Embed Size (px)

Citation preview

Financial Advisor SeriesFOUNDATIONS OF FINANCIAL PLANNING:

AN OVERVIEWAllen McLellan, Editor

FA262.03.1

This publication is designed to provide accurate and authoritative information about thesubject covered. While every precaution has been taken in the preparation of this material,the authors, and The American College assume no liability for damages resulting from theuse of the information contained in this publication. The American College is not engagedin rendering legal, accounting, or other professional advice. If legal or other expert advice isrequired, the services of an appropriate professional should be sought.

© 2012 The American College PressAll rights reservedISBN-10: 1-58293-105-4ISBN-13:978-1-58293-105-0Library of Congress Control No.: 2012934702270 S. Bryn Mawr AvenueBryn Mawr, PA 19010(888) AMERCOL (263–7265)theamericancollege.eduPrinted in the United States of America

FINANCIAL ADVISOR SERIES

Sales Skills Techniques

Techniques for Exploring Personal Markets

Techniques for Meeting Client Needs

Techniques for Prospecting: Prospect or Perish

Women and Money—Matters of Trust

Product Essentials

Essentials of Annuities

Essentials of Business Insurance

Essentials of Disability Income Insurance

Essentials of Life Insurance Products

Essentials of Long–Term Care Insurance

Essentials of Multiline Insurance Products

Planning Foundations

Foundations of Estate Planning

Foundations of Retirement Planning

Foundations of Financial Planning: An Overview

Foundations of Financial Planning: The Process

Foundations of Investment Planning

iii

THE AMERICAN COLLEGE

The American College® is an independent, nonprofit, accredited institution founded in 1927that offers professional certification and graduate-degree distance education to men andwomen seeking career growth in financial services.

The Center for Financial Advisor Education at The American College offers both the LUTCFand the Financial Services Specialist (FSS) professional designations to introduce studentsin a classroom environment to the technical side of financial services, while at the same timeproviding them with the requisite sales-training skills.

The Solomon S. Huebner School® of The American College administers the Chartered LifeUnderwriter (CLU®); the Chartered Financial Consultant (ChFC®); the Chartered Advisor forSenior Living (CASL®); the Registered Health Underwriter (RHU®); the Registered EmployeeBenefits Consultant (REBC®); the Chartered Healthcare Consultant™ and the CharteredLeadership Fellow® (CLF®) professional designation programs. In addition, the HuebnerSchool also administers The College's CFP Board—registered education program for thoseindividuals interested in pursuing CFP® certification, the CFP® Certification Curriculum.

The Richard D. Irwin Graduate School® of The American College offers the master ofscience in financial services (MSFS) degree, the Graduate Financial Planning Track(another CFP Board-registered education program), and several graduate-level certificatesthat concentrate on specific subject areas. It also offers the Chartered Advisor inPhilanthropy (CAP®) and the master of science in management (MSM), a one-year programwith an emphasis in leadership. The National Association of Estate Planners & Councilshas named The College as the provider of the education required to earn its prestigiousAEP designation.

The American College is accredited by The Middle States Commission on HigherEducation, 3624Market Street, Philadelphia, PA 19104 at telephone number 267.284.5000.

The Middle States Commission on Higher Education is a regional accrediting agencyrecognized by the U.S. Secretary of Education and the Commission on Recognition ofPostsecondary Accreditation. Middle States accreditation is an expression of confidencein an institution's mission and goals, performance, and resources. It attests that in thejudgment of the Commission on Higher Education, based on the results of an internalinstitutional self-study and an evaluation by a team of outside peer observers assignedby the Commission, an institution is guided by well-defined and appropriate goals; that ithas established conditions and procedures under which its goals can be realized; that itis accomplishing them substantially; that it is so organized, staffed, and supported that itcan be expected to continue to do so; and that it meets the standards of the Middle StatesAssociation. The American College has been accredited since 1978.

v

vi Foundations of Financial Planning: An Overview

The American College does not discriminate on the basis of race, religion, sex, handicap, ornational and ethnic origin in its admissions policies, educational programs and activities, oremployment policies.

The American College is located at 270 S. Bryn Mawr Avenue, Bryn Mawr, PA 19010. Thetoll-free number of the Office of Professional Education is (888) AMERCOL (263-7265); thefax number is (610) 526-1465; and the home page address is theamericancollege.edu.

Certified Financial Planner Board of Standards, Inc., owns the certification marks CFP®,CERTIFIED FINANCIAL PLANNER™, and CFP (with flame logo)®, which it awards toindividuals who successfully complete initial and ongoing certification requirements.

CONTENTS

Financial Advisor Series ..............................................................................iiiThe American College................................................................................. vTable of Contents........................................................................................viiAcknowledgments .....................................................................................xxiAbout the Author...................................................................................... xxiiiSpecial Notes to Advisors.........................................................................xxvOverview of the Book ............................................................................. xxvii

1 The Financial Planning Process ........................................................ 1.1

Emergence of a New Profession......................................................... 1.1What Is Financial Planning?................................................................ 1.3

Financial Planning Is a Process ............................................... 1.4Steps in the Financial Planning Process: The Eight

Financial Planning Domains ............................................... 1.6Step 1: Establishing and Defining the Client-Planner

Relationship................................................................... 1.6Step 2: Gathering Information Necessary to Fulfill the

Engagement ................................................................. 1.9Step 3: Analyzing and Evaluating the Client’s Current

Financial Status .......................................................... 1.13Step 4: Developing the Recommendation(s) ................... 1.16Step 5: Communicating the Recommendation(s) ............ 1.18Step 6: Implementing the Recommendation(s) ............... 1.19Step 7: Monitoring the Recommendation(s) .................... 1.20Step 8: Practicing Within Professional and Regulatory

Standards ................................................................... 1.21How Is Financial Planning Conducted? ............................................ 1.22

Single-Purpose Approach ...................................................... 1.23Multiple-Purpose Approach.................................................... 1.23Comprehensive Approach...................................................... 1.24

Financial Planning Areas of Specialization ....................................... 1.25Content of a Comprehensive Financial Plan..................................... 1.26

Life-Cycle Financial Planning ................................................. 1.28Format of a Comprehensive Financial Plan ........................... 1.30

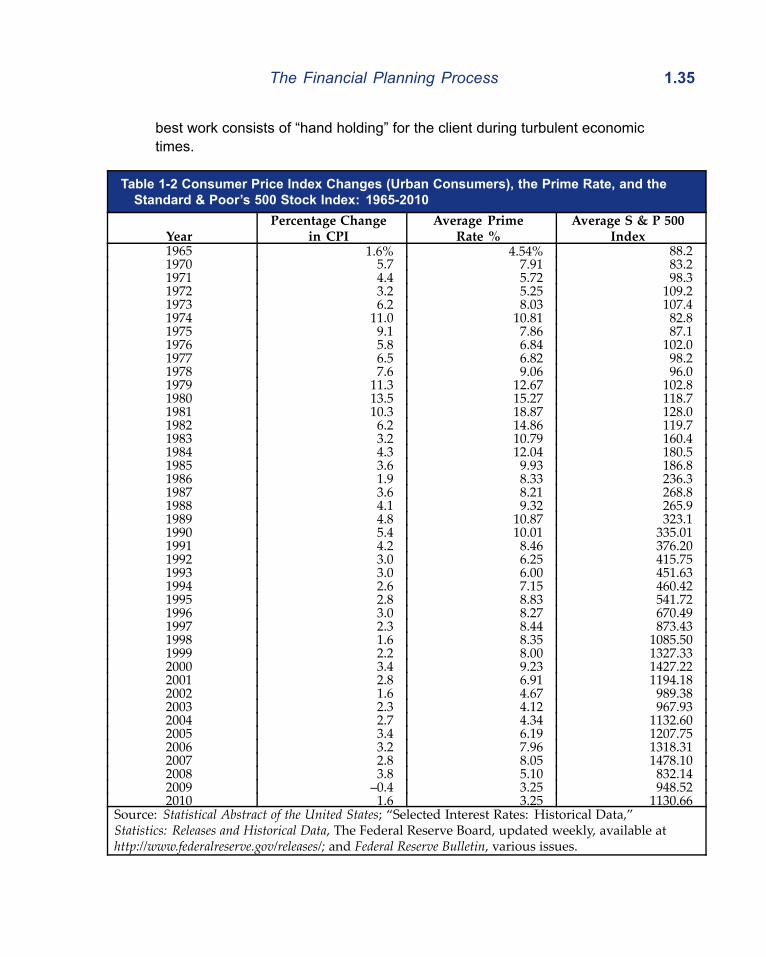

Trends Creating Opportunities for Financial PlanningAdvisors ....................................................................................... 1.33

Consumer Needs for Financial Planning........................................... 1.36Obstacles Confronting Consumers ........................................ 1.39Role of Financial Planning Advisors....................................... 1.40

vii

viii Foundations of Financial Planning: An Overview

Financial Planning Umbrella ............................................................. 1.40Chapter Review................................................................................. 1.41

Review Questions .................................................................. 1.41

2 Insurance Planning and Risk Management ...................................... 2.1

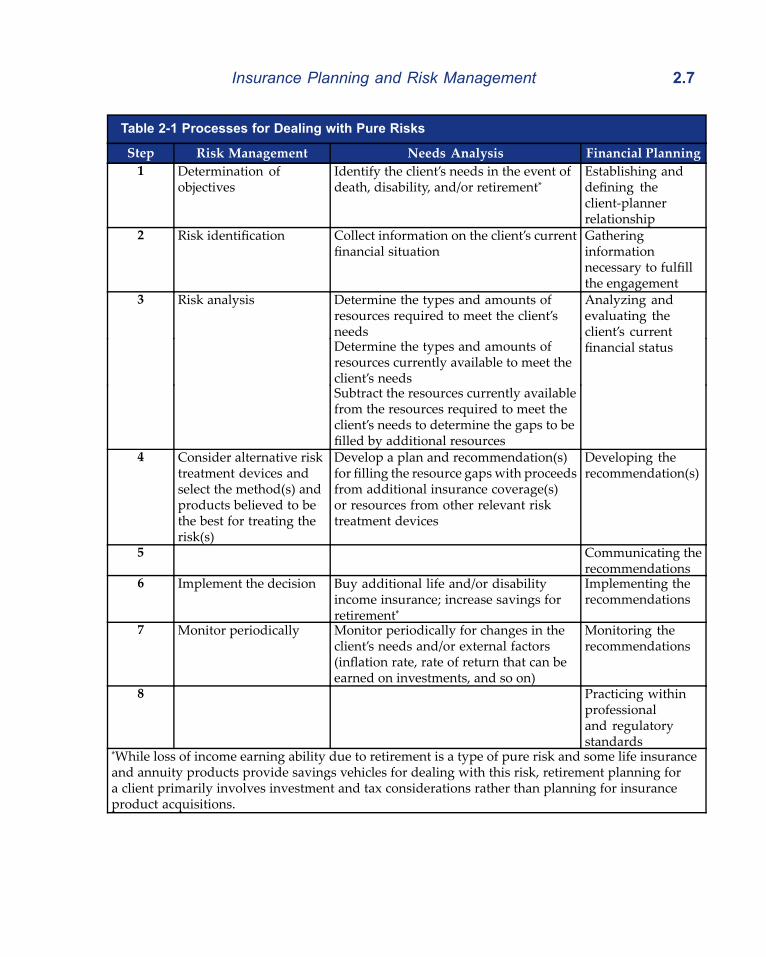

Importance of Protection Objectives ................................................... 2.1Risk ..................................................................................................... 2.2Types of Pure Risks ............................................................................ 2.4Planning for Pure Risks: Insurance and Other Techniques ................ 2.6

Establishing and Defining the Client-Advisor Relationship............................................................................................ 2.8

Gathering Information Necessary to Fulfill theEngagement........................................................................ 2.8

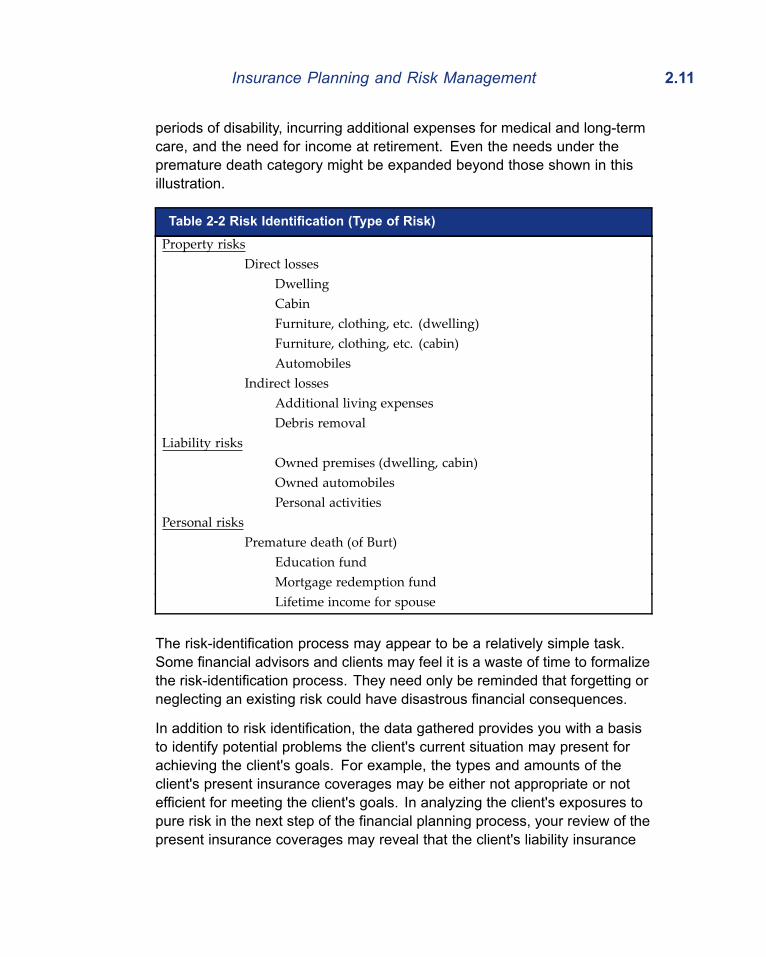

Analyzing and Evaluating the Client’s Current FinancialStatus ............................................................................... 2.12Risk Measurement ............................................................ 2.12

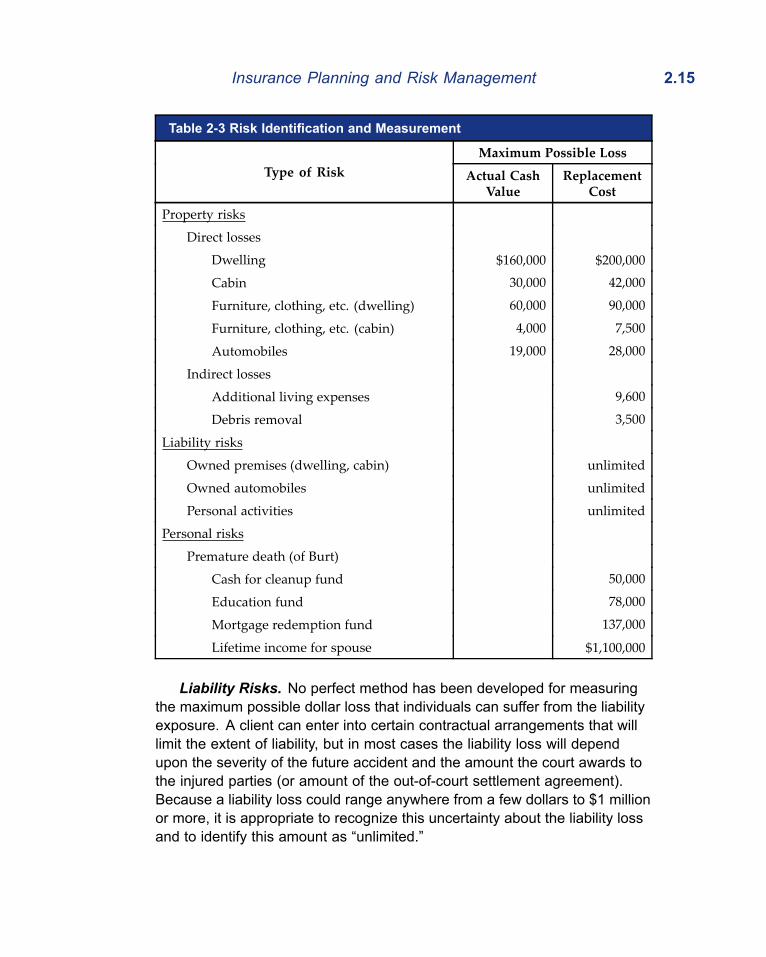

Property Risks ............................................................. 2.12Liability Risks............................................................... 2.15Personal Risks............................................................. 2.15

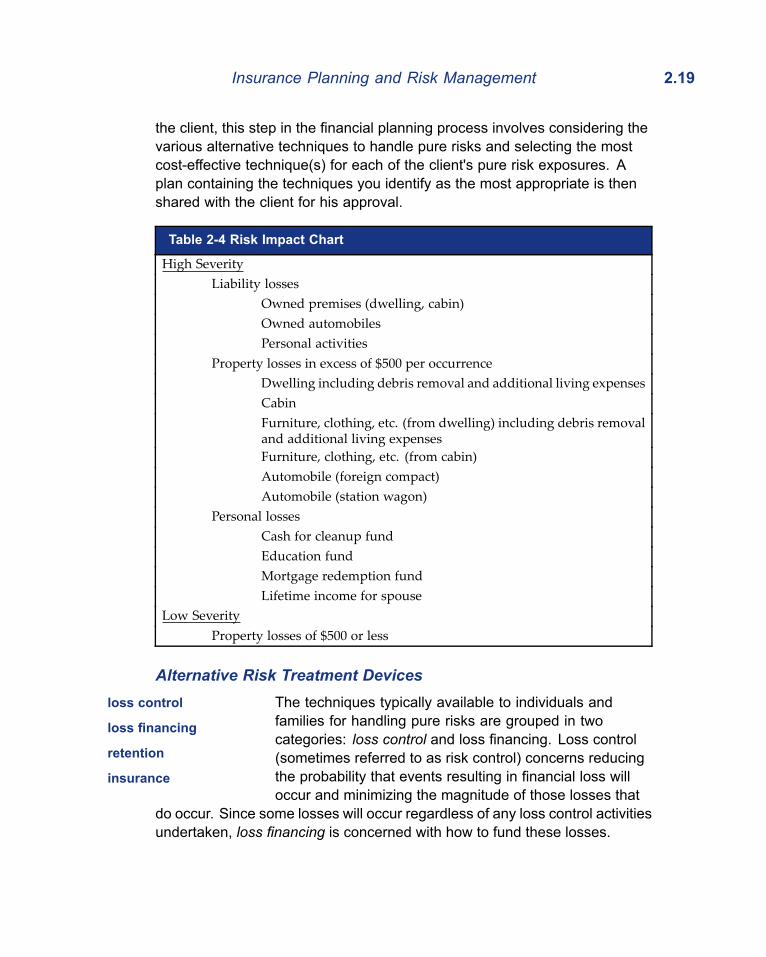

Risk Evaluation ................................................................. 2.18Developing the Recommendations ....................................... 2.18

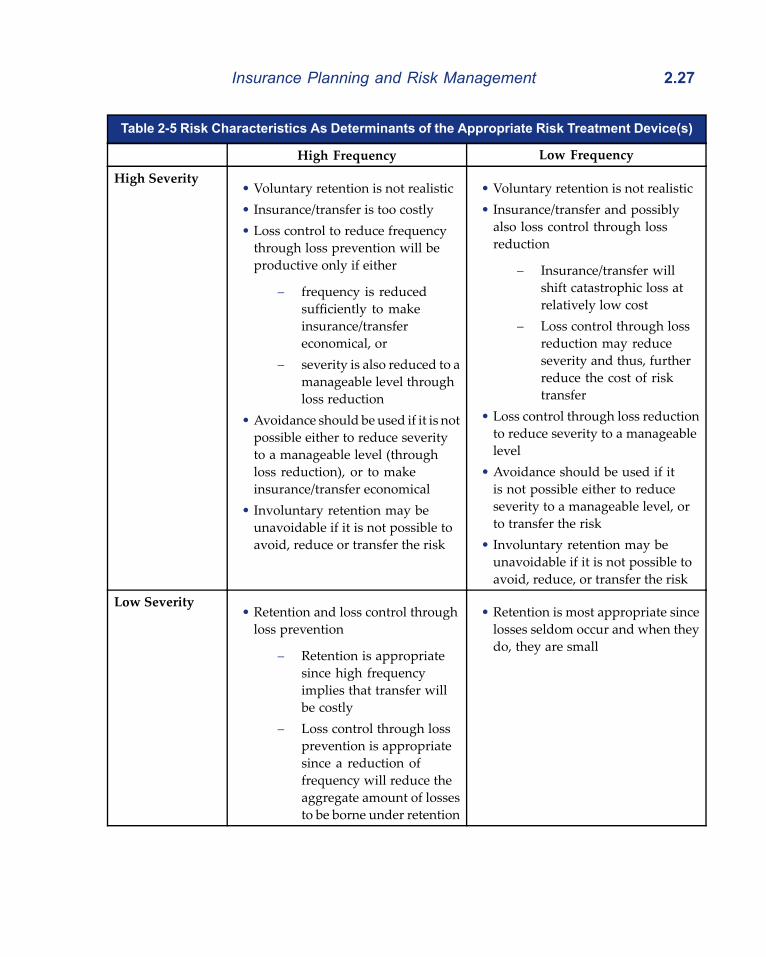

Alternative Risk Treatment Devices.................................. 2.19Risk Avoidance............................................................ 2.20Loss Prevention........................................................... 2.20Loss Reduction............................................................ 2.21Retention ..................................................................... 2.21Insurance..................................................................... 2.22

