Embed Size (px)

Citation preview

®

QoL Max Accumulator+An Individual Fixed Index Interest Flexible Premium Adjustable Life Insurance Policy Life Insurance Policy Illustration

Designed forMrs. VCClient State: ID

Presented byLee Rogers WA

Date PreparedJune 17, 2016

Issued by:

American General Life InsuranceCompany2727-A Allen ParkwayHouston, TX 77019

Please read your illustration carefully. It is designed to aid your understanding of the policy bydemonstrating how policy benefits and premiums are affected under different assumptions. Thisillustration is not a contract and is not intended to predict actual performance.

This information may be subject to change, and does not constitute legal, tax or accounting advicefrom American General Life Insurance Company (AGL), its employees, financial professionals orother representatives. Applicable laws and regulations are complex and subject to change. Any taxstatements in this material are not intended to suggest the avoidance of U.S. federal, state or localtax penalties. For advice concerning your individual circumstances, consult your attorney, tax advisoror accountant.

Issuing insurance company AGL is a member of American International Group, Inc. (AIG). Guaranteesare backed by the claims-paying ability of the issuing insurance company.

(Form ICC15-15646)

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 1 of 42

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 2 of 42

TABLE OF CONTENTS (For Basic Illustration)

Your Policy Highlights.......................................................................................................................................................................... Page 3

Your QoL Selectchoice II Accelerated Death Benefit Riders Summary............................................................................................... Page 4

Your QoL Select Choice II Critical Illness Accelerated Death Benefit........................................................................................ Page 4

Your QoL Select Choice II Chronic Illness Accelerated Death Benefit...................................................................................... Page 5

Your QoL Select Choice II Terminal Illness Accelerated Death Benefit..................................................................................... Page 5

Your Narrative Summary................................................................................................................................................................... Page 11

Life Insurance Illustration Summary........................................................................................................................................ Page 11

Policy Coverage Summary ...................................................................................................................................................... Page 11

Important Information About Your Illustration........................................................................................................................... Page 12

Your Accumulation Strategies.................................................................................................................................................. Page 13

Interest Crediting............................................................................................................................................................... Page 13

Historical Graphs ............................................................................................................................................................... Page 15

Min/Average/Max Historical Performance......................................................................................................................... Page 16

Historical Index Table........................................................................................................................................................ Page 17

Your Distribution Options......................................................................................................................................................... Page 18

Policy Loans...................................................................................................................................................................... Page 18

Your Income for Life Rider................................................................................................................................................. Page 19

Your Policy Features and Riders............................................................................................................................................. Page 20

Key Terms And Definitions....................................................................................................................................................... Page 21

Your Numeric Summary (Signature Page)........................................................................................................................................ Page 24

Your Tabular Detail ............................................................................................................................................................................ Page 25

Illustration Assumptions For Non-Guaranteed Interest Rates........................................................................................................... Page 30

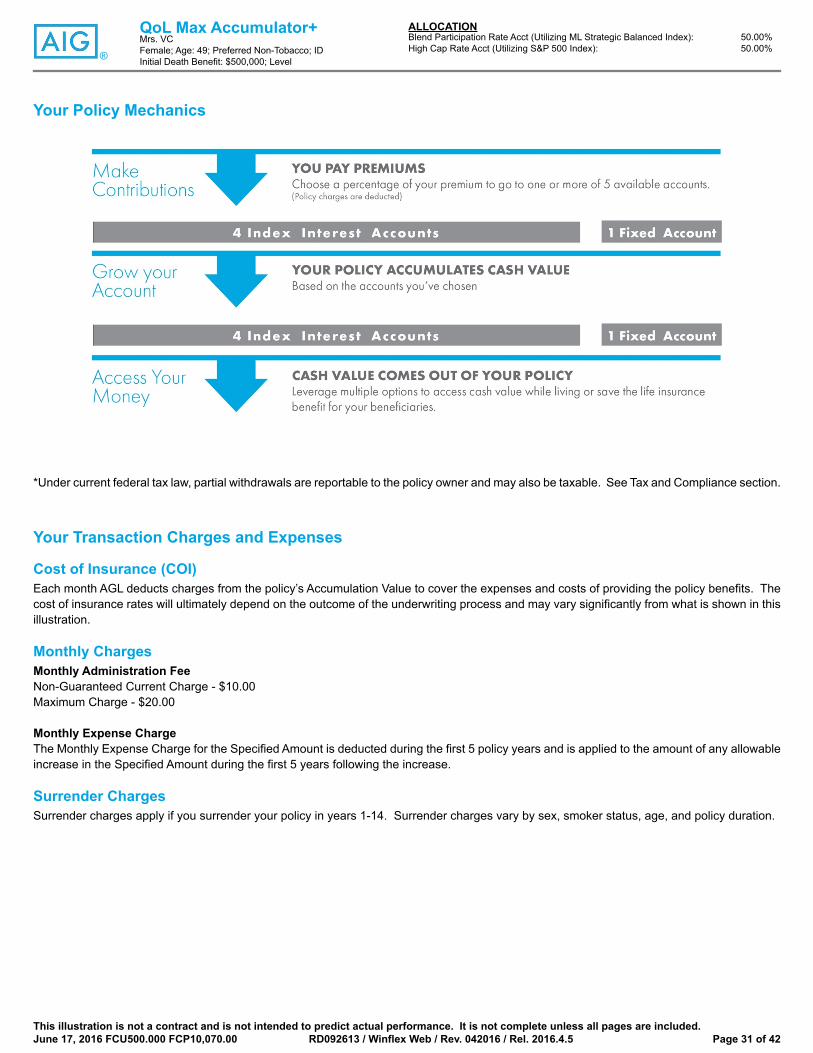

Your Policy Mechanics ...................................................................................................................................................................... Page 31

Your Transaction Charges And Expenses......................................................................................................................................... Page 31

Tax And Compliance.......................................................................................................................................................................... Page 32

Additional Information Regarding Your QoL SelectChoice II Accelerated Benefit Riders................................................................. Page 35

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

YOUR POLICY HIGHLIGHTSYour QoL Max Accumulator+ is an Individual Fixed Index Interest Flexible Premium Adjustable Life Insurance policy. Since it is a life insurancepolicy, your beneficiaries may receive a tax-free death benefit1 upon the insured's death, helping to protect your loved ones against financialuncertainty.

In addition to providing valuable life insurance protection, QoL Max Accumulator+ offers potential opportunities for you to receive benefits whileliving. These living benefits may be accessed through several means:

• Distributions via policy loans and withdrawals - Your cash accumulation can grow on a tax-deferred basis and you can potentiallyaccess it tax-free1 for any purpose, such as supplementing retirement income or helping with education funding.

• Distributions via a guaranteed income rider - With the Income for Life Rider2, you may receive a guaranteed annual stream ofincome upon exercise of the rider.

• Benefits via a chronic illness accelerated death benefit rider - With the Accelerated Access Solution® (AAS) rider, you mayreceive benefits in the event of a qualifying chronic illness.

1Based on current tax laws. Death benefit may not always qualify as tax-free. See the Tax and Compliance section.2Based on the factors used by the Company, it is possible that no benefit would be available under the rider. A one-time fee will apply when therider is exercised. See the Income for Life Rider section.3Initial planned premium.4Assumes initial distribution amount at age 66 for 36 years. See Tabular Detail section.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 3 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

YOUR QoL SELECTCHOICE II ACCELERATED DEATH BENEFIT RIDERS SUMMARYThe QoL SelectChoice II Accelerated Death Benefit Riders for Critical, Chronic and Terminal Illness are three valuable riders automaticallyincluded in your policy at no additional cost that allow you to access all or a portion of your QoL Max Accumulator+ policy death benefit if youhave a qualifying critical, chronic or terminal illness or condition. Each accelerated death benefit rider may be subject to requirements andlimitations not specifically described in this quotation. See each rider for additional terms, conditions, and limitations.

The QoL SelectChoice II Accelerated Death Benefit Riders allow you to receive a portion of the death benefit under the policy, during yourlifetime, upon submission of required documentation regarding a qualifying event. The death benefit that you elect to accelerate will be paid ata discounted amount because it is being paid prior to the actual time of death. However, the accelerated death benefit you receive will not beless than the guaranteed minimum benefit based on different categories of illnesses, subject to the terms and conditions of the rider.

The following are hypothetical examples of benefits that you may receive from the QoL SelectChoice II Accelerated Death Benefit Riders fordifferent types of illnesses if you file a claim to accelerate the full death benefit of your policy for a qualifying illness or event. The hypotheticalamounts shown assume that no policy premiums are unpaid and that there is no loan balance. Amounts do not reflect any applicable administrativecharge. Also, if you choose to elect less than your policy's full death benefit, the actual payment will be lower than the examples provided below,but your policy's remaining death benefit will be higher.

Please see the rider description section of this quotation for the definitions of these qualifying illnesses or conditions and for additional ImportantConsiderations and Disclosures.

QoL SELECTCHOICE II CRITICAL ILLNESS ACCELERATED DEATH BENEFIT

The values below represent the guaranteed minimum benefit and the potential benefit payout for a hypothetical example* when a claim is filedat the estimated age below to accelerate the full initial death benefit of the policy as a lump sum payment for a qualifying critical illness (MajorHeart Attack, Coronary Artery Bypass, Stroke, Invasive Cancer, Major Organ Transplant, End Stage Renal Failure, Paralysis, Coma, SevereBurn). For a qualifying critical illness, the actual benefit paid will never be less than the guaranteed minimum benefit (Minimum AcceleratedBenefit Amount) calculated using the applicable percentages on the Minimum Accelerated Benefit Percentage page of the Rider Schedule.

*The hypothetical example shown assumes that the policy is issued with a life insurance benefit of $500,000 on a female, age 45, StandardNon-Tobacco. Hypothetical amounts shown assume that no policy premiums are unpaid and that there is no loan balance. The potential benefitpayouts were calculated using assumptions that are not guaranteed and may be changed at any time. Actual payouts may be more or lessfavorable.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 4 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

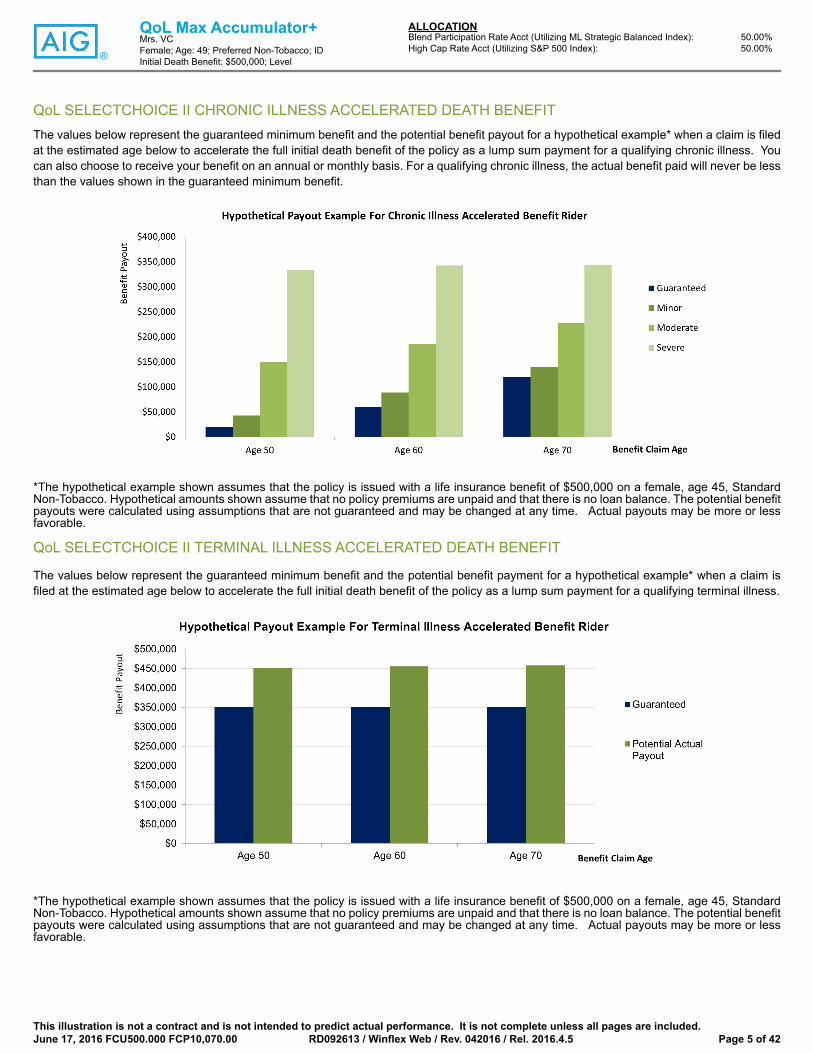

QoL SELECTCHOICE II CHRONIC ILLNESS ACCELERATED DEATH BENEFITThe values below represent the guaranteed minimum benefit and the potential benefit payout for a hypothetical example* when a claim is filedat the estimated age below to accelerate the full initial death benefit of the policy as a lump sum payment for a qualifying chronic illness. Youcan also choose to receive your benefit on an annual or monthly basis. For a qualifying chronic illness, the actual benefit paid will never be lessthan the values shown in the guaranteed minimum benefit.

*The hypothetical example shown assumes that the policy is issued with a life insurance benefit of $500,000 on a female, age 45, StandardNon-Tobacco. Hypothetical amounts shown assume that no policy premiums are unpaid and that there is no loan balance. The potential benefitpayouts were calculated using assumptions that are not guaranteed and may be changed at any time. Actual payouts may be more or lessfavorable.

QoL SELECTCHOICE II TERMINAL ILLNESS ACCELERATED DEATH BENEFIT

The values below represent the guaranteed minimum benefit and the potential benefit payment for a hypothetical example* when a claim isfiled at the estimated age below to accelerate the full initial death benefit of the policy as a lump sum payment for a qualifying terminal illness.

*The hypothetical example shown assumes that the policy is issued with a life insurance benefit of $500,000 on a female, age 45, StandardNon-Tobacco. Hypothetical amounts shown assume that no policy premiums are unpaid and that there is no loan balance. The potential benefitpayouts were calculated using assumptions that are not guaranteed and may be changed at any time. Actual payouts may be more or lessfavorable.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 5 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

