Withholding Taxes and Foreign Portfolio Investment

Martin Jacob

WHU – Otto Beisheim School of Management

Maximilian Todtenhaupt

Norwegian School of Economics and LMU Munich

This draft: March 2020

Abstract

We examine the role of withholding taxes on foreign portfolio

investment (FPI) using data on U.S. mutual fund holdings and on

bilateral FPI. Exploiting variation in withholding tax rates for 38

investor countries and 115 issuer countries over 2008–2015, we find

that, conversely to the intended design of the international tax system,

withholding taxes adversely affect FPI. We show that this is due to

compliance frictions in claiming foreign tax credits. We further provide

evidence that frictions in claiming foreign tax credits are reflected in

lower stock returns in the setting of American Depositary Receipts.

Keywords: Foreign portfolio investment, withholding taxes, shareholder taxation, home bias

JEL codes: D25; G11; G25; H20; H24

We gratefully acknowledge helpful comments from Harald Amberger, Dan Amiram, Tobias Bornemann, Alex

Edwards, Jesse van der Geest, Kevin Markle, Maximilian Müller, Terry Shevlin, Siew Hong Teoh, Ryan Wilson,

Chenqi Zhu, and seminar participants at the University of California, Irvine, WHU – Otto Beisheim School of

Management, and the University of Tuebingen.

1

1 Introduction

With globalization, the removal of trade barriers, and global economic integration, capital markets

are also becoming integrated across borders. In addition to firms directly investing via subsidiaries

abroad—foreign direct investment (FDI)—individual and institutional investors are increasingly

investing in shares of foreign companies. Globally, such foreign portfolio investment (FPI)

witnessed enormous growth, from USD 5 trillion in 2001 to USD 22 trillion in 2015 (12.3% of the

global financial wealth, or 32% of the global market capitalization).1 FPI is an important source of

financing for firms seeking capital to invest and, thus, for economic growth. According to

international portfolio theory (e.g., Adler and Dumas 1983), costs such as withholding taxes on

foreign dividends can theoretically reduce foreign investment (e.g., Cooper and Kaplanis 1986,

1994). On paper, the cross-border taxation of dividends via domestic dividend taxes and foreign

withholding taxes is therefore designed in a capital export–neutral way, which means that the

location of FPI is independent of taxation: Double tax agreements (DTAs) ensure that the

withholding tax rate in the foreign country (where the firm is located) is below the dividend tax

rate in the home country (where the investor is located).2 Since foreign withholding tax payments

are usually fully credited against the domestic dividend tax, they would be rendered irrelevant.

Therefore, cross-border equity investments and individual portfolio decisions should not be

affected by withholding taxes.

However, this irrelevance of withholding taxes for FPI is based on the assumption that

investors claim credits for the foreign withholding tax. In this paper, we challenge this view and

1 Source: Coordinated Portfolio Investment Survey (CPIS), International Monetary Fund (IMF). According to data

from Credit Suisse (Global Wealth Databook 2019), global financial wealth was USD 175.4 trillion in 2015. The

World Federation of Exchanges reports a global market capitalization of USD 67 trillion in 2015. 2 The very few cases with a withholding tax above the final dividend tax 0 F comprise mainly investments from tax havens,

where dividends are usually not tax exempt (e.g., Cayman Islands or Bermuda).

2

examine the effect of compliance frictions in claiming foreign tax credits on FPI. A significant

part of the tax credit—the difference between the withholding tax rate in the respective DTA and

the standard withholding tax in the foreign country—must be actively claimed from foreign tax

authorities, increasing the costs associated with cross-border investments. Anecdotal evidence

suggests substantial compliance issues in this process due to extensive reporting requirements,

lengthy processes, and fees.3 To date, the academic literature on FPI lacks an understanding of this

issue and its consequences.4 We fill this void by showing that compliance hurdles in claiming

foreign withholding tax credits have adverse effects on FPI. In short, although withholding taxes

on dividends should not matter for FPI, since they are designed in a capital export–neutral way,

withholding taxes can affect FPI due to compliance frictions in claiming foreign tax credits.

We build a large data set of dividend withholding tax rates for bilateral combinations of 38

investor countries and 115 issuer countries over the period 2008–2015, taking into account DTAs.

We obtain information on dividend tax rates in the investor’s home country to calculate the country

pair–specific effective dividend tax rate on cross-border FPI, assuming the credit is granted. A

novel aspect of our paper is the computation of what we call the withholding tax overpayment that

the investor must claim from the tax authorities of the foreign country. The withholding tax

overpayment is the difference between the actual tax rate withheld in the foreign country, which

is usually the same for all foreign investors, and the tax rate that is applicable under an effective

DTA for that particular country pair. The important insight highlighted in our paper is that claiming

back the withholding tax overpayment often comes at a high compliance cost. To summarize,

3 For example, the media (e.g., Lodge 2010), policy makers (e.g., European Commission 2016), think tanks (e.g.,

Næss-Schmidt et al. 2012), and investors (e.g., European Federation of Investors 2011) have been alerted that

withholding taxes are burdensome because of compliance issues. 4 For instance, Chan et al. (2005), Ammer et al. (2012), and Amiram and Frank (2016) study the effects of withholding

or dividend taxes on FPI, but do not consider compliance frictions.

3

while the effective dividend tax rate captures tax payments assuming that shareholders are granted

the full tax credit, our withholding tax overpayment variable isolates the compliance hurdle in the

cross-border withholding tax credit system for individual investors.

Our empirical analysis is based on data from two sources. First, we obtain information on

bilateral equity FPI holdings from the IMF’s Coordinated Portfolio Investment Survey (CPIS) over

the period 2008–2015. Second, we obtain foreign portfolio holdings for individual investors and

securities from the Form 13F filings of U.S. institutional investors with the U.S. Securities and

Exchange Commission (SEC).

In our bilateral tests, we exploit the variation in effective dividend taxes and withholding tax

overpayments in a generalized difference-in-differences design, using FPI as the dependent

variable. The level of withholding tax overpayment can change when DTAs change or when issuer

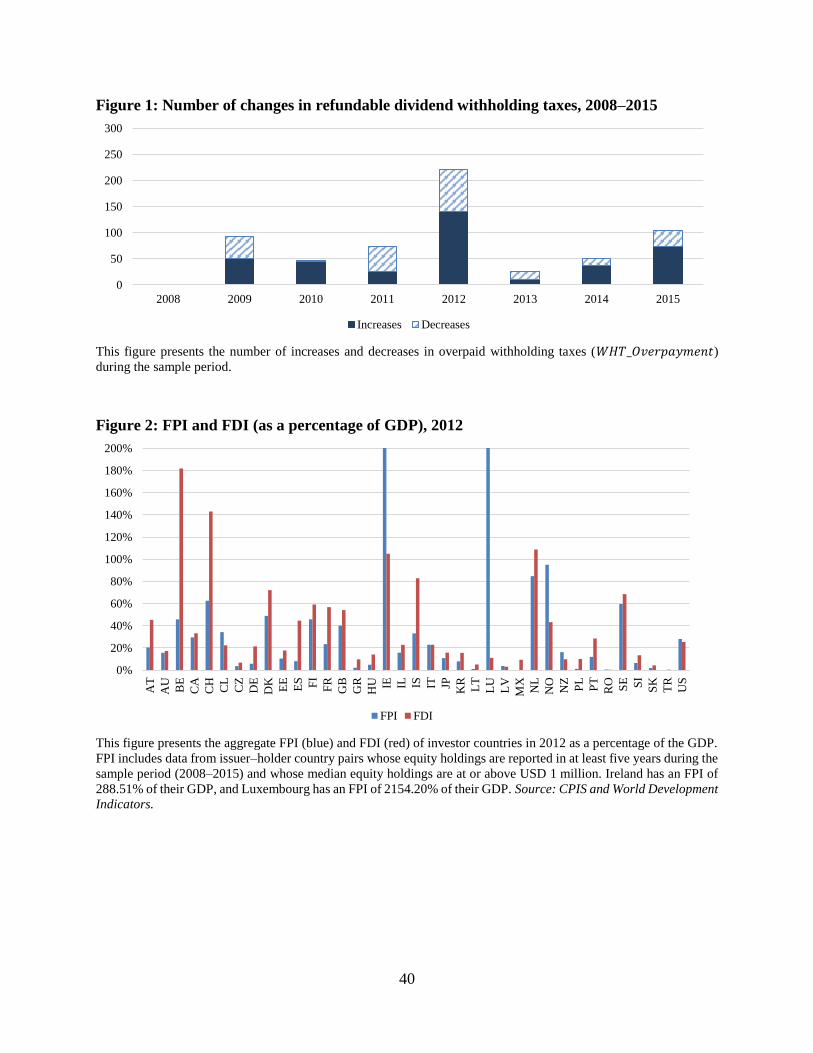

countries reform their withholding tax systems. We observe 616 bilateral changes (383 increases

and 233 decreases) in withholding tax overpayments in our sample. Most of these are driven by

changes in unilateral withholding tax rates, which reduces the likelihood of the changes in our

main independent variable being a response to (the lack of) country pair–specific FPI. We then

compare the FPI for a given country pair experiencing a change in withholding tax overpayment

to another country pair from either the same issuer or the same holder country, but without a change

in withholding tax overpayments (first difference) around the change in withholding tax

overpayment (second difference). The identification approach absorbs any issuer country–year as

well as investor country–year–specific and any time-invariant country pair–specific characteristics

to account for nontax characteristics driving bilateral FPI.

Our main results indeed indicate an economically large effect of compliance hurdles on FPI.

For an average country pair, a one percentage point decrease in withholding tax overpayments in

4

terms of cross-border dividends paid increases the investor country FPI to the issuer country by

2.3%, or USD 186 million.5 Note that the overall FPI in a particular issuer country is the sum of

FPI from all investor countries, such that the overall effect of reducing withholding tax

overpayments for an individual country is likely to be substantial. Consistent with this effect being

driven by dividend payments, we find a stronger tax effect of withholding tax overpayments on

FPI when companies in the foreign country have higher dividend payout ratios. This effect is robust

to the inclusion or exclusion of additional country pair–specific control variables, as well as to the

inclusion of the effective dividend tax rate that accounts for tax incentives, assuming no

compliance issues. Overall, these initial results suggest that compliance issues in claiming

withholding tax credits can have first-order effects on FPI.

Next, we examine the heterogeneity of the effect of compliance issues on FPI. Our argument

is that the statutory withholding tax is not a good proxy for the tax credit actually claimed because

some countries make it inherently complicated to claim withholding tax credits across borders. If,

however, institutional features make these claims less costly, the negative impact of withholding

tax overpayments should be alleviated. For instance, relief-at-source mechanisms that allow for

double tax relief at source by the dividend-paying firm significantly reduce the compliance burden

for the foreign investor. In our empirical tests, we find that this is indeed the case. Further, we also

test whether investors’ frictions in claiming tax credits across borders are lower if a given country

pair shares institutional, economic, or cultural characteristics. We find that the effect of

withholding tax overpayments on FPI becomes weaker for geographically close country pairs (i.e.,

neighboring countries), for pairs of countries that exchange high numbers of visitors, for issuer

countries with higher audit quality, and issuer–investor country pairs within the Eurozone.

5 This is equivalent to a semi-elasticity of -2.3. To put this figure into perspective, the literature review by de Mooij

and Ederveen (2003) reports a semi-elasticity of -3.3 to -4 for FDI with respect to the (corporate) tax rate.

5

We subject our results to two important additional analyses. First, we run a placebo test using

FDI. FDI is distinct from FPI because FDI captures substantial foreign shareholdings (above 10%

ownership), mostly those of corporations. FPI captures smaller equity investments (maximum 10%

ownership), mostly those of individuals or their intermediaries. FDI should not be sensitive to the

compliance issues inherent in our withholding tax overpayment measure, since corporations are

subject to a different withholding tax system, typically with 0% withholding tax rates (Barrios et

al. 2012). Since FDI is affected by the same underlying economic and political conditions in a

given country pair, using FDI as a placebo test addresses concerns that political and economic

conditions are correlated with changes in compliance issues, as well as with changes in FPI. We

find that FDI is uncorrelated with withholding tax overpayments, suggesting that our main results

are not driven by unobserved changes in country pair–specific political or economic conditions.

Second, we provide evidence in favor of the parallel trends assumption. FPI does not respond to

future changes in compliance hurdles, indicating that treated and control country pairs follow a

common trend prior to a change in withholding tax overpayments.

We next examine the role of withholding tax overpayments in FPI at the investor level, using

data on foreign investments by U.S. institutional investors from their mandatory 13F filings with

the SEC. Using this granular investment data, we confirm the findings from the bilateral tests. First,

we find that withholding tax overpayments reduce equity investments in foreign countries. Second,

the existence of a relief-at-source mechanism mutes the adverse effect of withholding tax

overpayments on foreign investments. Third, we find that the adverse effect of withholding tax

overpayments on foreign investments is stronger for firms with higher dividend yields.

We also provide evidence for the mechanism through which frictions in claiming tax credits

can affect FPI. If higher compliance costs for a particular investor decrease that investor’s effective

6

withholding tax credit, the investor’s effective tax burden on the equity investment increases.

Thereby, after-tax returns decline, resulting in lower portfolio investment by that investor. We test

this channel by using the unique setting of American Depositary Receipts (ADRs) and examine

the effect of withholding tax overpayments on ADR returns. In these tests, we benchmark this

return against the return of the underlying stock in its respective home market before the dividend

day. We find that higher withholding tax overpayments reduce the ADR return relative to the

underlying stock. This effect increases with firm dividend yield, since higher dividend yields

amplify the role of withholding tax overpayments. These results are consistent with compliance

issues in claiming tax credits across borders decreasing after-tax returns.

By providing evidence that compliance frictions in the form of withholding tax

(over)payments have adverse effects on FPI, our paper contributes to two streams of the literature.

First, we directly contribute to the literature on the role of taxes on FPI (e.g., Chan et al. 2005;

Ammer et al. 2012). We show that administrative frictions in the process of claiming foreign tax

credits have a first-order impact on cross-border equity investment. Put differently, even though

investors are entitled to the tax credits (ensuring on paper that taxes do not matter for FPI), we

show that complexity in the administrative process of claiming these credits substantially reduces

FPI and inhibits the integration of global capital markets. Thereby, we also expand the literature

that analyzes the direct and indirect effects of dividend taxes on foreign portfolios (Desai and

Dharmapala 2011; Amiram and Frank 2016). Further, our findings are related to the large literature

on the home bias puzzle (e.g., French and Poterba 1991; Cooper and Kaplanis 1994; Lewis 1999)

and explanations of this puzzle, such as asymmetric information between local and foreign

investors (e.g., Coval and Moskowitz 1999). We show that the process of claiming foreign tax

credits creates significant costs for individual investors, reducing investments in foreign shares.