Selecting Techniques for Handling a Client's PureRisks............................................................................ 2.25

A Plan Using the Selected Techniques ............................. 2.28Communicating the Recommendations and Implementing

the Recommendations ...................................................... 2.29Monitoring the Recommendations.......................................... 2.29

A Survey of Personal Insurance Coverages ..................................... 2.30Meeting Personal Risks.......................................................... 2.30

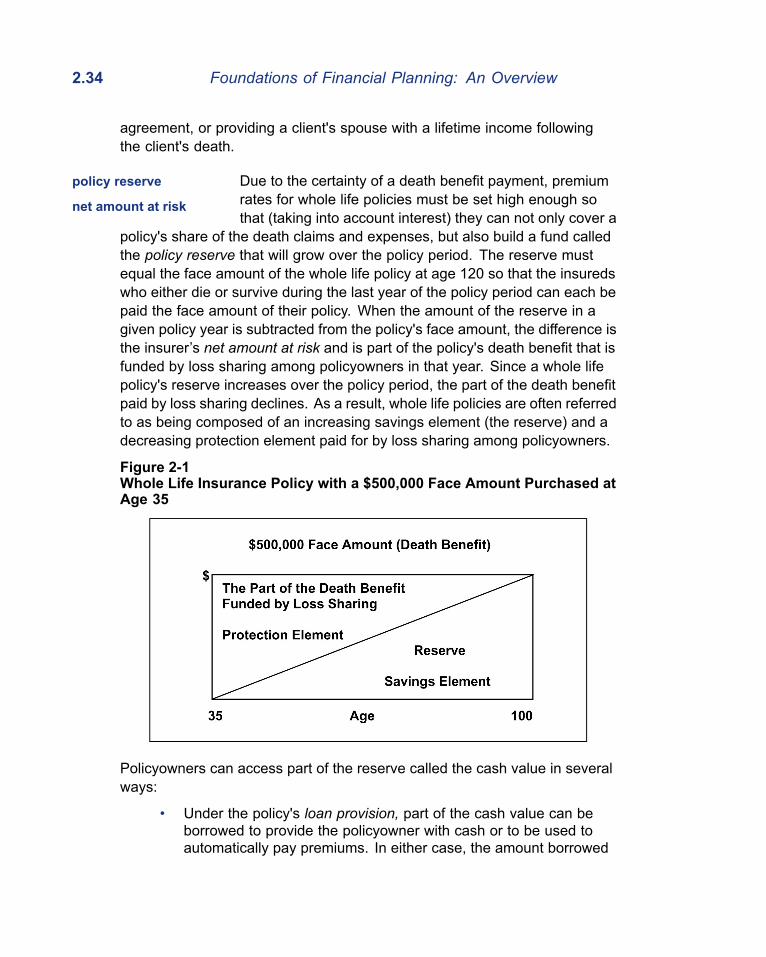

Life Insurance ................................................................... 2.30Term Life Insurance..................................................... 2.31Whole Life Insurance................................................... 2.33Universal Life (UL) Insurance ...................................... 2.36

Annuities ........................................................................... 2.38Individual Health Insurance............................................... 2.40

Medical Expense Insurance ........................................ 2.41

Foundations of Financial Planning: An Overview ix

Disability Income Insurance......................................... 2.41Long-Term Care Insurance.......................................... 2.45

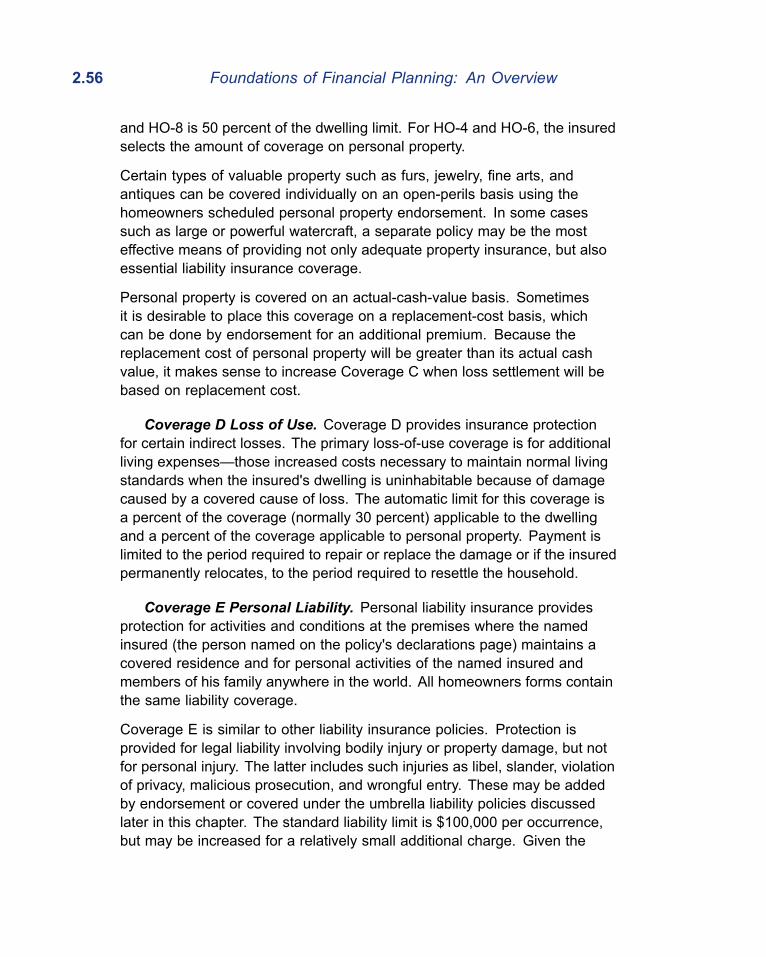

Meeting Property and Liability Risks ...................................... 2.52Homeowners Insurance.................................................... 2.52

Coverage A Dwelling ................................................... 2.54Coverage B Other Structures ...................................... 2.54Coverage C Personal Property.................................... 2.55Coverage D Loss of Use ............................................. 2.56Coverage E Personal Liability ..................................... 2.56Coverage F Medical Payments to Others.................... 2.57

Personal Auto Insurance................................................... 2.57Part A Liability Coverage............................................. 2.58Part B Medical Payments Coverage............................ 2.59Part C Uninsured Motorists Coverage......................... 2.59Part D Coverage for Damage to Your Auto ................. 2.60No-Fault Benefits......................................................... 2.60

Umbrella Liability Insurance.............................................. 2.61A Concluding Comment ......................................................... 2.62

Chapter Review................................................................................. 2.63Review Questions .................................................................. 2.63

3 Employee Benefits Planning .............................................................. 3.1

Scope and Significance of Employee Benefits.................................... 3.1Meaning of Employee Benefits................................................. 3.1Significance of Employee Benefits ........................................... 3.2Growth of Employee Benefits................................................... 3.3

Industrialization ................................................................... 3.3Organized Labor ................................................................. 3.4Wage Controls .................................................................... 3.4Cost Advantages................................................................. 3.5Inflation ............................................................................... 3.5Legislation........................................................................... 3.5

Importance of Benefit Planning........................................................... 3.5Benefit-Planning for the Employer............................................ 3.6Advisor Awareness of Employee Benefits................................ 3.7

The Basis of a Financial Plan ............................................. 3.8The Purchase of Additional Insurance and Retirement

Benefits.......................................................................... 3.8A Source for Negotiating a Compensation Package........... 3.9

Eligibility for Benefits ........................................................................... 3.9Covered Classifications............................................................ 3.9Full-Time Employment ........................................................... 3.10

x Foundations of Financial Planning: An Overview

Probationary Periods.............................................................. 3.10Insurability .............................................................................. 3.10Premium Contributions........................................................... 3.10Termination of Coverage ........................................................ 3.10

Types of Employee Benefits.............................................................. 3.11Medical Expense Insurance ................................................... 3.12

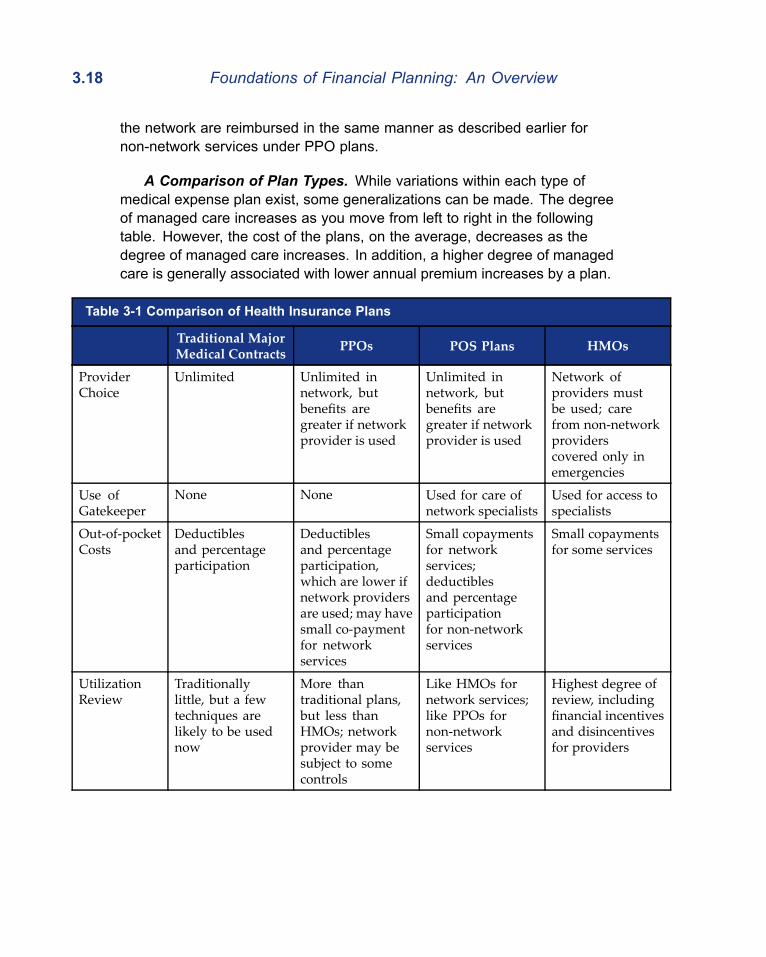

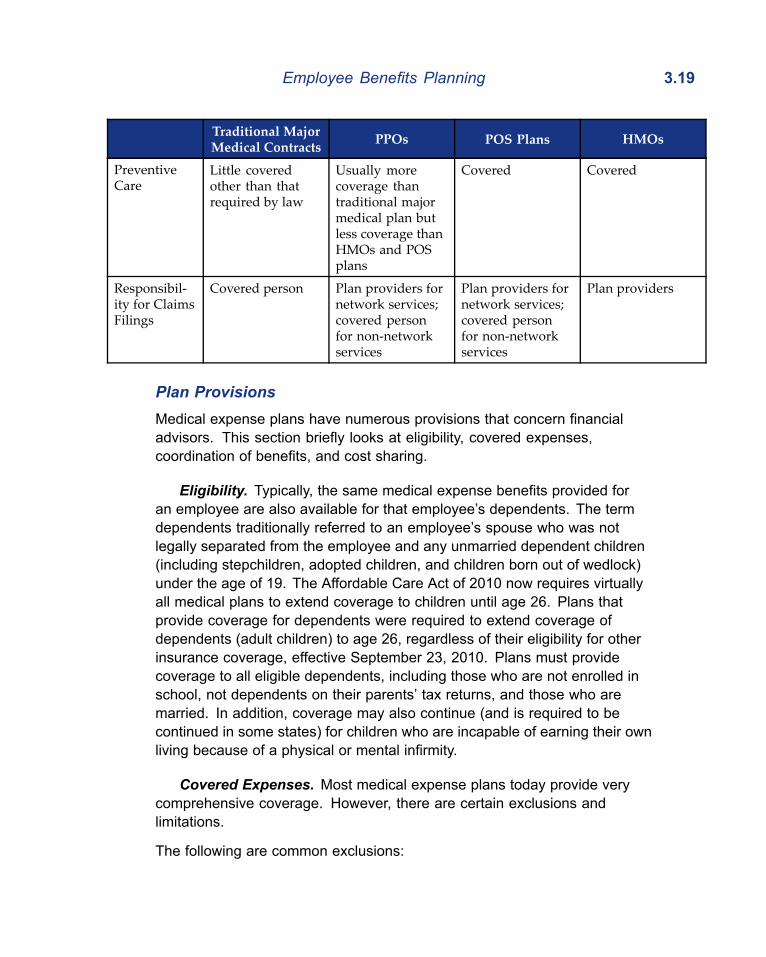

Types of Plans .................................................................. 3.12HMOs .......................................................................... 3.15PPOs ........................................................................... 3.17POS Plans ................................................................... 3.17A Comparison of Plan Types ....................................... 3.18

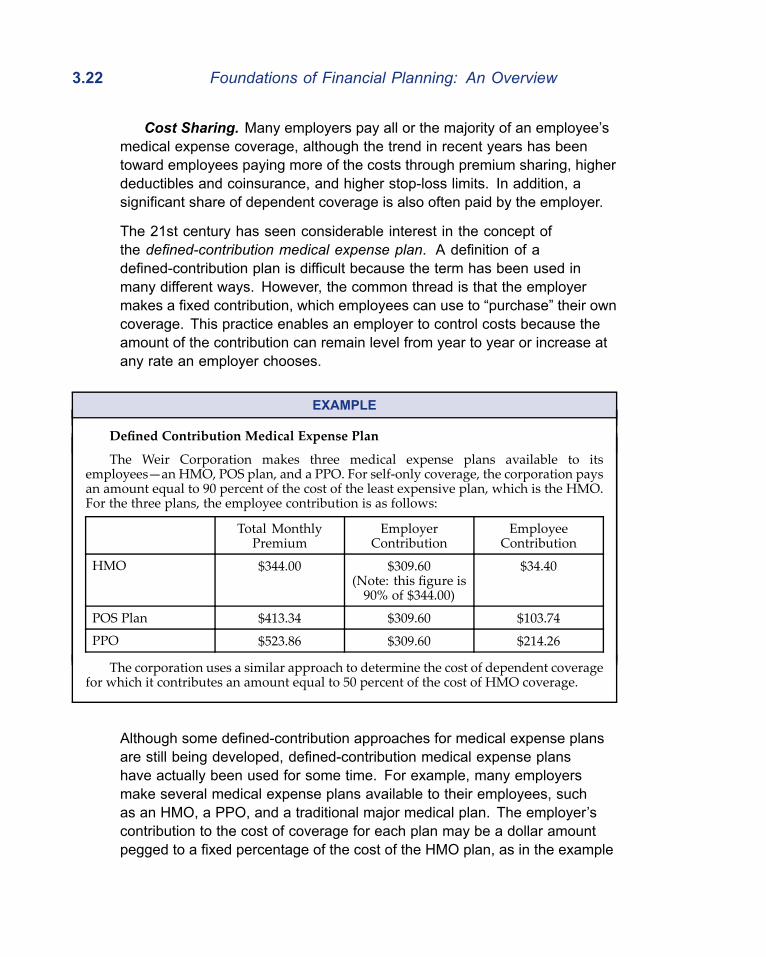

Plan Provisions ................................................................. 3.19Eligibility....................................................................... 3.19Covered Expenses ...................................................... 3.19Coordination of Benefits .............................................. 3.21Cost Sharing................................................................ 3.22

Additional Benefits for Executives..................................... 3.23Taxation............................................................................. 3.23Coverage after Termination of Employment...................... 3.24

COBRA........................................................................ 3.24Conversion .................................................................. 3.25Portability..................................................................... 3.26Postretirement Coverage............................................. 3.26

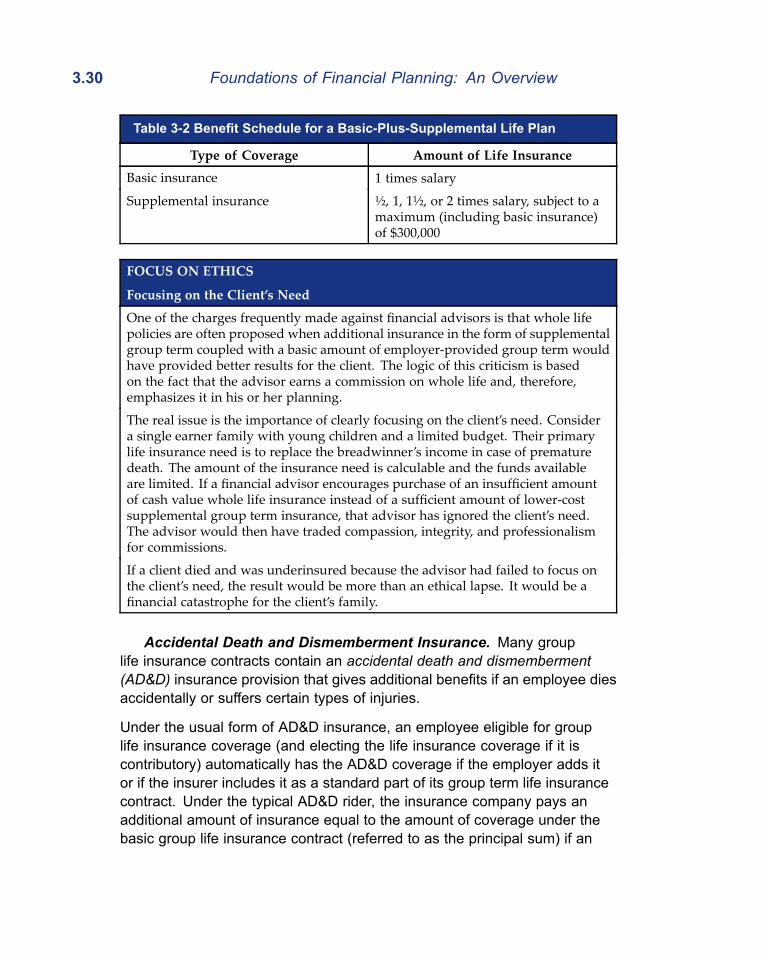

Life Insurance......................................................................... 3.27Benefit Schedule............................................................... 3.27

Multiple-of-Earnings Schedules................................... 3.28Specified-Dollar-Amount Schedules............................ 3.28Reduction in Benefits................................................... 3.28

Termination of Coverage................................................... 3.28Conversion .................................................................. 3.28Portability of Term Coverage ....................................... 3.29

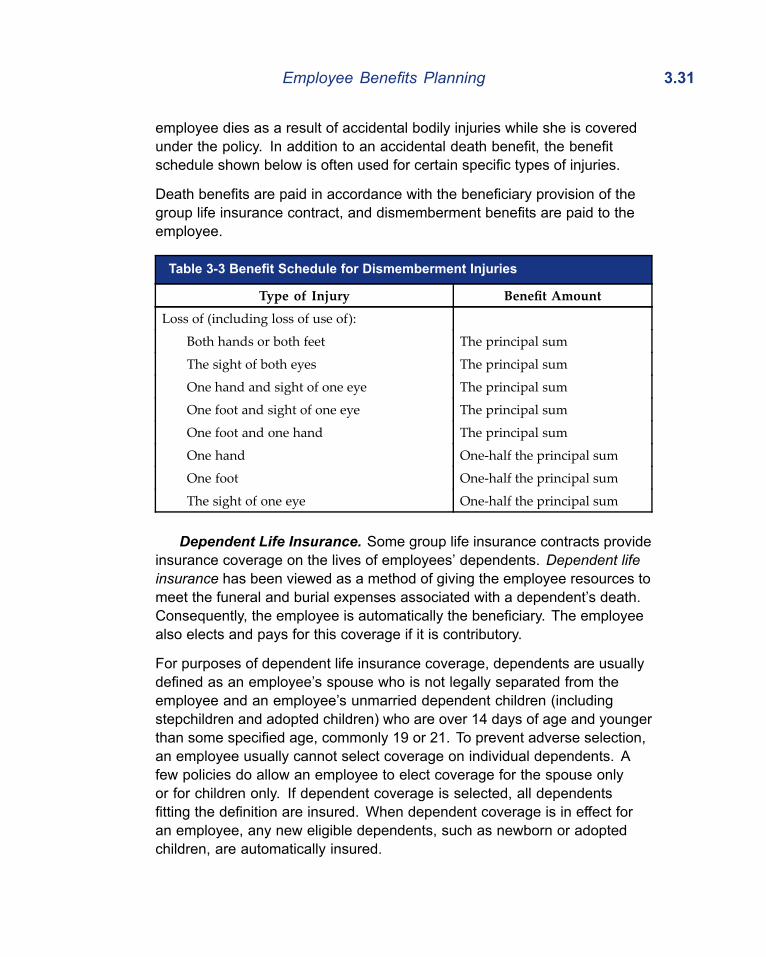

Added Coverages ............................................................. 3.29Supplemental Life Insurance....................................... 3.29Accidental Death and Dismemberment

Insurance ............................................................... 3.30Dependent Life Insurance ........................................... 3.31

