Embed Size (px)

Citation preview

Zambia: The Case For

Eurobond 3

1

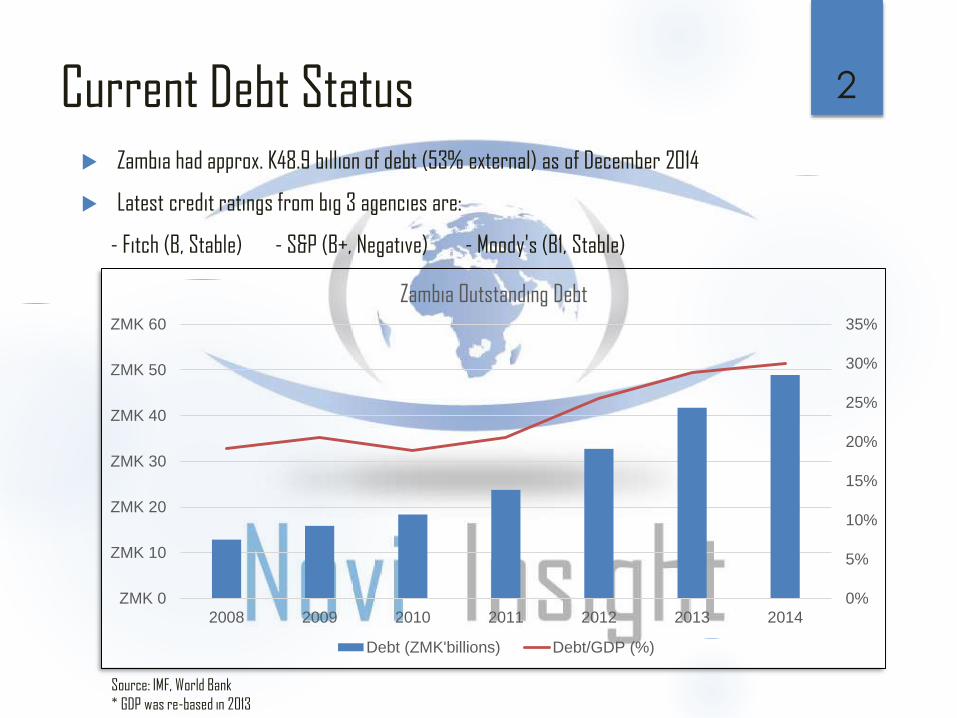

Current Debt Status Zambia had approx. K48.9 billion of debt (53% external) as of December 2014

Latest credit ratings from big 3 agencies are:

- Fitch (B, Stable) - S&P (B+, Negative) - Moody's (B1, Stable)

Source: IMF, World Bank

* GDP was re-based in 2013

2

0%

5%

10%

15%

20%

25%

30%

35%

ZMK 0

ZMK 10

ZMK 20

ZMK 30

ZMK 40

ZMK 50

ZMK 60

2008 2009 2010 2011 2012 2013 2014

Zambia Outstanding Debt

Debt (ZMK'billions) Debt/GDP (%)

