Embed Size (px)

Citation preview

#cbizmhmwebinar 1

CBIZ & MHM Executive Education Series™

Revenue Recognition Updates for Manufacturers James Comito and Mark Winiarski September 8 or November 11

#cbizmhmwebinar 2

About Us

• Together, CBIZ & MHM are a Top Ten accounting provider • Offices in most major markets • Tax, audit and attest* and advisory services • Over 2,900 professionals nationwide

A member of Kreston International A global network of independent accounting firms

#cbizmhmwebinar 3

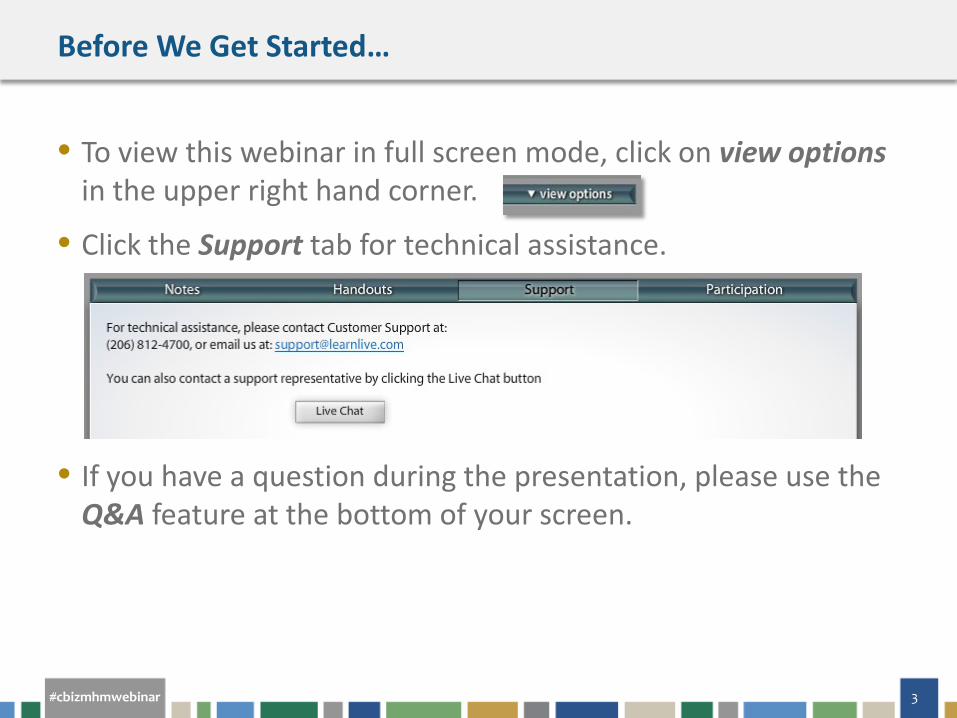

Before We Get Started…

• To view this webinar in full screen mode, click on view options in the upper right hand corner.

• Click the Support tab for technical assistance.

• If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

#cbizmhmwebinar 4

CPE Credit

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar. External participants will receive their CPE certificate via email immediately following the webinar.

#cbizmhmwebinar 5

Disclaimer

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

#cbizmhmwebinar 6

Presenters

The Director of MHM’s Professional Standards Group, James has

expertise in all aspects of revenue recognition, business combinations,

impairment of goodwill and other intangible assets, accounting for

stock-based compensation, accounting for equity and debt instruments

and other accounting issues.

James also has significant experience with a variety of other regulatory

and corporate governance issues pertaining to publicly traded

companies, including all aspects of internal control.

In addition, James frequently speaks on accounting and auditing matters

at various events for MHM.

858.795.2029 • [email protected]

JAMES COMITO, CPA MHM’s National Director of

Professional Standards

#cbizmhmwebinar 7

Presenters

Located in our Kansas City office, Mark is a member of our Professional

Standards Group (PSG). Mark's role includes instructing in our national

training program, presenting as a subject matter expert at webinars and

conferences, and preparing MHM publications on accounting and

auditing issues.

As a PSG member, Mark consults with clients and engagement teams

across the country in many areas of accounting and auditing. Mark has

served clients as an auditor, consultant and advisor in numerous

industries including manufacturing, distribution, mining, retail sales,

services and software.

