

To compare: The 2001 white paper still contained the specific value according to which the “market value of the rails in goods transport until 2020 should be increased from eight to 15 percent“. This was ambitious and precise and would have corresponded to about four times the amount of transportation efficiency on the railway in absolute figures. But the new white paper does not even mention this target. The reason why seems to be clear: during the past decade the participation of the railways in goods transport was not increased and now in this white paper the target is worded as follows: “30 percent of the road goods transport over 300 km (distance) should be transferred to other transport vehicles such as rail and ship transport by 2030; more than 50 percent by 2050.”

But was has to be critical remarked: at this point there is no link to the current situation: how much percentage of the EU-wide road goods transport with over 300 km distance is presently transported by trucks? How many of them are then “30 percent”, respectively “50 percent”?

This target says even in an inverse conclusion that goods transport with distances shorter than 300 km is excluded from this transfer option. But how many trucks operate at a distance of over 300 km, the German transportation statistics provides the following answers: the average distance of transportation in German goods transport was only 100 km in 2009 (whereby it was still only 84 km in 2000). There is international truck transport of course, which is not exactly unimportant (in German statistics this is stated as being truck transport with foreign trucks), and which generally speaking has a considerably higher distance of transportation. However, as a kind of counterweight there is still the truck transport from the plants and factories, this is truck transportation by those companies which transport their own goods and produce with their own trucks. This truck transport from the plants is not included in the aforementioned “commercial truck transport“; it covers significantly smaller distances. In the overall balance it could be that the average transportation distance for the entire truck transport in Germany is in actual fact around 100 km. The... In total this means that truck transportation covering a distance of over 300 km represent just a small portion of the market.

Another example: the 2001 white paper contained impressive graphics on the diverging development of the rail and road infrastructure: the road network within the EU becomes longer from year to year while the rail network is cut. On this issue the former transport commissioner, Loyola de Palacio, bravely stated, “that on an average over the past thirty years 600 rail kilometres disappear each year but 1200 motorway kilometres are newly constructed.” The 2011 white paper remains silent on this issue.

11

The green papers were published under the auspices of the respective commission for environment. With a view to

environmental politics they were usually more advanced than the EU white papers on transport. The white papers on

transport were prepared under the auspices of the respective EU commission for transport.

Final Report Train and Railway Infrastructure Network (TRAIN)

18

Six errors in the White and Green Papers

Taking into account those aspects which are of significance for the unions in rail engineering and railways and those in environmental associations Winfried Wolf has discovered six decisive items or errors which appear in all white and green papers and which focus from his point of view on the wrong aspects of transport and welfare. In the following paragraphs Mr Wolf will specify the errors which have characterised the EU white and green papers for more than two decades.

(1) Optimistic growth

The new white paper demands that “growth in transport be guaranteed“. Mr. Kallas postulates, “The widespread assumption that mobility has to be restricted in order to combat the climate change is simply not true.” In actual fact, 25 percent of all greenhouse gases within the EU which are responsible for the climatic change are the result of the transport sector, 90 percent of which are from road and air transport. Within the EU the transport sector is the only economic sector in which CO2 emissions continue to increase. They even increase so quickly that they compensate for all decreases which already occurred and will be planned in all other EU economic sectors. The much quoted savings in emissions from individual private vehicles, trucks and aircraft are by far offset by the general increase in transport from private vehicles, trucks and aircraft.

(2) Inefficiency and congestion

The new white paper states that “congestion is a major concern in the EU transport sector“. In a manner typical for this document it also states abruptly and without further evidence as to how this claim ensued: “Congestion costs will increase by about 50% by 2050.” Increase on what basis? How high are these “costs caused by congestion“ today? How are they calculated?

After all: which infrastructures are “congested“? Those who are familiar with this issue realise that, above all, Kallas distinguishes from the so-called “congestion costs” at this point. However, leading transport experts rightfully dispute the fact that this type of “costs“ are of any relevance; in particular, they should not be allowed to be elevated to the level of external costs.12

(3) External costs

This topic is largely excluded from the white paper on transport and then, when it is addressed, it is played down. This is in direct contrast to the green and white papers published in 1992 and 1995.

The white paper ignores the demand for an internalisation of external costs to the actual transport costs which has been on the agenda for more than two decades. Instead, it states: “The Commission will develop guidelines for the application of internalisation charges …” by the way: for at least 15 years recognised studies have been carried out on the amount of external costs in transport and the demand to integrate them. However, the 2011 white paper wishes to first develop “guidelines“, which is a pure expression of lack of action and a continuation of playing for time.

In air transport the issue of external costs is particularly obvious; the CO2 emissions from air transport are regarded as particularly critical because they mainly occur at great altitudes and damage the environment significantly more than emissions close to the ground. In spite of this, kerosene is not even subjected to

12

Congestion costs are costs which usually only occur in road transport because this type of transport causes huge traffic

jams due to its anarchic organisation (“everyone travels on his/her own“), while air and rail transport is organised

according to schedule and the capacities available. Consequently, recording so-called congestion costs as “external costs“

has to give a distorted image.