7

Second, we contribute to the literature on the role of taxes in the trading of cross-listed assets

(e.g., Callaghan and Barry 2003), as well as the prices of such assets (Blouin et al. 2009). We show

that not only nominal tax payments but also frictions in claiming tax credits affect asset prices.

Such frictions result in the lower asset prices of ADRs relative to their underlying issues traded in

the home market. Altogether, we show that compliance frictions in claiming tax credits have real

consequences on aggregate cross-border investment, as well as on cross-listed firms’ asset prices.

These effects translate into lower after-tax returns for affected firms. Since lower after-tax returns

imply the provision of less capital, this reduces firm investment. Higher tax revenues from

unclaimed credits could thus come at the cost of reduced investment and economic growth.6

2 Institutional Background and Hypotheses

In most countries, individual investors are taxed on their worldwide capital income,

independently of whether they hold foreign stocks directly, or through institutional investors, as is

the case for the large majority of investors (e.g., Ferreira and Matos 2008). In the latter case, the

foreign income of the institutional investor is either directly passed through as taxable capital

income to the individual shareholder (e.g., as a mutual fund dividend) or affects the individual

shareholder’s taxable returns on his or her investment fund holdings. Individual investors with

direct or indirect foreign equity holdings receiving foreign dividends or realizing capital gains

from selling shares in foreign firms are taxed at the rates applicable in their home country. While

capital gains are only taxed in the home country, foreign dividends can also be taxed abroad, that

is, in the residence country of the dividend-paying company, if that foreign country levies a

withholding tax on dividends. Without appropriate relief, this leads to double taxation, since

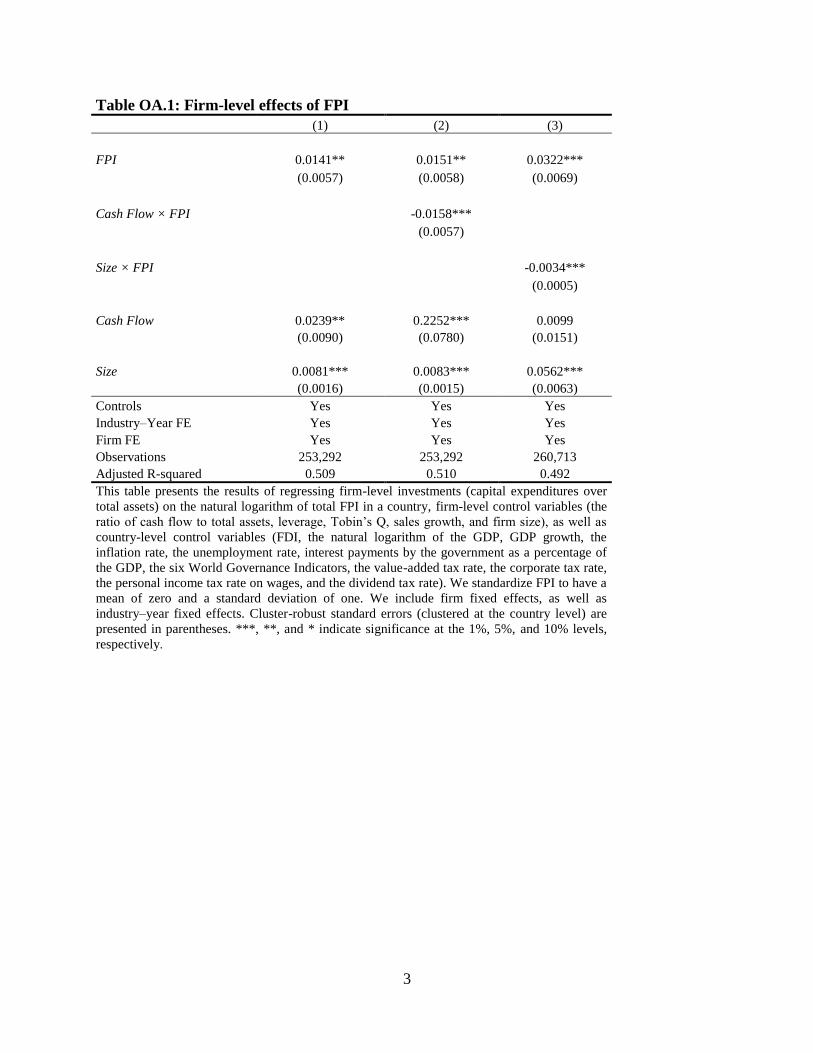

6 To document that the positive relation between FPI and firm-level investment also holds in our sample, we run firm-

level tests, as shown in the Online Appendix. We find that FPI is positively associated with firm-level investment and

that firms’ investments become less sensitive to internal cash flows or financial frictions as FPI increases.

8

foreign-source dividends are taxed more heavily than domestic-source dividends. To illustrate,

consider a foreign-source dividend payment 𝐷 to which the foreign country applies a withholding

tax rate of 𝜏𝑤 and the home country applies a dividend tax rate of 𝜏ℎ , such that the after-tax

dividend is (1 − 𝜏𝑤 − 𝜏ℎ)𝐷. If the same dividend were from a domestic source, the after-tax

dividend would be (1 − 𝜏ℎ)𝐷, implying a double taxation of 𝜏𝑤𝐷.

To mitigate the adverse effects of this double taxation, countries typically allow investors to

credit dividend withholding taxes paid abroad (𝜏𝑤𝐷) against domestic dividend tax payments

(𝜏ℎ𝐷). This approach prevents double taxation if the foreign withholding tax rate is below the

domestic dividend tax rate (𝜏ℎ > 𝜏𝑤). Many countries have therefore signed bilateral DTAs that

limit withholding tax rates (to 10% or 15% for most OECD model treaties). Effectively, this

combination of low withholding tax rates in the foreign country with foreign tax credits results in

capital export neutrality for most country pairs around the world. Hence, FPI is unaffected by

dividend taxes.

However, this argumentation is based on the assumption that the full available credit can be

claimed without additional costs. Due to administrative compliance hurdles, this is rarely the case

in practice because foreign countries initially deduct the standard withholding tax rate applicable

to domestic investors ( 𝜏𝑙𝑜𝑐𝑎𝑙𝑤 ) 7 while the investor’s home country credits only the foreign

withholding tax rate agreed upon in the DTA (𝜏𝐷𝑇𝐴𝑤 ) against domestic dividend taxes. We denote

the remaining credit, that is, the difference between the withholding tax for local investors and the

withholding tax in the DTA (𝜏𝑙𝑜𝑐𝑎𝑙𝑤 − 𝜏𝐷𝑇𝐴

𝑤 ), as the withholding tax overpayment.8 This part must

be claimed from the foreign country. Such reclamation involves lengthy procedures in which the

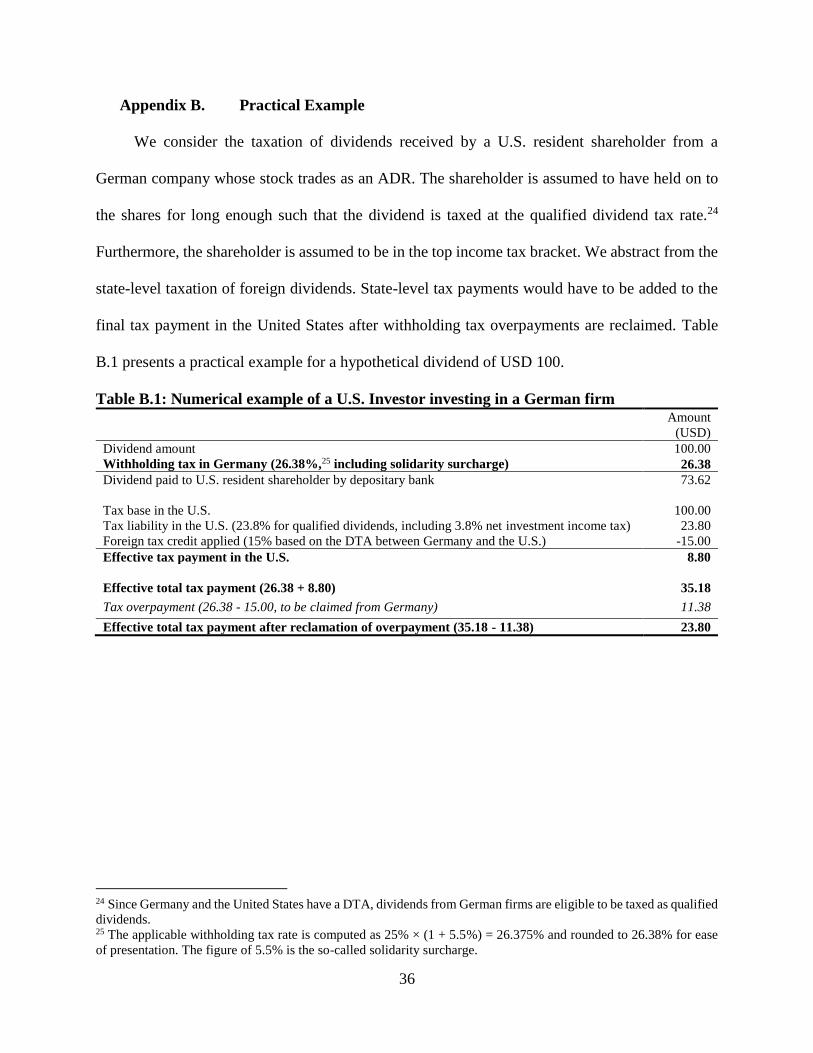

7 In most countries, this same dividend withholding tax rate is applied to domestic investors. 8 In Appendix B, we provide a brief practical example for a U.S. shareholder receiving dividends from a German

company.

9

individual or institutional investor must apply to each individual foreign tax authority for the

reclamation of the withholding tax overpayment on dividends received from equity held in the

corresponding country. Tax authorities often take several years to process these claims and can

require additional information (e.g., proof of residence or proof of stock ownership).

This process not only is burdensome for individual investors but also imposes significant

administrative costs on institutional investors, who must provide this information separately for

each of their individual shareholders.9 The authorities then have to transfer the reclaimed amounts

across borders to the investor’s account. Therefore, investors often do not retrieve their

withholding tax overpayments at all, or they do so with a substantial delay and/or at a significant

compliance cost in terms of either their own time or fees paid to agencies that process the

reclamation10 or to government institutions that provide the necessary forms. Indeed, anecdotal

evidence suggests that many investors do not claim withholding tax overpayments at all (see also

Zwick 2018 and the case of eligible firms not claiming tax credits).11

Frictions in claiming withholding tax overpayment can thus reduce the after-tax return from

investing in a particular country by imposing additional administrative costs on eligible investors

claiming tax credits. Since both institutional investors, whose after-tax returns determine their

inflows (Bergstresser and Poterba 2002), and individual investors with direct foreign holdings seek

9 These issues have been highlighted by institutional investors on several occasions (e.g., in consultations with the

European Commission; see the 2017 Code of Conduct on Withholding Tax published by the European Commission,

Ref. Ares(2017)5654449 – November 20, 2017). 10 Goal Group, a withholding tax reclamation service provider, estimates that, in 2017, about USD 3.5 billion in

dividend withholding tax overpayment were never claimed. Globally, this figure amounts to USD 18 billion annually

(http://www.goalgroup.com/media/66497/Athanasiou-08-27-2018-.pdf). 11 A U.S. shareholder who would like to claim withholding tax overpayments in Germany needs a Certification of

Residency (IRS Form 6166), which costs USD 85. Because of this, BASF, a large German chemical company, urges

U.S. shareholders to “weigh the cost of obtaining this form along with the processing fees associated submitting tax

relief claims through the Depositary Bank and its agents against the anticipated amount of recovery from German

source income to determine if it is cost-effective to file claims in the German market” (see

https://www.basf.com/global/de/investors/share-and-adrs/adrs-for-us-investors/taxation/faq-adr-taxation.html,

retrieved October 9, 2019).

10

to invest in countries with higher after-tax returns, FPI should be lower in countries with a high

level of withholding tax overpayment. This leads us to our first hypothesis, as follows.

H1: Conditional on the overall effective tax burden on dividends received from each

country, FPI is lower in countries with higher withholding tax overpayment.

There are three reasons we might not observe a negative effect of withholding tax

overpayments on FPI. First, withholding tax overpayments for individual countries might not be

sufficiently salient to investors (Chetty et al. 2009; Frydman and Wang 2019). Firms might not

inform all their foreign shareholders about their specific rights to claim withholding tax

overpayments, and country-specific withholding taxes applicable to local investors are often not

featured prominently in the firm’s investment prospectus.

Second, the cost of withholding tax overpayments could be too small to affect investment

behavior. For example, if private agencies are able to process shareholder reclamations efficiently

and there is competition among them, the service fees they can demand could be relatively small.

In this context, we also note that one could consider round tripping (e.g., via equity swaps) to

circumvent withholding tax overpayment. In practice, it appears too costly to do so via hubs such

as Singapore or the United Kingdom because of transaction costs and high fees (Dharmapala and

Desai 2011), which prevents individual and institutional investors from setting up treaty-shopping

systems. Thus, as pointed out by Desai and Dharmapala (2011) and Hanlon et al. (2015), the

circumvention of dividend withholding tax is difficult.

Third, if firms will not pay or reduce dividends in response to withholding tax overpayments,

these could be less of an issue. However, we consider it unlikely that firms will reduce dividends

in response to withholding taxes because (1) dividends tend to be sticky (Lintner 1956), (2) the

reduction or cutting of dividends is negatively perceived by capital markets (e.g., Bhattacharya

11

1979; Miller and Rock 1985), and (3) the majority of shareholders are domestic (e.g., Coval and

Moskowitz 1999). Hence, FPI is unlikely to be a first-order determinant of payout policies. Taken

together, whether withholding tax overpayments affect FPI is an empirical question.

Further, we argue that the effect of withholding tax overpayments on FPI depends on the

actual compliance hurdles that make the reclamation of overpayments difficult. In particular, the

availability of so-called relief-at-source mechanisms that allow the lower DTA withholding tax

rate to be applied immediately upon dividend distribution (thus avoiding the reclamation of

withholding tax overpayment) reduces the compliance cost of double taxation relief. Furthermore,

the cultural and economic proximity between issuer and investor countries could reduce the

compliance costs of claiming withholding tax overpayments across borders (e.g., Felbermayr and

Toubal 2010). For instance, cross-border communications can be easier if the investor’s home

country and the foreign country are geographically closer to each other or share a common cultural

understanding due to social and economic bilateral integration. In addition, collecting the

necessary information from issuing firms and transmitting it to the tax authorities could be easier

in countries with higher-quality reporting and auditing standards. Thus, we expect heterogeneity

in the responsiveness of FPI with respect to the compliance costs of investors claiming withholding

tax overpayments in the foreign country. This leads us to our second hypothesis, as follows.

H2: Withholding tax overpayments have a weaker effect on FPI if the compliance burden

of claiming withholding tax overpayments is smaller.

