Embed Size (px)

Citation preview

www.smbcgroup.com Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

Harnessing private financing to Boost

Infrastructure

21 March 2017

10th Annual Meeting of the OECD Network of Senior PPP and Infrastructure officials

www.smbcgroup.com

Europe, Middle East & Africa

2

www.smbcgroup.com

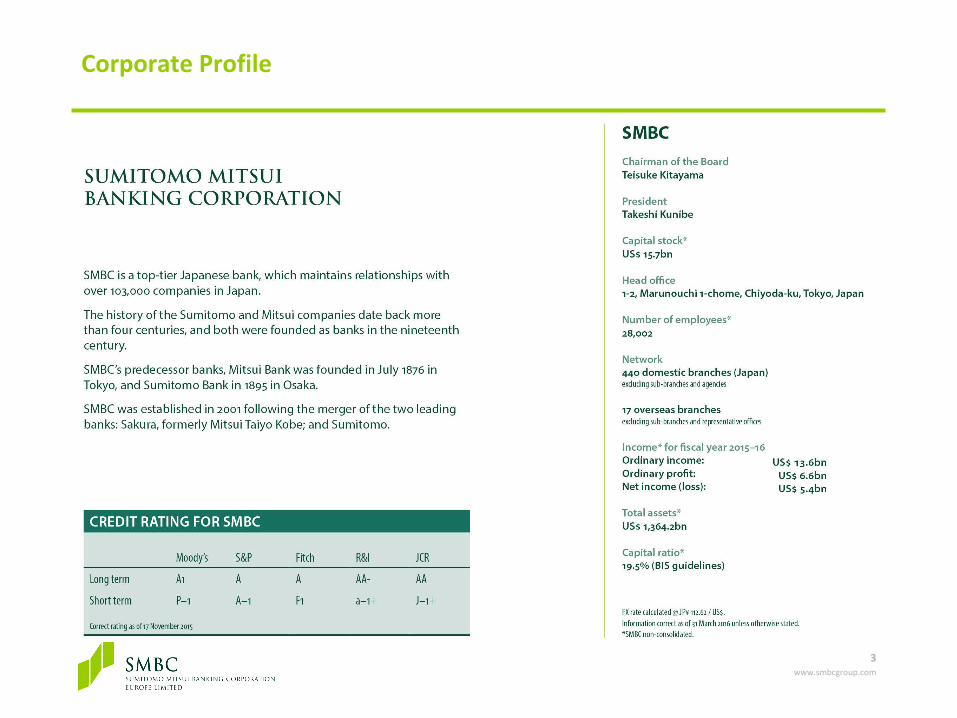

Corporate Profile

3

www.smbcgroup.com

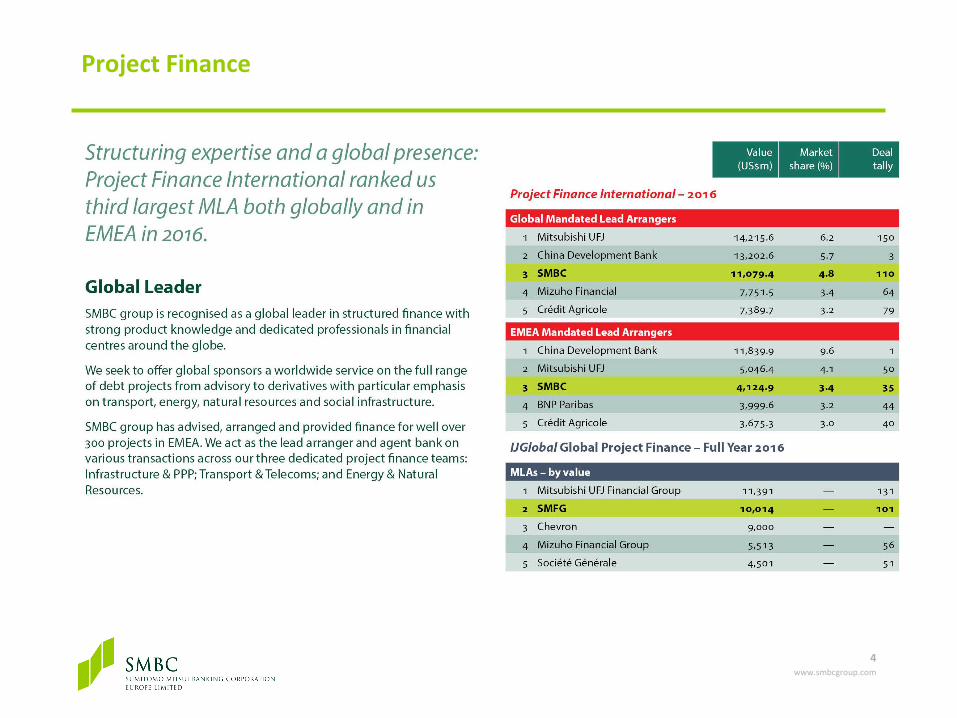

Project Finance

4

www.smbcgroup.com

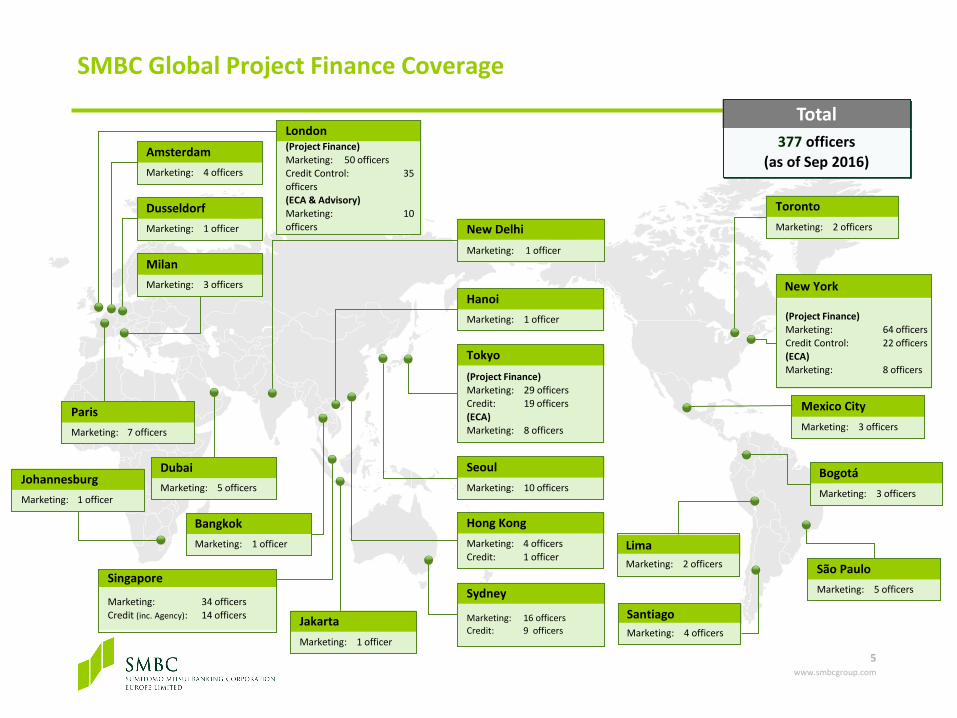

SMBC Global Project Finance Coverage

(Project Finance)

Marketing: 50 officers

Credit Control: 35

officers

(ECA & Advisory)

Marketing: 10

officers

London

Marketing: 1 officer

Johannesburg

Marketing: 4 officers

Amsterdam

Marketing: 1 officer

Dusseldorf

Marketing: 3 officers

Milan

Total

377 officers

(as of Sep 2016)

(Project Finance)

Marketing: 29 officers

Credit: 19 officers

(ECA)

Marketing: 8 officers

Tokyo

Marketing: 10 officers

Seoul

Marketing: 4 officers

Credit: 1 officer

Hong Kong

Marketing: 34 officers

Credit (inc. Agency): 14 officers

Singapore

Marketing: 1 officer

Jakarta Marketing: 16 officers

Credit: 9 officers

Sydney

Marketing: 1 officer

Hanoi

Marketing: 1 officer

Bangkok

Marketing: 1 officer

New Delhi

Marketing: 5 officers

Dubai

(Project Finance)

Marketing: 64 officers

Credit Control: 22 officers

(ECA)