Final Report Train and Railway Infrastructure Network (TRAIN)

19

mineral oil tax. The numerous references within national debates on the environment which state that one single country can hardly start kerosene taxation on its own and that “this type of thing” has to be regulated on a global level or at least on a uniform EU level is countered in the white paper as follows:

“Attention is needed however to avoid imposing excessive burdens on EU operations which could compromise the EU role as ‘global aviation hub’. Airport capacity needs to be optimised and (…), increased to face growing demand for travel.”

In actual fact, the majority of all flights by European airlines are domestic flights within an EU country or flights within Europe (= intra-European flights). If European kerosene tax (or adequate charges such as kerosene charges) were introduced, foreign airlines would have to pay these taxes (or charges) within the EU as well.

The reference that all this is performed because one has to “face growing demand for travel” lacks credibility. This demand does not grow from natural causes, it grows primarily as a result of a policy on the transport market which has made flying extremely affordable while rail transport has become considerably more expensive. For example, this caused flights within the German borders to increase by 70 percent from 1995 to 2010 while long-distance rail travel during this time frame stagnated, despite the availability of many high-speed rail connections. The reason for this twisted development is mainly due to the fact that flying within this time frame was significantly more economic while the prices for long-distance rail travel increased by a nominal, average 45 percent and by more than an effective 25 percent (inflation adjustment).

(4) Unilateral understanding of rail transport

The new white paper on transport demands: “By 2050, complete a European high-speed rail network“ and “Triple the length of the existing high-speed rail network by 2030”. (…) By 2050 the majority of medium-distance passenger transport should go by rail.”

Again, these objectives sound ambitious. Apart from the fact that, for example, “tripling the length of the existing high-speed rail network” is an illusion and at the same time misleading13, the insignificant truth is that, although there has been an increase in high-speed rail networks and an expansion of high-speed transport over the past 25 years, the entire length of the rail networks has decreased year by year. It was not possible to increase the proportion of rails for all transport services.

The reason why can be explained in a modified version of famous words once spoken by Bill Clinton as follows “It’s the economy of railways, stupid”! 90 percent of all rail transport takes place in Germany, i.e. in a large country, in urban transport and transport for distances less than 50 km per trip. If you take into account the transport efficiency14 instead of the amount of traffic per se, a good 50 percent of all passenger kilometres in rail transport are still urban transport. The trend is also even on the increase; the portion of urban transport in Germany is on the rise. Even if the entire urban transport is not included and only long-distance transport is taken into account the average distance travelled during each long-distance train journey is around 250 km. This means on the other hand that even the majority of pure long-distance rail travel does not play a greater role, whether the train travels at high-speed or at regular speed. The possible time gains in this range of around 250 km travel distance are relatively low. Also, for the average long-distance traveller, criteria such as punctuality, comfort, seat availability and the price of tickets are much more important than the question of whether the train travels at high-speed or at “regular train speed”.

13

In France and Germany expansion of a high-speed network took place in parallel to the reduction of the overall

network. Often high-speed networks simply replace existing networks for conventional train transport. The phrase

“completion of a high-speed network” suggests that something additional will be built to complement the classical

network. This only applies to a small portion of the new high-speed networks. 14

Amount of traffic = number of all journeys made; traffic efficiency = number of journeys made multiplied by the

kilometres driven (= “passenger kilometres”).

Final Report Train and Railway Infrastructure Network (TRAIN)

20

But the EU white paper on transport is once again only mentioning high-speed transport on trains –wishing to develop and promote them the authors are focussing on a minority of clients. Extensive calculations which include the costs for the infrastructure reveal, by the way, that high-speed transport shows a considerably greater deficit than conventional rail transport.

(5) Market credibility: concentration on competition and privatisation

The 2011 EU white paper on transport states the “objective of the EU Commission” is “for the next decade create a genuine Single European Transport Area by eliminating all residual barriers between modes and national systems (…) and facilitate the emergence of multinational and multimodal operators.” An extensive “market opening” should be obtained for the rail sector in particular. This affirms the initiative to “open the domestic rail passengers market to competition, including mandatory award of public service contracts under competitive tendering (…) Ensure effective and non-discriminatory access to rail infrastructure, including rail-related services, in particular through structural separation between infrastructure management and service provision.”

The demand to separate network from operation is nothing new for the EU Commission. The background for this is the general support for privatisation within the rail operation and stripping the uniform rail companies the way they still prevail in the whole of Europe today.

This is demonstrated by the two poles within the European rail service – Switzerland and the UK. One of the best rail system worldwide is the one in Switzerland; it is also a rail service which costs the tax payer considerably less per each unit than any other European rail service.15 It is also an integrated rail service – the infrastructure and operation are both governed by one company, the Swiss rail operator (SBB).

The opposite pole is represented by the rail service in the UK; this was recently assessed by the conservative-liberal government who published an extensive report - the McNulty Report. The findings of this report on privatisation of British Rail are as follows: following the privatisation, ticket prices soared tremendously; the British rail services now have the highest rail tariffs within the EU. Government subsidies for the rail system have increased three-fold and the efficiency of the rail systems are one third lower than those comparable ones in Europe. The rail systems in the UK are known as a perfect example of the stringent separation of rail networks and operation, whereby the infrastructure was also privatised between 1996 and 2001 (with catastrophic consequences); since 2002 the rail network has been under government control again.

