Embed Size (px)

Citation preview

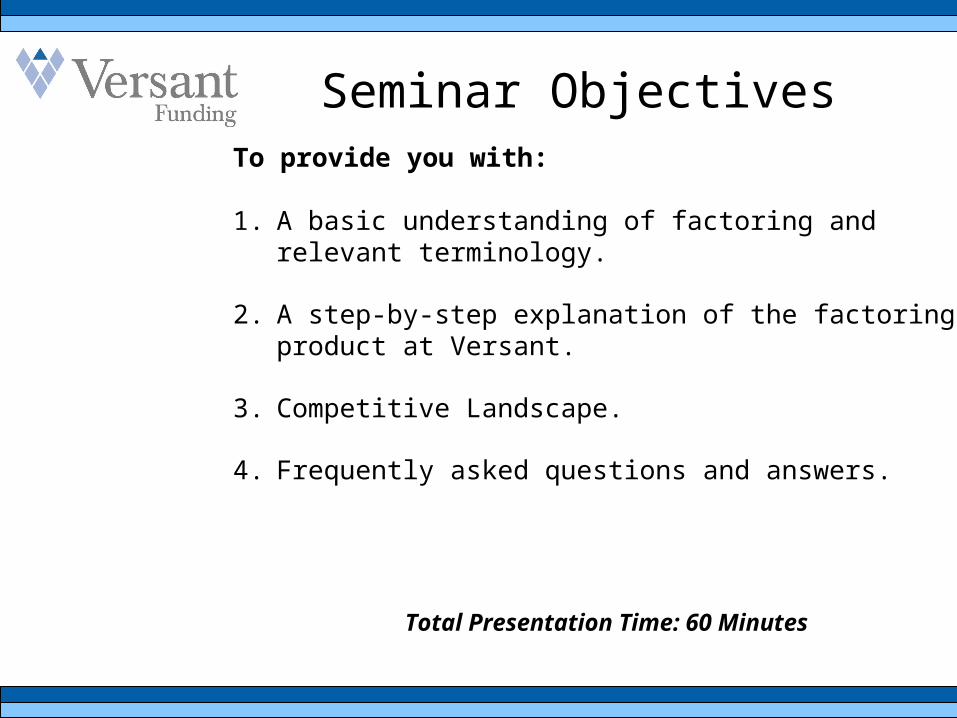

Seminar ObjectivesTo provide you with:

1. A basic understanding of factoring and relevant terminology.

2. A step-by-step explanation of the factoring product at Versant.

3. Competitive Landscape.

4. Frequently asked questions and answers.

Total Presentation Time: 60 Minutes

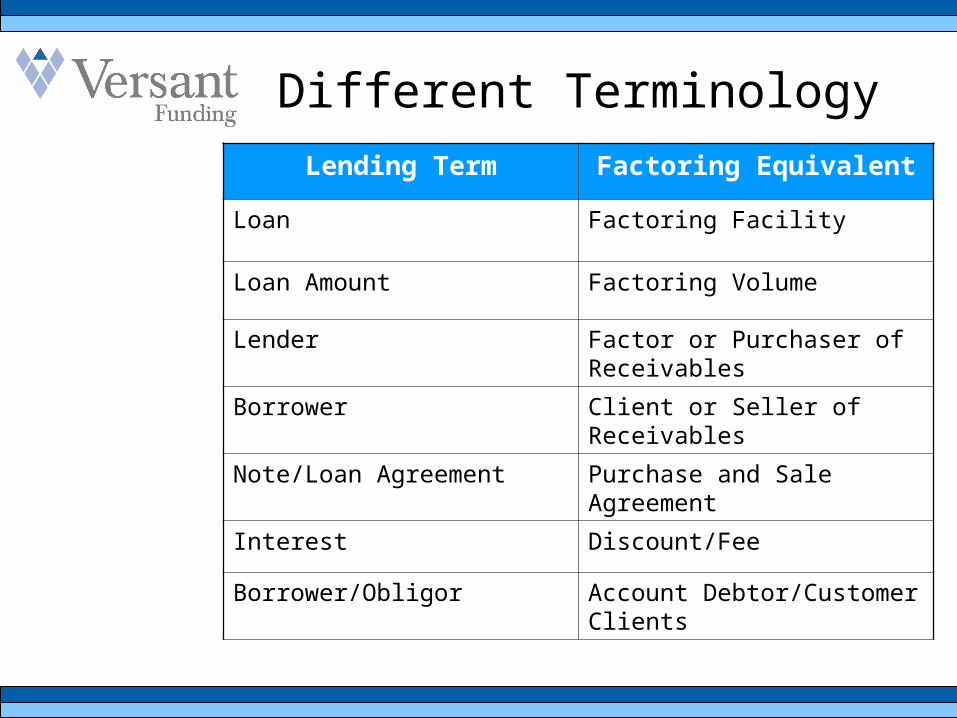

Different Terminology

Lending Term Factoring Equivalent

Loan Factoring Facility

Loan Amount Factoring Volume

Lender Factor or Purchaser of Receivables

Borrower Client or Seller of Receivables

Note/Loan Agreement Purchase and Sale Agreement

Interest Discount/Fee

Borrower/Obligor Account Debtor/Customer Clients

What is Factoring?

The sale of a company's accounts receivable invoices to a factor, in order to obtain working capital.

Although there are numerous types of factoring; Versant offers full notification, non-recourse

factoring. This means that account debtors (customers of the client company) are notified to pay Versant directly while the credit risk of non payment is assumed by Versant.

Prospective Client Profile• Small to medium-sized companies with annual revenues of $1

million to $50 million.

• Businesses that need liquidity quickly who cannot wait 30, 60, or 90 days for payment of their accounts receivable.

• Businesses that need funds but have limited access to traditional credit markets due to lack of track record, limited capital base, or poor earnings history – typically: – Start-up companies– Fast-growing companies– Seasonal businesses– Companies that have experienced losses

• Client’s customers are typically large corporations, municipalities or other government agencies.

• With the exception of the medical and construction fields - Versant will provide factoring to a wide-range of industries with good quality receivables.

How Can Versant Help Your Clients?

• Versant’s unique factoring product can provide immediate liquidity for your clients.– A typical deal can be closed and funded within five

business days of the initial referral.