…..cont’d

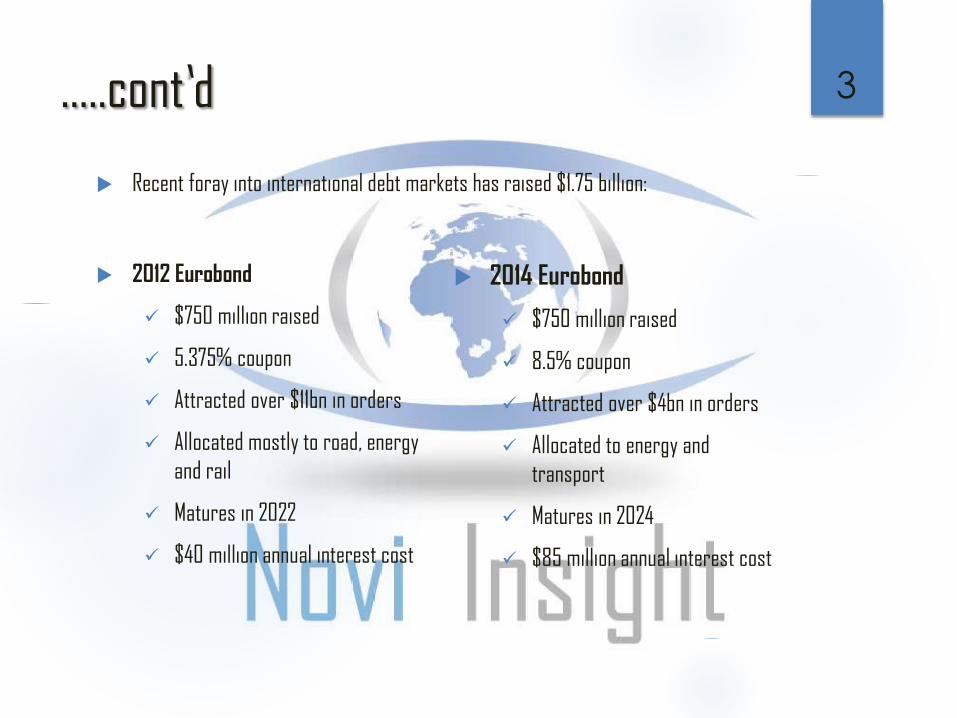

2012 Eurobond

$750 million raised

5.375% coupon

Attracted over $11bn in orders

Allocated mostly to road, energy

and rail

Matures in 2022

$40 million annual interest cost

2014 Eurobond

$750 million raised

8.5% coupon

Attracted over $4bn in orders

Allocated to energy and

transport

Matures in 2024

$85 million annual interest cost

Recent foray into international debt markets has raised $1.75 billion:

3

…..cont’d

However, this is a drop in the bucket compared to the investment that is required to

grow key sectors of the economy.

Some key sectors have not been adequately included in the investment plan

Especially in light of the fact that 50% of the population is below the age of 15 and

employment growth is not increasing at fast enough rate

4

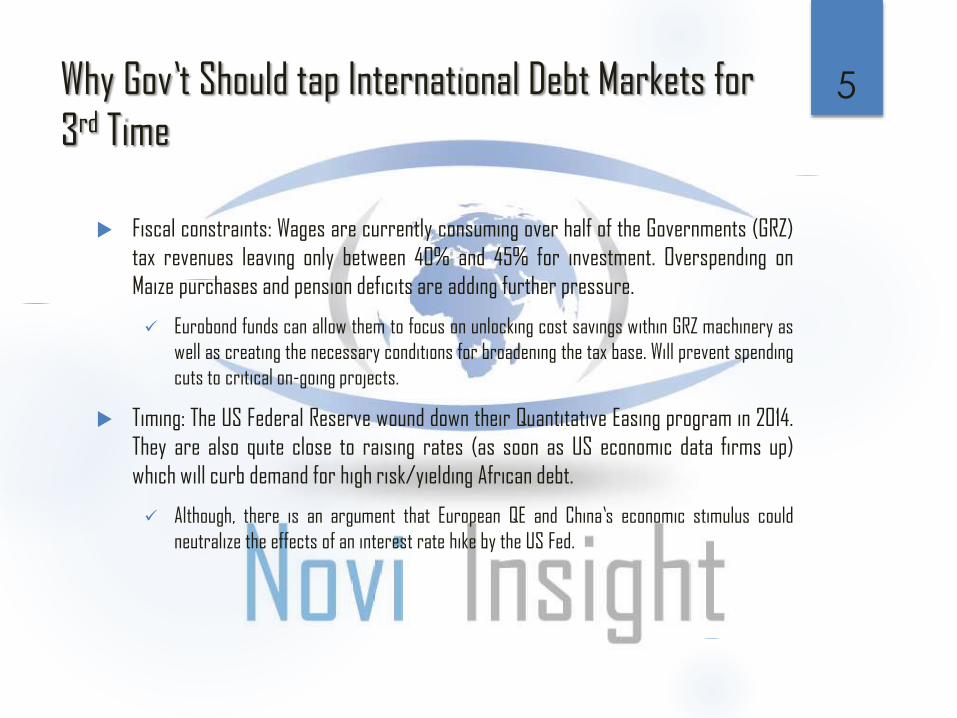

Why Gov’t Should tap International Debt Markets for

3rd Time

Fiscal constraints: Wages are currently consuming over half of the Governments (GRZ)

tax revenues leaving only between 40% and 45% for investment. Overspending on

Maize purchases and pension deficits are adding further pressure.