The demands for “competition“, privatisation and the separation of network from operation are unrealistic; on no account do they serve the purpose of reaching the objective of an improved rail system. Even in Japan, a country with a relatively successful privatised rail sector, there are different rail companies which all act as integrated companies and on the basis of regional monopolies Moreover...

(6) Public service mobility

The EU white paper on transport stated that: “Mobility is vital for the internal market and for the quality of life (…) Transport enables economic growth and job creation (…) Curbing mobility is not an option.”

15

According to PRIMON reports prepared by Booz Allen Hamilton “the average annual government subsidies in EURO

cents per unit of kilometre for rail systems (Ptkm) during the time frame 1995 to 2003” were: Switzerland 2.4 cents,

Sweden 4.0, UK 5.3, France 6.2, Austria 6.6, Germany 7.0, Denmark 6.7, The Netherlands 9.2 and Italy 9.4 cents. This

means that the somewhat miserable range of rail transport in Austria or Germany costs the taxpayer per unit of service

almost three times as much as it costs the Swiss taxpayer for the almost luxurious range of rail transport available in

his/her country. These reports (PRIMON = Privatisation with and without networks“) were prepared by persons who are

focussed on privatising the German railway system (Deutsche Bahn AG).

Final Report Train and Railway Infrastructure Network (TRAIN)

21

The white paper at this point confuses mobility with kilometre efficiency. People do not become mobile when they have travelled as many kilometres as possible; mobility is qualitative – in accordance with the optimal satisfaction of mobility objectives. This also means that the time spent for the mobility service is regarded as a loss. A policy on transport which reduces the time spent in traffic/transport is more a gain in the quality of life. The continuous expansion of transport networks, in particular roads, was until now always connected with an increase in the time spent in traffic/transport – for example because “car cities” are linked with urban sprawl.

The claim that “mobility“ is linked with the “creation of jobs“ is extremely brief; it actually means that the ruling structure of the transport sector is linked with the increase in private vehicle and truck traffic and the tremendously increasing air traffic as well as the creation of jobs. Actually, the number of jobs in the overall European automobile industry has been predominantly stable for the past 25 years; within the classical automobile manufacturing countries such as Spain, the UK, France and Italy it has even decreased considerably. In Germany it was just possible to keep the job number level (800,000). Only in Central and Eastern Europe the number of jobs increased significantly. However, in the same time frame there was a reduction of around one million employees in the rail sector and rail industry within the EU-27 region.

The legitimacy of climate change makes it self-evident that there is an urgent requirement for the reduction of motorized transport services – which in the end could be a prerequisite for the later generation being able to enjoy a life worth living with mobility as well.

Final Report Train and Railway Infrastructure Network (TRAIN)

22

5. The crisis in the rail industry - more European than global

In order to grasp the dimension of insufficient investment in the rail industry, this chapter will analyze the macro-economic dimension and particularly the impact of the crisis on the sector.

A long-term industry limited by the European financial and economic crisis

The rail industry is a long-term industry, which involves spatial and structural planning. Consequently the development costs are very high and life cycles of production and operating very long. The dependent activities are therefore programmed and clocked by large local, regional or national infrastructure plans. The entire industry is also structured by certification and standardization. It is also an industry which gets back on the forefront because of changes in European societies: sustainable development, stronger needs for mobility and energy conservation increases the need for rail, while at the same time the debt crisis greatly reduces the resources of communities in Europe. The sector is largely financed (80%) by municipalities and regions. Recently projects in Portugal, Italy, and Spain were stopped. This is clearly a shift from the investment forecasts for 2012.

As already discussed there is a commitment from the European Commission to liberalization, more competition and creating a single network, which is multimodal and integrated. This leads to necessities and investments in terms of standardization, harmonization, certification and interoperability. But this approach does not sufficiently match all the challenges such as industrial policy for rail, maintenance of a competitive supply chain and employment.

A contradiction between economic and social logic is that the freight traffic has the potential to grow, but it lacks investments and is even in particular on decline. There are big potential deals in maintenance, development, fleet renewal and adaptation of the networks, but the lack of funding pushes manufacturers into troubles (including AFR in France, ABFR, Wagonbau Niesky in Germany).

Many national railway networks (infrastructure) must be renovated. In France 32,000 km has to be renewed and 1000 km cost about € 2 billion. This also requires, in a situation of fiscal restraint, trade-offs between hardware and infrastructure. Many Central and Eastern European countries (CEECs) have problems making use of the funds for rail investments that are provided by the European Union. Millions of Euros are not invested

Final Report Train and Railway Infrastructure Network (TRAIN)

23

even though railway systems in Central and Eastern European could be modernized at only 20% of the usual

market rate. Major investments are necessary to secure the very survival of rail transport in CEE countries.16

Increased competition between industrial players The European rail sector is a major provider of jobs in Europe and is recognized as a world leader, a position that was gained over a long period of time through the development of innovative, high-technology solutions. However, this leadership is challenged by emerging competitors from Asia, some of whom are already in a position to supply rail products on world markets at very competitive prices.

