Embed Size (px)

Citation preview

2016 European Venture Capital Report

January 2017

About this report

Curation & research

by Dealroom’s team

Machine learning and

natural language

processing

Analytics and growth signals on 500,000+ companies

10,000+ contributors

(founders, VCs, …)

Automatic data feeds

and web crawlers

Market insights from industry insiders and journalists

Manually verify data and enrich content

Predict company activity, identify growth trends

2

About Dealroom.co■ Founded in 2013 in Amsterdam, Dealroom has become Europe’s leading

venture capital database, tracking over 500,000 high-growth companies and 10,000 investors in Europe and beyond

■ Dealroom provides a 360° view by combining research with big data and machine learning, plus contributions from over 10,000 local market experts

■ Customers (funds, corporates, banks, consultants) use its online tools and bespoke research to stay ahead of developments and for decision-support

Scope of this report■ This report covers venture capital funding in Europe and Israel (including Russia

and Turkey). Includes: angel & seed rounds, VC series, growth equity, converts

■ Excluded are: private equity buyouts, M&A, private placements, lending capital

■ Throughout this presentation, footnotes reference to relevant online resources found on https://app.dealroom.co

AuthorsYoram Wijngaarde (Founder & CEO)Formerly tech & media M&A at Lehman Brothers and NOAH Advisors

Julien Puls (Data analyst & researcher)Formerly at CMB CapitalUniversité Jean Moulin, Lyon

Special thanks to for massive contributions to the data

“verified open-data” model

1. Headline stats in Europe

2. Identified trends and drivers

3. Top verticals and business models

4. Investment sources trends

5. Overviews of top countries

6. Outtakes: additional data

Contents

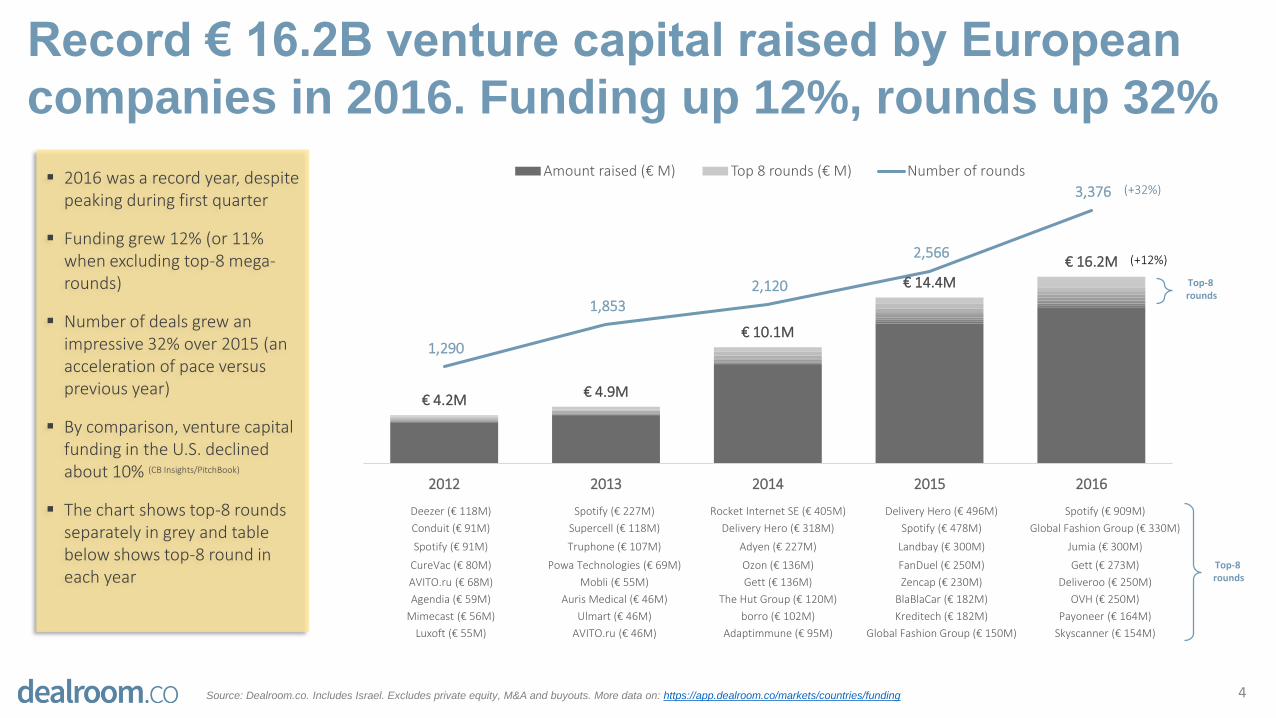

Record € 16.2B venture capital raised by European

companies in 2016. Funding up 12%, rounds up 32%

2016 was a record year, despite peaking during first quarter

Funding grew 12% (or 11% when excluding top-8 mega-rounds)

Number of deals grew an impressive 32% over 2015 (an acceleration of pace versus previous year)

By comparison, venture capital funding in the U.S. declined about 10% (CB Insights/PitchBook)

The chart shows top-8 rounds separately in grey and table below shows top-8 round in each year

4

€ 4.2M€ 4.9M

€ 10.1M

€ 14.4M

€ 16.2M

1,290

1,853

2,120

2,566

3,376

2012 2013 2014 2015 2016

Amount raised (€ M) Top 8 rounds (€ M) Number of rounds

Deezer (€ 118M) Spotify (€ 227M) Rocket Internet SE (€ 405M) Delivery Hero (€ 496M) Spotify (€ 909M)

Conduit (€ 91M) Supercell (€ 118M) Delivery Hero (€ 318M) Spotify (€ 478M) Global Fashion Group (€ 330M)

Spotify (€ 91M) Truphone (€ 107M) Adyen (€ 227M) Landbay (€ 300M) Jumia (€ 300M)

CureVac (€ 80M) Powa Technologies (€ 69M) Ozon (€ 136M) FanDuel (€ 250M) Gett (€ 273M)

AVITO.ru (€ 68M) Mobli (€ 55M) Gett (€ 136M) Zencap (€ 230M) Deliveroo (€ 250M)

Agendia (€ 59M) Auris Medical (€ 46M) The Hut Group (€ 120M) BlaBlaCar (€ 182M) OVH (€ 250M)

Mimecast (€ 56M) Ulmart (€ 46M) borro (€ 102M) Kreditech (€ 182M) Payoneer (€ 164M)

Luxoft (€ 55M) AVITO.ru (€ 46M) Adaptimmune (€ 95M) Global Fashion Group (€ 150M) Skyscanner (€ 154M)

Top-8 rounds

Top-8 rounds

(+32%)

(+12%)

Source: Dealroom.co. Includes Israel. Excludes private equity, M&A and buyouts. More data on: https://app.dealroom.co/markets/countries/funding

€ 888M

€ 1,331M€ 1,118M

€ 1,569M

€ 2,015M

€ 2,478M

€ 3,618M

€ 2,116M

€ 3,552M€ 3,848M

€ 4,310M

€ 3,535M

€ 4,627M€ 4,238M

€ 3,513M€ 3,799M

389

467 499 498

544 561 530

485

636 561 648

721

883 836

786

871

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2013 2014 2015 2016

Amount raised (€ M) Top 8 rounds (€ M) Number of rounds

Q4: €3.8 billion raised by European companies.

Number of rounds in Q4 were second highest ever

5

Funding peaked during Q1, in € terms.

Number of rounds during Q4 were close to an all-time high.

Source: Dealroom.co. Note: blue font indicates biotech. Excludes private equity, M&A and buyouts. More data on: https://app.dealroom.co/markets/countries/funding

Q4 ranks as #5 highest quarter ever.

Top-8 rounds

Top-8 rounds

Truphone Supercell Powa Spotify Klarna Ozon Rocket Adyen Delivery Hero Spotify FanDuel CureVac Spotify GFG OVH Payoneer

€ 107M € 118M € 69M € 227M € 90M € 136M € 405M € 227M € 496M € 478M € 250M € 100M € 909M € 330M € 250M € 164M

AVITO.ru Auris Medical Shazam Mobli Delivery Hero Takeaway Delivery Hero Powa HelloFresh INFINIDAT BlaBlaCar Atom Bank Jumia Gett Deliveroo SIGFOX

€ 46M € 46M € 36M € 55M € 80M € 94M € 318M € 73M € 110M € 136M € 182M € 98M € 300M € 273M € 250M € 150M

Hybris Ulmart Evotec Arria NLG NovImmune Delivery Hero Gett Blue Yonder SIGFOX Funding Circle GFG Deliveroo Skyscanner Cabify OurCrowd Devialet

€ 27M € 46M € 36M € 37M € 60M € 77M € 136M € 68M € 105M € 136M € 150M € 91M € 154M € 109M € 66M € 100M

3V Symphogen Crocus ADC SoundCloud Sarenza The Hut Group Cell Medica Foodpanda Home24 Reward Gtwy Ebury Cool Blue Farfetch Sabio Gett

€ 23M € 41M € 34M € 36M € 55M € 74M € 120M € 60M € 104M € 120M € 144M € 76M € 140M € 100M € 60M € 91M

Game Insight NumberFour NewVoiceMedia Funding Circle Hoccer Westwing Adaptimmune Truecaller WorldRemit Auto1 Group Letgo Symphogen Deezer Letgo Darktrace Voyager Labs

€ 23M € 35M € 32M € 34M € 50M € 72M € 95M € 55M € 91M € 107M € 91M € 68M € 100M € 91M € 58M € 91M

Ostrovok Opsona Delivery Hero Wilocity Avantium Farfetch BlaBlaCar Ascendis Verne Global Delivery Hero Prodigy ObsEva MindMaze SoundCloud LINKBYNET Carrick

€ 23M € 33M € 27M € 32M € 46M € 60M € 91M € 55M € 89M € 100M € 91M € 55M € 91M € 87M € 50M € 86M

Farfetch GenSight WiThings Merus Hailo iZettle ironSource Huddle Farfetch Foodpanda CeQur Cybereason Starling Bank Jumia Jumia HelloFresh

€ 18M € 32M € 27M € 31M € 46M € 50M € 77M € 46M € 78M € 91M € 91M € 54M € 58M € 75M € 50M € 85M

NewVoiceMedia ResearchGate ObsEva Biocartis Kaltura HelloFresh Biocartis StoreDot TransferWise Wallapop Kreditech TransferWise WISeKey SIRIN Labs Silent Circle Sonnenbatterie

€ 18M € 32M € 26M € 30M € 43M € 46M € 65M € 46M € 53M € 91M € 83M € 53M € 55M € 66M € 46M € 77M

€ 1.3B € 1.3B

€ 3.2B

€ 3.8B

€ 3.2B

€ 0.6B € 0.6B

€ 2.0B

€ 2.9B

€ 2.0B

€ 0.5B€ 0.6B

€ 0.8B

€ 1.5B

€ 2.7B

€ 0.5B € 0.5B

€ 1.2B

€ 1.8B

€ 2.7B

€ 0.2B€ 0.3B

€ 0.5B

€ 1.0B

€ 1.6B

€ 1.1B

€ 1.6B

€ 2.4B

€ 3.4B

€ 4.0B

410

542

644

545 520

165 245

288 353 380

118 167 180

243

590

88 132

166 241 231

57 42 82

163

366

452

725 760

1,021

1,289

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

United Kingdom Germany France Israel Sweden Other

Amount raised (€ billion) Number of rounds

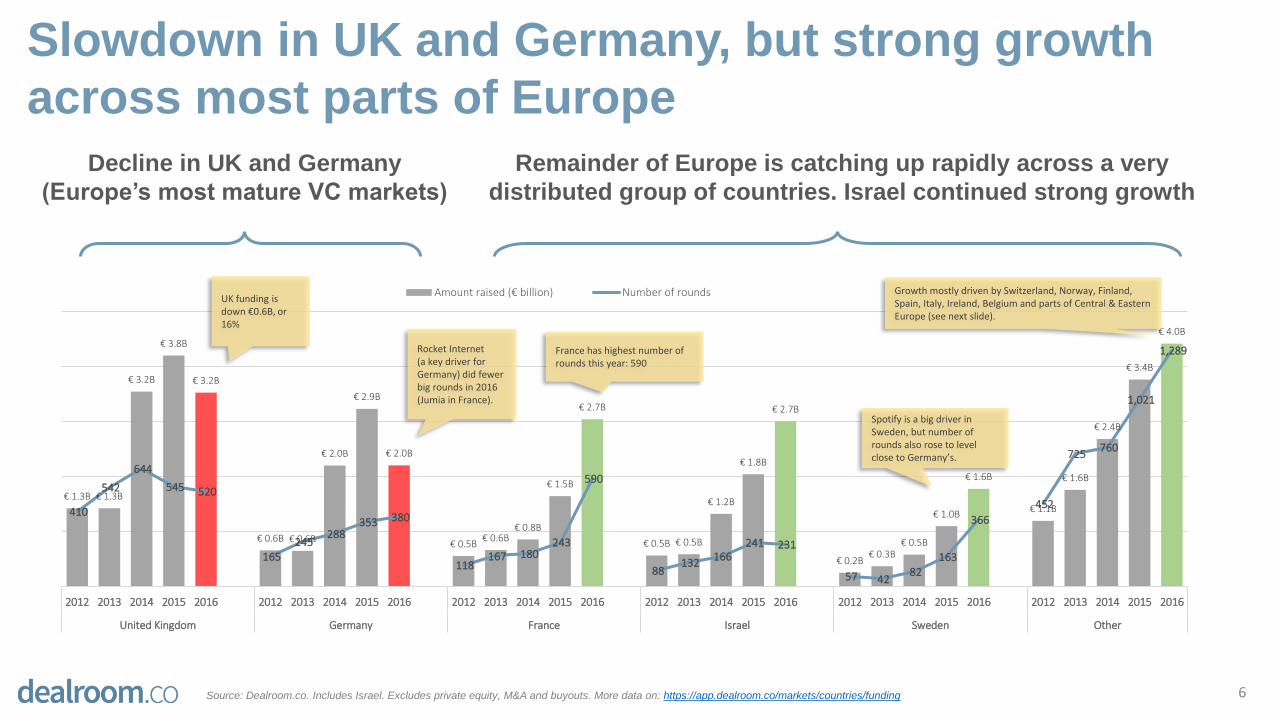

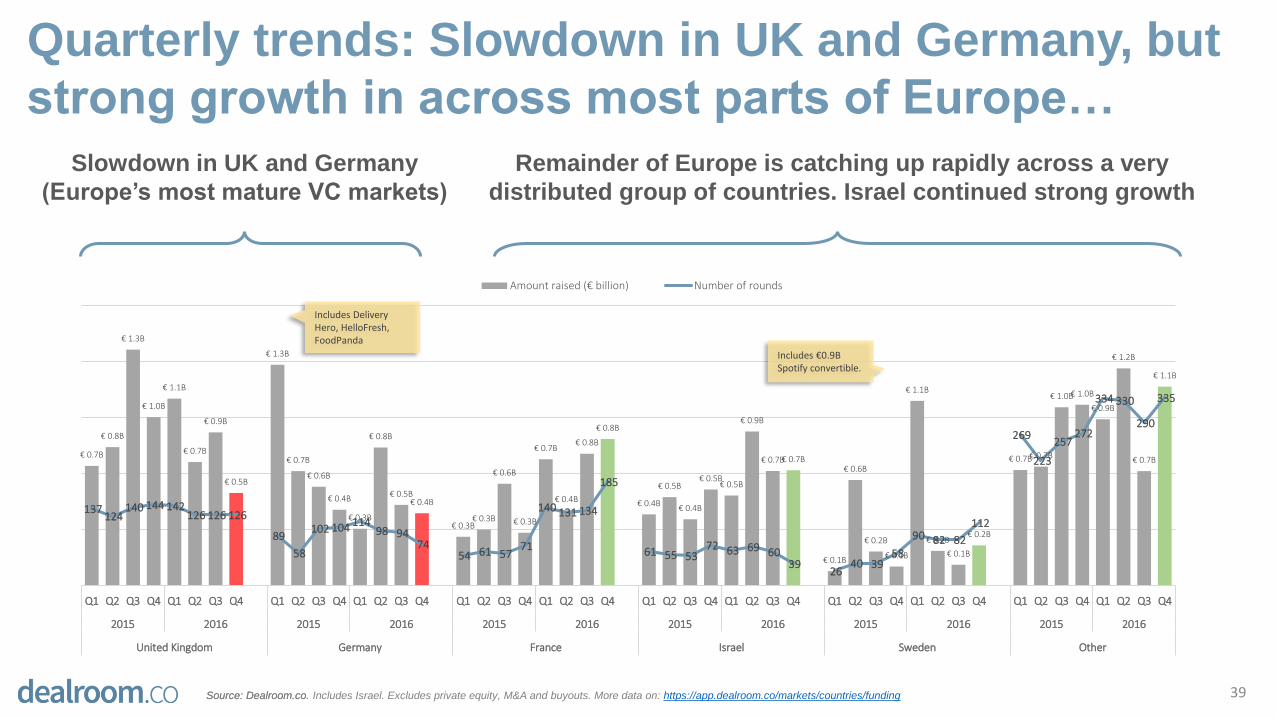

Slowdown in UK and Germany, but strong growth

across most parts of Europe

6

Rocket Internet (a key driver for Germany) did fewer big rounds in 2016 (Jumia in France).

UK funding is down €0.6B, or 16%

Decline in UK and Germany

(Europe’s most mature VC markets)

Remainder of Europe is catching up rapidly across a very

distributed group of countries. Israel continued strong growth

France has highest number of rounds this year: 590

Spotify is a big driver in Sweden, but number of rounds also rose to level close to Germany’s.

