Embed Size (px)

DESCRIPTION

eXtension webinar on income taxes and tax planning

Citation preview

Year-End Tax Planning Strategies

Barbara O’Neill, Ph.D., CFP®, AFC, CHC Rutgers Cooperative Extension

Webinar Objectives

• Increase participants’ knowledge about income tax filing process

• Increase participants’ knowledge of tax planning strategies

• Provide update of 2014 and 2015 tax law changes

• Provide information about income tax resources

• Help participants save money on income taxes

Webinar Topics • Federal income tax rates

• Tax deductions and credits

• Tax filing process

• Tax avoidance vs. tax evasion

• Tax record-keeping

• Common tax errors

• 10 year-end tax planning strategies

• Tax planning resources

Question #1 What questions do people have about income taxes at the end of a calendar year?

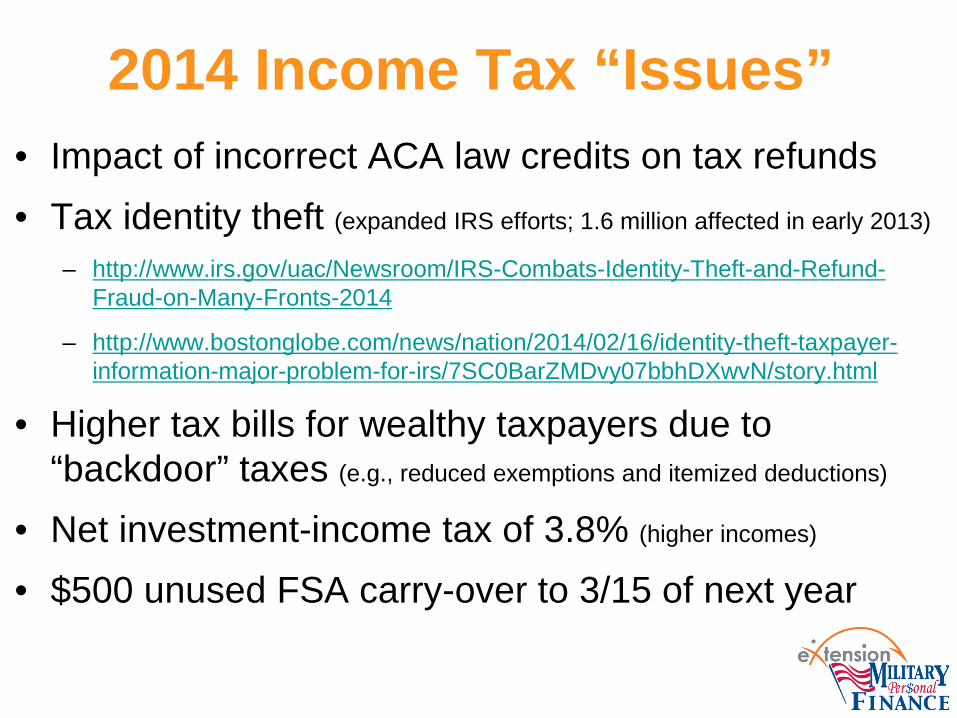

2014 Income Tax “Issues” • Impact of incorrect ACA law credits on tax refunds • Tax identity theft (expanded IRS efforts; 1.6 million affected in early 2013)

– http://www.irs.gov/uac/Newsroom/IRS-Combats-Identity-Theft-and-Refund-Fraud-on-Many-Fronts-2014

– http://www.bostonglobe.com/news/nation/2014/02/16/identity-theft-taxpayer-information-major-problem-for-irs/7SC0BarZMDvy07bbhDXwvN/story.html

• Higher tax bills for wealthy taxpayers due to “backdoor” taxes (e.g., reduced exemptions and itemized deductions)

• Net investment-income tax of 3.8% (higher incomes)

• $500 unused FSA carry-over to 3/15 of next year

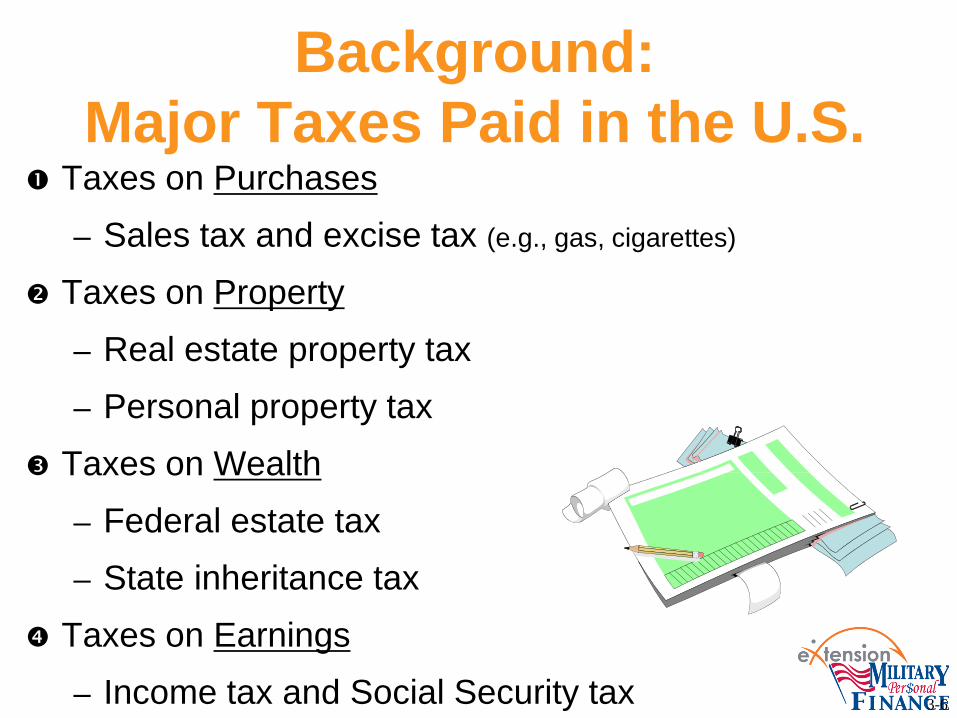

Background:

Major Taxes Paid in the U.S. Taxes on Purchases

– Sales tax and excise tax (e.g., gas, cigarettes)

Taxes on Property – Real estate property tax – Personal property tax

Taxes on Wealth – Federal estate tax – State inheritance tax

Taxes on Earnings – Income tax and Social Security tax 3-6

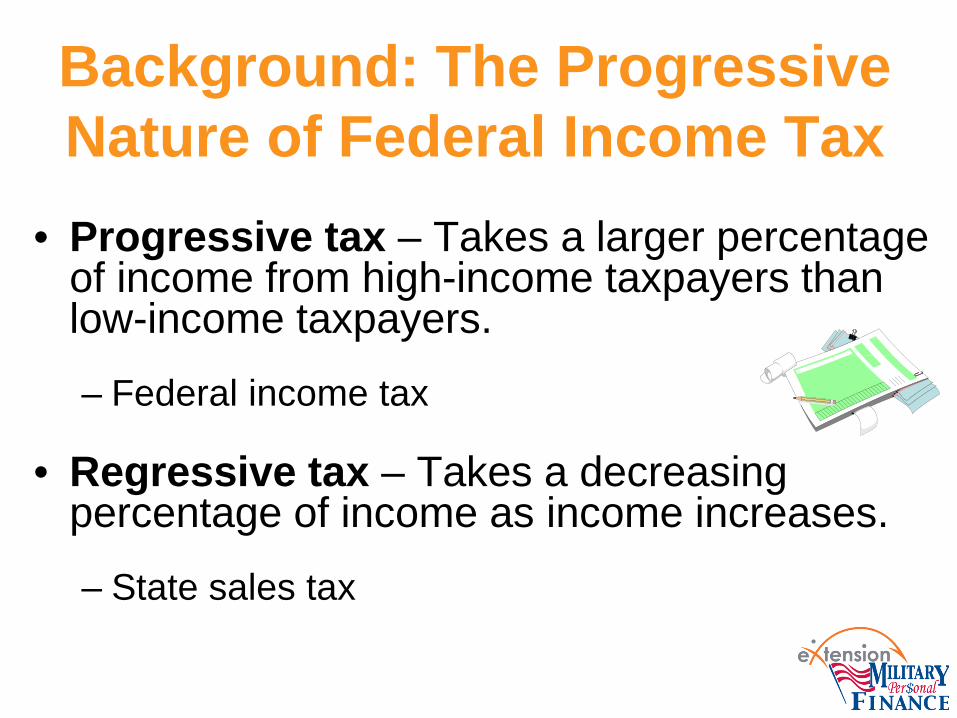

Background: The Progressive Nature of Federal Income Tax

• Progressive tax – Takes a larger percentage of income from high-income taxpayers than low-income taxpayers.

– Federal income tax

• Regressive tax – Takes a decreasing percentage of income as income increases.

– State sales tax

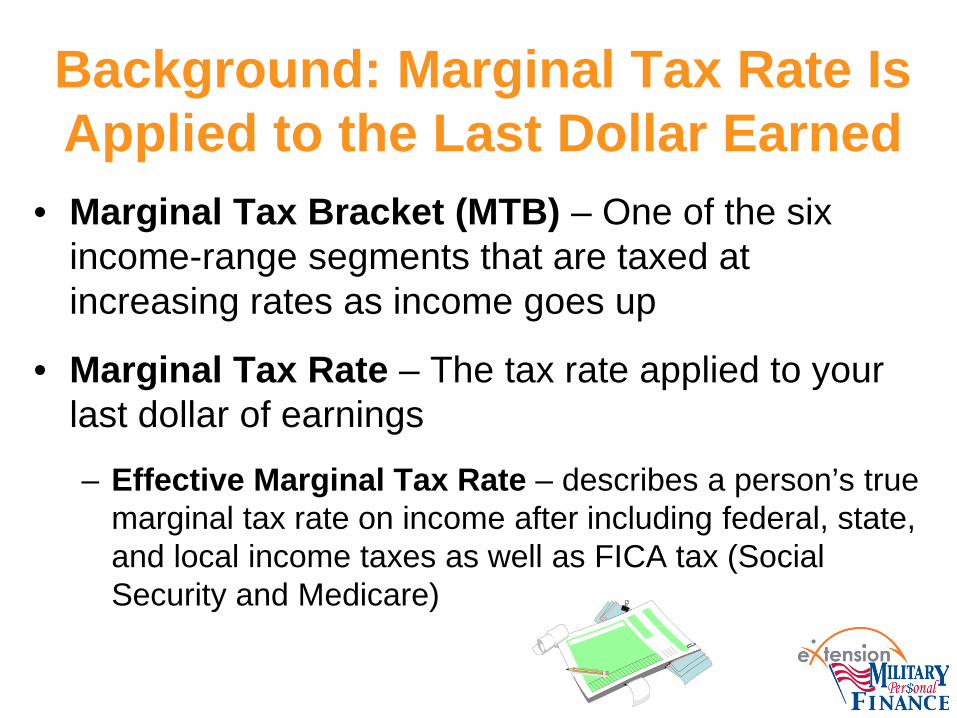

Background: Marginal Tax Rate Is Applied to the Last Dollar Earned

• Marginal Tax Bracket (MTB) – One of the six income-range segments that are taxed at increasing rates as income goes up

