Embed Size (px)

Citation preview

Doing Less with Less

IRI Innovation Leaders’ NetworkFall 2013

USG Libertyville

Doing Less with Less

• Making better choices• Better prioritization• Increasing speed• Maintaining culture• Maintaining innovation pace

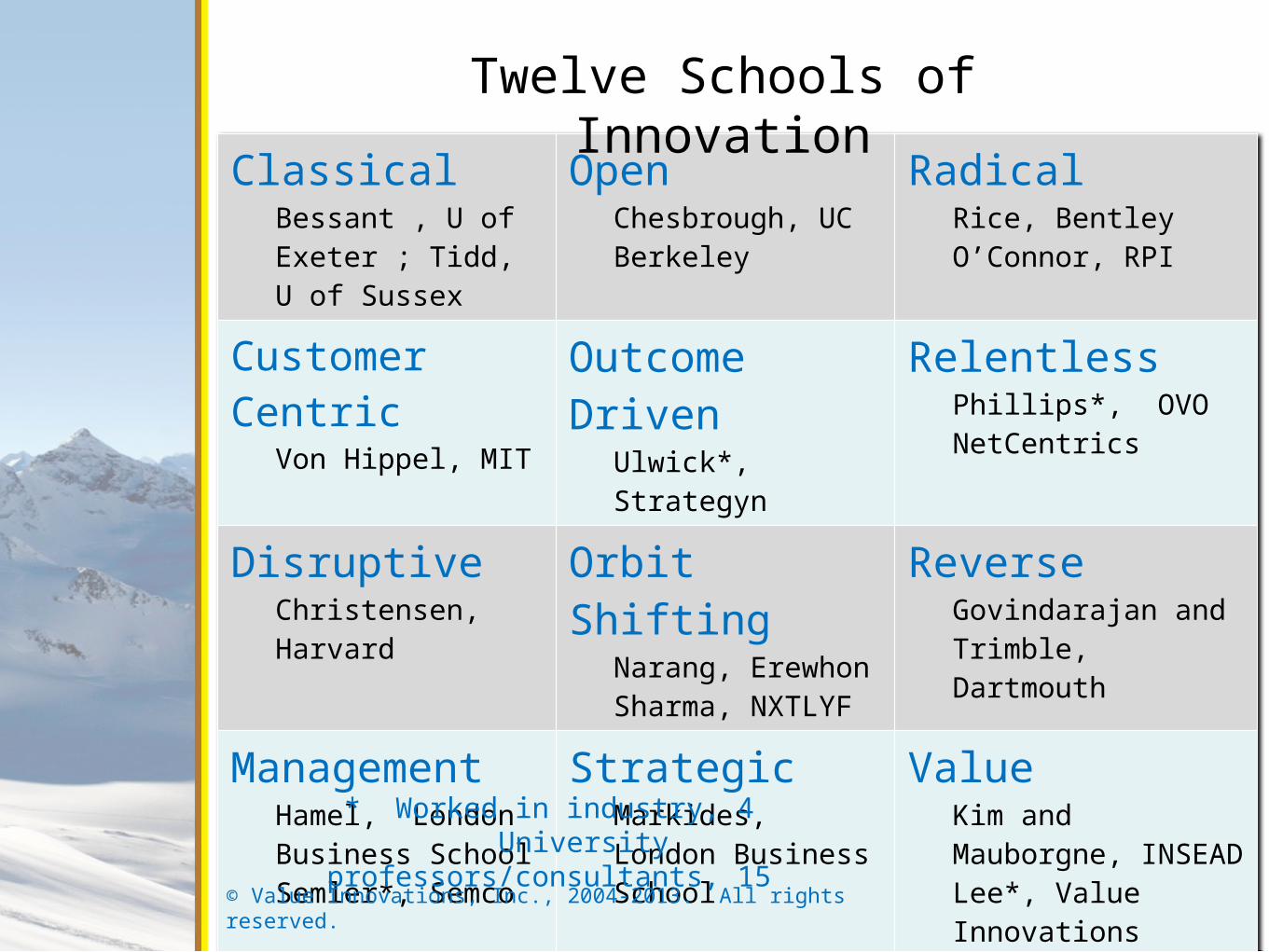

Classical Bessant , U of Exeter ; Tidd, U of Sussex

OpenChesbrough, UC Berkeley

RadicalRice, BentleyO’Connor, RPI

Customer Centric

Von Hippel, MIT

Outcome Driven

Ulwick*, Strategyn

RelentlessPhillips*, OVO NetCentrics

DisruptiveChristensen, Harvard

Orbit ShiftingNarang, ErewhonSharma, NXTLYF

ReverseGovindarajan and Trimble, Dartmouth

ManagementHamel, London Business SchoolSemler*, Semco

StrategicMarkides, London Business School

ValueKim and Mauborgne, INSEADLee*, Value Innovations

Twelve Schools of Innovation

* Worked in industry, 4 University professors/consultants, 15

© Value Innovations, Inc., 2004-2013. All rights reserved.

