Embed Size (px)

Citation preview

EECONOMIC CONOMIC AANALYSIS, NALYSIS,

SSTATISTICS, TATISTICS, PPROBABILITY AND ROBABILITY AND RRISK ISK

Hisham Haridy, PMP, PMI-RMP, PMI-SPCCP_Section VI

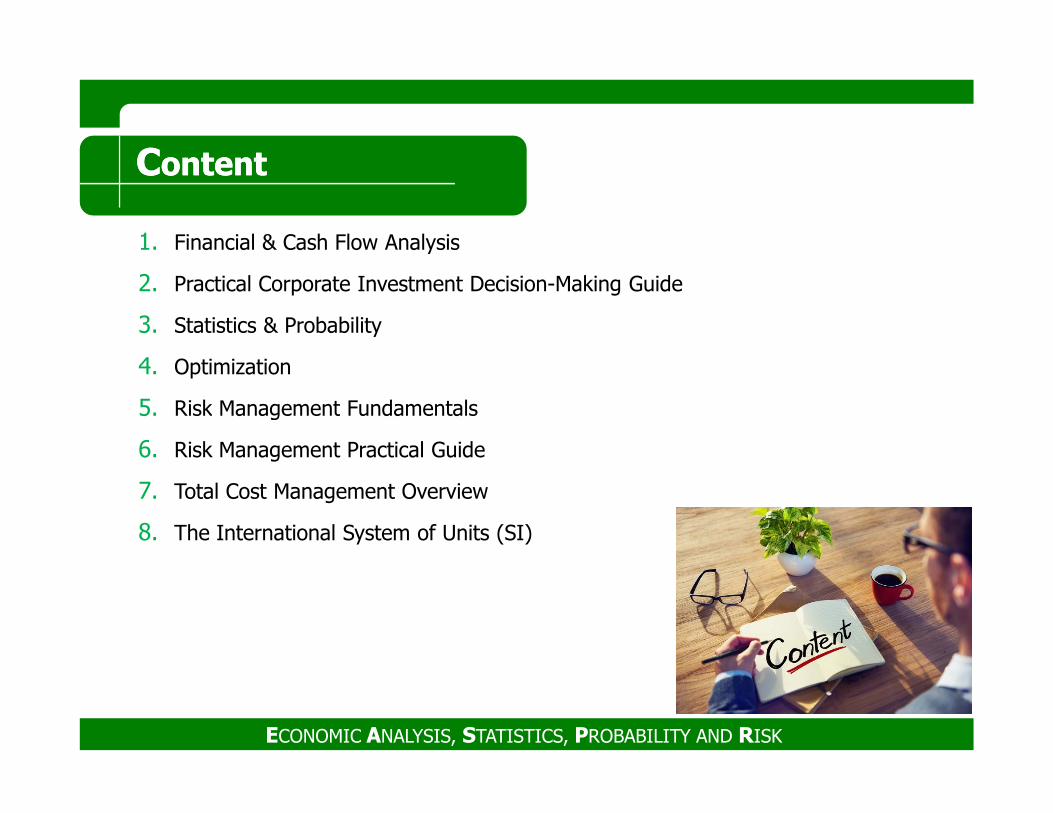

1. Financial & Cash Flow Analysis

2. Practical Corporate Investment Decision-Making Guide

3. Statistics & Probability

4. Optimization

5. Risk Management Fundamentals

CContentontent

5. Risk Management Fundamentals

6. Risk Management Practical Guide

7. Total Cost Management Overview

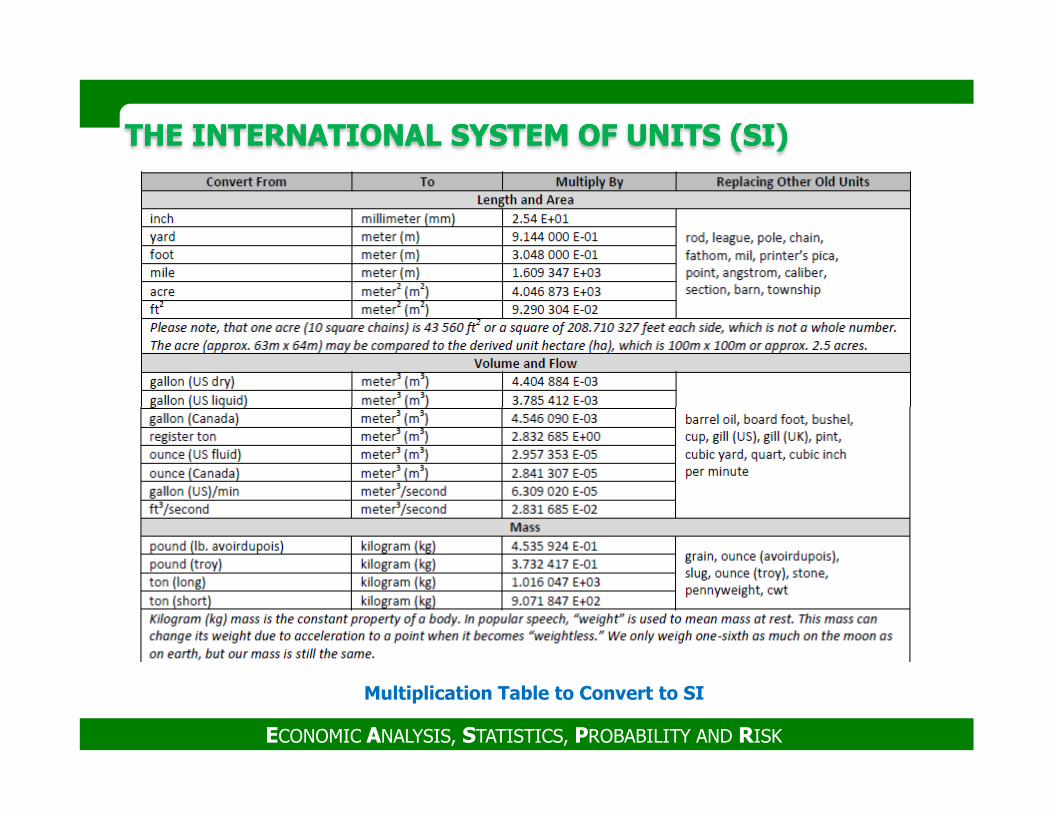

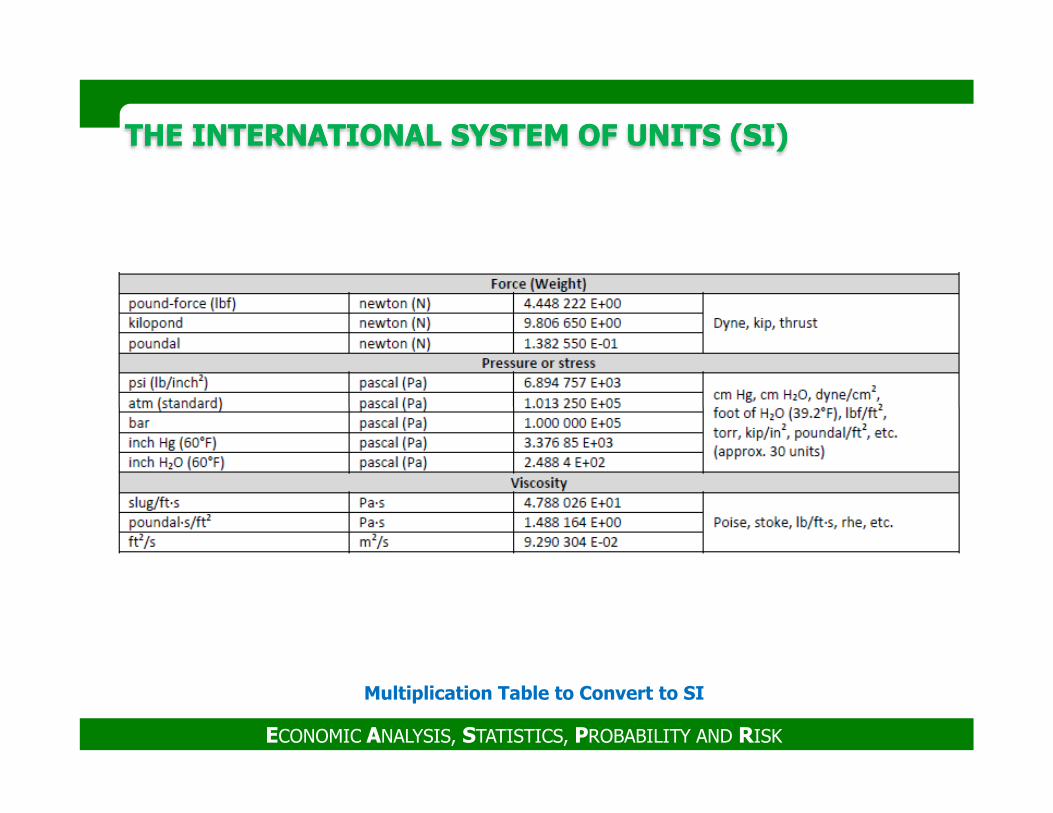

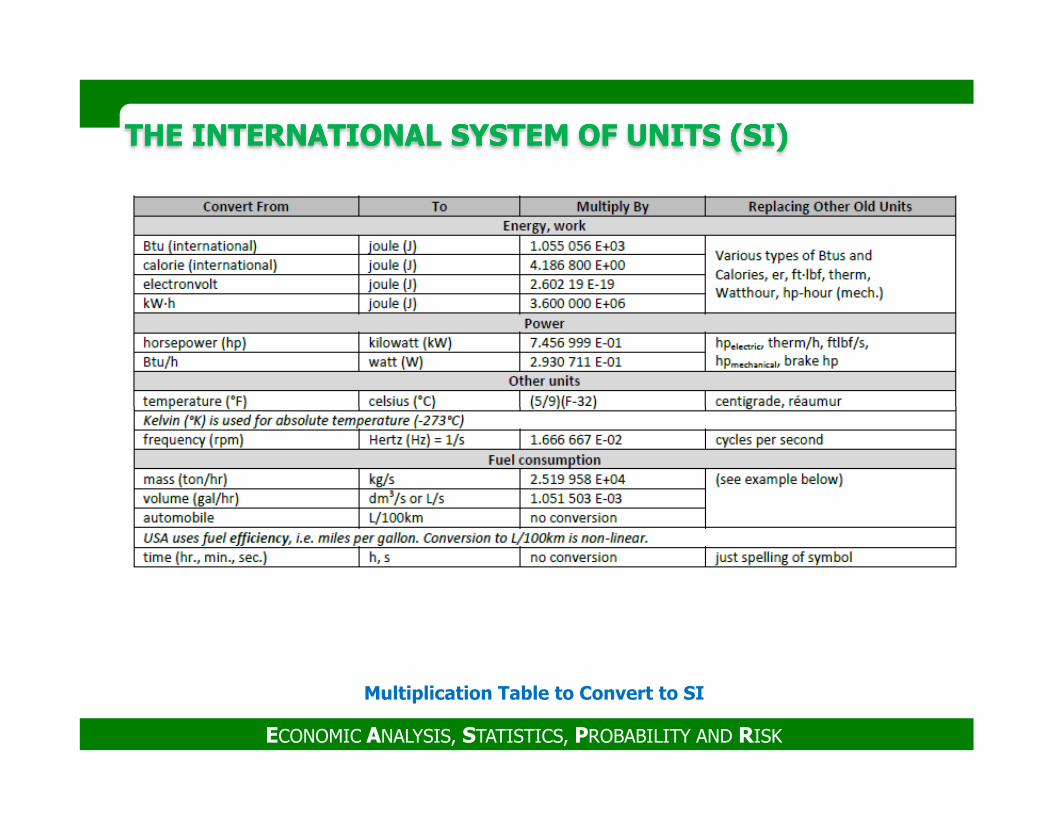

8. The International System of Units (SI)

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

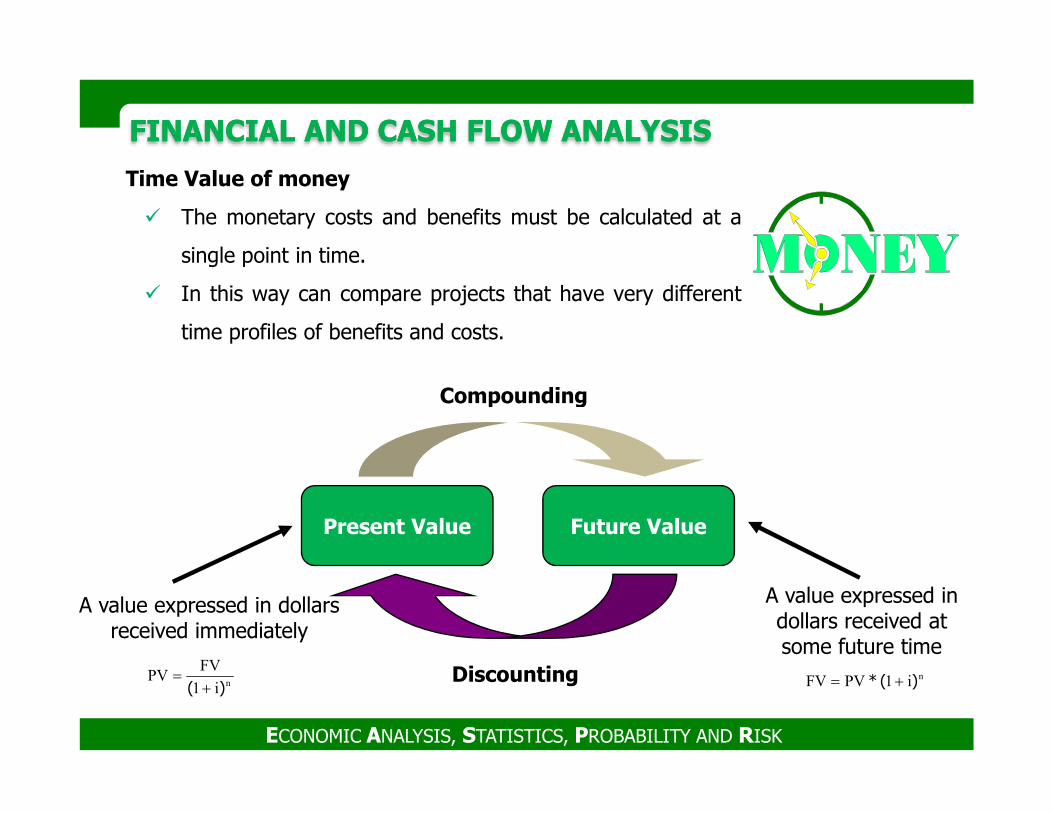

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

Time Value of money

� The monetary costs and benefits must be calculated at a

single point in time.

� In this way can compare projects that have very different

time profiles of benefits and costs.

Compounding

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Future ValuePresent Value

Compounding

Discounting

A value expressed in dollars received immediately

A value expressed in dollars received at some future time

ni1PVFV )(* +=ni1

FVPV

)( +=

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

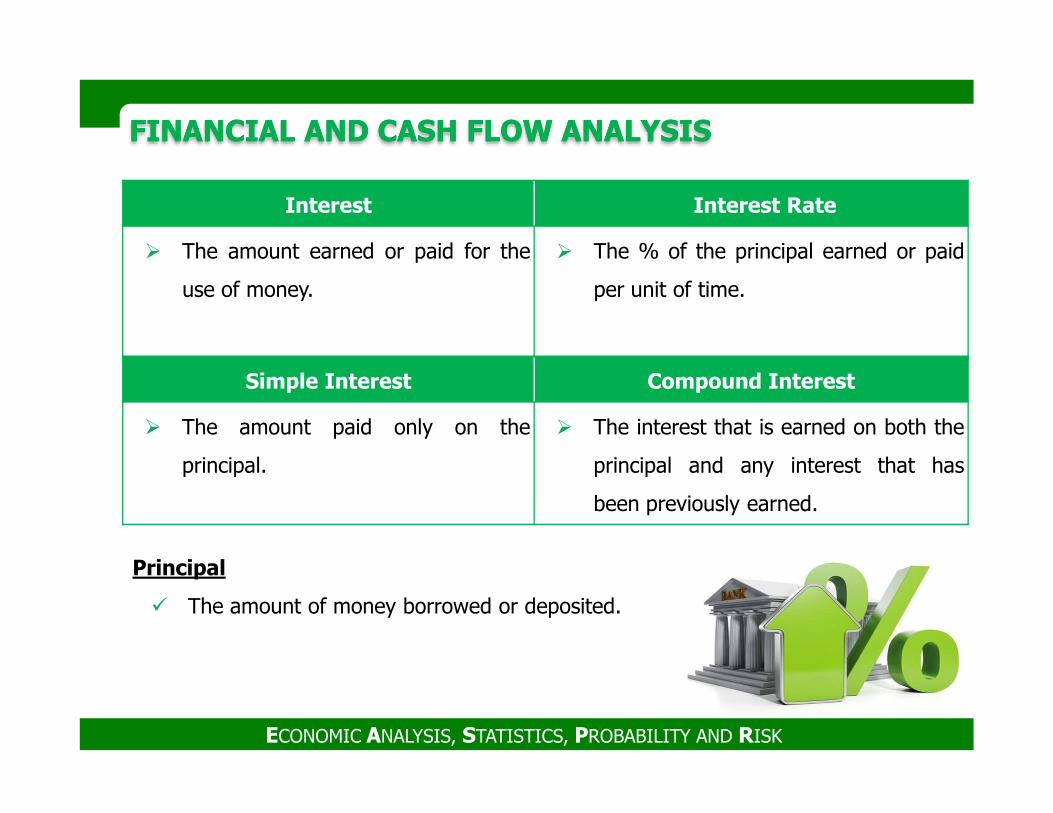

Simple Interest Compound Interest

Interest � Interest Rate

� The amount earned or paid for the

use of money.

� The % of the principal earned or paid

per unit of time.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� The amount paid only on the

principal.

� The interest that is earned on both the

principal and any interest that has

been previously earned.

Principal

� The amount of money borrowed or deposited.

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

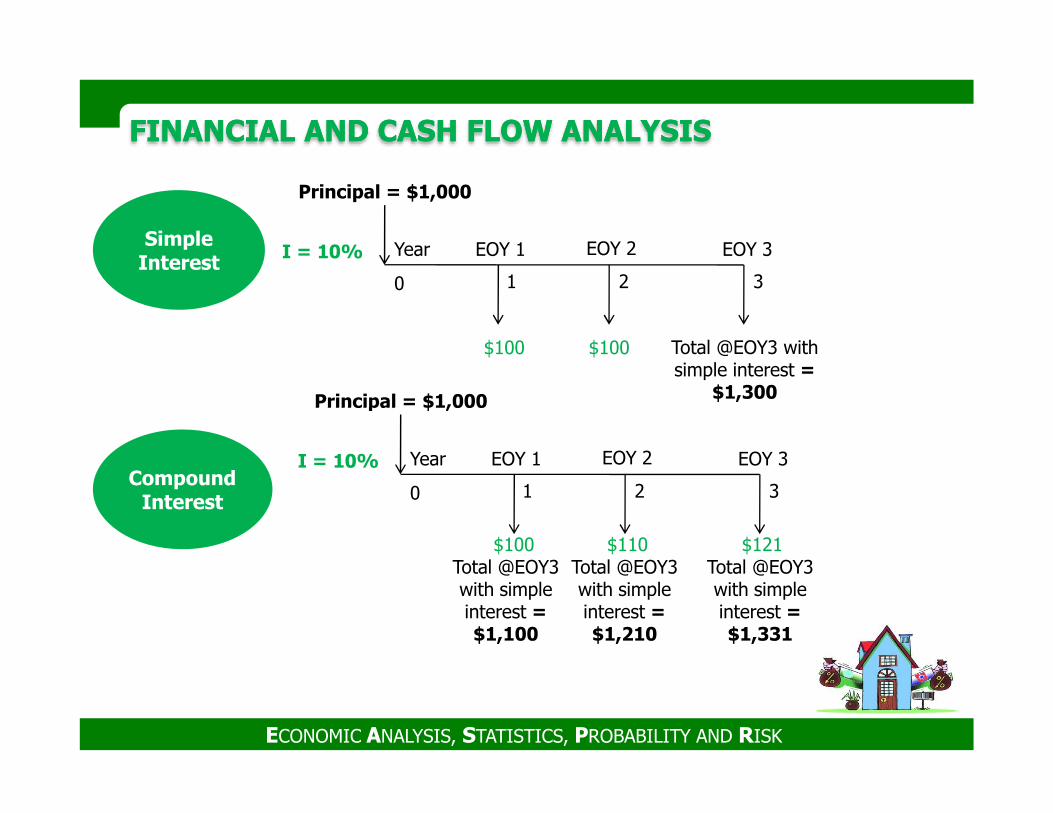

$100 $100

I = 10%

0 1 2

EOY 1 EOY 2

Principal = $1,000

3

Total @EOY3 with simple interest =

$1,300

Year EOY 3

Principal = $1,000

Simple Interest

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

I = 10%

0 1 2

EOY 1 EOY 2

Principal = $1,000

3

Total @EOY3 with simple interest = $1,331

Year EOY 3

$100 $110Total @EOY3 with simple interest = $1,210

Total @EOY3 with simple interest = $1,100

$121

Compound Interest

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

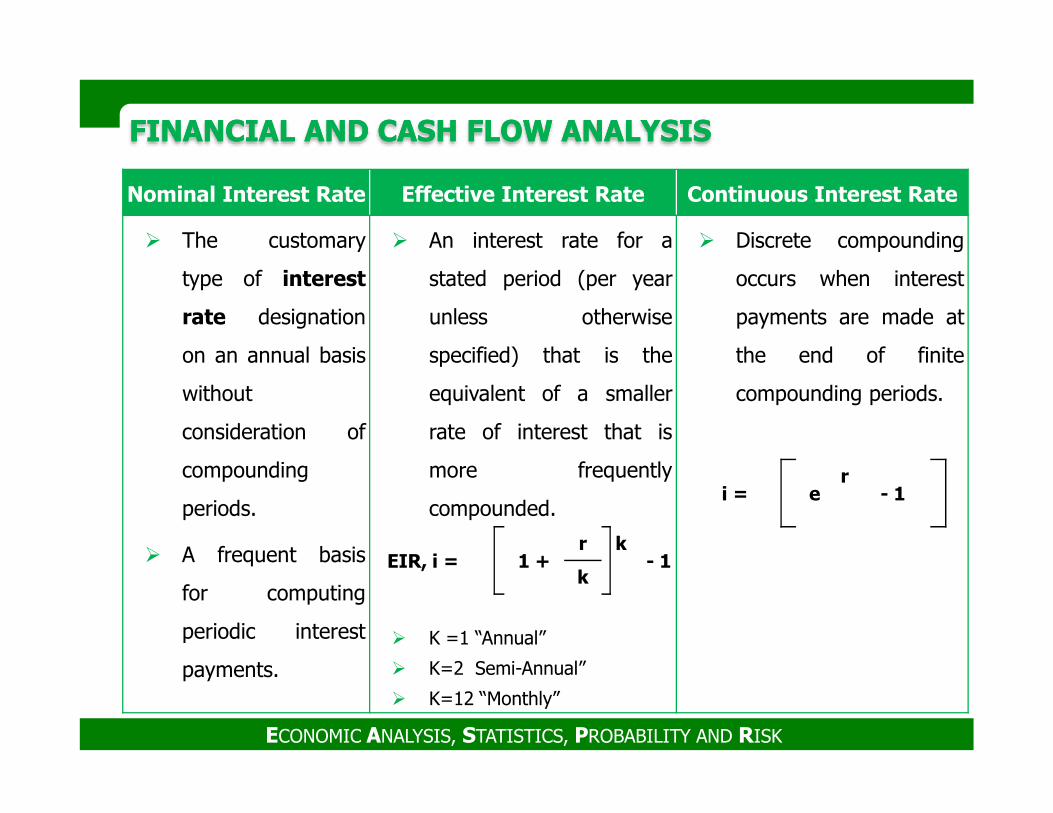

Nominal Interest Rate Effective Interest Rate Continuous Interest Rate

� The customary

type of interest

rate designation

on an annual basis

without

� An interest rate for a

stated period (per year

unless otherwise

specified) that is the

equivalent of a smaller

� Discrete compounding

occurs when interest

payments are made at

the end of finite

compounding periods.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

consideration of

compounding

periods.

� A frequent basis

for computing

periodic interest

payments.

rate of interest that is

more frequently

compounded.

� K =1 “Annual”

� K=2 Semi-Annual”

� K=12 “Monthly”

EIR, i = 1 +r k

- 1k

i = er

- 1

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

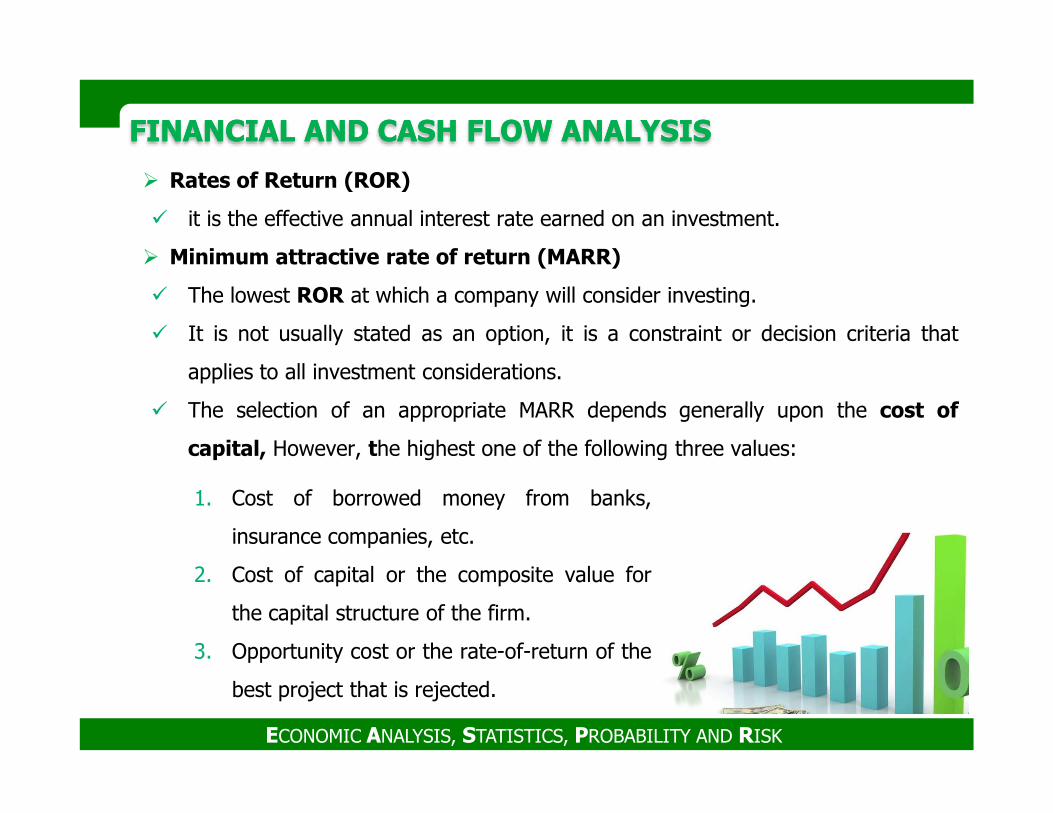

� Rates of Return (ROR)

� it is the effective annual interest rate earned on an investment.

� Minimum attractive rate of return (MARR)

� The lowest ROR at which a company will consider investing.

� It is not usually stated as an option, it is a constraint or decision criteria that

applies to all investment considerations.

� The selection of an appropriate MARR depends generally upon the cost of

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� The selection of an appropriate MARR depends generally upon the cost of

capital, However, the highest one of the following three values:

1. Cost of borrowed money from banks,

insurance companies, etc.

2. Cost of capital or the composite value for

the capital structure of the firm.

3. Opportunity cost or the rate-of-return of the

best project that is rejected.

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

BANK

Loans Share capital

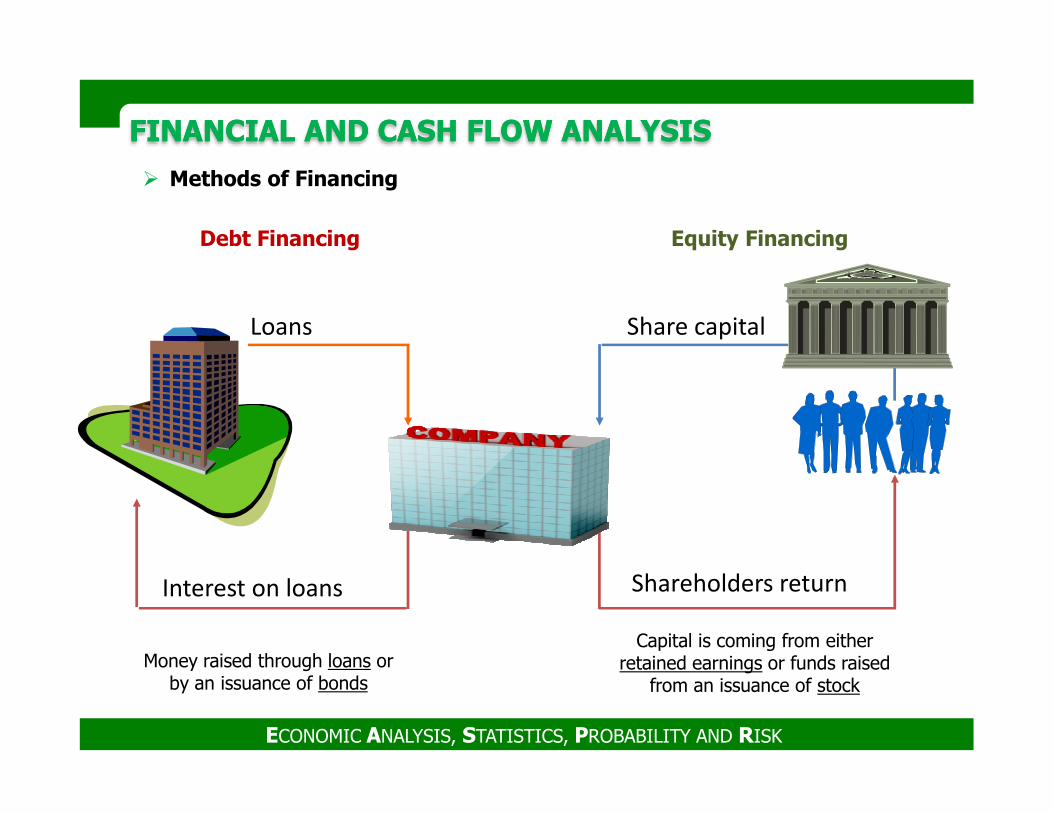

� Methods of Financing

Debt Financing Equity Financing

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Interest on loans Shareholders return

Money raised through loans or by an issuance of bonds

Capital is coming from either retained earnings or funds raised

from an issuance of stock

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

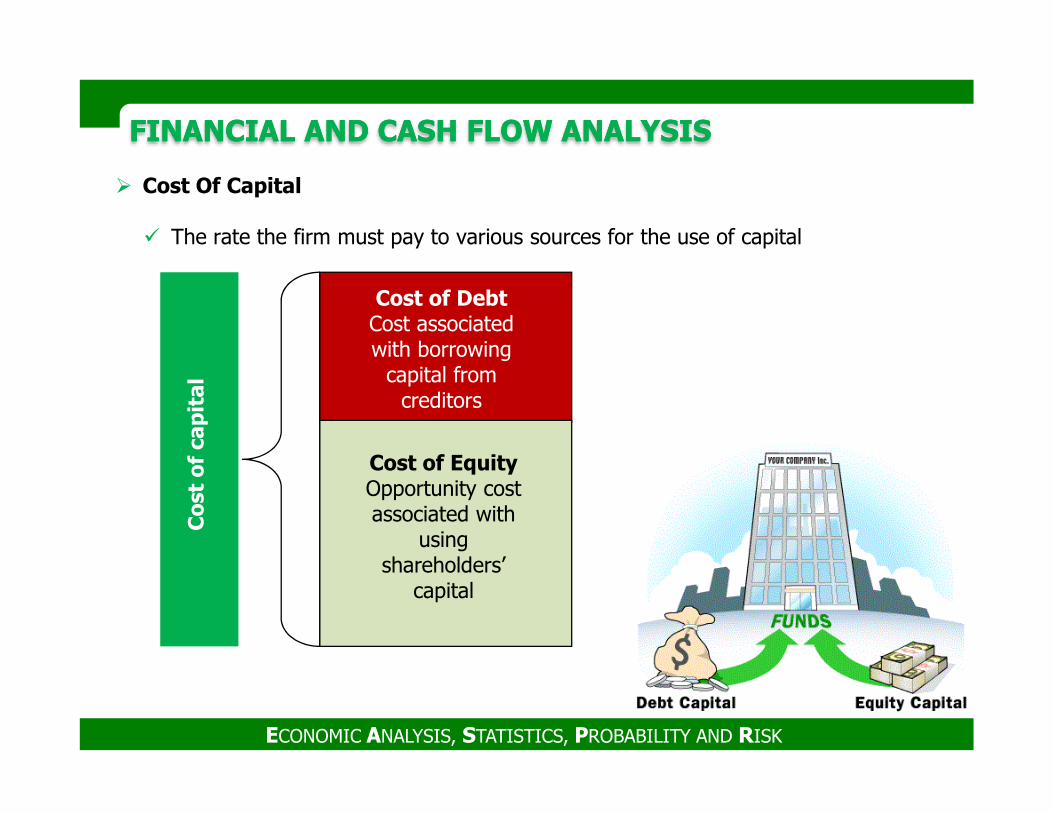

� Cost Of Capital

� The rate the firm must pay to various sources for the use of capital

Cost of DebtCost associated with borrowing

capital from creditors

Co

st o

f ca

pit

al

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Cost of EquityOpportunity cost associated with

using shareholders’

capital

creditors

Co

st o

f ca

pit

al

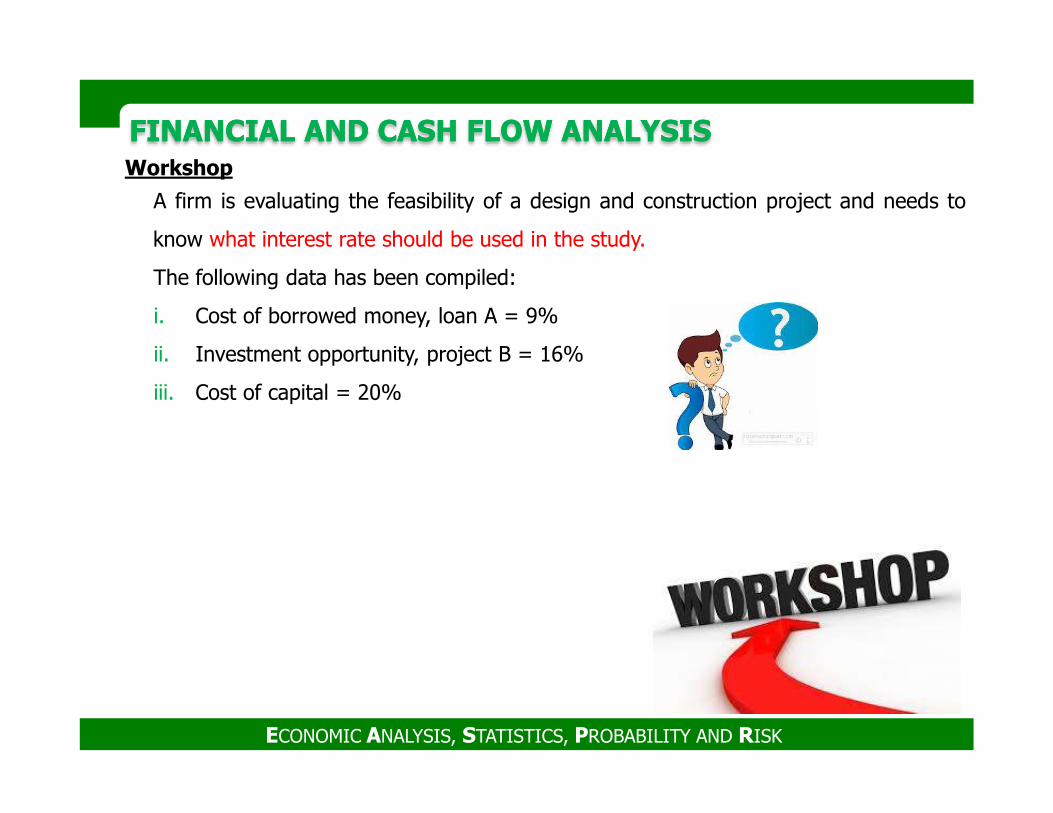

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS Workshop

A firm is evaluating the feasibility of a design and construction project and needs to

know what interest rate should be used in the study.

The following data has been compiled:

i. Cost of borrowed money, loan A = 9%

ii. Investment opportunity, project B = 16%

iii. Cost of capital = 20%

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

� Discount Rate

� The rate of interest reflecting the investor's time value of money, used to

determine discount factors for converting benefits and costs occurring at different

times to a base time.

� The discount rate may be expressed as nominal or real

� The equivalent amount X given amount Y,

� Interest rate i

(X/Y, i, n)

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Interest rate i

� The number of discounting or compounding periods n.

