Embed Size (px)

Citation preview

Barings Bank

An Analysis

http://www.aw-

bc.com/scp/0321197488/assets/downloads/ch7.pdf

1

The Background

Founded in 1762, Barings Bank

(previously known as Baring Brothers &

Co.) was the oldest merchant banking

company in England.

Barings collapsed on February 26, 1995

as the result of the activities of one of its

traders, Nick Leeson, who lost $1.4 billion

by investing in the Singapore

International Monetary Exchange

(SIMEX) with primarily derivative

securities.

2

The Background - 2

Following the collapse, Barings was

purchased by the Dutch bank/insurance

company ING (for the nominal sum of one

pound) and today no longer exists as a

corporate entity; however, the Baring

family’s name lives on in Baring Asset

Management

3

Nick Leeson

In January 1992, Barings assigned

Leeson to its newly opened Singapore

branch; shortly thereafter, he became

head of derivatives trading at Barings’

Singapore office, Barings Futures

Singapore (BFS)

While in Singapore, Leeson focused his

trading activities on futures contracts in

three major markets: the Japanese Nikkei

225 stock index, 10-year Japanese

government bonds, and euro-yen

deposits.

4

Nick Leeson’s Trades

Because the Japanese Nikkei 225 stock

index, 10-year Japanese government bonds,

and euro-yen deposits were traded

simultaneously on the Osaka Securities

Exchange (OSE) and the Singapore

International Monetary Exchange (SIMEX),

Leeson’s job eventually became one of

taking advantage of arbitrage opportunities

between the two markets.

But Leeson was not just arbitraging, and

between July 1992 and February 1995

(about two and a half years), he incurred

losses of over $1 billion. How was this

5

The 88888 Account

6

Perverse Incentives

7

Arbitrage

8

Except, Not

9

Arbitrage

Whenever Leeson traded more contracts

than his limits allowed and whenever he

had losing trades that would have

blemished his reputation as a brilliant

trader, Leeson assigned the extra trades

and the losing transactions to the 88888

Account.

He also used the account to conceal the

fact that he was speculating and not

arbitraging.

10

Un-Arbitrage

Remember that Leeson was supposed to

be long and short in approximately equal

amounts on the different exchanges, and

it was for this reason that his supervisors

allowed him to have such large positions.

In reality, he was long in amounts that

were two or three times larger than his

supervisors realized, and he did not have

short positions to offset these enormous

exposures.

11

Introducing the Doubling

After the other Asian stock markets cooled

down in 1994, Leeson concentrated his

trading on Japanese stock index futures and

Japanese government bond futures. He bet

that Japanese stocks and interest rates

would rise at precisely the time Japanese

market was sinking.

Instead of selling to neutralize his position,

Leeson viewed every dip in the Nikkei

average as a buying opportunity. As a result,

his losses piled up in the 88888 Account. To

recoup his losses, he began the fatal

strategy of doubling

12

From Bad to Worse

During his next round of speculative trades, Leeson’s losses in the 88888 Account reached £70 million (more than $100 million), and he was well into his doubling strategy again, but this time he faced a major problem.

The purchase or sale of futures contracts required the bank to deposit funds in a margin account with SIMEX and OSE, the two exchanges on which Leeson was placing most of his trades. His positions were marked to market on a daily basis, and as his losses grew, BFS did not have enough cash to meet Leeson’s growing margin calls, so Barings’ London had to wire BFS the needed funds.

13

From Bad to Worse 2

Without sufficient oversight at Barings, the only effective restraint on Leeson’s reckless doubling strategy was margin calls.

He fabricated a story that the transfers were needed mostly to meet the margin calls of Barings’ customers, many of whom lived in different time zones and had trouble clearing checks in time.

He also convinced Barings London that part of the large margin calls was a normal counterpart of his profitable arbitrage trading activities

14

From Bad to Worse 3

Leeson argued that arbitrage

transactions, in general, earn so little

profit per transaction that he needed large

gross positions to conduct his deals.

Because these positions were on two

separate exchanges, each with its own

margin requirements and therefore having

no mutual netting provisions, he had to

pay margins on the gross positions in both

markets

No one at Barings London seemed to

question Leeson’s explanation

15

So what’s the problem?

16

The Tragic Saga Continues

Through his deception and Barings’ carelessness, Leeson was able to pursue the doubling strategy of recouping losses by piling up long positions in Nikkei 225 futures contracts and short positions in Japanese government bond futures.