We also explore the mechanism underlying the investment effect of dividend withholding

taxes. Theory suggests that, because withholding tax overpayments and the reclamation process

impose additional costs on investors, these costs should increase the after-tax return for investing

in the issuing firm. That is, the withholding of tax overpayments should be reflected in security

12

prices. We use ADRs to test this mechanism. An ADR is a security that is traded on the U.S. stock

market and represents a particular foreign security, in the sense that, in principle, it can always be

exchanged for a predetermined amount of shares of the underlying foreign security. To obtain an

ADR, a U.S. investor (or broker–dealer) must deposit the underlying foreign security with a

depositary bank in the country of residence of the issuing foreign firm. The depository bank than

hands out the ADR. Owners of ADRs receive the same amount of dividends as the owners of the

underlying security, but are treated as foreign shareholders for dividend tax purposes. Hence, they

receive the dividend net of standard withholding taxes levied by the foreign country at a rate of

𝜏𝑙𝑜𝑐𝑎𝑙𝑤 . Investors have to claim a withholding tax overpayment at a rate of 𝜏𝑙𝑜𝑐𝑎𝑙

𝑤 − 𝜏𝐷𝑇𝐴𝑤 from the

foreign tax authority if a DTA between the United States and the foreign country yields a lower

withholding tax rate. Ceteris paribus, this reduces the value of the dividends to an U.S. investor

relative to the value of the dividends to an investor residing in the respective foreign country. If

this scenario is reflected in the returns, the larger the withholding tax overpayment, the lower the

return on the ADR should be relative to the return on the underlying foreign security in the days

before the ex-dividend day (i.e., the day when the security begins trading without the dividend).

In other words, the spread between the ADR return and the underlying security return decreases

with the withholding tax overpayment. We formulate this in the following hypothesis.12

H3: The return of an ADR relative to its underlying foreign security in the days before the

ex-dividend day is smaller if the withholding tax overpayment is larger.

12 One reason we might not find the hypothesized effect is potential arbitrage opportunities between the ADR and the

underlying security. For example, McDonald (2001) and Blouin et al. (2009) find evidence of costly cross-border tax

arbitrage that leads to partial price convergence. If sufficient arbitrage opportunities existed with respect to dividend

capitalization, withholding tax overpayments would be reflected in both the ADR price and the price of the underlying

security and the return spread between the two would not be affected.

13

3 Empirical Approach

3.1 Data on the Taxation of Cross-Border Dividends

We obtain information on the taxation of cross-border dividends from the International

Bureau of Fiscal Documentation (IBFD) Tax Research Platform. As of 2008, IBFD provides

detailed information on national and international tax law for a large number of countries around

the world. We proceed in three steps. First, we collect the domestic tax rates for dividends received

by a foreign listed company (𝜏ℎ,𝑡𝑑 ) for each investor country and each issuer country of our sample

over the sample period. In doing so, we account for investor country–specific treatments of foreign

dividends. For example, some countries apply an imputation credit for dividends from domestic

companies that is not available for foreign-source dividends. In case countries treat dividends

received from substantial and nonsubstantial holdings differently, we consider the rate applied to

dividends from nonsubstantial holdings, since FPI is defined as equity holdings with a voting

power of less than 10%. Second, for all issuer countries, we collect information on the local

withholding tax rate applied to dividends paid to nonresident individual shareholders (𝜏𝑙𝑜𝑐𝑎𝑙,𝑖𝑡𝑤 ).

Third, we collect information on DTAs and the withholding tax rates for cross-border dividends

paid to individuals as stipulated in these agreements (𝜏𝐷𝑇𝐴,𝑖ℎ𝑡𝑤 ).

The effective tax rate on dividends received by an investor residing in country ℎ from a

company residing in country 𝑖 in year 𝑡 is computed as 𝐸𝐹𝐹_𝑇𝐴𝑋𝑖ℎ𝑡 =

max(𝜏ℎ,𝑡𝑑 , min(𝜏𝑙𝑜𝑐𝑎𝑙,𝑖𝑡

𝑤 , 𝜏𝐷𝑇𝐴,𝑖ℎ𝑡𝑤 )). That is, from the investor’s perspective, dividends are taxed at

the higher rate of either the domestic rate on dividends, 𝜏ℎ,𝑡𝑑 , or the foreign withholding tax rate.

This is because all investor countries in our sample grant tax credits on foreign withholding taxes,

up to the tax payments in the home country (i.e., they do not refund excess foreign tax payments).

In 73.4% of the issuer investor–country–year combinations in our sample, a DTA establishes a

14

lower withholding tax rate, 𝜏𝐷𝑇𝐴,𝑖ℎ𝑡𝑤 , than the standard withholding tax rate in the issuer country.

Therefore, domestic dividend taxes rates are higher than foreign withholding tax rates in most

cases (89% of the sample), such that 𝜏ℎ𝑡𝑑 > min(𝜏𝑙𝑜𝑐𝑎𝑙,𝑖𝑡

𝑤 , 𝜏𝐷𝑇𝐴,𝑖ℎ𝑡𝑤 ). Hence, the effective dividend

tax rate 𝐸𝐹𝐹_𝑇𝐴𝑋𝑖ℎ𝑡 becomes 𝜏ℎ𝑡𝑑 for all potential investment locations, which ensures capital

export neutrality. The average effective dividend tax rate in our sample is 28.78%.

However, since the domestic tax authority only allows for credits up to the DTA rate,

𝜏𝐷𝑇𝐴,𝑖ℎ𝑡𝑤 , investors have to claim part of their eligible foreign tax credit from the foreign tax

authority in the form of withholding tax overpayment to arrive at this effective tax rate

(𝐸𝐹𝐹_𝑇𝐴𝑋𝑖ℎ𝑡 = 𝜏ℎ𝑡𝑑 ). We define this withholding tax overpayment as

𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖ℎ𝑡 = max(𝜏𝑙𝑜𝑐𝑎𝑙,𝑖ℎ𝑡𝑤 − 𝜏𝐷𝑇𝐴,𝑖ℎ𝑡

𝑤 , 0)

The average withholding tax overpayment in our sample is 5% of the dividend paid and

ranges up to 35% (applicable for FPIs from Denmark in Switzerland). Since the withholding tax

overpayment is defined for each possible country pair, there is large variation across country pairs

over time. In total, we observe 616 changes of 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡, including 383 increases and

233 decreases during our sample period (see Figure 1). The changes arise from the signing or

termination of DTAs, as well as from unilateral adjustments in withholding taxes in the issuer

country 𝑖, with the vast majority stemming from changes in the local withholding tax.13 Therefore,

changes in withholding tax overpayments are less likely to be driven by FPI considerations. In our

empirical strategy, we exploit all changes in withholding tax overpayments.

13 Of the 616 changes in 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡, 483 changes are due to a change in the local withholding taxes of the

issuer country, 36 changes are due to a change in the bilateral DTA, and 97 changes are the result of coinciding

changes in the local withholding taxes of the issuer country and the bilateral DTA. A change in the unilateral

withholding tax only triggers a change in 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 if the DTA withholding tax rate is below the unilateral

withholding tax.

15

3.2 Identification Strategy: Withholding Tax Overpayments and FPI

To analyze the effect of dividend withholding taxes on FPI, we merge our tax information

with two different data sources for FPI: aggregated bilateral foreign portfolio holdings for a large

set of developed economies, obtained from the CPIS, and the FPIs of individual U.S. institutional

investors, obtained from their mandatory 13F filings. For the bilateral analysis using CPIS data,

we estimate the following model:

𝐹𝑃𝐼𝑖ℎ𝑡 = 𝛽1𝐸𝐹𝐹_𝑇𝐴𝑋𝑖ℎ𝑡 + 𝛽2𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖ℎ𝑡 + 𝜷𝐗𝐢𝐡𝐭 + 𝝓𝒊𝒉 + 𝝓𝒉𝒕 + 𝝓𝒊𝒕 + 𝜖𝑖ℎ𝑡 (1)

where 𝐹𝑃𝐼𝑖ℎ𝑡 is the amount, in US dollars (USD), of foreign equity holdings in country 𝑖 in year 𝑡

of investors residing in country ℎ, defined in terms of its natural logarithm. Because of our fixed

effect structure (i.e., including investor–year fixed effects, see below), we estimate the effect of

our explanatory variables on FPI in country 𝑖 conditional on the overall FPI of country ℎ in a given

year 𝑡. This approach is thus equivalent to using as the dependent variable the shares of individual

issuer countries in the holder country’s portfolio as in Amiram and Frank (2016).

The variable 𝐸𝐹𝐹_𝑇𝐴𝑋𝑖ℎ𝑡 is the effective tax payment on dividends received from a firm

residing in country 𝑖 by an investor residing in country ℎ in year 𝑡 , as defined above, and

𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖ℎ𝑡 is the amount of withholding tax overpayment that the investor in country

ℎ must claim from the tax authorities in country 𝑖. Thus, 𝐸𝐹𝐹_𝑇𝐴𝑋𝑖ℎ𝑡 + 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖ℎ𝑡

is the initial tax rate paid by an investor on dividends received from a company in country 𝑖, while,

absent compliance frictions in the credit claiming process, the investor eventually pays only

𝐸𝐹𝐹_𝑇𝐴𝑋𝑖ℎ𝑡. Consistent with H1, we expect withholding tax overpayments to represent a friction

to investors, so that FPI decreases (𝛽2 < 0).

To isolate the effect of withholding tax overpayments and to arrive at a generalized

difference-in-differences design, we include a comprehensive set of fixed effects. These fixed

16

effects also serve as benchmarks in our portfolio location choice model ( e.g., Edison and Warnock

2004; Ivković and Weisbenner 2005). First, we include country pair fixed effects (𝝓𝒊𝒉) to control

for any differences across country pairs that could affect bilateral FPI, such as geographical,

cultural, or political proximity (Di Giovanni 2005) or a higher level of economic integration (Aviat

and Coeurdacier 2007). These fixed effects also ensure that the 𝛽2 coefficient is identified only

from changes in the withholding tax overpayment. Second, we include issuer country–specific

year fixed effects. These fixed effects control for any institutional, economic, legal, or other

changes in issuer country 𝑖 that could affect how much foreign equity is held there, such as

regulatory changes (Julio and Yook 2016) and changes in audit and reporting quality (Covrig et al.

2007; Chen et al. 2018), local economic growth (Portes and Rey 2005), and local stock prices

(Froot et al. 2001). Finally, we include holder country–year fixed effects that capture any change

in the holder country ℎ that could drive the overall level of its FPI, including macroeconomic

developments and policy changes in country ℎ, as well as changes in investor sentiment.

We further complement our regression model with a set of control variables (𝐗𝐢𝐡𝐭), that vary

at the country pair–year level. First, we include a dummy variable that indicates whether countries

𝑖 and ℎ have signed a DTA in a particular year. While DTAs affect withholding taxes, they can

have additional nontax effects on FPI, such as on the information exchange between countries

(Blonigen et al. 2014). Second, we include the difference in gross domestic product (GDP) growth

between the issuer country and the holder country divided by the GDP growth rate in the holder

country, the difference in credit provided to banks as a percentage of the GDP in the issuer country

divided by the credit provided to banks as a percentage of the GDP in the holder country, and the

difference in stocks traded as percentage of GDP in i divided by the stock traded as a percentage

17

of the GDP in the holder country. This controls for a potential correlation between the financial

and economic dynamics of the two countries.

To further ensure that the effect of dividend withholding tax overpayments is actually driven

by the taxation of dividends (vis-à-vis the taxation on capital gains), we also run a regression where

we interact 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 with the (demeaned and standardized) logarithm of the average

dividend payout ratio (weighted by the market value) in the issuer country based on the MSCI

country indexes in the three preceding years. Since 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 is expressed as a share

of dividend payments, such that the actual dollar amount of this overpayment depends on the

dividend amount paid by companies, we expect the adverse effect of 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 to be

stronger in years when companies in the issuer country pay more dividends.

In the second part of the analysis, we explore the effect of withholding tax overpayments on

FPI at the level of the individual investor, using data on the foreign holdings of institutional

investors obtained from their 13F filings to the SEC. For each investor, we aggregate the holdings

by country and quarter and estimate the following regression model:

𝐹𝑃𝐼𝑖𝑓𝑞 = 𝛽1𝐸𝐹𝐹_𝑇𝐴𝑋𝑖𝑞 + 𝛽2𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖𝑞 + 𝜷𝐗𝐢𝐪 + 𝝓𝒊 + 𝝓𝒒 + 𝝓𝒇𝒒 + 𝜖𝑖𝑓𝑞 (2)

where 𝐹𝑃𝐼𝑖𝑓𝑞 is the logarithm of the foreign holdings in country 𝑖 of investor 𝑓 in quarter 𝑞 ;

𝐸𝐹𝐹_𝑇𝐴𝑋𝑖𝑓𝑞 and 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖𝑓𝑞 are again the effective dividend tax rate and the

withholding tax overpayment, respectively, on dividends received from companies residing in

country 𝑖; and 𝝓𝒊 , 𝝓𝒒, and 𝝓𝒇𝒒 are issuer country, quarter, and investor–quarter fixed effects,

respectively. The country fixed effects capture the time-invariant preferences of U.S. investors for

a particular country, while the quarter fixed effects capture time trends. The investor-specific

quarter fixed effects (𝝓𝒇𝒒) capture the average evolution of a particular investor’s portfolio. Thus,

the coefficient of interest, 𝛽2, captures the deviation from the average evolution of the investor’s

18

portfolio that is induced by changes in the withholding tax overpayment. We augment the model

by a range of potential determinants of portfolio choice (e.g., Chan et al. 2005), including the issuer

country’s GDP growth, the logarithm of the GDP per capita, the logarithm of market capitalization,

the logarithm of the trade ratio (measured as the sum of exports and imports divided by the GDP),

and the logarithm of FDI inflows. We also include indicators for capital controls, the protection of

minority shareholders, and the quality of the legal system in the issuer country.

In an extension, we also run the regression at the level of the individual security, that is, the

dependent variable being the holdings of investor 𝑓 in security 𝑠 in quarter 𝑞, which is regressed

on the effective dividend tax rate and the withholding tax overpayment on dividends received from

the company issuing this security:

𝐹𝑃𝐼𝑠𝑓𝑞 = 𝛽1𝐸𝐹𝐹_𝑇𝐴𝑋𝑖𝑞 + 𝛽2𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖𝑞 + 𝛽3𝐸𝐹𝐹_𝑇𝐴𝑋𝑖𝑞 × 𝐷𝑌𝑠𝑞

+ 𝛽4𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖𝑞 × 𝐷𝑌𝑠𝑞 + 𝜷𝐗𝐢𝐟𝐪 + 𝝓𝒊𝒒 + 𝝓𝒔 + 𝝓𝒇𝒒 + 𝜖𝑠𝑖𝑓𝑞

(3)

The advantage of this model is that it allows us to relate the effect of withholding tax

overpayments directly to the dividend payments of the corresponding company (i.e., dividend

yields, 𝐷𝑌𝑠𝑞 ) and thus identify the effect of withholding tax overpayments from firm-level

variation in dividend payments, controlling for any change at the foreign country level via country–

quarter fixed effects (𝝓𝒊𝒒). A limitation of this regression is that, in contrast to equation (3), we

only observe portfolio changes in countries where the investor already holds assets; that is, we

capture the intensive margin but not the extensive margin of the investor’s portfolio choice.