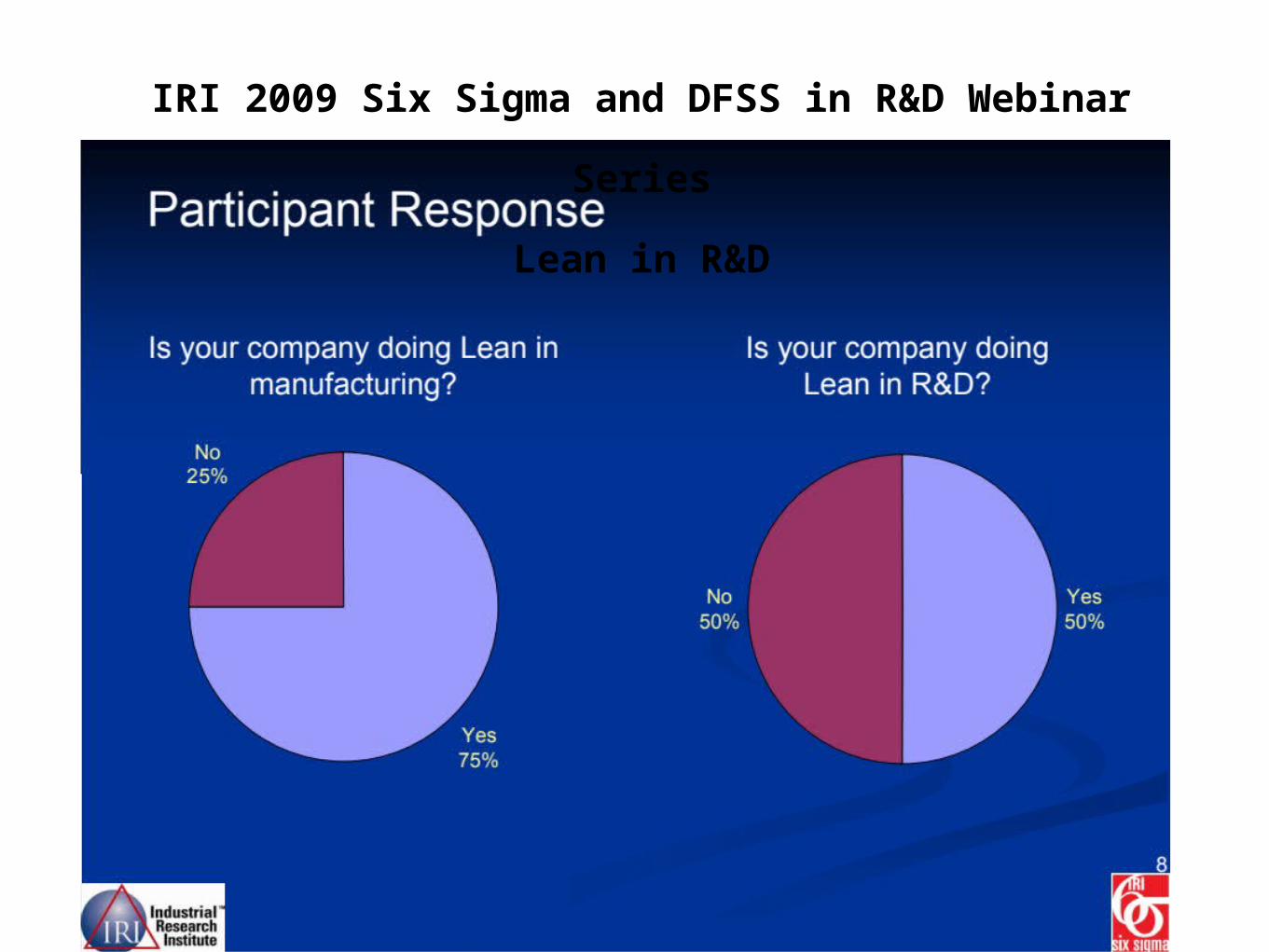

IRI 2009 Six Sigma and DFSS in R&D Webinar Series

Lean in R&D

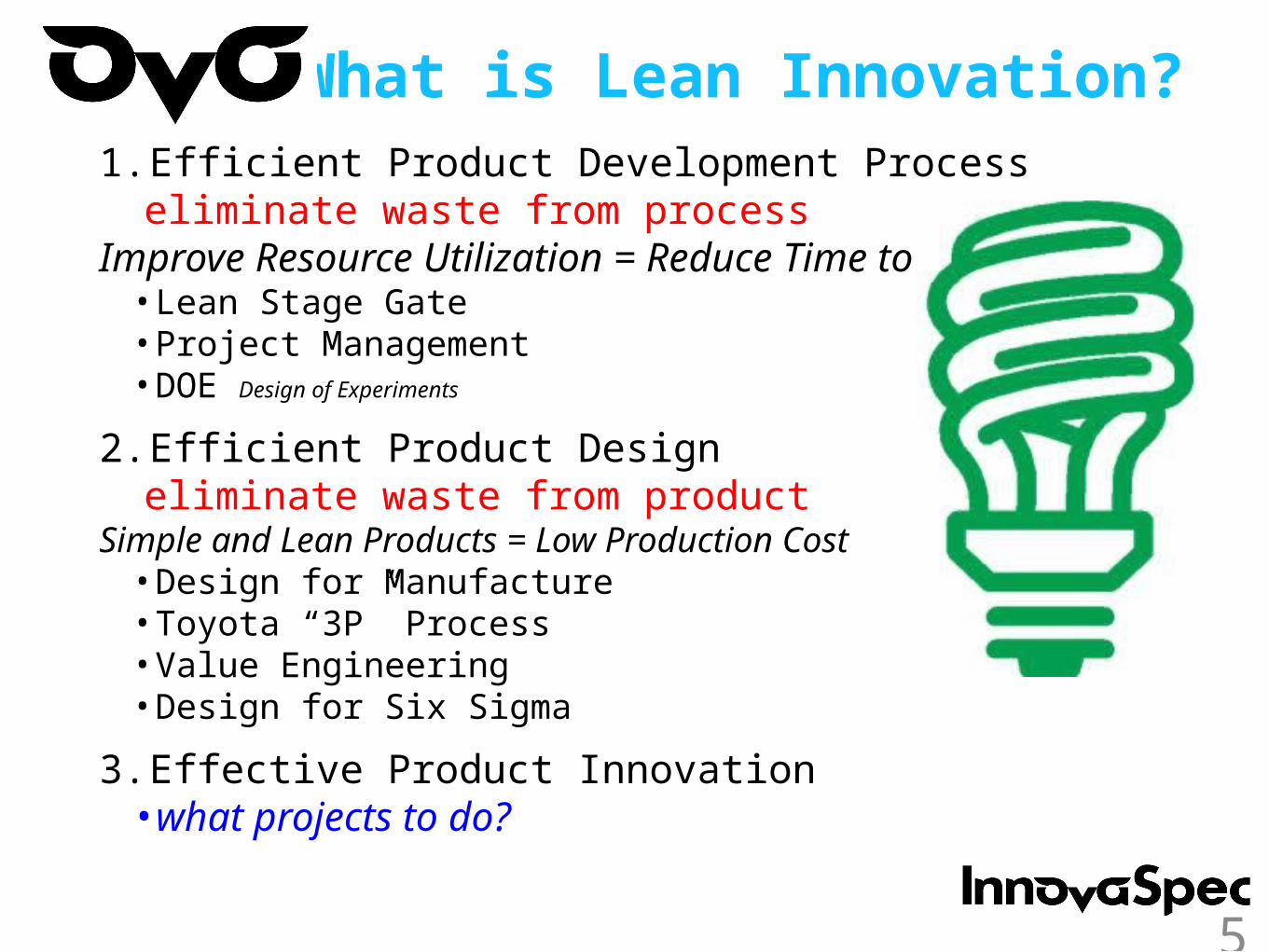

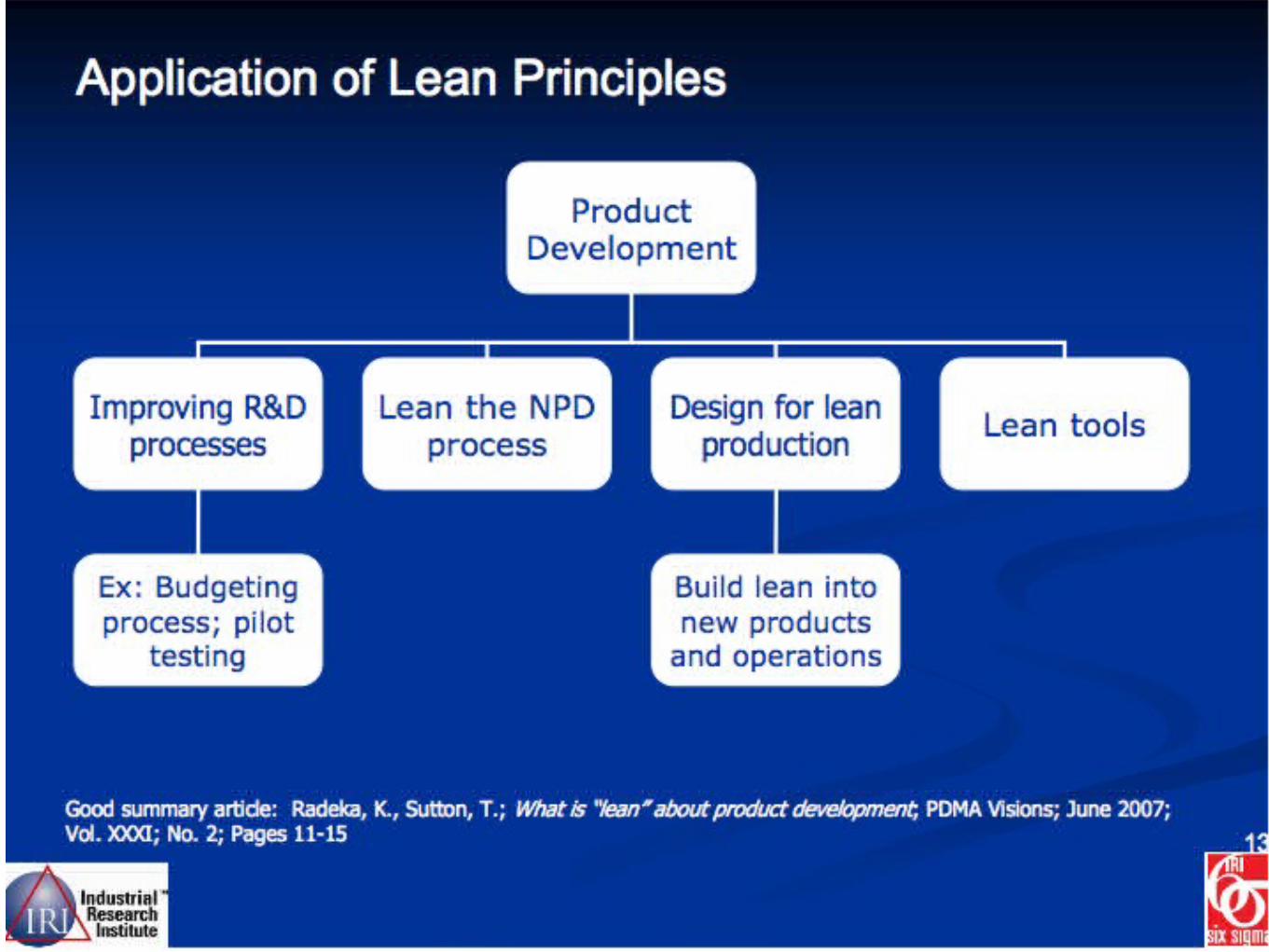

What is Lean Innovation?1. Efficient Product Development Process

eliminate waste from processImprove Resource Utilization = Reduce Time to Market • Lean Stage Gate• Project Management• DOE Design of Experiments