In 1994 and 1995, Leeson had increased his positions in Nikkei futures and Japanese government bond futures to approximately 8% and 24% of SIMEX’s total trading volume, respectively.

But Japanese stock prices kept falling, with only occasional rallies. During these rallies Leeson recovered slightly, but never enough to satisfy his needs.

17

The Tragic Saga Continues 2

The chronic weakness of Japanese stock prices pushed the 88888 Account deeper into the red each time, and Leeson kept buying more futures contracts, so that when (and if) Japanese stock prices ever rallied, the 88888 Account would be pulled back up to zero.

The need to make margin deposits was a thorn in Leeson’s side. He did not want to alert London by asking for too many wire transfers, yet he needed funds to keep buying futures contracts.

Only by having enormous futures positions could he recover his losses when the market bounced in the right direction.

18

If you need to sell straddles…

19

The Science Behind the Scam

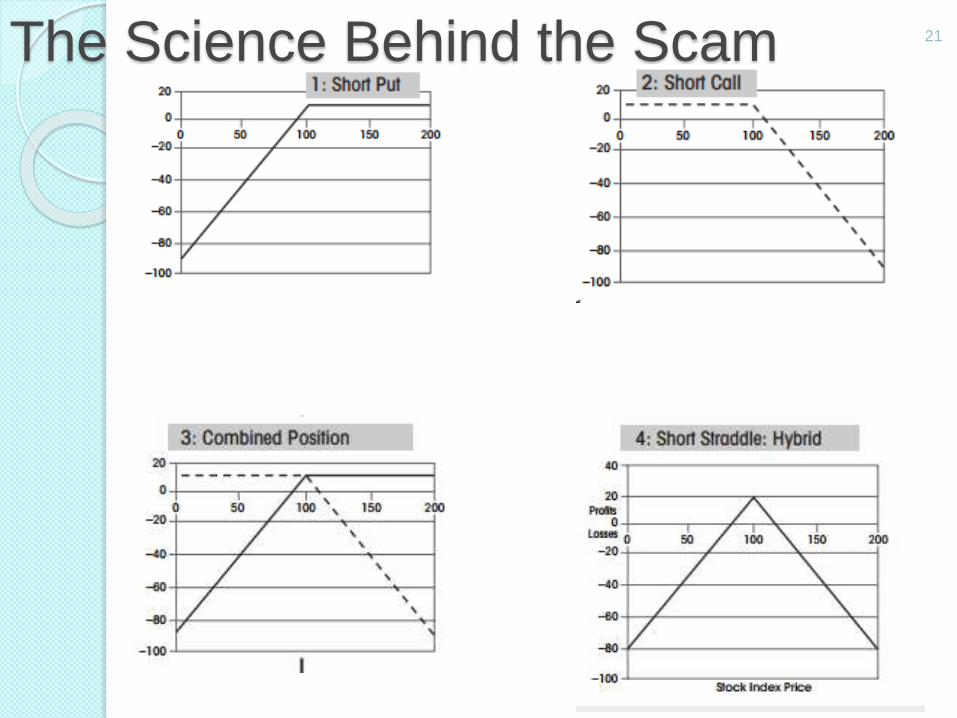

A short straddle is the derivative hybrid created when a short put option and a short call option with the same strike prices are simultaneously combined

The only way a short straddle can earn profits is if the price of the underlying asset does not move substantially in either direction. A short straddle looks like a mountain or an iceberg, with most of its mass underwater (i.e., below zero)

Notice how little of the straddle is above zero, compared to the total profit-and-loss profile. The portion of the short straddle that is above zero depends on the size of the premium relative to the total exposure

