Embed Size (px)

Citation preview

Groups of Claimants who will be asking a share of Revenue

• Employees, the vendors, the landlord, the u<lity suppliers, the printer, the sta<oner, the travel agent and so on. This group represents Opera<ng Expenses

• Shareholders or owners • Government • Lenders

Order of Payments

• Opera0ng Expenses • Lenders • Government • Shareholders or Owners

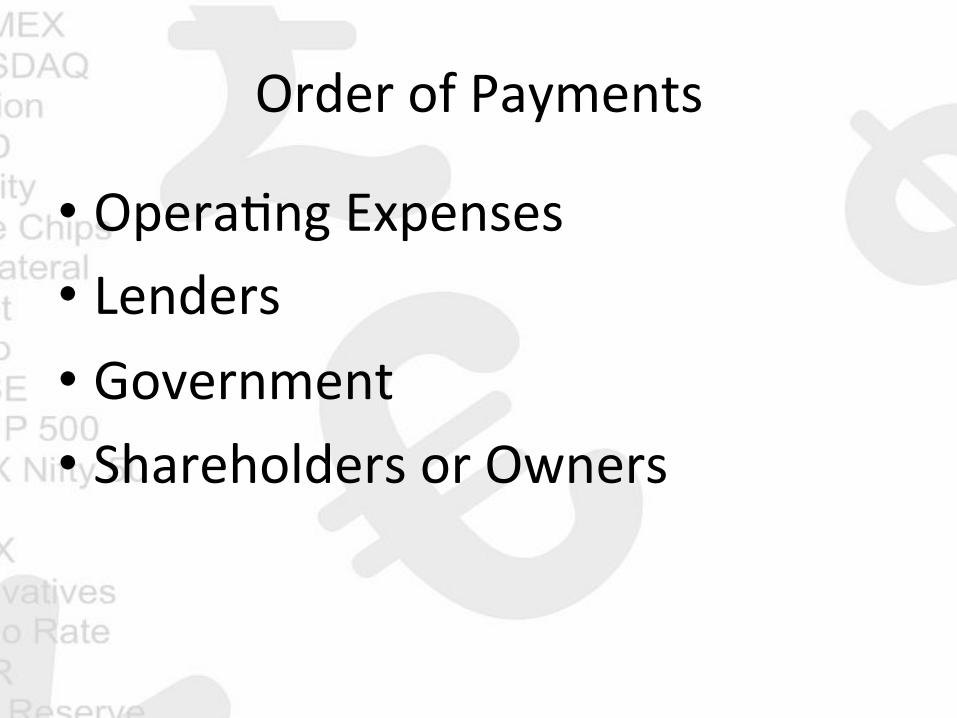

Profit & Loss A/c Sales

Less: Cost of Sales or Direct Expenses

Gross Profit

Less: Administrative and Selling & Distribution Expenses or Indirect Expenses

Profit before Interest, Depreciation and Tax Less: Depreciation

Profit before Interest or Operating Profit

Less: Interest

Profit Before Tax

Less: Provision for Taxation

Profit After Tax

Less: Dividends

Transferred to Reserves

Journey of a Business Idea

Capital

Money

Infrastructure Investment Operating Cycle