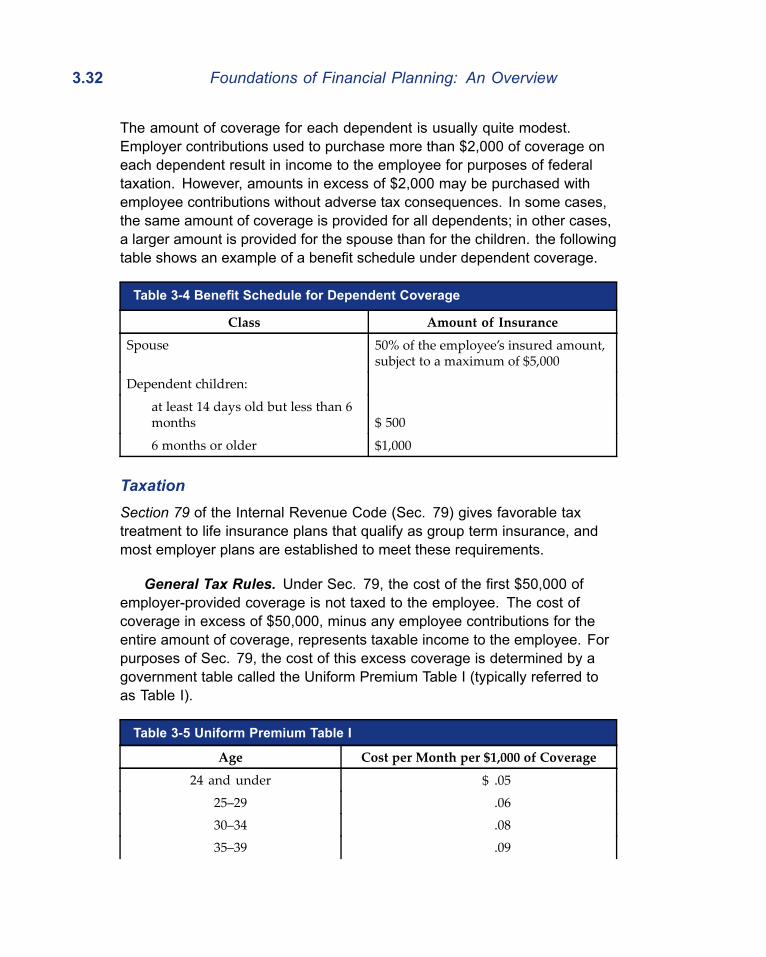

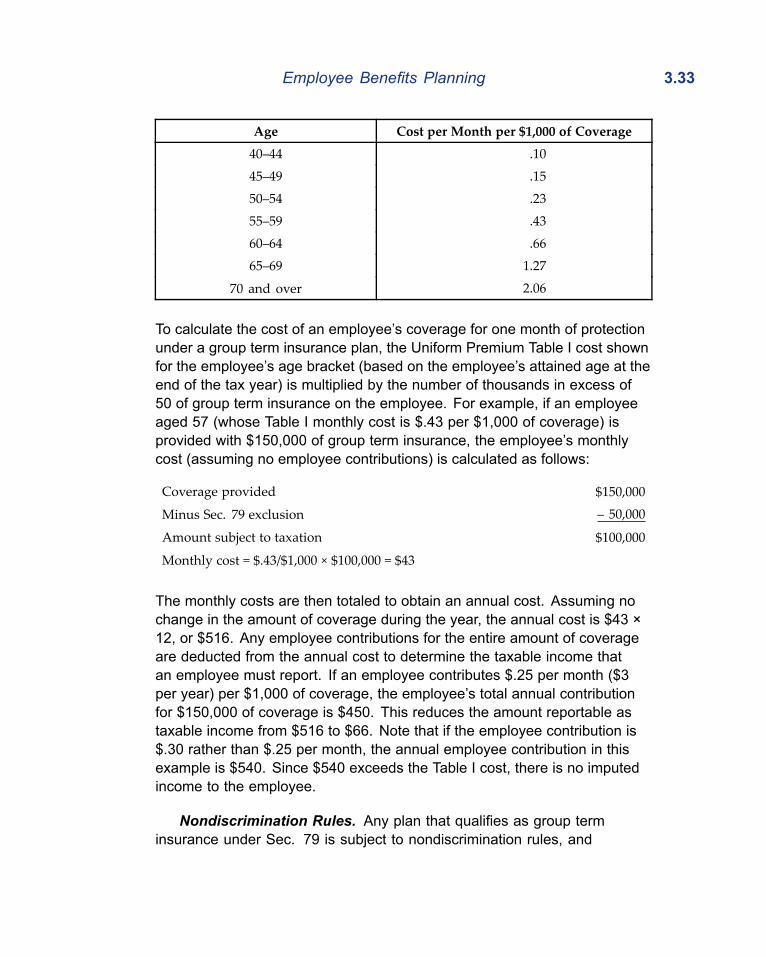

Taxation............................................................................. 3.32General Tax Rules ....................................................... 3.32Nondiscrimination Rules.............................................. 3.33Taxation of Proceeds................................................... 3.34Treatment of Added Coverages .................................. 3.34

Group Universal Life Insurance ........................................ 3.35Coverage Available ..................................................... 3.35

Foundations of Financial Planning: An Overview xi

Options at Retirement and Termination ....................... 3.35Taxation ....................................................................... 3.35

Disability Income Insurance ................................................... 3.36Short-Term Plans .............................................................. 3.36Long-Term Plans............................................................... 3.36

Benefits........................................................................ 3.37Supplemental Benefits................................................. 3.38

Taxation............................................................................. 3.38Dental Insurance .................................................................... 3.38

Benefits ............................................................................. 3.39Scheduled Plans.......................................................... 3.40Nonscheduled Plans.................................................... 3.40Combination Plans ...................................................... 3.41

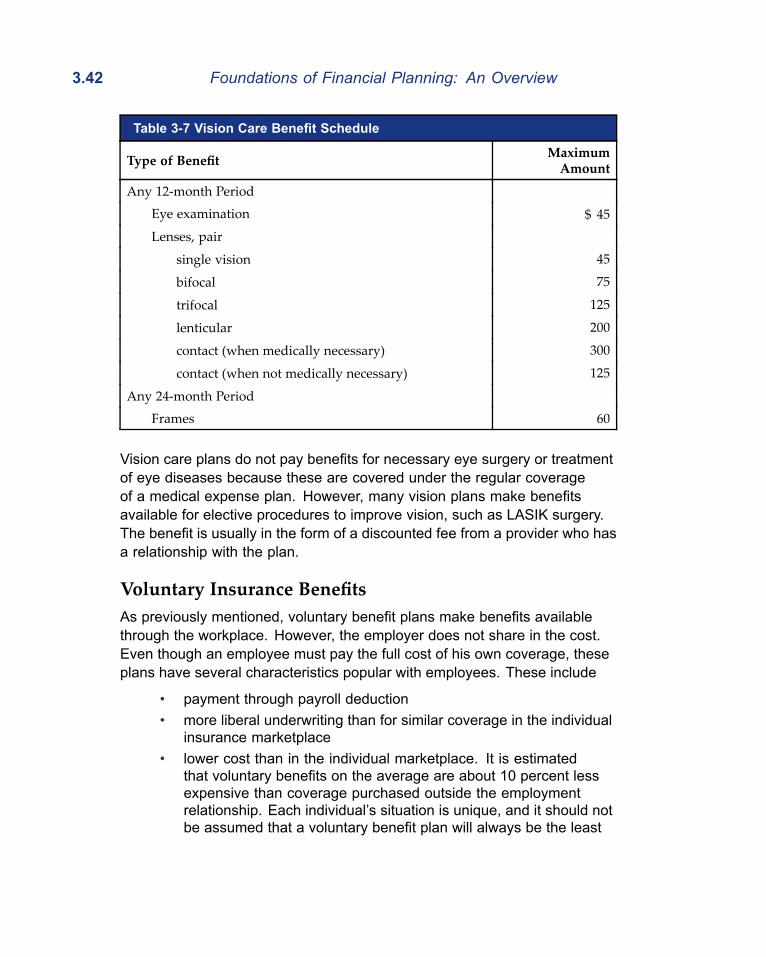

Taxation............................................................................. 3.41Vision Insurance..................................................................... 3.41Voluntary Insurance Benefits.................................................. 3.42

Legal Expense Insurance ................................................. 3.43Taxation ....................................................................... 3.43

Long-Term Care Insurance..................................................... 3.43Taxation............................................................................. 3.44

Supplemental Medical Expense Insurance ............................ 3.44Property and Liability Insurance............................................. 3.45

Taxation............................................................................. 3.45Miscellaneous Fringe Benefits ............................................... 3.45

Education Assistance........................................................ 3.45Adoption Assistance ......................................................... 3.46Dependent Care Assistance ............................................. 3.46

Child-Care Plans ......................................................... 3.47Eldercare Benefits ....................................................... 3.47Taxation of Benefits ..................................................... 3.47

Personal Time Off Without Pay (Family Leave) ................ 3.48State Laws................................................................... 3.48Federal Law................................................................. 3.48

Other Benefits ................................................................... 3.49Cafeteria Plans.................................................................................. 3.50

Nature..................................................................................... 3.50Types...................................................................................... 3.51

Chapter Review................................................................................. 3.53Review Questions .................................................................. 3.54

4 Investment Planning ........................................................................... 4.1

The Meaning of Investment................................................................. 4.1

xii Foundations of Financial Planning: An Overview

Investment versus Speculation ................................................ 4.2Expected Return and Risk........................................................ 4.3Basic Investment Theorems..................................................... 4.5

Service to the Client ............................................................................ 4.6Determining Risk Tolerance ..................................................... 4.7Asset Allocation Models ........................................................... 4.9

Categories of Investment Assets ...................................................... 4.10Cash Equivalents ................................................................... 4.10Bank Deposits ........................................................................ 4.11Money Market Instruments..................................................... 4.11Treasury Bills.......................................................................... 4.12Long-Term Debt Instruments.................................................. 4.13

Governmental Debt Securities .......................................... 4.13Corporate Debt Securities................................................. 4.14

Equity Securities..................................................................... 4.15Common Stock ................................................................. 4.15Preferred Stock ................................................................. 4.16American Depositary Receipts (ADRs)............................. 4.16Investment Companies ..................................................... 4.16

Real Estate and Other Investments ....................................... 4.20Real Estate ....................................................................... 4.20Other Investments............................................................. 4.21

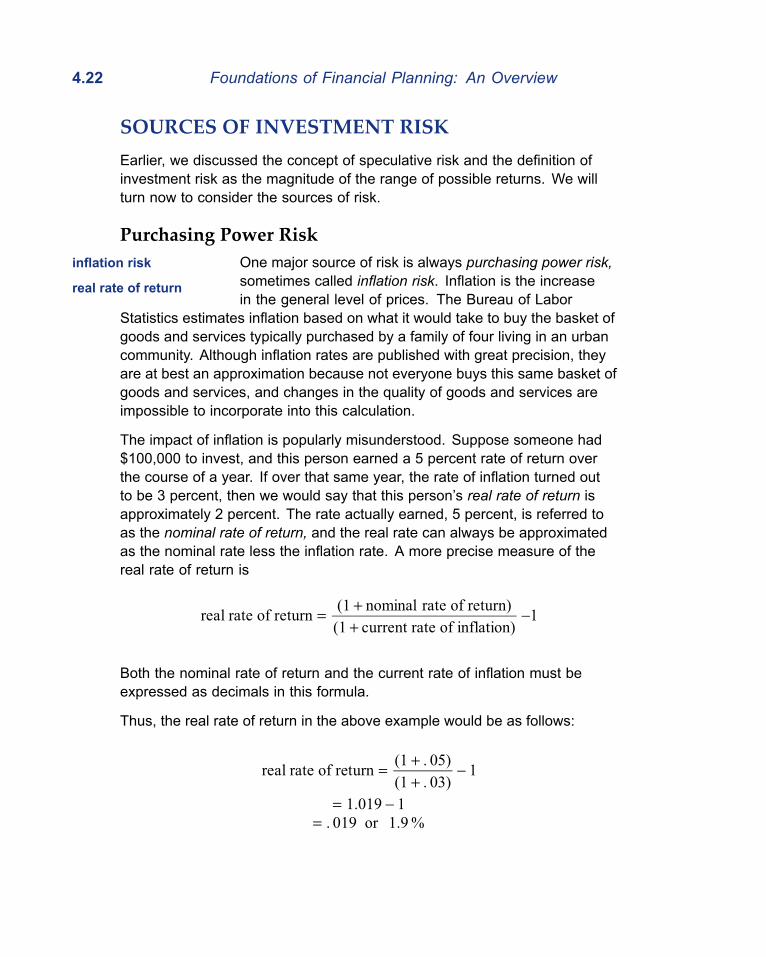

Sources of Investment Risk .............................................................. 4.22Purchasing Power Risk .......................................................... 4.22Interest Rate Risk................................................................... 4.23Business Risk......................................................................... 4.24

Special Portfolio Considerations ....................................................... 4.25Liquidity .................................................................................. 4.25Marketability ........................................................................... 4.27Taxation.................................................................................. 4.27Diversification ......................................................................... 4.30

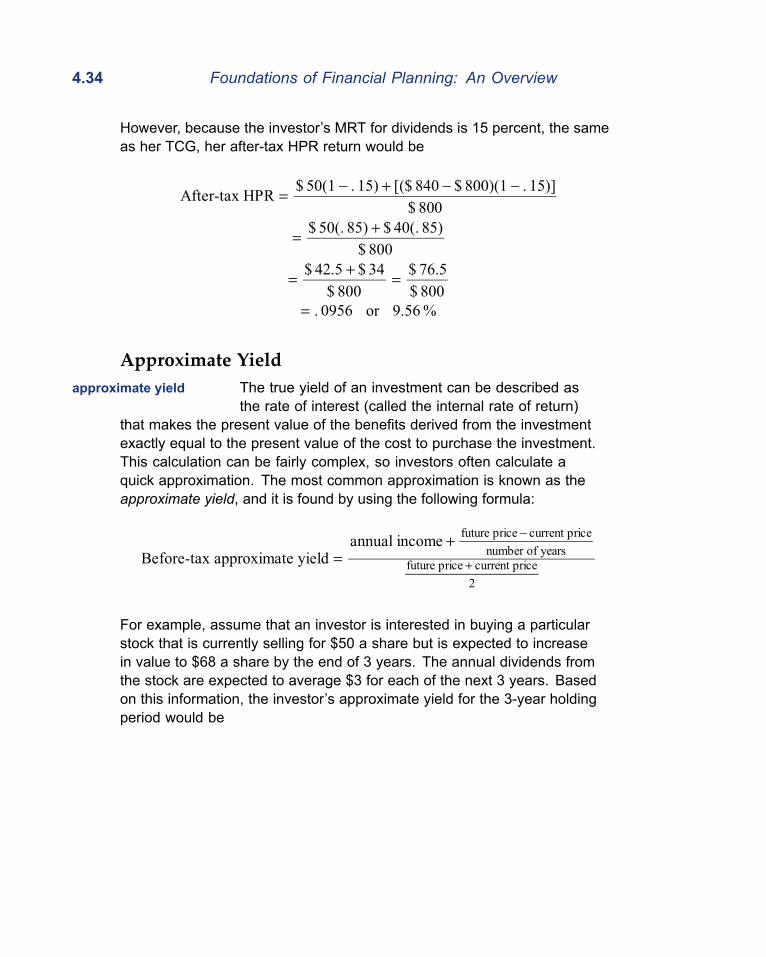

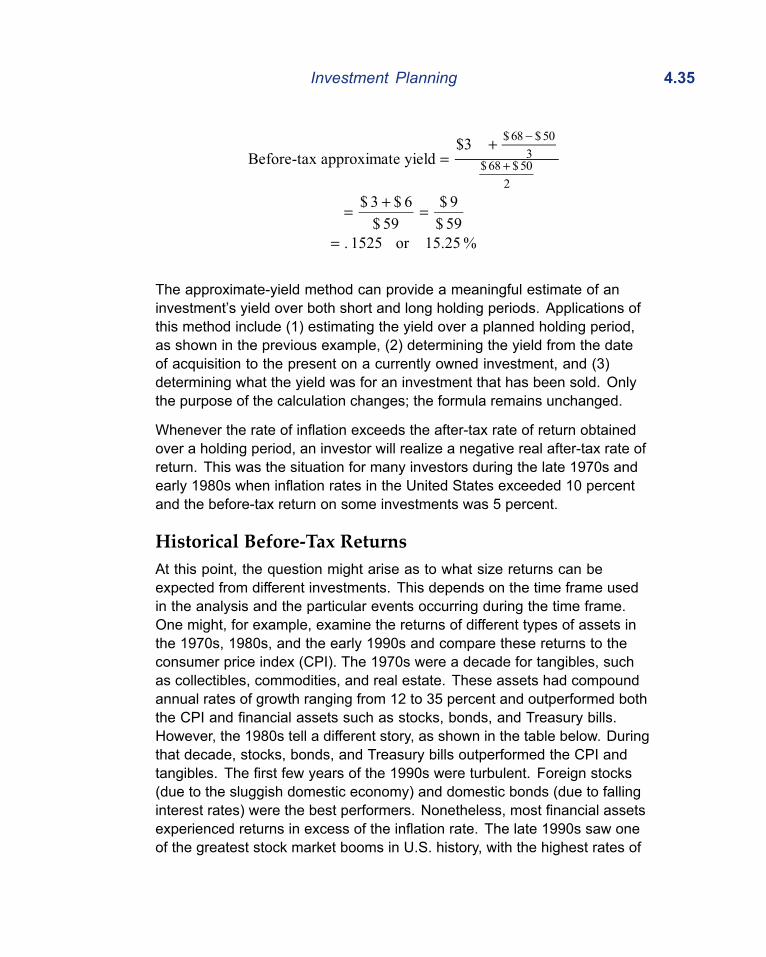

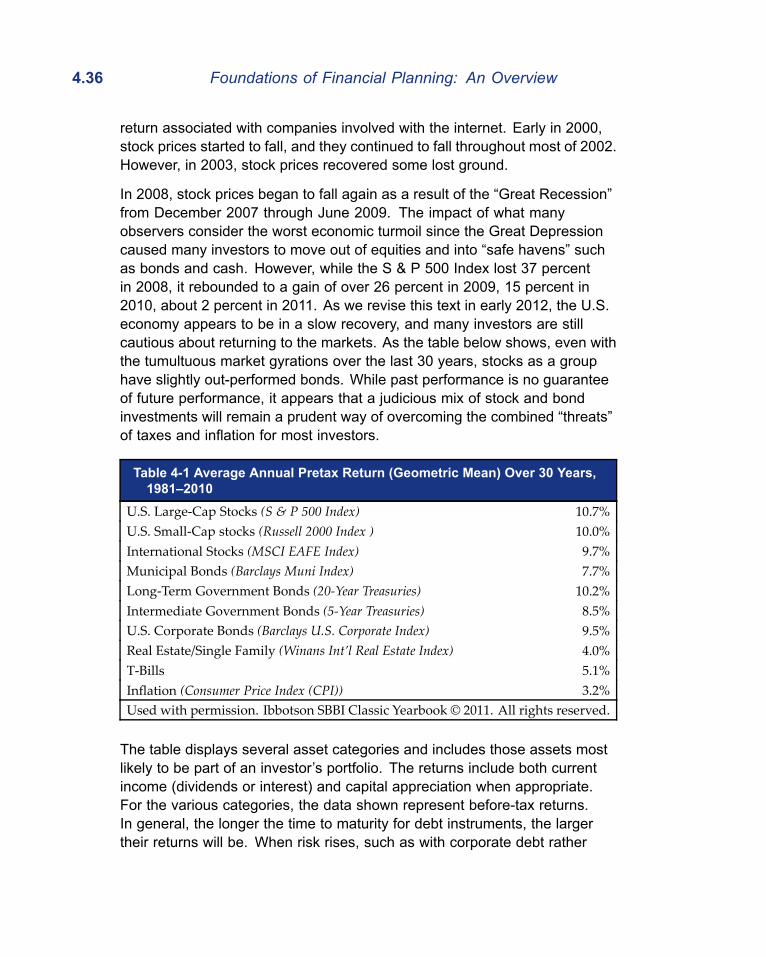

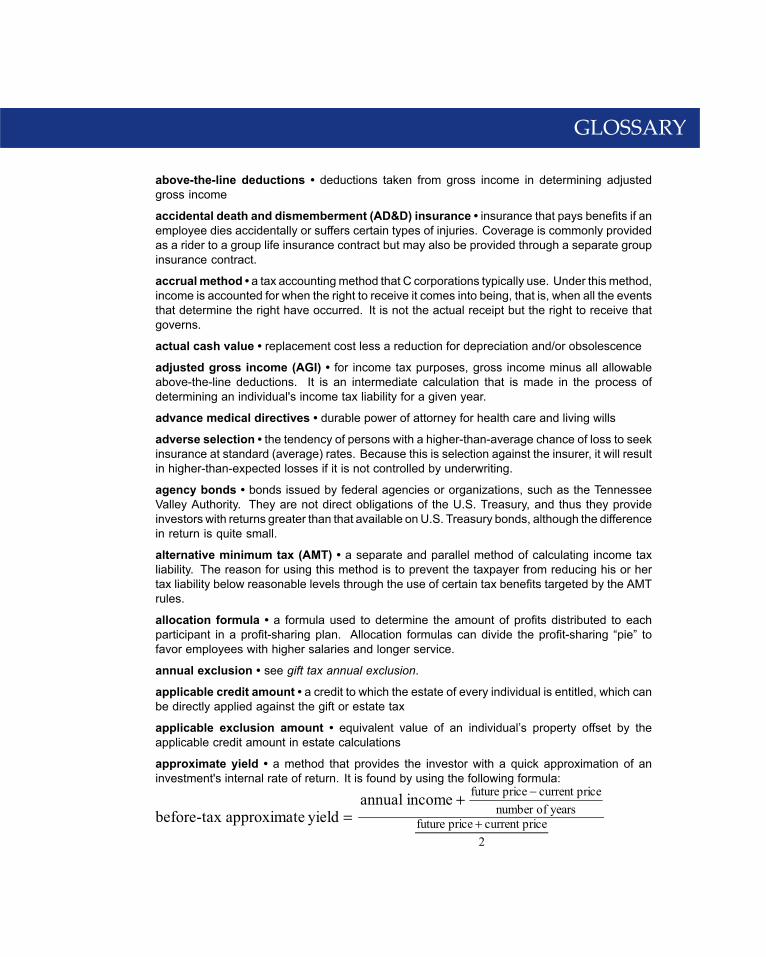

Investment Returns ........................................................................... 4.31Current Yield .......................................................................... 4.31Holding-Period Return (HPR)................................................. 4.33Approximate Yield .................................................................. 4.34Historical Before-Tax Returns................................................. 4.35