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

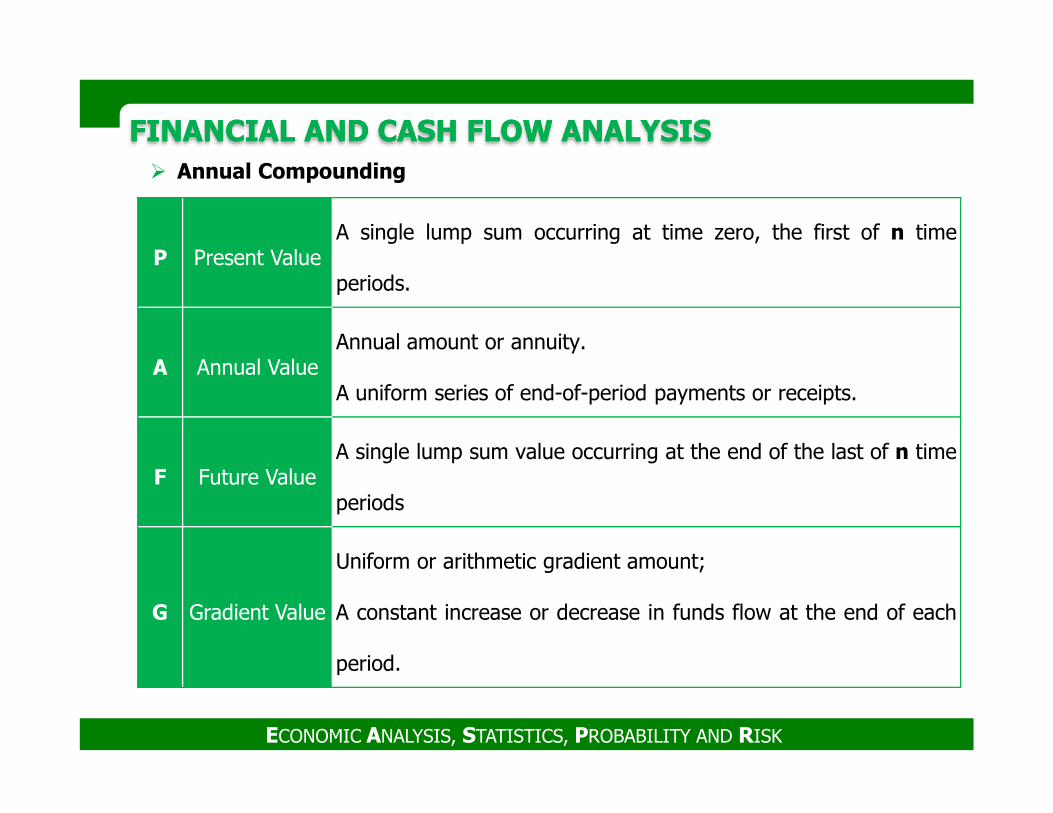

P Present Value A single lump sum occurring at time zero, the first of n time

periods.

A Annual Value Annual amount or annuity.

A uniform series of end-of-period payments or receipts.

� Annual Compounding

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

F Future Value A single lump sum value occurring at the end of the last of n time

periods

G Gradient Value

Uniform or arithmetic gradient amount;

A constant increase or decrease in funds flow at the end of each

period.

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

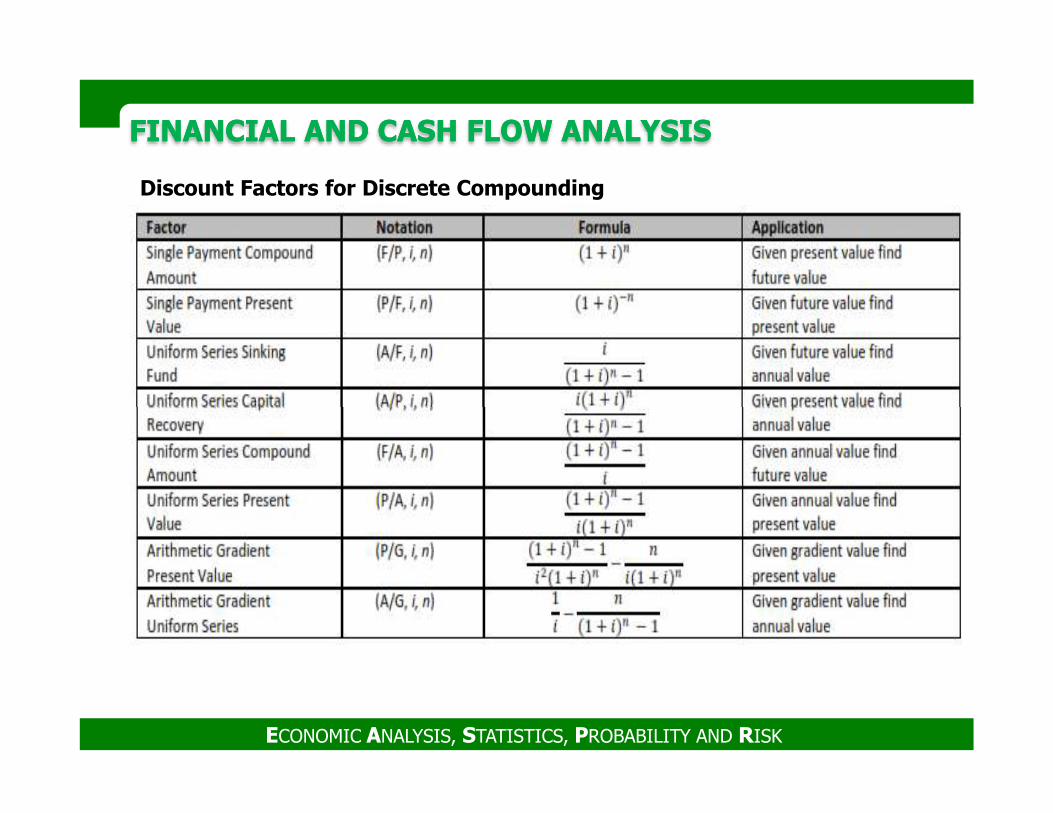

Discount Factors for Discrete Compounding

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

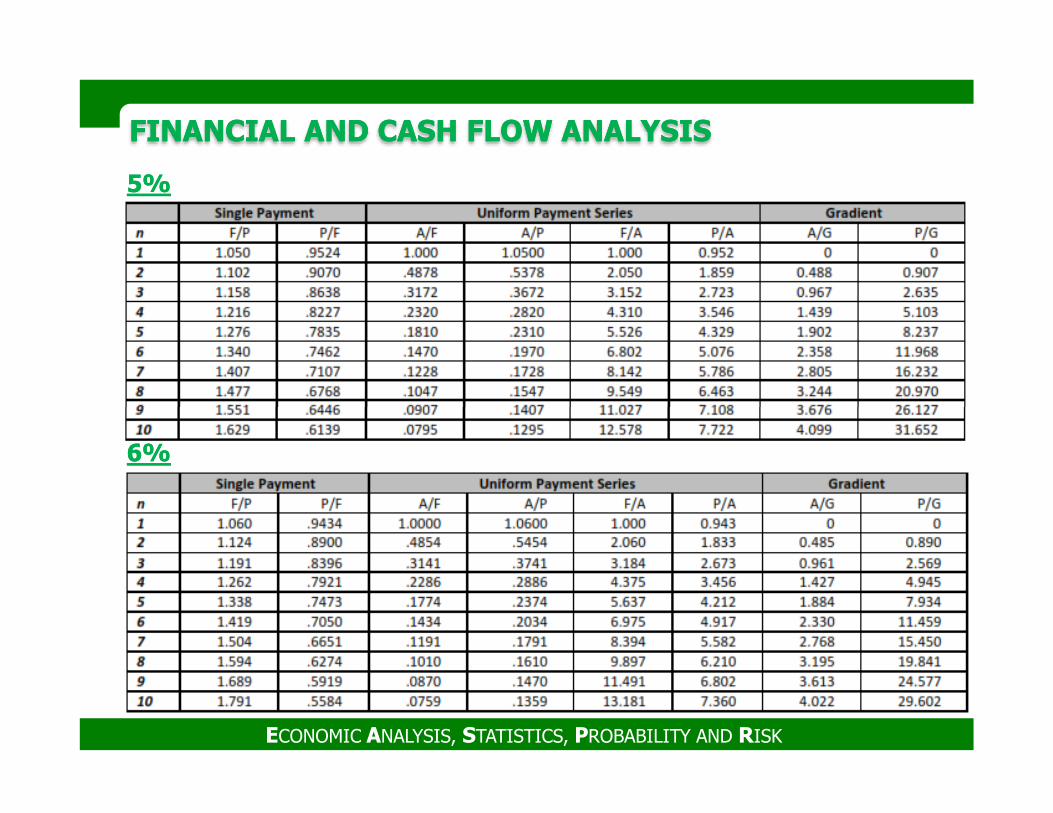

55%%

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

66%%

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

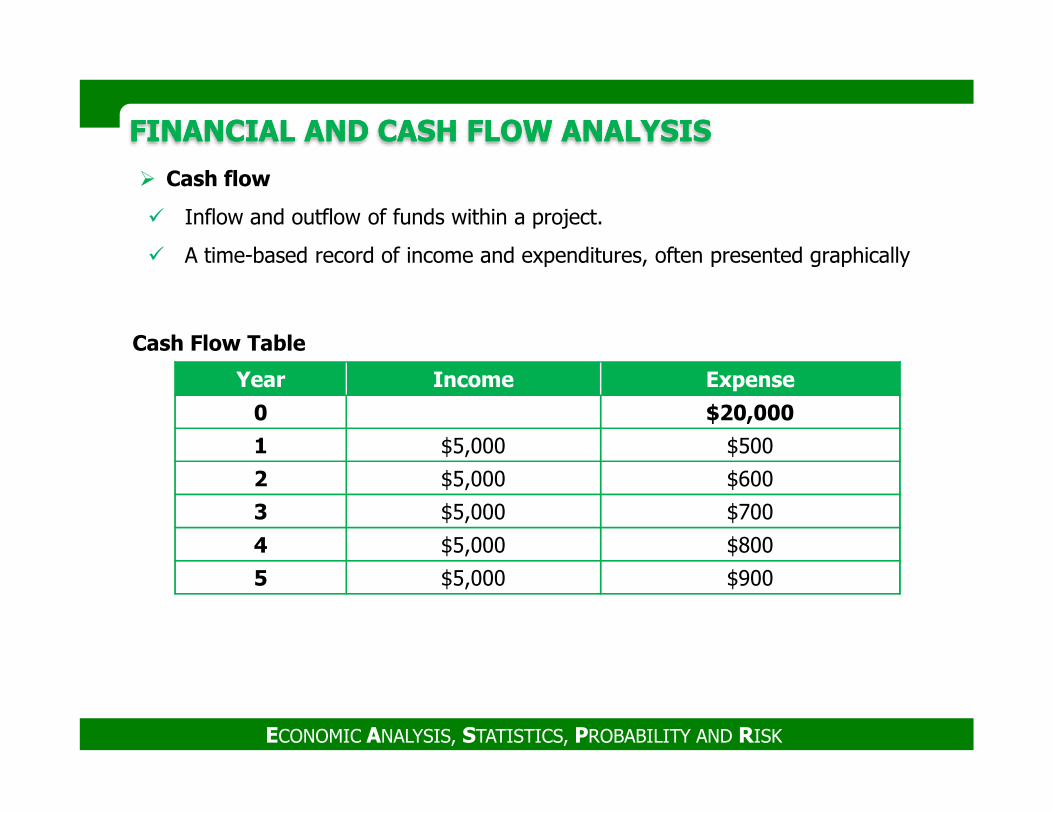

� Cash flow

� Inflow and outflow of funds within a project.

� A time-based record of income and expenditures, often presented graphically

Year Income Expense

0 $20,000

Cash Flow Table

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

0 $20,000

1 $5,000 $500

2 $5,000 $600

3 $5,000 $700

4 $5,000 $800

5 $5,000 $900

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

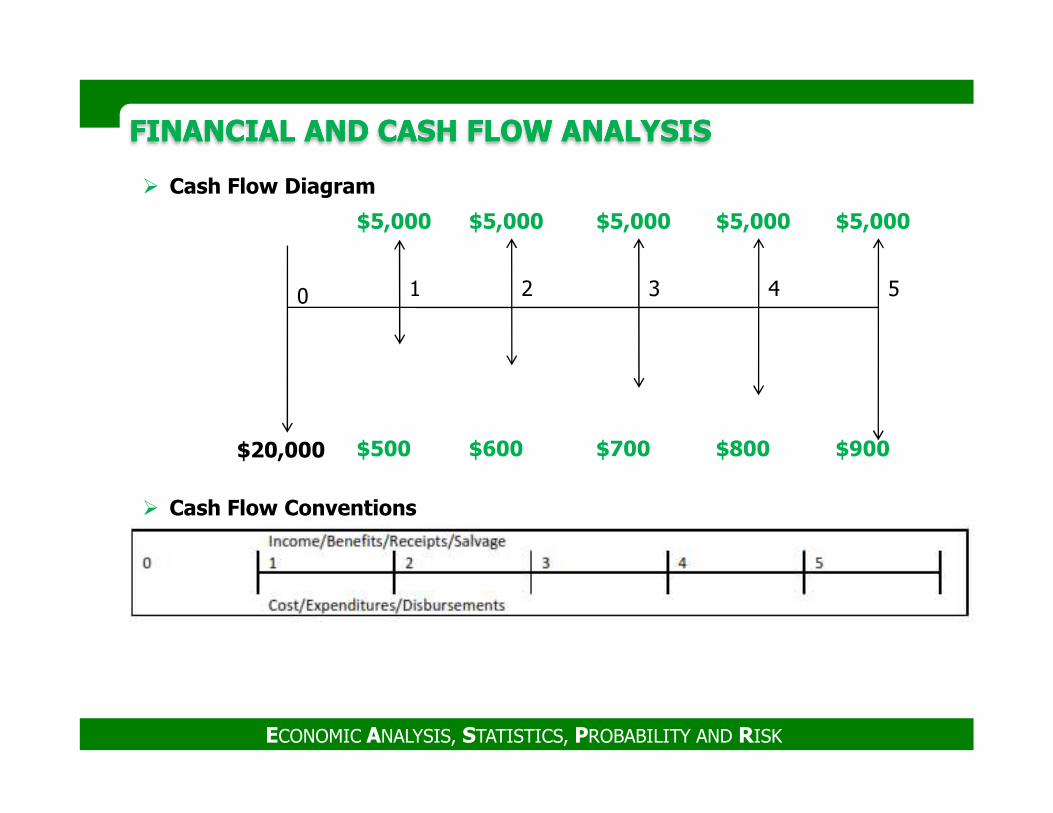

$5,000

0 1 2 3

$5,000 $5,000 $5,000 $5,000

4 5

� Cash Flow Diagram

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

$500 $600 $700 $800 $900$20,000

� Cash Flow Conventions

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

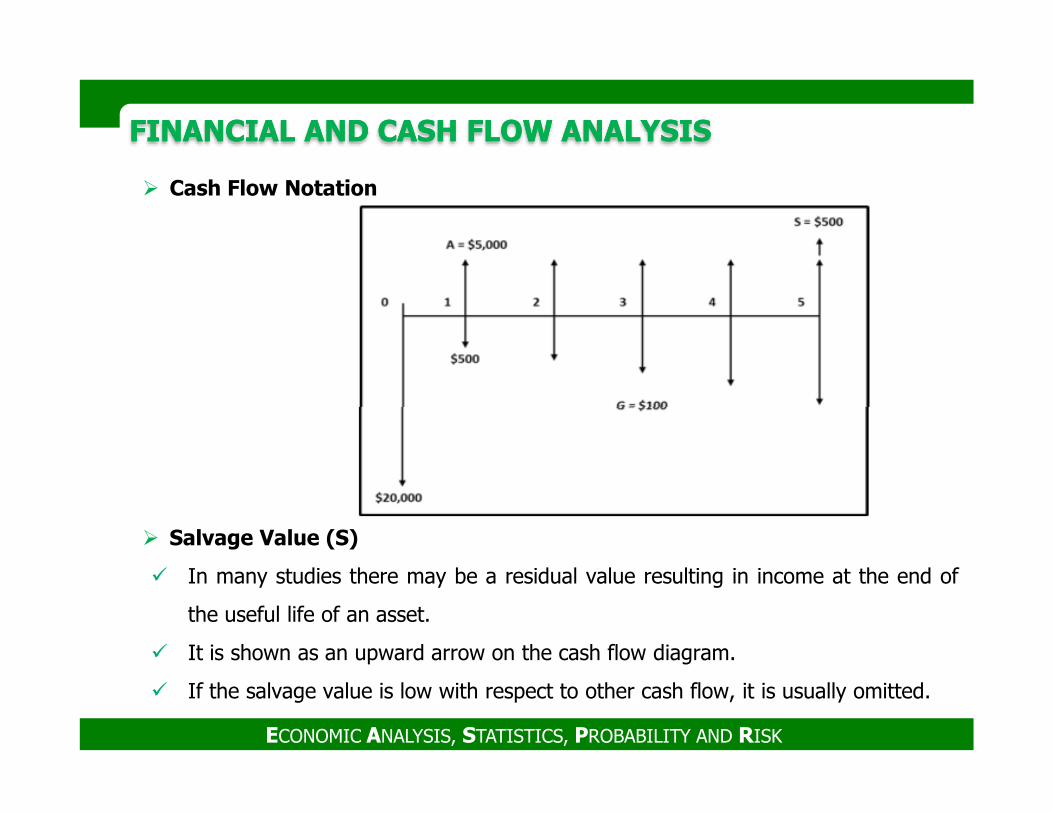

� Cash Flow Notation

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Salvage Value (S)

� In many studies there may be a residual value resulting in income at the end of

the useful life of an asset.

� It is shown as an upward arrow on the cash flow diagram.

� If the salvage value is low with respect to other cash flow, it is usually omitted.

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

CASH FLOW ANALYSIS METHODS

� There are two fundamental approaches to the analysis of a given cash flow,

1. Equivalent value

2. Rate-of-return

� Equivalent Net Value

� The equivalent net value method simply converts to one of the basic forms, (i.e.,

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� The equivalent net value method simply converts to one of the basic forms, (i.e.,

the equivalent present value, or annual value, using discount factors and the

required MARR).

� The "net" is the difference between all costs and all benefits (savings and other

gains).

� Thus, the Net Present Value (NPV) takes into account the time value of money

adjusting to expenditures and returns, as they occur over time, so they can be

evaluated equally.

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

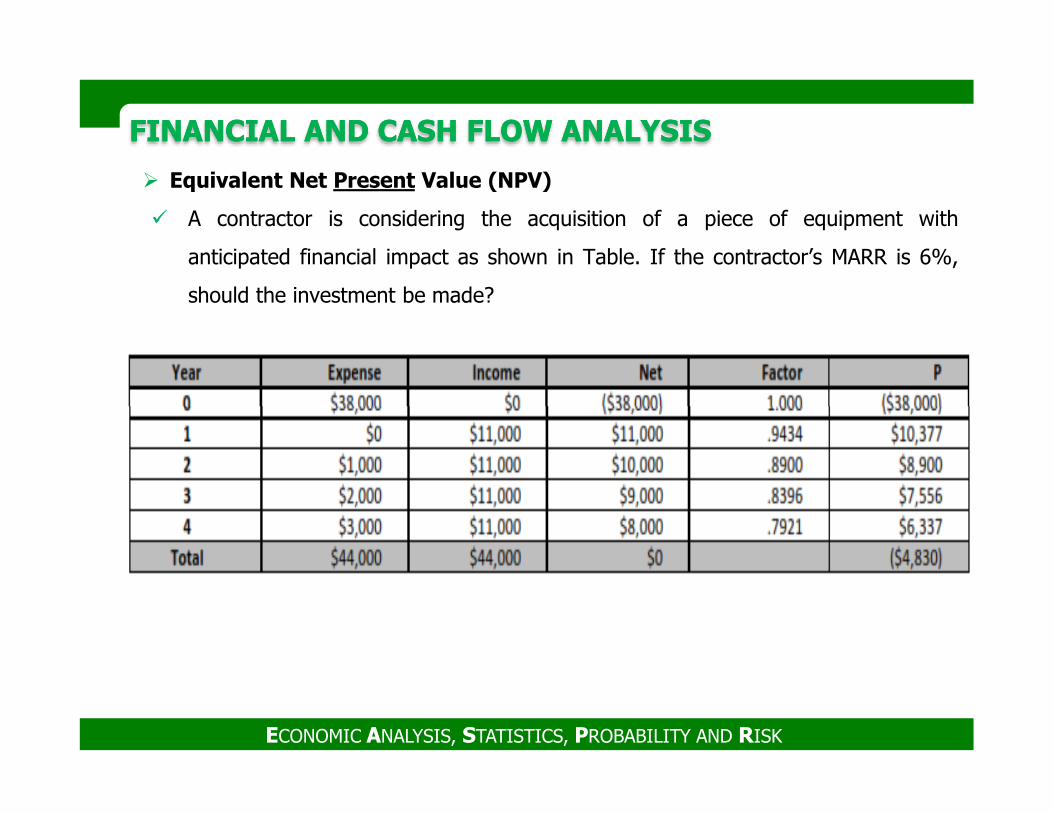

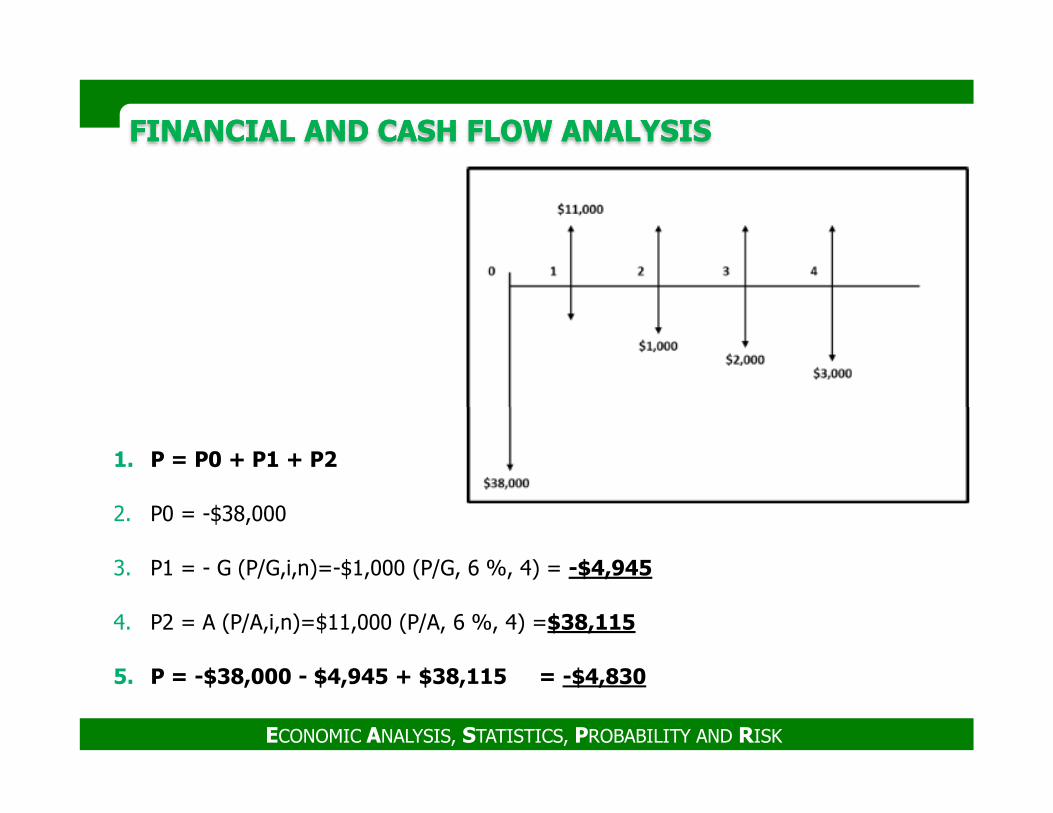

� Equivalent Net Present Value (NPV)

� A contractor is considering the acquisition of a piece of equipment with

anticipated financial impact as shown in Table. If the contractor’s MARR is 6%,

should the investment be made?

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

1. P = P0 + P1 + P2

2. P0 = -$38,000

3. P1 = - G (P/G,i,n)=-$1,000 (P/G, 6 %, 4) = -$4,945

4. P2 = A (P/A,i,n)=$11,000 (P/A, 6 %, 4) =$38,115

5. P = -$38,000 - $4,945 + $38,115 = -$4,830

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

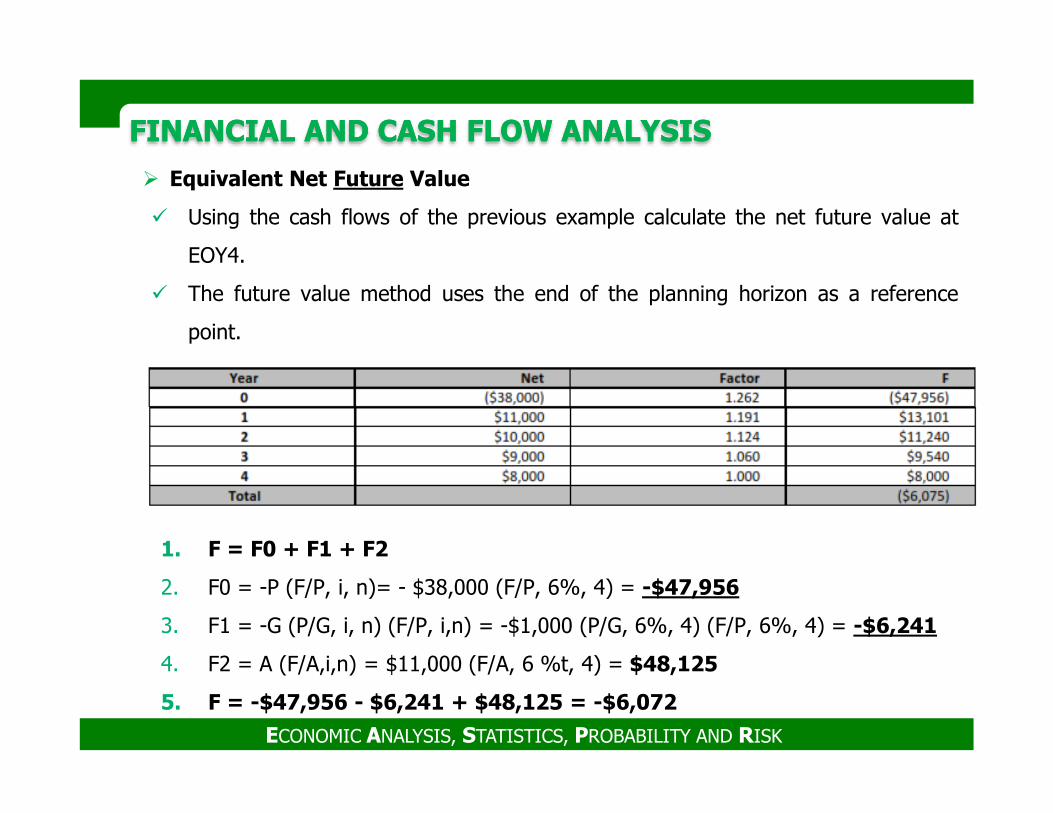

� Equivalent Net Future Value

� Using the cash flows of the previous example calculate the net future value at

EOY4.

� The future value method uses the end of the planning horizon as a reference

point.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

1. F = F0 + F1 + F2

2. F0 = -P (F/P, i, n)= - $38,000 (F/P, 6%, 4) = -$47,956

3. F1 = -G (P/G, i, n) (F/P, i,n) = -$1,000 (P/G, 6%, 4) (F/P, 6%, 4) = -$6,241

4. F2 = A (F/A,i,n) = $11,000 (F/A, 6 %t, 4) = $48,125

5. F = -$47,956 - $6,241 + $48,125 = -$6,072

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

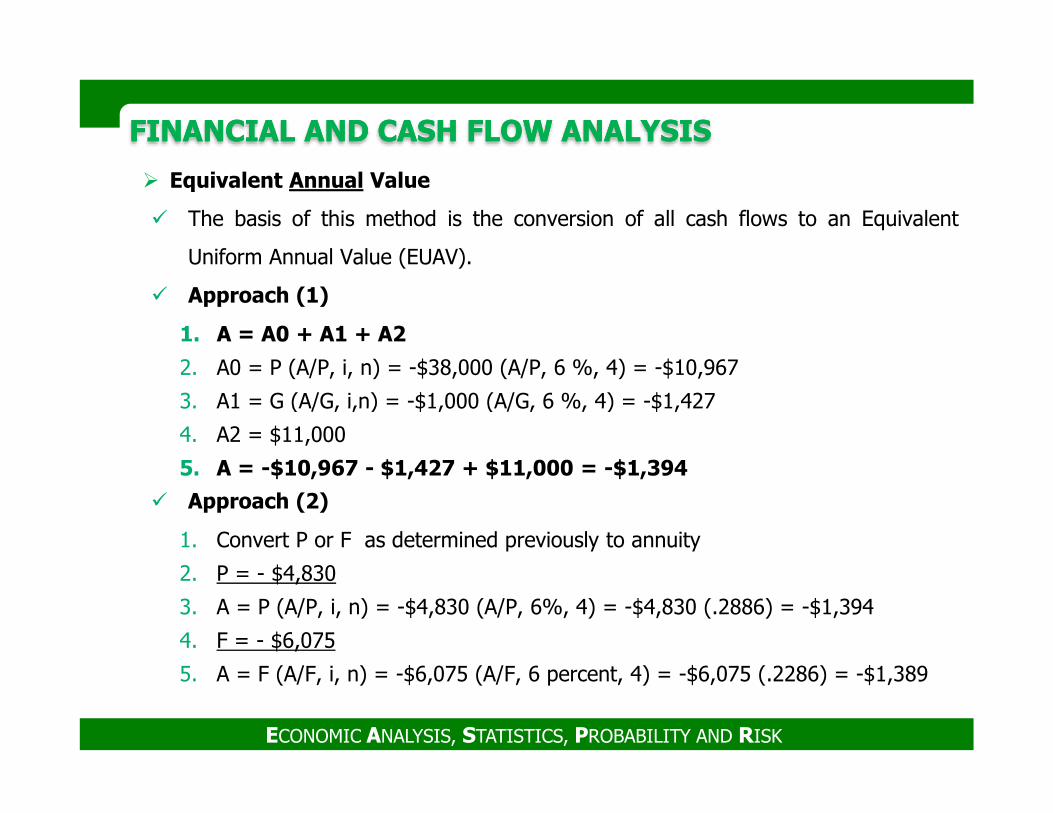

� Equivalent Annual Value

� The basis of this method is the conversion of all cash flows to an Equivalent

Uniform Annual Value (EUAV).

� Approach (1)

1. A = A0 + A1 + A2

2. A0 = P (A/P, i, n) = -$38,000 (A/P, 6 %, 4) = -$10,967

3. A1 = G (A/G, i,n) = -$1,000 (A/G, 6 %, 4) = -$1,427

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

3. A1 = G (A/G, i,n) = -$1,000 (A/G, 6 %, 4) = -$1,427

4. A2 = $11,000

5. A = -$10,967 - $1,427 + $11,000 = -$1,394

� Approach (2)

1. Convert P or F as determined previously to annuity

2. P = - $4,830

3. A = P (A/P, i, n) = -$4,830 (A/P, 6%, 4) = -$4,830 (.2886) = -$1,394

4. F = - $6,075

5. A = F (A/F, i, n) = -$6,075 (A/F, 6 percent, 4) = -$6,075 (.2286) = -$1,389

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

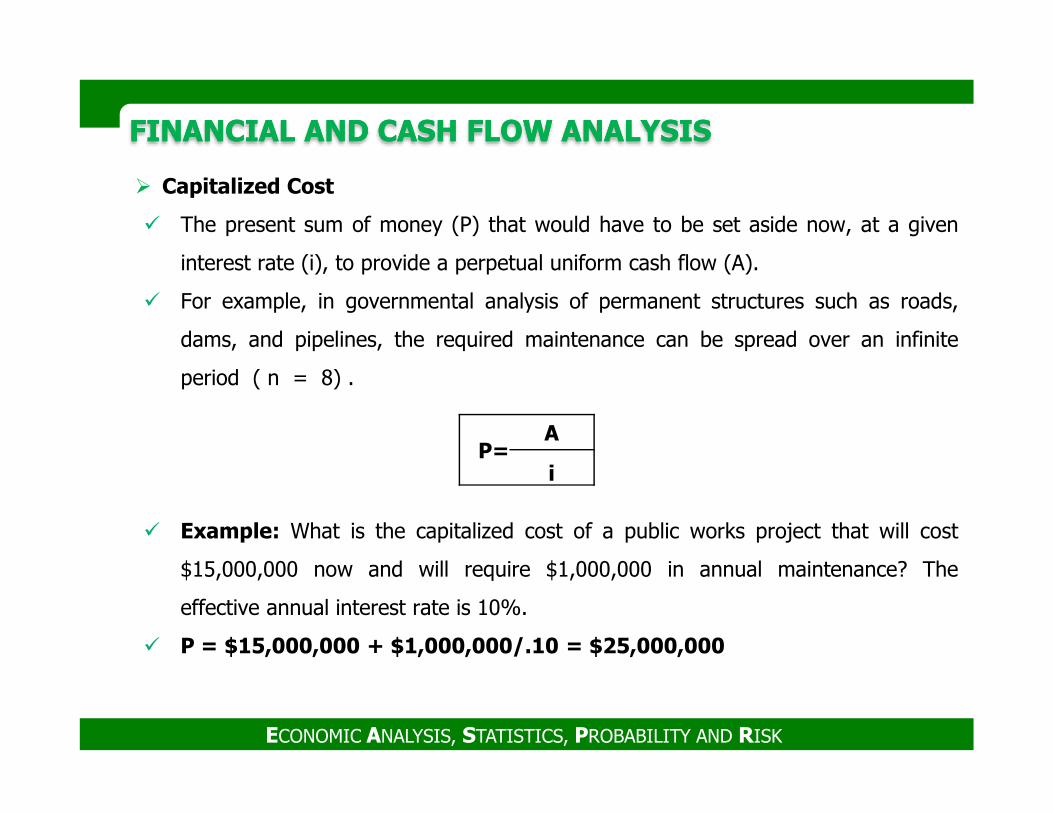

� Capitalized Cost

� The present sum of money (P) that would have to be set aside now, at a given

interest rate (i), to provide a perpetual uniform cash flow (A).

� For example, in governmental analysis of permanent structures such as roads,

dams, and pipelines, the required maintenance can be spread over an infinite

period ( n = 8) .

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Example: What is the capitalized cost of a public works project that will cost

$15,000,000 now and will require $1,000,000 in annual maintenance? The

effective annual interest rate is 10%.

� P = $15,000,000 + $1,000,000/.10 = $25,000,000

P=A

i

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

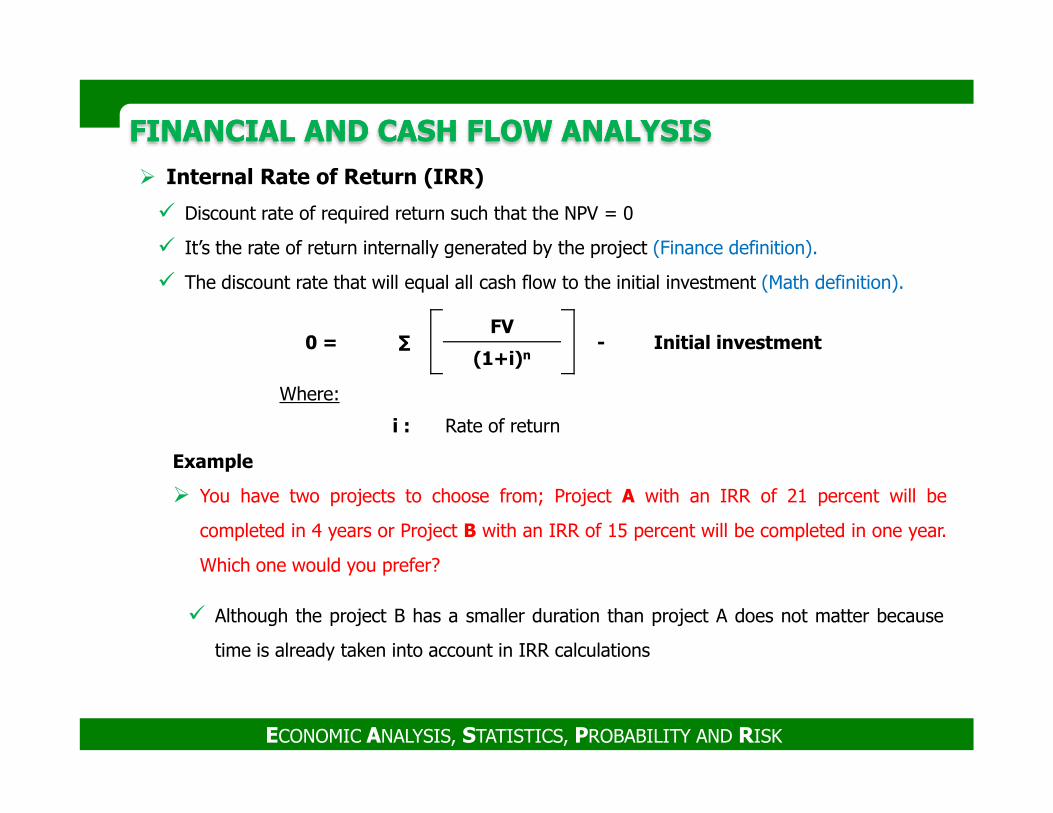

� Internal Rate of Return (IRR)

� Discount rate of required return such that the NPV = 0

� It’s the rate of return internally generated by the project (Finance definition).

� The discount rate that will equal all cash flow to the initial investment (Math definition).

0 = ∑FV

- Initial investment(1+i)n

Where:

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Although the project B has a smaller duration than project A does not matter because

time is already taken into account in IRR calculations

Example

� You have two projects to choose from; Project A with an IRR of 21 percent will be

completed in 4 years or Project B with an IRR of 15 percent will be completed in one year.

Which one would you prefer?

i : Rate of return

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

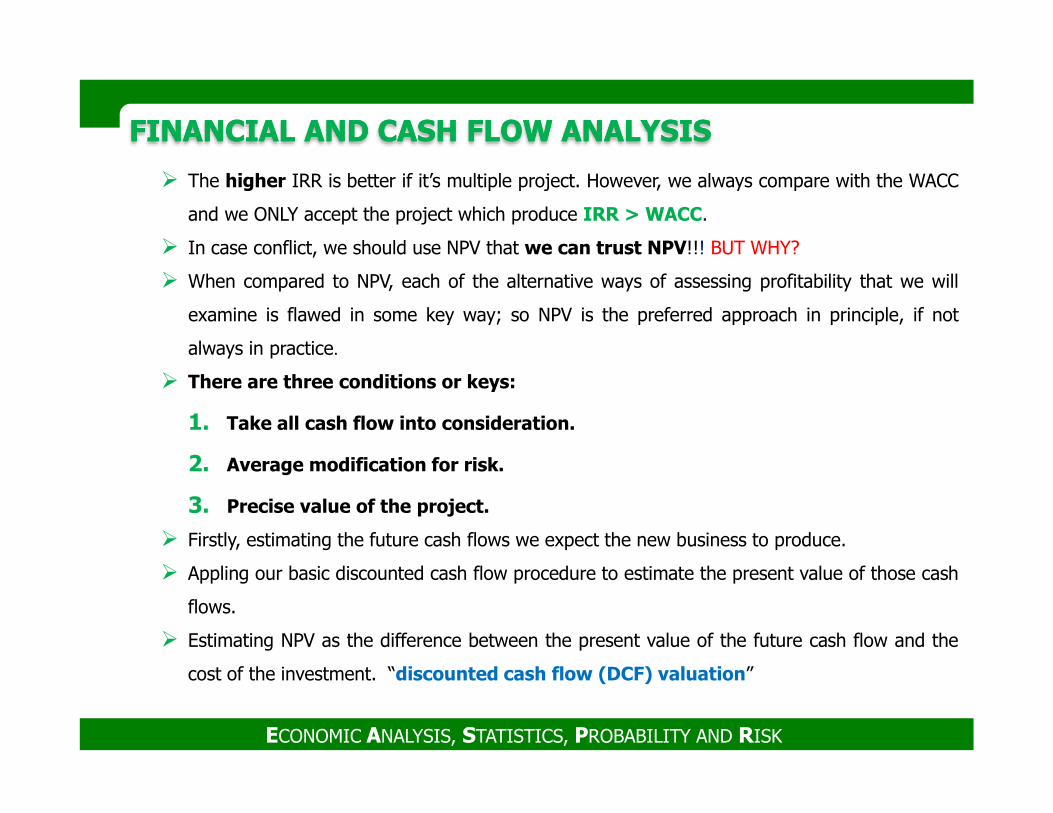

� The higher IRR is better if it’s multiple project. However, we always compare with the WACC

and we ONLY accept the project which produce IRR > WACC.

