Embed Size (px)

Citation preview

September 2015

From Idea to Investment Venture Capital workshop two-day program

Douglas Abrams

2

6XXXX

Douglas Abrams

About the facilitator

• Wharton MBA

• JP Morgan – Vice President - IB Technology, Global Markets Internet Marketing

• Parallax Capital Management – Co-founder and MD - Venture Capital

• Extream Ventures – Co-founder and MD - S$20 million VC fund

• Expara – Founder and MD - IDM Ventures Incubator, fund, advisory, training

• NUS – Adjunct Associate Professor, Business School, Entrepreneurship

• Sasin – Visiting Professor, Venture Capital

3

6XXXX

Douglas Abrams

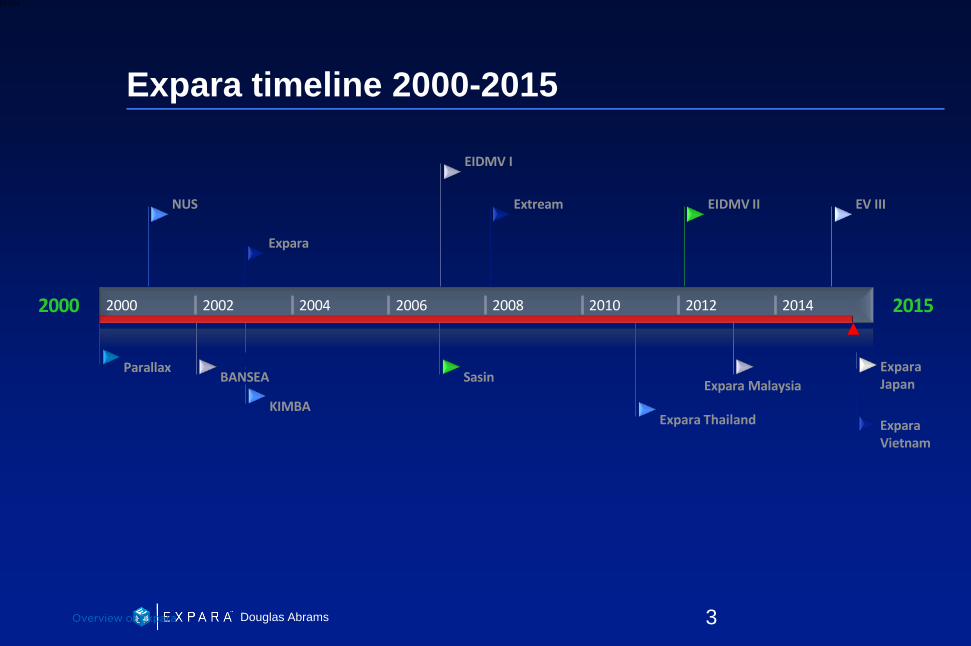

Expara timeline 2000-2015

3 Overview of Expara

2000 2015 2000 2002 2004 2006 2008 2010 2012 2014

NUS

Expara

EIDMV I

Extream EIDMV II EV III

Parallax BANSEA

KIMBA

Sasin

Expara Thailand

Expara Malaysia

Expara Vietnam

Expara Japan

4

6XXXX

Douglas Abrams

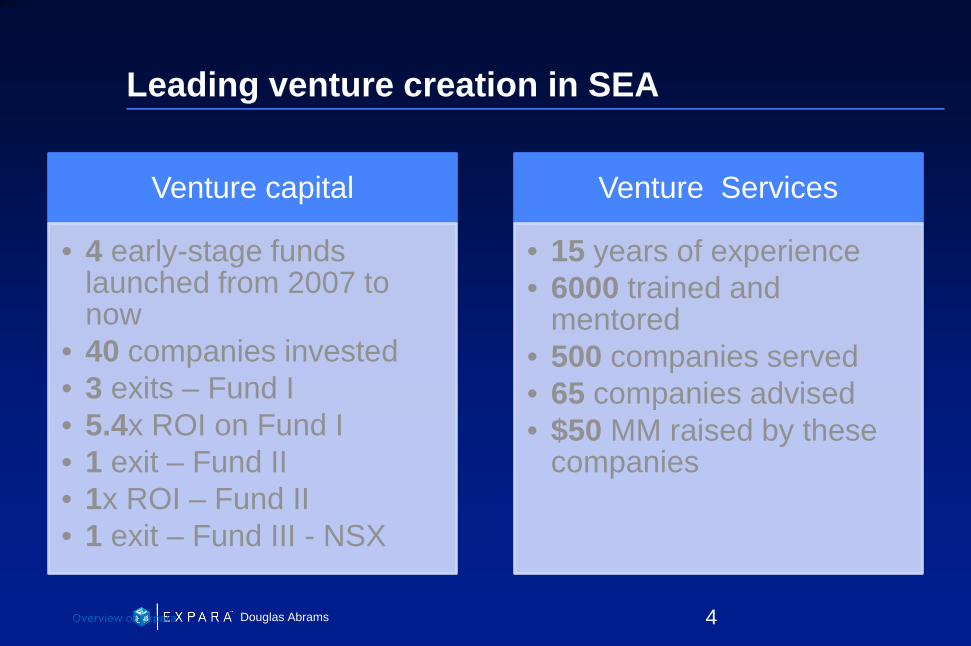

Leading venture creation in SEA

Venture capital

• 4 early-stage funds launched from 2007 to now

• 40 companies invested • 3 exits – Fund I • 5.4x ROI on Fund I • 1 exit – Fund II • 1x ROI – Fund II • 1 exit – Fund III - NSX

Venture Services

• 15 years of experience • 6000 trained and

mentored • 500 companies served • 65 companies advised • $50 MM raised by these

companies

4 Overview of Expara

5

6XXXX

Douglas Abrams

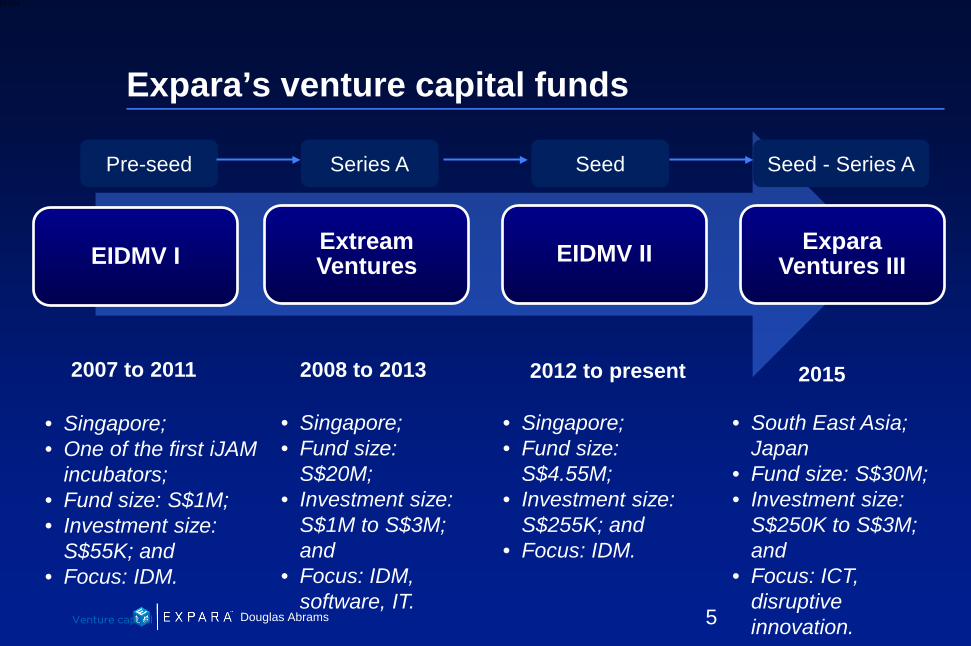

EIDMV I Extream Ventures EIDMV II Expara

Ventures III

2008 to 2013 2012 to present

2015 2007 to 2011

• Singapore; • One of the first iJAM

incubators; • Fund size: S$1M; • Investment size:

S$55K; and • Focus: IDM.

• Singapore; • Fund size:

S$20M; • Investment size:

S$1M to S$3M; and

• Focus: IDM, software, IT.

• Singapore; • Fund size:

S$4.55M; • Investment size:

S$255K; and • Focus: IDM.

Series A Seed Seed - Series A

• South East Asia; Japan

• Fund size: S$30M; • Investment size:

S$250K to S$3M; and

• Focus: ICT, disruptive innovation.

Expara’s venture capital funds

Pre-seed

5 Venture capital

6

6XXXX

Douglas Abrams

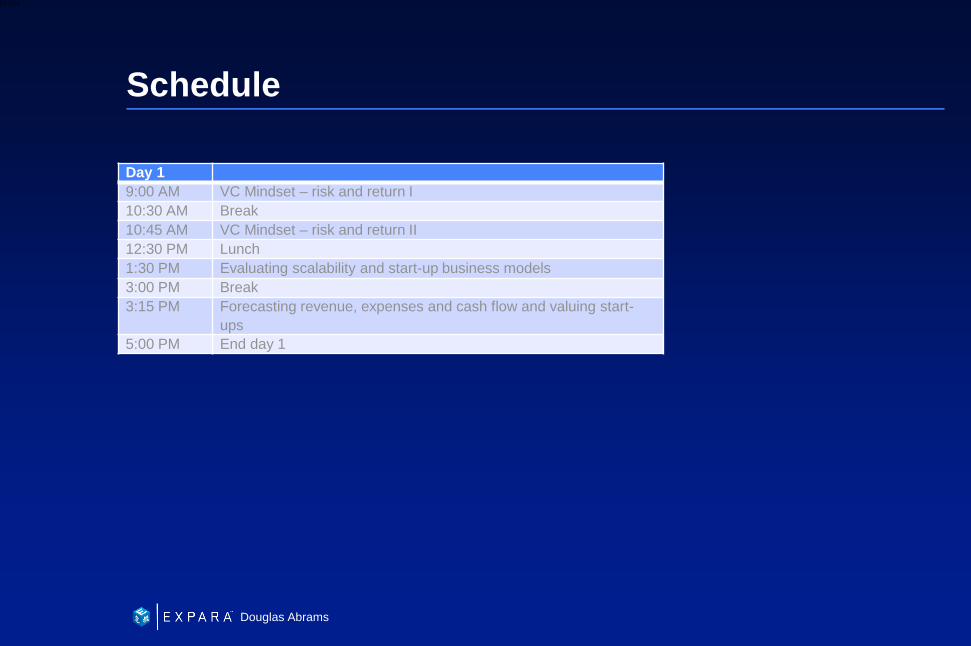

Schedule

Day 1 9:00 AM VC Mindset – risk and return I 10:30 AM Break 10:45 AM VC Mindset – risk and return II 12:30 PM Lunch 1:30 PM Evaluating scalability and start-up business models 3:00 PM Break 3:15 PM Forecasting revenue, expenses and cash flow and valuing start-

ups 5:00 PM End day 1

7

6XXXX

Douglas Abrams

Idea to Investment – Venture Capital

• Understanding the VC mindset – risk and return

• Evaluating scalability

• Evaluating start-up business models

• Forecasting revenue, expenses and cash flow

• Valuing start-ups

• VC investment process

• Understanding term sheets and deal structures

8

6XXXX

Douglas Abrams

Who are entrepreneurs and venture investors?

• Entrepreneurs – Lifestyle entrepreneurs - limited scope, complication and

risk. Slow growth. – High-growth entrepreneurs (scalable business)

Significant scope, complication, and risk. Rapid growth.

• Venture investors – Venture capitalists (VCs) – Angel investors – Corporate VCs and investors – Banks, government

9

6XXXX

Douglas Abrams

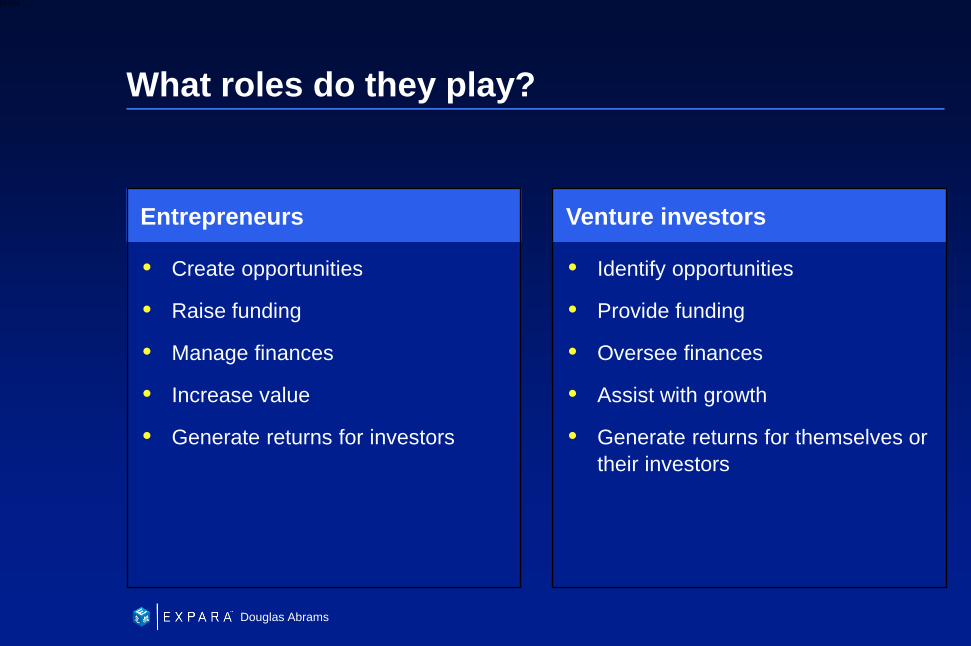

What roles do they play?

Identify opportunities

Provide funding

Oversee finances

Assist with growth

Generate returns for themselves or their investors

Venture investors

Create opportunities

Raise funding

Manage finances

Increase value

Generate returns for investors

Entrepreneurs

10

6XXXX

Douglas Abrams

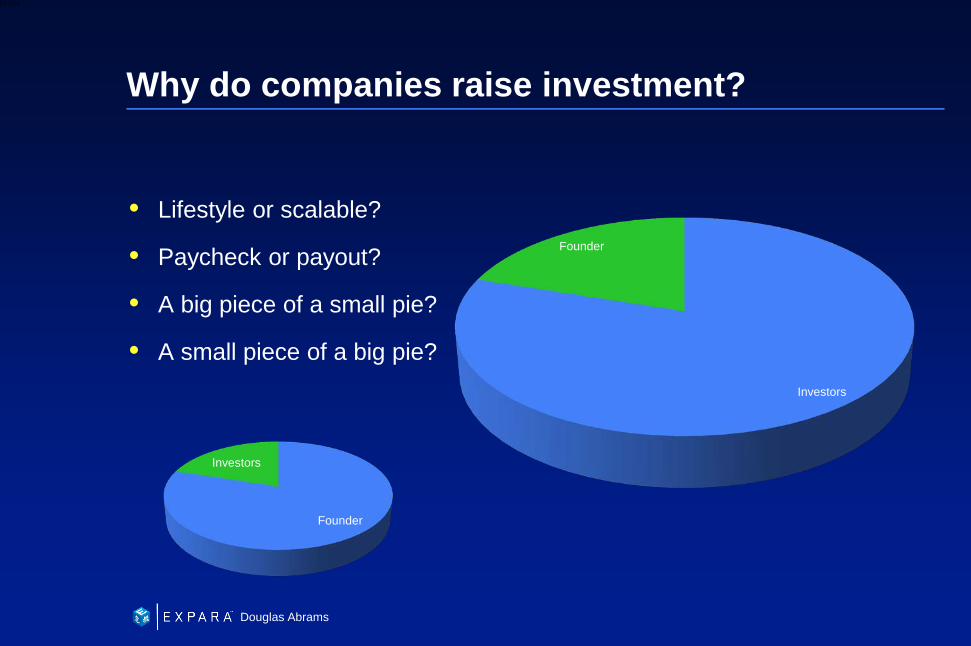

Why do companies raise investment?

Lifestyle or scalable?

Paycheck or payout?

A big piece of a small pie?

A small piece of a big pie?

Founder

Investors

Investors

Founder

11

6XXXX

Douglas Abrams

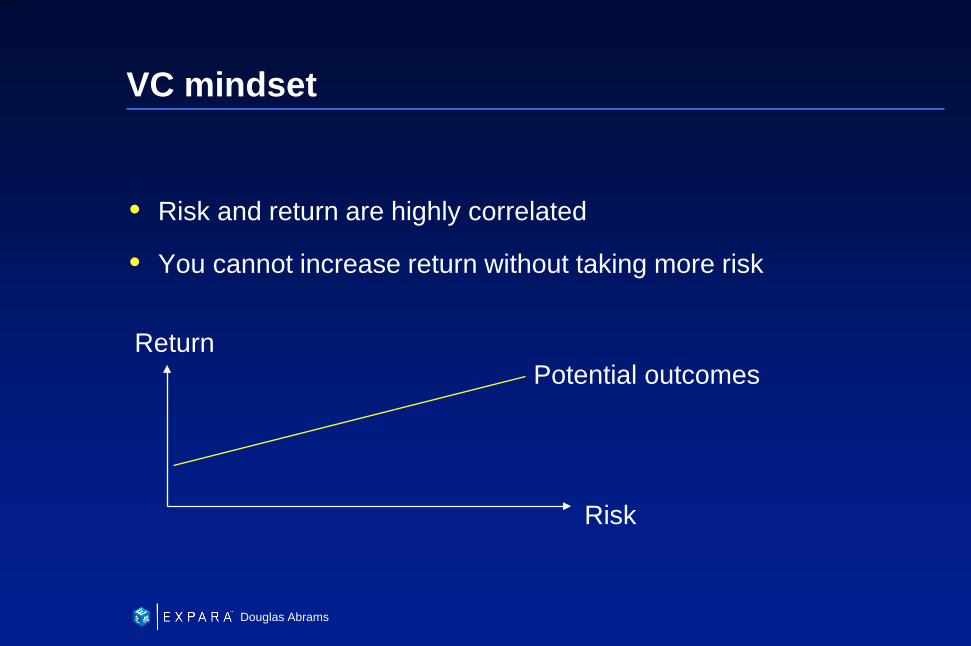

VC mindset

Risk and return are highly correlated

You cannot increase return without taking more risk

Return

Risk

Potential outcomes

12

6XXXX

Douglas Abrams

How do entrepreneurs fund growth?