2. Efficient Product Design eliminate waste from product

Simple and Lean Products = Low Production Cost• Design for Manufacture• Toyota “3P” Process• Value Engineering• Design for Six Sigma

3. Effective Product Innovation•what projects to do?

5

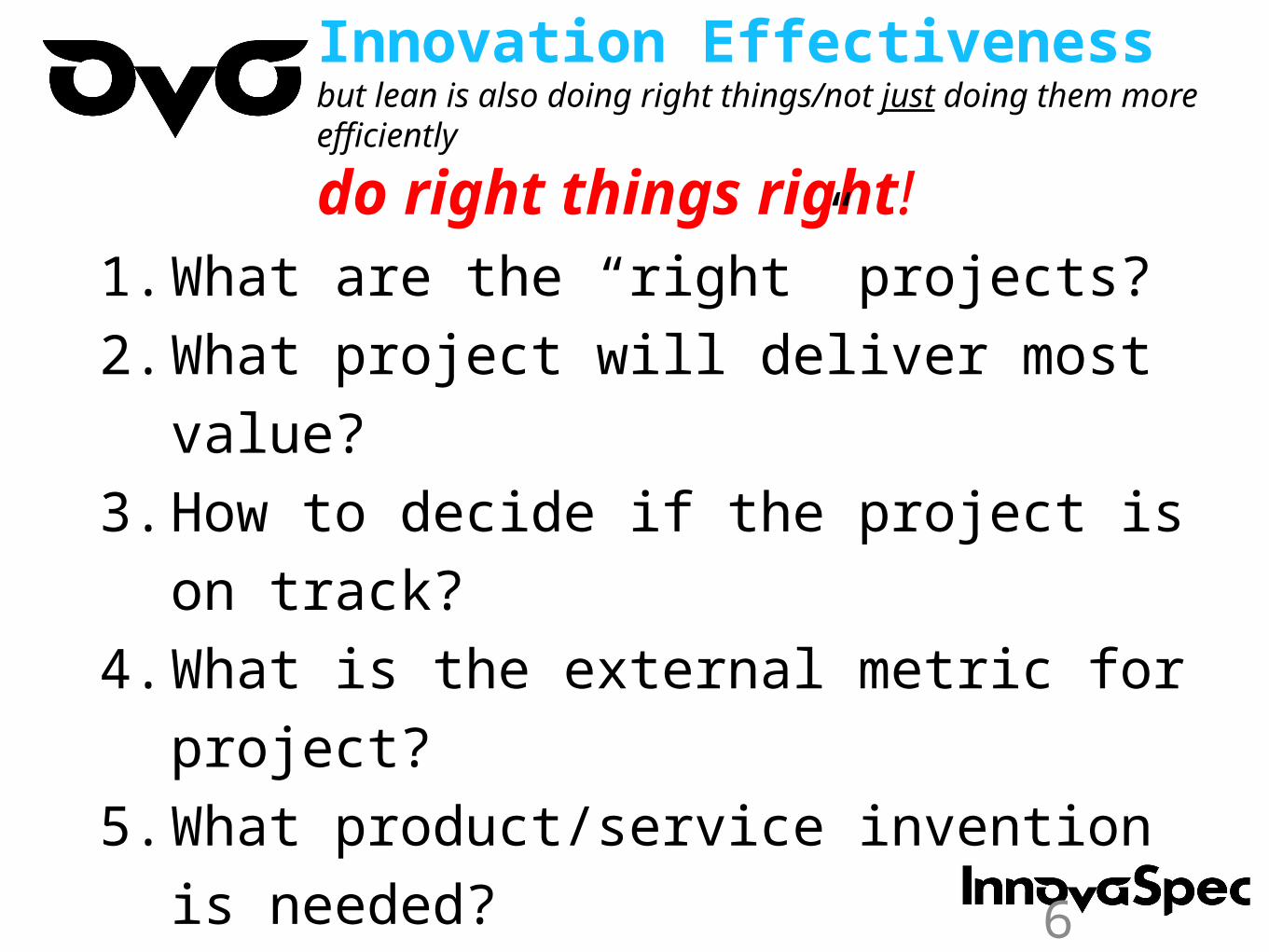

Innovation Effectivenessbut lean is also doing right things/not just doing them more efficiently

do right things right!1. What are the “right” projects?2. What project will deliver most value?3. How to decide if the project is on