� In case conflict, we should use NPV that we can trust NPV!!! BUT WHY?

� When compared to NPV, each of the alternative ways of assessing profitability that we will

examine is flawed in some key way; so NPV is the preferred approach in principle, if not

always in practice.

� There are three conditions or keys:

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

1. Take all cash flow into consideration.

2. Average modification for risk.

3. Precise value of the project.

� Firstly, estimating the future cash flows we expect the new business to produce.

� Appling our basic discounted cash flow procedure to estimate the present value of those cash

flows.

� Estimating NPV as the difference between the present value of the future cash flow and the

cost of the investment. “discounted cash flow (DCF) valuation”

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

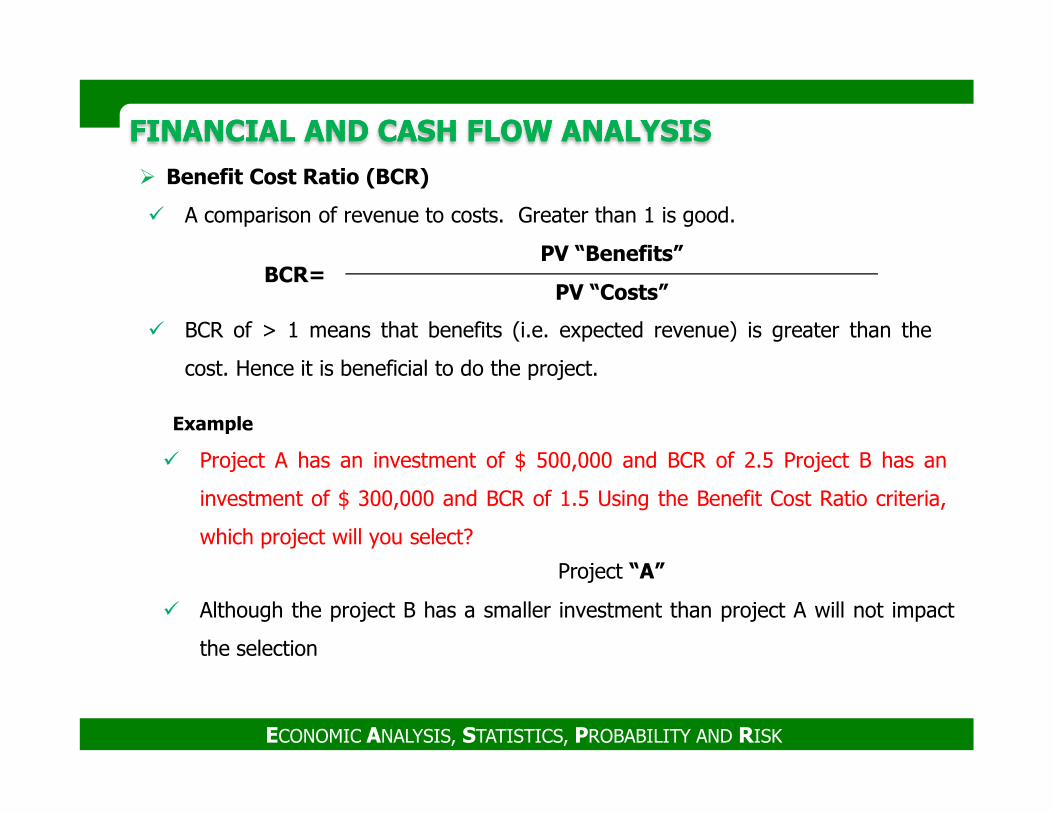

� Benefit Cost Ratio (BCR)

� A comparison of revenue to costs. Greater than 1 is good.

� BCR of > 1 means that benefits (i.e. expected revenue) is greater than the

cost. Hence it is beneficial to do the project.

BCR=PV “Benefits”

PV “Costs”

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Project “A”

Example

� Project A has an investment of $ 500,000 and BCR of 2.5 Project B has an

investment of $ 300,000 and BCR of 1.5 Using the Benefit Cost Ratio criteria,

which project will you select?

� Although the project B has a smaller investment than project A will not impact

the selection

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS Workshop

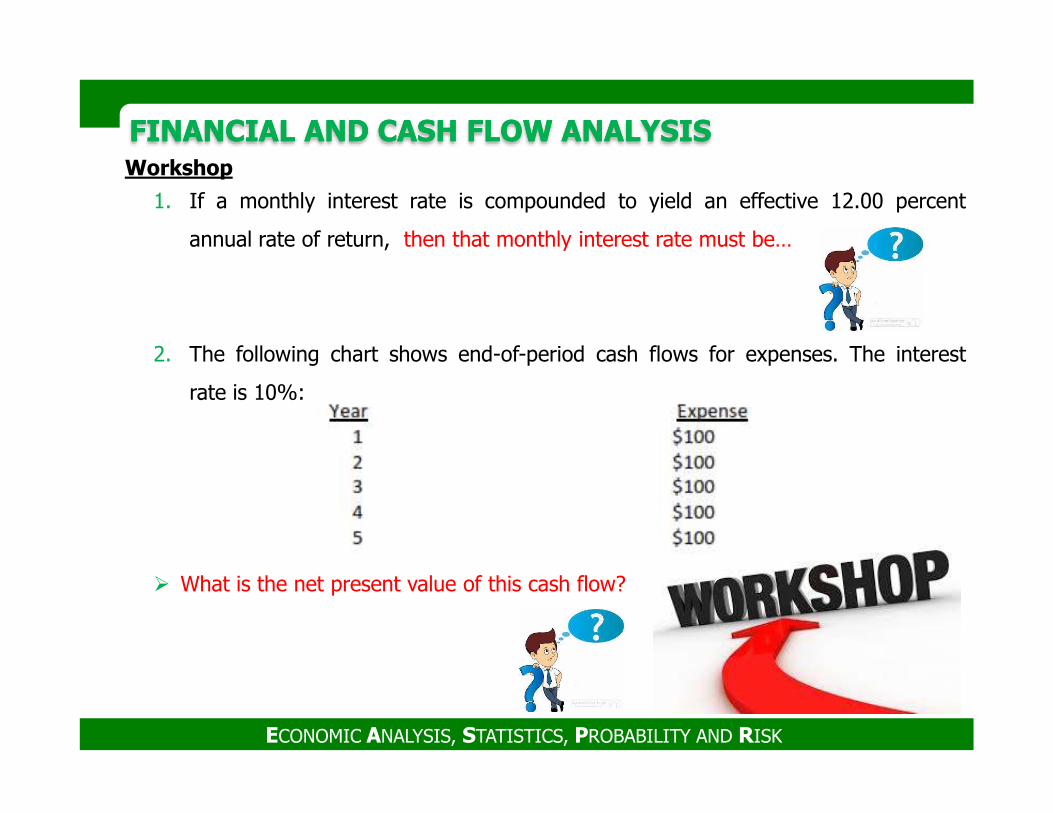

1. If a monthly interest rate is compounded to yield an effective 12.00 percent

annual rate of return, then that monthly interest rate must be…

2. The following chart shows end-of-period cash flows for expenses. The interest

rate is 10%:

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� What is the net present value of this cash flow?

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS Workshop

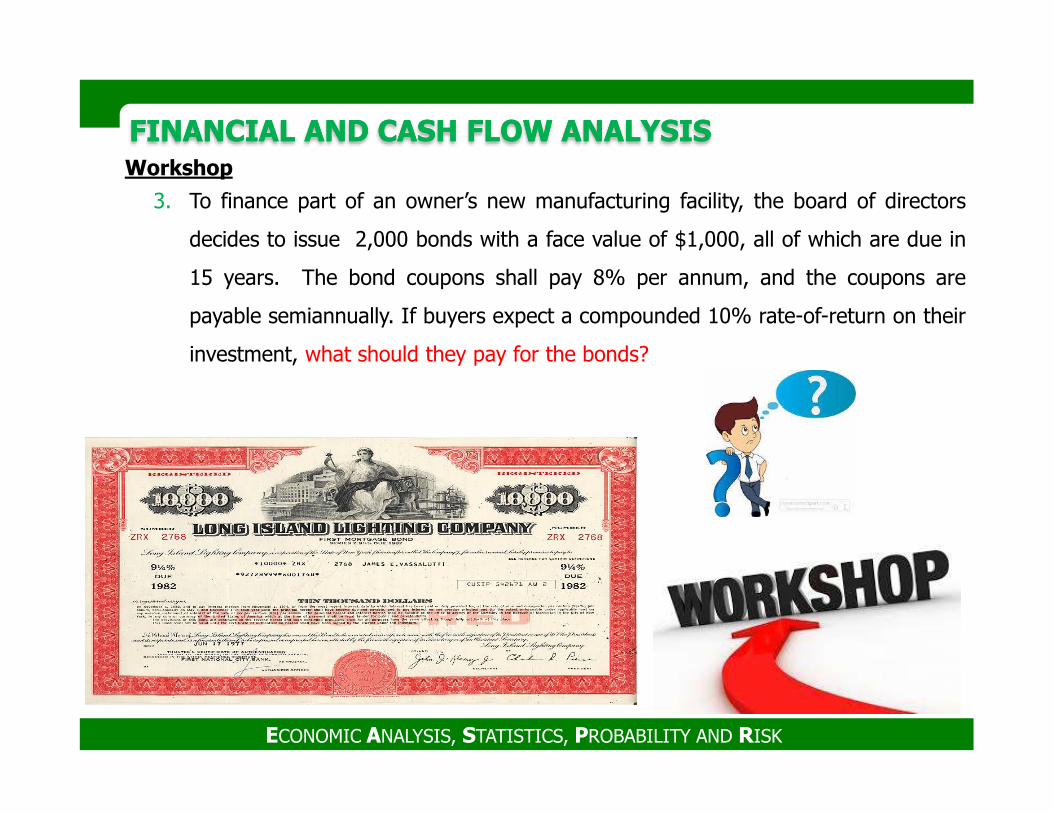

3. To finance part of an owner’s new manufacturing facility, the board of directors

decides to issue 2,000 bonds with a face value of $1,000, all of which are due in

15 years. The bond coupons shall pay 8% per annum, and the coupons are

payable semiannually. If buyers expect a compounded 10% rate-of-return on their

investment, what should they pay for the bonds?

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS Workshop

A chemical engineer obtains a 17-year patent for a new process and determines to

sell it, intending to invest the proceeds for his eventual retirement. A company

desires to purchase the patent and offers the engineer either of two options:

a. Sell the patent rights for royalties of $20,000 per year for four years, followed

by $10,000 per year for four additional years.

b. Immediately sell the patent rights for a lump-sum of $85,000.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

The engineer estimates the weighted average annual return after taxes on his

retirement investment accounts to be 11%. His effective income tax rate will be 40%

for the lump-sum option and 35% for periodic payments.

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS Workshop

1. The cash inflows for option “a” could be viewed equivalently as:A. $10,000 per year for years 1 through 8, plus $10,000 per year for years 1

through 4B. $20,000 per year for years 1 through 4, plus $10,000 per year for years 5

through 8C. Both A and BD. None of the above

2. The 11% discount rate is properly applied:

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

A. After expected income taxes are deducted from the cash inflows each yearB. Before expected income taxes are deducted from the cash inflows each yearC. Both A and B are correct due to equivalenceD. None of the above

3. The NPV of the after-tax cash flow for year 4 of option “a” is????

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

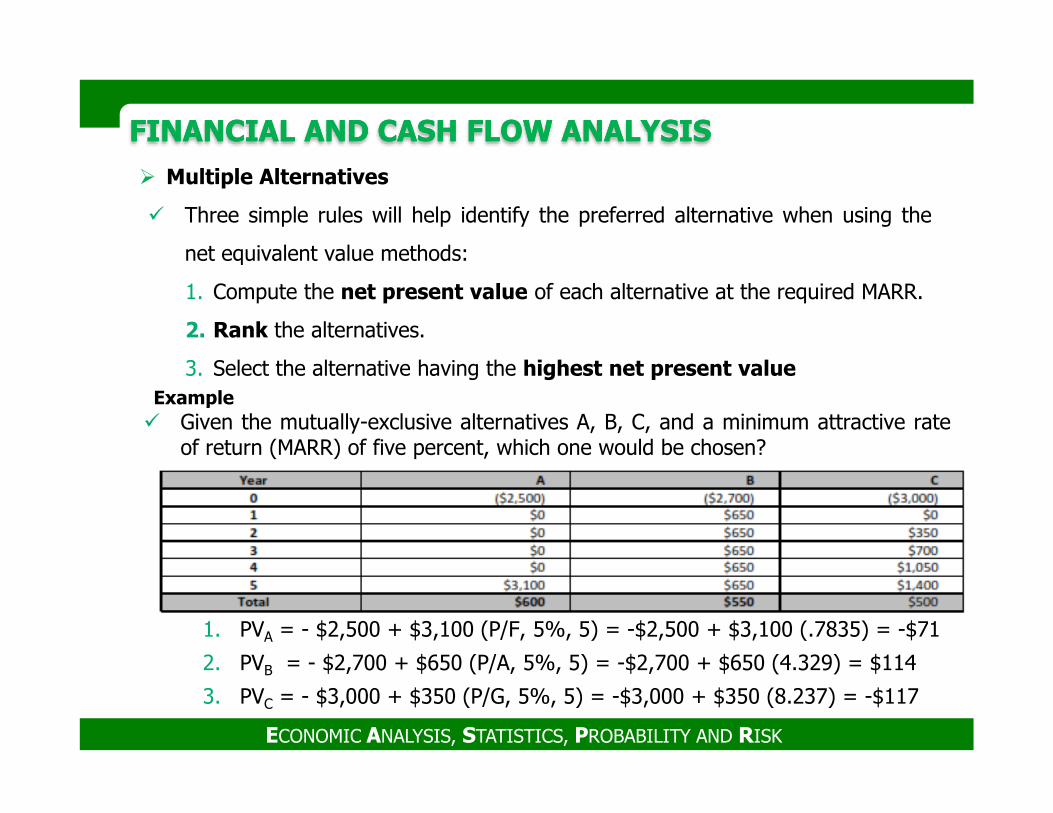

� Multiple Alternatives

� Three simple rules will help identify the preferred alternative when using the

net equivalent value methods:

1. Compute the net present value of each alternative at the required MARR.

2. Rank the alternatives.

3. Select the alternative having the highest net present valueExample

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Example� Given the mutually-exclusive alternatives A, B, C, and a minimum attractive rate

of return (MARR) of five percent, which one would be chosen?

1. PVA = - $2,500 + $3,100 (P/F, 5%, 5) = -$2,500 + $3,100 (.7835) = -$71

2. PVB = - $2,700 + $650 (P/A, 5%, 5) = -$2,700 + $650 (4.329) = $114

3. PVC = - $3,000 + $350 (P/G, 5%, 5) = -$3,000 + $350 (8.237) = -$117

FINANCIAL AND CASH FLOW ANALYSIS FINANCIAL AND CASH FLOW ANALYSIS

� Incremental Analysis

� This technique is based on the paired comparison of alternatives.

� The following steps should be followed in an incremental rate-of return analysis:

1. Identify all alternatives.

2. Calculate the ROR for each alternative and discard any alternative with ROR <

MARR.

3. Arrange remaining alternatives in ascending order of initial cost.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

3. Arrange remaining alternatives in ascending order of initial cost.

4. Calculate the ROR on the difference between the first two (lowest initial cost)

alternatives (if this ∆ROR = MARR, retain the higher cost alternative, otherwise

retain the lower cost alternative).

5. Select the retained alternative from the previous step, compare it to the next

higher alternative using the calculation of step 4 and calculate the rate-of-return

on their difference (if this ∆ROR = MARR, retain the higher cost alternative,

otherwise retain the lower cost alternative).

6. Repeat this process until all alternatives have been evaluated.

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

� Capital is financial assets or financial value of assets.

� Capital is a limited resource, and there are numerous projects that are

competing for funding.

� Investment decision makers review many projects and options to evaluate

what is best for the company.

� The Project Assessment Document (PAD) facilitate the review process.

� There are three important elements required by investment decision makers:

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� There are three important elements required by investment decision makers:

1. Value to the Company

2. Effect on Cash Flow

3. Transparency of Risk to the Company

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

i. Value to the Company

� Company’s market and operating condition.

� A project aligned with the core values (strategic vision) of the company.

� Business lines that are difficult to sustain and that pull a company away from its

strategic vision will erode the cash flow of the company over time.

ii. Effect on Cash Flow

� Cash flow analysis is generally more important than profit analysis.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Cash flow analysis is generally more important than profit analysis.

� It is important to determine the viability of company.

� Projects must support and improve the cash flow of a company.

� Not all projects generate profit, but they can improve the cash flow of a company.

iii. Transparency of Risk to the Company

� A transparent, clear, and realistic accounting of risks is vital to assessing a project.

� It is far better to fund a well-defined (but less profitable) project than to fund

(gamble on) a highly profitable project with uncertain risks.

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

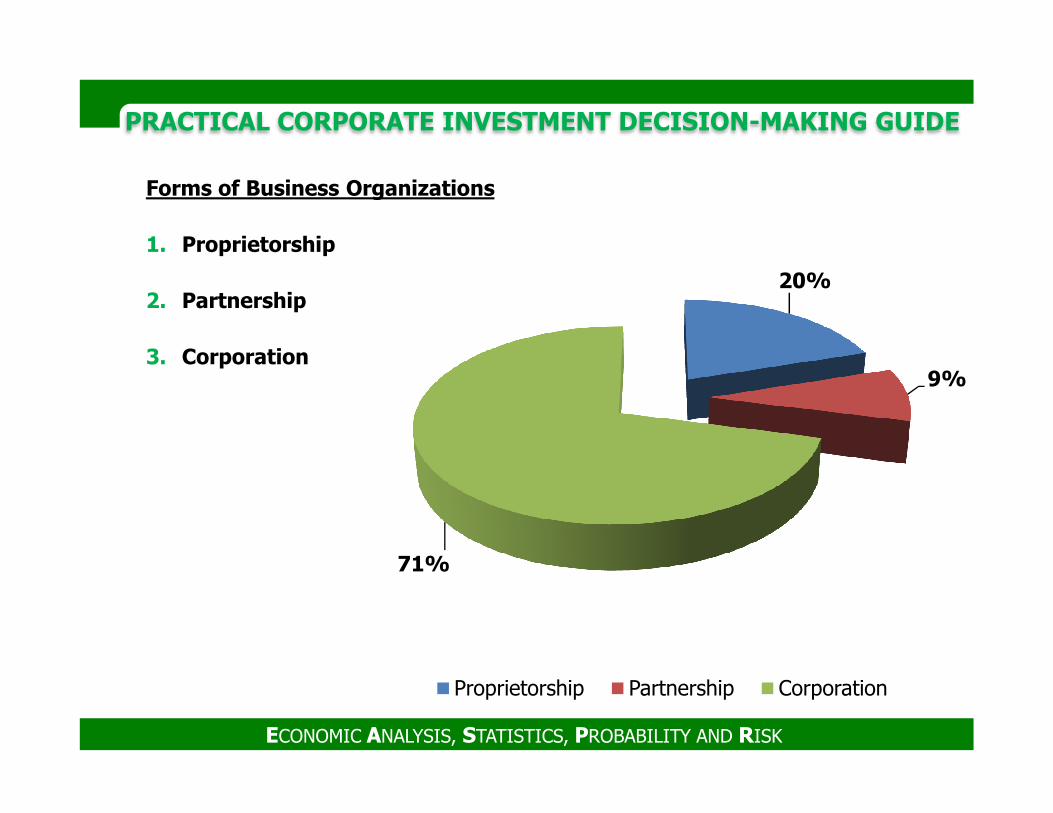

Forms of Business Organizations

1. Proprietorship

2. Partnership

3. Corporation

20%

9%

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

71%

Proprietorship Partnership Corporation

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

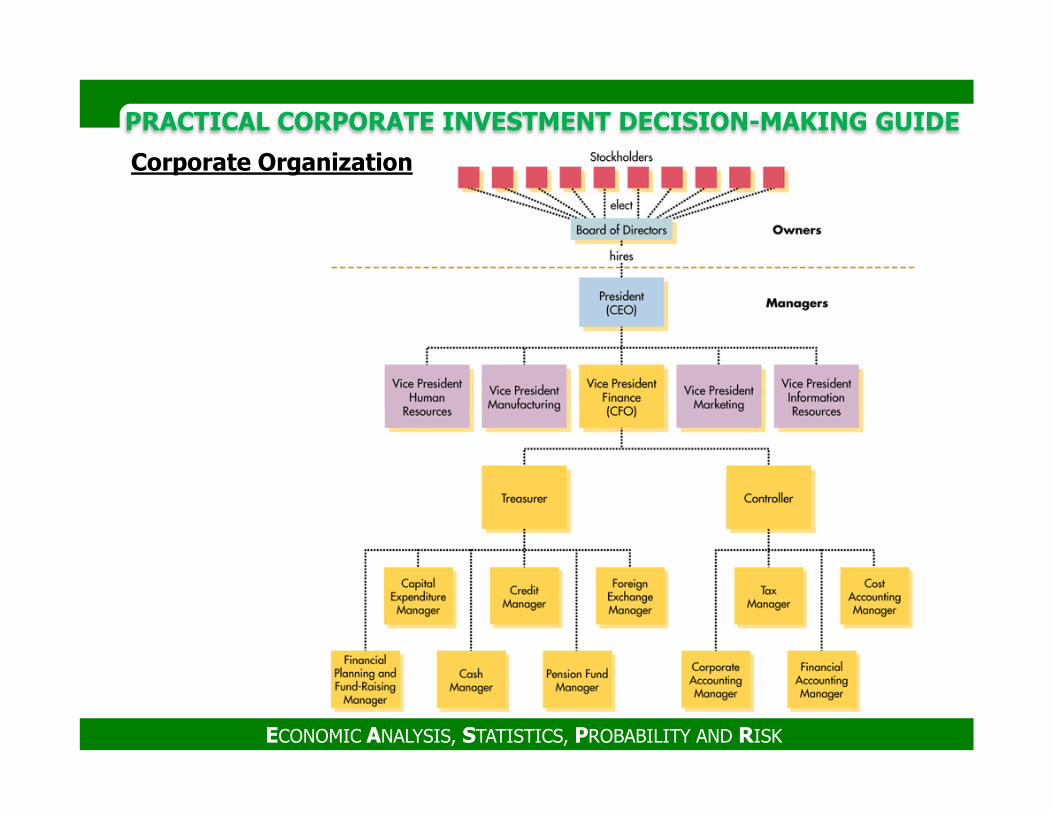

Corporate Organization

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

Goals of the Corporation

� Primary Goal

� MAXIMIZE Stockholder Wealth = MAXIMIZE Stock Price

� Managerial Incentives

Controlled by competitive forces

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Controlled by competitive forces

� Social Responsibility

� Must be mandated initially to reduce disadvantages

� Stock Price Maximization and Social Welfare

� Maximizing stock = benefiting society

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

� Front-End Engineering and Design (FEED)

� It helps establish a well-defined scope, budget, schedule, and identifies

risks, resulting in greater success during implementation and start-up.

� By undertaking FEED at the beginning of any project, you can minimize your

overall project risks.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Benchmark studies show benefits of up to 30% reduced cost and shorter

project execution times when FEED studies are performed.

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

� Front End Loading (FEL) or Pre-Project Planning (PPP)

� Defining the project scope and plans in a way that assures the best practical

level of definition is achieved as needed to support a project decision gate.

� FEL is pre-project planning to develop sufficient strategic information to

assess risks to make decisions concerning resources and insure success.

� The optimal critical success factors that define FEL are determined based upon

the project’s outcome as assessed by the key performance indicators.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

the project’s outcome as assessed by the key performance indicators.

� The key performance indicators

� By which an organization can measure the progress being made to ensure that

the critical success factors are being achieved.

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

� Average Annual Rate of Return (AARR)

� The measure (%) of profitability of an asset over a period of time.

� It is the average yearly profit over the operating lifecycle of a facility and

dividing it by the final cost of the project.

� It compares to the corporate discount rate of a company.

� Investment

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Investment

� The act of contributing money or capital into an enterprise with the expectation

of future profit.

� Investments have a limited decision time-frame to determine the impact of a

20-year life cycle on the company cash flow.

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

� Executive Summary

� There are 7 key elements to an executive summary:

1. Statement of the problem that the project addresses “how the project aligns

with their strategic investment portfolio”

2. Project Summary “what the project is, why it s important, and what the

value is to the investor”

3. Key Project Drivers “summarizes the key factors that influence the

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

3. Key Project Drivers “summarizes the key factors that influence the

economic indicators and cash flow for the company”

4. Primary Risks and Uncertainties

5. Capital Cost Variance

6. Average Annual Rate of Return Variance

7. Cash Flow Analysis

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

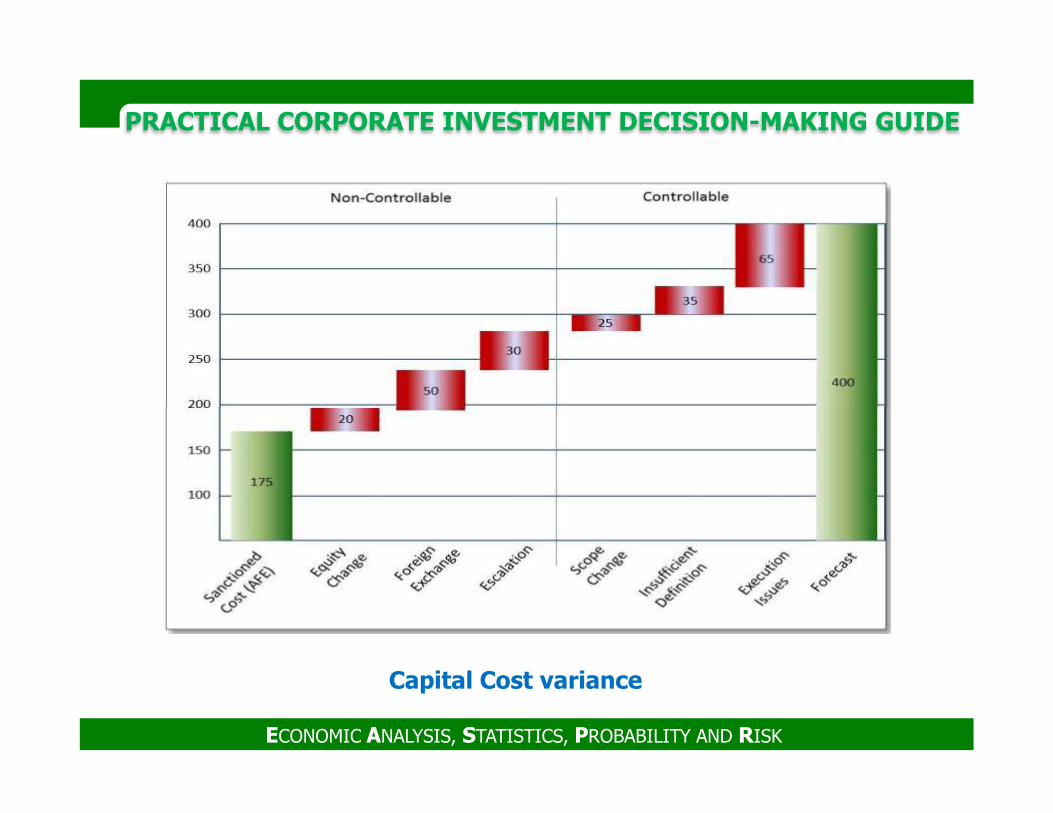

Capital Cost variance

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

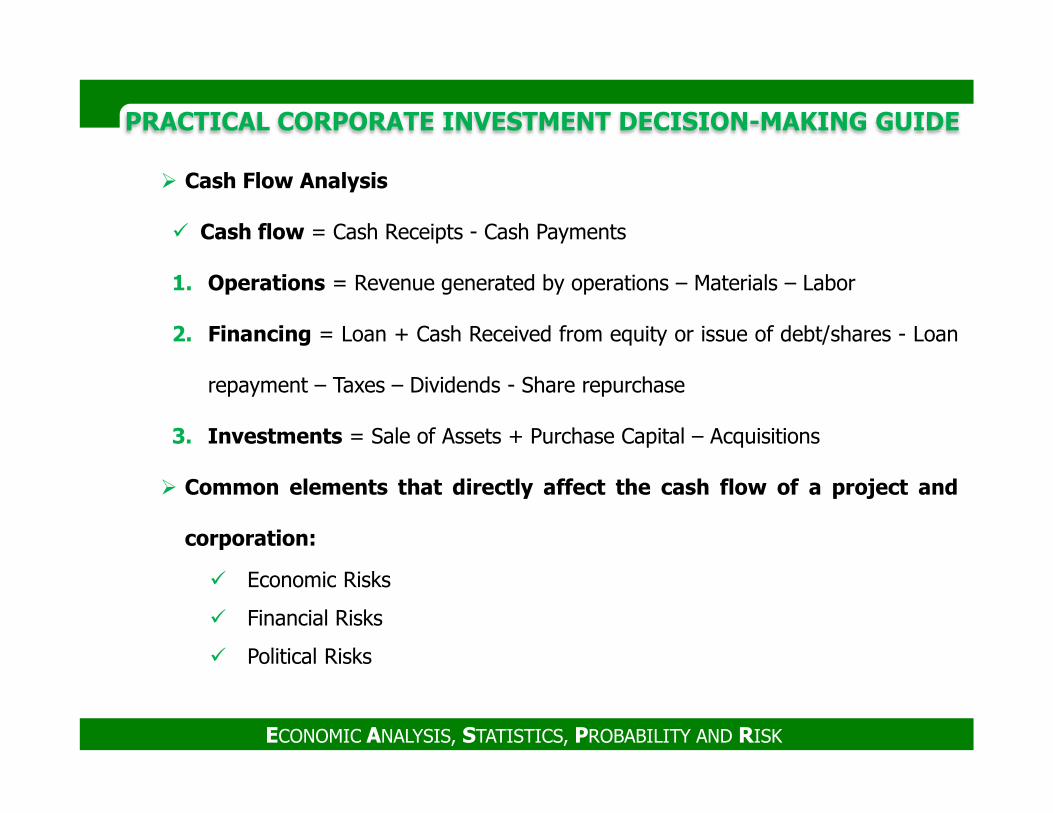

� Cash Flow Analysis

� Cash flow = Cash Receipts - Cash Payments

1. Operations = Revenue generated by operations – Materials – Labor

2. Financing = Loan + Cash Received from equity or issue of debt/shares - Loan

repayment – Taxes – Dividends - Share repurchase

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

3. Investments = Sale of Assets + Purchase Capital – Acquisitions

� Common elements that directly affect the cash flow of a project and

corporation:

� Economic Risks

� Financial Risks

� Political Risks

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

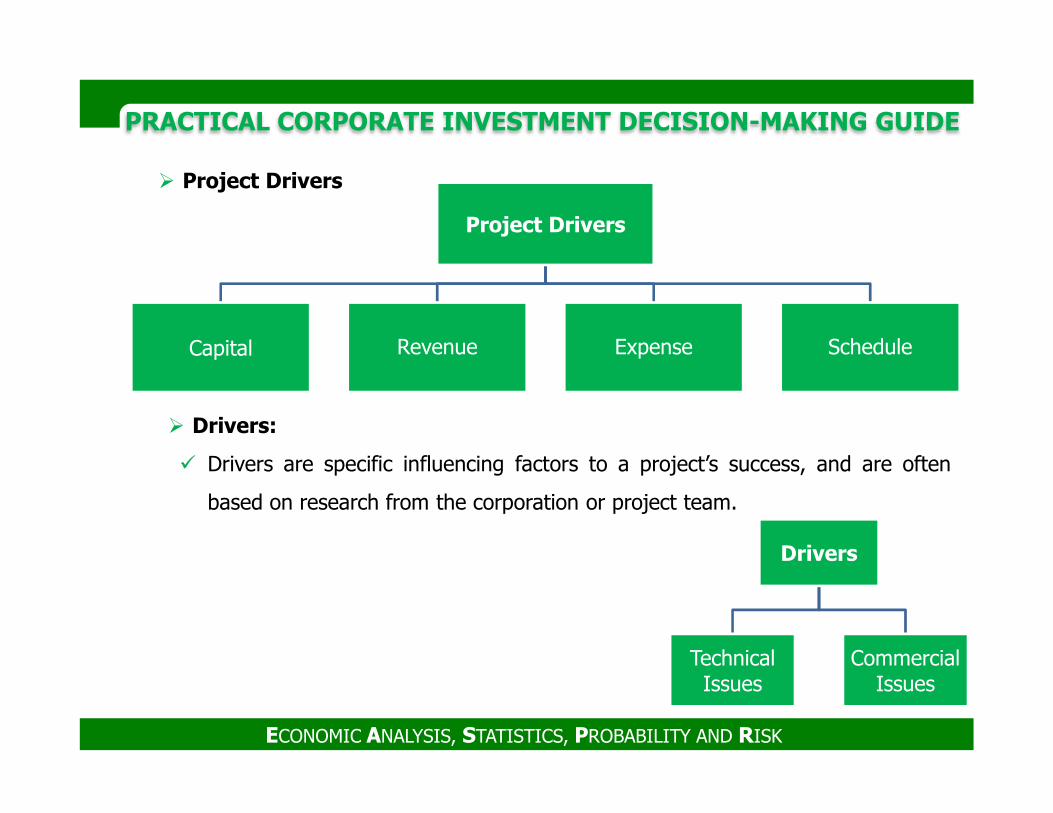

Project Drivers

Capital Revenue Expense Schedule

� Project Drivers

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Drivers:

� Drivers are specific influencing factors to a project’s success, and are often

based on research from the corporation or project team.

Drivers

Technical Issues

Commercial Issues

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

1. Capital Drivers

� The ultimate investment decision for the company must consider the total cost

of the project along with other cost drivers.

i. Technical Issues (The technical design alternatives need to be quantified in

terms of capital cost)

ii. Commercial Issues (Cost of land, cost of capital, credit risk, and taxation).

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

2. Revenue Drivers

� The primary revenue drivers for any commercial project are production (rate

and volume) and prices.

i. Technical Issues (Product strategy)

ii. Commercial Issues (keep the product viable over the planned life cycle and

keep the cash flow positive).

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

3. Expense Drivers

� The primary expense cost components are fixed operating costs, variable

operating costs, utilities, and fuel.

i. Fixed Operating Cost

ii. Variable Operating Cost

iii. Utilities

iv. Tariffs

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

iv. Tariffs

v. Regulations or regularity issues

4. Schedule Drivers

� The technical, commercial and political factors that contribute to the project

schedule and any uncertainty and risk.

i. Late Change to Scope or Design

ii. Force Majeure

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

� Economic Summary

� If the completed project is not meeting the economic indicators in the

future, then it is important to review the basis of the original economic premises

to determine what changed.

� Base Case Economic Indicators

� The project needs to declare the NPV, AARR on both a gross cost basis and net

cost basis.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

cost basis.

� Basic economic indicators should be considered to evaluate the project on a

near-term and long-term basis.

i. The Profitability Index (PI)

ii. The Return On Capital Employed (ROCE)

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

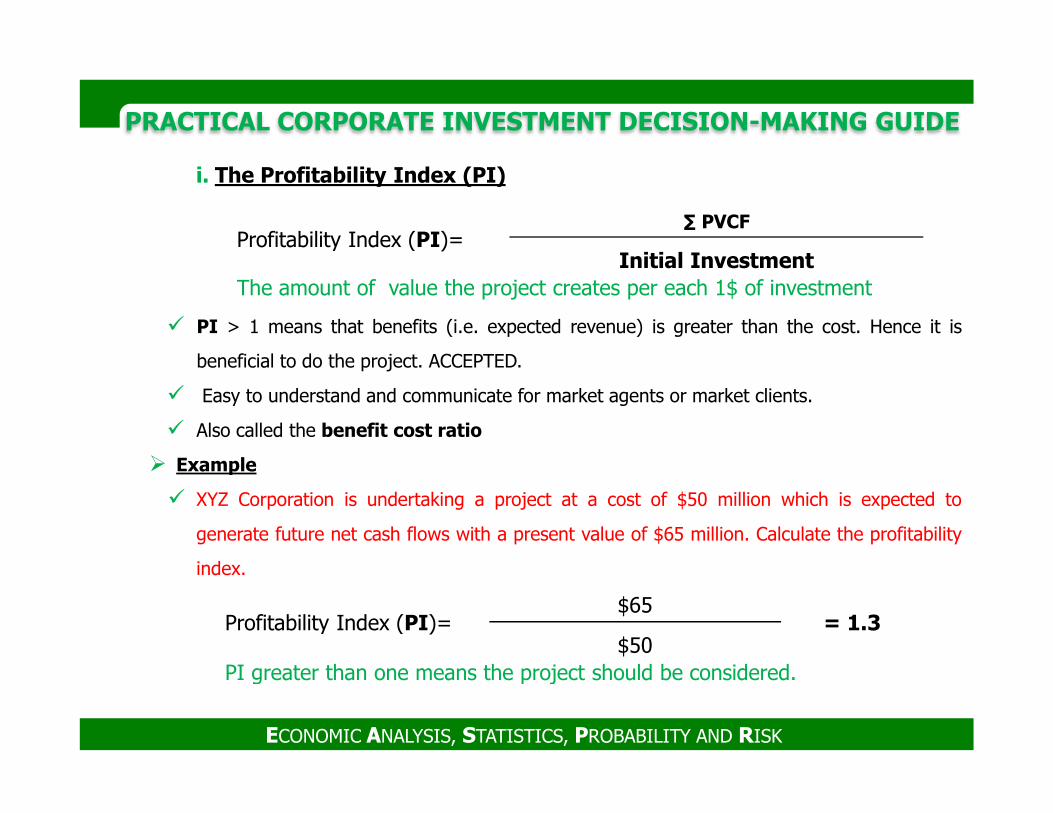

i. The Profitability Index (PI)

� PI > 1 means that benefits (i.e. expected revenue) is greater than the cost. Hence it is

beneficial to do the project. ACCEPTED.