Marketing: 8 officers

New York

Marketing: 3 officers

Mexico City

Marketing: 3 officers

Bogotá

Marketing: 5 officers

São Paulo

Lima

Marketing: 2 officers

Santiago

Marketing: 4 officers

Marketing: 2 officers

Toronto

Marketing: 7 officers

Paris

5

www.smbcgroup.com

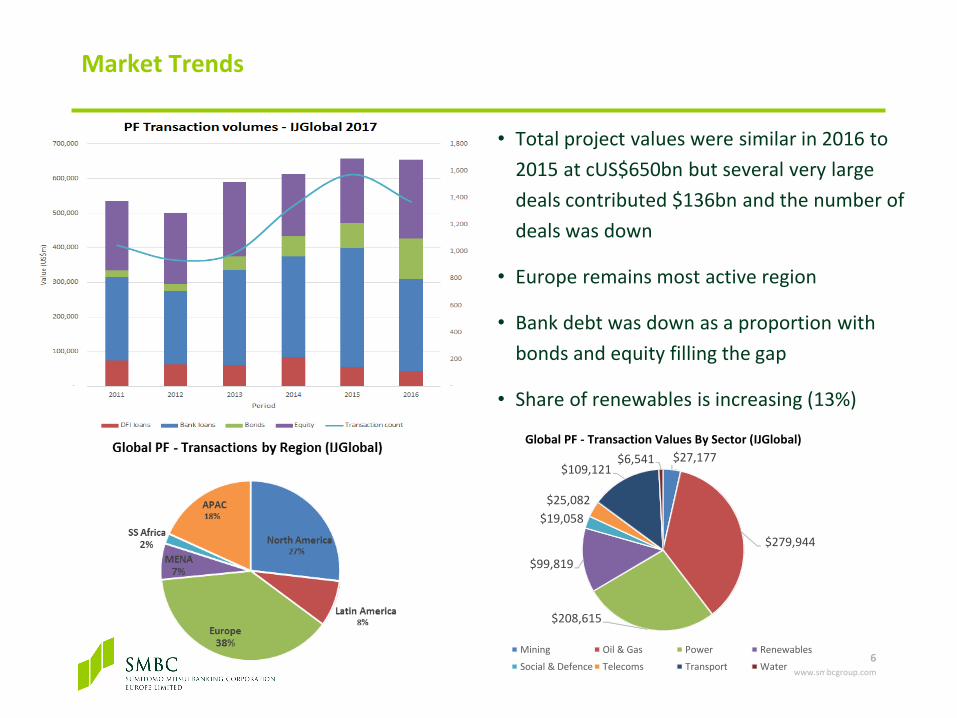

Market Trends

• Total project values were similar in 2016 to

2015 at cUS$650bn but several very large

deals contributed $136bn and the number of

deals was down

• Europe remains most active region

• Bank debt was down as a proportion with

bonds and equity filling the gap

• Share of renewables is increasing (13%)

6

$27,177

$279,944

$208,615

$99,819

$19,058

$25,082

$109,121 $6,541

Global PF - Transaction Values By Sector (IJGlobal)