Taken a view from the past Alstom, Ansaldo, Siemens, Bombardier, Talgo or Vossloh CAF are noticed to be powerful European player on the sector but the European technology leadership is in danger because technology is copied and redeployed by Chinese companies, which become the largest producers, but also outside of China companies from Korea (Rotem), Japan (Hitachi) are present or active on low cost products like Império Siemens in Romania.

In a context of lack of real market growth in Europe, there is an increased competition and therefore a downward trend in prices. This leads to the end of the national logic and there is strong demand from outside of Europe, indeed Asia has become the first rail market (31%). But these markets also increasingly require the relocation of production with consequences first on employment and later on R&D activities in Europe. Further on high speed trains like the TGV or ICE get most of the publicity and are a product to increase the railway images. But high speed rail to develop and maintain is very costly and reduce the use of cheaper and more efficient trains e.g. in metropolitan areas. According to information presented during the final conference to build a single kilometer of a high speed track in Germany costs around 50.000.000 Euros.17 The participants of the final conference discussed alternative investments in order to the concentrate investments not only on high speed tracks but to connect rural areas with the metropolitan areas and to offer new ways of mobility to the commuter.

Innovation needed Continuous innovation in the rail sector is also necessary to fulfill the European Union´s objective of shifting a significant share of the continent´s transport of passengers and goods from the road and air modes to more sustainable and less “carbon intensive” means such as rail. After more than 10 years of close cooperation in the field of research and technical development the European rail supply industry needs to make a step change in rail research and development into a higher level of activities and to set up a so called “Joint Technology Initiative (JTI)” . Therefore they are seeking the support of European Institutions in order to establish a rail related research initiative and encourage priority for Rail-related R&D and Innovation in the upcoming Horizon 2020 program - the framework program for research and innovation.18

16

Information presented by UNIFE and estimations given by participant of the final conference in Brussels at 5th

and 6th

of November

17 Gietinger Klaus 2012 – Mobility in the region, presented during the final conference

18 Information given by Mr. Philippe Citroen, General Secretary of UNIFE during the final conference

Final Report Train and Railway Infrastructure Network (TRAIN)

24

Due to the current structure of the sector, innovation in the rail industry faces a number of specific challenges in comparison to other modes of transport, roads and air in particular. The rail manufacturing industry does not generate sufficient operational margins neither to finance speculative research, nor to allow for short cycle renewal of the products;

the strong and complex interfacing of all parts of the rail system (infrastructure, control-command, electrification, vehicles) makes it difficult, even for a major supplier alone, to move the lines and propose breakthrough innovation,

the lack of standardized products acts as a deterrent for innovation,

last but not least, the products renewal cycle is extremely long (an electric locomotive of 40 years old is still a modern traction tool, intensively used) and tends to hamper innovation;

As discussed during the conference it is the strong belief of the railway manufacturing industry that a Joint Technology Initiative (JTI) will be crucial to the preservation of market leadership, whilst helping the EU to meet its policy objectives with regard to the environment, transport, and industrial policy.

The rail industry aims to obtain an approval of the European Parliament and Council to start the JTI work in the coming two years. UNIFE and its member companies call EU decision-makers to provide full support to the so called “SHIFT²RAIL initiative”.

