Embed Size (px)

DESCRIPTION

This document is for private circulation and information purposes only and should not be regarded as an investment, taxation or legal advice. Investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this publication and should under-stand that statements regarding future prospects may not be realized. In no circumstances it be used or considered as an offer to sale or a solicitation of any offer to buy or sell the securities mentioned in it. We and our affiliates, officers, directors and employees including persons involved in the preparation or issuance of this material may: (a) from time to time, have long or short positions in, and buy or sell the securities thereof, of company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) dis-cussed herein or act as an advisor or lender or borrower to such company or have other potential conflict of interest with respect to any recommendation and re-lated information and opinions. The information contained in this publication may have been taken from trade and statistical services and other sources, which we believe are reliable. We does not guarantee that such information is accurate or complete and it should not be relied upon as such. Any opinion ex-pressed reflects judgments at this date and are subject to change without notice. Caution: Risk of loss in trading & investment can be substantial. You should carefully consider whether trading & investment is appropriate for you in light of your experience, objectives, financial resources and other relevant circumstances.

Citation preview

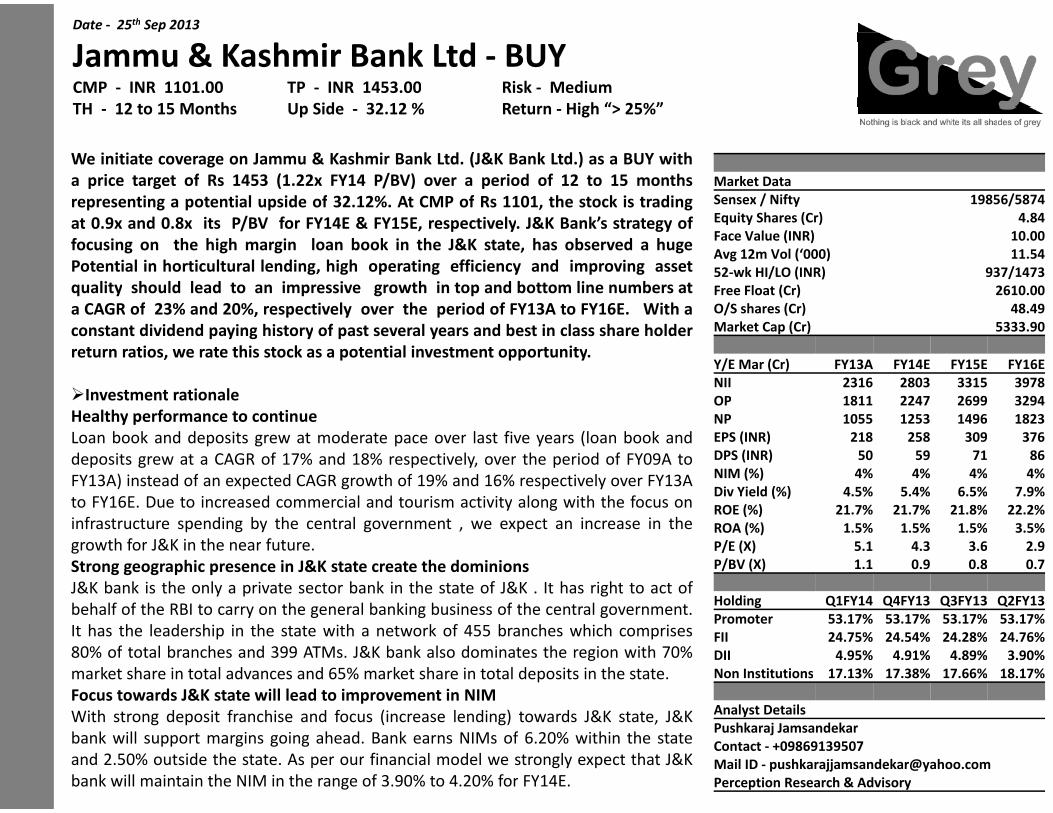

Date - 25th Sep 2013Date - 25th Sep 2013Date - 25 Sep 2013

Jammu & Kashmir Bank Ltd - BUYJammu & Kashmir Bank Ltd - BUYJammu & Kashmir Bank Ltd - BUYJammu & Kashmir Bank Ltd - BUYJammu & Kashmir Bank Ltd - BUYCMP - INR 1101.00 TP - INR 1453.00 Risk CMP - INR 1101.00 TP - INR 1453.00 Risk CMP - INR 1101.00 TP - INR 1453.00 Risk

TH - 12 to 15 Months Up Side - 32.12 % Return TH - 12 to 15 Months Up Side - 32.12 % Return TH - 12 to 15 Months Up Side - 32.12 % Return TH - 12 to 15 Months Up Side - 32.12 % Return

We initiate coverage on Jammu & Kashmir Bank Ltd. (J&K BankWe initiate coverage on Jammu & Kashmir Bank Ltd. (J&K BankWe initiate coverage on Jammu & Kashmir Bank Ltd. (J&K Bank

a price target of Rs 1453 (1.22x FY14 P/BV) over a perioda price target of Rs 1453 (1.22x FY14 P/BV) over a perioda price target of Rs 1453 (1.22x FY14 P/BV) over a period

representing a potential upside of 32.12%. At CMP of Rs 1101representing a potential upside of 32.12%. At CMP of Rs 1101representing a potential upside of 32.12%. At CMP of Rs 1101representing a potential upside of 32.12%. At CMP of Rs 1101

at 0.9x and 0.8x its P/BV for FY14E & FY15E, respectively. J&Kat 0.9x and 0.8x its P/BV for FY14E & FY15E, respectively. J&Kat 0.9x and 0.8x its P/BV for FY14E & FY15E, respectively. J&K

focusing on the high margin loan book in the J&K state,focusing on the high margin loan book in the J&K state,focusing on the high margin loan book in the J&K state,

Potential in horticultural lending, high operating efficiencyPotential in horticultural lending, high operating efficiencyPotential in horticultural lending, high operating efficiencyPotential in horticultural lending, high operating efficiency

quality should lead to an impressive growth in top and bottomquality should lead to an impressive growth in top and bottomquality should lead to an impressive growth in top and bottom

a CAGR of 23% and 20%, respectively over the period of FYa CAGR of 23% and 20%, respectively over the period of FYa CAGR of 23% and 20%, respectively over the period of FY

constant dividend paying history of past several years and bestconstant dividend paying history of past several years and bestconstant dividend paying history of past several years and best

return ratios, we rate this stock as a potential investment opportunity

constant dividend paying history of past several years and best

return ratios, we rate this stock as a potential investment opportunityreturn ratios, we rate this stock as a potential investment opportunityreturn ratios, we rate this stock as a potential investment opportunity

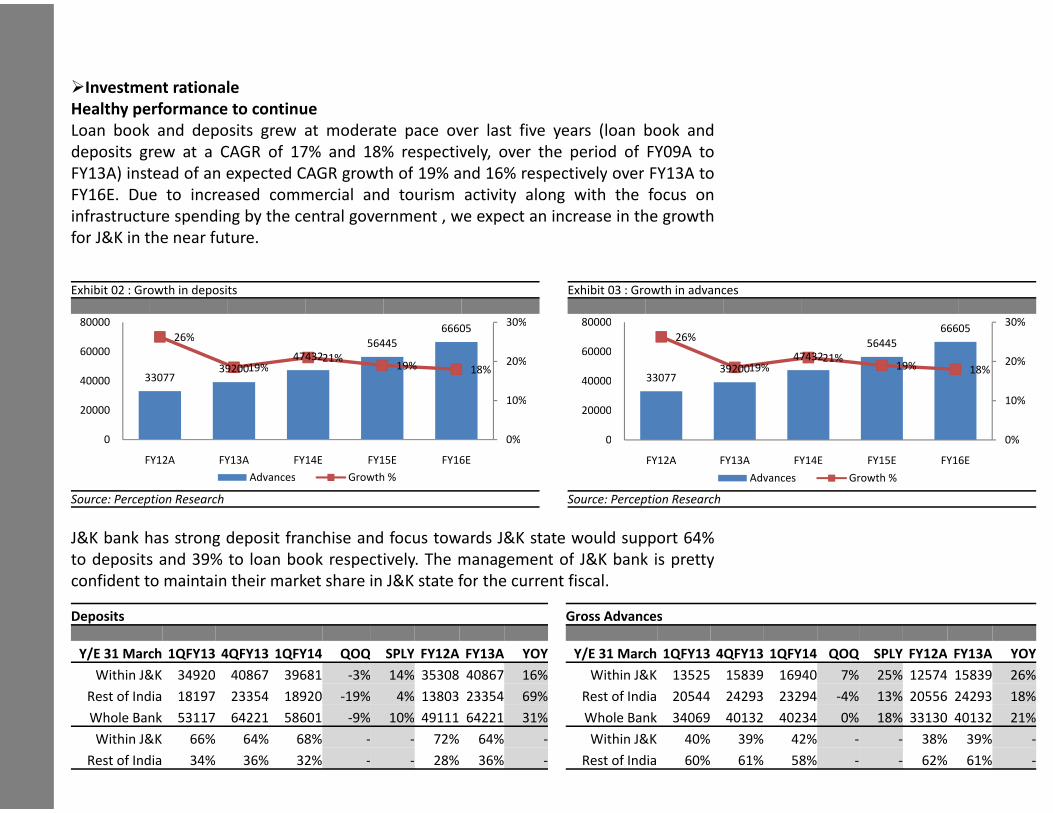

�Investment rationale�Investment rationale�Investment rationale

Healthy performance to continueHealthy performance to continueHealthy performance to continueHealthy performance to continue

Loan book and deposits grew at moderate pace over last fiveLoan book and deposits grew at moderate pace over last fiveLoan book and deposits grew at moderate pace over last five

deposits grew at a CAGR of 17% and 18% respectively, over thedeposits grew at a CAGR of 17% and 18% respectively, over thedeposits grew at a CAGR of 17% and 18% respectively, over the

FY13A) instead of an expected CAGR growth of 19% and 16% respectivelyFY13A) instead of an expected CAGR growth of 19% and 16% respectivelyFY13A) instead of an expected CAGR growth of 19% and 16% respectivelyFY13A) instead of an expected CAGR growth of 19% and 16% respectively

to FY16E. Due to increased commercial and tourism activity alongto FY16E. Due to increased commercial and tourism activity alongto FY16E. Due to increased commercial and tourism activity along

infrastructure spending by the central government , we expectinfrastructure spending by the central government , we expectinfrastructure spending by the central government , we expect

growth for J&K in the near future.growth for J&K in the near future.growth for J&K in the near future.

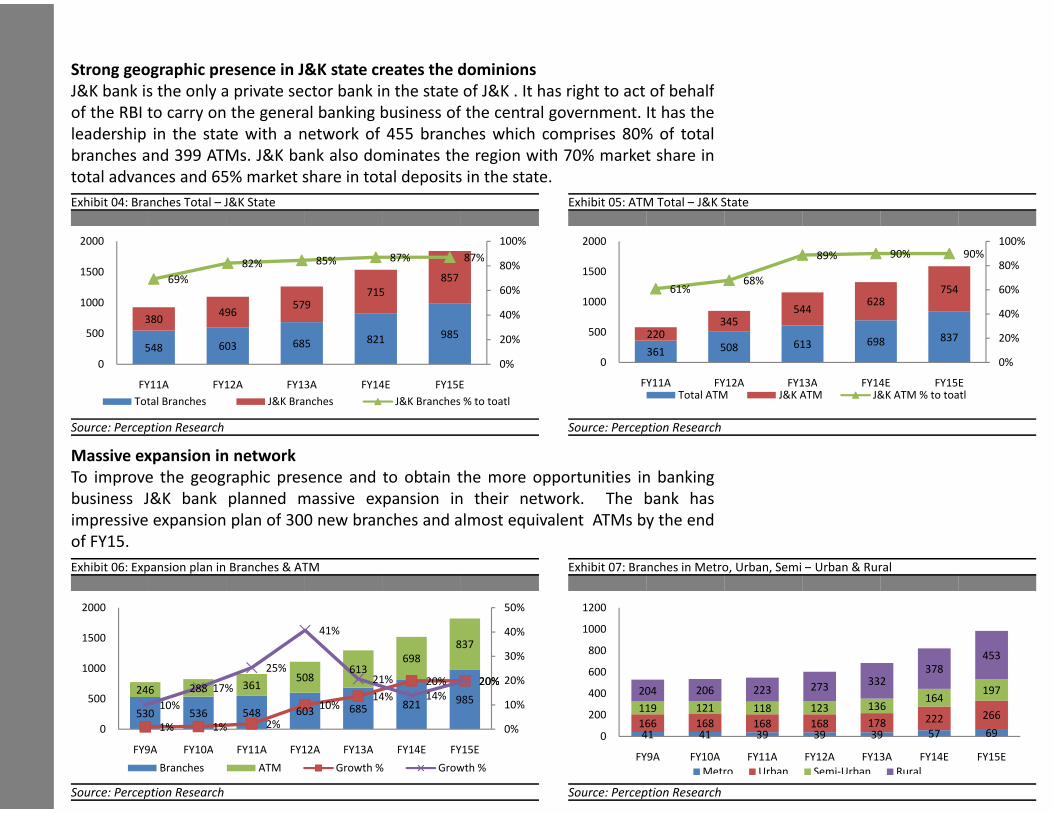

Strong geographic presence in J&K state create the dominionsStrong geographic presence in J&K state create the dominionsStrong geographic presence in J&K state create the dominionsStrong geographic presence in J&K state create the dominions

J&K bank is the only a private sector bank in the state of J&KJ&K bank is the only a private sector bank in the state of J&KJ&K bank is the only a private sector bank in the state of J&K

behalf of the RBI to carry on the general banking business of thebehalf of the RBI to carry on the general banking business of thebehalf of the RBI to carry on the general banking business of the

It has the leadership in the state with a network of 455 branchesIt has the leadership in the state with a network of 455 branchesIt has the leadership in the state with a network of 455 branchesIt has the leadership in the state with a network of 455 branches

80% of total branches and 399 ATMs. J&K bank also dominates80% of total branches and 399 ATMs. J&K bank also dominates80% of total branches and 399 ATMs. J&K bank also dominates

market share in total advances and 65% market share in total depositsmarket share in total advances and 65% market share in total depositsmarket share in total advances and 65% market share in total deposits

Focus towards J&K state will lead to improvement in NIMFocus towards J&K state will lead to improvement in NIMFocus towards J&K state will lead to improvement in NIMFocus towards J&K state will lead to improvement in NIM