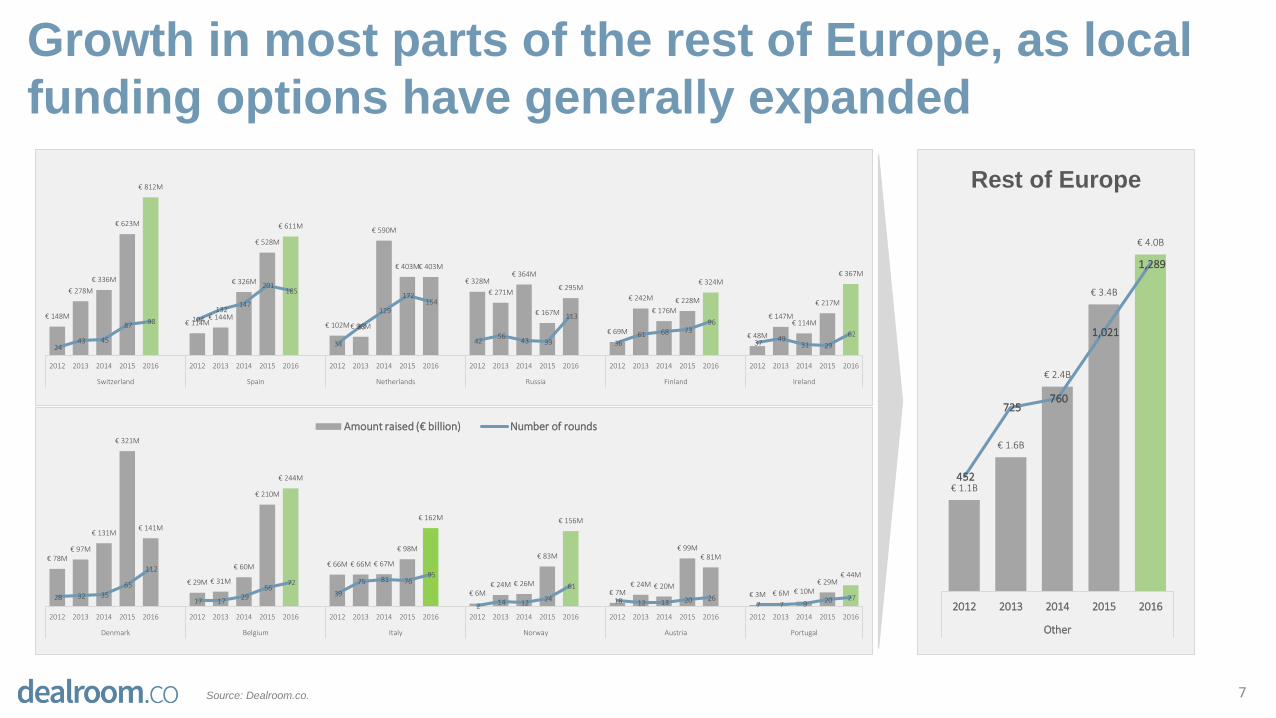

Growth mostly driven by Switzerland, Norway, Finland, Spain, Italy, Ireland, Belgium and parts of Central & Eastern Europe (see next slide).

Source: Dealroom.co. Includes Israel. Excludes private equity, M&A and buyouts. More data on: https://app.dealroom.co/markets/countries/funding

Growth in most parts of the rest of Europe, as local

funding options have generally expanded

7Source: Dealroom.co.

€ 148M

€ 278M

€ 336M

€ 623M

€ 812M

€ 114M€ 144M

€ 326M

€ 528M

€ 611M

€ 102M€ 96M

€ 590M

€ 403M€ 403M

€ 328M

€ 271M

€ 364M

€ 167M

€ 295M

€ 69M

€ 242M

€ 176M

€ 228M

€ 324M

€ 48M

€ 147M€ 114M

€ 217M

€ 367M

24 43 45

87 98 104 132

147

201 185

34

83

129

172 154

42 56

43 39

113

36 61 68 73

96

37 49

31 29

62

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

Switzerland Spain Netherlands Russia Finland Ireland

€ 78M€ 97M

€ 131M

€ 321M

€ 141M

€ 29M € 31M

€ 60M

€ 210M

€ 244M

€ 66M € 66M € 67M

€ 98M

€ 162M

€ 6M€ 24M € 26M

€ 83M

€ 156M

€ 7M€ 24M € 20M

€ 99M€ 81M

€ 3M € 6M € 10M€ 29M

€ 44M

28 32 35

65

112

17 17 29

56 72

39

75 81 76 95

2 14 12

24

61

18 12 13 20 26 7 7 9 20 27

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

Denmark Belgium Italy Norway Austria Portugal

Amount raised (€ billion) Number of rounds

€ 1.1B

€ 1.6B

€ 2.4B

€ 3.4B

€ 4.0B

452

725 760

1,021

1,289

2012 2013 2014 2015 2016

Other

Rest of Europe

1. Introduction: headline stats in Europe

2. Insights: understanding the key trends and drivers

3. Top verticals and business models

4. Investment sources trends

5. Overviews of top countries

6. Outtakes: additional data

Contents

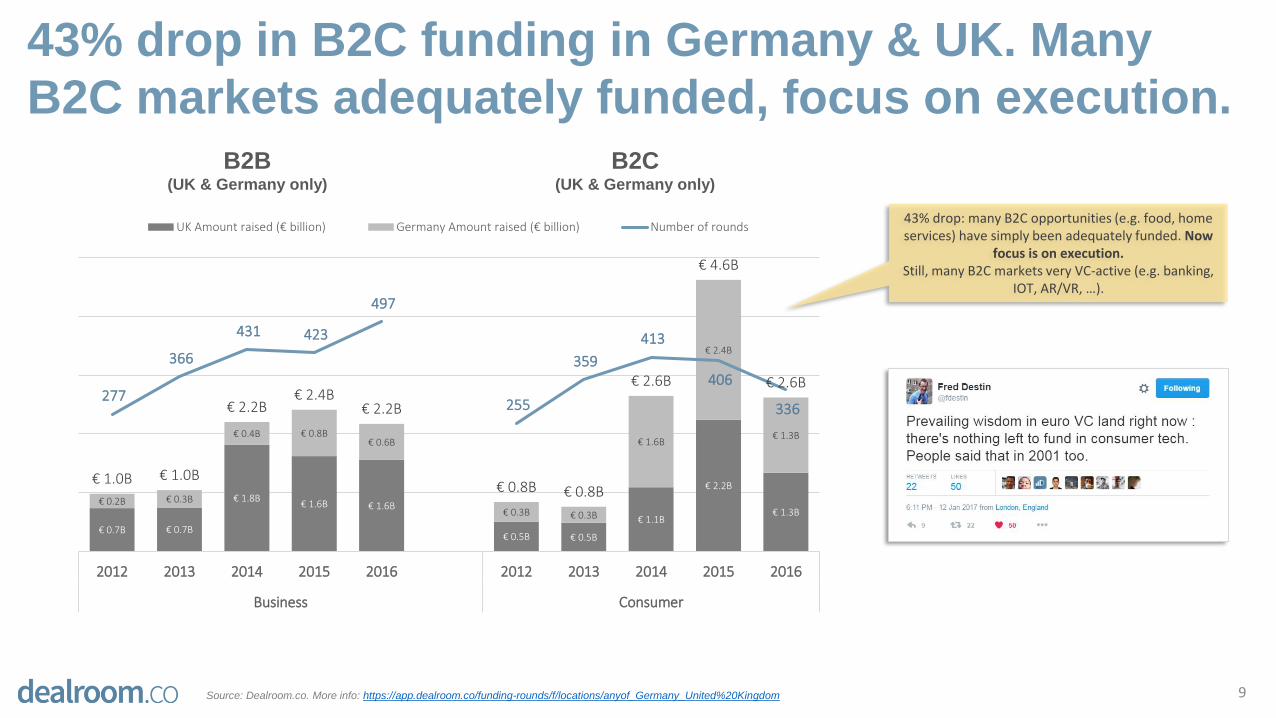

43% drop in B2C funding in Germany & UK. Many

B2C markets adequately funded, focus on execution.

9Source: Dealroom.co. More info: https://app.dealroom.co/funding-rounds/f/locations/anyof_Germany_United%20Kingdom

B2C (UK & Germany only)

B2B (UK & Germany only)

€ 0.7B € 0.7B

€ 1.8B€ 1.6B € 1.6B

€ 0.5B € 0.5B

€ 1.1B

€ 2.2B

€ 1.3B€ 0.2B € 0.3B

€ 0.4B € 0.8B€ 0.6B

€ 0.3B € 0.3B

€ 1.6B

€ 2.4B

€ 1.3B

€ 1.0B € 1.0B

€ 2.2B€ 2.4B

€ 2.2B

€ 0.8B € 0.8B

€ 2.6B

€ 4.6B

€ 2.6B277

366

431 423

497

255

359

413

406

336

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

Business Consumer

UK Amount raised (€ billion) Germany Amount raised (€ billion) Number of rounds43% drop: many B2C opportunities (e.g. food, home services) have simply been adequately funded. Now

focus is on execution. Still, many B2C markets very VC-active (e.g. banking,

IOT, AR/VR, …).

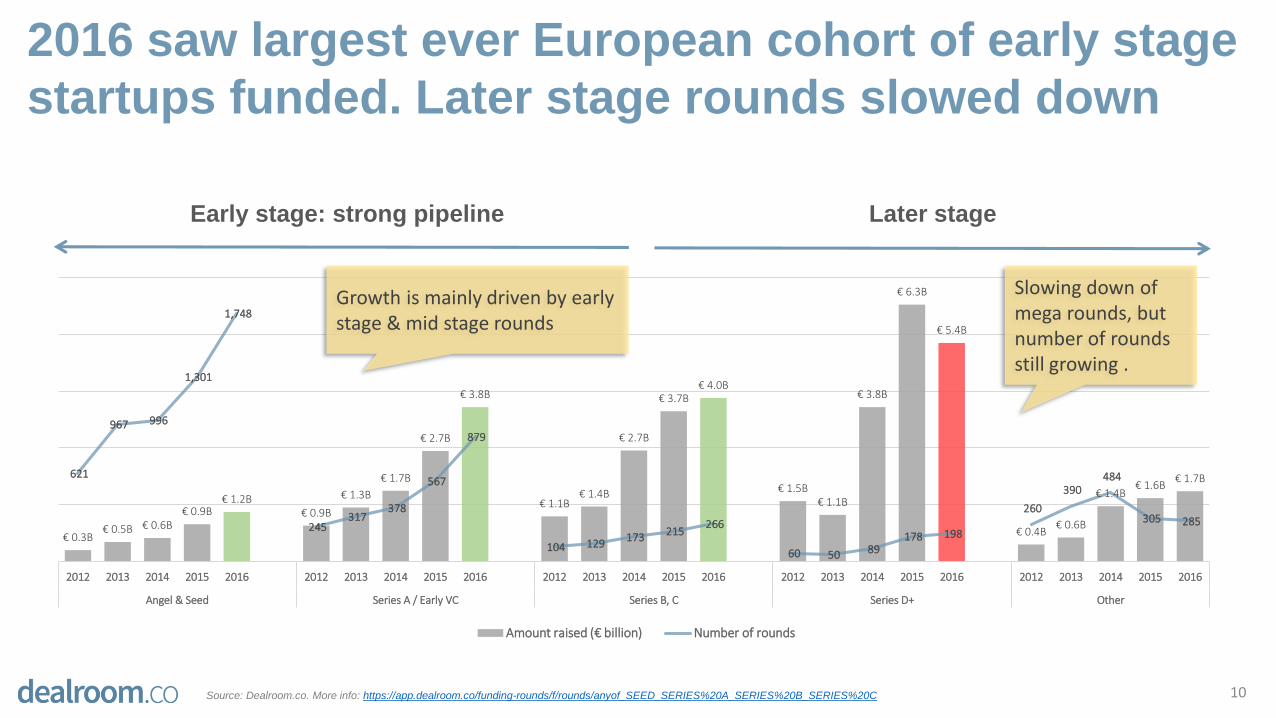

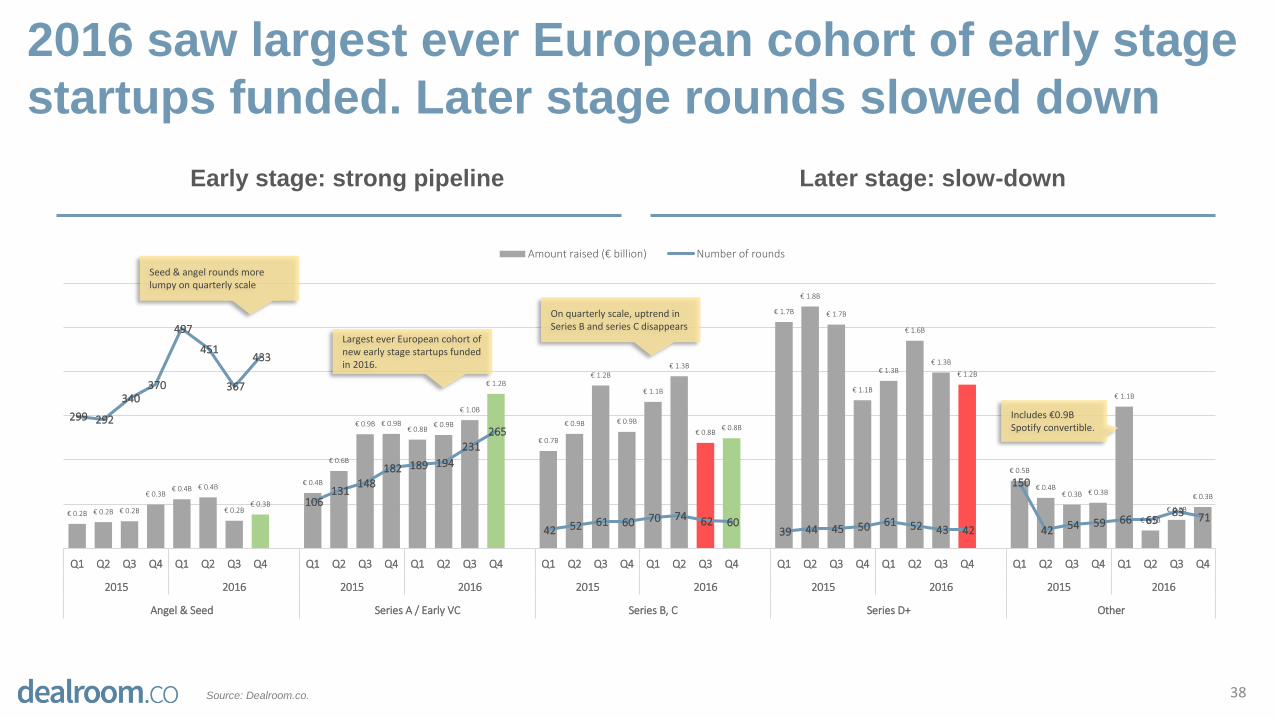

2016 saw largest ever European cohort of early stage

startups funded. Later stage rounds slowed down

10

€ 0.3B€ 0.5B € 0.6B

€ 0.9B€ 1.2B

€ 0.9B

€ 1.3B

€ 1.7B

€ 2.7B

€ 3.8B

€ 1.1B€ 1.4B

€ 2.7B

€ 3.7B€ 4.0B

€ 1.5B€ 1.1B

€ 3.8B

€ 6.3B

€ 5.4B

€ 0.4B€ 0.6B

€ 1.4B€ 1.6B

€ 1.7B621

967 996

1,301

1,748

245 317

378

567

879

104 129 173 215

266

60 50 89 178 198

260

390 484

305 285

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

Angel & Seed Series A / Early VC Series B, C Series D+ Other

Amount raised (€ billion) Number of rounds

Early stage: strong pipeline Later stage

Source: Dealroom.co. More info: https://app.dealroom.co/funding-rounds/f/rounds/anyof_SEED_SERIES%20A_SERIES%20B_SERIES%20C

Growth is mainly driven by early stage & mid stage rounds

Slowing down of mega rounds, but number of rounds still growing .

31%

16%

9% 5%

21%

8%

–

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Seed Series A Series B Series C Series D

2009 cohort 2010 cohort 2011 cohort 2012 cohort 2013 cohort% of startups reaching next funding round

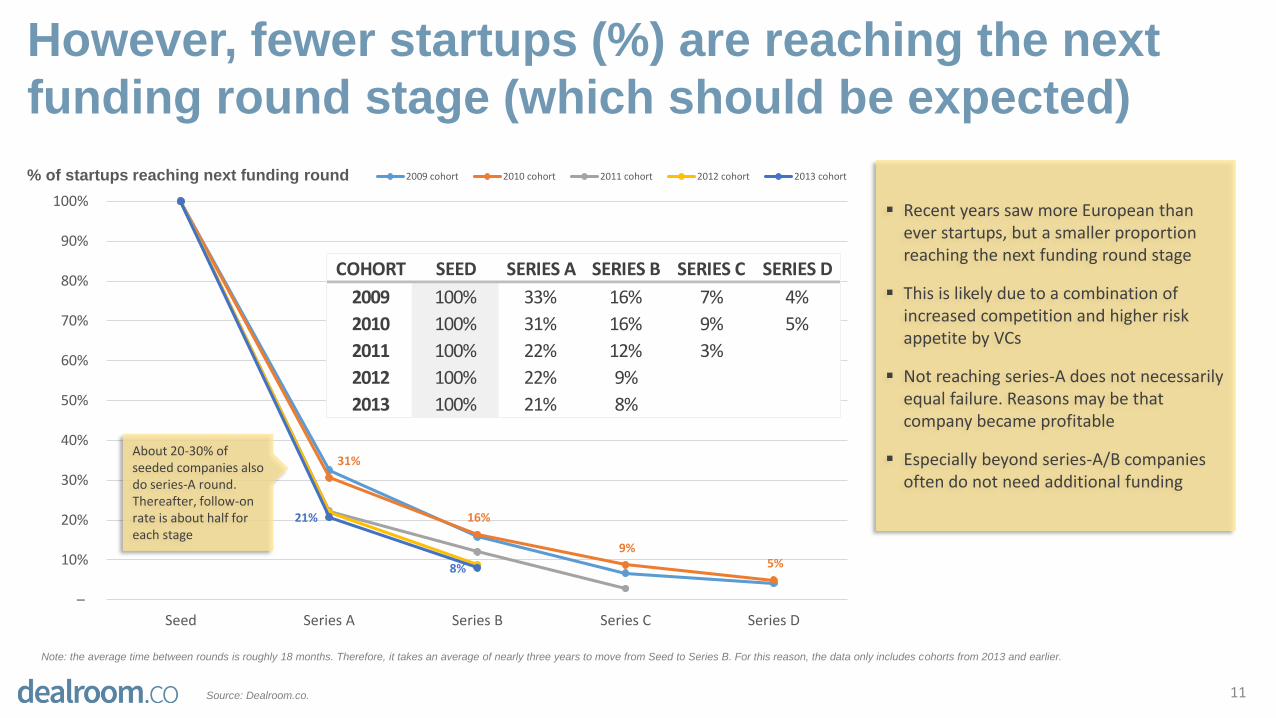

However, fewer startups (%) are reaching the next

funding round stage (which should be expected)

Note: the average time between rounds is roughly 18 months. Therefore, it takes an average of nearly three years to move from Seed to Series B. For this reason, the data only includes cohorts from 2013 and earlier.

COHORT SEED SERIES A SERIES B SERIES C SERIES D

2009 100% 33% 16% 7% 4%

2010 100% 31% 16% 9% 5%

2011 100% 22% 12% 3%

2012 100% 22% 9%

2013 100% 21% 8%

Recent years saw more European than ever startups, but a smaller proportion reaching the next funding round stage

This is likely due to a combination of increased competition and higher risk appetite by VCs

Not reaching series-A does not necessarily equal failure. Reasons may be that company became profitable

Especially beyond series-A/B companies often do not need additional funding

About 20-30% of seeded companies also do series-A round. Thereafter, follow-on rate is about half for each stage

11Source: Dealroom.co.