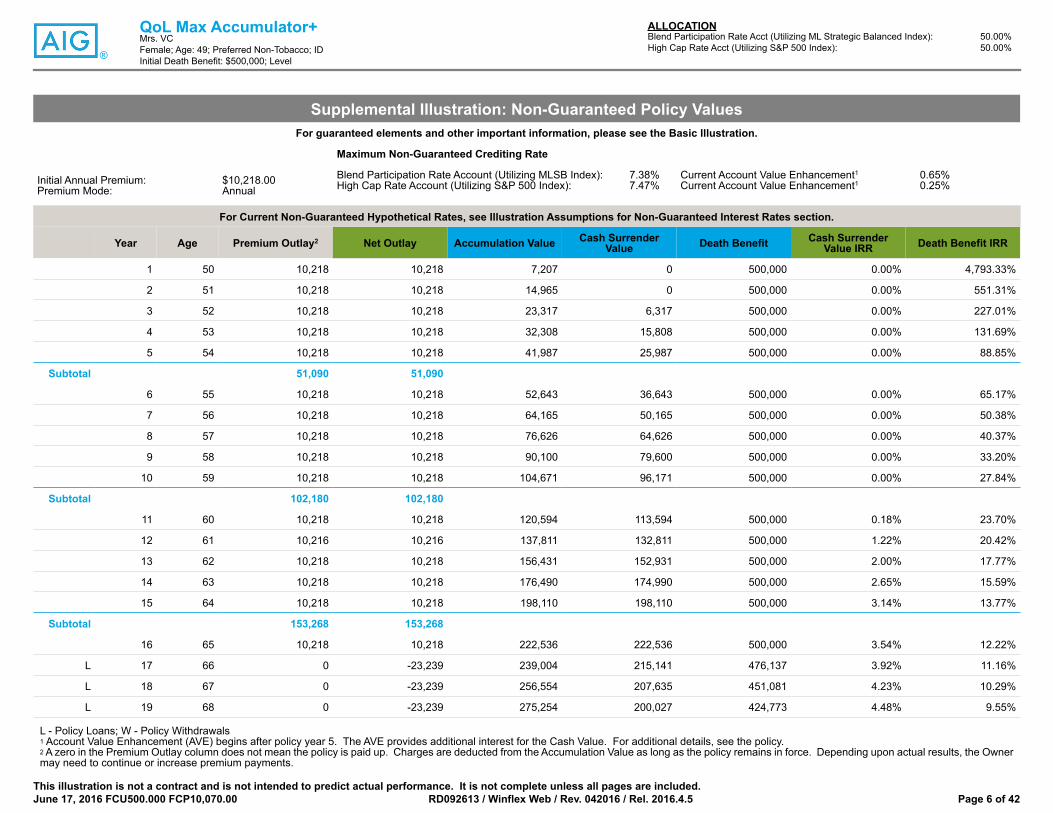

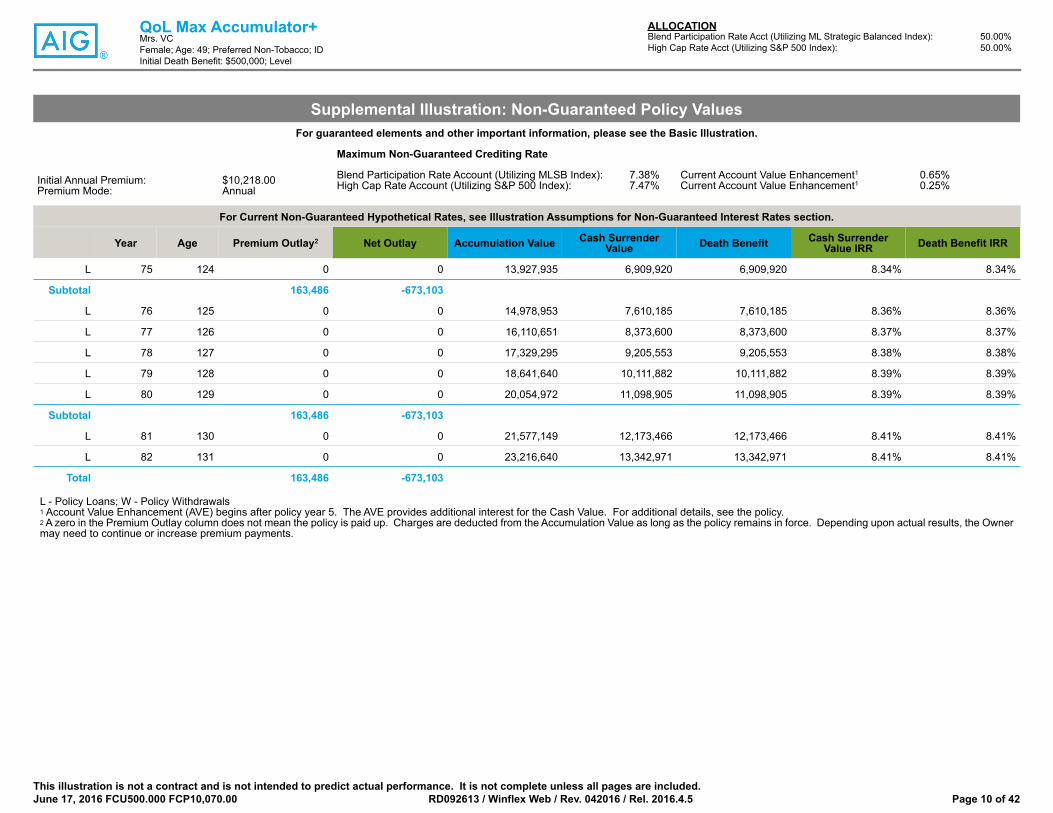

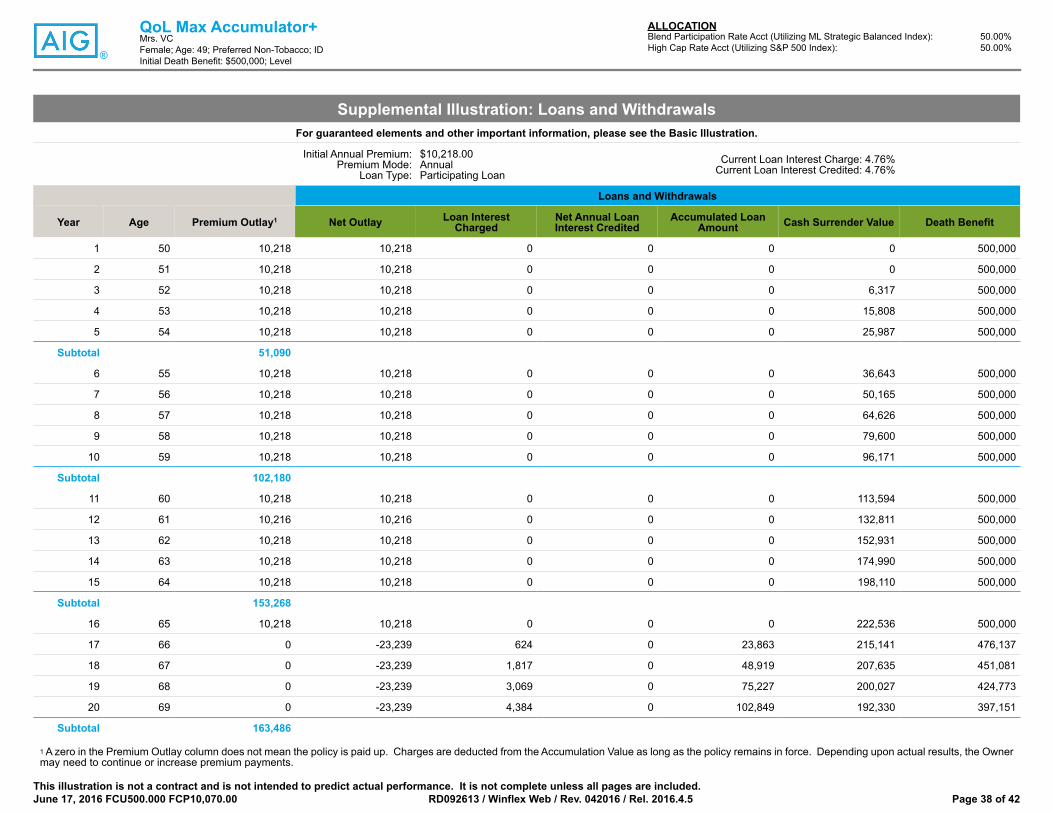

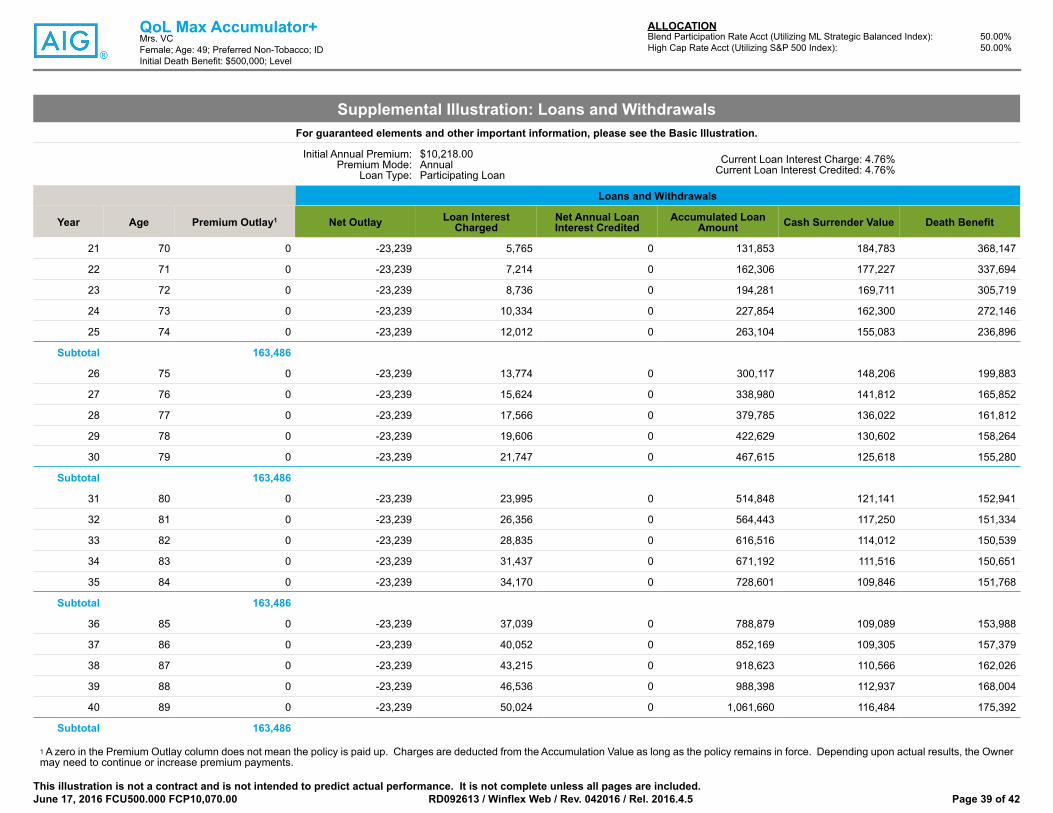

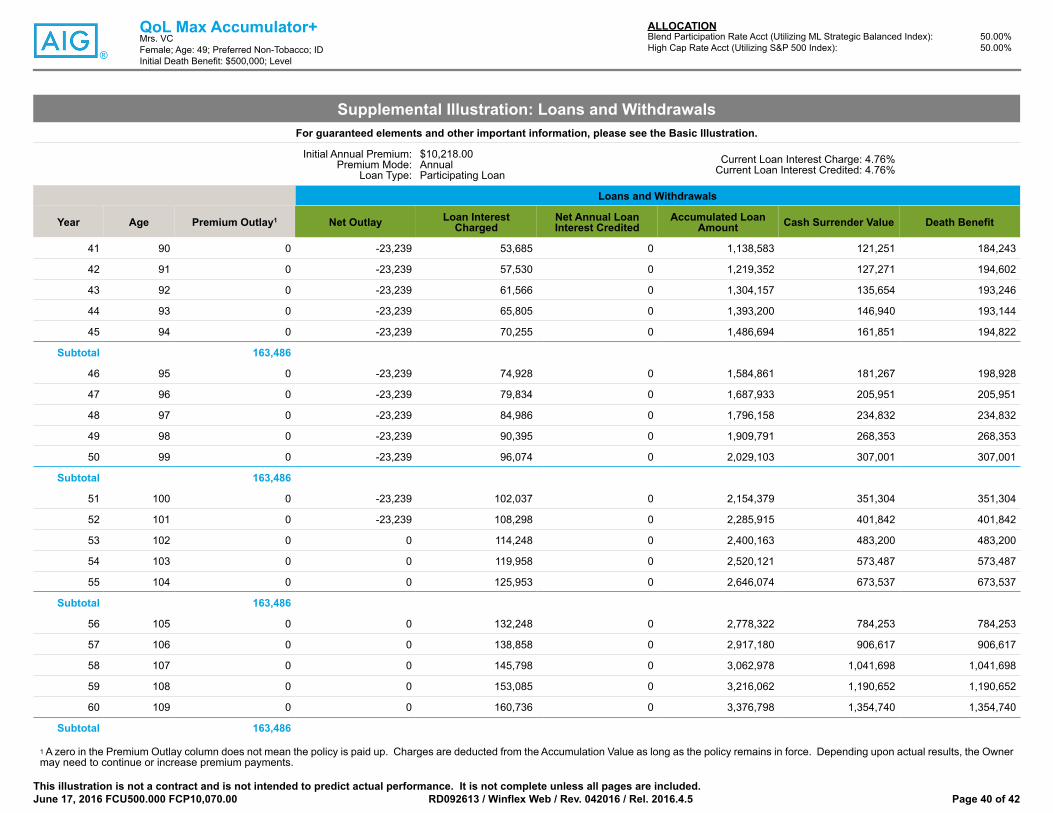

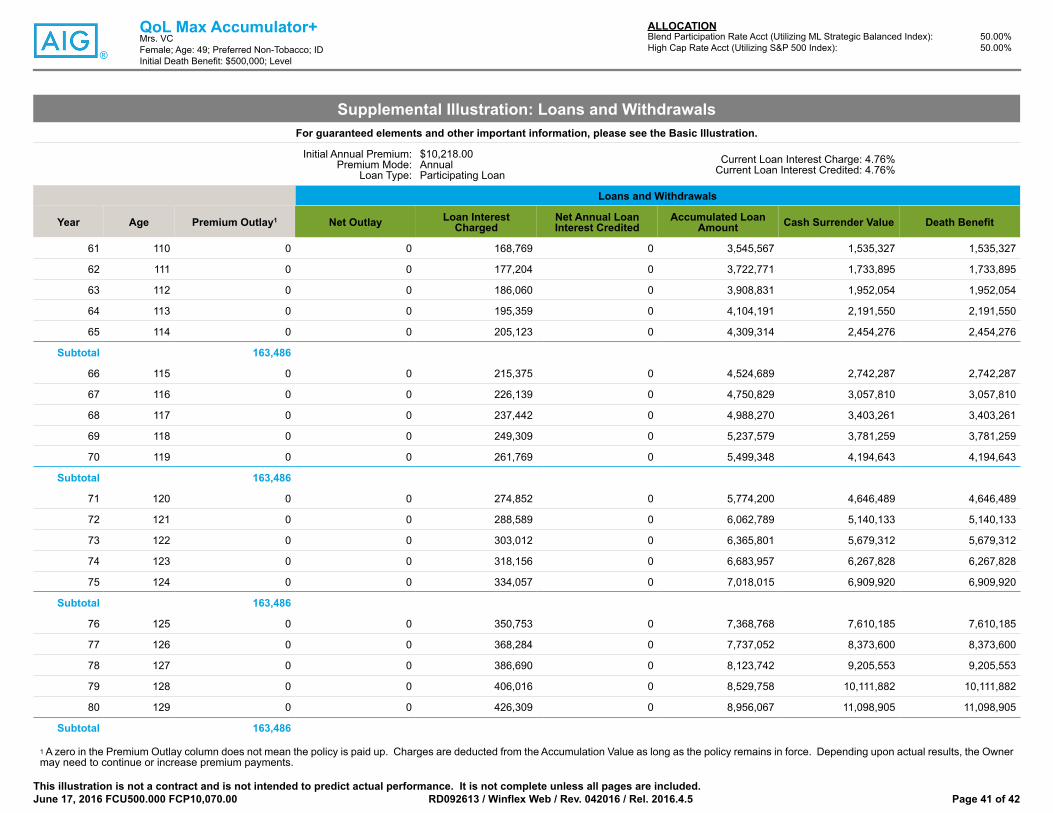

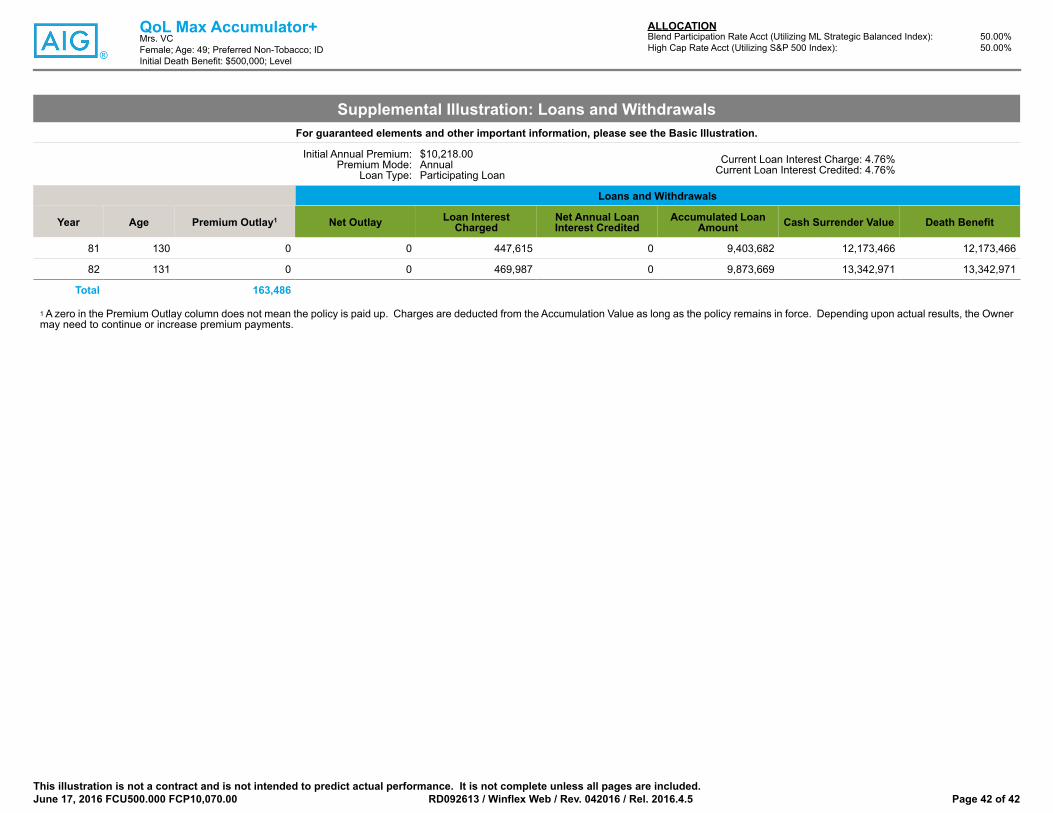

Supplemental Illustration: Non-Guaranteed Policy ValuesFor guaranteed elements and other important information, please see the Basic Illustration.