3.3 Testing H2

To test H2, we extend equation (1) by an interaction of the withholding tax overpayment

(𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡) and several proxy variables for administrative costs to file cross-border

withholding tax claims. First, we use a dummy variable that is equal to one if the issuer country’s

19

legislation on withholding taxes allows for relief at source, that is, the double taxation relief can

be applied immediately when the dividend is paid out to the foreign shareholder. The issuing

company then deducts only the lower withholding tax under the DTA from the gross dividend,

which allows the receiving shareholder to avoid having to claim withholding tax overpayment. To

be eligible for relief at source, shareholders (or their intermediaries) need to comply with

substantial documentation requirements, but this procedure often simplifies the reclamation of

withholding tax overpayments.14

Second, we extend the model with several proxies for compliance costs for claiming

withholding tax overpayments in the issuer country. For instance, we employ a dummy variable

indicating whether the investor and issuer countries share a common land border, which proxies

for geographical proximity. Prior literature shows that geographic distance leads to information

asymmetries that are likely to increase the communication costs between two locations (Ghoul et

al. 2013).15 The second proxy is the logarithm of the number of visitors from the holder country to

the issuer country as a share of the inhabitants of the holder country. Greater cross-border mobility

toward the issuer country could increase cultural knowledge (Parey and Waldinger 2011), which,

in turn, can improve communication and make it easier to apply for the cross-border refund of

withholding tax overpayments. We also explore reporting quality as a proxy for compliance costs.

A high level of reporting quality in the issuer country simplifies communications with tax

authorities, since it makes it easier to process corporate disclosures and to obtain the necessary

documentation to file reclaims (Holthausen 2009; Fang et al. 2015). Thus, we use a dummy

variable for high audit and reporting quality in the issuer country as an additional proxy for the

14 For this reason, the relief-at-source mechanism has been suggested as a possible policy solution to withholding tax

overpayments (e.g., Næss-Schmidt et al. 2012; Anon. 2013). 15 In untabulated results, we obtain qualitatively similar findings if we use the actual distance between capital cities.

20

administrative costs of cross-border tax reclaims. Finally, we use a dummy indicating whether the

holder and issuer countries are members of the eurozone. Operating under a common currency

avoids documentation requirements with regard to exchange rates and makes it easier to transfer

withholding tax claims granted to the investor.

3.4 Testing H3

The second part of our empirical analysis explores a potential mechanism through which

withholding taxes affect FPI (H3). We test whether the spread in returns between an ADR traded

in the United States and its underlying foreign security traded abroad is negatively associated with

the magnitude of the withholding tax overpayment in the days leading up to the ex-dividend day.

We estimate the following regression model:

𝑆𝑃𝑅𝐸𝐴𝐷𝑐,𝑖,𝑑 = 𝛽1𝐸𝐹𝐹_𝑇𝐴𝑋_𝐷𝑖,𝑑 + 𝛽2𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖,𝑑 + 𝜷𝐗 + 𝝓𝒅 + 𝝓𝒊 + 𝜖𝑐,𝑖,𝑑 (4)

where 𝑆𝑃𝑅𝐸𝐴𝐷𝑐,𝑖,𝑑 is the difference between the return on the ADR of company 𝑐 and the return

on its corresponding foreign market security in country 𝑖 on the last cum dividend day of dividend

𝑑 (i.e., the day before the ex-dividend day). Returns are computed as the difference in the stock

price (adjusted for stock splits) on the last cum dividend day and the stock price 30 trading days

earlier divided by the latter. Since we use the spread between the ADR return and its underlying

security, we effectively control for market trends. We include two tax-related variables in equation

(4): first, 𝐸𝐹𝐹_𝑇𝐴𝑋_𝐷𝑖,𝑑, the difference in the effective tax rate between a U.S. shareholder and a

shareholder in home market 𝑖 of company 𝑐 for dividend 𝑑 (𝐸𝐹𝐹_𝑇𝐴𝑋_𝐷𝑖,𝑑 = 𝐸𝐹𝐹_𝑇𝐴𝑋𝑖,ℎ,𝑡 −

𝜏𝑖𝑡𝑑 ), and, second, 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖,𝑑, the amount of withholding tax overpayment that the

investor in the United States has to claim from the tax authorities in the residence country 𝑖 of

company 𝑐. The terms 𝝓𝒅 and 𝝓𝒊 are fixed effects for the last cum dividend day of dividend 𝑑 and

home market 𝑖, respectively, and 𝐗 is a vector of control variables for company c that includes size

21

(total), total cash holdings over total assets, and the leverage ratio (total debt divided by total assets)

reported in the year prior to dividend 𝑑.

In this setting, the coefficient 𝛽2 captures the effect of the withholding tax overpayment on

the return spread between the ADR and the underlying security. Any difference in dividend

taxation between U.S. investors and investors residing in the home market of the ADR is captured

by 𝛽1. If withholding tax overpayments constitute a cost to U.S. investors, 𝑆𝑃𝑅𝐸𝐴𝐷𝑐,𝑖,𝑑 should be

negatively associated with 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖,𝑑 (i.e., 𝛽2 < 0).

The negative effect of withholding tax overpayments on the return spread should be more

pronounced for firms with higher dividend yields because the total withholding tax overpayment

is the product of the dividend amount and the tax rate difference between the local withholding tax

in the foreign market of the ADR’s underlying security and the applicable DTA withholding tax.

We test this prediction by adding interactions with the dividend yield to equation (4), to estimate

the following regression:

𝑆𝑃𝑅𝐸𝐴𝐷𝑐,𝑖,𝑑 = 𝛽1𝐸𝐹𝐹_𝑇𝐴𝑋_𝐷𝑖,𝑑 + 𝛽2𝐸𝐹𝐹_𝑇𝐴𝑋_𝐷𝑖,𝑑 × 𝐷𝑌𝑐,𝑑

+ 𝛽3𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖,𝑑 + 𝛽4𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡𝑖,𝑑 × 𝐷𝑌𝑐,𝑑

+ 𝛽5𝐷𝑌𝑐,𝑑 + 𝜷𝐗 + 𝝓𝒅 + 𝝓𝒊 + 𝜖𝑐,𝑖,𝑑

(5)

where 𝐷𝑌𝑐,𝑑 is the dividend yield, defined as the dividend 𝑑 divided by the ADR price 30 trading

days prior to the last cum dividend day, and 𝛽4 measures the effect of withholding tax

overpayments as a percentage of the dividend yield on the return spread. Consistent with H3, we

expect 𝛽4 to be negative if withholding tax overpayments are priced into ADR returns. The

coefficient 𝛽3 captures the effect of withholding tax overpayments independent of the dividend

yield. It can be negative if investors generally dislike withholding overpayments independent of

the actual cost they accrue.

22

3.5 Data

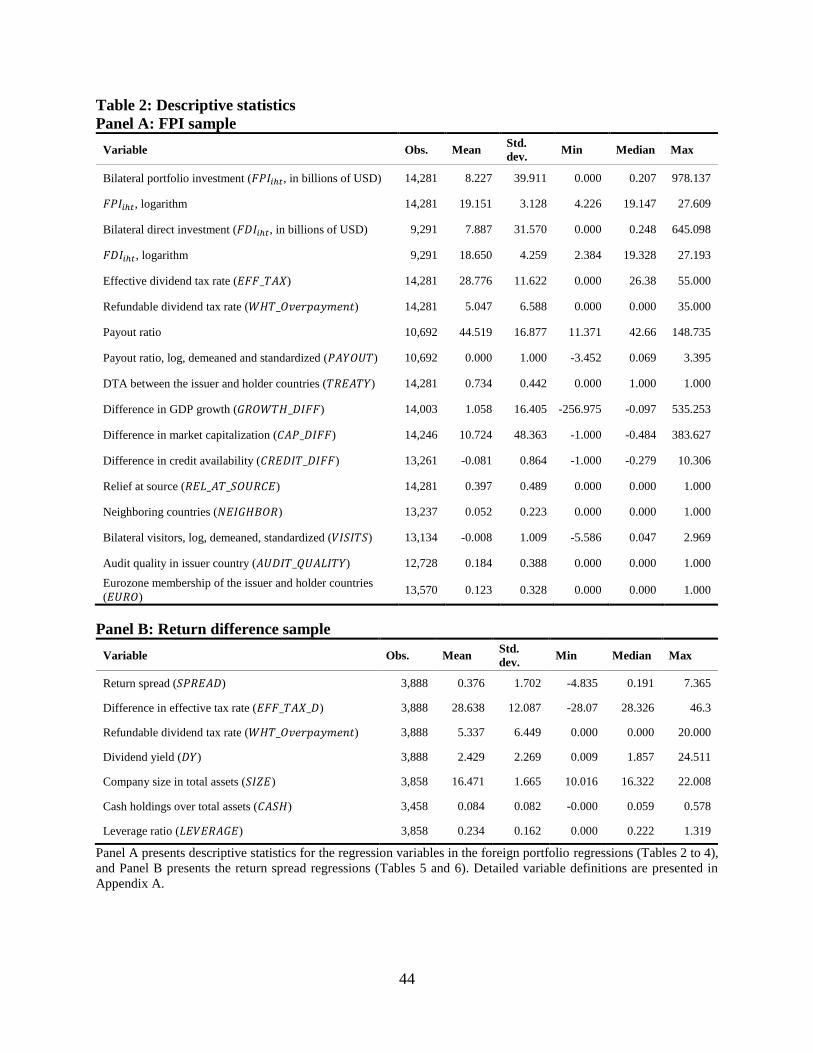

3.5.1 FPIs

To analyze FPI, we use two sets of data: bilateral FPI data and data on U.S. mutual fund

holdings. For both sets, FPI is defined as foreign equity holdings that entitle shareholders to voting

rights of less than 10%. Bilateral FPI is obtained from the IMF’s Coordinated Portfolio Investment

Survey (CPIS). For each participating country, the corresponding central bank collects information

on foreign equity held by resident investors. The data are available on an annual basis, and

separately for each issuer country; that is, for a particular investor country ℎ, we know the level of

foreign equity held in each issuer country 𝑖 on an annual basis. Collecting data from the asset-

owning country rather than from the security-issuing country helps ensure data precision because

investors are more likely to know where their foreign equity is issued than issuers would know the

residence of all their investors.

The data in the CPIS have been collected since 1997. However, participation varied in the

first years (see also Amiram and Frank 2016) and the data are not complete in very recent years.

Since our bilateral withholding tax data are available from 2008 onward, we use CPIS data from

2008 to 2015. During this period, a large number of countries consistently reported foreign equity

holdings in CPIS. We include the foreign equity holdings of 38 developed countries, including all

major OECD and European Union member states. Table 1 reports the number of observations in

the sample and the amount invested per investor country. To further ensure data quality, we use

only issuer–investor country pairs that report bilateral equity holdings for at least five years and

which have a median of USD 1 million in equity holdings during the sample period. This leaves

us with 115 issuer countries and 1,869 country pairs in our regression sample.

23

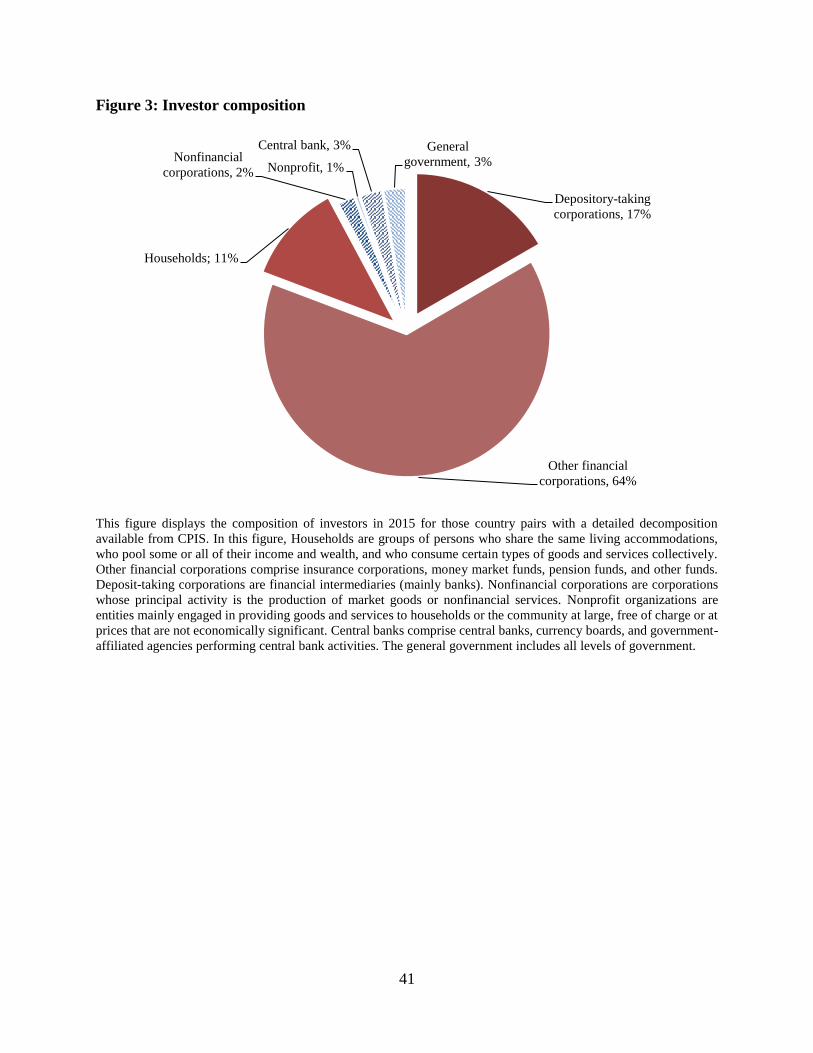

Figure 2 displays FPI by investor country in 2012 as a share of the GDP relative to the FDI

in 2012. In many countries, the FPI is substantial and similar in size to the FDI. The average level

of FPI of an investor country in a particular issuer country is USD 8.2 billion, whereas the average

FDI for a country pair is USD 7.9 billion (see Table 2). In 2012, our sample comprises a total of

USD 14.79 trillion in foreign equity holdings. Although a large part of the foreign equity in our

sample is both held by U.S. investors (USD 5.17 trillion in 2012, see Table 1) and invested in the

United States (USD 2.47 trillion in 2012), small, open economies such as the Netherlands and

Belgium are also particularly involved in cross-border investment relative to the size of their

economy via both FPI and FDI. Two countries that stand out are Ireland and Luxembourg, with

shares of FPI above 100% of their GDP, likely reflecting the fact that these locations are often

used as tax shelters by investors (Hanlon et al. 2015). Note that the investor country–specific year

fixed effects included in our empirical model fully capture these country-specific effects and

dynamics. Further, we show in a robustness test that no single investor country is driving our

findings.