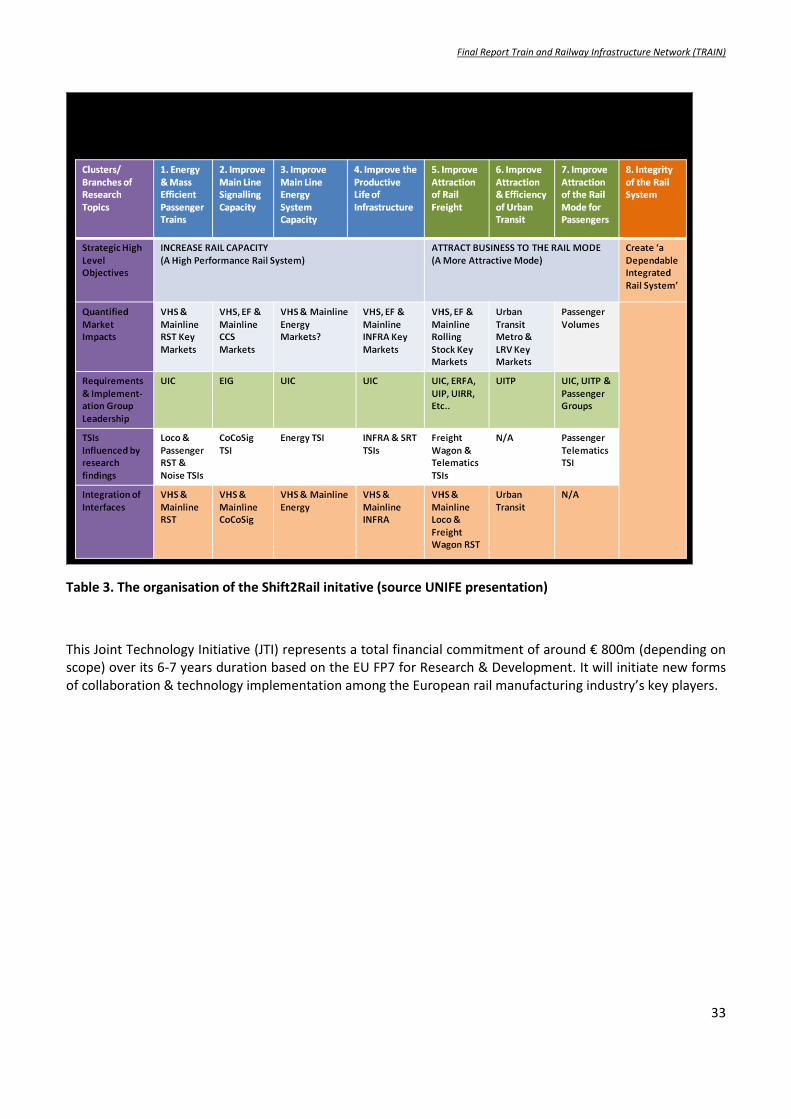

SHIFT²RAIL will develop and implement a new way of addressing the challenges for innovation in technology highlighted above.19 Two key objectives have been identified by the initiative:

Increasing capacity to enable rail to absorb a greater share of traffic growth,

Attract business and improve the efficiency of the rail transportation mode as a whole

There is need for further modernization and innovation especially on these fields that will be covered by the initiative:

Improve the energy and mass of material

Increase the attractiveness of rail freight

Increase the attractiveness of rail systems

Increase the capacity of large lines

Ensure the security and integrity of the rail system, to which is added the need to maintain a technological edge, and / or lower costs

19

See http://www.unife.org/page.asp?pid=194

Final Report Train and Railway Infrastructure Network (TRAIN)

25

The impact of the financial crisis

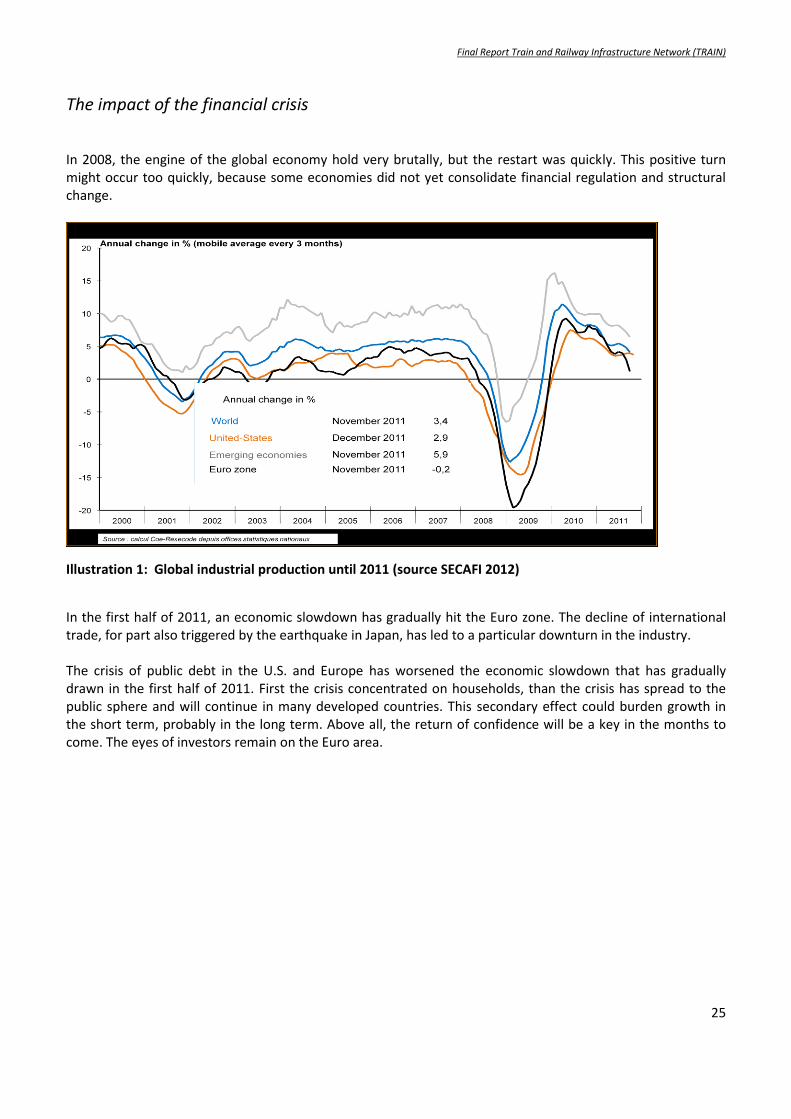

In 2008, the engine of the global economy hold very brutally, but the restart was quickly. This positive turn might occur too quickly, because some economies did not yet consolidate financial regulation and structural change.

