Embed Size (px)

Citation preview

Financial InclusionShashank Chowdhury12th November 2014

What is Financial Inclusion

“Financial inclusion is the process of ensuring access to appropriate financial products and services needed by all members of the society in general and vulnerable groups in particular, at an affordable cost in a fair and transparent manner by mainstream institutional players” - RBI

Process

Bank Led ModelMainstream Banking Institutions

BranchesBusiness Correspondents

Other IntermediariesTelcosTechnology PartnersMFIs/NBFCs/NGOsServe the important objective of Bringing People and Communities in the fold of Financial Inclusion

Appropriate Financial Products and Services

Majority requireA basic No Frills Savings AccountA basic ‘No Questions Asked’ CreditA basic Insurance of Life

Many requireFixed DepositsRecurring DepositsKCCGCCOther Loans

Housing Consumer Small and Medium Business

Society in General and the Vulnerable in Particular

VulnerableInability to withstand the effects of a hostile environment

Resources required to withstand Money

SavingsEarnings Growing at par with InflationFuture Protection

KnowledgePossible hazardsRemedies

Affordable Costs

For the ConsumerCost not to exceed the Benefit Costs have been a primary reasons for exclusion

For the ProviderPricing of products and services not to be less than cost Technology has made it possible to match the expectations

TelecommunicationCBSPower

Fair and Transparent Manner

Success of a System depends on its acceptance and credibility

Delivery of ServiceShould be fair to the consumer

Provide satisfying evidenceProvide an opportunity to escalate

Should be transparent to Stakeholders

RegulatorGovernmentBank ManagementPublic in General

Mainstream Institutional Players

BanksCommercial Regional RuralCooperative

LIC

GIC and its Subsidiaries

Initiatives

SHG-Bank Linkage Model, one of the largest micro finance models in the world, under which 4.79 million SHGs have been credit linked, covering 97 million poor households (till March 2012)Core Banking PlatformSubstantially liberalised the BC based service delivery model in phases.Permitted domestic scheduled commercial banks to freely open branches in Tier 2 to Tier 6 centres.Mandated banks to open at least 25% of all new branches in unbanked rural centres.Substantially relaxed the Know Your Customer (KYC) documentation requirements for opening bank accounts for small customers.Encouraged Electronic Benefit Transfer for routing social security payments through the banking channel.Pricing for banks totally freed; Interest rates on advances totally deregulated.Separate programme for Urban Financial Inclusion initiated.

Features of Strategic Initiatives

Structured Phase wise CoverageBranches and ICT Based BC outletsInteroperabilityEfficient Cash Management, Documents, Redressal of Customer Grievances and Supervision of BCsThe evolution of the BC model comprises of the following four stages

Stage 1 : Mobile Business CorrespondentsStage 2 : Fixed Location Business Correspondent OutletsStage 3 : Low Cost Intermediate Brick & Mortar Structures (Ultra Small Branches)Stage 4 : Full fledged Brick & Mortar Branches

Financial Inclusion Plan (FIP) for Banks - All domestic commercial banks - public and private sector have drawn a Board approved three year FIP starting April 2010.

Constraints

Demand side Low Literacy LevelsIrregular IncomeFrequent Micro TransactionsLack of Trust in Formal Banking SystemCultural ( Gender and other values)

Supply sideOutreachRegulationBusiness Models ( High Fixed Costs)Limited number of Service ProvidersProducts and Services and Not AlignedAge FactorBank Charges