913.234.1656 • [email protected] • @KCWini

MARK WINIARSKI, CPA MHM Shareholder

#cbizmhmwebinar 8

Agenda

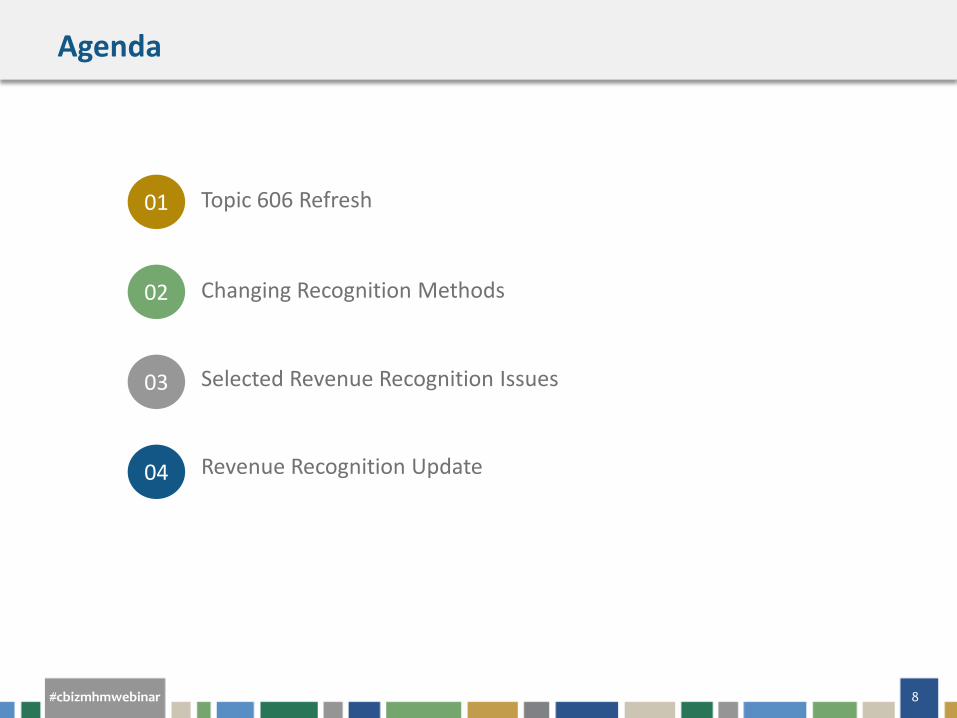

Topic 606 Refresh

02

01

03

04

Changing Recognition Methods

Selected Revenue Recognition Issues

Revenue Recognition Update

#cbizmhmwebinar 9

TOPIC 606 REFRESH

Overview of the New Revenue Recognition Guidance

#cbizmhmwebinar 10

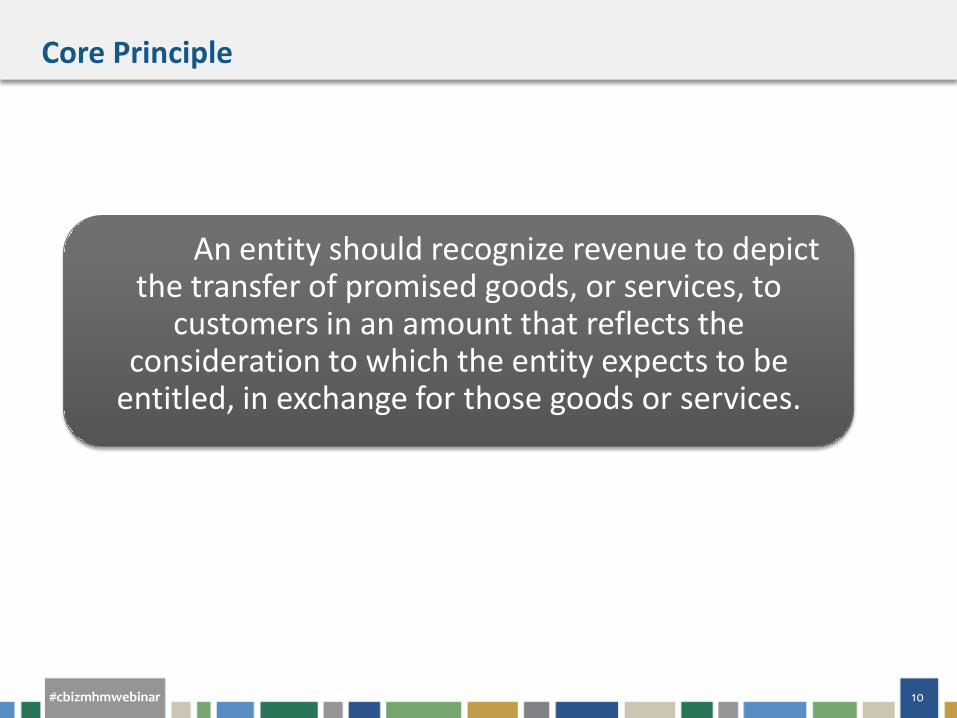

An entity should recognize revenue to depict the transfer of promised goods, or services, to

customers in an amount that reflects the consideration to which the entity expects to be

entitled, in exchange for those goods or services.

Core Principle

#cbizmhmwebinar 11

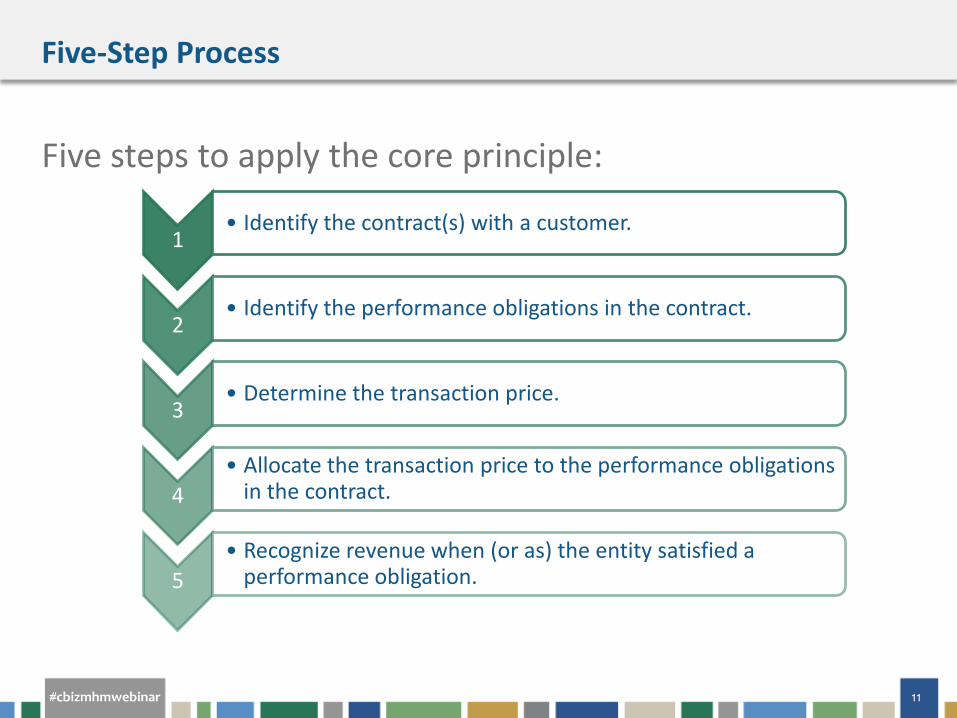

Five steps to apply the core principle:

Five-Step Process

1 • Identify the contract(s) with a customer.