• Marginal Tax Rate – The tax rate applied to your last dollar of earnings

– Effective Marginal Tax Rate – describes a person’s true marginal tax rate on income after including federal, state, and local income taxes as well as FICA tax (Social Security and Medicare)

Background: Federal Tax Rates Tax Rates Are: • Established by Congress and change periodically

• Based on many things including:

• Amount and type of income

• Filing status - e.g. married, joint, single

Marginal rates: 10%, 15%, 25%, 28%, 33%, 35%, and 39.6% • Tax rate on last dollar of income earned

• Beginning in tax year 2013, the tax rate of 39.6% was added for individuals whose income exceeds $400,000 ($450,000 for married taxpayers filing a joint return)

• Rutgers fact sheet: http://njaes.rutgers.edu/money/taxinfo/

9

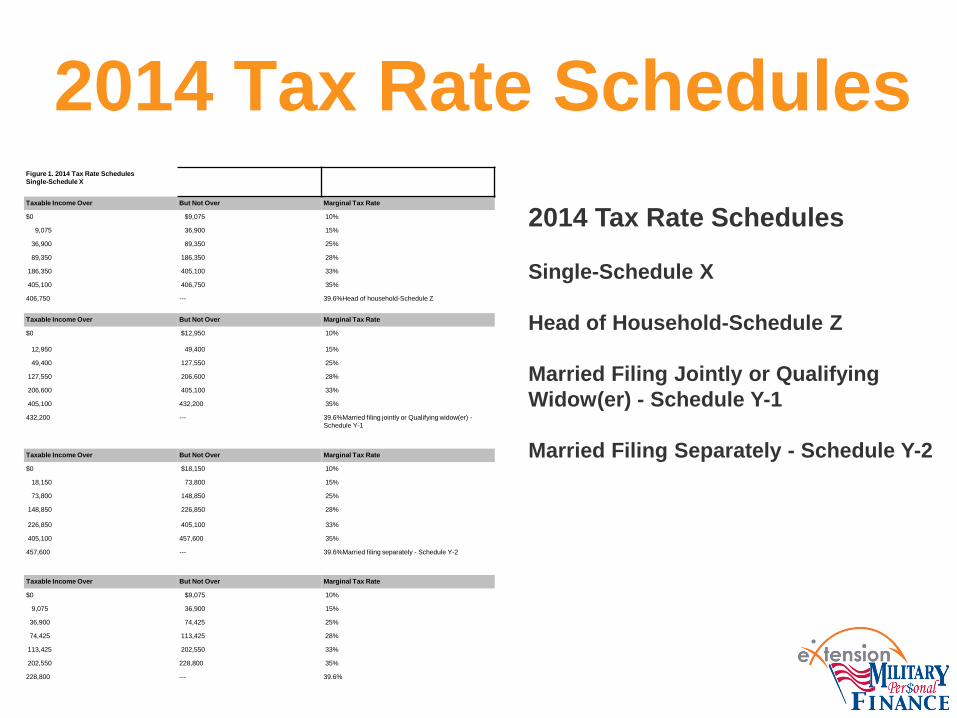

2014 Tax Rate Schedules Figure 1. 2014 Tax Rate Schedules Single-Schedule X

Taxable Income Over But Not Over Marginal Tax Rate

$0 $9,075 10%

9,075 36,900 15%

36,900 89,350 25%

89,350 186,350 28%

186,350 405,100 33%

405,100 406,750 35%

406,750 --- 39.6%Head of household-Schedule Z

Taxable Income Over But Not Over Marginal Tax Rate

$0 $12,950 10%

12,950 49,400 15%

49,400 127,550 25%

127,550 206,600 28%

206,600 405,100 33%

405,100 432,200 35%

432,200 --- 39.6%Married filing jointly or Qualifying widow(er) - Schedule Y-1

Taxable Income Over But Not Over Marginal Tax Rate

$0 $18,150 10%

18,150 73,800 15%

73,800 148,850 25%

148,850 226,850 28%

226,850 405,100 33%

405,100 457,600 35%

457,600 --- 39.6%Married filing separately - Schedule Y-2

Taxable Income Over But Not Over Marginal Tax Rate

$0 $9,075 10%

9,075 36,900 15%

36,900 74,425 25%

74,425 113,425 28%

113,425 202,550 33%

202,550 228,800 35%

228,800 --- 39.6%

2014 Tax Rate Schedules Single-Schedule X Head of Household-Schedule Z Married Filing Jointly or Qualifying Widow(er) - Schedule Y-1 Married Filing Separately - Schedule Y-2

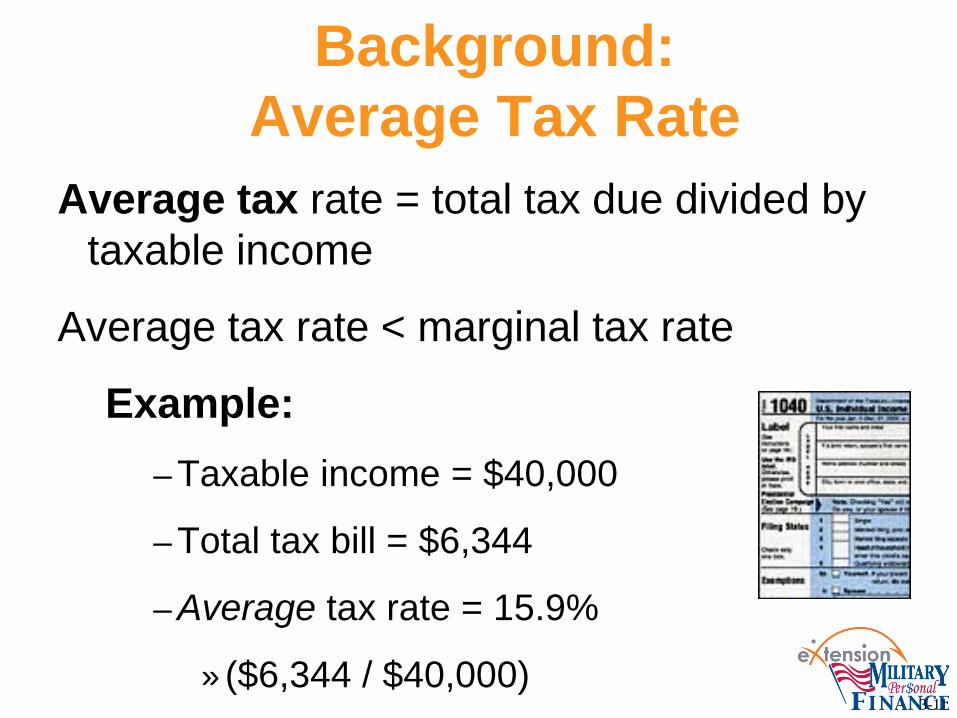

Background: Average Tax Rate

Average tax rate = total tax due divided by taxable income

Average tax rate < marginal tax rate

Example: – Taxable income = $40,000

– Total tax bill = $6,344

– Average tax rate = 15.9%

» ($6,344 / $40,000) 3-11

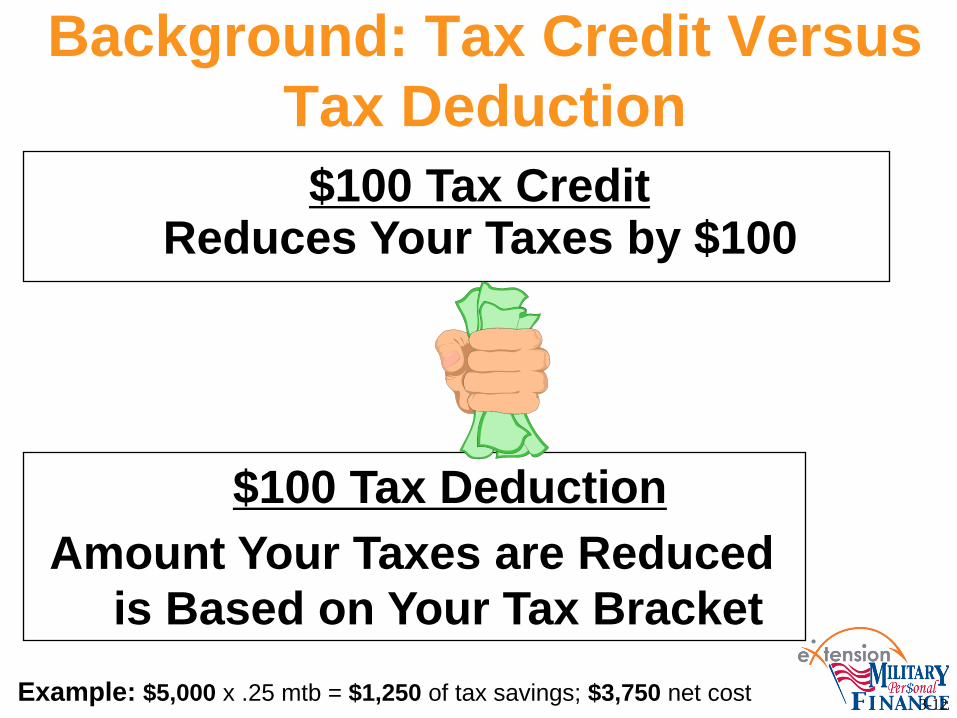

Background: Tax Credit Versus Tax Deduction $100 Tax Credit

Reduces Your Taxes by $100

$100 Tax Deduction Amount Your Taxes are Reduced

is Based on Your Tax Bracket

3-12 Example: $5,000 x .25 mtb = $1,250 of tax savings; $3,750 net cost

Background: Types of Deductions

Deduction = An amount subtracted from gross income to reduce the amount of income subject to tax. • Standard Deduction- Amount established each year by tax

code; no need to itemize deductions; amount is based on a taxpayer's filing status, age, etc; no receipts needed

• Itemized Deduction- Specific amounts spent on certain goods and services throughout the year; allowed deductions are outlined by the IRS and include such expenditures as mortgage interest, state and local taxes, charitable donations

www.investopedia.com/terms/i/itemizeddeduction.asp#ixzz1zxopAxpP www.money-zine.com/Calculators/Mortgage-Calculators/Mortgage-Tax-Deduction-Calculator/ (Mortgage tax deduction calculator)

13

Background: Itemizing Required for Charitable Gift Benefits

• You can give thousands of dollars, but if you claim the standard deduction on your tax return, charitable gifts will do you no tax good.