track?4. What is the external metric for

project?5. What product/service invention is

needed?6. Where do ideas come from to feed the

Lean Sigma Innovation Process?6

InnovaSpec Lean Innovation Bookshelf

8

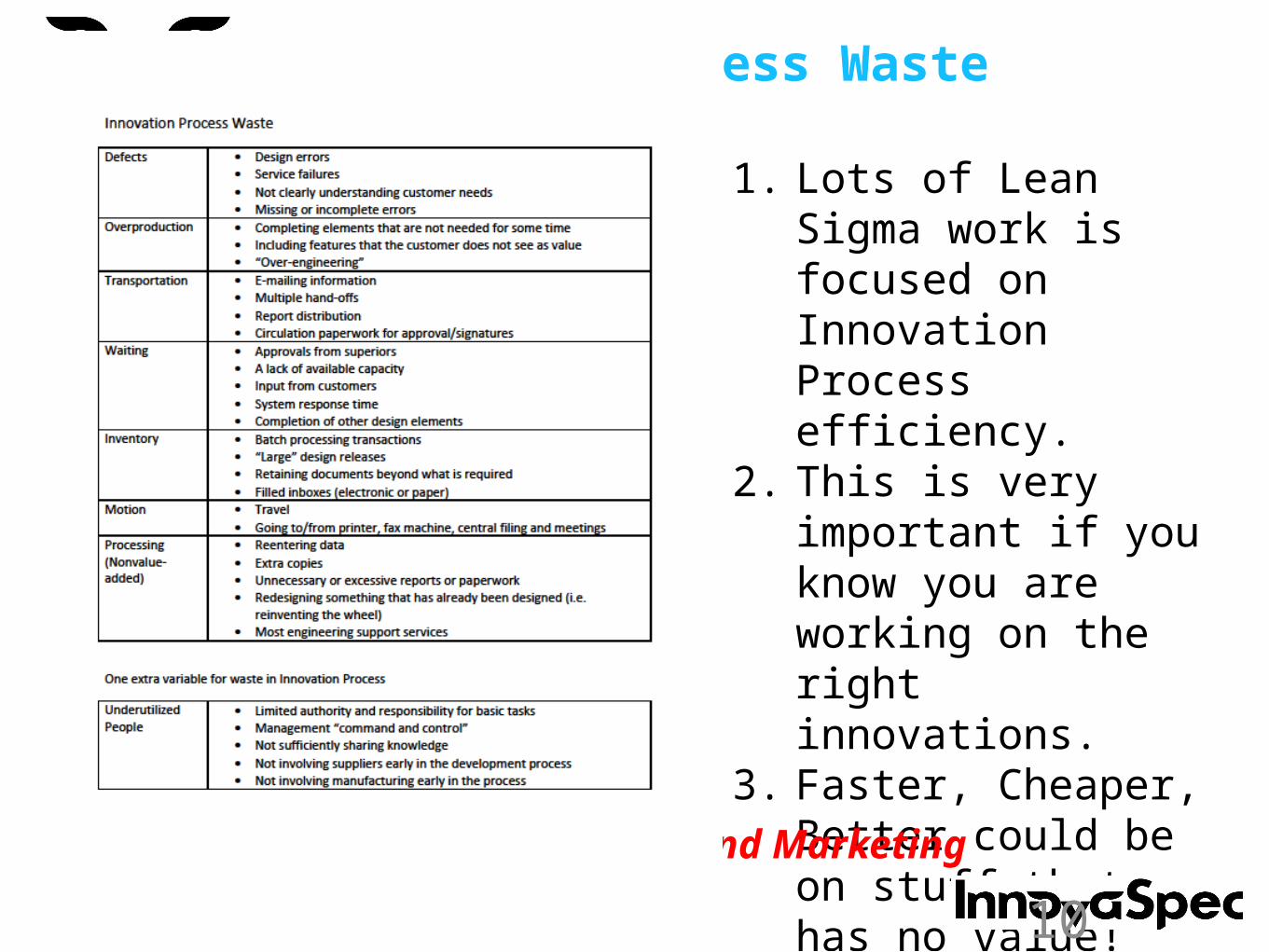

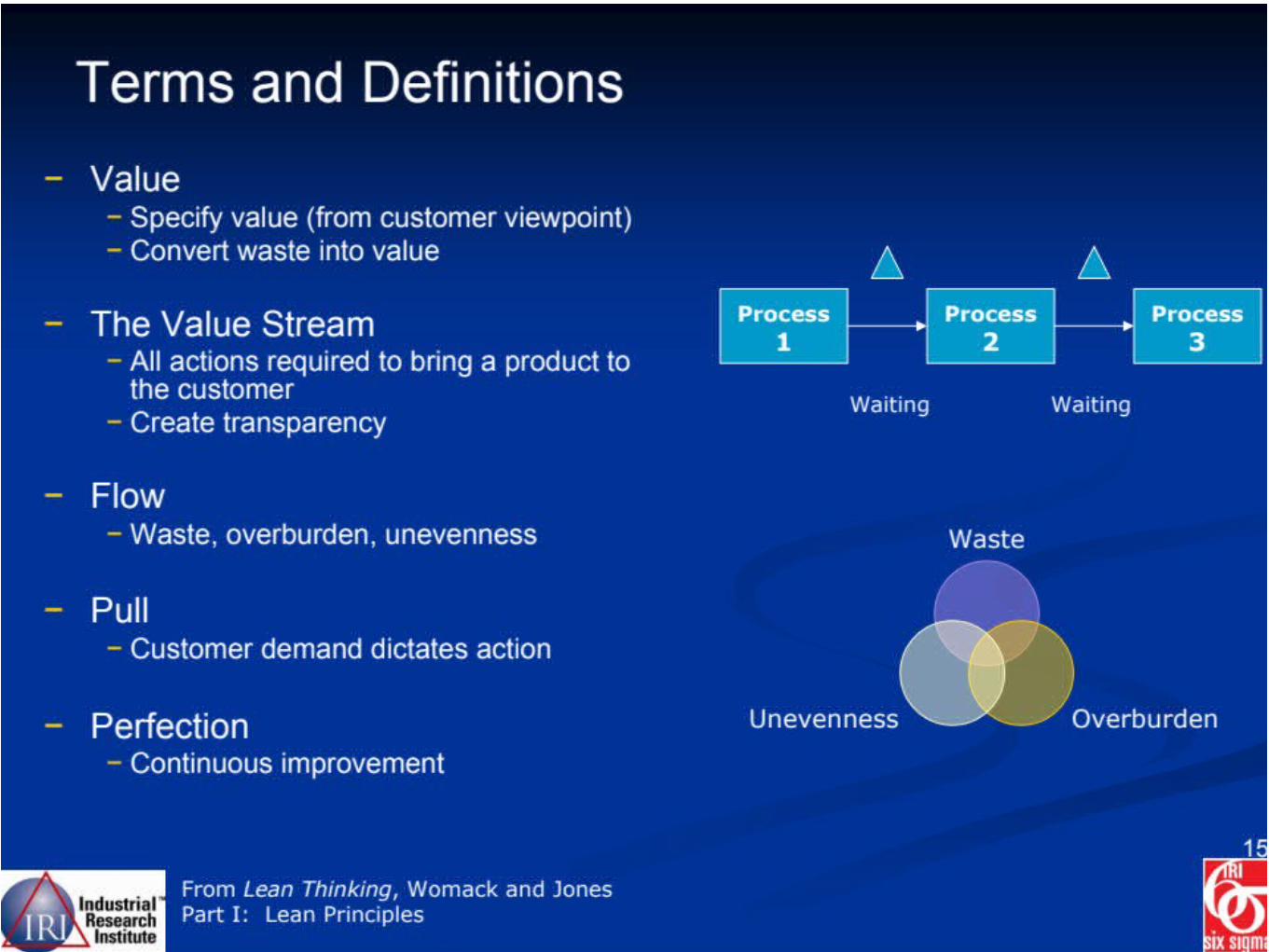

Innovation Process Waste Categories

1. Lots of Lean Sigma work is focused on Innovation Process efficiency.

2. This is very important if you know you are working on the right innovations.

3. Faster, Cheaper, Better could be on stuff that has no value!

Need to involve Customers and Marketing

10

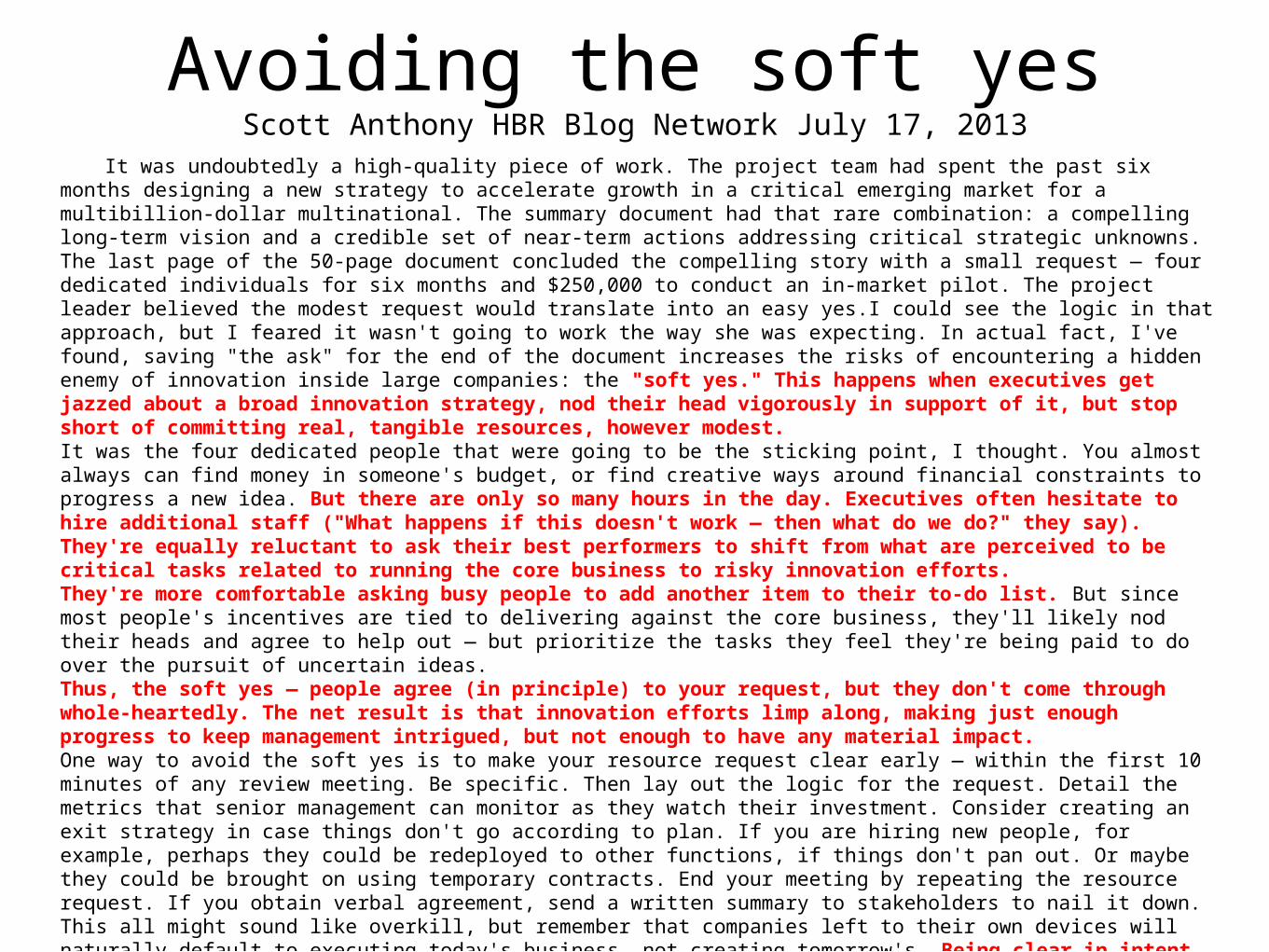

Avoiding the soft yesScott Anthony HBR Blog Network July 17, 2013

It was undoubtedly a high-quality piece of work. The project team had spent the past six months designing a new strategy to accelerate growth in a critical emerging market for a multibillion-dollar multinational. The summary document had that rare combination: a compelling long-term vision and a credible set of near-term actions addressing critical strategic unknowns.The last page of the 50-page document concluded the compelling story with a small request — four dedicated individuals for six months and $250,000 to conduct an in-market pilot. The project leader believed the modest request would translate into an easy yes.I could see the logic in that