Maximum Non-Guaranteed Crediting Rate

Initial Annual Premium:Premium Mode:

$10,218.00Annual

Blend Participation Rate Account (Utilizing MLSB Index): 7.38%High Cap Rate Account (Utilizing S&P 500 Index): 7.47%

Current Account Value Enhancement1 0.65%Current Account Value Enhancement1 0.25%

For Current Non-Guaranteed Hypothetical Rates, see Illustration Assumptions for Non-Guaranteed Interest Rates section.

Year Age Premium Outlay2 Net Outlay Accumulation Value Cash SurrenderValue Death Benefit Cash Surrender

Value IRR Death Benefit IRR

1 50 10,218 10,218 7,207 0 500,000 0.00% 4,793.33%

2 51 10,218 10,218 14,965 0 500,000 0.00% 551.31%

3 52 10,218 10,218 23,317 6,317 500,000 0.00% 227.01%

4 53 10,218 10,218 32,308 15,808 500,000 0.00% 131.69%

5 54 10,218 10,218 41,987 25,987 500,000 0.00% 88.85%

Subtotal 51,090 51,090

6 55 10,218 10,218 52,643 36,643 500,000 0.00% 65.17%

7 56 10,218 10,218 64,165 50,165 500,000 0.00% 50.38%

8 57 10,218 10,218 76,626 64,626 500,000 0.00% 40.37%

9 58 10,218 10,218 90,100 79,600 500,000 0.00% 33.20%

10 59 10,218 10,218 104,671 96,171 500,000 0.00% 27.84%

Subtotal 102,180 102,180

11 60 10,218 10,218 120,594 113,594 500,000 0.18% 23.70%

12 61 10,216 10,216 137,811 132,811 500,000 1.22% 20.42%

13 62 10,218 10,218 156,431 152,931 500,000 2.00% 17.77%

14 63 10,218 10,218 176,490 174,990 500,000 2.65% 15.59%

15 64 10,218 10,218 198,110 198,110 500,000 3.14% 13.77%

Subtotal 153,268 153,268

16 65 10,218 10,218 222,536 222,536 500,000 3.54% 12.22%

L 17 66 0 -23,239 239,004 215,141 476,137 3.92% 11.16%

L 18 67 0 -23,239 256,554 207,635 451,081 4.23% 10.29%

L 19 68 0 -23,239 275,254 200,027 424,773 4.48% 9.55%

L - Policy Loans; W - Policy Withdrawals1 Account Value Enhancement (AVE) begins after policy year 5. The AVE provides additional interest for the Cash Value. For additional details, see the policy.2 A zero in the Premium Outlay column does not mean the policy is paid up. Charges are deducted from the Accumulation Value as long as the policy remains in force. Depending upon actual results, the Ownermay need to continue or increase premium payments.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 6 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

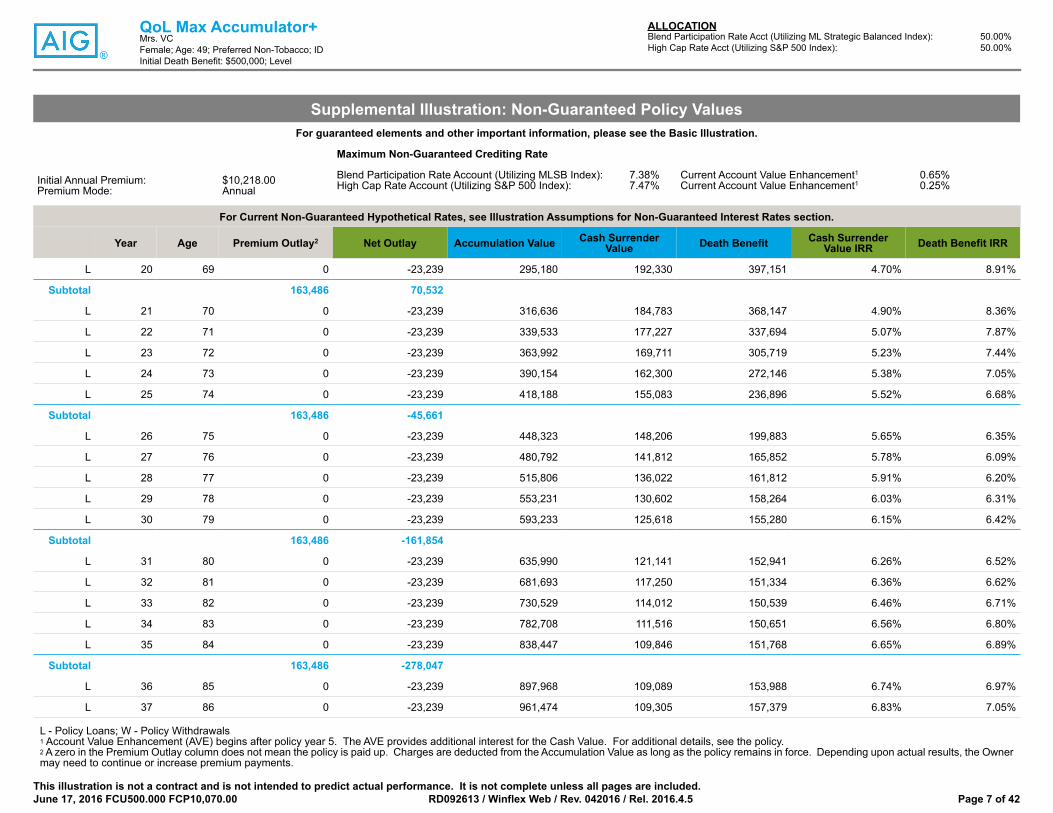

Supplemental Illustration: Non-Guaranteed Policy ValuesFor guaranteed elements and other important information, please see the Basic Illustration.

Maximum Non-Guaranteed Crediting Rate

Initial Annual Premium:Premium Mode:

$10,218.00Annual

Blend Participation Rate Account (Utilizing MLSB Index): 7.38%High Cap Rate Account (Utilizing S&P 500 Index): 7.47%

Current Account Value Enhancement1 0.65%Current Account Value Enhancement1 0.25%

For Current Non-Guaranteed Hypothetical Rates, see Illustration Assumptions for Non-Guaranteed Interest Rates section.

Year Age Premium Outlay2 Net Outlay Accumulation Value Cash SurrenderValue Death Benefit Cash Surrender

Value IRR Death Benefit IRR

L 20 69 0 -23,239 295,180 192,330 397,151 4.70% 8.91%

Subtotal 163,486 70,532

L 21 70 0 -23,239 316,636 184,783 368,147 4.90% 8.36%

L 22 71 0 -23,239 339,533 177,227 337,694 5.07% 7.87%

L 23 72 0 -23,239 363,992 169,711 305,719 5.23% 7.44%

L 24 73 0 -23,239 390,154 162,300 272,146 5.38% 7.05%

L 25 74 0 -23,239 418,188 155,083 236,896 5.52% 6.68%

Subtotal 163,486 -45,661

L 26 75 0 -23,239 448,323 148,206 199,883 5.65% 6.35%

L 27 76 0 -23,239 480,792 141,812 165,852 5.78% 6.09%

L 28 77 0 -23,239 515,806 136,022 161,812 5.91% 6.20%

L 29 78 0 -23,239 553,231 130,602 158,264 6.03% 6.31%

L 30 79 0 -23,239 593,233 125,618 155,280 6.15% 6.42%

Subtotal 163,486 -161,854

L 31 80 0 -23,239 635,990 121,141 152,941 6.26% 6.52%

L 32 81 0 -23,239 681,693 117,250 151,334 6.36% 6.62%

L 33 82 0 -23,239 730,529 114,012 150,539 6.46% 6.71%

L 34 83 0 -23,239 782,708 111,516 150,651 6.56% 6.80%

L 35 84 0 -23,239 838,447 109,846 151,768 6.65% 6.89%

Subtotal 163,486 -278,047

L 36 85 0 -23,239 897,968 109,089 153,988 6.74% 6.97%

L 37 86 0 -23,239 961,474 109,305 157,379 6.83% 7.05%

L - Policy Loans; W - Policy Withdrawals1 Account Value Enhancement (AVE) begins after policy year 5. The AVE provides additional interest for the Cash Value. For additional details, see the policy.2 A zero in the Premium Outlay column does not mean the policy is paid up. Charges are deducted from the Accumulation Value as long as the policy remains in force. Depending upon actual results, the Ownermay need to continue or increase premium payments.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 7 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

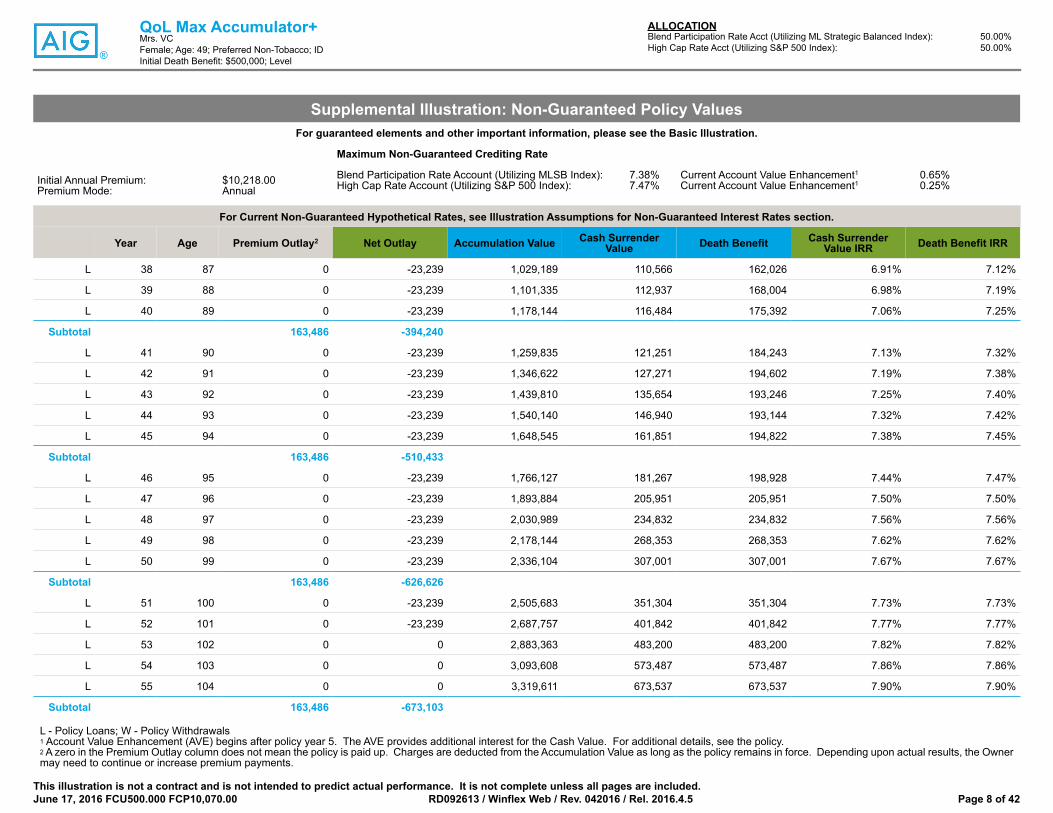

Supplemental Illustration: Non-Guaranteed Policy ValuesFor guaranteed elements and other important information, please see the Basic Illustration.

Maximum Non-Guaranteed Crediting Rate

Initial Annual Premium:Premium Mode:

$10,218.00Annual

Blend Participation Rate Account (Utilizing MLSB Index): 7.38%High Cap Rate Account (Utilizing S&P 500 Index): 7.47%

Current Account Value Enhancement1 0.65%Current Account Value Enhancement1 0.25%

For Current Non-Guaranteed Hypothetical Rates, see Illustration Assumptions for Non-Guaranteed Interest Rates section.

Year Age Premium Outlay2 Net Outlay Accumulation Value Cash SurrenderValue Death Benefit Cash Surrender

Value IRR Death Benefit IRR

L 38 87 0 -23,239 1,029,189 110,566 162,026 6.91% 7.12%

L 39 88 0 -23,239 1,101,335 112,937 168,004 6.98% 7.19%

L 40 89 0 -23,239 1,178,144 116,484 175,392 7.06% 7.25%

Subtotal 163,486 -394,240

L 41 90 0 -23,239 1,259,835 121,251 184,243 7.13% 7.32%

L 42 91 0 -23,239 1,346,622 127,271 194,602 7.19% 7.38%

L 43 92 0 -23,239 1,439,810 135,654 193,246 7.25% 7.40%

L 44 93 0 -23,239 1,540,140 146,940 193,144 7.32% 7.42%

L 45 94 0 -23,239 1,648,545 161,851 194,822 7.38% 7.45%

Subtotal 163,486 -510,433

L 46 95 0 -23,239 1,766,127 181,267 198,928 7.44% 7.47%

L 47 96 0 -23,239 1,893,884 205,951 205,951 7.50% 7.50%

L 48 97 0 -23,239 2,030,989 234,832 234,832 7.56% 7.56%

L 49 98 0 -23,239 2,178,144 268,353 268,353 7.62% 7.62%

L 50 99 0 -23,239 2,336,104 307,001 307,001 7.67% 7.67%

Subtotal 163,486 -626,626

L 51 100 0 -23,239 2,505,683 351,304 351,304 7.73% 7.73%

L 52 101 0 -23,239 2,687,757 401,842 401,842 7.77% 7.77%

L 53 102 0 0 2,883,363 483,200 483,200 7.82% 7.82%

L 54 103 0 0 3,093,608 573,487 573,487 7.86% 7.86%

L 55 104 0 0 3,319,611 673,537 673,537 7.90% 7.90%

Subtotal 163,486 -673,103

L - Policy Loans; W - Policy Withdrawals1 Account Value Enhancement (AVE) begins after policy year 5. The AVE provides additional interest for the Cash Value. For additional details, see the policy.2 A zero in the Premium Outlay column does not mean the policy is paid up. Charges are deducted from the Accumulation Value as long as the policy remains in force. Depending upon actual results, the Ownermay need to continue or increase premium payments.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 8 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

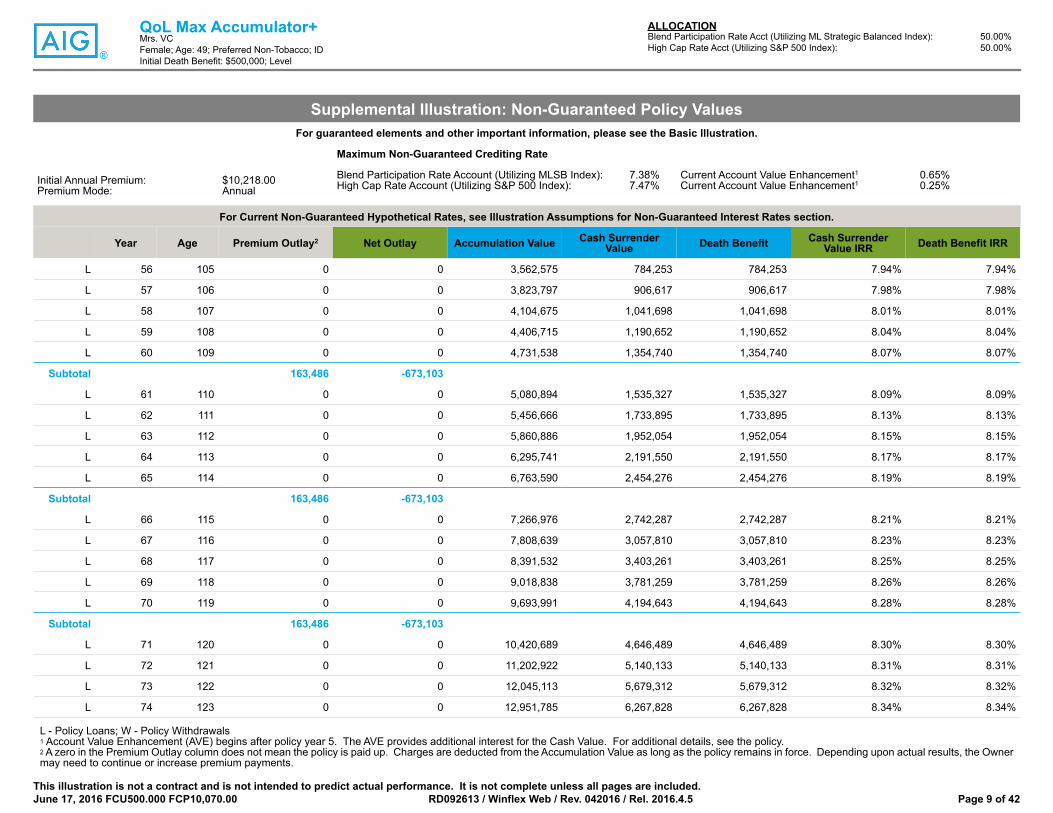

Supplemental Illustration: Non-Guaranteed Policy ValuesFor guaranteed elements and other important information, please see the Basic Illustration.

