Embed Size (px)

Citation preview

Industrial Cluster Development in Lao PDR: Opportunities and Chal-

lenges

Byoungki KimShiga UniversityJapan

Parallel Session 1.5: Accelerating Cluster Growth in Asian Countries

The Lao government has realized that promoting cluster formation is important for regional development in the future. The government has formed many Special Economic Zones (SEZ) with Public Private Partnerships (PPP) for joint development between the government and private sector in the delivery of public goods, infrastructure and services.

Incentives to attract firms• General customs and tax system• Fiscal incentives• Specific promotion incentivesIncentives to attract migration near the SEZs• Providing transport, electricity and water service

Promoting Industrial Location

Why is forming industrial clusters difficult in less developed countries such as Lao PDR?

Lao PDR• Size: 236,800 (100,210 Korea) Km2• Population: 6.8 (50.6 Korea) million person• GDP per capita: 1,785 US$

Vientiane Capital• Size: 3,920 (884 Daegu) Km2• Population: 797 (2,518 Daegu) 1000 person• Many SEZs have been established

Lao PDRLao is a land-locked country with inadequate infrastructure and a small population. Lao has introduced the New Economic Mechanism which shifted from a planned economy to a market-oriented economy in 1986. Locality of industry heavily depends on the population and transportation infrastructure.

https://en.wikipedia.org/wiki/Cochinchina

Source: Lao Ministry of Planning and Investment

Electricity Generation

6,671

Mining5,687

Agricultu

re

2,770

Service2,533

Industry & Handicraft1,972

Others 1,363

Construction 826

Hotel &

Restaurant 1,023

Telecommunication

663

FDI by Countries & Sectors(1989-2014, US$ million)

Country Projects Value1 China 830 5,3962 Thailand 746 4,4553 Vietnam 421 3,3944 Korea 291 7515 France 223 4916 Japan 102 4387 Netherlands 16 4348 Malaysia 101 3829 Norway 6 346

10 UK 52 198TOTAL 2,788 16,287

(Total 23,509 US$ million)

Lao introduced FDI Law in 1988. Since then the flow of FDI has increased sharply.

Lao Ministry of Planning and Investment

Specail Economic Zone Establish Amount Investor1 Savan-Seno Special Economic Zone 2003 74 Government 100%

2 Boten Beautiful Land Specific Economic Zone 2003 500 Private 100% (China)

3 Golden Triangle Special Economic Zone 2007 87 Gvernment + Private (China)

4 Vientiane Industrial and Trade Area 2011 43 Government + Private (Taiwan)

5 Saysetha Development Zone 2010 128 Government + Private (Lao & China)

6 Phoukhyo Specific Economic Zone 2010 100 Private 100% (Lao)

7 Thatluang Lake Specific Economic Zone 2011 1,600 Private 100% (China)

8 Longthanh- Vientiane Specific Economic Zone 2012 1,000 Private 100% (Vietnema)

9 Dongphosy Specific Economic Zone 2012 50 Private 100% (Malaysia)

10 Thakhek Specific Economic Zone 2012 80 Government 100%

Special Economic Zones

(mil US$)

Savan - Seno SEZis the first SEZ

Market-oriented economy• Leading industry has been the agriculture• Outputs of the secondary industry

increasedNatural resources were found• Mining industry greatly outgrew the

manufacturing sector.ADB Greater Mekong Sub-region

Savan - Seno SEZ

Service Sector• Banking, Financial Institution and Insurance, Tourism Promotion Service,

Hotel, Resort, Restaurant, Amusement Park, Entertainment Center, Sport Center, Conference Hall, Skills Center, School, Hospital

Trade Sector• Duty Free Shop, Duty Free Border Trade, Exhibition -Trade Promotion

Center, Wholesale-Retail Store, Department StoreDistribution Logistics Service Sector • Transportation Business, Distribution Service, Warehouse, Cool StorageIndustrial Sector• Electrical Wire, Manufacturing Factory, Food-Processing Factory, Wood

Products Industry, Textile, Shoe, Bag, Manufacturing Plant, Automobile Assembly, Plant and other Electronic, Parts Assembly Plant

• 57 companies invested more than US$200 million for establishing factories in the zone. (September 2015)

• Creating more than 1,600 jobs.• The value of products exported in the past 2 years more than US$50

million.

IMF, World Economic Outlook Database, Oct 2015 (2015 estimated)UN, World Population Prospects: The 2015 Revision (2015 estimated)

10 40 80 1300

8000

6000

4000

2000

China8,280$ 1,376

Thailand5,426$ 68

Vietnam2,171$ 93

Lao1,785$ 6.8 Cambodia

1,140$ 16

Myanmar1,269$ 54

Population (mil)

GDP per capita (current US$)

Industrial Clusters

Industrial Clusters

Industrial Clusters

SEZ(China + 1) (Thai + 1)

Branch Plant Economic Zone• Increasing labor cost• Political instability• Natural disaster

complementary

Lao

Thailand

1stproduction

stage

2nd

productionstage

finalproduction

stage

3rd

productionstage

Tax exemption

Domesticor

Export

Manufacturing sectors are strongly reliant on outside expertise and resources, for example from China, Thailand and Vietnam may lead to proportionately less research and development spending in Laos.

Branch Plant Economic Zone

SEZ

Procurement of Raw Materials and Parts

Source: JETRO (Japan External Trade Organization)

China

Indonesia

India

Malaysia

Thailand

Vietnam

Laos

Cambodia

0 10 20 30 40 50 60 70 80 90 100

Local Japan ASEAN China other

Lao

Vertical cluster (supply chain) has some comparative advantages in labor cost and various incentives for suppliers, but disadvantages with transportation costs.

SEZs in Lao are located in border district, most of them are at border with Thailand. An SEZ in border area in Lao side can be a local city in Thailand from the economic point of view (cross border facilities like international bridges and custom services have been developed). • Low-cost labor (labor intensive goods)• Insufficient Human resource development• Insufficient research institute• Firms from various fields are concentrated• Small number of firms are participating (less competition) Competitive firms do not want to participate to the SEZ

Branch Plant Economic Zone

Bangkok

Hanoi

Hochim

inhDanan

Vientiane

Phnom penh

Yangon0

50

100

150

200

Legal minimum wage

Bangkok

Hanoi

Hochim

inhDanan

Vientiane

Phnom penh

Yangon0.00

0.05

0.10

0.15

0.20

0.25

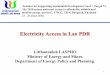

Electricity

Bangkok

Hanoi

Hochim

inhDanan

Vientiane

Phnom penh

Yangon0

20

40

60

80

100

Office rental

Bangkok

Hanoi

Hochim

inhDanan

Vientiane

Phnom penh

Yangon0

500

1,000

1,500

2,000

2,500

Transportation freightTo Yokohama40ft container

Source: JETRO (Japan External Trade Organization)

Comparison of Costs1kwh

US$

M2/month

month

Vientiane

Vientiane

Vientiane

Vientiane

Lao is disadvantaged for industrial expansion because of it’s geographical location, insufficient human resource development including labor supply.

From the Land-locked to the Land-linked Nation

• High value-added clusters using local resources e.g., Precision instrument industry, industry relate to hydropower, Jewelry and agro-industry should be encouraged.

• Specialized resources are often specific for an industry and important for its competitiveness. And specific resources can be created to compensate for factor disadvantages.

• Wide range clusters including Thai-Lao, Lao-China, and Thai-Lao-China would also be advantageous to the development of industrial clusters in Indochina peninsula. https://en.wikipedia.org/wiki/Cochinchina