� Easy to understand and communicate for market agents or market clients.

Profitability Index (PI)=∑ PVCF

Initial InvestmentThe amount of value the project creates per each 1$ of investment

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Also called the benefit cost ratio

� Example

� XYZ Corporation is undertaking a project at a cost of $50 million which is expected to

generate future net cash flows with a present value of $65 million. Calculate the profitability

index.

Profitability Index (PI)=$65

= 1.3$50

PI greater than one means the project should be considered.

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

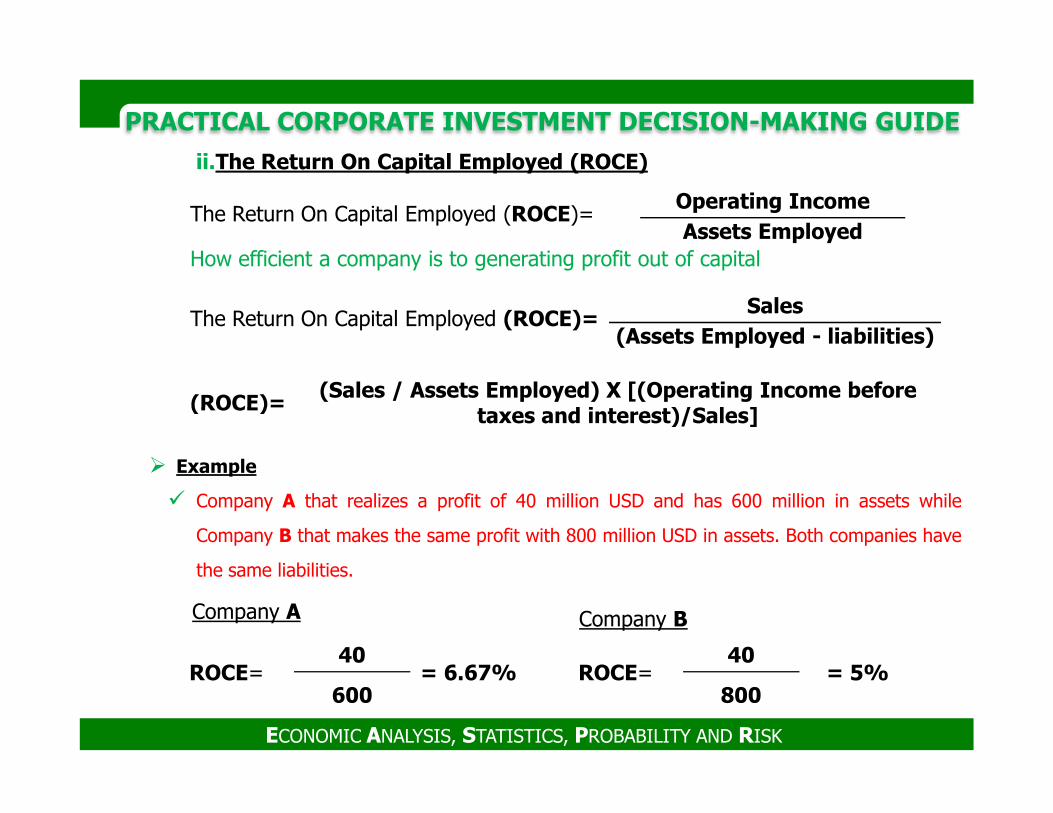

ii.The Return On Capital Employed (ROCE)

The Return On Capital Employed (ROCE)=Operating Income

Assets EmployedHow efficient a company is to generating profit out of capital

The Return On Capital Employed (ROCE)=Sales

(Assets Employed - liabilities)

(ROCE)=(Sales / Assets Employed) X [(Operating Income before

taxes and interest)/Sales]

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Example

� Company A that realizes a profit of 40 million USD and has 600 million in assets while

Company B that makes the same profit with 800 million USD in assets. Both companies have

the same liabilities.

ROCE=40

= 6.67%600

ROCE=40

= 5%800

Company A Company B

(ROCE)=taxes and interest)/Sales]

PRACTICAL CORPORATE INVESTMENT DECISION-MAKING GUIDE

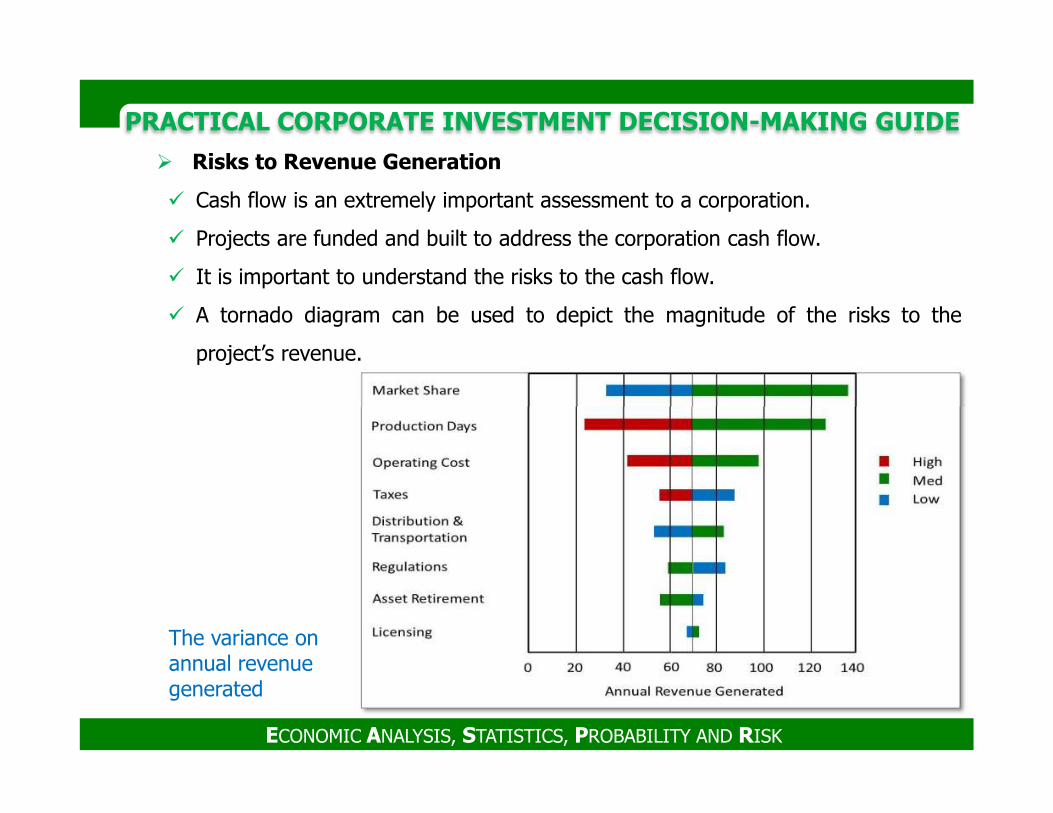

� Risks to Revenue Generation

� Cash flow is an extremely important assessment to a corporation.

� Projects are funded and built to address the corporation cash flow.

� It is important to understand the risks to the cash flow.

� A tornado diagram can be used to depict the magnitude of the risks to the

project’s revenue.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

The variance on annual revenue generated

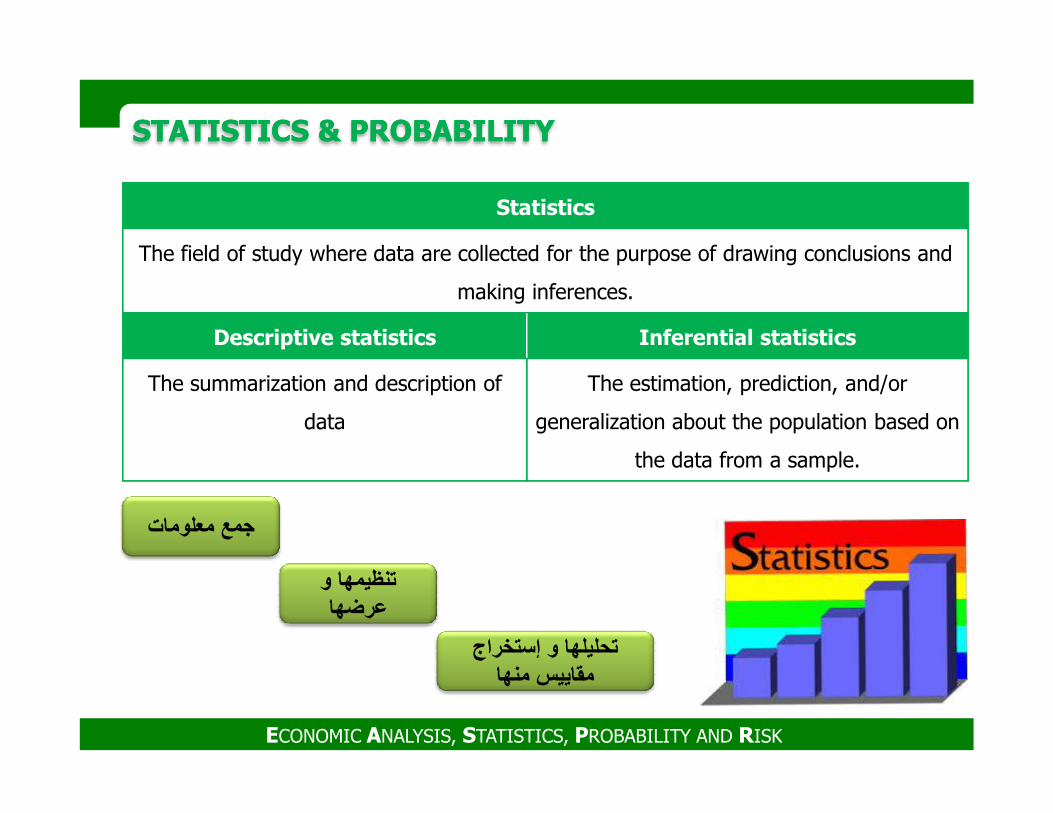

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

Statistics

The field of study where data are collected for the purpose of drawing conclusions and

making inferences.

Descriptive statistics Inferential statistics

The summarization and description of The estimation, prediction, and/or

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

data generalization about the population based on

the data from a sample.

جمع معلومات

تنظيمھا و عرضھا

تحليلھا و إستخراج مقاييس منھا

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

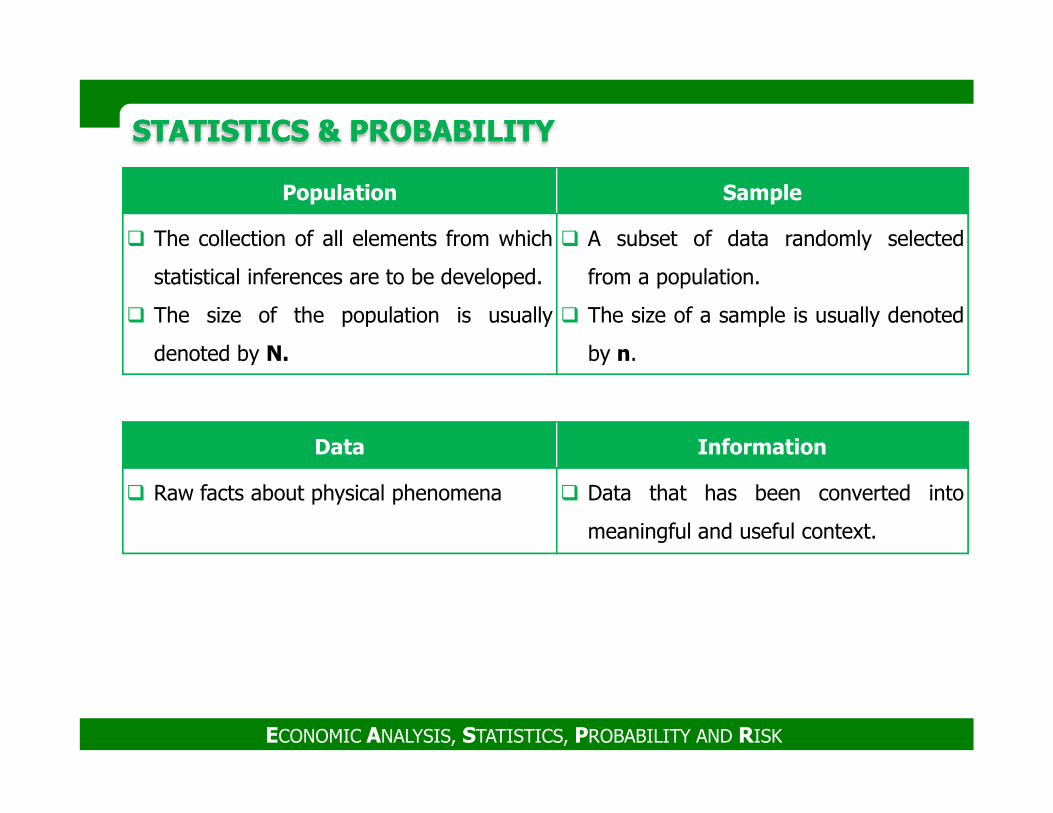

Population Sample

� The collection of all elements from which

statistical inferences are to be developed.

� The size of the population is usually

denoted by N.

� A subset of data randomly selected

from a population.

� The size of a sample is usually denoted

by n.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Data Information

� Raw facts about physical phenomena � Data that has been converted into

meaningful and useful context.

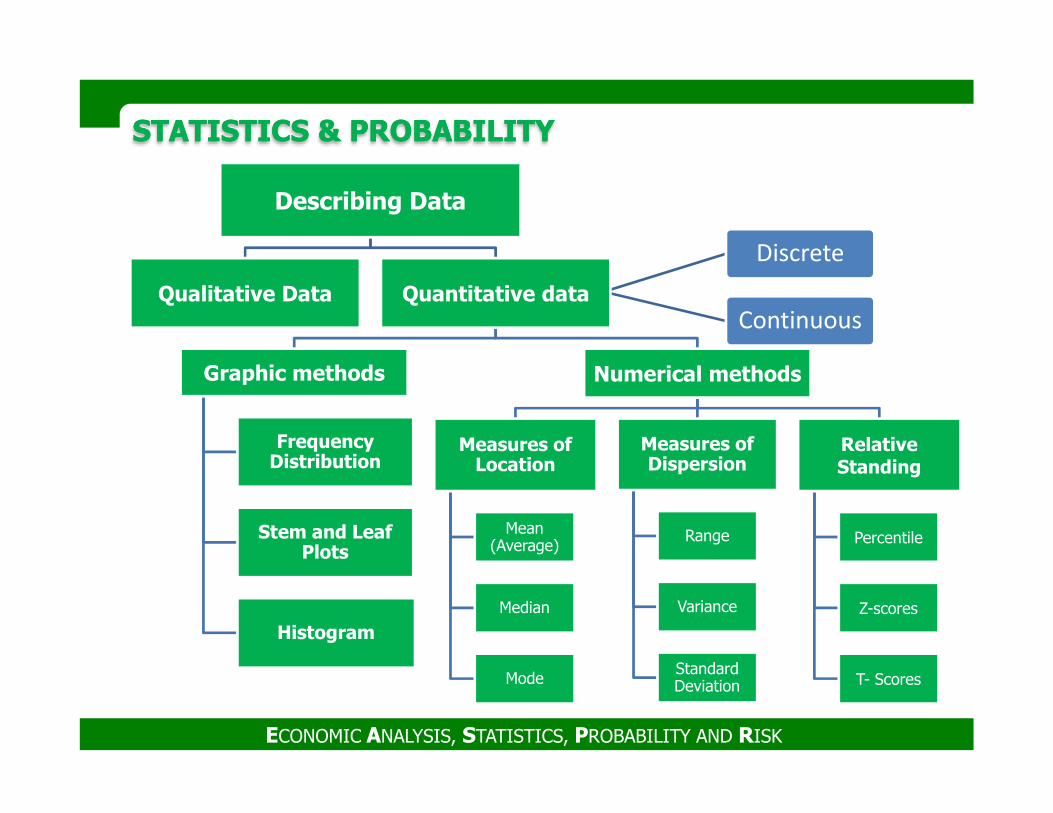

Quantitative

Discrete

Continuous

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

Describing Data

Qualitative Data Quantitative data

Graphic methods Numerical methods

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Frequency Distribution

Stem and Leaf Plots

Histogram

Measures of Location

Mean (Average)

Median

Mode

Measures of Dispersion

Range

Variance

Standard Deviation

Relative Standing

Percentile

Z-scores

T- Scores

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

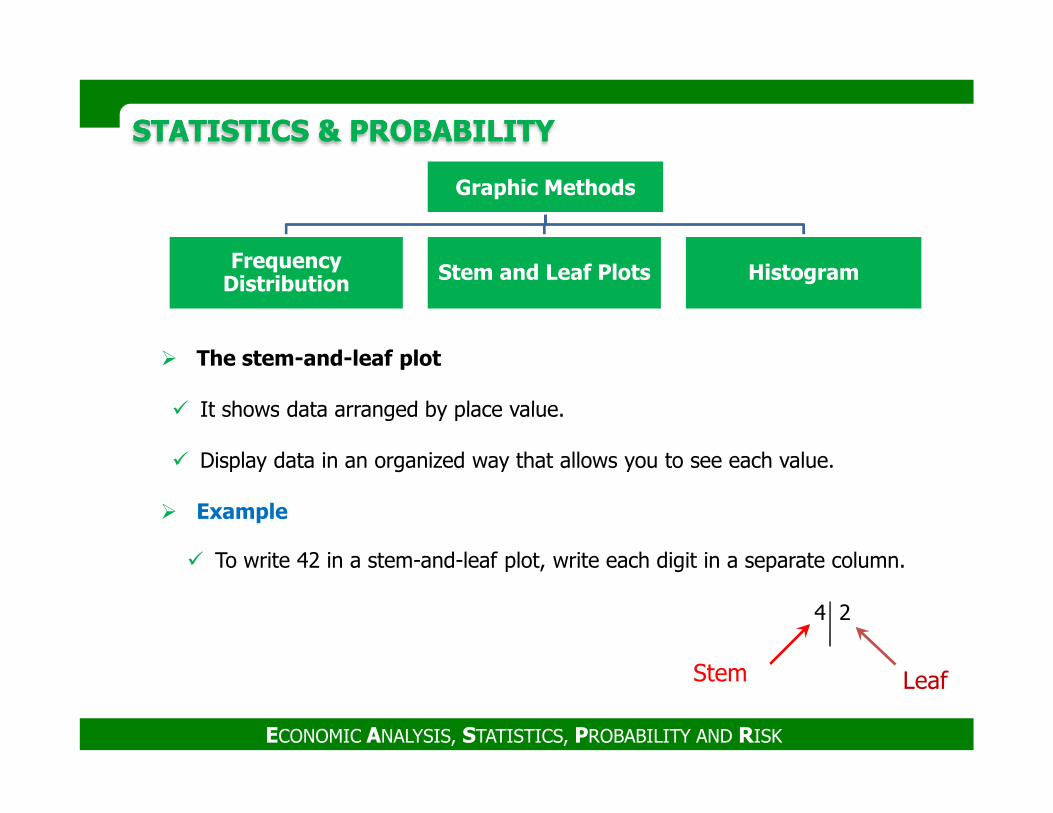

Graphic Methods

Frequency Distribution Stem and Leaf Plots Histogram

� The stem-and-leaf plot

� It shows data arranged by place value.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� It shows data arranged by place value.

� Display data in an organized way that allows you to see each value.

� Example

4 2

� To write 42 in a stem-and-leaf plot, write each digit in a separate column.

Stem Leaf

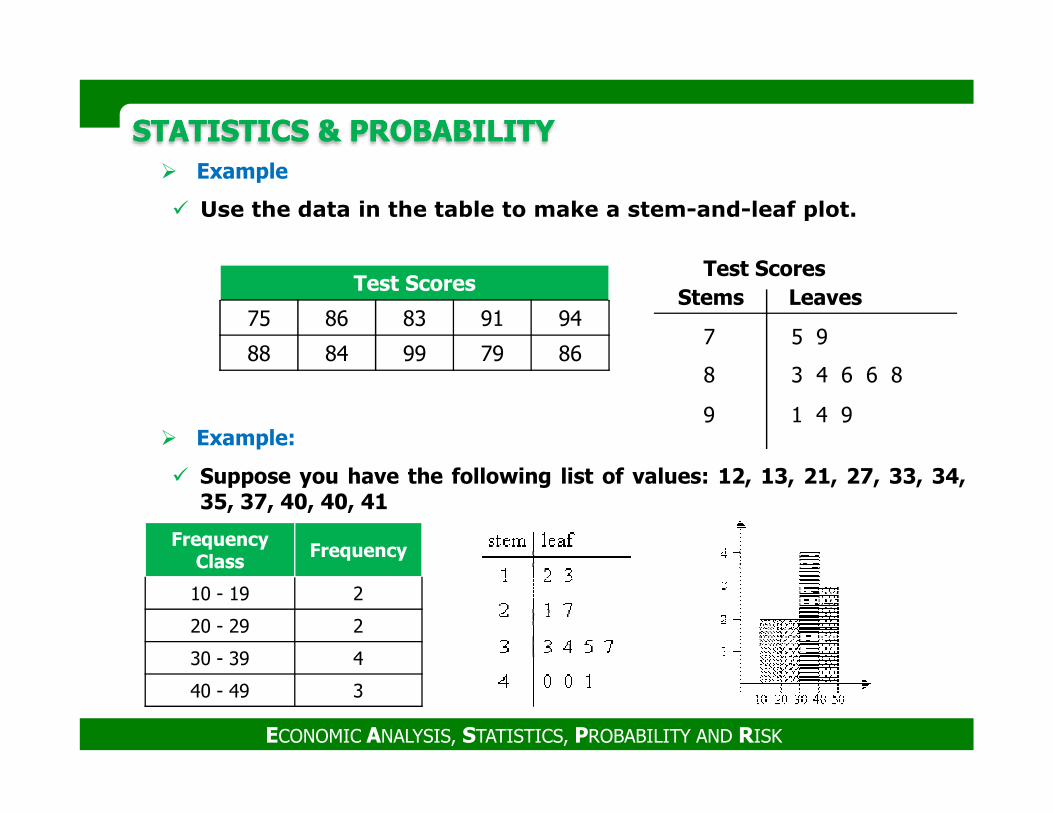

STATISTICS & PROBABILITY STATISTICS & PROBABILITY � Example

� Use the data in the table to make a stem-and-leaf plot.

Test Scores

75 86 83 91 94

88 84 99 79 86

StemsTest Scores

Leaves

7

8

9

5 9

3 4 6 6 8

1 4 9

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

9 1 4 9

FrequencyClass

Frequency

10 - 19 2

20 - 29 2

30 - 39 4

40 - 49 3

� Example:

� Suppose you have the following list of values: 12, 13, 21, 27, 33, 34,35, 37, 40, 40, 41

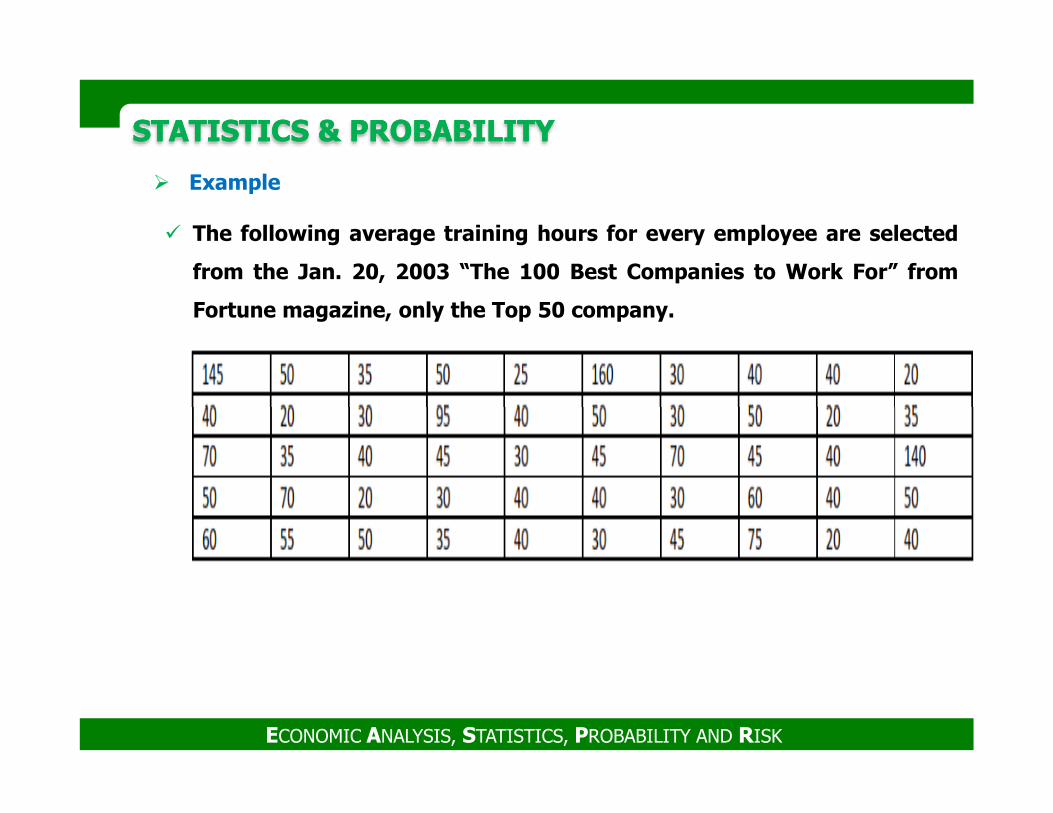

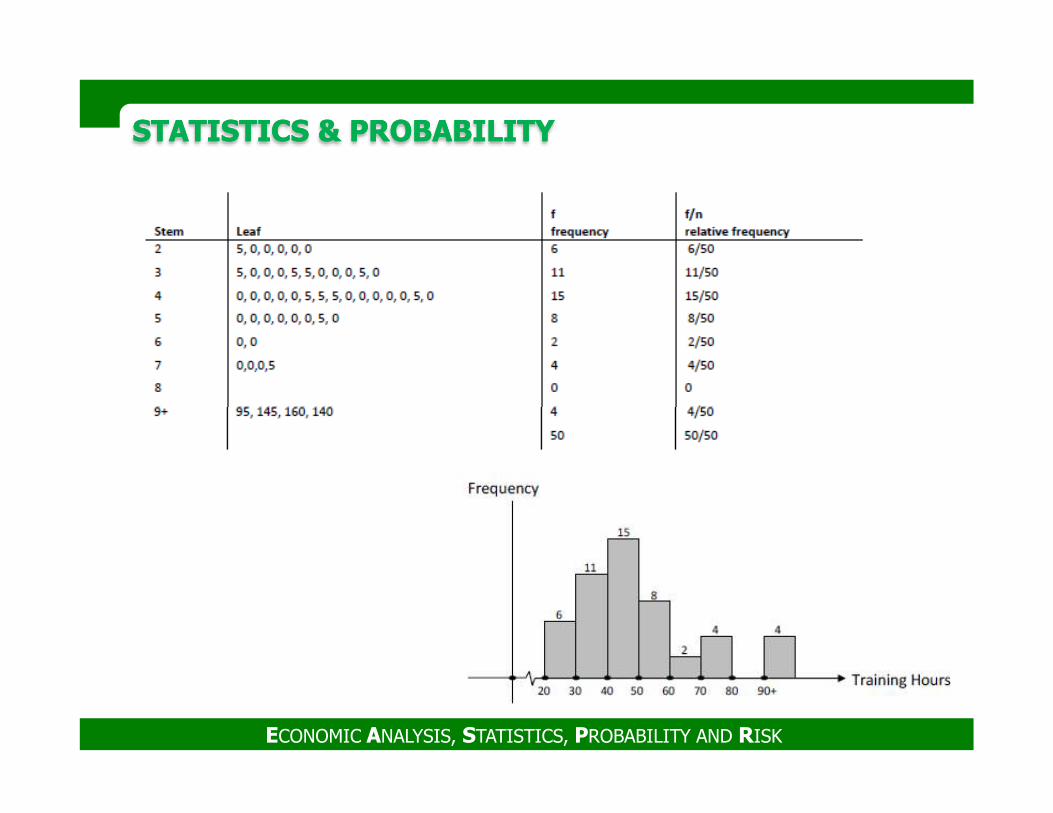

� Example

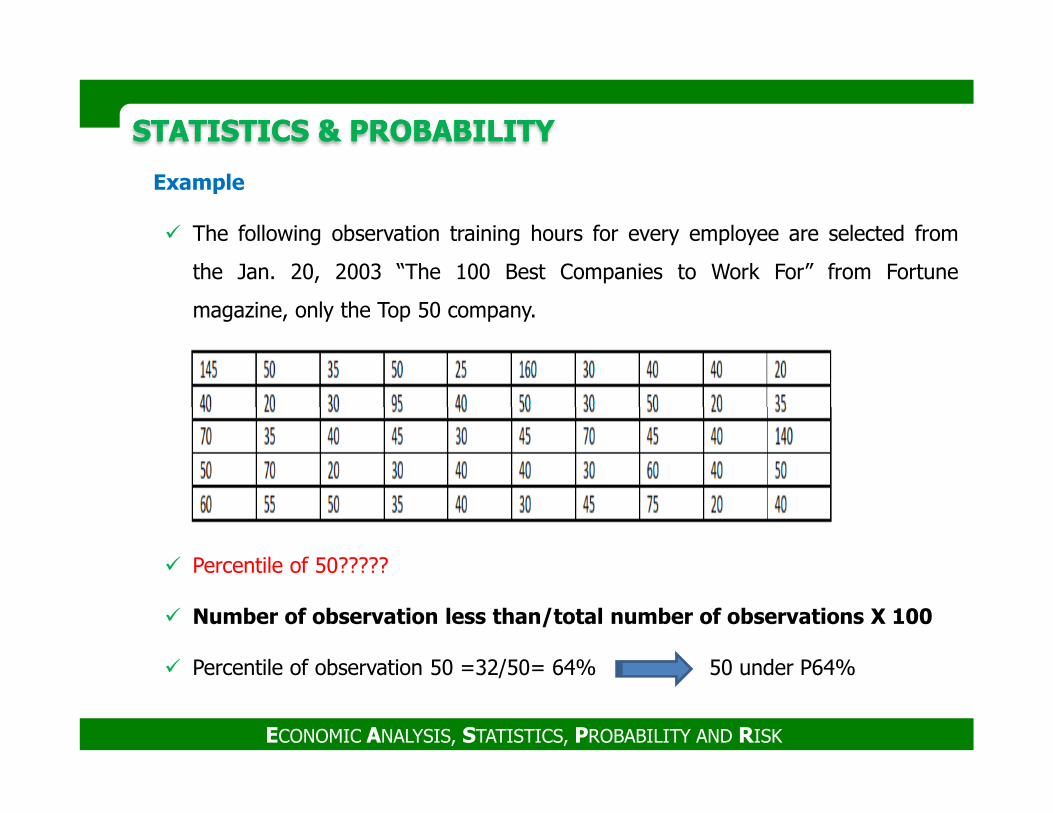

� The following average training hours for every employee are selected

from the Jan. 20, 2003 “The 100 Best Companies to Work For” from

Fortune magazine, only the Top 50 company.

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

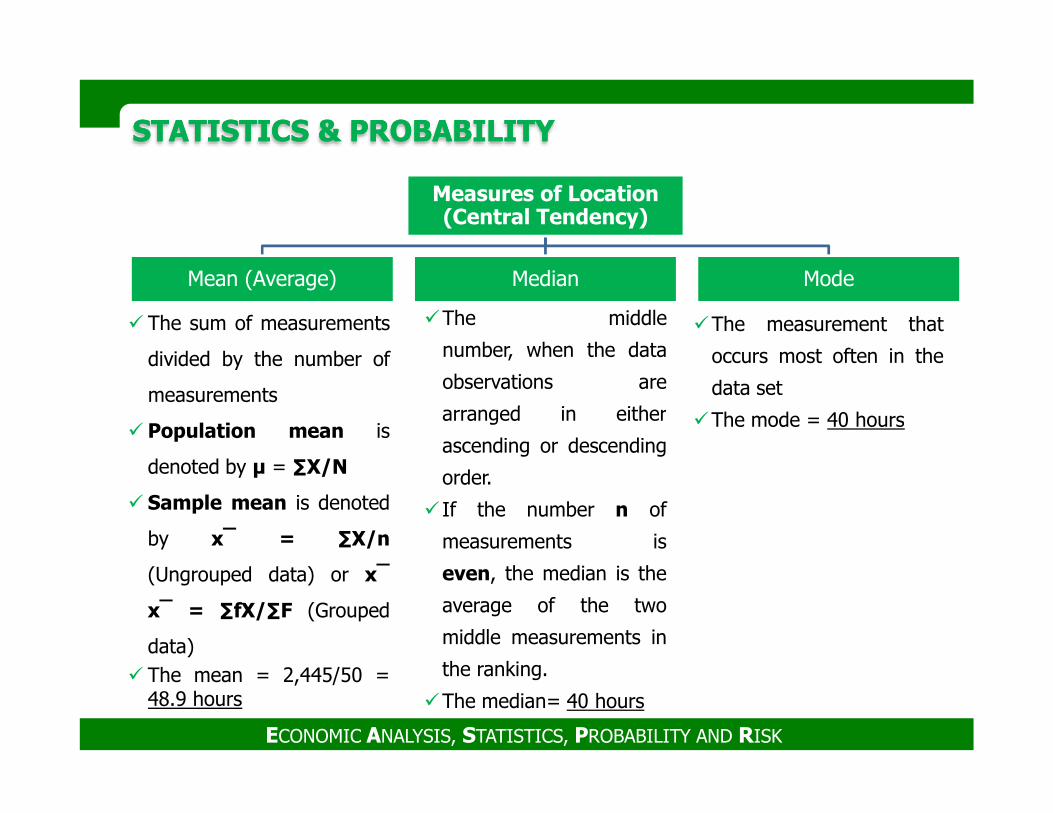

� The sum of measurements

divided by the number of

measurements

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

Measures of Location (Central Tendency)

Mean (Average) Median Mode

�The middle

number, when the data

observations are

arranged in either

�The measurement that

occurs most often in the

data set

The mode = 40 hours� Population mean is

denoted by µ = ∑X/N

� Sample mean is denoted

by x‾ = ∑X/n

(Ungrouped data) or x‾

x‾ = ∑fX/∑F (Grouped

data)� The mean = 2,445/50 =

48.9 hours

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

arranged in either

ascending or descending

order.

� If the number n of

measurements is

even, the median is the

average of the two

middle measurements in

the ranking.

�The median= 40 hours

�The mode = 40 hours

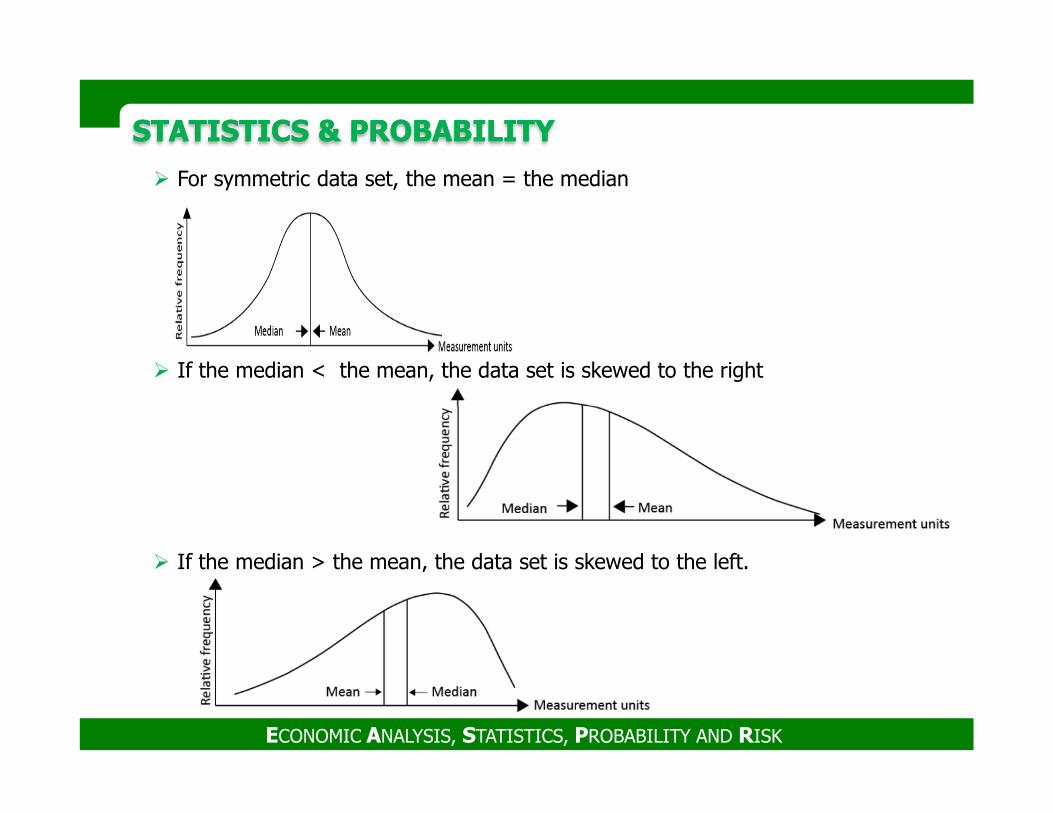

� For symmetric data set, the mean = the median

� If the median < the mean, the data set is skewed to the right

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

� If the median > the mean, the data set is skewed to the left.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

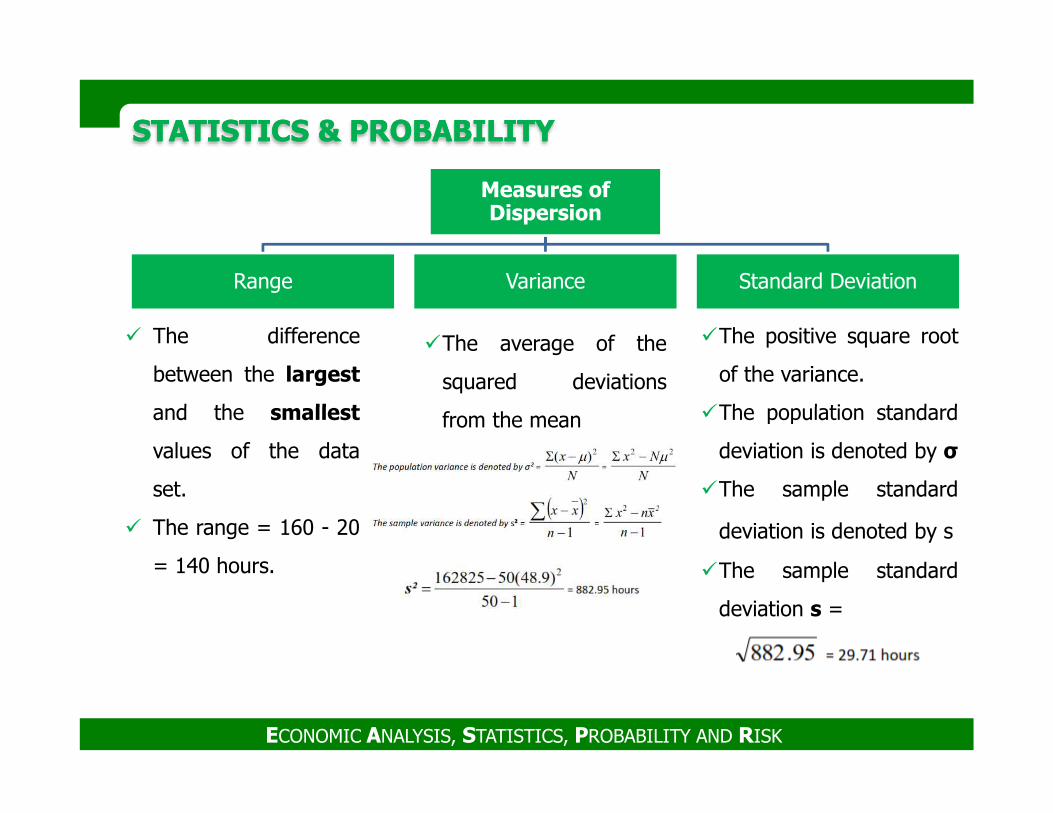

� The difference

between the largest

and the smallest

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

Measures of Dispersion

Range Variance Standard Deviation

�The average of the

squared deviations

from the mean

�The positive square root

of the variance.