Eurobond funds can allow them to focus on unlocking cost savings within GRZ machinery as

well as creating the necessary conditions for broadening the tax base. Will prevent spending

cuts to critical on-going projects.

Timing: The US Federal Reserve wound down their Quantitative Easing program in 2014.

They are also quite close to raising rates (as soon as US economic data firms up)

which will curb demand for high risk/yielding African debt.

Although, there is an argument that European QE and China’s economic stimulus could

neutralize the effects of an interest rate hike by the US Fed.

5

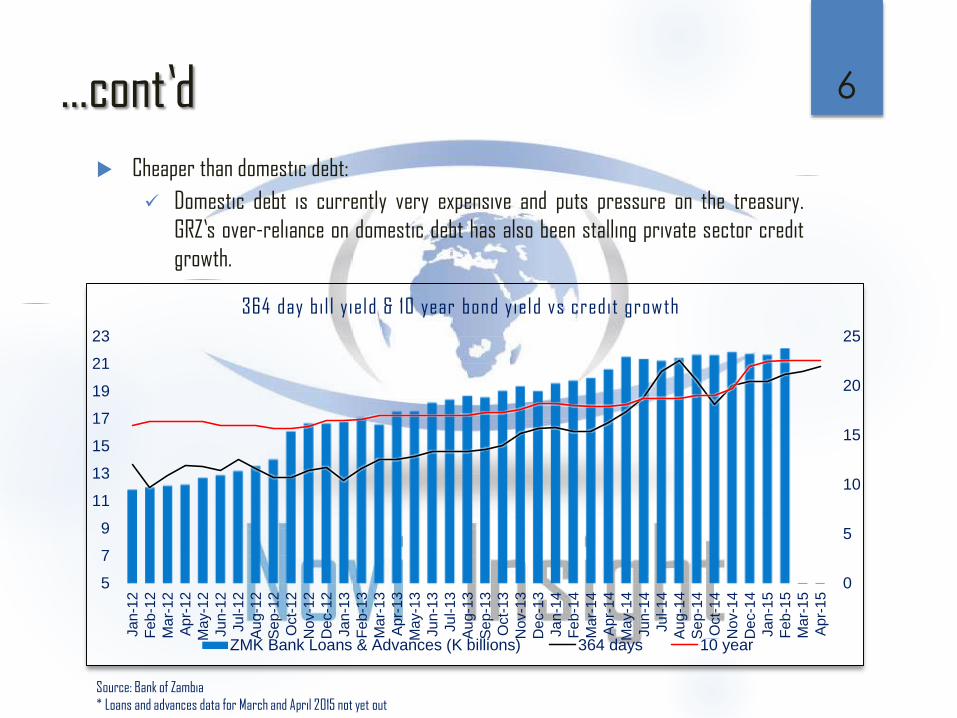

…cont’d

Cheaper than domestic debt:

Domestic debt is currently very expensive and puts pressure on the treasury.

GRZ’s over-reliance on domestic debt has also been stalling private sector credit

growth.

6

0

5

10

15

20

25

5

7

9

11

13

15

17

19

21

23

Ja

n-1

2

Feb

-12

Ma

r-1

2

Ap

r-1

2

Ma

y-1

2

Ju

n-1

2

Ju

l-1

2

Aug-1

2

Se

p-1

2

Oct-

12

No

v-1

2

De

c-1

2

Ja

n-1

3

Feb

-13

Mar-

13

Ap

r-1

3

Ma

y-1

3

Ju

n-1

3

Ju

l-1

3

Au

g-1

3

Se

p-1

3

Oct-

13

No

v-1

3

De

c-1

3

Ja

n-1

4

Feb

-14

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Ju

n-1

4

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oct-

14

No

v-1

4

De

c-1

4

Ja

n-1

5

Feb

-15

Mar-

15

Ap

r-1

5

364 day bi l l yield & 10 year bond yield vs credit growth

ZMK Bank Loans & Advances (K billions) 364 days 10 year

Source: Bank of Zambia

* Loans and advances data for March and April 2015 not yet out

Stipulations

GRZ needs to put it’s house in order in 2015:

Optimally price fuel and remove current ‘subsidy’

Keep Maize purchases within budget (research from 2011 has shown that it is not a

significant factor in winning elections!)