With strong deposit franchise and focus (increase lending) towardsWith strong deposit franchise and focus (increase lending) towardsWith strong deposit franchise and focus (increase lending) towards

bank will support margins going ahead. Bank earns NIMs of 6bank will support margins going ahead. Bank earns NIMs of 6bank will support margins going ahead. Bank earns NIMs of 6

and 2.50% outside the state. As per our financial model we stronglyand 2.50% outside the state. As per our financial model we stronglyand 2.50% outside the state. As per our financial model we strongly

bank will maintain the NIM in the range of 3.90% to 4.20% for FYbank will maintain the NIM in the range of 3.90% to 4.20% for FYbank will maintain the NIM in the range of 3.90% to 4.20% for FYbank will maintain the NIM in the range of 3.90% to 4.20% for FY

BUYBUYBUYBUYBUYRisk - MediumRisk - MediumRisk - Medium

Return - High “> 25%” Return - High “> 25%” Return - High “> 25%” Return - High “> 25%”

Bank Ltd.) as a BUY withBank Ltd.) as a BUY withBank Ltd.) as a BUY with

period of 12 to 15 months Market Dataperiod of 12 to 15 months Market Dataperiod of 12 to 15 months

1101, the stock is trading

Market Data

Sensex / Nifty 19856/58741101, the stock is trading Sensex / Nifty 19856/58741101, the stock is trading Sensex / Nifty 19856/5874

Equity Shares (Cr) 4.841101, the stock is trading

J&K Bank’s strategy of Equity Shares (Cr) 4.84J&K Bank’s strategy of Equity Shares (Cr) 4.84

Face Value (INR) 10.00J&K Bank’s strategy of

has observed a hugeFace Value (INR) 10.00

has observed a hugeFace Value (INR) 10.00

Avg 12m Vol (‘000) 11.54has observed a huge

and improving assetAvg 12m Vol (‘000) 11.54

and improving assetAvg 12m Vol (‘000) 11.54

52-wk HI/LO (INR) 937/1473and improving asset 52-wk HI/LO (INR) 937/1473and improving asset

bottom line numbers at52-wk HI/LO (INR) 937/1473

Free Float (Cr) 2610.00bottom line numbers at Free Float (Cr) 2610.00bottom line numbers at

FY13A to FY16E. With aFree Float (Cr) 2610.00

O/S shares (Cr) 48.49FY13A to FY16E. With a O/S shares (Cr) 48.49FY13A to FY16E. With a

best in class share holder

O/S shares (Cr) 48.49

Market Cap (Cr) 5333.90best in class share holder Market Cap (Cr) 5333.90best in class share holder

opportunity.

Market Cap (Cr) 5333.90best in class share holder

opportunity.opportunity.Y/E Mar (Cr) FY13A FY14E FY15E FY16E

opportunity.Y/E Mar (Cr) FY13A FY14E FY15E FY16EY/E Mar (Cr) FY13A FY14E FY15E FY16E

NII 2316 2803 3315 3978NII 2316 2803 3315 3978NII 2316 2803 3315 3978

OP 1811 2247 2699 3294OP 1811 2247 2699 3294OP 1811 2247 2699 3294

NP 1055 1253 1496 1823NP 1055 1253 1496 1823

five years (loan book andNP 1055 1253 1496 1823

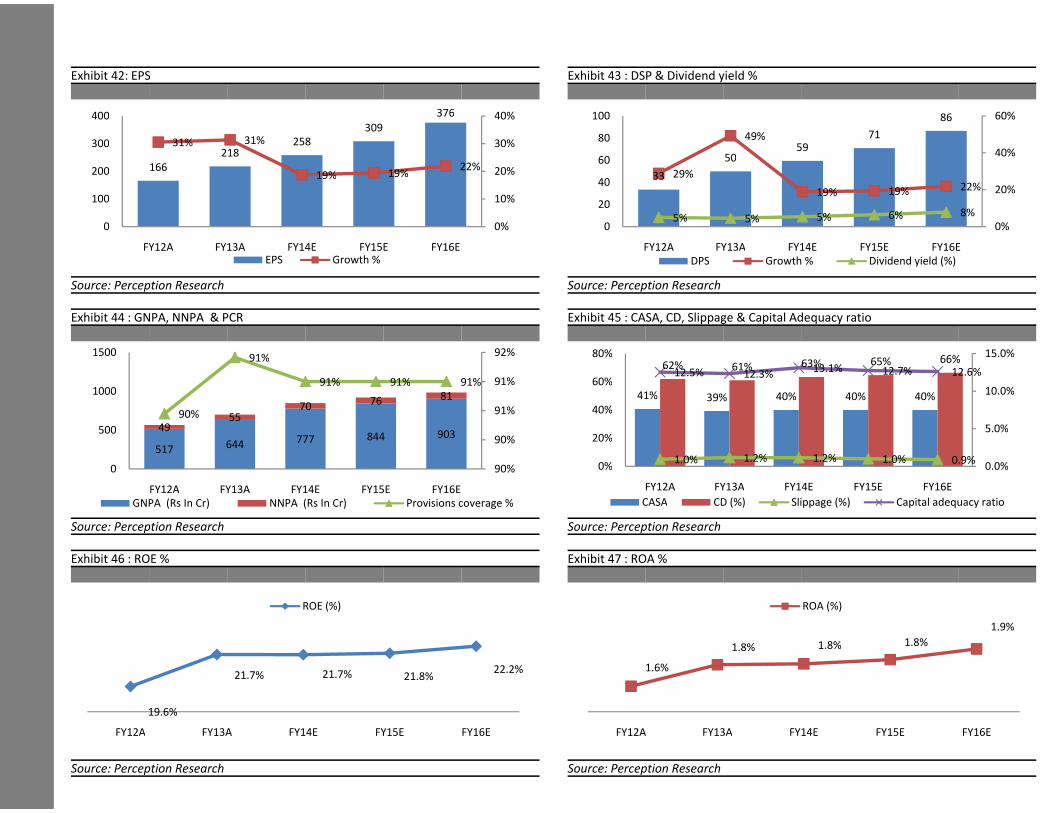

EPS (INR) 218 258 309 376five years (loan book and EPS (INR) 218 258 309 376five years (loan book and

the period of FY09A to

EPS (INR) 218 258 309 376

DPS (INR) 50 59 71 86the period of FY09A to DPS (INR) 50 59 71 86the period of FY09A to

respectively over FY13A

DPS (INR) 50 59 71 86

NIM (%) 4% 4% 4% 4%respectively over FY13A

NIM (%) 4% 4% 4% 4%respectively over FY13A

NIM (%) 4% 4% 4% 4%

Div Yield (%) 4.5% 5.4% 6.5% 7.9%respectively over FY13A

along with the focus onDiv Yield (%) 4.5% 5.4% 6.5% 7.9%

along with the focus onDiv Yield (%) 4.5% 5.4% 6.5% 7.9%

ROE (%) 21.7% 21.7% 21.8% 22.2%along with the focus on

expect an increase in theROE (%) 21.7% 21.7% 21.8% 22.2%

expect an increase in theROE (%) 21.7% 21.7% 21.8% 22.2%

ROA (%) 1.5% 1.5% 1.5% 3.5%expect an increase in the ROA (%) 1.5% 1.5% 1.5% 3.5%

P/E (X) 5.1 4.3 3.6 2.9P/E (X) 5.1 4.3 3.6 2.9

dominions

P/E (X) 5.1 4.3 3.6 2.9

P/BV (X) 1.1 0.9 0.8 0.7dominions P/BV (X) 1.1 0.9 0.8 0.7dominions P/BV (X) 1.1 0.9 0.8 0.7dominions

J&K . It has right to act ofJ&K . It has right to act ofHolding Q1FY14 Q4FY13 Q3FY13 Q2FY13

J&K . It has right to act of

the central government.Holding Q1FY14 Q4FY13 Q3FY13 Q2FY13

the central government.Holding Q1FY14 Q4FY13 Q3FY13 Q2FY13

Promoter 53.17% 53.17% 53.17% 53.17%the central government.

branches which comprisesPromoter 53.17% 53.17% 53.17% 53.17%

branches which comprisesPromoter 53.17% 53.17% 53.17% 53.17%

FII 24.75% 24.54% 24.28% 24.76%branches which comprises FII 24.75% 24.54% 24.28% 24.76%branches which comprises

dominates the region with 70%FII 24.75% 24.54% 24.28% 24.76%

DII 4.95% 4.91% 4.89% 3.90%dominates the region with 70% DII 4.95% 4.91% 4.89% 3.90%dominates the region with 70%

deposits in the state.DII 4.95% 4.91% 4.89% 3.90%

Non Institutions 17.13% 17.38% 17.66% 18.17%deposits in the state. Non Institutions 17.13% 17.38% 17.66% 18.17%deposits in the state. Non Institutions 17.13% 17.38% 17.66% 18.17%

Analyst Detailstowards J&K state, J&K Analyst Detailstowards J&K state, J&K Analyst Details

Pushkaraj Jamsandekartowards J&K state, J&K

6.20% within the statePushkaraj Jamsandekar

6.20% within the statePushkaraj Jamsandekar

Contact - +098691395076.20% within the state

strongly expect that J&KContact - +09869139507

strongly expect that J&KContact - +09869139507

Mail ID - [email protected] expect that J&K

FY14E.Mail ID - [email protected]

FY14E.Mail ID - [email protected]

Perception Research & AdvisoryFY14E. Perception Research & AdvisoryFY14E. Perception Research & Advisory

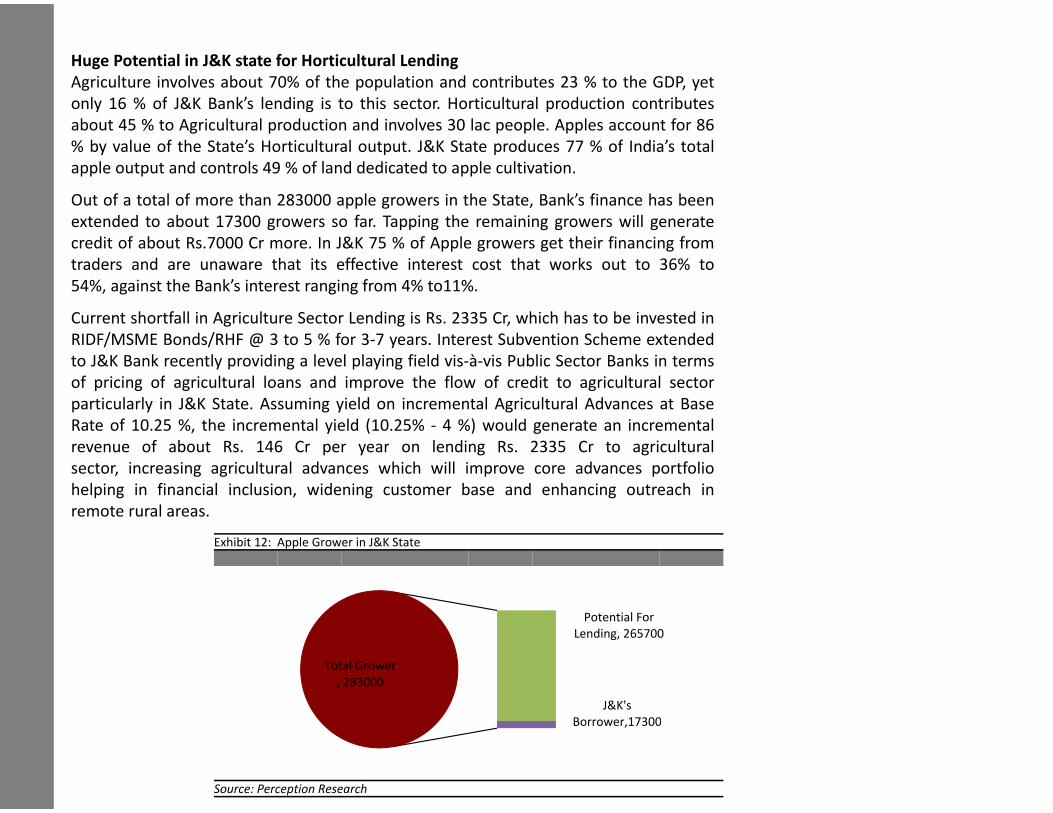

Huge Potential in J&K state for Horticultural LendingHuge Potential in J&K state for Horticultural LendingHuge Potential in J&K state for Horticultural Lending

J&K State produces 77 % of India’s total apple output andJ&K State produces 77 % of India’s total apple output andJ&K State produces 77 % of India’s total apple output andJ&K State produces 77 % of India’s total apple output and

dedicated to apple cultivation. Out of a total of more than 283000dedicated to apple cultivation. Out of a total of more than 283000dedicated to apple cultivation. Out of a total of more than 283000

State, Bank’s finance has been extended to about 17300 growersState, Bank’s finance has been extended to about 17300 growersState, Bank’s finance has been extended to about 17300 growers

remaining growers will generate credit of about Rs.7000 Cr moreremaining growers will generate credit of about Rs.7000 Cr moreremaining growers will generate credit of about Rs.7000 Cr moreremaining growers will generate credit of about Rs.7000 Cr more

Apple growers get their financing from traders and are unawareApple growers get their financing from traders and are unawareApple growers get their financing from traders and are unaware

cost works out to 36% to 54%, against the Bank’s interest rangingcost works out to 36% to 54%, against the Bank’s interest rangingcost works out to 36% to 54%, against the Bank’s interest ranging

Current shortfall in Agriculture Sector Lending is Rs. 2335Current shortfall in Agriculture Sector Lending is Rs. 2335Current shortfall in Agriculture Sector Lending is Rs. 2335Current shortfall in Agriculture Sector Lending is Rs. 2335

incremental Agricultural Advances at Base Rate of 10.25 %incremental Agricultural Advances at Base Rate of 10.25 %incremental Agricultural Advances at Base Rate of 10.25 %

(10.25% –4%) would generate an incremental revenue of about(10.25% –4%) would generate an incremental revenue of about(10.25% –4%) would generate an incremental revenue of about

lending Rs. 2335 Cr to agricultural sector.lending Rs. 2335 Cr to agricultural sector.lending Rs. 2335 Cr to agricultural sector.

Massive expansion in networkMassive expansion in networkMassive expansion in networkMassive expansion in network

To improve the geographic presence and to obtain the moreTo improve the geographic presence and to obtain the moreTo improve the geographic presence and to obtain the more

business J&K bank planned massive expansion in their networkbusiness J&K bank planned massive expansion in their networkbusiness J&K bank planned massive expansion in their network

impressive expansion plan of 300 new branches and almost equivalentimpressive expansion plan of 300 new branches and almost equivalentimpressive expansion plan of 300 new branches and almost equivalentimpressive expansion plan of 300 new branches and almost equivalent

of FY15.of FY15.of FY15.