�The population standardand the smallest

values of the data

set.

� The range = 160 - 20

= 140 hours.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

from the mean �The population standard

deviation is denoted by σ

�The sample standard

deviation is denoted by s

�The sample standard

deviation s =

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

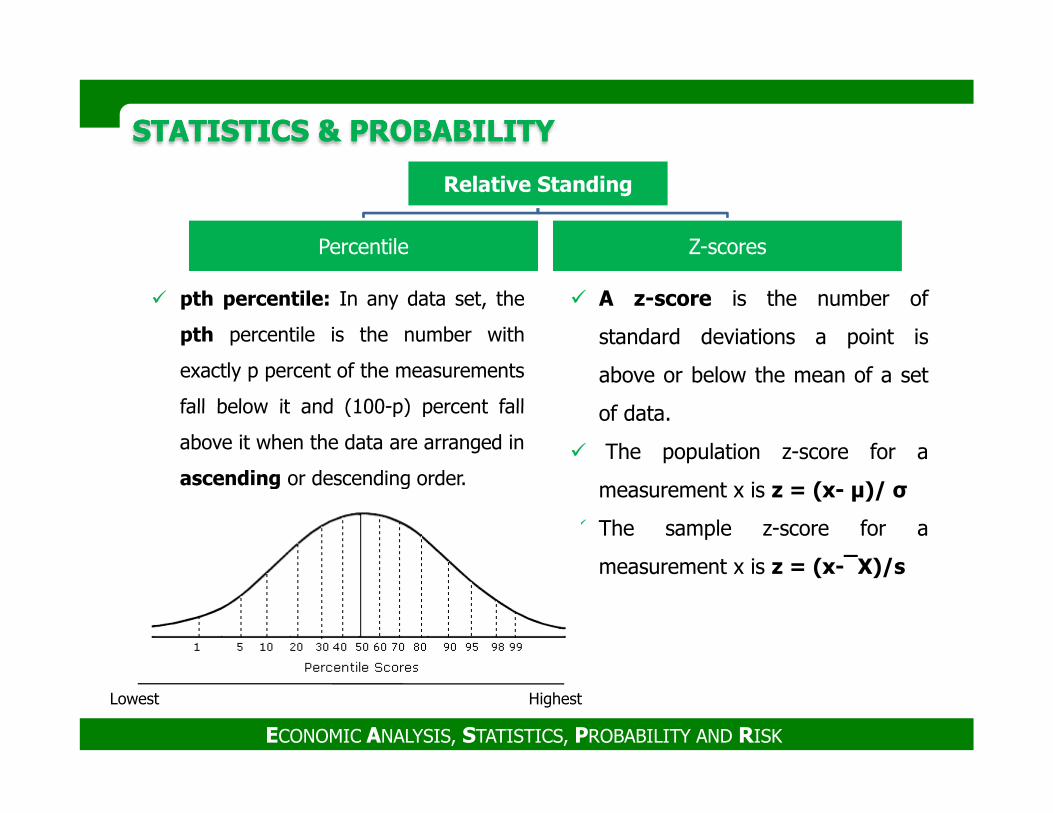

Relative Standing

Percentile Z-scores

� pth percentile: In any data set, the

pth percentile is the number with

exactly p percent of the measurements

fall below it and (100-p) percent fall

� A z-score is the number of

standard deviations a point is

above or below the mean of a set

of data.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

fall below it and (100-p) percent fall

above it when the data are arranged in

ascending or descending order.

of data.

� The population z-score for a

measurement x is z = (x- µ)/ σ

� The sample z-score for a

measurement x is z = (x-‾X)/s

Lowest Highest

Example

� The following observation training hours for every employee are selected from

the Jan. 20, 2003 “The 100 Best Companies to Work For” from Fortune

magazine, only the Top 50 company.

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

� Percentile of 50?????

� Number of observation less than/total number of observations X 100

� Percentile of observation 50 =32/50= 64% 50 under P64%

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

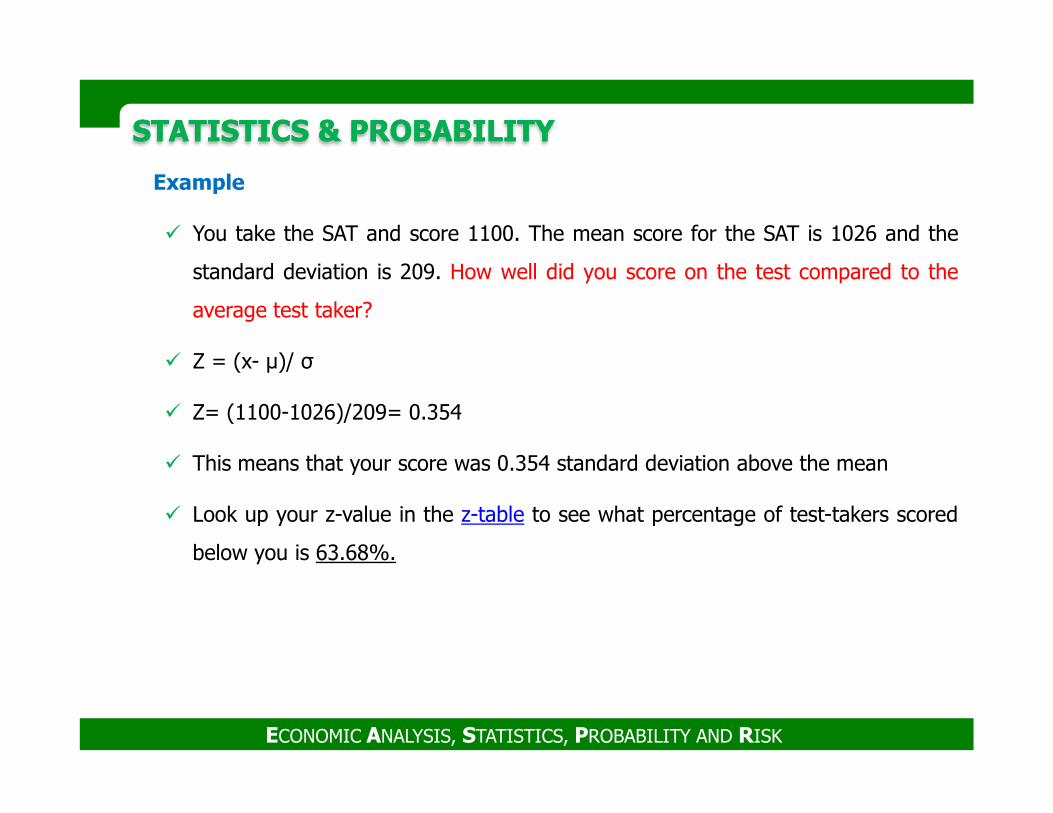

Example

� You take the SAT and score 1100. The mean score for the SAT is 1026 and the

standard deviation is 209. How well did you score on the test compared to the

average test taker?

� Z = (x- µ)/ σ

� Z= (1100-1026)/209= 0.354

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

� Z= (1100-1026)/209= 0.354

� This means that your score was 0.354 standard deviation above the mean

� Look up your z-value in the z-table to see what percentage of test-takers scored

below you is 63.68%.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

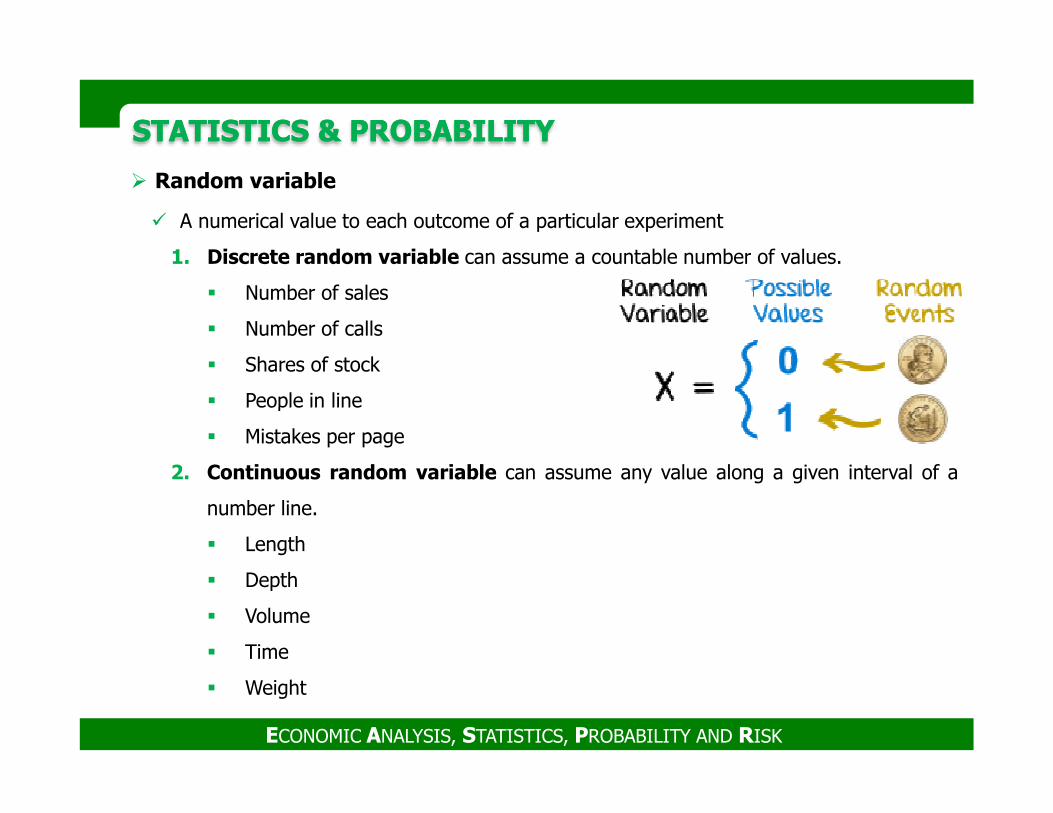

� Random variable

� A numerical value to each outcome of a particular experiment

1. Discrete random variable can assume a countable number of values.

� Number of sales

� Number of calls

� Shares of stock

� People in line

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� People in line

� Mistakes per page

2. Continuous random variable can assume any value along a given interval of a

number line.

� Length

� Depth

� Volume

� Time

� Weight

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

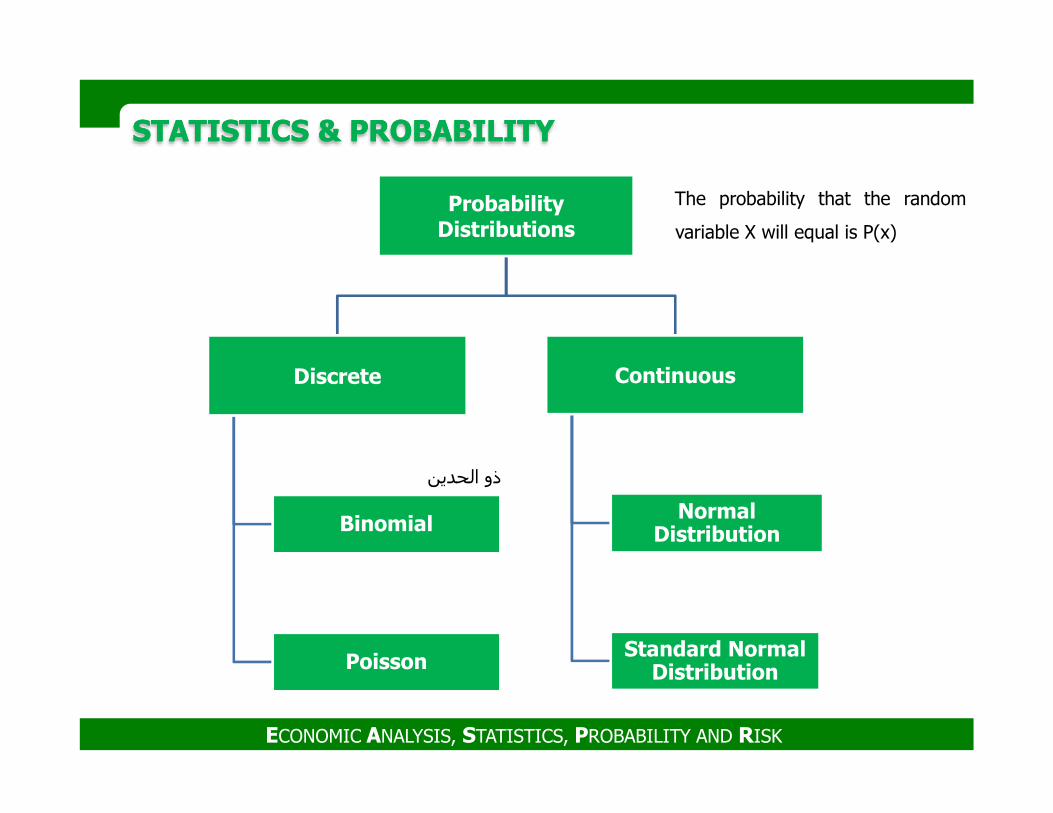

Probability Distributions

Discrete Continuous

The probability that the random

variable X will equal is P(x)

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Binomial

Poisson

Normal Distribution

Standard Normal Distribution

الحدين ذو

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

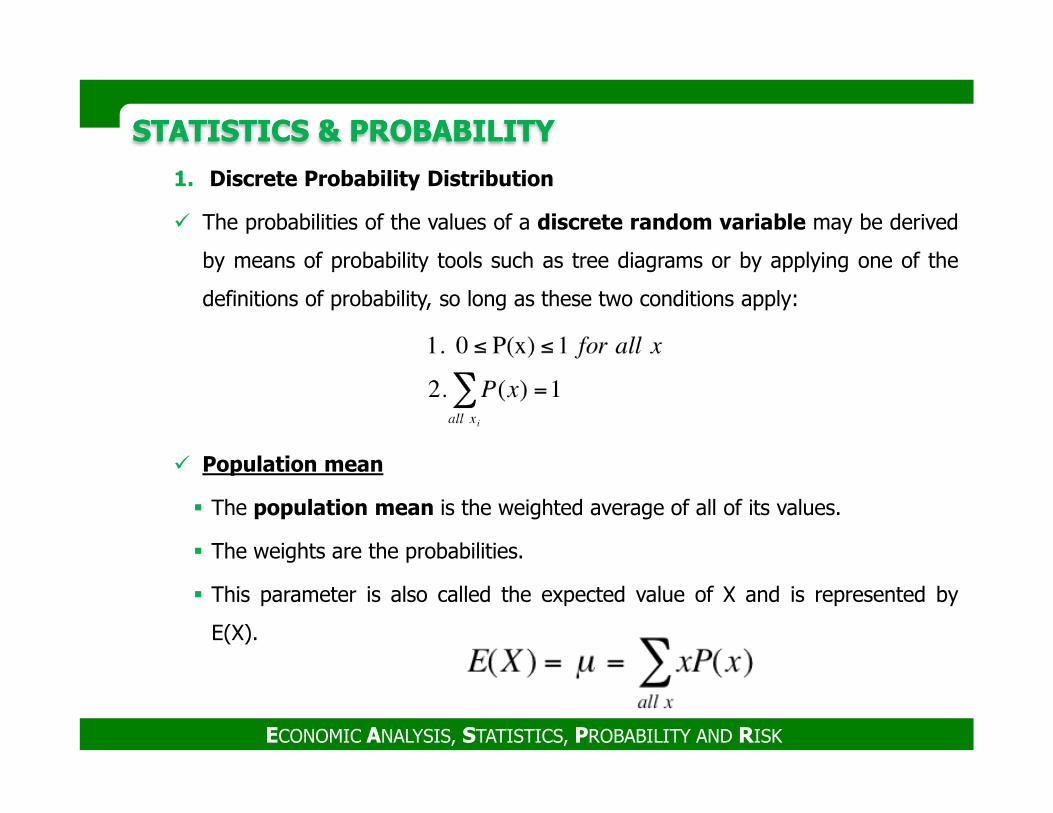

1. Discrete Probability Distribution

� The probabilities of the values of a discrete random variable may be derived

by means of probability tools such as tree diagrams or by applying one of the

definitions of probability, so long as these two conditions apply:

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Population mean

� The population mean is the weighted average of all of its values.

� The weights are the probabilities.

� This parameter is also called the expected value of X and is represented by

E(X).

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

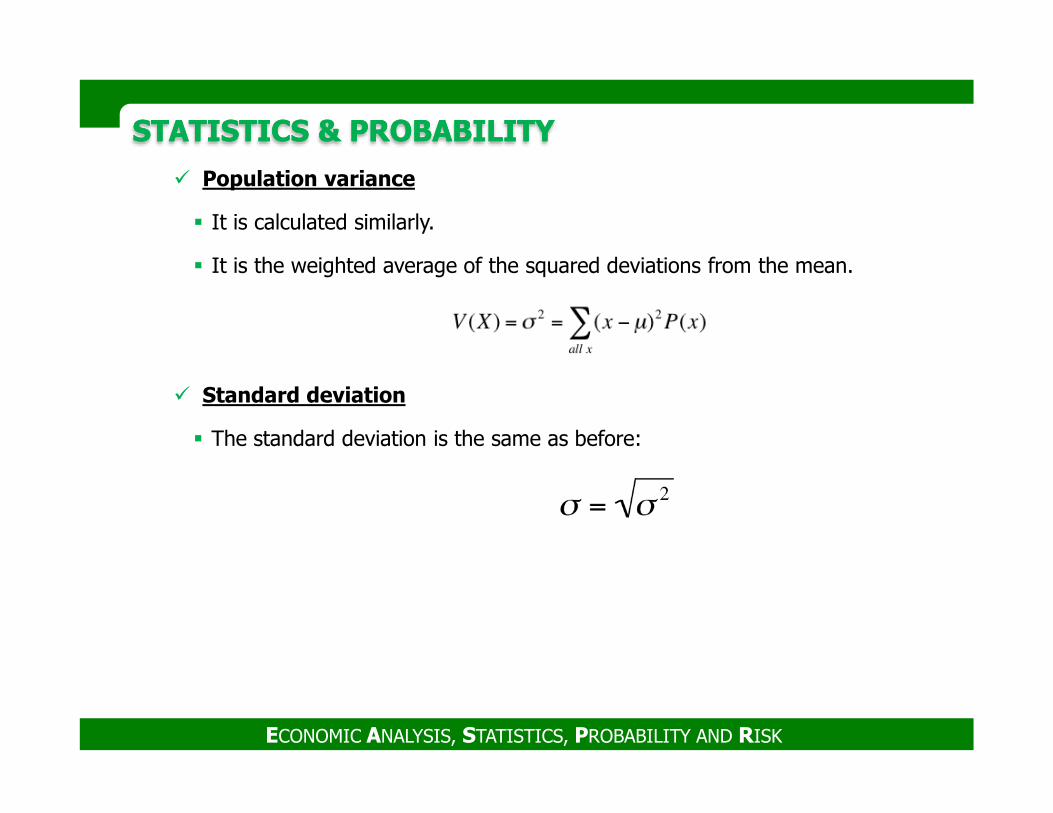

� Population variance

� It is calculated similarly.

� It is the weighted average of the squared deviations from the mean.

� Standard deviation

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� The standard deviation is the same as before:

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

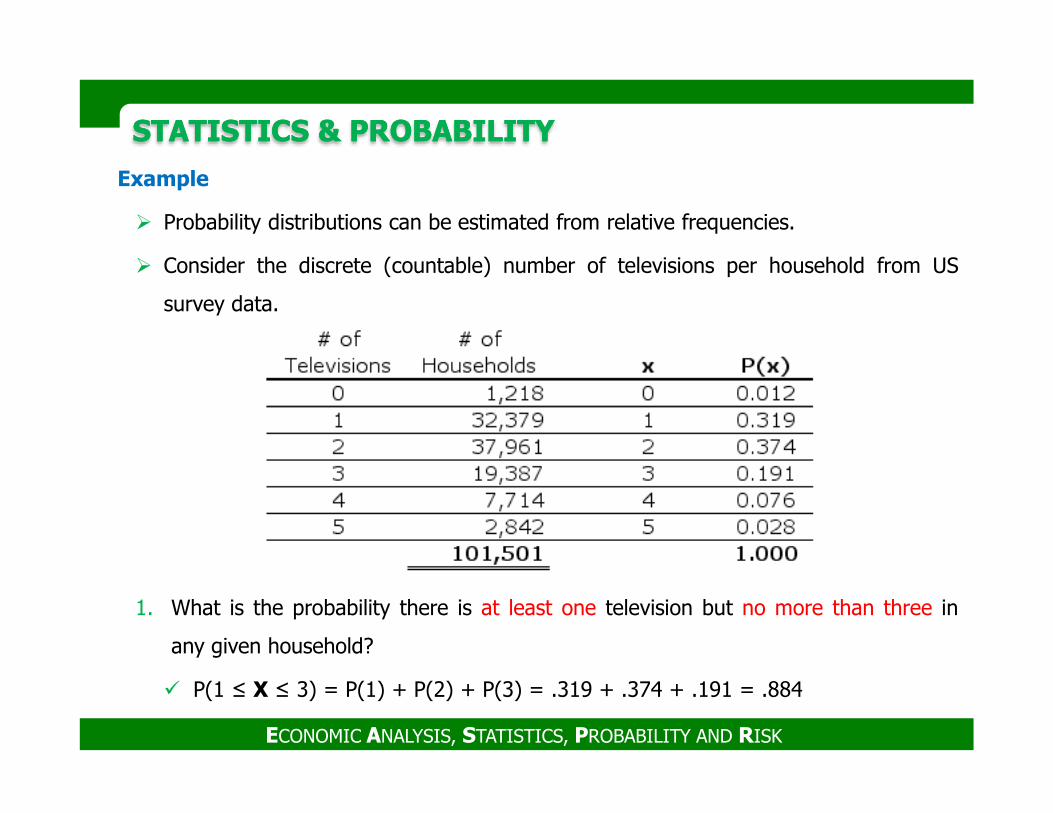

Example

� Probability distributions can be estimated from relative frequencies.

� Consider the discrete (countable) number of televisions per household from US

survey data.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

1. What is the probability there is at least one television but no more than three in

any given household?

� P(1 ≤ X ≤ 3) = P(1) + P(2) + P(3) = .319 + .374 + .191 = .884

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

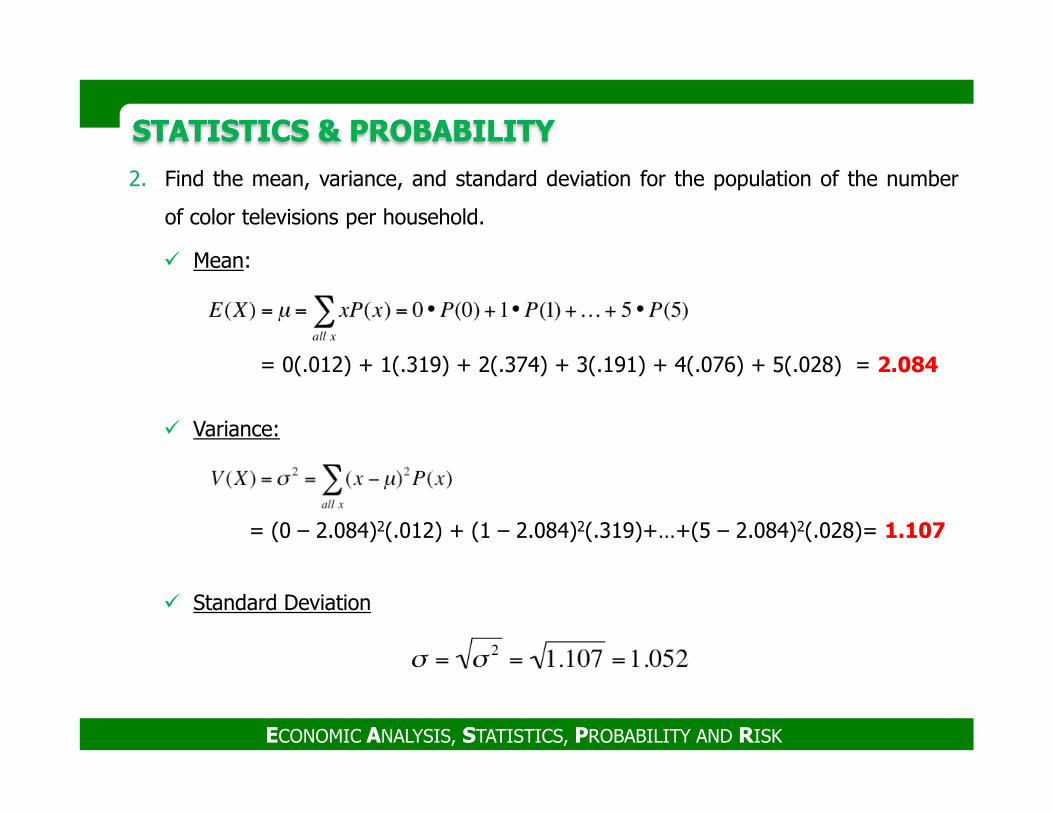

2. Find the mean, variance, and standard deviation for the population of the number

of color televisions per household.

� Mean:

= 0(.012) + 1(.319) + 2(.374) + 3(.191) + 4(.076) + 5(.028) = 2.084

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Variance:

� Standard Deviation

= (0 – 2.084)2(.012) + (1 – 2.084)2(.319)+…+(5 – 2.084)2(.028)= 1.107

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

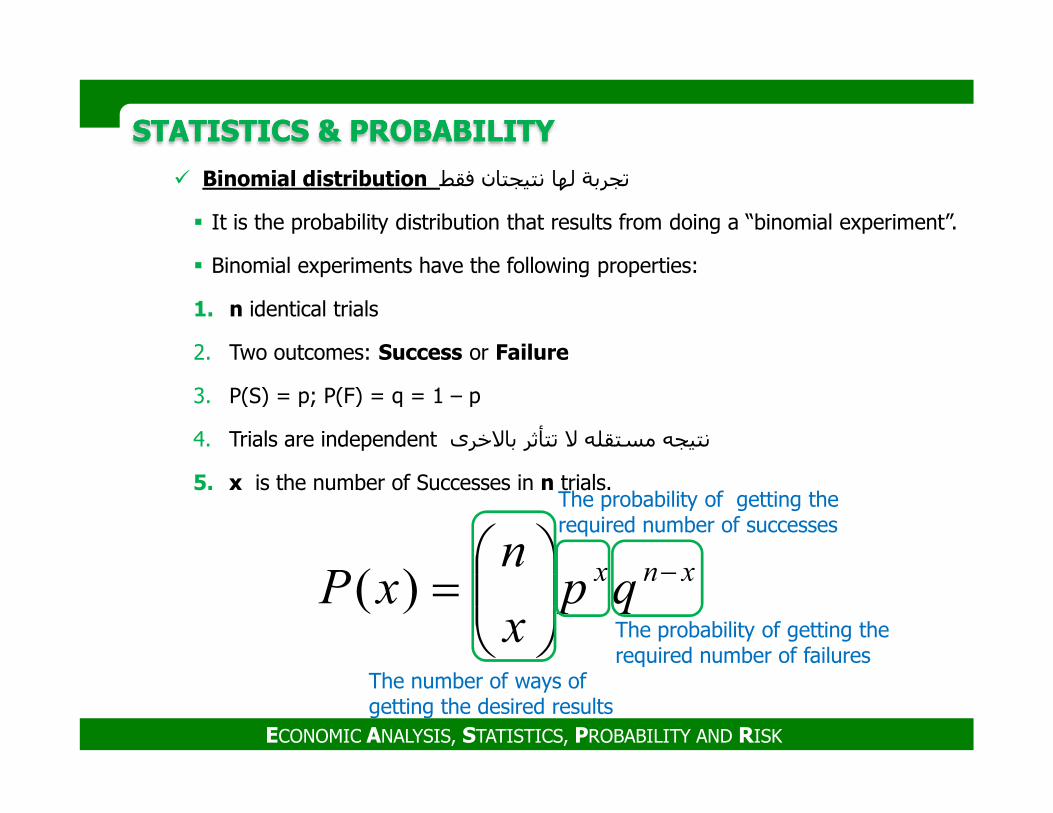

� Binomial distribution تجربة لھا نتيجتان فقط

� It is the probability distribution that results from doing a “binomial experiment”.

� Binomial experiments have the following properties:

1. n identical trials

2. Two outcomes: Success or Failure

3. P(S) = p; P(F) = q = 1 – p

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

3. P(S) = p; P(F) = q = 1 – p

4. Trials are independent باwخرى تتأثر w مستقله نتيجه

5. x is the number of Successes in n trials.

xnxqp

x

nxP

−

=)(

The number of ways of getting the desired results

The probability of getting the required number of successes

The probability of getting the required number of failures

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

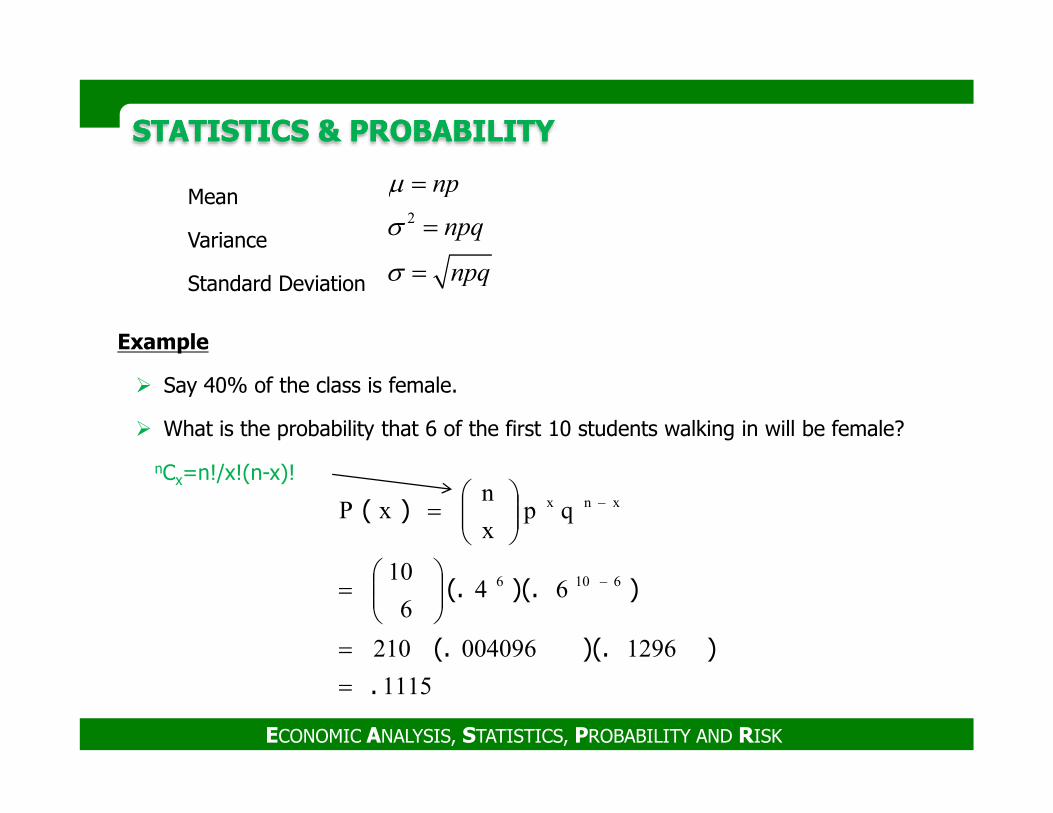

Example

� Say 40% of the class is female.

Mean

Variance

Standard Deviation

2

np

npq

npq

µ

σ

σ

=

=

=

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� What is the probability that 6 of the first 10 students walking in will be female?

1115

1296004096210

646

10

qpx

nxP

6106

xnx

.

))(.(.

))(.(.

)(

=

=

=

=

−

−

nCx=n!/x!(n-x)!

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

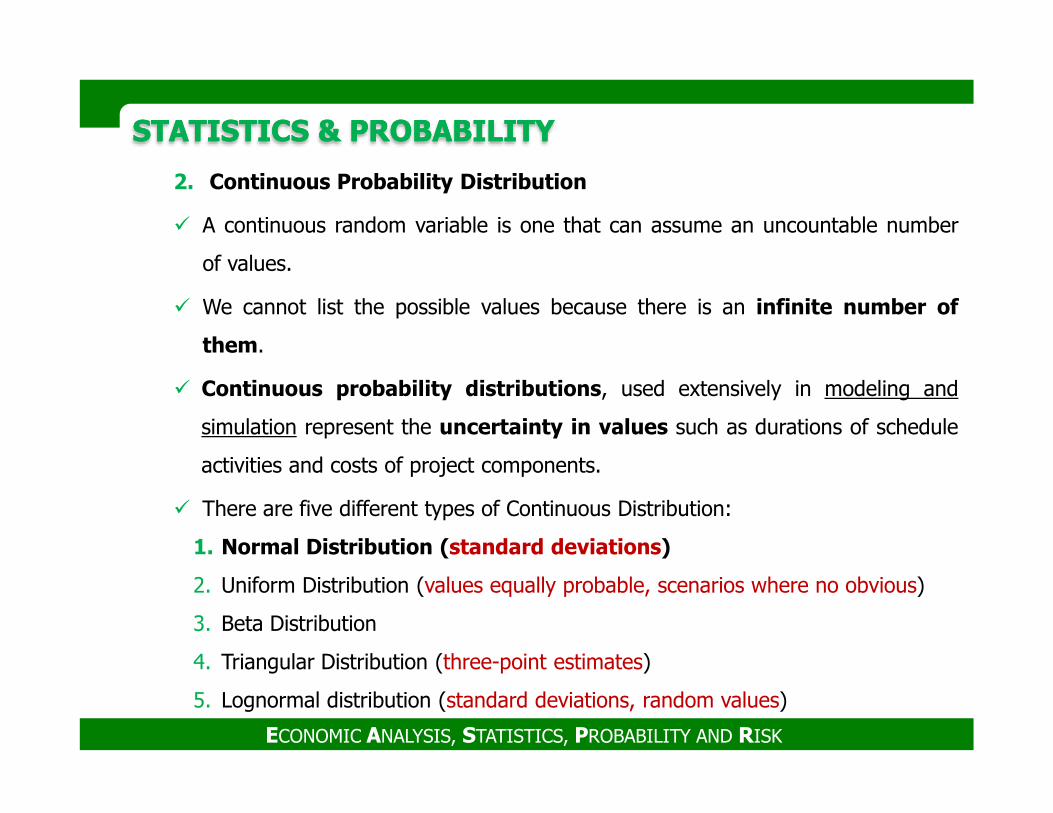

2. Continuous Probability Distribution

� A continuous random variable is one that can assume an uncountable number

of values.

� We cannot list the possible values because there is an infinite number of

them.

� Continuous probability distributions, used extensively in modeling and

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

simulation represent the uncertainty in values such as durations of schedule

activities and costs of project components.

