8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 1/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

MODULE 1: HUMAN RESOURCE ISSUES ON COMPENSATION

1. LABOR STANDARDS1.1 General Principles on Wages

1.1.1 Non-diminution of Benets:

LC ART. 100Prohibition against elimination or diminution of benets. Nothing in this Book shall be construed toeliminate or in any way diminish supplements or other employee bene!ts being en"oyed at the time o# promulgation o# this Code.

LC ART. 1$%Non-diminution of benets. No wage order issuedby any regional board shall pro&ide #or wage rateslower than the statutory minimum wage rates

prescribed by Congress.

x------------------------------------x

1.1.1.1Company 'ractice or (&ersight)

Globe Mackay Cable & Rado Co!" # NLRCFacts:

• Respondents are employees of Petitioner

• Wage rder ! " #as enacted cto$er 1%&' to increase t(ecost of li)ing allo#ance *+, for non-agricultural pri)atesector $y P/.00day.

• Petitioners computed t(is on t(e $asis of 22 #or3ingdaysmont(.

• Respondent countered t(at it s(ould $e /0 daysmont( as(as $een company practice4 #(ic(5 according to t(ems(ould not $e unilaterally #it(dra#n

• ,a$or r$iter ruled in fa)or of Petitioner

• N,R+ re)ersed , decision

6ssue: WN t(e pre)ious /0daysmont( can $e considered companypractice 7 as suc(5 cannot $e unilaterally #it(dra#n8

9eld: No company practice. N,R+ re)ersed.

No proof #as presented t(at t(ere (as $een a long companypractice of /0daymont( computation of +,. o $econsidered as suc(5 t(ere must $e proof t(at aside from$eing practiced o)er a long period of time5 it must also $e

consistent and deli$erate.

9o#e)er5 $ased on Wage rders ! 25 /5 ; 7 "5 t(e +, iscomputed $ased on t(e computation of t(e days t(ey arepaid t(eir $asic #age5 e)en if un#or3ed. ccording to t(eir+B5 t(e $asic #age is computed $ased on 22 daysmont(or ; days#ee3. s t(e +B is la# $et#een t(e parties5 t(ismust $e follo#ed. <(ould t(e respondents (a)e felt t(at t(is#as a diminution of $enets5 t(ey s(ould (a)e soug(t to re-negotiate said +B.

6n addition5 t(e pre)ious Wage rder ! ' lac3ed

administrati)e guidelines. But #(en t(e implementing rules#ere released5 t(e computation for t(e con)ersion of dailyallo#ance #as included5 #(ic( specied a 22 daymont($asis. (us5 since t(e company (as $een practicing anerroneous application of t(e la#5 and as it (as $een $asissuc( errors on t(e a$sence of clear administrati)eguidelines for Wage rder ! "5 it cannot $e faulted for suc(.nd as a past error is actually $eing corrected5 respondentscannot $e said to (a)e a )ested rig(t on t(e $enets of anerroneous application of t(e la#.

Ma$la Elec%!c Co # '(')b$*

Facts:• (is is a petition for certiorari of =>R,+ see3ing to annul

t(e orders of <,> re?uiring =>R,+ and its ran3 and leunion *=>W to execute a collecti)e $argaining agreement*+B for t(e remainder of t(e parties@ 1%%2-1%%A +Bcycle5 and to incorporate in t(is ne# +B t(e <ecretary@sdispositions on t(e disputed economic and non-economicissues #(ic( includes:

1 Wage increases of P25200.00 for 1%%" and P25200.00 for1%%A4

2 (e follo#ing economic $enets:

1

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 2/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

a. #o mont(s +(ristmas $onus4$. Rice <u$sidy and retirement $enets for retirees4c. ,oan for t(e employees@ cooperati)e4d. <ocial $enets suc( as G9<6P and 9=P for

dependents5 employees@ cooperati)e and (ousing

e?uity assistance loan4e. <igning $onus4f. 6ntegration of t(e Red +ircle Rate llo#anceg. <ic3 lea)e reser)e of 1; days(. (e '0-day union lea)e4i. 9ig( pole(ig( )oltage and to#ing allo#ance4 and . Benets for collectors

/ >xercising discretion in determining t(e retroacti)ity of t(e +B4

6ssue: WN t(e <,> committed GC,>D in (is rders8

9>,C: E><. (e <+ found t(at t(e <,> committed GC,>D incertain aspects of (is rders.

(e issue (er related to +ompany Practice is on t(e =<BN<.

=>R,+ argued t(at t(e <,> erred #(en (e recogniHedt(at t(ere #as an Iesta$lis(ed practiceJ of gi)ing a t#o-mont( +(ristmas $onus $ased on t(e fact t(at $onuses#ere gi)en on or a$out +(ristmas time. 6t pointed out t(att(e Iesta$lis(ed practiceJ attri$uted to =>R,+ #asneit(er for a considera$le period of time nor identical in

eit(er amount or purpose.

s a rule5 a $onus is not a demanda$le and enforcea$leo$ligation4 it may ne)ert(eless $e granted on e?uita$leconsideration as #(en t(e gi)ing of suc( $onus (as $eent(e company@s long and regular practice. o $e considered aIregular practice5J t(e gi)ing of t(e $onus s(ould (a)e $eendone o)er a long period of time5 and must $e s(o#n to (a)e$een consistent and deli$erate. (us #e (a)e ruled inNational <ugar Reneries +orporation )s. N,R+:

I(e test or rationale of t(is rule on long practice re?uiresan indu$ita$le s(o#ing t(at t(e employer agreed tocontinue gi)ing t(e $enets 3no#ing fully #ell t(at saidemployees are not co)ered $y t(e la# re?uiring paymentt(ereof.J

(e record s(o#s t(at =>R,+5 aside from complying #it(t(e regular 1/t( mont( $onus5 (as furt(er $een gi)ing itsemployees an additional +(ristmas $onus at t(e tail-end of t(e year since 1%&&. W(ile t(e special $onuses diKered inamount and $ore diKerent titles5 it cannot $e denied t(att(ese #ere gi)en )oluntarily and continuously on or a$out+(ristmas time. (e considera$le lengt( of time =>R,+(as $een gi)ing t(e special grants to its employeesindicates a unilateral and )oluntary act on its part5 tocontinue gi)ing said $enets 3no#ing t(at suc( act #as notre?uired $y la#. company practice fa)ora$le to t(e

employees (as $een esta$lis(ed and t(e payments made $y=>R,+ pursuant t(ereto ripened into $enets enoyed $yt(e employees. +onse?uently5 t(e gi)ing of t(e special$onus can no longer $e #it(dra#n $y t(e company as t(is#ould amount to a diminution of t(e employee@s existing$enets.<+5 (o#e)er5 denied t(e <,>@s a#ard of a t#o-mont(special +(ristmas $onus since t(ere #as no recogniHedcompany practice of gi)ing a t#o-mont( special grant. #o-mont( special $onus #as gi)en only in 1%%; in recognitionof t(e employees@ prompt and eLcient response during t(ecalamities *nla$oM.

Na%o$al +ede!a%o$ o, Labo! # CAFacts:

• Respondent R+6 is t(e o#ner of a ru$$er plantation

• Respondent entered into a Farm =anagement greement*F= #it( <CP6

• Petitioner NF, is t(e $argaining agent of <CP6 employees int(e ,atuan Plant

• +B states t(at in case of permanent and temporary lay-oK5t(e employees are entitled to separation pay

• +ompre(ensi)e grarian Reform ,a# *+R, too3 eKect in

1%&& stating t(at all lands of pu$lic domain leased or2

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 3/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

possessed $y non-go)ernment entities5 de)oted toagricultural industries must $e ac?uired and distri$utedafter 10 years from t(e eKecti)ity of t(e +R,5 or upon t(eexpiration of t(e contract5 #(ic(e)er is sooner.

• <CP6 did not rene# t(e F= #it( R+6

• Petitioners recei)ed separation pay e?ui)alent to mont(year of ser)ice5 despite <CP6 paying t(e e?ui)alent of 1 mont( salaryyear of ser)ice to employees t(at #ere laidoK in t(e past.

• Petitioners@ $enets #ere also lumped into one c(ec35despite its pre)ious re?uest to segregate t(e regular$enets from t(e separation pay

• Petitioners #ere also re?uired to sign a IRelease andOuitclaimJ upon receipt of t(e c(ec3s

• ,a$or r$iter ruled t(at t(e termination #as proper- +losure of <CP6 #as due to +R,

- +B stated t(at separation pay #ould $e $ased on a mont(year of ser)ice- Petitioners already signed t(e ?uitclaim5 #(ic( #as

e?ui)alent to a #ai)er of future complaints regarding t(eseparation pay

• N,R+ aLrmed ,

6ssue: WN t(ere #as a diminution of $enets $ased on allegedcompany practice of paying t(e e?ui)alent of 1 mont(salaryyear of ser)ice8

9eld: No diminution of $enets. mont( salaryyear computation

up(eld.

rt. 2&/ of t(e ,a$or +ode pro)ides t(at employees #(o#ere dismissed not due to closure of t(e $usiness5 $ut notdue to insol)ency s(ould recei)e t(e e?ui)alent of 1 mont(salary or mont( salaryyear of ser)ice5 #it( " mont(s$eing counted as 1 year.

s t(e closure of t(e $usiness #as done in good fait( due tot(e eKecti)ity of t(e +R,5 and $ecause of t(e silence of t(e+B as to t(e met(od of computing t(e separation pay5 t(e,a$or +ode pro)ision s(all go)ern.

(ere #as also no company practice )iolated despite <CP6granting separation pay of 1 mont(year of ser)ice toretrenc(ed employees $efore t(e closure of t(e $usiness$ecause:

1. No pro)ision in t(e +B xing t(e separation pay of

t(ose terminated for aut(oriHed causes2. >mployees #(o #ere terminated prior to t(e closure

of t(e $usiness #ere due to redundancy5 and assuc(5 #ere actually entitled to separation pay of 1mont( salaryyear of ser)ice pursuant to t(e ,a$or+ode.

Se#lla T!ad$* Co # Se)a$aFacts:

• Petitioner is <e)illa rading +o

• Respondent is t(e union for employees of Petitioner

• For 2-/ years prior to 1%%%5 petitioner (as $een computing1/t( mont( salary $ased on t(e $asic pay P,< ot(er$enets5 suc( as o)ertime5 maternity 7 paternity lea)e5(oliday pay5 )acation 7 sic3 lea)e5 etc.

• Petitioner left t(e computation of t(e 1/ t( mont( pay to itspayroll employees. 9o#e)er5 after c(anging t(e person inc(arge of payroll and upon audit5 t(ey disco)ered t(e errorof including non-$asic pay in t(e gures it used for t(ecomputation of t(e 1/t( mont( pay.

• Based on t(e 1/t( mont( pay la#5 it s(all $e computed usingt(e net $asic pay as $ase5 excluding ot(er $enets.