Mining Oil & Gas Power Renewables

Social & Defence Telecoms Transport Water

www.smbcgroup.com

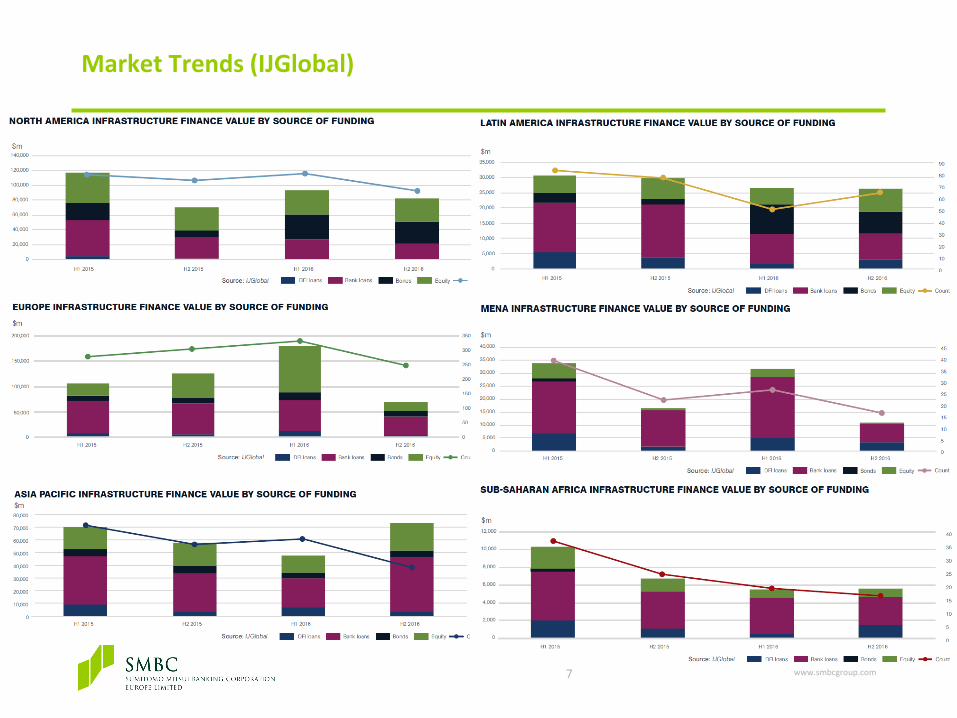

Market Trends (IJGlobal)

7

www.smbcgroup.com

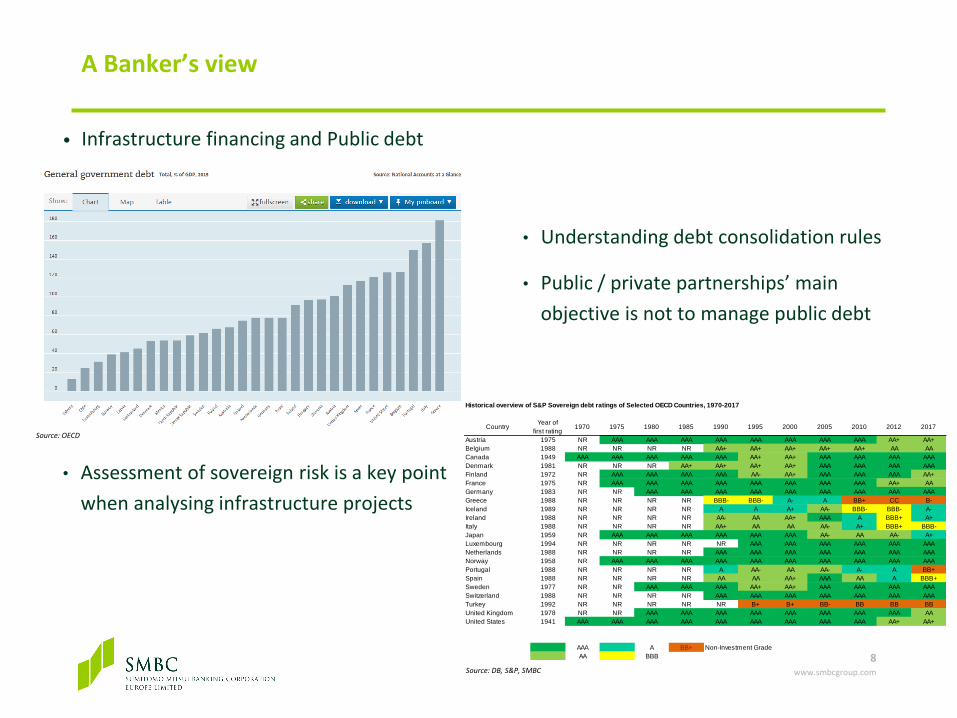

• Infrastructure financing and Public debt

8

Historical overview of S&P Sovereign debt ratings of Selected OECD Countries, 1970-2017

