Embed Size (px)

DESCRIPTION

Citation preview

1

Financial Stability Review 23/10/2013

2 2

Key points

3

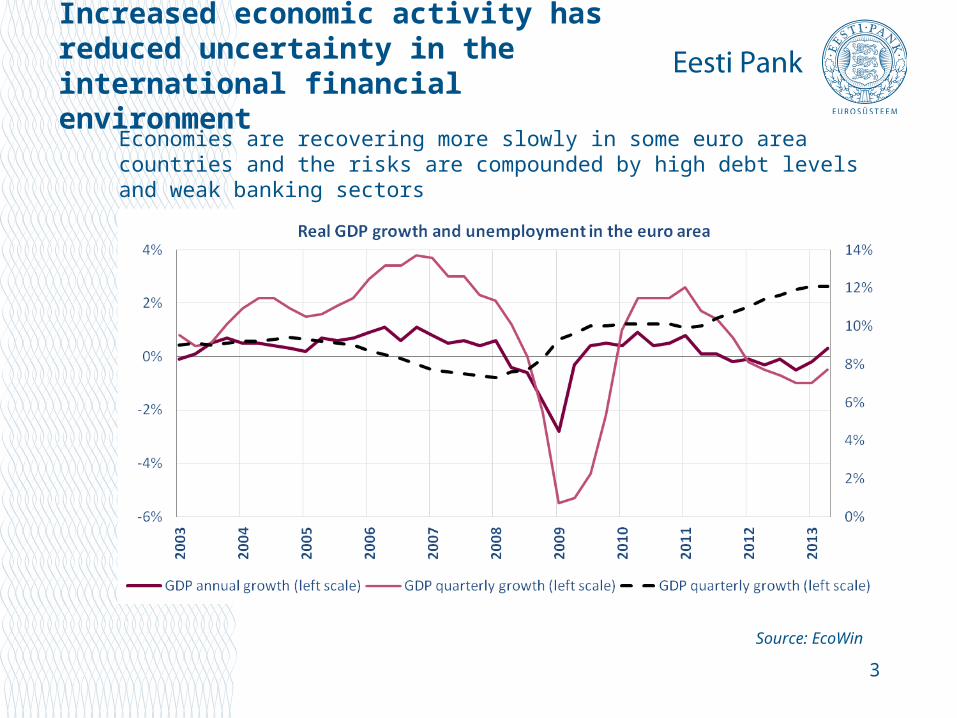

Increased economic activity has reduced uncertainty in the international financial environment

Economies are recovering more slowly in some euro area countries and the risks are compounded by high debt levels and weak banking sectors