Illustration 1: Global industrial production until 2011 (source SECAFI 2012)

In the first half of 2011, an economic slowdown has gradually hit the Euro zone. The decline of international trade, for part also triggered by the earthquake in Japan, has led to a particular downturn in the industry. The crisis of public debt in the U.S. and Europe has worsened the economic slowdown that has gradually drawn in the first half of 2011. First the crisis concentrated on households, than the crisis has spread to the public sphere and will continue in many developed countries. This secondary effect could burden growth in the short term, probably in the long term. Above all, the return of confidence will be a key in the months to come. The eyes of investors remain on the Euro area.

Final Report Train and Railway Infrastructure Network (TRAIN)

26

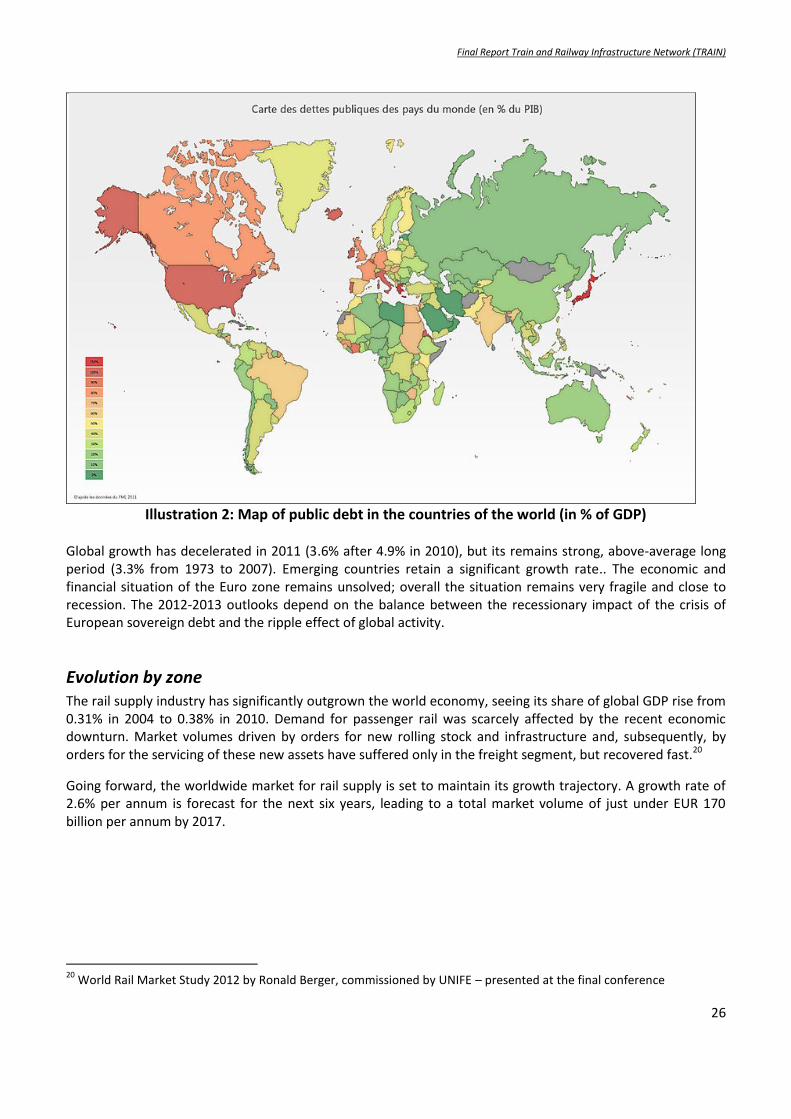

Illustration 2: Map of public debt in the countries of the world (in % of GDP)

Global growth has decelerated in 2011 (3.6% after 4.9% in 2010), but its remains strong, above-average long period (3.3% from 1973 to 2007). Emerging countries retain a significant growth rate.. The economic and financial situation of the Euro zone remains unsolved; overall the situation remains very fragile and close to recession. The 2012-2013 outlooks depend on the balance between the recessionary impact of the crisis of European sovereign debt and the ripple effect of global activity.

Evolution by zone The rail supply industry has significantly outgrown the world economy, seeing its share of global GDP rise from 0.31% in 2004 to 0.38% in 2010. Demand for passenger rail was scarcely affected by the recent economic downturn. Market volumes driven by orders for new rolling stock and infrastructure and, subsequently, by orders for the servicing of these new assets have suffered only in the freight segment, but recovered fast.20

Going forward, the worldwide market for rail supply is set to maintain its growth trajectory. A growth rate of 2.6% per annum is forecast for the next six years, leading to a total market volume of just under EUR 170 billion per annum by 2017.