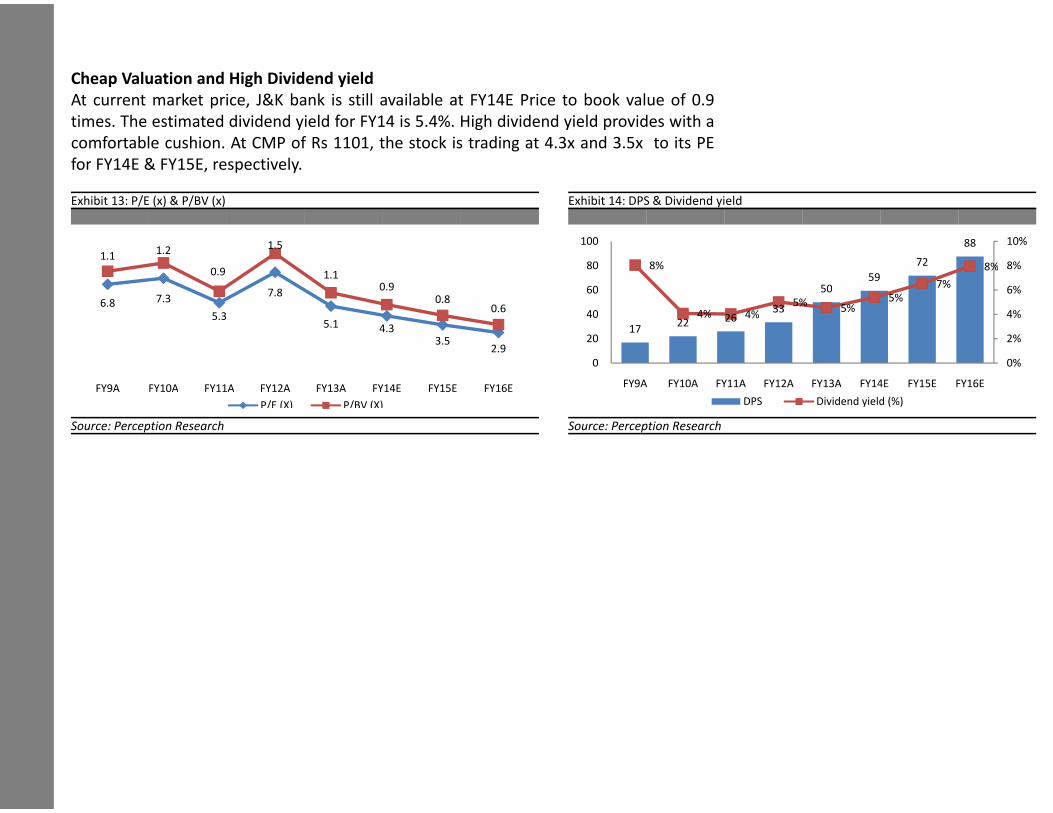

Cheap Valuation and High Dividend yieldCheap Valuation and High Dividend yieldCheap Valuation and High Dividend yield

At current market price, J&K bank is still available at FY14E PriceAt current market price, J&K bank is still available at FY14E PriceAt current market price, J&K bank is still available at FY14E Price

times. The estimated dividend yield for FY14 is 5.4%. High dividend

At current market price, J&K bank is still available at FY14E Price

times. The estimated dividend yield for FY14 is 5.4%. High dividendtimes. The estimated dividend yield for FY14 is 5.4%. High dividendtimes. The estimated dividend yield for FY14 is 5.4%. High dividend

comfortable cushion. At CMP of Rs 1101, the stock is trading atcomfortable cushion. At CMP of Rs 1101, the stock is trading atcomfortable cushion. At CMP of Rs 1101, the stock is trading at

for FY14E & FY15E, respectively.for FY14E & FY15E, respectively.for FY14E & FY15E, respectively.

and controls 49 % of landand controls 49 % of landand controls 49 % of landand controls 49 % of land

283000 apple growers in the283000 apple growers in the283000 apple growers in the

growers so far. Tapping thegrowers so far. Tapping thegrowers so far. Tapping the

more. In J&K state’s 75% ofmore. In J&K state’s 75% ofmore. In J&K state’s 75% ofmore. In J&K state’s 75% of

unaware that its effective interestunaware that its effective interestunaware that its effective interest

ranging from 4% to 11%.ranging from 4% to 11%.ranging from 4% to 11%.

2335 cr. Assuming yield on2335 cr. Assuming yield on2335 cr. Assuming yield on2335 cr. Assuming yield on

%, the incremental yield%, the incremental yield%, the incremental yield

about Rs. 146 Cr per year onabout Rs. 146 Cr per year onabout Rs. 146 Cr per year on

opportunities in bankingopportunities in bankingopportunities in banking

network. The bank hasnetwork. The bank hasnetwork. The bank has

equivalent ATMs by the endequivalent ATMs by the endequivalent ATMs by the endequivalent ATMs by the end

Price to book value of 0.9Price to book value of 0.9Price to book value of 0.9

dividend yield provides with a

Price to book value of 0.9

dividend yield provides with adividend yield provides with adividend yield provides with a

at 4.3x and 3.5x to its PEat 4.3x and 3.5x to its PEat 4.3x and 3.5x to its PE

�Concerns�Concerns�Concerns

Change in political environmentChange in political environmentChange in political environmentChange in political environment

Instable geopolitical uncertainty in the J&K State would hamperInstable geopolitical uncertainty in the J&K State would hamperInstable geopolitical uncertainty in the J&K State would hamper

sentiment.sentiment.sentiment.

Rupee depreciationRupee depreciationRupee depreciationRupee depreciation

The rupee has depreciated about 25 % this year and touchedThe rupee has depreciated about 25 % this year and touchedThe rupee has depreciated about 25 % this year and touched

lower rupee value is the major concern for Indian economiclower rupee value is the major concern for Indian economiclower rupee value is the major concern for Indian economic

adverse impact on Indian banking sector.adverse impact on Indian banking sector.adverse impact on Indian banking sector.adverse impact on Indian banking sector.

Higher inflation rateHigher inflation rateHigher inflation rate

Higher inflation rate is another major concern in India. Bank lendingHigher inflation rate is another major concern in India. Bank lendingHigher inflation rate is another major concern in India. Bank lending

an inverse relation, observing the past trend it was absolutelyan inverse relation, observing the past trend it was absolutelyan inverse relation, observing the past trend it was absolutely

inflation rate moves up it starts pulling down the bank lending rateinflation rate moves up it starts pulling down the bank lending rateinflation rate moves up it starts pulling down the bank lending rateinflation rate moves up it starts pulling down the bank lending rate

Negative investor sentimentNegative investor sentimentNegative investor sentiment

Higher inflation rate, unexpected rupee depreciation, lowerHigher inflation rate, unexpected rupee depreciation, lowerHigher inflation rate, unexpected rupee depreciation, lower

uncertainty in political environment may hamper investor (FII &uncertainty in political environment may hamper investor (FII &uncertainty in political environment may hamper investor (FII &uncertainty in political environment may hamper investor (FII &

Low GDP growth or below expectationLow GDP growth or below expectationLow GDP growth or below expectation

For the current fiscal, India is targeting 4 to 5 percent GDP growthFor the current fiscal, India is targeting 4 to 5 percent GDP growthFor the current fiscal, India is targeting 4 to 5 percent GDP growth

negatively impact on Indian banking sector.negatively impact on Indian banking sector.negatively impact on Indian banking sector.negatively impact on Indian banking sector.

hamper the overall businesshamper the overall businesshamper the overall business

touched a record low of 68.80.touched a record low of 68.80.touched a record low of 68.80.

economic growth, along with aneconomic growth, along with aneconomic growth, along with an

lending and inflation havelending and inflation havelending and inflation have

absolutely clear that once theabsolutely clear that once theabsolutely clear that once the

rate.rate.rate.rate.

lower capital expenditure andlower capital expenditure andlower capital expenditure and

& DII) sentiment.& DII) sentiment.& DII) sentiment.& DII) sentiment.

growth. Lower in GDP maygrowth. Lower in GDP maygrowth. Lower in GDP may

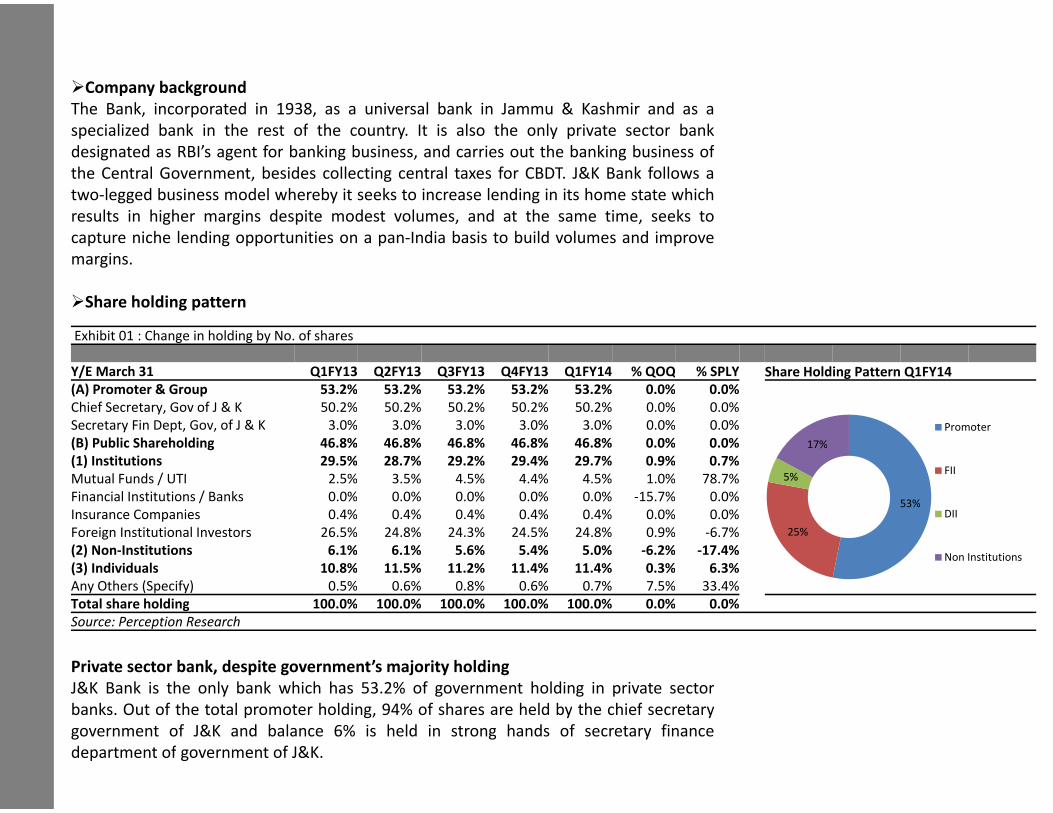

�Company background�Company background�Company background

The Bank, incorporated in 1938, as a universal bank in JammuThe Bank, incorporated in 1938, as a universal bank in JammuThe Bank, incorporated in 1938, as a universal bank in JammuThe Bank, incorporated in 1938, as a universal bank in Jammu

specialized bank in the rest of the country. It is also thespecialized bank in the rest of the country. It is also thespecialized bank in the rest of the country. It is also the

designated as RBI’s agent for banking business, and carries outdesignated as RBI’s agent for banking business, and carries outdesignated as RBI’s agent for banking business, and carries out

the Central Government, besides collecting central taxes for CBDTthe Central Government, besides collecting central taxes for CBDTthe Central Government, besides collecting central taxes for CBDTthe Central Government, besides collecting central taxes for CBDT

two-legged business model whereby it seeks to increase lendingtwo-legged business model whereby it seeks to increase lendingtwo-legged business model whereby it seeks to increase lending

results in higher margins despite modest volumes, and at theresults in higher margins despite modest volumes, and at theresults in higher margins despite modest volumes, and at the

capture niche lending opportunities on a pan-India basis to buildcapture niche lending opportunities on a pan-India basis to buildcapture niche lending opportunities on a pan-India basis to buildcapture niche lending opportunities on a pan-India basis to build

margins.margins.margins.

�Share holding pattern�Share holding pattern�Share holding pattern

Exhibit 01 : Change in holding by No. of sharesExhibit 01 : Change in holding by No. of sharesExhibit 01 : Change in holding by No. of shares

Y/E March 31 Q1FY13 Q2FY13 Q3FY13 Q4FY13Y/E March 31 Q1FY13 Q2FY13 Q3FY13 Q4FY13Y/E March 31 Q1FY13 Q2FY13 Q3FY13 Q4FY13

(A) Promoter & Group 53.2% 53.2% 53.2% 53.2%(A) Promoter & Group 53.2% 53.2% 53.2% 53.2%(A) Promoter & Group 53.2% 53.2% 53.2% 53.2%

Chief Secretary, Gov of J & K 50.2% 50.2% 50.2% 50.2%Chief Secretary, Gov of J & K 50.2% 50.2% 50.2% 50.2%Chief Secretary, Gov of J & K 50.2% 50.2% 50.2% 50.2%

Secretary Fin Dept, Gov, of J & K 3.0% 3.0% 3.0% 3.0%Secretary Fin Dept, Gov, of J & K 3.0% 3.0% 3.0% 3.0%

(B) Public Shareholding 46.8% 46.8% 46.8% 46.8%(B) Public Shareholding 46.8% 46.8% 46.8% 46.8%(B) Public Shareholding 46.8% 46.8% 46.8% 46.8%

(1) Institutions 29.5% 28.7% 29.2% 29.4%(1) Institutions 29.5% 28.7% 29.2% 29.4%(1) Institutions 29.5% 28.7% 29.2% 29.4%

Mutual Funds / UTI 2.5% 3.5% 4.5% 4.4%Mutual Funds / UTI 2.5% 3.5% 4.5% 4.4%Mutual Funds / UTI 2.5% 3.5% 4.5% 4.4%

Financial Institutions / Banks 0.0% 0.0% 0.0% 0.0%Financial Institutions / Banks 0.0% 0.0% 0.0% 0.0%Financial Institutions / Banks 0.0% 0.0% 0.0% 0.0%

Insurance Companies 0.4% 0.4% 0.4% 0.4%Insurance Companies 0.4% 0.4% 0.4% 0.4%Insurance Companies 0.4% 0.4% 0.4% 0.4%

Foreign Institutional Investors 26.5% 24.8% 24.3% 24.5%Foreign Institutional Investors 26.5% 24.8% 24.3% 24.5%Foreign Institutional Investors 26.5% 24.8% 24.3% 24.5%

(2) Non-Institutions 6.1% 6.1% 5.6% 5.4%(2) Non-Institutions 6.1% 6.1% 5.6% 5.4%(2) Non-Institutions 6.1% 6.1% 5.6% 5.4%

(3) Individuals 10.8% 11.5% 11.2% 11.4%(3) Individuals 10.8% 11.5% 11.2% 11.4%(3) Individuals 10.8% 11.5% 11.2% 11.4%

Any Others (Specify) 0.5% 0.6% 0.8% 0.6%Any Others (Specify) 0.5% 0.6% 0.8% 0.6%Any Others (Specify) 0.5% 0.6% 0.8% 0.6%

Total share holding 100.0% 100.0% 100.0% 100.0%Total share holding 100.0% 100.0% 100.0% 100.0%Total share holding 100.0% 100.0% 100.0% 100.0%

Source: Perception ResearchSource: Perception ResearchSource: Perception Research

Private sector bank, despite government’s majority holding Private sector bank, despite government’s majority holding Private sector bank, despite government’s majority holding

J&K Bank is the only bank which has 53.2% of governmentJ&K Bank is the only bank which has 53.2% of governmentJ&K Bank is the only bank which has 53.2% of governmentJ&K Bank is the only bank which has 53.2% of government

banks. Out of the total promoter holding, 94% of shares are heldbanks. Out of the total promoter holding, 94% of shares are heldbanks. Out of the total promoter holding, 94% of shares are held

government of J&K and balance 6% is held in strong handsgovernment of J&K and balance 6% is held in strong handsgovernment of J&K and balance 6% is held in strong hands

department of government of J&K.department of government of J&K.department of government of J&K.department of government of J&K.