Internally generated

Debt

Hybrid

Equity

13

6XXXX

Douglas Abrams

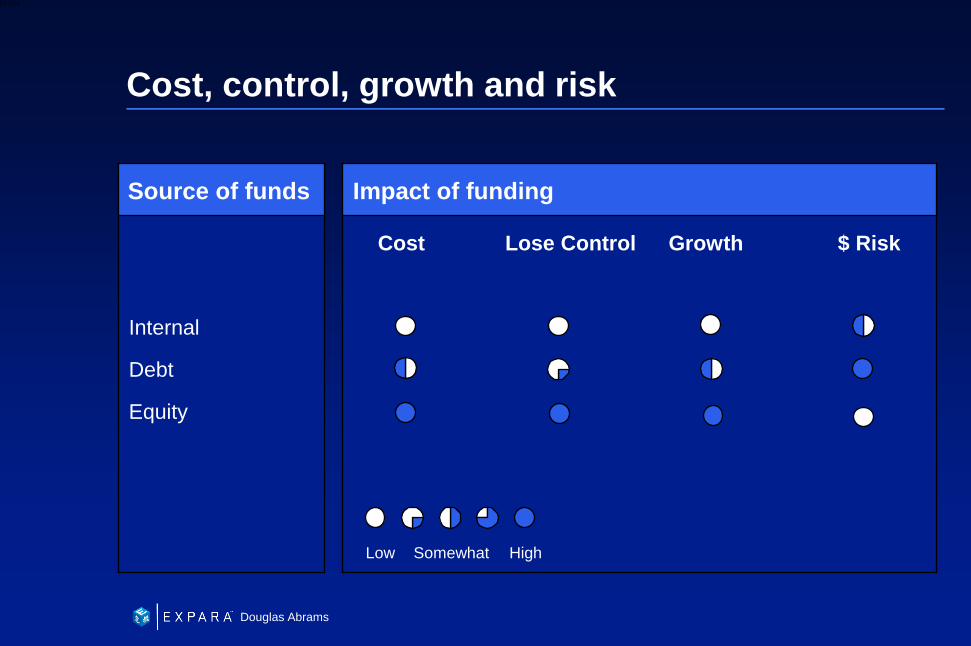

Cost, control, growth and risk

Internal

Debt

Equity

Source of funds

Cost Lose Control Growth $ Risk

Impact of funding

Low Somewhat High

14

6XXXX

Douglas Abrams

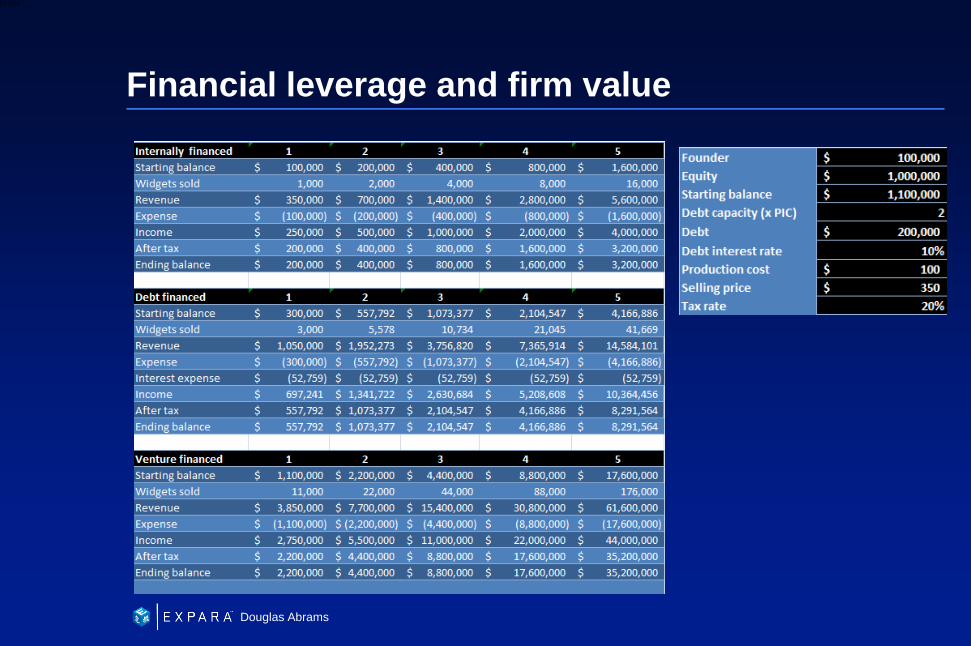

Financial leverage and firm value

15

6XXXX

Douglas Abrams

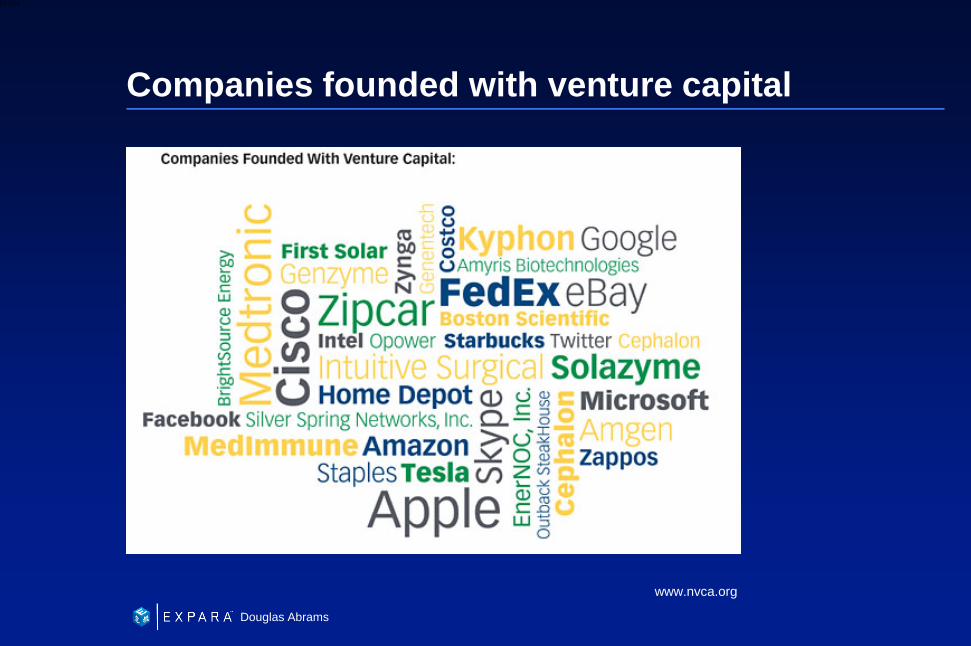

Companies founded with venture capital

www.nvca.org

16

6XXXX

Douglas Abrams

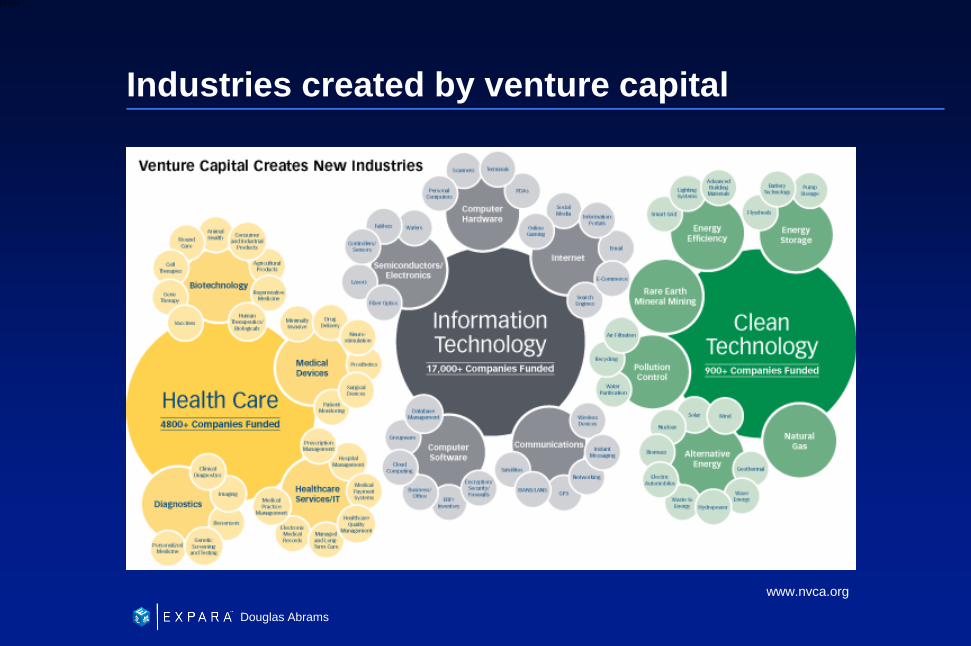

Industries created by venture capital

www.nvca.org

17

6XXXX

Douglas Abrams

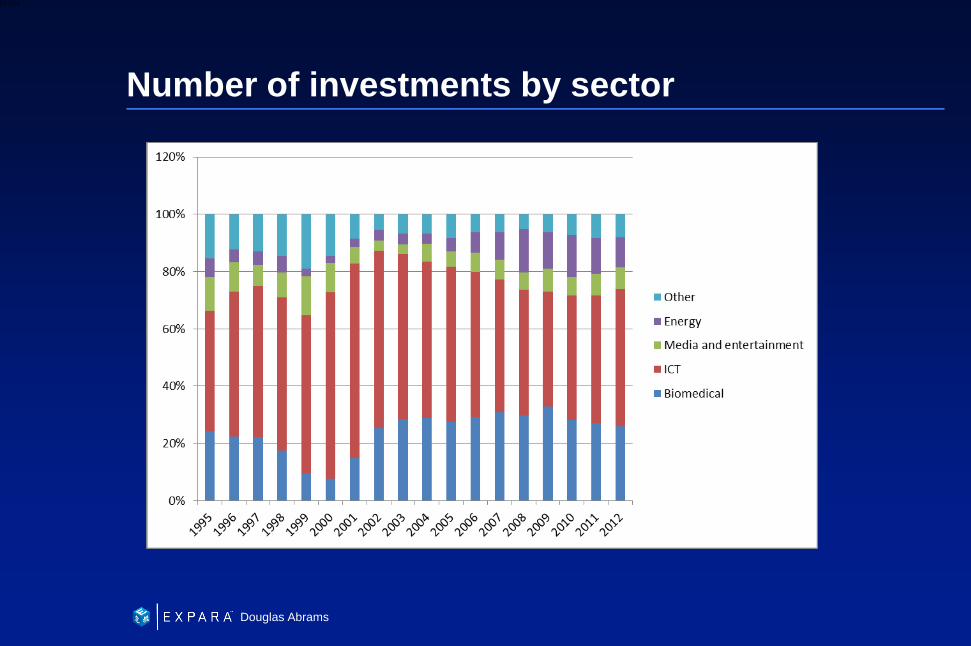

Number of investments by sector

18

6XXXX

Douglas Abrams

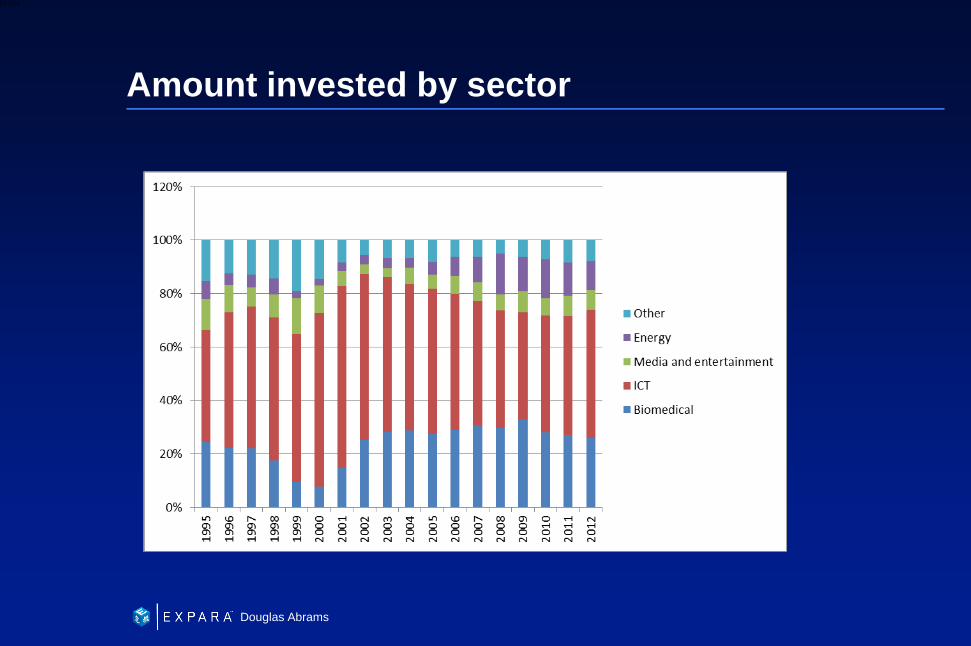

Amount invested by sector

19

6XXXX

Douglas Abrams

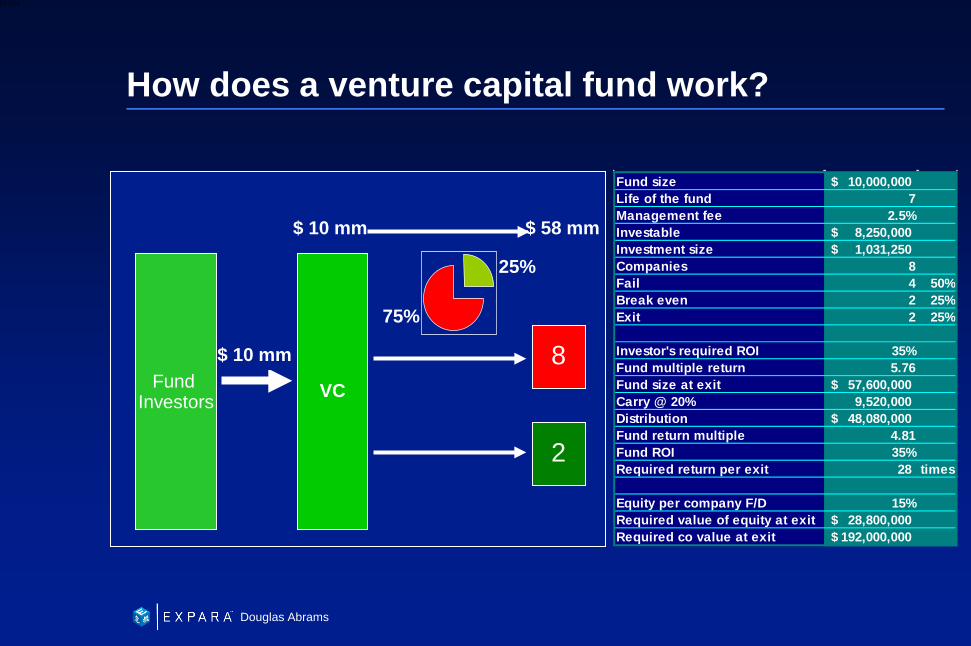

How does a venture capital fund work?

Fund Investors

VC

8

$ 10 mm

2

$ 10 mm

$ 58 mm

25%

75%

Fund size 10,000,000$ Life of the fund 7Management fee 2.5%Investable 8,250,000$ Investment size 1,031,250$ Companies 8Fail 4 50%Break even 2 25%Exit 2 25%

Investor's required ROI 35%Fund multiple return 5.76Fund size at exit 57,600,000$ Carry @ 20% 9,520,000 Distribution 48,080,000$ Fund return multiple 4.81Fund ROI 35%Required return per exit 28 times

Equity per company F/D 15%Required value of equity at exit 28,800,000$ Required co value at exit 192,000,000$

20

6XXXX

Douglas Abrams

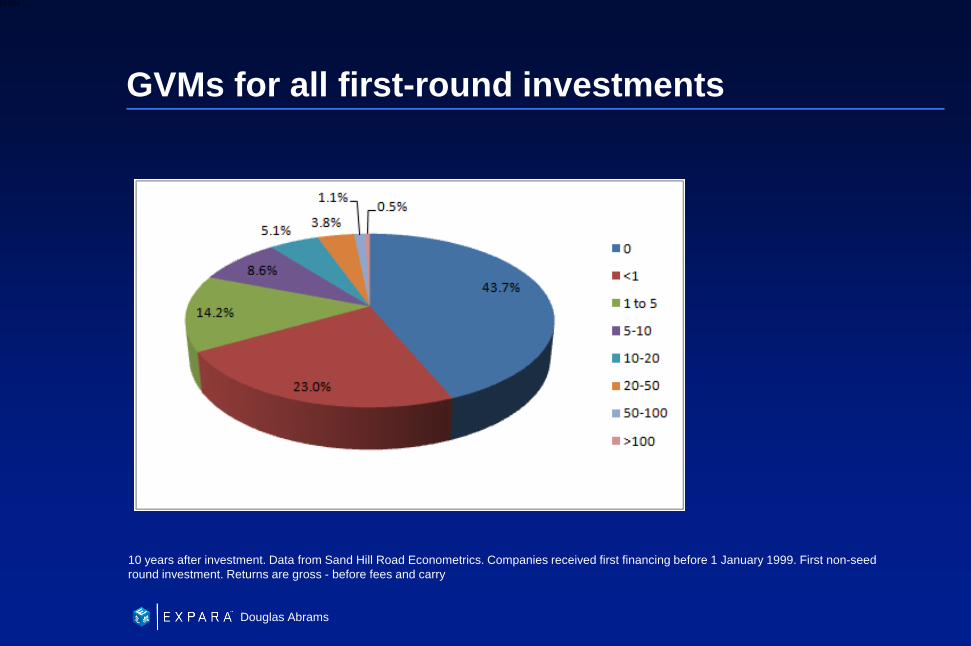

GVMs for all first-round investments

10 years after investment. Data from Sand Hill Road Econometrics. Companies received first financing before 1 January 1999. First non-seed round investment. Returns are gross - before fees and carry

21

6XXXX

Douglas Abrams

How do VCs make money?

Trade sale – sell to another company

IPO – sell to the public through listing on an exchange

23

6XXXX

Douglas Abrams

Why invest in venture capital?

As of June 30, 2014. The Cambridge Associates LLC U.S. Venture Capital Index® is an end-to-end calculation based on data compiled from 1,508 U.S. venture capital funds (963 early stage, 165 late & expansion stage, 374 multi-stage and 6 venture debt funds), including fully liquidated partnerships, formed between 1981 and 2014. (1)Pooled end-to-end return, net of fees, expenses, and carried interest.(2) 2007-2015 Sources: Cambridge Associates LLC, Barclays, Dow Jones Indexes, Frank Russell Company, Standard & Poor's, Thomson Reuters Datastream, and Wilshire Associates, Inc

Case Shiller Real Estate Index 4.1 Expara IDM Ventures (2) 43.03

24

6XXXX

Douglas Abrams

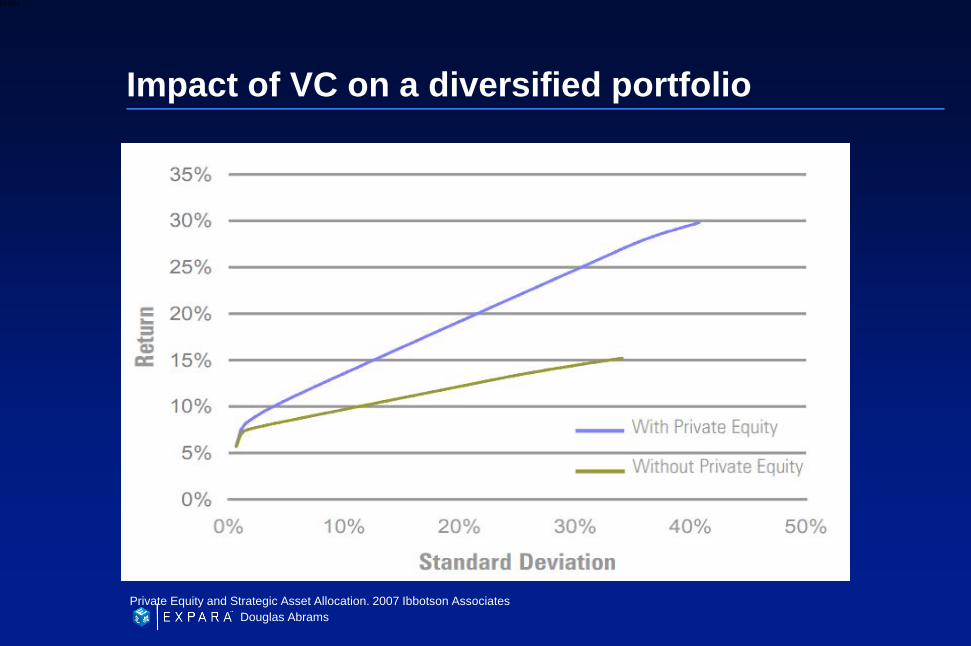

Impact of VC on a diversified portfolio

Private Equity and Strategic Asset Allocation. 2007 Ibbotson Associates

25

6XXXX

Douglas Abrams

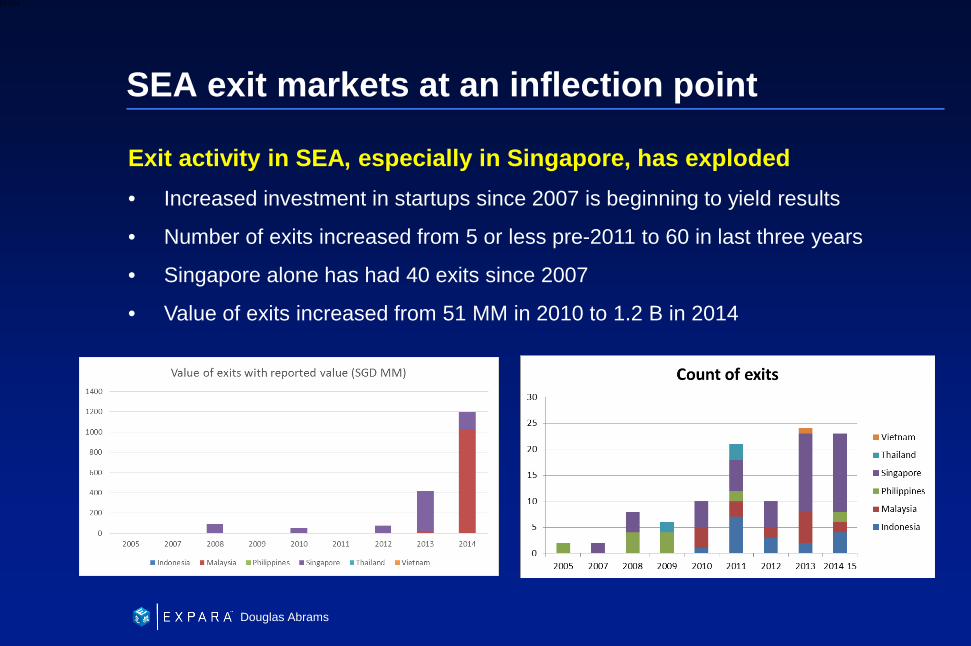

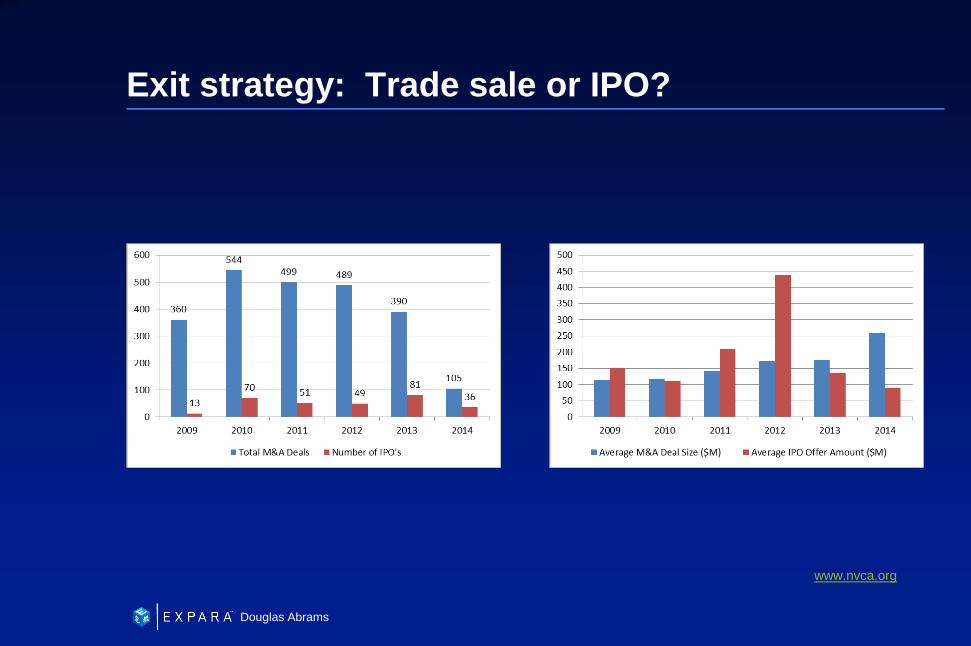

SEA exit markets at an inflection point

Exit activity in SEA, especially in Singapore, has exploded • Increased investment in startups since 2007 is beginning to yield results