20

World Rail Market Study 2012 by Ronald Berger, commissioned by UNIFE – presented at the final conference

Final Report Train and Railway Infrastructure Network (TRAIN)

27

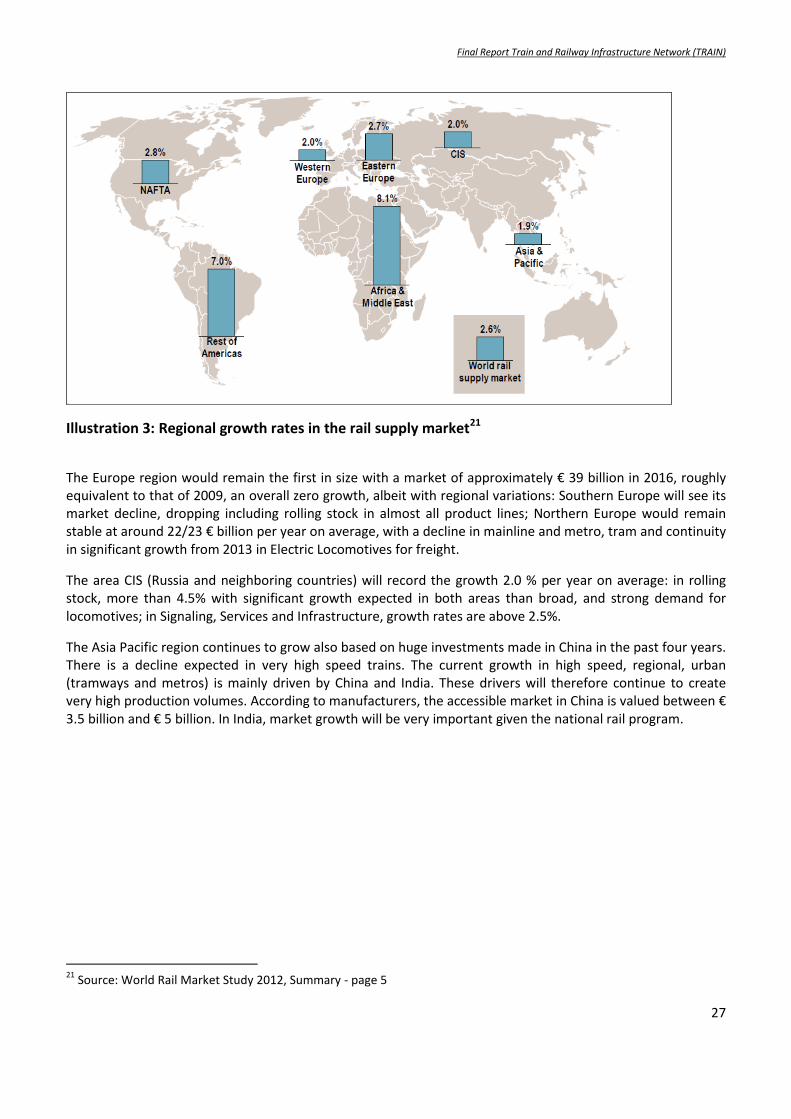

Illustration 3: Regional growth rates in the rail supply market21

The Europe region would remain the first in size with a market of approximately € 39 billion in 2016, roughly equivalent to that of 2009, an overall zero growth, albeit with regional variations: Southern Europe will see its market decline, dropping including rolling stock in almost all product lines; Northern Europe would remain stable at around 22/23 € billion per year on average, with a decline in mainline and metro, tram and continuity in significant growth from 2013 in Electric Locomotives for freight.

The area CIS (Russia and neighboring countries) will record the growth 2.0 % per year on average: in rolling stock, more than 4.5% with significant growth expected in both areas than broad, and strong demand for locomotives; in Signaling, Services and Infrastructure, growth rates are above 2.5%.

The Asia Pacific region continues to grow also based on huge investments made in China in the past four years. There is a decline expected in very high speed trains. The current growth in high speed, regional, urban (tramways and metros) is mainly driven by China and India. These drivers will therefore continue to create very high production volumes. According to manufacturers, the accessible market in China is valued between € 3.5 billion and € 5 billion. In India, market growth will be very important given the national rail program.

21

Source: World Rail Market Study 2012, Summary - page 5

Final Report Train and Railway Infrastructure Network (TRAIN)