Complement changes to retirement age by implementing further pension reforms

Make necessary changes at state-owned entities to unlock savings and efficiency

then dispose of some to raise much needed cash

Further reforms in terms of regulation and processes in order to make business

ambiance more efficient and easier

Implement more robust measures to capture more tax revenue from rental income

(tenants will not do this on your behalf!)

2015 needs to be about cost cutting, efficiency and raising cash. If impetus

to do this is not there then then the bond should not be issued.

7

How Much Should be Raised?

Should look to raise at least $1.5 billion in Quarter 1 of 2016

Implications:

Total debt will increase by $1.5 billion to just below $10 billion, ceteris paribus(below 40% of GDP)

Debt service costs will increase depending on coupon

Sequential Eurobond maturities with $750m repaid in 2022, $1bn repaid in 2024

and $1.5bn repaid in 2026 will put pressure on budgets in those years

If Kwacha continues to weaken against the US dollar, interest costs would rise

8

Where it Should be Invested

$500m Allocated to Internet and Communications:

Internet has not received enough focus/investment by GRZ and should be one of thepriority sectors because it has tremendous applications across all sectors.

Sector is also heavily taxed despite the heavy capital expenditure requirements. Ontop of all this, the country’s geographical position (landlocked) keeps it far awayfrom under-sea cables. Consequently, internet costs are quite high.

Zambia needs further investment into ICT infrastructure around the country as wellas tax incentives stimulate further investment by private companies. This wouldsignificantly cut down business costs as well as increase connectivity countrywide.

E.g. It’s commendable to erect mobile towers in rural areas but service providers won’tbe motivated to set up and operate their equipment on them (costly) because they cantmake as much money there as they can in densely populated urban areas like Lusakawhich have wealthier users. Tax incentives required!

9

…cont’d

$500m Allocated to Rail:

$120m from Eurobond 1 was not enough to revamp rail sector. Need further

investment into technology, staff training and other core assets.

Would boost cargo and passenger revenues as well as relieve the pressure on

newly minted road infrastructure.

Would also boost inter-regional trade (cementing ‘hub’ status) and efficiency.

This would also put the sector in a better position to win cargo business from

mining/cement companies who are ramping up production.

Investment in this sector will pay for itself in the long run

10

…cont’d

$300m Allocated to Venture Capital Program:

Current ‘Youth Development Fund’ format very limited and not doing well (millions in

defaulting loans)

Identify (rigorously) 5 high potential locally owned businesses in each priority sector

(manufacturing, agriculture, tourism and construction). Take 15 to 20% stake.

Incubate/support them and help with financing needs. Dispose of stake via IPO after

firms start growing profitably.

Create backlinks with selected universities by identifying top talent which can be put

on educational track armed with the right skills to work in (or at the very least gain

internship experience) at one of the companies in priority sector.

Execution requires transparency and delegation to foreign/domestic private sector

players who understand dynamics of priority sectors domestically as well as on a

global basis.

Would boost youth employment as well as stimulate growth in capital market activity

(more jobs).

11

…cont’d

$200m Allocated to Construction in Rural Areas:

Construct better quality housing/facilities for government workers (health,

education, police) in rural areas so that more quality hires would be willing to

relocate there. Could be powered by solar.

Target areas should have a certain critical mass of people as well as economic

growth prospects.

The idea is to boost service delivery and make rural areas more attractive to work,

live in, invest in etc. so as to increase economic activity and job growth there.

This also complements the Link 8,000 road project.

12

Return on Investment

Rewards will start being reaped in 5 – 10 year horizon:

Cheaper internet and increased connectivity countrywide boosting various sectors

from education to business

Job growth (more importantly for youths) and new sectors forming and

contributing to GDP and wealth creation

Actual diversification and broadening of economic base

Increased population density in rural areas with better infrastructure and service

provision (plus economic growth in those areas)

Exponential growth will lead to increased generation of tax revenues for GRZ to

invest in better service delivery

13

The End.

14