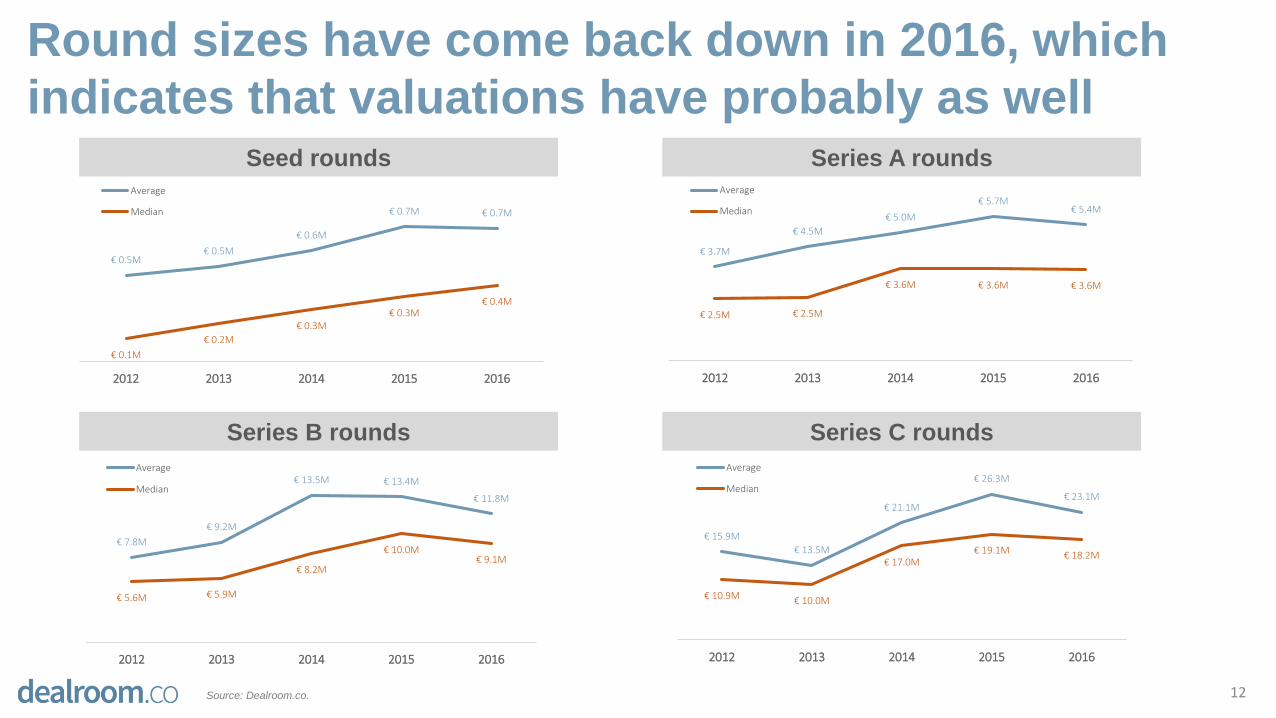

Round sizes have come back down in 2016, which

indicates that valuations have probably as well

12Source: Dealroom.co.

€ 0.5M€ 0.5M

€ 0.6M

€ 0.7M € 0.7M

€ 0.1M

€ 0.2M

€ 0.3M€ 0.3M

€ 0.4M

2012 2013 2014 2015 2016

Average

Median

Series C rounds

Seed rounds Series A rounds

€ 3.7M

€ 4.5M

€ 5.0M

€ 5.7M€ 5.4M

€ 2.5M € 2.5M

€ 3.6M € 3.6M € 3.6M

2012 2013 2014 2015 2016

Average

Median

€ 7.8M

€ 9.2M

€ 13.5M € 13.4M

€ 11.8M

€ 5.6M € 5.9M

€ 8.2M

€ 10.0M€ 9.1M

2012 2013 2014 2015 2016

Average

Median

€ 15.9M

€ 13.5M

€ 21.1M

€ 26.3M

€ 23.1M

€ 10.9M € 10.0M

€ 17.0M€ 19.1M € 18.2M

2012 2013 2014 2015 2016

Average

Median

Series B rounds

1. Introduction: headline stats in Europe

2. Insights: understanding the key trends and drivers

3. Top verticals and business models

4. Investment sources trends

5. Overviews of top countries

6. Outtakes: additional data

Contents

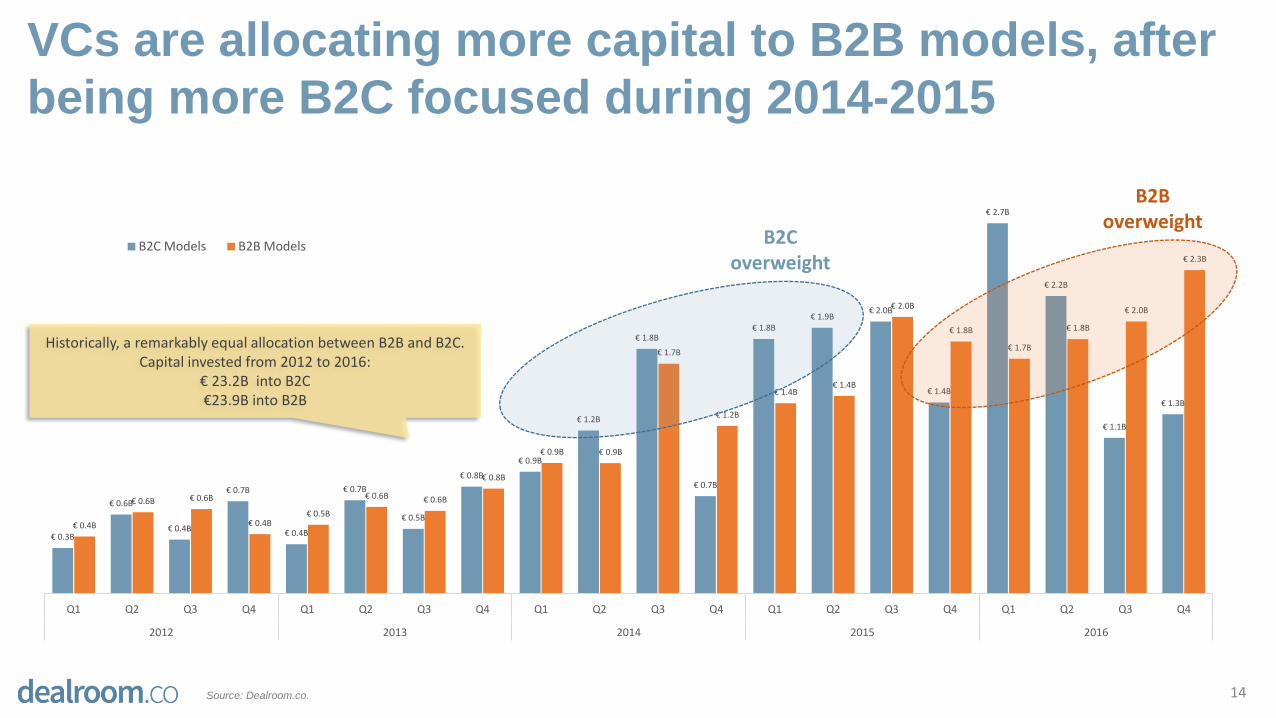

VCs are allocating more capital to B2B models, after

being more B2C focused during 2014-2015

14Source: Dealroom.co.

€ 0.3B

€ 0.6B

€ 0.4B

€ 0.7B

€ 0.4B

€ 0.7B

€ 0.5B

€ 0.8B

€ 0.9B

€ 1.2B

€ 1.8B

€ 0.7B

€ 1.8B€ 1.9B

€ 2.0B

€ 1.4B

€ 2.7B

€ 2.2B

€ 1.1B

€ 1.3B

€ 0.4B

€ 0.6B € 0.6B

€ 0.4B€ 0.5B

€ 0.6B € 0.6B

€ 0.8B

€ 0.9B € 0.9B

€ 1.7B

€ 1.2B

€ 1.4B€ 1.4B

€ 2.0B

€ 1.8B

€ 1.7B

€ 1.8B

€ 2.0B

€ 2.3B

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015 2016

B2C Models B2B Models

Historically, a remarkably equal allocation between B2B and B2C. Capital invested from 2012 to 2016:

€ 23.2B into B2C€23.9B into B2B

B2C overweight

B2B overweight

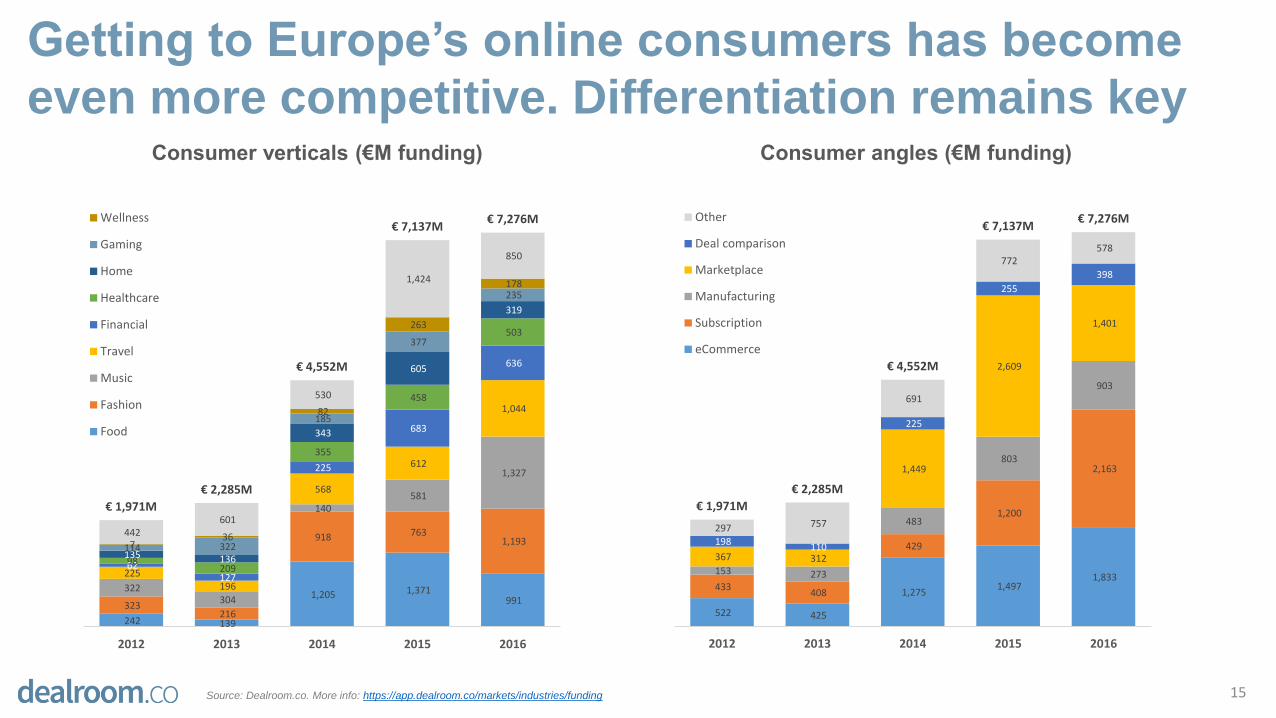

Getting to Europe’s online consumers has become

even more competitive. Differentiation remains key

15Source: Dealroom.co. More info: https://app.dealroom.co/markets/industries/funding

Consumer verticals (€M funding) Consumer angles (€M funding)

522 425

1,275 1,497

1,833 433

408

429

1,200

2,163

153 273

483

803

903

367 312

1,449

2,609

1,401

198 110

225

255

398

297 757

691

772 578

€ 1,971M

€ 2,285M

€ 4,552M

€ 7,137M€ 7,276M

2012 2013 2014 2015 2016

Other

Deal comparison

Marketplace

Manufacturing

Subscription

eCommerce

242 139

1,205 1,371 991 323

216

918 763 1,193

322 304

140 581

1,327

225 196

568

612

1,044

62 127

225

683

636

98 209

355

458

503

135 136

343

605

319

114 322

185

377

235

7 36

82

263

178

442 601

530

1,424

850

€ 1,971M

€ 2,285M

€ 4,552M

€ 7,137M€ 7,276M

2012 2013 2014 2015 2016

Wellness

Gaming

Home

Healthcare

Financial

Travel

Music

Fashion

Food

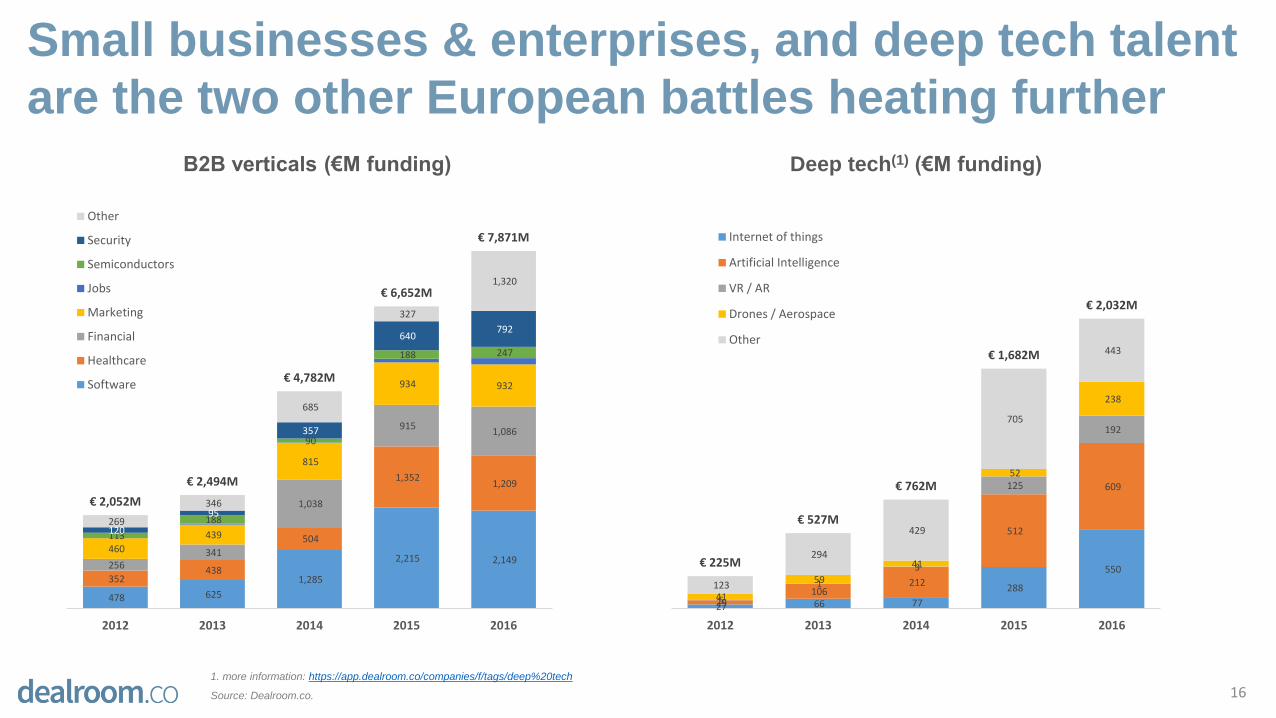

Small businesses & enterprises, and deep tech talent

are the two other European battles heating further

161. more information: https://app.dealroom.co/companies/f/tags/deep%20tech

Source: Dealroom.co.

B2B verticals (€M funding) Deep tech(1) (€M funding)

478 625

1,285

2,215 2,149

352 438

504

1,352 1,209

256 341

1,038

915 1,086

460

439

815

934 932

113

188

90

188 247

120

95

357

640 792

269

346

685

327

1,320

€ 2,052M

€ 2,494M

€ 4,782M

€ 6,652M

€ 7,871M

2012 2013 2014 2015 2016

Other

Security

Semiconductors

Jobs

Marketing

Financial

Healthcare

Software

27 66 77

288

550

29 106

212

512

609

5

1

3

125

192

41

59

41

52

238

123

294

429

705

443

€ 225M

€ 527M

€ 762M

€ 1,682M

€ 2,032M

2012 2013 2014 2015 2016

Internet of things

Artificial Intelligence

VR / AR

Drones / Aerospace

Other

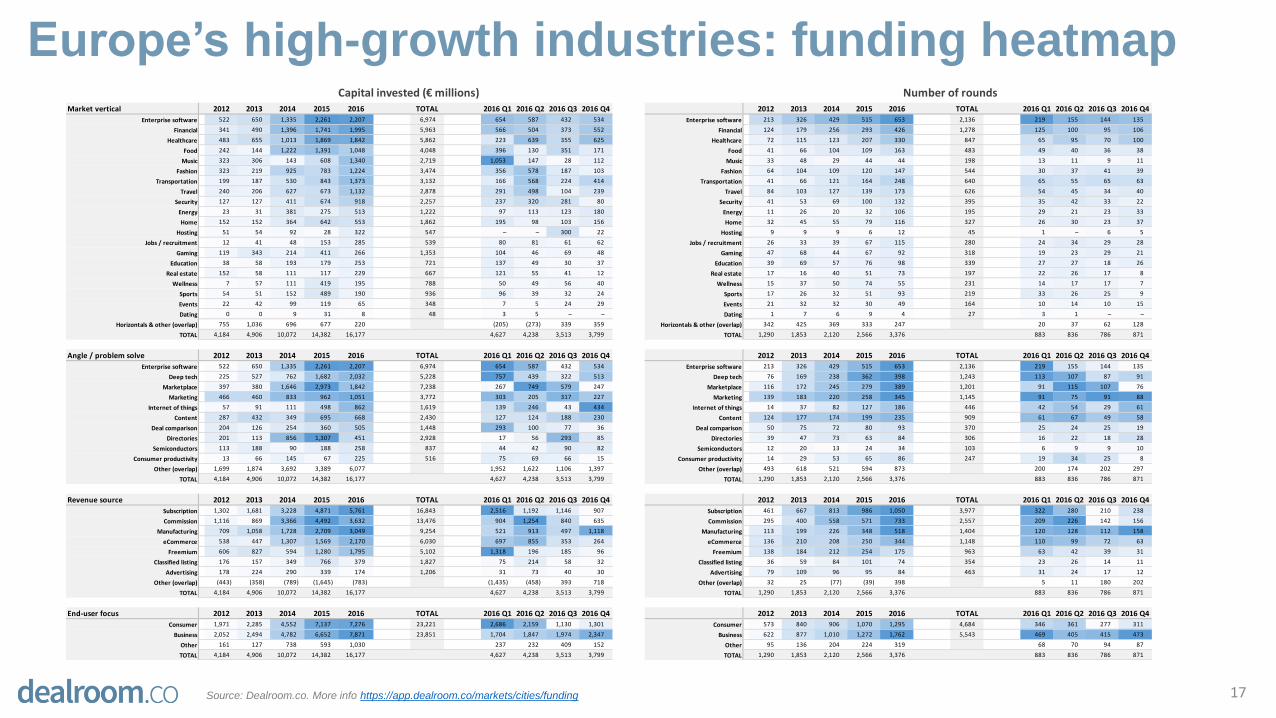

Europe’s high-growth industries: funding heatmap

17Source: Dealroom.co. More info https://app.dealroom.co/markets/cities/funding

Capital invested (€ millions) Number of rounds Capital invested 2012-2016 (€ millions)Market vertical 2012 2013 2014 2015 2016 TOTAL 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2012 2013 2014 2015 2016 TOTAL 2016 Q1 2016 Q2 2016 Q3 2016 Q4

