Embed Size (px)

Citation preview

Today we are going to be discussing the concepts of IRA

maximization and reviewing five different strategies. All of our

clients are different, in a different situation and each of these

strategies may or may not fit a particular client. We are not

trying to fit a square peg in a round hole. We put the client first

and that’s really what we want to do. These strategies are going

to allow us to transfer the value of the IRA efficiently and we

are going to potentially enhance the overall amount to the

beneficiaries.

So what is IRA Max? What is IRA Max to us?

Let’s talk about what IRA Max is not first. It’s not IRA rescue,

it’s not some bogus sales pitch that is being put out there by

other agents or insurance companies, we are not taking a

bunch of money out of it IRA, slamming it into an IUL. (Index

Universal Life) For more information on IRA rescue please visit

www.stopirarescue.com. This consumer protection website

was set up by a colleague that I work with and I have nothing to

do with his website. It’s just a great resource if you need more

information.

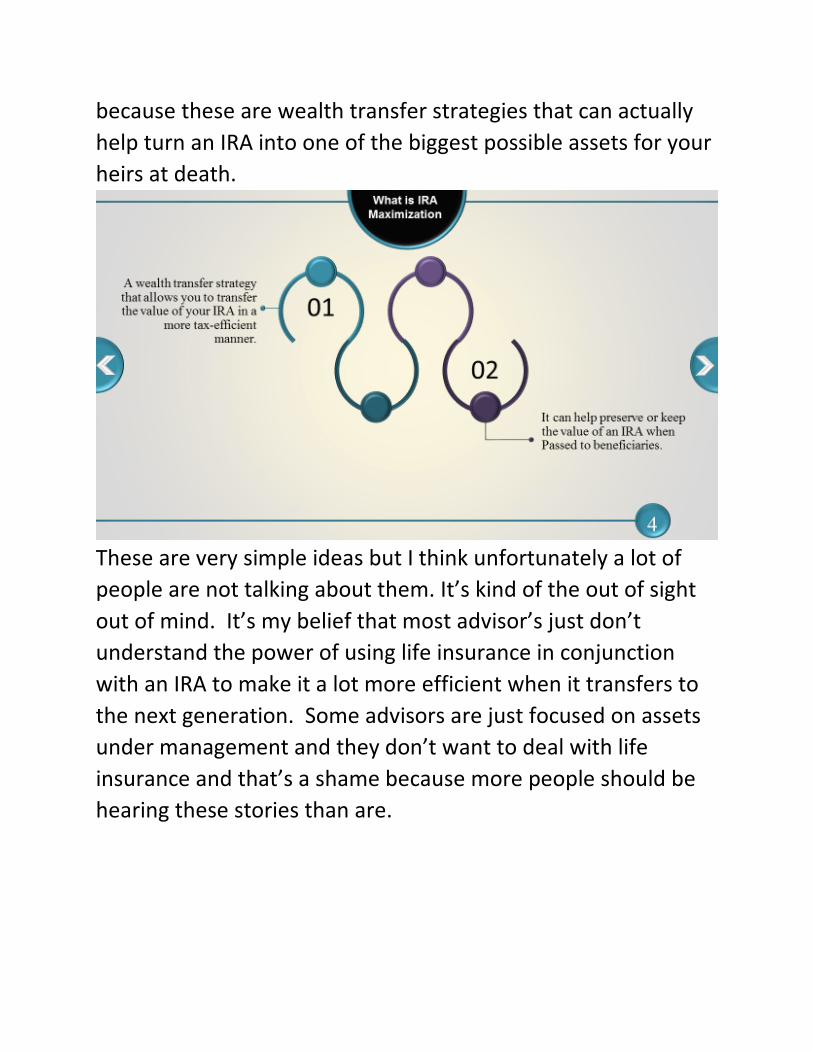

This is really a legitimate strategy and it’s about doing what’s

right. It may not be for all of our clients but it may be for a few,

and enhancing the legacy for a few for these clients can be

pretty significant. So like I said, this is going to be legitimate,

because these are wealth transfer strategies that can actually

help turn an IRA into one of the biggest possible assets for your

heirs at death.

These are very simple ideas but I think unfortunately a lot of

people are not talking about them. It’s kind of the out of sight

out of mind. It’s my belief that most advisor’s just don’t

understand the power of using life insurance in conjunction

with an IRA to make it a lot more efficient when it transfers to

the next generation. Some advisors are just focused on assets

under management and they don’t want to deal with life

insurance and that’s a shame because more people should be

hearing these stories than are.

So the question is, who can benefit from it?