Cash

Raw Materials Sales

Debtors Creditors

Other Expenses

WORKING CAPITAL

• GROSS WORKING CAPITAL • NET WORKING CAPITAL • CURRENT ASSETS FUNDED BY CURRENT LIABILITIES

• CURRENT ASSETS INCREASE REQUIREMENT OF CASH

• CURRENT LIABILITIES DECREASE REQUIREMENT OF CASH

• CHEAPEST SOURCE OF FUND -‐ Creditors

CASH

BILLS PAYABLE/ CREDITORS

RAW MATERIALS

FINISHED GOODS

OTHER EXPENSES

BILLS RECEIVABLES/ DEBTORS

Purchase of Raw Materials

Produc0on

Collec0on

Credit Sales

OPERATING CYCLE

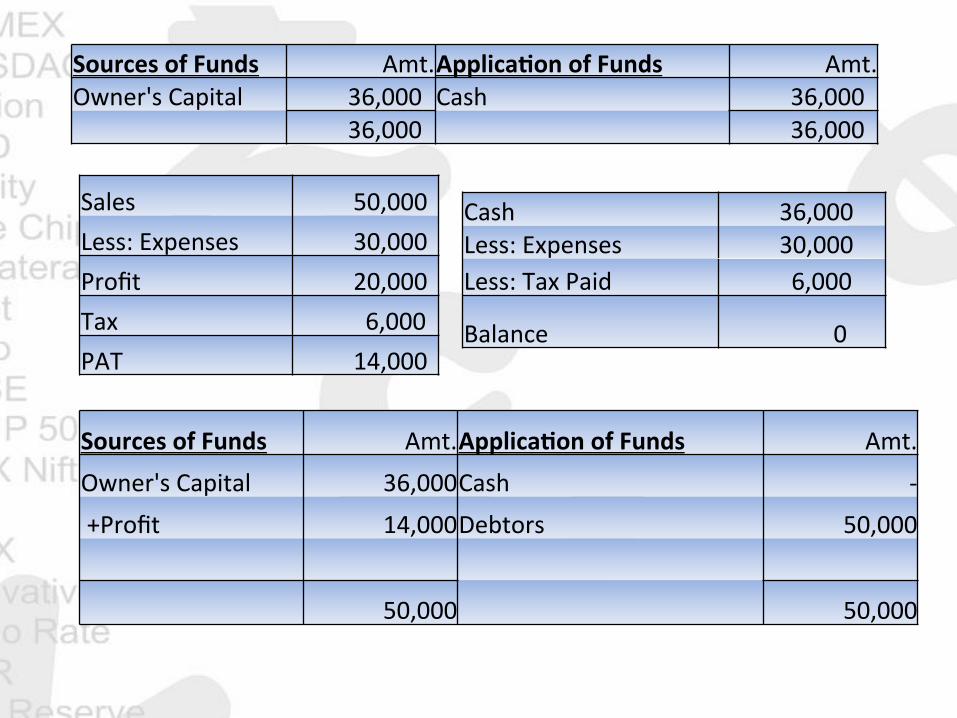

The Profit that never Was!

Sales 50,000 Less: Expenses 30,000 Profit 20,000 Tax 6,000 PAT 14,000

Sources of Funds Amt. Applica<on of Funds Amt. Owner's Capital 36,000 Cash 36,000 36,000 36,000

Cash 36,000 Less: Expenses 30,000 Less: Tax Paid 6,000

Balance 0

Sources of Funds Amt. Applica<on of Funds Amt. Owner's Capital 36,000 Cash -‐ +Profit 14,000 Debtors 50,000