� There are five different types of Continuous Distribution:

1. Normal Distribution (standard deviations)

2. Uniform Distribution (values equally probable, scenarios where no obvious)

3. Beta Distribution

4. Triangular Distribution (three-point estimates)

5. Lognormal distribution (standard deviations, random values)

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

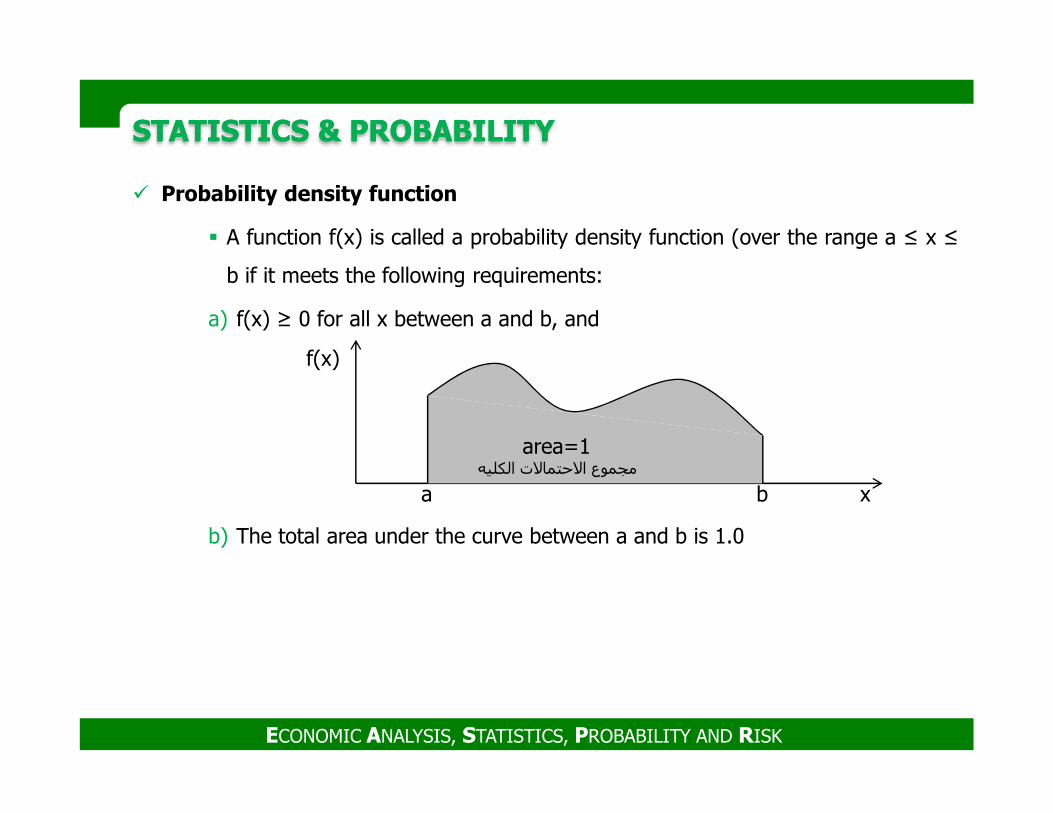

� Probability density function

� A function f(x) is called a probability density function (over the range a ≤ x ≤

b if it meets the following requirements:

a) f(x) ≥ 0 for all x between a and b, and

f(x)

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

b) The total area under the curve between a and b is 1.0

xba

area=1مجموع اwحتماwت الكليه

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

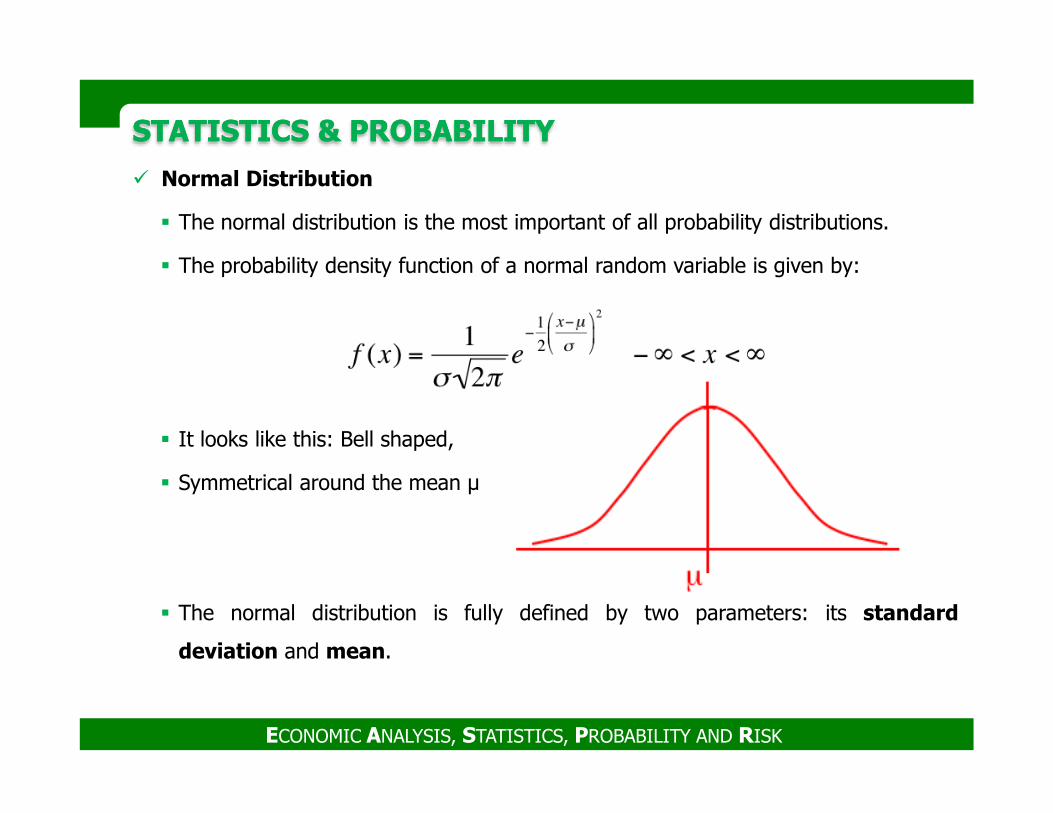

� Normal Distribution

� The normal distribution is the most important of all probability distributions.

� The probability density function of a normal random variable is given by:

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� It looks like this: Bell shaped,

� Symmetrical around the mean µ

� The normal distribution is fully defined by two parameters: its standard

deviation and mean.

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

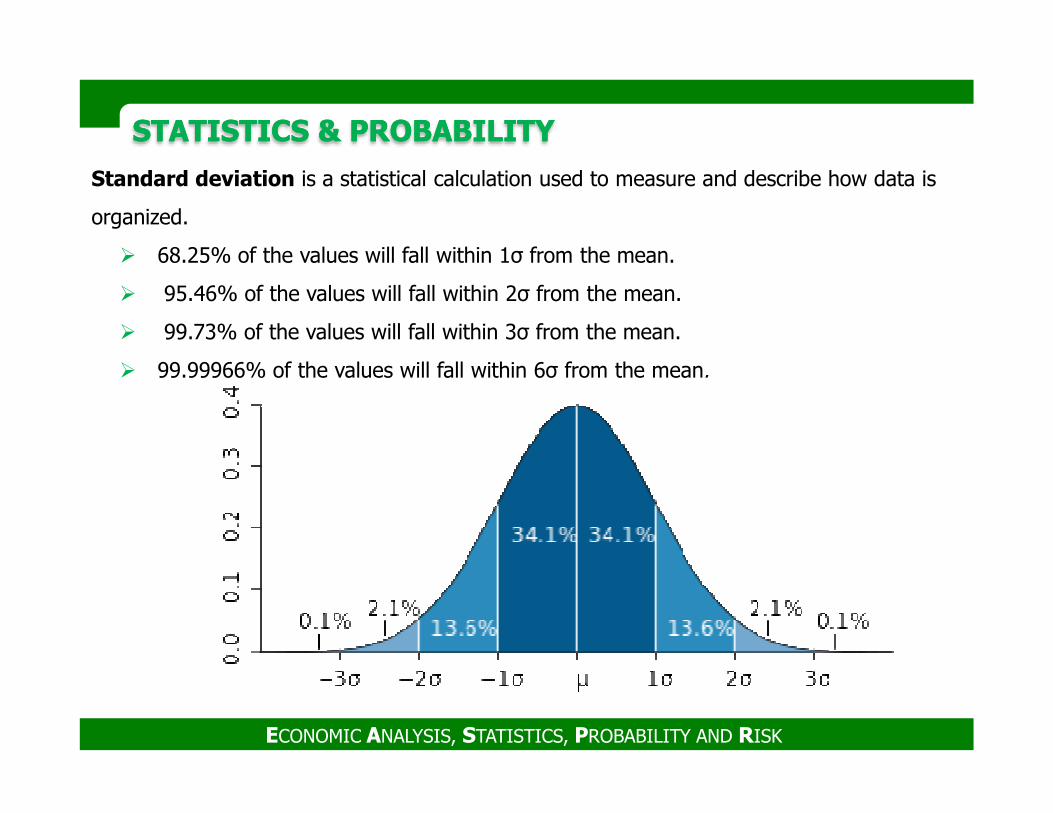

Standard deviation is a statistical calculation used to measure and describe how data is

organized.

� 68.25% of the values will fall within 1σ from the mean.

� 95.46% of the values will fall within 2σ from the mean.

� 99.73% of the values will fall within 3σ from the mean.

� 99.99966% of the values will fall within 6σ from the mean.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

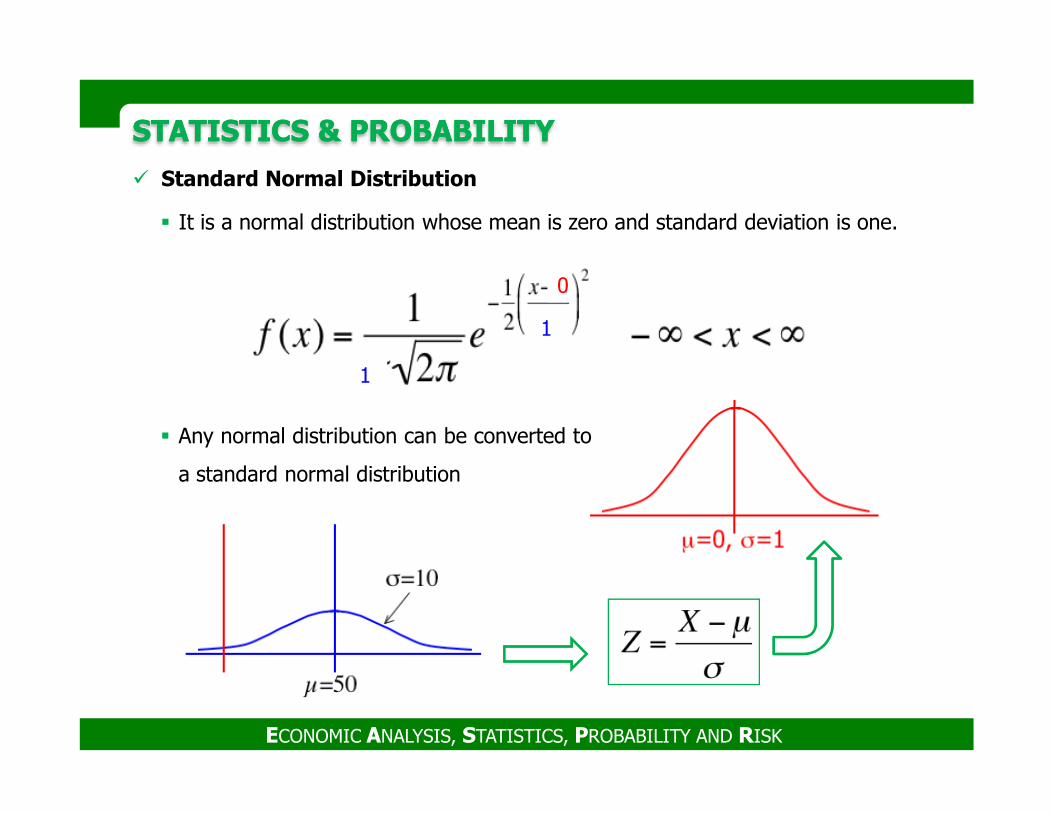

� Standard Normal Distribution

� It is a normal distribution whose mean is zero and standard deviation is one.

0

1

1

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Any normal distribution can be converted to

a standard normal distribution

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

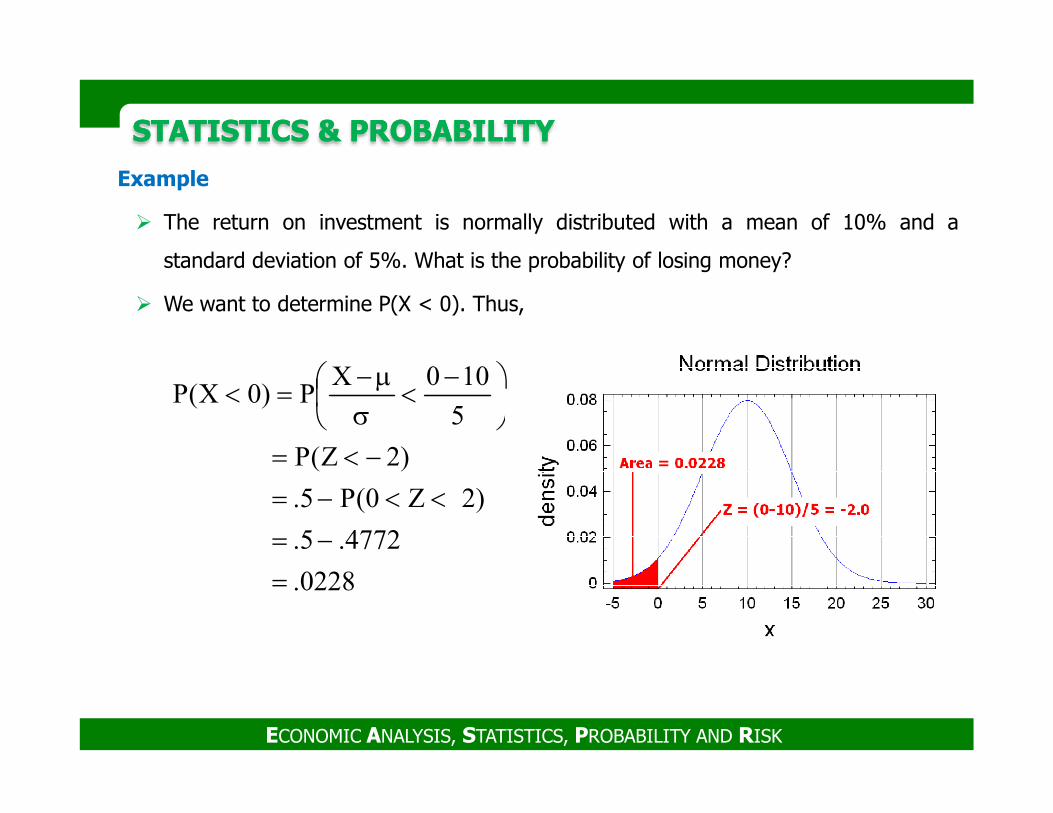

Example

� The return on investment is normally distributed with a mean of 10% and a

standard deviation of 5%. What is the probability of losing money?

� We want to determine P(X < 0). Thus,

5

100XP)0X(P

−<

σµ−

=<

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

0228.

4772.5.

)2Z0(P5.

)2Z(P

5P)0X(P

=

−=

<<−=

−<=

<σ

=<

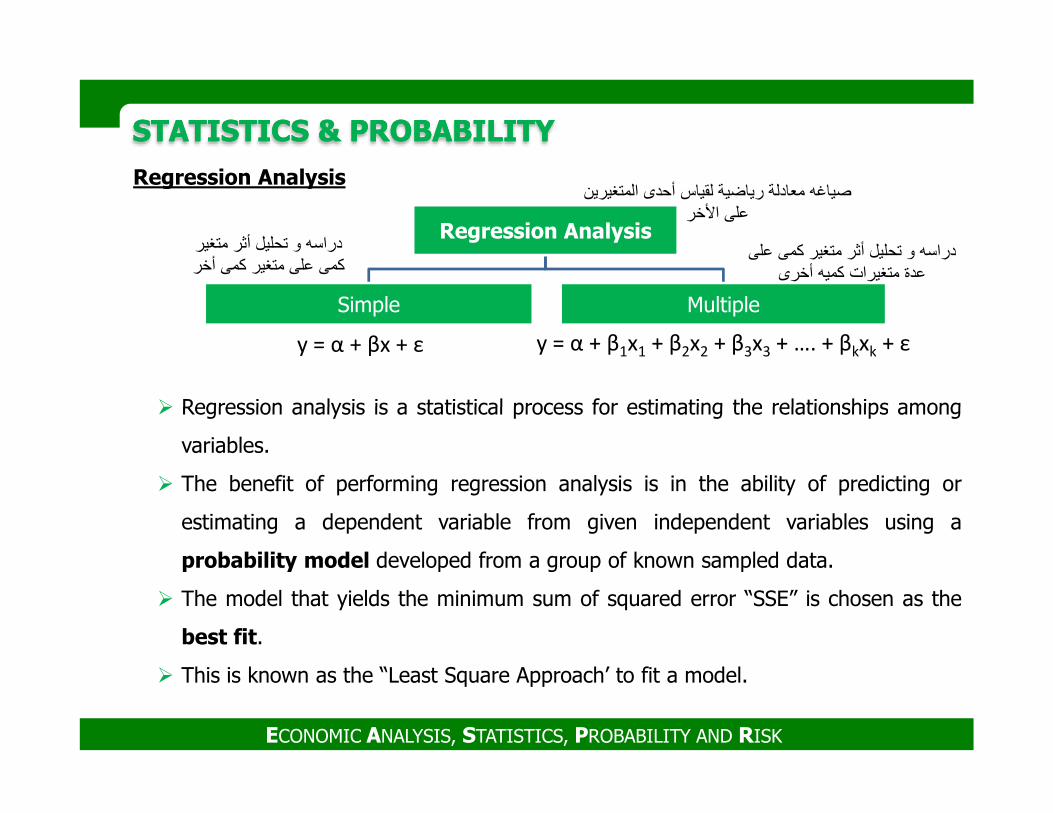

Regression Analysis

� Regression analysis is a statistical process for estimating the relationships among

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

Regression Analysis

Simple Multiple

دراسه و تحليل أثر متغير كمى على متغير كمى أخر

صياغه معادلة رياضية لقياس أحدى المتغيرين على ا خر

دراسه و تحليل أثر متغير كمى على عدة متغيرات كميه أخرى

y = α + β1x1 + β2x2 + β3x3 + …. + βkxk + εy = α + βx + ε

� Regression analysis is a statistical process for estimating the relationships among

variables.

� The benefit of performing regression analysis is in the ability of predicting or

estimating a dependent variable from given independent variables using a

probability model developed from a group of known sampled data.

� The model that yields the minimum sum of squared error “SSE” is chosen as the

best fit.

� This is known as the “Least Square Approach’ to fit a model.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

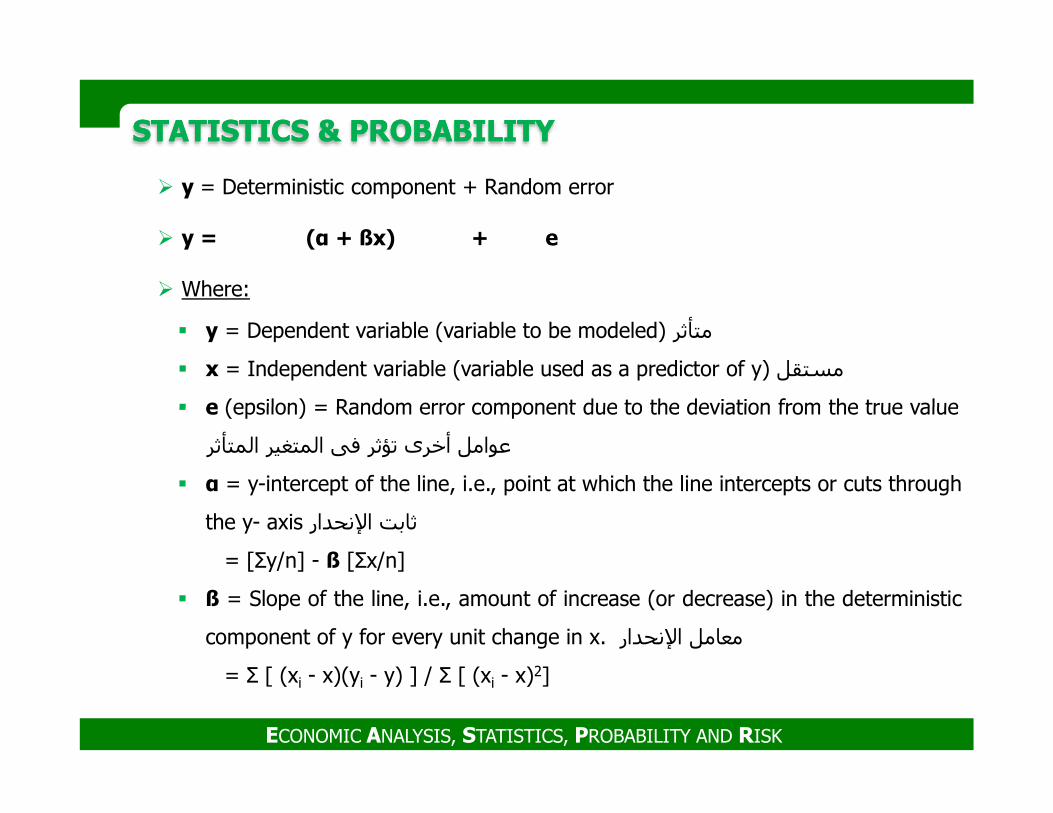

� y = Deterministic component + Random error

� y = (α + ßx) + e

� Where:

� y = Dependent variable (variable to be modeled) متأثر

� x = Independent variable (variable used as a predictor of y) مستقل

� e (epsilon) = Random error component due to the deviation from the true value

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

� e (epsilon) = Random error component due to the deviation from the true value

المتأثر المتغير فى تؤثر أخرى عوامل

� α = y-intercept of the line, i.e., point at which the line intercepts or cuts through

the y- axis ا�نحدار ثابت

= [Σy/n] - ß [Σx/n]

� ß = Slope of the line, i.e., amount of increase (or decrease) in the deterministic

component of y for every unit change in x. ا�نحدار معامل

= Σ [ (xi - x)(yi - y) ] / Σ [ (xi - x)2]

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

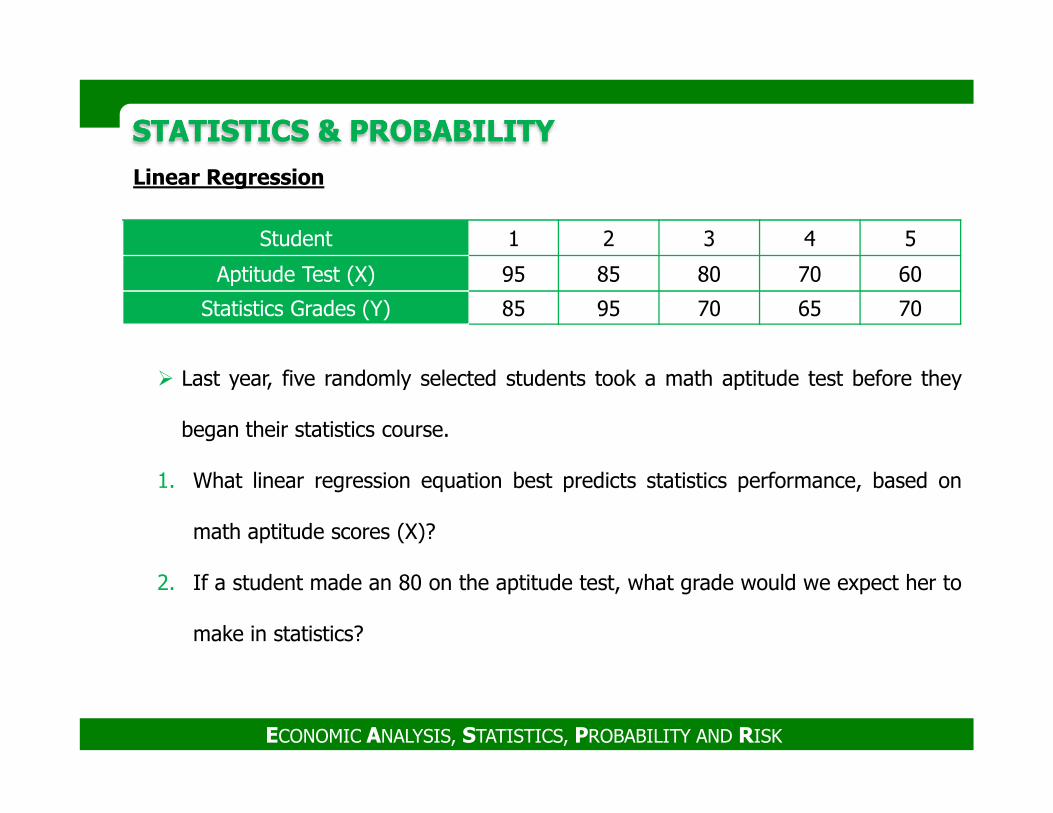

Linear Regression

� Last year, five randomly selected students took a math aptitude test before they

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

Student 1 2 3 4 5

Aptitude Test (X) 95 85 80 70 60

Statistics Grades (Y) 85 95 70 65 70

began their statistics course.

1. What linear regression equation best predicts statistics performance, based on

math aptitude scores (X)?

2. If a student made an 80 on the aptitude test, what grade would we expect her to

make in statistics?

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

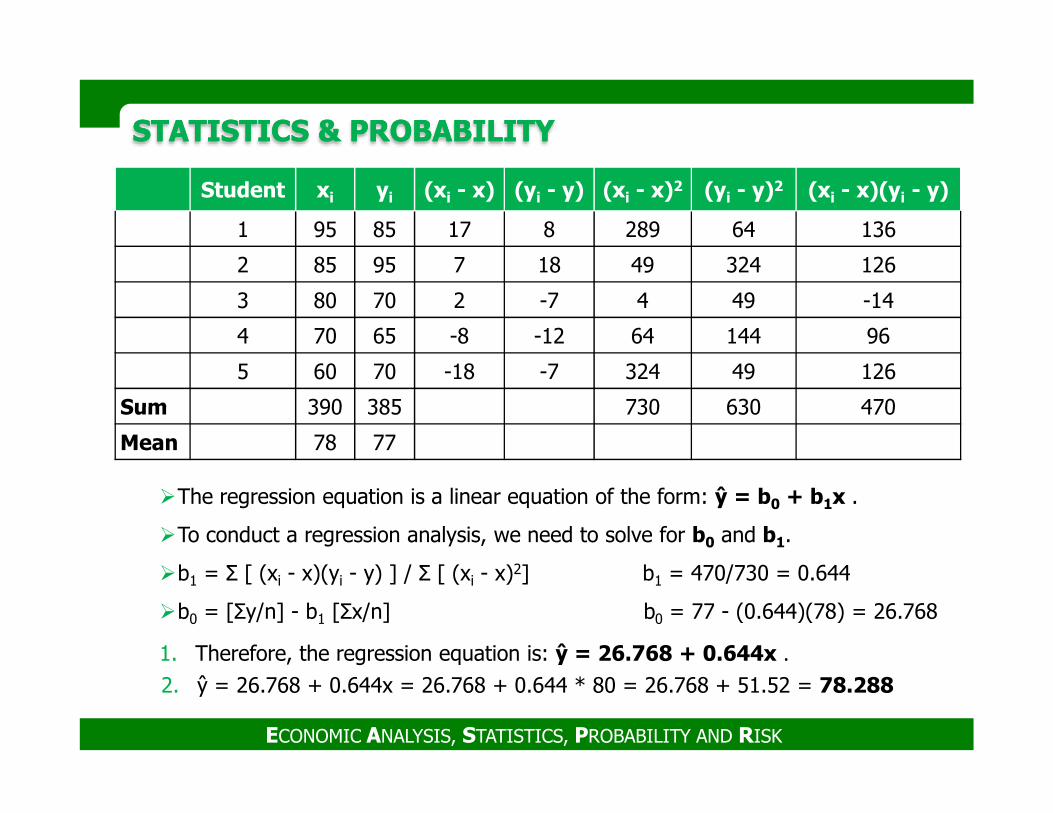

Student xi yi (xi - x) (yi - y) (xi - x)2 (yi - y)2 (xi - x)(yi - y)

1 95 85 17 8 289 64 136

2 85 95 7 18 49 324 126

3 80 70 2 -7 4 49 -14

4 70 65 -8 -12 64 144 96

5 60 70 -18 -7 324 49 126

Sum 390 385 730 630 470

�The regression equation is a linear equation of the form: ŷ = b0 + b1x .

�To conduct a regression analysis, we need to solve for b0 and b1.

�b1 = Σ [ (xi - x)(yi - y) ] / Σ [ (xi - x)2] b1 = 470/730 = 0.644

�b0 = [Σy/n] - b1 [Σx/n] b0 = 77 - (0.644)(78) = 26.768

1. Therefore, the regression equation is: ŷ = 26.768 + 0.644x .

2. ŷ = 26.768 + 0.644x = 26.768 + 0.644 * 80 = 26.768 + 51.52 = 78.288

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Sum 390 385 730 630 470

Mean 78 77

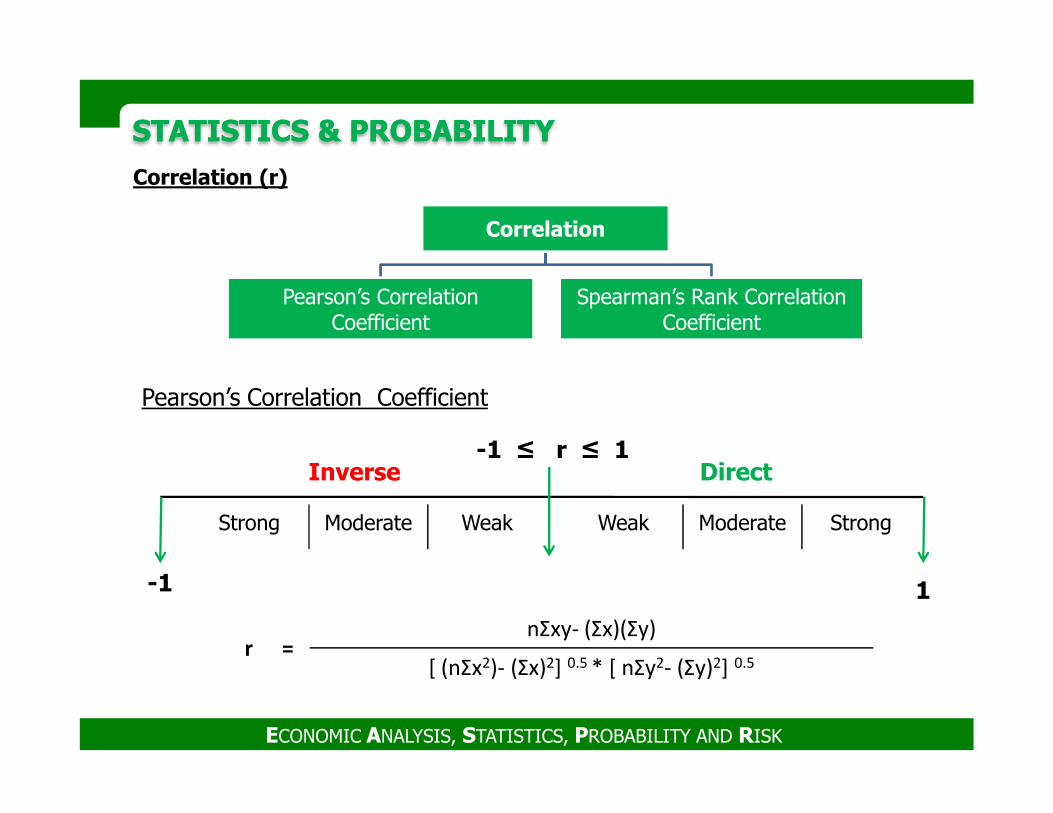

Correlation (r)

STATISTICS & PROBABILITY STATISTICS & PROBABILITY

Correlation

Pearson’s Correlation Coefficient

Spearman’s Rank Correlation Coefficient

Pearson’s Correlation Coefficient

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Strong Moderate Weak Weak Moderate Strong

-1 ≤ r ≤ 1

-1 1

DirectInverse

Pearson’s Correlation Coefficient

r =

nΣxy- (Σx)(Σy)

[ (nΣx2)- (Σx)2] 0.5 * [ nΣy2- (Σy)2] 0.5

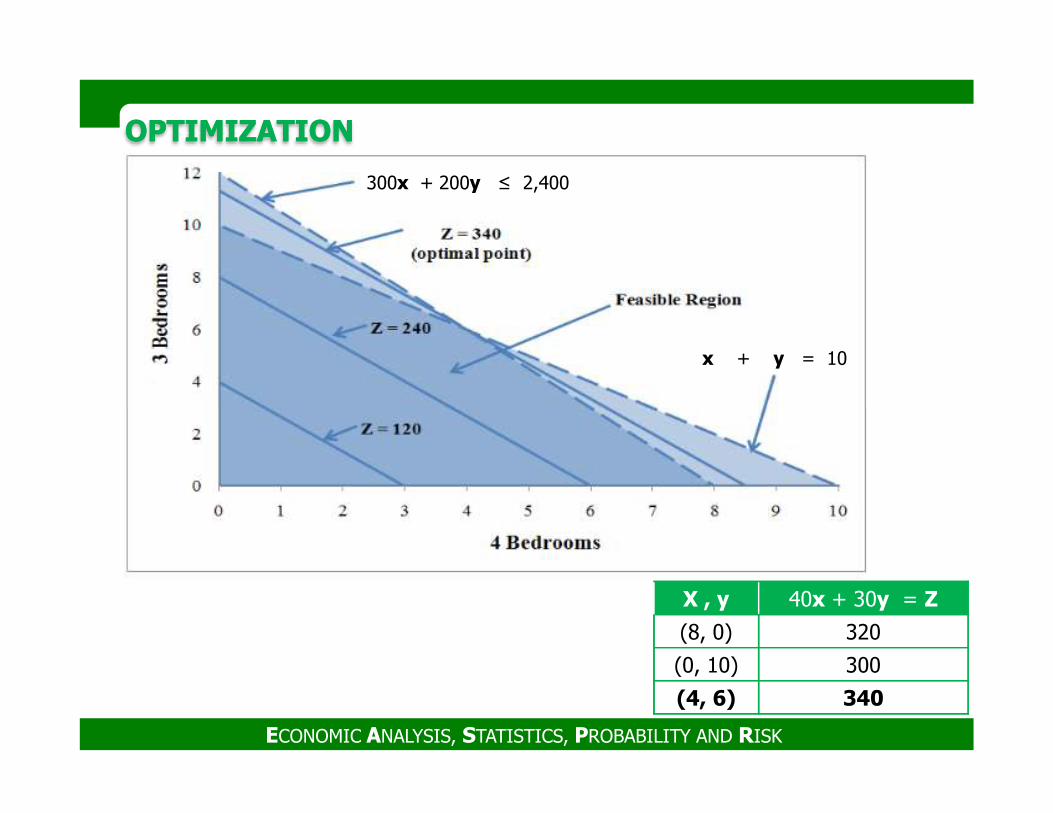

OPTIMIZATION OPTIMIZATION

� Optimization is the process of determining the BEST performance for a system.

� Models are simplified representations of reality by simple or complex systems

used to optimize the performance of the real system.

� There are numerous techniques for optimization such as;

1. Linear Programming

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

2. Monte Carlo Simulation

3. Sensitivity Analysis

OPTIMIZATION OPTIMIZATION

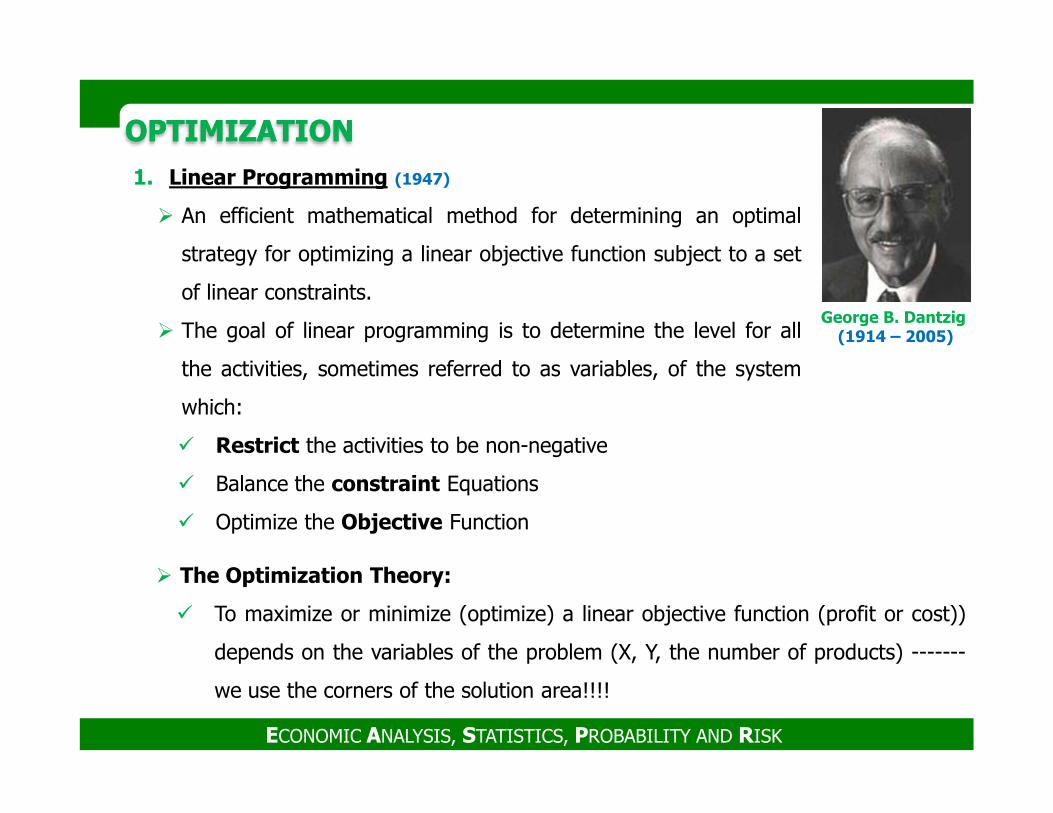

1. Linear Programming (1947)

� An efficient mathematical method for determining an optimal

strategy for optimizing a linear objective function subject to a set

of linear constraints.

� The goal of linear programming is to determine the level for all

the activities, sometimes referred to as variables, of the system

which:

George B. Dantzig(1914 – 2005)

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

which:

� Restrict the activities to be non-negative

� Balance the constraint Equations

� Optimize the Objective Function

� The Optimization Theory:

� To maximize or minimize (optimize) a linear objective function (profit or cost))

depends on the variables of the problem (X, Y, the number of products) -------

we use the corners of the solution area!!!!