Source: EcoWin

4

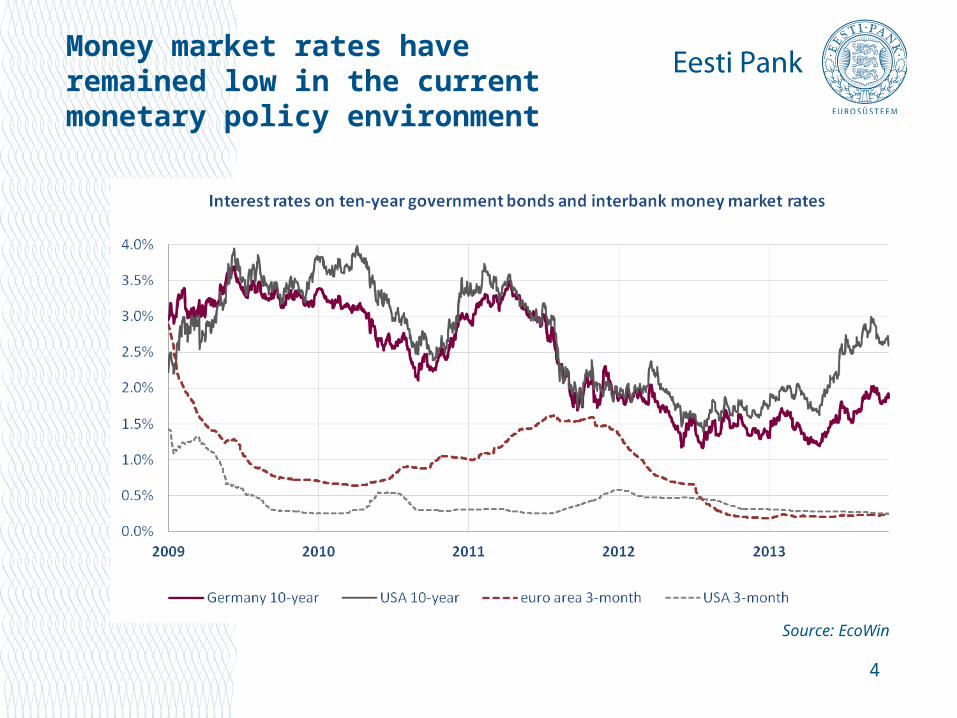

Money market rates have remained low in the current monetary policy environment

Source: EcoWin

5

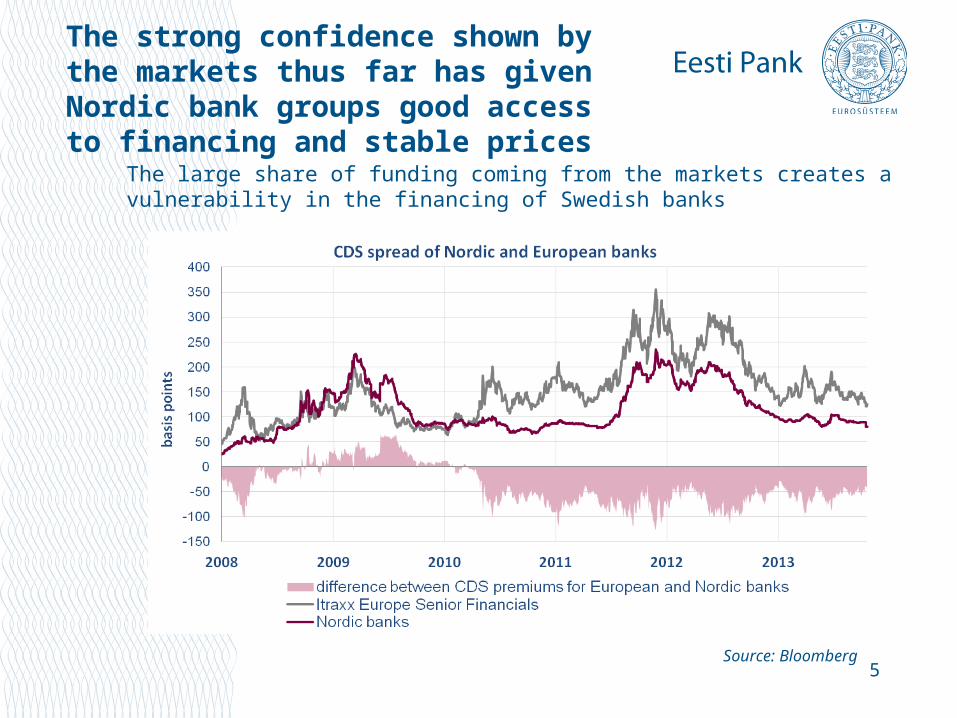

The strong confidence shown by the markets thus far has given Nordic bank groups good access to financing and stable prices

The large share of funding coming from the markets creates a vulnerability in the financing of Swedish banks