50,000 50,000

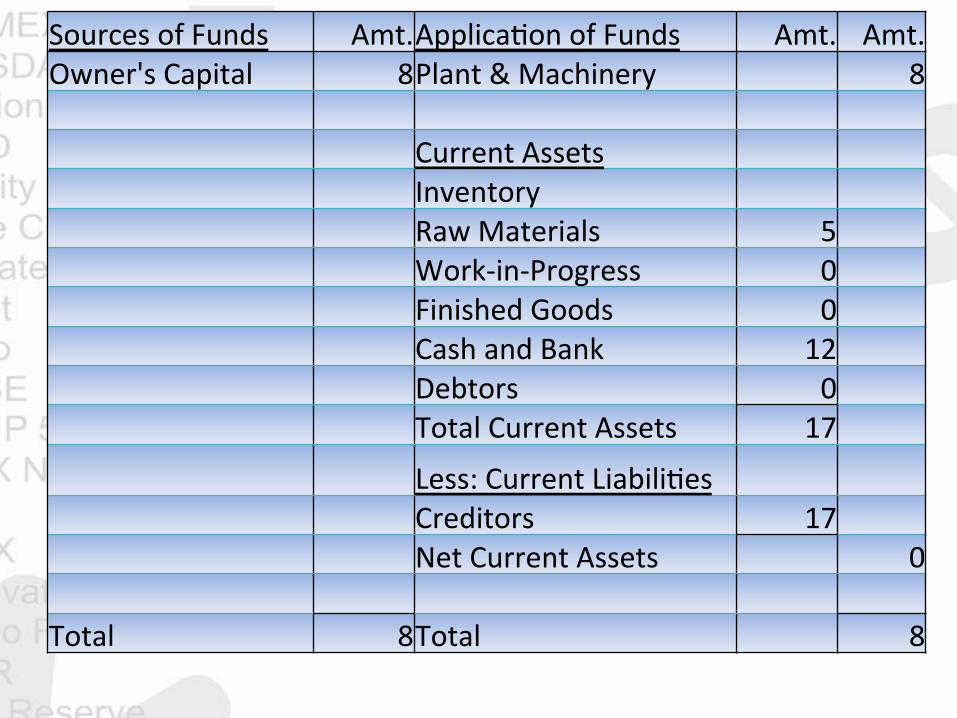

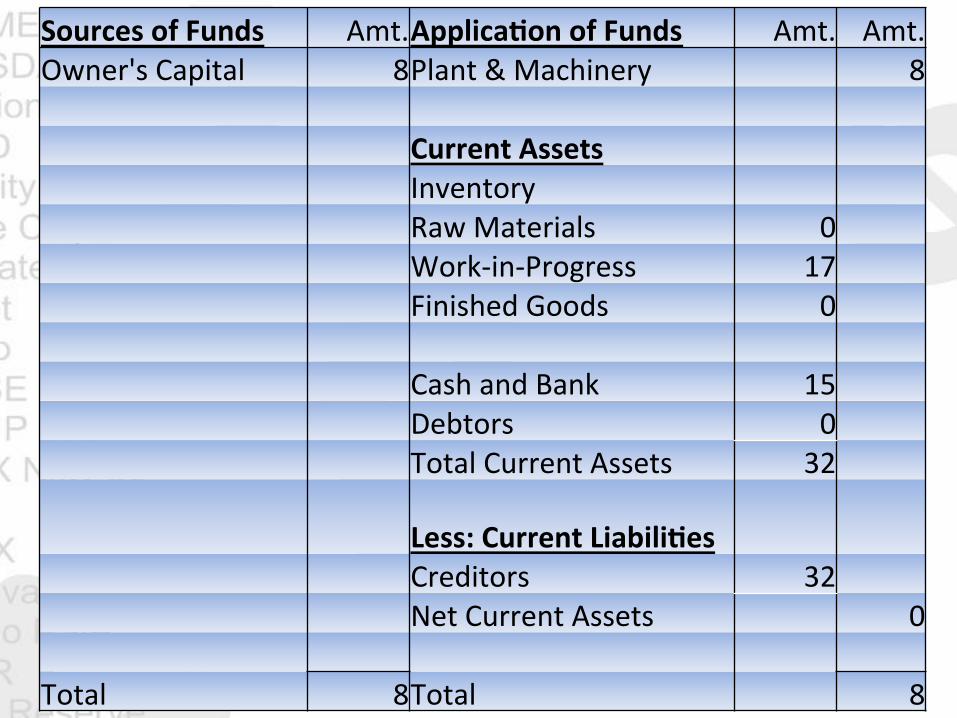

Case Study on Bad Inventory Management

Hindi Movie – Manufacturing Collars

Sources of Funds Amt. Applica0on of Funds Amt. Amt. Owner's Capital 8 Plant & Machinery 8 Current Assets Inventory Raw Materials 5 Work-‐in-‐Progress 0 Finished Goods 0 Cash and Bank 12 Debtors 0 Total Current Assets 17