• You must itemize expenses on Schedule A to deduct charitable donations.

• Donors' deductions are limited to 50% of adjusted gross income; rollover of excess for up to 5 years

http://www.bankrate.com/finance/taxes/get-a-tax-deduction-for-charitable-giving-1.aspx

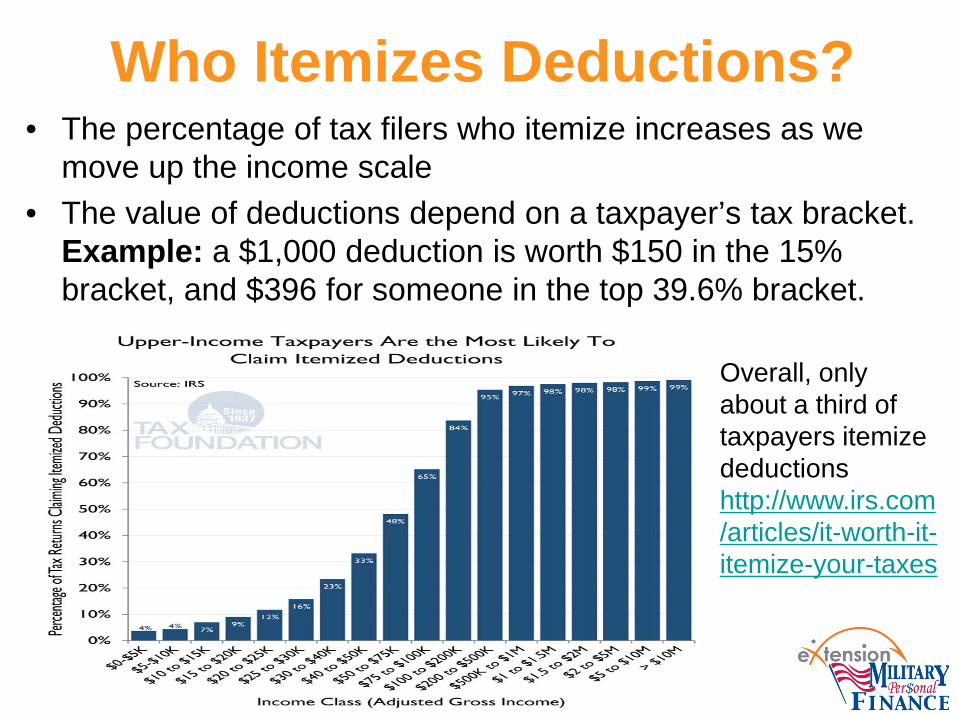

Who Itemizes Deductions? • The percentage of tax filers who itemize increases as we

move up the income scale • The value of deductions depend on a taxpayer’s tax bracket.

Example: a $1,000 deduction is worth $150 in the 15% bracket, and $396 for someone in the top 39.6% bracket.

Overall, only about a third of taxpayers itemize deductions http://www.irs.com/articles/it-worth-it-itemize-your-taxes

Background: Refundable and Non-Refundable Tax Credits

• Refundable: When tax credits are greater than the amount of tax you owe, the IRS sends you a tax refund for the difference – Example: Earned Income Tax Credit (EITC)

• Non-Refundable: Credit can’t be used to increase your tax refund or to create a tax refund when you wouldn’t have already had one. In other words, your savings cannot exceed the amount of tax you owe. – Example: Child and Dependent Care Expenses Credit

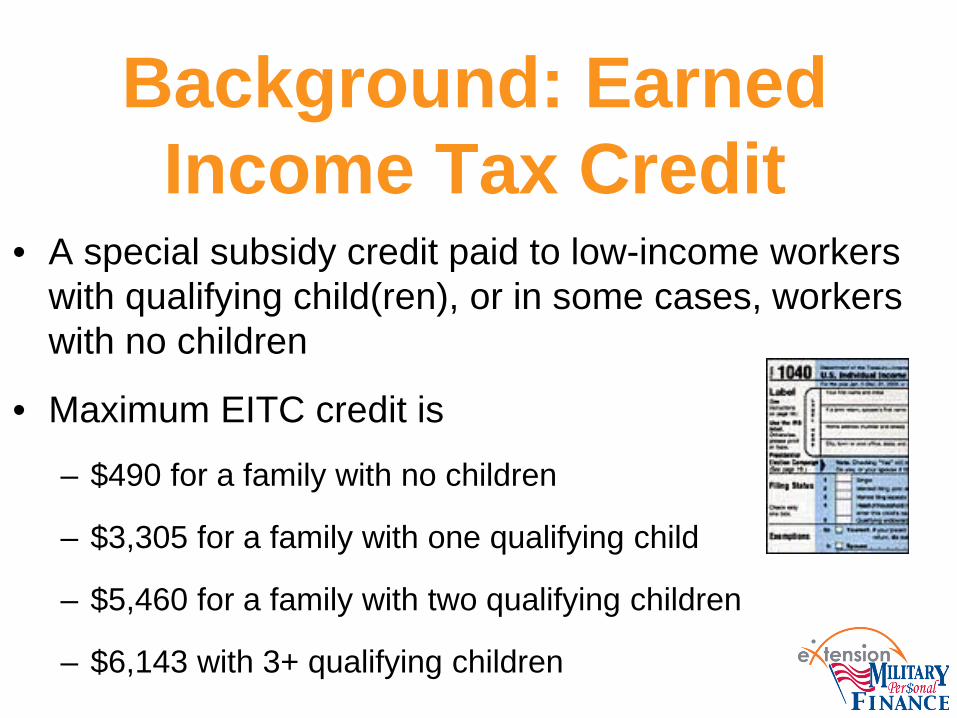

Background: Earned Income Tax Credit

• A special subsidy credit paid to low-income workers with qualifying child(ren), or in some cases, workers with no children

• Maximum EITC credit is

– $490 for a family with no children

– $3,305 for a family with one qualifying child

– $5,460 for a family with two qualifying children

– $6,143 with 3+ qualifying children

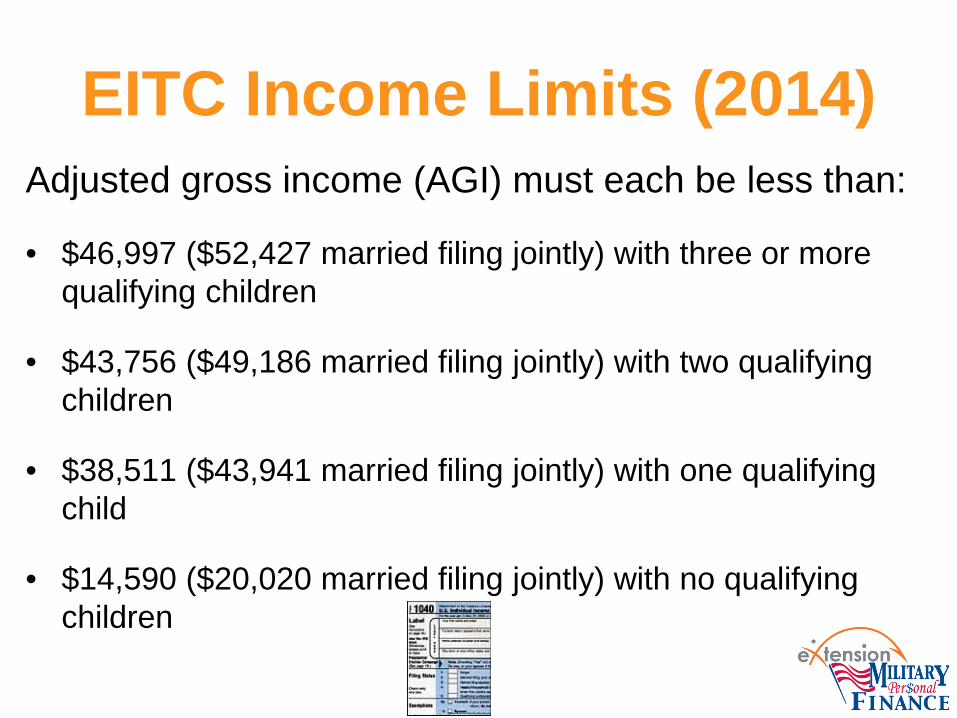

EITC Income Limits (2014) Adjusted gross income (AGI) must each be less than:

• $46,997 ($52,427 married filing jointly) with three or more qualifying children