2 • Identify the performance obligations in the contract.

3 • Determine the transaction price.

4 • Allocate the transaction price to the performance obligations

in the contract.

5 • Recognize revenue when (or as) the entity satisfied a

performance obligation.

#cbizmhmwebinar 12

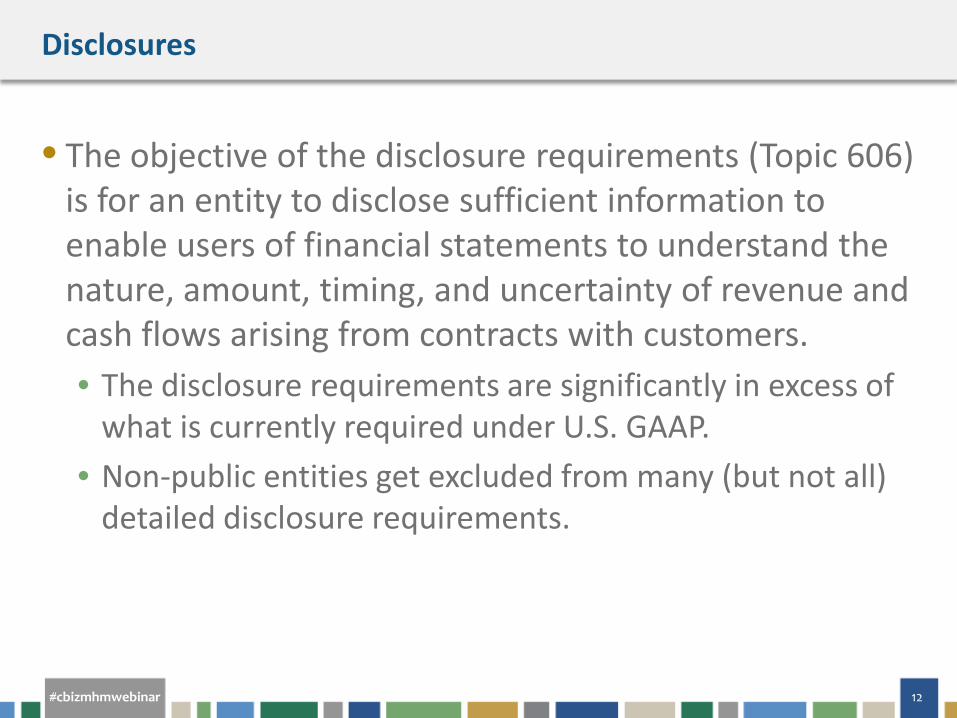

• The objective of the disclosure requirements (Topic 606) is for an entity to disclose sufficient information to enable users of financial statements to understand the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. • The disclosure requirements are significantly in excess of

what is currently required under U.S. GAAP. • Non-public entities get excluded from many (but not all)

detailed disclosure requirements.

Disclosures

#cbizmhmwebinar 13

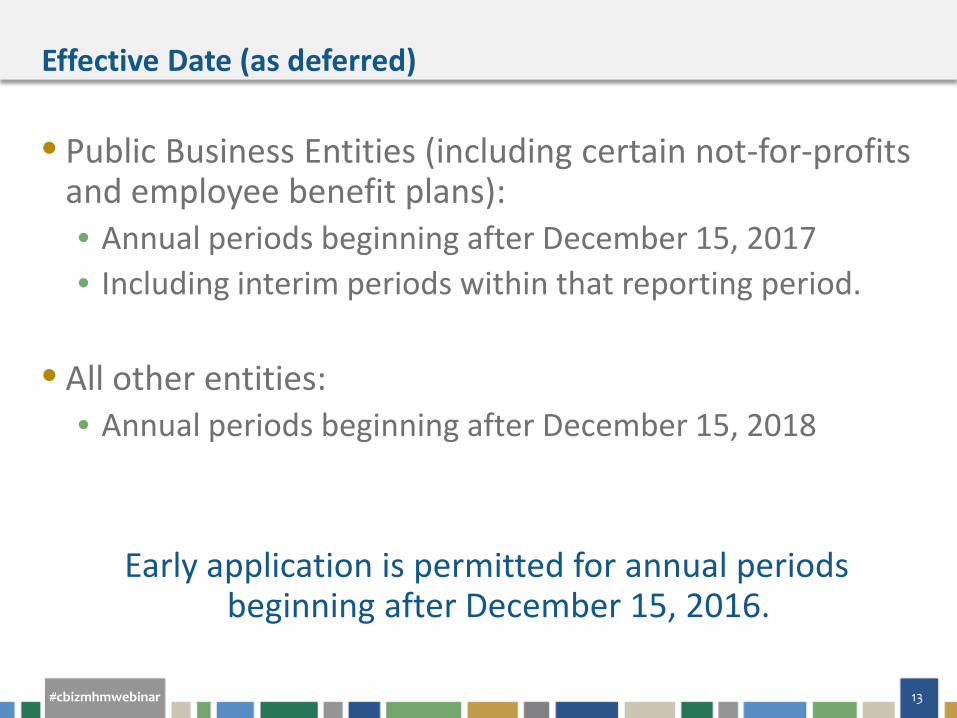

• Public Business Entities (including certain not-for-profits and employee benefit plans): • Annual periods beginning after December 15, 2017 • Including interim periods within that reporting period.

• All other entities:

• Annual periods beginning after December 15, 2018

Early application is permitted for annual periods

beginning after December 15, 2016.