Source: Bloomberg

6

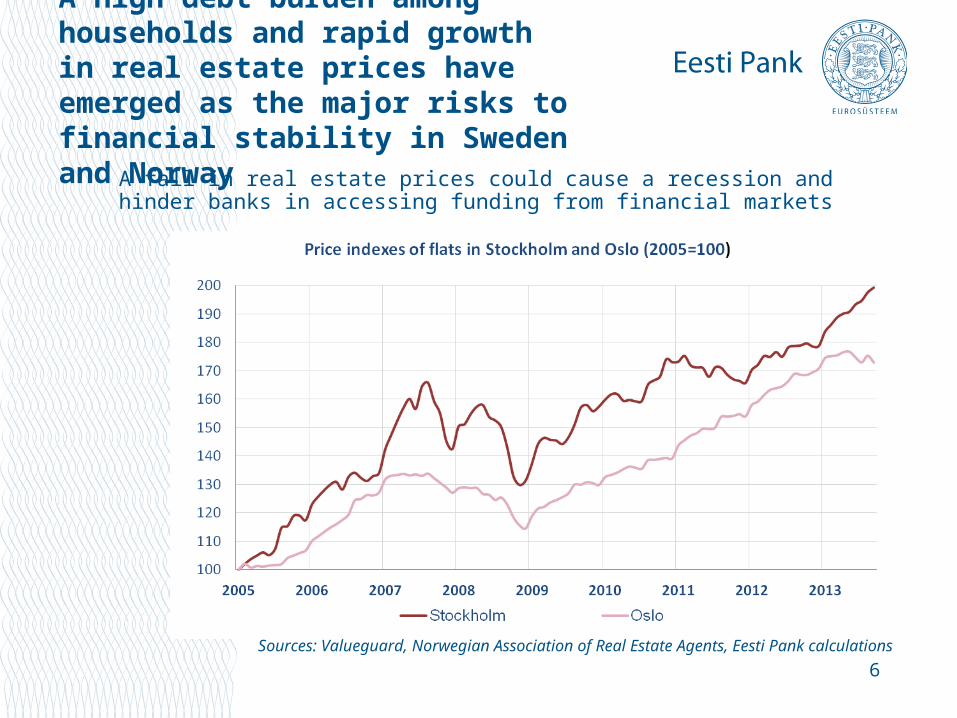

A high debt burden among households and rapid growth in real estate prices have emerged as the major risks to financial stability in Sweden and Norway

A fall in real estate prices could cause a recession and hinder banks in accessing funding from financial markets

Sources: Valueguard, Norwegian Association of Real Estate Agents, Eesti Pank calculations