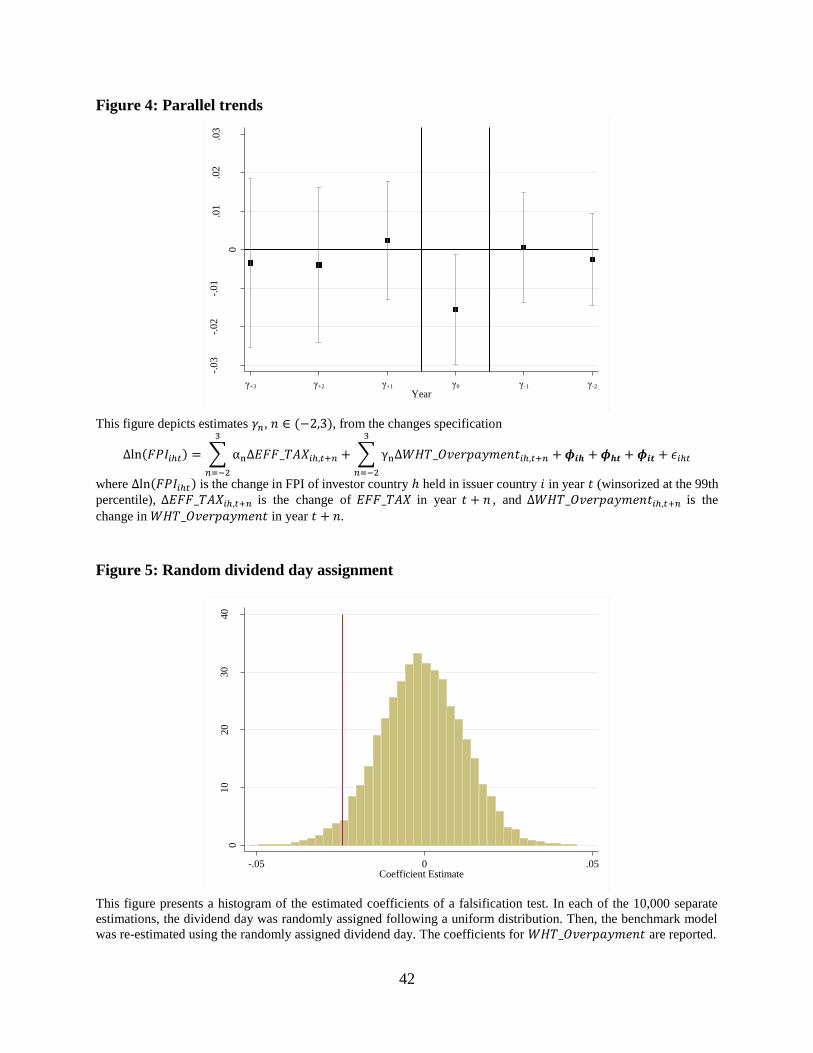

Few countries report equity FPI disaggregated for specific investor types. Data from

countries that report such detail suggest that the bulk of the FPI (92% in 2015) comes from

households and their intermediaries, such as investment funds or banks (see Figure 3). The ultimate

owners of this FPI are thus taxed at the personal level and are directly affected by the withholding

tax systems that we study. While 11% of FPI is held directly by households, the vast majority of

foreign stocks are held indirectly through institutional investors, consistent with their dominance

among foreign investors reported in previous studies (e.g., Dahlquist and Robertsson 2001;

Ferreira and Matos 2008; Ammer et al. 2012).

24

Data on U.S. institutional investor holdings are obtained from their SEC 13F filings. The

SEC requires institutional investment managers with more than USD 100 billion of assets under

management to disclose their equity holdings on a quarterly basis. The mandatory 13F filings have

been previously used to study institutional investor behavior (e.g., Lewellen 2011; Blouin et al.

2017). We obtain the data from Backus et al. (2019), who have scraped all the 13F filings from

the SEC webpage.16 Consistent with the FPI definition for the CPIS data in our main test, we use

the foreign holdings with a voting rights share of less than 10% of institutional investors residing

in the United States for the sample period 2008–2015. We merge this information with pricing

data from Compustat to obtain the market value of the holdings. During the sample period, we

observe 4,537 institutional investors holding, on average, USD 17 million in each individual

security. A limitation of the 13F filings is that they report only the holdings of securities traded on

the U.S. market (i.e., stocks of cross-listed companies and ADRs). Direct holdings via foreign

stock exchanges are not reported. However, U.S. investors tend to prefer U.S. traded securities

(e.g., Lang et al. 2003; Edison and Warnock 2004), as reflected in the size of the funds reported in

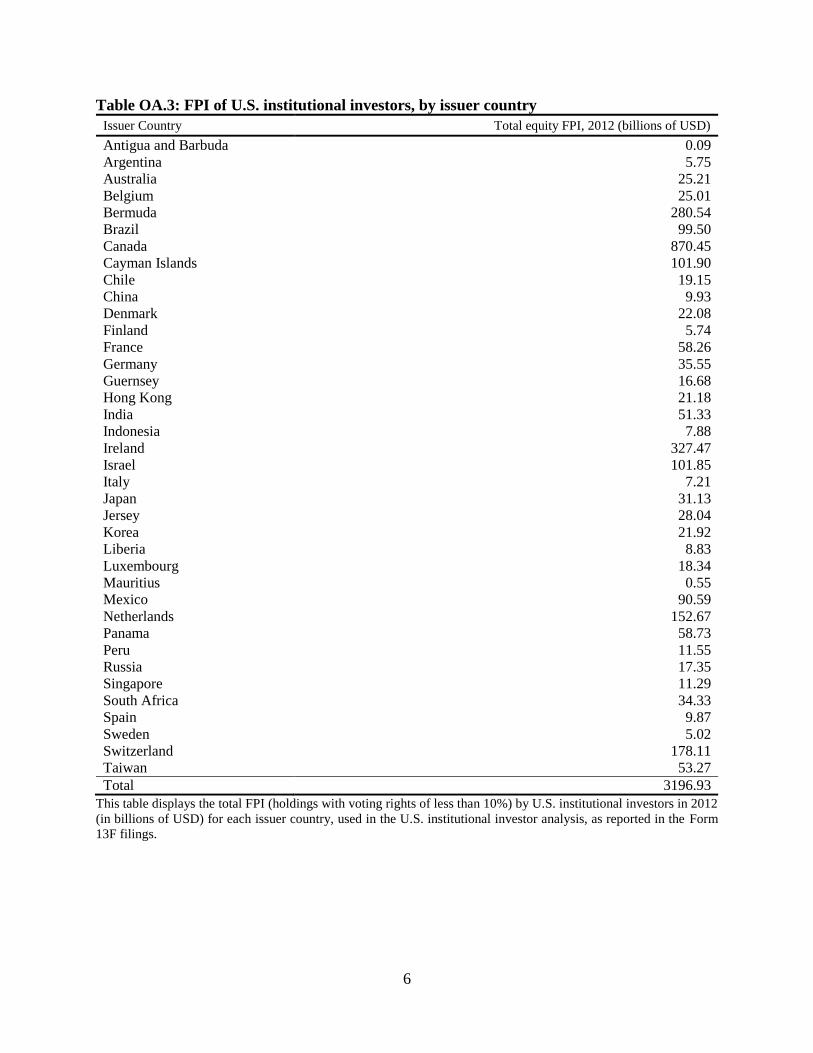

the 13F filings. For 2012, the FPI in our 13F sample amounts to USD 3.2 trillion, or about 62% of

the U.S. FPI reported by CPIS.17

3.5.2 Relief-at-Source Mechanisms

Using information from national tax authorities, as well as financial service providers (i.e.,

BNY Mellon, Clearstream), we collect data on the availability of relief-at-source mechanisms for

dividend withholding taxes on foreign investors in the issuer countries. We define a relief-at-

source mechanism as a provision that allows the dividend-paying company to deduct the

16 The data were downloaded from Michael Sinkinson’s webpage and they contain several improvements over the

Thomson Reuters S34 database, an alternative source for 13F filings. 17 See Table 1. For further details on the distribution of U.S. institutional investor countries and more summary

statistics, see the corresponding table in the Online Appendix.

25

shareholder-specific effective dividend withholding tax rate (taking into account reductions due to

DTAs with the shareholder’s country of residence) from dividend payments rather than the higher

standard withholding tax. Only 26% of the issuer countries in our sample have such a mechanism

(hosting about 46% of the FPI in the CPIS sample). To be eligible for these relief-at-source

provisions, foreign shareholders or their intermediaries usually have to file applications and

provide documentation to the tax authorities in the issuer country prior to the dividend distribution.

3.5.3 ADRs

For the ADR pricing analysis, we use data on ADRs traded on OTC markets, for which

pricing and dividend information is available from WRDS and FINRA. OTC markets host the

large majority (approximately three-quarters) of ADRs. Foreign firms have mainly chosen to place

their ADRs on OTC markets to avoid having to comply with the complex regulations for stock

exchange listings introduced by the Sarbanes–Oxley Act of 2002. Furthermore, in 2008, the SEC

exempted foreign issuers from registration if they traded on OTC markets.

To study the pricing of ADRs, we combine four sets of data: (1) We collect ticker symbols,

market locations, countries, and the ISIN of the underlying securities for all ADRs from J.P.

Morgan’s website (adr.com). (2) We obtain information on the daily prices of ADRs on over-the-

counter (OTC) markets from WRDS OTC Markets database. (3) Daily pricing data for the

underlying security and financial data for the issuing firm are available from Datastream.

(4) Information on dividend amounts, relevant dividend dates (i.e., record day, declaration day,

ex-dividend day), and dividend characteristics (e.g., taxable vs. nontaxable) are available from the

Financial Industry Regulatory Authority (FINRA). FINRA reports data on all securities for which

trades and events are reported via FINRA’s OTC Reporting Facility.

26

Since OTC pricing data are not available for full years prior to 2012, we use ADR data over

the period 2012–2018. Consistent with prior research, we exclude thinly traded ADRs (Callaghan

and Barry 2003), that is, we exclude ADRs in years in which they are traded on fewer than 100

trading days. We also exclude ADRs from Japan and Korea because firms listed in these countries

declare dividends traditionally only several weeks after the ex-dividend day, such that it is

impossible to accurately capitalize them around the ex-dividend day.18 We consider taxable cash

dividends with dividend payments at or below 25% of the security value. Dividends above this

threshold constitute a small minority of cases for which substantially different regulations apply,

particularly with respect to the ex-dividend date.19 This approach leads to a sample of 3,888

dividend payments by 652 different foreign companies that issued ADRs on U.S. OTC markets.

These companies reside in 40 different countries. The average dividend yield is 2.4% (see Panel

B of Table 2), and the return spread between the ADRs and the underlying security on the last

cum-dividend day is 0.38 percentage points, ranging from -4.84 to 7.36 percentage points. This

spread is similar to those observed in earlier studies (Blouin et al. 2009).

4 Results

4.1 FPI

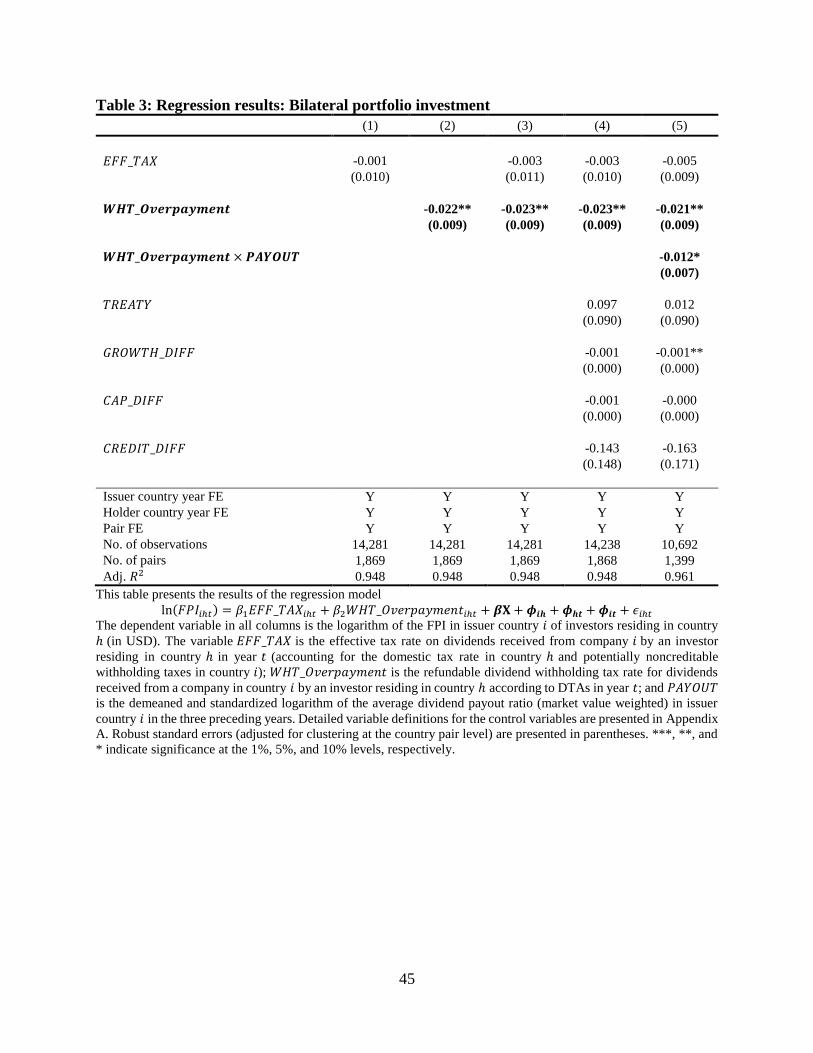

The results of testing equation (1) are presented in Table 3. Columns (1) to (3) present the

results of a model including the tax rate variables and a set of fixed effects with no country pair

controls. According to H1, dividend withholding taxes are only neutral with respect to the FPI

location if one assumes that withholding tax overpayments can be easily and fully claimed. Our

empirical results suggest that withholding tax overpayments matter for FPI. Across all

18 This is also reflected in the fact that Japanese and Korean ADRs are usually not quoted ex-dividends. 19 Both FINRA and stock exchanges set the ex-dividend day of a dividend payment of more than 25% of the company’s

stock price on the first business day after the payment date, that is, usually several days after the record date.

27

specifications in Table 3 and consistent with H1, we observe a significantly negative coefficient

for 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 that is robust to the inclusion of additional control variables (see column

(4)). Consistent with the notion that this effect is related to dividend payments, we find a

significantly negative coefficient when we interact 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 with 𝑃𝐴𝑌𝑂𝑈𝑇 in

column (5), which implies that frictions from dividend withholding tax overpayments are stronger

when issuer countries pay more dividends.20

Thus, withholding tax overpayments are an additional friction in cross-border portfolio

investment that lead to less FPI in locations from which investors face high levels of withholding

tax overpayment. The results are also economically large. The estimates from column (3) in Table

3 indicate that a one percentage point increase in the withholding tax overpayment rate for a

particular investor–issuer country pair lowers FPI for this country pair by 2.3% annually.