20

The Science Behind the Scam 21

The Science Behind the Scam

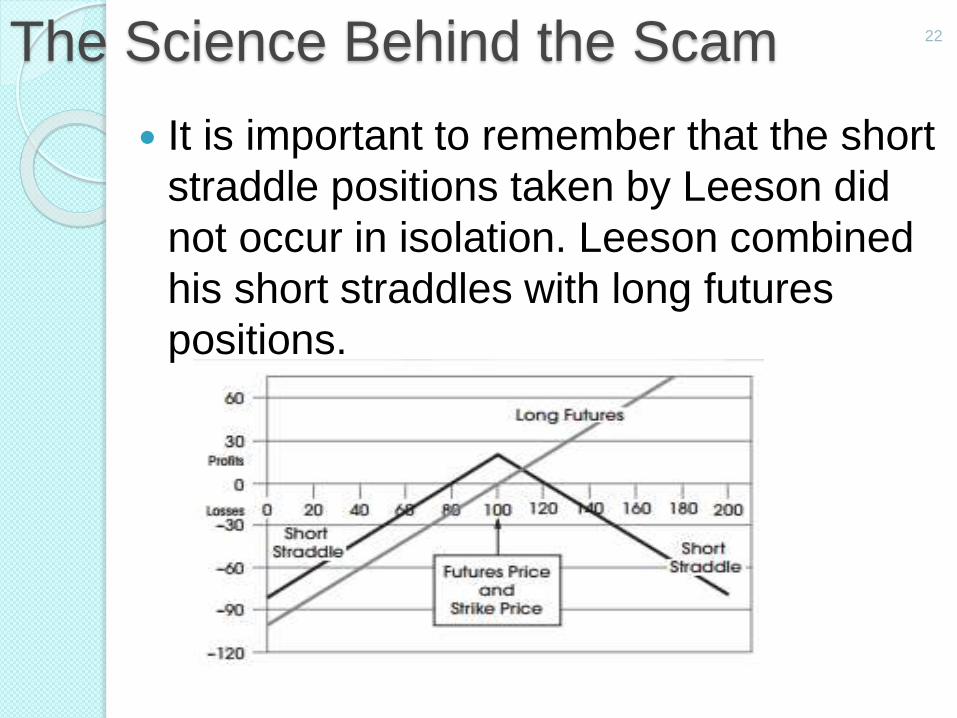

It is important to remember that the short

straddle positions taken by Leeson did

not occur in isolation. Leeson combined

his short straddles with long futures

positions.

22

The Science Behind the Scam

For every straddle he sold, Barings got cash, and Leeson used the cash to pay the required initial margin deposits on new trades and also to meet the mounting margin calls on his existing stock index futures positions.

To profit from the long futures position, the stock price had to rise above the futures price, but if it rose too much, every yen of gain made on the futures position would be offset by losses on the short straddle (or more specifically on the short call portion of the straddle).

23

The Science Behind the Scam

On the down side, the situation was much

more risky. A decline in the stock price

caused simultaneous losses on the

futures position and the straddle position

(or more specifically, the short put portion

of the straddle).

The only thing standing in the way of

losses at almost every price level was the

premium that was collected up front, at

the time the straddle was sold.