Well there are quite a few people that can benefit from it but

let me give you a client profile. The three categories above

apply to IRA Max strategies but let’s talk about age. Obviously

we are dealing with an IRA, so we are dealing with qualified

assets, so we need to be at least 59 ½ right? In the example

that we are going to go through, we are typically going to use

70. The age we are using is seventy because 70 1/2 of course is

RMD time. But who does this fit? Individuals who don’t need

their IRA assets for their retirement income needs. These

people are not interested really in generating an income off of

it, rather they are interested in transferring it and really

creating a legacy for the beneficiaries. So really the question

that people should be asking is:

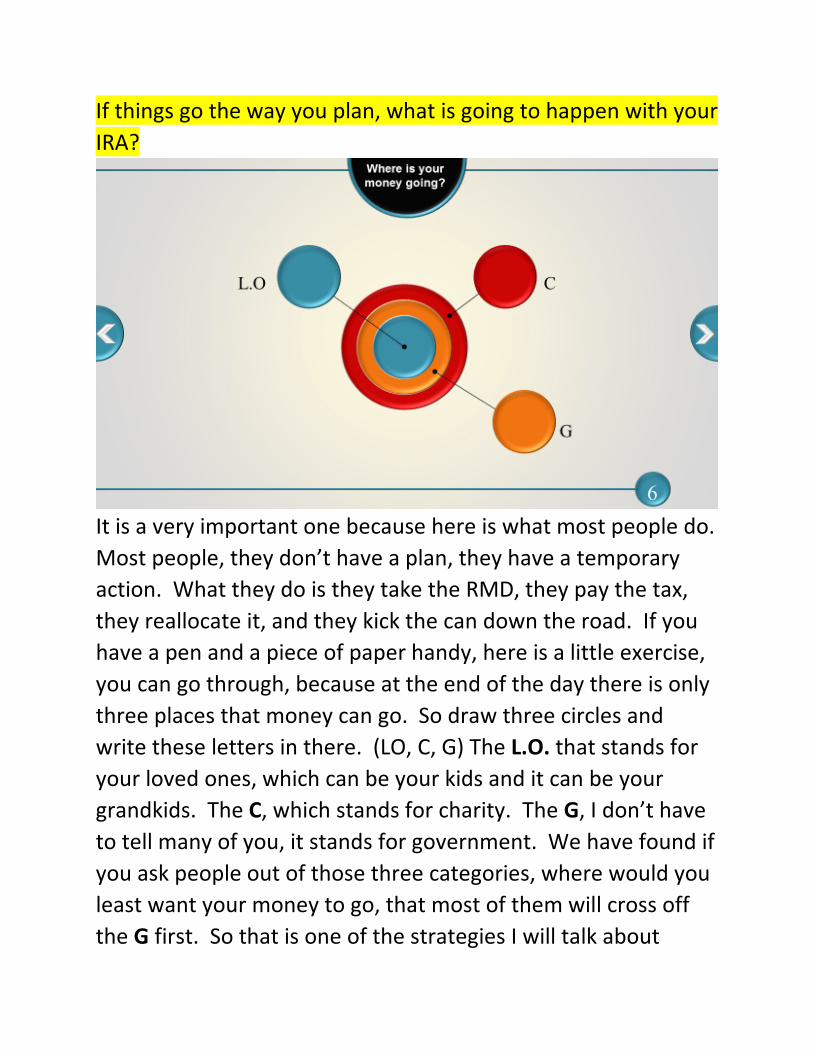

If things go the way you plan, what is going to happen with your

IRA?

It is a very important one because here is what most people do.