7

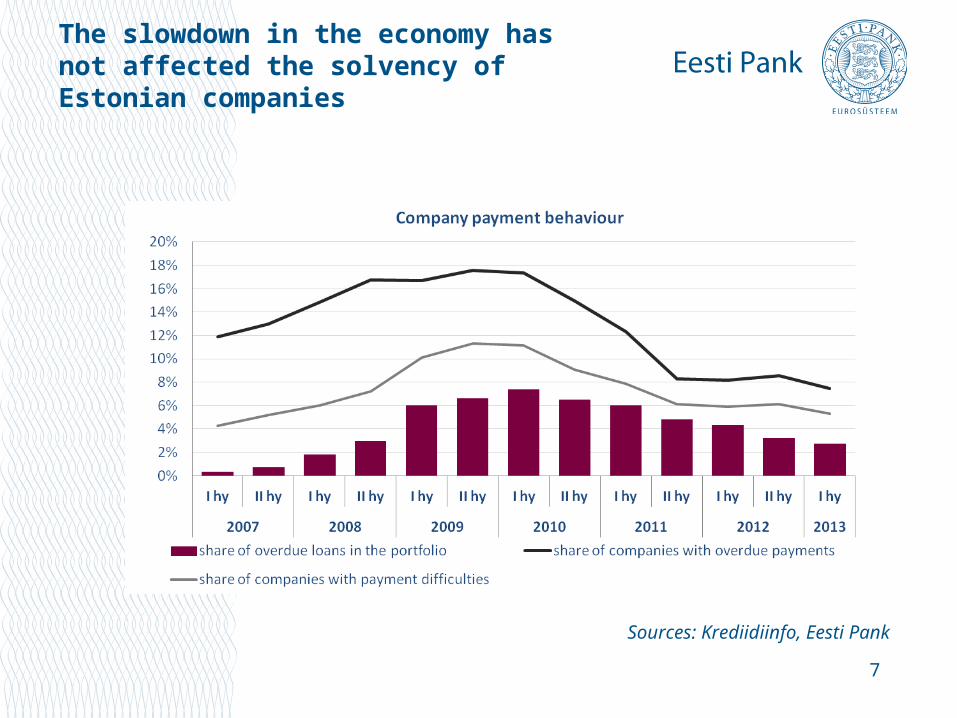

The slowdown in the economy has not affected the solvency of Estonian companies

Sources: Krediidiinfo, Eesti Pank

8

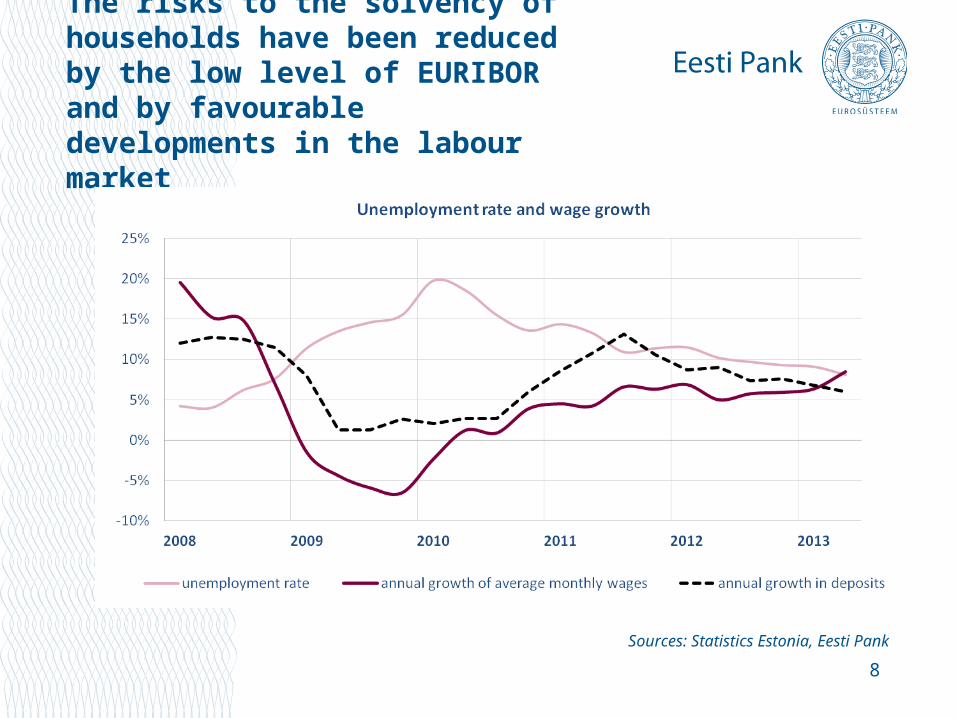

The risks to the solvency of households have been reduced by the low level of EURIBOR and by favourable developments in the labour market