• $43,756 ($49,186 married filing jointly) with two qualifying children

• $38,511 ($43,941 married filing jointly) with one qualifying child

• $14,590 ($20,020 married filing jointly) with no qualifying children

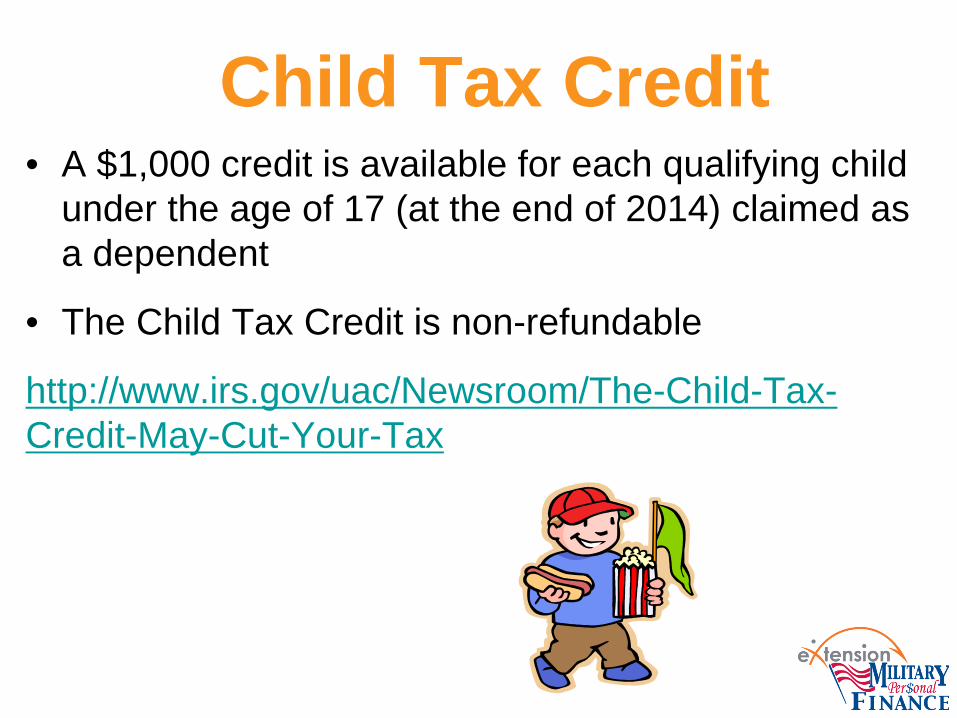

Child Tax Credit • A $1,000 credit is available for each qualifying child

under the age of 17 (at the end of 2014) claimed as a dependent

• The Child Tax Credit is non-refundable

http://www.irs.gov/uac/Newsroom/The-Child-Tax-Credit-May-Cut-Your-Tax

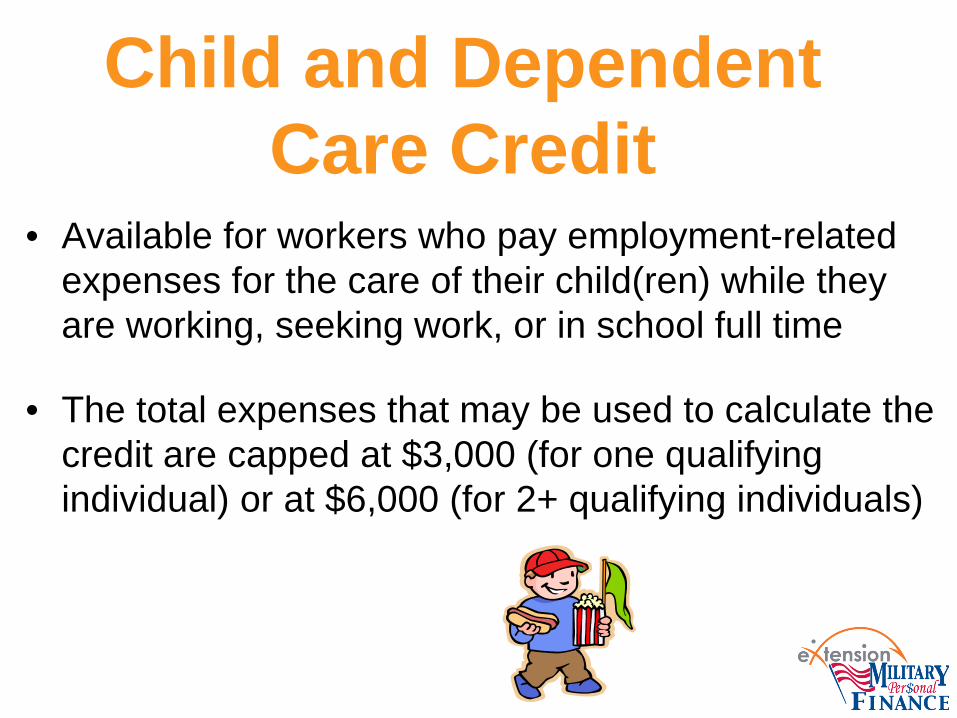

Child and Dependent Care Credit

• Available for workers who pay employment-related expenses for the care of their child(ren) while they are working, seeking work, or in school full time

• The total expenses that may be used to calculate the credit are capped at $3,000 (for one qualifying individual) or at $6,000 (for 2+ qualifying individuals)

Retirement Savings Contribution Credit (Saver’s Tax Credit)

• Singles with adjusted gross incomes of $30,000 or less and joint filers earning $60,000 or less can claim this credit (in 2014)

• Credit is 10%, 20%, or 50% of every dollar contributed to an IRA or employer-sponsored retirement savings plan, up to $2,000, depending on income range

http://www.irs.gov/Retirement-Plans/Plan-Participant,-Employee/Retirement-Topics-Retirement-Savings-Contributions-Credit-(Saver%E2%80%99s-Credit)

Recommended Resource “The Bible”: Annual Limits Relating to Financial Planning (College for Financial Planning): http://www.cffpinfo.com/annual-limits/

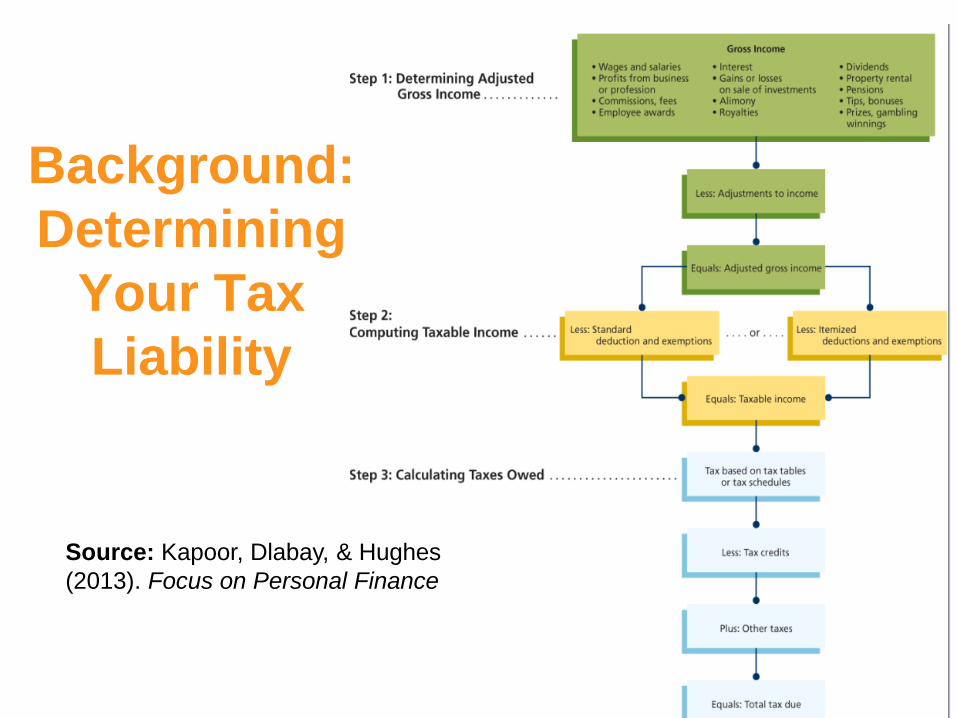

Background: Determining

Your Tax Liability

Source: Kapoor, Dlabay, & Hughes (2013). Focus on Personal Finance

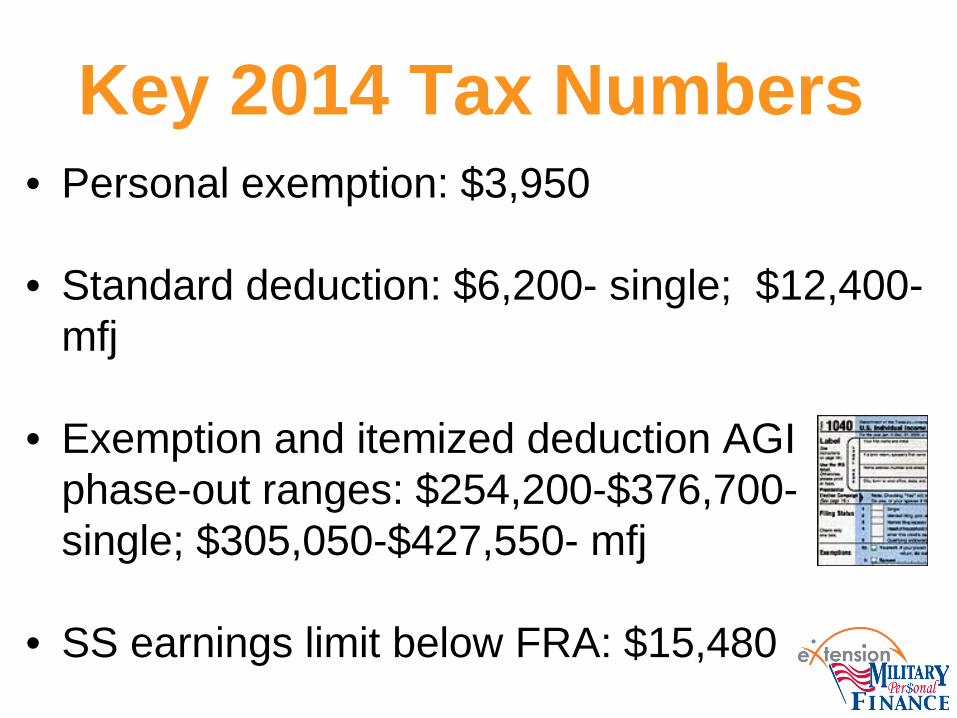

Key 2014 Tax Numbers • Personal exemption: $3,950 • Standard deduction: $6,200- single; $12,400-

mfj • Exemption and itemized deduction AGI

phase-out ranges: $254,200-$376,700- single; $305,050-$427,550- mfj

• SS earnings limit below FRA: $15,480

Background: Completing the Federal Income Tax Return

Filing status and exemptions Income Adjustments to income Tax computation Tax credits Other taxes (such as from self-employment) Payments (total withholding and other payments) Refund or amount you owe

• Refunds can be directly deposited to a bank account • Payments may be directly debited from a bank account

Signature (most common filing error) 3-25

Background: Tax-Rate Schedules and Tax Tables

• Tax-Rate Schedules – Used by persons with a taxable income of $100,000 or more; requires a mathematical computation to determine tax liability

• Tax Tables – Used to look up one’s tax liability according to tax filing status and income range