24

The Science Behind the Scam 25

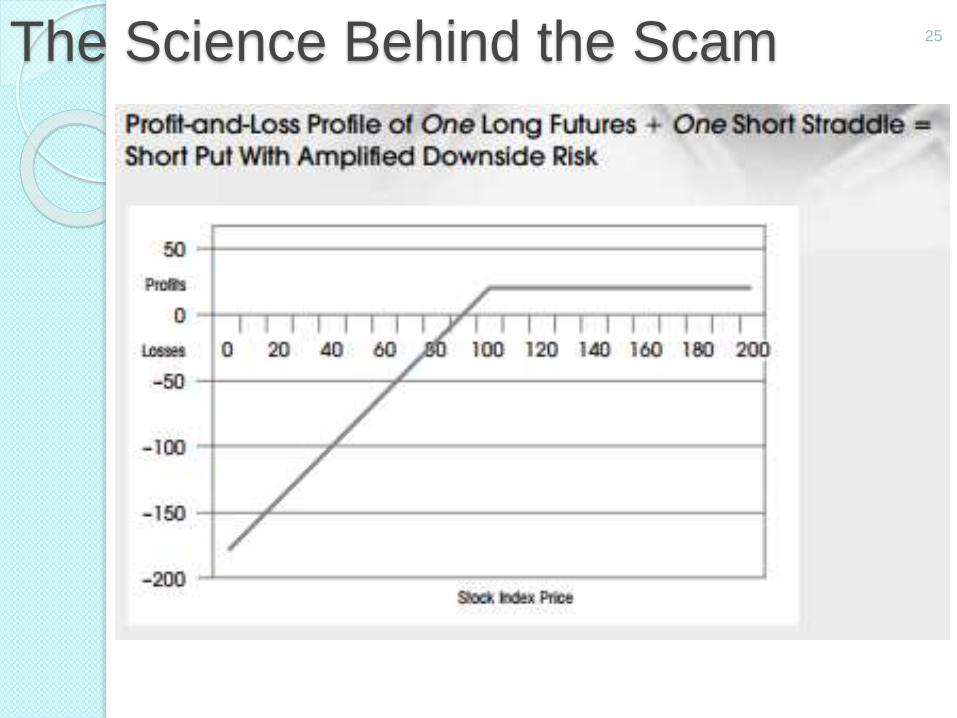

The Science Behind the Scam

The profit-and-loss profile from combining a

short straddle and a long futures position

gives the illusion that Leeson had a viable

trading strategy, and he just guessed wrong

in terms of the price movement.

The diagram shows a large span of prices

to the right of the strike price, which offer, at

least, a glimmer of hope that profits could

be earned.

Unfortunately, we will find that this was not

the case. In fact, Barings would have been

lucky if Leeson had put the bank in such a

position.

26

The Science Behind the Scam

The illusion is revealed once you realize

that Leeson’s need for large sums of

cash to fund his margin calls forced him

to sell disproportionate numbers of short

straddles for each long futures position

he took.

The previous diagram shows the results

if one long futures contract is combined

with one short straddle, but this one-for-

one combination was not what Leeson

did. Rather, he combined numerous

short straddles with each long futures

position.

27

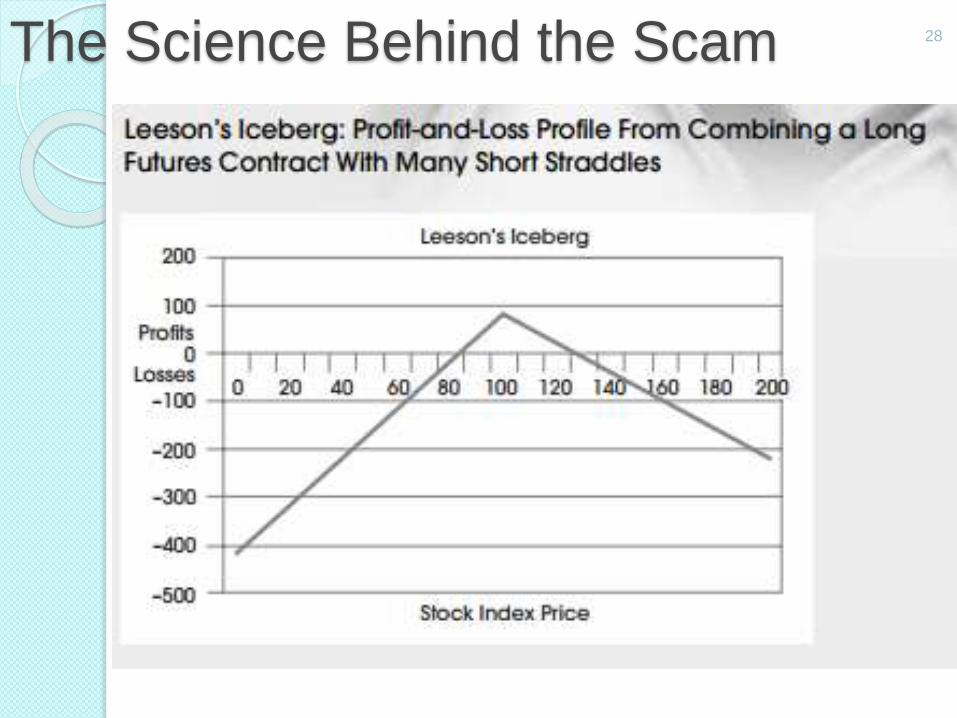

The Science Behind the Scam 28

The Science Behind the Scam

This diagram shows the profit-and-loss

profile when numerous short straddles are

combined with a long forward contract. The

hybrid payoff profile looks, again, like an

iceberg (“Leeson’s Iceberg”), because 90%

or more is underwater (i.e., in the red).

The only outcome that could have been even

slightly profitable was if Japanese stock

prices hovered at or near their current levels,

in which case the stock index futures

contracts would have generated small gains,

and the put and call options would have

expired out of the money

29

The Gambler’s Ruin: Derivatives

Remix

If stock prices rose too much, the gains

on the futures contracts would have been

overwhelmed by the losses on the

mountain of short calls. If stock prices

fell, the losses on the long futures would

have been amplified by the losses on the

mountain of short puts.