Most people, they don’t have a plan, they have a temporary

action. What they do is they take the RMD, they pay the tax,

they reallocate it, and they kick the can down the road. If you

have a pen and a piece of paper handy, here is a little exercise,

you can go through, because at the end of the day there is only

three places that money can go. So draw three circles and

write these letters in there. (LO, C, G) The L.O. that stands for

your loved ones, which can be your kids and it can be your

grandkids. The C, which stands for charity. The G, I don’t have

to tell many of you, it stands for government. We have found if

you ask people out of those three categories, where would you

least want your money to go, that most of them will cross off

the G first. So that is one of the strategies I will talk about

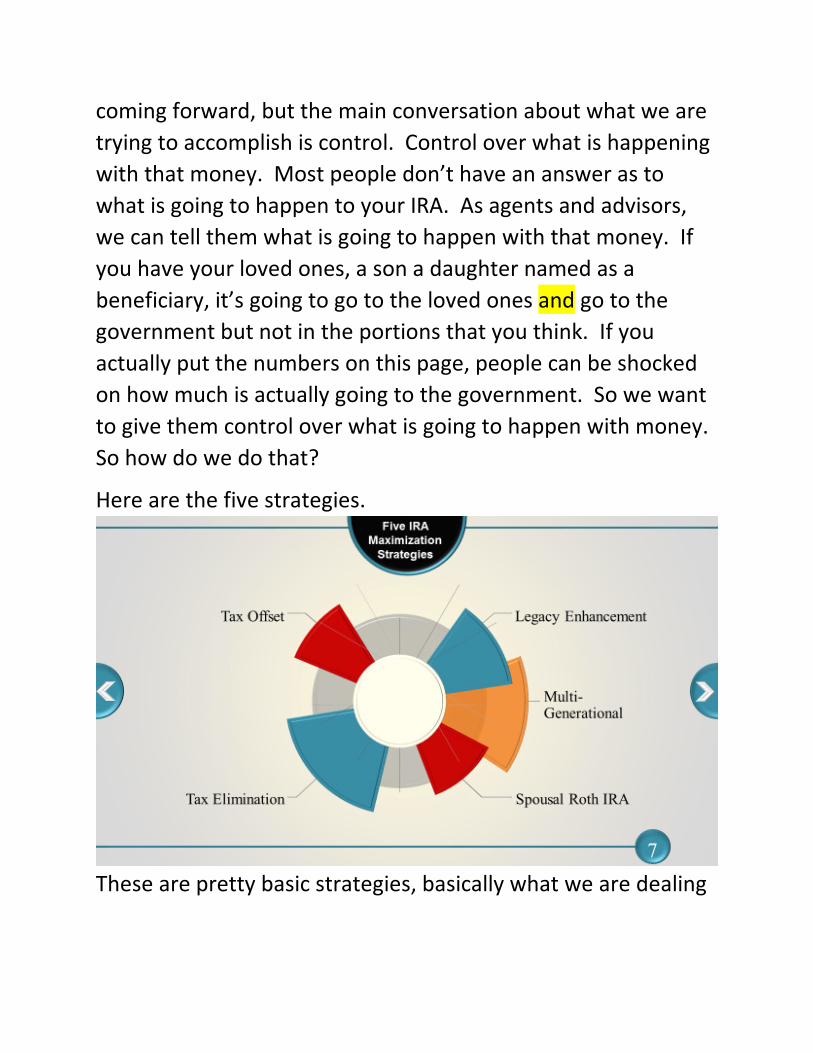

coming forward, but the main conversation about what we are

trying to accomplish is control. Control over what is happening

with that money. Most people don’t have an answer as to

what is going to happen to your IRA. As agents and advisors,

we can tell them what is going to happen with that money. If

you have your loved ones, a son a daughter named as a

beneficiary, it’s going to go to the loved ones and go to the

government but not in the portions that you think. If you

actually put the numbers on this page, people can be shocked

on how much is actually going to the government. So we want

to give them control over what is going to happen with money.

So how do we do that?

Here are the five strategies.

These are pretty basic strategies, basically what we are dealing

with is, where do we name the beneficiaries of the IRA and

where do we name the beneficiaries of life insurance.

Tax offset, helps minimize the tax burden your beneficiaries

receive due to inheriting the IRA. It’s done by using a life

insurance policy to offset the projected amount of income

taxes they would owe when they inherit the IRA. (Keep thinking

about those three circles as we go through this.)

Tax elimination, that’s going to cross that G off the list. This

strategy is for those that have charitable interests and also

want to leave assets to their heirs. Wouldn’t it be nice to be

able to give more to your favorite charity without taking away

from your children’s inheritance? The strategy is designed to

help eliminate income tax on the death of the IRA owner by

designating a charity as the IRA beneficiary. The charity

receives the IRA tax free and the beneficiaries receive the death

benefit from the life insurance proceeds tax free.

Legacy enhancement, maybe you just want to give more, we

just don’t want to take care of the taxes but we want to

leverage what we are going to give to the next generation. This

is done by reallocating the after-tax excess earnings from the

IRA into a life insurance policy that can potentially increase the

overall inheritance.

Multi-generational planning with IRA stretch is going to be the

most powerful one of them all. When you look at the numbers

it’s going to look ridiculous but it works and we can prove it.

This strategy is for those that want to create a financial legacy

that last generations. This strategy is based on the fact that

when an IRA is passed to the grandchildren, the tax deferral

period allowed by the IRS is often dramatically increased. If you

are looking to create a legacy for multiple generations this can

be an effective strategy. (You really need to look at the

number on this one to appreciate the effectiveness of this

strategy.)

Spousal Roth IRA, creates a plan to provide the money needed,

so your spouse can convert a traditional IRA to a Roth IRA and

create a financial legacy for your heirs. This strategy is really

similar to tax offset.

I have tried to keep this information basic to provide a 10,000-

foot overview if you will to give you some ideas without

overwhelming the reader with boring technical details. For in

depth analysis of the different case studies I have professional

marketing pieces that provide better details than what I can put

together in a short, readable, ebook.

So in conclusion, it kind of goes back to what I was trying to do,

where we were trying to create control. Think back to those

three circles, think back to what’s going to happen with that

asset. I’m not saying everybody with an IRA or significant IRA is

going to be a candidate for this, but we have turned that short

term action into a long term strategy. We have given them

control over what will happen. Maybe not full control because

uncle Sam is going to do what they are going to do but, we’ve

given them some control. Give us a call we will work with you

on an individual basis because there are so many variables that

go into this it really needs to be customized for your specific set

of circumstances. Below is my personal contact information.

Feel free to contact me with questions or to look at

hypothetical case studies. We don’t pitch a company or a

particular product, we put the client first utilizing the best

product to achieve the desired result for that particular client.

This is how generational wealth is created!