Enterprise software 522 650 1,335 2,261 2,207 6,974 654 587 432 534 Enterprise software 213 326 429 515 653 2,136 219 155 144 135

Financial 341 490 1,396 1,741 1,995 5,963 566 504 373 552 Financial 124 179 256 293 426 1,278 125 100 95 106

Healthcare 483 655 1,013 1,869 1,842 5,862 223 639 355 625 Healthcare 72 115 123 207 330 847 65 95 70 100

Food 242 144 1,222 1,391 1,048 4,048 396 130 351 171 Food 41 66 104 109 163 483 49 40 36 38

Music 323 306 143 608 1,340 2,719 1,053 147 28 112 Music 33 48 29 44 44 198 13 11 9 11

Fashion 323 219 925 783 1,224 3,474 356 578 187 103 Fashion 64 104 109 120 147 544 30 37 41 39

Transportation 199 187 530 843 1,373 3,132 166 568 224 414 Transportation 41 66 121 164 248 640 65 55 65 63

Travel 240 206 627 673 1,132 2,878 291 498 104 239 Travel 84 103 127 139 173 626 54 45 34 40

Security 127 127 411 674 918 2,257 237 320 281 80 Security 41 53 69 100 132 395 35 42 33 22

Energy 23 31 381 275 513 1,222 97 113 123 180 Energy 11 26 20 32 106 195 29 21 23 33

Home 152 152 364 642 553 1,862 195 98 103 156 Home 32 45 55 79 116 327 26 30 23 37

Hosting 51 54 92 28 322 547 – – 300 22 Hosting 9 9 9 6 12 45 1 – 6 5

Jobs / recruitment 12 41 48 153 285 539 80 81 61 62 Jobs / recruitment 26 33 39 67 115 280 24 34 29 28

Gaming 119 343 214 411 266 1,353 104 46 69 48 Gaming 47 68 44 67 92 318 19 23 29 21

Education 38 58 193 179 253 721 137 49 30 37 Education 39 69 57 76 98 339 27 27 18 26

Real estate 152 58 111 117 229 667 121 55 41 12 Real estate 17 16 40 51 73 197 22 26 17 8

Wellness 7 57 111 419 195 788 50 49 56 40 Wellness 15 37 50 74 55 231 14 17 17 7

Sports 54 51 152 489 190 936 96 39 32 24 Sports 17 26 32 51 93 219 33 26 25 9

Events 22 42 99 119 65 348 7 5 24 29 Events 21 32 32 30 49 164 10 14 10 15

Dating 0 0 9 31 8 48 3 5 – – Dating 1 7 6 9 4 27 3 1 – –

Horizontals & other (overlap) 755 1,036 696 677 220 (205) (273) 339 359 Horizontals & other (overlap) 342 425 369 333 247 20 37 62 128

TOTAL 4,184 4,906 10,072 14,382 16,177 4,627 4,238 3,513 3,799 TOTAL 1,290 1,853 2,120 2,566 3,376 883 836 786 871

Angle / problem solve 2012 2013 2014 2015 2016 TOTAL 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2012 2013 2014 2015 2016 TOTAL 2016 Q1 2016 Q2 2016 Q3 2016 Q4

Enterprise software 522 650 1,335 2,261 2,207 6,974 654 587 432 534 Enterprise software 213 326 429 515 653 2,136 219 155 144 135

Deep tech 225 527 762 1,682 2,032 5,228 757 439 322 513 Deep tech 76 169 238 362 398 1,243 113 107 87 91

Marketplace 397 380 1,646 2,973 1,842 7,238 267 749 579 247 Marketplace 116 172 245 279 389 1,201 91 115 107 76

Marketing 466 460 833 962 1,051 3,772 303 205 317 227 Marketing 139 183 220 258 345 1,145 91 75 91 88

Internet of things 57 91 111 498 862 1,619 139 246 43 434 Internet of things 14 37 82 127 186 446 42 54 29 61

Content 287 432 349 695 668 2,430 127 124 188 230 Content 124 177 174 199 235 909 61 67 49 58

Deal comparison 204 126 254 360 505 1,448 293 100 77 36 Deal comparison 50 75 72 80 93 370 25 24 25 19

Directories 201 113 856 1,307 451 2,928 17 56 293 85 Directories 39 47 73 63 84 306 16 22 18 28

Semiconductors 113 188 90 188 258 837 44 42 90 82 Semiconductors 12 20 13 24 34 103 6 9 9 10

Consumer productivity 13 66 145 67 225 516 75 69 66 15 Consumer productivity 14 29 53 65 86 247 19 34 25 8

Other (overlap) 1,699 1,874 3,692 3,389 6,077 1,952 1,622 1,106 1,397 Other (overlap) 493 618 521 594 873 200 174 202 297

TOTAL 4,184 4,906 10,072 14,382 16,177 4,627 4,238 3,513 3,799 TOTAL 1,290 1,853 2,120 2,566 3,376 883 836 786 871

Revenue source 2012 2013 2014 2015 2016 TOTAL 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2012 2013 2014 2015 2016 TOTAL 2016 Q1 2016 Q2 2016 Q3 2016 Q4

Subscription 1,302 1,681 3,228 4,871 5,761 16,843 2,516 1,192 1,146 907 Subscription 461 667 813 986 1,050 3,977 322 280 210 238

Commission 1,116 869 3,366 4,492 3,632 13,476 904 1,254 840 635 Commission 295 400 558 571 733 2,557 209 226 142 156

Manufacturing 709 1,058 1,728 2,709 3,049 9,254 521 913 497 1,118 Manufacturing 113 199 226 348 518 1,404 120 128 112 158

eCommerce 538 447 1,307 1,569 2,170 6,030 697 855 353 264 eCommerce 136 210 208 250 344 1,148 110 99 72 63

Freemium 606 827 594 1,280 1,795 5,102 1,318 196 185 96 Freemium 138 184 212 254 175 963 63 42 39 31

Classified listing 176 157 349 766 379 1,827 75 214 58 32 Classified listing 36 59 84 101 74 354 23 26 14 11

Advertising 178 224 290 339 174 1,206 31 73 40 30 Advertising 79 109 96 95 84 463 31 24 17 12

Other (overlap) (443) (358) (789) (1,645) (783) (1,435) (458) 393 718 Other (overlap) 32 25 (77) (39) 398 5 11 180 202

TOTAL 4,184 4,906 10,072 14,382 16,177 4,627 4,238 3,513 3,799 TOTAL 1,290 1,853 2,120 2,566 3,376 883 836 786 871

End-user focus 2012 2013 2014 2015 2016 TOTAL 2016 Q1 2016 Q2 2016 Q3 2016 Q4 2012 2013 2014 2015 2016 TOTAL 2016 Q1 2016 Q2 2016 Q3 2016 Q4

Consumer 1,971 2,285 4,552 7,137 7,276 23,221 2,686 2,159 1,130 1,301 Consumer 573 840 906 1,070 1,295 4,684 346 361 277 311

Business 2,052 2,494 4,782 6,652 7,871 23,851 1,704 1,847 1,974 2,347 Business 622 877 1,010 1,272 1,762 5,543 469 405 415 473

Other 161 127 738 593 1,030 237 232 409 152 Other 95 136 204 224 319 68 70 94 87

TOTAL 4,184 4,906 10,072 14,382 16,177 4,627 4,238 3,513 3,799 TOTAL 1,290 1,853 2,120 2,566 3,376 883 836 786 871

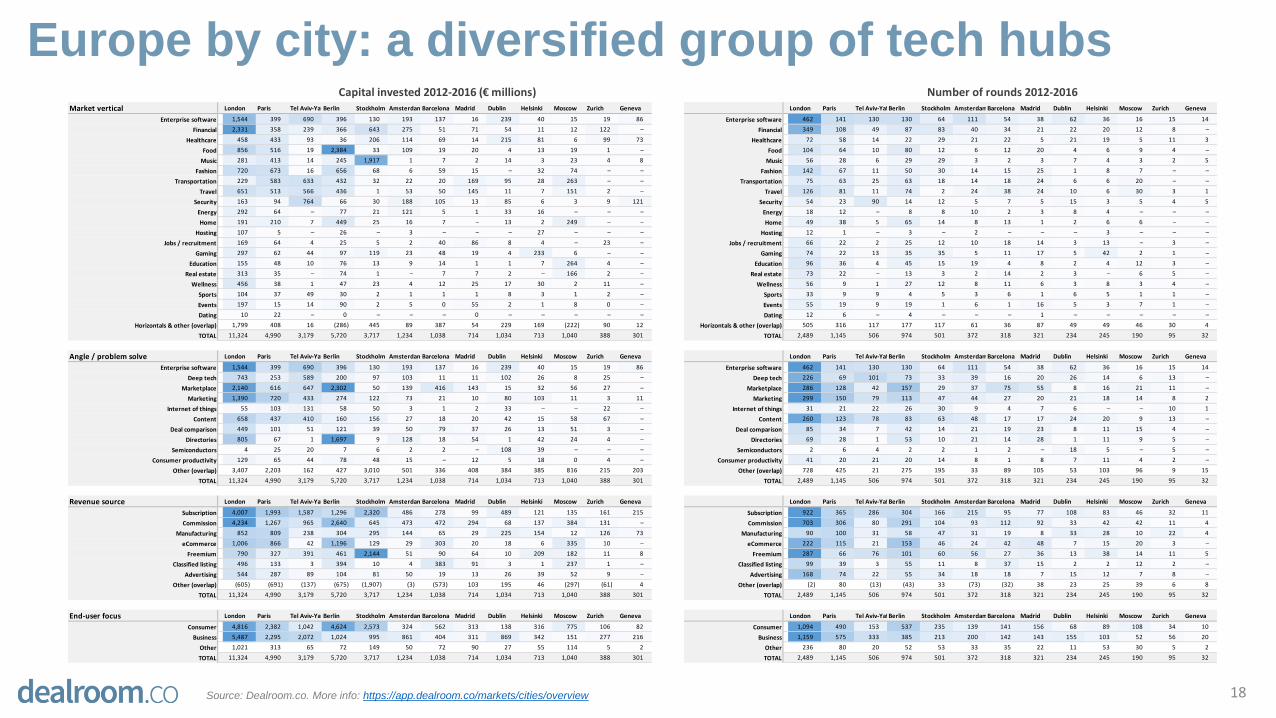

Europe by city: a diversified group of tech hubs

18Source: Dealroom.co. More info: https://app.dealroom.co/markets/cities/overview

Capital invested 2012-2016 (€ millions) Number of rounds 2012-2016Market vertical London Paris Tel Aviv-YafoBerlin Stockholm AmsterdamBarcelona Madrid Dublin Helsinki Moscow Zurich Geneva London Paris Tel Aviv-YafoBerlin Stockholm AmsterdamBarcelona Madrid Dublin Helsinki Moscow Zurich Geneva

Enterprise software 1,544 399 690 396 130 193 137 16 239 40 15 19 86 Enterprise software 462 141 130 130 64 111 54 38 62 36 16 15 14

Financial 2,331 358 239 366 643 275 51 71 54 11 12 122 – Financial 349 108 49 87 83 40 34 21 22 20 12 8 –

Healthcare 458 433 93 36 206 114 69 14 215 81 6 99 73 Healthcare 72 58 14 22 29 21 22 5 21 19 5 11 3

Food 856 516 19 2,384 33 109 19 20 4 13 19 1 – Food 104 64 10 80 12 6 12 20 4 6 9 4 –

Music 281 413 14 245 1,917 1 7 2 14 3 23 4 8 Music 56 28 6 29 29 3 2 3 7 4 3 2 5

Fashion 720 673 16 656 68 6 59 15 – 32 74 – – Fashion 142 67 11 50 30 14 15 25 1 8 7 – –

Transportation 229 583 633 432 32 22 20 169 95 28 263 – – Transportation 75 63 25 63 18 14 18 24 6 6 20 – –

Travel 651 513 566 436 1 53 50 145 11 7 151 2 – Travel 126 81 11 74 2 24 38 24 10 6 30 3 1

Security 163 94 764 66 30 188 105 13 85 6 3 9 121 Security 54 23 90 14 12 5 7 5 15 3 5 4 5

Energy 292 64 – 77 21 121 5 1 33 16 – – – Energy 18 12 – 8 8 10 2 3 8 4 – – –

Home 191 210 7 449 25 16 7 – 13 2 249 – – Home 49 38 5 65 14 8 13 1 2 6 6 – –

Hosting 107 5 – 26 – 3 – – – 27 – – – Hosting 12 1 – 3 – 2 – – – 3 – – –

Jobs / recruitment 169 64 4 25 5 2 40 86 8 4 – 23 – Jobs / recruitment 66 22 2 25 12 10 18 14 3 13 – 3 –

Gaming 297 62 44 97 119 23 48 19 4 233 6 – – Gaming 74 22 13 35 35 5 11 17 5 42 2 1 –

Education 155 48 10 76 13 9 14 1 1 7 264 4 – Education 96 36 4 45 15 19 4 8 2 4 12 3 –

Real estate 313 35 – 74 1 – 7 7 2 – 166 2 – Real estate 73 22 – 13 3 2 14 2 3 – 6 5 –

Wellness 456 38 1 47 23 4 12 25 17 30 2 11 – Wellness 56 9 1 27 12 8 11 6 3 8 3 4 –

Sports 104 37 49 30 2 1 1 1 8 3 1 2 – Sports 33 9 9 4 5 3 6 1 6 5 1 1 –

Events 197 15 14 90 2 5 0 55 2 1 8 0 – Events 55 19 9 19 1 6 1 16 5 3 7 1 –

Dating 10 22 – 0 – – – 0 – – – – – Dating 12 6 – 4 – – – 1 – – – – –

Horizontals & other (overlap) 1,799 408 16 (286) 445 89 387 54 229 169 (222) 90 12 Horizontals & other (overlap) 505 316 117 177 117 61 36 87 49 49 46 30 4

TOTAL 11,324 4,990 3,179 5,720 3,717 1,234 1,038 714 1,034 713 1,040 388 301 TOTAL 2,489 1,145 506 974 501 372 318 321 234 245 190 95 32

Angle / problem solve London Paris Tel Aviv-YafoBerlin Stockholm AmsterdamBarcelona Madrid Dublin Helsinki Moscow Zurich Geneva London Paris Tel Aviv-YafoBerlin Stockholm AmsterdamBarcelona Madrid Dublin Helsinki Moscow Zurich Geneva

Enterprise software 1,544 399 690 396 130 193 137 16 239 40 15 19 86 Enterprise software 462 141 130 130 64 111 54 38 62 36 16 15 14

Deep tech 743 253 589 200 97 103 11 11 102 26 8 25 – Deep tech 226 69 101 73 33 39 16 20 26 14 6 13 –

Marketplace 2,140 616 647 2,302 50 139 416 143 15 32 56 27 – Marketplace 286 128 42 157 29 37 75 55 8 16 21 11 –

Marketing 1,390 720 433 274 122 73 21 10 80 103 11 3 11 Marketing 299 150 79 113 47 44 27 20 21 18 14 8 2

Internet of things 55 103 131 58 50 3 1 2 33 – – 22 – Internet of things 31 21 22 26 30 9 4 7 6 – – 10 1

Content 658 437 410 160 156 27 18 20 42 15 58 67 – Content 260 123 78 83 63 48 17 17 24 20 9 13 –

Deal comparison 449 101 51 121 39 50 79 37 26 13 51 3 – Deal comparison 85 34 7 42 14 21 19 23 8 11 15 4 –

Directories 805 67 1 1,697 9 128 18 54 1 42 24 4 – Directories 69 28 1 53 10 21 14 28 1 11 9 5 –

Semiconductors 4 25 20 7 6 2 2 – 108 39 – – – Semiconductors 2 6 4 2 2 1 2 – 18 5 – 5 –

Consumer productivity 129 65 44 78 48 15 – 12 5 18 0 4 – Consumer productivity 41 20 21 20 14 8 1 8 7 11 4 2 –

Other (overlap) 3,407 2,203 162 427 3,010 501 336 408 384 385 816 215 203 Other (overlap) 728 425 21 275 195 33 89 105 53 103 96 9 15

TOTAL 11,324 4,990 3,179 5,720 3,717 1,234 1,038 714 1,034 713 1,040 388 301 TOTAL 2,489 1,145 506 974 501 372 318 321 234 245 190 95 32

Revenue source London Paris Tel Aviv-YafoBerlin Stockholm AmsterdamBarcelona Madrid Dublin Helsinki Moscow Zurich Geneva London Paris Tel Aviv-YafoBerlin Stockholm AmsterdamBarcelona Madrid Dublin Helsinki Moscow Zurich Geneva

Subscription 4,007 1,993 1,587 1,296 2,320 486 278 99 489 121 135 161 215 Subscription 922 365 286 304 166 215 95 77 108 83 46 32 11

Commission 4,234 1,267 965 2,640 645 473 472 294 68 137 384 131 – Commission 703 306 80 291 104 93 112 92 33 42 42 11 4

Manufacturing 852 809 238 304 295 144 65 29 225 154 12 126 73 Manufacturing 90 100 31 58 47 31 19 8 33 28 10 22 4

eCommerce 1,006 866 42 1,196 129 29 303 20 18 6 335 10 – eCommerce 222 115 21 153 46 24 42 48 7 15 20 3 –

Freemium 790 327 391 461 2,144 51 90 64 10 209 182 11 8 Freemium 287 66 76 101 60 56 27 36 13 38 14 11 5

Classified listing 496 133 3 394 10 4 383 91 3 1 237 1 – Classified listing 99 39 3 55 11 8 37 15 2 2 12 2 –

Advertising 544 287 89 104 81 50 19 13 26 39 52 9 – Advertising 168 74 22 55 34 18 18 7 15 12 7 8 –

Other (overlap) (605) (691) (137) (675) (1,907) (3) (573) 103 195 46 (297) (61) 4 Other (overlap) (2) 80 (13) (43) 33 (73) (32) 38 23 25 39 6 8

TOTAL 11,324 4,990 3,179 5,720 3,717 1,234 1,038 714 1,034 713 1,040 388 301 TOTAL 2,489 1,145 506 974 501 372 318 321 234 245 190 95 32

End-user focus London Paris Tel Aviv-YafoBerlin Stockholm AmsterdamBarcelona Madrid Dublin Helsinki Moscow Zurich Geneva London Paris Tel Aviv-YafoBerlin Stockholm AmsterdamBarcelona Madrid Dublin Helsinki Moscow Zurich Geneva

Consumer 4,816 2,382 1,042 4,624 2,573 324 562 313 138 316 775 106 82 Consumer 1,094 490 153 537 235 139 141 156 68 89 108 34 10