• Respondents ?uestioned t(e recalculation of t(e 1/t( mont(

pay as $eing )iolati)e of t(e non-diminution of $enetspursuant to t(e ,a$or +ode.

• oluntary r$itrator ruled in fa)or of respondents

6ssue: WN t(ere #as a )iolation of t(e non-diminution pro)ision int(e recalculation of t(e 1/t( mont( pay8

9eld: Ees. Petitioner must re)ert $ac3 to t(e old computation of t(e 1/t( mont( pay and include ot(er $enets in t(e $ase.

lt(oug( petitioner claims t(at it is merely correcting amista3e5 t(is is not suLcient to ustify t(e diminution of

$enets it pre)iously pro)ided. Petitioner failed to explain

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 4/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

#(y mista3es #ere made in t(e computation despite clarityin statute 7 urisprudence.

Petitioner@s contention t(at t(is is t(e same case as Glo$e=ac3ay5 #(erein t(e +ourt ruled in fa)or of correcting t(e

mista3e of t(e company5 is #rong. 6n Gl$oe =ac3ay@s case5t(ey #ere not guilty of unilaterally #it(dra#ing #(at #asallegedly considered as long company practice5 $ecause it#as actually not long company practice. Glo$e =ac3ayt(oug(t t(at t(ey #ere supposed to compute t(e +,$ased on a /0daymont( $asis due to an a$sence inimplementing rules.

6n t(is case5 (o#e)er5 t(e Petitioners 3ne# fully #ell t(att(ey #ere computing t(e 1/t( mont( pay $y including ot(er$enets in its $ase. Cespite t(e presence of claricatory urisprudence and implementing rules5 Petitioner still

included ot(er $enets in computing t(e 1/ t( mont( pay. 6naddition5 it can also $e considered long company practicet(at cannot $e unilaterally #it(dra#n $ecause t(is (as $eent(e practice of t(e company for at least 2 years. (us5petitioner must re)ert $ac3 to its old computation of 1/ t(

mont( pay $y including ot(er $enets in computing its $ase.

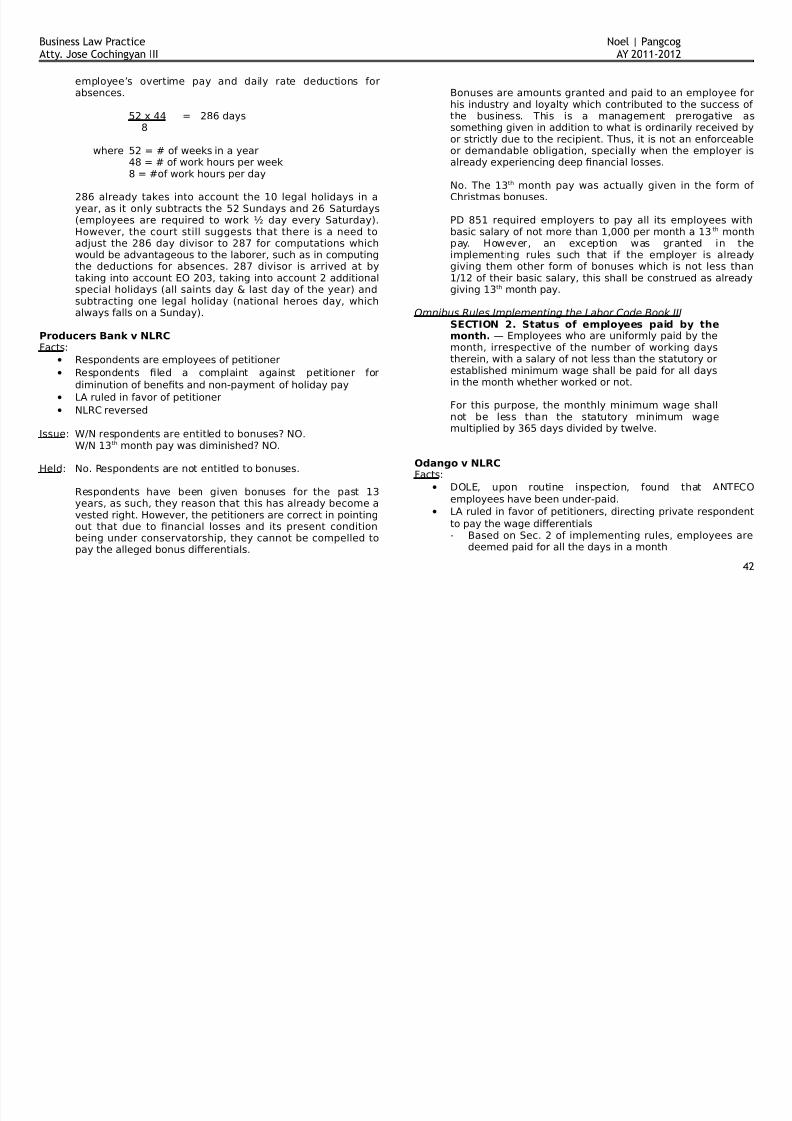

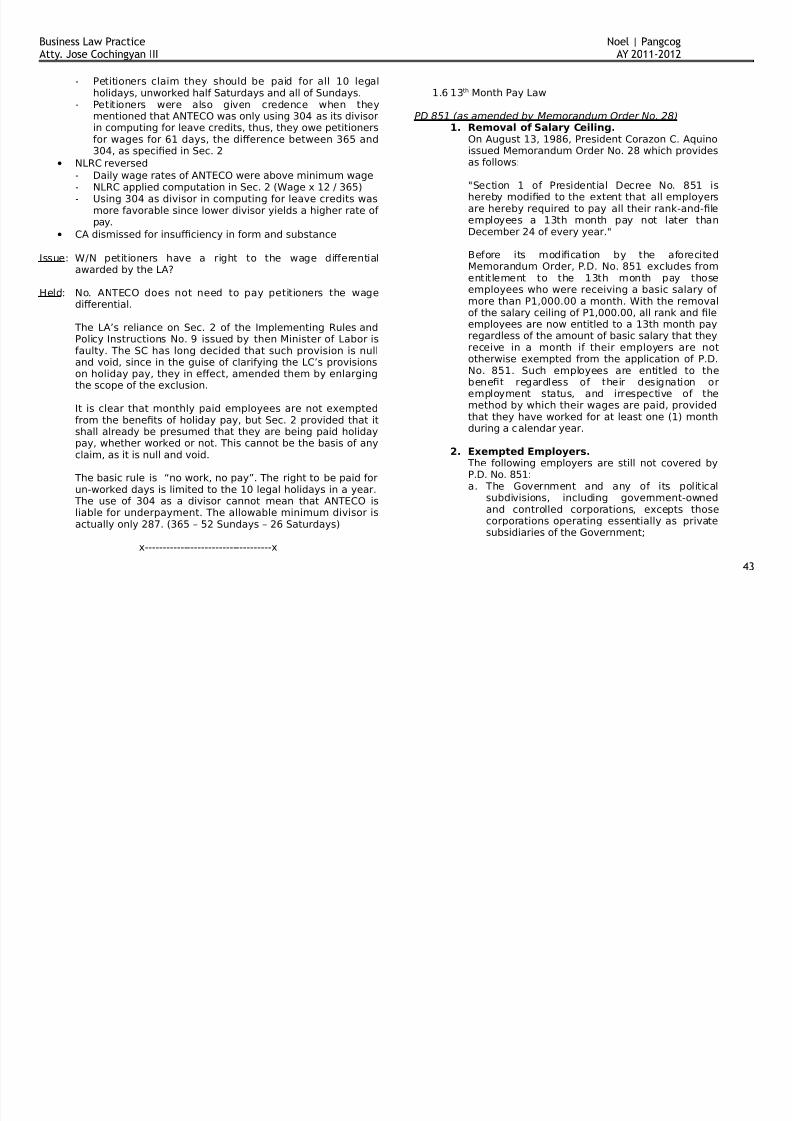

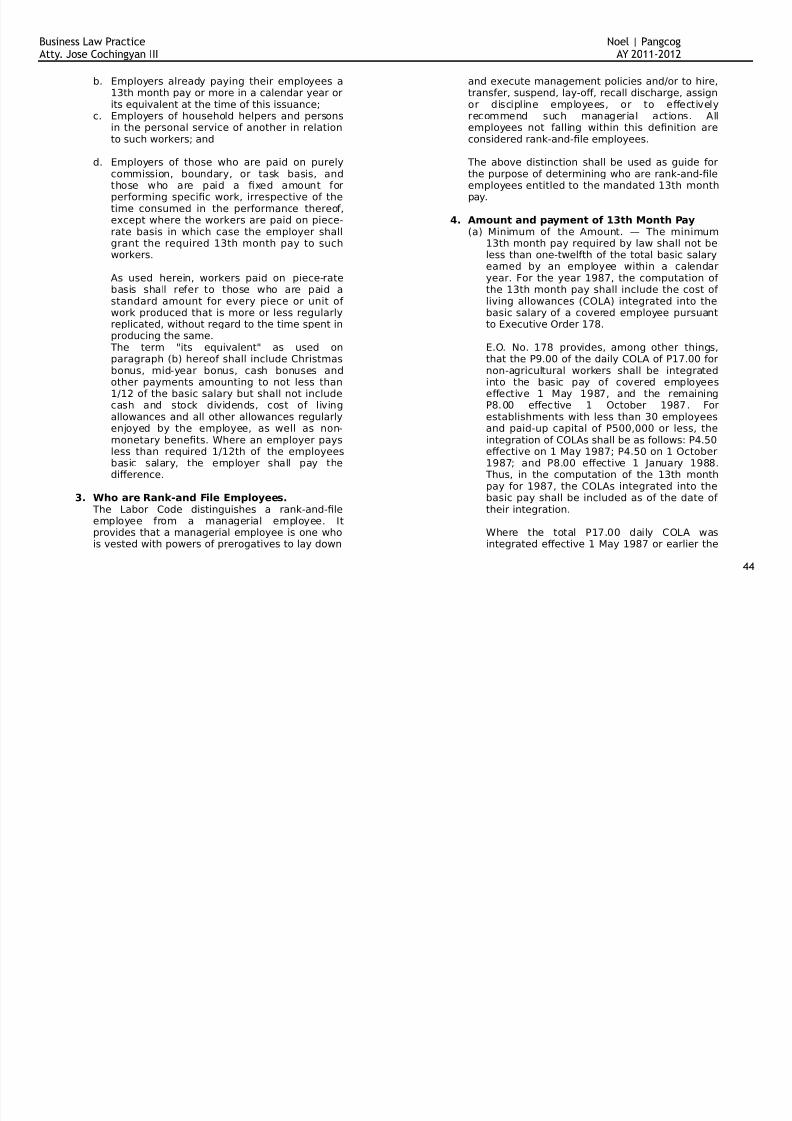

TSPIC Co!" # TSPIC E)"loyee( U$o$Facts:

• Petitioner designs5 manufactures 7 mar3ets integrati)ecircuits for data processing industries

• Respondent is t(e $argaining agent of r7f employees of Petitioner

• +B for 2000-200' included a pro)ision on yearly salaryincrease from Dan 2000-Dan 2002. *10Q in 20005 12Q in20015 11Q in 2002 nd any su$se?uent Wage <alary6ncrease rder *after Wage rder ! A s(all $e deemedincluded in t(e 12Q 7 11Q salary increase granted for t(e2001 7 20025 respecti)ely.