• Number of exits increased from 5 or less pre-2011 to 60 in last three years

• Singapore alone has had 40 exits since 2007

• Value of exits increased from 51 MM in 2010 to 1.2 B in 2014

26

6XXXX

Douglas Abrams

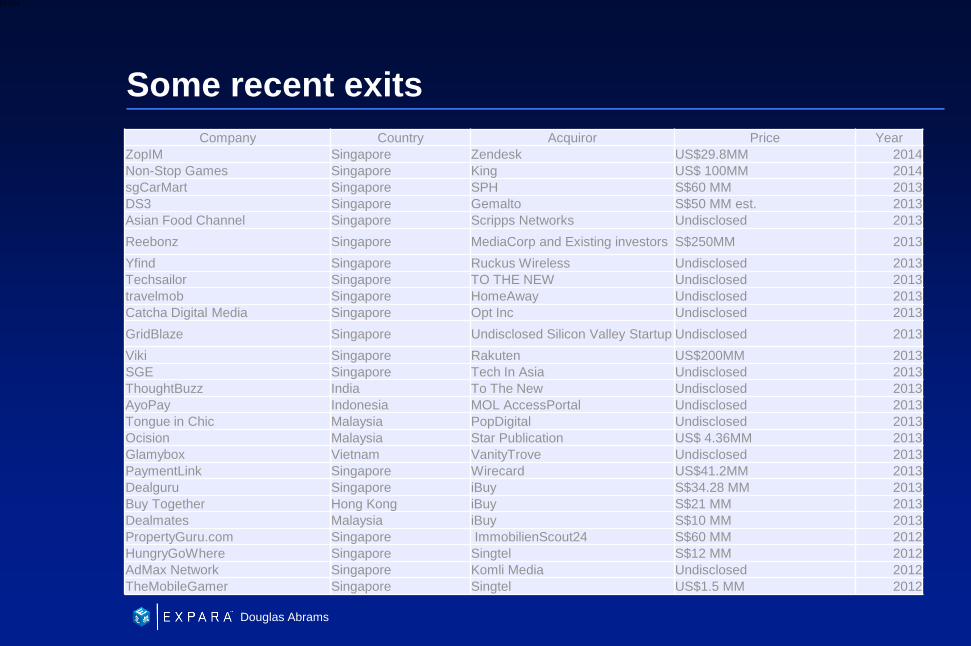

Some recent exits Company Country Acquiror Price Year

ZopIM Singapore Zendesk US$29.8MM 2014 Non-Stop Games Singapore King US$ 100MM 2014 sgCarMart Singapore SPH S$60 MM 2013 DS3 Singapore Gemalto S$50 MM est. 2013 Asian Food Channel Singapore Scripps Networks Undisclosed 2013

Reebonz Singapore MediaCorp and Existing investors S$250MM 2013

Yfind Singapore Ruckus Wireless Undisclosed 2013 Techsailor Singapore TO THE NEW Undisclosed 2013 travelmob Singapore HomeAway Undisclosed 2013 Catcha Digital Media Singapore Opt Inc Undisclosed 2013

GridBlaze Singapore Undisclosed Silicon Valley Startup Undisclosed 2013

Viki Singapore Rakuten US$200MM 2013 SGE Singapore Tech In Asia Undisclosed 2013 ThoughtBuzz India To The New Undisclosed 2013 AyoPay Indonesia MOL AccessPortal Undisclosed 2013 Tongue in Chic Malaysia PopDigital Undisclosed 2013 Ocision Malaysia Star Publication US$ 4.36MM 2013 Glamybox Vietnam VanityTrove Undisclosed 2013 PaymentLink Singapore Wirecard US$41.2MM 2013 Dealguru Singapore iBuy S$34.28 MM 2013 Buy Together Hong Kong iBuy S$21 MM 2013 Dealmates Malaysia iBuy S$10 MM 2013 PropertyGuru.com Singapore ImmobilienScout24 S$60 MM 2012 HungryGoWhere Singapore Singtel S$12 MM 2012 AdMax Network Singapore Komli Media Undisclosed 2012 TheMobileGamer Singapore Singtel US$1.5 MM 2012

27

6XXXX

Douglas Abrams

Why fear risk?

Fear is good when it helps us stay alive

It is rational to be risk-averse in life-and-death situations

Most investment decisions are not life-and-death situations

28

6XXXX

Douglas Abrams

Just do it

Everything that is worth doing is difficult

If it is easy, it is probably not worth doing

You should never hesitate to do something difficult

29

6XXXX

Douglas Abrams

Risk and return – small versus scalable business

Small business: limited scope, complication and risk. Slow growth.

Scalable business: significant scope, complication, and risk. Rapid growth.

30

6XXXX

Douglas Abrams

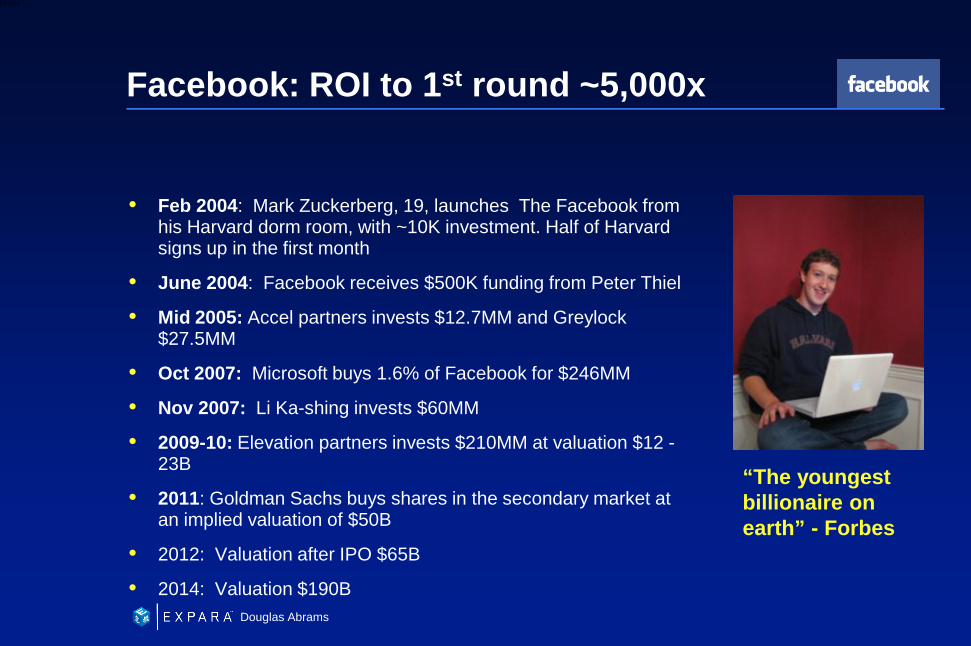

Facebook: ROI to 1st round ~5,000x

Feb 2004: Mark Zuckerberg, 19, launches The Facebook from his Harvard dorm room, with ~10K investment. Half of Harvard signs up in the first month

June 2004: Facebook receives $500K funding from Peter Thiel

Mid 2005: Accel partners invests $12.7MM and Greylock $27.5MM

Oct 2007: Microsoft buys 1.6% of Facebook for $246MM

Nov 2007: Li Ka-shing invests $60MM

2009-10: Elevation partners invests $210MM at valuation $12 - 23B

2011: Goldman Sachs buys shares in the secondary market at an implied valuation of $50B

2012: Valuation after IPO $65B

2014: Valuation $190B

“The youngest billionaire on earth” - Forbes

31

6XXXX

Douglas Abrams

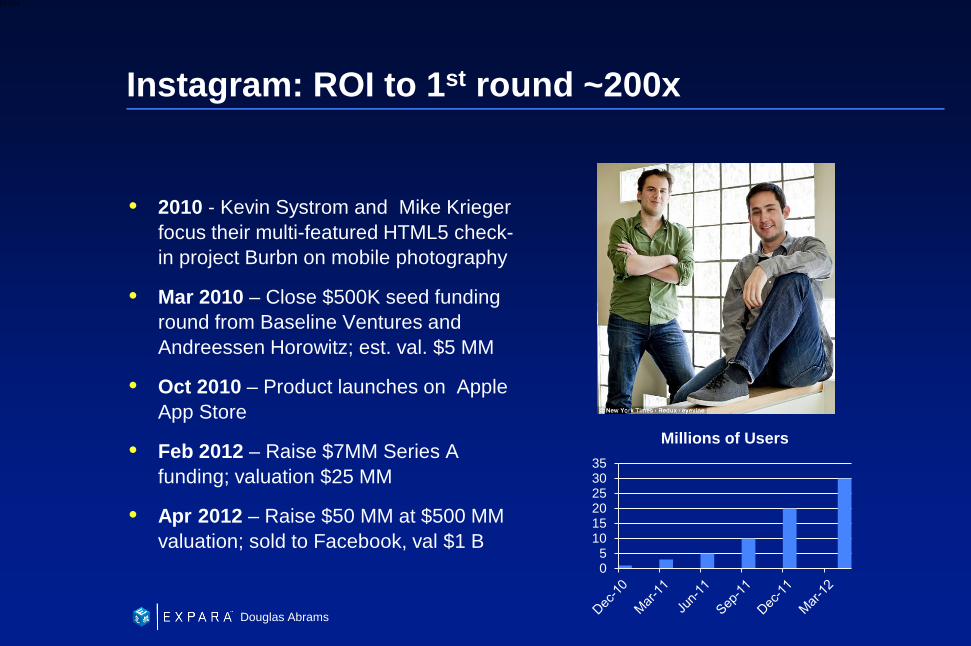

Instagram: ROI to 1st round ~200x

2010 - Kevin Systrom and Mike Krieger focus their multi-featured HTML5 check-in project Burbn on mobile photography

Mar 2010 – Close $500K seed funding round from Baseline Ventures and Andreessen Horowitz; est. val. $5 MM

Oct 2010 – Product launches on Apple App Store

Feb 2012 – Raise $7MM Series A funding; valuation $25 MM

Apr 2012 – Raise $50 MM at $500 MM valuation; sold to Facebook, val $1 B

05

101520253035

Millions of Users

32

6XXXX

Douglas Abrams

Google: ROI to 1st round ~1000x

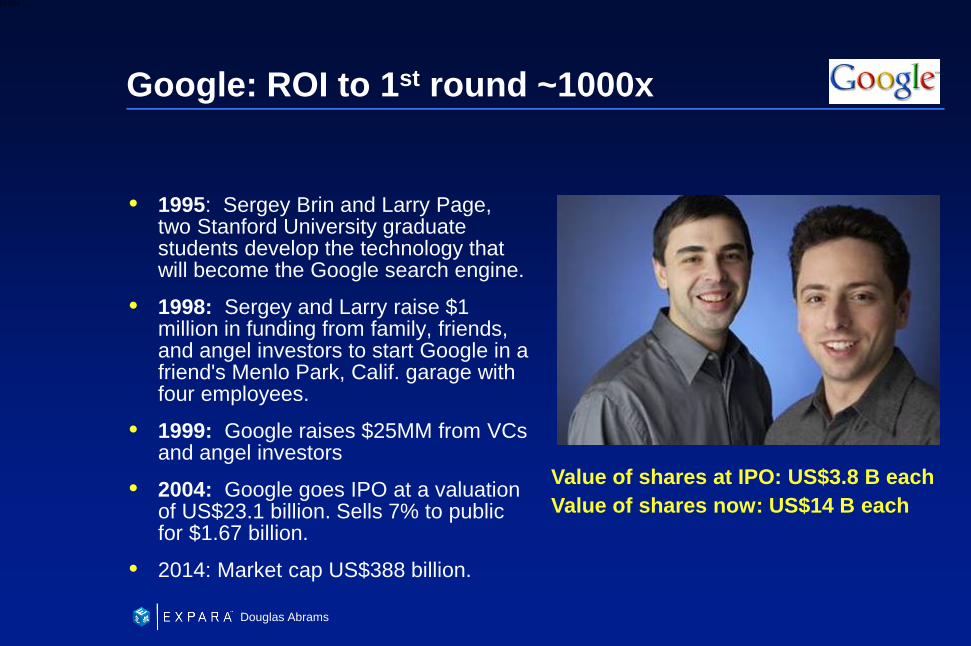

1995: Sergey Brin and Larry Page, two Stanford University graduate students develop the technology that will become the Google search engine.

1998: Sergey and Larry raise $1 million in funding from family, friends, and angel investors to start Google in a friend's Menlo Park, Calif. garage with four employees.

1999: Google raises $25MM from VCs and angel investors

2004: Google goes IPO at a valuation of US$23.1 billion. Sells 7% to public for $1.67 billion.

2014: Market cap US$388 billion.

Value of shares at IPO: US$3.8 B each Value of shares now: US$14 B each

33

6XXXX

Douglas Abrams

YouTube: ROI to 1st round ~125x

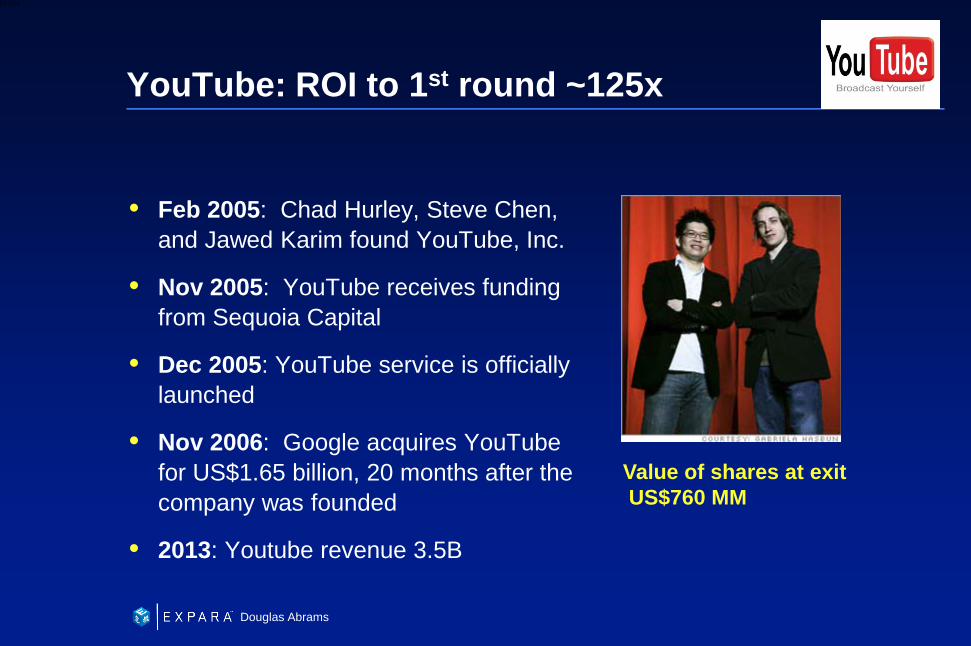

Feb 2005: Chad Hurley, Steve Chen, and Jawed Karim found YouTube, Inc.

Nov 2005: YouTube receives funding from Sequoia Capital

Dec 2005: YouTube service is officially launched

Nov 2006: Google acquires YouTube for US$1.65 billion, 20 months after the company was founded