Effective Date (as deferred)

#cbizmhmwebinar 14

• Retrospectively to each prior reporting period presented • Practical expedients provided

• Modified retrospectively

• Cumulative effect of initially applying the guidance recognized at the date of initial adoption

• Disclosure showing revenue recognition under Topic 605 in the year of adoption

• An explanation of the reasons for significant changes

Transition Method

#cbizmhmwebinar 15

CHANGING RECOGNITION METHODS

Revenue recognition could be different

#cbizmhmwebinar 16

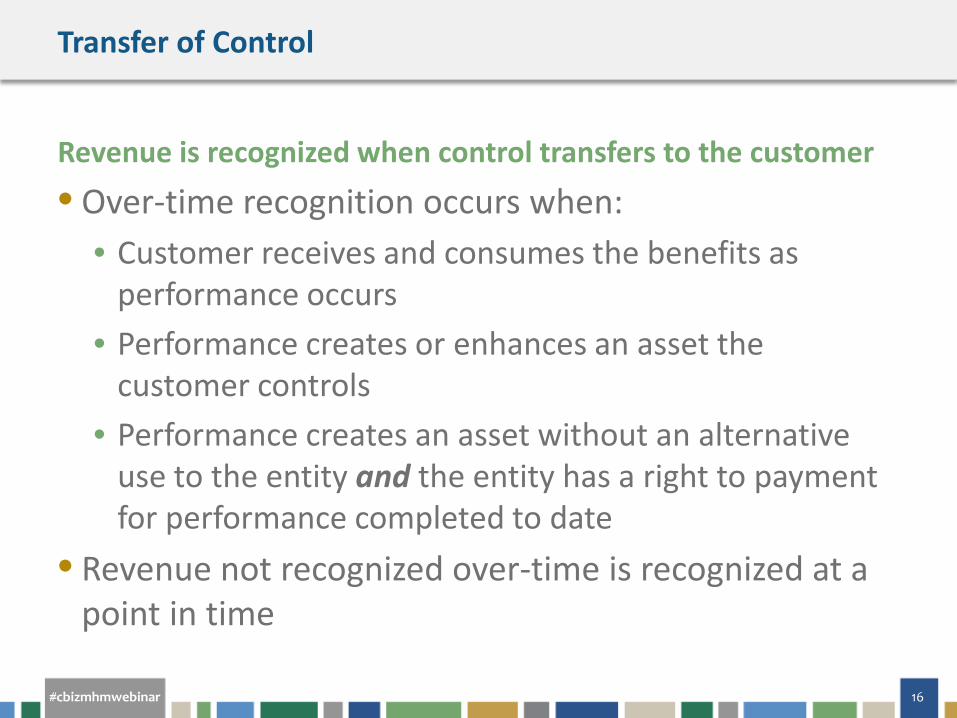

Transfer of Control

Revenue is recognized when control transfers to the customer

• Over-time recognition occurs when: • Customer receives and consumes the benefits as

performance occurs • Performance creates or enhances an asset the

customer controls • Performance creates an asset without an alternative

use to the entity and the entity has a right to payment for performance completed to date

• Revenue not recognized over-time is recognized at a point in time

#cbizmhmwebinar 17

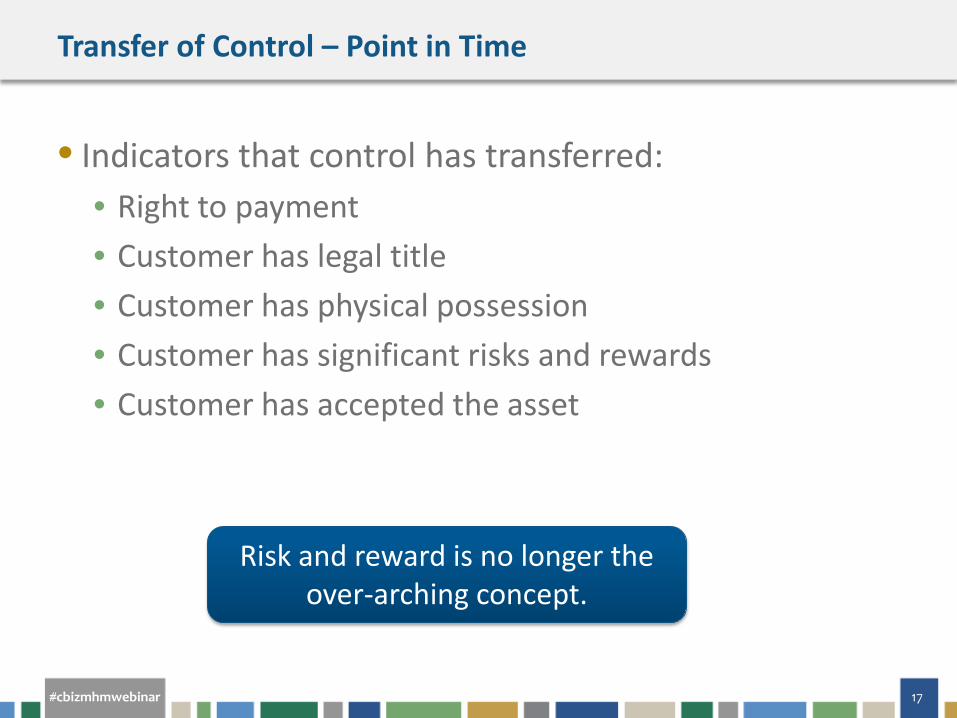

Transfer of Control – Point in Time

• Indicators that control has transferred: • Right to payment • Customer has legal title • Customer has physical possession • Customer has significant risks and rewards • Customer has accepted the asset

Risk and reward is no longer the over-arching concept.

