TeachME Financial Literacy Information and Resources to Help Your Students

Achieve the New Maine Learning Results Standards

David G. Lemoine, Maine State Treasurer

Why is financial literacy important?

High School Students Most 18-year-olds can

obtain credit cards in their own name.

Credit-card companies have become more aggressive at marketing to young people.

College Students Two-thirds of college

students have a credit card; the average is 3 cards per student.

About 64% pay off the balance each month.

The average credit-card debt for students who carry a balance is $2,200-$2,800.

Source: “Learning, Earning and Investing,” NCEE 2004

The Financial World Has Become More Complex

The Internet has increased the number of financial services offered to consumers.

Credit-scoring technology has improved.

There has been an increase in the number of financial products that are offered.

It’s Hard to Learn What You Are Not Taught

Personal finance is a growing national priority. 40 states (up from 34 in 2004 and 21 in 1998) have adopted personal finance educational standards.*

But young people can’t learn financial skills unless they are taught.

*Source: NCEE 2007 Survey of the States report card

The New Maine Learning Results: Parameters for Essential Instruction

Students draw on concepts and processes from economics to understand issues of personal finance.

(Chapter 132, Section C, Revised Maine Learning Results Standards, Social Studies)

The New Maine Learning Results

Economic Knowledge, Concepts, Themes, and

Patterns (Chapter 132, Section C1)

Pre-Kindergarten-2nd Grade

Result: Students understand the nature of economics as well as key foundation ideas.

Pre-K-2 (continued)

Students must…

- Describe economics as how people make choices about how to use scarce resources to meet their wants and needs.

- Describe how money is earned and managed in order to buy goods and services and save for the future.

Attaining the benchmark Students identify examples of jobs and entrepreneurs

in their community (i.e. teacher, fireman, banker, parents or other family members)

Students understand that grown-ups go off to work each day, and that they work in order to earn money and buy things (such as food, a house, etc.)

Students gain excitement about employment or business

Source: Jumpstart Coalition

“The darkest hour in any man’s life is when he sits down to plan how to get money without earning it.”

- Horace Greely

3rd Grade-5th Grade

Result: Students understand personal economics.

3rd Grade-5th Grade (continued)

Students must…

- Describe situations in which personal choices are related to the use of financial resources and financial institutions including the use of money, consumption, savings, investment, and banking.

Attaining the benchmark Students identify different places where people put

their money (i.e. banks, credit unions, investment firms, etc.)

Students identify different kinds of accounts and their purposes (checking, saving, certificates of deposit, stocks, retirement accounts, college savings, etc.)

Students take a field trip to a financial institution Banker, credit union officer or broker comes to the

classroom and makes a presentationSource: Jumpstart

“A bank is a place that will lend you money if you can prove that you don’t need it.”

- Bob Hope

6th Grade-8th Grade

Result: Students understand the principles and processes of personal economics.

6th Grade-8th Grade (continued)

Students must…

- Identify factors that contribute to personal spending and savings decisions including work, wages, income, expenses, and budgets as they relate to the study of individual financial choices.

Attaining the benchmark

Students understand how training and education affect their career choices and income potential

Students understand how to construct a household budget (including expenses and setting money aside for the future)

Source: Jumpstart

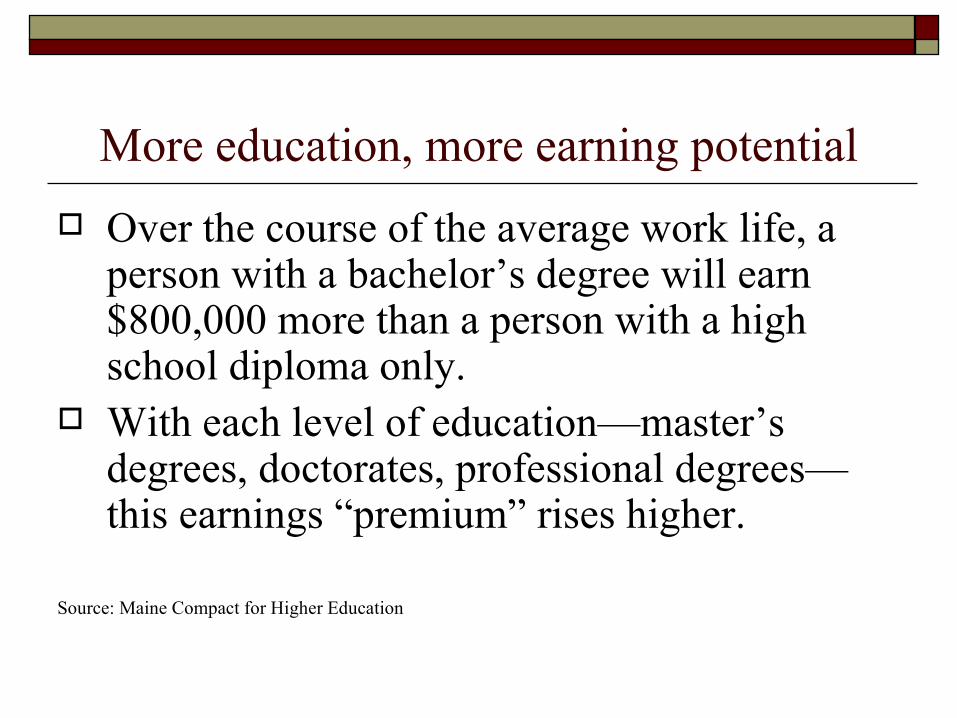

More education, more earning potential

Over the course of the average work life, a person with a bachelor’s degree will earn $800,000 more than a person with a high school diploma only.