Business 5,487 2,295 2,072 1,024 995 861 404 311 869 342 151 277 216 Business 1,159 575 333 385 213 200 142 143 155 103 52 56 20

Other 1,021 313 65 72 149 50 72 90 27 55 114 5 2 Other 236 80 20 52 53 33 35 22 11 53 30 5 2

TOTAL 11,324 4,990 3,179 5,720 3,717 1,234 1,038 714 1,034 713 1,040 388 301 TOTAL 2,489 1,145 506 974 501 372 318 321 234 245 190 95 32

1. Introduction: headline stats in Europe

2. Insights: understanding the key trends and drivers

3. Top verticals and business models

4. Investment sources trends

5. Overviews of top countries

6. Outtakes: additional data

Contents

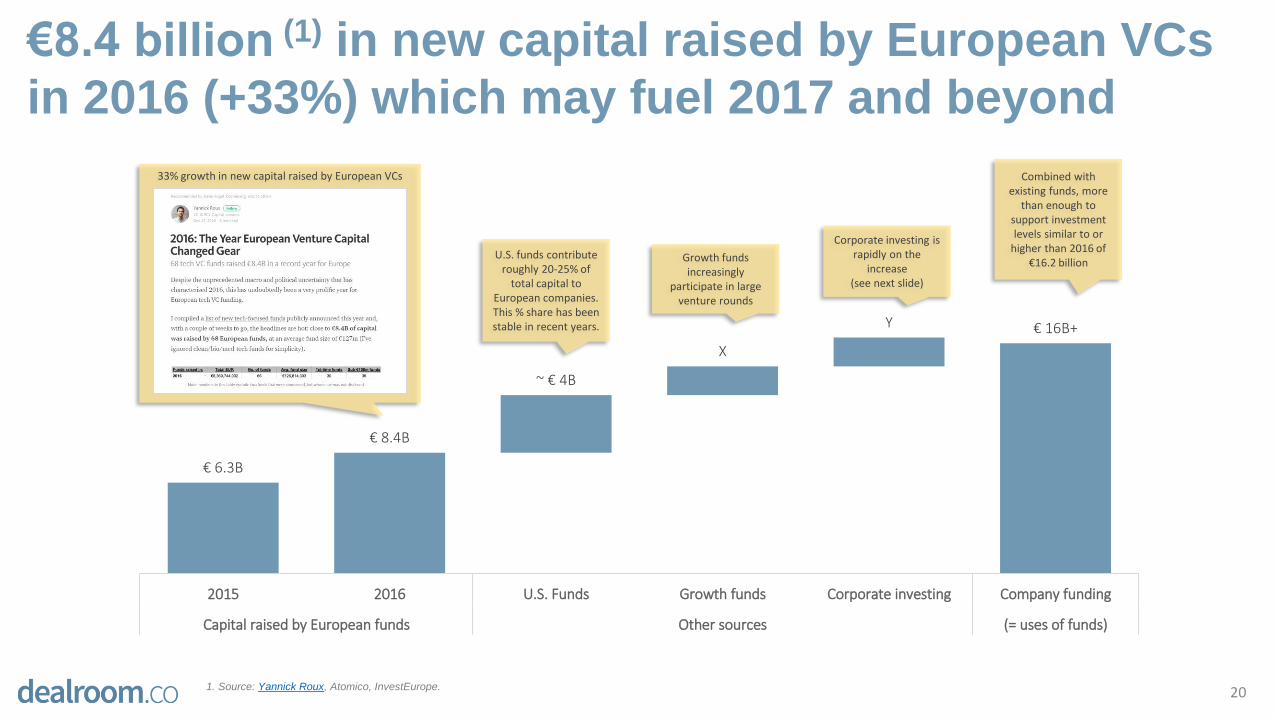

€ 6.3B

€ 8.4B

~ € 4B

X

Y € 16B+

2015 2016 U.S. Funds Growth funds Corporate investing Company funding

Capital raised by European funds Other sources (= uses of funds)

€8.4 billion (1) in new capital raised by European VCs

in 2016 (+33%) which may fuel 2017 and beyond

201. Source: Yannick Roux, Atomico, InvestEurope.

33% growth in new capital raised by European VCs

U.S. funds contribute roughly 20-25% of

total capital to European companies. This % share has been stable in recent years.

Growth funds increasingly

participate in large venture rounds

Corporate investing is rapidly on the

increase (see next slide)

Combined with existing funds, more

than enough to support investment levels similar to or

higher than 2016 of €16.2 billion

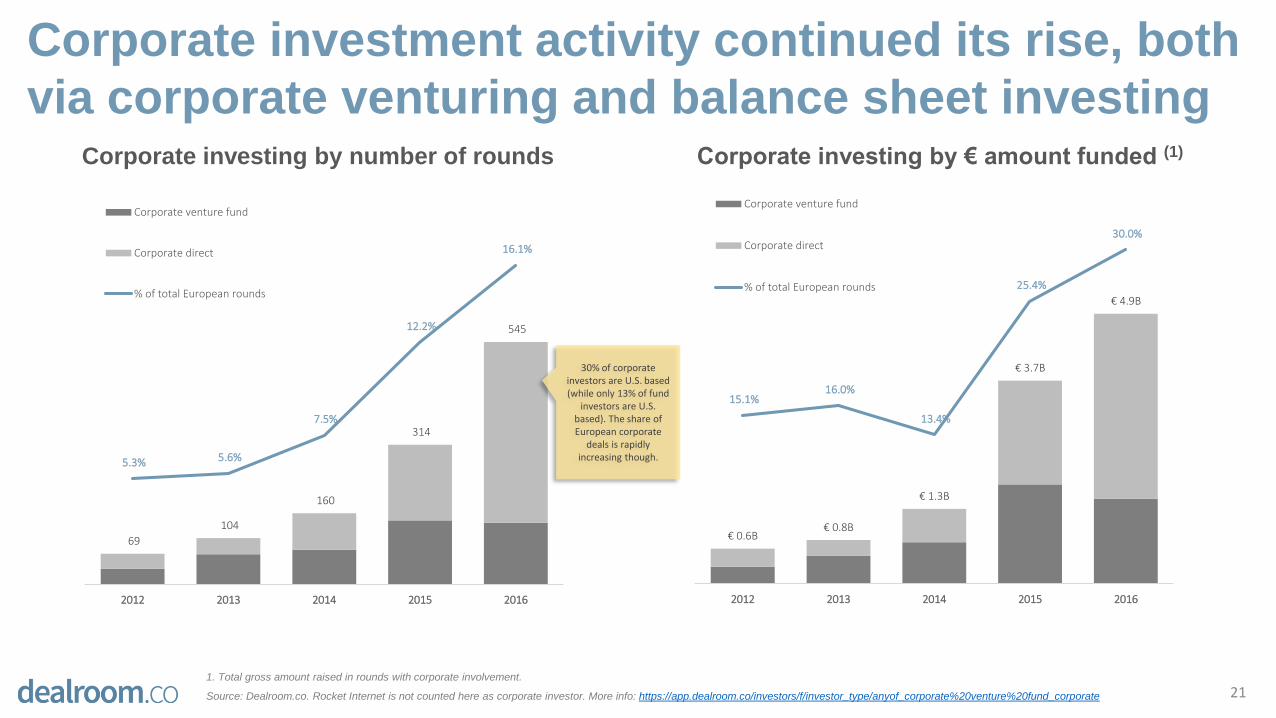

Corporate investment activity continued its rise, both

via corporate venturing and balance sheet investing

211. Total gross amount raised in rounds with corporate involvement.

Source: Dealroom.co. Rocket Internet is not counted here as corporate investor. More info: https://app.dealroom.co/investors/f/investor_type/anyof_corporate%20venture%20fund_corporate

Corporate investing by number of rounds Corporate investing by € amount funded (1)

69

104

160

314

545

5.3% 5.6%

7.5%

12.2%

16.1%

2012 2013 2014 2015 2016

Corporate venture fund

Corporate direct

% of total European rounds

€ 0.6B€ 0.8B

€ 1.3B

€ 3.7B

€ 4.9B

15.1% 16.0%

13.4%

25.4%

30.0%

2012 2013 2014 2015 2016

Corporate venture fund

Corporate direct

% of total European rounds

30% of corporate investors are U.S. based (while only 13% of fund

investors are U.S. based). The share of European corporate

deals is rapidly increasing though.

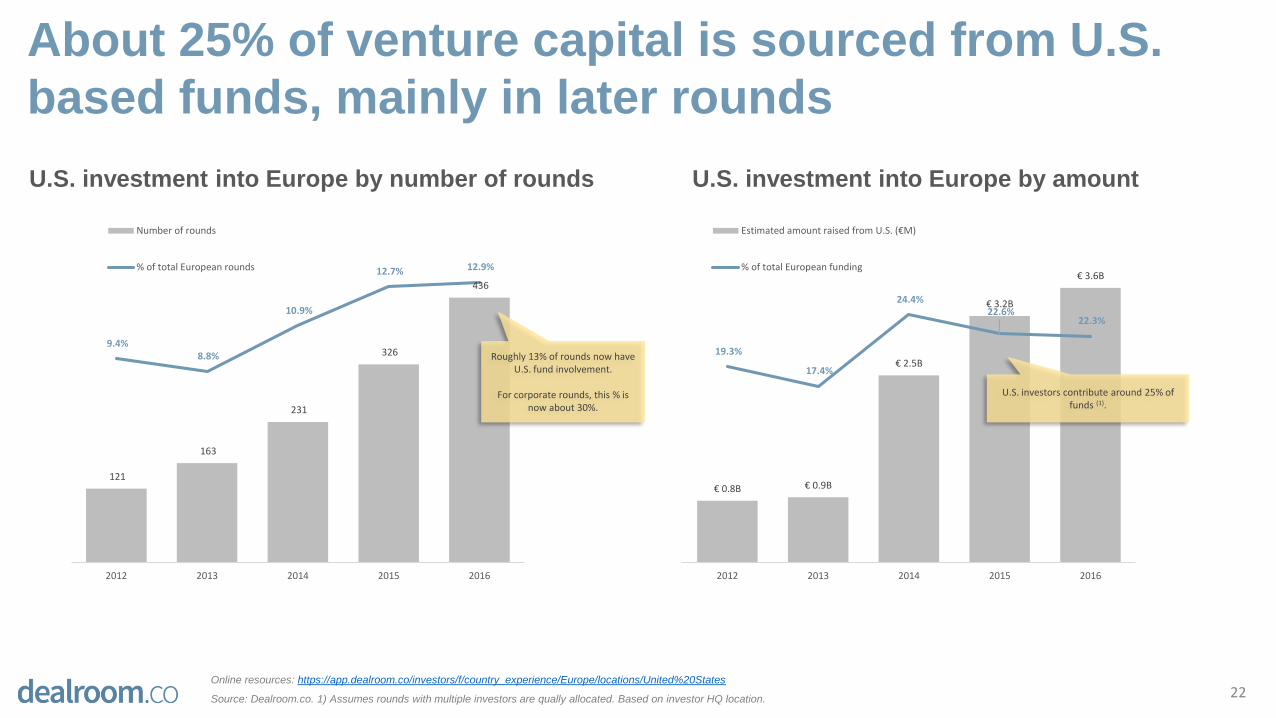

About 25% of venture capital is sourced from U.S.

based funds, mainly in later rounds

22Online resources: https://app.dealroom.co/investors/f/country_experience/Europe/locations/United%20States

Source: Dealroom.co. 1) Assumes rounds with multiple investors are qually allocated. Based on investor HQ location.

121

163

231

326

436

9.4% 8.8%

10.9%

12.7% 12.9%

2012 2013 2014 2015 2016

Number of rounds

% of total European rounds

U.S. investment into Europe by number of rounds U.S. investment into Europe by amount

€ 0.8B € 0.9B

€ 2.5B

€ 3.2B

€ 3.6B

19.3%

17.4%

24.4% 22.6%

22.3%

2012 2013 2014 2015 2016

Estimated amount raised from U.S. (€M)

% of total European funding

Roughly 13% of rounds now have U.S. fund involvement.

For corporate rounds, this % is now about 30%.

U.S. investors contribute around 25% of funds (1).

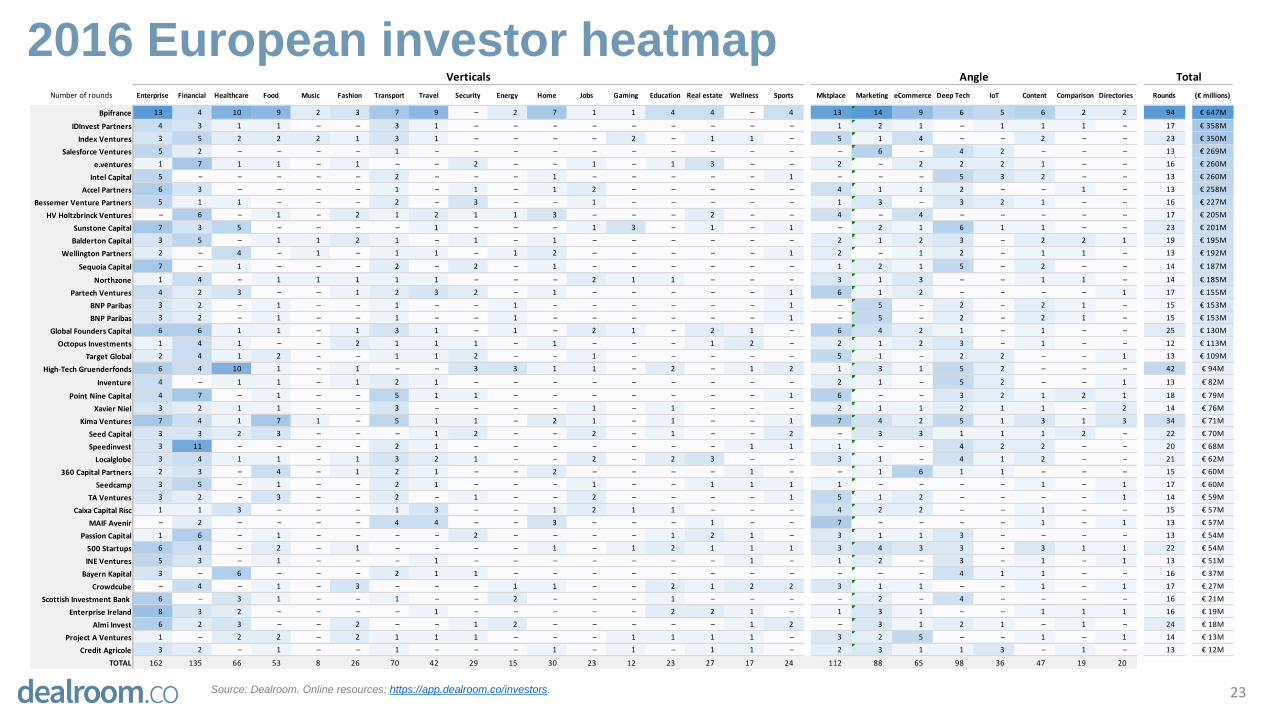

2016 European investor heatmap

23Source: Dealroom. Online resources: https://app.dealroom.co/investors.

Verticals Angle Total

Number of rounds Enterprise Financial Healthcare Food Music Fashion Transport Travel Security Energy Home Jobs Gaming Education Real estate Wellness Sports Mktplace Marketing eCommerce Deep Tech IoT Content Comparison Directories Rounds (€ millions)

Bpifrance 13 4 10 9 2 3 7 9 – 2 7 1 1 4 4 – 4 13 14 9 6 5 6 2 2 94 € 647M

IDInvest Partners 4 3 1 1 – – 3 1 – – – – – – – – – 1 2 1 – 1 1 1 – 17 € 358M

Index Ventures 3 5 2 2 2 1 3 1 – – – – 2 – 1 1 – 5 1 4 – – 2 – – 23 € 350M

Salesforce Ventures 5 2 – – – – 1 – – – – – – – – – – – 6 – 4 2 – – – 13 € 269M

e.ventures 1 7 1 1 – 1 – – 2 – – 1 – 1 3 – – 2 – 2 2 2 1 – – 16 € 260M

Intel Capital 5 – – – – – 2 – – – 1 – – – – – 1 – – – 5 3 2 – – 13 € 260M

Accel Partners 6 3 – – – – 1 – 1 – 1 2 – – – – – 4 1 1 2 – – 1 – 13 € 258M

Bessemer Venture Partners 5 1 1 – – – 2 – 3 – – 1 – – – – – 1 3 – 3 2 1 – – 16 € 227M

HV Holtzbrinck Ventures – 6 – 1 – 2 1 2 1 1 3 – – – 2 – – 4 – 4 – – – – – 17 € 205M

Sunstone Capital 7 3 5 – – – – 1 – – – 1 3 – 1 – 1 – 2 1 6 1 1 – – 23 € 201M

Balderton Capital 3 5 – 1 1 2 1 – 1 – 1 – – – – – – 2 1 2 3 – 2 2 1 19 € 195M

Wellington Partners 2 – 4 – 1 – 1 1 – 1 2 – – – – – 1 2 – 1 2 – 1 1 – 13 € 192M

Sequoia Capital 7 – 1 – – – 2 – 2 – 1 – – – – – – 1 2 1 5 – 2 – – 14 € 187M

Northzone 1 4 – 1 1 1 1 1 – – – 2 1 1 – – – 3 1 3 – – 1 1 – 14 € 185M

Partech Ventures 4 2 3 – – 1 2 3 2 – 1 – – – – – 1 6 1 2 – – – – 1 17 € 155M

BNP Paribas 3 2 – 1 – – 1 – – 1 – – – – – – 1 – 5 – 2 – 2 1 – 15 € 153M

BNP Paribas 3 2 – 1 – – 1 – – 1 – – – – – – 1 – 5 – 2 – 2 1 – 15 € 153M

Global Founders Capital 6 6 1 1 – 1 3 1 – 1 – 2 1 – 2 1 – 6 4 2 1 – 1 – – 25 € 130M

Octopus Investments 1 4 1 – – 2 1 1 1 – 1 – – – 1 2 – 2 1 2 3 – 1 – – 12 € 113M

Target Global 2 4 1 2 – – 1 1 2 – – 1 – – – – – 5 1 – 2 2 – – 1 13 € 109M

High-Tech Gruenderfonds 6 4 10 1 – 1 – – 3 3 1 1 – 2 – 1 2 1 3 1 5 2 – – – 42 € 94M