Investment Principles, Strategies, and Techniques........................... 4.37Meeting Emergency and Protection Needs First.................... 4.37Matching Investment Instruments with Investment

Goals................................................................................. 4.37Holding Periods for Equity Investments ................................. 4.38Tax-Saving Rationale ............................................................. 4.38Understanding the Investment ............................................... 4.39

Foundations of Financial Planning: An Overview xiii

Using a Consistent Pattern of Investing ................................. 4.39The Power of Compounding................................................... 4.40High-Pressure Sales Tactics .................................................. 4.40Avoiding Discretionary Power ................................................ 4.41Applying Control through the Financial Planning

Process ............................................................................. 4.42Investment Markets and Regulation.................................................. 4.42

Investment Markets ................................................................ 4.42True-Auction Markets........................................................ 4.42Negotiated Markets........................................................... 4.43Dealer Markets.................................................................. 4.44Organized Securities Markets........................................... 4.44

Regulation of the Markets ...................................................... 4.45Securities Act of 1933....................................................... 4.45Securities Exchange Act of 1934...................................... 4.45The Investment Advisors Act of 1940 ............................... 4.46Investment Company Act of 1940..................................... 4.46Securities Investor Protection Act of 1970 ....................... 4.46

A Final Word ..................................................................................... 4.47Chapter Review................................................................................. 4.48

Review Questions .................................................................. 4.48

5 Income Tax Planning........................................................................... 5.1

The Purpose of Income Tax Planning ................................................. 5.1The Principle of Gross Income............................................................ 5.2Exclusions from Gross Income ........................................................... 5.3Deductions .......................................................................................... 5.4

Adjusted Gross Income............................................................ 5.4Taxable Income ........................................................................ 5.5The Standard Deduction or Itemized Deductions..................... 5.6Categories of Deductions ......................................................... 5.7Depreciation: A Special Type of Deduction.............................. 5.8

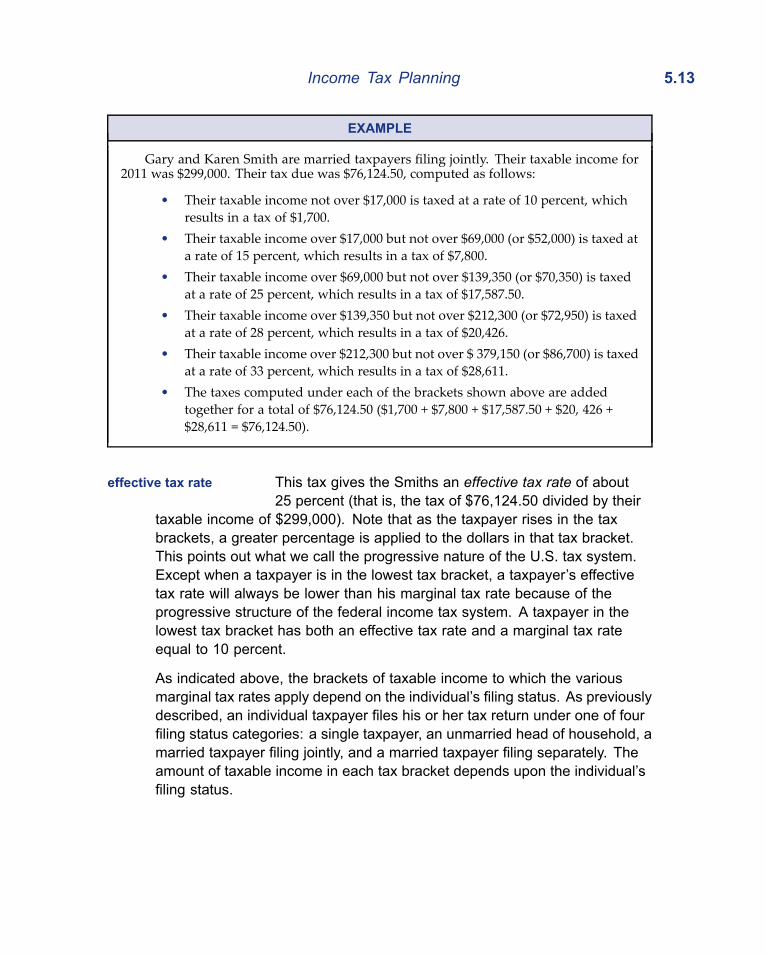

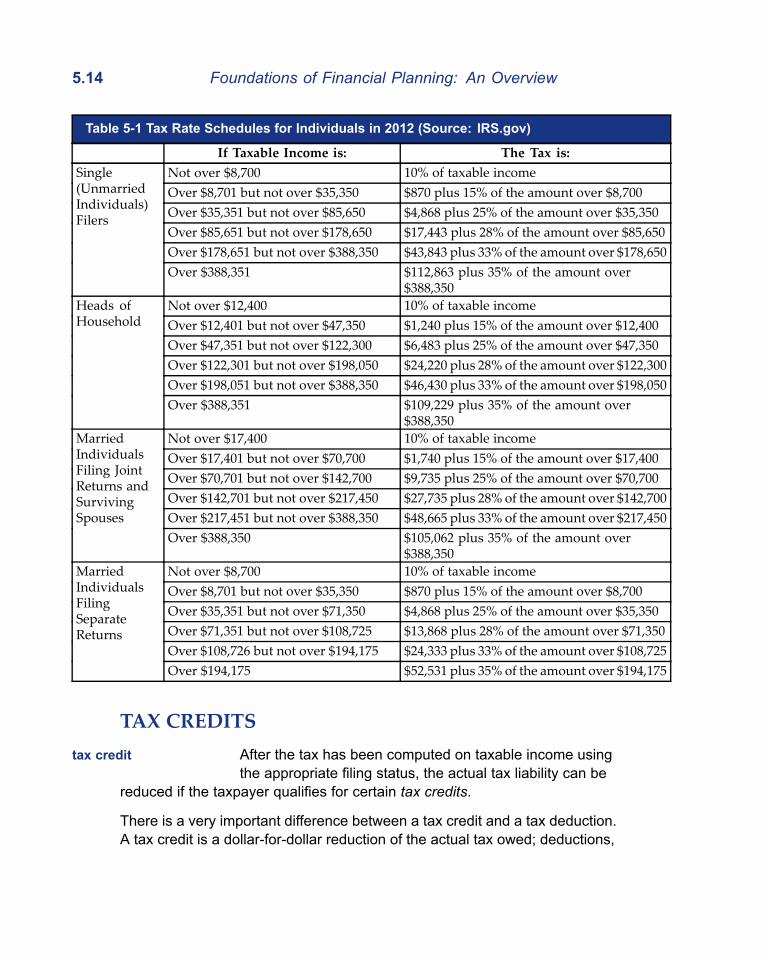

Personal and Dependency Exemptions ............................................ 5.11Tax Rates and Brackets .................................................................... 5.12Tax Credits ........................................................................................ 5.14The Alternative Minimum Tax (AMT)................................................. 5.15Tax Periods and Accounting Methods............................................... 5.16Three Important Issues ..................................................................... 5.17

The “What” Issue: The Economic Benefit Doctrine................ 5.18The “To Whom” Issue: The Fruit and Tree Doctrine............... 5.18The “When” Issue: The Constructive Receipt Doctrine........... 5.19

Basic Income-Tax-Planning Concepts .............................................. 5.20

xiv Foundations of Financial Planning: An Overview

Income and Deduction Shifting .............................................. 5.21Avoiding Limitations on Deductions ....................................... 5.22Deferral and Acceleration Techniques.................................... 5.23The Passive-Loss Rules......................................................... 5.24Tax-Exempt Transactions....................................................... 5.25Nonrecognition Transactions.................................................. 5.25

Computation of Gain or Loss ............................................ 5.26How Nonrecognition Transactions Differ from Taxable

Transactions ................................................................ 5.27Transactions That Result in a Taxable Loss........................... 5.28Ordinary versus Capital Gain and Loss.................................. 5.28

Capital Gain versus Ordinary Income............................... 5.28Tax Treatment of Dividends as Capital Gains................... 5.30Tax Treatment of Capital Losses ...................................... 5.30Sec. 1231 Assets: Depreciable Property and Real

Property Used in a Trade or Business......................... 5.31Taxable Entities ................................................................................. 5.32Conclusion ........................................................................................ 5.32Chapter Review................................................................................. 5.33

Review Questions .................................................................. 5.33

6 Retirement Planning............................................................................ 6.1

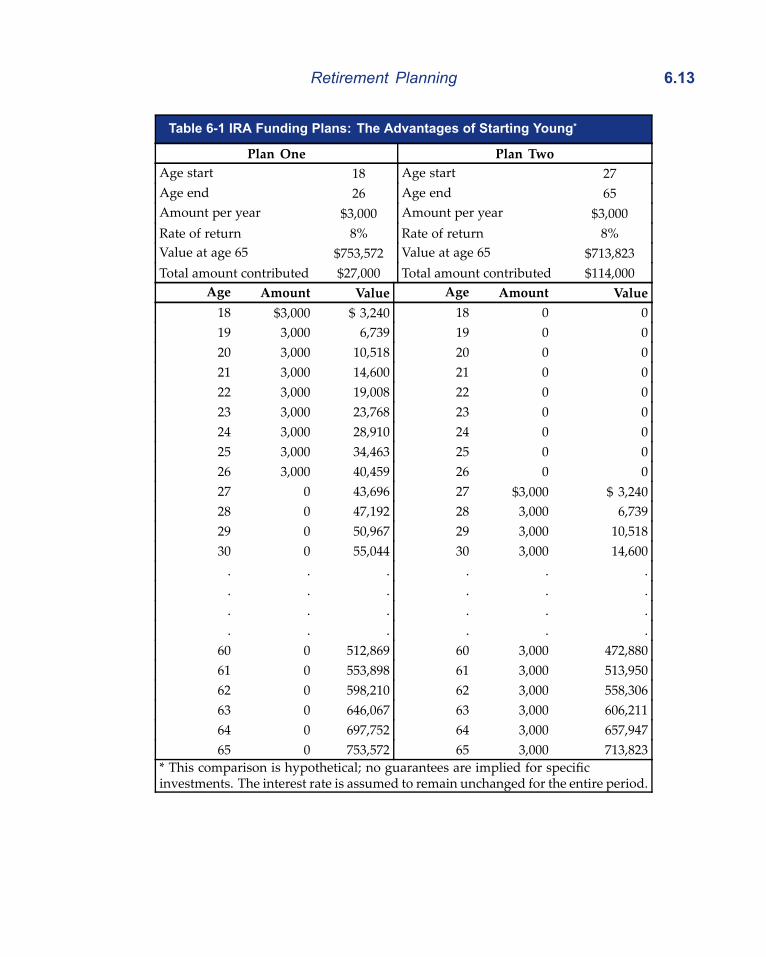

Starting Retirement Planning When Young......................................... 6.2The Role of the Retirement Advisor .................................................... 6.3

Holistic Retirement Planning .................................................... 6.3Responsibilities of the Retirement Advisor............................... 6.6Retirement Planning and the Financial Planning

Process ............................................................................... 6.7Step 1: Establishing and Defining the Client-Planner

Relationship................................................................... 6.7Step 2: Gathering Information Necessary to Fulfill the

Engagement .................................................................. 6.8Step 3: Analyzing and Evaluating the Client’s Current

Financial Status ............................................................. 6.8Step 4: Developing the Recommendation(s)...................... 6.9Step 5: Communicating the Recommendation(s)............... 6.9Step 6: Implementing the Recommendation(s) ................ 6.10

The Art of Financial Planning for Retirement .................................... 6.10Older Clients Still Need to Plan for Retirement ...................... 6.12Overcoming Roadblocks to Retirement Saving...................... 6.14

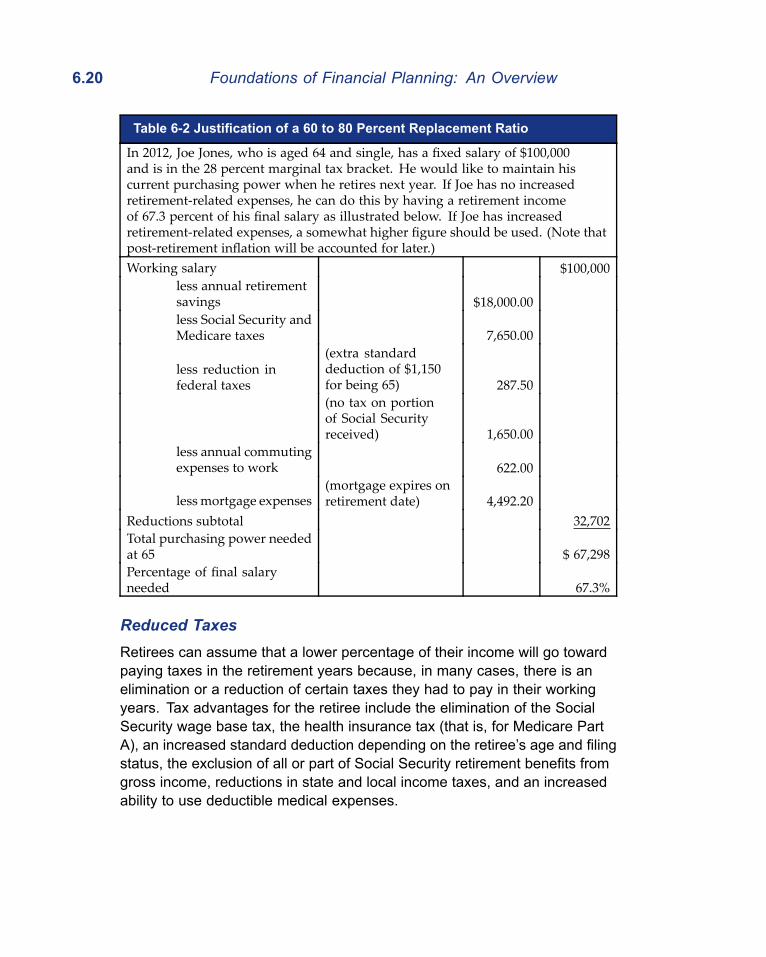

Developing a Retirement Plan .......................................................... 6.17Replacement Ratio Method.................................................... 6.19

Foundations of Financial Planning: An Overview xv

Reduced Taxes ................................................................. 6.20Reduced Living Expenses ................................................ 6.21Additional Factors ............................................................. 6.21

Expense Method .................................................................... 6.21The Effects of Inflation............................................................ 6.22

Potential Sources of Retirement Income........................................... 6.24Tax-Advantaged Qualified Plans ............................................ 6.25

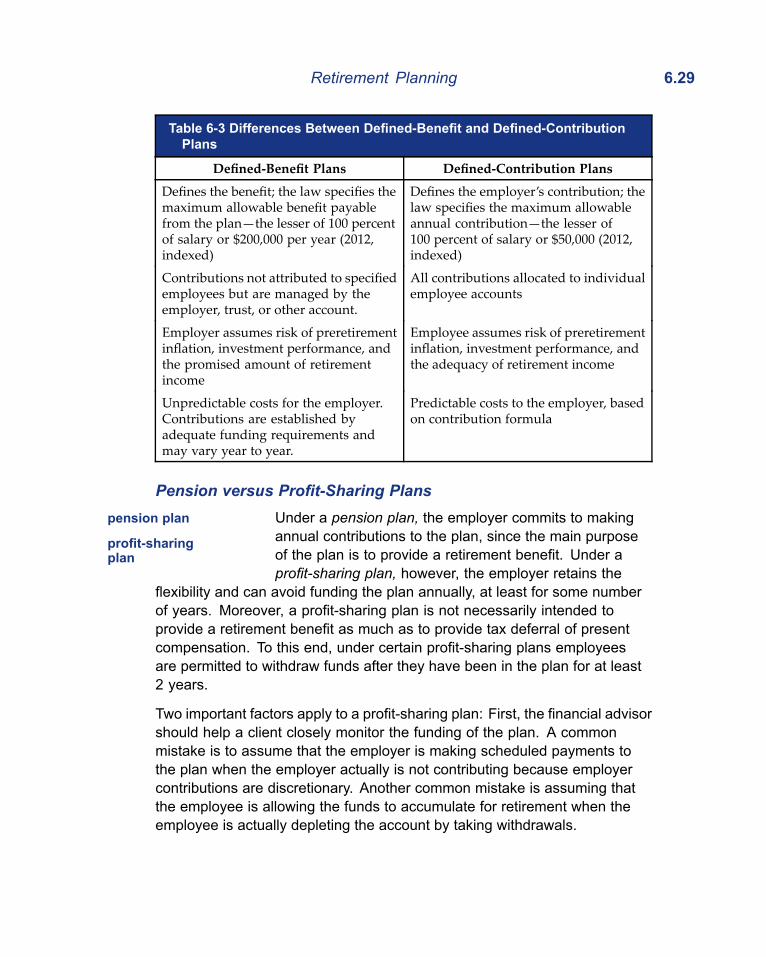

Defined-Benefit versus Defined-ContributionPlans............................................................................ 6.26

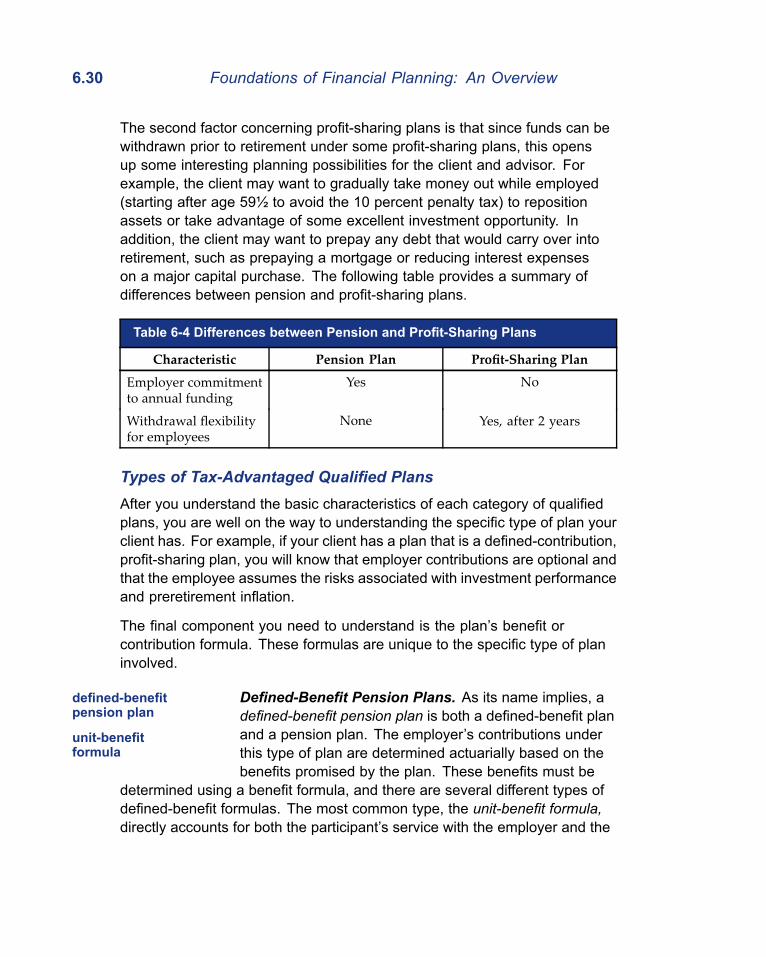

Pension versus Profit-Sharing Plans ................................ 6.29Types of Tax-Advantaged Qualified Plans ........................ 6.30