OPTIMIZATION OPTIMIZATION

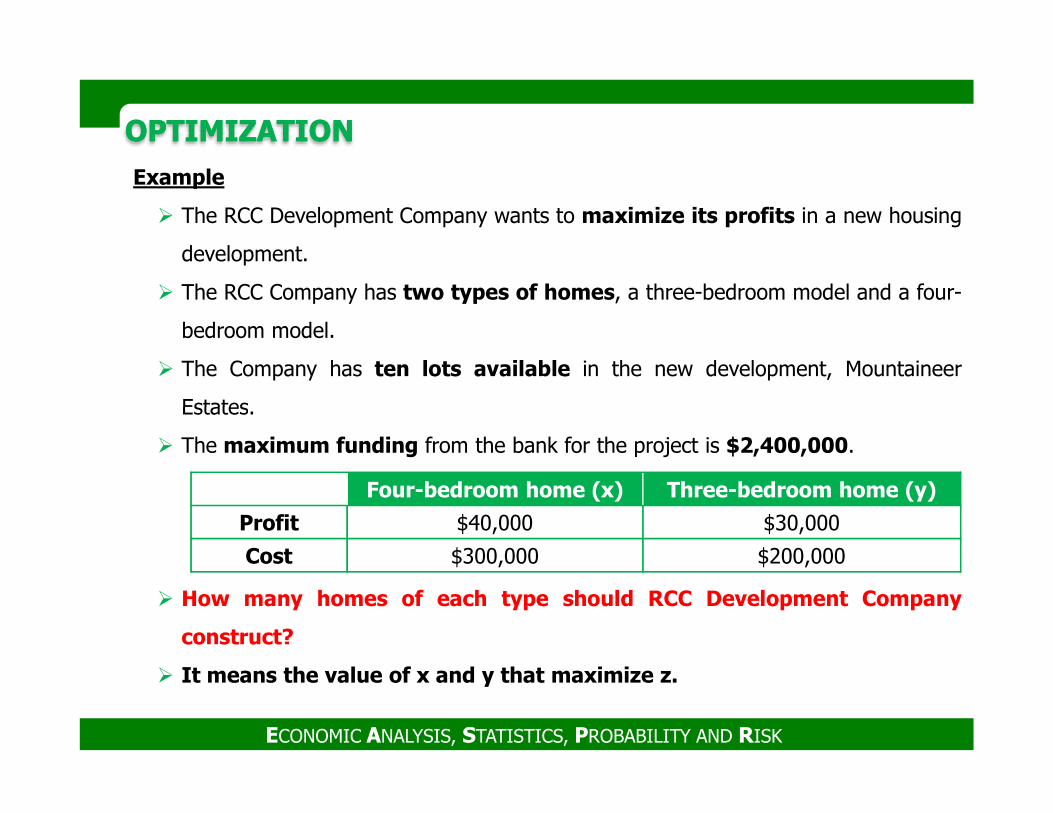

Example

� The RCC Development Company wants to maximize its profits in a new housing

development.

� The RCC Company has two types of homes, a three-bedroom model and a four-

bedroom model.

� The Company has ten lots available in the new development, Mountaineer

Estates.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Estates.

� The maximum funding from the bank for the project is $2,400,000.

� How many homes of each type should RCC Development Company

construct?

� It means the value of x and y that maximize z.

Four-bedroom home (x) Three-bedroom home (y)

Profit $40,000 $30,000

Cost $300,000 $200,000

OPTIMIZATION OPTIMIZATION

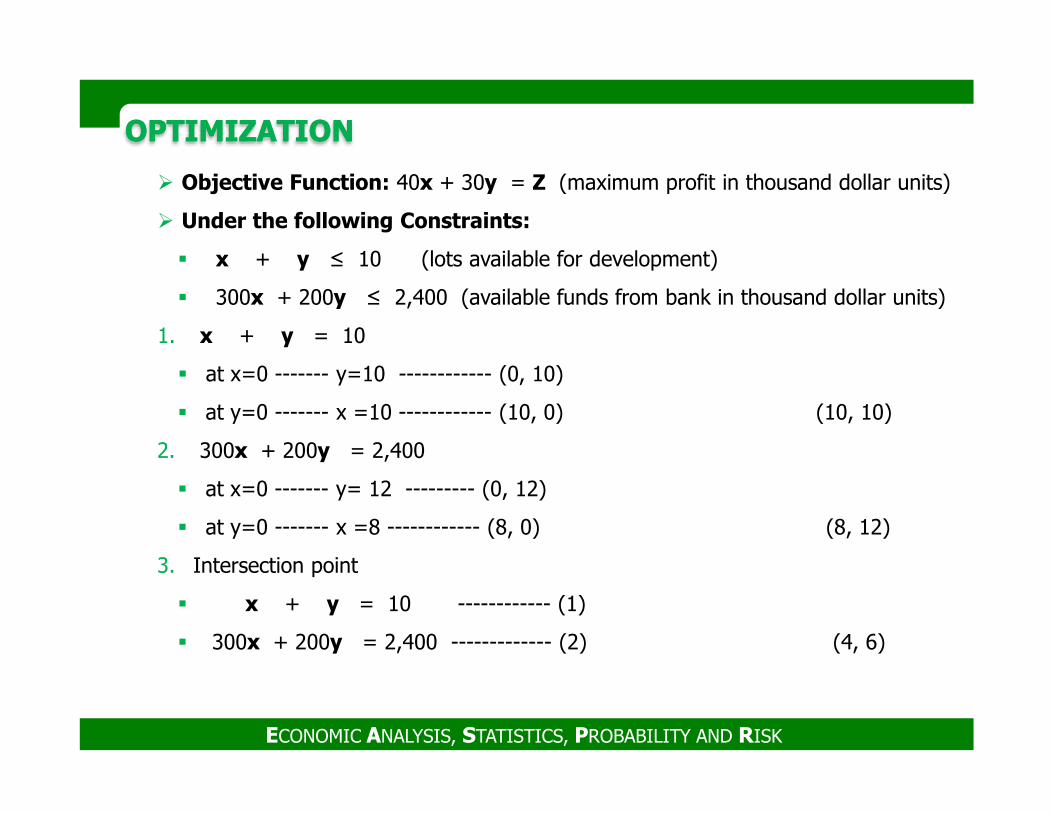

� Objective Function: 40x + 30y = Z (maximum profit in thousand dollar units)

� Under the following Constraints:

� x + y ≤ 10 (lots available for development)

� 300x + 200y ≤ 2,400 (available funds from bank in thousand dollar units)

1. x + y = 10

� at x=0 ------- y=10 ------------ (0, 10)

� at y=0 ------- x =10 ------------ (10, 0) (10, 10)

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� at y=0 ------- x =10 ------------ (10, 0) (10, 10)

2. 300x + 200y = 2,400

� at x=0 ------- y= 12 --------- (0, 12)

� at y=0 ------- x =8 ------------ (8, 0) (8, 12)

3. Intersection point

� x + y = 10 ------------ (1)

� 300x + 200y = 2,400 ------------- (2) (4, 6)

OPTIMIZATION OPTIMIZATION

300x + 200y ≤ 2,400

x + y = 10

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

X , y 40x + 30y = Z

(8, 0) 320

(0, 10) 300

(4, 6) 340

OPTIMIZATION OPTIMIZATION

2. Monte Carlo Simulation (1949)

� It uses the generation of a series of random numbers to simulate

a population followed by statistical analysis to make predictions.

� Useful in studying complex systems with significant uncertainty

in the inputs, such as in estimating costs.

� It is used in investment analysis to evaluate the risk in making investments.

� There are numerous commercial computer software programs available to perform

Stanisław M. Ulam(1909 - 1984)

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� There are numerous commercial computer software programs available to perform

Monte Carlo Simulations such Crystal Ball, @Risk, Risk Solver, Arena, and

GoldSim.

OPTIMIZATION OPTIMIZATION

3. Sensitivity Analysis

� A technique used to quantify the variation in the solution with respect to the

variables and the constants used in the formulation of the problem.

� Sensitivity analysis is done to investigate the impact of changes in variables and

assumptions made for constants used upon the solution obtained, often referred

to as the base case.

� The purpose is to determine which variables and constants have the most

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� The purpose is to determine which variables and constants have the most

influence upon the solution.

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS

Risk

� AACE Recommended Practice 10S-90

1. The possibility of suffering harm or loss (American Heritage Dictionary,

Houghton Mifflin Co.)

2. Uncertainty of an event which if occurred would result in a negative

or positive effect on the project (Project Management Institute).

� AACE Recommended Practice 10S-90, Cost Engineering Terminology, 2009

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� AACE Recommended Practice 10S-90, Cost Engineering Terminology, 2009

1. An ambiguous term that can mean any of the following:

� All uncertainty (threats + opportunities)

� Undesirable outcomes (uncertainty = risks + opportunities)

� The net impact or effect of uncertainty (threats – opportunities).

2. Probability of an undesirable outcome.

3. In total cost management, an uncertain event or condition that could

affect a project objective or business goal.

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS

Risk Management (TCM 7.6.1 Description)

�Risk management is the process of identifying risk factors (risk assessment),

analyzing and quantifying the properties of those factors (risk analysis), treating

the impact of the factors on planned asset or project performance and developing a

risk management plan (risk treatment), and implementing the risk management

plan (risk control).

�The goal of risk management is to increase the probability that a planned asset or

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

�The goal of risk management is to increase the probability that a planned asset or

project outcome will occur without decreasing the value of the asset or project.

�Risk management presumes that deviations from plans may result in unintended

results (positive or negative) that should be identified and managed.

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS

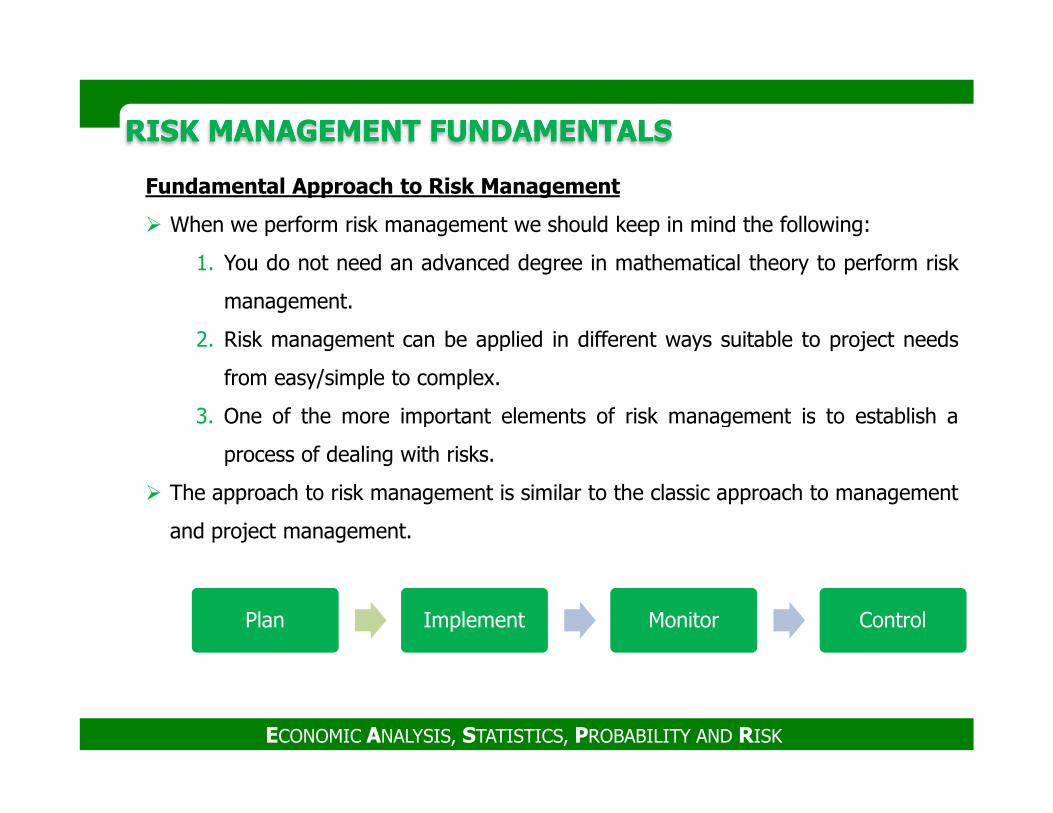

Fundamental Approach to Risk Management

� When we perform risk management we should keep in mind the following:

1. You do not need an advanced degree in mathematical theory to perform risk

management.

2. Risk management can be applied in different ways suitable to project needs

from easy/simple to complex.

3. One of the more important elements of risk management is to establish a

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

3. One of the more important elements of risk management is to establish a

process of dealing with risks.

� The approach to risk management is similar to the classic approach to management

and project management.

Plan Implement Monitor Control

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS

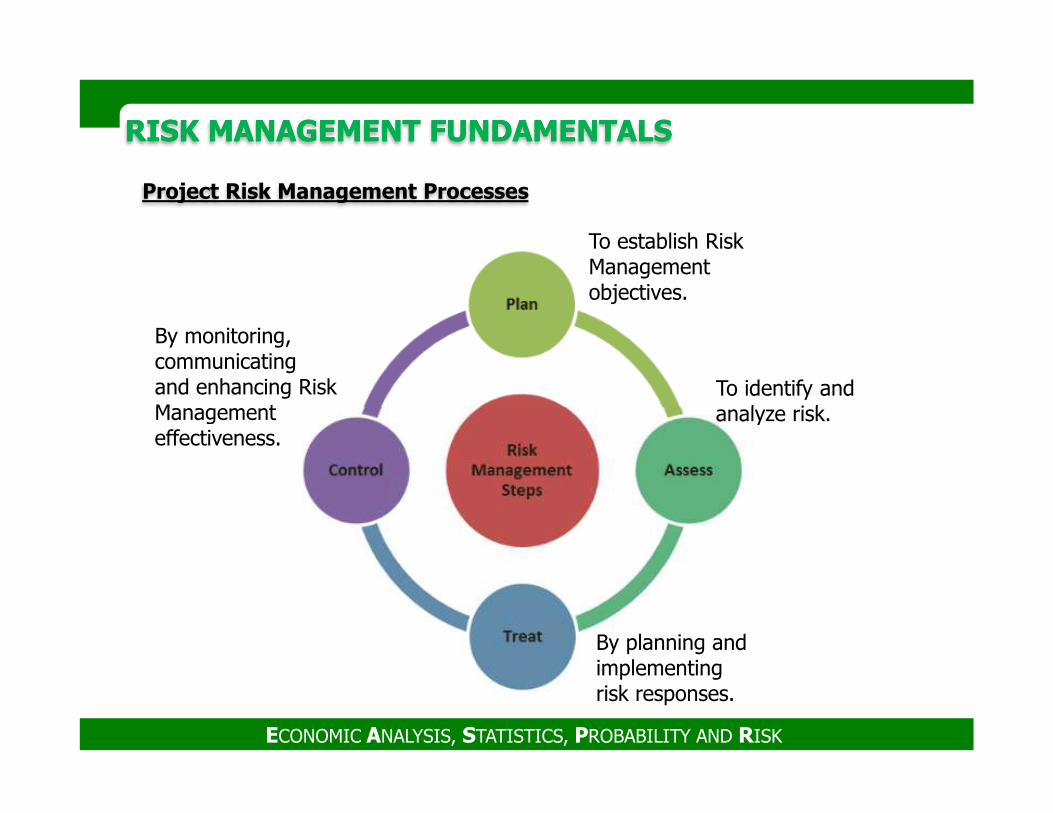

Project Risk Management Processes

To establish Risk Management objectives.

By monitoring, communicating and enhancing Risk Management

To identify and analyze risk.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Management effectiveness.

analyze risk.

By planning and implementing risk responses.

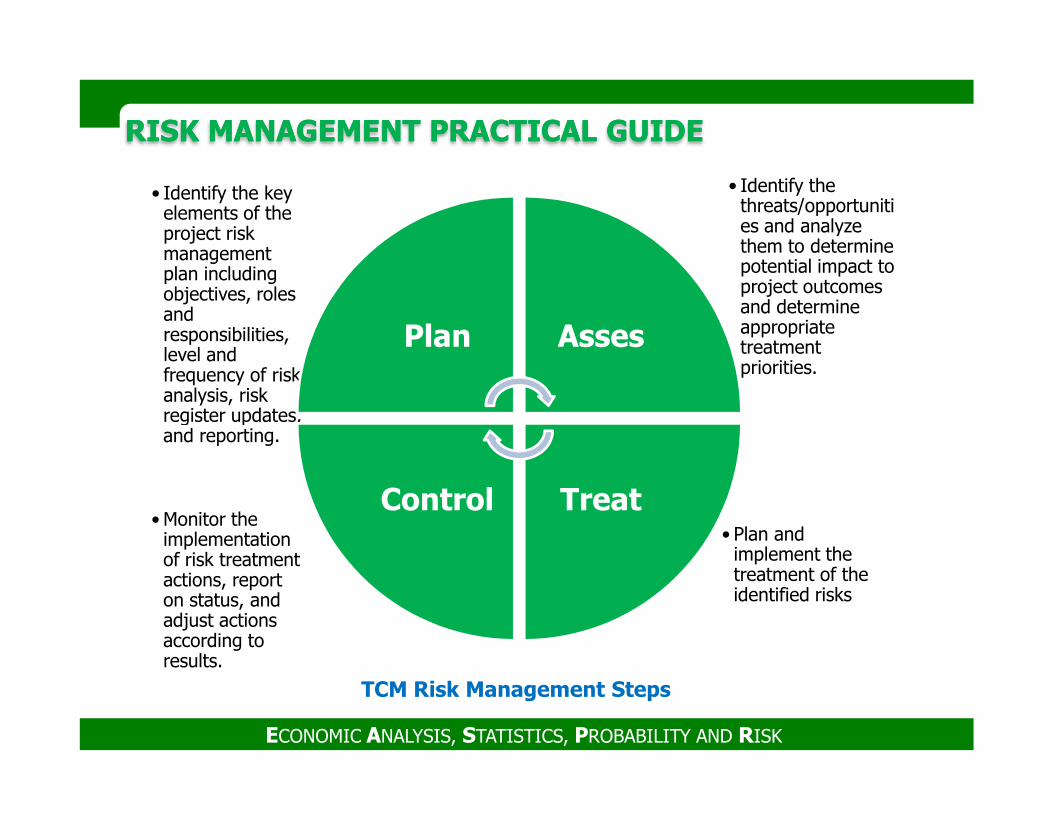

RISK MANAGEMENT PRACTICAL GUIDERISK MANAGEMENT PRACTICAL GUIDE

• Identify the threats/opportunities and analyze them to determine potential impact to project outcomes and determine appropriate treatment priorities.

• Identify the key elements of the project risk management plan including objectives, roles and responsibilities, level and frequency of risk analysis, risk register updates,

Plan Asses

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

TCM Risk Management Steps

• Plan and implement the treatment of the identified risks

• Monitor the implementation of risk treatment actions, report on status, and adjust actions according to results.

register updates, and reporting.

TreatControl

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS1. Risk Planning

� Establish the approach, form, content

� Define results of risk management

� Define key terms

� Establish criteria for risk identification and assessment, analysis approaches and

general risk treatment strategies

� The outline of the risk management implementation should be in the project

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� The outline of the risk management implementation should be in the project

plan at the start of basic engineering.

� The final version of the risk management plan should be reviewed and

approved early in detailed engineering.

� The first workshops should take place during project development (prior to the

start of detailed design).

� The earlier a project can recognize and implement risk management treatment

the more effective it will be.

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS2. Risk Assessment

a) Risk Identification

b) Risk Analysis (Qualitative and Quantitative)

� The steps:

1. The risk management lead notifies the participants and schedules the

meetings and interviews.

2. Meetings and interviews to identify threats and opportunities are conducted,

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

2. Meetings and interviews to identify threats and opportunities are conducted,

based on the risk management criteria formulated in planning, approved by

management, and distributed to participants (i.e., risk identification).

3. Threat or opportunity items and any additional needed resources are

quantified and evaluated by the appropriate subject matter experts. The

results of analysis are prepared to support the treatment phase (i.e., risk

analysis).

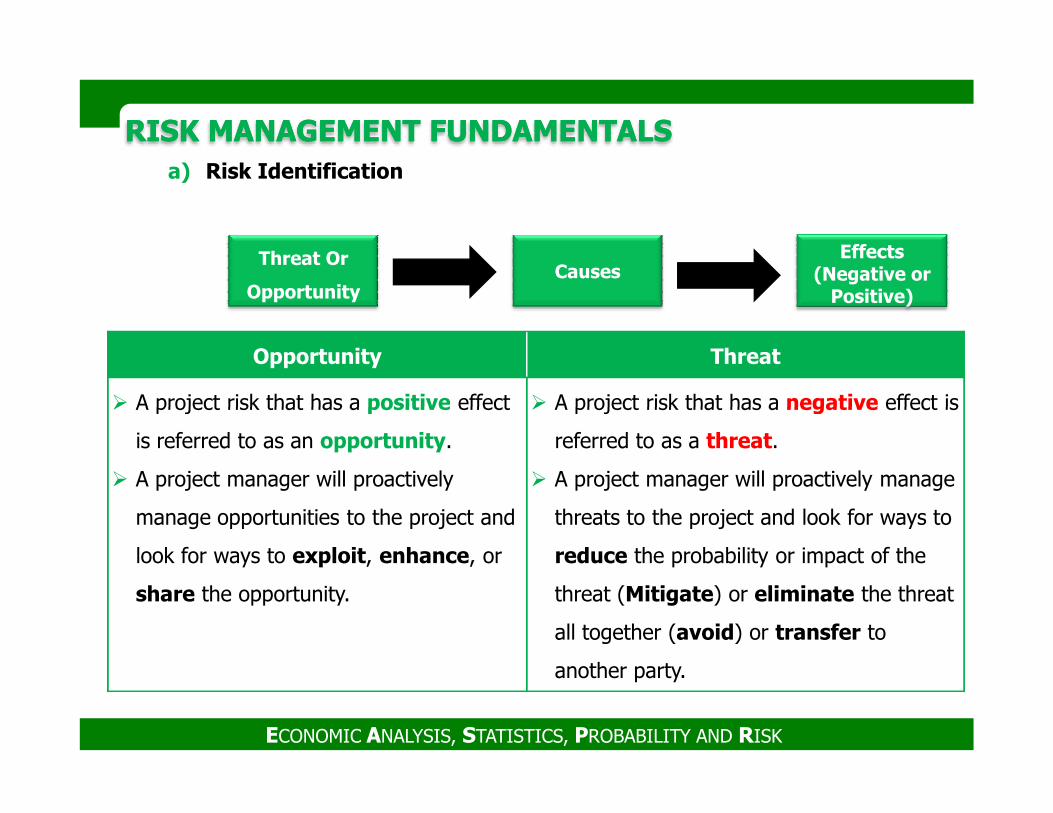

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALSa) Risk Identification

Threat Or

OpportunityCauses

Effects (Negative or

Positive)

Opportunity Threat

� A project risk that has a positive effect � A project risk that has a negative effect is

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� A project risk that has a positive effect

is referred to as an opportunity.

� A project manager will proactively

manage opportunities to the project and

look for ways to exploit, enhance, or

share the opportunity.

� A project risk that has a negative effect is

referred to as a threat.

� A project manager will proactively manage

threats to the project and look for ways to

reduce the probability or impact of the

threat (Mitigate) or eliminate the threat

all together (avoid) or transfer to

another party.

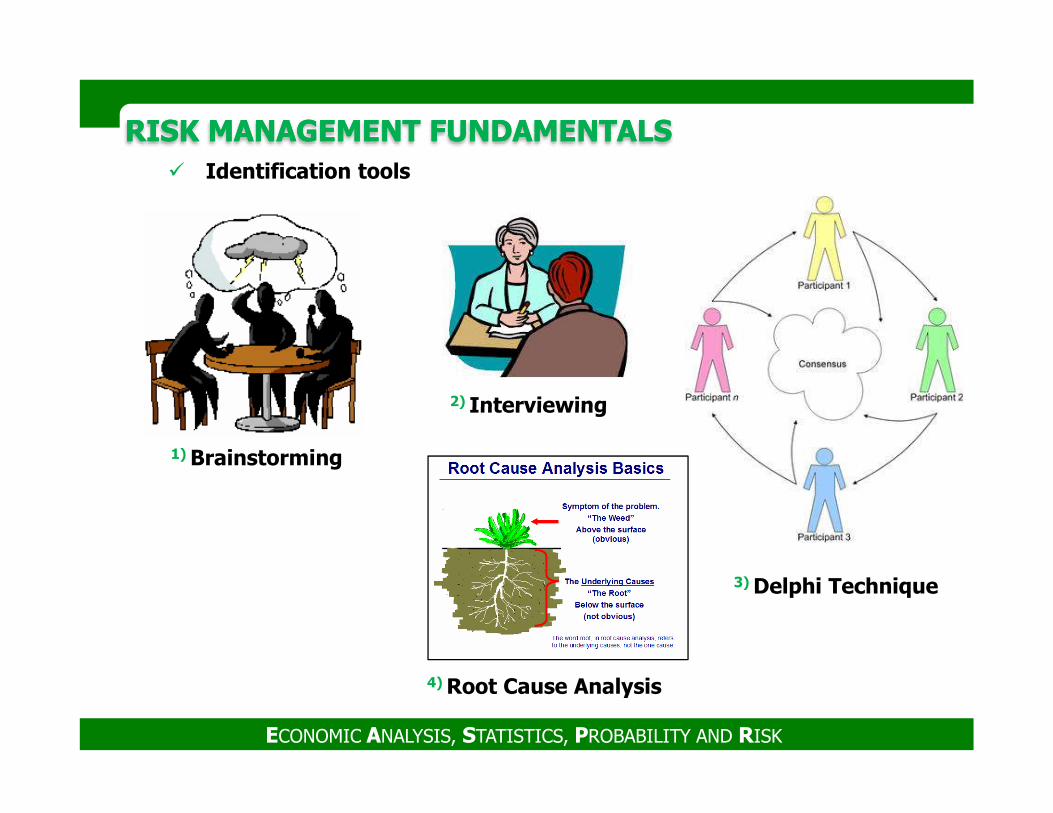

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS� Identification tools

2) Interviewing

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

1) Brainstorming

3) Delphi Technique

2) Interviewing

4) Root Cause Analysis

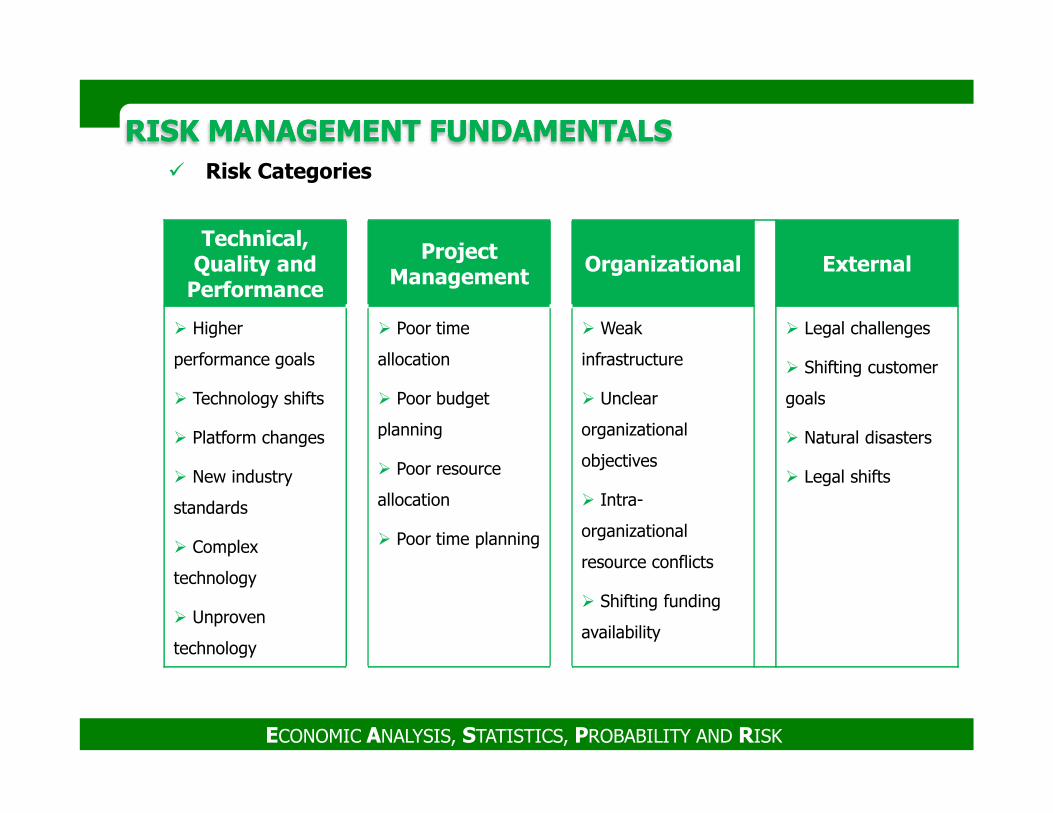

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS� Risk Categories

Technical, Quality and

Performance

Project Management

Organizational External

� Higher

performance goals

� Technology shifts

� Poor time

allocation

� Poor budget

� Weak

infrastructure

� Unclear

� Legal challenges

� Shifting customer

goals

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Technology shifts

� Platform changes

� New industry

standards

� Complex

technology

� Unproven

technology

� Poor budget

planning

� Poor resource

allocation

� Poor time planning

� Unclear

organizational

objectives

� Intra-

organizational

resource conflicts

� Shifting funding

availability

goals

� Natural disasters

� Legal shifts

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS

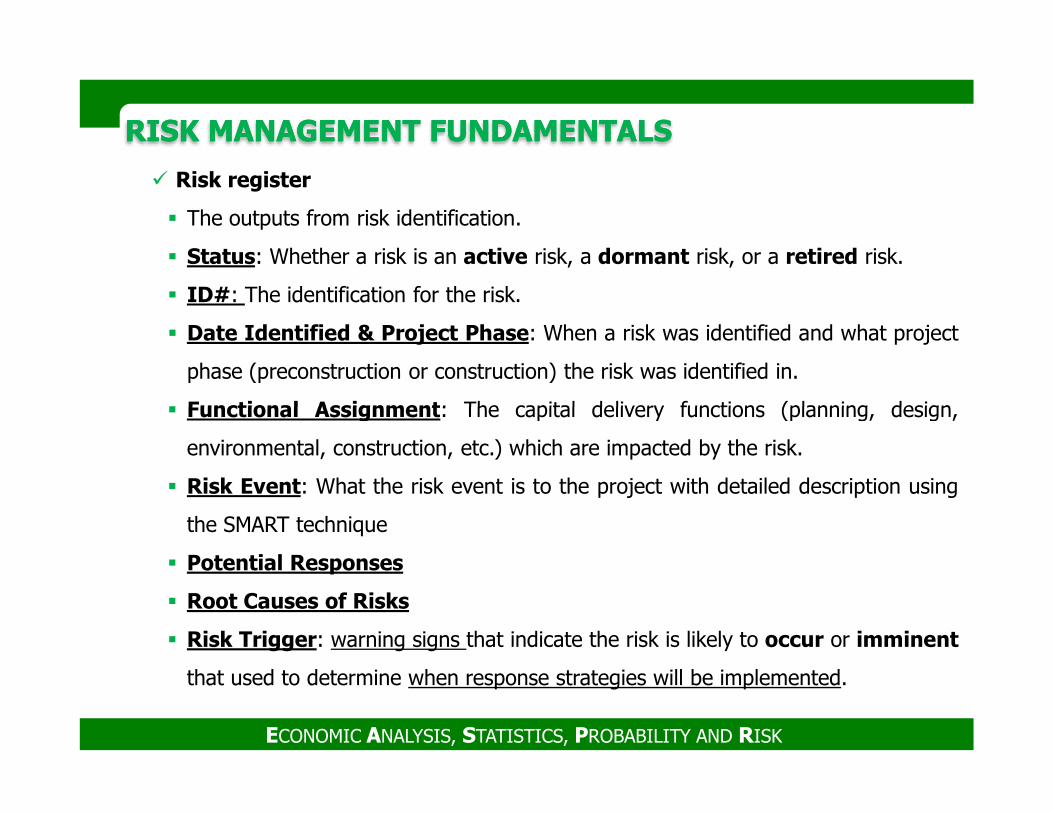

� Risk register

� The outputs from risk identification.

� Status: Whether a risk is an active risk, a dormant risk, or a retired risk.

� ID#: The identification for the risk.

� Date Identified & Project Phase: When a risk was identified and what project

phase (preconstruction or construction) the risk was identified in.

� Functional Assignment: The capital delivery functions (planning, design,

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Functional Assignment: The capital delivery functions (planning, design,

environmental, construction, etc.) which are impacted by the risk.

� Risk Event: What the risk event is to the project with detailed description using

the SMART technique

� Potential Responses

� Root Causes of Risks

� Risk Trigger: warning signs that indicate the risk is likely to occur or imminent

that used to determine when response strategies will be implemented.

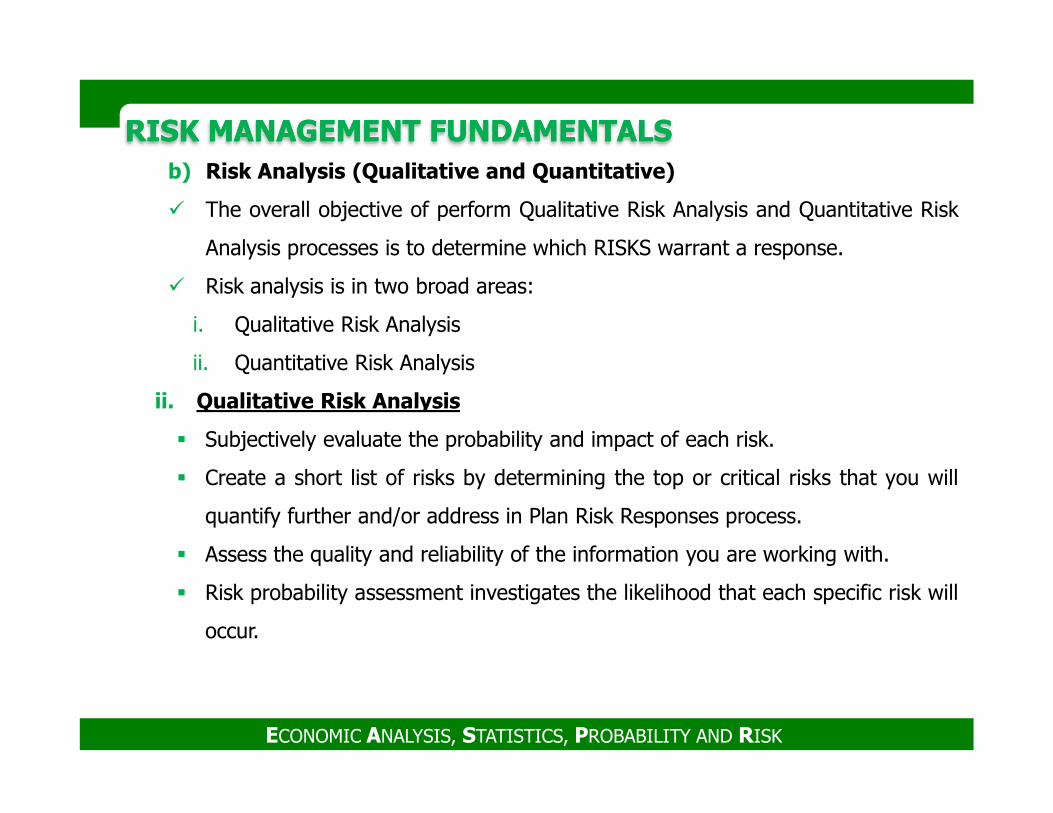

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALSb) Risk Analysis (Qualitative and Quantitative)

� The overall objective of perform Qualitative Risk Analysis and Quantitative Risk

Analysis processes is to determine which RISKS warrant a response.

� Risk analysis is in two broad areas:

i. Qualitative Risk Analysis

ii. Quantitative Risk Analysis

ii. Qualitative Risk Analysis

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

ii. Qualitative Risk Analysis

� Subjectively evaluate the probability and impact of each risk.

� Create a short list of risks by determining the top or critical risks that you will

quantify further and/or address in Plan Risk Responses process.

� Assess the quality and reliability of the information you are working with.

� Risk probability assessment investigates the likelihood that each specific risk will

occur.