Inventure 4 – 1 1 – 1 2 1 – – – – – – – – – 2 1 – 5 2 – – 1 13 € 82M

Point Nine Capital 4 7 – 1 – – 5 1 1 – – – – – – – 1 6 – – 3 2 1 2 1 18 € 79M

Xavier Niel 3 2 1 1 – – 3 – – – – 1 – 1 – – – 2 1 1 2 1 1 – 2 14 € 76M

Kima Ventures 7 4 1 7 1 – 5 1 1 – 2 1 – 1 – – 1 7 4 2 5 1 3 1 3 34 € 71M

Seed Capital 3 3 2 3 – – – 1 2 – – 2 – 1 – – 2 – 3 3 1 1 1 2 – 22 € 70M

Speedinvest 3 11 – – – – 2 1 – – – – – – – 1 1 1 – – 4 2 2 – – 20 € 68M

Localglobe 3 4 1 1 – 1 3 2 1 – – 2 – 2 3 – – 3 1 – 4 1 2 – – 21 € 62M

360 Capital Partners 2 3 – 4 – 1 2 1 – – 2 – – – – 1 – – 1 6 1 1 – – – 15 € 60M

Seedcamp 3 5 – 1 – – 2 1 – – – 1 – – 1 1 1 1 – – – – 1 – 1 17 € 60M

TA Ventures 3 2 – 3 – – 2 – 1 – – 2 – – – – 1 5 1 2 – – – – 1 14 € 59M

Caixa Capital Risc 1 1 3 – – – 1 3 – – 1 2 1 1 – – – 4 2 2 – – 1 – – 15 € 57M

MAIF Avenir – 2 – – – – 4 4 – – 3 – – – 1 – – 7 – – – – 1 – 1 13 € 57M

Passion Capital 1 6 – 1 – – – – 2 – – – – 1 2 1 – 3 1 1 3 – – – – 13 € 54M

500 Startups 6 4 – 2 – 1 – – – – 1 – 1 2 1 1 1 3 4 3 3 – 3 1 1 22 € 54M

INE Ventures 5 3 – 1 – – – 1 – – – – – – – 1 – 1 2 – 3 – 1 – 1 13 € 51M

Bayern Kapital 3 – 6 – – – 2 1 1 – – – – – – – – – – – 4 1 1 – – 16 € 37M

Crowdcube – 4 – 1 – 3 – – – 1 1 – – 2 1 2 2 3 1 1 – – 1 – 1 17 € 27M

Scottish Investment Bank 6 – 3 1 – – 1 – – 2 – – – 1 – – – – 2 – 4 – – – – 16 € 21M

Enterprise Ireland 8 3 2 – – – – 1 – – – – – 2 2 1 – 1 3 1 – – 1 1 1 16 € 19M

Almi Invest 6 2 3 – – 2 – – 1 2 – – – – – 1 2 – 3 1 2 1 – 1 – 24 € 18M

Project A Ventures 1 – 2 2 – 2 1 1 1 – – – 1 1 1 1 – 3 2 5 – – 1 – 1 14 € 13M

Credit Agricole 3 2 – 1 – – 1 – – – 1 – 1 – 1 1 – 2 3 1 1 3 – 1 – 13 € 12M

TOTAL 162 135 66 53 8 26 70 42 29 15 30 23 12 23 27 17 24 112 88 65 98 36 47 19 20

1. Introduction: headline stats in Europe

2. Insights: understanding the key trends and drivers

3. Top verticals and business models

4. Investment sources trends

5. Overviews of top countries

6. Outtakes: additional data

Contents

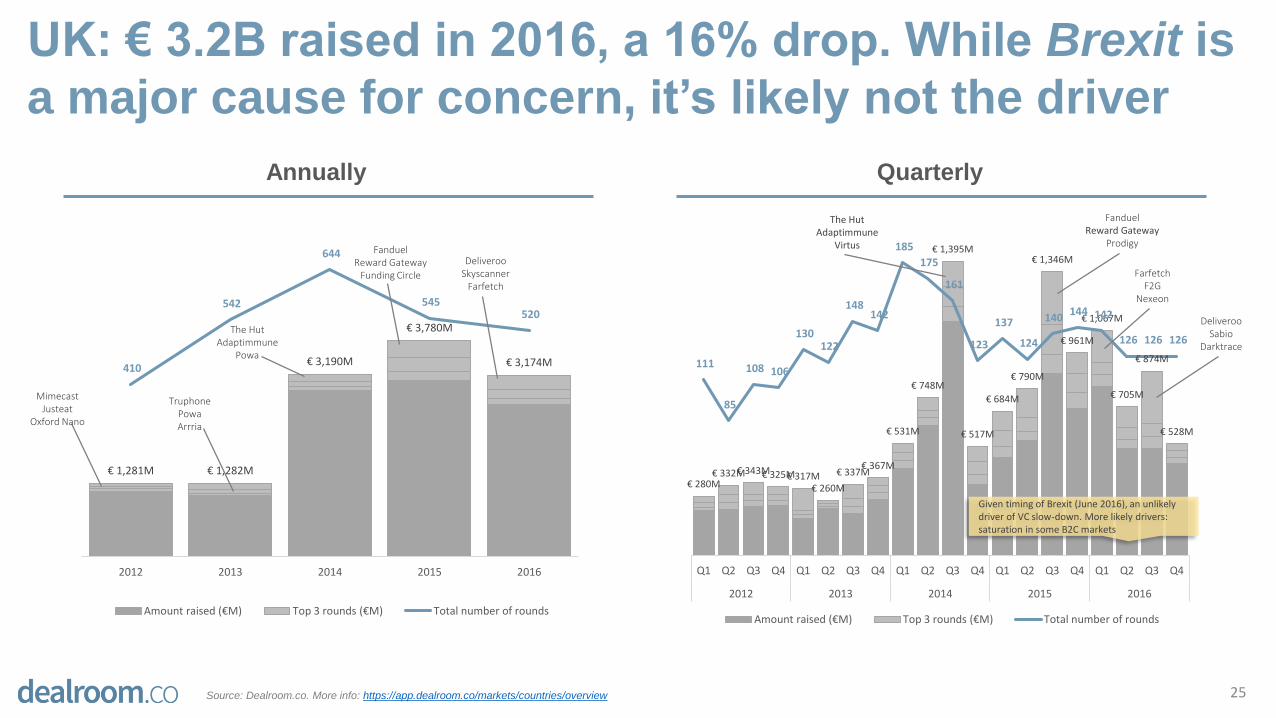

UK: € 3.2B raised in 2016, a 16% drop. While Brexit is

a major cause for concern, it’s likely not the driver

25Source: Dealroom.co. More info: https://app.dealroom.co/markets/countries/overview

€ 1,281M € 1,282M

€ 3,190M

€ 3,780M

€ 3,174M410

542

644

545 520

2012 2013 2014 2015 2016

Amount raised (€M) Top 3 rounds (€M) Total number of rounds

€ 280M€ 332M€ 343M€ 325M€ 317M

€ 260M

€ 337M€ 367M

€ 531M

€ 748M

€ 1,395M

€ 517M

€ 684M

€ 790M

€ 1,346M

€ 961M

€ 1,067M

€ 705M

€ 874M

€ 528M

111

85

108 106

130 122

148 142

185

175

161

123

137

124

140 144 142

126 126 126

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015 2016

Amount raised (€M) Top 3 rounds (€M) Total number of rounds

QuarterlyAnnually

Given timing of Brexit (June 2016), an unlikely driver of VC slow-down. More likely drivers: saturation in some B2C markets

TruphonePowaArrria

MimecastJusteat

Oxford Nano

The HutAdaptimmune

Powa

FanduelReward Gateway

Funding Circle

DeliverooSkyscanner

Farfetch

FanduelReward Gateway

Prodigy

DeliverooSabio

Darktrace

FarfetchF2G

Nexeon

The HutAdaptimmune

Virtus

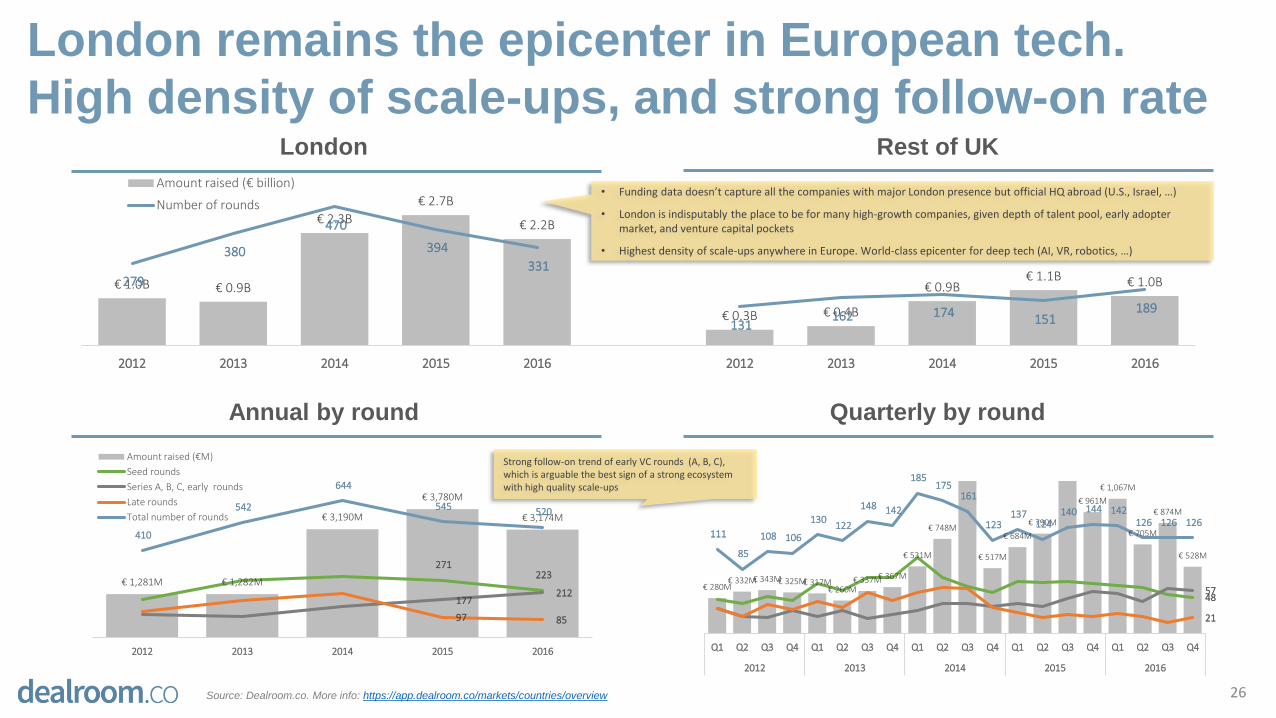

London remains the epicenter in European tech.

High density of scale-ups, and strong follow-on rate

26

Rest of UKLondon

Quarterly by roundAnnual by round

€ 280M€ 332M€ 343M€ 325M€ 317M

€ 260M€ 337M€ 367M

€ 531M

€ 748M

€ 517M

€ 684M

€ 790M

€ 961M

€ 1,067M

€ 705M

€ 874M

€ 528M

48 57

21

111

85

108 106

130 122

148 142

185 175

161

123 137

124 140 144 142

126 126 126

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015 2016

€ 1,281M € 1,282M

€ 3,190M

€ 3,780M

€ 3,174M

271 223

177 212

97 85

410

542

644

545 520

2012 2013 2014 2015 2016

Amount raised (€M)

Seed rounds

Series A, B, C, early rounds

Late rounds

Total number of rounds

Strong follow-on trend of early VC rounds (A, B, C), which is arguable the best sign of a strong ecosystem with high quality scale-ups

€ 1.0B € 0.9B

€ 2.3B

€ 2.7B

€ 2.2B

€ 0.3B € 0.4B

€ 0.9B€ 1.1B € 1.0B279

380

470

394

331

131 162 174 151

189

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

Amount raised (€ billion)

Number of rounds• Funding data doesn’t capture all the companies with major London presence but official HQ abroad (U.S., Israel, …)

• London is indisputably the place to be for many high-growth companies, given depth of talent pool, early adopter market, and venture capital pockets

• Highest density of scale-ups anywhere in Europe. World-class epicenter for deep tech (AI, VR, robotics, …)

Source: Dealroom.co. More info: https://app.dealroom.co/markets/countries/overview

Germany: € 2.0B raised in 2016, a 32% drop due to

lack of Rocket mega-rounds, and limited replacement

27

QuarterlyAnnual

€ 593M € 583M

€ 1,981M

€ 2,909M

€ 1,985M

165

245

288

353 380

2012 2013 2014 2015 2016

Top 3 rounds (€M)

Amount raised (€M)

Total number of rounds

€ 142M€ 143M€ 210M

€ 97M€ 126M€ 188M€ 169M

€ 100M

€ 324M€ 397M

€ 1,001M

€ 259M

€ 1,259M

€ 653M€ 564M

€ 433M

€ 324M

€ 788M

€ 460M€ 413M

44

32

45 44 50

65 67 63

74 72 74 68

89

58

102 104

114

98 94

74

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015 2016

Rocket InternetDelivery Hero

Westwing

In recent years, Germany has been characterized by mega rounds, thus heavily skewing the results. Rocket backed Jumia is based in Paris.

Delivery HeroGlobal Fashion

Home24

Round types - quarterlyRound types - annual

€ 142M€ 143M€ 210M

€ 97M€ 126M€ 188M€ 169M

€ 100M

€ 324M€ 397M

€ 1,001M

€ 259M

€ 1,259M

€ 653M€ 564M

€ 433M€ 324M

€ 788M

€ 460M€ 413M

35 29

10

44 32

45 44 50 65 67 63

74 72 74 68 89

58

102 104 114

98 94 74

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015 2016

€ 593M € 583M

€ 1,981M

€ 2,909M

€ 1,985M

154 188

110 122 89 70

165

245 288

353 380

2012 2013 2014 2015 2016

Amount raised (€M)Seed roundsSeries A, B, C, early roundsLate roundsTotal number of rounds

Global FashionSoundCloudHelloFresh

Rocket InternetDelivery Hero

FoodPanda

Delivery HeroHelloFreshFoodPanda

Global FashionSoundCloud

Source: Dealroom.co. More info: https://app.dealroom.co/markets/countries/overview

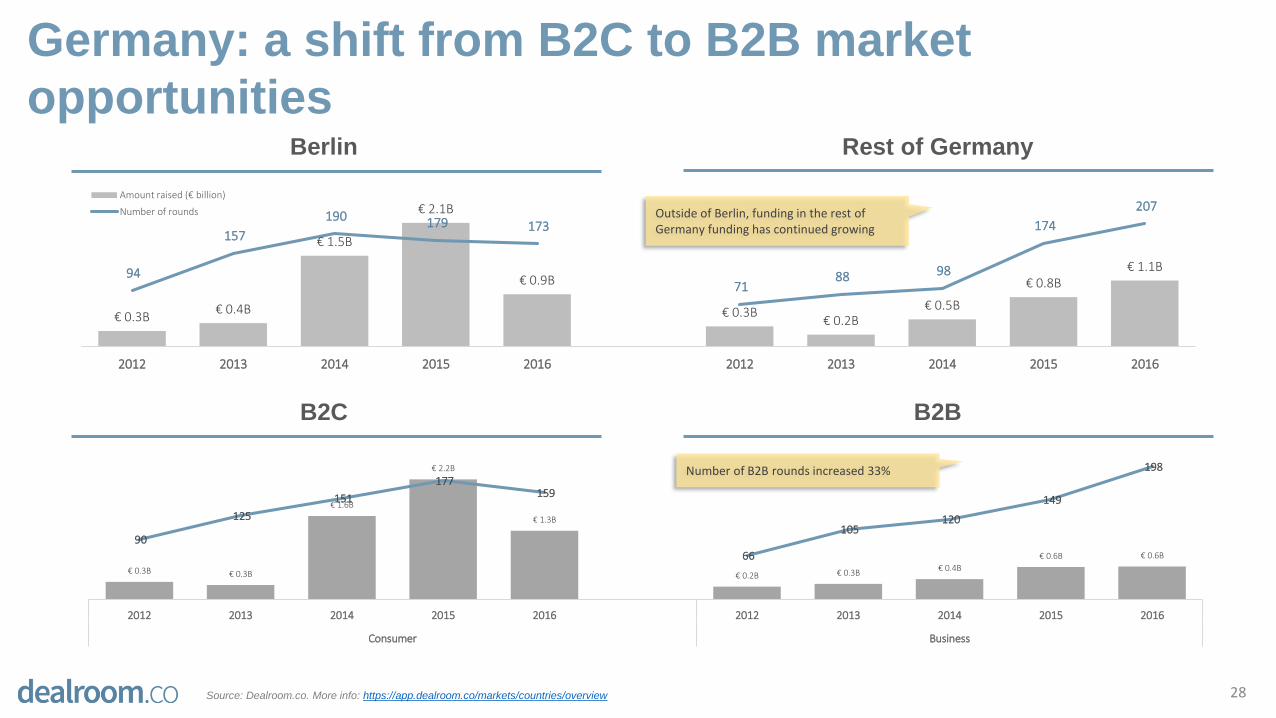

Germany: a shift from B2C to B2B market

opportunities

28

Rest of GermanyBerlin

B2BB2C

€ 0.3B€ 0.4B

€ 1.5B

€ 2.1B

€ 0.9B

€ 0.3B€ 0.2B

€ 0.5B

€ 0.8B€ 1.1B94

157

190 179 173

71 88 98

174

207

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

Amount raised (€ billion)

Number of rounds Outside of Berlin, funding in the rest of Germany funding has continued growing

€ 0.3B € 0.3B

€ 1.6B

€ 2.2B

€ 1.3B

€ 0.2B € 0.3B€ 0.4B

€ 0.6B € 0.6B

90

125

151

177 159

66

105 120

149

198

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

Consumer Business

Number of B2B rounds increased 33%

Source: Dealroom.co. More info: https://app.dealroom.co/markets/countries/overview

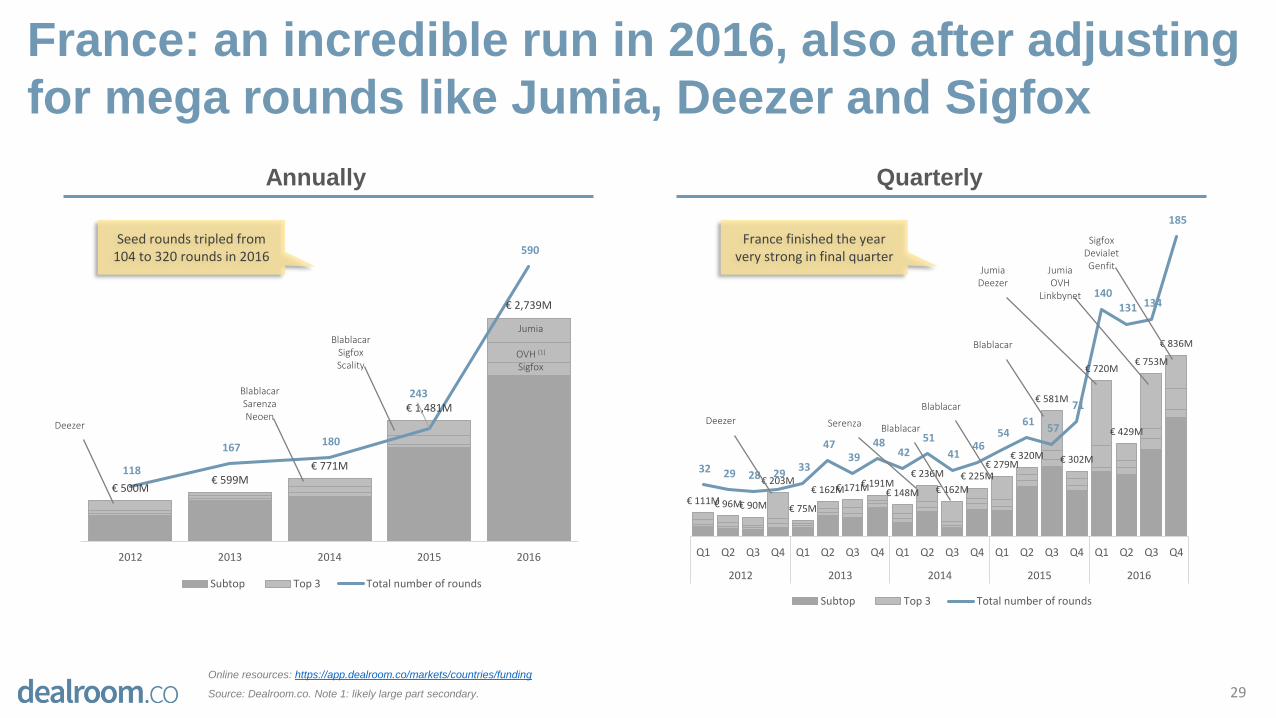

France: an incredible run in 2016, also after adjusting

for mega rounds like Jumia, Deezer and Sigfox

29Online resources: https://app.dealroom.co/markets/countries/funding

Source: Dealroom.co. Note 1: likely large part secondary.