• Factoring transactions will typically range in size between $1million to $30 million in sales on an annual basis. Versant will fund larger transactions if the circumstances are appropriate.

• Versant’s factoring product is non-recourse to the client and does not require an audit of the client’s business financial performance.

Typical Use of Factoring Funds

• Project Financing

• Business Growth Financing

• Business Acquisition Financing

• Bridge Financing

• Financing Working Capital Needs

• Realization of Supplier Discounts

• Preparation for High Season

• Crisis Management

• Debtor-In-Possession (DIP) Financing

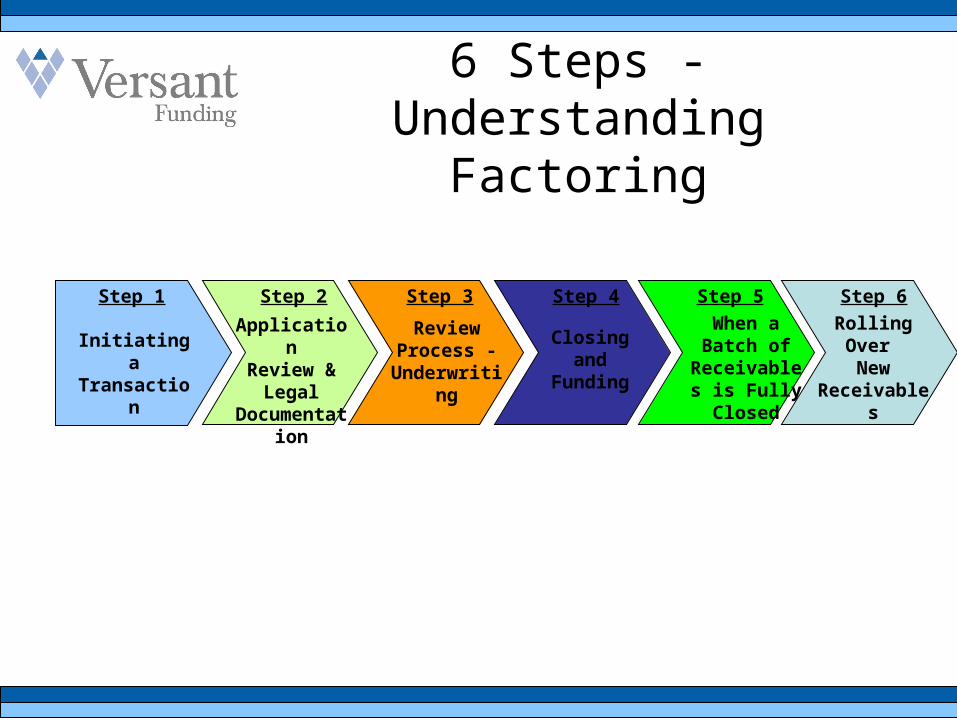

6 Steps - Understanding Factoring

Initiating a Transaction

Step 1 Step 2

Review Process - Underwriting

Step 3

ApplicationReview &

Legal Documentation

Step 4

Closing andFunding

Step 5 When a Batch of Receivables is Fully Closed

Step 6 Rolling Over

New Receivables

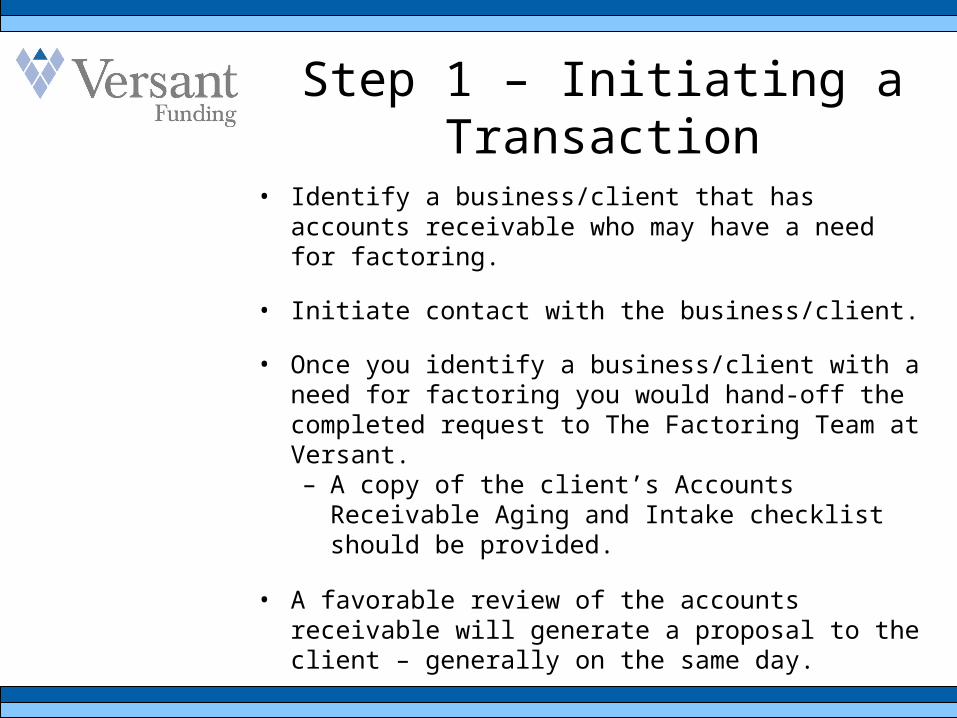

Step 1 – Initiating a Transaction

• Identify a business/client that has accounts receivable who may have a need for factoring.

• Initiate contact with the business/client.

• Once you identify a business/client with a need for factoring you would hand-off the completed request to The Factoring Team at Versant. – A copy of the client’s Accounts Receivable Aging

and Intake checklist should be provided.

• A favorable review of the accounts receivable will generate a proposal to the client – generally on the same day.

