Embed Size (px)

Citation preview

www.i5invest.com

FinTech in Austria and InternationallyOeNB September 2016

2 | 12/09/2016

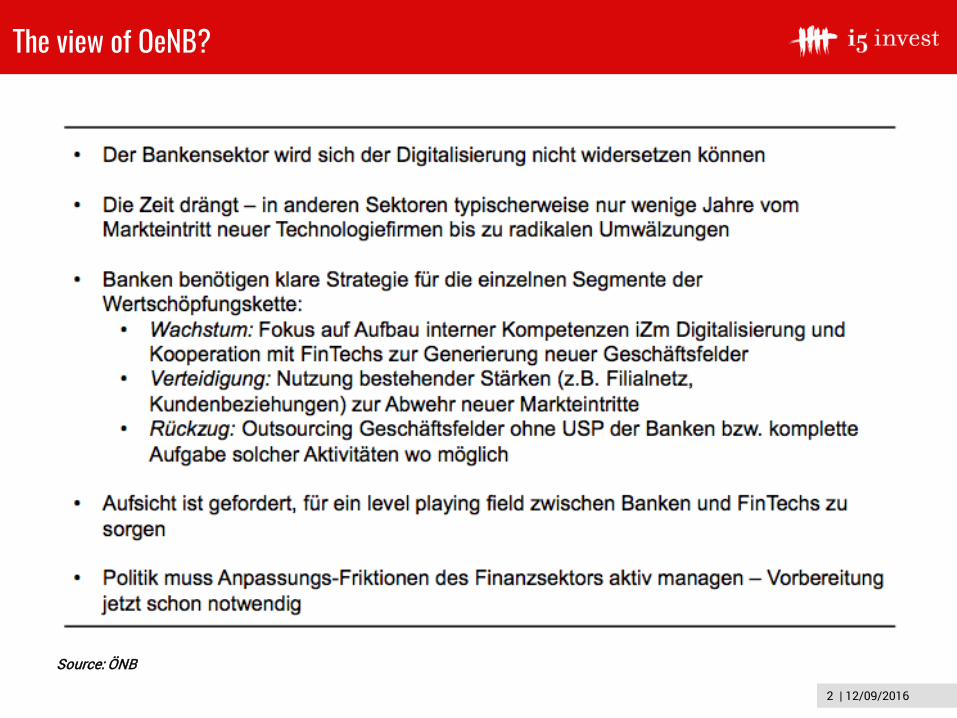

The view of OeNB?