#cbizmhmwebinar 18

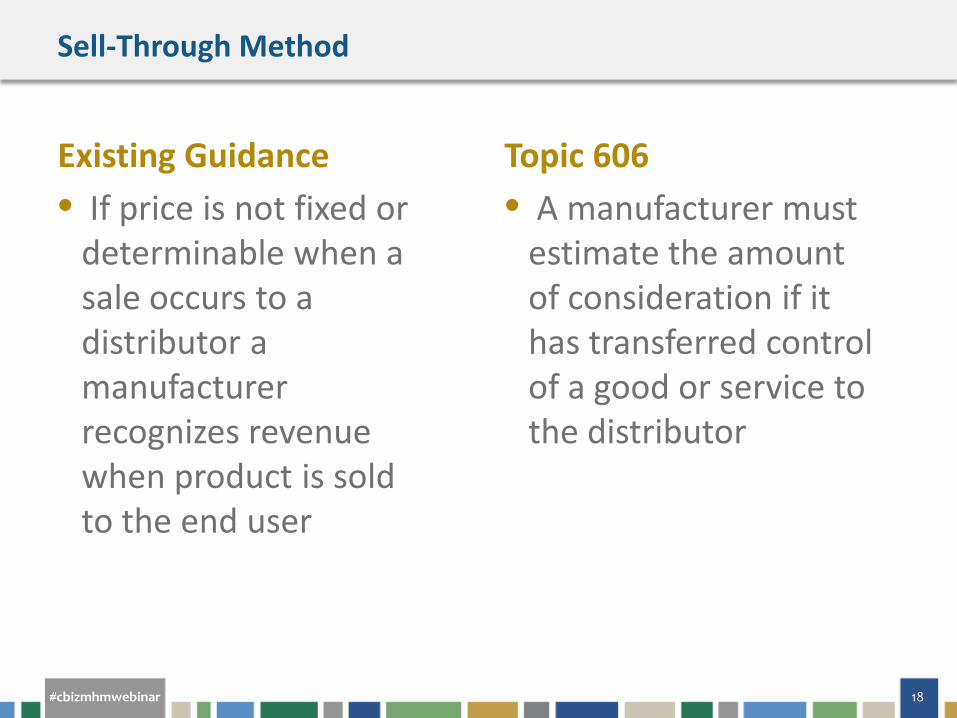

Sell-Through Method

Existing Guidance • If price is not fixed or

determinable when a sale occurs to a distributor a manufacturer recognizes revenue when product is sold to the end user

Topic 606 • A manufacturer must

estimate the amount of consideration if it has transferred control of a good or service to the distributor

#cbizmhmwebinar 19

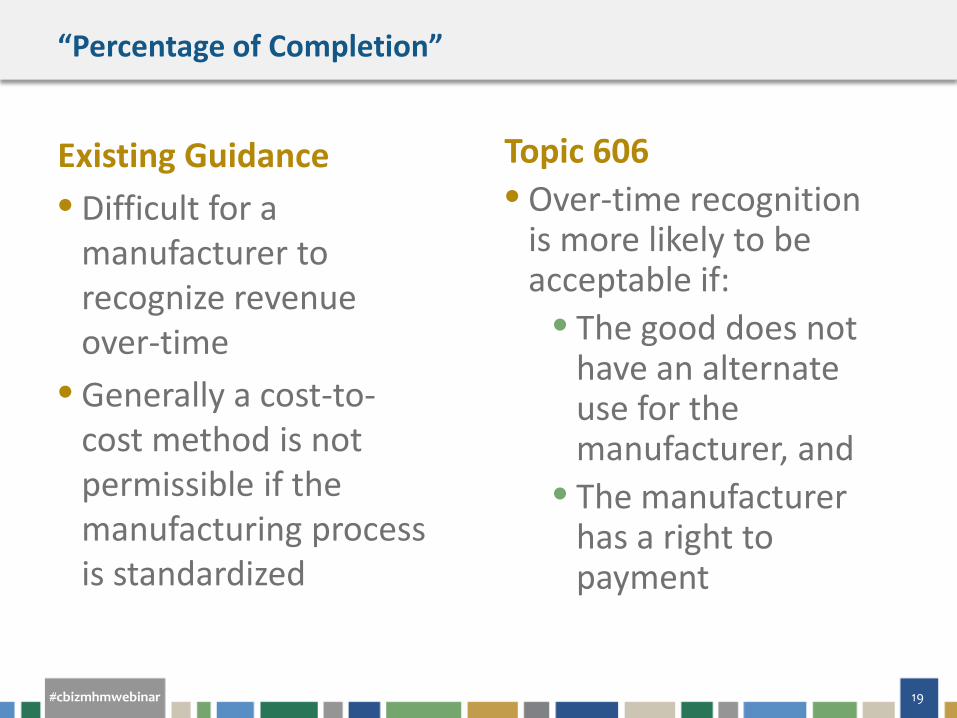

“Percentage of Completion”

Existing Guidance • Difficult for a

manufacturer to recognize revenue over-time

• Generally a cost-to-cost method is not permissible if the manufacturing process is standardized