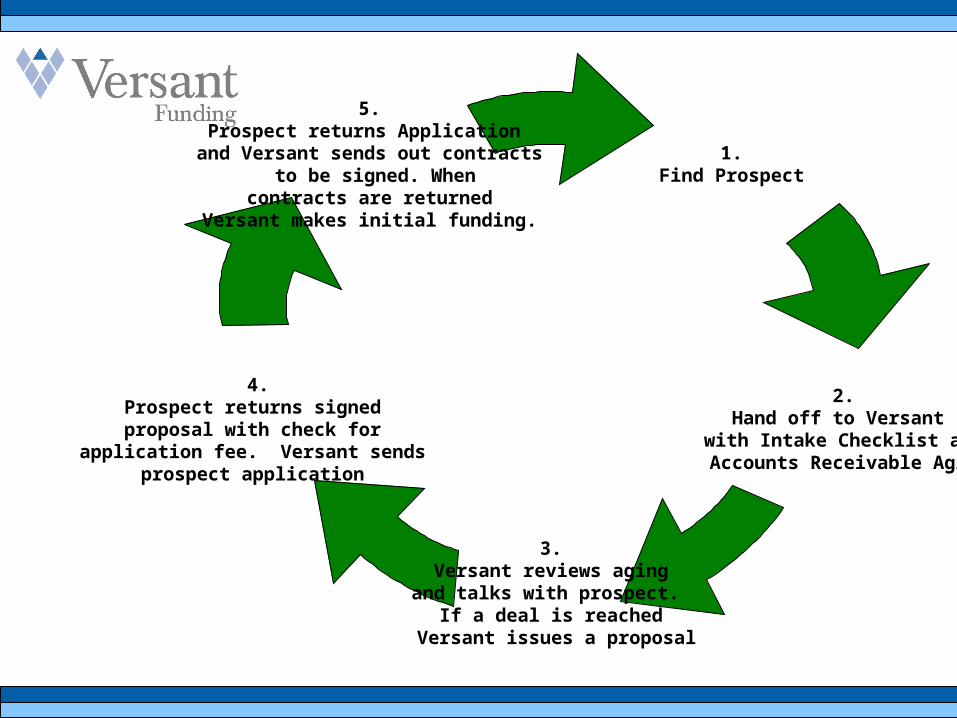

1.Find Prospect

2.Hand off to Versant

with Intake Checklist and Accounts Receivable Aging

5.Prospect returns Application

and Versant sends out contracts to be signed. When

contracts are returned Versant makes initial funding.

3.Versant reviews aging

and talks with prospect. If a deal is reached

Versant issues a proposal

4.Prospect returns signed proposal with check for

application fee. Versant sends prospect application

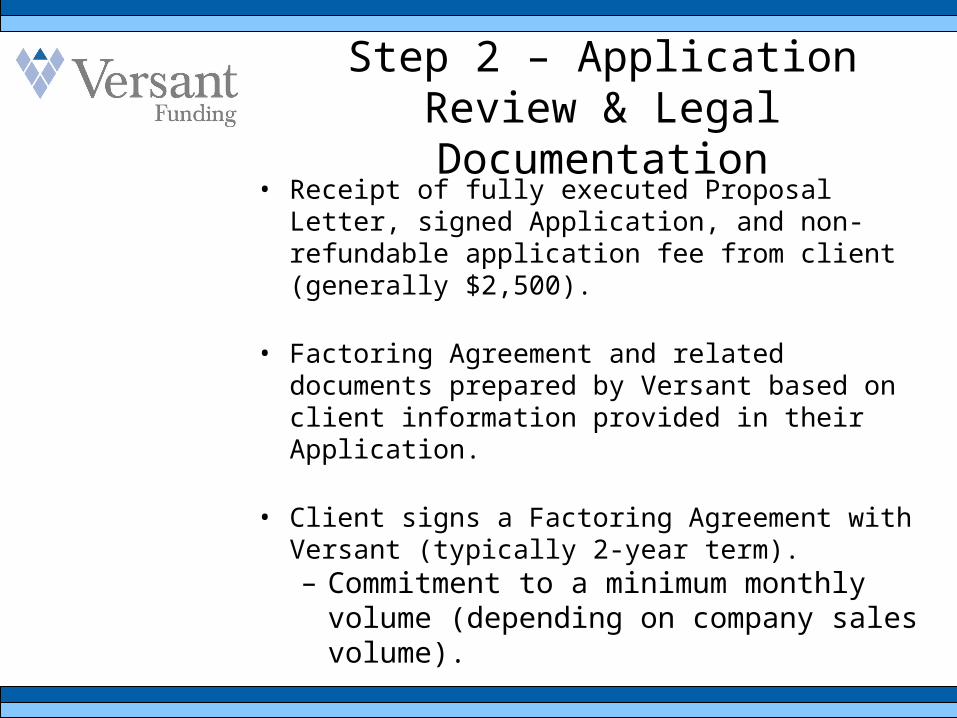

Step 2 – Application Review & Legal Documentation

• Receipt of fully executed Proposal Letter, signed Application, and non-refundable application fee from client (generally $2,500).

• Factoring Agreement and related documents prepared by Versant based on client information provided in their Application.

• Client signs a Factoring Agreement with Versant (typically 2-year term).– Commitment to a minimum monthly

volume (depending on company sales volume).

Step 3 – Review Process - Underwriting

• Client delivers Accounts Receivable Aging of receivables to be factored.

• Public records search of UCC filings and liens.

• Account Debtor (customer) credit review is conducted.

• Receivable verification (Versant conducts calls to account debtors).

• Purchase and sale agreement for each batch of receivables is executed.

• Performance guarantee by principals/operators to deliver conforming goods and proper services to debtor.– This is a non-recourse transaction - no personal

guarantee of credit for the accounts receivable is required - Versant assumes the credit risk.

Step 3 – Review Process - Underwriting

• 100% Security Interest taken on all of the assets of the client. Versant will subordinate on all assets other than the A/R if required by another lender.

• Package of invoices, purchase orders, delivery receipts and accounts receivable aging report delivered.

• Original invoices with Versant assignment sticker mailed to account debtors.

• Notification of assignment of accounts receivable prepared, sent via certified mail (return receipt requested) and faxed (confirmation receipt retained).

• Receivables selected and batched.

• UCC filed.