Stability

ICT based BC ModelTechnology BC/BCABank

Evolving Models

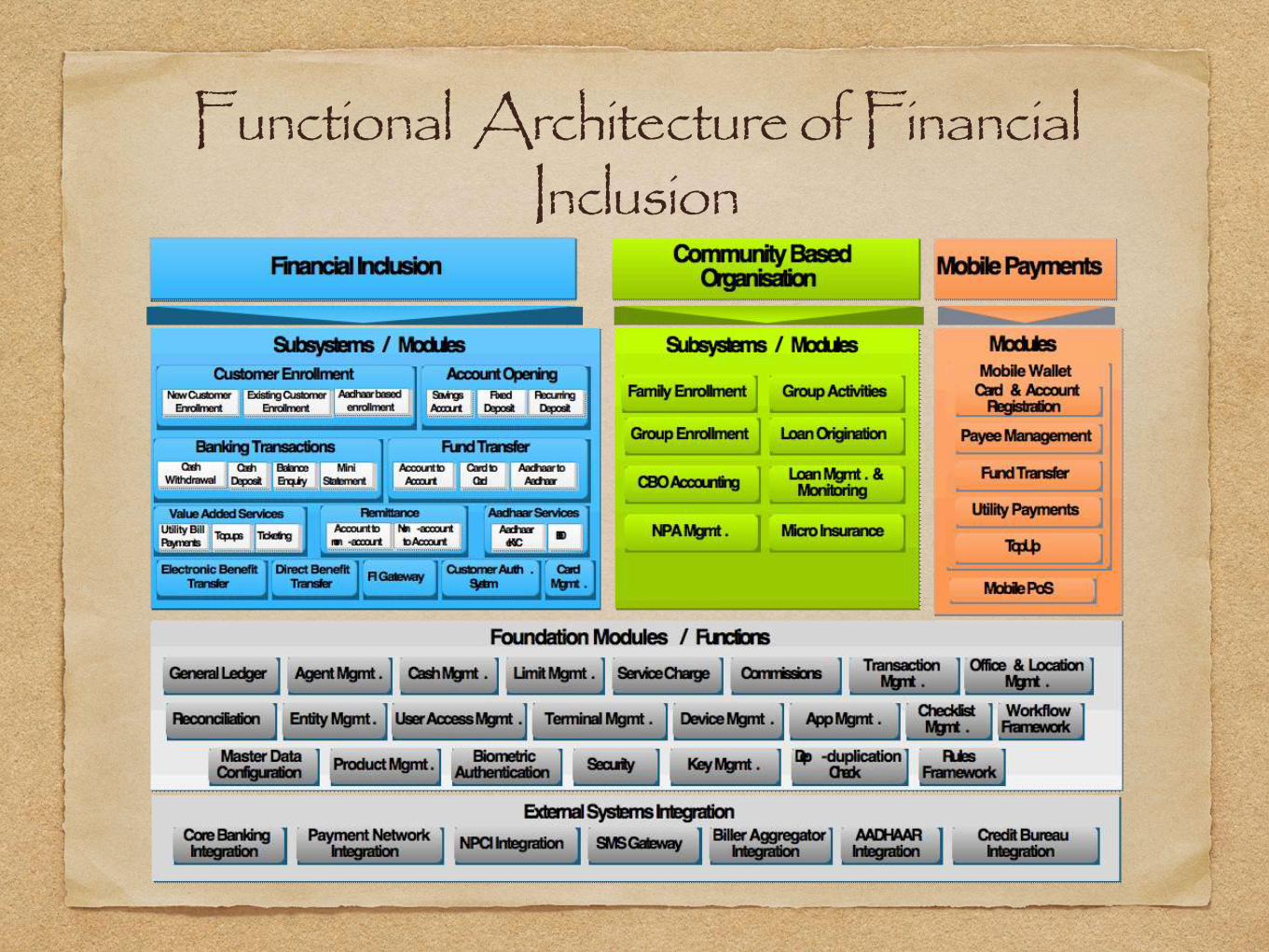

Functional Architecture of Financial Inclusion

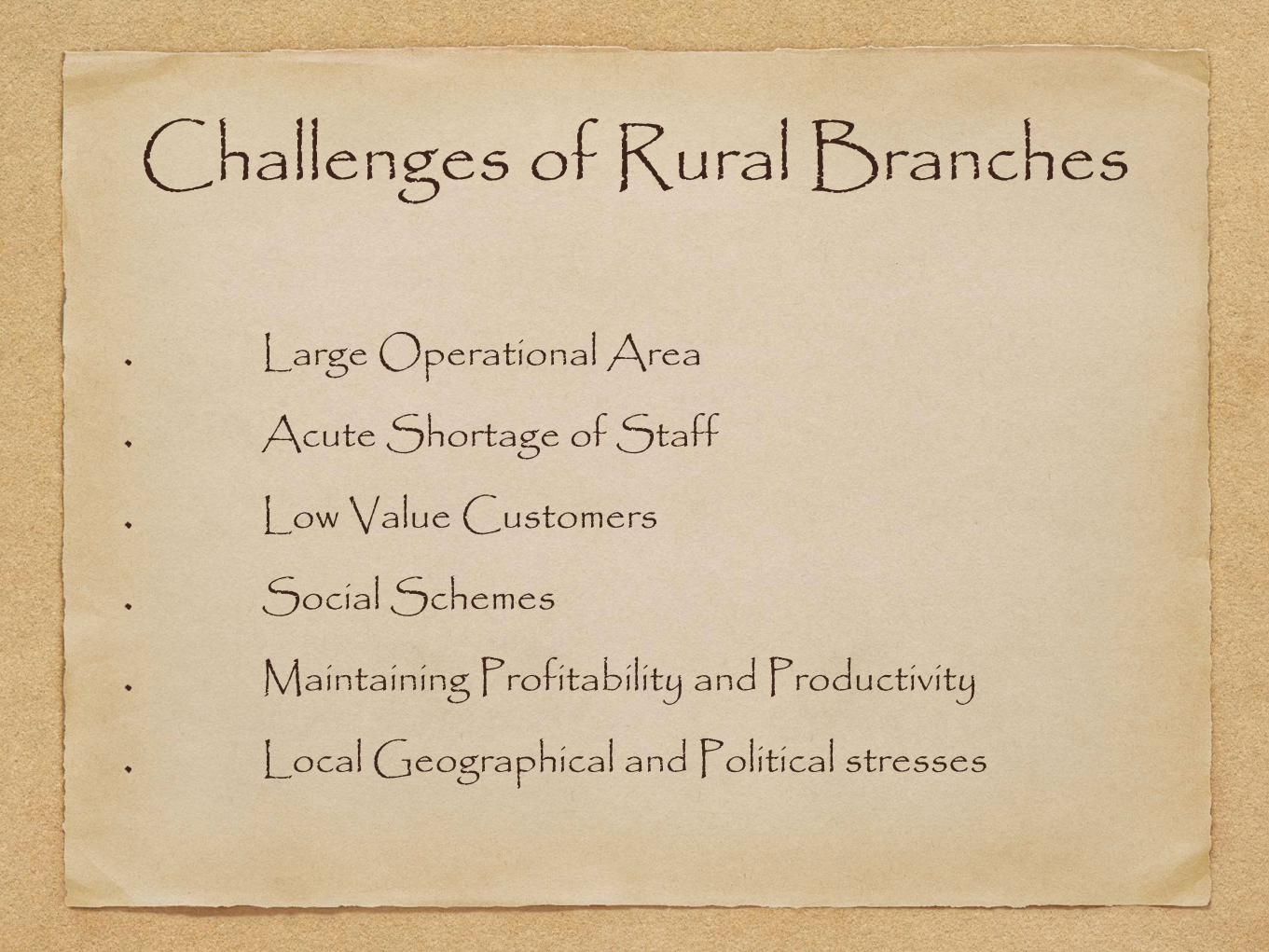

Challenges of Rural Branches

Large Operational Area

Acute Shortage of Staff