Sources: Statistics Estonia, Eesti Pank

9

Real estate prices have risen faster than nominal GDP

Sources: Statistics Estonia, Estonian Land Board

10

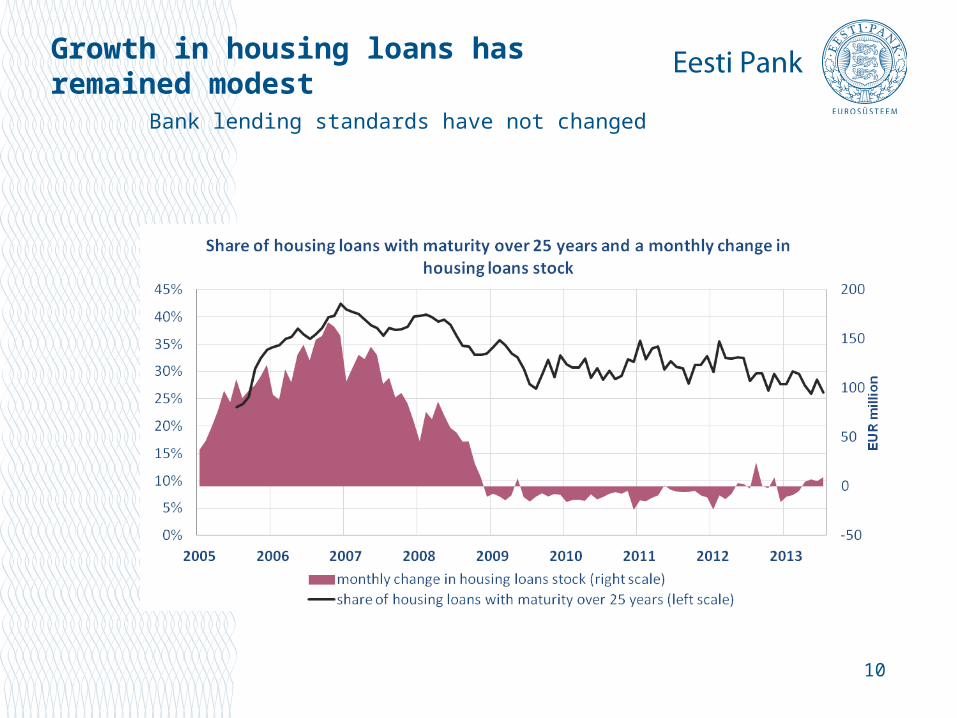

Growth in housing loans has remained modest

Bank lending standards have not changed

11

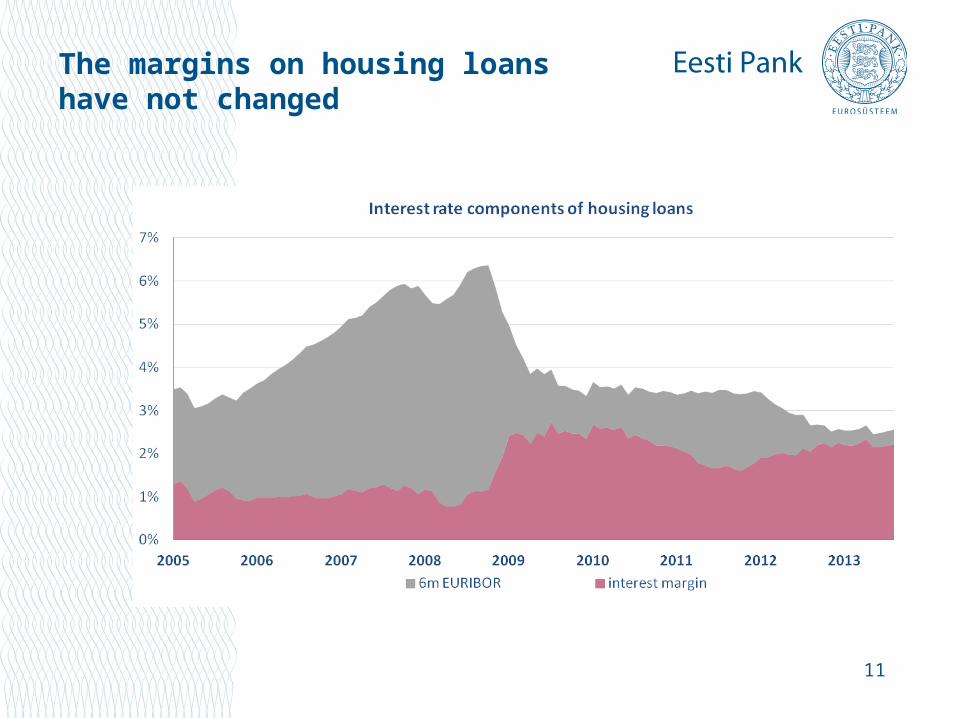

The margins on housing loans have not changed

12

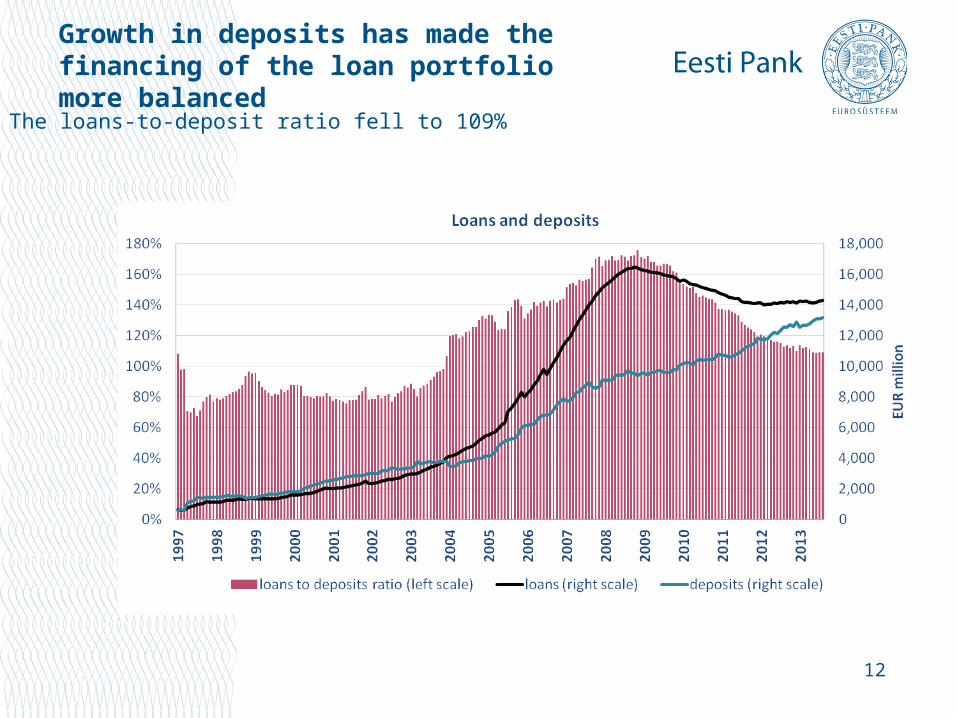

Growth in deposits has made the financing of the loan portfolio more balanced

The loans-to-deposit ratio fell to 109%

13