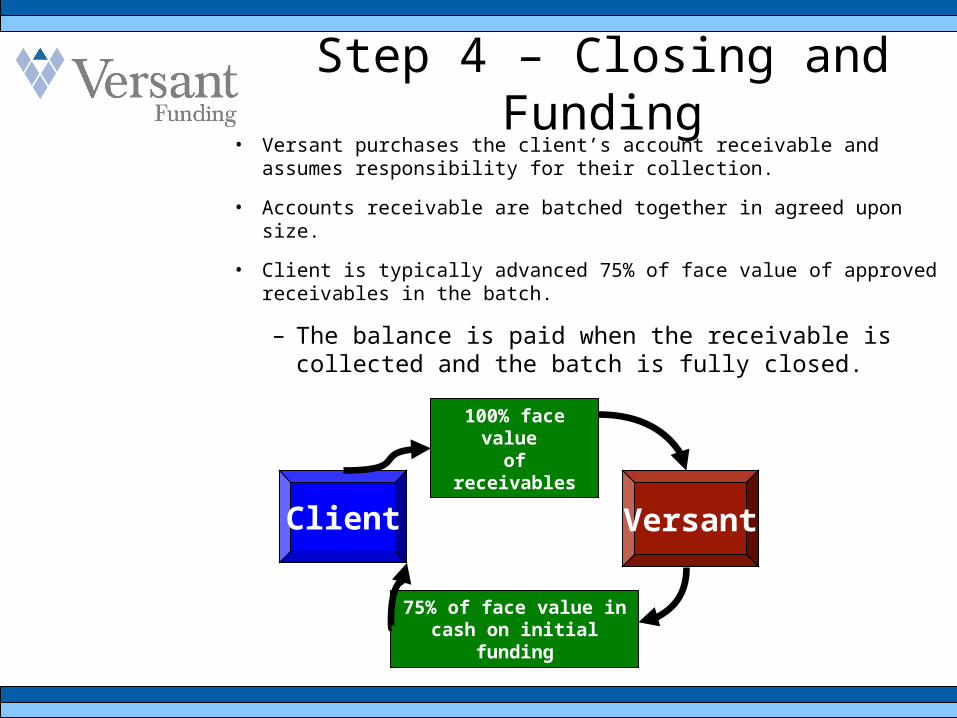

Step 4 – Closing and Funding

• Versant purchases the client’s account receivable and assumes responsibility for their collection.

• Accounts receivable are batched together in agreed upon size.

• Client is typically advanced 75% of face value of approved receivables in the batch.

– The balance is paid when the receivable is collected and the batch is fully closed.

100% face value of receivables

Versant

75% of face value in cash on initial funding

Client

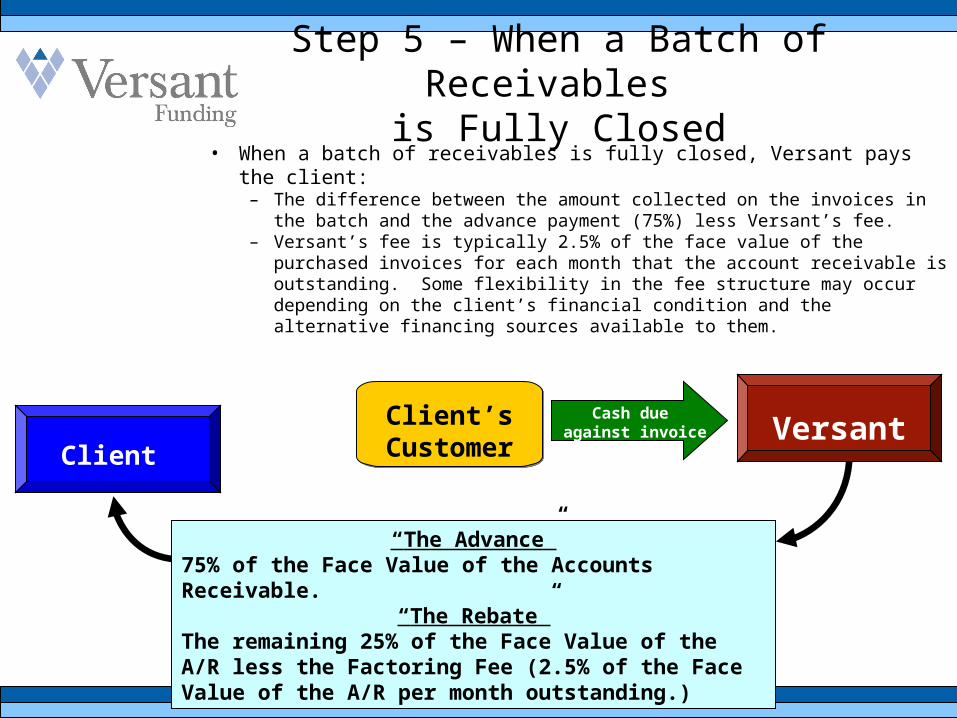

Step 5 – When a Batch of Receivables is Fully Closed

• When a batch of receivables is fully closed, Versant pays the client:– The difference between the amount collected on the invoices in the batch

and the advance payment (75%) less Versant’s fee.– Versant’s fee is typically 2.5% of the face value of the purchased invoices for

each month that the account receivable is outstanding. Some flexibility in the fee structure may occur depending on the client’s financial condition and the alternative financing sources available to them.

Client

Cash due against invoice

“The Advance”75% of the Face Value of the Accounts Receivable.

“The Rebate”The remaining 25% of the Face Value of the A/R less the Factoring Fee (2.5% of the Face Value of the A/R per month outstanding.)

Client’sCustomer

Versant

• Online platform (FactorSQL Software) enables clients to review reports and determine if/when it’s economical to close out aged receivables “batches.”