Topic 606 • Over-time recognition

is more likely to be acceptable if: • The good does not

have an alternate use for the manufacturer, and

• The manufacturer has a right to payment

#cbizmhmwebinar 20

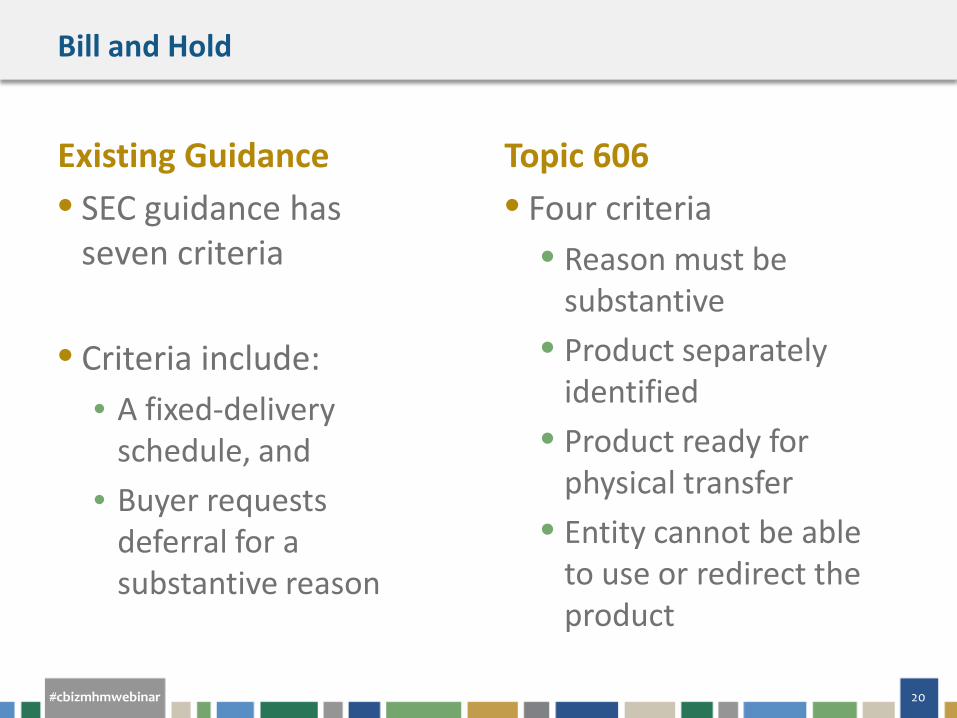

Bill and Hold

Existing Guidance • SEC guidance has

seven criteria

• Criteria include: • A fixed-delivery

schedule, and • Buyer requests

deferral for a substantive reason

Topic 606 • Four criteria

• Reason must be substantive

• Product separately identified

• Product ready for physical transfer

• Entity cannot be able to use or redirect the product

#cbizmhmwebinar 21

SELECTED REVENUE RECOGNITION ISSUES

Challenges for manufacturers

#cbizmhmwebinar 22

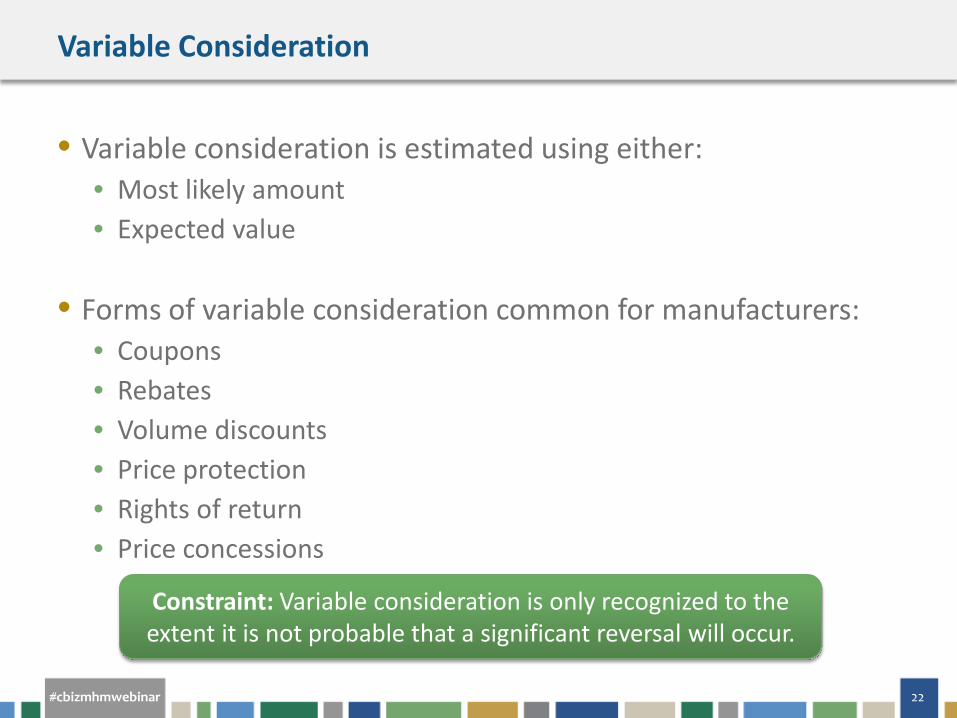

Variable Consideration

• Variable consideration is estimated using either: • Most likely amount • Expected value

• Forms of variable consideration common for manufacturers:

• Coupons • Rebates • Volume discounts • Price protection • Rights of return • Price concessions

Constraint: Variable consideration is only recognized to the extent it is not probable that a significant reversal will occur.

#cbizmhmwebinar 23

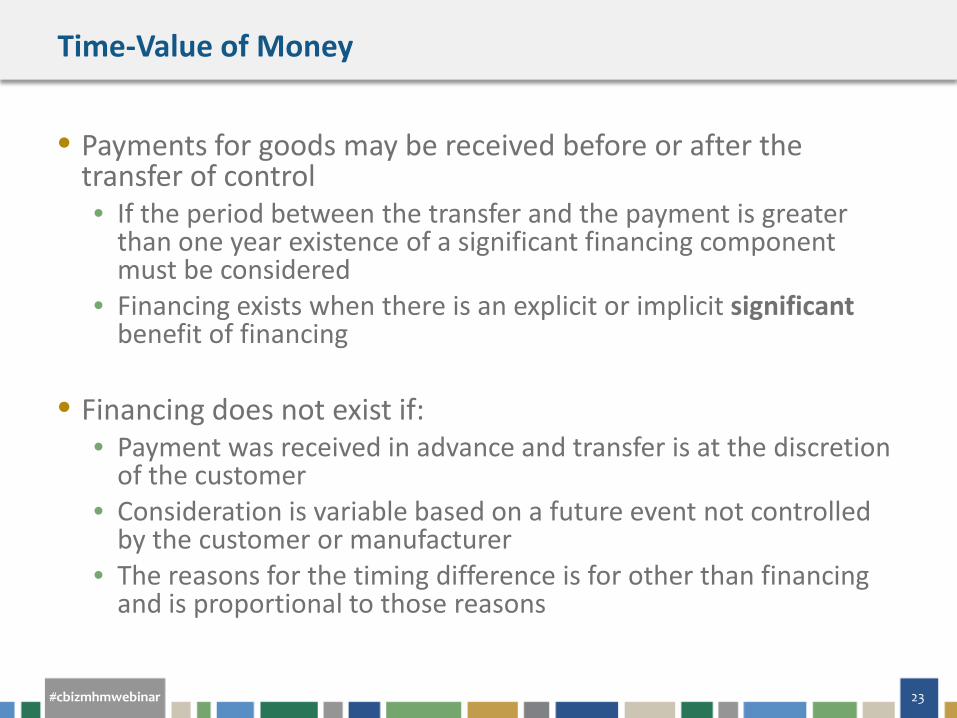

Time-Value of Money

• Payments for goods may be received before or after the transfer of control • If the period between the transfer and the payment is greater

than one year existence of a significant financing component must be considered

• Financing exists when there is an explicit or implicit significant benefit of financing