2013: Youtube revenue 3.5B

Value of shares at exit US$760 MM

34

6XXXX

Douglas Abrams

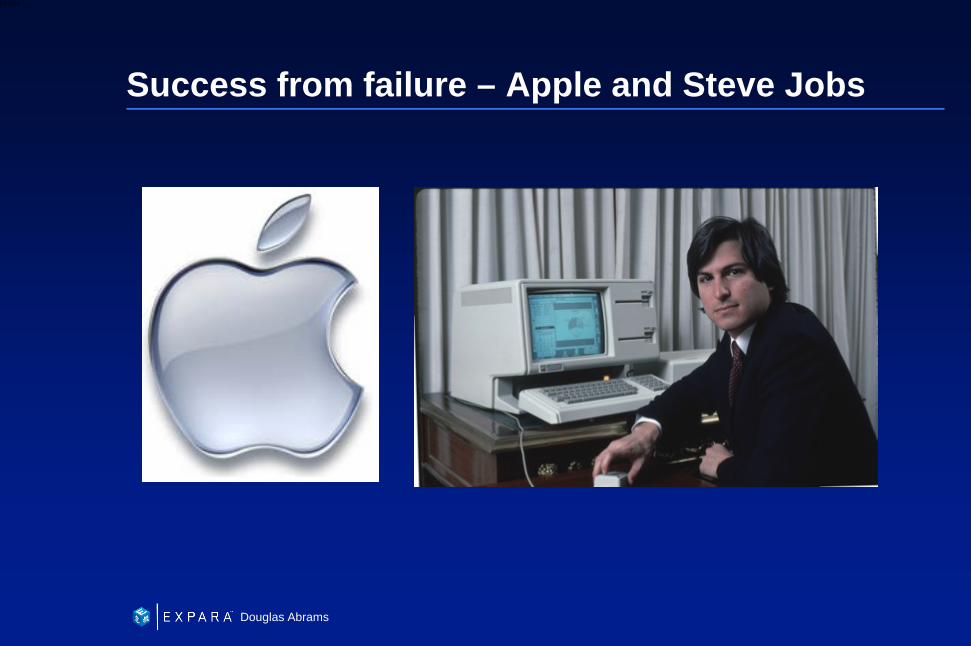

Success from failure – Apple and Steve Jobs

35

6XXXX

Douglas Abrams

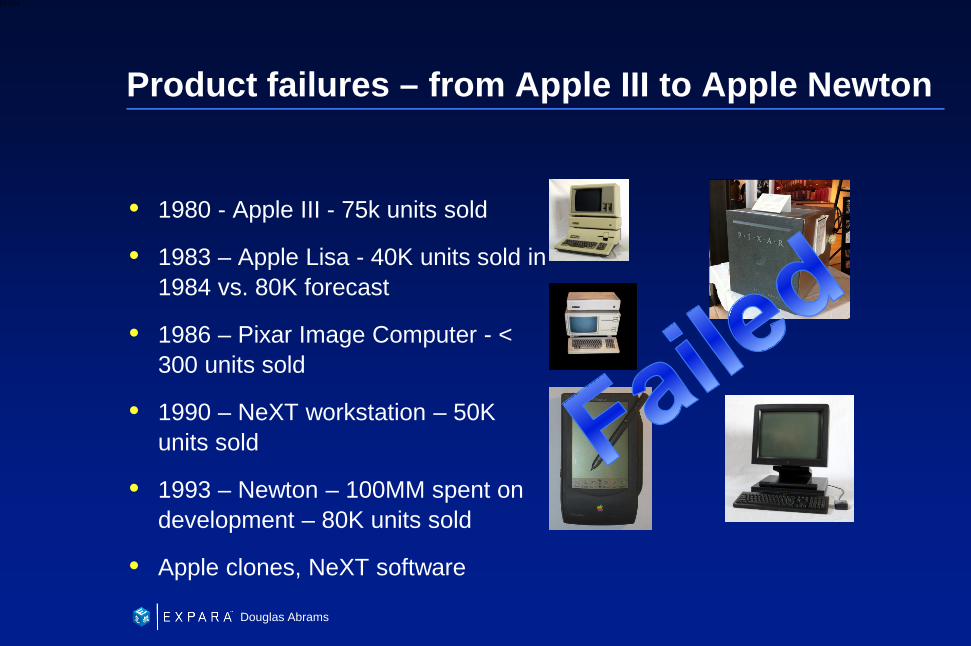

Product failures – from Apple III to Apple Newton

1980 - Apple III - 75k units sold

1983 – Apple Lisa - 40K units sold in 1984 vs. 80K forecast

1986 – Pixar Image Computer - < 300 units sold

1990 – NeXT workstation – 50K units sold

1993 – Newton – 100MM spent on development – 80K units sold

Apple clones, NeXT software

36

6XXXX

Douglas Abrams

Market failure - Apple stock price – 1988 to 1998

37

6XXXX

Douglas Abrams

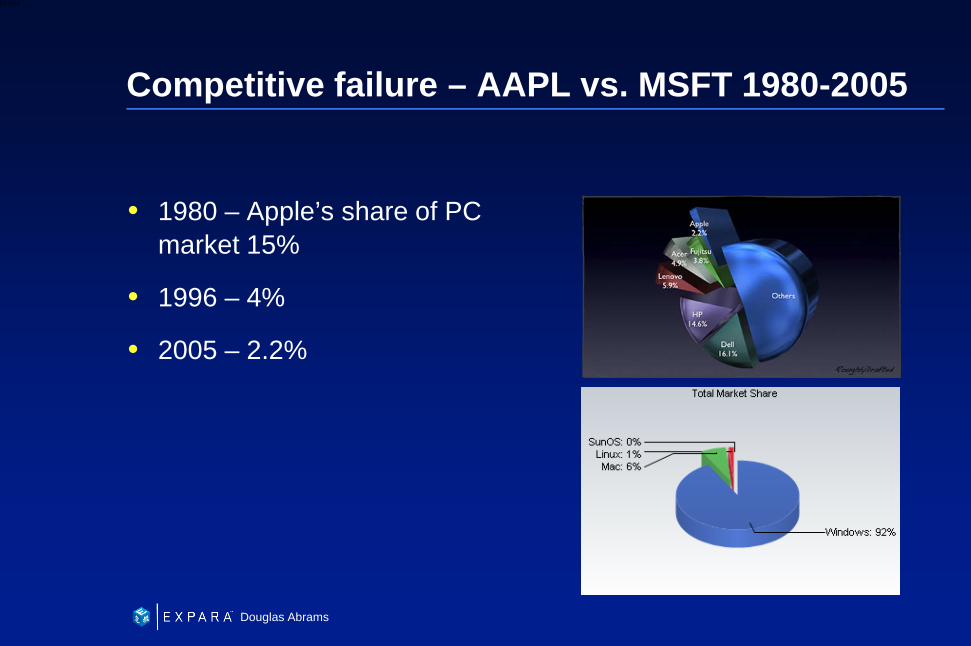

Competitive failure – AAPL vs. MSFT 1980-2005

• 1980 – Apple’s share of PC market 15%

• 1996 – 4%

• 2005 – 2.2%

38

6XXXX

Douglas Abrams

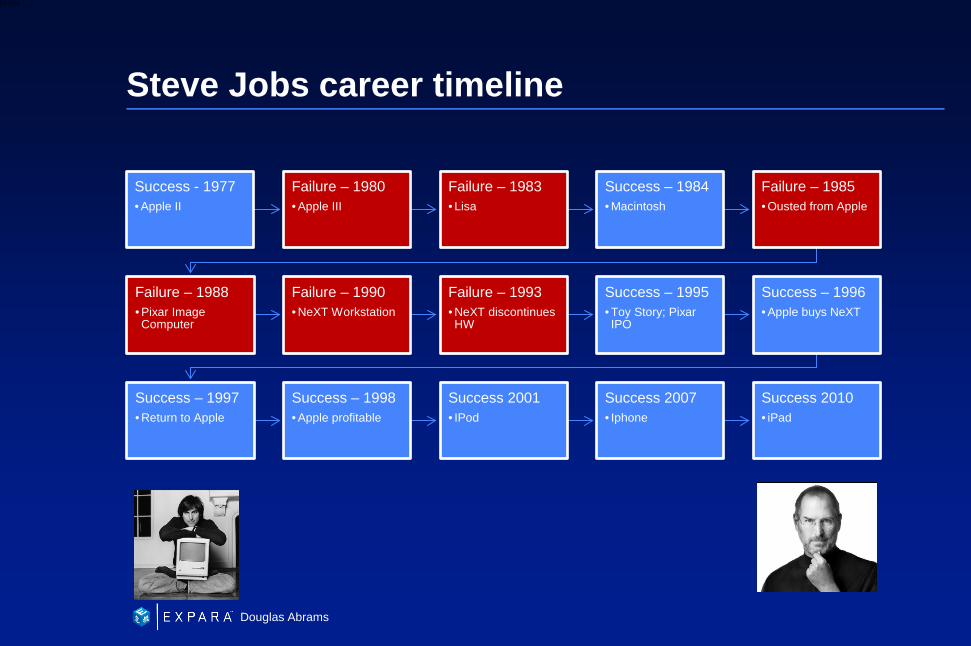

Steve Jobs career timeline

Success - 1977 • Apple II

Failure – 1980 • Apple III

Failure – 1983 • Lisa

Success – 1984 • Macintosh

Failure – 1985 • Ousted from Apple

Failure – 1988 • Pixar Image Computer

Failure – 1990 • NeXT Workstation

Failure – 1993 • NeXT discontinues HW

Success – 1995 • Toy Story; Pixar IPO

Success – 1996 • Apple buys NeXT

Success – 1997 • Return to Apple

Success – 1998 • Apple profitable

Success 2001 • IPod

Success 2007 • Iphone

Success 2010 • iPad

39

6XXXX

Douglas Abrams

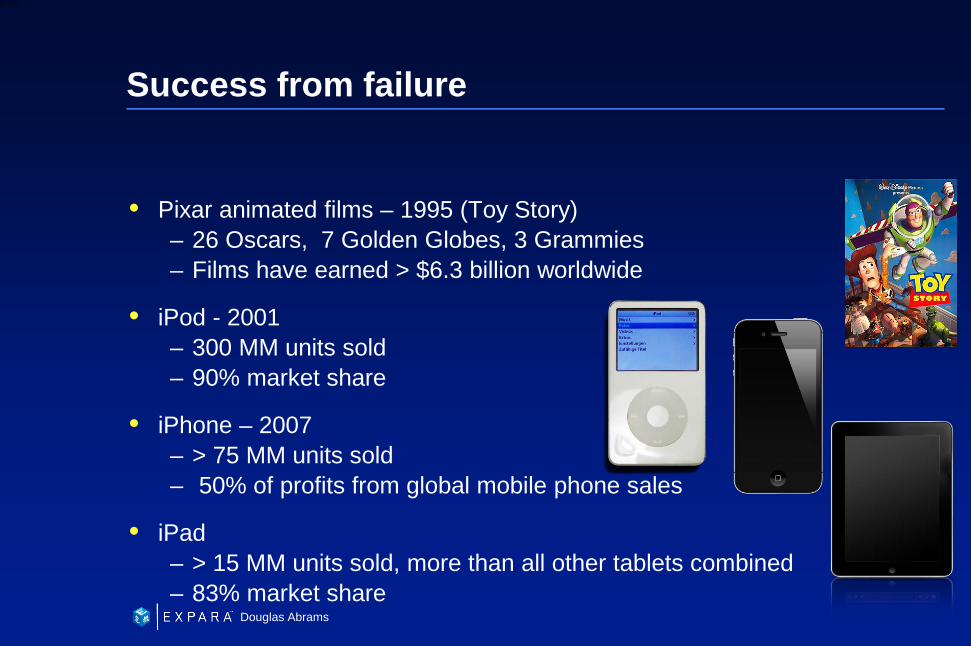

Success from failure

Pixar animated films – 1995 (Toy Story) – 26 Oscars, 7 Golden Globes, 3 Grammies – Films have earned > $6.3 billion worldwide

iPod - 2001 – 300 MM units sold – 90% market share

iPhone – 2007 – > 75 MM units sold – 50% of profits from global mobile phone sales

iPad – > 15 MM units sold, more than all other tablets combined – 83% market share

40

6XXXX

Douglas Abrams

Apple stock price 2004 – 2015 +7,910%

41

6XXXX

Douglas Abrams

Idea to Investment – Venture Capital

• Understanding the VC mindset – risk and return

• Evaluating scalability

• Evaluating start-up business models

• Forecasting revenue, expenses and cash flow

• Valuing start-ups

• VC investment process

• Understanding term sheets and deal structures

42

6XXXX

Douglas Abrams

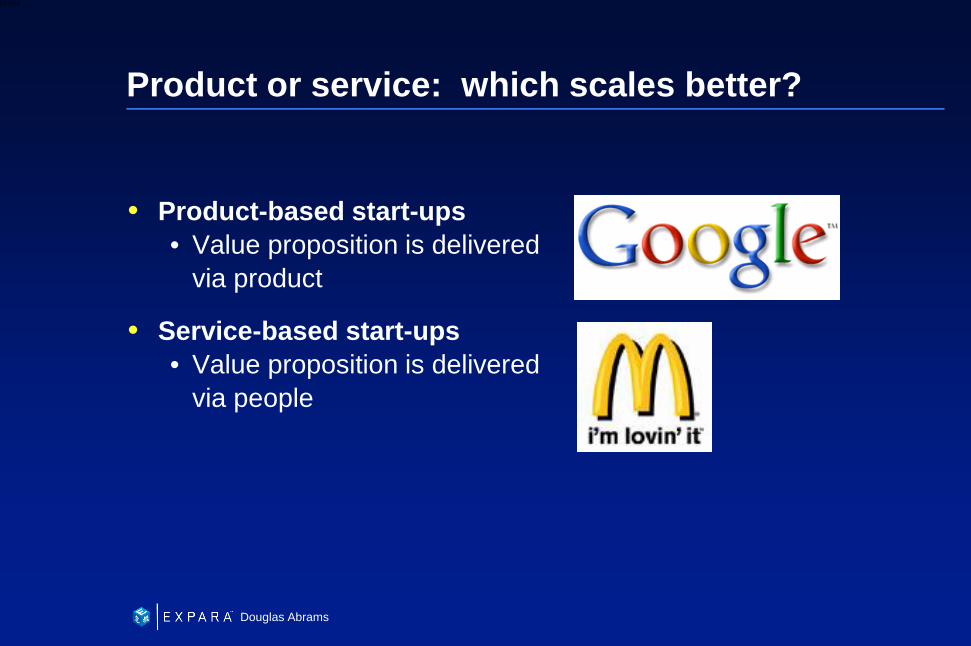

Product or service: which scales better?

• Product-based start-ups • Value proposition is delivered

via product

• Service-based start-ups • Value proposition is delivered

via people

43

6XXXX

Douglas Abrams

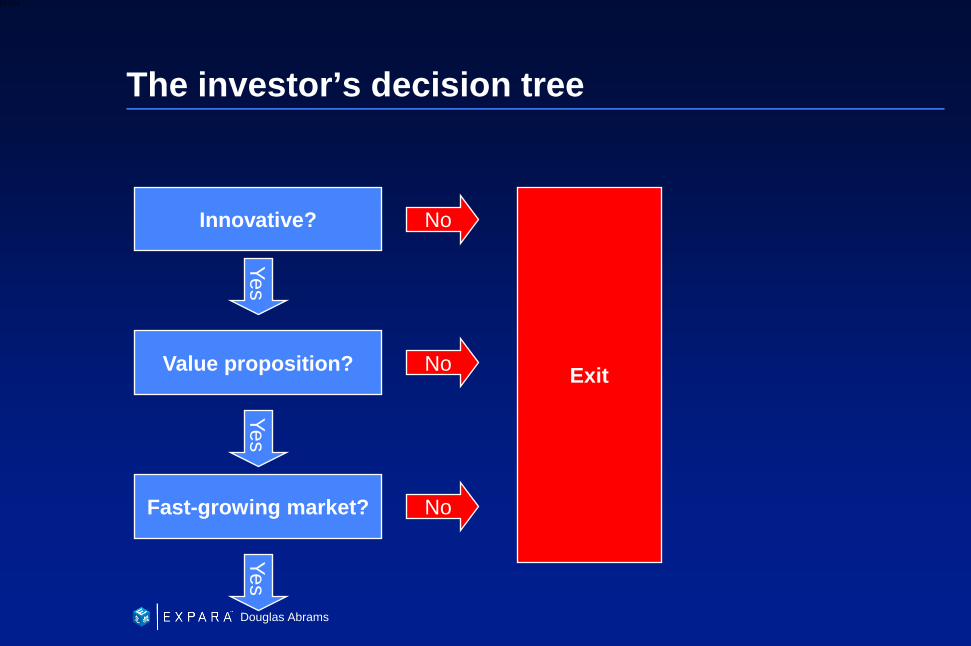

The investor’s decision tree

Innovative?

Yes

Value proposition?

Yes

Fast-growing market?

Yes

Exit

No

No

No

44

6XXXX

Douglas Abrams

Key elements for success

• Solve a problem for customers – Value proposition

• Develop an innovative product – Innovation

• Identify your customers – Market identification and analysis

• Reach your customers – Marketing strategy

• Compete when others enter - Sustainable competitive advantage

• Make money – Business model and financial plan

• Team – A team or B team

45

6XXXX

Douglas Abrams

Value proposition – how much does it hurt?

Painkiller

Vitamin

Candy

46

6XXXX

Douglas Abrams

Value proposition – degrees of recognition

• Latent problem – they have a problem but don’t know it

• Passive problem – they know they have a problem but not looking for a solution yet

• Active or urgent problem – they know they have a problem, are actively looking for a solution but no serious work done yet to solve

• A vision – they have an idea for solving the problem and a home-grown solution but are prepared to pay for a better solution

47

6XXXX

Douglas Abrams

Value proposition and innovation

1. What is the painful problem they are solving for customers?

2. What is their product and what is innovative about it?

3. What are the shortfalls of the current solutions?

4. How do they solve this problem and can they quantify your benefit?

5. How does their innovation enable you to accomplish this?

48

6XXXX

Douglas Abrams

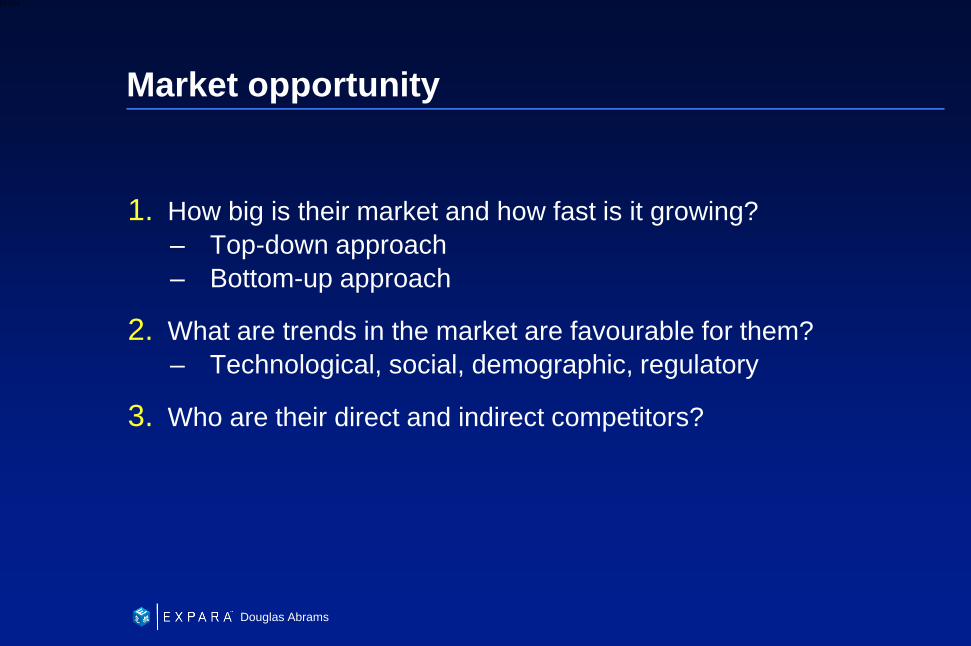

Market opportunity

1. How big is their market and how fast is it growing? – Top-down approach – Bottom-up approach

2. What are trends in the market are favourable for them? – Technological, social, demographic, regulatory

3. Who are their direct and indirect competitors?

49

6XXXX

Douglas Abrams

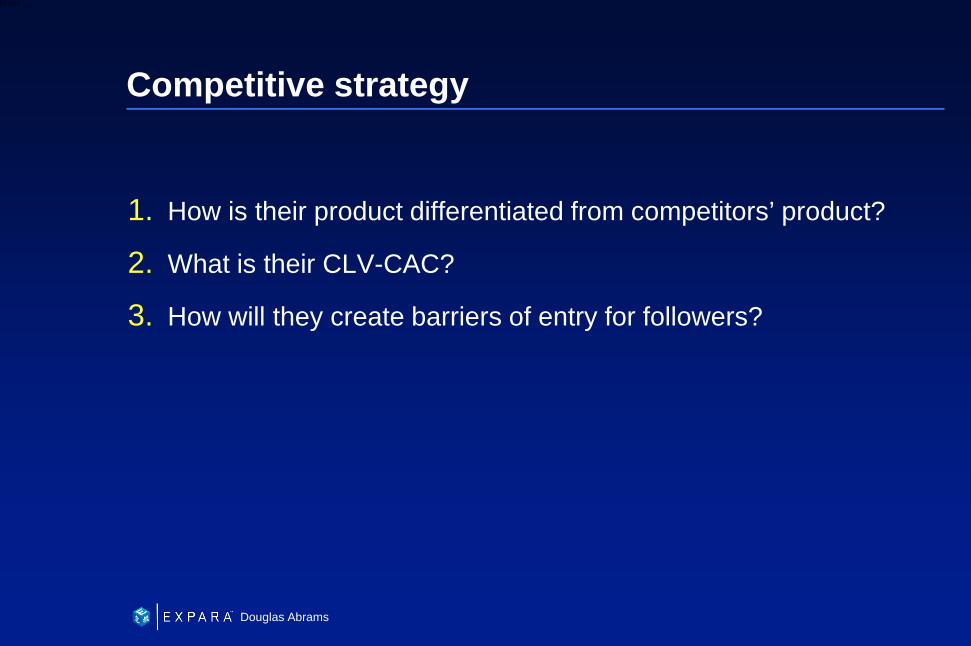

Competitive strategy

1. How is their product differentiated from competitors’ product?

2. What is their CLV-CAC?

3. How will they create barriers of entry for followers?

50

6XXXX

Douglas Abrams

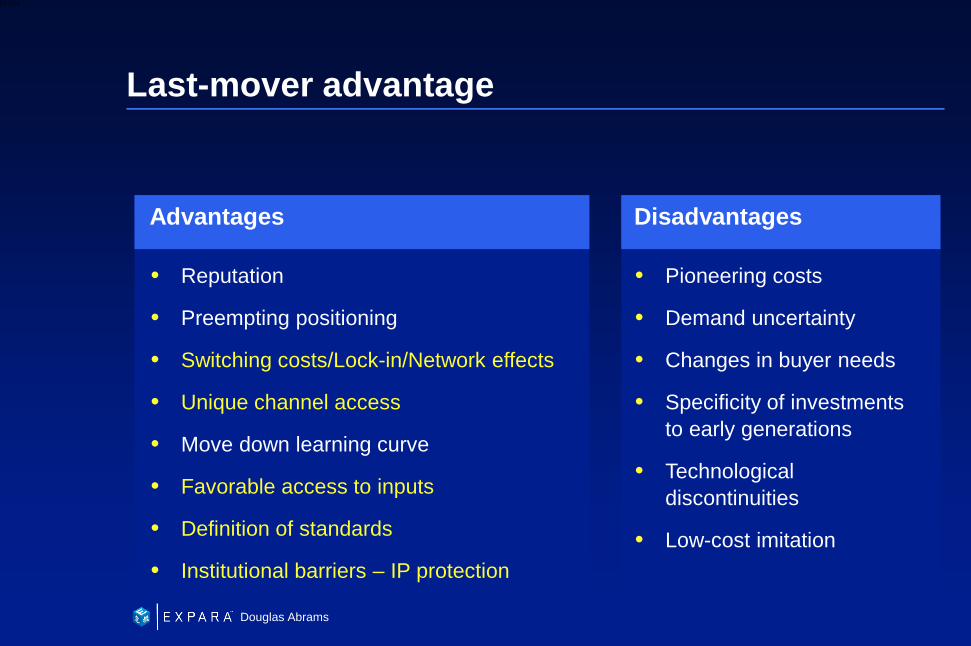

Last-mover advantage

• Reputation

• Preempting positioning

• Switching costs/Lock-in/Network effects

• Unique channel access

• Move down learning curve

• Favorable access to inputs

• Definition of standards

• Institutional barriers – IP protection

Advantages

• Pioneering costs

• Demand uncertainty

• Changes in buyer needs

• Specificity of investments to early generations

• Technological discontinuities

• Low-cost imitation

Disadvantages

51

6XXXX

Douglas Abrams

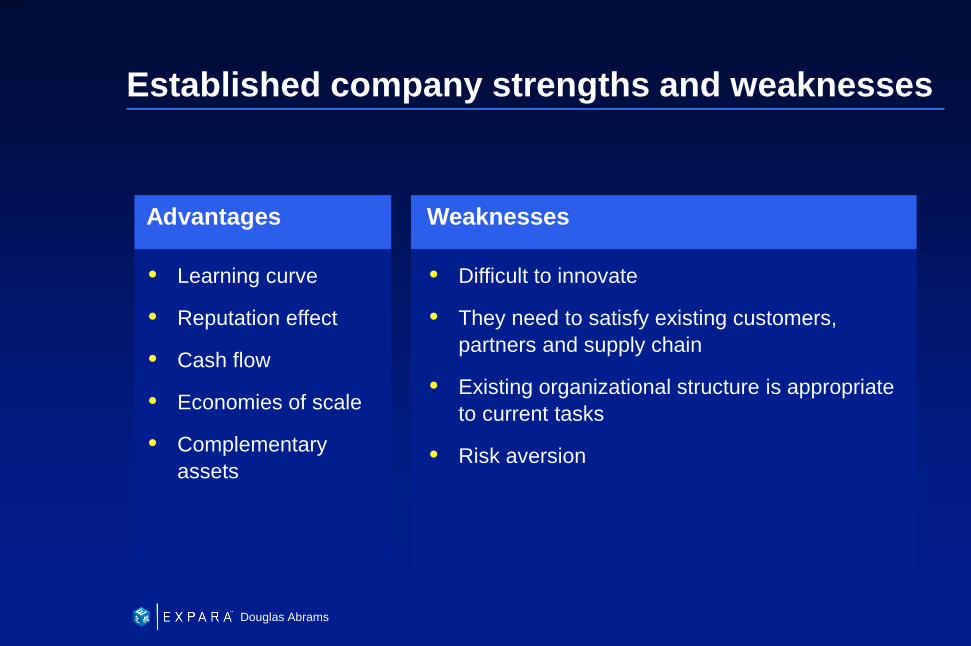

Established company strengths and weaknesses

Learning curve

Reputation effect

Cash flow

Economies of scale

Complementary assets

Advantages

Difficult to innovate

They need to satisfy existing customers, partners and supply chain

Existing organizational structure is appropriate to current tasks

Risk aversion

Weaknesses

52

6XXXX

Douglas Abrams

Opportunities that favor new firms

Existing firms frozen in the headlights

Disruptive technologies and business models

Uncertainty: existing firms’ advantages in market research are neutralized; risk propensity