Maximum Non-Guaranteed Crediting Rate

Initial Annual Premium:Premium Mode:

$10,218.00Annual

Blend Participation Rate Account (Utilizing MLSB Index): 7.38%High Cap Rate Account (Utilizing S&P 500 Index): 7.47%

Current Account Value Enhancement1 0.65%Current Account Value Enhancement1 0.25%

For Current Non-Guaranteed Hypothetical Rates, see Illustration Assumptions for Non-Guaranteed Interest Rates section.

Year Age Premium Outlay2 Net Outlay Accumulation Value Cash SurrenderValue Death Benefit Cash Surrender

Value IRR Death Benefit IRR

L 56 105 0 0 3,562,575 784,253 784,253 7.94% 7.94%

L 57 106 0 0 3,823,797 906,617 906,617 7.98% 7.98%

L 58 107 0 0 4,104,675 1,041,698 1,041,698 8.01% 8.01%

L 59 108 0 0 4,406,715 1,190,652 1,190,652 8.04% 8.04%

L 60 109 0 0 4,731,538 1,354,740 1,354,740 8.07% 8.07%

Subtotal 163,486 -673,103

L 61 110 0 0 5,080,894 1,535,327 1,535,327 8.09% 8.09%

L 62 111 0 0 5,456,666 1,733,895 1,733,895 8.13% 8.13%

L 63 112 0 0 5,860,886 1,952,054 1,952,054 8.15% 8.15%

L 64 113 0 0 6,295,741 2,191,550 2,191,550 8.17% 8.17%

L 65 114 0 0 6,763,590 2,454,276 2,454,276 8.19% 8.19%

Subtotal 163,486 -673,103

L 66 115 0 0 7,266,976 2,742,287 2,742,287 8.21% 8.21%

L 67 116 0 0 7,808,639 3,057,810 3,057,810 8.23% 8.23%

L 68 117 0 0 8,391,532 3,403,261 3,403,261 8.25% 8.25%

L 69 118 0 0 9,018,838 3,781,259 3,781,259 8.26% 8.26%

L 70 119 0 0 9,693,991 4,194,643 4,194,643 8.28% 8.28%

Subtotal 163,486 -673,103

L 71 120 0 0 10,420,689 4,646,489 4,646,489 8.30% 8.30%

L 72 121 0 0 11,202,922 5,140,133 5,140,133 8.31% 8.31%

L 73 122 0 0 12,045,113 5,679,312 5,679,312 8.32% 8.32%

L 74 123 0 0 12,951,785 6,267,828 6,267,828 8.34% 8.34%

L - Policy Loans; W - Policy Withdrawals1 Account Value Enhancement (AVE) begins after policy year 5. The AVE provides additional interest for the Cash Value. For additional details, see the policy.2 A zero in the Premium Outlay column does not mean the policy is paid up. Charges are deducted from the Accumulation Value as long as the policy remains in force. Depending upon actual results, the Ownermay need to continue or increase premium payments.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 9 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

Supplemental Illustration: Non-Guaranteed Policy ValuesFor guaranteed elements and other important information, please see the Basic Illustration.

Maximum Non-Guaranteed Crediting Rate

Initial Annual Premium:Premium Mode:

$10,218.00Annual

Blend Participation Rate Account (Utilizing MLSB Index): 7.38%High Cap Rate Account (Utilizing S&P 500 Index): 7.47%

Current Account Value Enhancement1 0.65%Current Account Value Enhancement1 0.25%

For Current Non-Guaranteed Hypothetical Rates, see Illustration Assumptions for Non-Guaranteed Interest Rates section.

Year Age Premium Outlay2 Net Outlay Accumulation Value Cash SurrenderValue Death Benefit Cash Surrender

Value IRR Death Benefit IRR

L 75 124 0 0 13,927,935 6,909,920 6,909,920 8.34% 8.34%

Subtotal 163,486 -673,103

L 76 125 0 0 14,978,953 7,610,185 7,610,185 8.36% 8.36%

L 77 126 0 0 16,110,651 8,373,600 8,373,600 8.37% 8.37%

L 78 127 0 0 17,329,295 9,205,553 9,205,553 8.38% 8.38%

L 79 128 0 0 18,641,640 10,111,882 10,111,882 8.39% 8.39%

L 80 129 0 0 20,054,972 11,098,905 11,098,905 8.39% 8.39%

Subtotal 163,486 -673,103

L 81 130 0 0 21,577,149 12,173,466 12,173,466 8.41% 8.41%

L 82 131 0 0 23,216,640 13,342,971 13,342,971 8.41% 8.41%

Total 163,486 -673,103

L - Policy Loans; W - Policy Withdrawals1 Account Value Enhancement (AVE) begins after policy year 5. The AVE provides additional interest for the Cash Value. For additional details, see the policy.2 A zero in the Premium Outlay column does not mean the policy is paid up. Charges are deducted from the Accumulation Value as long as the policy remains in force. Depending upon actual results, the Ownermay need to continue or increase premium payments.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 10 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

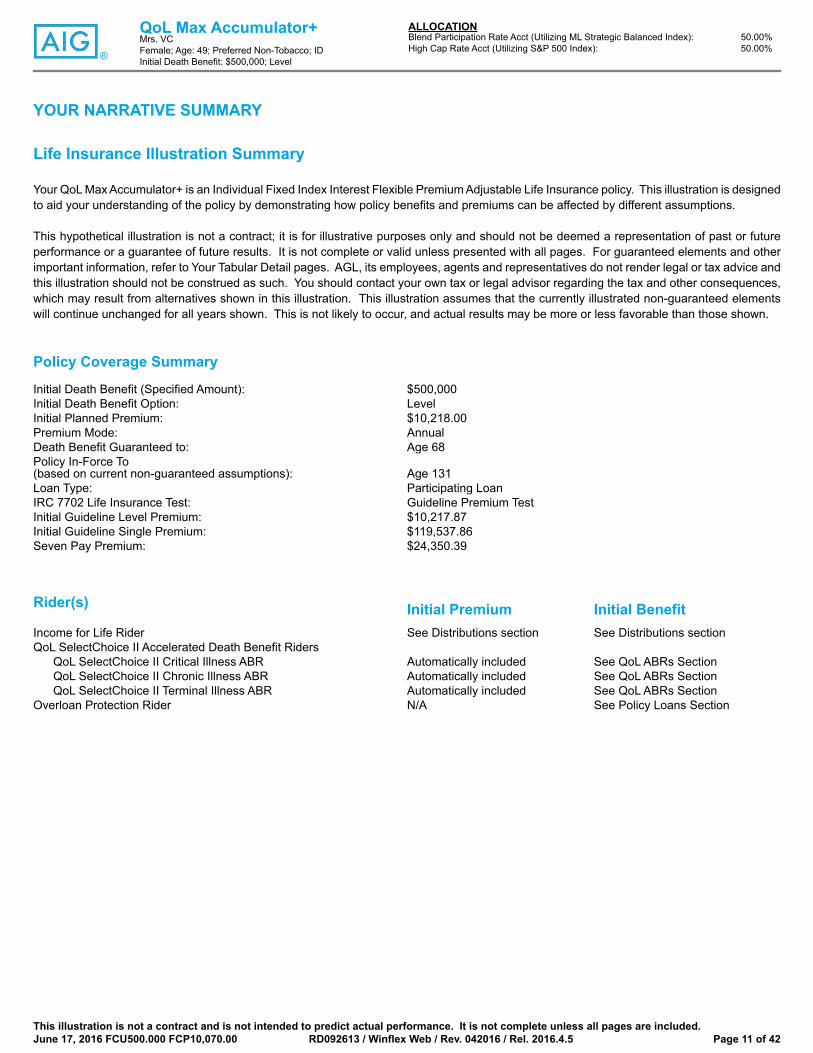

YOUR NARRATIVE SUMMARY

Life Insurance Illustration Summary

Your QoL Max Accumulator+ is an Individual Fixed Index Interest Flexible Premium Adjustable Life Insurance policy. This illustration is designedto aid your understanding of the policy by demonstrating how policy benefits and premiums can be affected by different assumptions.

This hypothetical illustration is not a contract; it is for illustrative purposes only and should not be deemed a representation of past or futureperformance or a guarantee of future results. It is not complete or valid unless presented with all pages. For guaranteed elements and otherimportant information, refer to Your Tabular Detail pages. AGL, its employees, agents and representatives do not render legal or tax advice andthis illustration should not be construed as such. You should contact your own tax or legal advisor regarding the tax and other consequences,which may result from alternatives shown in this illustration. This illustration assumes that the currently illustrated non-guaranteed elementswill continue unchanged for all years shown. This is not likely to occur, and actual results may be more or less favorable than those shown.

Policy Coverage Summary

Initial Death Benefit (Specified Amount): $500,000Initial Death Benefit Option: LevelInitial Planned Premium: $10,218.00Premium Mode: AnnualDeath Benefit Guaranteed to: Age 68Policy In-Force To(based on current non-guaranteed assumptions): Age 131Loan Type: Participating LoanIRC 7702 Life Insurance Test: Guideline Premium TestInitial Guideline Level Premium: $10,217.87Initial Guideline Single Premium: $119,537.86Seven Pay Premium: $24,350.39

Rider(s) Initial Premium Initial BenefitIncome for Life Rider See Distributions section See Distributions sectionQoL SelectChoice II Accelerated Death Benefit Riders

QoL SelectChoice II Critical Illness ABR Automatically included See QoL ABRs SectionQoL SelectChoice II Chronic Illness ABR Automatically included See QoL ABRs SectionQoL SelectChoice II Terminal Illness ABR Automatically included See QoL ABRs Section

Overloan Protection Rider N/A See Policy Loans Section

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 11 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

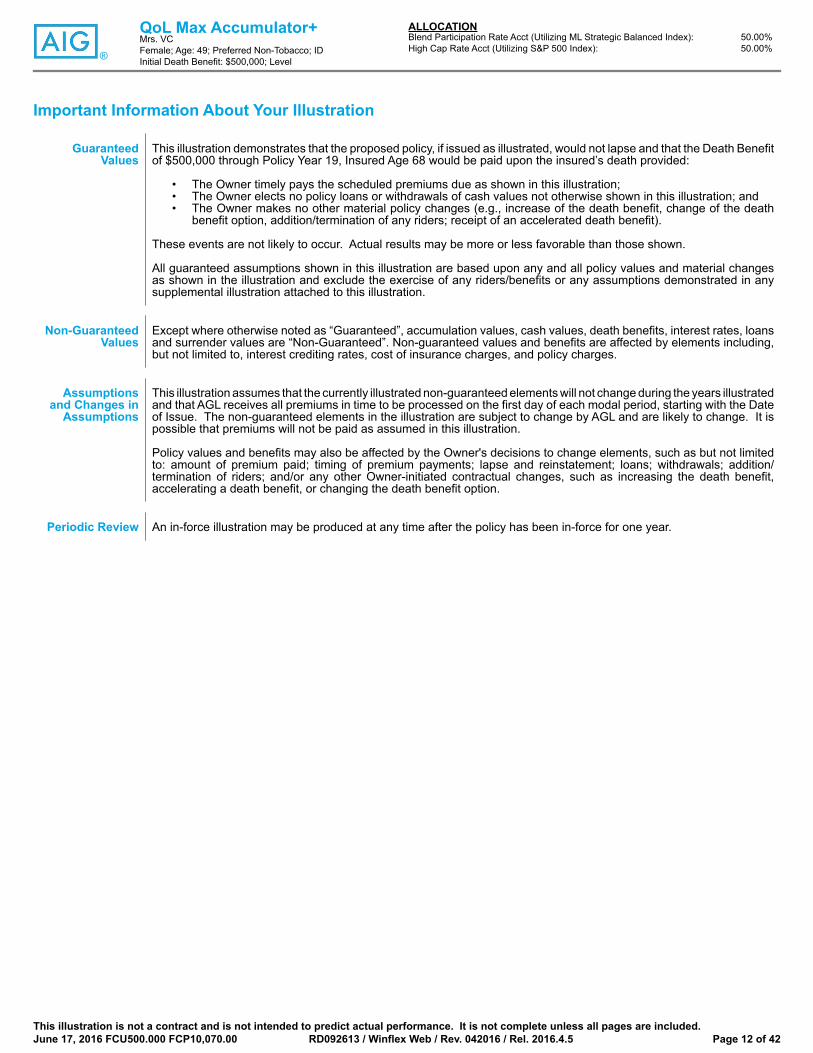

Important Information About Your Illustration

GuaranteedValues

This illustration demonstrates that the proposed policy, if issued as illustrated, would not lapse and that the Death Benefitof $500,000 through Policy Year 19, Insured Age 68 would be paid upon the insured’s death provided:

• The Owner timely pays the scheduled premiums due as shown in this illustration;• The Owner elects no policy loans or withdrawals of cash values not otherwise shown in this illustration; and• The Owner makes no other material policy changes (e.g., increase of the death benefit, change of the death

benefit option, addition/termination of any riders; receipt of an accelerated death benefit).

These events are not likely to occur. Actual results may be more or less favorable than those shown.

All guaranteed assumptions shown in this illustration are based upon any and all policy values and material changesas shown in the illustration and exclude the exercise of any riders/benefits or any assumptions demonstrated in anysupplemental illustration attached to this illustration.

Non-GuaranteedValues

Except where otherwise noted as “Guaranteed”, accumulation values, cash values, death benefits, interest rates, loansand surrender values are “Non-Guaranteed”. Non-guaranteed values and benefits are affected by elements including,but not limited to, interest crediting rates, cost of insurance charges, and policy charges.

Assumptionsand Changes in

Assumptions

This illustration assumes that the currently illustrated non-guaranteed elements will not change during the years illustratedand that AGL receives all premiums in time to be processed on the first day of each modal period, starting with the Dateof Issue. The non-guaranteed elements in the illustration are subject to change by AGL and are likely to change. It ispossible that premiums will not be paid as assumed in this illustration.

Policy values and benefits may also be affected by the Owner's decisions to change elements, such as but not limitedto: amount of premium paid; timing of premium payments; lapse and reinstatement; loans; withdrawals; addition/termination of riders; and/or any other Owner-initiated contractual changes, such as increasing the death benefit,accelerating a death benefit, or changing the death benefit option.