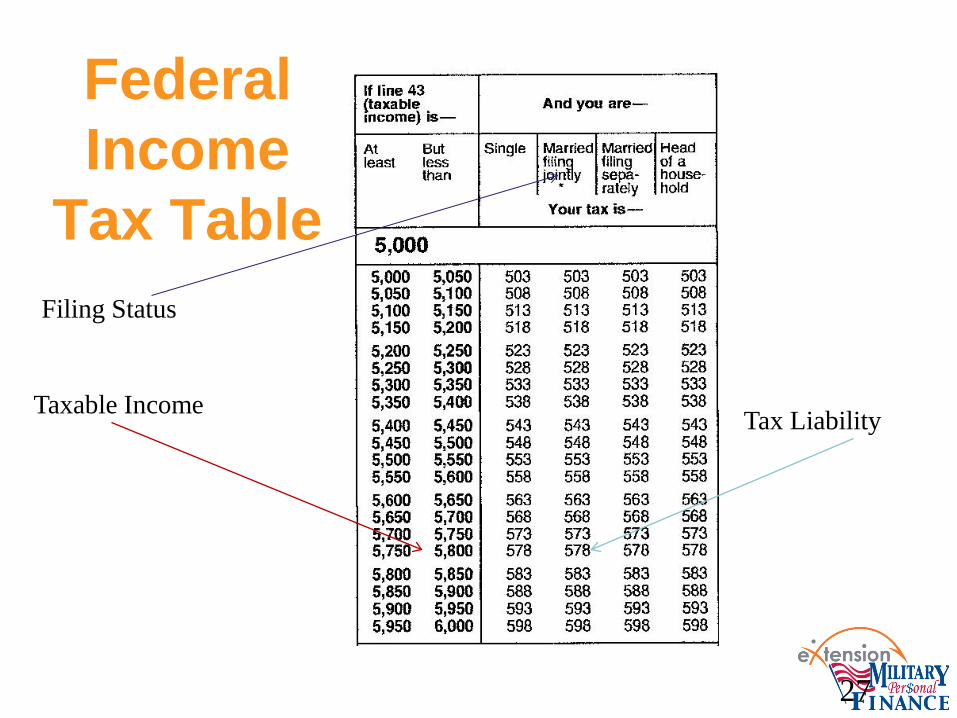

Federal Income

Tax Table Filing Status

Taxable Income Tax Liability

27

Background: Alternative Minimum Tax (AMT)

– Paid by taxpayers with high amounts of certain

deductions and various types of income

– Designed to ensure that those who receive tax breaks also pay their fair share of taxes

– Has increasingly been affecting less affluent taxpayers, especially in high-tax states (e.g., NJ)

– A high proportion of long-term capital gains to ordinary income can trigger the AMT

3-28

Background: Tax Avoidance and Tax Evasion

Tax Avoidance (Minimization) – Legitimate methods to reduce your tax obligation to

your fair share but no more (e.g., deductions, credits, tax-deferred/tax-free investing)

– Decisions related to purchasing, investing, and retirement planning are heavily affected by tax laws (e.g., home, IRAs)

– Keep good tax records (W-2s, 1099s, receipts, copies)

Tax Evasion – Illegally not paying taxes you owe, such as not

reporting all income or overstating deductions

3-29

Question #2 Who are some high profile tax evaders in U.S. history?

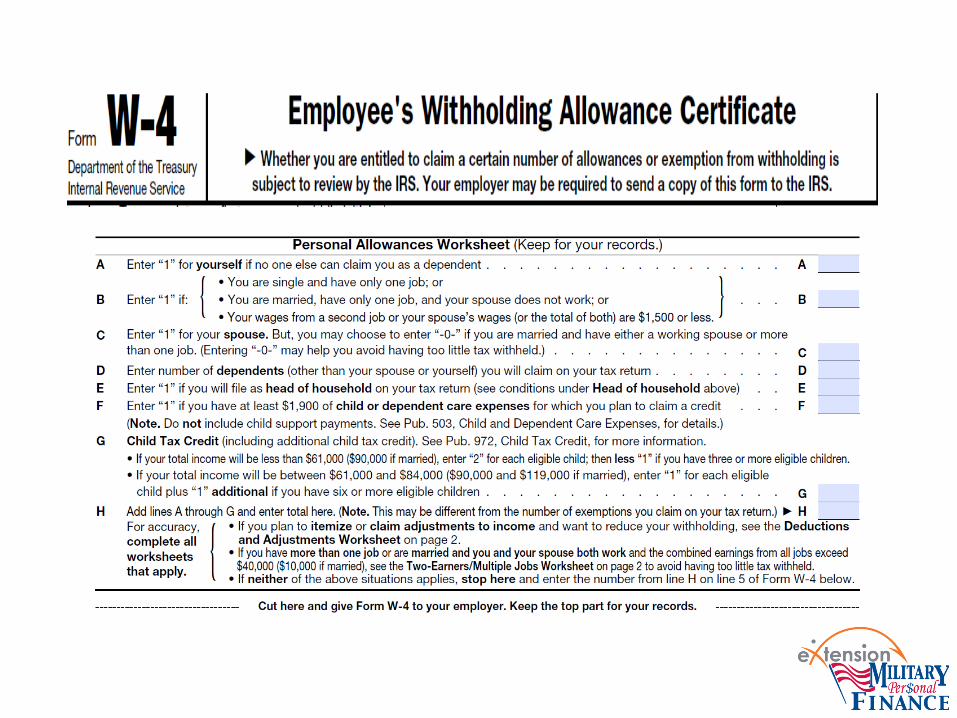

Background: Form W-4 Determines Taxes Withheld

• Typically completed on first day of job

• Employer uses information on W-4 to determine how much tax to withhold

• Recommended practice: review number of withholding allowances each year

• Can add “extra” tax withholding amounts through employer to cover “marriage tax penalty” and/or investment, unemployment, or consulting income

33

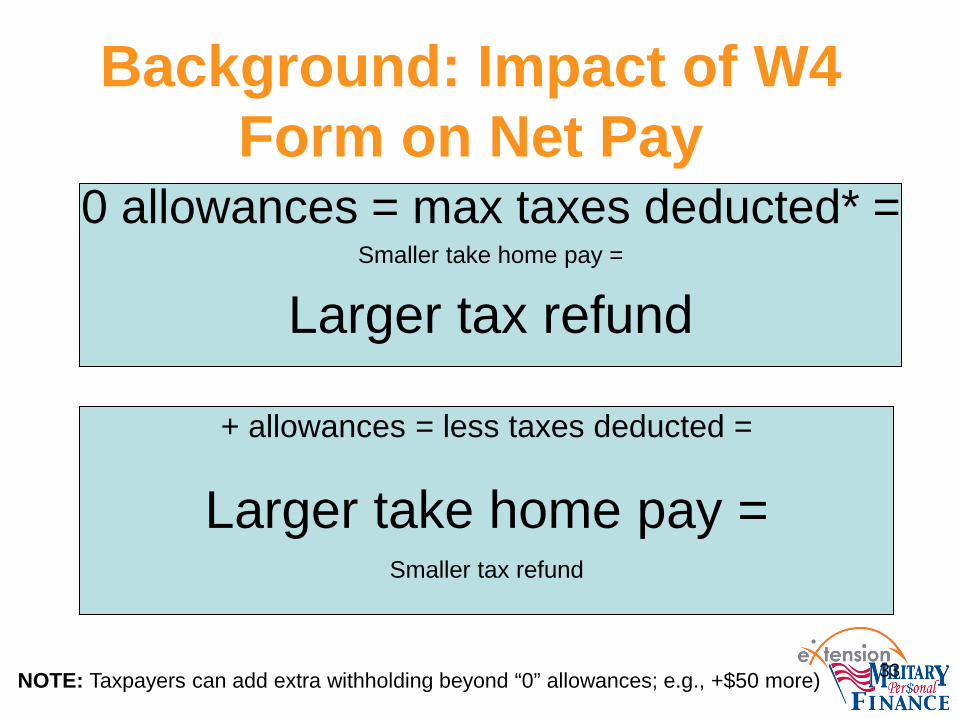

Background: Impact of W4 Form on Net Pay

0 allowances = max taxes deducted* = Smaller take home pay =

Larger tax refund

+ allowances = less taxes deducted =

Larger take home pay = Smaller tax refund

NOTE: Taxpayers can add extra withholding beyond “0” allowances; e.g., +$50 more)

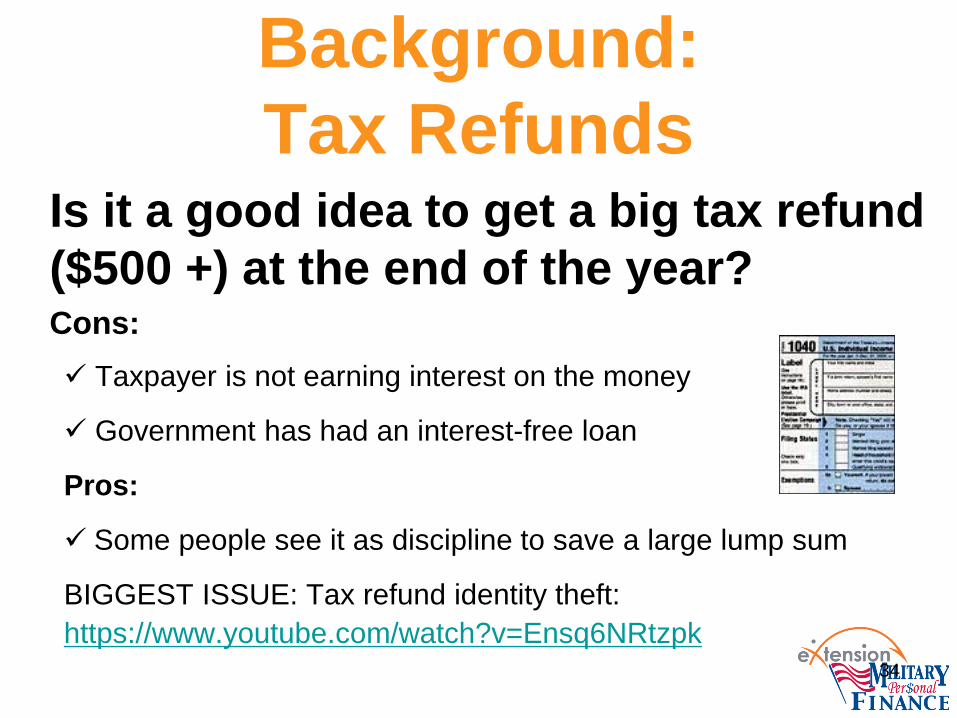

Is it a good idea to get a big tax refund ($500 +) at the end of the year? Cons: Taxpayer is not earning interest on the money

Government has had an interest-free loan

Pros:

Some people see it as discipline to save a large lump sum

BIGGEST ISSUE: Tax refund identity theft: https://www.youtube.com/watch?v=Ensq6NRtzpk

Background: Tax Refunds

34

Question #3 What is your opinion about tax over-withholding?