Technologies: Discrete versus systemic technologies, based on human capital, general purpose rather than specific

Bad customers: Enter market that is unattractive to existing competitors due to established cost structure

53

6XXXX

Douglas Abrams

Idea to Investment – Venture Capital

Understanding the VC mindset – risk and return

Evaluating scalability

Evaluating start-up business models

Forecasting revenue, expenses and cash flow

Valuing start-ups

VC investment process

Understanding term sheets and deal structures

54

6XXXX

Douglas Abrams

Key evaluation criteria

Business model

Financial projections

Valuation

Funding required & equity offered

Use of Proceeds

Exit Strategy and ROI

Cap table

55

6XXXX

Douglas Abrams

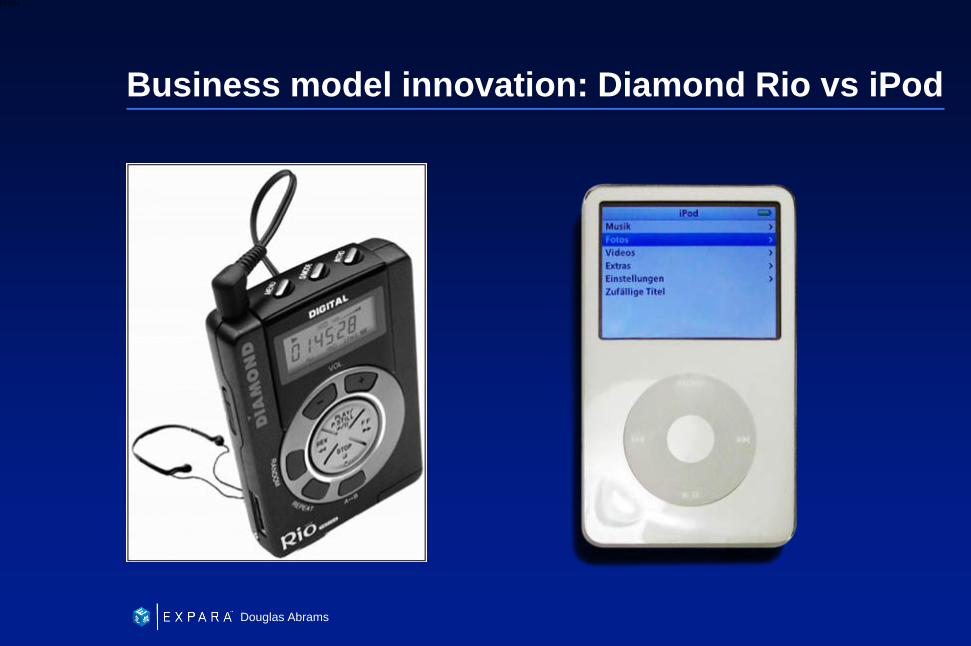

Business model innovation: Diamond Rio vs iPod

56

6XXXX

Douglas Abrams

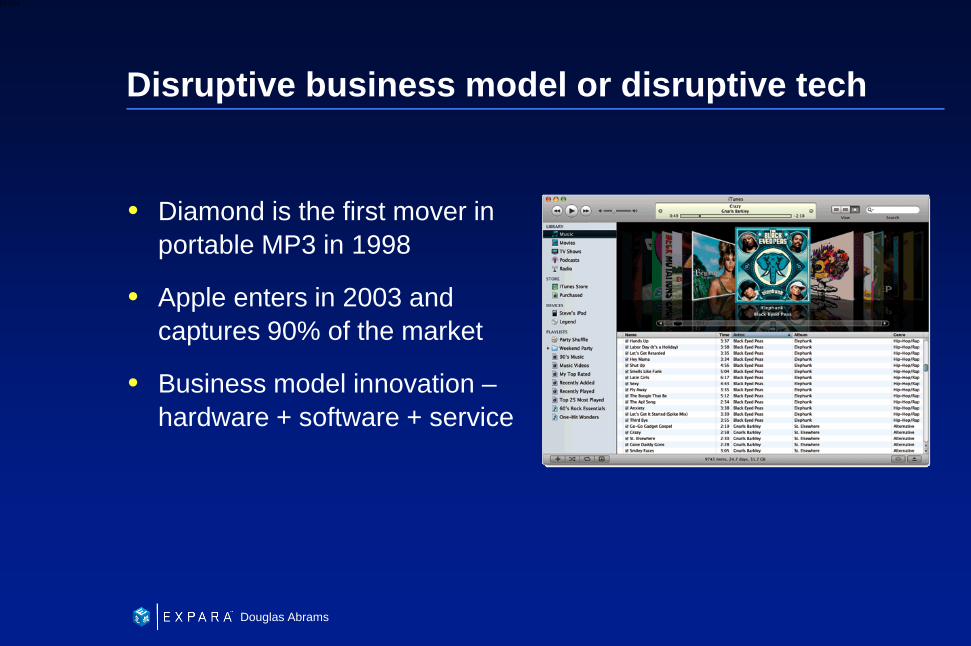

Disruptive business model or disruptive tech

• Diamond is the first mover in portable MP3 in 1998

• Apple enters in 2003 and captures 90% of the market

• Business model innovation – hardware + software + service

57

6XXXX

Douglas Abrams

Disruptive models from Gillette to Google

• Gillette – razor and blade

• Southwest Airlines – budget airlines

• Dell Computer – mass customization

• Charles Schwab – on-line broker

• Amazon – ecommerce

• eBay – peer to peer marketplace

• Google – search-based advertising

58

6XXXX

Douglas Abrams

Business model – how will they make money?

• Revenue models

• Cost structures

59

6XXXX

Douglas Abrams

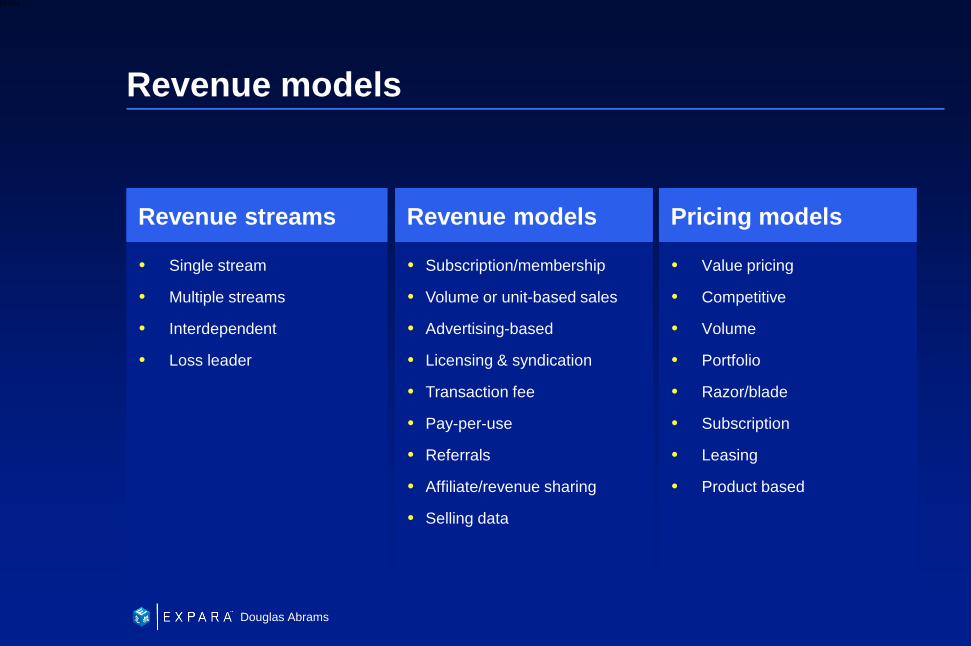

Revenue models

• Subscription/membership

• Volume or unit-based sales

• Advertising-based

• Licensing & syndication

• Transaction fee

• Pay-per-use

• Referrals

• Affiliate/revenue sharing

• Selling data

Revenue models

• Single stream

• Multiple streams

• Interdependent

• Loss leader

Revenue streams

• Value pricing

• Competitive

• Volume

• Portfolio

• Razor/blade

• Subscription

• Leasing

• Product based

Pricing models

60

6XXXX

Douglas Abrams

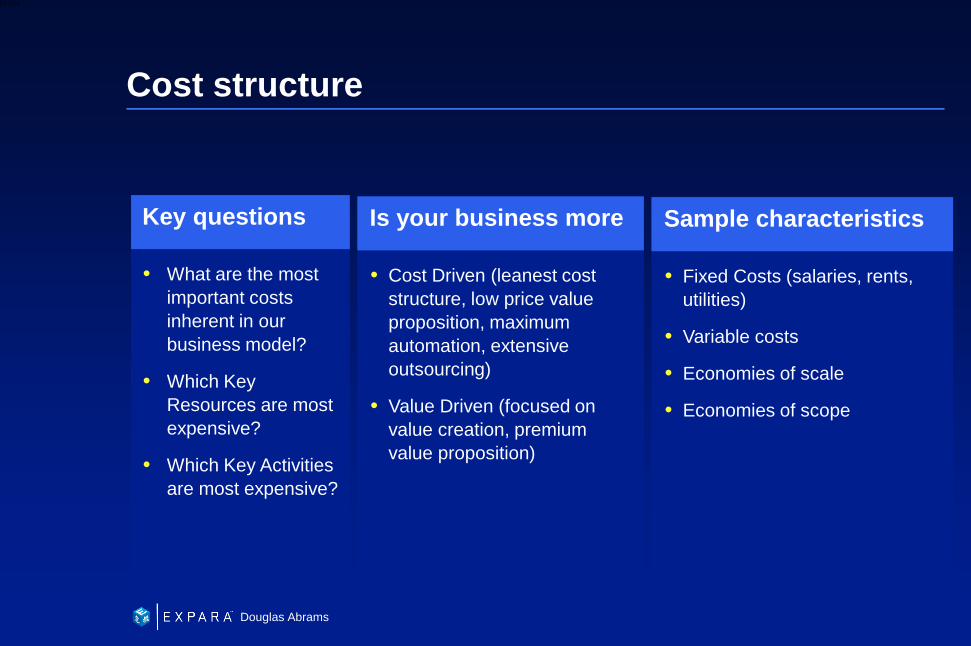

Cost structure

• What are the most important costs inherent in our business model?

• Which Key Resources are most expensive?

• Which Key Activities are most expensive?

Key questions

• Cost Driven (leanest cost structure, low price value proposition, maximum automation, extensive outsourcing)

• Value Driven (focused on value creation, premium value proposition)

Is your business more

• Fixed Costs (salaries, rents, utilities)

• Variable costs

• Economies of scale

• Economies of scope

Sample characteristics

61

6XXXX

Douglas Abrams

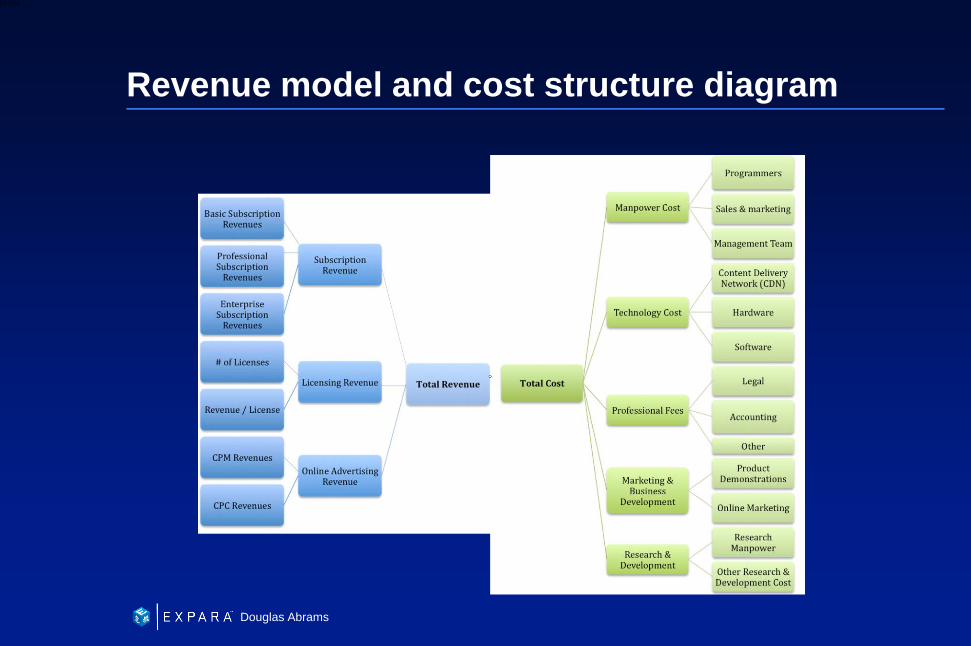

Revenue model and cost structure diagram

62

6XXXX

Douglas Abrams

Idea to Investment – Venture Capital

• Understanding the VC mindset – risk and return

• Evaluating scalability

• Evaluating start-up business models

• Forecasting revenue, expenses and cash flow

• Valuing start-ups

• VC investment process

• Understanding term sheets and deal structures

63

6XXXX

Douglas Abrams

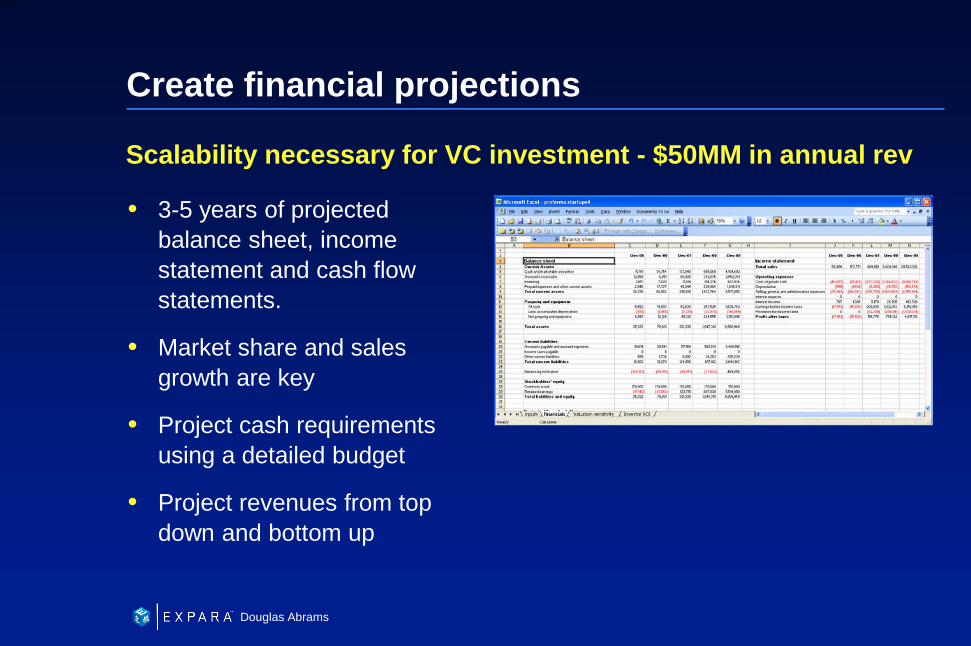

Create financial projections

• 3-5 years of projected balance sheet, income statement and cash flow statements.