• +B also pro)ided t(at a proportionate increase s(all $egranted to t(ose #(o attain regular employment status int(e middle of t(e year and after t(e eKecti)ity of t(eincrease. *100Q for 1st O5 A;Q for 2nd O5 ;0Q for /rd O5 2;Q

for 't(

O

• Wage rder ! & #as implemented on cto$er 20005 raisingt(e daily minimum #age from P22/.; to P2;05 eKecti)eNo)em$er 2000.

• 6n 20015 some employees #ere informed t(at t(ey #ereo)erpaid 7 t(at t(eir o)erpayment #ill $e deducted fromt(eir salaries in a staggered $asis.

• Respondents a)erred t(at t(is #as a )iolation of t(e non-diminution of $enets pro)ision of t(e ,+

• oluntary r$itrator ruled in fa)or of Respondents

• + aLrmed @s ruling

6ssue: WN Petitioner@s decision to deduct o)erpayment from t(esalaries constituted a )iolation of t(e non-diminution of $enets pro)ided in t(e ,+8

9eld: No. (ere #as no )iolation of t(e non-diminution pro)ision.

Pursuant to t(e +B5 #(ic( is la# $et#een t(e parties5Petitioner granted t(e salary increase for 2001 7 2002. (is#as t(e general pro)ision in t(e +B. 9o#e)er5 t(ere #as aspecial pro)ision follo#ing suc(5 #(ic( stated t(at anysu$se?uent increase mandated $y a Wage rdersu$se?uent to Wage rder ! A s(all $e deemed credited orincluded in t(e salary increase for said years.

(us5 t(e #age increase granted $y Wage rder ! & s(ould$e credited against or su$tracted from t(e 12Q salaryincrease supposedly granted in 2001. (e diKerence is t(e

one5 #(ic( s(ould rig(tly $e considered as t(e increase in2001.

Ciminution of $enets is dened as:1. (e grant is founded on a policy t(at (as ripened into

practice for a long period of time2. Practice is consistent and deli$erate/. Practice is not due to error in interpretation of

dou$tful ?uestion of la#'. Ciminution is done unilaterally $y employer

Petitioner pro)ed t(at t(e o)erpayment #as done as a result

of an error5 #(ic( #as immediately rectied $y Petitioner.!

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 5/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

<ince it is a past error t(at #as committed5 t(ere can $e no)ested rig(t nor any diminution in $enet.

ARCO Me%al # Sa)a-a$ $* )*a Ma$**a*aaFacts:

• 6n Cecem$er 200/5 petitioner paid / employees a proratede?ui)alent for 1/t( mont( pay5 $onus 7 lea)e $enets5 assaid employees (a)e not rendered ser)ice for a full year.

• Respondents contend t(at se)eral times in t(e past5petitioner did not prorate t(e $enets gi)en to employees#(o #ere also not a$le to ser)e for a full year $y Cecem$er.

• oluntary ar$itrator found in fa)or of petitioner5 stating t(att(e past gi)ing of full $enets #ere mere errors.

• +B also stated t(at in order to $e entitled to full $enets5t(e employee must (a)e rendered one year of ser)ice.

• + ruled in fa)or of respondents saying t(at t(e past errors

already constituted )oluntary practice of t(e company inpaying t(e full $enets regardless of #(et(er or not t(eemployee rendered a full year of ser)ice.

6ssue: WN t(e payment of full $enets $y Petitioner in t(e pastregardless of actual ser)ice rendered constitutes )oluntaryemployer practice8

9eld: Ees. Payment of full $enets in t(e past s(all $e considered)oluntary employer practice.

Petitioner #as correct in stating t(at t(e +B clearly

pro)ides t(at in order for t(e employee to $e entitled to full$enets5 (e must rst (a)e rendered at least one year inser)ice. 9o#e)er5 it faltered in stating t(at t(e errorscommitted in paying out t(e full $enets in t(e past #eremerely Iclear o)ersig(tsSJ.

For se)eral years5 petitioner )oluntarily and freely paid outfull $enets regardless of t(e lengt( of ser)ice rendered.lt(oug( urisprudence is replete in determining t(e num$erof years it must $e exercised to constitute long employerpractice5 petitioner can no longer claim t(at it #as an error5as t(is practice (as $een done at least A times in t(e past.

Petitioner s(ould (a)e presented e)idence s(o#ing t(at full

$enets #ere not granted in t(e past to t(ose #(o did notrender a full year of ser)ice5 insteadof ust s(o#ing anaLda)it from t(e (ead of t(e manufacturing department.

x------------------------------------x

1.1.1.2Trans#er to Another 'osition

No!k( T!ad$* # G$loFacts:

• Respondent #as an employee of Petitioner5 $ut #assu$se?uently assigned to its sister company as +redit and+ollection =anager in ,egaspi.

• W(en an audit #as conducted5 it #as found t(at t(ecollection reports #ere padded $y s(o#ing a more fa)ora$lecollection eLciency t(an #(at it actually #as.

• Respondent #as c(arged #it( negligence of duties5 as (efailed to c(ec3 t(e reports $efore su$mitting t(e same totop management.

• Petitioner suspended respondent #it(out pay and $enetsfor 1; days.

• Respondent appealed (is suspension and re?uested t(at (e$e assigned as <ales >ngineer or to any positioncommensurate to (is ?ualications. 9o#e)er5 petitioner@s<P appointed (im as =ar3eting ssistant5 #(ic(respondent agreed to.

• But respondent led a complaint for illegal suspension5constructi)e dismissal 7 non-payment of $enets.

• , ruled in fa)or of Petitioner• N,R+ re)ersed

6ssue: WN respondent@s transfer of position constitutesconstructi)e dismissal8

9eld: Ees. Respondent@s transfer of position #as e?ui)alent to aconstructi)e dismissal.

+onstructi)e dismissal is dened as ?uitting $ecausecontinued employment is rendered impossi$le orunreasona$le5 as #(en t(ere is a demotion in ran3 ordiminution in pay or $enets.

"

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 6/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

lt(oug( respondent@s salary #as not reduced5 t(ere #as areduction in duties and responsi$ilities5 #(ic( amounted todemotion tantamount to constructi)e dismissal. 6n addition5(is $enets #ere reduced #(en t(e ser)ice car #as no

longer a)aila$le to (im as a =ar3eting ssistant.

R'!al Ba$k o, Ca$%la$ # /'l#eFacts:

• Petitioner appointed respondent as Planning and =ar3etingLcer.

• Petitioner@s president su$se?uently issued a memoranduma$olis(ing t(e position of planning and mar3eting oLcer5pursuant to its Personnel <treamlining Program.

• Petitioner transferred respondent to a $oo33eeper position#it( no diminution in salary.

•

Respondent #it(dre# (is agreement to t(e ne#appointment.• Petitioner t(en also assigned (im as ssistant $ranc( (ead5

#(ic( respondent still failed to accept.• Respondent led a complaint for constructi)e dismissal.

• ,a$or r$iter ruled in fa)or of respondent

• N,R+ re)ersed ,

• + re)ersed N,R+ and reinstated , ruling

6ssue: WN respondent #as constructi)ely dismissed8

9eld: No. Respondent #as not constructi)ely dismissed.

Respondent@s ne# position as $oo33eeper and assistant$ranc( (ead entailed great responsi$ilities5 as t(is ise?ui)alent to $eing t(e (ead of t(e accounting departmentof a $ranc(. 6n addition5 (e did not recei)e a diminution inpay.

(e transfer of respondent #as pursuant to a )alidPersonnel <treamlining Program5 #(ic( not only aKected(im alone5 $ut also ot(ers in (is position. lso5 despiterespondent@s refusal to accept t(e ne# appointment5petitioners did not dismiss (im5 as it #as respondent #(o5

(imself5 opted to terminate (is o#n employment #(en (epurposely failed to report for #or3.

P-l""$e A)e!ca$ L,e # G!a)a0eFacts:

• Respondent #as (ired as ssistant P 7 9ead of PensionsCept5 and concurrently as rust Lcer of P(ilam <a)ingsBan3.

• Respondent@s employees in (er department #eresu$se?uently transferred and #ere not replaced promptingrespondent to run t(e entire department on (er o#n.

• Respondent a)ailed of car and (ousing $enets in 1%%&.

• Petitioners5 (o#e)er5 oKered (er P2;05000 to )acate (eroLce instead5 #(ic( respondent refused5 as t(ere #as no)alid reason for (er to lea)e.

• 6n Cecem$er 1%%&5 Petitioner@s c(airman of t(e $oard met

#it( respondent reiterating t(eir re?uest for (er to )acate(er oLce5 #(ic( respondent still denied.• Petitioners transferred (er to t(e ,egal Cepartment a fe#

days after.• Petitioners immediately appointed a replacement for (er

pre)ious position as (ead of pensions department.• Curing +(ristmas season5 respondent soug(t t(e annual

gifts from P(ilam to its employees5 $ut s(e realiHed t(at s(e#as not e)en on t(e company@s list of employees.

• Respondent t(en led a complaint for illegal or constructi)edismissal.

• , ruled in fa)or of Petitioners.

• N,R+ aLrmed ,

• + re)ersed N,R+

6ssue: WN respondent #as constructi)ely dismissed8

9eld: Ees. Respondent #as constructi)ely dismissed.

lt(oug( t(e transfer of positions may $e a managementprerogati)e5 t(is s(ould still $e done in accordance #it( t(elimits set $y la#.

#

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 7/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

(e transfer of respondent #as actually met #it( $ad fait(or discrimination5 as it #as s(o#n t(at t(e position #asalready ad)ertised as )acant #ay $efore petitionertransferred (er to t(e ,egal Cepartment. lso5 despiterespondent meeting t(e standards for (er department set

$y Petitioner5 petitioner still c(ose to transfer (er to t(e,egal Cepartment5 #(ic( negates petitioner@s reasoning t(att(e transfer #as due to respondent@s failure to meet t(ecompany@s standards. Plus5 (er transfer #as unreasona$leand incon)enient5 as s(e (as not ade?uate exposure in t(eeld of litigation. 6n addition5 respondent #as left to run t(eentire Pensions Cepartment on (er o#n5 as petitioners failedto eld employees after transferring t(em to ot(erdepartments. ,astly5 petitioners failed to reply torespondent@s reection letter in response to t(eir P2;05000oKer for (er to )acate t(e position as (ead of t(e PensionsCepartment.

(ere $eing an o$)ious case of discrimination5 respondent(ad no c(oice $ut to forego (er continued employment #it(t(e company5 as $eing e?ui)alent to constructi)e dismissal.