Less: Current Liabili0es Creditors 17 Net Current Assets 0 Total 8 Total 8

Sources of Funds Amt. Applica<on of Funds Amt. Amt. Owner's Capital 8 Plant & Machinery 8 Current Assets Inventory Raw Materials 0 Work-‐in-‐Progress 17 Finished Goods 0 Cash and Bank 0 Debtors 0 Total Current Assets 17 Less: Current Liabili<es Creditors 17 Net Current Assets 0 Total 8 Total 8

Sources of Funds Amt. Applica<on of Funds Amt. Amt. Owner's Capital 8 Plant & Machinery 8 Current Assets Inventory Raw Materials 0 Work-‐in-‐Progress 17 Finished Goods 0 Cash and Bank 15 Debtors 0 Total Current Assets 32

Less: Current Liabili<es Creditors 32 Net Current Assets 0 Total 8 Total 8

Cash Conversion Cycle

Inventory Period Collec<on Period

Payment Period Cash Conversion Cycle

Raw Materials Purchased Sales Cash Received From Customer

Start of Credit Period Payment Made to Vendor

Prac0cal Applica0ons – Accounts Receivables

• How Sa0sfied is your Customer? – Are you selling to Customers who pay bills on 0me? – Do you have Customer In0macy to talk about Payment Terms?

– Do you provide Excellent Customer Service so as to enable your Customers to pay on 0me?

– Is the product free of defects? – Are invoices accurate? – Does the mailroom send invoices on a 0mely basis? – Is the recep0onist helpful?

Prac0cal Applica0ons

• Inventory – Engineering – do you request special products all the 0me?

– Opera0ons – Are you fond of keeping lots of Stock? • Expenses – Do you defer Expenses? – Do you consider Timing of Cash Flows when purchasing?

• Giving Credit – Do you give credit to poten0al customers too easily? – Do you withhold credit when you should give it?

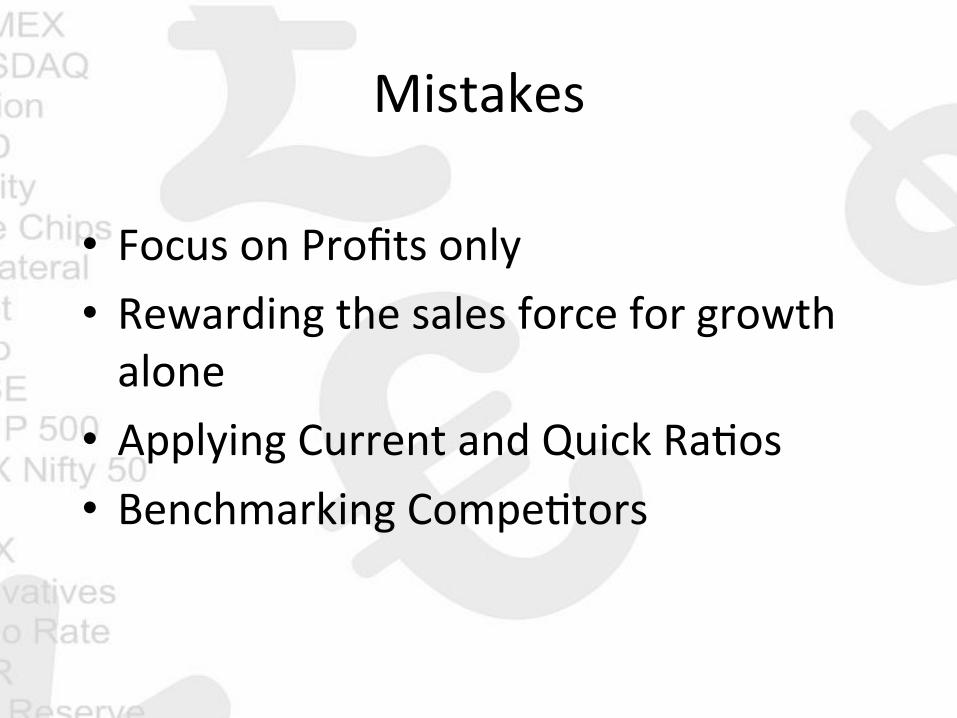

Mistakes

• Focus on Profits only • Rewarding the sales force for growth alone • Applying Current and Quick Ra0os • Benchmarking Compe0tors