Low Value Customers

Social Schemes

Maintaining Profitability and Productivity

Local Geographical and Political stresses

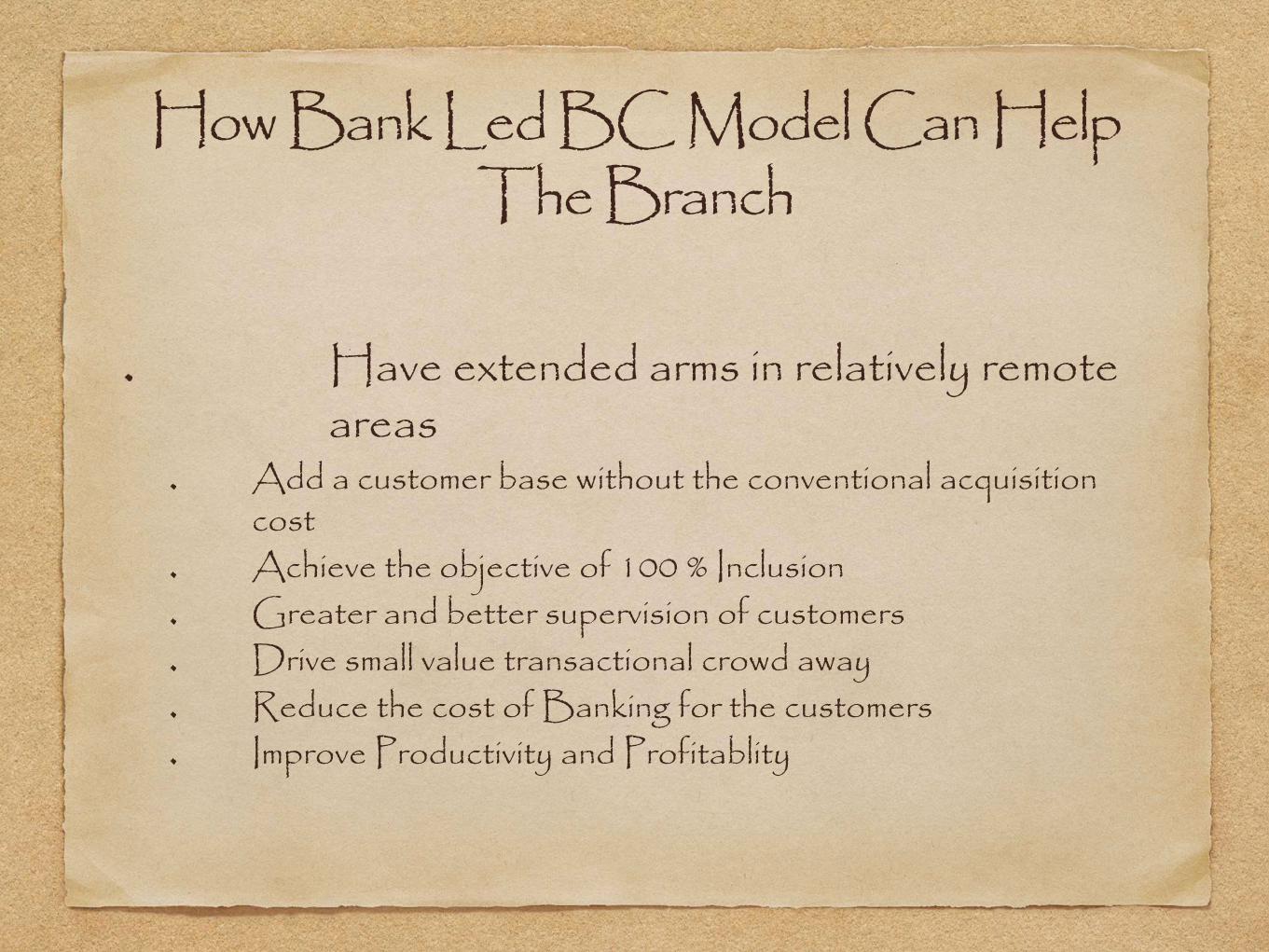

How Bank Led BC Model Can HelpThe Branch

Have extended arms in relatively remote areas

Add a customer base without the conventional acquisition costAchieve the objective of 100 % InclusionGreater and better supervision of customers Drive small value transactional crowd awayReduce the cost of Banking for the customersImprove Productivity and Profitablity