approach, but I feared it wasn't going to work the way she was expecting. In actual fact, I've found, saving "the ask" for the end of the document increases the risks of encountering a hidden enemy of innovation inside large companies: the "soft yes." This happens when executives get jazzed about a broad innovation strategy, nod their head vigorously in support of it, but stop short of committing real, tangible resources, however modest.It was the four dedicated people that were going to be the sticking point, I thought. You almost always can find money in someone's budget, or find creative ways around financial constraints to progress a new idea. But there are only so many hours in the day. Executives often hesitate to hire additional staff ("What happens if this doesn't work — then what do we do?" they say). They're equally reluctant to ask their best performers to shift from what are perceived to be critical tasks related to running the core business to risky innovation efforts.They're more comfortable asking busy people to add another item to their to-do list. But since most people's incentives are tied to delivering against the core business, they'll likely nod their heads and agree to help out — but prioritize the tasks they feel they're being paid to do over the pursuit of uncertain ideas.Thus, the soft yes — people agree (in principle) to your request, but they don't come through whole-heartedly. The net result is that innovation efforts limp along, making just enough progress to keep management intrigued, but not enough to have any material impact.One way to avoid the soft yes is to make your resource request clear early — within the first 10 minutes of any review meeting. Be specific. Then lay out the logic for the request. Detail the metrics that senior management can monitor as they watch their investment. Consider creating an exit strategy in case things don't go according to plan. If you are hiring new people, for example, perhaps they could be redeployed to other functions, if things don't pan out. Or maybe they could be brought on using temporary contracts. End your meeting by repeating the resource request. If you obtain verbal agreement, send a written summary to stakeholders to nail it down.This all might sound like overkill, but remember that companies left to their own devices will naturally default to executing today's business, not creating tomorrow's. Being clear in intent, consistent in your explanations, and persistent in getting formal agreement can ensure that you get the resources you need when you need them.More blog posts by Scott AnthonyMore on: Getting buy-in

SCOTT ANTHONYScott Anthony is the managing partner of the innovation and growth consulting firm.