Working Capital Management

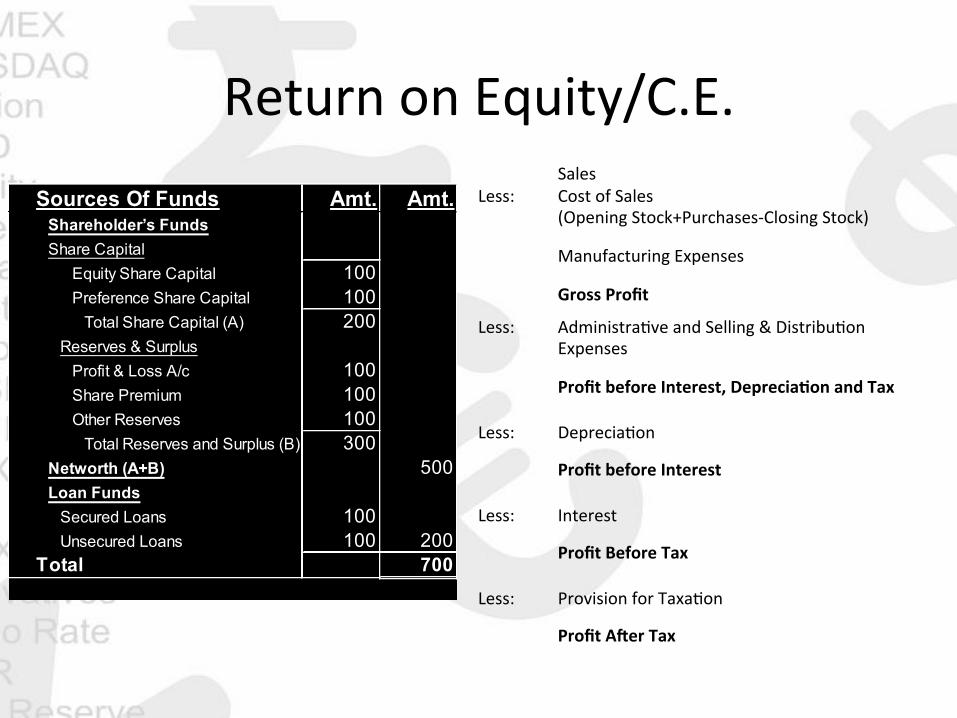

Return on Equity/C.E. Sources Of Funds Amt. Amt.

Shareholder’s FundsShare Capital

Equity Share Capital 100Preference Share Capital 100

Total Share Capital (A) 200Reserves & Surplus

Profit & Loss A/c 100Share Premium 100Other Reserves 100

Total Reserves and Surplus (B) 300Networth (A+B) 500Loan Funds

Secured Loans 100Unsecured Loans 100 200

Total 700Application Of Funds

Sales Less: Cost of Sales

(Opening Stock+Purchases-‐Closing Stock)

Manufacturing Expenses

Gross Profit

Less: Administra0ve and Selling & Distribu0on Expenses

Profit before Interest, Deprecia<on and Tax

Less: Deprecia0on

Profit before Interest

Less: Interest

Profit Before Tax

Less: Provision for Taxa0on

Profit ANer Tax

Equity (Shares of Rs. 10/-‐ Each) 100,000 1,900,000

Debt 1,900,000 100,000 Total Capital Employed 2,000,000 2,000,000 Sales 5,000,000 5,000,000 Less: Opera0ng Expenses 90% 4,500,000 4,500,000