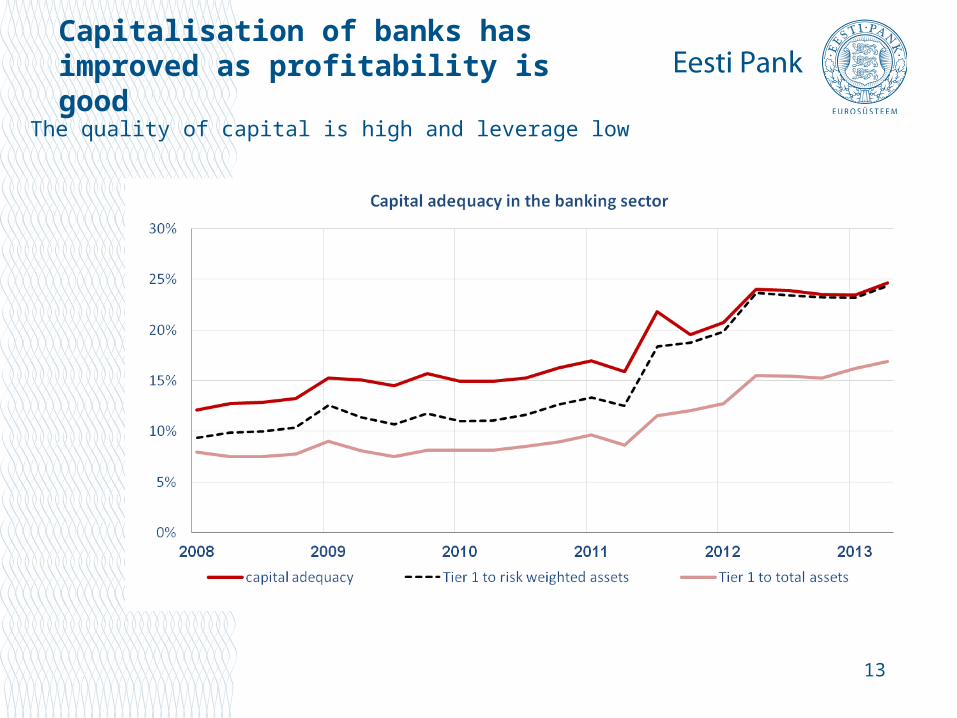

Capitalisation of banks has improved as profitability is good

The quality of capital is high and leverage low

14

Main risks and consequences

15

Most of the risks to financial stability in Estonia are small

16

The recession in the euro area weakened the asset quality of euro area banks significantly

17

The Nordic financial sector is considered secure but risks have increased in the real estate market

18

The banks operating in Estonia need to continue to be careful in issuing real estate loans