Step 5 – When a Batch of Receivables

is Fully Closed

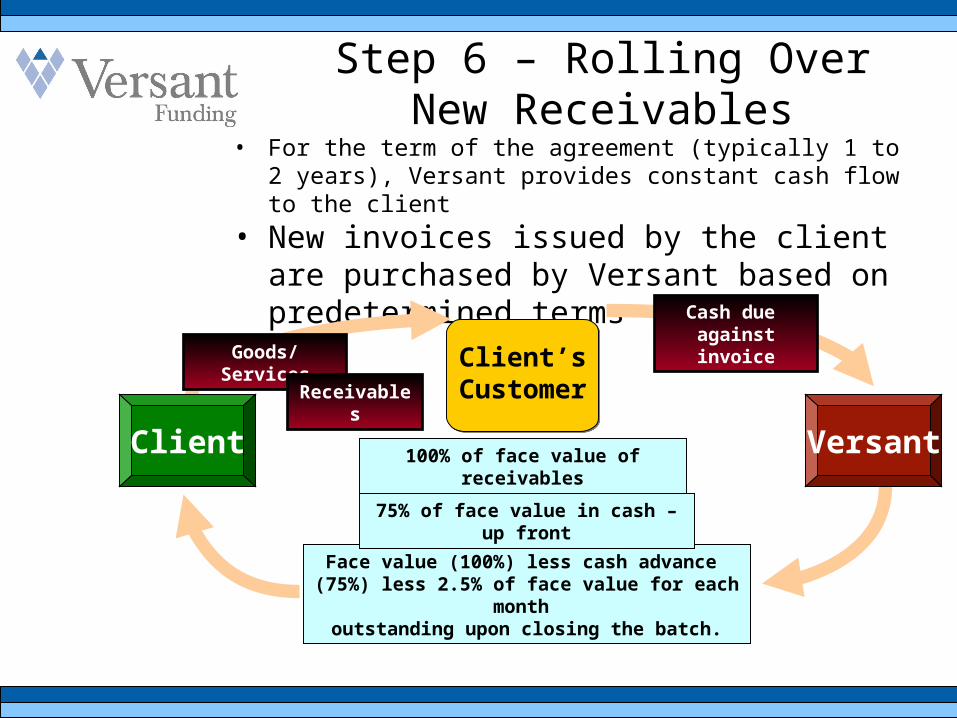

Step 6 – Rolling Over New Receivables

• For the term of the agreement (typically 1 to 2 years), Versant provides constant cash flow to the client

• New invoices issued by the client are purchased by Versant based on predetermined terms

Face value (100%) less cash advance (75%) less 2.5% of face value for each month

outstanding upon closing the batch.

Cash due against invoice

Goods/Services

Client

Receivables

75% of face value in cash – up front

100% of face value of receivables

Client’sCustomer

Versant

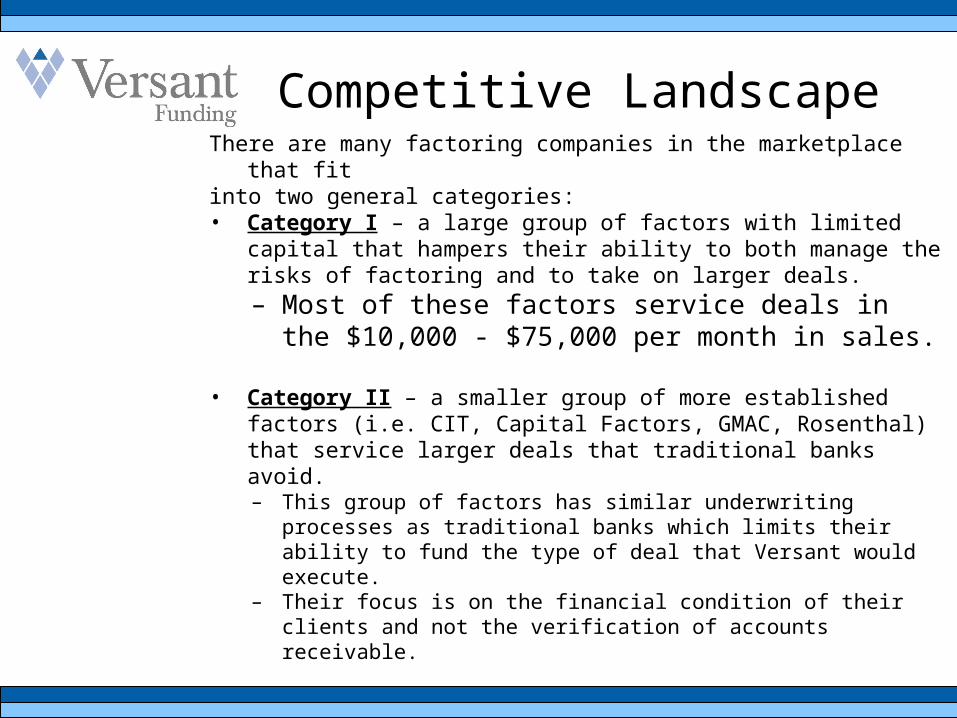

Competitive Landscape

Competitive LandscapeThere are many factoring companies in the marketplace that fit into two general categories:• Category I – a large group of factors with limited capital that

hampers their ability to both manage the risks of factoring and to take on larger deals. – Most of these factors service deals in the

$10,000 - $75,000 per month in sales.

• Category II – a smaller group of more established factors (i.e. CIT, Capital Factors, GMAC, Rosenthal) that service larger deals that traditional banks avoid. – This group of factors has similar underwriting processes as

traditional banks which limits their ability to fund the type of deal that Versant would execute.

– Their focus is on the financial condition of their clients and not the verification of accounts receivable.