Jammu & Kashmir and as aJammu & Kashmir and as aJammu & Kashmir and as aJammu & Kashmir and as a

only private sector bankonly private sector bankonly private sector bank

out the banking business ofout the banking business ofout the banking business of

CBDT. J&K Bank follows aCBDT. J&K Bank follows aCBDT. J&K Bank follows aCBDT. J&K Bank follows a

lending in its home state whichlending in its home state whichlending in its home state which

the same time, seeks tothe same time, seeks tothe same time, seeks to

build volumes and improvebuild volumes and improvebuild volumes and improvebuild volumes and improve

Q4FY13 Q1FY14 % QOQ % SPLY Share Holding Pattern Q1FY14Q4FY13 Q1FY14 % QOQ % SPLY Share Holding Pattern Q1FY14Q4FY13 Q1FY14 % QOQ % SPLY Share Holding Pattern Q1FY14

53.2% 53.2% 0.0% 0.0%53.2% 53.2% 0.0% 0.0%53.2% 53.2% 0.0% 0.0%

50.2% 50.2% 0.0% 0.0%50.2% 50.2% 0.0% 0.0%50.2% 50.2% 0.0% 0.0%

3.0% 3.0% 0.0% 0.0% Promoter3.0% 3.0% 0.0% 0.0%

46.8% 46.8% 0.0% 0.0%

Promoter

46.8% 46.8% 0.0% 0.0% 17%46.8% 46.8% 0.0% 0.0%

29.4% 29.7% 0.9% 0.7%

17%

29.4% 29.7% 0.9% 0.7%29.4% 29.7% 0.9% 0.7%

4.4% 4.5% 1.0% 78.7% 5%FII

4.4% 4.5% 1.0% 78.7% 5%FII

4.4% 4.5% 1.0% 78.7%

0.0% 0.0% -15.7% 0.0%

5%

0.0% 0.0% -15.7% 0.0%53%

0.0% 0.0% -15.7% 0.0%

0.4% 0.4% 0.0% 0.0%53%

DII0.4% 0.4% 0.0% 0.0%53%

DII0.4% 0.4% 0.0% 0.0%

24.5% 24.8% 0.9% -6.7% 25%

DII

24.5% 24.8% 0.9% -6.7% 25%24.5% 24.8% 0.9% -6.7%

5.4% 5.0% -6.2% -17.4%

25%

5.4% 5.0% -6.2% -17.4%Non Institutions

5.4% 5.0% -6.2% -17.4%

11.4% 11.4% 0.3% 6.3%Non Institutions

11.4% 11.4% 0.3% 6.3%11.4% 11.4% 0.3% 6.3%

0.6% 0.7% 7.5% 33.4%0.6% 0.7% 7.5% 33.4%0.6% 0.7% 7.5% 33.4%

100.0% 100.0% 0.0% 0.0%100.0% 100.0% 0.0% 0.0%100.0% 100.0% 0.0% 0.0%

holding in private sectorholding in private sectorholding in private sectorholding in private sector

held by the chief secretaryheld by the chief secretaryheld by the chief secretary

hands of secretary financehands of secretary financehands of secretary finance

�Investment rationale�Investment rationale�Investment rationale

Healthy performance to continueHealthy performance to continueHealthy performance to continueHealthy performance to continue

Loan book and deposits grew at moderate pace over last fiveLoan book and deposits grew at moderate pace over last fiveLoan book and deposits grew at moderate pace over last five

deposits grew at a CAGR of 17% and 18% respectively, overdeposits grew at a CAGR of 17% and 18% respectively, overdeposits grew at a CAGR of 17% and 18% respectively, over

FY13A) instead of an expected CAGR growth of 19% and 16% respectivelyFY13A) instead of an expected CAGR growth of 19% and 16% respectivelyFY13A) instead of an expected CAGR growth of 19% and 16% respectivelyFY13A) instead of an expected CAGR growth of 19% and 16% respectively

FY16E. Due to increased commercial and tourism activity alongFY16E. Due to increased commercial and tourism activity alongFY16E. Due to increased commercial and tourism activity along

infrastructure spending by the central government , we expectinfrastructure spending by the central government , we expectinfrastructure spending by the central government , we expect

for J&K in the near future.for J&K in the near future.for J&K in the near future.for J&K in the near future.

Exhibit 02 : Growth in depositsExhibit 02 : Growth in depositsExhibit 02 : Growth in deposits

6660530%80000

6660526%

30%80000

56445

6660526%

4743256445

26%

60000 4743256445

21%19% 20%

60000

3920047432

19%21%

19% 18%20%

330773920019% 19% 18%

40000 3307740000

10%

40000

10%20000

10%2000020000

0%0 0%0 0%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

Advances Growth %Advances Growth %Advances Growth %

Source: Perception ResearchSource: Perception Research

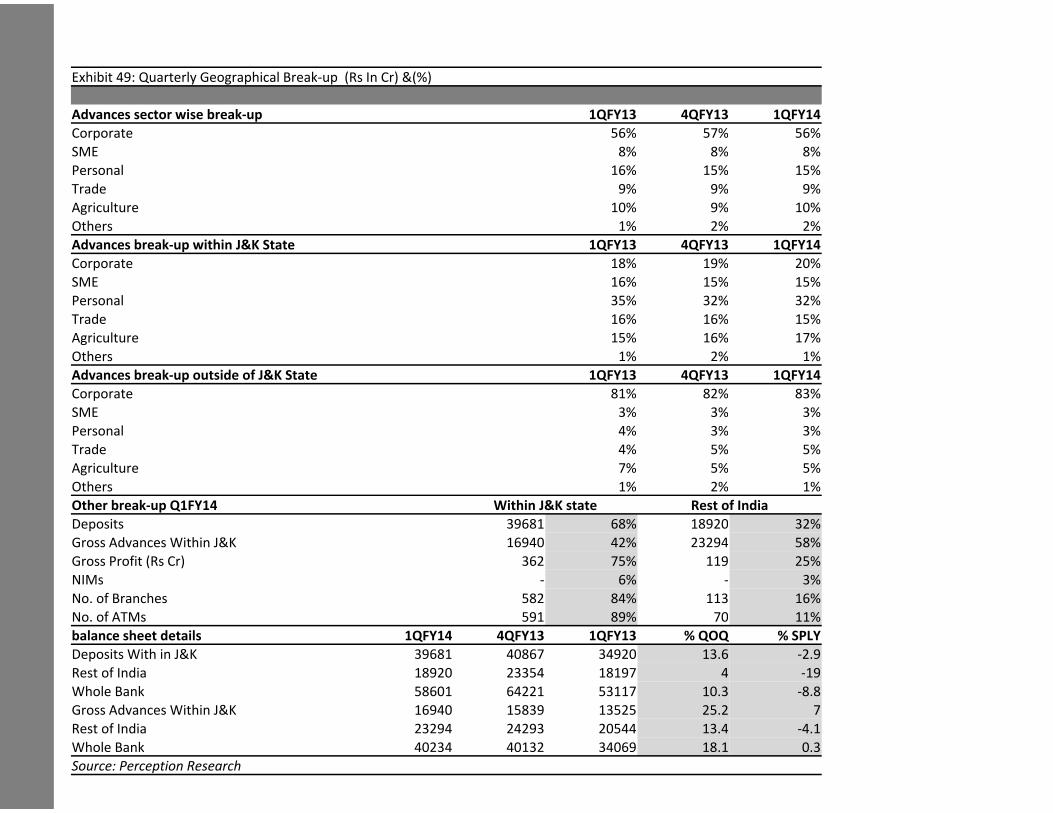

J&K bank has strong deposit franchise and focus towards J&KJ&K bank has strong deposit franchise and focus towards J&KJ&K bank has strong deposit franchise and focus towards J&KJ&K bank has strong deposit franchise and focus towards J&K

to deposits and 39% to loan book respectively. The managementto deposits and 39% to loan book respectively. The managementto deposits and 39% to loan book respectively. The management

confident to maintain their market share in J&K state for the currentconfident to maintain their market share in J&K state for the currentconfident to maintain their market share in J&K state for the current

Deposits Deposits Deposits

Y/E 31 March 1QFY13 4QFY13 1QFY14 QOQ SPLY FY12A FY13A YOYY/E 31 March 1QFY13 4QFY13 1QFY14 QOQ SPLY FY12A FY13A YOYY/E 31 March 1QFY13 4QFY13 1QFY14 QOQ SPLY FY12A FY13A YOY

Within J&K 34920 40867 39681 -3% 14% 35308 40867 16%Within J&K 34920 40867 39681 -3% 14% 35308 40867 16%Within J&K 34920 40867 39681 -3% 14% 35308 40867 16%

Rest of India 18197 23354 18920 -19% 4% 13803 23354 69%Rest of India 18197 23354 18920 -19% 4% 13803 23354 69%Rest of India 18197 23354 18920 -19% 4% 13803 23354 69%

Whole Bank 53117 64221 58601 -9% 10% 49111 64221 31%Whole Bank 53117 64221 58601 -9% 10% 49111 64221 31%Whole Bank 53117 64221 58601 -9% 10% 49111 64221 31%

Within J&K 66% 64% 68% - - 72% 64%Within J&K 66% 64% 68% - - 72% 64%Within J&K 66% 64% 68% - - 72% 64%

Rest of India 34% 36% 32% - - 28% 36%Rest of India 34% 36% 32% - - 28% 36%Rest of India 34% 36% 32% - - 28% 36%

five years (loan book andfive years (loan book andfive years (loan book and

over the period of FY09A toover the period of FY09A toover the period of FY09A to

respectively over FY13A torespectively over FY13A torespectively over FY13A torespectively over FY13A to

along with the focus onalong with the focus onalong with the focus on

an increase in the growthan increase in the growthan increase in the growth

Exhibit 03 : Growth in advancesExhibit 03 : Growth in advancesExhibit 03 : Growth in advances

6660530%80000

6660526%

30%80000

56445

6660526%

4743256445

26%

60000 4743256445

21%19% 20%

60000

3920047432

19%21%

19% 18%20%

330773920019% 19% 18%

40000 3307740000

10%

40000

10%20000

10%2000020000

0%0 0%0 0%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

Advances Growth %Advances Growth %Advances Growth %

Source: Perception ResearchSource: Perception Research

state would support 64%state would support 64%state would support 64%state would support 64%

management of J&K bank is prettymanagement of J&K bank is prettymanagement of J&K bank is pretty

current fiscal.current fiscal.current fiscal.

Gross AdvancesGross AdvancesGross Advances

YOY Y/E 31 March 1QFY13 4QFY13 1QFY14 QOQ SPLY FY12A FY13A YOYYOY Y/E 31 March 1QFY13 4QFY13 1QFY14 QOQ SPLY FY12A FY13A YOYYOY Y/E 31 March 1QFY13 4QFY13 1QFY14 QOQ SPLY FY12A FY13A YOY

16% Within J&K 13525 15839 16940 7% 25% 12574 15839 26%16% Within J&K 13525 15839 16940 7% 25% 12574 15839 26%16% Within J&K 13525 15839 16940 7% 25% 12574 15839 26%

69% Rest of India 20544 24293 23294 -4% 13% 20556 24293 18%69% Rest of India 20544 24293 23294 -4% 13% 20556 24293 18%69% Rest of India 20544 24293 23294 -4% 13% 20556 24293 18%

31% Whole Bank 34069 40132 40234 0% 18% 33130 40132 21%31% Whole Bank 34069 40132 40234 0% 18% 33130 40132 21%31% Whole Bank 34069 40132 40234 0% 18% 33130 40132 21%

- Within J&K 40% 39% 42% - - 38% 39% -- Within J&K 40% 39% 42% - - 38% 39% -- Within J&K 40% 39% 42% - - 38% 39% -

- Rest of India 60% 61% 58% - - 62% 61% -- Rest of India 60% 61% 58% - - 62% 61% -- Rest of India 60% 61% 58% - - 62% 61% -

Strong geographic presence in J&K state creates the dominionsStrong geographic presence in J&K state creates the dominionsStrong geographic presence in J&K state creates the dominionsStrong geographic presence in J&K state creates the dominions

J&K bank is the only a private sector bank in the state of J&K . ItJ&K bank is the only a private sector bank in the state of J&K . ItJ&K bank is the only a private sector bank in the state of J&K . It

of the RBI to carry on the general banking business of the centralof the RBI to carry on the general banking business of the centralof the RBI to carry on the general banking business of the central

leadership in the state with a network of 455 branches whichleadership in the state with a network of 455 branches whichleadership in the state with a network of 455 branches which

branches and 399 ATMs. J&K bank also dominates the region withbranches and 399 ATMs. J&K bank also dominates the region withbranches and 399 ATMs. J&K bank also dominates the region withbranches and 399 ATMs. J&K bank also dominates the region with

total advances and 65% market share in total deposits in the statetotal advances and 65% market share in total deposits in the statetotal advances and 65% market share in total deposits in the state

Exhibit 04: Branches Total – J&K StateExhibit 04: Branches Total – J&K State

100%2000 100%2000

82% 85% 87% 87%

100%2000

82% 85% 87% 87%80%

150085769%

82% 85% 80%1500

715

85769%60%

1500

71569%

60%

579715 60%

1000

380496

57940%

1000

380496 40%

985

380

500

548 603 685 821 985 20%500

548 603 685 821 985 20%548 603 685

0%0 0%0 0%0

FY11A FY12A FY13A FY14E FY15EFY11A FY12A FY13A FY14E FY15EFY11A FY12A FY13A FY14E FY15E

Total Branches J&K Branches J&K Branches % to toatlTotal Branches J&K Branches J&K Branches % to toatlTotal Branches J&K Branches J&K Branches % to toatl

Source: Perception ResearchSource: Perception ResearchSource: Perception Research

Massive expansion in networkMassive expansion in networkMassive expansion in network

To improve the geographic presence and to obtain the moreTo improve the geographic presence and to obtain the moreTo improve the geographic presence and to obtain the more

business J&K bank planned massive expansion in their networkbusiness J&K bank planned massive expansion in their networkbusiness J&K bank planned massive expansion in their network

impressive expansion plan of 300 new branches and almost equivalentimpressive expansion plan of 300 new branches and almost equivalentimpressive expansion plan of 300 new branches and almost equivalentimpressive expansion plan of 300 new branches and almost equivalent

of FY15.of FY15.of FY15.