Source: ÖNB

3 | 12/09/2016

Table of contents

Who we are1

3

Requirements and Challenges in FinTech2

4

Investments and Markets – International vs Austria

5

Current FinTech Trends

Regulation – Best Practices 6

FinTech Partnership Scenarios

Glossary – FinTech Terms7

4 | 12/09/2016

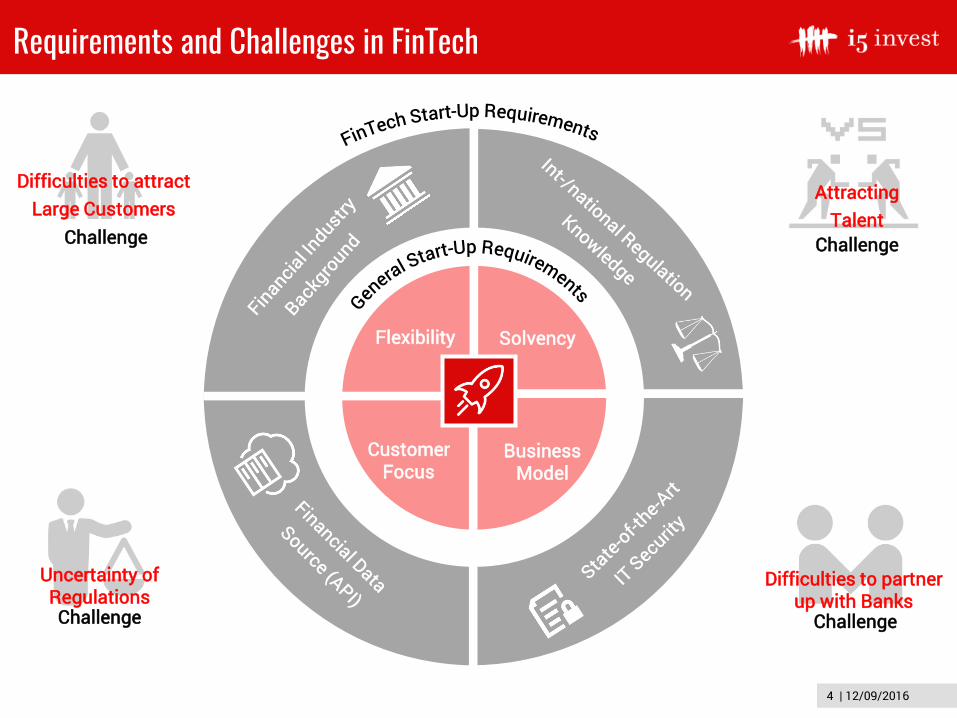

Requirements and Challenges in FinTech

Business Model

Customer Focus

SolvencyFlexibility

Attracting Talent

Uncertainty ofRegulations

Difficulties to partner up with Banks

Difficulties to attractLarge Customers

Challenge

Challenge

Challenge

Challenge

5 | 12/09/2016

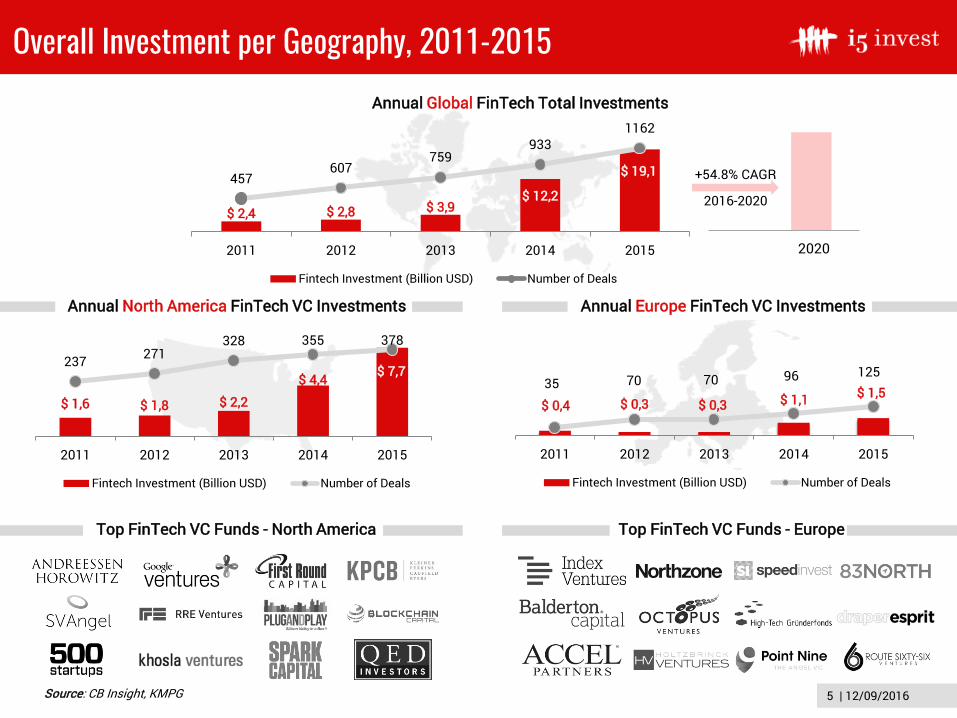

Overall Investment per Geography, 2011-2015

$ 2,4 $ 2,8 $ 3,9$ 12,2

$ 19,1457607

759933

1162

0

500

1000

1500

$ ,$ 5,

$ 10,$ 15,$ 20,$ 25,

2011 2012 2013 2014 2015

Fintech Investment (Billion USD) Number of Deals

Annual Global FinTech Total Investments

Annual North America FinTech VC Investments Annual Europe FinTech VC Investments

Top FinTech VC Funds - North America Top FinTech VC Funds - Europe

$ 1,6 $ 1,8 $ 2,2

$ 4,4 $ 7,7237 271

328 355 378

0

100

200

300

400

$ ,$ 1,$ 2,$ 3,$ 4,$ 5,$ 6,$ 7,$ 8,

2011 2012 2013 2014 2015

Fintech Investment (Billion USD) Number of Deals