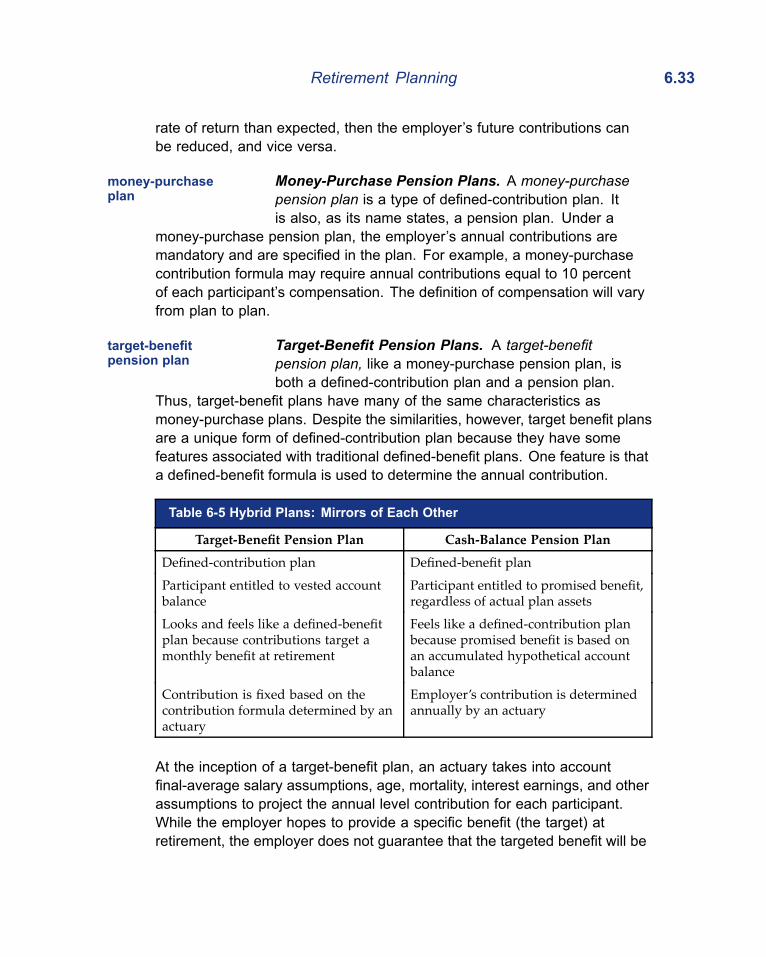

Defined-Benefit Pension Plans.................................... 6.30Cash-Balance Pension Plans ...................................... 6.32Money-Purchase Pension Plans ................................. 6.33Target-Benefit Pension Plans ...................................... 6.33Profit-Sharing Plans..................................................... 6.34401(k) Plans ................................................................ 6.34Stock Bonus Plans and ESOPs................................... 6.36

Other Tax-Advantaged Plans ................................................. 6.38Simplified Employee Pension (SEP)................................. 6.38SIMPLEs........................................................................... 6.38

Salary Deferral Contributions ...................................... 6.39403(b) Plans...................................................................... 6.40

Nonqualified Plans ................................................................. 6.40IRAs........................................................................................ 6.42

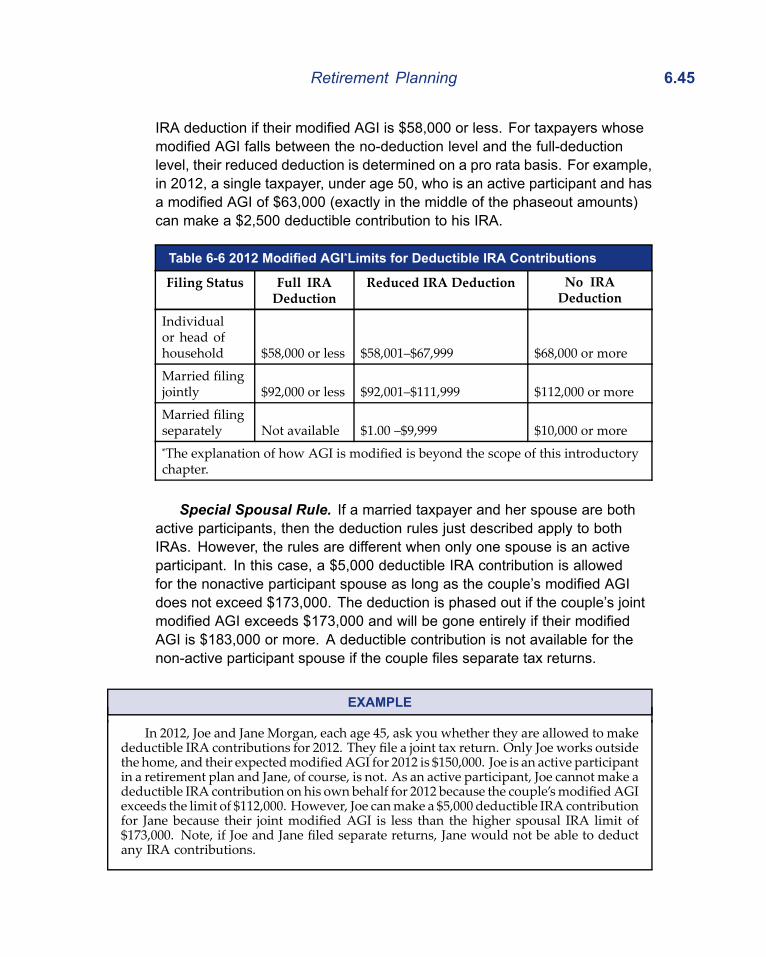

Traditional IRAs ................................................................ 6.43Active Participant......................................................... 6.43Monetary Limits ........................................................... 6.44Special Spousal Rule .................................................. 6.45Distributions................................................................. 6.46

Roth IRAs.......................................................................... 6.46Overcoming Inadequate Retirement Resources ............................... 6.48

Trading Down to a Less Expensive Home ............................. 6.48Obtaining a Reverse Mortgage .............................................. 6.49Postretirement Employment ................................................... 6.50Pension Maximization ............................................................ 6.52

Chapter Review................................................................................. 6.53Review Questions .................................................................. 6.54

7 Estate Planning.................................................................................... 7.1

The Goals of Estate Planning ............................................................. 7.1Starting the Process............................................................................ 7.3

xvi Foundations of Financial Planning: An Overview

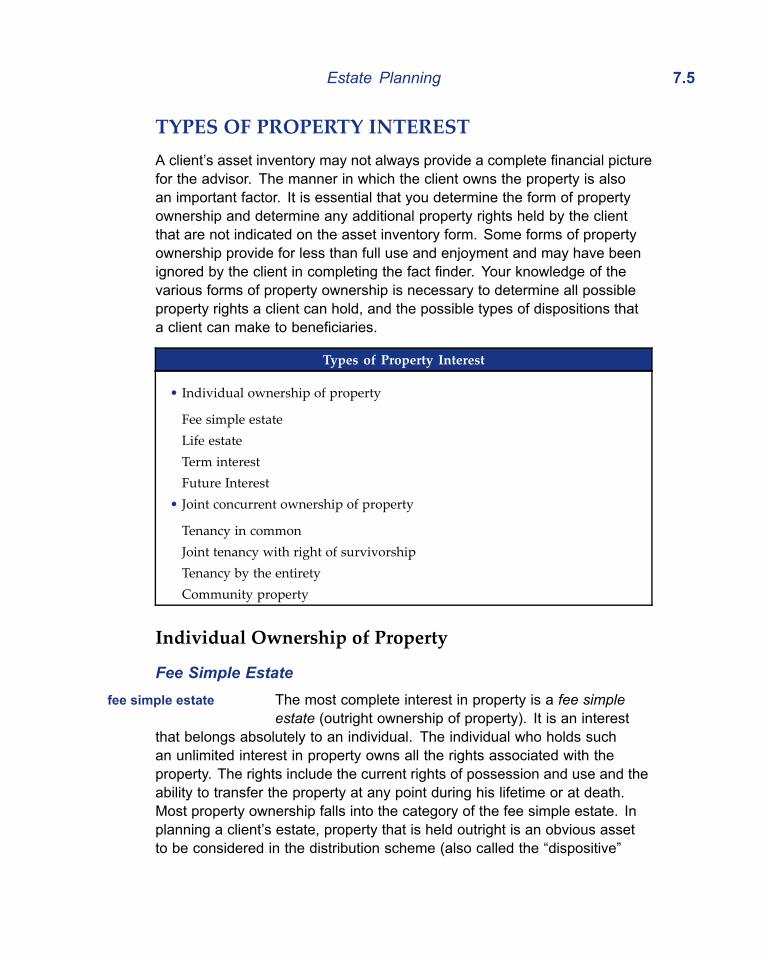

Types of Property Interest ................................................................... 7.5Individual Ownership of Property ............................................. 7.5

Fee Simple Estate............................................................... 7.5Life Estate ........................................................................... 7.6Estate for Term of Years ..................................................... 7.6Future Interest..................................................................... 7.7

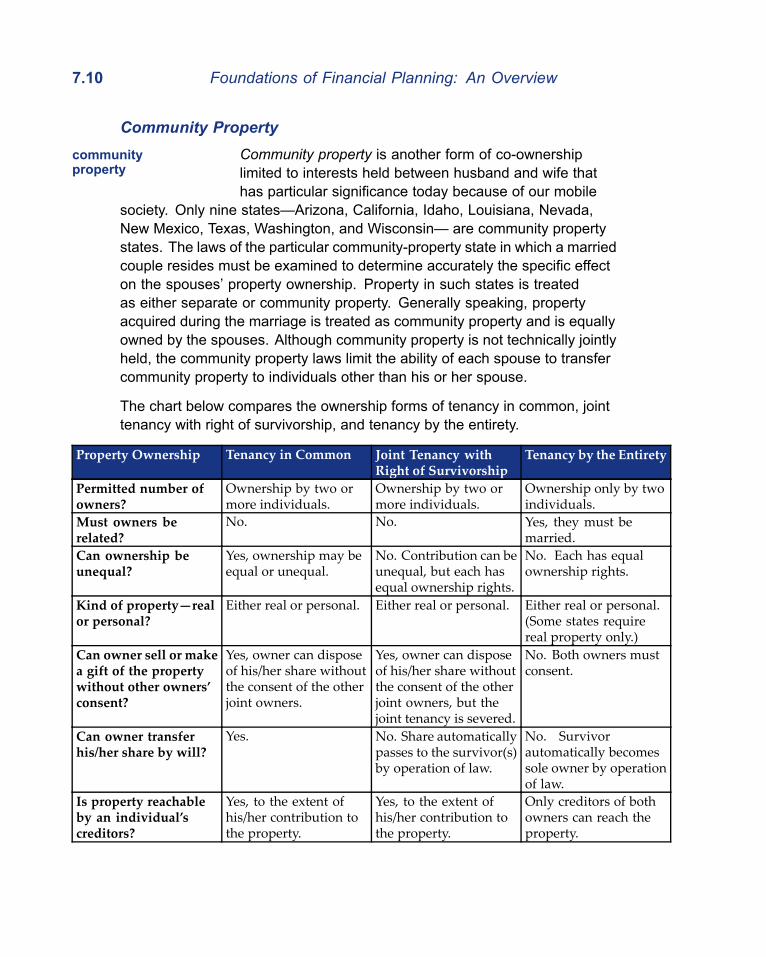

Joint Concurrent Ownership of Property .................................. 7.8Tenancy in Common ........................................................... 7.8Joint Tenancy with Right of Survivorship ............................ 7.8Tenancy by the Entirety....................................................... 7.9Community Property ......................................................... 7.10

Other Property Rights............................................................. 7.11Beneficial Interests............................................................ 7.11Powers .............................................................................. 7.11

Power of Appointment ................................................. 7.11Power of Attorney ........................................................ 7.12

Estate Planning Documents.............................................................. 7.12Wills........................................................................................ 7.13

Requirements for a Valid Will ............................................ 7.13What Can a Valid Will Accomplish? .................................. 7.13

Trusts ..................................................................................... 7.14Living (Inter Vivos) Trust ................................................... 7.15Testamentary Trust ........................................................... 7.17

Durable Powers of Attorney ................................................... 7.17Advance Medical Directives ................................................... 7.20

Transfers at Death ............................................................................ 7.21The Probate Estate ................................................................ 7.22

Transfers through Will Provisions ..................................... 7.22Transfers by Intestacy....................................................... 7.23

The Nonprobate Estate .......................................................... 7.24Transfers by Operation of Law.......................................... 7.24Transfers by Operation of Contract................................... 7.25

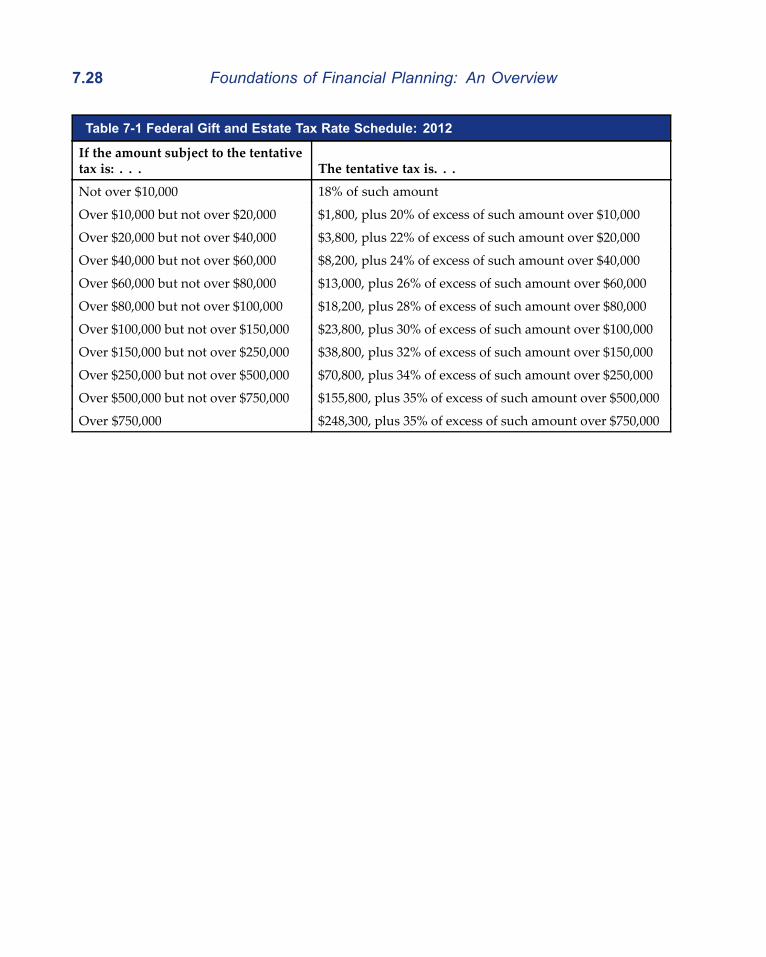

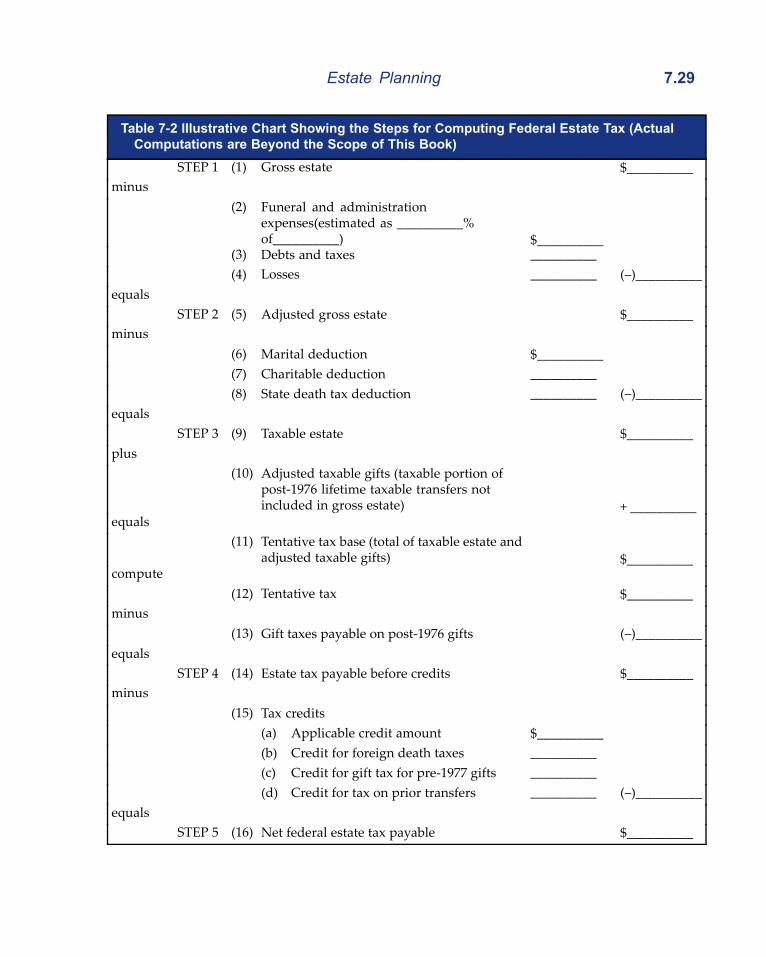

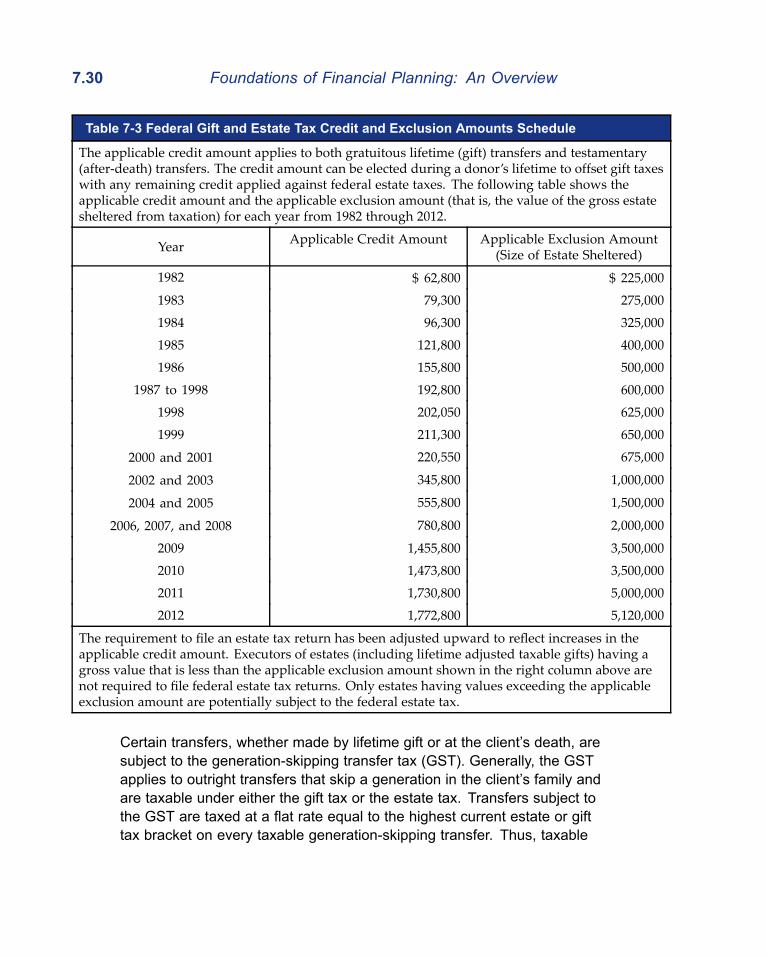

Taxes Imposed on Transfers of Wealth............................................. 7.26Federal Transfer Taxes .......................................................... 7.27

Federal Gift Tax................................................................. 7.31Exempt Transfers ........................................................ 7.31Gift Tax Annual Exclusion............................................ 7.32Deductions from the Gift Tax Base.............................. 7.33Applicable Credit Amount ............................................ 7.33

Federal Estate Tax............................................................ 7.34The Gross Estate......................................................... 7.34Items Deductible from the Gross Estate...................... 7.35Marital Deduction......................................................... 7.35

Foundations of Financial Planning: An Overview xvii

Charitable Deduction ................................................... 7.35Applicable Exclusion Amount ...................................... 7.35State Death Tax Credit ................................................ 7.36

Generation-Skipping Transfer Tax (GST Tax)................... 7.36Types of Transfers....................................................... 7.36Lifetime Exemption and Annual Exclusion .................. 7.38

State Death Taxes.................................................................. 7.38State Inheritance Tax ........................................................ 7.39State Estate Tax................................................................ 7.39Credit Estate Tax............................................................... 7.39Planning for State Death Taxes ........................................ 7.40

Preserving the Client’s Wealth .......................................................... 7.41The Advantages of Lifetime Gifts ........................................... 7.41

Nontax Advantages of Lifetime Gifts................................. 7.41Tax Advantages of Lifetime Gifts ...................................... 7.42Opportunities Created by the Gift Tax Annual

Exclusion ..................................................................... 7.42Gifts to Minors................................................................... 7.43

Uniform Gifts to Minors Act (UGMA) or UniformTransfers to Minors Act (UTMA) ............................ 7.43

Sec. 2503(b) Trust....................................................... 7.44Sec. 2503(c) Trust....................................................... 7.44Irrevocable Trust with Current Withdrawal

Powers ................................................................... 7.44Federal Estate Tax Planning ............................................. 7.45