Evaluated at the average sample FPI, this implies an average decrease in FPI of USD 186 million

per country pair for each percentage point of withholding tax overpayment. Note that, since overall

FPI in a particular issuer country is the sum of the FPI from all investor countries, the overall effect

for an individual country is likely to be substantially larger. For example, in 2015, the investor

countries in our sample held USD 857 billion in equity FPI in Germany. Our estimates suggest

that FPI to Germany increases by USD 19 billion if withholding tax overpayments in Germany are

reduced by one percentage point.

Further, the estimated coefficient of 𝐸𝐹𝐹_𝑇𝐴𝑋 is weak and nonsignificant across all

specifications. This is because foreign withholding tax rates are often below the domestic dividend

tax rate. The international tax system of foreign tax credits and withholding tax rates aims to

20 The variable 𝑃𝐴𝑌𝑂𝑈𝑇 is demeaned and standardized such that the coefficient is to be interpreted as estimated

responses to deviations from the mean. Note that issuer country–year fixed effects capture any direct effect of issuer–

country payout ratios on equity FPI.

28

preserve capital export neutrality by ensuring that investors face the same tax rate on dividends

from any issuer country. Hence, 𝐸𝐹𝐹_𝑇𝐴𝑋 does not vary across issuer countries. It could impact

overall FPI, but should not differentially affect investments in individual issuer countries. The

evolution of the overall level of FPI is absorbed by the investor country–year fixed effects.

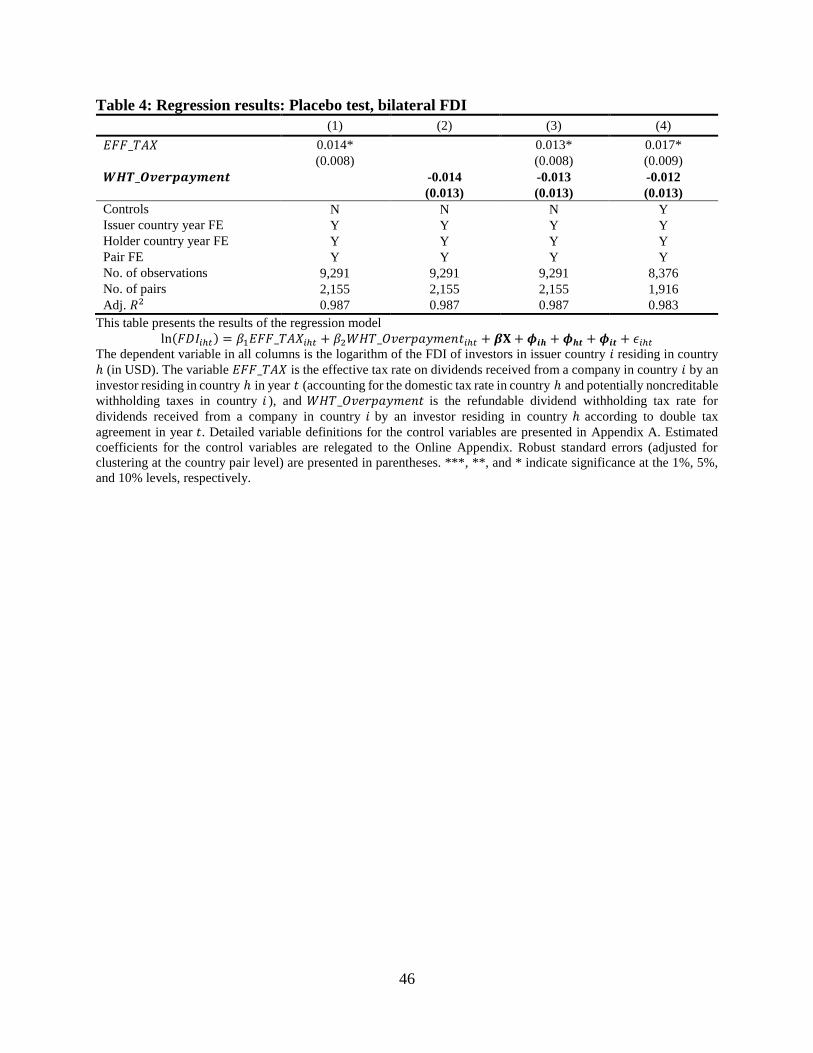

We subject our results to two robustness tests.21 First, we address concerns that withholding

tax overpayments are correlated with unobserved country pair–year–specific variation driving FPI

and taxes by using the logarithm of FDI as the dependent variable instead. FDI should not respond

to withholding tax overpayments, since they are not applicable to such investments. FDI would,

however, be affected by similar bilateral dynamics as FPI. This point is reflected in a high

correlation (0.64 in our sample) between FPI and FDI. If the coefficient estimates on

𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 in Table 3 capture some of these dynamics, they should also show up in the

regressions with FDI. However, we find in Table 4 that FDI does not respond to bilateral changes

in 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡, reassuring us that the results in Table 3 are not driven by unobserved

country pair–year–specific variation in economic conditions.

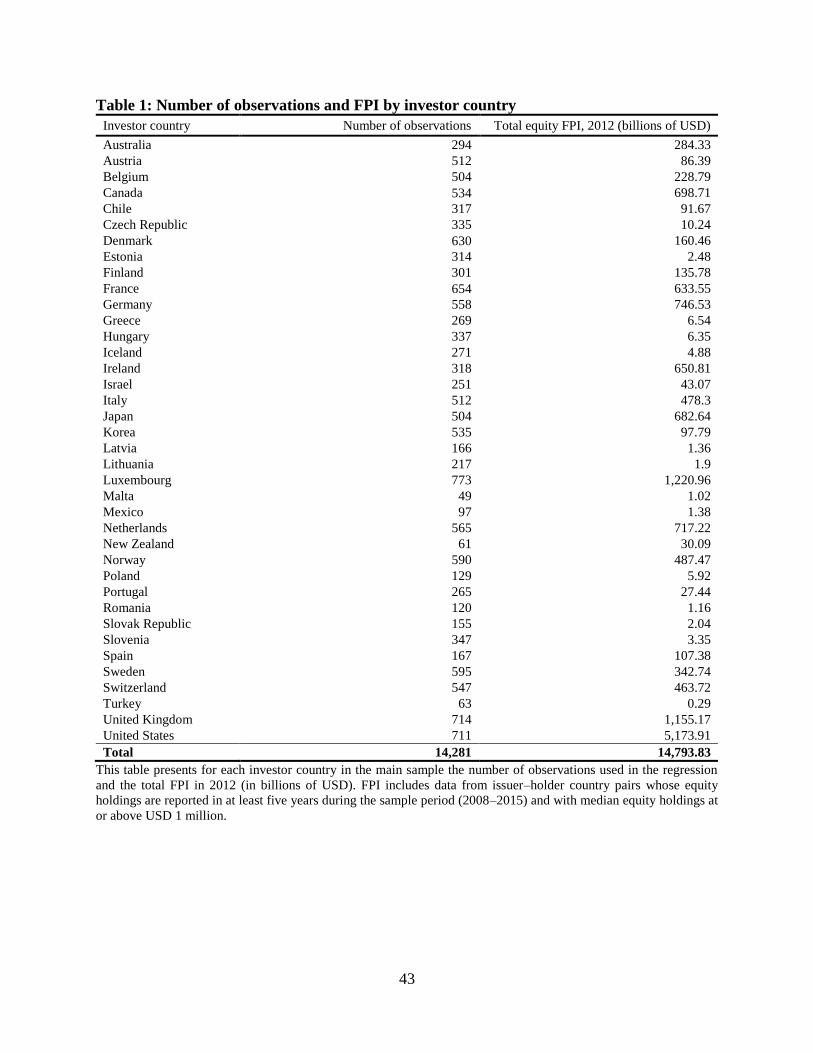

Second, we test whether there are any pre-trends in the explanatory variable. To this end, we

run a changes model that regresses year-on-year changes in the logarithm of FPI in year 𝑡

(winsorized at the 99th percentile) on the year-on-year change of the tax variables in 𝑡, as well as

on the year-on-year changes of the tax variables in the years before and after 𝑡. If there are no pre-

trends, changes in FPI in the current year (𝑡) should not respond to changes in the tax variables in

future years (e.g., 𝑡 + 1, 𝑡 + 2, and 𝑡 + 3), but only to tax variable changes in the current year (𝑡).

Furthermore, if the effect of withholding tax overpayments on FPI is persistent, FPI changes in the

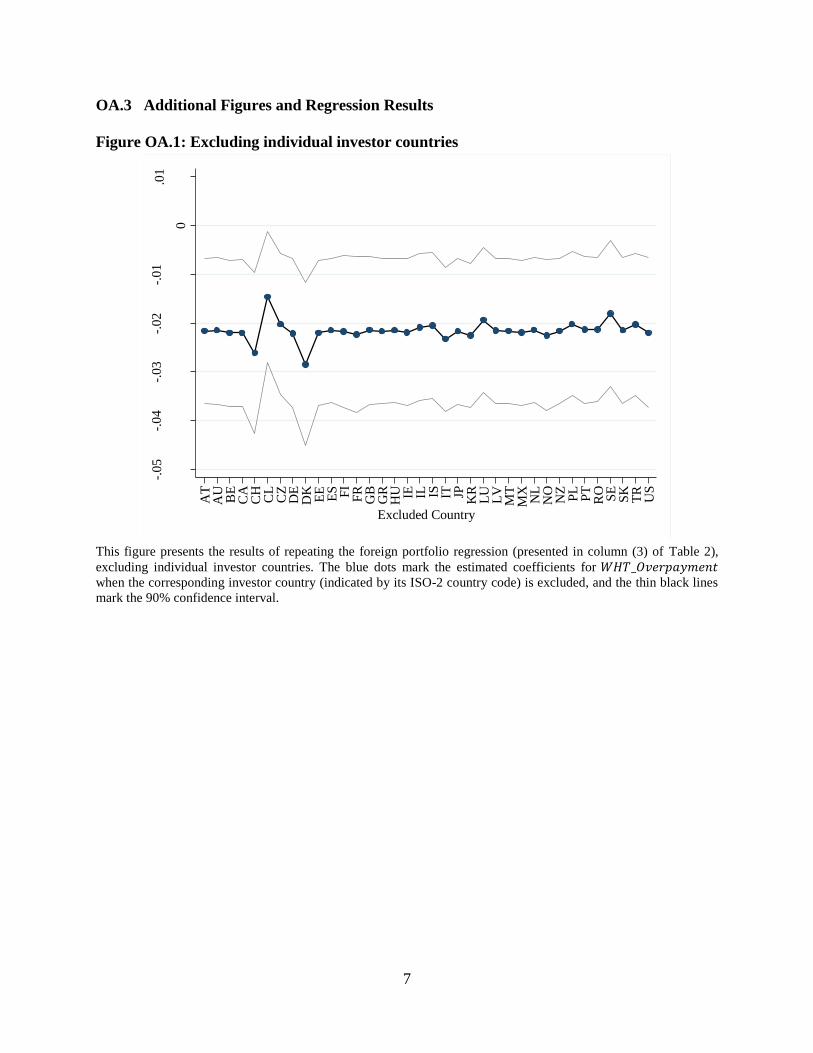

21 We also check whether our results are driven by single countries by excluding them one by one from the regression.

In the Online Appendix, we present the estimated coefficients for 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 by rerunning specification

(3) from Table 3, excluding individual investor countries. Throughout the specifications, the estimated coefficient

remains significantly negative. Thus, our findings are not the result of a particular country’s investment behavior.

29

current year would not respond to the tax variable changes in previous years (e.g., 𝑡 − 1 or 𝑡 − 2).

Figure 4 plots the results of this exercise for our variable of interest, 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 .

Although current increases in 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 reduce FPI, we find future changes in

𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 to have no significant effects on current FPI changes. We also cannot reject

the hypothesis of parallel pre-trends (i.e., that all estimated coefficients for

𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 changes in future years are jointly zero; t-statistic = 0.10), which further

validates our research design. Figure 4 also shows that the effect is immediate and persistent, as

indicated by the nonsignificant coefficients on lagged changes in 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 ,

suggesting that investors consider the compliance frictions ex ante in their investment decisions.

This result is consistent with institutional investors—the main driver of FPI—openly raising

concerns about the issue of frictions in claiming tax credits (e.g., European Federation of Investors

2011).

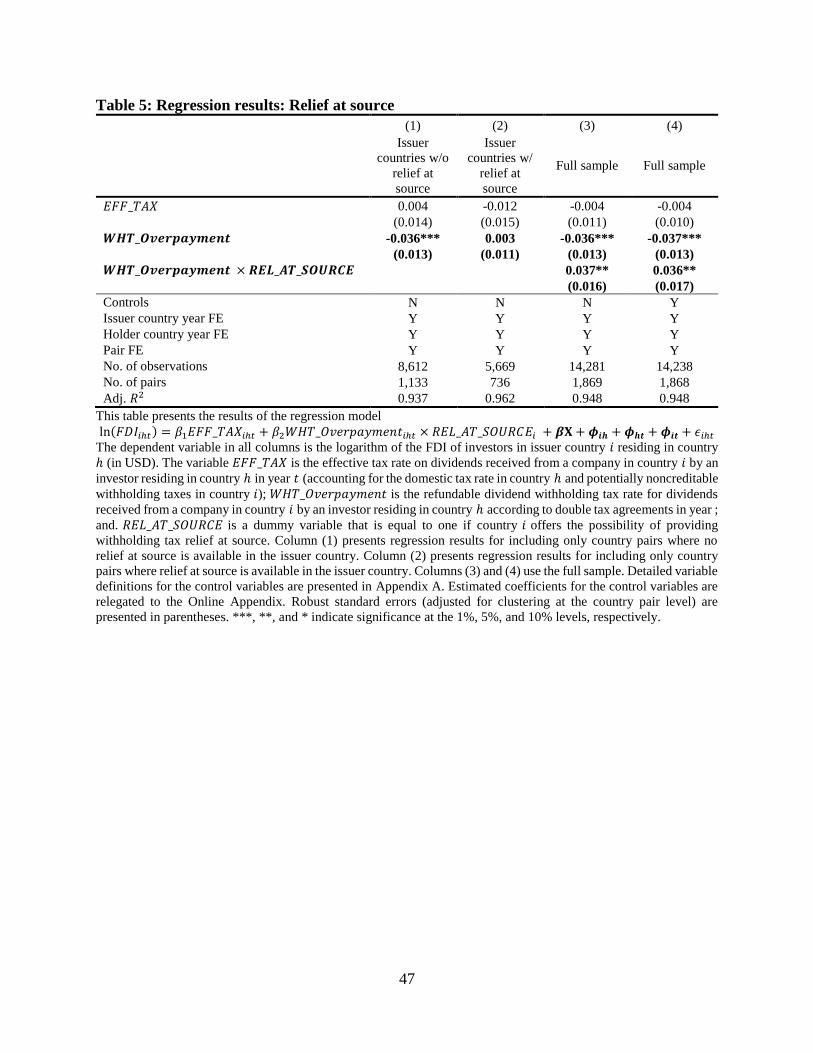

4.2 Heterogeneity in the FPI Effect of Withholding Tax Overpayments

In the next step, we examine the heterogeneity in the FPI effect of withholding tax

overpayments across country pairs (H2). Table 5 presents the results of our first test relating to the

existence of relief-at-source mechanisms. Column (1) shows the regression results for a sample

that includes only country pairs with an issuer country that does not allow for relief at source. The

coefficient of 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 remains significantly negative and increases in magnitude

compared to the baseline results presented in Table 3, consistent with the notion that it is issuer

countries without relief at source that impose the greatest frictions on foreign investors. In column

(2), we present the results for the subsample of country pairs where relief at source is available in

the issuer country. Here, the effect of 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 is nonsignificant, and, most

importantly, the economic magnitude of the coefficient is very close to zero. These results suggest

30

that the distortive effect of withholding tax overpayments is alleviated if the issuer country allows

for some sort of relief-at-source mechanism. Withholding tax overpayments no longer have

adverse effects on FPI given a relief-at-source mechanism in place. This finding is similar in the

full sample when interacting the relief-at-source dummy with 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡. Columns (3)

and (4) of Table 5 present these results without and with controls, respectively. This test also allows

us to show that the 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 coefficients for the two groups are statistically different

from each other.