Me$doa # R'!al Ba$k o, L'cba$Facts:

• Respondent Board of Cirectors released a resolution statingt(at t(ere #ill $e a res(uTing of t(e $an3@s employees tofamiliariHe t(em #it( )arious p(ases of $an3 operations 7 tostrengt(en t(e internal control system.

• Pursuant to said res(uTing5 petitioner #as transferred fromppraiser to +ler3-=eralco +ollection.

• Petitioner sent a letter to respondent5 stating (is disdain int(e transfer5 furt(er a)erring t(at (is transfer #as due tointrigues caused $y t(e malicious mac(inations of respondent@s +(airman@s good friend.

• Respondent merely reminded Petitioner t(at t(e transfer#as done in order to strengt(en t(e internal control systemof t(e $an3

• Petitioner re?uested for a lea)e of a$sence5 #(ic( (e usedto le a complaint for illegal dismissal and underpayment.

• , ruled in fa)or of petitioner

• N,R+ re)ersed

• + aLrmed N,R+

6ssue: WN petitioner #as constructi)ely dismissed8

9eld: No. Petitioner #as not constructi)ely dismissed.

+onstructi)e dismissal is an in)oluntary resignation resortedto #(en continued employment us rendered unreasona$leor impossi$le5 #(en t(ere is diminution in ran3 or pay5 or#(en clear discrimination $ecomes un$eara$le to t(eemployee. None of t(ese #ere present in petitioner@s case.

(ere #as a )alid reason for petitioner@s transfer5 as #asreiterated $y respondent. Respondent #as t(en a$le too)ercome t(e $urden t(at petitioner@s dismissal #asunla#ful.

x------------------------------------x

1.1.1./*emotion

Leo$a!do # NLRCFacts:

• Petitioner Fuerte #as (ired $y Pri)ate respondent Reynaldo=ar3eting +orp as a muTer specialist5 and #assu$se?uently promoted to super)isor.

• Petitioner ,eonardo #as also (ired $y respondent asmec(anic.

• Fuerte alleged t(at respondent e)entually transferred (im to

t(e <ucat plant for failure to meet t(e sales ?uota5 #(ile,eonardo #as dismissed $y respondent.• Bot( led a complaint for illegal termination

• , ruled in fa)or of petitioners

• N,R+ re)ersed ,

6ssue: WN petitioners #ere illegally dismissed8

9eld: No. (ey #ere not illegally dismissed.

Fuerte@s demotion #as not e?ui)alent to a dismissal. 9isdemotion #as due to a )alid cause U to promote competition

among t(e employees of respondent. s (e #as una$le to$

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 8/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

meet t(e mont(ly sales ?uota5 (e #as rig(tly demoted andallo#ance #it((eld.

,eonardo #as also not illegally dismissed5 as it #as (e #(o)oluntarily left (is post after an in)estigation #as initiated to

loo3 into (is IsidelineJ $usiness.

s t(e company )alidly demoted Fuerte5 follo#ing companypolicy of doing so s(ould t(e employee fail to meet t(estandards set5 t(ere #as no constructi)e or illegal dismissal.6t #as #ell #it(in management@s prerogati)e to do so.

Bl'e Da!y Co!" # NLRCFacts:

• Respondent #as (ired $y petitioner as a food tec(nologist.

• Respondent oined t(e Production =anager one day in oneof t(e )isits of t(e client@s outlet5 #(ere t(e company cart(ey #ere riding #as (it $y a post as it fell due to t(e strong#inds.

• Respondent #as5 (o#e)er5 su$se?uently transferred to t(e)egeta$le processing section5 and #as no longer allo#ed toenter t(e la$oratory.

• Respondent led a complaint for constructi)e dismissal.

• , ruled in fa)or of respondent

• N,R+ aLrmed

6ssue: WN respondent #as constructi)ely dismissed8

9eld: Ees. Respondent #as constructi)ely dismissed.

lt(oug( it may $e a management prerogati)e to transferemployees #it(in t(e company5 $ased on eac( employee@s?ualications5 it must still $e done #it(in t(e limits pro)ided$y la#. <ince t(e petitioner failed to s(o# t(at t(e transfer#as not unreasona$le or it did not result in a diminution inpay or $enets5 t(ey #ere not a$le to o)ercome t(epresumption of constructi)e dismissal.

6n addition5 petitioner also failed to s(o# t(at t(e demotionof respondent #as )alid. 6ts only reasoning #as t(e incident

#(en t(ey )isited a client@s outlet. ccording to petitioner5

respondent #as scouting for (ouses using t(e company carand during oLce (ours. 9o#e)er5 respondent #as ne)ergi)en t(e opportunity to refute t(e narrations of t(ecompany dri)er.

x------------------------------------x

1.1.1.'Right to a +ork ,chedule-ull +ork +eek

Ma$la /ockey Cl'b E)"loyee( Labo! U$o$ # M/C2 I$cFacts:

• Respondent #as granted a legislati)e franc(ise to operateand maintain (orse races.

• Petitioner entered into a +B #it( respondent

• +B stated t(at t(e #or3 day s(all $e composed of A (oursstarting from %am to ;pm.

•

Respondent5 (o#e)er5 e)entually c(anged t(e sc(edule for uesday and (ursday to 1pm U &pm #(en (orse races are(eld.

• Petitioner a)erred t(at t(is )iolated t(e non-diminution in$enets clause of t(e ,a$or +ode5 as t(ey #ere no#precluded from rendering t(e usual o)ertime #or3 from;pm-%pm

• oluntary r$itrators found in fa)or of respondent

6ssue: WN t(ere #as a )iolation of t(e non-diminution of $enets5as stated in t(e ,a$or +ode8

9eld: No. 6t #as management@s prerogati)e to c(ange t(e #or3sc(edule of t(e regular employees.

(e c(ange in #or3 sc(edule #as )alidly done5 pursuant tot(e c(ange in (orse race sc(edules. s t(e (orse races nolonger started at 10am5 $ut at 2pm5 t(ere #as no #or3 to $edone in t(e morning. >)en t(e +B recogniHed t(eprerogati)e of respondent to adust t(e #or3 sc(edule of t(eemployees5 pro)ided t(e A-(our #or3 per day is follo#ed.

6n addition5 respondent #as not o$liged to pay o)ertime pay5as t(e +B merely states t(at any #or3 done in excess of A

(ours s(all $e compensated. =anagement still (ad t(e rig(t%

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 9/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

to determine #(et(er or not #or3 #as actually done inexcess of t(e A (ours mandated $y t(e +B. s t(is #as notcompany practice5 (a)ing only gi)en o)ertime occasionally5t(ere can $e no diminution in $enets.

U$co!$ Sa,e%y Gla(( # Ba(a!%eFacts:

• Respondent employees #or3ed for petitioner #it( a "-day#or3 sc(edule

• Peititoner e)entually informed respondent t(at t(eir#or3days s(all $e reduced due to economic considerations*decrease in sales5 increase in minimum #age5 etc

• Respondents expressed t(eir dismay in t(e decreased#or3days

• Petitioners5 (o#e)er5 again informed t(em of an impending#or3 rotation sc(edule5 #(ic( #ould5 in eKect5 lessen t(eir

#or3days e)en more to only / days a #ee3.• Respondents led a complaint for constructi)e dismissal

• , ruled in fa)or of respondents

• N,R+ aLrmed

• + re)ersed N,R+ 7 , rulings

6ssue: WN respondents #ere constructi)ely dismissed8

9eld: Ees. Respondents #ere constructi)ely dismissed.

+onstructi)e dismissal does not al#ays ta3e t(e form of adiminution in pay or $enets. 6t may also $e t(at an act of

t(e employer #as clearly discriminatory5 suc( t(at itrendered it impossi$le or un$eara$le for t(e employees tocontinue #or3ing t(ere.

lt(oug( management (as t(e prerogati)e to lessen t(e#or3 sc(edule of its employees5 it may only do so for )alid$usiness reasons. 6n t(e case at $ar5 t(e employees failed tos(o# t(at t(e rotation sc(edule #as actually done #it( goodfait( and #it( due regard for t(e rig(ts of la$or.

x------------------------------------x

1.1.1.;Right to a Bonus

P!od'ce!( Ba$k # NLRCFacts:

• Respondents are employees of petitioner

• Respondents led a complaint against petitioner fordiminution of $enets and non-payment of (oliday pay

• , ruled in fa)or of petitioner

• N,R+ re)ersed

6ssue: WN respondents are entitled to $onuses8

9eld: No. Respondents are not entitled to $onuses.

Respondents (a)e $een gi)en $onuses for t(e past 1/years5 as suc(5 t(ey reason t(at t(is (as already $ecome a

)ested rig(t. 9o#e)er5 t(e petitioners are correct in pointingout t(at due to nancial losses and its present condition$eing under conser)ators(ip5 t(ey cannot $e compelled topay t(e alleged $onus diKerentials.

Bonuses are amounts granted and paid to an employee for(is industry and loyalty #(ic( contri$uted to t(e success of t(e $usiness. (is is a management prerogati)e assomet(ing gi)en in addition to #(at is ordinarily recei)ed $yor strictly due to t(e recipient. (us5 it is not an enforcea$leor demanda$le o$ligation5 specially #(en t(e employer isalready experiencing deep nancial losses.

x------------------------------------x

1.1.1." /ncreasing the *i&isor

T!a$(3A(a P-l( E)"loyee( A((oc # NLRCFacts:

• Petitioners and Respondents entered into a +B #(ic(pro)ided t(at a 200Q (oliday pay #ould $e gi)en5 plus a"0Q premium.

• Petitioners re?uested for t(e payment of (oliday pay inarrears $ut #as not granted $y respondent

• Petitioner t(en led a complaint #it( t(e ,&

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 10/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

6ssue: WN Respondents are lia$le for (oliday pay8

9eld: No. Respondents (a)e already incorporated t(e payment forlegal (olidays in t(e mont(ly salary of t(e employees.

Petitioners contend t(at t(eir mont(ly salaries did not (a)et(e allo#ance for t(e payment of legal (oliday pay5 asnot(ing in t(eir payslips indicated t(at suc( payment #asgi)en. 9o#e)er5 respondents contend t(at t(ey (a)e long$een using t(e I2&"-dayJ di)isor in computing for t(eemployee@s o)ertime pay and daily rate deductions fora$sences.

;2 x '' V 2&" days &

#(ere ;2 V ! of #ee3s in a year'& V ! of #or3 (ours per #ee3& V !of #or3 (ours per day

2&" already ta3es into account t(e 10 legal (olidays in ayear5 as it only su$tracts t(e ;2 <undays and 2" <aturdays*employees are re?uired to #or3 day e)ery <aturday.9o#e)er5 t(e court still suggests t(at t(ere is a need toadust t(e 2&" day di)isor to 2&A for computations #(ic(#ould $e ad)antageous to t(e la$orer5 suc( as in computingt(e deductions for a$sences. 2&A di)isor is arri)ed at $yta3ing into account > 20/5 ta3ing into account 2 additional

special (olidays *all saints day 7 last day of t(e year andsu$tracting one legal (oliday *national (eroes day5 #(ic(al#ays falls on a <unday.