$ 0,4 $ 0,3 $ 0,3 $ 1,1 $ 1,535 70 70 96 125

0

100

200

300

400

$ 0,$ 1,$ 2,$ 3,$ 4,$ 5,$ 6,$ 7,$ 8,

2011 2012 2013 2014 2015

Fintech Investment (Billion USD) Number of Deals

Source: CB Insight, KMPG

2020

+54.8% CAGR

2016-2020

6 | 12/09/2016

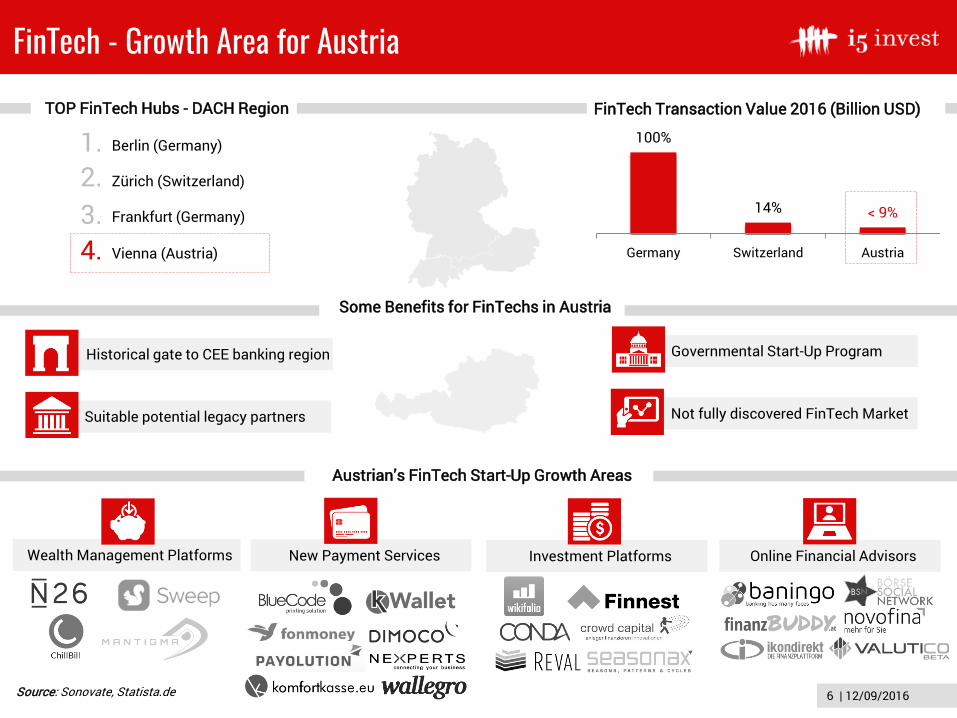

100%

14% < 9%$ 0,

$ 50,

$ 100,

$ 150,

Germany Switzerland Austria

FinTech - Growth Area for Austria

Source: Sonovate, Statista.de

Wealth Management Platforms New Payment Services Investment Platforms Online Financial Advisors

vAustrian’s FinTech Start-Up Growth Areas

1.2.3.4.

Berlin (Germany)

Zürich (Switzerland)

Frankfurt (Germany)

Vienna (Austria)

TOP FinTech Hubs - DACH Region FinTech Transaction Value 2016 (Billion USD)

Historical gate to CEE banking region Governmental Start-Up Program

Not fully discovered FinTech MarketSuitable potential legacy partners

vSome Benefits for FinTechs in Austria

7 | 12/09/2016

v

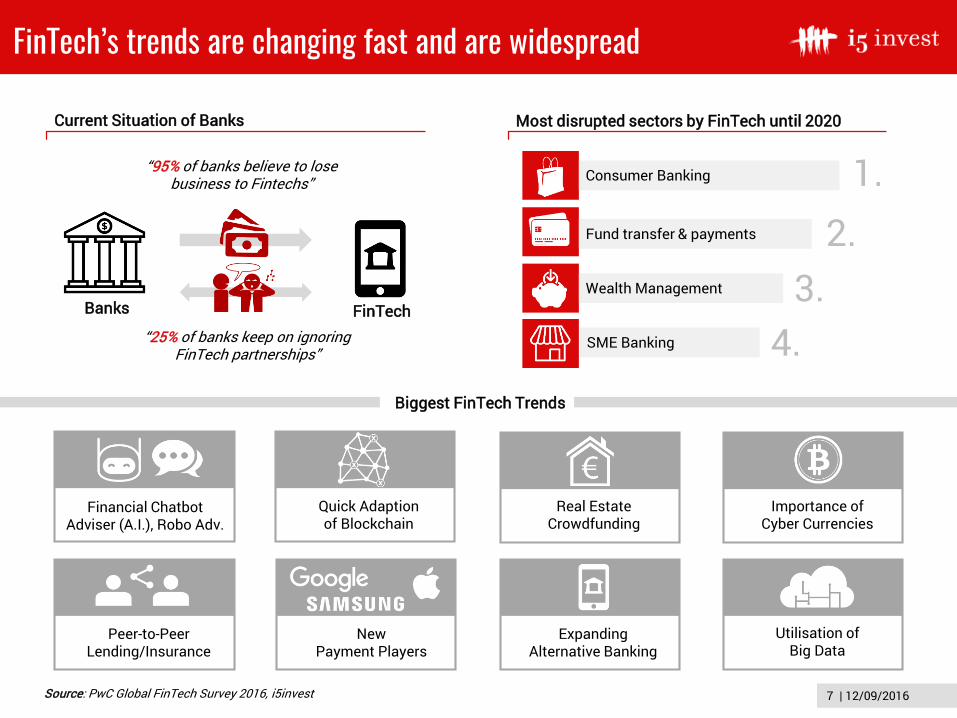

FinTech’s trends are changing fast and are widespread

“95% of banks believe to lose business to Fintechs”

“25% of banks keep on ignoring FinTech partnerships”

Banks FinTech

Consumer Banking

Fund transfer & payments

Wealth Management

SME Banking

1.2.