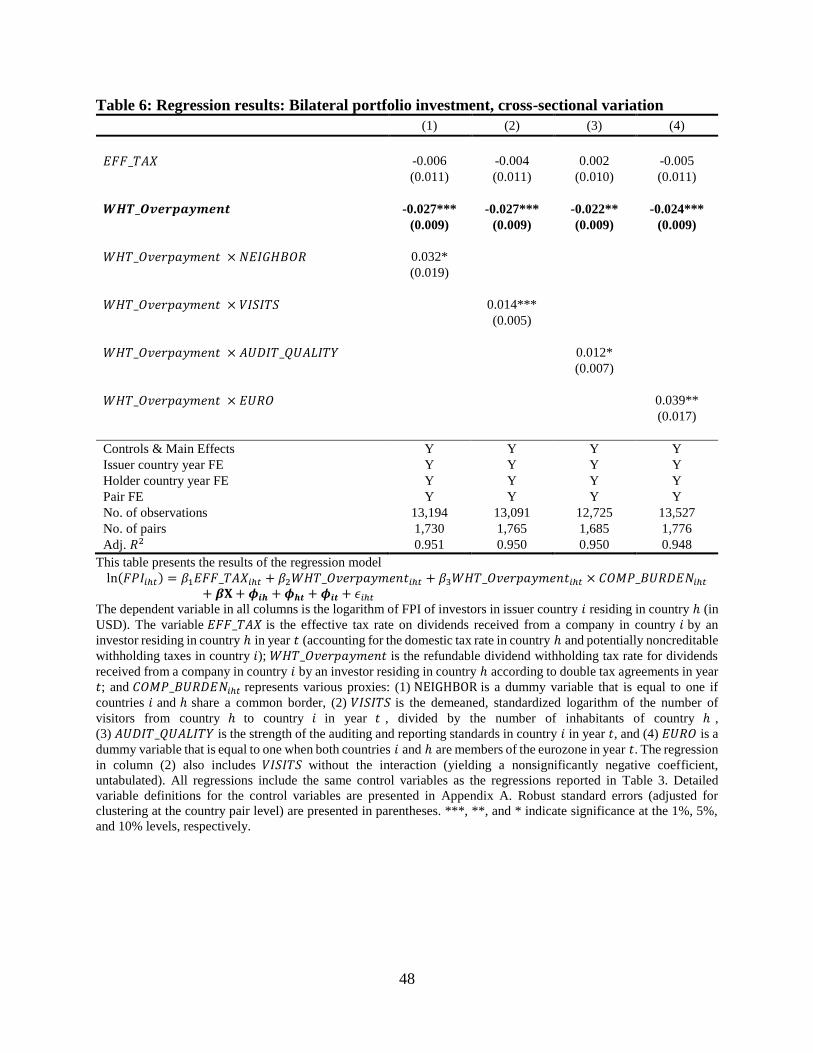

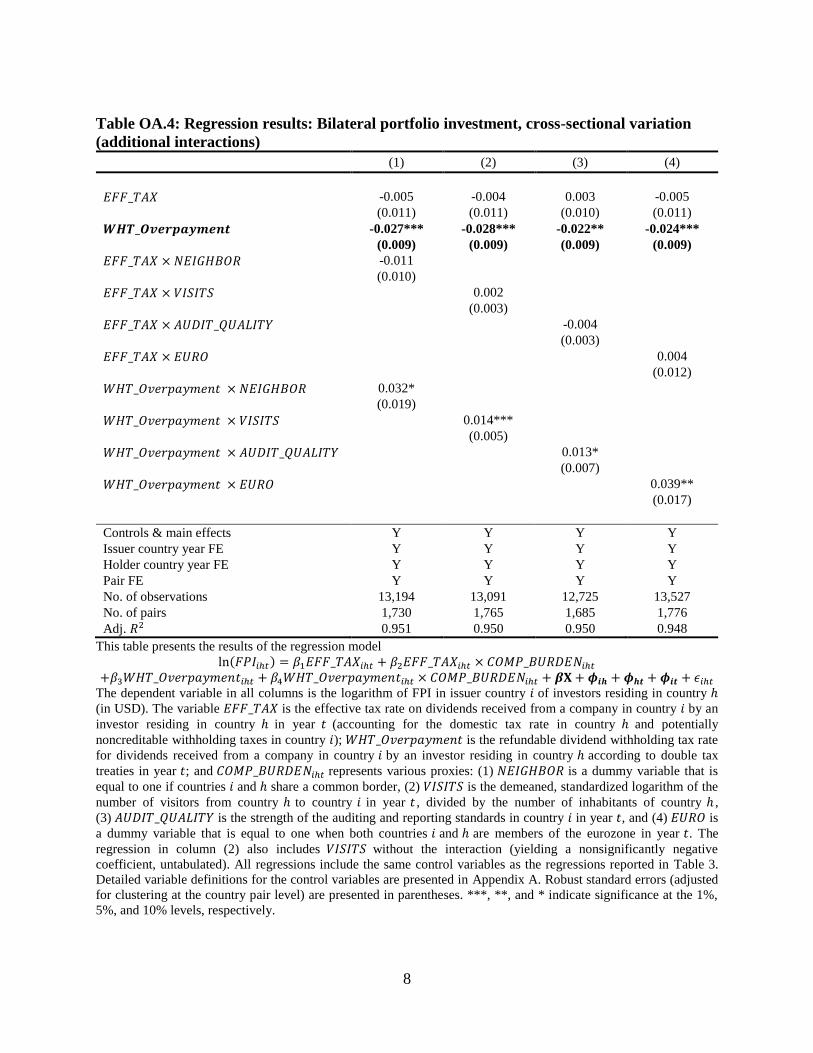

Next, we interact 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 with various proxies for the administrative costs to

file cross-border withholding tax claims.22 The results are presented in Table 6. Consistent with

H2, the negative effect of 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 on FPI is attenuated for investor–issuer country

pairs that are neighbors (column (1)) or have a higher number of bilateral visits (column (2)). Note

that our measure for bilateral visits is demeaned and standardized such that the coefficient must be

interpreted as estimated responses to deviations from its mean. Similarly, better audit and reporting

quality (column (3)) as well as a common currency (column (4)) mitigate the burden of

withholding tax overpayments. Across all specifications, the estimated coefficient on

𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 remains negative and significant. Hence, while the average effect of

𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 is significantly negative, there is substantial heterogeneity in the effect

across issuer and investor countries with respect to administrative costs for withholding tax

overpayment reclamation. These results further corroborate the notion that the compliance burden

of claiming withholding tax overpayments drives their negative effect on FPI.

22 As an additional test, we run regressions including the interactions of our cross-sectional test variables with

𝐸𝐹𝐹_𝑇𝐴𝑋. The results for these regressions are presented in the Online Appendix. If the proxy variables accurately

capture bilateral variation in compliance costs for withholding tax claims, the effect of 𝐸𝐹𝐹_𝑇𝐴𝑋, which constitutes

the tax payment—assuming that any overpayment has already been claimed—should not vary with these variables.

Indeed, none of the interactions with 𝐸𝐹𝐹_𝑇𝐴𝑋 turns out to be significant, while the estimated coefficients of the

interactions with 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 remain significant, with the expected sign.

31

4.3 Withholding Tax Overpayments and FPI: Investor-Level Evidence

While the previous results are based on aggregated FPI data, we next test H1 and H2 using

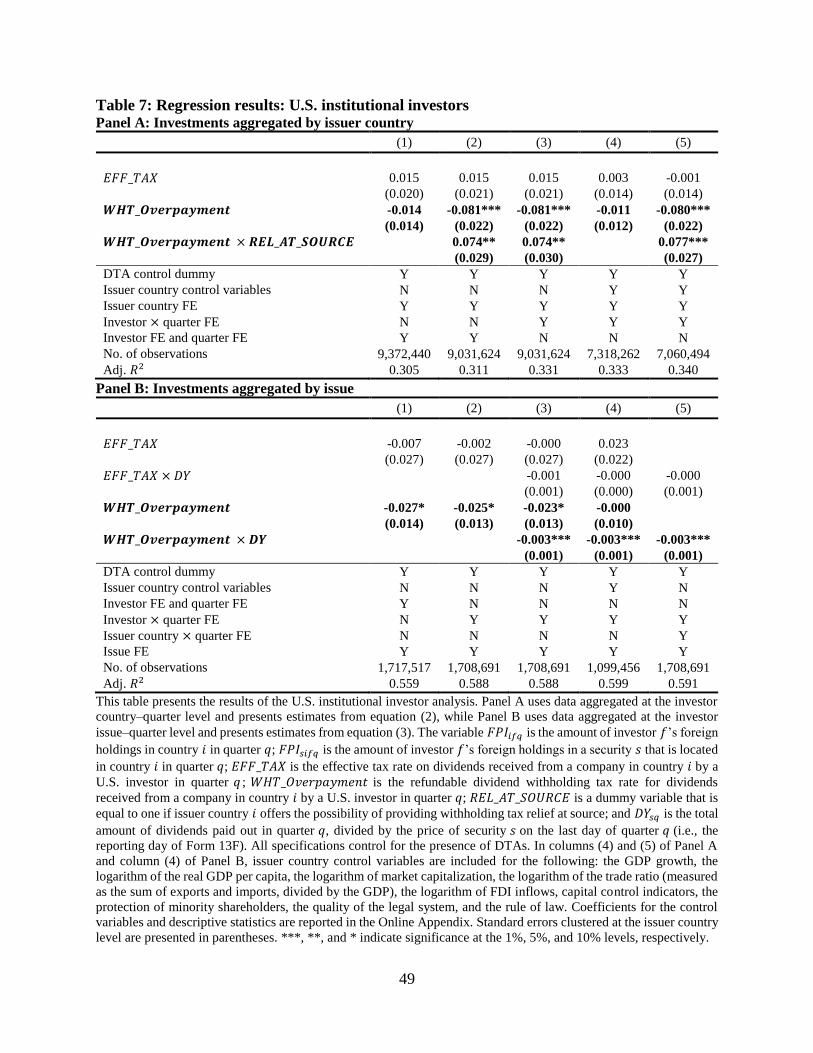

investor-level data on the foreign equity holdings of U.S. institutional investors. Panel A of Table

7 presents the results from estimating equation (2) for each possible combination of investor,

foreign country, and quarter. In column (1), we do not find any effect of withholding tax

overpayments on foreign investment. The potential reason for this nonsignificant average effect

can be seen in columns (2) and (3): once we interact 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛t with the relief-at-source

indicator, we find that withholding tax overpayments without a relief-at-source mechanism have a

significantly negative effect on foreign equity investments by institutional investors, as indicated

by the negative and significant 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 coefficient. The positive and significant

interaction of 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 and 𝑅𝐸𝐿_𝐴𝑇_𝑆𝑂𝑈𝑅𝐶𝐸 suggests that withholding tax

overpayments do not affect foreign investments if there a relief-at-source mechanism is in place

(the untabulated sum of coefficients -0.008 is nonsignificant). These results hold even when we

include a battery of country-level control variables (columns (4) and (5)).

In Panel B of Table 7, we turn to analyses where each observation represents an investment

by a mutual fund in a specific foreign firm in a given quarter. Columns (1) and (2) show that, on

average, withholding tax overpayments reduce institutional investors’ equity holdings in a specific

foreign firm. In columns (3) and (4), we additionally interact withholding tax overpayments with

the dividend yield (𝐷𝑌) to examine the role of dividend payouts at the investor–firm pair level.