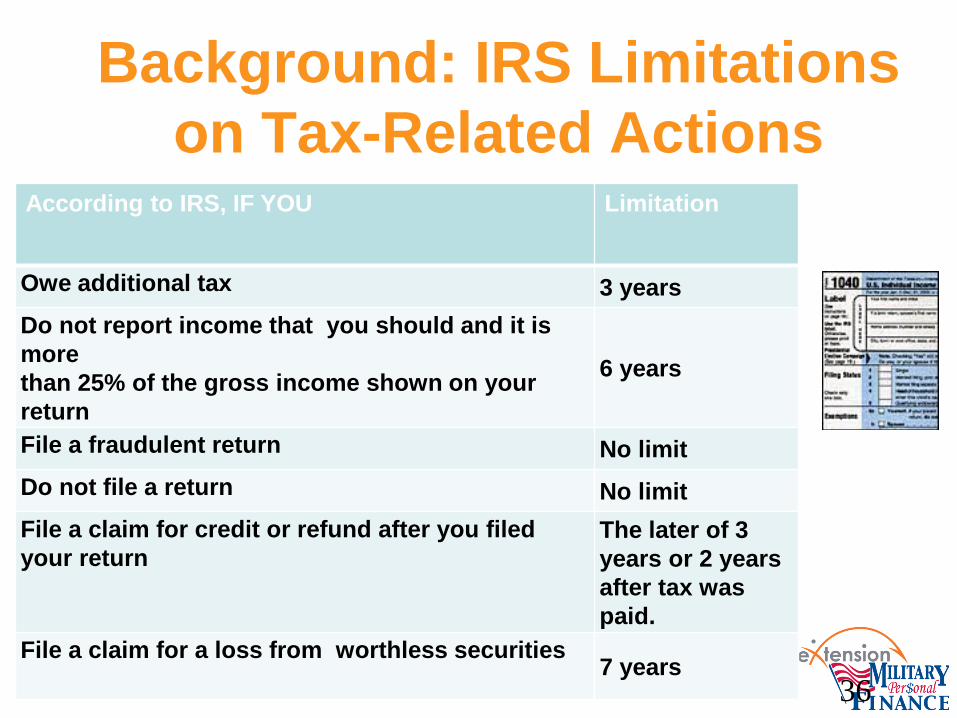

Background: IRS Limitations on Tax-Related Actions

According to IRS, IF YOU Limitation

Owe additional tax 3 years Do not report income that you should and it is more than 25% of the gross income shown on your return

6 years

File a fraudulent return No limit Do not file a return No limit File a claim for credit or refund after you filed your return

The later of 3 years or 2 years after tax was paid.

File a claim for a loss from worthless securities 7 years

36

Background: Record Retention

• How Long to Keep Financial Records (Bankrate) – http://www.bankrate.com/finance/personal-

finance/how-long-to-keep-financial-records.aspx

• Keep investment records to document capital gains and the tax basis of the investments (length of investment ownership + at least 6 years)

37

Strategy: Keep Tax Records a Long Time

• Never discard records relating to – Home purchases

– Contributions to retirement accounts

– Retirement account rollovers and conversions

• When in doubt about keeping a tax record, do NOT throw it out!

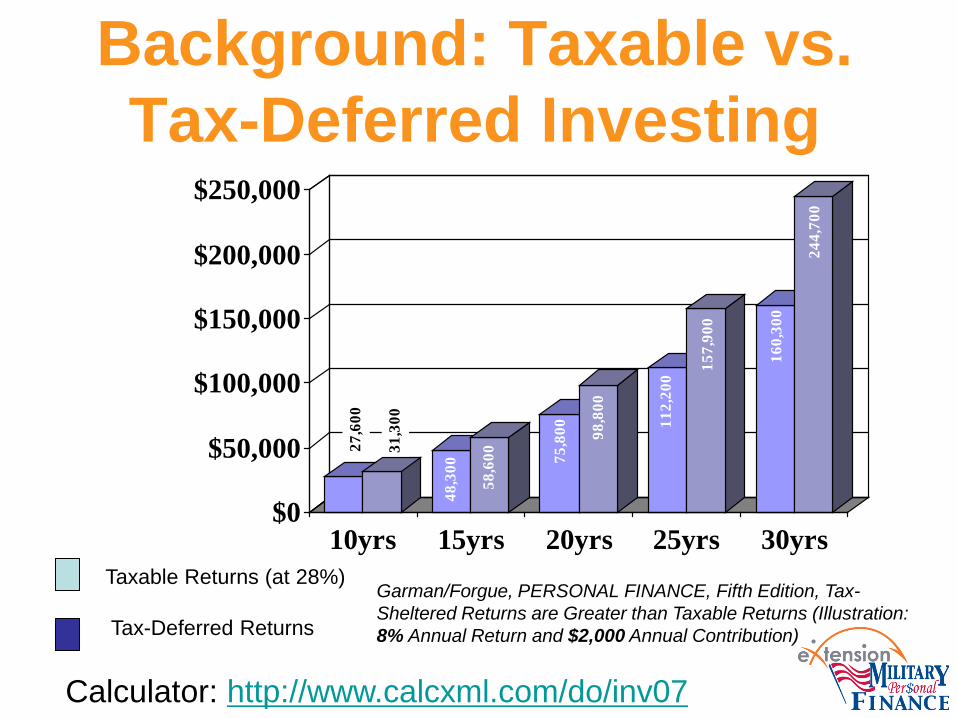

Background: Taxable vs. Tax-Deferred Investing

27,6

00

31,3

00

48,3

00

58,6

00 75,8

00 98,8

00

112,

200

157,

900

160,

300

244,

700

$0

$50,000

$100,000

$150,000

$200,000

$250,000

10yrs 15yrs 20yrs 25yrs 30yrsTaxable Returns (at 28%) Tax-Deferred Returns

Garman/Forgue, PERSONAL FINANCE, Fifth Edition, Tax-Sheltered Returns are Greater than Taxable Returns (Illustration: 8% Annual Return and $2,000 Annual Contribution)

Calculator: http://www.calcxml.com/do/inv07

Background: Common Tax Errors

• Claiming wrong number of dependents • Failing to itemize deductions • Forgetting charitable gifts made via payroll deduction

and texting • Overlooking medical expenses • “Double-dipping’ on education benefits • Reporting an erroneous investment cost basis • Not including previous year’s state tax refund • Not signing the tax return (if paper filed)

Question #4 What other income tax errors have you or your clients made?

Background: Tax Deduction Timing

• Donations and payments for deductible expenses must be made by the end of the tax year for which you want to claim a deduction

• If you put a check dated Dec. 31 in the mail by that day, you are OK

• Donations and payments charged by year's end to a credit card are also OK, even if you don't pay the card's bill until the next year

http://www.bankrate.com/finance/taxes/get-a-tax-deduction-for-charitable-giving-1.aspx

Year-End Tax Planning “Year-end tax planning is essentially a matter of projecting your GROSS income for the year and looking for ways to minimize your TAXABLE income.” Source: 2014 Year-End Tax Planning Guide (Newkirk Publications): http://www.newkirk.com/pdf_forms/low_review.pdf

Taxpayers Still Have Time! • BAD News: People SHOULD have started

2014 tax planning on 1/1/14

• GOOD News: It is NOT too late to take some effective tax savings measures for 2014 – Some actions need to be taken by 12/31 (e.g.,

charitable gifts)

– Some actions need to be taken by 4/15/15 (e.g., IRA contribution for 2014)

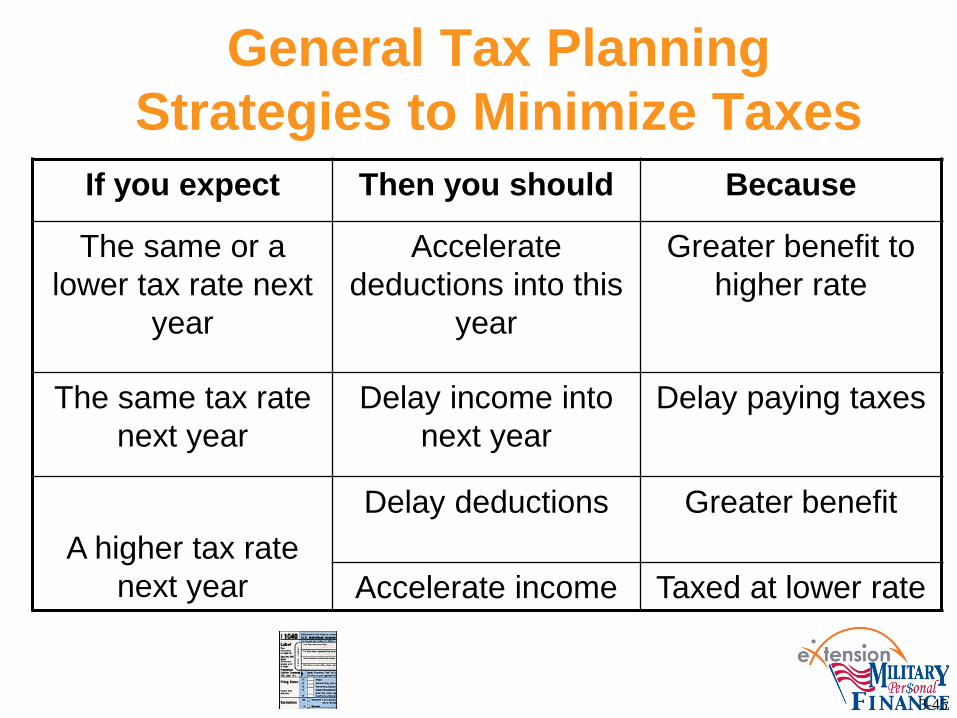

General Tax Planning Strategies to Minimize Taxes

If you expect Then you should Because

The same or a lower tax rate next

year

Accelerate deductions into this

year

Greater benefit to higher rate

The same tax rate next year

Delay income into next year

Delay paying taxes

A higher tax rate

next year

Delay deductions Greater benefit

Accelerate income Taxed at lower rate

3-45

10 Year-End Tax Planning

Strategies

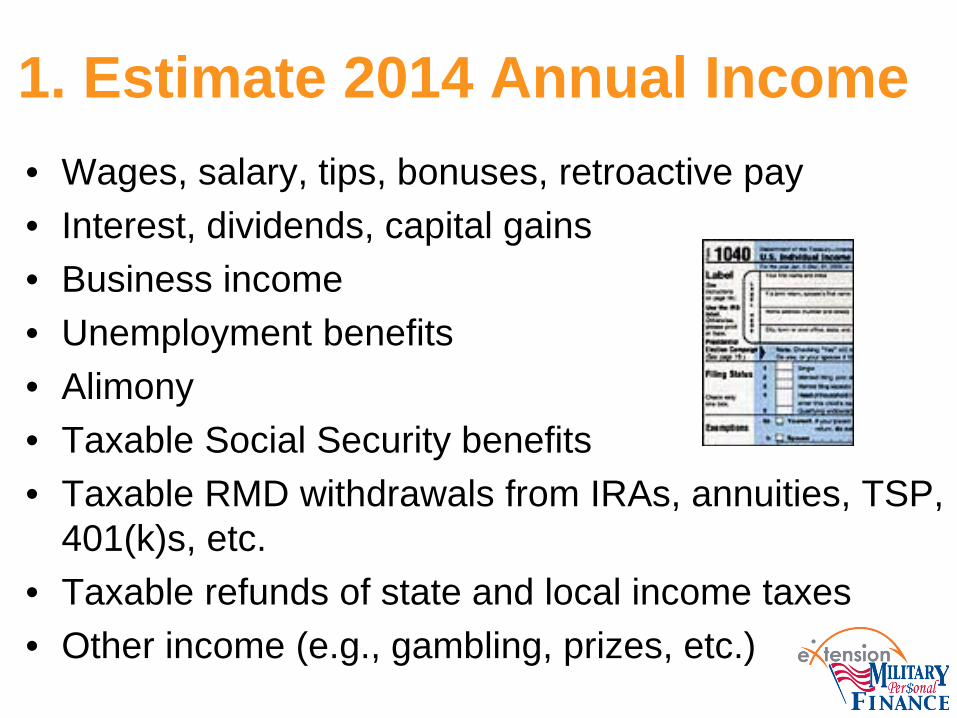

1. Estimate 2014 Annual Income • Wages, salary, tips, bonuses, retroactive pay • Interest, dividends, capital gains • Business income • Unemployment benefits • Alimony • Taxable Social Security benefits • Taxable RMD withdrawals from IRAs, annuities, TSP,

401(k)s, etc. • Taxable refunds of state and local income taxes • Other income (e.g., gambling, prizes, etc.)