Exhibit 06: Expansion plan in Branches & ATMExhibit 06: Expansion plan in Branches & ATMExhibit 06: Expansion plan in Branches & ATM

50%2000 50%2000 50%2000

41% 40%1500

837

41% 40%1500

83730%

1500

698

83730%

613698

25%30%

1000508

61320% 20%

25%21% 20% 20%

1000

246 288 361508 20% 20%

17%21% 20% 20%

985246 288 361

14%

20% 20%17%

21%

14%

20% 20%

500603 685 821 985

246

10%14%

10%14%

10%500

530 536 548 603 685 821 98510%10% 10%

500

530 536 548 603 685

1% 1% 2% 0%0 1% 1% 2% 0%0 1% 1% 0%0

FY9A FY10A FY11A FY12A FY13A FY14E FY15EFY9A FY10A FY11A FY12A FY13A FY14E FY15EFY9A FY10A FY11A FY12A FY13A FY14E FY15E

Branches ATM Growth % Growth %Branches ATM Growth % Growth %Branches ATM Growth % Growth %

Source: Perception ResearchSource: Perception ResearchSource: Perception Research

dominionsdominionsdominionsdominions

It has right to act of behalfIt has right to act of behalfIt has right to act of behalf

central government. It has thecentral government. It has thecentral government. It has the

which comprises 80% of totalwhich comprises 80% of totalwhich comprises 80% of total

with 70% market share inwith 70% market share inwith 70% market share inwith 70% market share in

state.state.state.

Exhibit 05: ATM Total – J&K StateExhibit 05: ATM Total – J&K State

100%200090% 90%

100%2000

89% 90% 90%100%2000

89% 90% 90%80%

150068%

80%1500

75461%68%

60%

1500

62875461%

68%60%

1000544

62875461% 60%

1000544

62840%

1000

345544 40%

837220345

20%500

508 613 698 837220 20%500

361 508 613 698 837220 20%

361 508 613

0%0 0%0 0%0

FY11A FY12A FY13A FY14E FY15EFY11A FY12A FY13A FY14E FY15ETotal ATM J&K ATM J&K ATM % to toatl

FY11A FY12A FY13A FY14E FY15ETotal ATM J&K ATM J&K ATM % to toatlTotal ATM J&K ATM J&K ATM % to toatl

Source: Perception ResearchSource: Perception ResearchSource: Perception Research

opportunities in bankingopportunities in bankingopportunities in banking

network. The bank hasnetwork. The bank hasnetwork. The bank has

equivalent ATMs by the endequivalent ATMs by the endequivalent ATMs by the endequivalent ATMs by the end

Exhibit 07: Branches in Metro, Urban, Semi – Urban & RuralExhibit 07: Branches in Metro, Urban, Semi – Urban & RuralExhibit 07: Branches in Metro, Urban, Semi – Urban & Rural

120012001200

10001000

453800 453800

378

453

600332

378600

197204 206 223 273332

400

600

164197204 206 223 273

332400

119 121 118 123 136164

197204 206 223400

222 266119 121 118 123 136

164

200166 168 168 168 178 222 266119 121 118 123

200

41 41 39 39 39 57 69166 168 168 168 178 222

0 41 41 39 39 39 57 6900

FY9A FY10A FY11A FY12A FY13A FY14E FY15EFY9A FY10A FY11A FY12A FY13A FY14E FY15EFY9A FY10A FY11A FY12A FY13A FY14E FY15E

Metro Urban Semi-Urban RuralMetro Urban Semi-Urban Rural

Source: Perception ResearchSource: Perception ResearchSource: Perception Research

Focus towards J&K state will lead to improvement in NIMFocus towards J&K state will lead to improvement in NIMFocus towards J&K state will lead to improvement in NIMFocus towards J&K state will lead to improvement in NIM

With strong deposit franchise and focus (increase lending) towardsWith strong deposit franchise and focus (increase lending) towardsWith strong deposit franchise and focus (increase lending) towards

support margins going ahead. Bank earns NIMs of 6.20% withinsupport margins going ahead. Bank earns NIMs of 6.20% withinsupport margins going ahead. Bank earns NIMs of 6.20% within

outside the state. We expected NIM to sustain at current levelsoutside the state. We expected NIM to sustain at current levelsoutside the state. We expected NIM to sustain at current levels

the range of 61 to 65 percent, going ahead, and credit growththe range of 61 to 65 percent, going ahead, and credit growththe range of 61 to 65 percent, going ahead, and credit growththe range of 61 to 65 percent, going ahead, and credit growth

portfolio) is expected to grow at a faster pace. J&K Bank hasportfolio) is expected to grow at a faster pace. J&K Bank hasportfolio) is expected to grow at a faster pace. J&K Bank has

FY13, which we expect to improve to 63% in FY14E andFY13, which we expect to improve to 63% in FY14E andFY13, which we expect to improve to 63% in FY14E and

management has guided credit growth (22-25%) will outpacemanagement has guided credit growth (22-25%) will outpacemanagement has guided credit growth (22-25%) will outpacemanagement has guided credit growth (22-25%) will outpace

We have factored in 21% credit growth and 16.5% deposit growthWe have factored in 21% credit growth and 16.5% deposit growthWe have factored in 21% credit growth and 16.5% deposit growth

Exhibit 08:Loan Book - J&K stats and Rest of IndiaExhibit 08:Loan Book - J&K stats and Rest of IndiaExhibit 08:Loan Book - J&K stats and Rest of India

30%80000

26%

30%80000

26% 25%23%

26%23% 23%

25%60000 23% 23% 23%

21% 20%60000

3862021%

18% 18%20%

332983862018% 18%

16% 16% 15%

20%

4000028701

3329813%

16% 16% 15%40000

2429328701

3329813%

10%

15%40000

2055624293

2870113%10%

2000029135

2055624293 10%

20000

19536 24113 2913520556

5%20000

12574 15839 19536 24113 29135 5%12574 15839 19536

0%0 0%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

J&K State Rest of India Growth (%) Growth (%)J&K State Rest of India Growth (%) Growth (%)J&K State Rest of India Growth (%) Growth (%)

Source: Perception ResearchSource: Perception Research

Exhibit 10:NIM - J&K stateExhibit 10:NIM - J&K stateExhibit 10:NIM - J&K state

FY15E, 6.2% FY16E, 6.2%FY15E, 6.2% FY16E, 6.2%

FY13A, 6.2%

FY15E, 6.2% FY16E, 6.2%

FY13A, 6.2%FY13A, 6.2%

FY14E, 6.1%FY14E, 6.1%FY14E, 6.1%

FY12A, 6.0%FY12A, 6.0%FY12A, 6.0%

0 1 2 3 4 5 60 1 2 3 4 5 6

Source: Perception ResearchSource: Perception ResearchSource: Perception Research

towards J&K state wouldtowards J&K state wouldtowards J&K state would

within the state and 2.5%within the state and 2.5%within the state and 2.5%

levels of 4%+ as its CD ratio inlevels of 4%+ as its CD ratio inlevels of 4%+ as its CD ratio in

growth with J&K (higher yieldinggrowth with J&K (higher yieldinggrowth with J&K (higher yieldinggrowth with J&K (higher yielding

has a CD ratio of 61% as onhas a CD ratio of 61% as onhas a CD ratio of 61% as on

64% in FY15E. Even the64% in FY15E. Even the64% in FY15E. Even the

deposit growth (17-18%).deposit growth (17-18%).deposit growth (17-18%).deposit growth (17-18%).

growth in FY14E.growth in FY14E.growth in FY14E.

Exhibit 09: Deposits - J&K stats and Rest of IndiaExhibit 09: Deposits - J&K stats and Rest of IndiaExhibit 09: Deposits - J&K stats and Rest of India

80%120000

69%

80%120000

69%100000 69%60%

100000

4109760%

8000034865

4109780000

2843034865

41097

40%60000

80000

2335428430

3486540%60000

1380323354

28430 40%

40000

60000

5913913803

23354

24% 22% 23% 20%40000

40867 46387 52297 5913913803

16% 14%

24% 22% 23%18% 20%

20000

40000

35308 40867 46387 52297 5913912%

16% 14% 13% 13%22% 23%

18% 20%20000 35308 40867 4638712%

16% 14% 13% 13%20000

0%0 0%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

J&K State Rest of India Growth (%) Growth (%)J&K State Rest of India Growth (%) Growth (%)J&K State Rest of India Growth (%) Growth (%)

Source: Perception ResearchSource: Perception Research

Exhibit 11:NIM - Rest of IndiaExhibit 11:NIM - Rest of IndiaExhibit 11:NIM - Rest of India

FY15E, 2.6%FY15E, 2.6%FY16E, 2.6%

FY15E, 2.6%FY16E, 2.6%FY16E, 2.6%

FY13A, 2.6%FY13A, 2.6%

FY12A, 2.5% FY14E, 2.5%FY12A, 2.5% FY14E, 2.5%FY12A, 2.5% FY14E, 2.5%

0 1 2 3 4 5 60 1 2 3 4 5 60 1 2 3 4 5 6

Source: Perception ResearchSource: Perception ResearchSource: Perception Research

Huge Potential in J&K state for Horticultural LendingHuge Potential in J&K state for Horticultural LendingHuge Potential in J&K state for Horticultural LendingHuge Potential in J&K state for Horticultural Lending

Agriculture involves about 70% of the population and contributesAgriculture involves about 70% of the population and contributesAgriculture involves about 70% of the population and contributes

only 16 % of J&K Bank’s lending is to this sector. Horticulturalonly 16 % of J&K Bank’s lending is to this sector. Horticulturalonly 16 % of J&K Bank’s lending is to this sector. Horticultural

about 45 % to Agricultural production and involves 30 lac peopleabout 45 % to Agricultural production and involves 30 lac peopleabout 45 % to Agricultural production and involves 30 lac people

% by value of the State’s Horticultural output. J&K State produces% by value of the State’s Horticultural output. J&K State produces% by value of the State’s Horticultural output. J&K State produces% by value of the State’s Horticultural output. J&K State produces

apple output and controls 49 % of land dedicated to apple cultivationapple output and controls 49 % of land dedicated to apple cultivationapple output and controls 49 % of land dedicated to apple cultivation

Out of a total of more than 283000 apple growers in the State,Out of a total of more than 283000 apple growers in the State,Out of a total of more than 283000 apple growers in the State,

extended to about 17300 growers so far. Tapping the remaining

Out of a total of more than 283000 apple growers in the State,

extended to about 17300 growers so far. Tapping the remainingextended to about 17300 growers so far. Tapping the remainingextended to about 17300 growers so far. Tapping the remaining

credit of about Rs.7000 Cr more. In J&K 75 % of Apple growerscredit of about Rs.7000 Cr more. In J&K 75 % of Apple growerscredit of about Rs.7000 Cr more. In J&K 75 % of Apple growers

traders and are unaware that its effective interest cost thattraders and are unaware that its effective interest cost thattraders and are unaware that its effective interest cost that

54%, against the Bank’s interest ranging from 4% to11%.54%, against the Bank’s interest ranging from 4% to11%.54%, against the Bank’s interest ranging from 4% to11%.54%, against the Bank’s interest ranging from 4% to11%.

Current shortfall in Agriculture Sector Lending is Rs. 2335 Cr, whichCurrent shortfall in Agriculture Sector Lending is Rs. 2335 Cr, whichCurrent shortfall in Agriculture Sector Lending is Rs. 2335 Cr, which

RIDF/MSME Bonds/RHF @ 3 to 5 % for 3-7 years. Interest SubventionRIDF/MSME Bonds/RHF @ 3 to 5 % for 3-7 years. Interest SubventionRIDF/MSME Bonds/RHF @ 3 to 5 % for 3-7 years. Interest Subvention

to J&K Bank recently providing a level playing field vis-à-vis Publicto J&K Bank recently providing a level playing field vis-à-vis Publicto J&K Bank recently providing a level playing field vis-à-vis Publicto J&K Bank recently providing a level playing field vis-à-vis Public

of pricing of agricultural loans and improve the flow of creditof pricing of agricultural loans and improve the flow of creditof pricing of agricultural loans and improve the flow of credit

particularly in J&K State. Assuming yield on incremental Agriculturalparticularly in J&K State. Assuming yield on incremental Agriculturalparticularly in J&K State. Assuming yield on incremental Agricultural

Rate of 10.25 %, the incremental yield (10.25% - 4 %) wouldRate of 10.25 %, the incremental yield (10.25% - 4 %) wouldRate of 10.25 %, the incremental yield (10.25% - 4 %) wouldRate of 10.25 %, the incremental yield (10.25% - 4 %) would

revenue of about Rs. 146 Cr per year on lending Rs.revenue of about Rs. 146 Cr per year on lending Rs.revenue of about Rs. 146 Cr per year on lending Rs.

sector, increasing agricultural advances which will improvesector, increasing agricultural advances which will improvesector, increasing agricultural advances which will improve

helping in financial inclusion, widening customer base andhelping in financial inclusion, widening customer base andhelping in financial inclusion, widening customer base andhelping in financial inclusion, widening customer base and

remote rural areas.remote rural areas.remote rural areas.

Exhibit 12: Apple Grower in J&K StateExhibit 12: Apple Grower in J&K StateExhibit 12: Apple Grower in J&K State

Total Grower Total Grower Total Grower

, 283000, 283000, 283000

Source: Perception ResearchSource: Perception Research

contributes 23 % to the GDP, yetcontributes 23 % to the GDP, yetcontributes 23 % to the GDP, yet

Horticultural production contributesHorticultural production contributesHorticultural production contributes

people. Apples account for 86people. Apples account for 86people. Apples account for 86

produces 77 % of India’s totalproduces 77 % of India’s totalproduces 77 % of India’s totalproduces 77 % of India’s total

cultivation.cultivation.cultivation.