QuarterlyAnnually

€ 500M€ 599M

€ 771M

€ 1,481M

€ 2,739M

118

167 180

243

590

2012 2013 2014 2015 2016

Subtop Top 3 Total number of rounds

€ 111M€ 96M€ 90M

€ 203M

€ 75M

€ 162M€ 171M€ 191M€ 148M

€ 236M

€ 162M

€ 225M€ 279M

€ 320M

€ 581M

€ 302M

€ 720M

€ 429M

€ 753M

€ 836M

32 29 28 29 33

47 39

48 42

51

41 46

54 61

57

71

140 131 134

185

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015 2016

Subtop Top 3 Total number of rounds

BlablacarSigfoxScality

Jumia

OVH (1)

Sigfox

BlablacarSarenzaNeoen

Deezer

Blablacar

JumiaDeezer

JumiaOVH

Linkbynet

SigfoxDevialetGenfit

France finished the year very strong in final quarter

Seed rounds tripled from 104 to 320 rounds in 2016

Blablacar

BlablacarDeezer Serenza

€ 0.4B € 0.3B€ 0.5B

€ 0.9B

€ 1.7B

€ 0.1B€ 0.3B € 0.3B

€ 0.6B

€ 1.1B

84 109 118

146

293

34 58 62

97

297

2012 2013 2014 2015 2016 2012 2013 2014 2015 2016

Amount raised (€ billion) Number of rounds

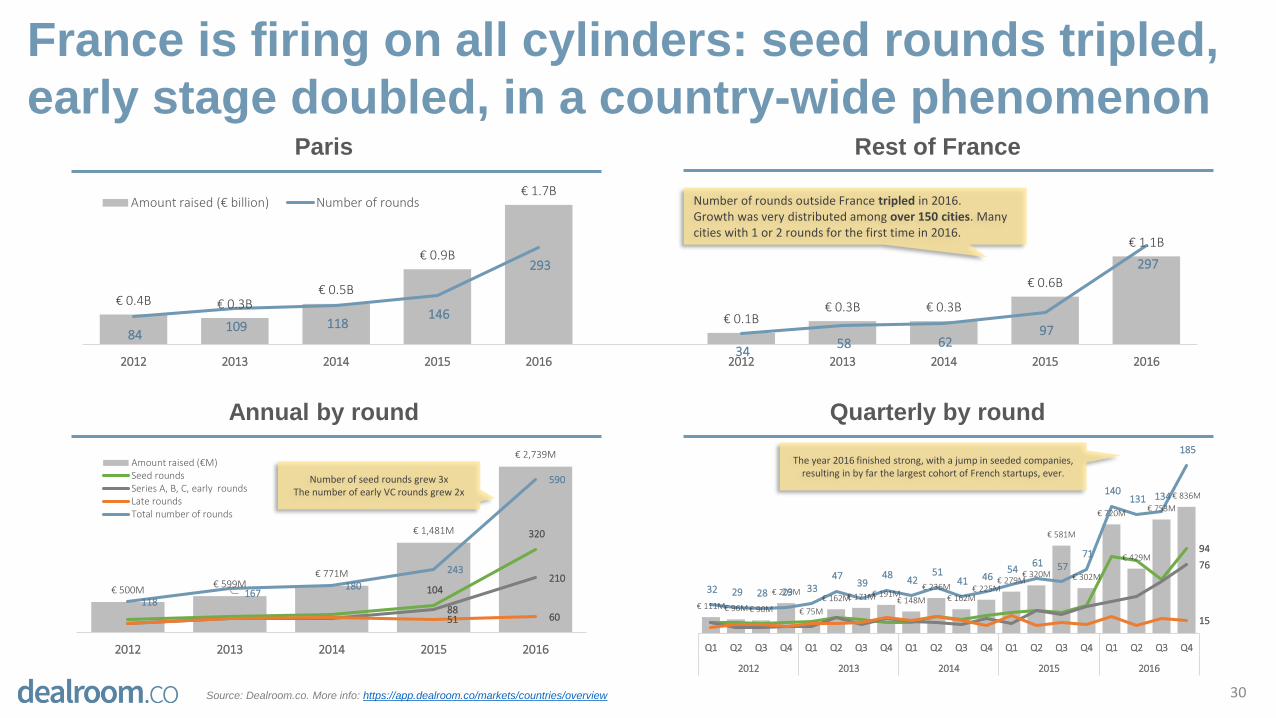

France is firing on all cylinders: seed rounds tripled,

early stage doubled, in a country-wide phenomenon

30

Rest of FranceParis

Number of rounds outside France tripled in 2016.Growth was very distributed among over 150 cities. Many cities with 1 or 2 rounds for the first time in 2016.

€ 111M€ 96M € 90M

€ 203M

€ 75M

€ 162M€ 171M€ 191M€ 148M

€ 236M€ 162M

€ 225M€ 279M

€ 320M

€ 581M

€ 302M

€ 720M

€ 429M

€ 753M

€ 836M

94

76

15

32 29 28 29 33 47

39 48

42 51

41 46 54

61 57 71

140 131 134

185

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015 2016

€ 500M€ 599M

€ 771M

€ 1,481M

€ 2,739M

104

320

88

210

51 60

118 167

180

243

590

2012 2013 2014 2015 2016

Amount raised (€M)Seed roundsSeries A, B, C, early roundsLate roundsTotal number of rounds

Quarterly by roundAnnual by round

Number of seed rounds grew 3xThe number of early VC rounds grew 2x

The year 2016 finished strong, with a jump in seeded companies, resulting in by far the largest cohort of French startups, ever.

Source: Dealroom.co. More info: https://app.dealroom.co/markets/countries/overview

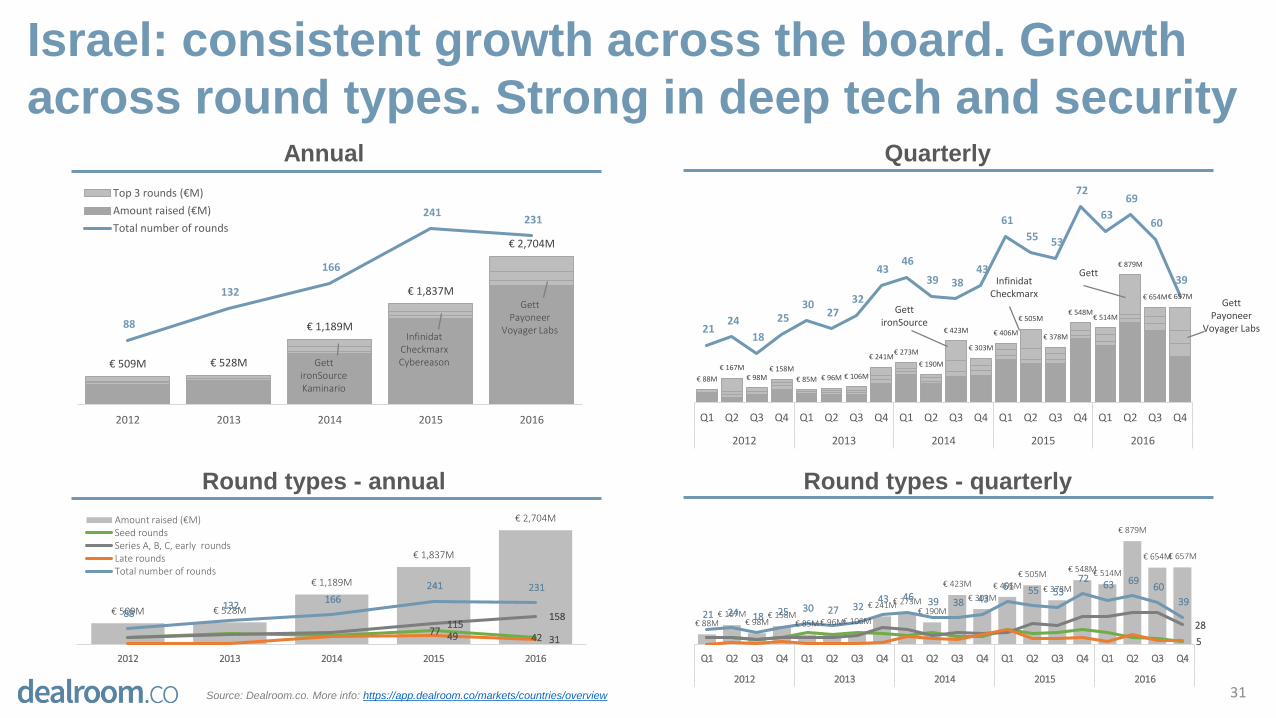

Israel: consistent growth across the board. Growth

across round types. Strong in deep tech and security

31

QuarterlyAnnual

Round types - quarterlyRound types - annual

€ 88M€ 167M

€ 98M€ 158M

€ 85M € 96M€ 106M

€ 241M€ 273M€ 190M

€ 423M

€ 303M

€ 406M

€ 505M

€ 378M

€ 548M€ 514M

€ 879M

€ 654M€ 657M

5

28 21 24 18 25 30 27 32

43 46 39 38 43 61 55 53

72 63 69

60

39

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015 2016

€ 509M € 528M

€ 1,189M

€ 1,837M

€ 2,704M

77 42

115 158

49 31

88 132

166

241 231

2012 2013 2014 2015 2016

Amount raised (€M)Seed roundsSeries A, B, C, early roundsLate roundsTotal number of rounds

€ 509M € 528M

€ 1,189M

€ 1,837M

€ 2,704M

88

132

166

241 231

2012 2013 2014 2015 2016

Top 3 rounds (€M)

Amount raised (€M)

Total number of rounds

€ 88M

€ 167M

€ 98M€ 158M

€ 85M € 96M € 106M

€ 241M€ 273M

€ 190M

€ 423M

€ 303M

€ 406M

€ 505M

€ 378M

€ 548M€ 514M

€ 879M

€ 654M€ 657M

21 24

18

25 30

27 32

43 46

39 38 43

61

55 53

72

63

69

60

39

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015 2016

GettPayoneer

Voyager LabsInfinidat

CheckmarxCybereasonGett

ironSourceKaminario

GettironSource

InfinidatCheckmarx

Gett

GettPayoneer

Voyager Labs

Source: Dealroom.co. More info: https://app.dealroom.co/markets/countries/overview

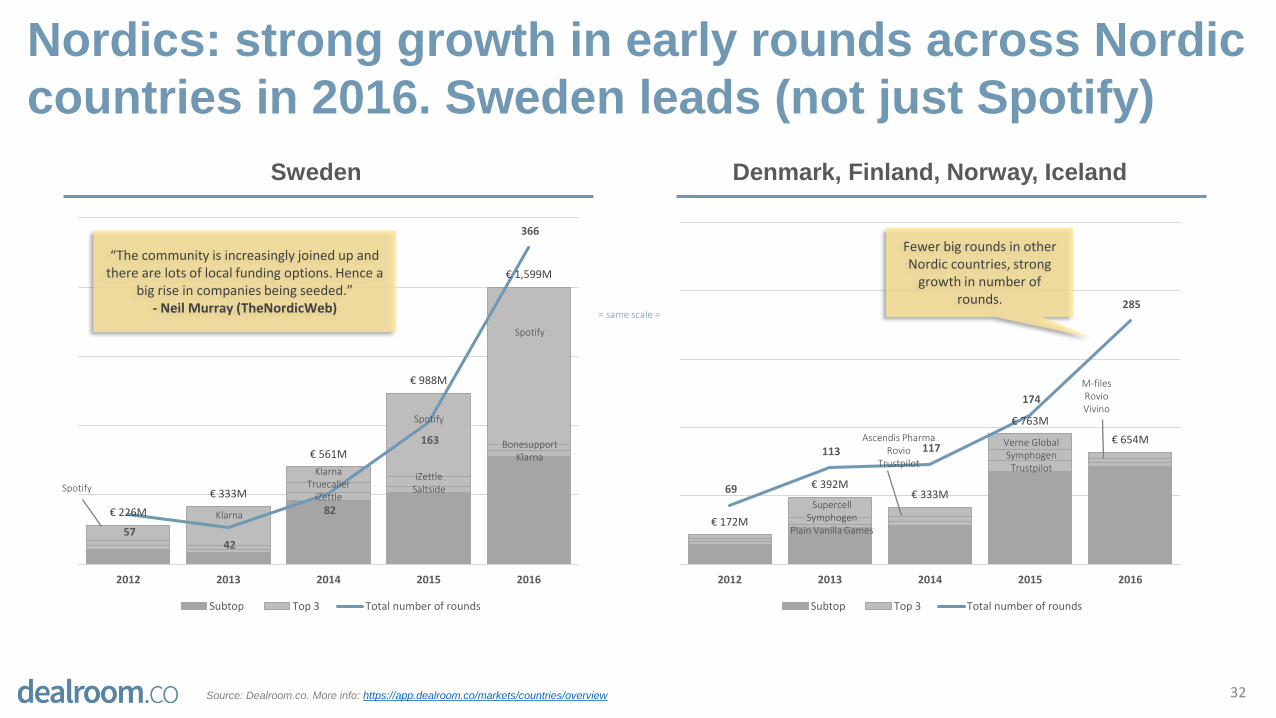

Nordics: strong growth in early rounds across Nordic

countries in 2016. Sweden leads (not just Spotify)

32

Denmark, Finland, Norway, IcelandSweden

€ 226M

€ 333M

€ 561M

€ 988M

€ 1,599M

57 42

82

163

366

2012 2013 2014 2015 2016

Subtop Top 3 Total number of rounds

€ 172M

€ 392M€ 333M

€ 763M

€ 654M

69

113 117

174

285

2012 2013 2014 2015 2016

Subtop Top 3 Total number of rounds

Spotify

Spotify

Spotify

KlarnaTruecaller

iZettle

Klarna

iZettleSaltside

BonesupportKlarna

Verne GlobalSymphogenTrustpilot

M-filesRovioVivino

Ascendis PharmaRovio

Trustpilot

Fewer big rounds in other Nordic countries, strong

growth in number of rounds.

SupercellSymphogen

Plain Vanilla Games

“The community is increasingly joined up and there are lots of local funding options. Hence a

big rise in companies being seeded.”- Neil Murray (TheNordicWeb) = same scale =

Source: Dealroom.co. More info: https://app.dealroom.co/markets/countries/overview

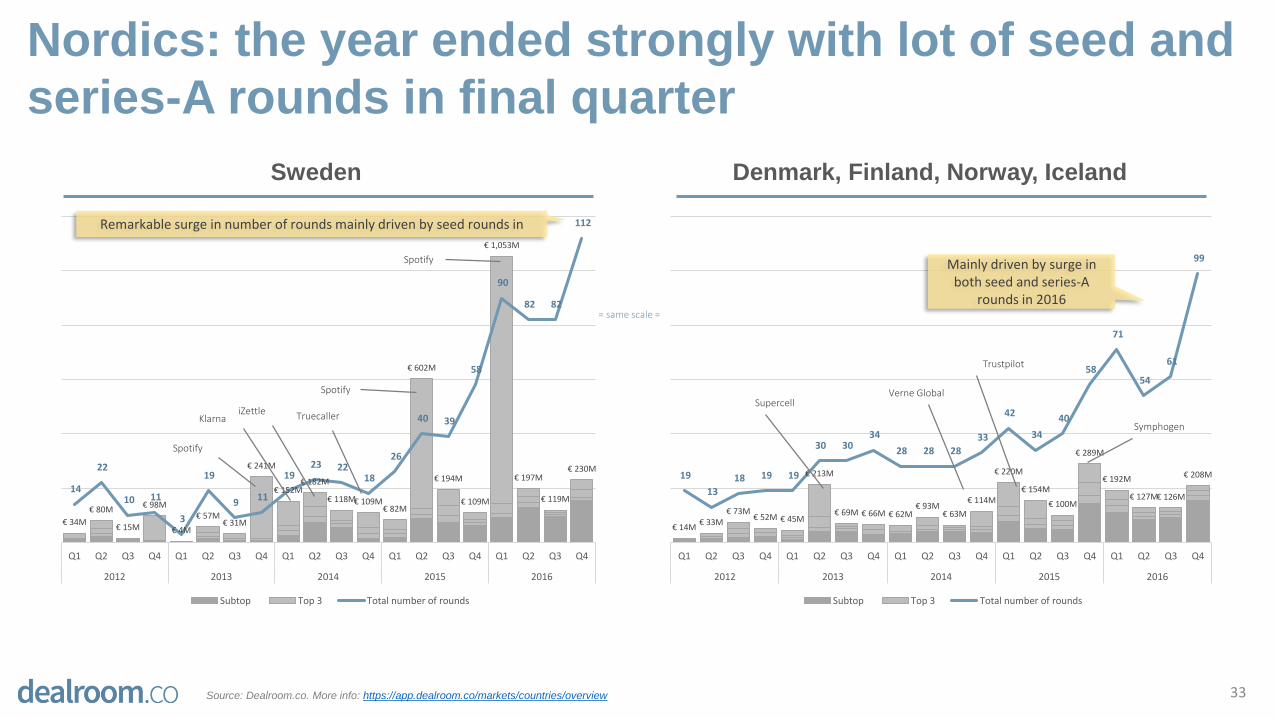

Nordics: the year ended strongly with lot of seed and

series-A rounds in final quarter

33

€ 34M

€ 80M

€ 15M

€ 98M

€ 4M

€ 57M€ 31M

€ 241M

€ 152M€ 182M

€ 118M€ 109M€ 82M

€ 602M

€ 194M

€ 109M

€ 1,053M

€ 197M

€ 119M

€ 230M

14

22

10 11

3

19

9 11

19 23 22

18

26

40 39

58

90

82 82

112

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015 2016

Subtop Top 3 Total number of rounds

€ 14M€ 33M

€ 73M€ 52M € 45M

€ 213M

€ 69M € 66M € 62M€ 93M

€ 63M

€ 114M

€ 220M

€ 154M

€ 100M

€ 289M

€ 192M

€ 127M€ 126M

€ 208M19

13

18 19 19

30 30 34

28 28 28

33

42

34

40

58

71

54

61

99

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015 2016

Subtop Top 3 Total number of rounds

Denmark, Finland, Norway, IcelandSweden

Spotify

Spotify

Symphogen

Spotify

Verne GlobalSupercell

Trustpilot

KlarnaiZettle Truecaller

Remarkable surge in number of rounds mainly driven by seed rounds in

Mainly driven by surge in both seed and series-A

rounds in 2016= same scale =

Source: Dealroom.co. More info: https://app.dealroom.co/markets/countries/overview