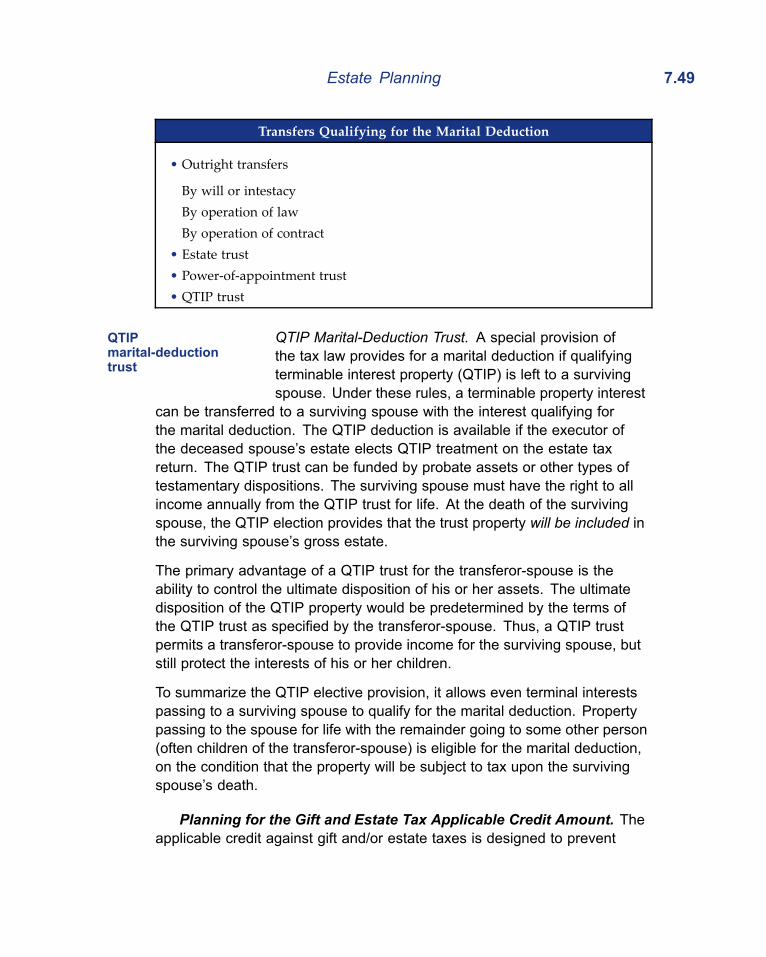

Planning for the Marital Deduction .............................. 7.45Portability Under the New Estate Tax Law............. 7.46Outright Transfers .................................................. 7.47Estate Trust ............................................................ 7.48Power-of-Appointment Trust .................................. 7.48QTIP Marital-Deduction Trust ................................ 7.48

Planning for the Gift and Estate Tax ApplicableCredit Amount ........................................................ 7.49

Coordination of the Marital Deduction and theApplicable Credit Amount....................................... 7.50

Planning Charitable Contributions ............................... 7.52Advantages of Gifts to Charity ............................... 7.52Gifts of Remainder Interests to Charity .................. 7.52Donating Income Interests to Charity..................... 7.53

Life Insurance in the Estate and/or Financial Plan............ 7.53Life Insurance for Estate Enhancement ...................... 7.54Life Insurance for Estate Liquidity ............................... 7.54Life Insurance Trusts ................................................... 7.55

xviii Foundations of Financial Planning: An Overview

Revocable Life Insurance Trusts............................ 7.55Irrevocable Life Insurance Trusts........................... 7.55

Conclusion ........................................................................................ 7.56Chapter Review................................................................................. 7.57

Review Questions .................................................................. 7.58

8 Social Security, Medicare, and Medicare Supplements................... 8.1

Social Security and Medicare.............................................................. 8.1The Importance, Coverage, and Financing of Social

Security and Medicare ........................................................ 8.2Importance of Programs ..................................................... 8.2Extent of Coverage ............................................................. 8.2Tax Rates and Wage Bases................................................ 8.2

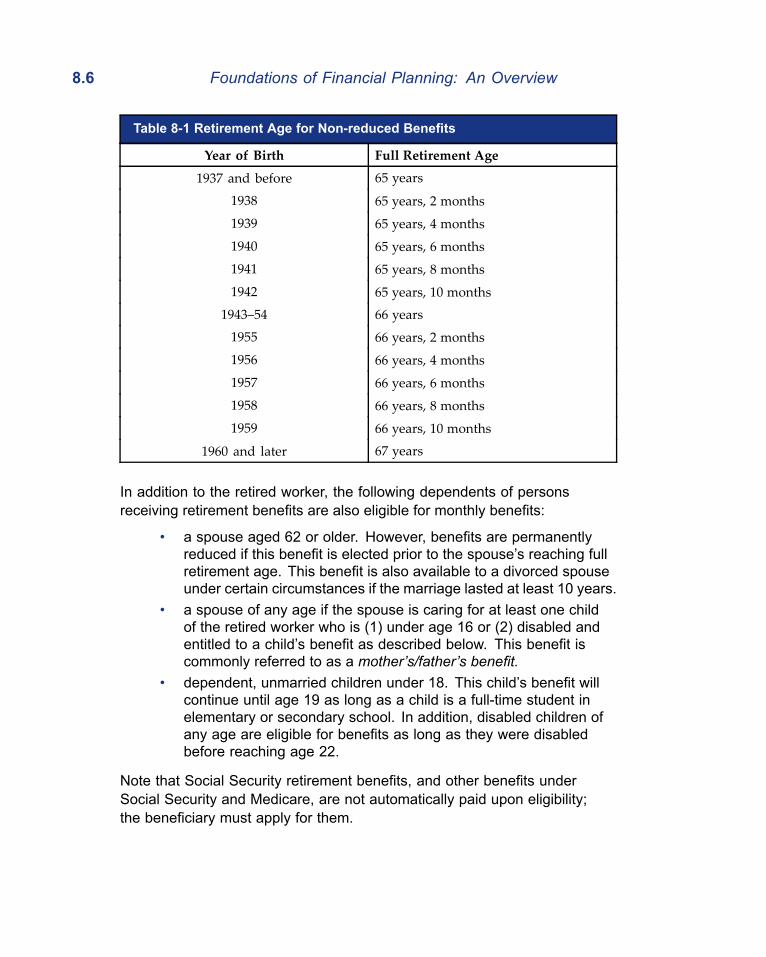

Eligibility for Social Security ..................................................... 8.4Fully Insured ....................................................................... 8.4Currently Insured ................................................................ 8.4Disability Insured................................................................. 8.5

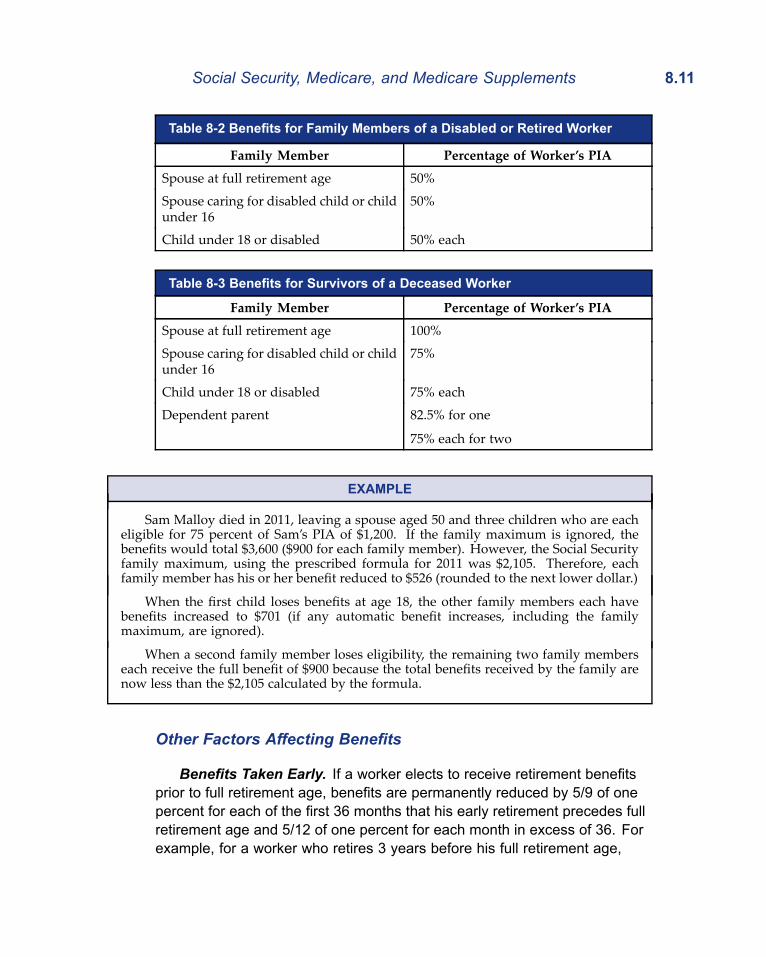

Social Security Benefits............................................................ 8.5Retirement Benefits ............................................................ 8.5Survivors Benefits ............................................................... 8.7Disability Benefits................................................................ 8.8Eligibility for Dual Benefits .................................................. 8.8Termination of Benefits ....................................................... 8.9

Social Security Benefit Amounts ............................................ 8.10Calculating Benefits .......................................................... 8.10Other Factors Affecting Benefits ....................................... 8.11

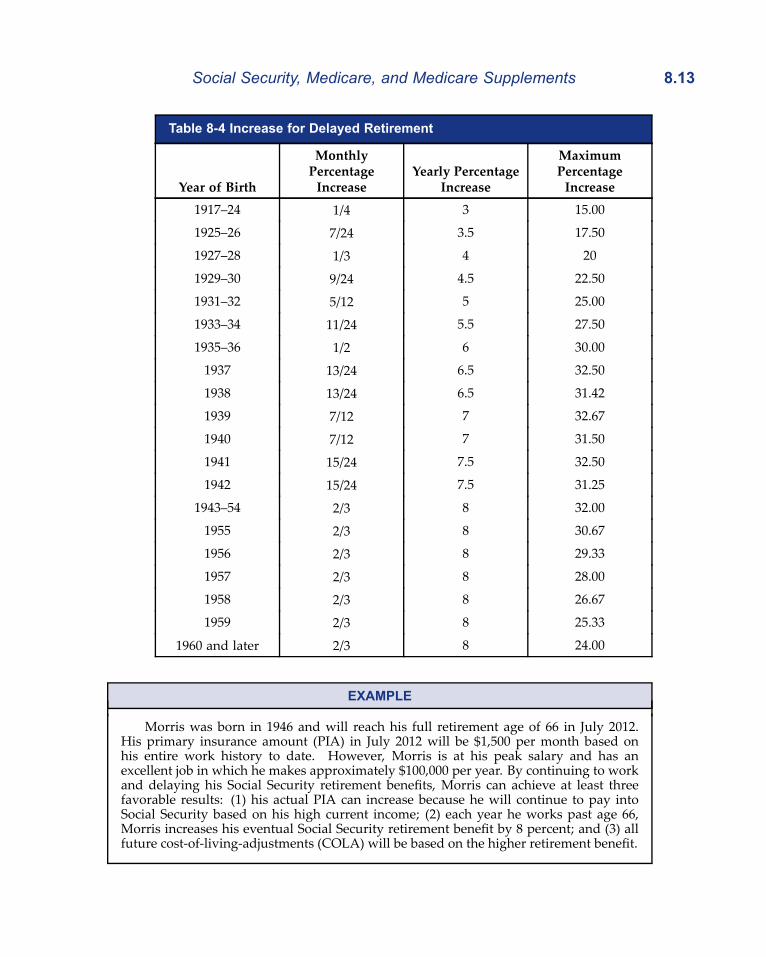

Benefits Taken Early.................................................... 8.11Delayed Retirement..................................................... 8.12Earnings Test............................................................... 8.14Cost-of-Living Adjustments.......................................... 8.15Offset for Other Benefits.............................................. 8.15

Requesting Benefit Information......................................... 8.16Eligibility for Medicare ............................................................ 8.16Medicare Part A: Hospital Benefits......................................... 8.18

Hospital Benefits ............................................................... 8.18Skilled-Nursing Facility Benefits........................................ 8.20Home Health Care Benefits .............................................. 8.21Hospice Benefits ............................................................... 8.21Exclusions......................................................................... 8.22

Medicare Part B Benefits........................................................ 8.23Benefits ............................................................................. 8.23Exclusions......................................................................... 8.24

Foundations of Financial Planning: An Overview xix

Amount of Benefits............................................................ 8.24Medicare Part C ..................................................................... 8.26Medicare Part D Prescription Drug Plans .............................. 8.27

Coverage to Supplement Medicare................................................... 8.30Employer Plans to Supplement Medicare .............................. 8.30Individual Medigap Policies to Supplement Medicare ............ 8.30

Basic Benefits ................................................................... 8.31Changes in Medigap Benefits ........................................... 8.32

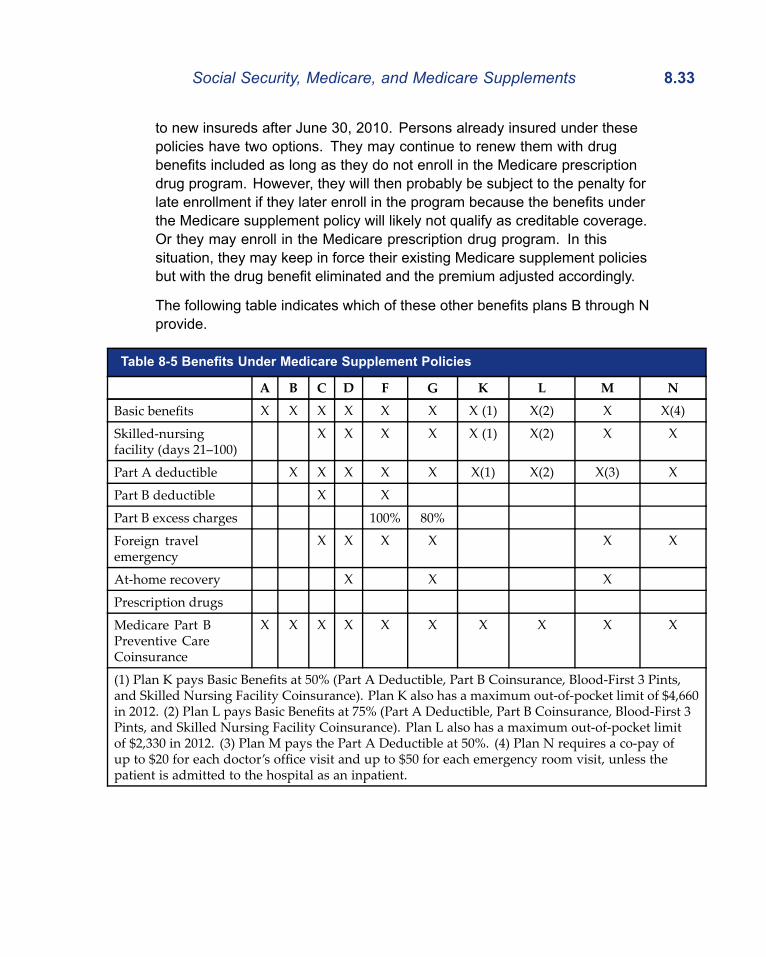

Additional Medicare Supplement Plan Benefits........... 8.32Eligibility ............................................................................ 8.34

Postscript .......................................................................................... 8.34Chapter Review................................................................................. 8.35

Review Questions .................................................................. 8.35

APPENDICES

Answers to Questions....................................................................... A.1

Bibliography....................................................................................... B.1

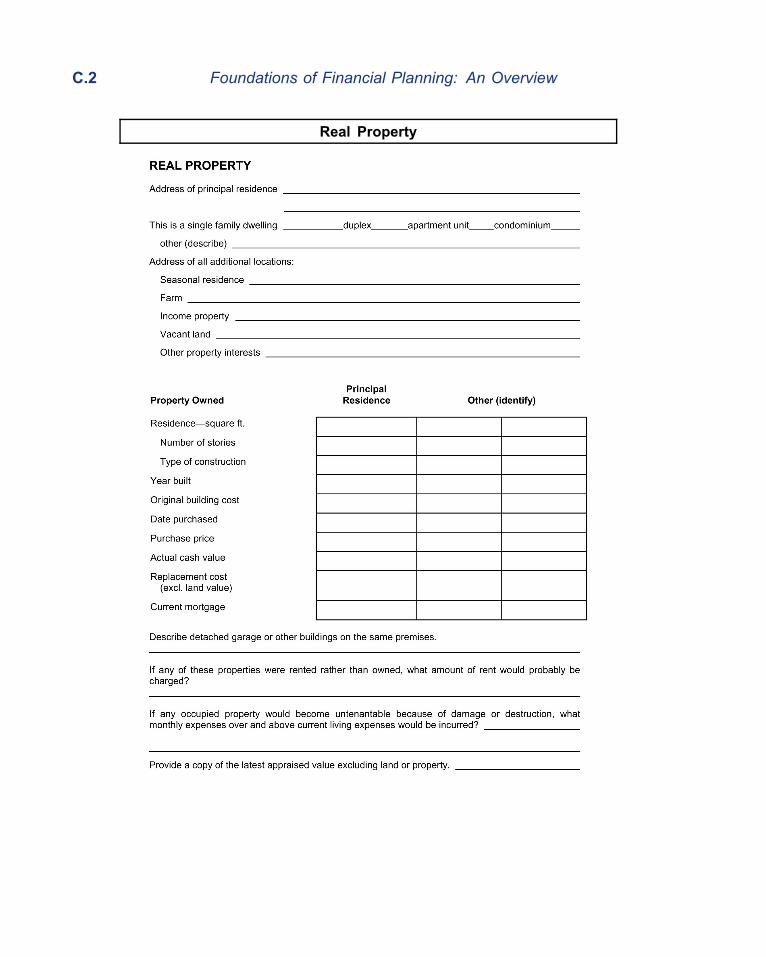

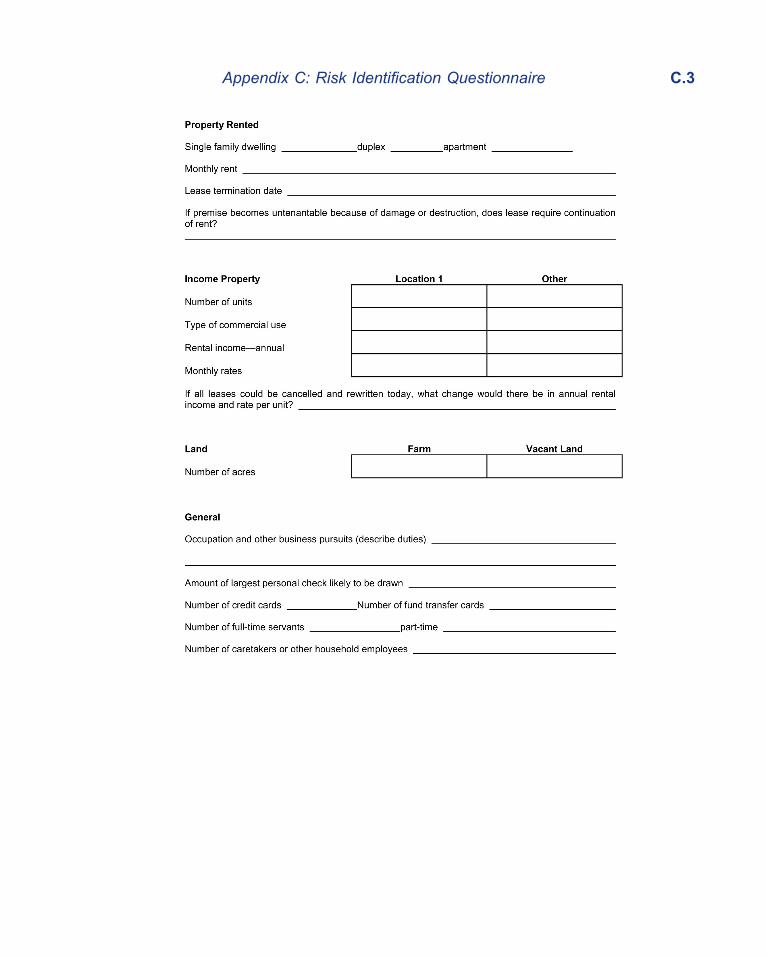

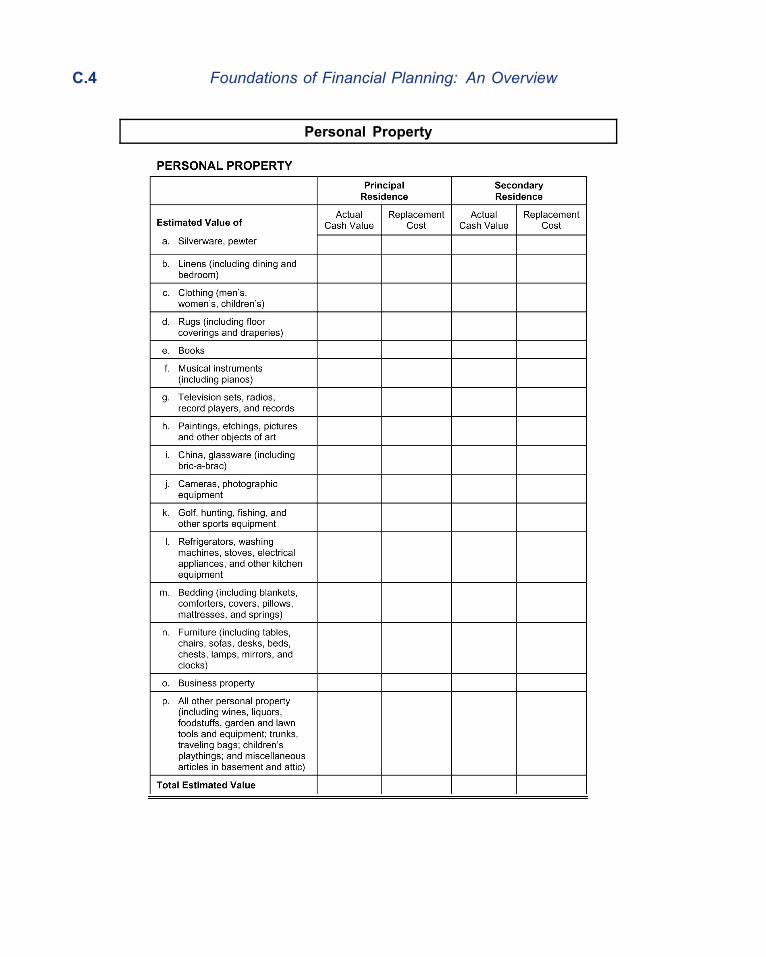

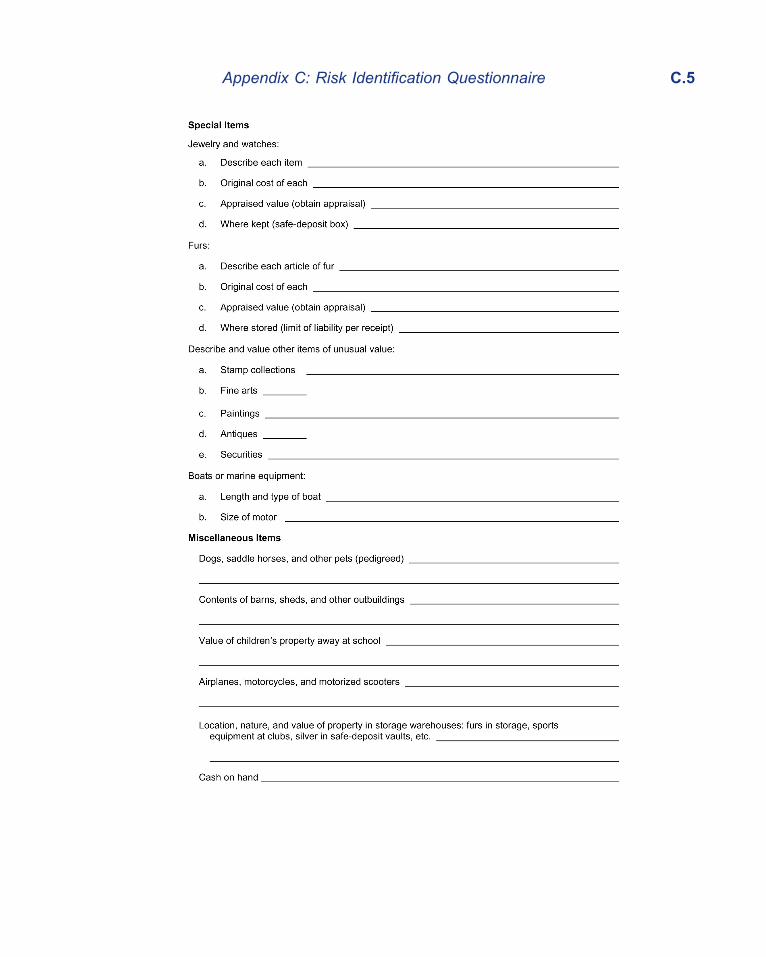

Risk Identification Questionnaire .................................................... C.1