With each level of education—master’s degrees, doctorates, professional degrees—this earnings “premium” rises higher.

Source: Maine Compact for Higher Education

“The trouble with being educated is that it takes a long time, it uses up the better part of your life, and when you are finished what you know is that you would have benefited more by going into banking.”

- Philip K. Dick

9th Grade-Diploma

Result: Students understand the principles and processes of personal economics.

9th Grade-Diploma (continued) Students must…

- Explain how the study of economics is the basis of individual personal finance management including saving and investing.

- Evaluate different forms of money management, and the positive and negative impacts that credit can have on individual finances, using economic reasoning.

Attaining the benchmark Students understand the reasons for saving for the

short term (an upcoming vacation, an emergency fund for car repairs, etc.)

Students understand the reasons for saving for the long term (college, to buy a house, for retirement, etc.)

Students understand the value of investing and different investment options for different goals

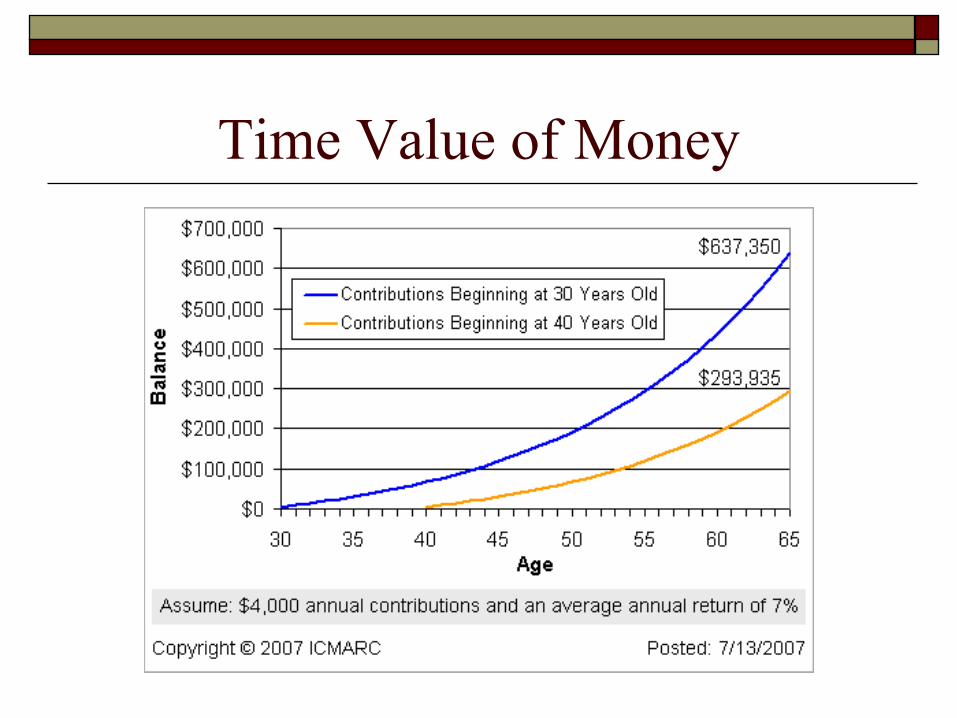

Students understand the time value of money (compounding interest)

Source: Jumpstart

Time Value of Money

Attaining the benchmark (cont.) Students understand different forms of credit and

debt Students understand positive and negative impacts of

a credit card Positive: building a credit history for future Negative: accumulation of debt leading to inability to

make payments; inability to access future credit because of damaged credit history

Source: Jumpstart

“I went to the bank and went over my savings. I found out I have all the money that I’ll ever need…if I die tomorrow.”

- Henny Youngman

Financial Literacy Resources America Saves

(202) 387-6121 www.americasaves.org

American Financial Services Association Education Foundation 919 18th St., N.W. Washington, DC 20006-5503 (202) 296-5544 www.afsaef.org

Resources (continued) Choose to Save® Education Program

Employee Benefit Research Institute/American Savings Education Council 2121 K St., N.W., Suite 600 Washington, DC 20037-1896 (202) 775-9130 www.choosetosave.org

Financial Services Education Coalition Financial Management ServiceU.S. Treasury 401 14th Street, S.W., Room 304D Washington, DC 20024-2106 (202) 874-6908 or fax: (202) 874-7321 www.occ.treas.gov/cdd/finlitresdir.htm

Resources (continued) Jump$tart Coalition for Personal Financial Literacy

919 18th St., N.W., Suite 300 Washington, DC 20006-5517 (888) 45-EDUCATE www.jumpstartcoalition.org

Institute for Financial LiteracyP.O. Box 1842Portland, ME 04104 www.financiallit.org

National Community Reinvestment Coalition Financial Literacy Campaign 733 15th St., N.W., Suite 540 Washington, DC 20005-2129 (202) 628-8866 www.ncrc.org

Resources (continued)

National Council on Economic Education (NCEE)1140 Avenue of the Americas New York, NY 10036-5803 (800) 338-1192 www.ncee.net

National Endowment for Financial Education (NEFE) 5299 DTC Blvd., Suite 1300 Greenwood Village, CO 80111-3334 (303) 741-6333 www.nefe.org

Participate in our November 27, 2007 Teacher Training Seminar!

The State Treasurer’s Office is hosting a financial literacy training seminar for teachers K-12 on Tuesday, November 27, 2007 presented by the National Council on Economic Education (NCEE) and the Jump$tart Coalition.

To register, contact Kevin Thurston, Director of Special Projects at the Treasurer’s Office, at [email protected] or at 624-7476.

For more information…

Visit the State Treasurer’s website at: www.maine.gov/treasurer/teachmefinlit

Recommended