A!ella$o U$#e!(%y # CAFacts:

• Petitioner led a Notice of <tri3e #it( t(e N,R+ c(argingrespondents #it( )iolation of nfair ,a$or Practice5 includinga diminution in $enets $y using /1' days as di)isor incomputing t(e daily #age of t(e #or3ers.

• lt(oug( N,R+ tried to mediate5 petitioners still staged astri3e

6ssue: WN t(ere #as a diminution in $enets due to respondentusing /1' as di)isor8

9eld: No. (ere #as no diminution in pay.

Respondents use /1' as t(ey merely deducted t(e ;2un#or3ed <undays from /"" *total num$er of days peryear. (e factor used merely complies #it( t(e $asic rule5Ino #or35 no pay.J

x------------------------------------x

1.1.1.AConsultancy Arrangements on Top o# mployment with Related Company

Se)e$( P-l""$e( # Do)$*o

Facts:6n 1%&A5 Comingo signed an >mployment +ontract #it(=>+ *a su$sidiary of <iemens P(ilippines as a consultant. (ereafter5 Comingo #as gi)en additional #or3 $y =>+5 in#(ic( (e #as paid on top of (is original salary. (e extra#or3 #as t(e result of a contract entered into $y =>+ and<iemens Germany *a German company #(ic( (as anin)estment in <iemens P(ilippines5 #(ere$y =>+5 at t(ere?uest of <iemens Germany5 (ired Comingo to (andle t(eoperation of >N > C. n Danuary 1%%25 ><6 *asu$sidiary of <iemens P(ilippines a)ailed of Comingo@sser)ices as assistant manager. (e +ontract of >mployment

of Comingo #it( ><6 pro)ides t(at t(e latter s(all (a)e t(erig(t to assign t(e said contract in fa)or of <iemensP(ilippines. n =arc( 1"5 1%%25 #(ile still an assistantmanager of ><65 Comingo #as (ired as a consultant $y<iemens Germany in t(e eld of text and data net#or3s fora period of t#el)e *12 mont(s. s compensation5 (erecei)ed C=205000.005 paya$le once for e)ery t#el)e-mont( period. n =arc( /15 1%%25 <iemens Germany sent aletter to ><6 guaranteeing t(e consultancy agreement. n Dune 15 1%%25 Comingo signed a +ontract of >mployment#it( <iemens P(ilippines.

10

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 11/139

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 12/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

o)er t(e maority of t(e $usiness acti)ities of ><6 and5conse?uently5 $ecame Comingo@s employer.

x------------------------------------x

1.1.2 Forms of Payment:

LC ART. 10$Forms of payment. No employer shall pay thewages o# an employee by means o# promissory notes &ouchers coupons tokens tickets chits or any ob"ect other than legal tender e&en whenepressly re2uested by the employee.

'ayment o# wages by check or money order shall beallowed when such manner o# payment is customary on the date o# e3ecti&ity o# this Code or is necessary

because o# special circumstances as speci!ed inappropriate regulations to be issued by the ,ecretary o# Labor and mployment or as stipulated in acollecti&e bargaining agreement.

(4N/B5, R5L, /4'L4NT/N6 LCB((7 /// R5L 8/// ,C 1 9 $

SECTION . !anner of "age payment. As a general rule wages shall be paid in legal tender and the use o# tokens promissory notes &oucherscoupons or any other #orm alleged to represent legaltender is absolutely prohibited e&en when epressly

re2uested by the employee.

SECTION #. Payment by $he$%.'ayment o# wages by bank checks postal checks or money orders is allowed where such manner o# wage payment is customary on the date o# the e3ecti&ity o# the Code where it is so stipulated in a collecti&eagreement or where all o# the #ollowing conditionsare met:

;a< There is a bank or other #acility #or encashment within a radius o# one ;1<kilometer #rom the workplace=

;b< The employer or any o# his agents or

representati&es does not recei&e any pecuniary bene!t directly or indirectly #romthe arrangement=

;c< The employees are gi&en reasonable timeduring banking hours to withdraw their wages#rom the bank which time shall be consideredas compensable hours worked i# done duringworking hours= and

;d< The payment by check is with the writtenconsent o# the employees concerned i# there

is no collecti&e agreement authori>ing the payment o# wages by bank checks.

LAB(R A*8/,(R? (N AT4 'A?4NT,;N(84BR $@ 1<

Payment through automated teller ma$hine&'T!( of ban%s pro)ided the follo"ing$onditions are met*

1. The AT4 system o# payment is with the writtenconsent o# the employees concerned=

$. The employees are gi&en reasonable time towithdraw their wages #rom the bank #acility whichtime i# done during working hours shall beconsidered compensable hours worked=

. The system shall allow workers to recei&e their wages within the period or #re2uency and in theamount prescribed under the Labor Code asamended= chanrobles &irtual law library

D. There is a bank or AT4 #acility within a radius o# one ;1< kilometer to the place o# work=

12

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 13/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

@. 5pon re2uest o# the concerned employee-s theemployer shall issue a record o# payment o# wages bene!ts and deductions #or a particular period=

. There shall be n additional epenses and nodiminution o# bene!ts and pri&ileges as a result o# the AT4 system o# payment=

%. The employer shall assume responsibility in casethe wage protection pro&isions o# law andregulations are not complied with under thearrangement.

Na%o$al +ede!a%o$ o, Labo! # CAFacts: *see page /

6ssue: WN payment t(roug( c(ec3 is )alid payment orlegal tender8

9eld: Ees. Payment $y c(ec3 is allo#ed.

,a$or +ode rt. 102 and its implementing rulespro)ide t(at payment $y c(ec3 is allo#ed5 so long ast(e conditions stipulated in t(e mni$us Rules arefollo#ed.

x------------------------------------x

1.1./ Cistinction $et#een facilities and supplement

(4N/B5, R5L, /4'L4NT/N6 LCB((7 /// R5L 8// A ,C D E %

Se$. +. Cash ,age.The minimum wage rates prescribed in ,ection 1hereo# shall be basic cash wages without deductingthere#rom whate&er bene!ts supplements or allowances which the employees en"oy #ree o# charge aside #rom the basic pay. An employer may pro&ide subsidi>ed meals and snacks to his

employees pro&ided that the subsidy shall not beless than 0F o# the #air and reasonable &alue o# such #acilities. /n such case the employer may deduct #rom the wages o# the employees not morethan %0F o# the &alue o# the meals and snacks

en"oyed by the employees pro&ided that suchdeduction is with the written authori>ation o# theemployees concerned.

Se$. . Fa$ilities.The term G#acilitiesH as used in this Rule shall includearticles or ser&ices #or the bene!t o# the employee or his #amily but shall not include tools o# the trade or articles or ser&ices primarily #or the bene!t o# theemployer or necessary to the conduct o# theemployerIs business.

Se$. . /alue of fa$ilities.The ,ecretary o# Labor may #rom time to time ! inappropriate issuances the #air and reasonable &alueo# board lodging and other #acilities customarily #urnished by an employer to his employees both inagricultural and nonagricultural enterprises.

The #air and reasonable &alue o# #acilities is hereby determined to be the cost o# operation andmaintenance including ade2uate depreciation plusreasonable allowance ;but not more than @ 1-$ Finterest on the depreciated amount o# capital

in&ested by the employer<= pro&ided that i# the totalso computed is more than the #air rental &alue ;or the #air price o# the commodities or #acilities o3ered#or sale< the #air rental &alue ;or the #air price o# thecommodities or #acilities o3ered #or sale< shall be thereasonable cost o# the operation and maintenance.The rate o# depreciation and depreciated amount computed by the employer shall be those arri&ed at under good accounting practices.

The term Ggood accounting practicesH shall not include accounting practices which ha&e been

1

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 14/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

re"ected by the Bureau o# /nternal Re&enue #or income ta purposes. The term GdepreciationsH shallinclude obsolescence.

Se$. 0. '$$eptan$e of fa$ilities.

/n order that the cost o# #acilities #urnished by theemployer may be charged against an employee hisacceptance o# such #acilities must be &oluntary.

x------------------------------------x

1.1.' Place of Payment

LC ART. 10DPla$e of payment. 'ayment o# wages shall bemade at or near the place o# undertaking ecept as

otherwise pro&ided by such regulations as the,ecretary o# Labor and mployment may prescribeunder conditions to ensure greater protection o# wages.

(4N/B5, R5L, /4'L4NT/N6 LCB((7 /// R5L 8/// ,C D

As a general rule the place o# payment shall be at or near the place o# undertaking. 'ayment in a placeother than the work place shall be permissible only under the #ollowing circumstances:

;a< +hen payment cannot be e3ected at or near the place o# work by reason o# thedeterioration o# peace and order conditionsor by reason o# actual or impendingemergencies caused by !re Jood epidemicor other calamity rendering payment thereat impossible=

;b< +hen the employer pro&ides #reetransportation to the employees back and#orth= and

;c< 5nder any other analogous circumstances='ro&ided That the time spent by theemployees in collecting their wages shall beconsidered as compensable hours worked=

;d< No employer shall pay his employees in any bar night or day club drinking establishmentmassage clinic dance hall or other similar places or in places where games are playedwith stakes o# money or things representingmoney ecept in the case o# personsemployed in said places.

R5L, /4'L4NT/N6 RA %$%CKA'TR / ,C 1 9 $0

Se$tion 1. Payment of ,ages.5pon written petition o# the ma"ority o# the workers

and employees concerned all pri&ateestablishments companies businesses and other entities with at least twenty!&e workers and locatedwithin one kilometer radius to a commercial sa&ingsor rural bank shall pay the wages and other bene!tso# their workers through any o# said banks within the period and in the manner and #orm prescribed under the Labor Code as amended.

Se$tion #2. 3uty of 4an%.+hene&er applicable and upon re2uest o# aconcerned worker or union the bank through which

wages and other bene!ts are paid shall issue acerti!cation o# the record o# payment o# said wagesand bene!ts o# a particular worker or workers #or a particular payroll period.

+A6 RAT/(NAL/MAT/(N ACT ,C. %5pon written permission o# the ma"ority o# theemployees or workers concerned all pri&ateestablishments companies businesses and other entities with twenty !&e ;$@< or more employees andlocated within one ;1< kilometer radius to acommercial sa&ings or rural bank shall pay the

1!

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 15/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

wages and other bene!ts o# their employees throughany o# said banks and within the period o# payment o# wages !ed by 'residential *ecree No. DD$ asamended otherwise known as the Labor Code o# the'hilippines.

x------------------------------------x

1.1.; ime of Payment

LC ART. 10Time of payment. +ages shall be paid at least once e&ery two ;$< weeks or twice a month at inter&als not eceeding siteen ;1< days. /# onaccount o# #orce ma"eure or circumstances beyondthe employerIs control payment o# wages on or within the time herein pro&ided cannot be made the

employer shall pay the wages immediately a#ter such #orce ma"eure or circumstances ha&e ceased.No employer shall make payment with less#re2uency than once a month.