28

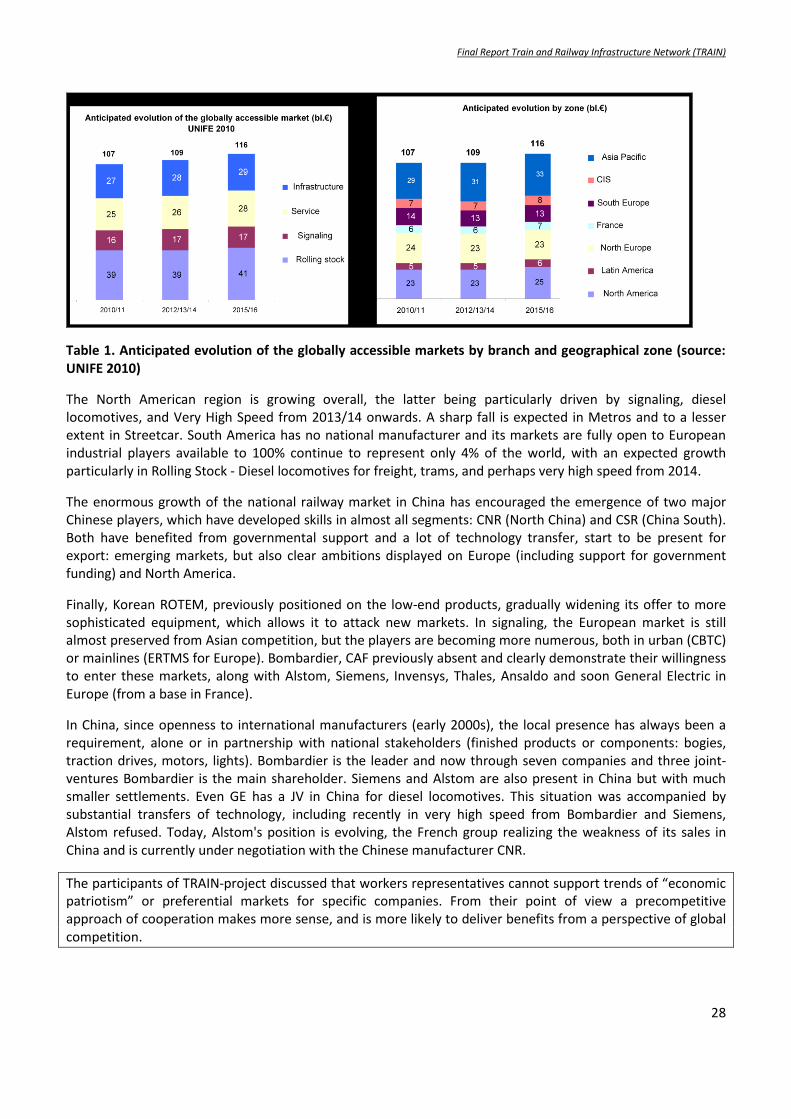

Table 1. Anticipated evolution of the globally accessible markets by branch and geographical zone (source: UNIFE 2010)

The North American region is growing overall, the latter being particularly driven by signaling, diesel locomotives, and Very High Speed from 2013/14 onwards. A sharp fall is expected in Metros and to a lesser extent in Streetcar. South America has no national manufacturer and its markets are fully open to European industrial players available to 100% continue to represent only 4% of the world, with an expected growth particularly in Rolling Stock - Diesel locomotives for freight, trams, and perhaps very high speed from 2014.

The enormous growth of the national railway market in China has encouraged the emergence of two major Chinese players, which have developed skills in almost all segments: CNR (North China) and CSR (China South). Both have benefited from governmental support and a lot of technology transfer, start to be present for export: emerging markets, but also clear ambitions displayed on Europe (including support for government funding) and North America.

Finally, Korean ROTEM, previously positioned on the low-end products, gradually widening its offer to more sophisticated equipment, which allows it to attack new markets. In signaling, the European market is still almost preserved from Asian competition, but the players are becoming more numerous, both in urban (CBTC) or mainlines (ERTMS for Europe). Bombardier, CAF previously absent and clearly demonstrate their willingness to enter these markets, along with Alstom, Siemens, Invensys, Thales, Ansaldo and soon General Electric in Europe (from a base in France).

In China, since openness to international manufacturers (early 2000s), the local presence has always been a requirement, alone or in partnership with national stakeholders (finished products or components: bogies, traction drives, motors, lights). Bombardier is the leader and now through seven companies and three joint-ventures Bombardier is the main shareholder. Siemens and Alstom are also present in China but with much smaller settlements. Even GE has a JV in China for diesel locomotives. This situation was accompanied by substantial transfers of technology, including recently in very high speed from Bombardier and Siemens, Alstom refused. Today, Alstom's position is evolving, the French group realizing the weakness of its sales in China and is currently under negotiation with the Chinese manufacturer CNR.

The participants of TRAIN-project discussed that workers representatives cannot support trends of “economic patriotism” or preferential markets for specific companies. From their point of view a precompetitive approach of cooperation makes more sense, and is more likely to deliver benefits from a perspective of global competition.

Final Report Train and Railway Infrastructure Network (TRAIN)

29

6. The challenges of the sector from the European employer perspective

The concept of Trans-European Networks (TEN in the EU jargon) emerged in the 1980s in conjunction with the proposed Single Market. But it made little sense to talk of one big market, with freedom of movement for goods, persons and services, unless the various regions and national networks were properly linked by modern and efficient infrastructure.

According to Article 10 of the Decision No 1692/96/EC of the European Parliament and of the Council of 23 July 1996 on “Community Guidelines for the Development of the Trans-European Transport Network”, the rail network should include the infrastructures and the facilities which enable rail and road and, where appropriate, maritime services and air transport services to be integrated. In this regard, particular attention should be paid to the connection of regional airports to the network.

One or more of the following functions should be met by any component of the rail network:

it should play an important role in long-distance passenger traffic

it should permit interconnection with airports, where appropriate

it should permit access to regional and local rail networks

it should facilitate freight transport by means of the identification and development of trunk routes dedicated to freight or routes on which freight trains have a priority

it should play an important role in combined transport

it should permit interconnection via ports of common interest with short sea shipping and inland waterways