Periodic Review An in-force illustration may be produced at any time after the policy has been in-force for one year.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 12 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

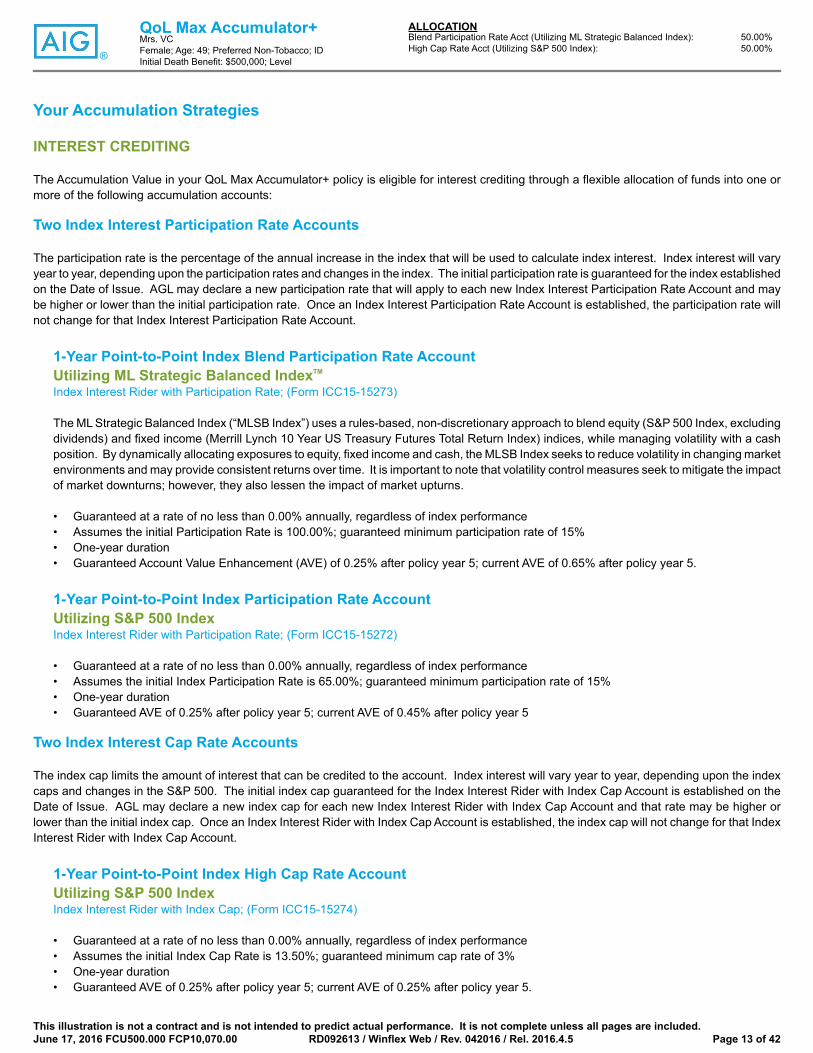

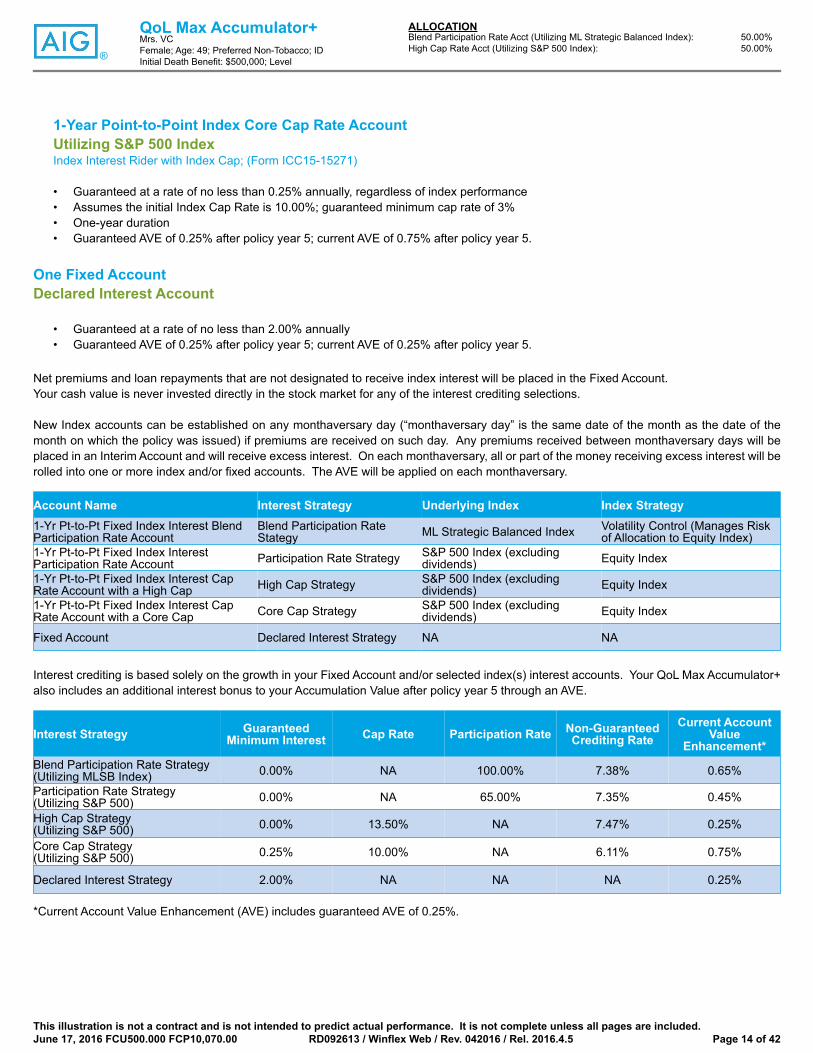

Your Accumulation Strategies

INTEREST CREDITING

The Accumulation Value in your QoL Max Accumulator+ policy is eligible for interest crediting through a flexible allocation of funds into one ormore of the following accumulation accounts:

Two Index Interest Participation Rate Accounts

The participation rate is the percentage of the annual increase in the index that will be used to calculate index interest. Index interest will varyyear to year, depending upon the participation rates and changes in the index. The initial participation rate is guaranteed for the index establishedon the Date of Issue. AGL may declare a new participation rate that will apply to each new Index Interest Participation Rate Account and maybe higher or lower than the initial participation rate. Once an Index Interest Participation Rate Account is established, the participation rate willnot change for that Index Interest Participation Rate Account.

1-Year Point-to-Point Index Blend Participation Rate Account Utilizing ML Strategic Balanced IndexTM

Index Interest Rider with Participation Rate; (Form ICC15-15273)

The ML Strategic Balanced Index (“MLSB Index”) uses a rules-based, non-discretionary approach to blend equity (S&P 500 Index, excludingdividends) and fixed income (Merrill Lynch 10 Year US Treasury Futures Total Return Index) indices, while managing volatility with a cashposition. By dynamically allocating exposures to equity, fixed income and cash, the MLSB Index seeks to reduce volatility in changing marketenvironments and may provide consistent returns over time. It is important to note that volatility control measures seek to mitigate the impactof market downturns; however, they also lessen the impact of market upturns.

• Guaranteed at a rate of no less than 0.00% annually, regardless of index performance• Assumes the initial Participation Rate is 100.00%; guaranteed minimum participation rate of 15%• One-year duration• Guaranteed Account Value Enhancement (AVE) of 0.25% after policy year 5; current AVE of 0.65% after policy year 5.

1-Year Point-to-Point Index Participation Rate Account Utilizing S&P 500 Index Index Interest Rider with Participation Rate; (Form ICC15-15272)

• Guaranteed at a rate of no less than 0.00% annually, regardless of index performance• Assumes the initial Index Participation Rate is 65.00%; guaranteed minimum participation rate of 15%• One-year duration• Guaranteed AVE of 0.25% after policy year 5; current AVE of 0.45% after policy year 5

Two Index Interest Cap Rate Accounts

The index cap limits the amount of interest that can be credited to the account. Index interest will vary year to year, depending upon the indexcaps and changes in the S&P 500. The initial index cap guaranteed for the Index Interest Rider with Index Cap Account is established on theDate of Issue. AGL may declare a new index cap for each new Index Interest Rider with Index Cap Account and that rate may be higher orlower than the initial index cap. Once an Index Interest Rider with Index Cap Account is established, the index cap will not change for that IndexInterest Rider with Index Cap Account.

1-Year Point-to-Point Index High Cap Rate Account Utilizing S&P 500 Index Index Interest Rider with Index Cap; (Form ICC15-15274)

• Guaranteed at a rate of no less than 0.00% annually, regardless of index performance• Assumes the initial Index Cap Rate is 13.50%; guaranteed minimum cap rate of 3%• One-year duration• Guaranteed AVE of 0.25% after policy year 5; current AVE of 0.25% after policy year 5.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 13 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

1-Year Point-to-Point Index Core Cap Rate Account Utilizing S&P 500 Index Index Interest Rider with Index Cap; (Form ICC15-15271)

• Guaranteed at a rate of no less than 0.25% annually, regardless of index performance• Assumes the initial Index Cap Rate is 10.00%; guaranteed minimum cap rate of 3%• One-year duration• Guaranteed AVE of 0.25% after policy year 5; current AVE of 0.75% after policy year 5.

One Fixed Account Declared Interest Account

• Guaranteed at a rate of no less than 2.00% annually• Guaranteed AVE of 0.25% after policy year 5; current AVE of 0.25% after policy year 5.

Net premiums and loan repayments that are not designated to receive index interest will be placed in the Fixed Account.Your cash value is never invested directly in the stock market for any of the interest crediting selections.

New Index accounts can be established on any monthaversary day (“monthaversary day” is the same date of the month as the date of themonth on which the policy was issued) if premiums are received on such day. Any premiums received between monthaversary days will beplaced in an Interim Account and will receive excess interest. On each monthaversary, all or part of the money receiving excess interest will berolled into one or more index and/or fixed accounts. The AVE will be applied on each monthaversary.

Account Name Interest Strategy Underlying Index Index Strategy

1-Yr Pt-to-Pt Fixed Index Interest BlendParticipation Rate Account

Blend Participation RateStategy ML Strategic Balanced Index Volatility Control (Manages Risk

of Allocation to Equity Index)1-Yr Pt-to-Pt Fixed Index InterestParticipation Rate Account Participation Rate Strategy S&P 500 Index (excluding

dividends) Equity Index

1-Yr Pt-to-Pt Fixed Index Interest CapRate Account with a High Cap High Cap Strategy S&P 500 Index (excluding

dividends) Equity Index

1-Yr Pt-to-Pt Fixed Index Interest CapRate Account with a Core Cap Core Cap Strategy S&P 500 Index (excluding

dividends) Equity Index

Fixed Account Declared Interest Strategy NA NA

Interest crediting is based solely on the growth in your Fixed Account and/or selected index(s) interest accounts. Your QoL Max Accumulator+also includes an additional interest bonus to your Accumulation Value after policy year 5 through an AVE.

Interest Strategy GuaranteedMinimum Interest Cap Rate Participation Rate Non-Guaranteed

Crediting RateCurrent Account

ValueEnhancement*

Blend Participation Rate Strategy(Utilizing MLSB Index) 0.00% NA 100.00% 7.38% 0.65%

Participation Rate Strategy(Utilizing S&P 500) 0.00% NA 65.00% 7.35% 0.45%

High Cap Strategy(Utilizing S&P 500) 0.00% 13.50% NA 7.47% 0.25%

Core Cap Strategy(Utilizing S&P 500) 0.25% 10.00% NA 6.11% 0.75%

Declared Interest Strategy 2.00% NA NA NA 0.25%

*Current Account Value Enhancement (AVE) includes guaranteed AVE of 0.25%.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 14 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

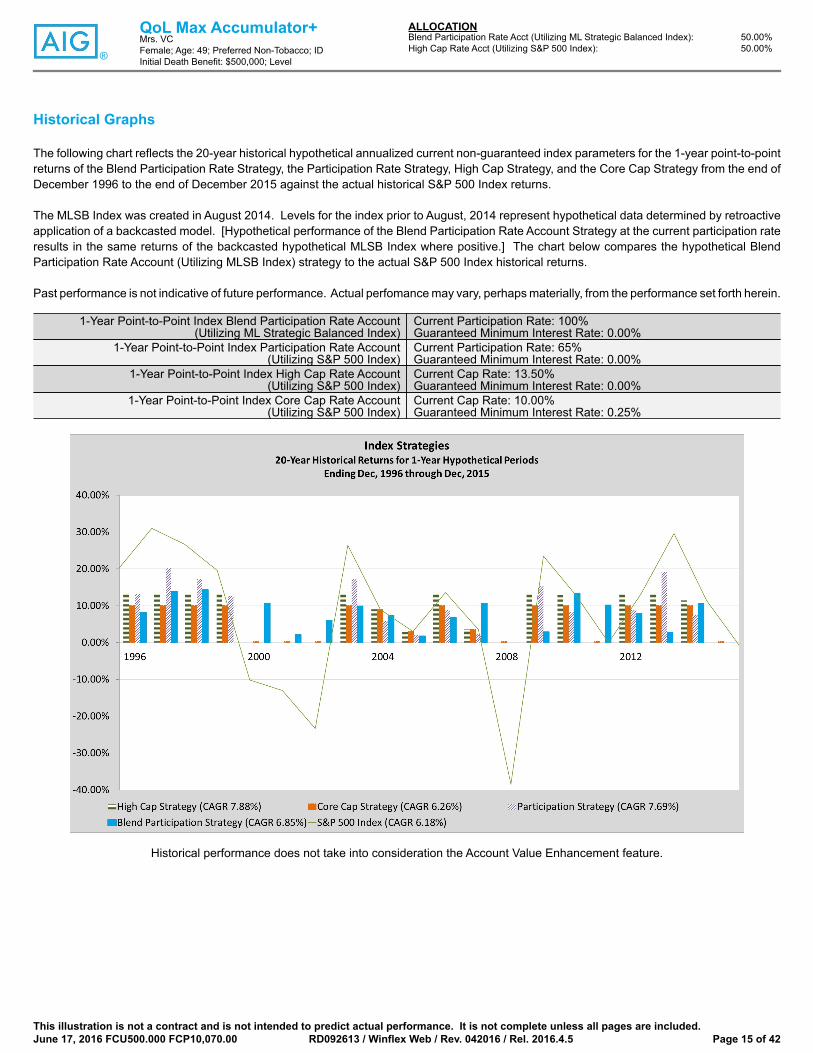

Historical Graphs

The following chart reflects the 20-year historical hypothetical annualized current non-guaranteed index parameters for the 1-year point-to-pointreturns of the Blend Participation Rate Strategy, the Participation Rate Strategy, High Cap Strategy, and the Core Cap Strategy from the end ofDecember 1996 to the end of December 2015 against the actual historical S&P 500 Index returns.

The MLSB Index was created in August 2014. Levels for the index prior to August, 2014 represent hypothetical data determined by retroactiveapplication of a backcasted model. [Hypothetical performance of the Blend Participation Rate Account Strategy at the current participation rateresults in the same returns of the backcasted hypothetical MLSB Index where positive.] The chart below compares the hypothetical BlendParticipation Rate Account (Utilizing MLSB Index) strategy to the actual S&P 500 Index historical returns.

Past performance is not indicative of future performance. Actual perfomance may vary, perhaps materially, from the performance set forth herein.