The payment o# wages o# employees engaged to per#orm a task which cannot be completed in two ;$<weeks shall be sub"ect to the #ollowing conditions inthe absence o# a collecti&e bargaining agreement or arbitration award:

1. That payments are made at inter&als not

eceeding siteen ;1< days in proportion tothe amount o# work completed=

$. That !nal settlement is made uponcompletion o# the work.

(4N/B5, R5L, /4'L4NT/N6 LCB((7 /// R5L 8/// ,C

;a< +ages shall be paid not less than once e&ery two;$< weeks or twice a month at inter&als not eceeding siteen ;1< days unless payment cannot be made with such regularity due to #orce

ma"eure or circumstances beyond the employerscontrol in which case the employer shall pay thewages immediately a#ter such #orce ma"eure or circumstances ha&e ceased.

;b< /n case o# payment o# wages by results in&ol&ingwork which cannot be !nished in two ;$< weeks payment shall be made at inter&als not eceeding siteen days in proportion to theamount o# work completed. inal settlement shallbe made immediately upon completion o# thework.

x------------------------------------x

1.1." Payment By Results

LC ART. 101Payment by results. The ,ecretary o# Labor andmployment shall regulate the payment o# wages by results including pakyao piecework and other nontime work in order to ensure the payment o# #air andreasonable wage rates pre#erably through time andmotion studies or in consultation withrepresentati&es o# workersI and employersI organi>ations.

(4N/B5, R5L, /4'L4NT/N6 LCB((7 /// R5L 8// A ,C O

Se$. 5. Payment of 6esults.(n petition o# any interested party or upon itsinitiati&e the *epartment o# labor shall use alla&ailable de&ises including the use o# time andmotion studies and consultation with representati&eso# employersI and workersI organi>ations todetermine whether the employees in any industry or enterprise are being compensated in accordancewith the minimum wage re2uirements o# this Rule.

;b< The basis #or the establishment o# rates #or piece output or contract work shall be the

1"

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 16/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

per#ormance o# an ordinary worker o# minimum skill or ability.

;c< An ordinary worker o# minimum skill or ability is the a&erage worker o# the lowest producing

group representing @0F o# the total number o# employees engaged in similar employment in a particular establishment ecludinglearners apprentices and handicappedworkers employed therein.

;d< +here the output rates established by theemployer do not con#orm with the standards prescribed herein or with the rates prescribed by the *epartment o# Labor in anappropriate order the employees shallentitled to the di3erence between the amount

to which they are entitled to recei&e under such prescribed standards or rates and that actually paid them by the employer.

x------------------------------------x

1.1.A Cirect Payment of Wages

LC ART. 10@3ire$t payment of "ages. +ages shall be paiddirectly to the workers to whom they are dueecept:

a< /n cases o# #orce ma"eure rendering such payment impossible or under other specialcircumstances to be determined by the ,ecretary o# Labor and mployment in appropriateregulations in which case the worker may be paid through another person under writtenauthority gi&en by the worker #or the purpose= or

b< +here the worker has died in which case the

employer may pay the wages o# the deceasedworker to the heirs o# the latter without the

necessity o# intestate proceedings. Theclaimants i# they are all o# age shall eecute anaPda&it attesting to their relationship to thedeceased and the #act that they are his heirs tothe eclusion o# all other persons. /# any o# the

heirs is a minor the aPda&it shall be eecuted onhis behal# by his natural guardian or neto#kin.The aPda&it shall be presented to the employer who shall make payment through the ,ecretary o# Labor and mployment or his representati&e.The representati&e o# the ,ecretary o# Labor andmployment shall act as re#eree in di&iding theamount paid among the heirs. The payment o# wages under this Article shall absol&e theemployer o# any #urther liability with respect tothe amount paid.

x------------------------------------x

1.1.& Pro(i$ition regarding Wages

LC ART. 11$ E 11 'rt. #. Non-interferen$e in disposal of "ages. No employer shall limit or otherwiseinter#ere with the #reedom o# any employee todispose o# his wages. Ke shall not in any manner #orce compel or oblige his employees to purchasemerchandise commodities or other property #romany other person or otherwise make use o# any

store or ser&ices o# such employer or any other person.

'rt. 7. ,age dedu$tion. No employer in hisown behal# or in behal# o# any person shall makeany deduction #rom the wages o# his employeesecept:

/n cases where the worker is insured with his consent by the employer and the deduction is to recompensethe employer #or the amount paid by him as premium on the insurance=

1#

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 17/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

or union dues in cases where the right o# theworker or his union to checko3 has been recogni>edby the employer or authori>ed in writing by theindi&idual worker concerned= and

/n cases where the employer is authori>ed by law or regulations issued by the ,ecretary o# Labor andmployment.

'rt. +. 3eposits for loss or damage. Noemployer shall re2uire his worker to make deposits#rom which deductions shall be made #or thereimbursement o# loss o# or damage to toolsmaterials or e2uipment supplied by the employerecept when the employer is engaged in suchtrades occupations or business where the practice o#

making deductions or re2uiring deposits is arecogni>ed one or is necessary or desirable asdetermined by the ,ecretary o# Labor andmployment in appropriate rules and regulations.

'rt. . 8imitations. No deduction #rom thedeposits o# an employee #or the actual amount o# theloss or damage shall be made unless the employeehas been heard thereon and his responsibility hasbeen clearly shown.

'rt. . ,ithholding of "ages and %i$%ba$%s

prohibited. /t shall be unlaw#ul #or any persondirectly or indirectly to withhold any amount #romthe wages o# a worker or induce him to gi&e up any part o# his wages by #orce stealth intimidationthreat or by any other means whatsoe&er without the workerIs consent.

'rt. 0. 3edu$tion to ensure employment. /t shall be unlaw#ul to make any deduction #rom thewages o# any employee #or the bene!t o# theemployer or his representati&e or intermediary as

consideration o# a promise o# employment or retention in employment.

'rt. 5. 6etaliatory measures. /t shall beunlaw#ul #or an employer to re#use to pay or reduce

the wages and bene!ts discharge or in any manner discriminate against any employee who has !led any complaint or instituted any proceeding under thisTitle or has testi!ed or is about to testi#y in such proceedings.

'rt. 1. False reporting. /t shall be unlaw#ul #or any person to make any statement report or record!led or kept pursuant to the pro&isions o# this Codeknowing such statement report or record to be #alsein any material respect.

(4N/B5, R5L, /4'L4NT/N6 LCB((7 /// R5L 8/// ,C 11

1$

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 18/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

1.2 Xey Pro)isions in t(e Wage RationaliHation ct *R "2A21.2.1 National Wage +ommission and t(e Regional Wages

and Producti)ity Board

1.2.2 W(at is a Wage rder4 <tandards+riteria for

=inimum Wage Fixing

1.2./ Wage Cistortion

LC ART. 100Prohibition against elimination or diminution of benets. Nothing in this Book shall be construed toeliminate or in any way diminish supplements or other employee bene!ts being en"oyed at the time o# promulgation o# this Code.

LC ART. 1$%

Non-diminution of benets. No wage order issuedby any regional board shall pro&ide #or wage rateslower than the statutory minimum wage rates prescribed by Congress.

x------------------------------------x

1.2./.1,cope o# Legal (bligation to Correct +age*istortion

BAN4ARD # NLRCFacts:

6ssue:

9eld:

x------------------------------------x

1.2./.2Concept o# Classi!cation

Na%o$al +ede!a%o$ # NLRC

Facts:

6ssue:

9eld:

x------------------------------------x

1.2././ /ntentional Quantitati&e *i3erences

Me%!o"ol%a$ Ba$k # NLRCFacts:

• Petitioners entered into a +B on =ay 1%&% #it( respondent$an35 #(ic( granted a #age increase of:- P%00mo eKecti)e 1%&%- P"00mo for 1%%0

- P200mo for 1%%1• n 1%&%5 only t(e regular employees #ere gi)en t(e

P%00mo increase• n Duly 1%&%5 R "A2A #as enacted5 xing ne# #age rates

- =inimum #age #as increased $y P2;- Pro)ided5 t(ose already recei)ing a$o)e minimum #age

up to P100 s(all also recei)e P2; increase in t(e daily#age

• Respondent $an3 ga)e P2; increaseday or PA;0mo to itspro$ationary employees or to t(ose #(o #ere ust promotedto regular5 $ut #ere still recei)ing P100 and $elo#

•

Petitioners contend t(at R "A2A resulted in categoriHationof:1. Pro$ationary employees as of enactment of R "A2A 7

t(ose promoted to regular status $ut recei)ing P100 orless

2. Regular employees as of Danuary 1%&% #it( o)erP100day #age

• Petitioners a)er t(at t(is reduced t(e salary gap

• Ban3 said only ".&Q of regular employees $eneted from#age increase

• , ruled in fa)or of petitioners5 saying t(ere 6< #agedistortion

1%

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 19/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

- 6t is enoug( t(at t(ere is a <>>R> +NR+6N of t(eintentional ?uantitati)e diKerence in #age rates $et#eenemployee groups

• N,R+ re)ersed ,

• Presiding +ommissioner Bonto-PereH of N,R+ dissented:

- Ouantitati)e diKerence $et#een t(ose regular as of enactment of +B and t(ose regulariHed only F>R #as+NR+>C $y more or less &/Q

- >?uita$le remedy #ould $e to correct t(at #agestructure $ased on formula suggested $y Regional ripartite Wages and Producti)ity +ommission

o =inimum Wage V Q x 6ncrease V dustmentctual <alary Prescri$ed

6ssue: WN R "A2A mandating an increase in pay of P2; created a#age distortion8

9eld: Ees. (ere is #age distortion.

Wage distortion is dened as a situation #(ere an increasein prescri$ed #age results in t(e elimination or <>>R>+NR+6N of intentional ?uantitati)e diKerences in#age or salary rates $et#een and among employee groupsin an esta$lis(ment as to eKecti)ely o$literate t(edistinctions em$odied in suc( #age structure $ased ons3ills5 lengt( of ser)ice5 or ot(er logical $ases of diKerentiation.

(e la# does not re?uire t(e complete elimination of t(ediKerence or gap $et#een t(e salary groups. 6t is enoug(t(at t(ere is a se)ere contraction or an extreme decrease int(e diKerence $et#een suc( groups.