We find results consistent with our prediction that the adverse effect of frictions in claiming foreign

withholding tax overpayments is stronger when firms pay dividends. This finding is indicated by

the negative and significant coefficient for 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 × 𝐷𝑌 . In column (5), we

additionally include foreign country–quarter fixed effects to absorb any foreign country–specific

32

observable and unobservable characteristic and dynamics (e.g., the main effect of

𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡). Again, we find empirical support for the prediction that the adverse effect

of frictions in claiming foreign withholding tax overpayments is stronger when foreign firms pay

dividends. Overall, the results in Table 7 confirm the findings in the bilateral analysis. Both micro-

and macro-level tests suggest compliance frictions in claiming foreign tax credits that reduce FPI.23

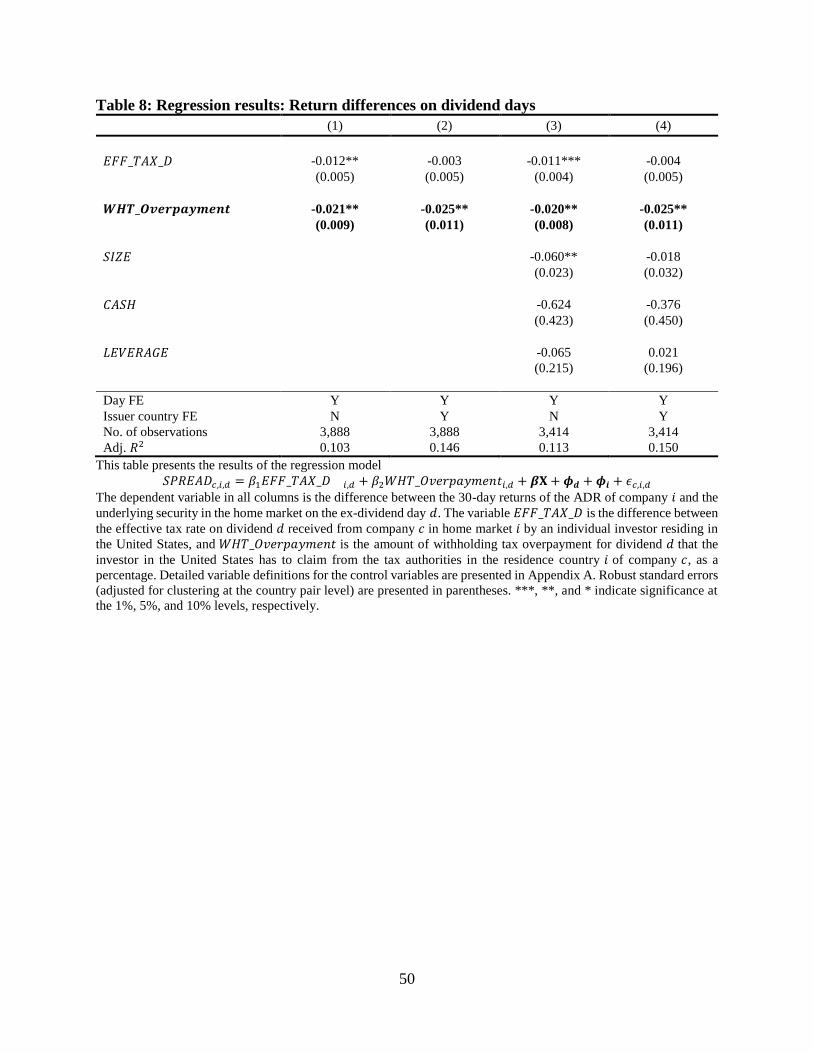

4.4 Withholding Tax Overpayments and Returns

In the final step, we examine the mechanism—lower returns—through which withholding

tax overpayments can affect FPI (H3). The results for the ADR pricing analysis are displayed in

Table 8. In columns (1) and (2), we only include the variables of interest and different sets of fixed

effects in the regression model. We find the withholding tax overpayment to have a negative effect

on the spread between ADR returns and the returns of their underlying securities in both

specifications, supporting H3. The effect is larger when we include issuer country fixed effects in

addition to day fixed effects, pointing to confounding factors at the country level. For example,

issuer countries with high dividend withholding taxes can also have better institutions or more

dynamic stock markets. Our results remain robust when adding firm-level control variables

capturing size, leverage, and cash flow in columns (3) and (4). Taking the estimate in column (4)

as a benchmark, we find that the difference between the return of an ADR and the return of its

underlying security decreases by 25 basis points in response to a one percentage point increase in

withholding tax overpayment. This result implies that investors perceive withholding tax

overpayments as an additional cost and have a lower valuation of dividends from stock with larger

withholding tax overpayments, which is reflected in the issuing firm’s lower ADR returns.

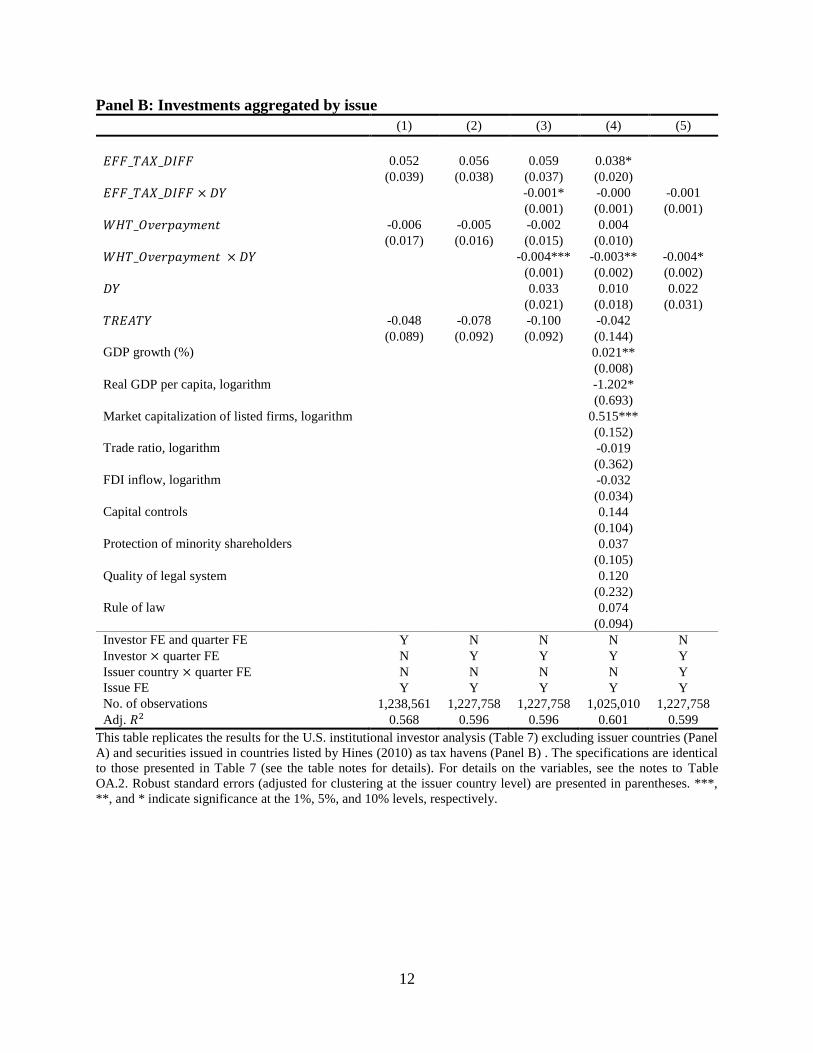

23 In the Online Appendix, we show that these results are robust to the exclusion of locations that commonly serve as

financial centers (e.g., tax havens).

33

To demonstrate that the effect of withholding tax overpayments is related to the valuation of

dividends and not to other unobservable factors, we conduct a placebo test in which we randomly

assign the dividend day within each issuer–year and then rerun specification (2) of Table 8. We

repeat this exercise for 10,000 different random assignments of the dividend day and find that the

estimated coefficient for 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 is significantly negative (95% confidence interval)

and smaller or equal to our benchmark coefficient in only 3% of the estimations (see Figure 5).

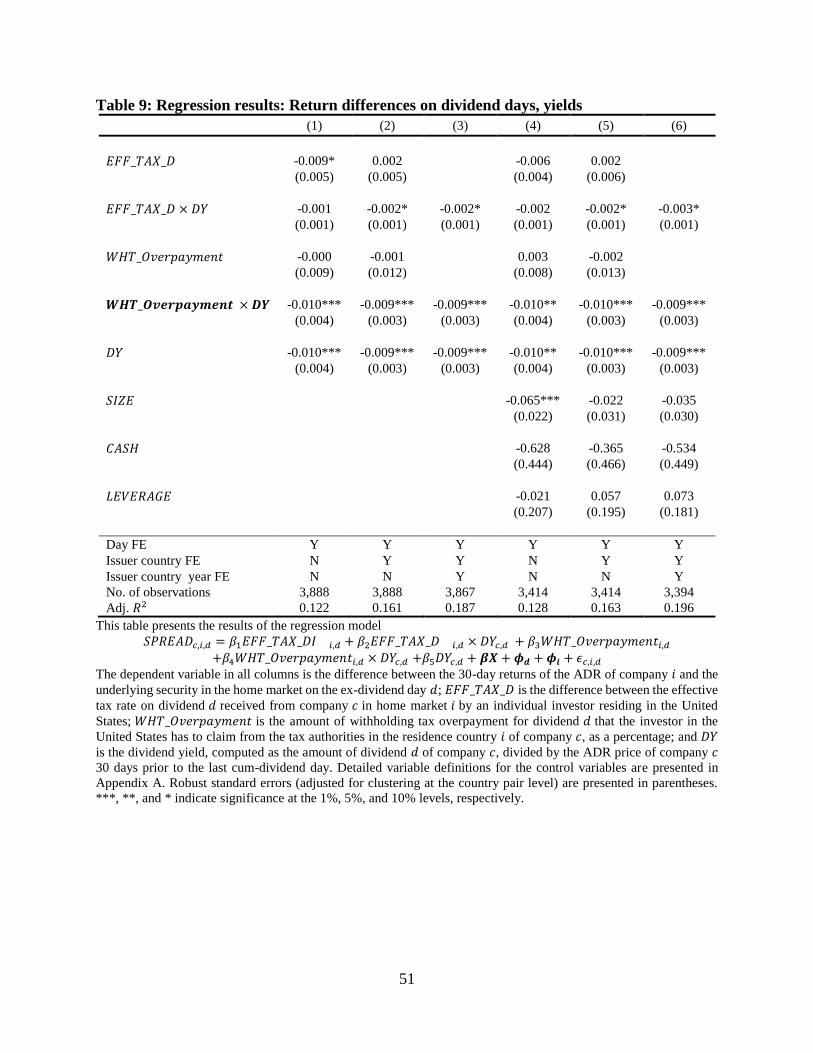

Since the magnitude of withholding tax overpayments depends on the size of the dividend,

we expect the negative effect of withholding tax overpayments on the return spread to increase

with the dividend yield. Table 9 presents the results of adding interactions of the dividend yield

with the tax rate variables to the benchmark model. We first present the results from parsimonious

models without and with issuer country fixed effects in columns (1) and (2) and then add issuer

country–specific year fixed effects in column (3). Columns (4) to (6) include additional firm-level

controls. The estimated coefficient for the interaction of 𝑊𝐻𝑇_𝑂𝑣𝑒𝑟𝑝𝑎𝑦𝑚𝑒𝑛𝑡 and the dividend

yield (𝐷𝑌) is significantly negative in all specifications, which implies that larger dividend yields

lead to a more negative effect of withholding tax overpayments. Note that, with the issuer country–

specific year fixed effects in columns (3) and (6), the identification is further strengthened, since

any issuer country–specific dynamics are controlled for and the impact of withholding tax

overpayments is identified from variations in their effect across dividend payments with different

dividend yields.

5 Conclusion

This paper examines the effect of compliance frictions in claiming foreign withholding taxes

on FPI. While the international withholding tax system is generally designed such that it does not

distort the location of FPI, we show that withholding taxes can affect FPI due to compliance

34

hurdles in claiming foreign tax credits. A significant part of the tax credit—the difference between

the reduced withholding tax rate in the respective DTA and the standard withholding tax in the

foreign country (the withholding tax overpayment)—must be claimed from foreign tax authorities.

We show that claiming these foreign credits results in frictions that prevent investors from

investing abroad. A one percentage point decrease in the rate of withholding tax overpayments

increases FPI by a particular investor country in the issuer country by 2.3%. This effect is

attenuated when there is a relief-at-source mechanism and for geographically close countries,

country pairs with high numbers of mutual visitors, issuer countries with higher audit quality, and

countries in the eurozone. Finally, we also show that withholding tax overpayments are reflected

in share prices, indicating that withholding tax overpayments represent an economically significant

cost to investors.

Our results show that compliance costs in granting withholding tax credits to foreign

investors adversely affect FPI. While such frictions in the process of claiming tax credits could

secure tax revenues for the country in which the firm is located, reduced FPI could come at the

cost of lowering the investment activities of domestic firms and, in particular, of financially

constrained firms, which could benefit from increased access to capital via FPI. Hence, our results

also have policy implications. Higher tax revenues from unclaimed credits come at the cost of

reduced investment and, thus, economic growth. We do not, however, conduct a full welfare

analysis. Our results are informative to the debate on cross-border investments and offer another

potential friction contributing to the home bias (French and Poterba 1991; Cooper and Kaplanis

1994; Lewis 1999).

35

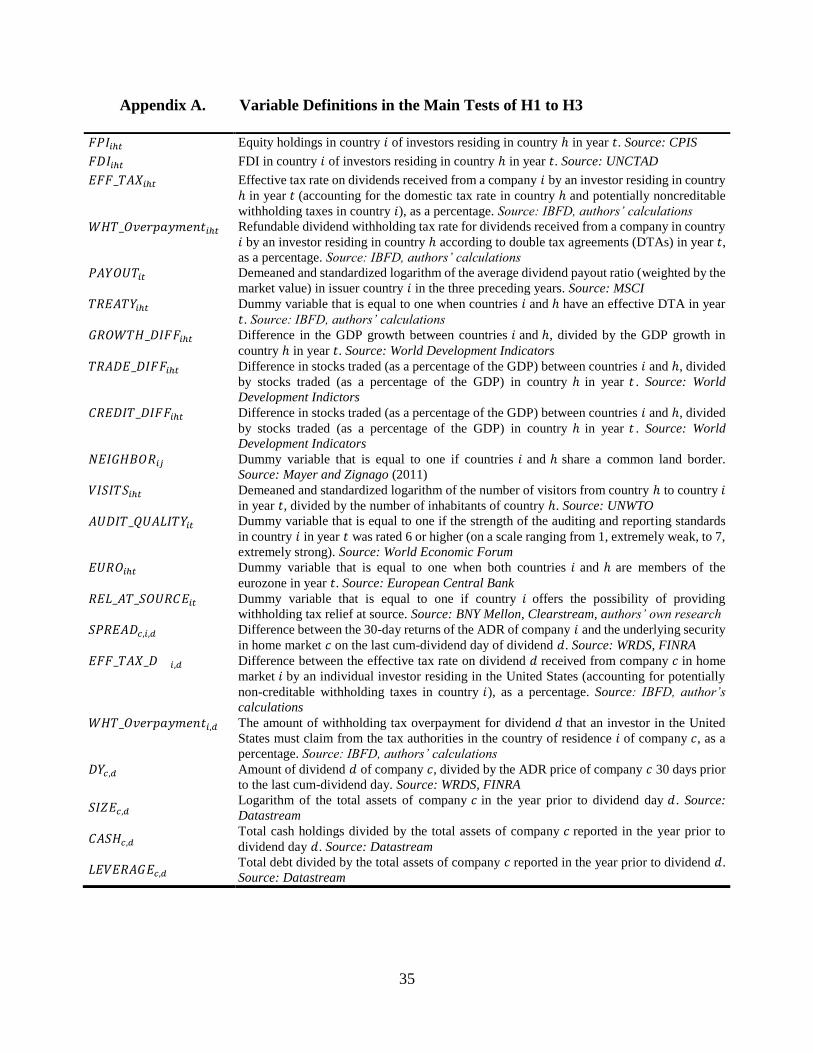

Appendix A. Variable Definitions in the Main Tests of H1 to H3

𝐹𝑃𝐼𝑖ℎ𝑡 Equity holdings in country 𝑖 of investors residing in country ℎ in year 𝑡. Source: CPIS

𝐹𝐷𝐼𝑖ℎ𝑡 FDI in country 𝑖 of investors residing in country ℎ in year 𝑡. Source: UNCTAD