State, Bank’s finance has beenState, Bank’s finance has beenState, Bank’s finance has been

remaining growers will generate

State, Bank’s finance has been

remaining growers will generateremaining growers will generateremaining growers will generate

growers get their financing fromgrowers get their financing fromgrowers get their financing from

that works out to 36% tothat works out to 36% tothat works out to 36% to

which has to be invested inwhich has to be invested inwhich has to be invested in

Subvention Scheme extendedSubvention Scheme extendedSubvention Scheme extended

Public Sector Banks in termsPublic Sector Banks in termsPublic Sector Banks in termsPublic Sector Banks in terms

credit to agricultural sectorcredit to agricultural sectorcredit to agricultural sector

Agricultural Advances at BaseAgricultural Advances at BaseAgricultural Advances at Base

would generate an incrementalwould generate an incrementalwould generate an incrementalwould generate an incremental

2335 Cr to agricultural2335 Cr to agricultural2335 Cr to agricultural

core advances portfoliocore advances portfoliocore advances portfolio

and enhancing outreach inand enhancing outreach inand enhancing outreach inand enhancing outreach in

Potential For Potential For Potential For

Lending, 265700Lending, 265700Lending, 265700

J&K's J&K's

Borrower,17300Borrower,17300Borrower,17300

Cheap Valuation and High Dividend yieldCheap Valuation and High Dividend yieldCheap Valuation and High Dividend yield

At current market price, J&K bank is still available at FY14E Price

Cheap Valuation and High Dividend yield

At current market price, J&K bank is still available at FY14E PriceAt current market price, J&K bank is still available at FY14E PriceAt current market price, J&K bank is still available at FY14E Price

times. The estimated dividend yield for FY14 is 5.4%. High dividendtimes. The estimated dividend yield for FY14 is 5.4%. High dividendtimes. The estimated dividend yield for FY14 is 5.4%. High dividend

comfortable cushion. At CMP of Rs 1101, the stock is trading atcomfortable cushion. At CMP of Rs 1101, the stock is trading atcomfortable cushion. At CMP of Rs 1101, the stock is trading at

for FY14E & FY15E, respectively.for FY14E & FY15E, respectively.for FY14E & FY15E, respectively.for FY14E & FY15E, respectively.

Exhibit 13: P/E (x) & P/BV (x) Exhibit 13: P/E (x) & P/BV (x)

1.51.2 1.51.1

1.2 1.51.1

1.2

0.90.9 1.10.9 1.10.9

7.37.8

0.90.86.8 7.3

7.80.8

0.66.8 7.3

5.3

0.80.6

5.35.1 4.3

0.65.3

5.1 4.34.33.53.5

2.92.9

FY9A FY10A FY11A FY12A FY13A FY14E FY15E FY16EFY9A FY10A FY11A FY12A FY13A FY14E FY15E FY16E

P/E (X) P/BV (X)P/E (X) P/BV (X)

Source: Perception ResearchSource: Perception Research

Price to book value of 0.9Price to book value of 0.9Price to book value of 0.9Price to book value of 0.9

dividend yield provides with adividend yield provides with adividend yield provides with a

at 4.3x and 3.5x to its PEat 4.3x and 3.5x to its PEat 4.3x and 3.5x to its PE

Exhibit 14: DPS & Dividend yieldExhibit 14: DPS & Dividend yield

88 10%100 88 10%100

72

88 10%100

728% 8% 8%8059

728% 8% 8%80

5059

7%6%60 50

5%

7%6%60

33

50

5%5%

5%6%60

26334% 4%

5%5%

5%

4%40

1722 26

334% 4%5%

4%40

1722 26

2%2017

2%20 2%20

0%0 0%0 0%0

FY9A FY10A FY11A FY12A FY13A FY14E FY15E FY16EFY9A FY10A FY11A FY12A FY13A FY14E FY15E FY16EFY9A FY10A FY11A FY12A FY13A FY14E FY15E FY16E

DPS Dividend yield (%)DPS Dividend yield (%)DPS Dividend yield (%)

Source: Perception ResearchSource: Perception Research

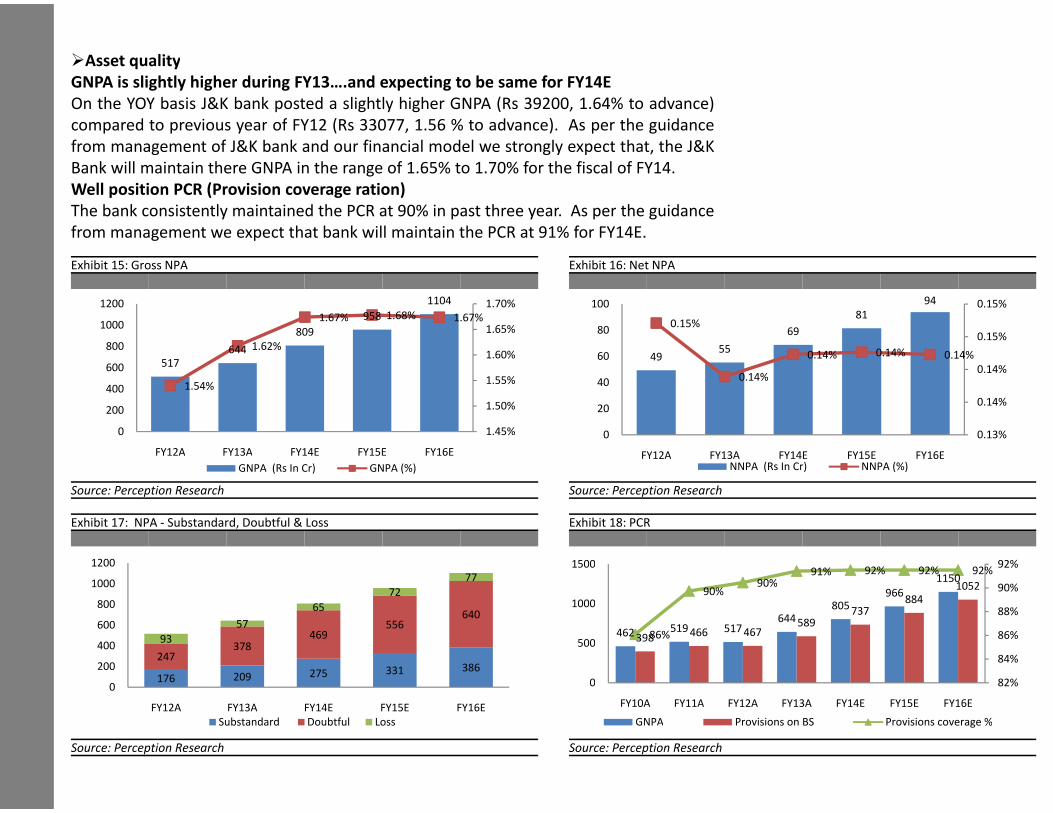

�Asset quality�Asset quality�Asset qualityAsset quality

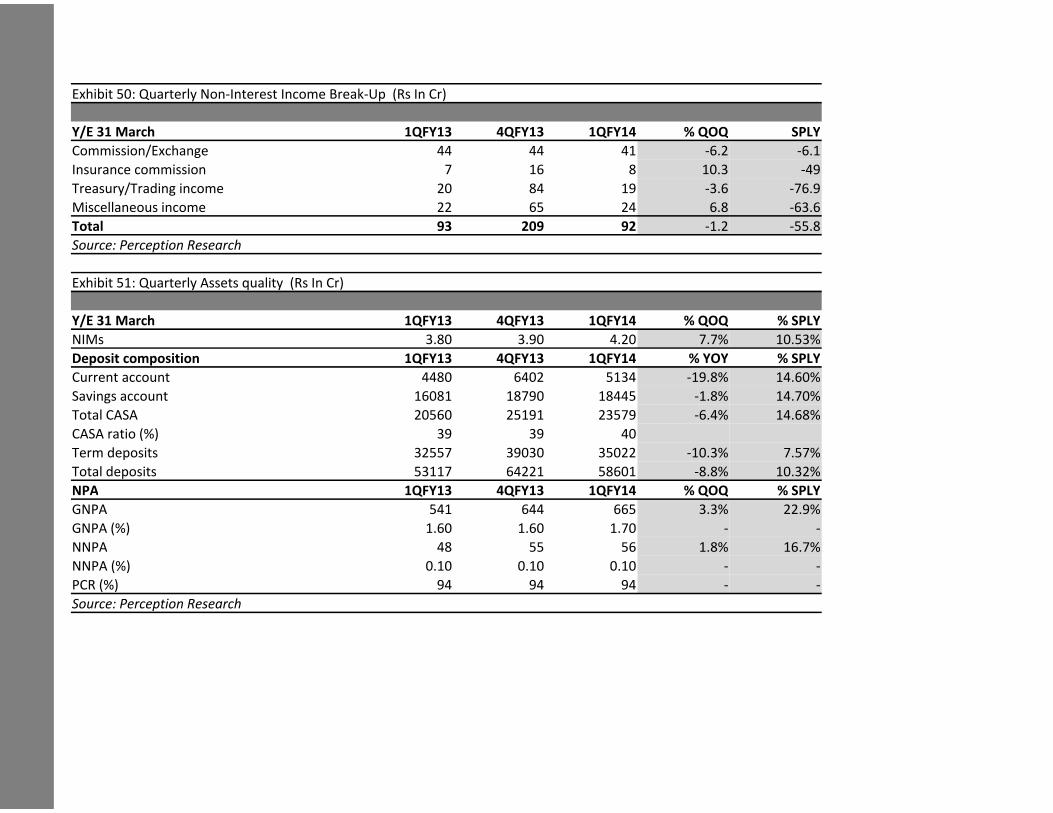

GNPA is slightly higher during FY13….and expecting to be sameGNPA is slightly higher during FY13….and expecting to be sameGNPA is slightly higher during FY13….and expecting to be same

On the YOY basis J&K bank posted a slightly higher GNPA (Rs 39200On the YOY basis J&K bank posted a slightly higher GNPA (Rs 39200On the YOY basis J&K bank posted a slightly higher GNPA (Rs 39200

compared to previous year of FY12 (Rs 33077, 1.56 % to advance)compared to previous year of FY12 (Rs 33077, 1.56 % to advance)compared to previous year of FY12 (Rs 33077, 1.56 % to advance)

from management of J&K bank and our financial model we stronglyfrom management of J&K bank and our financial model we stronglyfrom management of J&K bank and our financial model we stronglyfrom management of J&K bank and our financial model we strongly

Bank will maintain there GNPA in the range of 1.65% to 1.70% forBank will maintain there GNPA in the range of 1.65% to 1.70% forBank will maintain there GNPA in the range of 1.65% to 1.70% for

Well position PCR (Provision coverage ration)Well position PCR (Provision coverage ration)Well position PCR (Provision coverage ration)

The bank consistently maintained the PCR at 90% in past threeThe bank consistently maintained the PCR at 90% in past threeThe bank consistently maintained the PCR at 90% in past threeThe bank consistently maintained the PCR at 90% in past three

from management we expect that bank will maintain the PCR atfrom management we expect that bank will maintain the PCR atfrom management we expect that bank will maintain the PCR at

Exhibit 15: Gross NPAExhibit 15: Gross NPAExhibit 15: Gross NPA

11041104 1.70%1200958

1104

1.67% 1.68% 1.67%

1.70%12009581.67% 1.68% 1.67%

1.65%1000809

9581.67% 1.68% 1.67%1.65%1000

809

1.62%

1.65%

800

1000

644 1.62%1.60%

800

517

644 1.62%1.60%

800

5171.60%

600 517

1.55%600

1.54%1.55%

400 1.54%400

1.50%200 1.50%200

1.45%0

200

1.45%0 1.45%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

GNPA (Rs In Cr) GNPA (%)GNPA (Rs In Cr) GNPA (%)GNPA (Rs In Cr) GNPA (%)

Source: Perception ResearchSource: Perception Research

Exhibit 17: NPA - Substandard, Doubtful & LossExhibit 17: NPA - Substandard, Doubtful & LossExhibit 17: NPA - Substandard, Doubtful & Loss

12001200

77

1200

771000

72

771000

65

72800

64065800

556640

57

65

600469

556640

57600

378469

556

93

57

400

600

37846993

400247

378400

275 331 386247

200176 209 275 331 386200176 209 275 331

00

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

Substandard Doubtful LossSubstandard Doubtful Loss

Source: Perception ResearchSource: Perception ResearchSource: Perception Research

same for FY14Esame for FY14Esame for FY14E

39200, 1.64% to advance)39200, 1.64% to advance)39200, 1.64% to advance)

advance). As per the guidanceadvance). As per the guidanceadvance). As per the guidance

strongly expect that, the J&Kstrongly expect that, the J&Kstrongly expect that, the J&Kstrongly expect that, the J&K

for the fiscal of FY14.for the fiscal of FY14.for the fiscal of FY14.

year. As per the guidanceyear. As per the guidanceyear. As per the guidanceyear. As per the guidance

at 91% for FY14E.at 91% for FY14E.at 91% for FY14E.

Exhibit 16: Net NPAExhibit 16: Net NPAExhibit 16: Net NPA

9494 0.15%10081

94 0.15%10081

0.15%69

0.15%0.15%

80 69 0.15%80

4955

0.14% 0.14% 0.14%

0.15%

60 4955

0.14% 0.14% 0.14%60 49 0.14% 0.14%

0.14%60

0.14%0.14%

40 0.14%40

0.14%

40

0.14%20

0.14%20

0.13%0 0.13%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16ENNPA (Rs In Cr) NNPA (%)NNPA (Rs In Cr) NNPA (%)NNPA (Rs In Cr) NNPA (%)

Source: Perception ResearchSource: Perception Research

Exhibit 18: PCRExhibit 18: PCRExhibit 18: PCR

91% 92% 92% 92%92%1500

115091% 92% 92% 92%

92%1500

1150105290%

91% 92% 92% 92%

90%966

1150

8841052

90%90% 90%

805966

8841052

90% 90%

1000

644805

737884

88%1000

519 517644

805

589737 88%

462 519 517644

398466 467

58986% 86%462 519 517

398466 46786% 86%

500462 39886% 86%

500

84%

500

84%

82%0 82%0 82%0

FY10A FY11A FY12A FY13A FY14E FY15E FY16EFY10A FY11A FY12A FY13A FY14E FY15E FY16E

GNPA Provisions on BS Provisions coverage %GNPA Provisions on BS Provisions coverage %GNPA Provisions on BS Provisions coverage %

Source: Perception ResearchSource: Perception ResearchSource: Perception Research