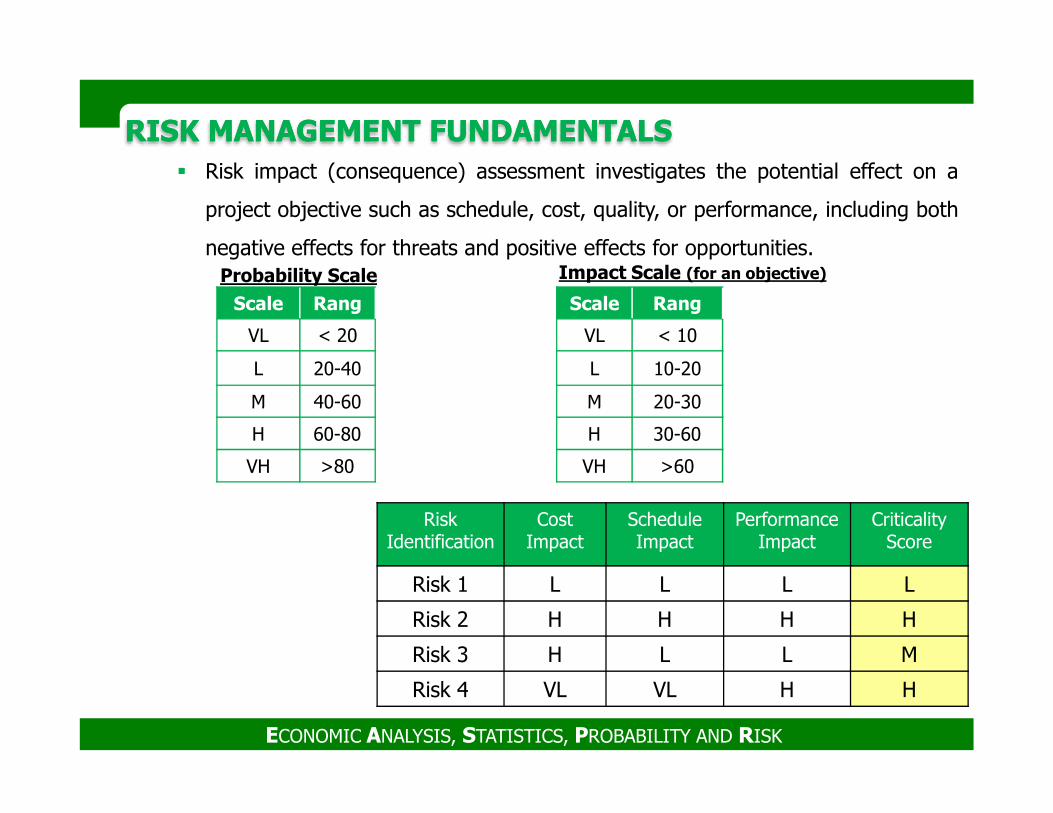

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS� Risk impact (consequence) assessment investigates the potential effect on a

project objective such as schedule, cost, quality, or performance, including both

negative effects for threats and positive effects for opportunities.Probability Scale

Scale Rang

VL < 20

L 20-40

M 40-60

Impact Scale (for an objective)

Scale Rang

VL < 10

L 10-20

M 20-30

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Risk Identification

Cost Impact

Schedule Impact

Performance Impact

Criticality Score

Risk 1 L L L L

Risk 2 H H H H

Risk 3 H L L M

Risk 4 VL VL H H

M 40-60

H 60-80

VH >80

M 20-30

H 30-60

VH >60

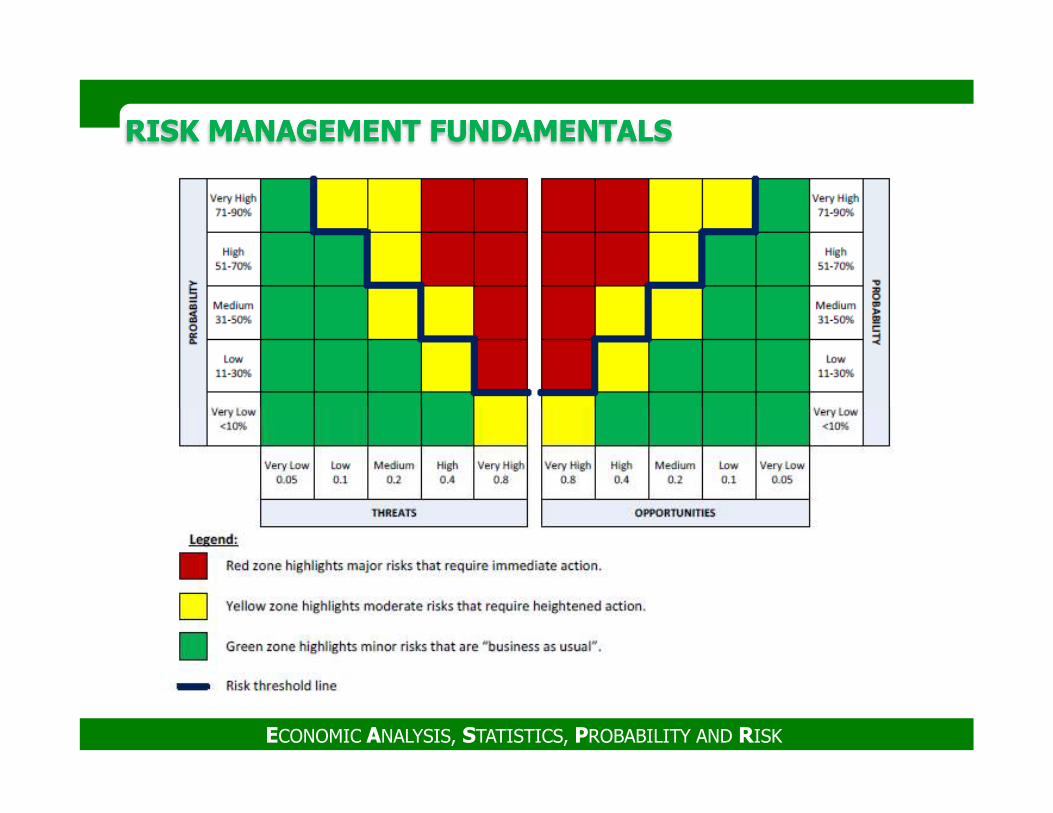

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS� Evaluation of each risk’s importance and, hence, priority for attention is

typically conducted using a look-up table or a probability and impact

matrix.

� P-I matrix can be based on ordinal very)ترتيبي low, low, medium, high, and

very high ) or cardinal /1.)العدد .3/ .5/ .7/ .9 or 1/ 2/ 3/ 4/ 5) scales.

� The organization should determine which combinations of probability and

impact result in a classification of high risk “red condition”, moderate risk

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

impact result in a classification of high risk “red condition”, moderate risk

“yellow condition”, and low risk “green condition”.

� For consistency with other risk assessment terms, a 1-5 scale for

probability is used.

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALSii. Quantitative Risk Analysis

� Quantitative risk analysis is the application of mathematical techniques and

models to numerically establish the probability of risk and the consequences of

risk.

� Objectively evaluate the probability and impact of each risk.

� Decide which risks warrant a response.

� Determine the level of risk the project currently has and whether that level of

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Determine the level of risk the project currently has and whether that level of

risk is acceptable for the expected gain from the product of the project.

� Determine how much the project will cost and how long it will take if no further

risk management actions are taken to decrease project risk.

� Determine which risk require response planning.

� Determine the probability of achieving cost or schedule objectives for the

project.

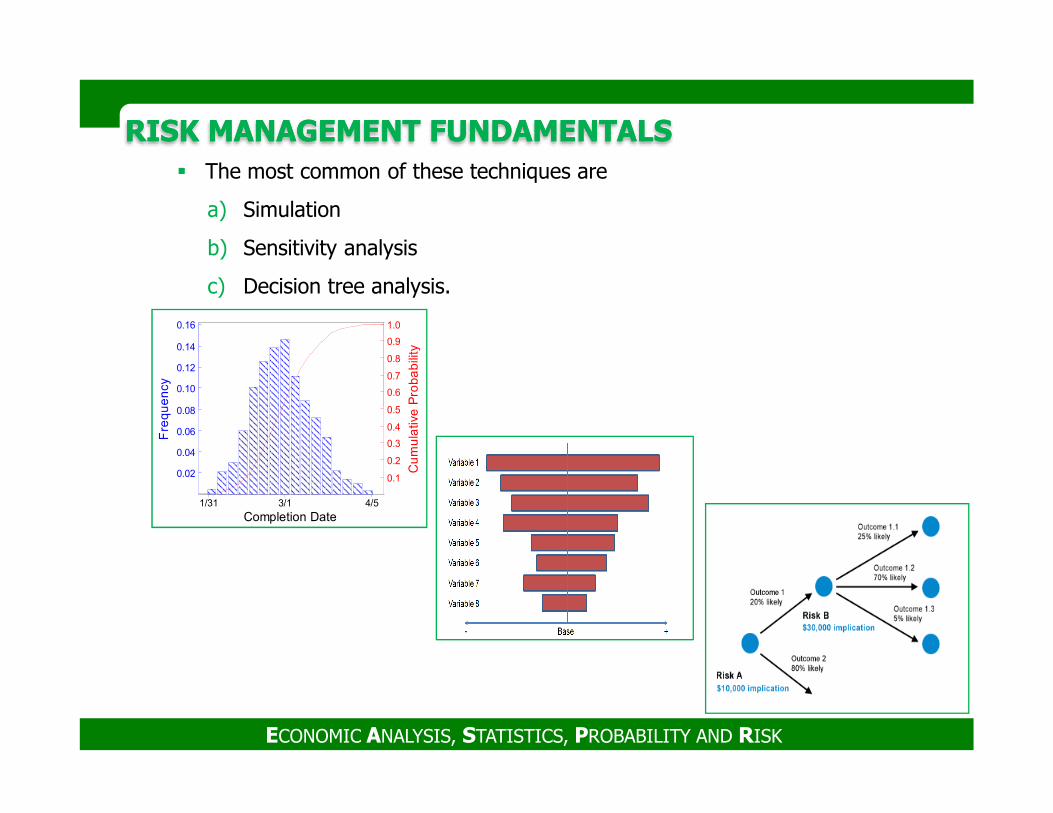

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS� The most common of these techniques are

a) Simulation

b) Sensitivity analysis

c) Decision tree analysis.

Fre

qu

en

cy

Cu

mu

lativ

e P

rob

ab

ility

0.5

0.6

0.7

0.8

0.9

1.0

0.08

0.10

0.12

0.14

0.16

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Completion Date

Fre

qu

en

cy

Cu

mu

lativ

e P

rob

ab

ility

3/11/31 4/5

0.1

0.2

0.3

0.4

0.5

0.02

0.04

0.06

0.08

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS

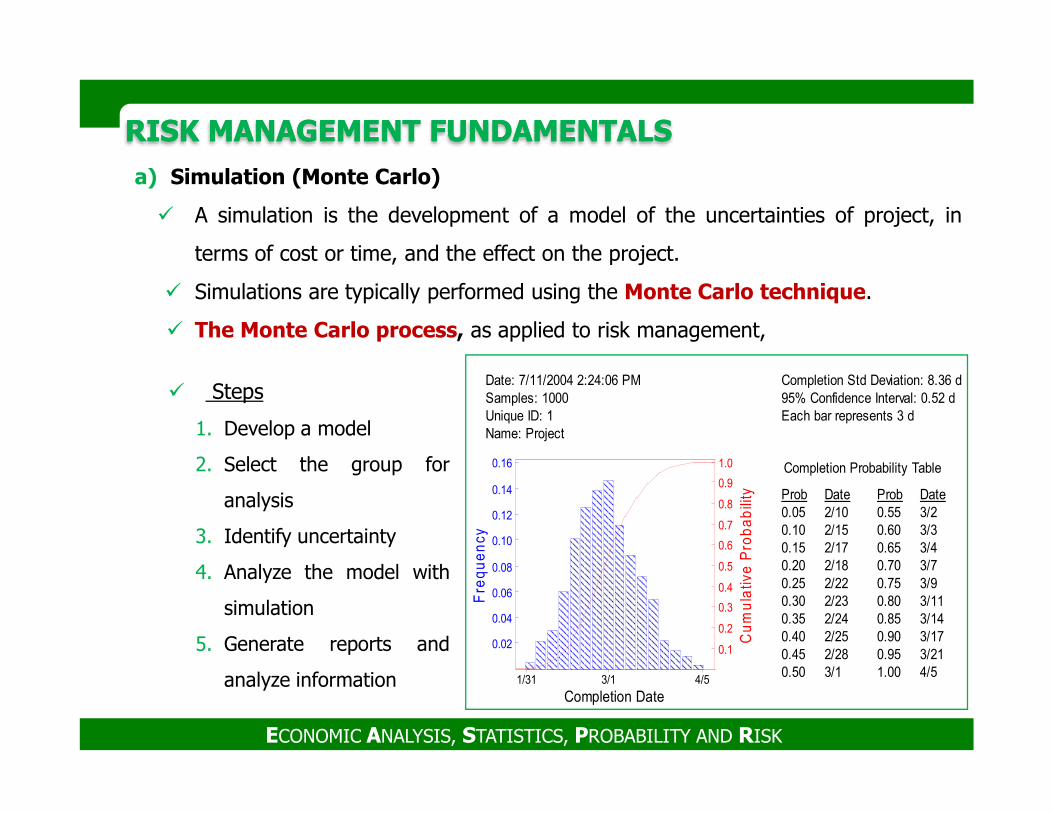

Date: 7/11/2004 2:24:06 PMSamples: 1000

Completion Std Deviation: 8.36 d95% Confidence Interval: 0.52 d� Steps

a) Simulation (Monte Carlo)

� A simulation is the development of a model of the uncertainties of project, in

terms of cost or time, and the effect on the project.

� Simulations are typically performed using the Monte Carlo technique.

� The Monte Carlo process, as applied to risk management,

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Unique ID: 1Name: Project

Each bar represents 3 d

Completion Date

Fre

qu

en

cy

Cu

mu

lativ

e P

rob

ab

ility

3/11/31 4/5

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16 Completion Probability Table

Prob ProbDate Date0.05 2/100.10 2/150.15 2/170.20 2/180.25 2/220.30 2/230.35 2/240.40 2/250.45 2/280.50 3/1

0.55 3/20.60 3/30.65 3/40.70 3/70.75 3/90.80 3/110.85 3/140.90 3/170.95 3/211.00 4/5

1. Develop a model

2. Select the group for

analysis

3. Identify uncertainty

4. Analyze the model with

simulation

5. Generate reports and

analyze information

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS

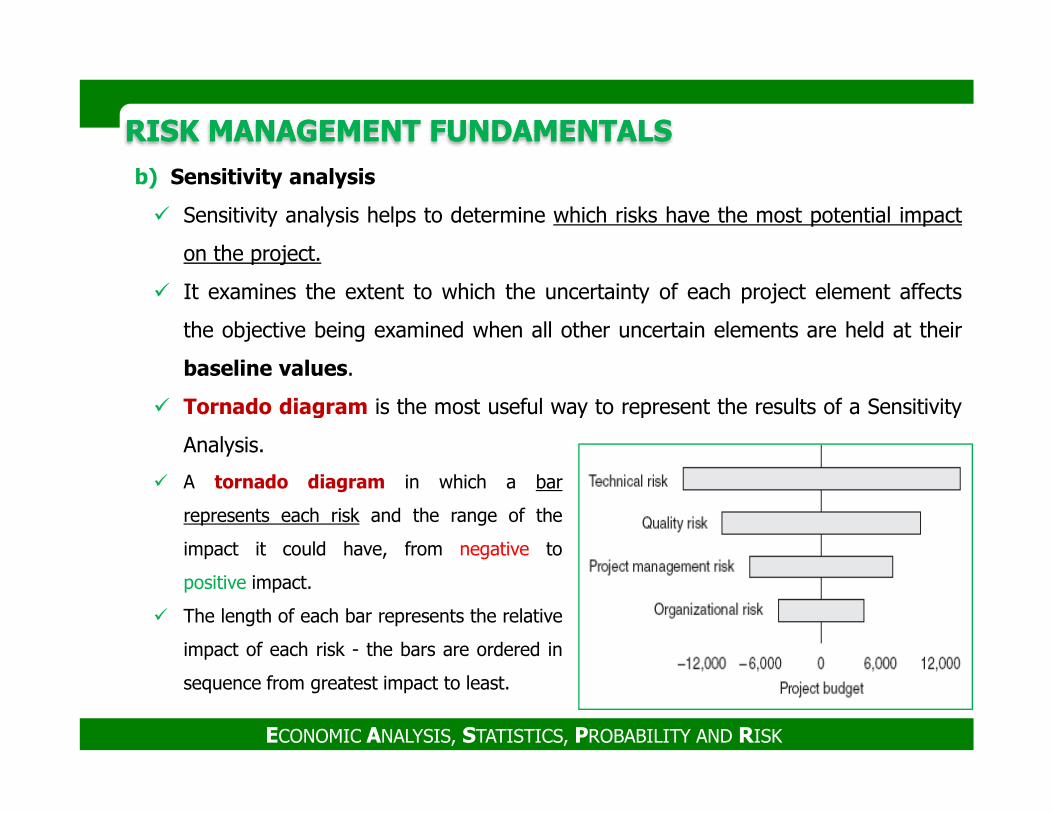

b) Sensitivity analysis

� Sensitivity analysis helps to determine which risks have the most potential impact

on the project.

� It examines the extent to which the uncertainty of each project element affects

the objective being examined when all other uncertain elements are held at their

baseline values.

� Tornado diagram is the most useful way to represent the results of a Sensitivity

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Tornado diagram is the most useful way to represent the results of a Sensitivity

Analysis.

� A tornado diagram in which a bar

represents each risk and the range of the

impact it could have, from negative to

positive impact.

� The length of each bar represents the relative

impact of each risk - the bars are ordered in

sequence from greatest impact to least.

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS

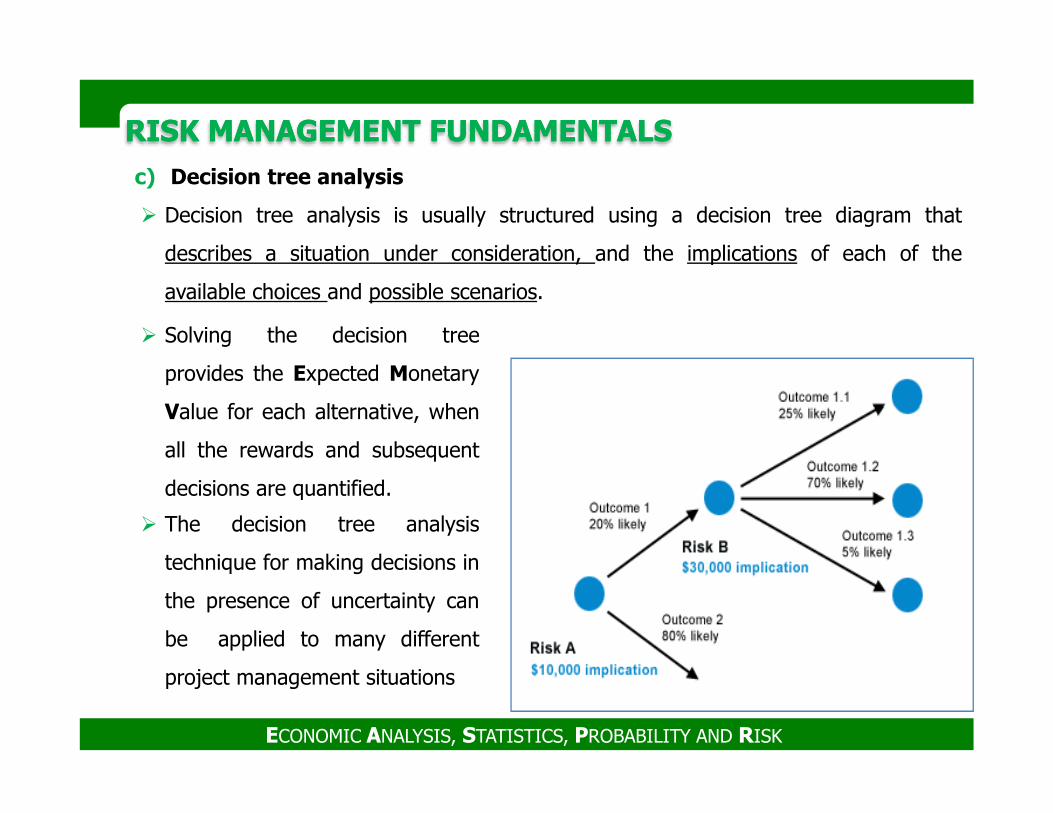

c) Decision tree analysis

� Decision tree analysis is usually structured using a decision tree diagram that

describes a situation under consideration, and the implications of each of the

available choices and possible scenarios.

� Solving the decision tree

provides the Expected Monetary

Value for each alternative, when

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Value for each alternative, when

all the rewards and subsequent

decisions are quantified.

� The decision tree analysis

technique for making decisions in

the presence of uncertainty can

be applied to many different

project management situations

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALSRisk Management Software

1. Cost Risk Analysis

� Crystal Ball, Oracle Corp.

� @Risk, Palisade Corp.

� Risk Solver, Frontline Systems Inc.

2. Schedule Risk Analysis

� @Risk for Project, Palisade Corp.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� @Risk for Project, Palisade Corp.

� Primavera, Oracle Corp.

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS

Contingency

� An amount added to an estimate to allow for items, conditions, or events for which

the state, occurrence, or effect is uncertain and that experience shows will likely

result, in aggregate, in additional costs.

� Typically, estimates using statistical analysis or judgment, based on past asset or

project experience.

� Contingency usually excludes:

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Contingency usually excludes:

� Major scope changes such as changes in end product specification, capacities,

building sizes, and location of the asset or project.

� Extraordinary events such as major strikes and natural disasters.

� Management reserves.

� Escalation and currency effects.

RISK MANAGEMENT PRACTICAL GUIDERISK MANAGEMENT PRACTICAL GUIDE

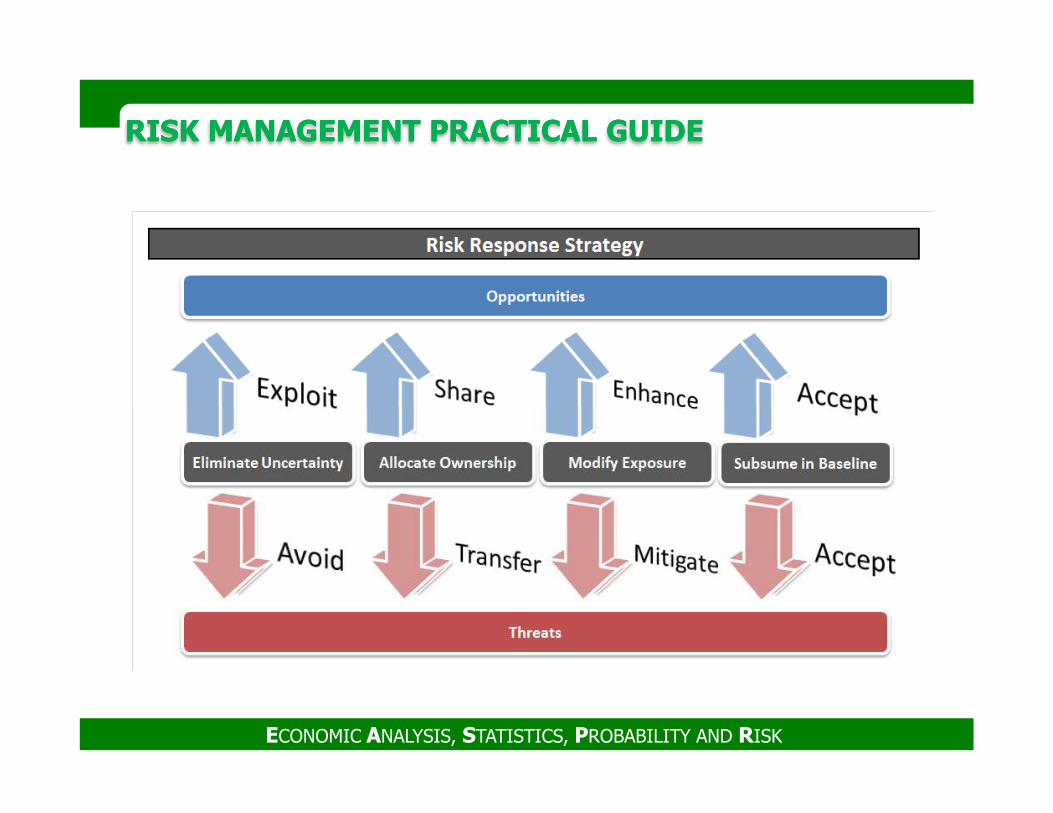

3. Risk Treatment

� The risk management team and other members would develop recommendations

and decisions on how to treat those risks.

� Risks should be assigned risk owners who will be responsible for overseeing the

implementation of the risk treatment action, which should be reflected in a risk

register.

� Key actions performed during the risk treatment phase include (TCM Framework ):

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Key actions performed during the risk treatment phase include (TCM Framework ):

1. Evaluating all appropriate response strategies.

2. Selecting an appropriate risk response plan strategy (or combination of strategies).

3. Developing action items in support of the selected response.

4. Validating proposed actions with assigned actionees, including dates for implementation.

5. Ascertaining post-response targets and gains.

6. Ascertaining response plan resource requirements.

7. Updating project schedule or budget if the anticipated treatment value gain is positive.

8. Identifying any secondary threats or opportunities that may arise from the response.

RISK MANAGEMENT PRACTICAL GUIDERISK MANAGEMENT PRACTICAL GUIDE

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

RISK MANAGEMENT PRACTICAL GUIDERISK MANAGEMENT PRACTICAL GUIDE

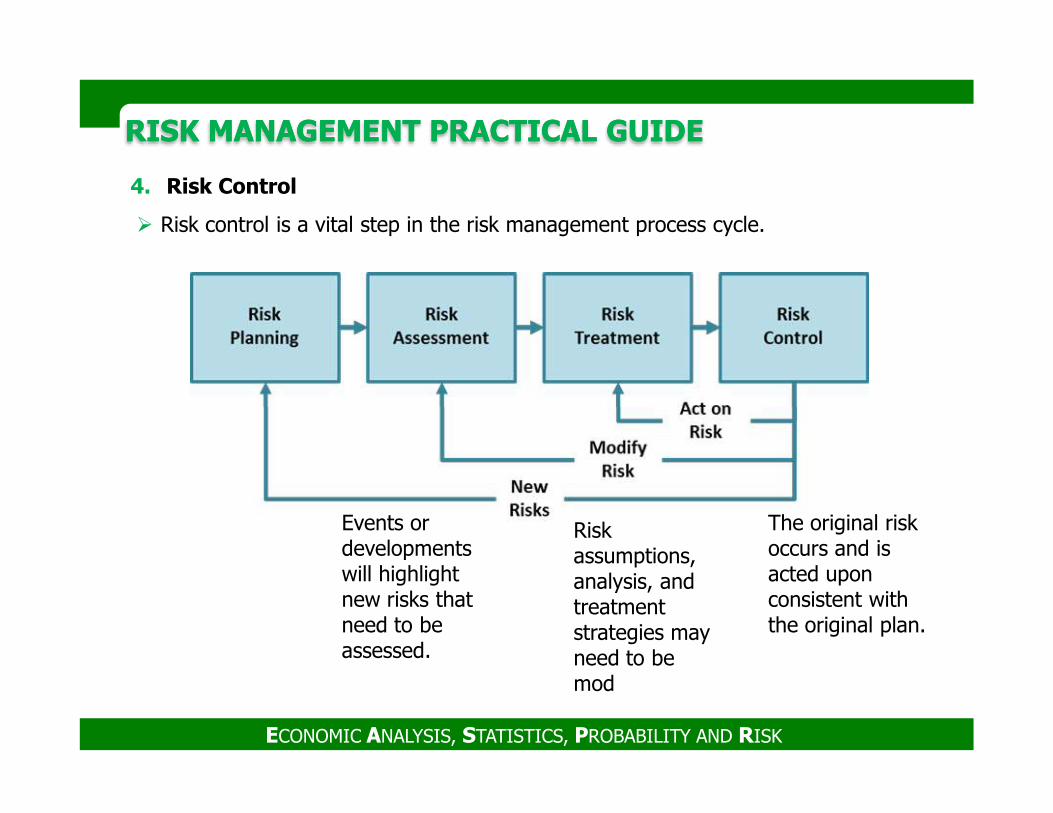

4. Risk Control

� Risk control is a vital step in the risk management process cycle.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

The original risk occurs and is acted upon consistent with the original plan.

Risk assumptions, analysis, and treatment strategies may need to be mod

Events or developments will highlight new risks that need to be assessed.

RISK MANAGEMENT PRACTICAL GUIDERISK MANAGEMENT PRACTICAL GUIDE

� Risk reassessment

� Additional Risk Identification, Qualitative Risk Analysis, Quantitative Risk Analysis,

and Risk Response Planning.

� Control Risks often results in identification of new risks, reassessment of

current risks, and the closing of risks that are outdated.

� Project risk reassessments should be regularly scheduled.

� The results of such reassessments may include newly identifications, additional

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� The results of such reassessments may include newly identifications, additional

qualitative or quantitative risk analysis, and further risk response planning.

� There are two major times when a risk reassessment might occur:

a) When new risks are identified.

b) When changes occur on the project.

RISK MANAGEMENT PRACTICAL GUIDERISK MANAGEMENT PRACTICAL GUIDE

� Risk Audit

� Risk audits examine and document the effectiveness of risk responses in dealing

with identified risks and their root causes, as well as the effectiveness of the risk

management process.

� It is arranged by project manager and results in identification of lessons learned for

the project and for other project in the organization.

� Risk audits are evidence of how seriously risk should be taken on a project.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Risk audits are evidence of how seriously risk should be taken on a project.

� A risk audit includes:

a) Reviewing if the right risk owners have been assigned to each risk

b) Determining if the risk owners are effective.

c) Examining and documenting the effectiveness of contingency plans and

fallback plans

RISK MANAGEMENT PRACTICAL GUIDERISK MANAGEMENT PRACTICAL GUIDE

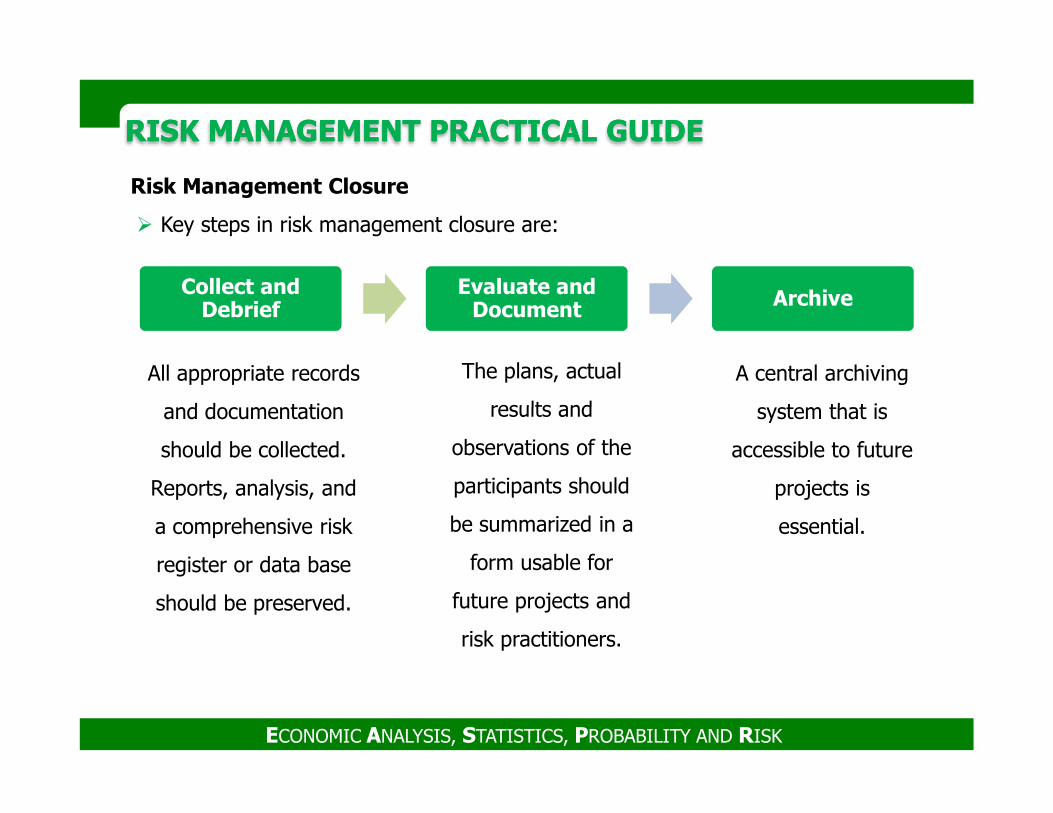

Risk Management Closure

� Key steps in risk management closure are:

Collect and Debrief

Evaluate and Document Archive

All appropriate records

and documentation

The plans, actual

results and

A central archiving

system that is

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

and documentation

should be collected.

Reports, analysis, and

a comprehensive risk

register or data base

should be preserved.

results and

observations of the

participants should

be summarized in a

form usable for

future projects and

risk practitioners.

system that is

accessible to future

projects is

essential.

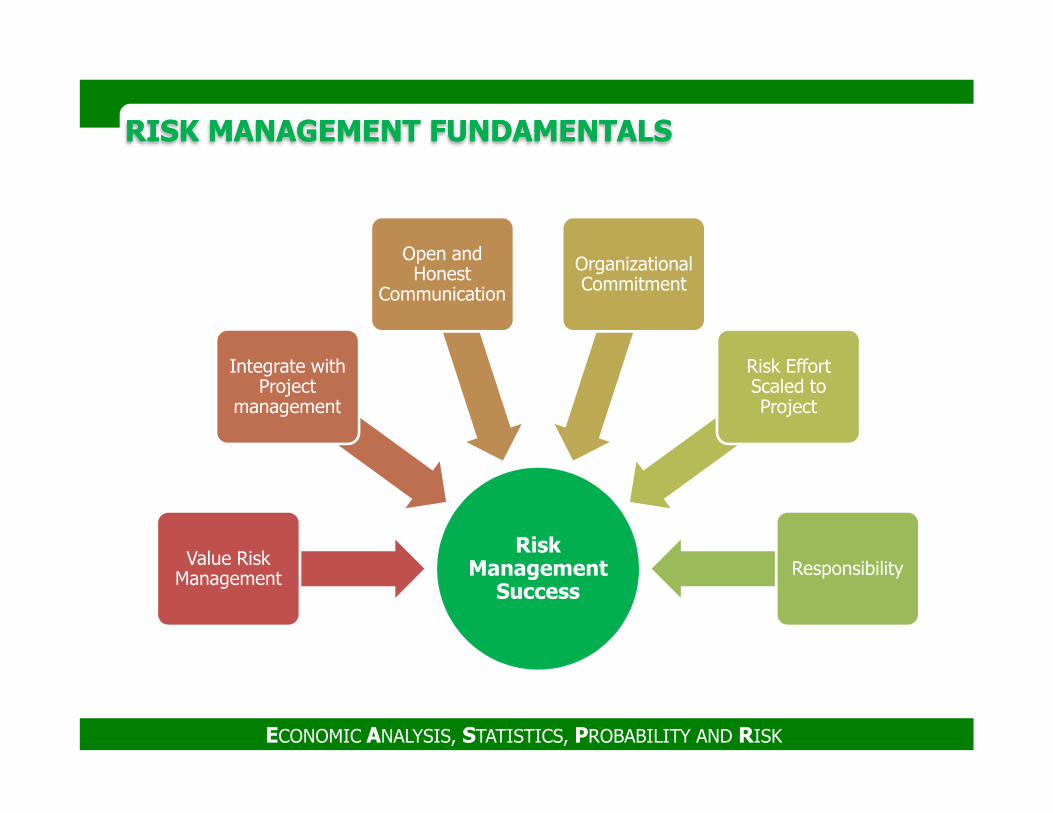

RISK MANAGEMENT FUNDAMENTALSRISK MANAGEMENT FUNDAMENTALS

Integrate with Project

management

Open and Honest

Communication

Organizational Commitment

Risk Effort Scaled to Project

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

Risk Management

Success

Value Risk Management

management Project

Responsibility

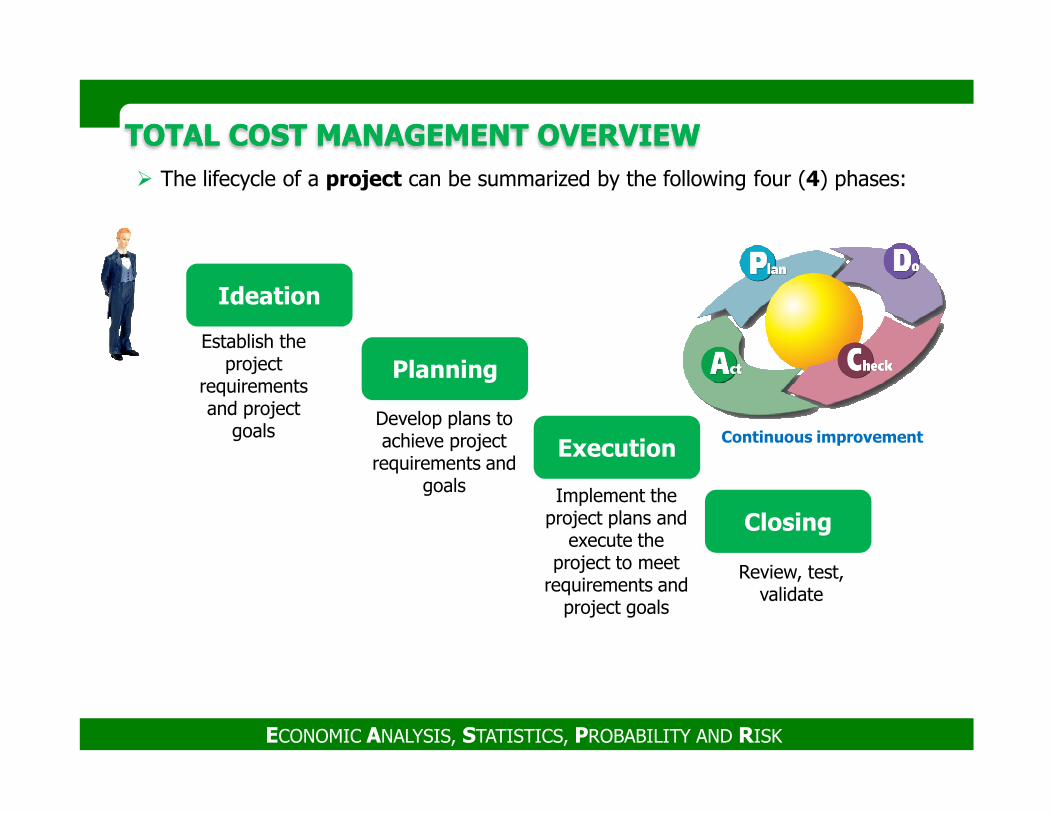

TOTAL COST MANAGEMENT OVERVIEWTOTAL COST MANAGEMENT OVERVIEW

� Total Cost Management (TCM) is described as the “sum of the practices and

processes that an enterprise uses to manage the total lifecycle cost

investment in its portfolio of strategic assets”.

� TCM attempts to illustrate the integration of all the various skills and knowledge

areas that are required for processes to support overall management of both

strategic assets as well as the individual projects, undertaken to create and

develop those assets.

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

develop those assets.

� TCM is accomplished through the application of:

� Cost engineering and cost management principles

� Proven methodologies

� The latest technologies in support of the management process

TOTAL COST MANAGEMENT OVERVIEWTOTAL COST MANAGEMENT OVERVIEW

� Strategic Assets are physical or intellectual property that has long-term or lasting

value to an enterprise.

� They are expected to provide a positive economic benefit and are created

through the investment of money, time, and resources. Examples include:

� Buildings

� Software applications

Retail products

ECONOMIC ANALYSIS, STATISTICS, PROBABILITY AND RISK

� Retail products

� Theater production

� It is important to note that TCM recognizes the term “cost” as going beyond the

traditional monetary definition to include any investment of resources in the

enterprise’s assets.

� TCM is a comprehensive approach to managing the total resource investment in

assets.

TOTAL COST MANAGEMENT OVERVIEWTOTAL COST MANAGEMENT OVERVIEW

� Total Cost Management Processes

� Plan-Do-Check-Act (PDCA) Management Cycle

� Often referred to as the Deming or Shewhart Cycle