• Market share and sales growth are key

• Project cash requirements using a detailed budget

• Project revenues from top down and bottom up

Scalability necessary for VC investment - $50MM in annual rev

64

6XXXX

Douglas Abrams

Create pro-forma financial statements

• Balance statement - the company’s financial condition

• Income statement (P&L) - the success of the business

• Cash flow statement - cash availability and needs of the business

65

6XXXX

Douglas Abrams

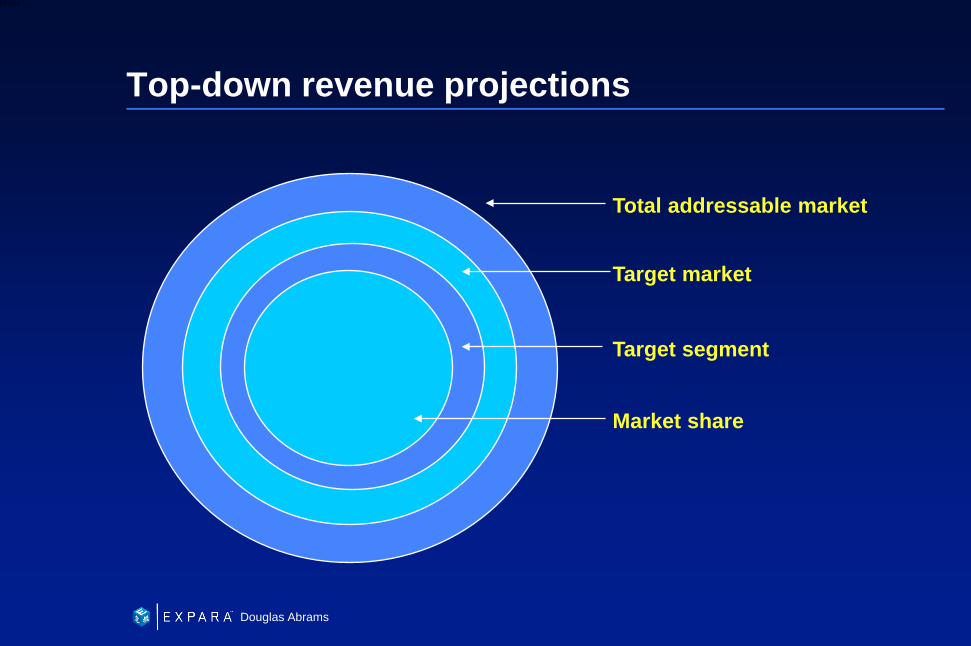

Top-down revenue projections

Total addressable market

Target market

Target segment

Market share

66

6XXXX

Douglas Abrams

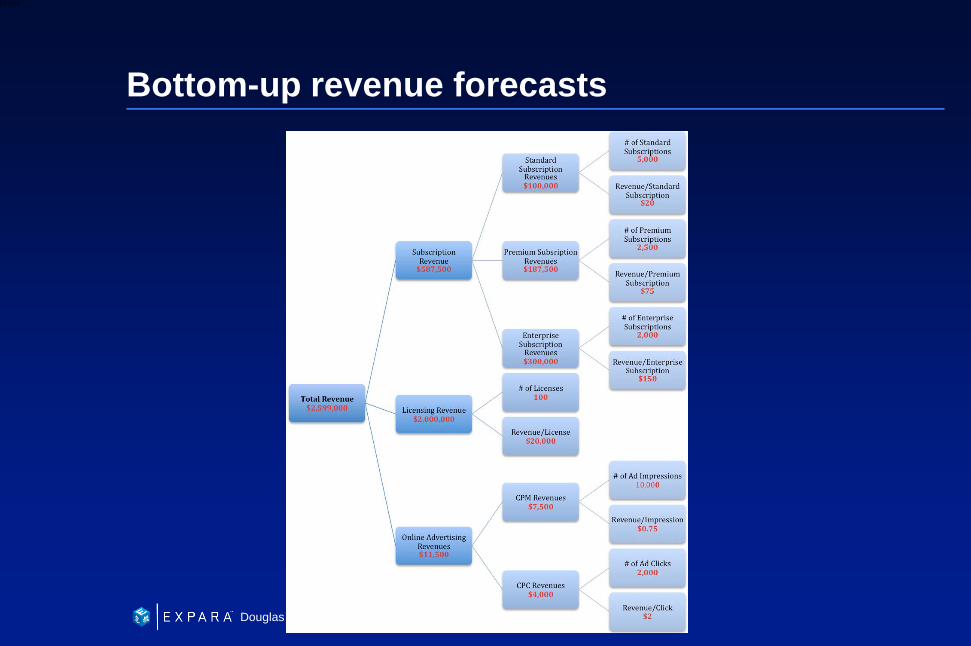

Bottom-up revenue forecasts

67

6XXXX

Douglas Abrams

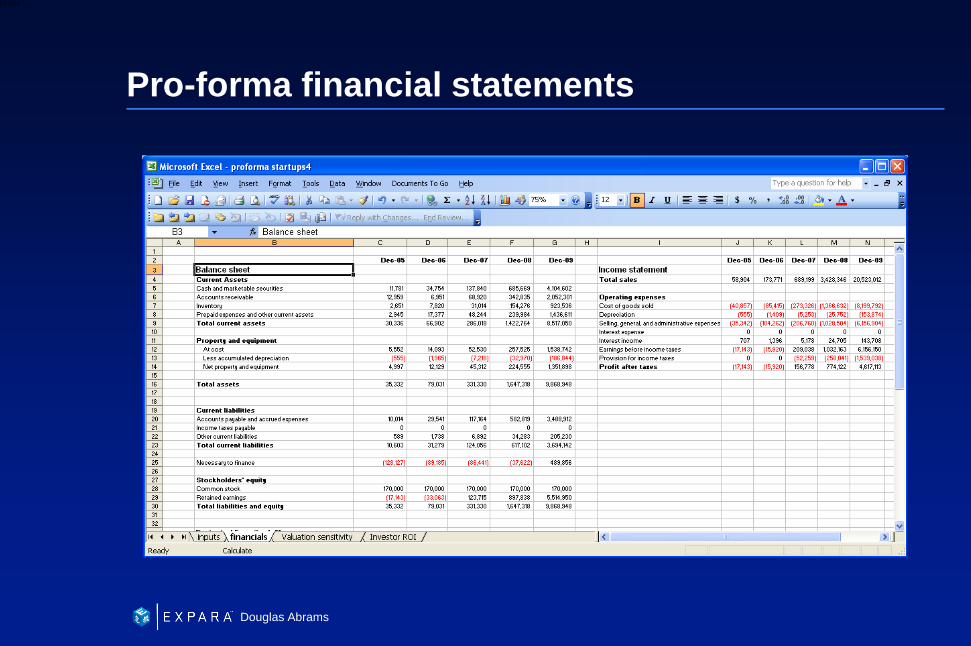

Pro-forma financial statements

68

6XXXX

Douglas Abrams

Idea to Investment – Venture Capital

• Understanding the VC mindset – risk and return

• Evaluating scalability

• Evaluating start-up business models

• Forecasting revenue, expenses and cash flow

• Valuing start-ups

• VC investment process

• Understanding term sheets and deal structures

69

6XXXX

Douglas Abrams

Company valuation methods

• Price to earnings (p/e)

• Dividend yield

• Multiple of book value

• Comparables

• Discounted Cash Flow (DCF)

• VC method

70

6XXXX

Douglas Abrams

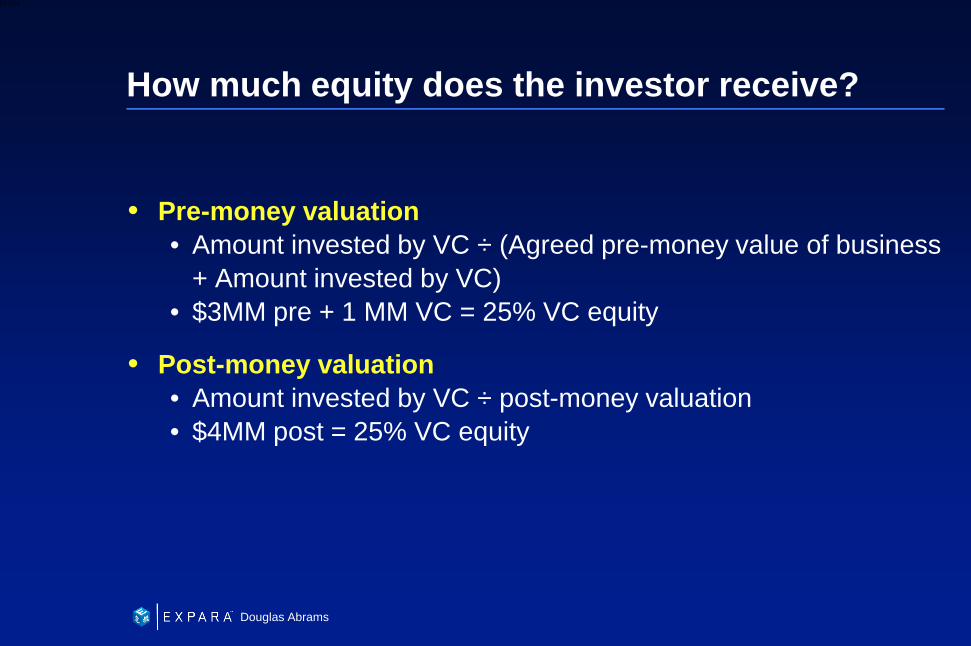

How much equity does the investor receive?

• Pre-money valuation • Amount invested by VC ÷ (Agreed pre-money value of business

+ Amount invested by VC) • $3MM pre + 1 MM VC = 25% VC equity

• Post-money valuation • Amount invested by VC ÷ post-money valuation • $4MM post = 25% VC equity

71

6XXXX

Douglas Abrams

Comparables

• Use value that has already been established either in public markets or through a sale for a comparable company

• Difficulties • How to find comps • Accounting methods vary • Public versus private liquidity • Changing market conditions

72

6XXXX

Douglas Abrams

DCF Valuation Model

• Firm value is discounted present value of future cash flows

• Percent of sales forecasting

• Tie income-statement and balance sheet figures to future sales

• Variable costs and most current assets and liabilities tend to vary directly with sales

• Only future sales require prediction; relationship between items can be calculated more easily

73

6XXXX

Douglas Abrams

Discounted cash flow

• Project cash flow from operations for 3-5 years

• Adjust the cash flow for factors such as non-recurring items of income and expense, depreciation, amortization, interest and taxes

• Discount the cash flow as adjusted, using alternative assumptions for time and risk factors.

74

6XXXX

Douglas Abrams

VC method of valuation

• What is the required investment today? (I$)

• What is the exit valuation for this company? ($EV)

• What is the target multiple of money on our investment? (M)

• What is the expected retention percentage? (%RP)

• Estimate the total valuation for the company today? TV = ($EV * %RP / M)

• What is the proposed ownership percentage today? (%P)

• Estimate the partial valuation for this investment PV = (%P * TV)

• Investment recommendation: compare partial valuation to required investment PV > I$ ?

75

6XXXX

Douglas Abrams

Idea to Investment – Venture Capital

• Understanding the VC mindset – risk and return

• Evaluating scalability

• Evaluating start-up business models

• Forecasting revenue, expenses and cash flow

• Valuing start-ups

• VC investment process

• Understanding term sheets and deal structures

76

6XXXX

Douglas Abrams

Schedule

Day 2 9:00 AM VC investment process 10:30 AM Break 10:45 AM Term sheets and deal structure 12:30 PM Lunch 1:30 PM VC-startup negotiation exercise briefing 2:15 PM VC-startup negotiation team strategizing 3:00 PM Break 3:15 PM VC-startup negotiation exercise 4:30 PM VC startup negotiation game debrief 5:00 PM End day 2

77

6XXXX

Douglas Abrams

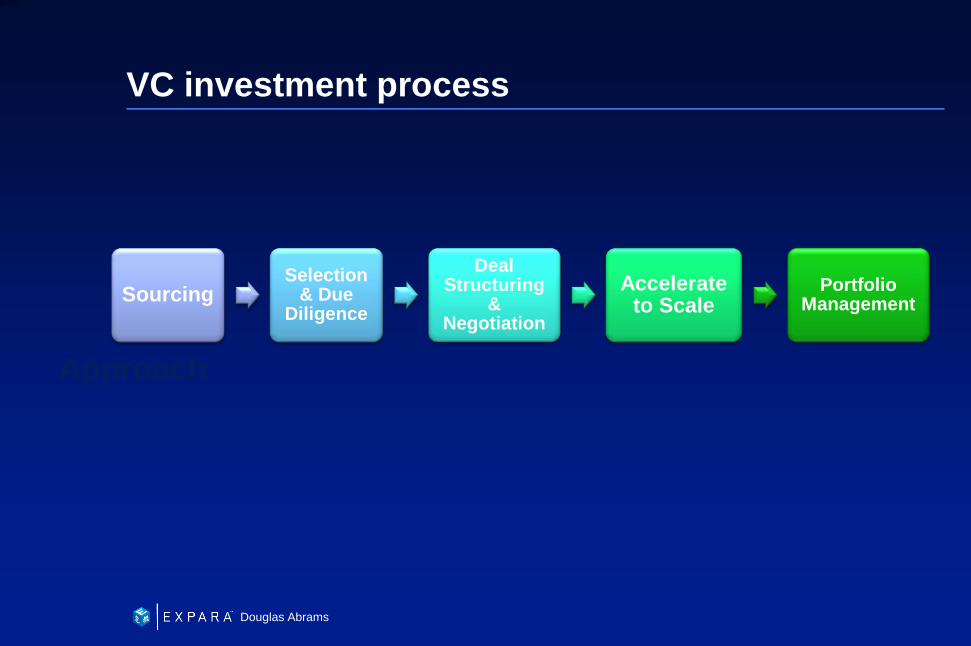

VC investment process

Approach

Sourcing Selection

& Due Diligence

Deal Structuring

& Negotiation

Accelerate to Scale

Portfolio Management

78

6XXXX

Douglas Abrams

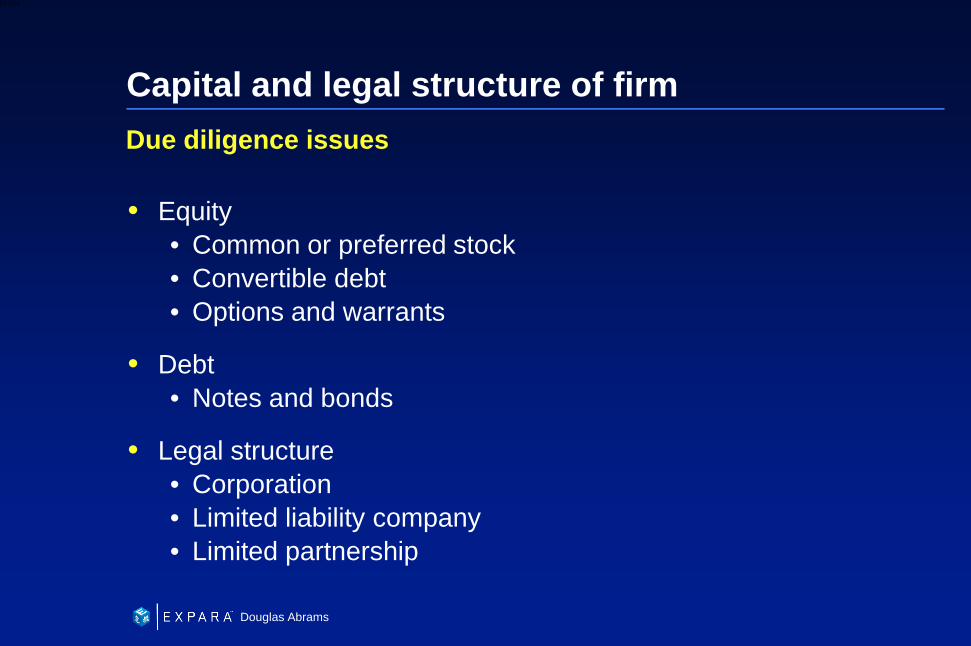

Capital and legal structure of firm

• Equity • Common or preferred stock • Convertible debt • Options and warrants

• Debt • Notes and bonds

• Legal structure • Corporation • Limited liability company • Limited partnership