1-Year Point-to-Point Index Blend Participation Rate Account (Utilizing ML Strategic Balanced Index)

Current Participation Rate: 100% Guaranteed Minimum Interest Rate: 0.00%

1-Year Point-to-Point Index Participation Rate Account (Utilizing S&P 500 Index)

Current Participation Rate: 65% Guaranteed Minimum Interest Rate: 0.00%

1-Year Point-to-Point Index High Cap Rate Account (Utilizing S&P 500 Index)

Current Cap Rate: 13.50% Guaranteed Minimum Interest Rate: 0.00%

1-Year Point-to-Point Index Core Cap Rate Account (Utilizing S&P 500 Index)

Current Cap Rate: 10.00% Guaranteed Minimum Interest Rate: 0.25%

Historical performance does not take into consideration the Account Value Enhancement feature.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 15 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

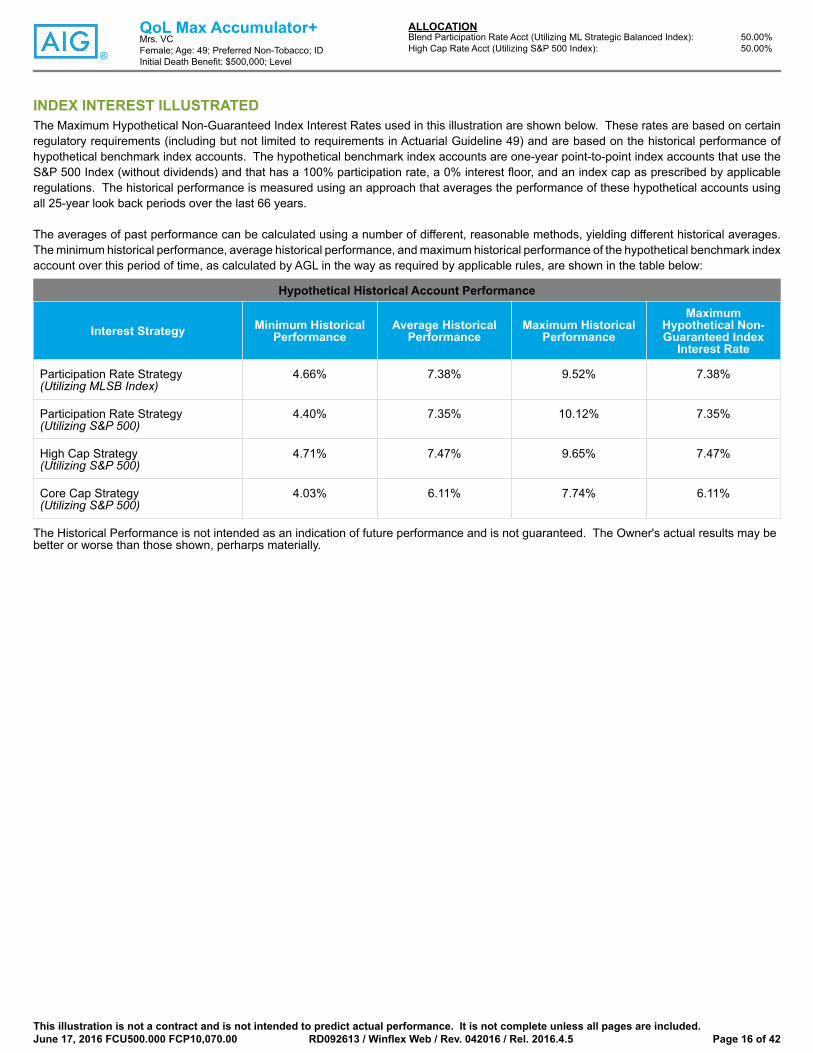

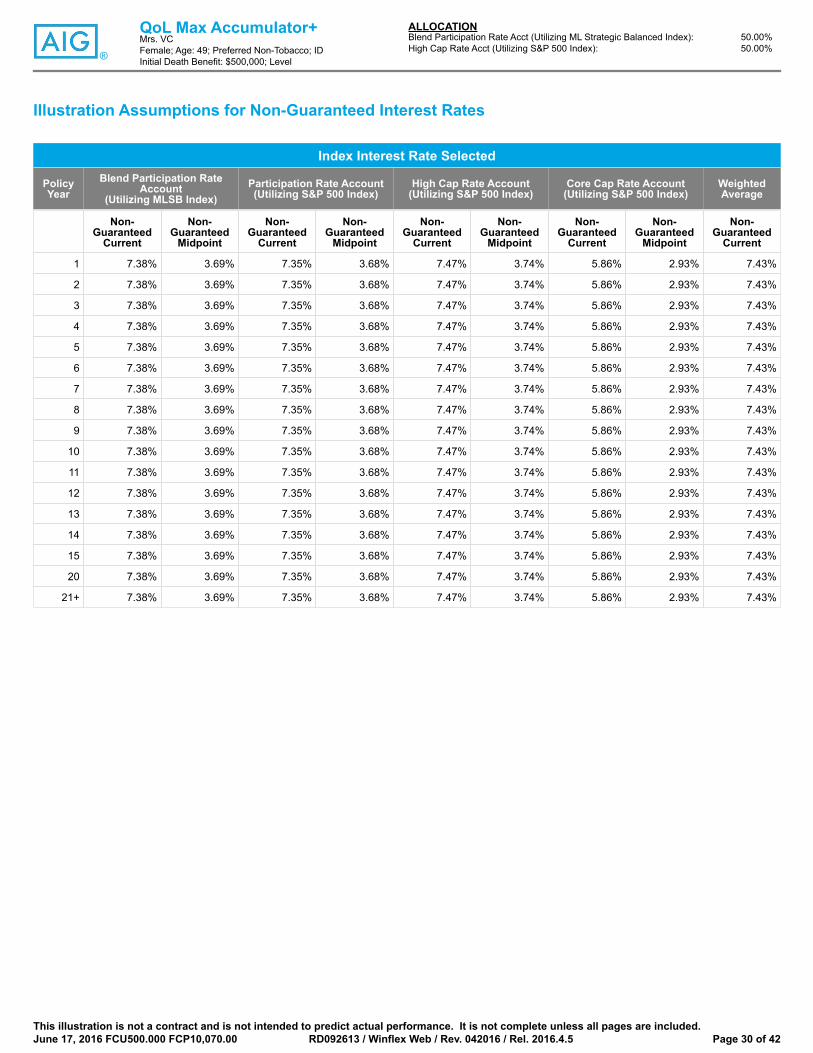

INDEX INTEREST ILLUSTRATEDThe Maximum Hypothetical Non-Guaranteed Index Interest Rates used in this illustration are shown below. These rates are based on certainregulatory requirements (including but not limited to requirements in Actuarial Guideline 49) and are based on the historical performance ofhypothetical benchmark index accounts. The hypothetical benchmark index accounts are one-year point-to-point index accounts that use theS&P 500 Index (without dividends) and that has a 100% participation rate, a 0% interest floor, and an index cap as prescribed by applicableregulations. The historical performance is measured using an approach that averages the performance of these hypothetical accounts usingall 25-year look back periods over the last 66 years.

The averages of past performance can be calculated using a number of different, reasonable methods, yielding different historical averages.The minimum historical performance, average historical performance, and maximum historical performance of the hypothetical benchmark indexaccount over this period of time, as calculated by AGL in the way as required by applicable rules, are shown in the table below:

Hypothetical Historical Account Performance

Interest Strategy Minimum HistoricalPerformance

Average HistoricalPerformance

Maximum HistoricalPerformance

MaximumHypothetical Non-Guaranteed Index

Interest Rate

Participation Rate Strategy(Utilizing MLSB Index)

4.66% 7.38% 9.52% 7.38%

Participation Rate Strategy(Utilizing S&P 500)

4.40% 7.35% 10.12% 7.35%

High Cap Strategy(Utilizing S&P 500)

4.71% 7.47% 9.65% 7.47%

Core Cap Strategy(Utilizing S&P 500)

4.03% 6.11% 7.74% 6.11%

The Historical Performance is not intended as an indication of future performance and is not guaranteed. The Owner's actual results may bebetter or worse than those shown, perharps materially.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 16 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

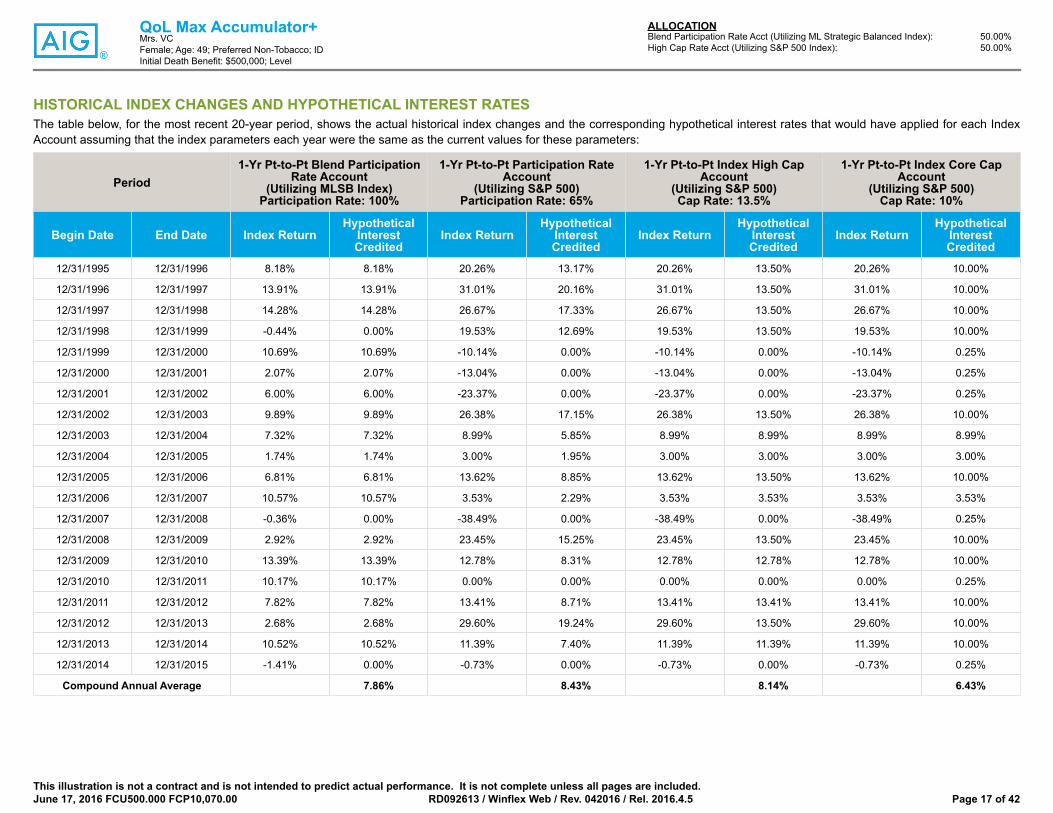

HISTORICAL INDEX CHANGES AND HYPOTHETICAL INTEREST RATESThe table below, for the most recent 20-year period, shows the actual historical index changes and the corresponding hypothetical interest rates that would have applied for each IndexAccount assuming that the index parameters each year were the same as the current values for these parameters:

Period1-Yr Pt-to-Pt Blend Participation

Rate Account(Utilizing MLSB Index)

Participation Rate: 100%

1-Yr Pt-to-Pt Participation RateAccount

(Utilizing S&P 500)Participation Rate: 65%

1-Yr Pt-to-Pt Index High CapAccount

(Utilizing S&P 500)Cap Rate: 13.5%

1-Yr Pt-to-Pt Index Core CapAccount

(Utilizing S&P 500)Cap Rate: 10%

Begin Date End Date Index ReturnHypothetical

InterestCredited

Index ReturnHypothetical

InterestCredited

Index ReturnHypothetical

InterestCredited

Index ReturnHypothetical

InterestCredited

12/31/1995 12/31/1996 8.18% 8.18% 20.26% 13.17% 20.26% 13.50% 20.26% 10.00%

12/31/1996 12/31/1997 13.91% 13.91% 31.01% 20.16% 31.01% 13.50% 31.01% 10.00%

12/31/1997 12/31/1998 14.28% 14.28% 26.67% 17.33% 26.67% 13.50% 26.67% 10.00%

12/31/1998 12/31/1999 -0.44% 0.00% 19.53% 12.69% 19.53% 13.50% 19.53% 10.00%

12/31/1999 12/31/2000 10.69% 10.69% -10.14% 0.00% -10.14% 0.00% -10.14% 0.25%

12/31/2000 12/31/2001 2.07% 2.07% -13.04% 0.00% -13.04% 0.00% -13.04% 0.25%

12/31/2001 12/31/2002 6.00% 6.00% -23.37% 0.00% -23.37% 0.00% -23.37% 0.25%

12/31/2002 12/31/2003 9.89% 9.89% 26.38% 17.15% 26.38% 13.50% 26.38% 10.00%

12/31/2003 12/31/2004 7.32% 7.32% 8.99% 5.85% 8.99% 8.99% 8.99% 8.99%

12/31/2004 12/31/2005 1.74% 1.74% 3.00% 1.95% 3.00% 3.00% 3.00% 3.00%

12/31/2005 12/31/2006 6.81% 6.81% 13.62% 8.85% 13.62% 13.50% 13.62% 10.00%

12/31/2006 12/31/2007 10.57% 10.57% 3.53% 2.29% 3.53% 3.53% 3.53% 3.53%

12/31/2007 12/31/2008 -0.36% 0.00% -38.49% 0.00% -38.49% 0.00% -38.49% 0.25%

12/31/2008 12/31/2009 2.92% 2.92% 23.45% 15.25% 23.45% 13.50% 23.45% 10.00%

12/31/2009 12/31/2010 13.39% 13.39% 12.78% 8.31% 12.78% 12.78% 12.78% 10.00%

12/31/2010 12/31/2011 10.17% 10.17% 0.00% 0.00% 0.00% 0.00% 0.00% 0.25%

12/31/2011 12/31/2012 7.82% 7.82% 13.41% 8.71% 13.41% 13.41% 13.41% 10.00%

12/31/2012 12/31/2013 2.68% 2.68% 29.60% 19.24% 29.60% 13.50% 29.60% 10.00%

12/31/2013 12/31/2014 10.52% 10.52% 11.39% 7.40% 11.39% 11.39% 11.39% 10.00%

12/31/2014 12/31/2015 -1.41% 0.00% -0.73% 0.00% -0.73% 0.00% -0.73% 0.25%

Compound Annual Average 7.86% 8.43% 8.14% 6.43%

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 17 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

Your Distribution Options

POLICY LOANS

Your QoL Max Accumulator+ policy offers two types of loans: Standard Loans and Participating Loans. Only one type of loan can be on a policyat any given time. You may switch between Standard and Participating loans a maximum of 3 times during the life of the policy. After the 10th policy anniversary, Preferred Loans are available. During the Allocation Restriction Period, Standard Loans are not available to switch toParticipating Loans.

Standard Loans

For a Standard Loan the amount of the loan will be deducted proportionately based on the Accumulation Value in each Index Account, theDeclared Interest Account, and the Interim Account and moved into the Fixed Account. The annual loan interest for Standard Loans is duein advance. The annual loan interest rate for Standard Loans is 1.96% (equal to an effective rate of 3.00% paid at the end of the policyyear). The interest credited to the loan amount is the 2.00% guaranteed interest in the Fixed Account. Standard Loan balances are noteligible for Account Value Enhancement.

Preferred Loans

After the 10th policy anniversary, your QoL Max Accumulator+ provides a preferred rate to your Standard Loan, or a Preferred Loan option.For a Preferred Loan, the amount of the loan will be deducted proportionately according to the Standard Loan rules. The annual loan interestfor Preferred Loans is due in advance. The annual loan interest rate for Preferred Loans will be no less than 1.96% and no more than 1.96%(equal of effective rates of not less than 2.00% and no more than 2.25% respectively, paid at the end of the policy year). The interest creditedto the loan amount is the 2.00% guaranteed interest in the Fixed Account. The Preferred Loan available is restricted to a policy year maximumof 10.00% of the Accumulation Value at the beginning of the policy year.

Participating Loans

For a Participating Loan, the amount of the loan will not be deducted and will remain in the existing interest accounts. The loan amount willcontinue to be eligible for Index Interest as if no loan had been taken from the policy. The annual loan interest for Participating Loans is duein advance. The annual loan interest rate for Participating Loans is declared monthly and will be no more than 7.40% (equal to an effectiverate of 8.00% paid at the end of the policy year). The initial annual loan interest rate due in advance is 4.76% (equal to an effective rate of5.00% paid at the end of the policy year).

There is a risk associated with Participating Loans because an Index Account's actual credited rate could be less than the ParticipatingAnnual Interest Rate. The use of Participating Loans could potentially result in policy lapse if poor index performance among the indices issustained. Participating Loans do not include participation in AGL's profits or surplus through receipt of dividends.

Under some circumstances policy loans and withdrawals are taxable. For advice concerning your individual circumstances, consult anattorney, tax advisor or accountant.

Overloan Protection Rider(Form 07620)

This optional rider guarantees your policy will not lapse due to a large outstanding loan by waiving future monthly deductions upon activationof the rider and by keeping the rider in-force when the loan amount exceeds the Account Value. The tax consequences of the Overloan ProtectionRider have not been determined by the IRS or the courts, and it is possible that the IRS could assert that the outstanding loan balance shouldbe treated as a taxable distribution when the Overloan Protection Rider is exercised. For advice concerning your individual circumstances,consult an attorney, tax advisor or accountant.