• Financing does not exist if:

• Payment was received in advance and transfer is at the discretion of the customer

• Consideration is variable based on a future event not controlled by the customer or manufacturer

• The reasons for the timing difference is for other than financing and is proportional to those reasons

#cbizmhmwebinar 24

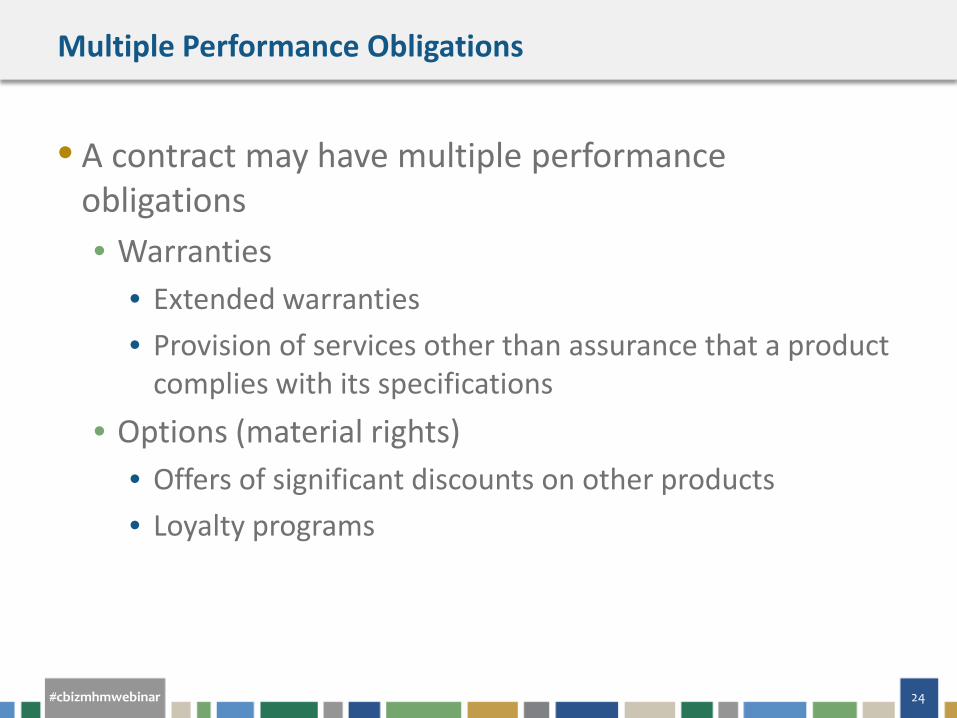

Multiple Performance Obligations

• A contract may have multiple performance obligations • Warranties

• Extended warranties • Provision of services other than assurance that a product

complies with its specifications • Options (material rights)

• Offers of significant discounts on other products • Loyalty programs

#cbizmhmwebinar 25

REVENUE RECOGNITION UPDATE

Upcoming changes to Topic 606

#cbizmhmwebinar 26

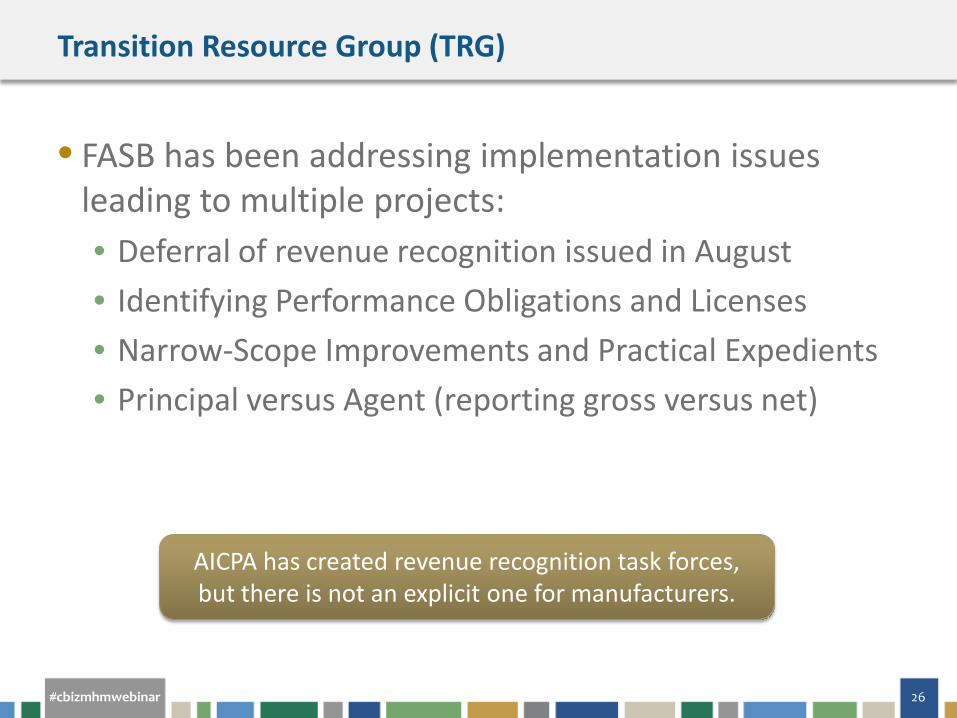

Transition Resource Group (TRG)

• FASB has been addressing implementation issues leading to multiple projects: • Deferral of revenue recognition issued in August • Identifying Performance Obligations and Licenses • Narrow-Scope Improvements and Practical Expedients • Principal versus Agent (reporting gross versus net)

AICPA has created revenue recognition task forces, but there is not an explicit one for manufacturers.