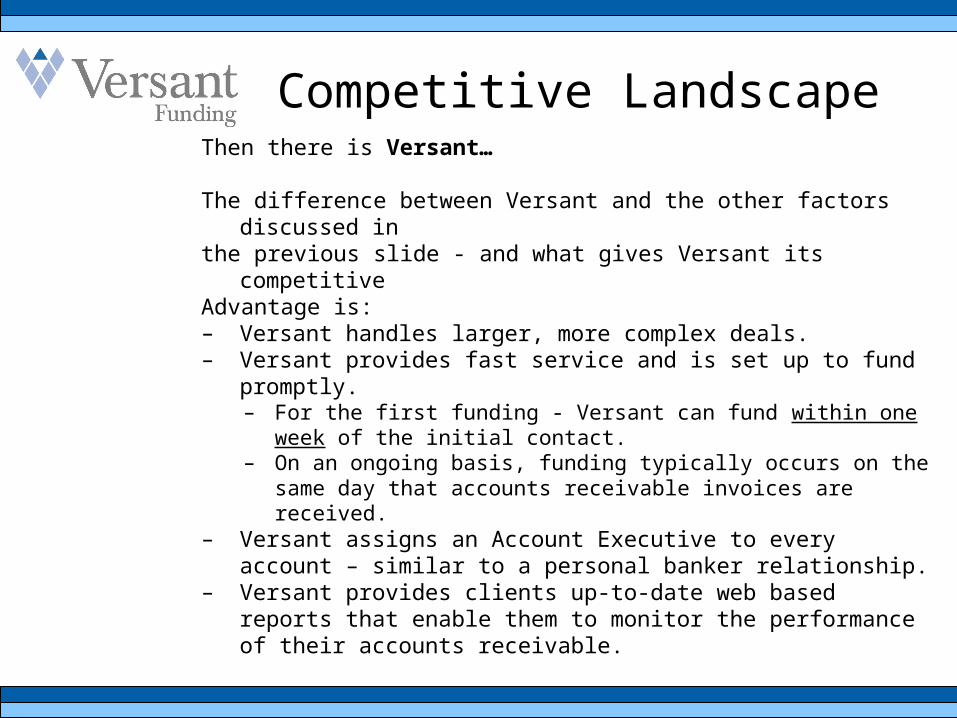

Competitive LandscapeThen there is Versant…

The difference between Versant and the other factors discussed in

the previous slide - and what gives Versant its competitive Advantage is:– Versant handles larger, more complex deals.– Versant provides fast service and is set up to fund promptly.

– For the first funding - Versant can fund within one week of the initial contact.

– On an ongoing basis, funding typically occurs on the same day that accounts receivable invoices are received.

– Versant assigns an Account Executive to every account – similar to a personal banker relationship.

– Versant provides clients up-to-date web based reports that enable them to monitor the performance of their accounts receivable.

Frequently Asked Questions and Answers

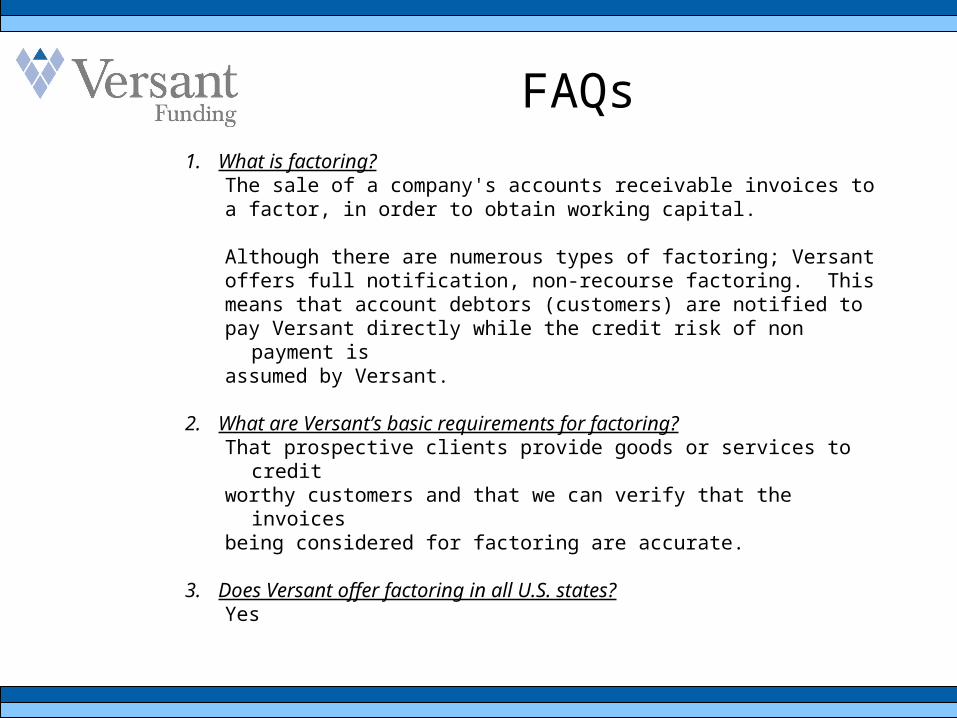

FAQs1. What is factoring?

The sale of a company's accounts receivable invoices to a factor, in order to obtain working capital.

Although there are numerous types of factoring; Versant offers full notification, non-recourse factoring. This means that account debtors (customers) are notified to pay Versant directly while the credit risk of non payment is assumed by Versant.

2. What are Versant’s basic requirements for factoring?That prospective clients provide goods or services to credit worthy customers and that we can verify that the invoices being considered for factoring are accurate.

3. Does Versant offer factoring in all U.S. states?Yes

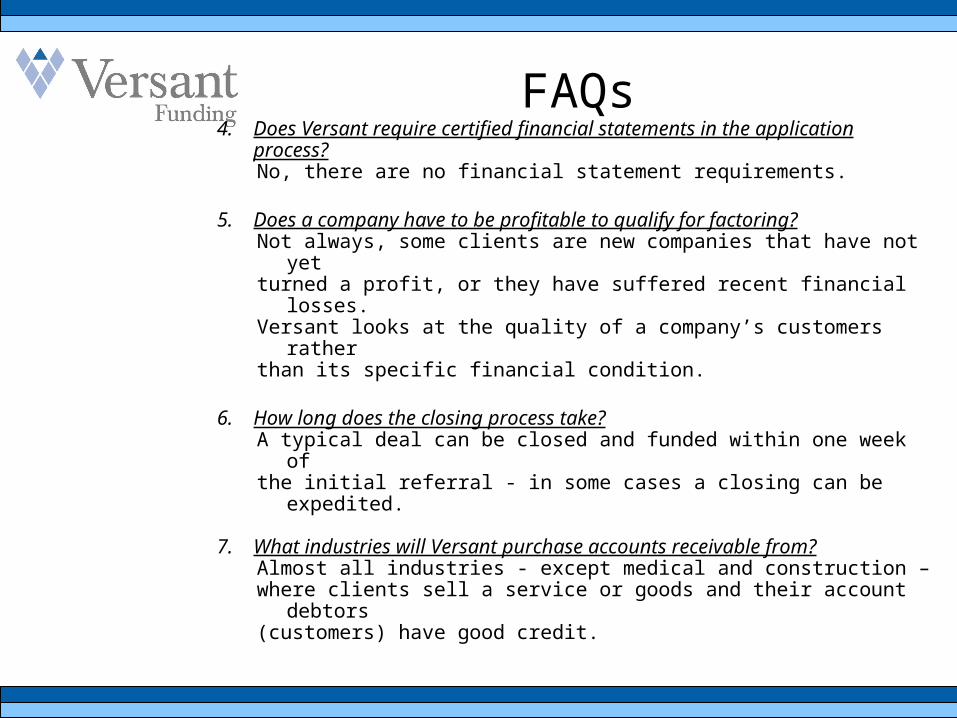

FAQs4. Does Versant require certified financial statements in the

application process?No, there are no financial statement requirements.