CountryYear of

first rating1970 1975 1980 1985 1990 1995 2000 2005 2010 2012 2017

Austria 1975 NR AAA AAA AAA AAA AAA AAA AAA AAA AA+ AA+

Belgium 1988 NR NR NR NR AA+ AA+ AA+ AA+ AA+ AA AA

Canada 1949 AAA AAA AAA AAA AAA AA+ AA+ AAA AAA AAA AAA

Denmark 1981 NR NR NR AA+ AA+ AA+ AA+ AAA AAA AAA AAA

Finland 1972 NR AAA AAA AAA AAA AA- AA+ AAA AAA AAA AA+

France 1975 NR AAA AAA AAA AAA AAA AAA AAA AAA AA+ AA

Germany 1983 NR NR AAA AAA AAA AAA AAA AAA AAA AAA AAA

Greece 1988 NR NR NR NR BBB- BBB- A- A BB+ CC B-

Iceland 1989 NR NR NR NR A A A+ AA- BBB- BBB- A-

Ireland 1988 NR NR NR NR AA- AA AA+ AAA A BBB+ A+

Italy 1988 NR NR NR NR AA+ AA AA AA- A+ BBB+ BBB-

Japan 1959 NR AAA AAA AAA AAA AAA AAA AA- AA AA- A+

Luxembourg 1994 NR NR NR NR NR AAA AAA AAA AAA AAA AAA

Netherlands 1988 NR NR NR NR AAA AAA AAA AAA AAA AAA AAA

Norway 1958 NR AAA AAA AAA AAA AAA AAA AAA AAA AAA AAA

Portugal 1988 NR NR NR NR A AA- AA AA- A- A BB+

Spain 1988 NR NR NR NR AA AA AA+ AAA AA A BBB+

Sweden 1977 NR NR AAA AAA AAA AA+ AA+ AAA AAA AAA AAA

Switzerland 1988 NR NR NR NR AAA AAA AAA AAA AAA AAA AAA

Turkey 1992 NR NR NR NR NR B+ B+ BB- BB BB BB

United Kingdom 1978 NR NR AAA AAA AAA AAA AAA AAA AAA AAA AA

United States 1941 AAA AAA AAA AAA AAA AAA AAA AAA AAA AA+ AA+

AAA A BB+ Non-Investment Grade

AA BBB Source: DB, S&P, SMBC

• Understanding debt consolidation rules

• Public / private partnerships’ main

objective is not to manage public debt

• Assessment of sovereign risk is a key point

when analysing infrastructure projects

Source: DB, S&P, SMBC

Source: OECD

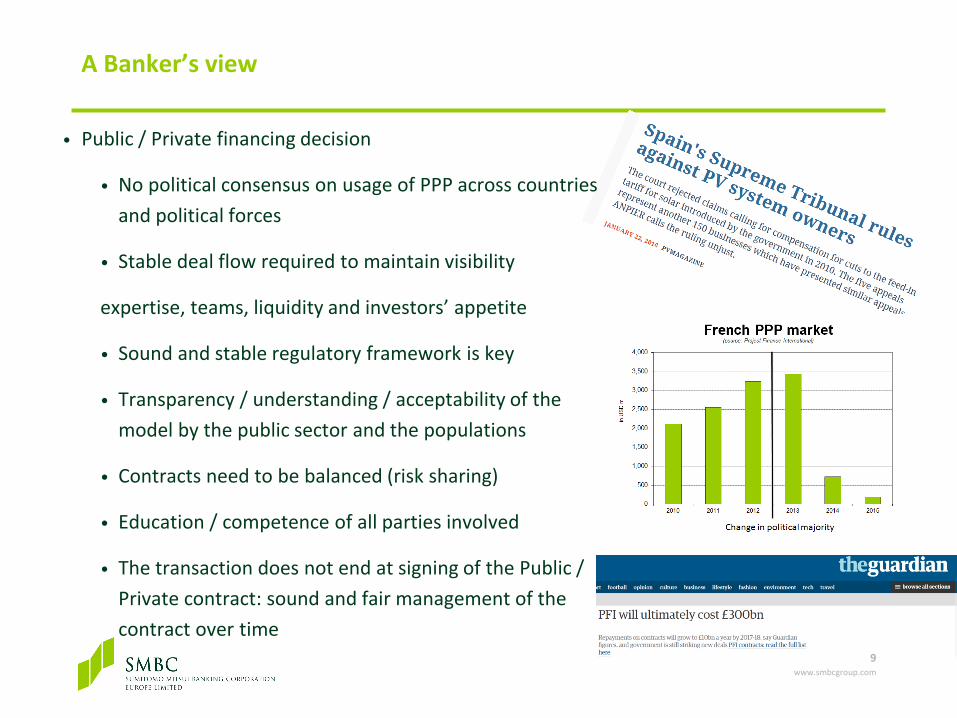

A Banker’s view

www.smbcgroup.com

• Public / Private financing decision

• No political consensus on usage of PPP across countries

and political forces

• Stable deal flow required to maintain visibility

expertise, teams, liquidity and investors’ appetite

• Sound and stable regulatory framework is key

• Transparency / understanding / acceptability of the

model by the public sector and the populations

• Contracts need to be balanced (risk sharing)