#cbizmhmwebinar 27

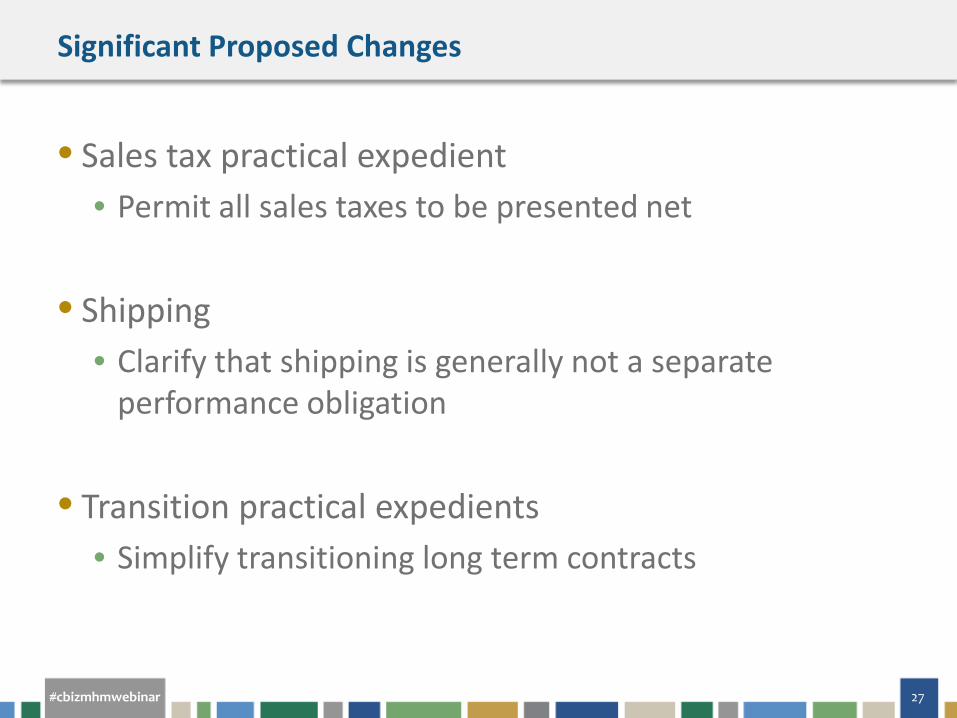

Significant Proposed Changes

• Sales tax practical expedient • Permit all sales taxes to be presented net

• Shipping

• Clarify that shipping is generally not a separate performance obligation

• Transition practical expedients

• Simplify transitioning long term contracts

#cbizmhmwebinar 28

? QUESTIONS

#cbizmhmwebinar 29

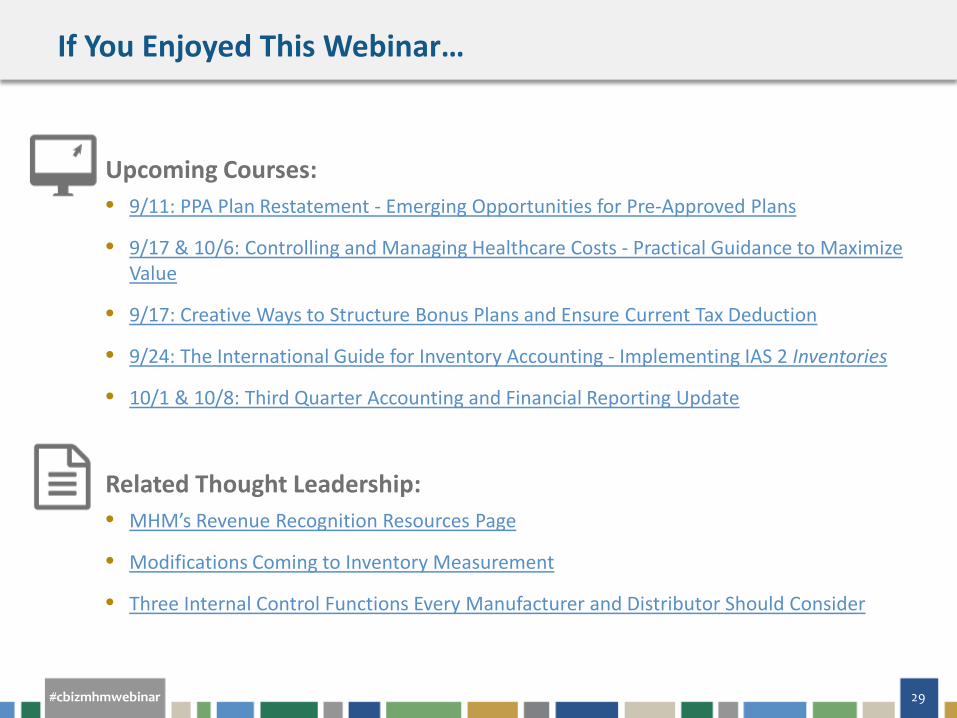

If You Enjoyed This Webinar…

Upcoming Courses: • 9/11: PPA Plan Restatement - Emerging Opportunities for Pre-Approved Plans

• 9/17 & 10/6: Controlling and Managing Healthcare Costs - Practical Guidance to Maximize Value

• 9/17: Creative Ways to Structure Bonus Plans and Ensure Current Tax Deduction

• 9/24: The International Guide for Inventory Accounting - Implementing IAS 2 Inventories

• 10/1 & 10/8: Third Quarter Accounting and Financial Reporting Update

Related Thought Leadership: • MHM’s Revenue Recognition Resources Page

• Modifications Coming to Inventory Measurement

• Three Internal Control Functions Every Manufacturer and Distributor Should Consider

#cbizmhmwebinar 30

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/ BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