Under some circumstances policy loans and withdrawals are taxable. Refer to Loans and Withdrawals in the Key Terms and Definitions sectionand Specified Amount Reductions in the Tax and Compliance section.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 18 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

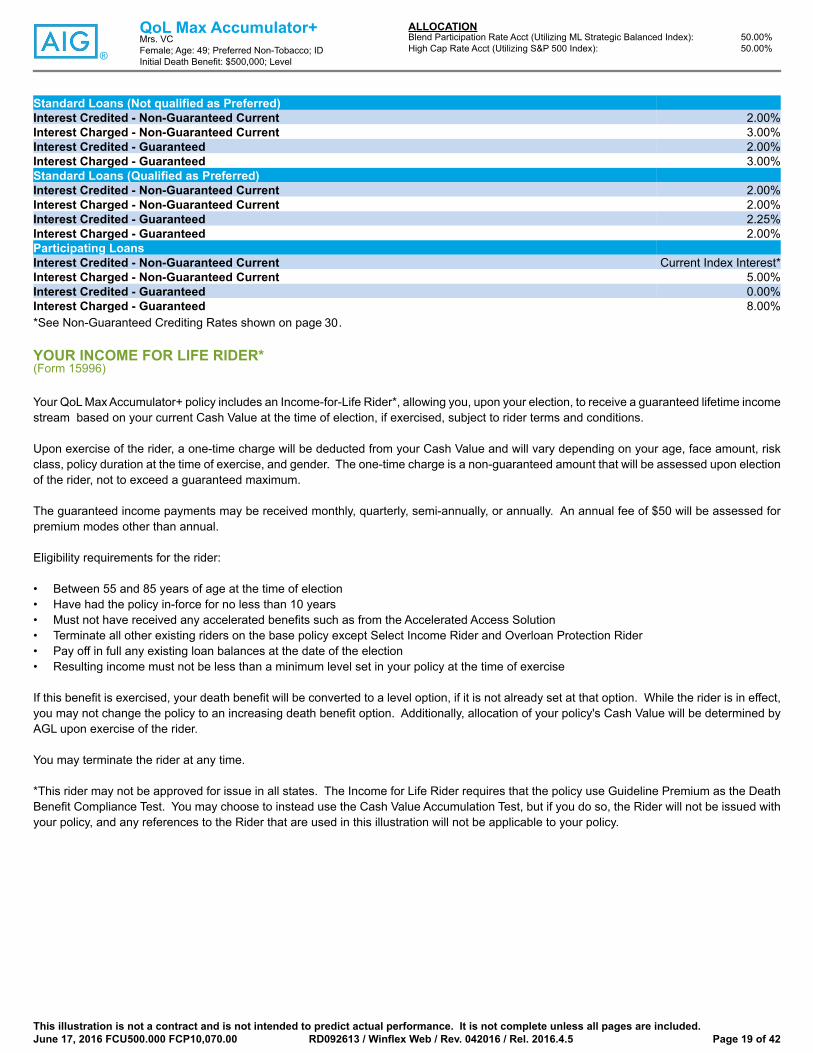

Standard Loans (Not qualified as Preferred)Interest Credited - Non-Guaranteed Current 2.00%Interest Charged - Non-Guaranteed Current 3.00%Interest Credited - Guaranteed 2.00%Interest Charged - Guaranteed 3.00%Standard Loans (Qualified as Preferred)Interest Credited - Non-Guaranteed Current 2.00%Interest Charged - Non-Guaranteed Current 2.00%Interest Credited - Guaranteed 2.25%Interest Charged - Guaranteed 2.00%Participating LoansInterest Credited - Non-Guaranteed Current Current Index Interest*Interest Charged - Non-Guaranteed Current 5.00%Interest Credited - Guaranteed 0.00%Interest Charged - Guaranteed 8.00%*See Non-Guaranteed Crediting Rates shown on page .

YOUR INCOME FOR LIFE RIDER*(Form 15996)

Your QoL Max Accumulator+ policy includes an Income-for-Life Rider*, allowing you, upon your election, to receive a guaranteed lifetime incomestream based on your current Cash Value at the time of election, if exercised, subject to rider terms and conditions.

Upon exercise of the rider, a one-time charge will be deducted from your Cash Value and will vary depending on your age, face amount, riskclass, policy duration at the time of exercise, and gender. The one-time charge is a non-guaranteed amount that will be assessed upon electionof the rider, not to exceed a guaranteed maximum.

The guaranteed income payments may be received monthly, quarterly, semi-annually, or annually. An annual fee of $50 will be assessed forpremium modes other than annual.

Eligibility requirements for the rider:

• Between 55 and 85 years of age at the time of election• Have had the policy in-force for no less than 10 years• Must not have received any accelerated benefits such as from the Accelerated Access Solution• Terminate all other existing riders on the base policy except Select Income Rider and Overloan Protection Rider• Pay off in full any existing loan balances at the date of the election• Resulting income must not be less than a minimum level set in your policy at the time of exercise

If this benefit is exercised, your death benefit will be converted to a level option, if it is not already set at that option. While the rider is in effect,you may not change the policy to an increasing death benefit option. Additionally, allocation of your policy's Cash Value will be determined byAGL upon exercise of the rider.

You may terminate the rider at any time.

*This rider may not be approved for issue in all states. The Income for Life Rider requires that the policy use Guideline Premium as the DeathBenefit Compliance Test. You may choose to instead use the Cash Value Accumulation Test, but if you do so, the Rider will not be issued withyour policy, and any references to the Rider that are used in this illustration will not be applicable to your policy.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 19 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

30

Your Riders

QoLSelectChoiceII

AcceleratedBenefit Riders

See Your QoL SelectChoice II Accelerated Benefits Summary section and Additional Information Regarding Your QoLSelectChoice II Accelerated Benefit Riders section.

Income for LifeRider

(Form 15996)

See Your Income for Life Rider section.

OverloanProtection Rider

(Form 07620)

See Overloan Protection Rider section.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 20 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

Key Terms and Definitions

Accumulation Value The Accumulation Value is the cash accumulation component of theproposed policy. It reflects net premiums received, withdrawals made,expenses charged, cost of insurance deducted and interest credited.The Accumulation Value can be positive, negative, or zero.

Account Value Enhancement A persistency bonus available that is credited to the index accountsor fixed account after policy year 5. This is in addition to the creditingearned through the index strategy.

Alternate Hypothetical Rate The alternate values are calculated based on the guaranteed interestrate of the Fixed Account, the non-guaranteed maximum cost ofinsurance, and non-guaranteed expense charges specified in thepolicy.

Cash Surrender Value The Cash Surrender Value is the amount available to the policy ownerwhen the policy is terminated for a reason other than the Insured'sdeath. This is equal to the Cash Value less policy loans andaccumulated interest and may be zero.

Cash Surrender Value IRR The IRR on the Cash Surrender Value for a policy year is the discountrate that results in a net present value of zero for a series of cashflows equal to the net outlay from policy issue through the policy yearand the Cash Surrender Value at the end of the same policy year.

Cash Value The Cash Value of this policy is equal to the Accumulation Value minusthe applicable surrender charge, if any.

Cost of Insurance Charges The basis for calculating the cost of insurance for the policy and anyriders added to the policy is outlined in the policy.

Current Non-Guaranteed Hypothetical Rate See Index Interest Illustrated section.

Death Benefit The death benefit is the amount of money payable to the beneficiaryif the Insured dies while the policy is in force. The Initial Amount isspecified in the policy at issue and the Specified Amount may bechanged subject to the policy’s provisions.

Death Benefit IRR The IRR on the Death Benefit for a policy year is the discount ratethat results in a net present value of zero for a series of cash flowsequal to the net outlay from policy issue through the policy year andthe Death Benefit at the end of the same policy year.

Guaranteed Rate The guaranteed values are calculated based on the guaranteedinterest rate, the guaranteed maximum cost of insurance, andguaranteed expense charges specified in the policy.

Income-for-Life Value See Income-for-Life Rider section.

Lapse Policy Lapse refers to termination of the policy. When a policy lapses,it has no cash value and no death benefit is payable.

Loans and Withdrawals Policy loans can be taken at any time while the policy is in force. Forillustration purposes, all loans are taken out in monthly installments.Annual loan interest is assessed at the end of the policy year. Referto the policy for more information about policy loans. Withdrawalsrepresent amounts withdrawn from the policy which are not loans.

Maximum Non-Guaranteed Hypothetical Rate See Index Interest Illustrated section.

The Maximum Non-Guaranteed Hypothetical Index Interest Rate isnot intended to predict future performance and is not guaranteed.The Owner's actual results may be better or worse than shown.

Monthly Charges This represents the sum of the Cost of Insurance amount, MonthlyAdministration Fee amount, Monthly Expense Charge amount, andany applicable rider charges for each month illustrated.

Net Annual Loan Interest Credited This represents interest credited to the Accumulation Value offset bypolicy loans. These amounts may be credited at a different rate thanthose values not offset by policy loans.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 21 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

Non-Guaranteed Midpoint Rate The Non-Guaranteed Midpoint Rate is based on interest rates andcosts of insurance that are the average of, or halfway between, theGuaranteed Rate with Maximum Charges and the Non-GuaranteedRate with Current Charges.

Non-Guaranteed Rate The Non-Guaranteed Rate used in this illustration is the user selectedinterest rate(s) up to the Maximum Current Non-GuaranteedHypothetical Rates for each Interest Account. The Non-GuaranteedRate is not intended to predict future performance and is notguaranteed. The Owner's actual results may be better or worse thanshown.

Partial Surrenders/Withdrawals This represents the amount withdrawn from the policy.

Premium Class Preferred Non-TobaccoSignificantly better than average mortality risk and a non-user oftobacco and/or other products that contain nicotine.

Premium Expense Charge See Your Transaction Charges section.

Premium Mode The Premium Mode is the frequency selected for recurring premiums.

Premium Outlay Premium outlay is the amount the Owner plans to pay for the policy.It is equal to planned premium payments and loan repayments.

Surrender Charges A surrender charge will be applied when the policy is surrendered orthe specified amount is reduced during the surrender charge period.If the specified amount is increased, the increased portion is subjectto a new surrender charge period. The initial surrender charge periodis 14 years. Refer to the policy for more information about SurrenderCharges.

Year and Age Year is the policy year; Age is the Insured's age at the Date of Issueplus on the Insured's nearest birthday the number of years the policyis assumed to have been in force.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 22 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

Important Disclosures Preceding Numeric Summary1. Life insurance is not an investment. You are purchasing a universal life insurance policy because you have a long term need for permanent

life insurance.

2. You should review the product materials provided by AGL for this individual fixed index interest flexible premium adjustable life insurancepolicy.

3. You selected the premium shown in the illustration to show AGL how much premium you intend to pay or otherwise to be applied aspremium, including but not limited to any funds from another insurer transferred pursuant to a Section 1035 Exchange under the InternalRevenue Code.

4. Premiums paid and amounts that may be credited to the policy may not be sufficient to cover the cost of insurance and/or administrativeexpenses. Paying less than the planned premium can have a negative impact on the policy and any guarantees. Reduced premiumpayments, loans, and/or withdrawals are examples of factors which could necessitate additional premiums to maintain your insurancecoverage. If this illustration shows that you have the option to allow policy charges to be paid using non-guaranteed values or if theillustration shows a premium outlay of lesser amounts or shorter duration than the contract premium, if any, you may need to continueor resume premium outlays.

5. Changes in the non-guaranteed elements of your policy may affect the amount of your insurance benefits, the duration of your insurancecoverage, and your policy value. The policy value may reduce to zero. If the net cash surrender value is insufficient to pay the chargeswhen due, and the death benefit protection is no longer in effect, your policy will lapse and terminate unless more premiums are paid.At such time, you will have no insurance coverage.

6. While index interest credited to the policy is related to the performance of the underlying index, it is not an investment in that index. Theactual amount of index interest credited to an index universal life insurance policy will vary based on the performance of the index, theinterest rate environment, the cost of options, and other economic factors.

7. There will be substantial variation in both the timing and amount of index interest credited over the life of the policy.

8. Historical performance of the S&P 500® and the ML Strategic Balanced IndexTM should not be considered a representation of futureperformance for any of the index interest strategies in the policy.

9. You should review the Tabular Detail - Alternate Rate pages, which show the effect of changing the hypothetical crediting rates of theIndex Accounts.

10. QoL Max Accumulator+ offers two types of policy loans as described in this illustration, and you are solely responsible for the selectionof the loan type.

11. Cost of insurance rates, insurance amounts, charges, riders, and endorsements offered, along with other parameters, may vary dependingon the agent through whom you purchase your policy.

12. Proper maintenance of the policy is essential, and it is recommended that you regularly review your policy. The only viable way to knowif an index universal life insurance policy is meeting your needs is to review the policy's performance no less frequently than once a year.Annual reviews of your policy should include review of the annual statement and review of an in-force illustration you request, which youshould review to determine whether any adjustments are necessary to your planned premium payments and to the allocation of yourcurrent crediting strategies, including index interest, and your review of any distributions to you under the policy.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 23 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

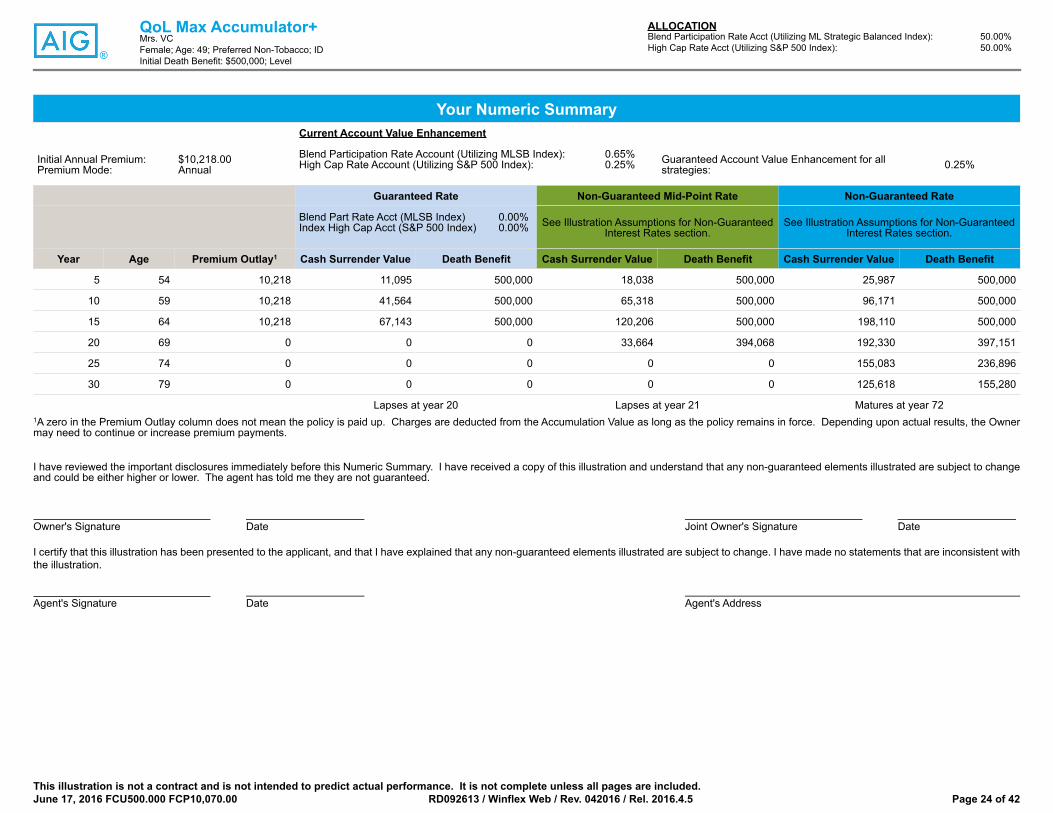

Your Numeric SummaryCurrent Account Value Enhancement

Initial Annual Premium:Premium Mode:

$10,218.00Annual

Blend Participation Rate Account (Utilizing MLSB Index): 0.65%High Cap Rate Account (Utilizing S&P 500 Index): 0.25% Guaranteed Account Value Enhancement for all

strategies: 0.25%

Guaranteed Rate Non-Guaranteed Mid-Point Rate Non-Guaranteed Rate

Blend Part Rate Acct (MLSB Index) 0.00%Index High Cap Acct (S&P 500 Index) 0.00% See Illustration Assumptions for Non-Guaranteed

Interest Rates section.See Illustration Assumptions for Non-Guaranteed

Interest Rates section.

Year Age Premium Outlay1 Cash Surrender Value Death Benefit Cash Surrender Value Death Benefit Cash Surrender Value Death Benefit

5 54 10,218 11,095 500,000 18,038 500,000 25,987 500,000

10 59 10,218 41,564 500,000 65,318 500,000 96,171 500,000

15 64 10,218 67,143 500,000 120,206 500,000 198,110 500,000

20 69 0 0 0 33,664 394,068 192,330 397,151

25 74 0 0 0 0 0 155,083 236,896

30 79 0 0 0 0 0 125,618 155,280

Lapses at year 20 Lapses at year 21 Matures at year 721A zero in the Premium Outlay column does not mean the policy is paid up. Charges are deducted from the Accumulation Value as long as the policy remains in force. Depending upon actual results, the Ownermay need to continue or increase premium payments.

I have reviewed the important disclosures immediately before this Numeric Summary. I have received a copy of this illustration and understand that any non-guaranteed elements illustrated are subject to changeand could be either higher or lower. The agent has told me they are not guaranteed.