• Education / competence of all parties involved

• The transaction does not end at signing of the Public /

Private contract: sound and fair management of the

contract over time

9

A Banker’s view

www.smbcgroup.com

• Regulatory environment for banks and investors significantly impacts the amount of liquidity

available for infrastructure projects (Basel 3-4, Solvency 2, etc.)

• Infrastructure consists of long term assets and long term funding availability is a key element of

the viability of infrastructure projects

• Facilitation of long term financing can be sought (repo / refinancing solutions, permit different

pools of liquidity, FX provisions, etc.)

• Limited liquidity for volume, traffic or merchant risk. Consider backstop provisions to mitigate

the risk and increase the liquidity available for these projects?

• Better use of public funds available for the sector / Understanding of the financial markets is key:

• Understanding of rules and regulations imposed to the financial sectors (Basel, Solvency etc.) when seeking use of private funds for new infrastructure projects

• Assess necessity to inject funds from public / sovereign institution in a context of abundant liquidity

• How can public funds be used as seed capital to develop new infrastructure markets?

10

A Banker’s view

www.smbcgroup.com

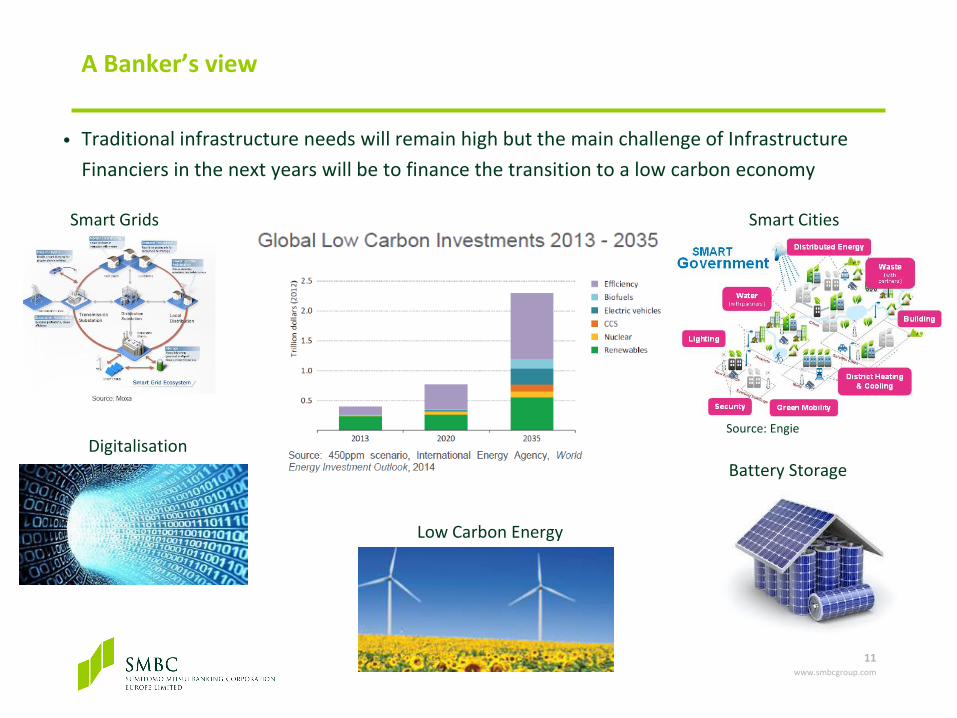

• Traditional infrastructure needs will remain high but the main challenge of Infrastructure

Financiers in the next years will be to finance the transition to a low carbon economy

Smart Grids Smart Cities

Low Carbon Energy

Digitalisation

Battery Storage

Source: Engie

11

A Banker’s view