5. Does a company have to be profitable to qualify for factoring?Not always, some clients are new companies that have not yet turned a profit, or they have suffered recent financial losses. Versant looks at the quality of a company’s customers ratherthan its specific financial condition.

6. How long does the closing process take?A typical deal can be closed and funded within one week of the initial referral - in some cases a closing can be expedited.

7. What industries will Versant purchase accounts receivable from?Almost all industries - except medical and construction – where clients sell a service or goods and their account debtors (customers) have good credit.

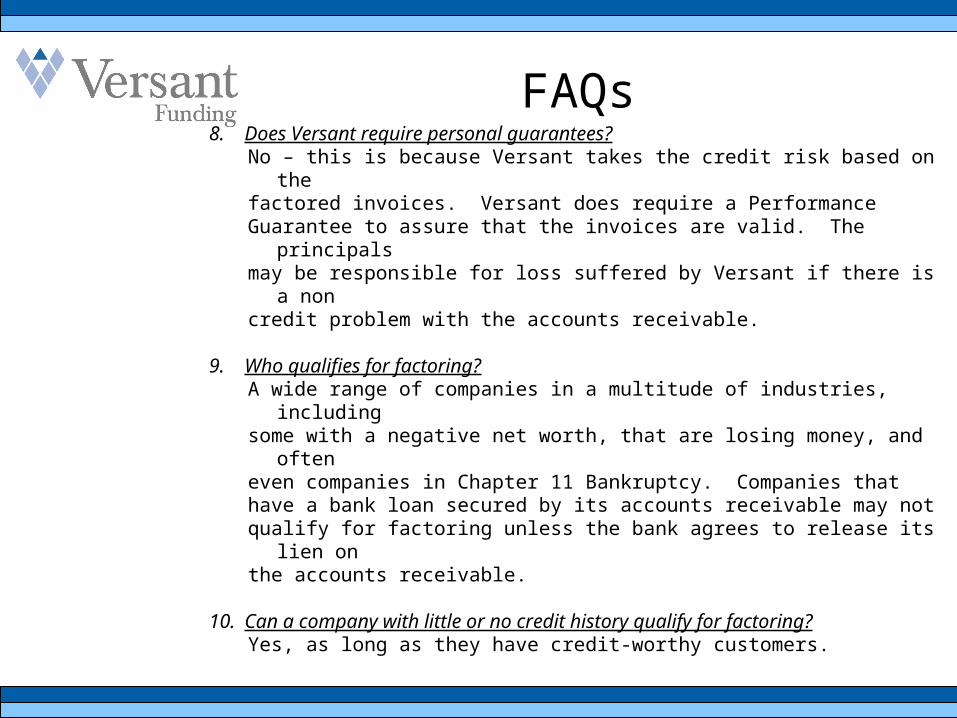

FAQs8. Does Versant require personal guarantees?

No – this is because Versant takes the credit risk based on the factored invoices. Versant does require a Performance Guarantee to assure that the invoices are valid. The principals may be responsible for loss suffered by Versant if there is a non credit problem with the accounts receivable.

9. Who qualifies for factoring?A wide range of companies in a multitude of industries, including some with a negative net worth, that are losing money, and often even companies in Chapter 11 Bankruptcy. Companies that have a bank loan secured by its accounts receivable may not qualify for factoring unless the bank agrees to release its lien on the accounts receivable.

10. Can a company with little or no credit history qualify for factoring?Yes, as long as they have credit-worthy customers.

FAQs

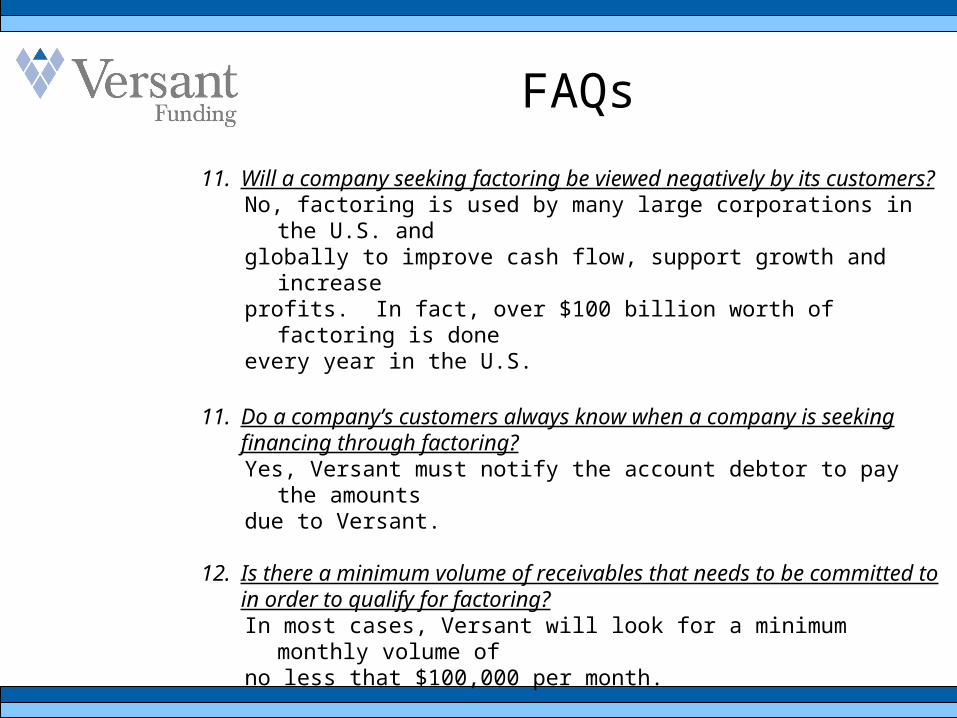

11. Will a company seeking factoring be viewed negatively by its customers?No, factoring is used by many large corporations in the U.S. and globally to improve cash flow, support growth and increase profits. In fact, over $100 billion worth of factoring is done every year in the U.S.