Opera0ng Profit (PBIT) 10% 500,000 500,000

Less: Interest 15% 285,000 15,000

PBT 215,000 485,000

Tax 30% 64,500 145,500

PAT 150,500 339,500 Return on Equity 151% 18% Return on Capital Employed 25% 25%

Earnings Per Share (Rs.) 15.05 1.79

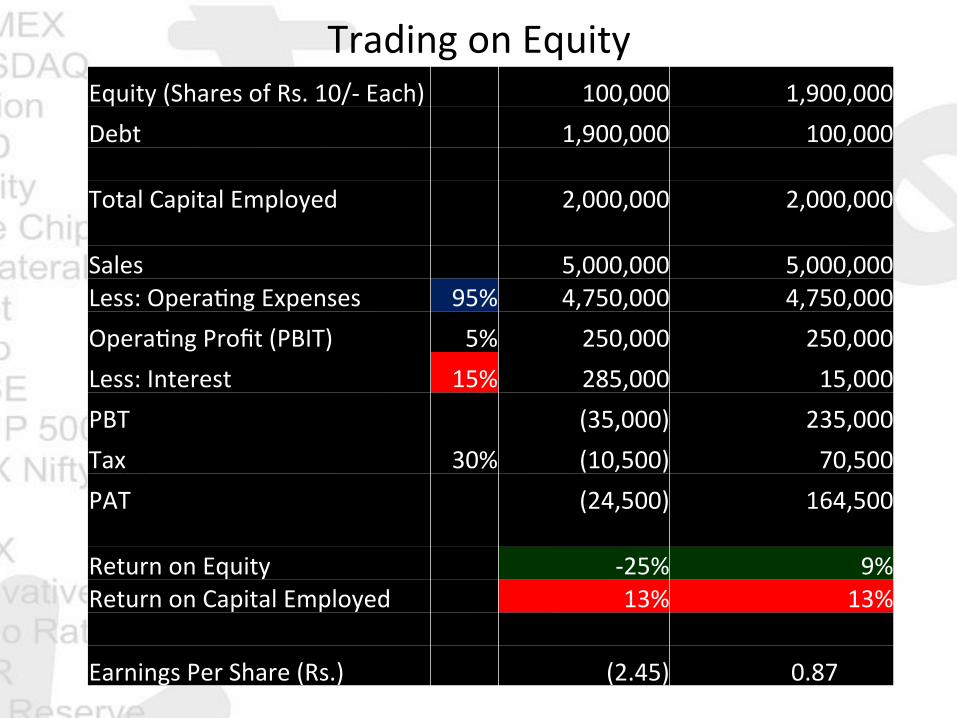

Trading on Equity

Trading on Equity Equity (Shares of Rs. 10/-‐ Each) 100,000 1,900,000 Debt 1,900,000 100,000 Total Capital Employed 2,000,000 2,000,000 Sales 5,000,000 5,000,000 Less: Opera0ng Expenses 94% 4,700,000 4,700,000 Opera0ng Profit (PBIT) 6% 300,000 300,000 Less: Interest 15% 285,000 15,000 PBT 15,000 285,000 Tax 30% 4,500 85,500 PAT 10,500 199,500 Return on Equity 11% 11% Return on Capital Employed 15% 15% Earnings Per Share (Rs.) 1.05 1.05

Trading on Equity Equity (Shares of Rs. 10/-‐ Each) 100,000 1,900,000 Debt 1,900,000 100,000 Total Capital Employed 2,000,000 2,000,000 Sales 5,000,000 5,000,000 Less: Opera0ng Expenses 95% 4,750,000 4,750,000 Opera0ng Profit (PBIT) 5% 250,000 250,000 Less: Interest 15% 285,000 15,000 PBT (35,000) 235,000 Tax 30% (10,500) 70,500 PAT (24,500) 164,500 Return on Equity -‐25% 9% Return on Capital Employed 13% 13% Earnings Per Share (Rs.) (2.45) 0.87