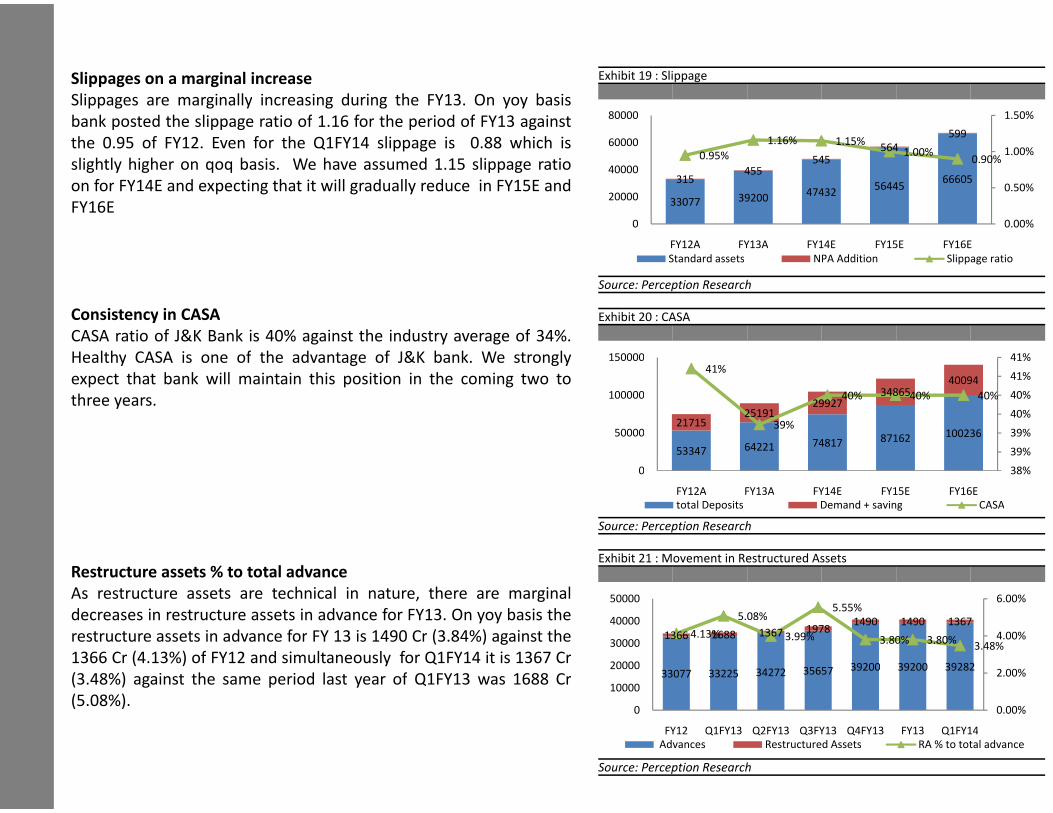

Slippages on a marginal increaseSlippages on a marginal increaseSlippages on a marginal increase

Slippages are marginally increasing during the FY13. On yoy

Slippages on a marginal increase

Slippages are marginally increasing during the FY13. On yoySlippages are marginally increasing during the FY13. On yoySlippages are marginally increasing during the FY13. On yoy

bank posted the slippage ratio of 1.16 for the period of FY13 againstbank posted the slippage ratio of 1.16 for the period of FY13 againstbank posted the slippage ratio of 1.16 for the period of FY13 against

the 0.95 of FY12. Even for the Q1FY14 slippage is 0.88 whichthe 0.95 of FY12. Even for the Q1FY14 slippage is 0.88 whichthe 0.95 of FY12. Even for the Q1FY14 slippage is 0.88 which

slightly higher on qoq basis. We have assumed 1.15 slippageslightly higher on qoq basis. We have assumed 1.15 slippageslightly higher on qoq basis. We have assumed 1.15 slippageslightly higher on qoq basis. We have assumed 1.15 slippage

on for FY14E and expecting that it will gradually reduce in FY15on for FY14E and expecting that it will gradually reduce in FY15on for FY14E and expecting that it will gradually reduce in FY15

FY16EFY16EFY16E

Consistency in CASAConsistency in CASAConsistency in CASAConsistency in CASA

CASA ratio of J&K Bank is 40% against the industry average ofCASA ratio of J&K Bank is 40% against the industry average ofCASA ratio of J&K Bank is 40% against the industry average of

Healthy CASA is one of the advantage of J&K bank. We stronglyHealthy CASA is one of the advantage of J&K bank. We stronglyHealthy CASA is one of the advantage of J&K bank. We strongly

expect that bank will maintain this position in the coming twoexpect that bank will maintain this position in the coming twoexpect that bank will maintain this position in the coming twoexpect that bank will maintain this position in the coming two

three years.three years.three years.

Restructure assets % to total advanceRestructure assets % to total advanceRestructure assets % to total advance

As restructure assets are technical in nature, there are marginalAs restructure assets are technical in nature, there are marginalAs restructure assets are technical in nature, there are marginalAs restructure assets are technical in nature, there are marginal

decreases in restructure assets in advance for FY13. On yoy basisdecreases in restructure assets in advance for FY13. On yoy basisdecreases in restructure assets in advance for FY13. On yoy basis

restructure assets in advance for FY 13 is 1490 Cr (3.84%) againstrestructure assets in advance for FY 13 is 1490 Cr (3.84%) againstrestructure assets in advance for FY 13 is 1490 Cr (3.84%) against

1366 Cr (4.13%) of FY12 and simultaneously for Q1FY14 it is 13671366 Cr (4.13%) of FY12 and simultaneously for Q1FY14 it is 13671366 Cr (4.13%) of FY12 and simultaneously for Q1FY14 it is 1367

(3.48%) against the same period last year of Q1FY13 was 1688

1366 Cr (4.13%) of FY12 and simultaneously for Q1FY14 it is 1367

(3.48%) against the same period last year of Q1FY13 was 1688(3.48%) against the same period last year of Q1FY13 was 1688(3.48%) against the same period last year of Q1FY13 was 1688

(5.08%).(5.08%).(5.08%).

Exhibit 19 : SlippageExhibit 19 : Slippage

yoy basis

Exhibit 19 : Slippage

yoy basisyoy basisyoy basis

against 1.50%80000against599

1.50%80000against

which is599

1.16% 1.15%60000which is 564

5991.16% 1.15%

1.00% 1.00%60000which is

slippage ratio 545564

0.95%

1.16% 1.15%1.00%

0.90%1.00%

60000

slippage ratio 455545

5640.95% 1.00%

0.90%1.00%

40000slippage ratio66605315

455545 0.90%

40000slippage ratio

15E and 5644566605315

455

0.50%

40000

15E and39200

4743256445

666053150.50%

2000015E and

33077 3920047432

56445 0.50%20000

33077 3920020000

0.00%0 0.00%0 0.00%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

Standard assets NPA Addition Slippage ratioStandard assets NPA Addition Slippage ratio

Source: Perception ResearchSource: Perception Research

Exhibit 20 : CASAExhibit 20 : CASA

of 34%.

Exhibit 20 : CASA

of 34%.of 34%.

strongly 41%150000strongly 41%150000strongly

two to41%

41%

41%150000

two to 4009441%

41%two to34865

40094

40%

41%

100000

two to

299273486540% 40% 40% 40%100000

2519129927

3486540% 40% 40% 40%100000

2171525191

2992740%

2171525191

39%40%

87162 10023621715 39%

39%50000

53347 64221 74817 87162 100236 39%50000

53347 64221 74817 87162

39%53347 64221 39%

38%0 38%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

total Deposits Demand + saving CASAtotal Deposits Demand + saving CASA

Source: Perception Research

total Deposits Demand + saving CASA

Source: Perception ResearchSource: Perception Research

Exhibit 21 : Movement in Restructured Assets Exhibit 21 : Movement in Restructured Assets Exhibit 21 : Movement in Restructured Assets

marginalmarginal 6.00%50000marginal5.55%

6.00%50000marginal

basis the 5.08%5.55%

6.00%50000

basis the 1490 1490 13675.08%5.55%

40000basis the

against the 1366 1688 1367 19781490 1490 1367

4.13%

5.08%

3.99% 4.00%

40000

against the 1366 1688 1367 19784.13% 3.99% 3.80% 3.80%3.48%

4.00%30000against the

1367 Cr

1366 1688 13674.13% 3.99% 3.80% 3.80%3.48%

4.00%30000

1367 Cr3.48%

20000

30000

1367 Cr

1688 Cr 33077 33225 34272 35657 39200 39200 392822.00%

200001367 Cr

1688 Cr 33077 33225 34272 35657 39200 39200 392822.00%

20000

1688 Cr 33077 33225 34272 35657 2.00%

100001688 Cr

10000

0.00%0 0.00%0 0.00%0

FY12 Q1FY13 Q2FY13 Q3FY13 Q4FY13 FY13 Q1FY14FY12 Q1FY13 Q2FY13 Q3FY13 Q4FY13 FY13 Q1FY14FY12 Q1FY13 Q2FY13 Q3FY13 Q4FY13 FY13 Q1FY14

Advances Restructured Assets RA % to total advanceAdvances Restructured Assets RA % to total advance

Source: Perception ResearchSource: Perception ResearchSource: Perception Research

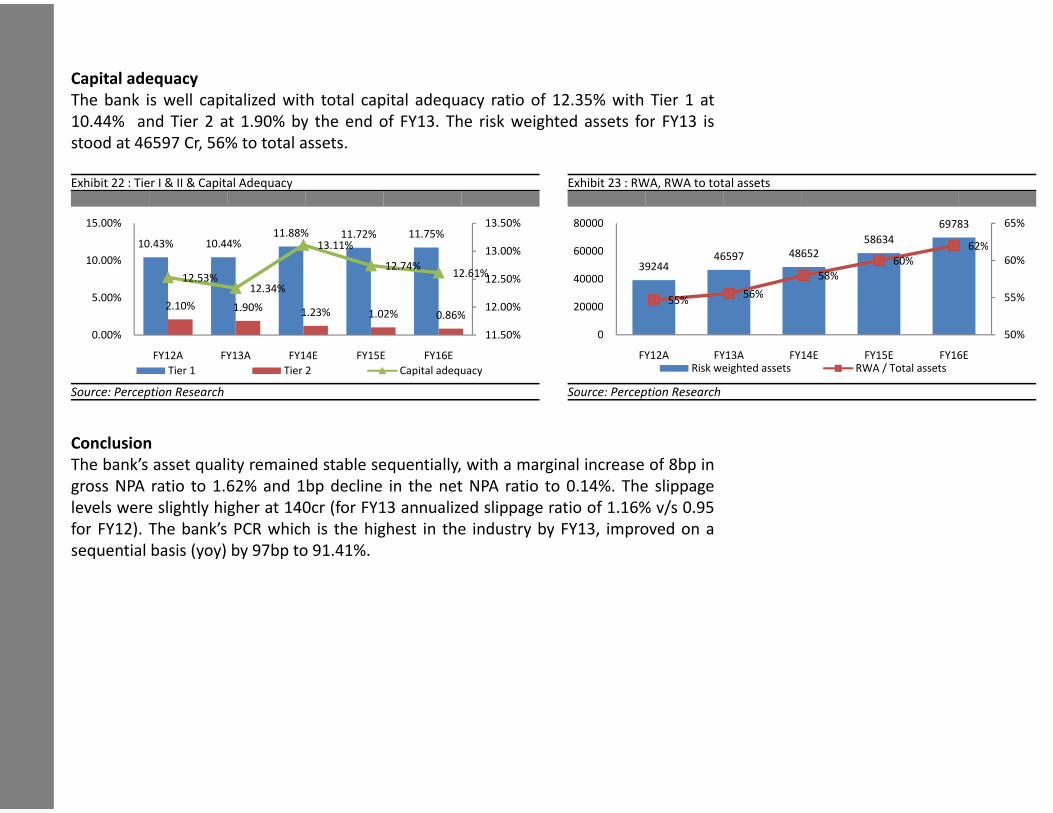

Capital adequacyCapital adequacyCapital adequacy

The bank is well capitalized with total capital adequacy ratio

Capital adequacy

The bank is well capitalized with total capital adequacy ratioThe bank is well capitalized with total capital adequacy ratioThe bank is well capitalized with total capital adequacy ratio

10.44% and Tier 2 at 1.90% by the end of FY13. The risk weighted10.44% and Tier 2 at 1.90% by the end of FY13. The risk weighted10.44% and Tier 2 at 1.90% by the end of FY13. The risk weighted

stood at 46597 Cr, 56% to total assets.stood at 46597 Cr, 56% to total assets.stood at 46597 Cr, 56% to total assets.

Exhibit 22 : Tier I & II & Capital AdequacyExhibit 22 : Tier I & II & Capital Adequacy

13.50%15.00%11.88% 11.72% 11.75%

13.50%15.00%

10.43% 10.44%11.88% 11.72% 11.75%

13.11%

13.50%15.00%

10.43% 10.44%11.88% 11.72% 11.75%

13.11%13.00%

10.43% 10.44% 13.11%13.00%

10.00%12.74%

12.61%

13.00%10.00%

12.53%12.74%

12.61%12.50%

10.00%

12.53%12.34%

12.61%12.50%12.53%

12.34%12.50%

5.00%2.10% 1.90%

12.34%

12.00%5.00%

2.10% 1.90% 1.23% 1.02% 0.86%12.00%

5.00%1.90% 1.23% 1.02% 0.86%

12.00%

11.50%0.00% 11.50%0.00% 11.50%0.00%

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

Tier 1 Tier 2 Capital adequacyTier 1 Tier 2 Capital adequacy

Source: Perception ResearchSource: Perception ResearchSource: Perception Research

ConclusionConclusionConclusionConclusion

The bank’s asset quality remained stable sequentially, with a marginalThe bank’s asset quality remained stable sequentially, with a marginalThe bank’s asset quality remained stable sequentially, with a marginal

gross NPA ratio to 1.62% and 1bp decline in the net NPA ratiogross NPA ratio to 1.62% and 1bp decline in the net NPA ratiogross NPA ratio to 1.62% and 1bp decline in the net NPA ratio

levels were slightly higher at 140cr (for FY13 annualized slippagelevels were slightly higher at 140cr (for FY13 annualized slippagelevels were slightly higher at 140cr (for FY13 annualized slippage

for FY12). The bank’s PCR which is the highest in the industryfor FY12). The bank’s PCR which is the highest in the industryfor FY12). The bank’s PCR which is the highest in the industryfor FY12). The bank’s PCR which is the highest in the industry

sequential basis (yoy) by 97bp to 91.41%.sequential basis (yoy) by 97bp to 91.41%.sequential basis (yoy) by 97bp to 91.41%.

of 12.35% with Tier 1 atof 12.35% with Tier 1 atof 12.35% with Tier 1 atof 12.35% with Tier 1 at

weighted assets for FY13 isweighted assets for FY13 isweighted assets for FY13 is

Exhibit 23 : RWA, RWA to total assetsExhibit 23 : RWA, RWA to total assets

69783 65%80000 69783 65%80000

58634

69783 65%80000

48652

5863462%60000

46597 4865260%

62%

60%60000

3924446597 48652

60% 60%60000

3924458%

60% 60%

40000 58%40000

55%56% 55%

40000

55%56% 55%

2000055% 55%

2000020000

50%0 50%0 50%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16ERisk weighted assets RWA / Total assetsRisk weighted assets RWA / Total assets