11. Do a company’s customers always know when a company is seeking financing through factoring?Yes, Versant must notify the account debtor to pay the amountsdue to Versant.

12. Is there a minimum volume of receivables that needs to be committed to in order to qualify for factoring?In most cases, Versant will look for a minimum monthly volume

ofno less that $100,000 per month.

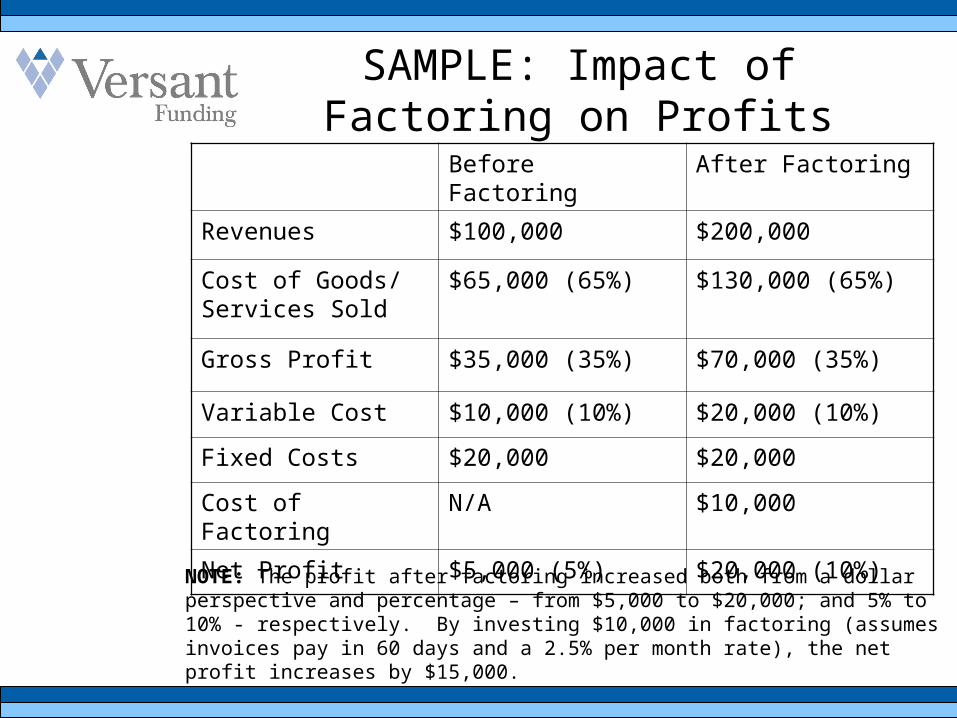

SAMPLE: Impact of Factoring on Profits

Before Factoring After Factoring

Revenues $100,000 $200,000

Cost of Goods/Services Sold

$65,000 (65%) $130,000 (65%)

Gross Profit $35,000 (35%) $70,000 (35%)

Variable Cost $10,000 (10%) $20,000 (10%)

Fixed Costs $20,000 $20,000

Cost of Factoring N/A $10,000

Net Profit $5,000 (5%) $20,000 (10%)

NOTE: The profit after factoring increased both from a dollar perspective and percentage – from $5,000 to $20,000; and 5% to 10% - respectively. By investing $10,000 in factoring (assumes invoices pay in 60 days and a 2.5% per month rate), the net profit increases by $15,000.

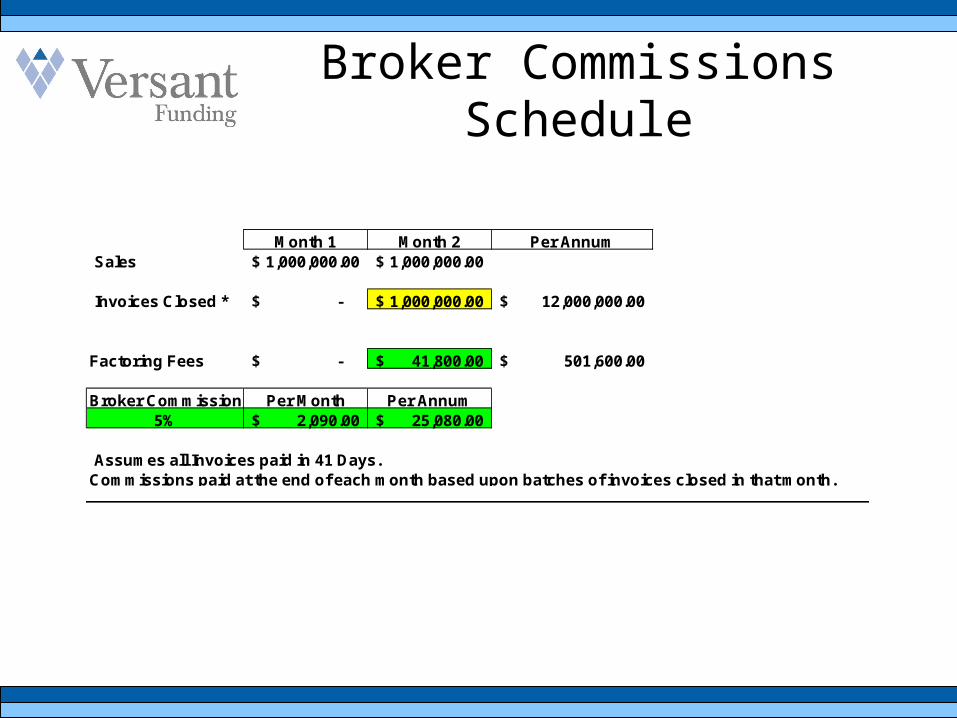

Broker Commissions Schedule

Month 1 Month 2 Per AnnumSales 1,000,000.00$ 1,000,000.00$

Invoices Closed * -$ 1,000,000.00$ 12,000,000.00$

Factoring Fees -$ 41,800.00$ 501,600.00$

Broker Commission** Per Month Per Annum5% 2,090.00$ 25,080.00$

Assumes all Invoices paid in 41 Days.Commissions paid at the end of each month based upon batches of invoices closed in that month.

For more information:Chris Lehnes

Versant Funding888 7th Avenue

New York, NY 10106203-664-1535