30

The Science Behind the Scam

By 31 December 1994, Leeson had accumulated losses of £208 million.

Japanese stocks never rose above 19,000, there was an earthquake in Kobe on 17 January 1995, and Japan’s long-awaited recovery was pushed farther

After the earthquake, the Nikkei Index fell to 18,950, forcing Leeson to engage in an even more frantic and massive operation that looked, in retrospect, like a single-handed effort to hold Japanese stock prices at the 19,000 level

31

The Science Behind the Scam

Over the next five trading days, Leeson bought a total of more than 20,000 futures contracts, and by 22 February 1995 his aggregate position was over 61,000 futures contracts.

Despite his frantic buying, Japanese common stocks fell sharply, and on Monday, 23 January 1995, the Nikkei index fell 1,000 points to 17,950.

For Leeson, the end was near. By February 1995, his losses had reached an astounding £830 million

32

Sounds like a movie, doesn’t it?

There actually is a movie.

It’s called Rogue Trader, and it stars Ewan

McGregor

33

A Bank for a Buck

It was not until the Singapore futures exchange issued a mega-margin call in January and February 1995 that Barings’ directors in London realized that Leeson’s trading was not arbitrage and that he was not a star trader.

The reckless trader had finally been identified. Barings sent a team of auditors to Singapore, but it was too late. The losses continued to mount, and soon exceeded the bank’s net worth of $500 million. Barings had no way to recover, and efforts to extricate itself from financial ruin failed.

In the end, ING Bank in the Netherlands bought Barings for £1.

34

What should we take away?

Banks are in the business of trading

financial instruments, such as currencies,

bonds, common stocks, and many other

financial assets, including derivatives

This trading can be done as a service to

clients and/or to earn outright trading

profits

For auditing and control purposes, the

difference is important

35

What should we take away 2

Trading that is done only as a service for customers requires the bank to have strict rules concerning account management and credit risk management for individual customers.

By contrast, trading done for the house requires strict exposure limits on the bank’s traders, because this type

of trading puts the bank’s equity directly at risk.

In either case, derivative trading requires top management to have a clear idea of how profits are earned and the risks associated with such returns. On both counts, the

36

What should we take away 2

Traders profit by taking advantage of

small movements in market prices.

Because there are so many different

markets and so many different

instruments, these traders tend to

specialize and become experts in their

own narrow segments of the financial

world.

Sometimes this depth of knowledge leads

traders to believe that they can actually

predict in which direction the market will

move

37

What should we take away 5

Derivatives can involve huge amounts of

leverage, and their net risks can be

masked by joining them in countless

combinations, permutations, and

variations.

Studying the Barings fiasco reveals that

no one—not the traders, bank

management, board of directors, or Bank

of England—was adequately supervising

Barings’ derivative risks.

38

If something seems too good to be

true… In 1993, Leeson’s office brought in about

20% of Barings worldwide profits, and during the first half of 1994, it was responsible for about 50% of the bank’s earnings.

By year-end 1994, Leeson’s reported profits were 500% of his budgeted estimate.

Instead of critical scrutiny, Barings management seems to have convinced itself that the source of the bank’s competitive advantage over rivals came from its simultaneous membership on the Japanese and Singapore exchanges.

Management also seemed to have prided itself for having the wisdom to hire Leeson, the golden boy of arbitrage trading.

39

Food for thought

Why did Nick Leeson sell numerous short

straddles for each long futures contract he

bought?

Explain Nick Leeson’s doubling strategy.

Has Nick Leeson drawn too much of the

blame for what went wrong at Barings

Bank? Who else bears some of the

responsibility? Why?

40

Food for thought

Was the Barings board of directors

culpable for the losses of Nick Leeson?

What is a fair way to evaluate the

performance of Barings’ board of

directors?

Nick Leeson traded simultaneously on

two exchanges in two different time

zones. Does the fact that he was trading

on two exchanges simultaneously

automatically mean he was speculating,

or is it what he was doing that made the

trades speculative?

41

Food for thought

Nick Leeson sold short straddles and

combined them with long futures

contracts. What would his expectation

have been if he combined long call

options on the Nikkei Index and with

short forward contracts? Why did he sell

options instead of buying them?

Was the existence of the 88888 Account

one of the fundamental problems at

Barings Bank PLC, or was the problem

with its use?

42