Glossary .....................................................................................Glossary.1

Index .................................................................................................Index.1

ACKNOWLEDGMENTS

Publication of this book required the collaborative efforts of the author as well asmany other individuals. I am especially grateful to Todd Denton and Jane Hassingerfor their outstanding production assistance. I also want to acknowledge Emily Schu’senthusiastic and competent technical help. I appreciate the following individuals whocontributed so much in the past while authoring or editing portions of the content ofthis book:

• Dr. Walt Woerheide, ChFC®, CFP®, Vice President of Academic Affairs,Dean, Professor of Investments, and holder of the Frank M. EngleDistinguished Chair in Economic Research at The American College.

• Theodore T. (Ted) Kurlowicz, JD, LLM, CAP®, ChFC®, CLU®, AEP,Charles E. Drimal Professor in Estate Planning, Professor of Taxation atThe American College.

• Connie Fontaine, JD, LLM, ChFC®, CLU®, Larry R. Pike Chair inInsurance and Investments, Associate Professor of Taxation at TheAmerican College.

• Christopher P. Woehrle, JD, LLM, Assistant Professor of Taxation at TheAmerican College.

Other past faculty members at The American College also contributed significantly,especially C. Bruce Worsham, JD, and Burton T. (Tom) Beam, ChFC®, CLU®,CPCU, CASL®. I am in debt to all who went before me.

It is foolish to believe that any book is perfect. Please take some time to give meyour constructive comments on how to improve future editions. As a motivation,remember that readers may someday be advising you and your family aboutfinancial planning!

Allen McLellan, The American College, Bryn Mawr, PA.

xxi

ABOUT THE AUTHOR

Allen C. McLellan, LUTCF, CLU, ChFC, CASL,CFP, is an Assistant Professor of Insurance at TheAmerican College. Allen graduated from the UnitedStates Air Force Academy with a BS in aeronauticalengineering. As an Air Force officer, Allen served as anavigator on several types of aircraft and completedthree professional development programs in residence:Squadron Officer School, Air Command and StaffCollege, and The Air War College. In 1984, he wasawarded the Secretary of the Air Force LeadershipAward as the top graduate in his Air Command and StaffCollege. Allen completed a MS in Aeronautics at the AirForce Institute of Technology and taught mathematicsat the Air Force Academy for four years, where he alsoserved as an instructor in the Academy’s navigationprogram. After Allen retired from the Air Force, heentered the financial services field and worked nearly16 years as an agent, registered representative, andfinancial planner. Much of his practice was focusedon senior issues such as Medicare, Medicaid, andlong-term care needs.Allen was active in the Life Underwriters Association(now the National Association of Insurance andFinancial Advisors) and served as president of hislocal association in Montgomery, AL. He was namedthe “Life Underwriter of the Year” by the Montgomeryassociation in 1999. At The American College, Allen isprincipal editor of Foundations of Financial Planning:An Overview, Foundations of Financial Planning: TheProcess, Foundations of Investment Planning, andHealth and Long-Term Care for Seniors. Allen is amember of NAIFA, the Air Force Association, and theMilitary Officers Association of America.

xxiii

SPECIAL NOTES TO ADVISORS

This publication is designed to provide accurate and authoritative information aboutthe subject covered. While every precaution has been taken in the preparation of thismaterial to insure that it is both accurate and up-to-date, it is still possible that someerrors eluded detection. Moreover, some material may become inaccurate and/oroutdated either because it is time sensitive or because new legislation will make it so.Still other material may be viewed as inaccurate because your company's productsand procedures are different from those described in the book. Therefore, the editor,authors, and The American College assume no liability for damages resulting fromthe use of the information contained in this book. The American College is notengaged in rendering legal, accounting, or other professional advice. If legal orother expert advice is required, the services of an appropriate professional shouldbe sought.

Caution Regarding Use of Text Materials: Any illustrations, fact finders,techniques, and/or approaches contained in this book are not to be used with thepublic unless you have obtained approval from your company. Your company'sgeneral support of The American College's educational programs and publicationsdoes not constitute blanket approval of any illustrations, fact finders, techniques,and/or approaches presented in this book, unless so communicated in writing byyour company.

Use of the term "Financial Advisor" as it appears in this book is intended as thegeneric reference to professional members of our reading audience. It is usedinterchangeably with the term "Advisor" so as to avoid unnecessary redundancy.Financial Advisor takes the place of the following terms:

Account Executive

Agent

Associate

Broker (stock or insurance)

Employee Benefit Specialist

Estate Planner

Financial Consultant

Financial Planner

Financial PlanningProfessional

Financial ServicesProfessional

Health Underwriter

Insurance Professional

Life Insurance Agent

Life Underwriter

Planner

Practitioner

Producer

Property & Casualty Agent

Registered InvestmentAdviser

Registered Representative

Retirement Planner

Senior Advisor

Tax Advisor

xxv

OVERVIEW OF THE BOOK

Foundations of Financial Planning: AnOverview is designed to be an overview of themajor planning components that make up a comprehensive financial plan. Althougheach of these components is covered in more depth in other American Collegepublications, this is the one College text where all these components are broughttogether to show what needs to be covered in a truly comprehensive financial plan.

NoteThis course is not part of The American College's LUTCF curriculum. It is arequired course for the FSS designation.

Chapter 1 begins the discussion by explaining that financial planning is an eight-stepprocess that can involve a single-purpose, multiple-purpose, or comprehensiveapproach, with the focus being on the later. The content of a comprehensivefinancial plan should include a discussion of each of the major planning areas.Priority given to a client’s goals in financial planning is strongly influenced by whichphase of the life cycle the client is experiencing. Financial planning is a processthat should be ongoing throughout the client's financial life.

Chapters 2 through 7 introduce the major planning components that make upcomprehensive financial planning. Chapter 2 discusses insurance planning,including the risk management process and insurance coverages. Chapter 3examines employee benefits planning, since many of the financial needs of a clientand her family may be met—or at least partially met—with benefits provided byand/or through an employer. Chapter 4 is an introduction to investment planning.It describes basic risk/return concepts, financial risk tolerance, asset allocationmodels, categories of investments, and several portfolio considerations. In chapter5, basic concepts of income taxation are presented with an emphasis on taxplanning. In chapter 6, retirement planning concepts are addressed, includingretirement income needs and the types of retirement plans available. Chapter 7covers estate planning, the final major planning area. The chapter 7 discussionfocuses on preserving the client's wealth for his family.

Although the Social Security and Medicare programs could have been covered inearlier chapters as subparts of one of the major planning areas, they are dealt withseparately in chapter 8 because of their importance as the foundation upon whichthe client's comprehensive financial plan should be built. The last part of chapter8 is devoted to explaining the various types of coverages designed to supplementMedicare.

xxvii

xxviii Foundations of Financial Planning: An Overview

Just a word on the author’s writing style. Throughout the text, I will alternate betweenusing “he/him/his” and “she/her/hers.” In my view, this eliminates the awkward styleof referring to “his or her,” “him or her,” and “his or hers,” and allows the text to flowmore naturally.

It is certainly our hope that this course will motivate students to seek more educationfrom The American College or elsewhere. Financial planning is a complicatedand ever-changing discipline. To serve well as a financial advisor will require yourdedication toward life-long learning to stay current and help your clients surviveand thrive in a complex environment.

1

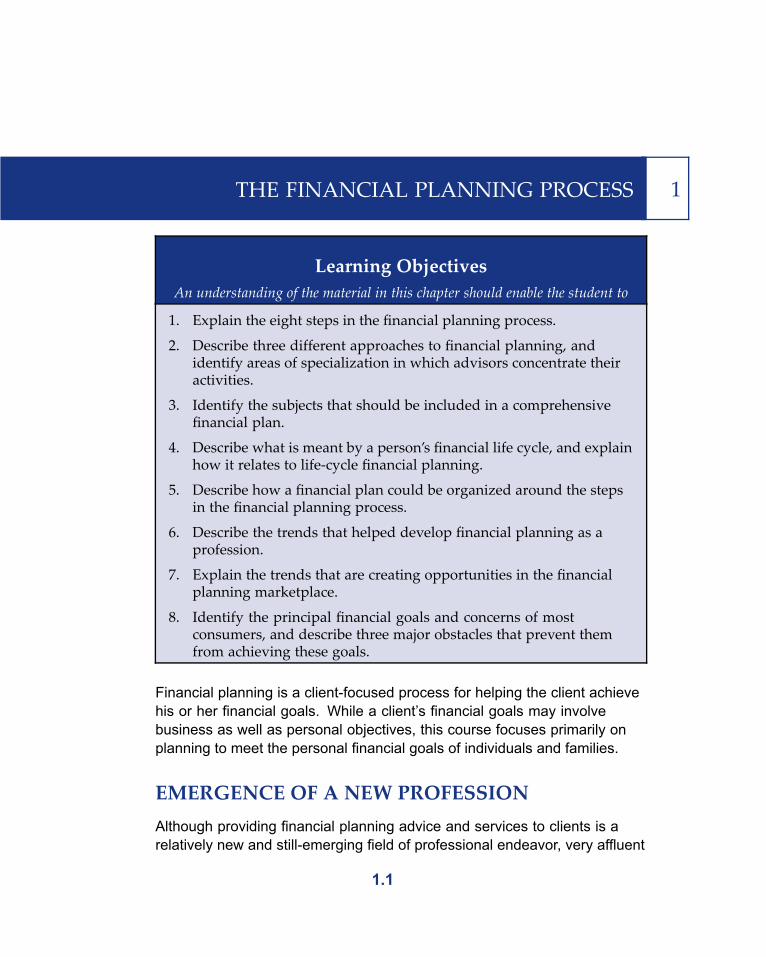

THE FINANCIAL PLANNING PROCESS 1

Learning ObjectivesAn understanding of the material in this chapter should enable the student to

1. Explain the eight steps in the financial planning process.

2. Describe three different approaches to financial planning, andidentify areas of specialization in which advisors concentrate theiractivities.

3. Identify the subjects that should be included in a comprehensivefinancial plan.

4. Describe what is meant by a person’s financial life cycle, and explainhow it relates to life-cycle financial planning.

5. Describe how a financial plan could be organized around the stepsin the financial planning process.

6. Describe the trends that helped develop financial planning as aprofession.

7. Explain the trends that are creating opportunities in the financialplanning marketplace.

8. Identify the principal financial goals and concerns of mostconsumers, and describe three major obstacles that prevent themfrom achieving these goals.

Financial planning is a client-focused process for helping the client achievehis or her financial goals. While a client’s financial goals may involvebusiness as well as personal objectives, this course focuses primarily onplanning to meet the personal financial goals of individuals and families.

EMERGENCE OF A NEW PROFESSIONAlthough providing financial planning advice and services to clients is arelatively new and still-emerging field of professional endeavor, very affluent

1.1

1.2 Foundations of Financial Planning: An Overview

individuals have had access to such help for many years. Moreover, somefinancial advisors, such as accountants and life insurance agents, arguethat they have been practicing financial planning all their professional lives.However, it is generally recognized that financial planning services that covera spectrum of client concerns have become available to most Americans inthe middle- and upper-middle-income brackets only in the past 40 to 45 years.

Financial advisors claiming to be practicing financial planning first appearedin numbers in the late 1960s, a period of rising inflation and interest rates.The financial planning movement grew rapidly during the 1970s as thegeneral trend of prices continued upward. By the late 1970s and into the early1980s, inflation and interest rates were virtually out of control. Confrontedwith very high income tax rates along with spiraling inflation and interestrates, American consumers clamored for help. The growth of the financialplanning movement was explosive. Often, however, what advisors labeled asfinancial planning consisted mostly of selling “get rich quick” products andelaborate income tax dodges, usually accompanied by an abundance of“hype.” A few advisors, sometimes with great zeal, preached the message ofcomprehensive financial planning as the financial salvation of the Americanhousehold.

By the mid-1980s, much of the turbulence in economic conditions began tosettle down. In addition, when income tax reform eliminated the most extremetypes of tax shelters from the marketplace, many so-called financial planningadvisors disappeared from the scene. Many advocates of a comprehensiveapproach to financial planning realized that this type of financial planning waspractical for only a small, affluent clientele, especially on a fee-for-servicebasis. Also, with the oldest members of the “baby boom” generation enteringtheir 40s, retirement planning became an increasingly important componentof financial planning practices.

In the 1990s, the financial planning profession gained some stability andmaturity. Today, it is possible to describe more realistically what financialplanning is and what client needs it can fulfill.

In the second decade of the 21st century, financial planning is more widelyaccepted and many specialized planning areas have developed. Today,financial planners specialize in education planning, divorce planning, incomedistribution and a number of other specialties. While this course does notprepare you to take the exam for the CFP® designation, we include thedescriptions of financial planning and the steps in the financial planningprocess followed by Certified Financial Planner® professionals. Our belief is

The Financial Planning Process 1.3

that other advisors like our students who may not hold the designation canbenefit significantly from the recommendations and procedures followedby CFP® designees.

WHAT IS FINANCIAL PLANNING?financial planning One factor that has hampered the development of financial

planning as a discipline and profession is that there hasbeen very little agreement among advisors as to what defines it. Indeed,there are as many definitions of financial planning as there are people whobelieve they are engaged in it. This debate, which continues among financialadvisors even today,1 is not merely an exercise in semantics. The discussionbecomes intensely practical when questions are raised about such issues aswho shall regulate those advisors engaged in financial planning, who shallset standards for the financial planning profession and how those advisorsshould be regulated and compensated.

The Securities and Exchange Commission (SEC) defines financial planningby outcome: “Financial planning can help assess every aspect of yourfinancial life—including saving, investments, insurance, taxes, retirement,and estate planning.”2 The Financial Planning Association (FPA), one offinancial planning’s largest member and advocate groups, defines financialplanning as “the long-term process of wisely managing your finances so youcan achieve your goals and dreams.”3 Definitions of financial planning varyacross the industry, yet common themes emerge. Financial planning is aprocess performed by professionals with training and expertise. Financialplanners span compensation models (some are fee-based, some paidon the sale of products, and some receive both fees and commissions),backgrounds (traditional college track or a career-changing professional),and specializations.

1. Shelley A. Lee, “What Is Financial Planning, Anyway?” Journal of Financial Planning, December

2001, pp. 36–46.

2. www.sec.gov/answers/finplan.htm.

3. Financial Planning Association — What is Financial Planning? accessed on

www.fpanet.org/Whatisfinancialplanning.

1.4 Foundations of Financial Planning: An Overview

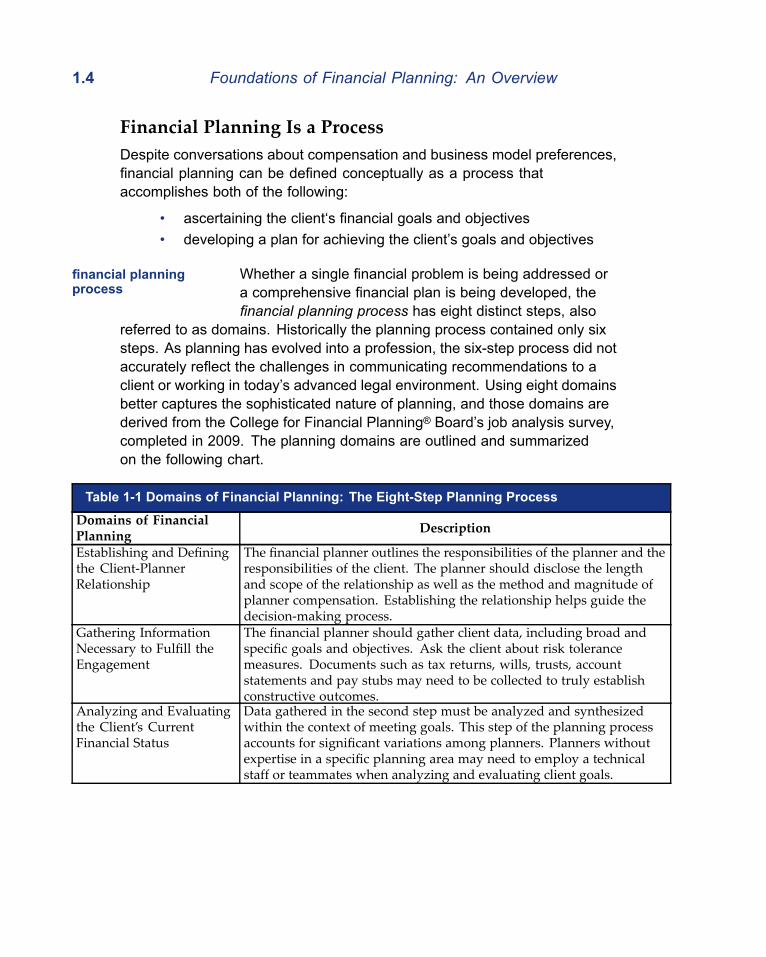

Financial Planning Is a ProcessDespite conversations about compensation and business model preferences,financial planning can be defined conceptually as a process thataccomplishes both of the following:

• ascertaining the client‘s financial goals and objectives• developing a plan for achieving the client’s goals and objectives

financial planningprocess

Whether a single financial problem is being addressed ora comprehensive financial plan is being developed, thefinancial planning process has eight distinct steps, also

referred to as domains. Historically the planning process contained only sixsteps. As planning has evolved into a profession, the six-step process did notaccurately reflect the challenges in communicating recommendations to aclient or working in today’s advanced legal environment. Using eight domainsbetter captures the sophisticated nature of planning, and those domains arederived from the College for Financial Planning® Board’s job analysis survey,completed in 2009. The planning domains are outlined and summarizedon the following chart.

Table 1-1 Domains of Financial Planning: The Eight-Step Planning Process

Domains of FinancialPlanning Description

Establishing and Definingthe Client-PlannerRelationship

The financial planner outlines the responsibilities of the planner and theresponsibilities of the client. The planner should disclose the lengthand scope of the relationship as well as the method and magnitude ofplanner compensation. Establishing the relationship helps guide thedecision-making process.

Gathering InformationNecessary to Fulfill theEngagement

The financial planner should gather client data, including broad andspecific goals and objectives. Ask the client about risk tolerancemeasures. Documents such as tax returns, wills, trusts, accountstatements and pay stubs may need to be collected to truly establishconstructive outcomes.

Analyzing and Evaluatingthe Client’s CurrentFinancial Status

Data gathered in the second step must be analyzed and synthesizedwithin the context of meeting goals. This step of the planning processaccounts for significant variations among planners. Planners withoutexpertise in a specific planning area may need to employ a technicalstaff or teammates when analyzing and evaluating client goals.