1. Introduction: headline stats in Europe

2. Insights: understanding the key trends and drivers

3. Top verticals and business models

4. Investment sources trends

5. Overviews of top countries

6. Outtakes: additional data

Contents

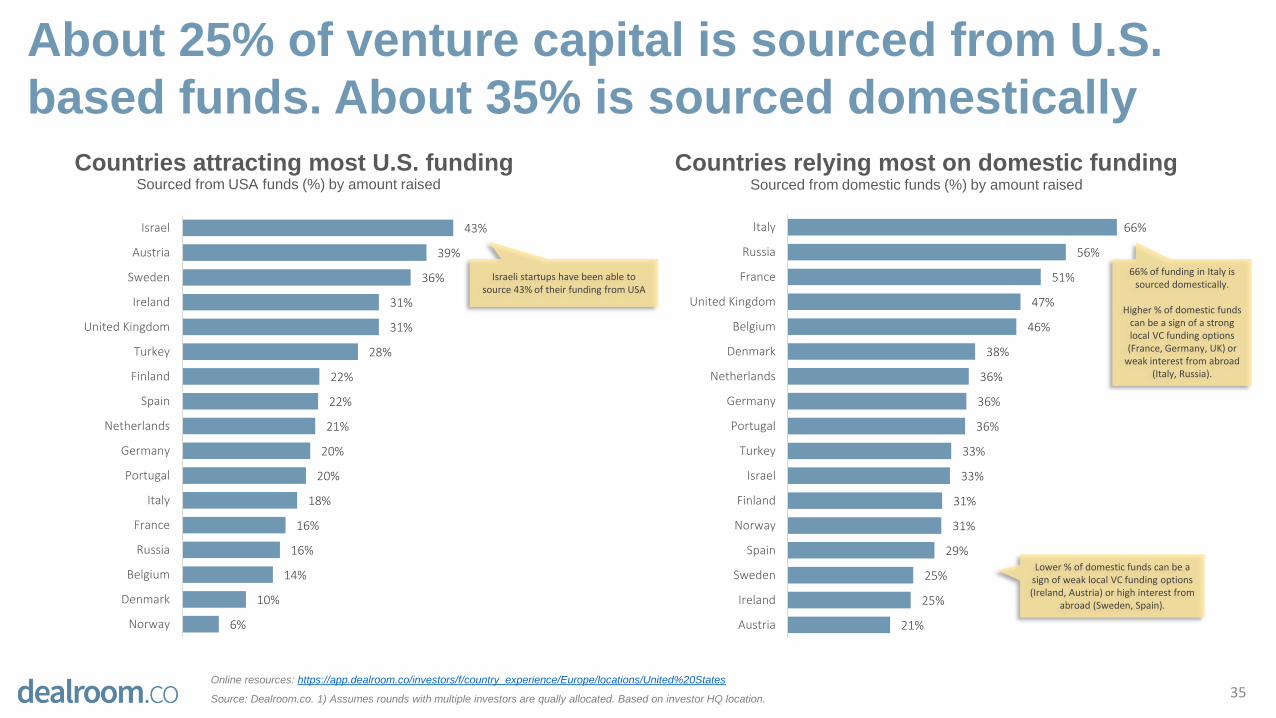

About 25% of venture capital is sourced from U.S.

based funds. About 35% is sourced domestically

35Online resources: https://app.dealroom.co/investors/f/country_experience/Europe/locations/United%20States

Source: Dealroom.co. 1) Assumes rounds with multiple investors are qually allocated. Based on investor HQ location.

Countries attracting most U.S. funding Countries relying most on domestic fundingSourced from USA funds (%) by amount raised Sourced from domestic funds (%) by amount raised

Israeli startups have been able to source 43% of their funding from USA

66% of funding in Italy is sourced domestically.

Higher % of domestic funds can be a sign of a strong local VC funding options (France, Germany, UK) or

weak interest from abroad (Italy, Russia).

43%

39%

36%

31%

31%

28%

22%

22%

21%

20%

20%

18%

16%

16%

14%

10%

6%

Israel

Austria

Sweden

Ireland

United Kingdom

Turkey

Finland

Spain

Netherlands

Germany

Portugal

Italy

France

Russia

Belgium

Denmark

Norway

66%

56%

51%

47%

46%

38%

36%

36%

36%

33%

33%

31%

31%

29%

25%

25%

21%

Italy

Russia

France

United Kingdom

Belgium

Denmark

Netherlands

Germany

Portugal

Turkey

Israel

Finland

Norway

Spain

Sweden

Ireland

Austria

Lower % of domestic funds can be a sign of weak local VC funding options (Ireland, Austria) or high interest from

abroad (Sweden, Spain).

€ 3.2B

€ 2.7B

€ 2.7B

€ 2.0B

€ 1.6B

€ 0.6B

€ 0.4B

€ 0.4B

€ 0.3B

€ 0.3B

€ 0.2B

€ 0.2B

€ 0.2B

€ 0.1B

€ 0.1B

€ 0.0B

€ 0.0B

USA

United Kingdom

France

Israel

Germany

Sweden

Spain

Netherlands

Ireland

Finland

Russia

Belgium

Italy

Norway

Denmark

Austria

Portugal

Turkey

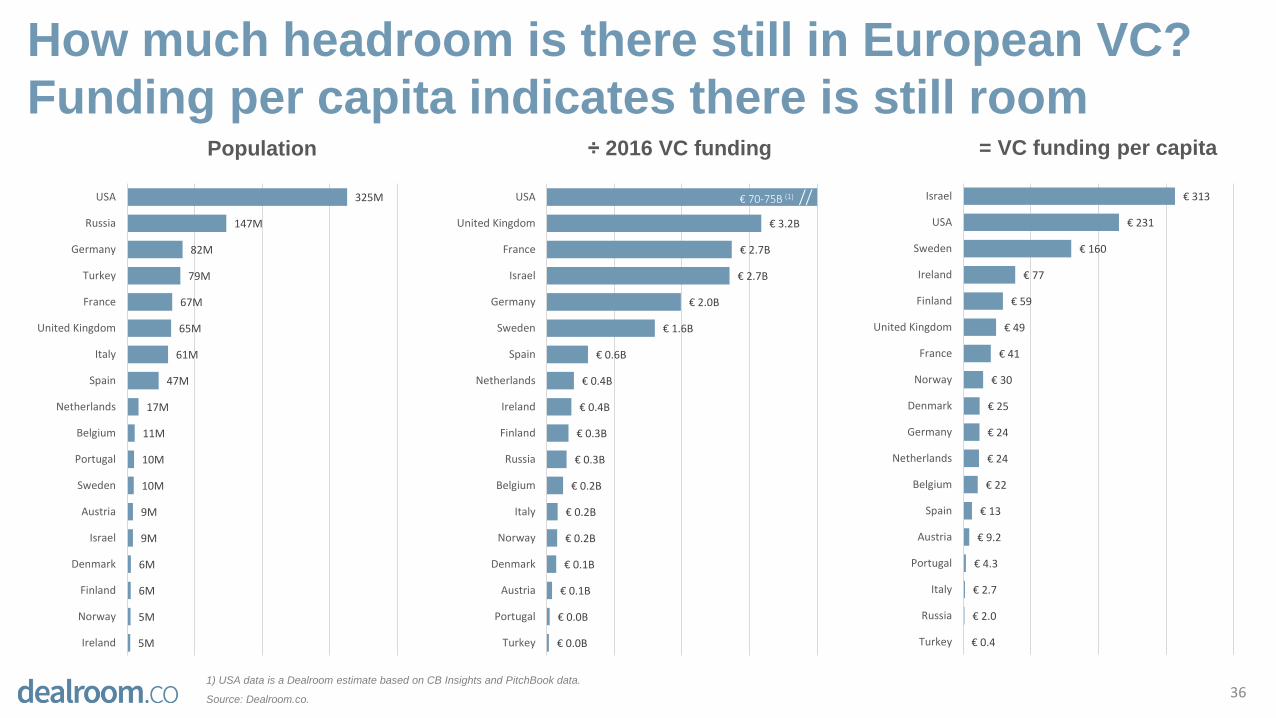

How much headroom is there still in European VC?

Funding per capita indicates there is still room

361) USA data is a Dealroom estimate based on CB Insights and PitchBook data.

Source: Dealroom.co.

325M

147M

82M

79M

67M

65M

61M

47M

17M

11M

10M

10M

9M

9M

6M

6M

5M

5M

USA

Russia

Germany

Turkey

France

United Kingdom

Italy

Spain

Netherlands

Belgium

Portugal

Sweden

Austria

Israel

Denmark

Finland

Norway

Ireland

Population = VC funding per capita÷ 2016 VC funding

€ 70-75B (1) // € 313

€ 231

€ 160

€ 77

€ 59

€ 49

€ 41

€ 30

€ 25

€ 24

€ 24

€ 22

€ 13

€ 9.2

€ 4.3

€ 2.7

€ 2.0

€ 0.4

Israel

USA

Sweden

Ireland

Finland

United Kingdom

France

Norway

Denmark

Germany

Netherlands

Belgium

Spain

Austria

Portugal

Italy

Russia

Turkey

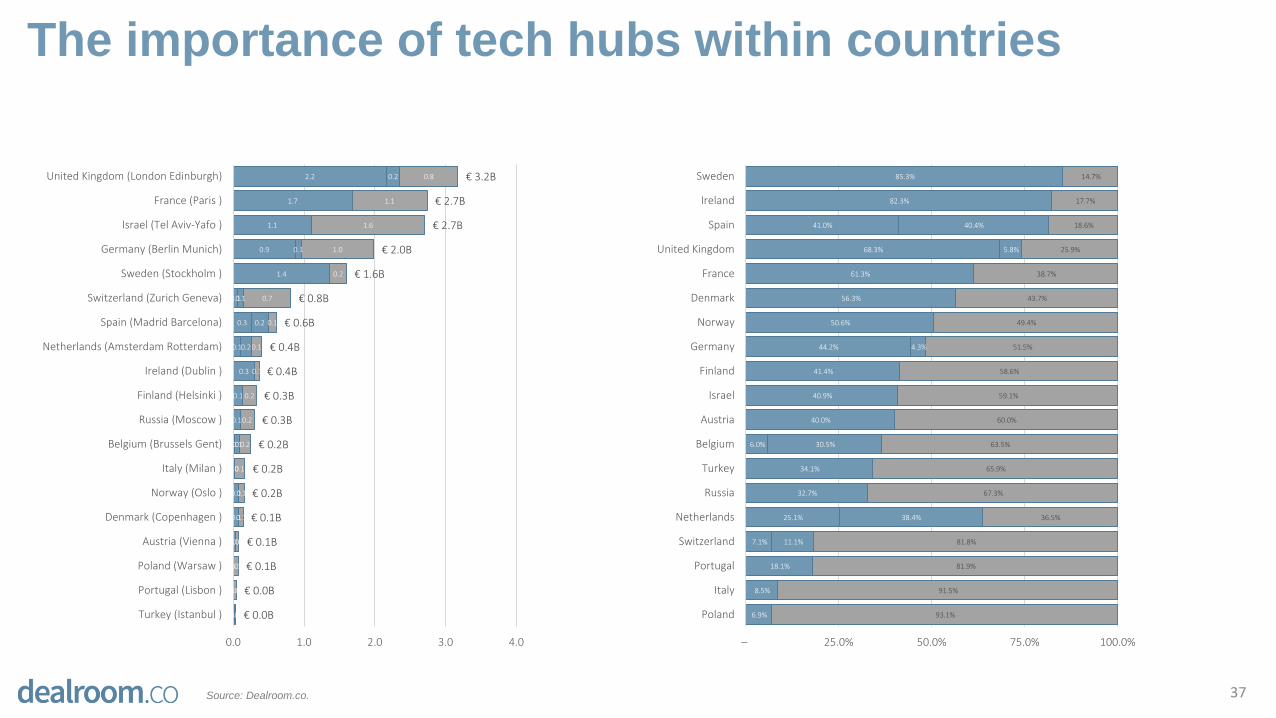

The importance of tech hubs within countries

37Source: Dealroom.co.

85.3%

82.3%

41.0%

68.3%

61.3%

56.3%

50.6%

44.2%

41.4%

40.9%

40.0%

6.0%

34.1%

32.7%

25.1%

7.1%

18.1%

8.5%

6.9%

40.4%

5.8%

4.3%

30.5%

38.4%

11.1%

14.7%

17.7%

18.6%

25.9%

38.7%

43.7%

49.4%

51.5%

58.6%

59.1%

60.0%

63.5%

65.9%

67.3%

36.5%

81.8%

81.9%

91.5%

93.1%

– 25.0% 50.0% 75.0% 100.0%

Sweden

Ireland

Spain

United Kingdom

France

Denmark

Norway

Germany

Finland

Israel

Austria

Belgium

Turkey

Russia

Netherlands

Switzerland

Portugal

Italy

Poland

2.2

1.7

1.1

0.9

1.4

0.1

0.3

0.1

0.3

0.1

0.1

0.0

0.0

0.1

0.1

0.0

0.0

0.0

0.0

0.2

0.1

0.1

0.2

0.2

0.1

0.8

1.1

1.6

1.0

0.2

0.7

0.1

0.1

0.1

0.2

0.2

0.2

0.1

0.1

0.1

0.0

0.1

0.0

0.0

€ 3.2B

€ 2.7B

€ 2.7B

€ 2.0B

€ 1.6B

€ 0.8B

€ 0.6B

€ 0.4B

€ 0.4B

€ 0.3B

€ 0.3B

€ 0.2B

€ 0.2B

€ 0.2B

€ 0.1B

€ 0.1B

€ 0.1B

€ 0.0B

€ 0.0B

0.0 1.0 2.0 3.0 4.0

United Kingdom (London Edinburgh)

France (Paris )

Israel (Tel Aviv-Yafo )

Germany (Berlin Munich)

Sweden (Stockholm )

Switzerland (Zurich Geneva)

Spain (Madrid Barcelona)

Netherlands (Amsterdam Rotterdam)

Ireland (Dublin )

Finland (Helsinki )

Russia (Moscow )

Belgium (Brussels Gent)

Italy (Milan )

Norway (Oslo )

Denmark (Copenhagen )

Austria (Vienna )

Poland (Warsaw )

Portugal (Lisbon )

Turkey (Istanbul )

2016 saw largest ever European cohort of early stage

startups funded. Later stage rounds slowed down

38

€ 0.2B € 0.2B € 0.2B

€ 0.3B€ 0.4B € 0.4B

€ 0.2B€ 0.3B

€ 0.4B

€ 0.6B

€ 0.9B € 0.9B€ 0.8B

€ 0.9B

€ 1.0B

€ 1.2B

€ 0.7B

€ 0.9B

€ 1.2B

€ 0.9B

€ 1.1B

€ 1.3B

€ 0.8B€ 0.8B

€ 1.7B

€ 1.8B

€ 1.7B

€ 1.1B

€ 1.3B

€ 1.6B

€ 1.3B

€ 1.2B

€ 0.5B

€ 0.4B€ 0.3B € 0.3B

€ 1.1B

€ 0.1B

€ 0.2B

€ 0.3B

299 292

340 370

497

451

367

433

106 131

148

182 189 194

231

265

42 52 61 60 70 74 62 60 39 44 45 50 61 52 43 42

150

42 54 59 66 65 83 71

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2015 2016 2015 2016 2015 2016 2015 2016 2015 2016

Angel & Seed Series A / Early VC Series B, C Series D+ Other

Amount raised (€ billion) Number of rounds

Source: Dealroom.co.

Early stage: strong pipeline Later stage: slow-down

Includes €0.9B Spotify convertible.

Seed & angel rounds more lumpy on quarterly scale

On quarterly scale, uptrend in Series B and series C disappears

Largest ever European cohort of new early stage startups funded in 2016.

€ 0.7B

€ 0.8B

€ 1.3B

€ 1.0B

€ 1.1B

€ 0.7B

€ 0.9B

€ 0.5B

€ 1.3B

€ 0.7B

€ 0.6B

€ 0.4B

€ 0.3B

€ 0.8B

€ 0.5B€ 0.4B

€ 0.3B€ 0.3B

€ 0.6B

€ 0.3B

€ 0.7B

€ 0.4B

€ 0.8B

€ 0.8B

€ 0.4B

€ 0.5B

€ 0.4B

€ 0.5B€ 0.5B

€ 0.9B

€ 0.7B€ 0.7B

€ 0.1B

€ 0.6B

€ 0.2B

€ 0.1B

€ 1.1B

€ 0.2B

€ 0.1B

€ 0.2B

€ 0.7B€ 0.7B

€ 1.0B€ 1.0B

€ 0.9B

€ 1.2B

€ 0.7B

€ 1.1B

137 124

140 144 142 126 126 126

89

58

102 104 114 98 94

74 54 61 57

71

140 131 134

185

61 55 53 72 63 69 60

39 26

40 39 58

90 82 82

112

269

223

257 272

334 330

290

335

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2015 2016 2015 2016 2015 2016 2015 2016 2015 2016 2015 2016

United Kingdom Germany France Israel Sweden Other

Amount raised (€ billion) Number of rounds

Quarterly trends: Slowdown in UK and Germany, but

strong growth in across most parts of Europe…

39Source: Dealroom.co.

Includes €0.9B Spotify convertible.

Includes Delivery Hero, HelloFresh, FoodPanda

Source: Dealroom.co. Includes Israel. Excludes private equity, M&A and buyouts. More data on: https://app.dealroom.co/markets/countries/funding

Slowdown in UK and Germany

(Europe’s most mature VC markets)

Remainder of Europe is catching up rapidly across a very

distributed group of countries. Israel continued strong growth

![VENTURE CAPITAL FOR SUSTAINABILITY 2007 REPORT [2007] Venture Capital... · growing sector as Venture Capital for Sustainability ... Venture Capitalists’ stake in ... Venture Capital](https://img.pdfslide.net/doc/110x75/5a7926b77f8b9a00168dc540/venture-capital-for-sustainability-2007-2007-venture-capitalgrowing-sector.jpg)