Owner's Signature Date Joint Owner's Signature Date

I certify that this illustration has been presented to the applicant, and that I have explained that any non-guaranteed elements illustrated are subject to change. I have made no statements that are inconsistent withthe illustration.

Agent's Signature Date Agent's Address

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 24 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

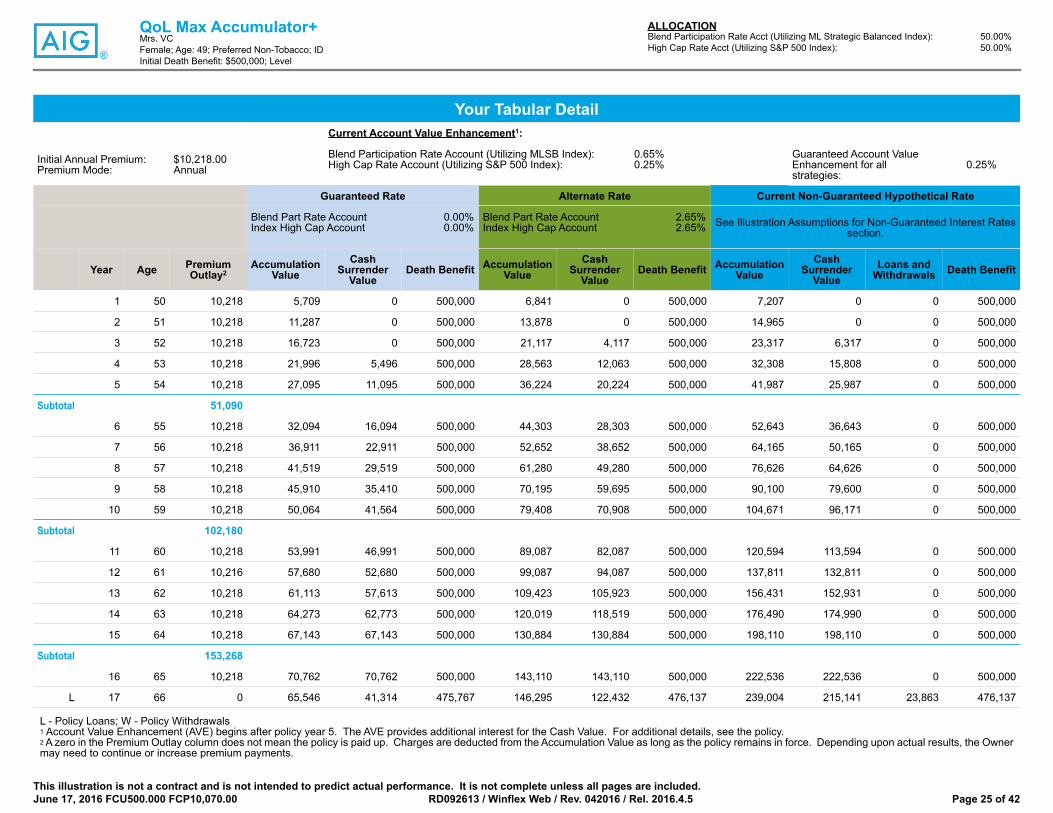

Your Tabular DetailCurrent Account Value Enhancement1:

Initial Annual Premium:Premium Mode:

$10,218.00Annual

Blend Participation Rate Account (Utilizing MLSB Index): 0.65%High Cap Rate Account (Utilizing S&P 500 Index): 0.25%

Guaranteed Account ValueEnhancement for allstrategies:

0.25%

Guaranteed Rate Alternate Rate Current Non-Guaranteed Hypothetical Rate

Blend Part Rate Account 0.00%Index High Cap Account 0.00%

Blend Part Rate Account 2.65%Index High Cap Account 2.65% See Illustration Assumptions for Non-Guaranteed Interest Rates

section.

Year Age PremiumOutlay2

AccumulationValue

CashSurrender

ValueDeath Benefit Accumulation

ValueCash

SurrenderValue

Death Benefit AccumulationValue

CashSurrender

ValueLoans and

Withdrawals Death Benefit

1 50 10,218 5,709 0 500,000 6,841 0 500,000 7,207 0 0 500,000

2 51 10,218 11,287 0 500,000 13,878 0 500,000 14,965 0 0 500,000

3 52 10,218 16,723 0 500,000 21,117 4,117 500,000 23,317 6,317 0 500,000

4 53 10,218 21,996 5,496 500,000 28,563 12,063 500,000 32,308 15,808 0 500,000

5 54 10,218 27,095 11,095 500,000 36,224 20,224 500,000 41,987 25,987 0 500,000

Subtotal 51,090

6 55 10,218 32,094 16,094 500,000 44,303 28,303 500,000 52,643 36,643 0 500,000

7 56 10,218 36,911 22,911 500,000 52,652 38,652 500,000 64,165 50,165 0 500,000

8 57 10,218 41,519 29,519 500,000 61,280 49,280 500,000 76,626 64,626 0 500,000

9 58 10,218 45,910 35,410 500,000 70,195 59,695 500,000 90,100 79,600 0 500,000

10 59 10,218 50,064 41,564 500,000 79,408 70,908 500,000 104,671 96,171 0 500,000

Subtotal 102,180

11 60 10,218 53,991 46,991 500,000 89,087 82,087 500,000 120,594 113,594 0 500,000

12 61 10,216 57,680 52,680 500,000 99,087 94,087 500,000 137,811 132,811 0 500,000

13 62 10,218 61,113 57,613 500,000 109,423 105,923 500,000 156,431 152,931 0 500,000

14 63 10,218 64,273 62,773 500,000 120,019 118,519 500,000 176,490 174,990 0 500,000

15 64 10,218 67,143 67,143 500,000 130,884 130,884 500,000 198,110 198,110 0 500,000

Subtotal 153,268

16 65 10,218 70,762 70,762 500,000 143,110 143,110 500,000 222,536 222,536 0 500,000

L 17 66 0 65,546 41,314 475,767 146,295 122,432 476,137 239,004 215,141 23,863 476,137

L - Policy Loans; W - Policy Withdrawals1 Account Value Enhancement (AVE) begins after policy year 5. The AVE provides additional interest for the Cash Value. For additional details, see the policy.2 A zero in the Premium Outlay column does not mean the policy is paid up. Charges are deducted from the Accumulation Value as long as the policy remains in force. Depending upon actual results, the Ownermay need to continue or increase premium payments.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 25 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

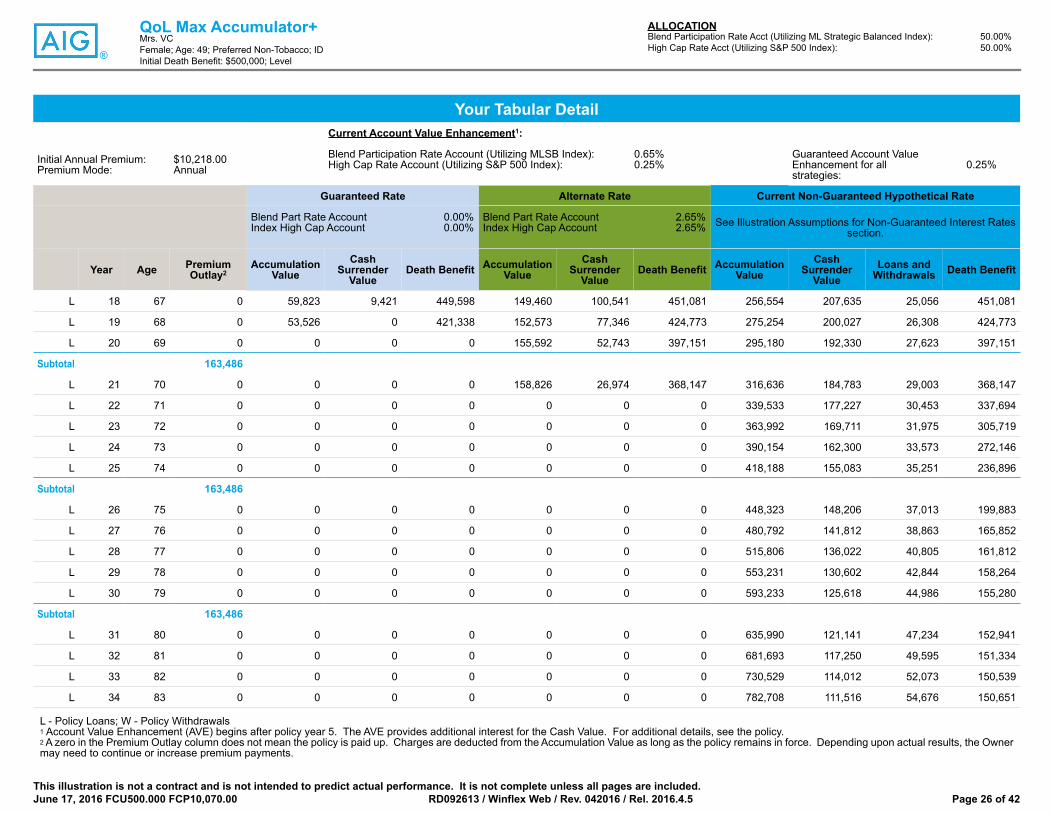

Your Tabular DetailCurrent Account Value Enhancement1:

Initial Annual Premium:Premium Mode:

$10,218.00Annual

Blend Participation Rate Account (Utilizing MLSB Index): 0.65%High Cap Rate Account (Utilizing S&P 500 Index): 0.25%

Guaranteed Account ValueEnhancement for allstrategies:

0.25%

Guaranteed Rate Alternate Rate Current Non-Guaranteed Hypothetical Rate

Blend Part Rate Account 0.00%Index High Cap Account 0.00%

Blend Part Rate Account 2.65%Index High Cap Account 2.65% See Illustration Assumptions for Non-Guaranteed Interest Rates

section.

Year Age PremiumOutlay2

AccumulationValue

CashSurrender

ValueDeath Benefit Accumulation

ValueCash

SurrenderValue

Death Benefit AccumulationValue

CashSurrender

ValueLoans and

Withdrawals Death Benefit

L 18 67 0 59,823 9,421 449,598 149,460 100,541 451,081 256,554 207,635 25,056 451,081

L 19 68 0 53,526 0 421,338 152,573 77,346 424,773 275,254 200,027 26,308 424,773

L 20 69 0 0 0 0 155,592 52,743 397,151 295,180 192,330 27,623 397,151

Subtotal 163,486

L 21 70 0 0 0 0 158,826 26,974 368,147 316,636 184,783 29,003 368,147

L 22 71 0 0 0 0 0 0 0 339,533 177,227 30,453 337,694

L 23 72 0 0 0 0 0 0 0 363,992 169,711 31,975 305,719

L 24 73 0 0 0 0 0 0 0 390,154 162,300 33,573 272,146

L 25 74 0 0 0 0 0 0 0 418,188 155,083 35,251 236,896

Subtotal 163,486

L 26 75 0 0 0 0 0 0 0 448,323 148,206 37,013 199,883

L 27 76 0 0 0 0 0 0 0 480,792 141,812 38,863 165,852

L 28 77 0 0 0 0 0 0 0 515,806 136,022 40,805 161,812

L 29 78 0 0 0 0 0 0 0 553,231 130,602 42,844 158,264

L 30 79 0 0 0 0 0 0 0 593,233 125,618 44,986 155,280

Subtotal 163,486

L 31 80 0 0 0 0 0 0 0 635,990 121,141 47,234 152,941

L 32 81 0 0 0 0 0 0 0 681,693 117,250 49,595 151,334

L 33 82 0 0 0 0 0 0 0 730,529 114,012 52,073 150,539

L 34 83 0 0 0 0 0 0 0 782,708 111,516 54,676 150,651

L - Policy Loans; W - Policy Withdrawals1 Account Value Enhancement (AVE) begins after policy year 5. The AVE provides additional interest for the Cash Value. For additional details, see the policy.2 A zero in the Premium Outlay column does not mean the policy is paid up. Charges are deducted from the Accumulation Value as long as the policy remains in force. Depending upon actual results, the Ownermay need to continue or increase premium payments.

This illustration is not a contract and is not intended to predict actual performance. It is not complete unless all pages are included.June 17, 2016 FCU500.000 FCP10,070.00 RD092613 / Winflex Web / Rev. 042016 / Rel. 2016.4.5 Page 26 of 42

®

QoL Max Accumulator+Mrs. VCFemale; Age: 49; Preferred Non-Tobacco; IDInitial Death Benefit: $500,000; Level

ALLOCATIONBlend Participation Rate Acct (Utilizing ML Strategic Balanced Index): 50.00%High Cap Rate Acct (Utilizing S&P 500 Index): 50.00%

Your Tabular DetailCurrent Account Value Enhancement1:

Initial Annual Premium:Premium Mode:

$10,218.00Annual

Blend Participation Rate Account (Utilizing MLSB Index): 0.65%High Cap Rate Account (Utilizing S&P 500 Index): 0.25%

Guaranteed Account ValueEnhancement for allstrategies:

0.25%

Guaranteed Rate Alternate Rate Current Non-Guaranteed Hypothetical Rate

Blend Part Rate Account 0.00%Index High Cap Account 0.00%

Blend Part Rate Account 2.65%Index High Cap Account 2.65% See Illustration Assumptions for Non-Guaranteed Interest Rates

section.

Year Age PremiumOutlay2

AccumulationValue

CashSurrender

ValueDeath Benefit Accumulation

ValueCash

SurrenderValue

Death Benefit AccumulationValue

CashSurrender

ValueLoans and

Withdrawals Death Benefit

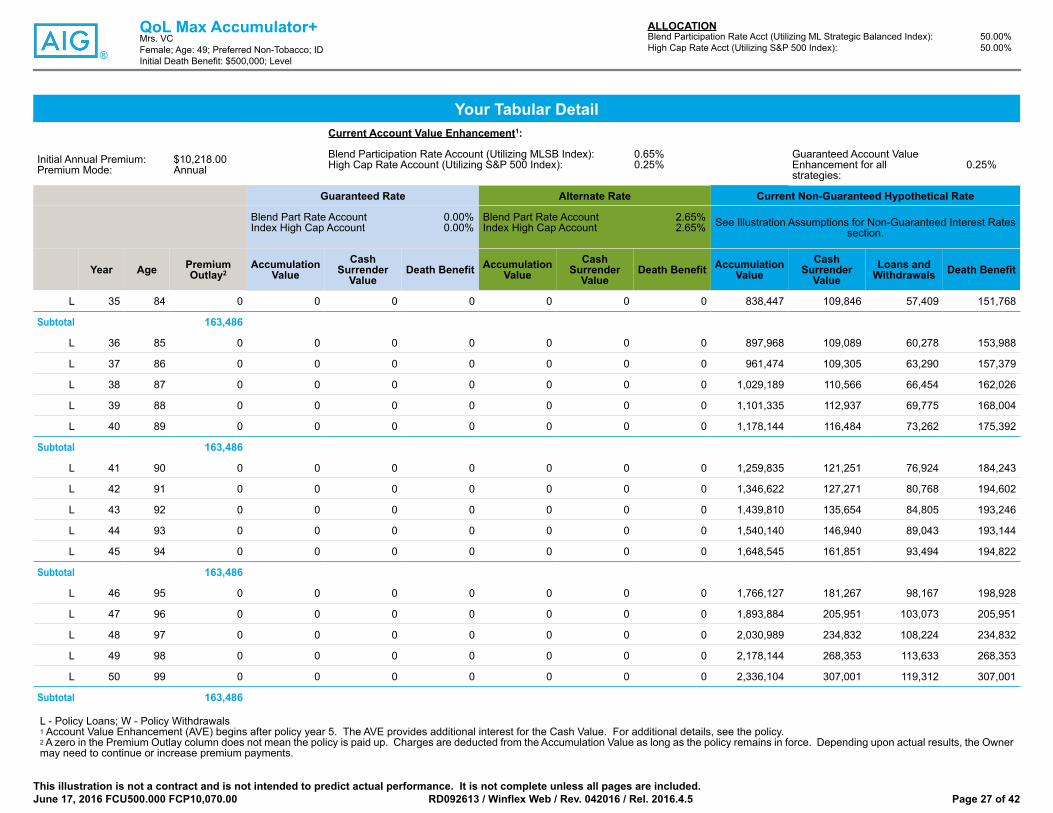

L 35 84 0 0 0 0 0 0 0 838,447 109,846 57,409 151,768

Subtotal 163,486

L 36 85 0 0 0 0 0 0 0 897,968 109,089 60,278 153,988

L 37 86 0 0 0 0 0 0 0 961,474 109,305 63,290 157,379