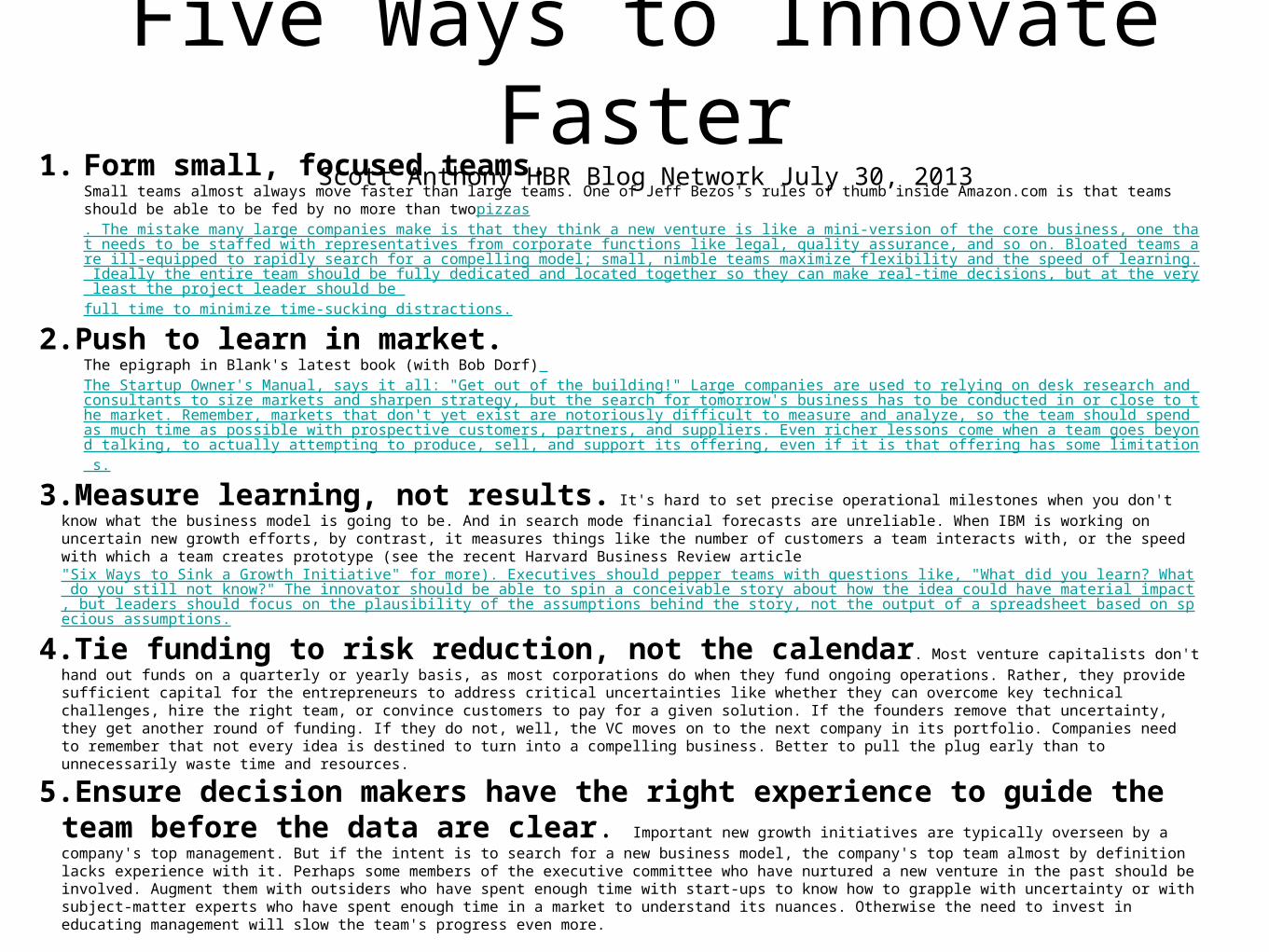

Five Ways to Innovate FasterScott Anthony HBR Blog Network July 30, 2013

1. Form small, focused teams. Small teams almost always move faster than large teams. One of Jeff Bezos's rules of thumb inside Amazon.com is that teams should be able to be fed by no more than two pizzas. The mistake many large companies make is that they think a new venture is like a mini-version of the core business, one that needs to be staffed with representatives from corporate functions like legal, quality assurance, and so on. Bloated teams are ill-equipped to rapidly search for a compelling model; small, nimble teams maximize flexibility and the speed of learning. Ideally the entire team should be fully dedicated and located together so they can make real-time decisions, but at the very least the project leader should be full time to minimize time-sucking distractions.

2.Push to learn in market. The epigraph in Blank's latest book (with Bob Dorf) The Startup Owner's Manual, says it all: "Get out of the building!" Large companies are used to relying on desk research and consultants to size markets and sharpen strategy, but the search for tomorrow's business has to be conducted in or close to the market. Remember, markets that don't yet exist are notoriously difficult to measure and analyze, so the team should spend as much time as possible with prospective customers, partners, and suppliers. Even richer lessons come when a team goes beyond talking, to actually attempting to produce, sell, and support its offering, even if it is that offering has some limitation s.

3.Measure learning, not results. It's hard to set precise operational milestones when you don't know what the business model is going to be. And in search mode financial forecasts are unreliable. When IBM is working on uncertain new growth efforts, by contrast, it measures things like the number of customers a team interacts with, or the speed with which a team creates prototype (see the recent Harvard Business Review article "Six Ways to Sink a Growth Initiative" for more). Executives should pepper teams with questions like, "What did you learn? What do you still not know?" The innovator should be able to spin a conceivable story about how the idea could have material impact, but leaders should focus on the plausibility of the assumptions behind the story, not the output of a spreadsheet based on specious assumptions.

4.Tie funding to risk reduction, not the calendar. Most venture capitalists don't hand out funds on a quarterly or yearly basis, as most corporations do when they fund ongoing operations. Rather, they provide sufficient capital for the entrepreneurs to address critical uncertainties like whether they can overcome key technical challenges, hire the right team, or convince customers to pay for a given solution. If the founders remove that uncertainty, they get another round of funding. If they do not, well, the VC moves on to the next company in its portfolio. Companies need to remember that not every idea is destined to turn into a compelling business. Better to pull the plug early than to unnecessarily waste time and resources.

5.Ensure decision makers have the right experience to guide the team before the data are clear. Important new growth initiatives are typically overseen by a company's top management. But if the intent is to search for a new business model, the company's top team almost by definition lacks experience with it. Perhaps some members of the executive committee who have nurtured a new venture in the past should be involved. Augment them with outsiders who have spent enough time with start-ups to know how to grapple with uncertainty or with subject-matter experts who have spent enough time in a market to understand its nuances. Otherwise the need to invest in educating management will slow the team's progress even more.

Here is one litmus test to gauge the degree to which you are following the approach I've just described. Ask the team the ratio of time spent preparing materials for management (or conducting desk research to feed into materials for management) versus time spent with customers, developing products, or talking to potential partners. If the ratio is higher than 1:3, you have a problem.These five pointers won't guarantee success. But following them will enable a team to discover as quickly as possible if there appears to be a viable path forward. If there is, then all the disciplines companies use to scale businesses typically prove helpful (unless the model that emerges has stark differences with the core business — but that's a different post). If there isn't, then at least the company learned that quickly and can move on to the next idea.