3.4.

Current Situation of Banks

Biggest FinTech Trends

Financial ChatbotAdviser (A.I.), Robo Adv.

Peer-to-PeerLending/Insurance

Quick Adaptionof Blockchain

New Payment Players

Real EstateCrowdfunding

Expanding Alternative Banking

Importance ofCyber Currencies

Utilisation of Big Data

Most disrupted sectors by FinTech until 2020

Source: PwC Global FinTech Survey 2016, i5invest

8 | 12/09/2016

v

Partnerships will be key in the future of BFSI

Non-/ and FinTech Start-Ups Large Banks and FinTechs Large Banks and Tech-Players

Information Technology is taking an ever more important part in the financial industry.Partnerships are therefore needed because

Differences in Management & Culture

Differences in Operational Processes

Regulatory Uncertainty IT Security

Bank’s biggest reservations regarding FinTech Partnerships

Source: PwC Global FinTech Survey 2016, i5invest

1. 2. 3. 4.

Customers get more digitalized

FinTechs only focus on one part of the supply chain

Partnerships are therefore needed between

Cost reduction and higher efficiency

“Enables n26’s customers to transfer money abroad in

different currencies”

“Enables myGeorge users to predict their future

account balance”

“Provides Barclays’ customers with new mobile commerce

and payments solutions”

The IT and Finance markets are broad

9 | 12/09/2016

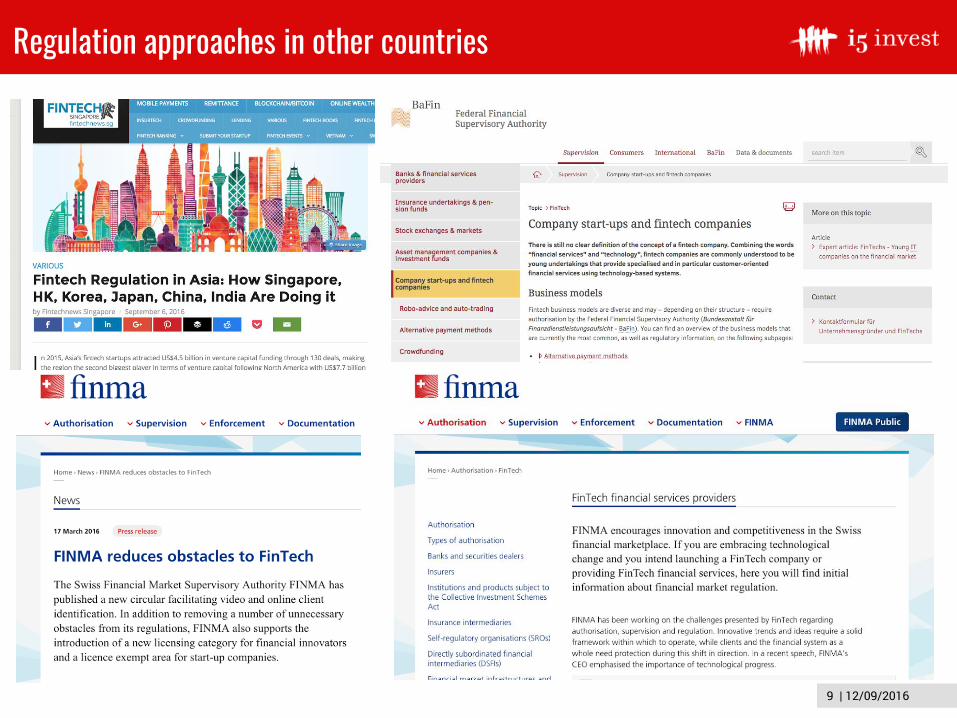

Regulation approaches in other countries

10 | 12/09/2016

How to ensure a safe regulative environment

Direct communication between regulators and fintechs.

Offer fast and transparent regulatory review of potential new fintech products or services.

Create a support system or kit to help fintech startups meet regulatory requirements.

Roll out consumer awareness initiatives to increase demand.

Encourage traditional financial institutions to invest in or partner with fintech startups — preferably non-exclusively.

1.

2.

3.

4.

5.

FMA FinTech

Regulation

www.i5invest.com

Follow us on