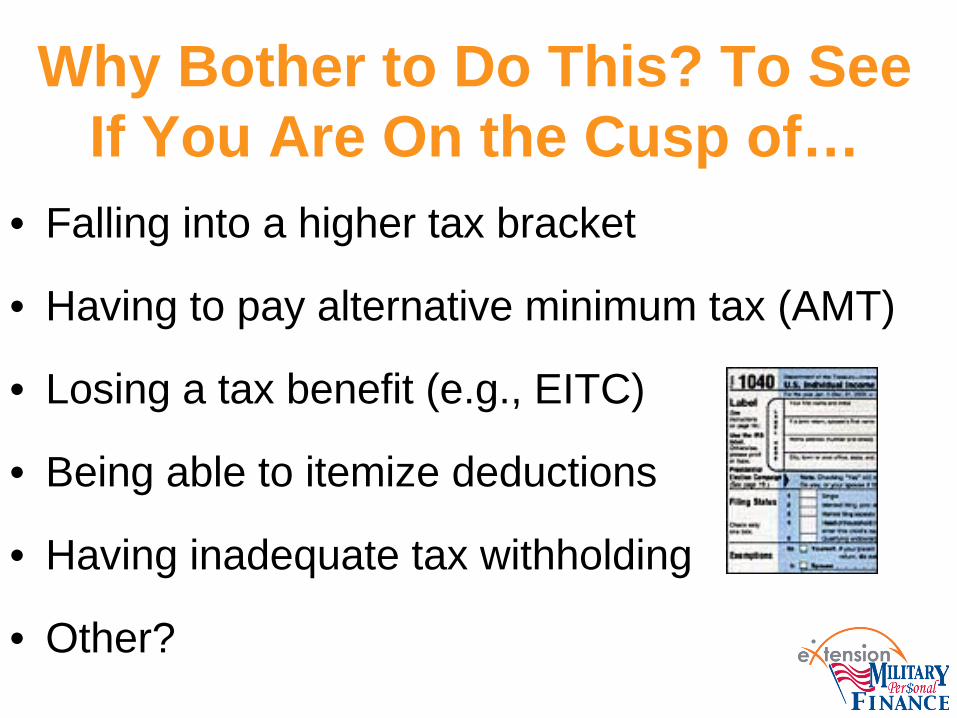

Why Bother to Do This? To See If You Are On the Cusp of…

• Falling into a higher tax bracket

• Having to pay alternative minimum tax (AMT)

• Losing a tax benefit (e.g., EITC)

• Being able to itemize deductions

• Having inadequate tax withholding

• Other?

2. Review Lifestyle Changes That Affect Income Taxes

• Marriage/remarriage • Divorce • Widowhood • Getting or losing a job or freelance work • Birth, adoption, or emancipation of a child • Retirement and receipt of Social Security • Getting or paying off a home mortgage • Other?

3. Review Tax Withholding So Far • You can pay taxes through payroll withholding or by

making estimated tax payments

• If you did not pay enough tax throughout the year, either through withholding or estimated tax payments, you may have to pay a underpayment penalty

• Most taxpayers can avoid this penalty if they owe less than $1,000 in tax (after subtracting withholdings and credits) or if they paid at least 90% of the tax for the current year, or 100% of the tax shown on the return for the prior year, whichever is smaller

http://www.irs.gov/taxtopics/tc306.html

IRS Tax Withholding Calculator

http://apps.irs.gov/app/withholdingcalculator/ Asks questions about filing status, number of jobs, tax credit eligibility, age (if someone is over 65), income (wage and non-wage), tax withholding to date and in one paycheck, anticipated deductions

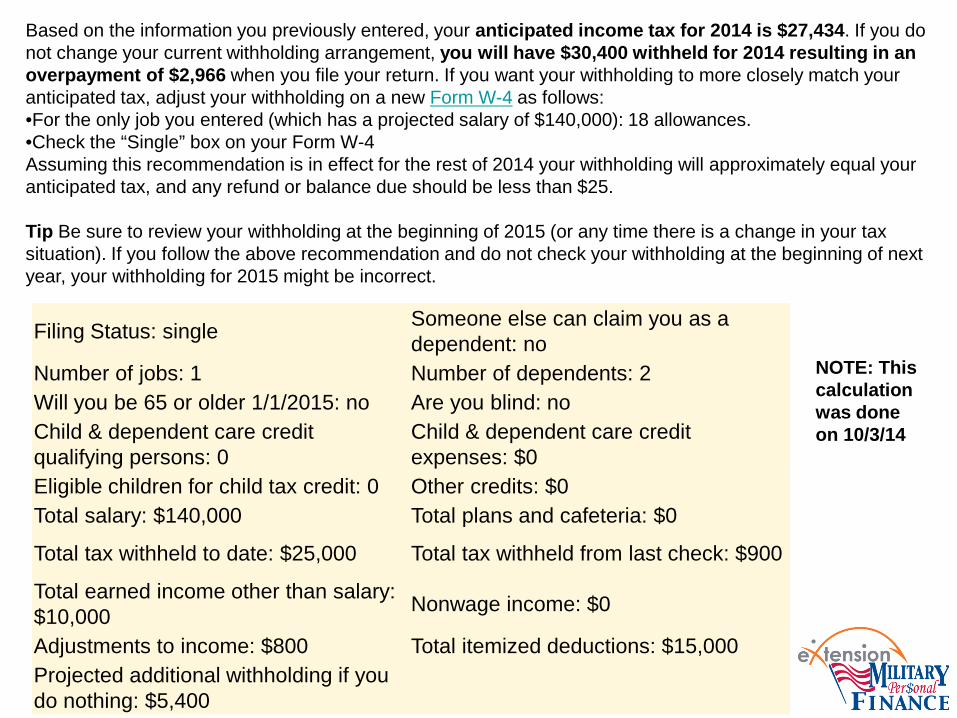

Filing Status: single Someone else can claim you as a dependent: no

Number of jobs: 1 Number of dependents: 2 Will you be 65 or older 1/1/2015: no Are you blind: no Child & dependent care credit qualifying persons: 0

Child & dependent care credit expenses: $0

Eligible children for child tax credit: 0 Other credits: $0 Total salary: $140,000 Total plans and cafeteria: $0

Total tax withheld to date: $25,000 Total tax withheld from last check: $900

Total earned income other than salary: $10,000 Nonwage income: $0

Adjustments to income: $800 Total itemized deductions: $15,000 Projected additional withholding if you do nothing: $5,400

Based on the information you previously entered, your anticipated income tax for 2014 is $27,434. If you do not change your current withholding arrangement, you will have $30,400 withheld for 2014 resulting in an overpayment of $2,966 when you file your return. If you want your withholding to more closely match your anticipated tax, adjust your withholding on a new Form W-4 as follows: •For the only job you entered (which has a projected salary of $140,000): 18 allowances. •Check the “Single” box on your Form W-4 Assuming this recommendation is in effect for the rest of 2014 your withholding will approximately equal your anticipated tax, and any refund or balance due should be less than $25. Tip Be sure to review your withholding at the beginning of 2015 (or any time there is a change in your tax situation). If you follow the above recommendation and do not check your withholding at the beginning of next year, your withholding for 2015 might be incorrect.

NOTE: This calculation was done on 10/3/14

4. Review and Revise W-4 Form With Employer for 2015 Taxes

• Downloadable form: http://www.irs.gov/pub/irs-pdf/fw4.pdf

• Consider changes in income, deductions, filing status, lifestyle, etc.

5. Review and Revise Form With Employer for 2015

Retirement Plan Savings • Authorize a certain percentage of your pay to be

saved up to maximum IRS or employer maximum limit (whichever is smaller)

• Save at least the amount required for a maximum employer match (if available)

• Caution: It is possible for high net worth people to over-save in tax-deferred plans; RMD concerns

Employer Tax-Deferred Retirement Savings Plans

• 457 deferred compensation plans

• 403(b) plans

• 401(k) plans

• Thrift Savings Plan (TSP) – $17,500 maximum contribution (in 2014)

– $5,500 extra catch-up contribution ($23,000 max) for workers age 50+ by year-end

Benefits of Tax-Deferred Employer Retirement Plans

• Earnings on investment grow tax-deferred until withdrawal

• Savings deducted directly from paycheck

• Wide investment selection (generally)

• Contribution made with before-tax dollars

– Example: $50,000 salary, $5,000 TSP or 403(b) plan contribution, $45,000 taxable income (federal income tax)

• Employer matching for many 401(k) plans and some 403(b) plans (e.g., private colleges)

Tips For Funding a Tax-Deferred Employer Retirement Plan

• Invest as much as you possibly can

• “Kick it [contribution] up a notch” when pay increases or household expenses (e.g., child care, car loan) end or decrease

• Diversify across asset classes

• Avoid market timing

• Choose low-expense investments with good historical performance

6. “Bunch” Itemized Deductions • When people find they don’t have enough deductions

to exceed the standard deduction, but they are close • Shift payment dates of some deductible items from

one year to another to increase itemized deductions – Items that can be “bunched” include

• Medical expenses

• Real estate taxes

• State and local income taxes

• Personal property taxes

• Home mortgage interest

• Charitable contributions (cash and property donations)

• Employee business expenses exceeding 2% of AGI

Employee Business Expenses • Can only deduct unreimbursed costs

• Must be able to itemize deductions

• Subject to 2% of AGI “floor”

• Need to file IRS Form 2106

• Must be able to prove expenses

– Mileage log/calendar/expense forms

– Receipts

Business Tax Deductions: Local Travel

• Standard mileage rate: 56 cents per mile (minus employer reimbursement)

• Alternative: deduct actual car expenses

– gas, insurance, oil, license, registration, parking, garage rent, tolls, repairs, tires, lease payments, depreciation, etc.