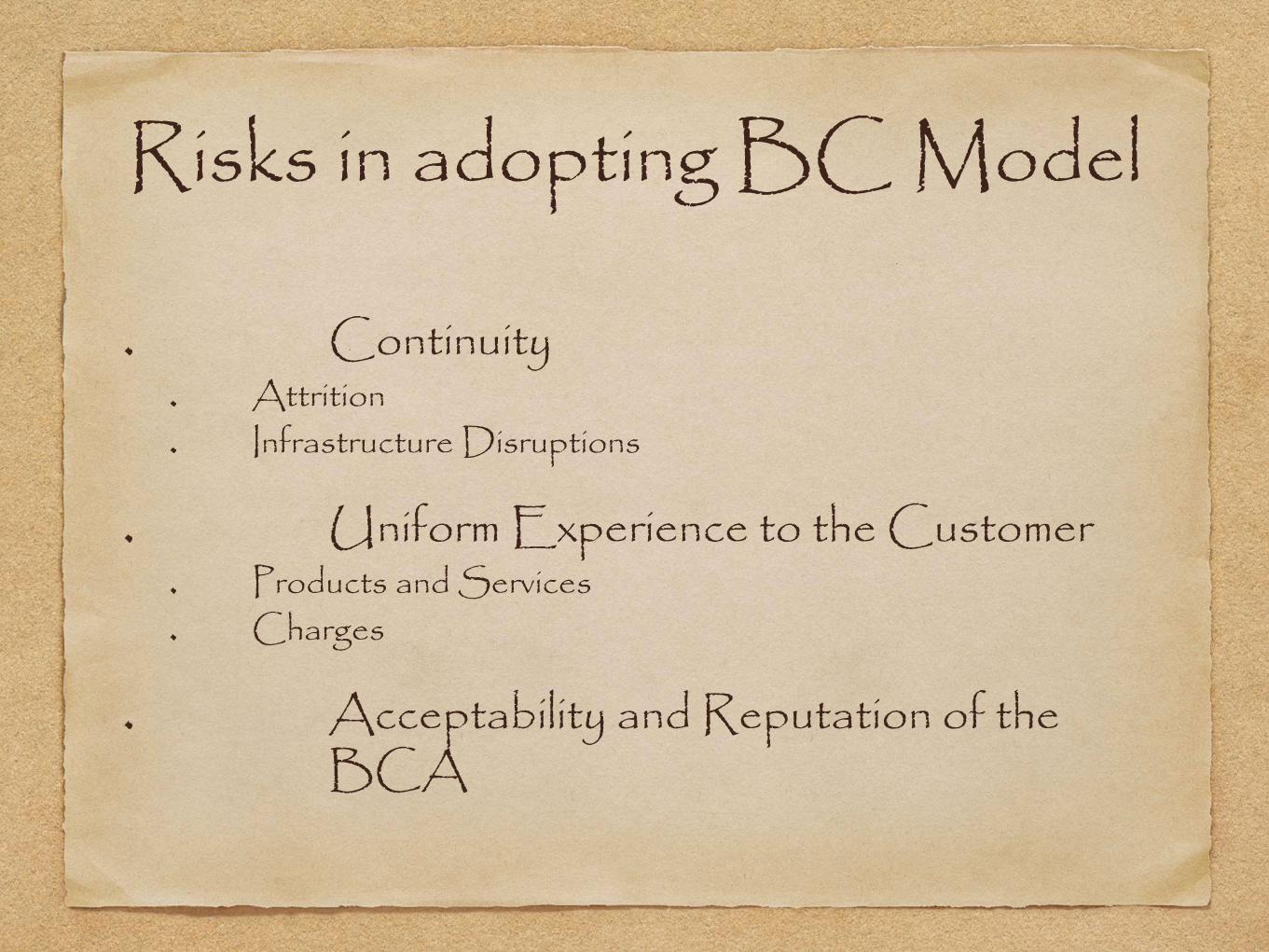

Risks in adopting BC Model

ContinuityAttritionInfrastructure Disruptions

Uniform Experience to the CustomerProducts and ServicesCharges

Acceptability and Reputation of the BCA

Ways to Adopt

Train the BCAFamiliarise with Products and Services of the BankFamiliarise the BCA with Ethics and Code of ConductMake him aware of the Organisational Vision and Mission of the Bank

Close SupervisionMeet the BCA frequently at his placeLet the people know that BCA is your representative just as you would do for your staffInform him regularly about the changes that are taking place

New ProductsInterest Rates

Best to give him Targets ( just like any other staff member) and apprise him of his achievements and shortfalls

![Financial Inclusion: General Overview, Central Banks …...Financial Inclusion [General Overview] •Financial inclusion or inclusive financing is the delivery of financial services](https://img.pdfslide.net/doc/110x75/5e95eef43708446e852354fe/financial-inclusion-general-overview-central-banks-financial-inclusion-general.jpg)