19

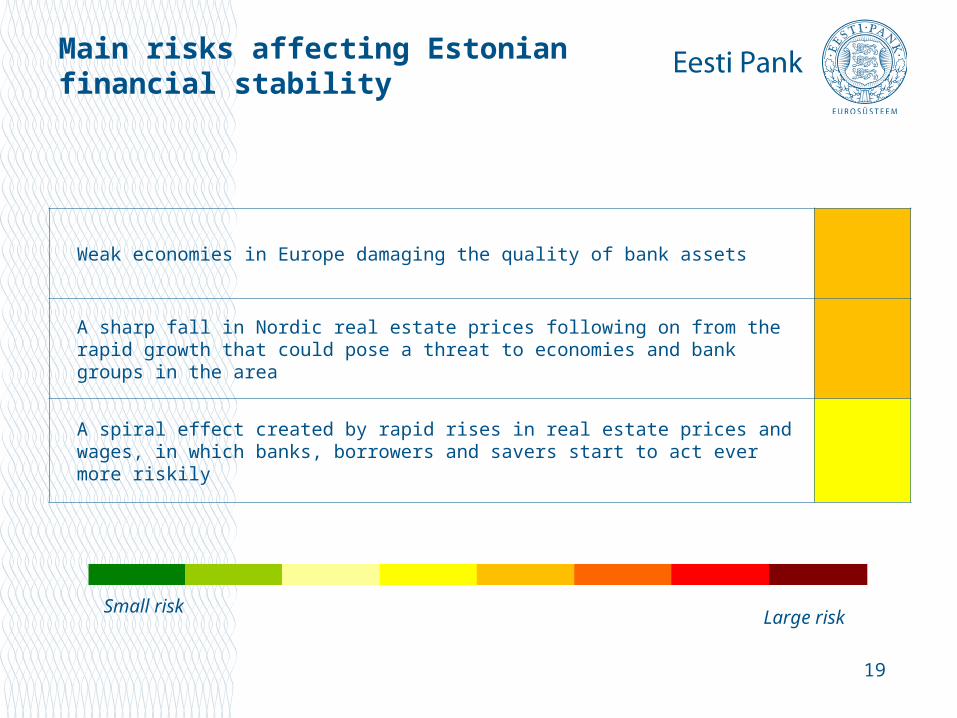

Main risks affecting Estonian financial stability

Small risk Large risk

Weak economies in Europe damaging the quality of bank assets

A sharp fall in Nordic real estate prices following on from the rapid growth that could pose a threat to economies and bank groups in the area

A spiral effect created by rapid rises in real estate prices and wages, in which banks, borrowers and savers start to act ever more riskily

20

For the Estonian banking sector to maintain its resilience it is important to keep the minimum capital requirement at 10%

21

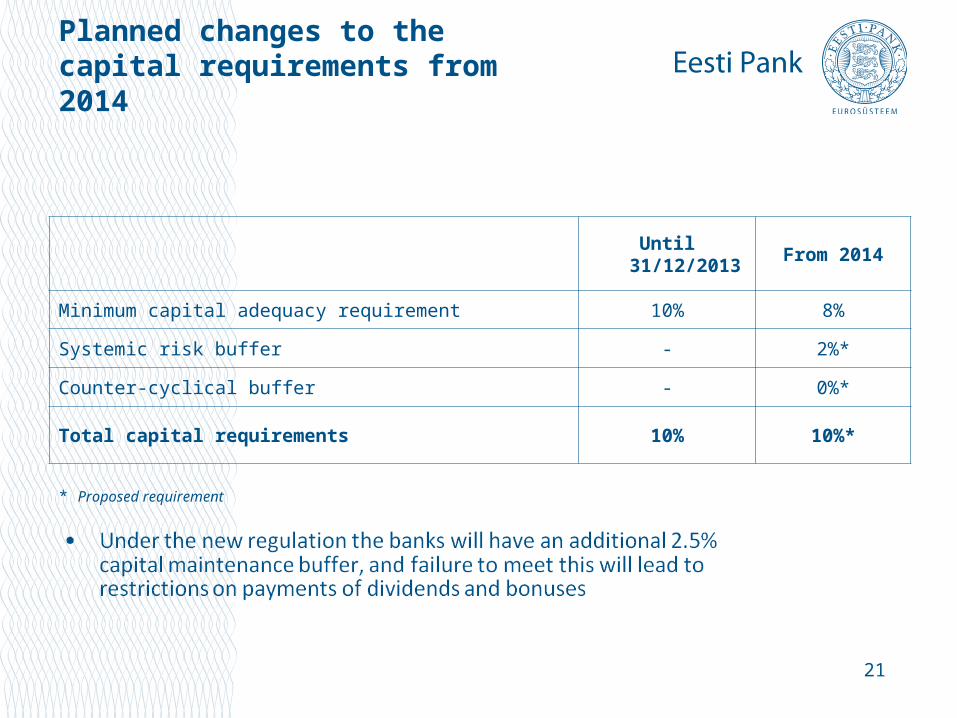

Planned changes to the capital requirements from 2014

Until 31/12/2013 From 2014

Minimum capital adequacy requirement 10% 8%

Systemic risk buffer - 2%*

Counter-cyclical buffer - 0%*

Total capital requirements 10% 10%*

* Proposed requirement