Source: Perception ResearchSource: Perception ResearchSource: Perception Research

marginal increase of 8bp inmarginal increase of 8bp inmarginal increase of 8bp in

ratio to 0.14%. The slippageratio to 0.14%. The slippageratio to 0.14%. The slippage

slippage ratio of 1.16% v/s 0.95slippage ratio of 1.16% v/s 0.95slippage ratio of 1.16% v/s 0.95

industry by FY13, improved on aindustry by FY13, improved on aindustry by FY13, improved on aindustry by FY13, improved on a

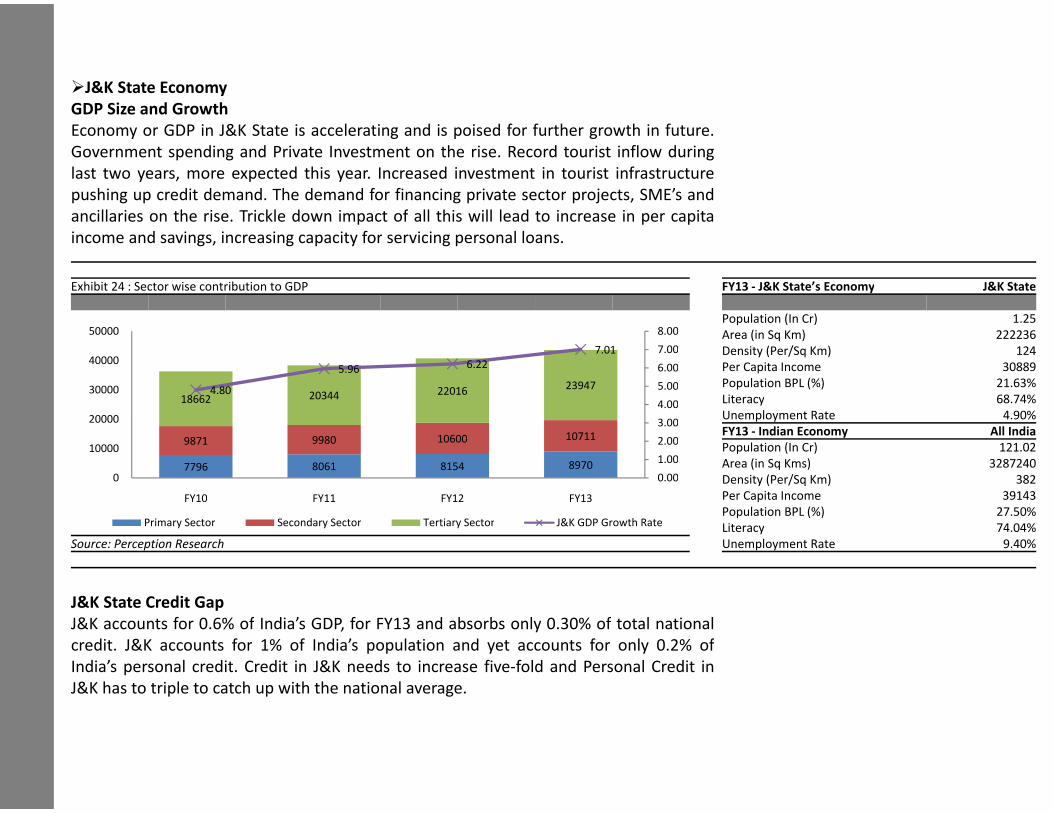

�J&K State Economy�J&K State Economy�J&K State Economy

GDP Size and GrowthGDP Size and GrowthGDP Size and GrowthGDP Size and Growth

Economy or GDP in J&K State is accelerating and is poised forEconomy or GDP in J&K State is accelerating and is poised forEconomy or GDP in J&K State is accelerating and is poised for

Government spending and Private Investment on the rise. RecordGovernment spending and Private Investment on the rise. RecordGovernment spending and Private Investment on the rise. Record

last two years, more expected this year. Increased investmentlast two years, more expected this year. Increased investmentlast two years, more expected this year. Increased investmentlast two years, more expected this year. Increased investment

pushing up credit demand. The demand for financing private sectorpushing up credit demand. The demand for financing private sectorpushing up credit demand. The demand for financing private sector

ancillaries on the rise. Trickle down impact of all this will leadancillaries on the rise. Trickle down impact of all this will leadancillaries on the rise. Trickle down impact of all this will lead

income and savings, increasing capacity for servicing personal loansincome and savings, increasing capacity for servicing personal loansincome and savings, increasing capacity for servicing personal loansincome and savings, increasing capacity for servicing personal loans

Exhibit 24 : Sector wise contribution to GDPExhibit 24 : Sector wise contribution to GDPExhibit 24 : Sector wise contribution to GDP

5000050000

6.22400005.96 6.22400005.96 6.22

220164.803000018662 20344 220164.803000018662 20344 220164.80

2000020000

9871 9980 10600

20000

9871 9980 1060010000

9871 9980 1060010000

7796 8061 8154

10000

7796 8061 81540

7796 8061 815400

FY10 FY11 FY12FY10 FY11 FY12

Primary Sector Secondary Sector Tertiary SectorPrimary Sector Secondary Sector Tertiary Sector

Source: Perception Research

Primary Sector Secondary Sector Tertiary Sector

Source: Perception ResearchSource: Perception Research

J&K State Credit GapJ&K State Credit GapJ&K State Credit GapJ&K State Credit Gap

J&K accounts for 0.6% of India’s GDP, for FY13 and absorbs onlyJ&K accounts for 0.6% of India’s GDP, for FY13 and absorbs onlyJ&K accounts for 0.6% of India’s GDP, for FY13 and absorbs only

credit. J&K accounts for 1% of India’s population and yet accountscredit. J&K accounts for 1% of India’s population and yet accountscredit. J&K accounts for 1% of India’s population and yet accounts

India’s personal credit. Credit in J&K needs to increase five-foldIndia’s personal credit. Credit in J&K needs to increase five-foldIndia’s personal credit. Credit in J&K needs to increase five-fold

J&K has to triple to catch up with the national average.J&K has to triple to catch up with the national average.J&K has to triple to catch up with the national average.J&K has to triple to catch up with the national average.

for further growth in future.for further growth in future.for further growth in future.

Record tourist inflow duringRecord tourist inflow duringRecord tourist inflow during

investment in tourist infrastructureinvestment in tourist infrastructureinvestment in tourist infrastructureinvestment in tourist infrastructure

sector projects, SME’s andsector projects, SME’s andsector projects, SME’s and

lead to increase in per capitalead to increase in per capitalead to increase in per capita

loans.loans.loans.loans.

FY13 - J&K State’s Economy J&K StateFY13 - J&K State’s Economy J&K StateFY13 - J&K State’s Economy J&K State

Population (In Cr) 1.25Population (In Cr) 1.25Population (In Cr) 1.25

Area (in Sq Km) 2222368.00 Area (in Sq Km) 2222368.00 Area (in Sq Km) 222236

Density (Per/Sq Km) 1247.01 7.00 Density (Per/Sq Km) 124

Per Capita Income 30889

7.01 7.00

Per Capita Income 308896.00 Per Capita Income 30889

Population BPL (%) 21.63%23947

6.00

Population BPL (%) 21.63%23947 5.00 Population BPL (%) 21.63%

Literacy 68.74%23947

4.00

5.00

Literacy 68.74%4.00 Literacy 68.74%

Unemployment Rate 4.90%3.00

4.00Unemployment Rate 4.90%

FY13 - Indian Economy All India3.00

FY13 - Indian Economy All India10711 2.00

3.00FY13 - Indian Economy All India

Population (In Cr) 121.0210711 2.00

Population (In Cr) 121.021.00

2.00Population (In Cr) 121.02

Area (in Sq Kms) 328724089701.00 Area (in Sq Kms) 3287240

Density (Per/Sq Km) 3828970

0.00

1.00

Density (Per/Sq Km) 3828970

0.00 Density (Per/Sq Km) 382

Per Capita Income 39143

0.00

Per Capita Income 39143FY13 Per Capita Income 39143

Population BPL (%) 27.50%FY13

Population BPL (%) 27.50%J&K GDP Growth Rate

Population BPL (%) 27.50%

Literacy 74.04%J&K GDP Growth Rate Literacy 74.04%

Unemployment Rate 9.40%

J&K GDP Growth Rate

Unemployment Rate 9.40%Unemployment Rate 9.40%

only 0.30% of total nationalonly 0.30% of total nationalonly 0.30% of total national

accounts for only 0.2% ofaccounts for only 0.2% ofaccounts for only 0.2% of

fold and Personal Credit infold and Personal Credit infold and Personal Credit in

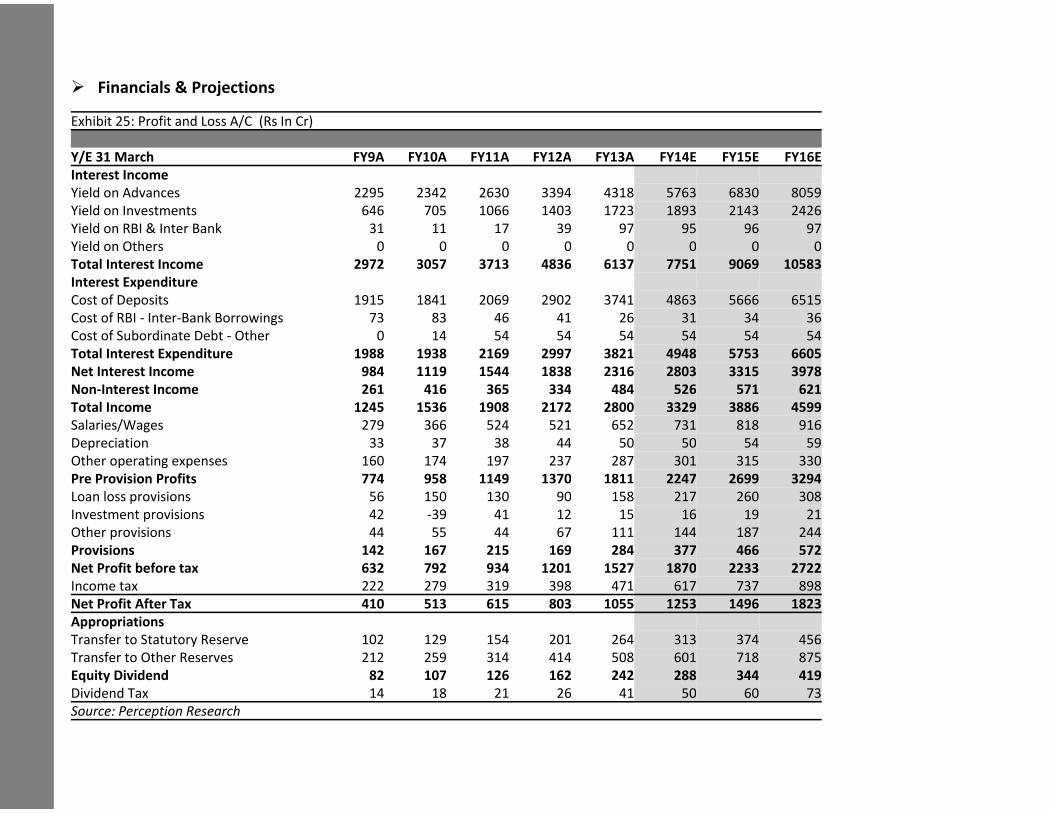

� Financials & Projections� Financials & Projections� Financials & Projections

Exhibit 25: Profit and Loss A/C (Rs In Cr)Exhibit 25: Profit and Loss A/C (Rs In Cr)Exhibit 25: Profit and Loss A/C (Rs In Cr)

Y/E 31 March FY9A FY10A FY11AY/E 31 March FY9A FY10A FY11AY/E 31 March FY9A FY10A FY11A

Interest IncomeInterest IncomeInterest Income

Yield on Advances 2295 2342 2630Yield on Advances 2295 2342 2630Yield on Advances 2295 2342 2630

Yield on Investments 646 705 1066Yield on Investments 646 705 1066

Yield on RBI & Inter Bank 31 11 17Yield on RBI & Inter Bank 31 11 17Yield on RBI & Inter Bank 31 11 17

Yield on Others 0 0 0Yield on Others 0 0 0Yield on Others 0 0 0

Total Interest Income 2972 3057 3713Total Interest Income 2972 3057 3713Total Interest Income 2972 3057 3713

Interest ExpenditureInterest ExpenditureInterest Expenditure

Cost of Deposits 1915 1841 2069Cost of Deposits 1915 1841 2069Cost of Deposits 1915 1841 2069

Cost of RBI - Inter-Bank Borrowings 73 83 46Cost of RBI - Inter-Bank Borrowings 73 83 46Cost of RBI - Inter-Bank Borrowings 73 83 46

Cost of Subordinate Debt - Other 0 14 54Cost of Subordinate Debt - Other 0 14 54Cost of Subordinate Debt - Other 0 14 54

Total Interest Expenditure 1988 1938 2169Total Interest Expenditure 1988 1938 2169Total Interest Expenditure 1988 1938 2169

Net Interest Income 984 1119 1544Net Interest Income 984 1119 1544Net Interest Income 984 1119 1544

Non-Interest Income 261 416 365Non-Interest Income 261 416 365Non-Interest Income 261 416 365

Total Income 1245 1536 1908Total Income 1245 1536 1908Total Income 1245 1536 1908

Salaries/Wages 279 366 524Salaries/Wages 279 366 524

Depreciation 33 37 38Depreciation 33 37 38Depreciation 33 37 38

Other operating expenses 160 174 197Other operating expenses 160 174 197Other operating expenses 160 174 197

Pre Provision Profits 774 958 1149Pre Provision Profits 774 958 1149Pre Provision Profits 774 958 1149

Loan loss provisions 56 150 130Loan loss provisions 56 150 130Loan loss provisions 56 150 130

Investment provisions 42 -39 41Investment provisions 42 -39 41Investment provisions 42 -39 41

Other provisions 44 55 44Other provisions 44 55 44Other provisions 44 55 44

Provisions 142 167 215Provisions 142 167 215Provisions 142 167 215

Net Profit before tax 632 792 934Net Profit before tax 632 792 934Net Profit before tax 632 792 934

Income tax 222 279 319Income tax 222 279 319Income tax 222 279 319

Net Profit After Tax 410 513 615Net Profit After Tax 410 513 615Net Profit After Tax 410 513 615

AppropriationsAppropriations

Transfer to Statutory Reserve 102 129 154

Appropriations

Transfer to Statutory Reserve 102 129 154Transfer to Statutory Reserve 102 129 154

Transfer to Other Reserves 212 259 314Transfer to Other Reserves 212 259 314Transfer to Other Reserves 212 259 314

Equity Dividend 82 107 126Equity Dividend 82 107 126Equity Dividend 82 107 126

Dividend Tax 14 18 21Dividend Tax 14 18 21Dividend Tax 14 18 21

Source: Perception ResearchSource: Perception ResearchSource: Perception Research