• Travel between 2 workplaces: deductible

• From home to (any) job: never deductible

Business Tax Deductions: Distant Travel

• Can deduct job travel away from home

• Must be away from tax home for > ordinary work day and need sleep/rest

• Only 50% of unreimbursed meal costs are deductible

• Can deduct laundry/cleaning bills and baggage tips

Business Tax Deductions On Schedule A, you can deduct:

– Union dues

– Professional association dues

– Fees for professional licenses (e.g., AFC)

– Research expenses (as part of job duties)

– Job search expenses in present occupation

– Subscriptions to professional journals and trade magazines

Alternative to Non-Deductible

Business Expenses Consider self-employment/consulting/freelance work options to fully write off business expenses otherwise subject to the 2% of AGI limit

– Same field as “day job” specialty area

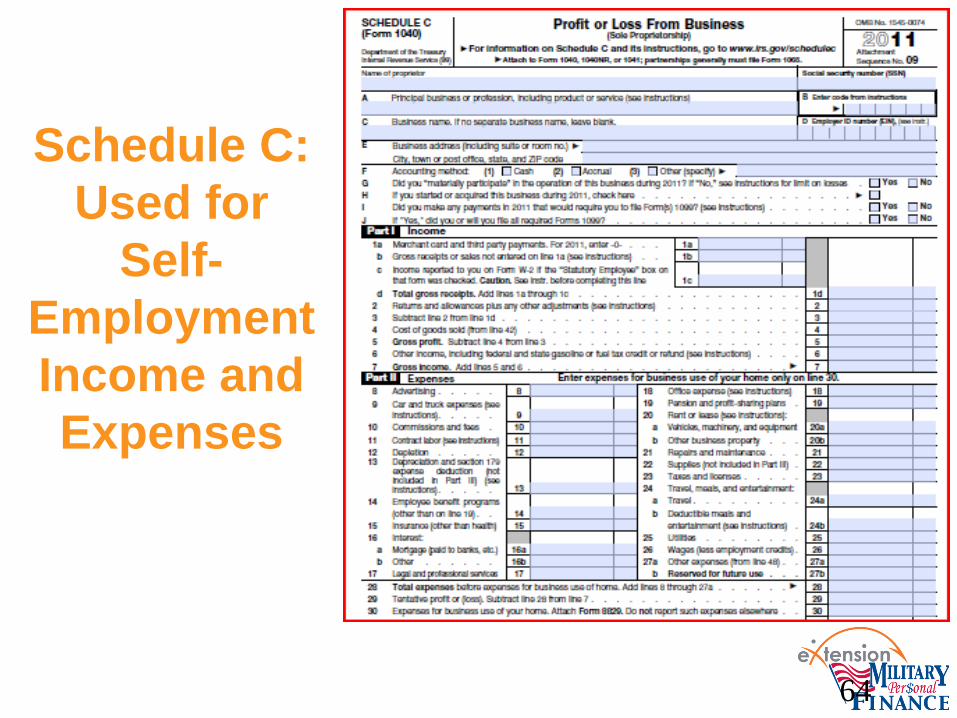

Schedule C: Used for

Self-Employment Income and Expenses

64

7. Check Your Investments

• Do you have capital gains for this tax year?

• Do you have any unrealized losses in other assets to sell before year-end to offset gains?

• If not, do you need to send estimated taxes for the gain (if extra withholding is not done through a job)?

– Fourth quarter estimated taxes are due by 1/15/15

• Declaring capital losses, while emotionally difficult, can help offset capital gains and reduce tax liability

8. Make Flexible Spending Account Decisions

• FSA: allows workers to put away tax-free money for qualified medical expenses

• Plan to spend down account by 12/31

• Can carry over up to $500 to next year (IRS rule) or employer may allow rollover of all unused funds (but is not required to do so)

• Consider 2015 changes in FSA contribution

• Resource: http://www.irs.gov/pub/irs-pdf/p969.pdf

9. Consider Charitable Donations • Donations can be as late as a check mailed or a credit card

charged on 12/31/14

• Gift must be to a qualified 501(c)(3) organization

• Donation of stock or non-cash property at fair market value

• If gift of $250+, must get letter from the qualified organization noting the amount of cash or a description of property contributed, and whether the organization provided any goods or services in exchange for the gift

• No income tax deduction for gifts to relatives but you can gift up to $14,000 without gift tax

10. Maximize “Above the Line” Deductions to Reduce AGI

• Traditional IRA contributions (if qualified by income) – Have until tax filing date next year to contribute

• Health savings account contributions • Moving expenses • Alimony payments • Retirement plan savings for self-employed persons • Health insurance for self-employed persons • Health insurance • Interest on student loans

Other Tax Tips • Check AMT status BEFORE you take a capital gain

or other large income source

– AMT Assistant: http://www.irs.gov/Businesses/Small-Businesses-&-Self-Employed/Alternative-Minimum-Tax-(AMT)-Assistant-for-Individuals

• Accelerate or defer AMT vulnerable items

– State income taxes and local property taxes

– In high tax states, losing these deductions hurts!!

• Comply with required minimum distribution rules for qualified retirement plans (if age 70 ½ +)

Question #5

Any other year-end income tax tips?

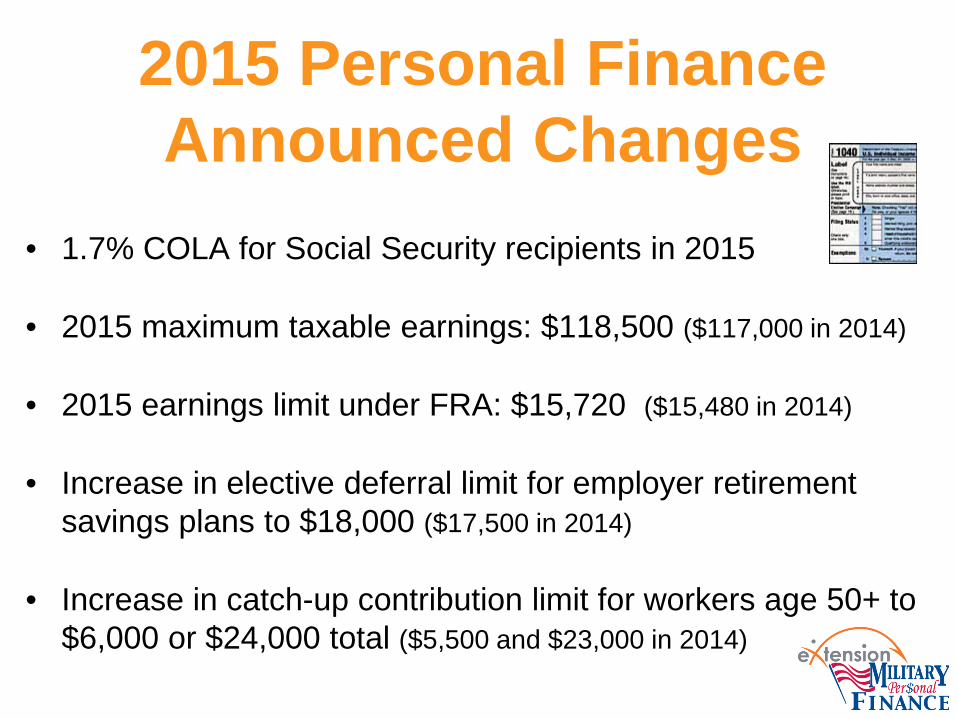

2015 Personal Finance Announced Changes

• 1.7% COLA for Social Security recipients in 2015

• 2015 maximum taxable earnings: $118,500 ($117,000 in 2014)

• 2015 earnings limit under FRA: $15,720 ($15,480 in 2014)

• Increase in elective deferral limit for employer retirement savings plans to $18,000 ($17,500 in 2014)

• Increase in catch-up contribution limit for workers age 50+ to $6,000 or $24,000 total ($5,500 and $23,000 in 2014)

Military-Specific Tax Information

• Free tax preparation software from Military OneSource

• Free tax centers at military installations in the U.S. and abroad (have quality review process; layers of support) – Fewer limitations on services provided than VITA tax sites

– Includes legal assistance and amended tax return assistance

• Continued use of TSP; increase pay % contribution in 2015?

• Liberal home sale rules: can suspend the “2 out of 5 year” test period for up to 10 years: http://www.figuide.com/military-tax-benefit-sale-of-primary-residence.html

• Reduced taxable income if deployed to a combat zone

Recommended Resources IRS Publication 17 (Your Federal Income Tax): http://www.irs.gov/pub/irs-pdf/p17.pdf 2014 Year-End Tax Planning Guide (Newkirk): http://www.newkirk.com/pdf_forms/low_review.pdf AAII Personal Tax Planning Guide (published annually): http://www.aaii.com/journal/article/the-individual-investors-guide-to-personal-tax-planning-2013

Minimize Income Taxes Through Proper Planning

Famous Quote by Judge Learned Hand (United States judge and judicial philosopher, 1872-1961):

"Anyone may arrange his affairs so that his taxes shall be as low as possible; he is not bound to choose that pattern which best pays the treasury. There is not even a patriotic duty to increase one's taxes. Over and over again the Courts have said that there is nothing sinister in so arranging affairs as to keep taxes as low as possible. Everyone does it, rich and poor alike and all do right, for nobody owes any public duty to pay more than the law demands."

Key Take-Aways • ACA law health insurance tax subsidies will

complicate 2014 income taxes

• Tax refund identity theft is increasing significantly

• Tax credits are refundable or non-refundable

• The Savers Credit helps low/moderate income families save for retirement

• Tax-deferred investments postpone income taxes

• Tax planning can legally lower income taxes

Key Take-Away Applications • Refer people to local Navigators and VITA sites for assistance

with ACA-related tax questions

• Encourage people to file taxes early and avoid a large tax refund that can be held up by thieves

• Encourage people to take advantage of tax credits that they qualify for

• Teach the benefits of the Retirement Savers Credit and how to “find” money to save

• Teach the benefits of tax-deferred plans; fund them personally

• Teach and follow the 10 tax planning strategies

Questions? Comments? Experiences?