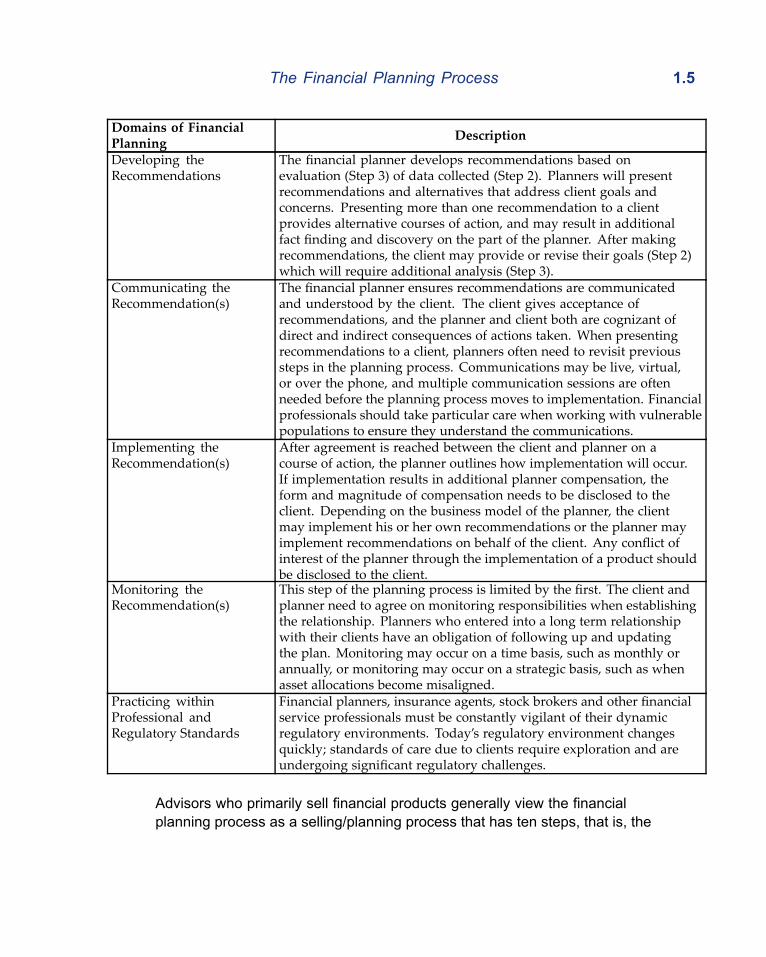

The Financial Planning Process 1.5

Domains of FinancialPlanning Description

Developing theRecommendations

The financial planner develops recommendations based onevaluation (Step 3) of data collected (Step 2). Planners will presentrecommendations and alternatives that address client goals andconcerns. Presenting more than one recommendation to a clientprovides alternative courses of action, and may result in additionalfact finding and discovery on the part of the planner. After makingrecommendations, the client may provide or revise their goals (Step 2)which will require additional analysis (Step 3).

Communicating theRecommendation(s)

The financial planner ensures recommendations are communicatedand understood by the client. The client gives acceptance ofrecommendations, and the planner and client both are cognizant ofdirect and indirect consequences of actions taken. When presentingrecommendations to a client, planners often need to revisit previoussteps in the planning process. Communications may be live, virtual,or over the phone, and multiple communication sessions are oftenneeded before the planning process moves to implementation. Financialprofessionals should take particular care when working with vulnerablepopulations to ensure they understand the communications.

Implementing theRecommendation(s)

After agreement is reached between the client and planner on acourse of action, the planner outlines how implementation will occur.If implementation results in additional planner compensation, theform and magnitude of compensation needs to be disclosed to theclient. Depending on the business model of the planner, the clientmay implement his or her own recommendations or the planner mayimplement recommendations on behalf of the client. Any conflict ofinterest of the planner through the implementation of a product shouldbe disclosed to the client.

Monitoring theRecommendation(s)

This step of the planning process is limited by the first. The client andplanner need to agree on monitoring responsibilities when establishingthe relationship. Planners who entered into a long term relationshipwith their clients have an obligation of following up and updatingthe plan. Monitoring may occur on a time basis, such as monthly orannually, or monitoring may occur on a strategic basis, such as whenasset allocations become misaligned.

Practicing withinProfessional andRegulatory Standards

Financial planners, insurance agents, stock brokers and other financialservice professionals must be constantly vigilant of their dynamicregulatory environments. Today’s regulatory environment changesquickly; standards of care due to clients require exploration and areundergoing significant regulatory challenges.

Advisors who primarily sell financial products generally view the financialplanning process as a selling/planning process that has ten steps, that is, the

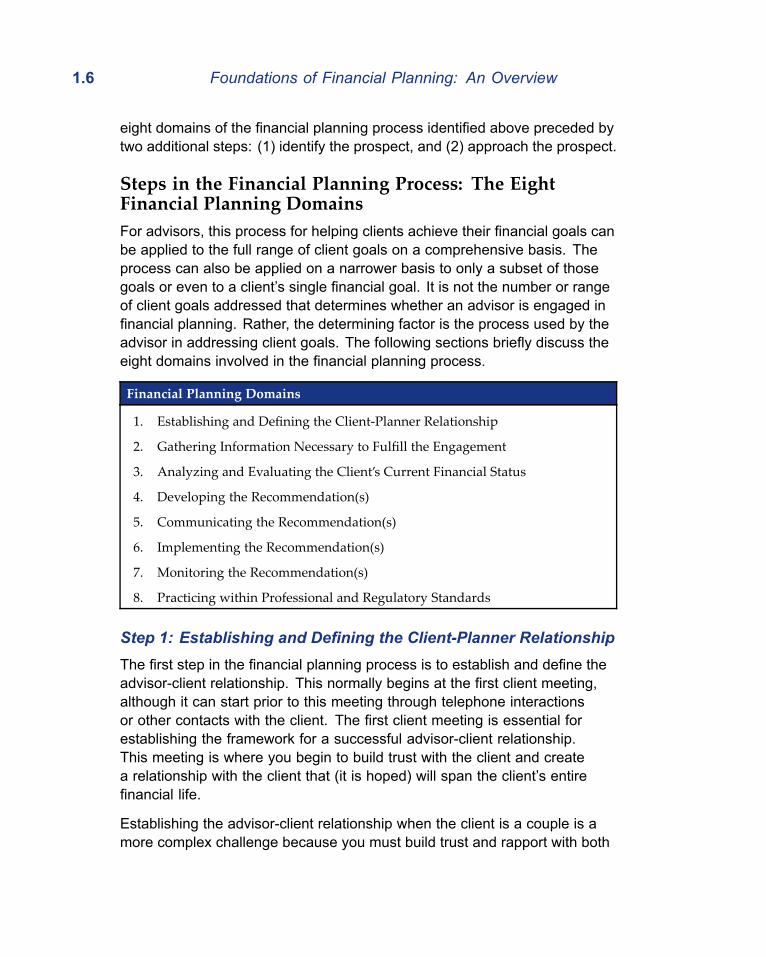

1.6 Foundations of Financial Planning: An Overview

eight domains of the financial planning process identified above preceded bytwo additional steps: (1) identify the prospect, and (2) approach the prospect.

Steps in the Financial Planning Process: The EightFinancial Planning DomainsFor advisors, this process for helping clients achieve their financial goals canbe applied to the full range of client goals on a comprehensive basis. Theprocess can also be applied on a narrower basis to only a subset of thosegoals or even to a client’s single financial goal. It is not the number or rangeof client goals addressed that determines whether an advisor is engaged infinancial planning. Rather, the determining factor is the process used by theadvisor in addressing client goals. The following sections briefly discuss theeight domains involved in the financial planning process.

Financial Planning Domains

1. Establishing and Defining the Client-Planner Relationship

2. Gathering Information Necessary to Fulfill the Engagement

3. Analyzing and Evaluating the Client’s Current Financial Status

4. Developing the Recommendation(s)

5. Communicating the Recommendation(s)

6. Implementing the Recommendation(s)

7. Monitoring the Recommendation(s)

8. Practicing within Professional and Regulatory Standards

Step 1: Establishing and Defining the Client-Planner RelationshipThe first step in the financial planning process is to establish and define theadvisor-client relationship. This normally begins at the first client meeting,although it can start prior to this meeting through telephone interactionsor other contacts with the client. The first client meeting is essential forestablishing the framework for a successful advisor-client relationship.This meeting is where you begin to build trust with the client and createa relationship with the client that (it is hoped) will span the client’s entirefinancial life.

Establishing the advisor-client relationship when the client is a couple is amore complex challenge because you must build trust and rapport with both

The Financial Planning Process 1.7

parties. Covering the goals of both parties in one financial plan requires youto completely understand the goals that both have in common and how thepartners’ needs may differ. Couples often have significantly different goals,priorities, risk tolerance or basic planning objectives. You must learn how tohelp couples negotiate through the planning process as a team, and in somesituations refer couples with vastly different interests to outside specialists.

EXAMPLE

Kirk is a financial planner in Philadelphia, PA. He recently met with Rick and CarolMarks, a married couple both age 42, who were referred to Kirk by another client. InKirk’s first meeting with Rick and Carol, they completed an extensive fact-finder and Kirkdiscovered the following:

• Rick has a very high financial risk tolerance and prefers investments, such assmall-cap stocks and emerging markets, which have the potential for highestreturns but are generally very volatile. Rick’s 401(k) suffered a 40 percentdecline in 2008–2009, but it has gained back most of that loss in 2010–2011.

• Carol’s father lost a small fortune in the stock market in 2001 when the“dot-com” market imploded. As a result, Carol is extremely fearful ofinvesting in any asset in which she can “lose her principal.” Carol’s entire401(k) is invested in a “stable value fund” that has averaged a 3.0 percentreturn over the last three years.

• Rick’s primary objective is rapid accumulation of funds so that they both canretire by age 58 and buy a condo in Florida.

• Carol’s top concern is to fund the education of their twins, Eric and Shelley,age 12. Carol wants to send both children to an Ivy League university, if theycan qualify. She is willing to work much longer, if necessary, to provide a topeducation for the children.

Note that with such widely different objectives and risk tolerances, Kirk’s job iscomplicated in building a financial plan that harmonizes the interests and attitudes ofboth Rick and Carol.

structuring In any kind of planned and purposeful communicationsetting, the first element that needs attention is

structuring. Structuring determines both the format and subject matter ofthe interaction—in our case, between you and the client(s). Your task instructuring is to make the purpose of the initial meeting and those that followclear to the client at the outset of the relationship. Structuring includes theinevitable introductions, an explanation of the financial planning process,a discussion of forms used (for example, a fact-finder form, risk tolerance

1.8 Foundations of Financial Planning: An Overview

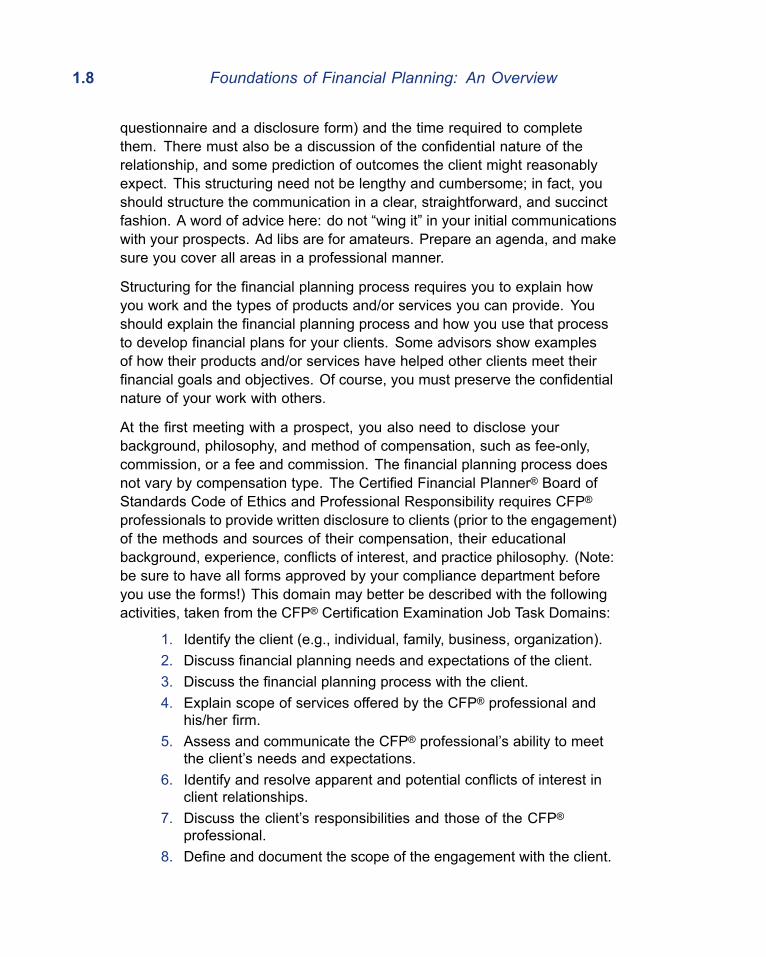

questionnaire and a disclosure form) and the time required to completethem. There must also be a discussion of the confidential nature of therelationship, and some prediction of outcomes the client might reasonablyexpect. This structuring need not be lengthy and cumbersome; in fact, youshould structure the communication in a clear, straightforward, and succinctfashion. A word of advice here: do not “wing it” in your initial communicationswith your prospects. Ad libs are for amateurs. Prepare an agenda, and makesure you cover all areas in a professional manner.

Structuring for the financial planning process requires you to explain howyou work and the types of products and/or services you can provide. Youshould explain the financial planning process and how you use that processto develop financial plans for your clients. Some advisors show examplesof how their products and/or services have helped other clients meet theirfinancial goals and objectives. Of course, you must preserve the confidentialnature of your work with others.

At the first meeting with a prospect, you also need to disclose yourbackground, philosophy, and method of compensation, such as fee-only,commission, or a fee and commission. The financial planning process doesnot vary by compensation type. The Certified Financial Planner® Board ofStandards Code of Ethics and Professional Responsibility requires CFP®

professionals to provide written disclosure to clients (prior to the engagement)of the methods and sources of their compensation, their educationalbackground, experience, conflicts of interest, and practice philosophy. (Note:be sure to have all forms approved by your compliance department beforeyou use the forms!) This domain may better be described with the followingactivities, taken from the CFP® Certification Examination Job Task Domains:

1. Identify the client (e.g., individual, family, business, organization).2. Discuss financial planning needs and expectations of the client.3. Discuss the financial planning process with the client.4. Explain scope of services offered by the CFP® professional and

his/her firm.5. Assess and communicate the CFP® professional’s ability to meet

the client’s needs and expectations.6. Identify and resolve apparent and potential conflicts of interest in

client relationships.7. Discuss the client’s responsibilities and those of the CFP®

professional.8. Define and document the scope of the engagement with the client.

The Financial Planning Process 1.9

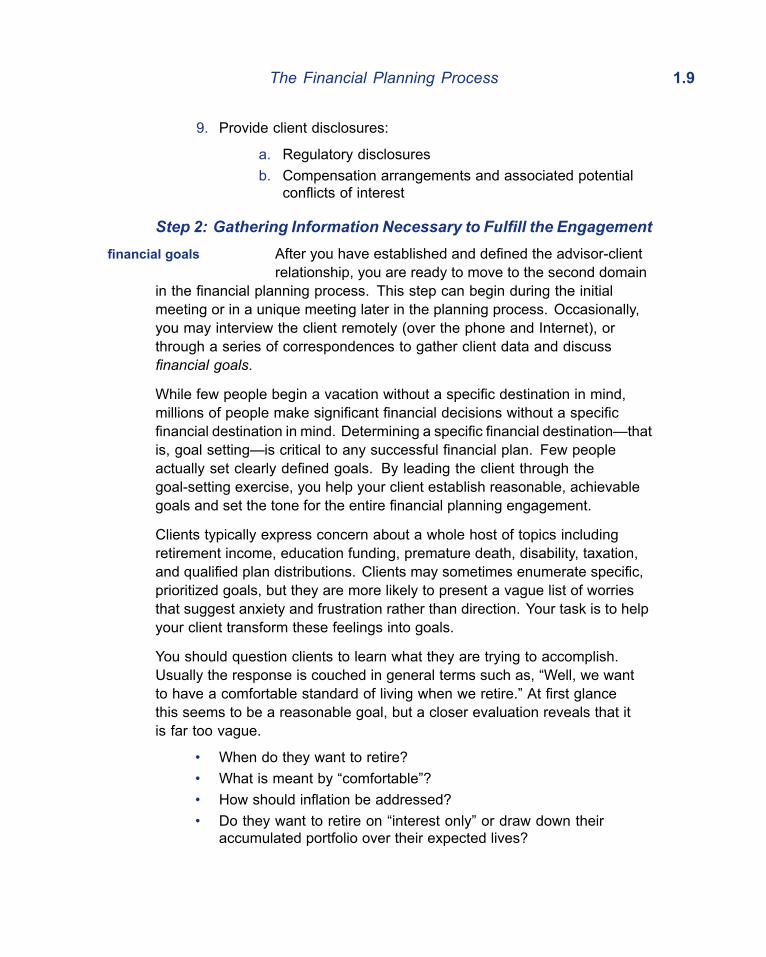

9. Provide client disclosures:

a. Regulatory disclosuresb. Compensation arrangements and associated potential

conflicts of interest

Step 2: Gathering Information Necessary to Fulfill the Engagementfinancial goals After you have established and defined the advisor-client

relationship, you are ready to move to the second domainin the financial planning process. This step can begin during the initialmeeting or in a unique meeting later in the planning process. Occasionally,you may interview the client remotely (over the phone and Internet), orthrough a series of correspondences to gather client data and discussfinancial goals.

While few people begin a vacation without a specific destination in mind,millions of people make significant financial decisions without a specificfinancial destination in mind. Determining a specific financial destination—thatis, goal setting—is critical to any successful financial plan. Few peopleactually set clearly defined goals. By leading the client through thegoal-setting exercise, you help your client establish reasonable, achievablegoals and set the tone for the entire financial planning engagement.

Clients typically express concern about a whole host of topics includingretirement income, education funding, premature death, disability, taxation,and qualified plan distributions. Clients may sometimes enumerate specific,prioritized goals, but they are more likely to present a vague list of worriesthat suggest anxiety and frustration rather than direction. Your task is to helpyour client transform these feelings into goals.

You should question clients to learn what they are trying to accomplish.Usually the response is couched in general terms such as, “Well, we wantto have a comfortable standard of living when we retire.” At first glancethis seems to be a reasonable goal, but a closer evaluation reveals that itis far too vague.

• When do they want to retire?• What is meant by “comfortable”?• How should inflation be addressed?• Do they want to retire on “interest only” or draw down their

accumulated portfolio over their expected lives?

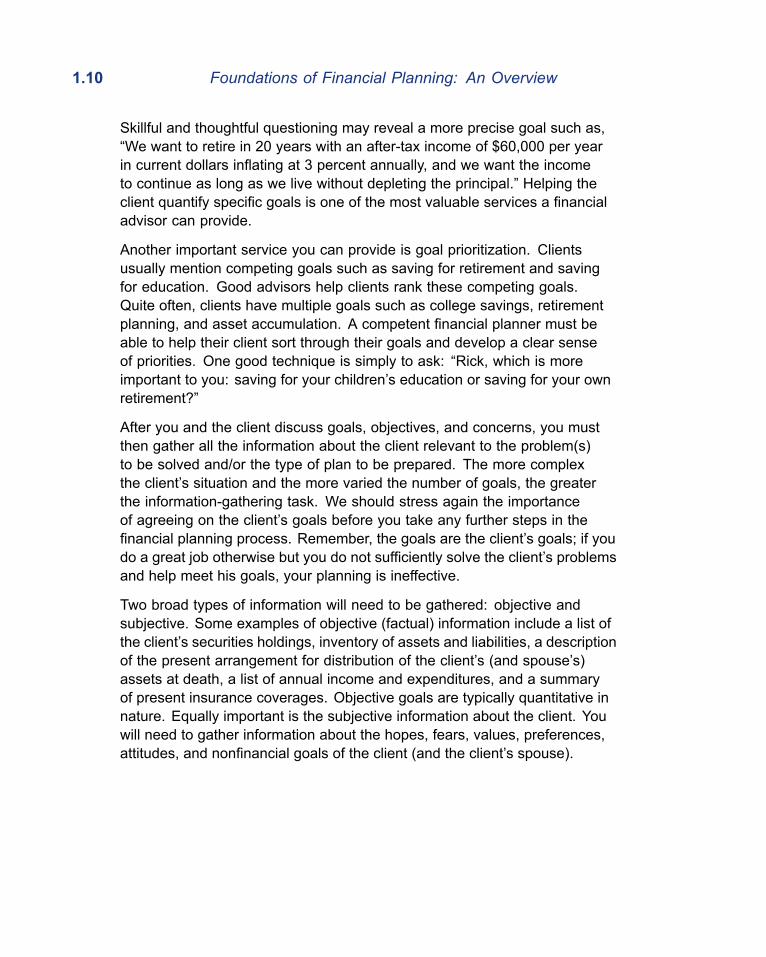

1.10 Foundations of Financial Planning: An Overview

Skillful and thoughtful questioning may reveal a more precise goal such as,“We want to retire in 20 years with an after-tax income of $60,000 per yearin current dollars inflating at 3 percent annually, and we want the incometo continue as long as we live without depleting the principal.” Helping theclient quantify specific goals is one of the most valuable services a financialadvisor can provide.