Due diligence issues

79

6XXXX

Douglas Abrams

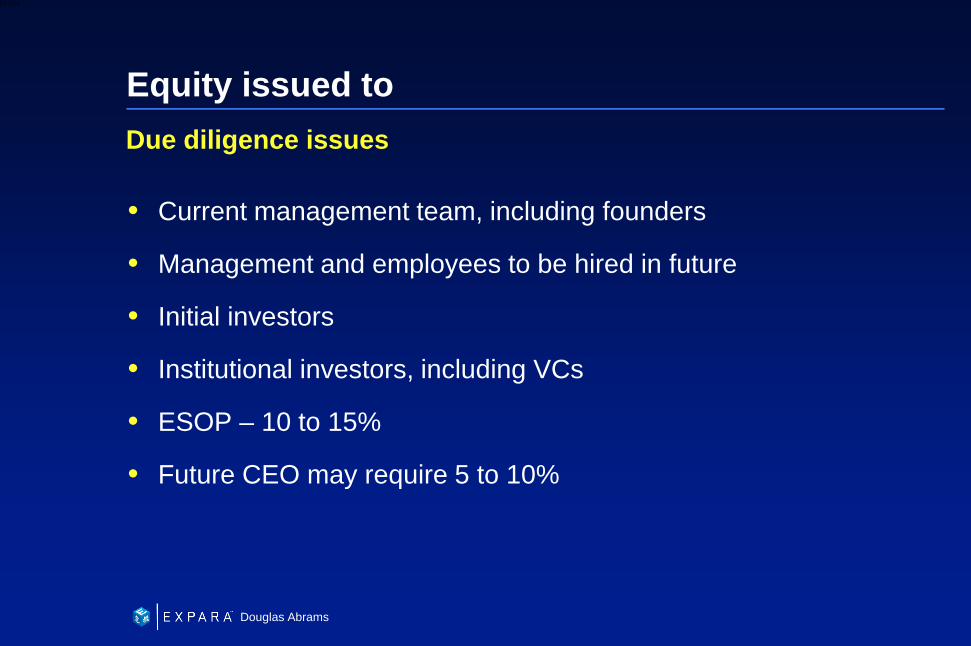

Equity issued to

• Current management team, including founders

• Management and employees to be hired in future

• Initial investors

• Institutional investors, including VCs

• ESOP – 10 to 15%

• Future CEO may require 5 to 10%

Due diligence issues

80

6XXXX

Douglas Abrams

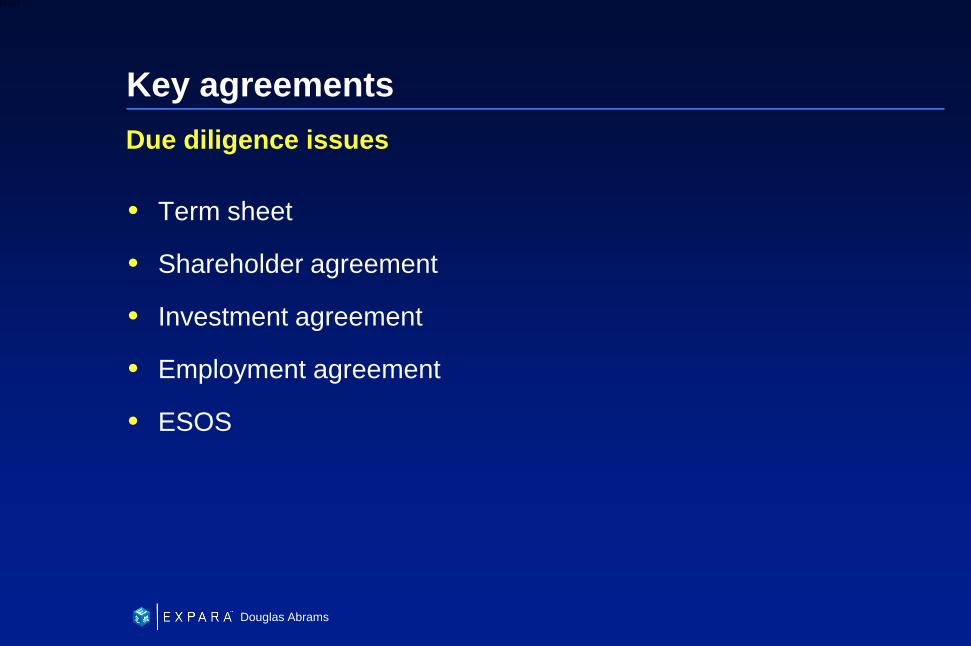

Key agreements

• Term sheet

• Shareholder agreement

• Investment agreement

• Employment agreement

• ESOS

Due diligence issues

82

6XXXX

Douglas Abrams

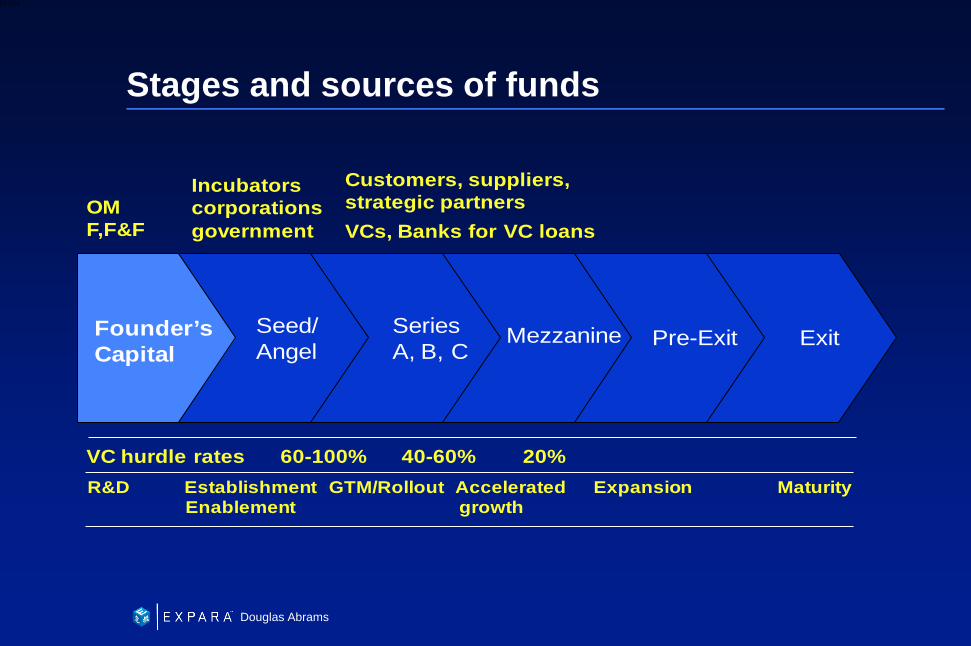

Stages and sources of funds

Founder’s Capital

Seed/Angel

Series A, B, C

Mezzanine Pre-Exit Exit

VC hurdle rates 60-100% 40-60% 20%

OM F,F&F

Incubators corporations government

Customers, suppliers, strategic partnersVCs, Banks for VC loans

R&D Establishment GTM/Rollout Accelerated Expansion MaturityEnablement growth

83

6XXXX

Douglas Abrams

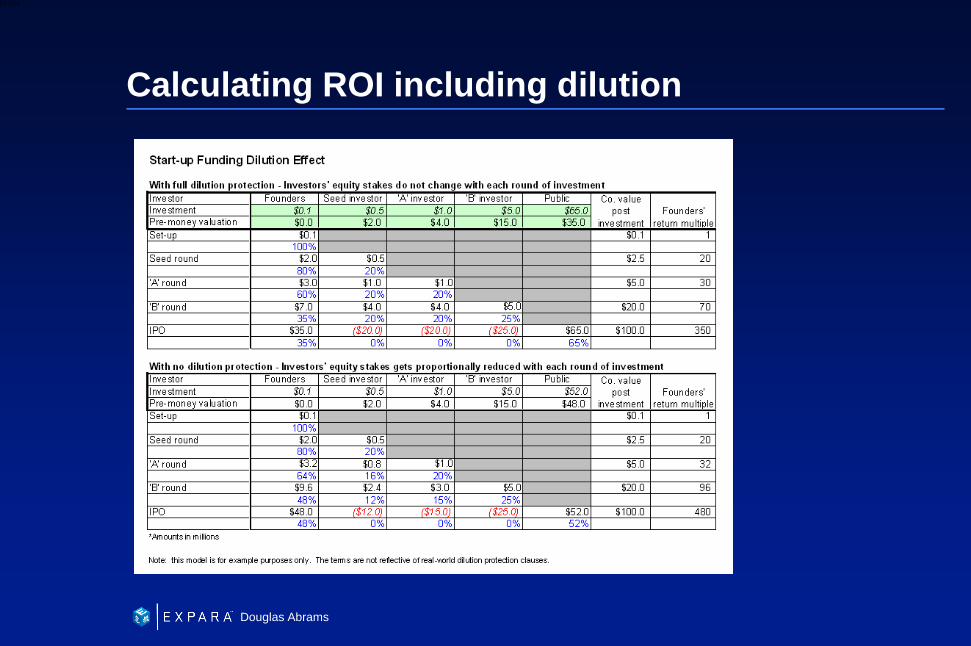

Calculating ROI including dilution

84

6XXXX

Douglas Abrams

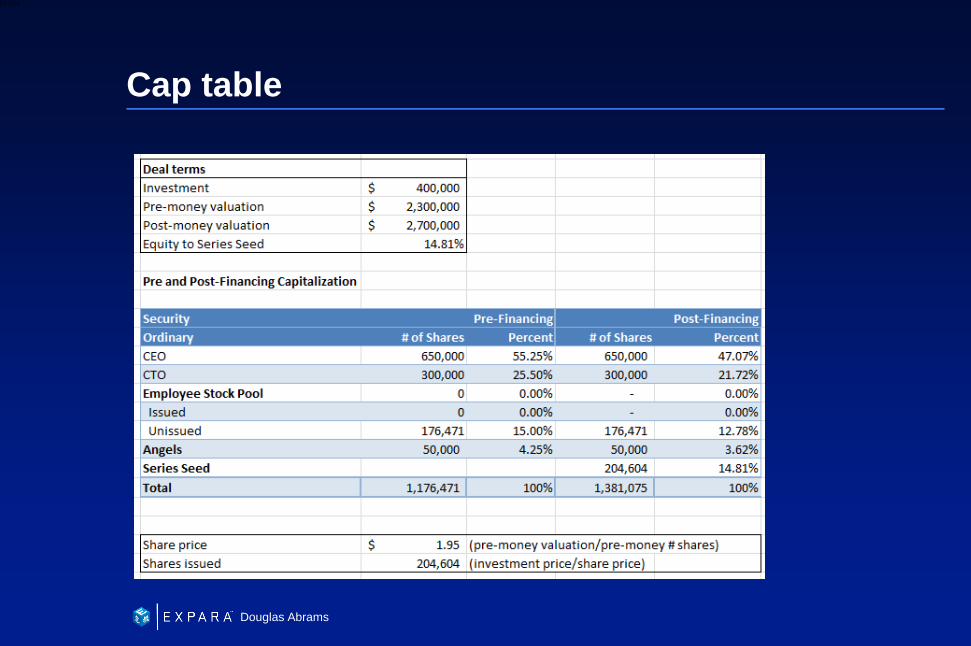

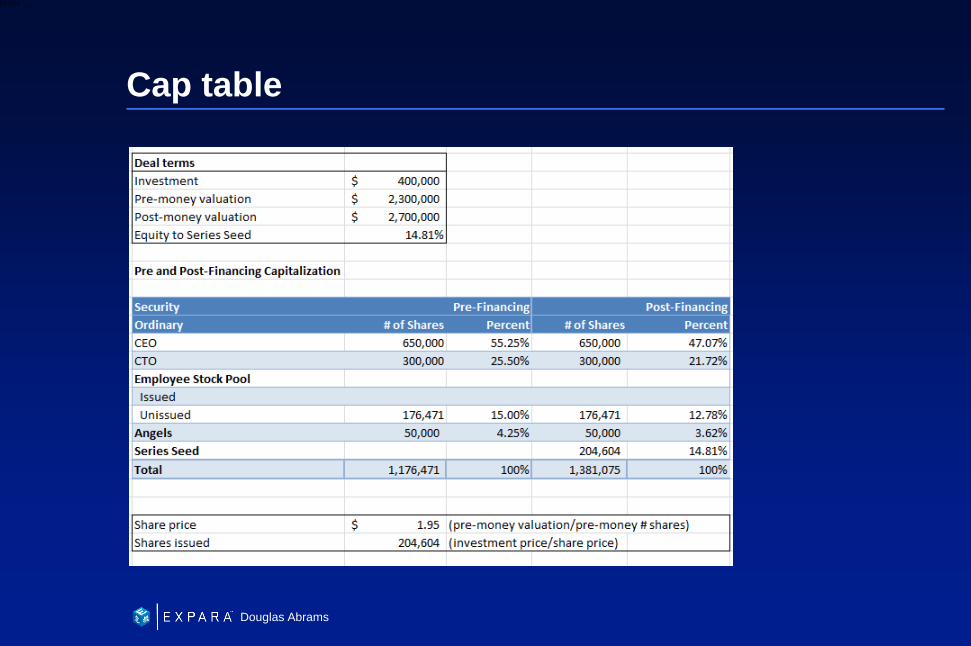

Cap table

85

6XXXX

Douglas Abrams

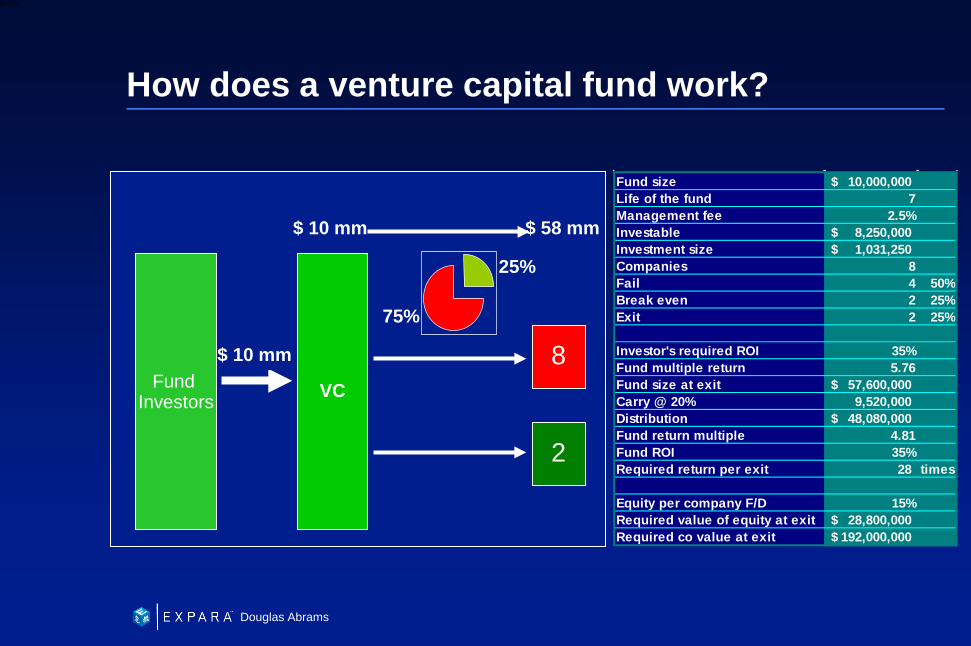

How does a venture capital fund work?

Fund Investors

VC

8

$ 10 mm

2

$ 10 mm

$ 58 mm

25%

75%

Fund size 10,000,000$ Life of the fund 7Management fee 2.5%Investable 8,250,000$ Investment size 1,031,250$ Companies 8Fail 4 50%Break even 2 25%Exit 2 25%

Investor's required ROI 35%Fund multiple return 5.76Fund size at exit 57,600,000$ Carry @ 20% 9,520,000 Distribution 48,080,000$ Fund return multiple 4.81Fund ROI 35%Required return per exit 28 times

Equity per company F/D 15%Required value of equity at exit 28,800,000$ Required co value at exit 192,000,000$

86

6XXXX

Douglas Abrams

Key terms of venture capital funds

• Fund size

• Term

• Management fee

• Distribution of returns – return of capital, performance fees, hurdle rate, catch-up

• Investment period

• Diversification and investment limits

87

6XXXX

Douglas Abrams

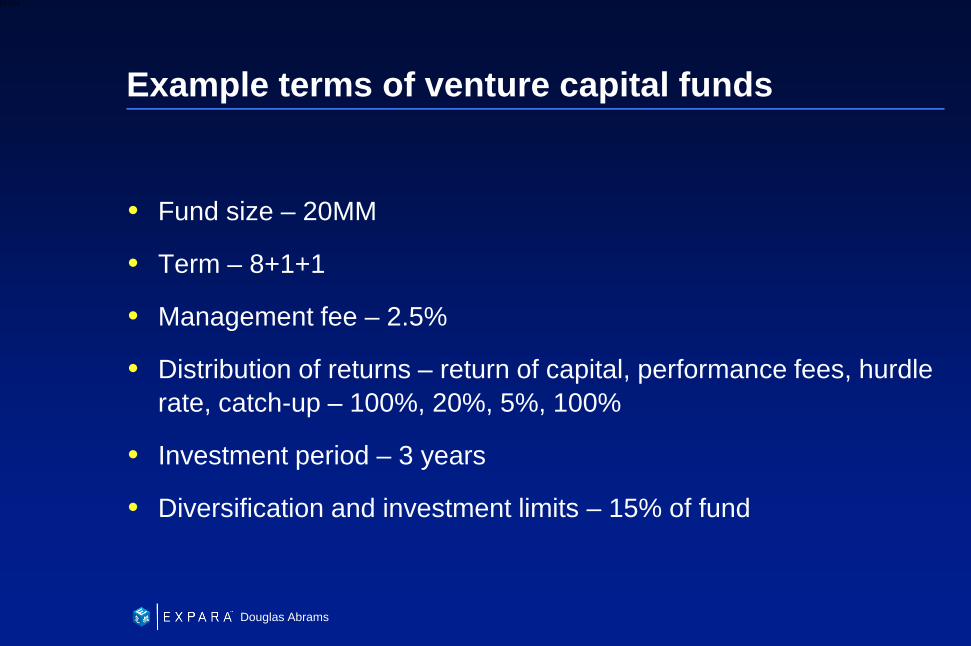

Example terms of venture capital funds

• Fund size – 20MM

• Term – 8+1+1

• Management fee – 2.5%

• Distribution of returns – return of capital, performance fees, hurdle rate, catch-up – 100%, 20%, 5%, 100%

• Investment period – 3 years

• Diversification and investment limits – 15% of fund

88

6XXXX

Douglas Abrams

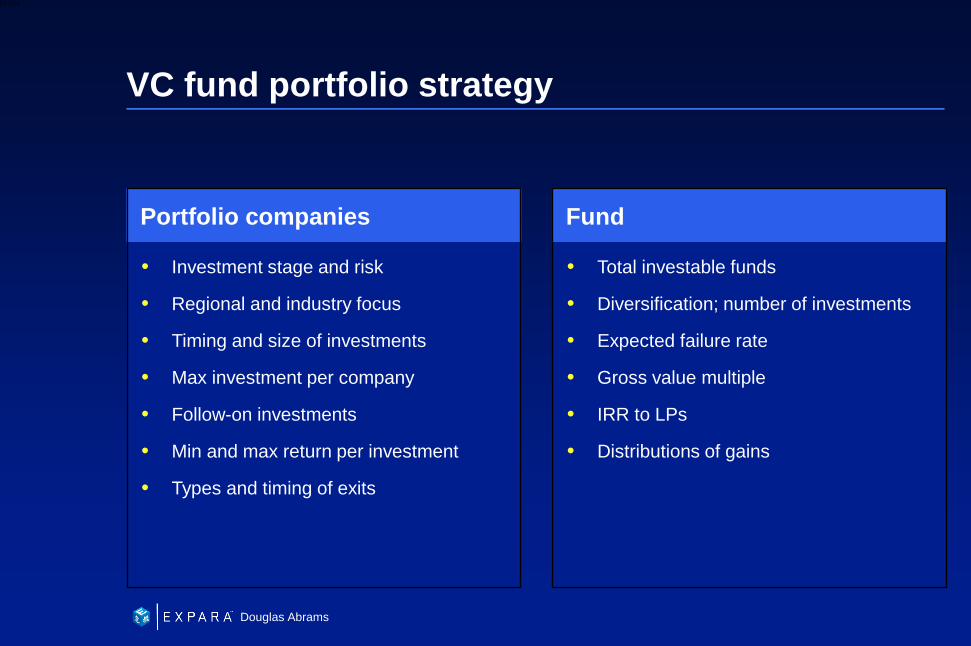

VC fund portfolio strategy

• Total investable funds

• Diversification; number of investments

• Expected failure rate

• Gross value multiple

• IRR to LPs

• Distributions of gains

Fund

• Investment stage and risk

• Regional and industry focus

• Timing and size of investments

• Max investment per company

• Follow-on investments

• Min and max return per investment

• Types and timing of exits

Portfolio companies

89

6XXXX

Douglas Abrams

Return to investors

• Best case and worst case

• Gross value multiple (GVM)

• Cash flows to investors

• IRR net of fees

90

6XXXX

Douglas Abrams

Investment strategy

• How many companies will you invest in?

• How will your investments break down by stage of investment?

• How will you define each stage of investment?

• Within each stage of investment, how will your investments break down by risk level?

• How much will you invest in each company?

• How many rounds of investments in each company?

• What will the timing be of your investments (e.g. year 1, how many of each type of investment, how much will each investment be, etc.). Include a capital deployment schedule that illustrates this.

91

6XXXX

Douglas Abrams

How will you generate returns?

• How many of your companies will fail, how many will exit?

• What will the timing be of your exits and failures?

• How will you exit?

• What will be the distribution of returns on your exits?

92

6XXXX

Douglas Abrams

Other strategic factors

• What industry verticals will you focus on for your investments?

• In what geographic regions will you invest?

• Any other special features of your fund strategy.

93

6XXXX

Douglas Abrams

Idea to Investment – Venture Capital

• Understanding the VC mindset – risk and return

• Evaluating scalability

• Evaluating start-up business models

• Forecasting revenue, expenses and cash flow

• Valuing start-ups

• VC investment process

• Understanding term sheets and deal structures

94

6XXXX

Douglas Abrams

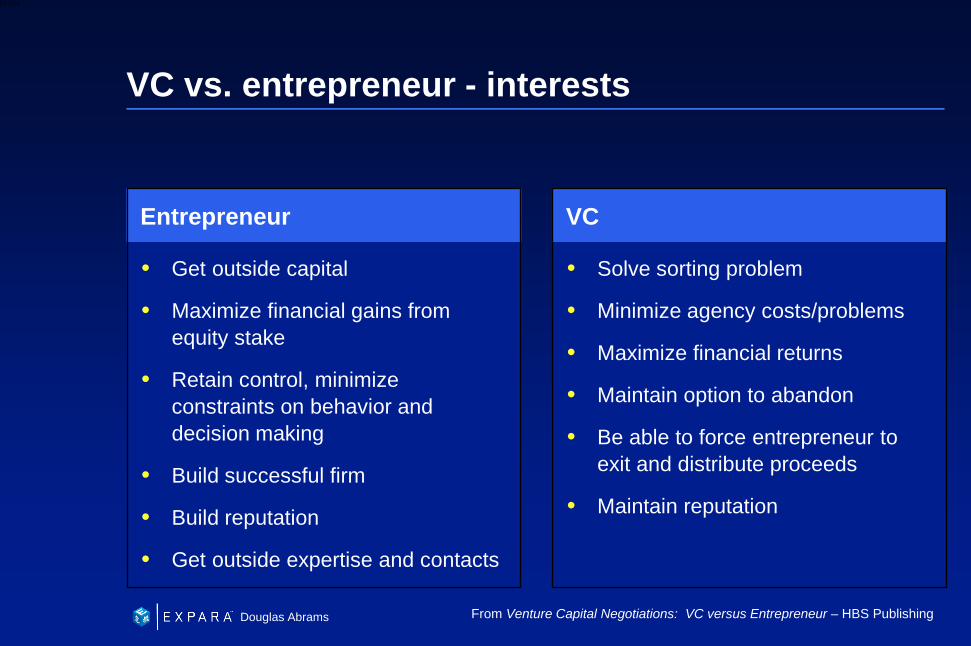

VC vs. entrepreneur - interests

• Solve sorting problem

• Minimize agency costs/problems

• Maximize financial returns

• Maintain option to abandon

• Be able to force entrepreneur to exit and distribute proceeds

• Maintain reputation

VC

• Get outside capital

• Maximize financial gains from equity stake

• Retain control, minimize constraints on behavior and decision making

• Build successful firm

• Build reputation

• Get outside expertise and contacts

Entrepreneur

From Venture Capital Negotiations: VC versus Entrepreneur – HBS Publishing

95

6XXXX

Douglas Abrams

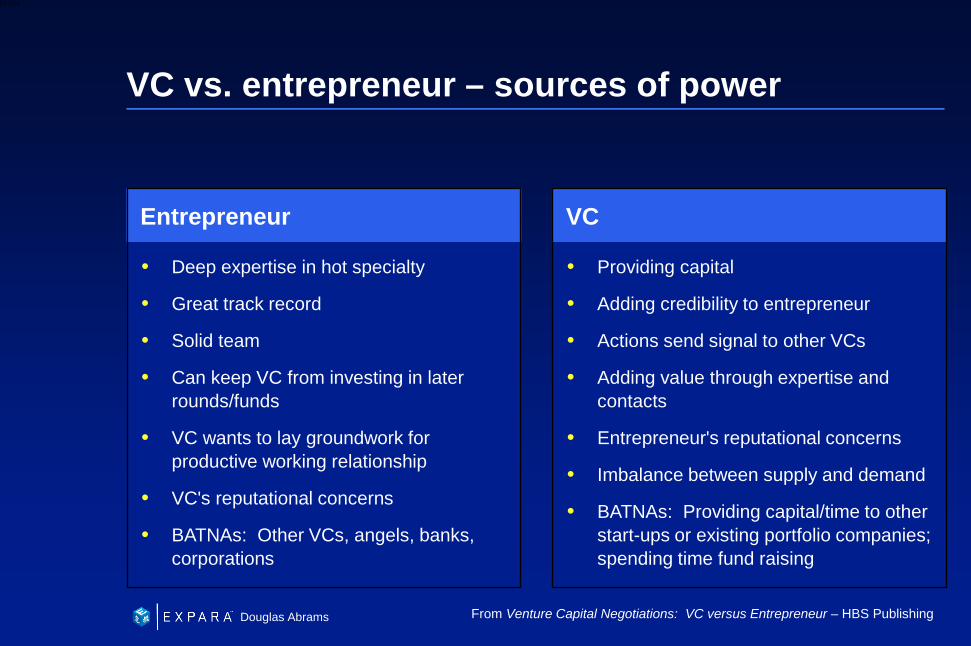

VC vs. entrepreneur – sources of power

• Providing capital

• Adding credibility to entrepreneur

• Actions send signal to other VCs

• Adding value through expertise and contacts

• Entrepreneur's reputational concerns

• Imbalance between supply and demand

• BATNAs: Providing capital/time to other start-ups or existing portfolio companies; spending time fund raising