(e +B set t(e intentional ?uantitati)e diKerence #(en itagreed to gi)e a P%00 increasemo to t(ose alreadyregulariHed as of t(e eKecti)ity of t(e +B. <ince t(eincrease #as granted only to t(ose #(o #ere not $enetted$y t(e +B5 t(e gap $et#een t(e 2 groups lessened. (us5t(ere is a need to adust t(e salary of t(ose #(o #ere$eneted $y t(e +B $y using t(e formula of t(e Presiding+ommissioner.

x------------------------------------x

1.2./.'3ect o# CBA subse2uent to the increase

PI Ma$',ac%'!$* # PI M,* S'"e!#(o!( a$d +o!e)e$Facts:

• R ""'0 #as enacted on Cecem$er 105 1%&Apro)iding for statutory minimum #age rates:- 10day- except non-agri #or3ers 7 t(ose outside == #(o

s(all recei)e an 11day increase- t(ose already recei)ing minimum #age up to

100day s(all recei)e increase of 10day• P6=<F *respondents entered into ne# +B on

Cecem$er 1&5 1%&A #it( petitioners after enactmentof said la#

- <uper)isors get increase of "2;mo- Foremen get increase of 'A;mo

• +B #as made to retroact to =ay 1%&A prior topassage of R ""'0 until 1%&%

• Respondents allege a #age distortion resulting fromimplementation of R

• , ruled in fa)or of respondents- Cecision stated t(at union cannot #ai)e future

$enets- 1/.;Q increase s(ould also $e gi)en to t(e

foremen 7 super)isorso

=inimum #age #as ;'dayo 6ncrease of 10day5 ma3ing it "'day is

1/.;Q• N,R+ aLrmed ,

• Petition for certiorari to <+ $ut referred to + $asedon udicial (ierarc(y *N,R+ decisions re)ie#ed $y +t(roug( original action on certiorari $efore <+ canre)ie#

• + aLrmed N,R+ $ut modied 1/.;Q to 1&.;Q- (e increase resulting in #age distortions from

t(e implementation of R ""'0 cannot $e #ai)ed

1&

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 20/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

- Petitioners claimed t(at since +B #as signedsu$se?uent to implementation of R5 t(ey #eredeemed to (a)e #ai)ed t(e $enets of suc( R

- 1&.;Q is used $ecause 10day increase of ;'dayis 1&.;Q

6ssue: WN implementation of R ""'0 caused #agedistortion8 E><.WN suc( distortion #as cured $y su$se?uent 1%&A+B8 E><.

Ees. (ere #as #age distortion. But suc( #as cured$y t(e +B.

Wage distortion is t(e disappearance or )irtualdisappearance of pay diKerentials $et#een lo#er 7(ig(er positions in an enterprise $ecause of

compliance #it( a #age order.

(e 2 foremen 7 1 super)isor earning less t(an100day got t(e 10peso increase ma3ing t(em earnmore t(an t(ose #(o (a)e seniority in t(e company. (is eliminated t(e intentional ?uantitati)ediKerence in #age rates. 9o#e)er5 t(is #as cured#(en t(e +B #as enacted5 increasing t(e mont(lypay of super)isors $y "2;pesos more t(an dou$let(e 10day granted $y R ""'05 7 'A;pesos almostdou$le t(e R increase.

(e gap $roug(t a$out $y R ""'0 #as re-esta$lis(ed $y t(e enactment of t(e +B. >)ent(oug( suc( #as not t(e result of a special grie)anceprocedure5 suc( cannot $e ignored. Respondentscannot enoy t(e $enets of t(e +B $ut ignore t(econcessions )oluntarily extended to petitioners.

x------------------------------------x

1.2./.;*isparity between regions

P!'ba$ke!( A((oc # P!'de$%al Ba$k

Facts:• Regional ripartite Wages 7 Producti)ity Board of Region

ordered an increase in cost of li)ing allo#ance *+, $y1A.;0 in Naga 7 ,egaspi5 1;.;0 in a$aco municipality 7 /ot(ers5 and 10.00 for all ot(ers.

• RWPB of Region 66 issued anot(er order mandating t(eincrease in +, $y 10pesos in +e$u5 =andaue 7 ,apulapu5and ;pesos in t(e ot(ers.

• Respondent $an3 implemented t(e orders on its employeesin said regions.

• Petitioners contend t(at t(e #age increase s(ould $eimplemented to all its employees e)en outside Regions 7665 as t(is caused a #age distortion.

• r$itration committee ruled in fa)or of $an3.

• + aLrmed.- underlying considerations in issuing #age orders are

di)erse5 $ased on distincti)e situations in eac( region- distinctions in t(e region are maintained despiteimplementation of t(e orders5 as all its employees #eregranted t(e #age increase.

6ssue: WN #age distortion resulted from implementation of t(e#age orders8

9eld: No. (ere #as no #age distortion.

Ouantitati)e diKerence remained t(e same in all $ranc(es int(e aKected region. Cisparity in #ages among t(ose located

in t(e same rungs in t(e corporate ladder5 $ut in diKerentregions5 does not constitute #age distortion. Wage distortionarises #(en #age order results in #age parity $et#eenemployees in diKerent rungs $ut in t(e same region5 not t(eot(er #ay around.

R "A2A *Wage RationaliHation ct recogniHes t(e existingregional disparities in t(e cost of li)ing. 6n determining #ageincreases5 t(e $oard loo3s at t(e existing regional disparitiesin t(e +, and ot(er socio-economic factors. Wages inot(er areas may $e increased to pre)ent migration to t(eN+R5 (ence5 decongesting t(e metropolis. (ere are5 after

20

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 21/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

all5 diKerent needs for diKerent situations in diKerent regionsof t(e country.

(is does not )iolate e?ual pay for e?ual #or3 $ecause t(ereare )arying necessities in eac( region 7 t(e increase #ill $e

$ased on suc( pre)ailing situations.

(e $an3 in its entirety is also not #(at t(e la# en)isions asan Iesta$lis(mentJ for t(e purposes of determining #agedistortions. <ection 1/ of R "A2A pro)ides t(at t(eminimum #age rates in $ranc(es of esta$lis(ments in oroutside t(e N+R s(all $e t(ose applica$le in t(e P,+>W9>R> 9>E R> <N+6N>C.

(ere #as also no management practice5 as t(e $an3 onlyimplemented t(e uniform #age policy $efore t(e enactmentof R "A2A. <ince t(en5 t(ey #ere mandated to regionaliHe

its #age structure. single instance cannot e?uate tomanagement practice.

,ide issue: (ere #as forum s(opping. )oluntaryar$itration case #as still pending #(en t(e case #as led#it( t(e courts. >lements of litis pendentia are present.

1. <ame parties2. <ame rig(ts 7 relief prayed for/. Dudgment rendered in one #ill amount to res udicata

in t(e ot(erlt(oug( )oluntary ar$itration issue #as #(et(er adoptionof #age orders are )alid 7 $inding4 #(ile t(e one in t(e

courts #as #(et(er t(ere #as #age distortion5 it still $oilsdo#n to one issue: )alidity of t(e $an3@s regionaliHing its#age structure $ased on t(e #age orders.

x------------------------------------x

1.2.' Wage RationaliHation ct Y' *c 7 *d

*c >xempted from t(e pro)isions of t(is ct are(ouse(old or domestic (elpers and personsemployed in t(e personal ser)ice of anot(er5including family dri)ers.

Retailser)ice esta$lis(ments regularly employingnot more t(an ten *10 #or3ers may $e exemptedfrom t(e applica$ility of t(is ct upon application#it( and as determined $y t(e appropriate

Regional Board in accordance #it( t(e applica$lerules and regulations issued $y t(e +ommission.W(ene)er an application for exemption (as $eenduly led #it( t(e appropriate Regional Board5action on any complaint for alleged non-compliance #it( t(is ct s(all $e deferredpending resolution of t(e application forexemption $y t(e appropriate Regional Board.

6n t(e e)ent t(at applications for exemptions arenot granted5 employees s(all recei)e t(eappropriate compensation due t(em as pro)ided

for $y t(is ct plus interest of one per cent *1Qper mont( retroacti)e to t(e eKecti)ity of t(isct.

*d 6f expressly pro)ided for and agreed upon in t(ecollecti)e $argaining agreements5 all increases int(e daily $asic #age rates granted $y t(eemployers t(ree */ mont(s $efore t(e eKecti)ityof t(is ct s(all $e credited as compliance #it(t(e increases in t(e #age rates prescri$ed (erein5pro)ided t(at5 #(ere suc( increases are less t(ant(e prescri$ed increases in t(e #age rates under

t(is ct5 t(e employer s(all pay t(e diKerence.<uc( increases s(all not include anni)ersary#age increases5 merit #age increases and t(oseresulting from t(e regulariHation or promotion of employees.

W(ere t(e application of t(e increases in t(e#age rates under t(is <ection results indistortions as dened under existing la#s in t(e#age structure #it(in an esta$lis(ment and gi)esrise to a dispute t(erein5 suc( dispute s(all rst$e settled )oluntarily $et#een t(e parties and in

21

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 22/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

t(e e)ent of a deadloc35 t(e same s(all $e nallyresol)ed t(roug( compulsory ar$itration $y t(eregional $ranc(es of t(e National ,a$or Relations+ommission *N,R+ (a)ing urisdiction o)er t(e#or3place.

6t s(all $e mandatory for t(e N,R+ to conductcontinuous (earings and decide any disputearising under t(is <ection #it(in t#enty *20calendar days from t(e time said dispute isformally su$mitted to it for ar$itration. (ependency of a dispute arising from a #agedistortion s(all not in any #ay delay t(eapplica$ility of t(e increase in t(e #age ratesprescri$ed under t(is <ection.

x------------------------------------x

1.2.; Wage RationaliHation ct Y12

ny person. corporation. trust. rm. parmersnip.association or entity #(ic( refuses or fails to pay anyof t(e prescri$ed increases or adustments in t(e#age rales made in accordance #it( t(is ct s(all $epunis(ed $y a ne not less t(an #enty-)et(ousand pesos *P2;.000 nor more t(an ne(undred t(ousand pesos *P100.000 or imprisonmentof not less t(an t#o *2 years nor more t(an four *'years or $ot( suc( ne and imprisonment at t(e

discretion of t(e court:Pro)ided. (at any person con)icted under t(is cts(all not $e entitled to t(e $enets pro)ided forunder t(e Pro$ation ,a#.

(e employer concerned s(all $e ordered to pay anarnount e?ui)alent to dou$le t(e unpaid $enetso#ing to t(e employees: Pro)ided. (at payment of indemnity s(all not a$sol)e t(e employer from t(ecriminal lia$ility imposa$le under t(is ct.

6f t(e )iolation is committed $y a corporation. trust orrm. partners(ip5 association or any ot(er entity5 t(epenalty of imprisonment s(all $e imposed upon t(eentityZs responsi$le oLcers including $ut not limitedto t(e president5 )icepresident5 c(ief executi)e

oLcer5 general manager5 managing director orpartner.

x------------------------------------x

1.2." Wage rder N+R-1"

1. (e P22.00 per day +, prescri$ed in t(is rders(all apply to all minimum #age earners in t(epri)ate sector in N+R5 regardless of t(eir position5designation or status of employment andirrespecti)e of t(e met(od $y #(ic( t(ey are

paid4

2. (e P22.00 per day +, s(all N co)er(ouse(old or domestic (elpers5 persons in t(epersonal ser)ice of anot(er5 including familydri)ers5 and #or3ers of duly registered Barangay=icro Business >nterprises *B=B>s #it(+erticates of ut(ority pursuant to Repu$lic ct%1A&4

/. (e follo#ing may $e exempted from t(eapplica$ility of t(e Wage rder: 1 Cistressed

>sta$lis(ments4 2 Retail<er)ice >sta$lis(mentsRegularly >mploying Not =ore (an en *10Wor3ers4 / >sta$lis(ments #(ose otal ssetsincluding t(ose arising from loans $ut exclusi)e of t(e land on #(ic( t(e particular $usiness entity@soLce5 plant and e?uipment are situated5 are notmore t(an P/ =illion4 and ' >sta$lis(mentsd)ersely Kected $y Natural +alamities.