VC

• Deep expertise in hot specialty

• Great track record

• Solid team

• Can keep VC from investing in later rounds/funds

• VC wants to lay groundwork for productive working relationship

• VC's reputational concerns

• BATNAs: Other VCs, angels, banks, corporations

Entrepreneur

From Venture Capital Negotiations: VC versus Entrepreneur – HBS Publishing

96

6XXXX

Douglas Abrams

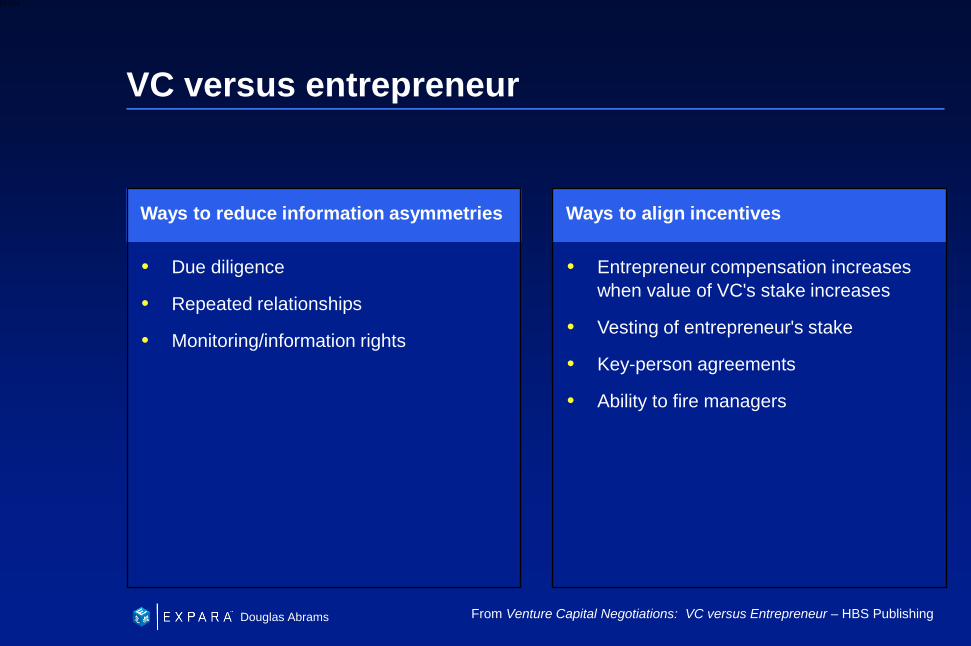

VC versus entrepreneur

• Entrepreneur compensation increases when value of VC's stake increases

• Vesting of entrepreneur's stake

• Key-person agreements

• Ability to fire managers

Ways to align incentives

• Due diligence

• Repeated relationships

• Monitoring/information rights

Ways to reduce information asymmetries

From Venture Capital Negotiations: VC versus Entrepreneur – HBS Publishing

97

6XXXX

Douglas Abrams

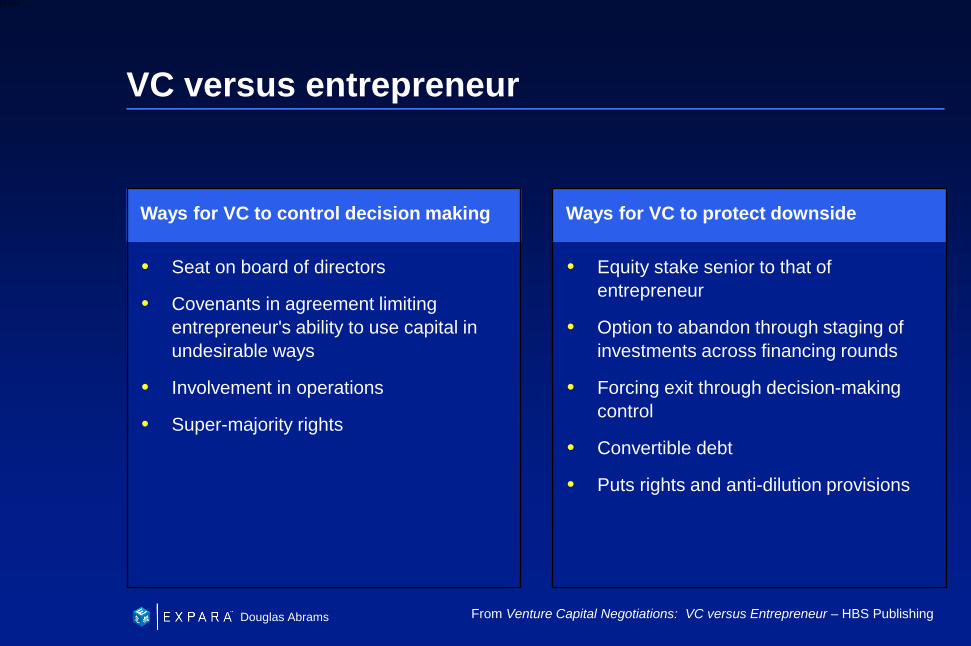

VC versus entrepreneur

• Equity stake senior to that of entrepreneur

• Option to abandon through staging of investments across financing rounds

• Forcing exit through decision-making control

• Convertible debt

• Puts rights and anti-dilution provisions

Ways for VC to protect downside

• Seat on board of directors

• Covenants in agreement limiting entrepreneur's ability to use capital in undesirable ways

• Involvement in operations

• Super-majority rights

Ways for VC to control decision making

From Venture Capital Negotiations: VC versus Entrepreneur – HBS Publishing

98

6XXXX

Douglas Abrams

Cap table

99

6XXXX

Douglas Abrams

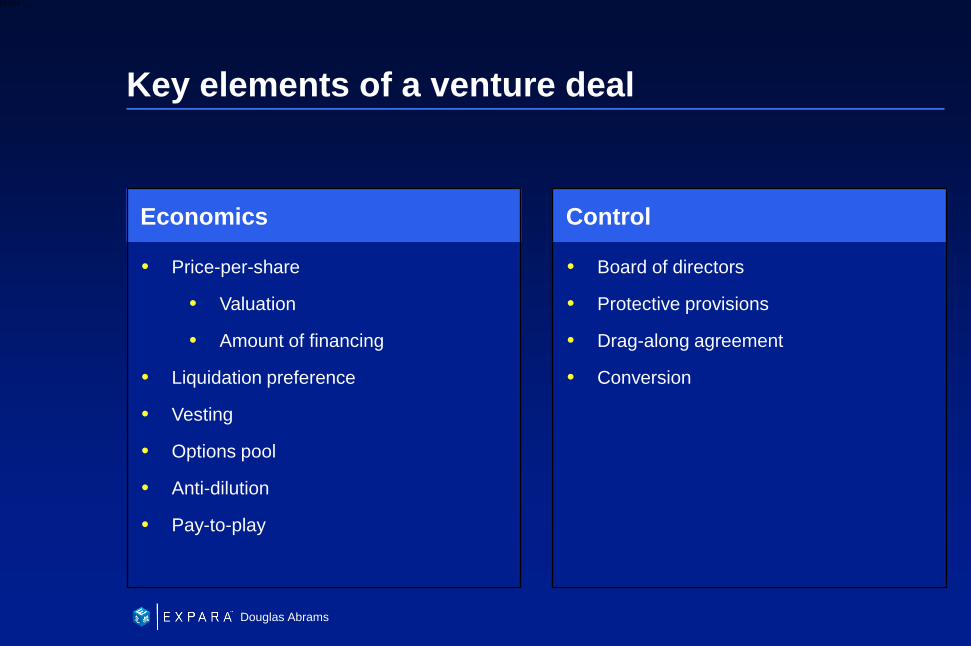

Key elements of a venture deal

• Board of directors

• Protective provisions

• Drag-along agreement

• Conversion

Control

• Price-per-share

• Valuation

• Amount of financing

• Liquidation preference

• Vesting

• Options pool

• Anti-dilution

• Pay-to-play

Economics

100

6XXXX

Douglas Abrams

Contact us

• Douglas Abrams

• Expara Pte. Ltd.

• www.expara.com

• 65-6323-3084, 65-9780-5381 (hp)

• Block 71 Ayer Rajah Crescent, #02-10/11 Singapore 139951

101

6XXXX

Douglas Abrams

Exercises

102

6XXXX

Douglas Abrams

Chapter 2 – VC players

2.1 Suppose that a $200M VC fund has a management fee of 2.5 percent per year for the first five years, with a reduction of 0.25 percent (25 basis points) in each year thereafter. All fees are paid on committed capital, and the fund has a 10-year life. What are the lifetime fees and investment capital for this fund?

2.2 (This is a little bit tricky.) Suppose that a $1B VC fund has fees of 2.0 percent per year in all years, with these fees paid on committed capital in the first five years and on net invested capital for years 6 through 10. You can assume the fund is fully invested by the beginning of year 6, then realizes 20 percent of its investment capital in each of the following five years. What are the lifetime fees and investment capital for this fund? (Make assumptions for any information that you think is still missing from the problem.)

103

6XXXX

Douglas Abrams

Chapter 2 – VC players

2.3 A VC firm is considering two different structures for its new $250M fund. Both structures would have management fees of 2 percent per year (on committed capital) for all 10 years. Under Structure I, the fund would receive an X percent carry with a basis of all committed capital. Under Structure II, the fund would receive a Y percent carry with a basis of all investment capital. For a given amount of (total) exit proceeds 5 $Z, solve for the amount of carried interest under both structures.

2.4 Talltree Ventures has raised their $250M fund, Talltree Ventures IV, with terms as given in Appendix 2.B of this chapter. Construct an example of fund performance where the clawback provision would be triggered. In this example, compute the carried interest paid in each year, and show the total amount that must be paid back by the GPs upon the liquidation of the fund.

104

6XXXX

Douglas Abrams

Chapter 3 – VC returns

3.1 The Bigco pension plan has invested in dozens of VC funds. The director of the pension plan is preparing his annual report to the Bigco board of directors. Summary information for Bigco’s VC portfolio is given in Exhibit 3-9. The board has asked for a five-year report of net returns and gross returns by year, plus the compound returns and annualized returns for all five years. You can assume that all new investments and management fees were paid for at the beginning of the year, and all distributions were paid at the end of the year.

3.2 Consider the case of XYZ Partners from Example 3.3. Now, instead of using a GVM of 2.5 (as in the example), assume that this GVM is unknown and equal to K.

(a) For any given K, solve for the carried interest, value multiple, and GP%. (b) How large must K be for the value multiple to be greater than 3? (c) How would your answer to parts (a) and (b) change if the carry basis were equal

to investment capital? (In the original example, the carry basis is equal to committed capital.)

105

6XXXX

Douglas Abrams

Chapter 3 – VC returns

3.3 True, False, or Uncertain: If both EBV and Owl have the same GVM, then the value multiple of Owl will be lower than the value multiple of EBV. (See Appendices 2.A and 2.C for more information on EBV and Owl.)

106

6XXXX

Douglas Abrams

Chapter 4 – Cost of capital for VC

4.1 The Largeco pension fund aggregates its entire portfolio every month across all asset classes and computes its net returns, Ri Exhibit 4-7 displays these monthly returns for one year, along with the market returns and the risk-free treasury bill rates for those months. Use Equations (4.1) and (4.2) to estimate the beta, alpha, and cost of capital for the Largeco portfolio. How do you evaluate its investment performance?

4.2 True, False, or Uncertain: Early stage venture capital should earn a higher expected return than later-stage venture capital, because early stage ventures have a higher failure rate than later-stage ventures.

107

6XXXX

Douglas Abrams

Chapter 4 – Cost of capital for VC

4.3 Consider the following three companies:

(i) Gasco owns and operates a chain of gas stations in the northeast United States.

(ii) Fuelco is a prerevenue company that is attempting to develop new fuel cell

technologies to replace the internal combustion engine.

(iii) Combco combines the operations of Gasco and Fuelco.

Use qualitative reasoning to order the cost of capital for these three companies from lowest to highest. (There is more than one reasonable way to answer this question, but there are also wrong ways to answer.)

108

6XXXX

Douglas Abrams

Chapter 8 – Term sheets

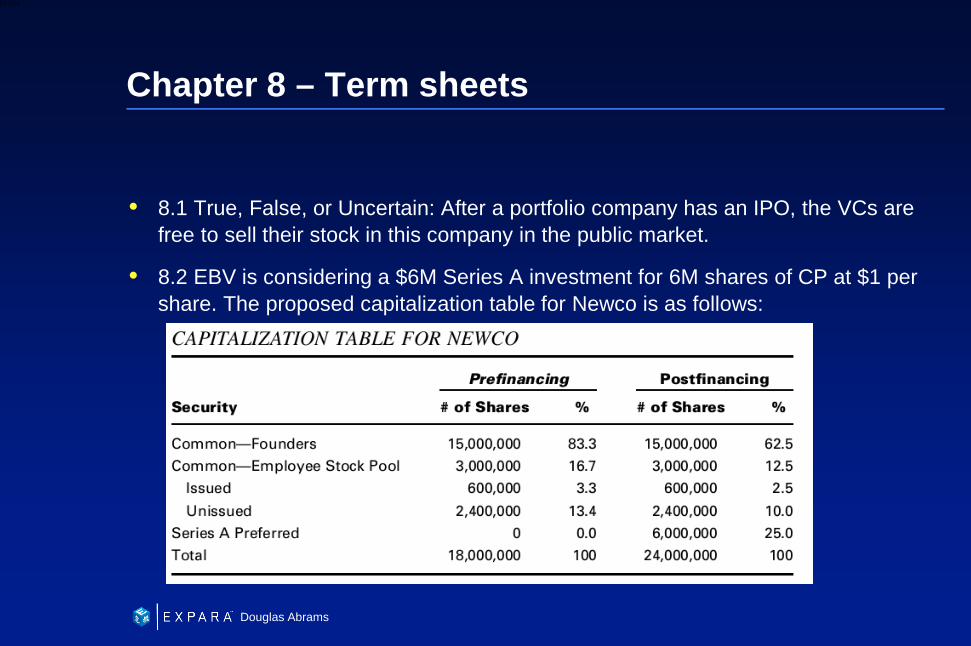

8.1 True, False, or Uncertain: After a portfolio company has an IPO, the VCs are free to sell their stock in this company in the public market.

8.2 EBV is considering a $6M Series A investment for 6M shares of CP at $1 per share. The proposed capitalization table for Newco is as follows:

109

6XXXX

Douglas Abrams

Chapter 8 – Term sheets

(a) What are the OPP and APP for the Series A?

(b) What is the fully diluted share count?

(c) What is the proposed ownership percentage?

(d) What is the post-money valuation?

(e) What is the pre-money valuation?

110

6XXXX

Douglas Abrams

Chapter 9 – Preferred stock

9.1 Suppose that it is one year after EBV’s investment in Newco (using the CP structure from Exercise 8.2), and Talltree makes a Series B investment for 6M shares of Newco at $0.2 per share. Following the Series B investment, what percentage of Newco (fully diluted) would be controlled by EBV? Consider the following cases:

Case I: Series A has no antidilution protection.

Case II: Series A has full-ratchet antidilution protection.

Case III: Series A has broad-base weighted-average antidilution protection.

Case IV: Series A has narrow-base weighted-average antidilution protection.

111

6XXXX

Douglas Abrams

Chapter 9 – Preferred stock

9.2 Suppose that EBV decides to consider six possible structures for the Series A stock in Exercise 8.2:

Structure I: The original structure considered in Exercise 8.2: 6M shares of CP.

Structure II: 6M shares of common.

Structure III: RP + 6M shares of common.

Structure IV: PCP with participation as-if 6M shares of common.

Structure V: PCPC with participation as-if 6M shares of common, with liquidation return capped at 5 times OPP.

Structure VI: RP ($4M APP) 1 5M shares of CP ($2M APP).

Structures IV and V have mandatory conversion upon a QPO, where a QPO is any offering of at least $5 per common share and $15M of proceeds. For the purpose of solving this problem, assume that any exit above $5 per share will qualify as a QPO (i.e., acquisitions for at least $5 per common share would also be considered to be QPOs). Draw an exit diagram for each structure.

112

6XXXX

Douglas Abrams

Chapter 10 – the VC method

10.1 Suppose that the following four funds—all with committed capital of $100M—have combined to form a syndicate to invest in Newco:

(I) ABC Fund, management fees of 2.5 percent per year of committed capital for all 10 years.

(II) DEF Fund, management fees of 2.5 percent per year for the first 5 years, then decreasing by 25 basis points per year in each year from 6 to 10. All fees calculated based on committed capital.

(III) UVW fund, management fees of 2.0 percent per year. During the first 5 years of the fund, these fees are charged based on committed capital. Beginning in year 6, the fees are charged based on net invested capital. UVW expects to be fully invested by the beginning of year 6, and also to have realized 25 percent of all investment capital by this time. In each of the subsequent 5 years, UVW expects to realize about 15 percent of all investment capital.

(IV) XYZ fund, management fees of 2.0 percent per year of committed capital for all 10 years. The XYZ fund expects to make all exits very quickly and to reinvest capital back into new investments. The total amount of investments is limited to $100M.

(a) Suppose that each fund in the syndicate invests $5M in Newco. What is the LP cost for each fund?

(b) It is possible that all four funds could agree on all the assumptions to the VC method, but still disagree about the wisdom of making this investment. Explain the economic logic behind this possibility.

113

6XXXX

Douglas Abrams

Chapter 10 – the VC method

10.2 EBV is considering a $5M Series A investment in Newco. EBV proposes to structure the investment as 6M shares of convertible preferred stock. The employees of Newco have claims on 10M shares of common stock. Thus, following the Series A investment, Newco will have 10M common shares outstanding and would have 16M shares outstanding on conversion of the CP. EBV estimates a 25 percent probability for a successful exit, with an expected exit time in 5 years and an exit valuation of $500M. The $100M EBV fund has annual fees of 2 percent for each of its 10 years of life and earns 20 percent carried interest on all profits.

(a) What is your investment recommendation for EBV? (Show all steps.)

(b) How sensitive is this recommendation to different assumptions about the exit valuation and the probability of success?

(c) Given the evidence described in Chapter 7, do you think that 25 percent is an aggressive assumption about the probability of success for a first-round investment?

10.3 Assume that EBV invested in Newco at the terms in Exercise 10.2, and it is now one year later. Talltree is considering a $10M Series B investment in Newco. Talltree proposes to structure the investment as 8M shares of convertible preferred stock. The employees of Newco have claims on 10M shares of common stock, and the previous venture investors (EBV) hold 6M shares of Series A convertible preferred. Thus, following the Series B investment, Newco will have 10M common shares outstanding, and would have 24M shares outstanding on conversion of the CP. Talltree estimates a 40 percent probability for a successful exit, with an expected exit time in 4 years and an exit valuation of $500M. The $250M Talltree fund has annual fees of 2 percent for each of its 10 years of life and earns 20 percent carried interest on all profits.

(a) What is your investment recommendation for Talltree? (Show all steps.)

(b) How sensitive is this recommendation to different assumptions about the exit valuation and the probability of success?

(c) Given the evidence described in Chapter 7, do you think that 40 percent is an aggressive assumption about the probability of success for a second-round investment?

114

6XXXX

Douglas Abrams

Chapter 10 – the VC method

10.4 Assume that EBV and Talltree invested in Newco at the terms in Exercises 10.2 and 10.3, and it is now one year later. Owl is considering a $20M Series C investment in Newco. Talltree proposes to structure the investment as 12M shares of convertible preferred stock. The employees of Newco have claims on 10M shares of common stock, and the previous venture investors hold 6M shares of Series A convertible preferred (EBV) and 8M shares of Series B Convertible Preferred (Talltree). Thus, following the Series C investment, Newco will have 10M common shares outstanding and would have 36M shares outstanding on conversion of the CP. Owl estimates a 50 percent probability for a successful exit, with an expected exit time in three years, and an exit valuation of $500M. The $500M Owl fund has fees as given in Appendix 2.C in Chapter 2.

(a) What is your investment recommendation for Owl? (Show all steps.)

(b) How sensitive is this recommendation to different assumptions about the exit valuation and the probability of success?

(c) Given the evidence described in Chapter 7, do you think that 50 percent is an aggressive assumption about the probability of success for a third-round investment?

115

6XXXX

Douglas Abrams

Chapter 11 – DCF analysis

11.1 EBV is considering an investment in Softco, an early-stage software company. If Softco can execute on its business plan, then EBV estimates it would be five years until a successful exit, when Softco would have about $75M in revenue, a 20 percent operating margin, a tax rate of 40 percent, and approximately $75M in capital. Subsequent to a successful exit, EBV believes that Softco could enjoy seven more years of rapid growth. To make the transaction work, EBV believes that the exit value must be at least $400M. How does this compare with the reality-check DCF? How much must the baseline assumptions change to justify this valuation?

11.2 True, False, or Uncertain: Firm value is maximized when the return on capital is exactly equal to the cost of capital.

11.3 True, False, or Uncertain: If two firms have exactly the same balance sheet and income statement on their respective graduation dates, then the firm with the higher growth rate will also have the higher graduation value.

11.4 Perform a reality-check DCF for a publicly traded company of your choice.

116

6XXXX

Douglas Abrams

Chapter 12 – comparables analysis

12.1 Softco, the company valued in Exercise 11.1, is expected to have the following business at exit:

Softco provides business process integration software and services for corporations across a broad range of enterprise markets. Its main product is the Softco business process integration software platform together with packaged applications and content, where it expects to derive 75 percent of its revenue. In addition, the company expects to earn the remainder of its revenue from mainframe outsourcing and midrange systems management.

Use whatever resources you want to identify at least two comparable companies for Softco and to estimate a relative valuation.

12.2 Consider the following “denominators” suggested as part of a comparables analysis:

(a) Number of unique visitors to a website

(b) Number of patents held by the company

(c) Level of dividends paid to common shareholders

(d) Number of demo software programs downloaded per month

For each of these four denominators, choose the numerator that is most appropriate for doing comparables analysis.

12.3 True, False, or Uncertain: The harmonic mean will always provide a lower valuation than the geometric mean, which in turn will always provide a lower valuation than the median.

12.4 True, False, or Uncertain: The levered beta for a company is always greater than or equal to the unlevered beta for the same company.

![Titanium Workshop - [Sainté Mobile Days]](https://img.pdfslide.net/doc/110x75/554d2016b4c905c5208b4a36/titanium-workshop-sainte-mobile-days.jpg)