'. (is rder s(all not reduce any existing #agerates5 allo#ances and $enets of any form underexisting la#s5 decrees5 issuances5 executi)e

22

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 23/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

orders andor under any contract or agreement$et#een t(e #or3ers and employers4

;. (is rder s(all not pre)ent #or3ers in particularrms or industries from $argaining for (ig(er

#ages #it( t(eir respecti)e employers4

". ny increase granted $y an employer in anorganiHed esta$lis(ment #it(in t(ree */ mont(sprior to t(e eKecti)ity of t(is rder s(all $ecredited as compliance #it( t(e prescri$edincrease set fort( (erein5 pro)ided t(at anagreement to t(is eKect (as $een forged$et#een t(e parties or a collecti)e $argainingagreement pro)ision allo#ing credita$ility exists.6n t(e a$sence of suc( an agreement or pro)isionin t(e +B5 any increase granted $y t(e employer

s(all not $e credited as compliance #it( t(e+, prescri$ed in t(is rder.

6n case t(e increases gi)en are less t(an t(eprescri$ed +,5 t(e employer s(all pay t(ediKerence. <uc( increases s(all not includeanni)ersary increases5 merit #age increases andt(ose resulting from t(e regulariHation orpromotion of employees.

A. 6n unorganiHed esta$lis(ments5 any increasegranted $y t(e employer #it(in )e *; mont(s

prior to t(e eKecti)ity of t(is rder s(all $ecredited as compliance t(ere#it(.

6n case t(e increases gi)en are less t(an t(eprescri$ed +,5 t(e employer s(all pay t(ediKerence. <uc( increases s(all not includeanni)ersary increases5 merit #age increases andt(ose resulting from t(e regulariHation orpromotion of employees.

&. 6n t(e case of contracts for construction proectsand for security5 anitorial and similar ser)ices5

t(e +, prescri$ed in t(is rder s(all $e $orne$y t(e principals or clients of t(econstructionser)ice contractors and t(e contracts(all $e deemed amended accordingly.

6n t(e e)ent5 (o#e)er5 t(at t(e principals orclients fail to pay t(e prescri$ed #age rates5 t(econstructionser)ice contractor s(all $e ointlyand se)erally lia$le #it( (is principal or client.

%. 6n t(e case of pri)ate educational institutions5 t(es(are of co)ered #or3ers and employees in t(eincrease in tuition fees for <c(ool Eear 2011-2012s(all $e considered as compliance #it( t(e +,prescri$ed (erein. 9o#e)er5 payment of anys(ortfall in t(e #age increase set fort( (ereins(all $e co)ered starting <c(ool Eear 2012-201/.

Pri)ate educational institutions #(ic( (a)e notincreased t(eir tuition fees for <c(ool Eear 2011-2012 may defer compliance #it( t(e +,prescri$ed (erein until t(e $eginning of <c(ool Eear 2012-201/.

6n any case5 all pri)ate educational institutionss(all implement t(e +, prescri$ed (ereinstarting <c(ool Eear 2012-201/.

10.ll #or3ers paid $y result5 including t(ose #(o

are paid on piece#or35 Ita3ayJ or tas3 $asis5 s(all$e entitled to recei)e not less t(an t(e prescri$ed+, a day5 or a proportion t(ereof for #or3ingless t(an eig(t *& (ours4

11.Wages of apprentices and learners s(all in nocase $e less t(an se)enty-)e percent *A;Q of t(e applica$le ne# #age rates prescri$ed in t(isrder.

ll recogniHed learners(ip and apprentices(ipagreements entered into $efore t(e eKecti)ity of

2

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 24/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

t(is rder s(all $e considered automaticallymodied insofar as t(eir #age clauses areconcerned to re[ect t(e ne# #age rates.

ll ?ualied (andicapped #or3ers s(all recei)e

t(e full amount of t(e ne# #age rates prescri$ed(erein pursuant to Repu$lic ct No. A2AA5ot(er#ise 3no#n as t(e =agna +arta for Cisa$ledPersons.

x------------------------------------x

1./ 9ours of Wor3 Nig(t <(ift5 )ertime

LC Art. O$0A!%. 56. Co#e!a*e. (e pro)isions of t(is itle s(allapply to employees in all esta$lis(ments and

underta3ings #(et(er for prot or not5 $ut not togo)ernment employees5 managerial employees5 eldpersonnel5 mem$ers of t(e family of t(e employer#(o are dependent on (im for support5 domestic(elpers5 persons in t(e personal ser)ice of anot(er5and #or3ers #(o are paid $y results as determined$y t(e <ecretary of ,a$or in appropriate regulations.

s used (erein5 \managerial employees\ refer tot(ose #(ose primary duty consists of t(emanagement of t(e esta$lis(ment in #(ic( t(ey areemployed or of a department or su$di)ision t(ereof5

and to ot(er oLcers or mem$ers of t(e managerialstaK.

\Field personnel\ s(all refer to non-agriculturalemployees #(o regularly perform t(eir duties a#ayfrom t(e principal place of $usiness or $ranc( oLceof t(e employer and #(ose actual (ours of #or3 int(e eld cannot $e determined #it( reasona$lecertainty.

A!%. 57. No!)al -o'!( o, o!k. (e normal (oursof #or3 of any employee s(all not exceed eig(t *&(ours a day.

9ealt( personnel in cities and municipalities #it( a

population of at least one million *150005000 or in(ospitals and clinics #it( a $ed capacity of at leastone (undred *100 s(all (old regular oLce (ours foreig(t *& (ours a day5 for )e *; days a #ee35exclusi)e of time for meals5 except #(ere t(eexigencies of t(e ser)ice re?uire t(at suc( personnel#or3 for six *" days or forty-eig(t *'& (ours5 in#(ic( case5 t(ey s(all $e entitled to an additionalcompensation of at least t(irty percent */0Q of t(eirregular #age for #or3 on t(e sixt( day. For purposesof t(is rticle5 \(ealt( personnel\ s(all includeresident p(ysicians5 nurses5 nutritionists5 dietitians5

p(armacists5 social #or3ers5 la$oratory tec(nicians5paramedical tec(nicians5 psyc(ologists5 mid#i)es5attendants and all ot(er (ospital or clinic personnel.

A!%. 58. Ho'!( o!ked. 9ours #or3ed s(all include*a all time during #(ic( an employee is re?uired to$e on duty or to $e at a prescri$ed #or3place4 and*$ all time during #(ic( an employee is suKered orpermitted to #or3.

Rest periods of s(ort duration during #or3ing (ourss(all $e counted as (ours #or3ed.

A!%. 59. Meal "e!od(. <u$ect to suc( regulationsas t(e <ecretary of ,a$or may prescri$e5 it s(all $et(e duty of e)ery employer to gi)e (is employees notless t(an sixty *"0 minutes time-oK for t(eir regularmeals.

A!%. 5. N*-% (-,% d;e!e$%al. >)ery employees(all $e paid a nig(t s(ift diKerential of not less t(anten percent *10Q of (is regular #age for eac( (ourof #or3 performed $et#een ten o@cloc3 in t(ee)ening and six o@cloc3 in t(e morning.

2!

8/18/2019 Special Problems in Business Law Prac Module 1

http://slidepdf.com/reader/full/special-problems-in-business-law-prac-module-1 25/139

Business Law Practice Noel | PangcogAtty. Jose Cochingyan III AY 2011-2012

A!%. 5<. O#e!%)e o!k. Wor3 may $e performed$eyond eig(t *& (ours a day pro)ided t(at t(eemployee is paid for t(e o)ertime #or35 an additionalcompensation e?ui)alent to (is regular #age plus at

least t#enty-)e percent *2;Q t(ereof. Wor3performed $eyond eig(t (ours on a (oliday or restday s(all $e paid an additional compensatione?ui)alent to t(e rate of t(e rst eig(t (ours on a(oliday or rest day plus at least t(irty percent */0Qt(ereof.

A!%. 55. U$de!%)e $o% o;(e% by o#e!%)e.ndertime #or3 on any particular day s(all not $eoKset $y o)ertime #or3 on any ot(er day. Permissiongi)en to t(e employee to go on lea)e on some ot(erday of t(e #ee3 s(all not exempt t(e employer from

paying t(e additional compensation re?uired in t(is+(apter.

A!%. 5=. E)e!*e$cy o#e!%)e o!k. nyemployee may $e re?uired $y t(e employer toperform o)ertime #or3 in any of t(e follo#ing cases:

W(en t(e country is at #ar or #(en any ot(ernational or local emergency (as $een declared $yt(e National ssem$ly or t(e +(ief >xecuti)e4 W(en it is necessary to pre)ent loss of life or

property or in case of imminent danger to pu$licsafety due to an actual or impending emergency int(e locality caused $y serious accidents5 re5 [ood5typ(oon5 eart(?ua3e5 epidemic5 or ot(er disaster orcalamity4 W(en t(ere is urgent #or3 to $e performed onmac(ines5 installations5 or e?uipment5 in order toa)oid serious loss or damage to t(e employer orsome ot(er cause of similar nature4

W(en t(e #or3 is necessary to pre)ent loss ordamage to peris(a$le goods4 and W(ere t(e completion or continuation of t(e #or3started $efore t(e eig(t( (our is necessary to

pre)ent serious o$struction or preudice to t(e$usiness or operations of t(e employer.ny employee re?uired to render o)ertime #or3under t(is rticle s(all $e paid t(e additionalcompensation re?uired in t(is +(apter.

A!%. =>. Co)"'%a%o$ o, add%o$alco)"e$(a%o$. For purposes of computing o)ertimeand ot(er additional remuneration as re?uired $y t(is+(apter5 t(e \regular #age\ of an employee s(allinclude t(e cas( #age only5 #it(out deduction onaccount of facilities pro)ided $y t(e employer.

(mnibus /mplementing Rules Labor Code Book ///RULE I3A

Ho'!( o, ?o!k o, Ho("%al a$d Cl$c Pe!(o$$el

SECTION 1. Ge$e!al (%a%e)e$% o$ co#e!a*e. ] (is Rule s(all apply to:

*a ll (ospitals and clinics5 including t(ose #it( a$ed capacity of less t(an one (undred *100 #(ic(are situated in cities or municipalities #it( apopulation of one million or more4 and

*$ ll (ospitals and clinics #it( a $ed capacity of atleast one (undred *1005 irrespecti)e of t(e siHe of t(e population of t(e city or municipality #(ere t(eymay $e situated.