Embed Size (px)

DESCRIPTION

Metal Bulletin Research's Senior Metals Analyst Atilla Widnell discusses the developments in DRI/HBI production and trade in the rest of the world. He also looks into the key growth areas/regions for future production.

Citation preview

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 1 1

AMM DRI & Mini-mills Conference

DRI explored – how is DRI being utilised globally?

10-11 September 2013, New Orleans, LA

Atilla Widnell Senior Metals Analyst

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 2

Disclaimer:

Prices and other information contained in this presentation have been obtained by us from various sources believed to be reliable. This

information has not been independently verified by us. Those prices and price indices that are evaluated or calculated by us represent an

approximate evaluation of current levels based upon dealings (if any) that may have been disclosed prior to publication to us. Such prices are

collated through regular contact with producers, traders, dealers, brokers and purchasers although not all market segments may be contacted

prior to the evaluation, calculation, or publication of any specific price or index. Actual transaction prices will reflect quantities, grades and

qualities, credit terms, and many other parameters. The prices are in no sense comparable to the quoted prices of commodities in which a

formal futures market exists.

Evaluations or calculations of prices and price indices by us are based upon certain market assumptions and evaluation methodologies, and

may not conform to prices or information available from third parties. There may be errors or defects in such assumptions or methodologies

that cause resultant evaluations to be inappropriate for use. Your use or reliance on any prices or other information published by us is at your

sole risk. Neither we nor any of our providers of information make any representations or warranties, express or implied as to the accuracy,

completeness or reliability of any advice, opinion, statement or other information forming any part of the published information or its fitness or

suitability for a particular purpose or use. Neither we, nor any of our officers, employees or representatives shall be liable to any person for any

losses or damages incurred, suffered or arising as a result of use or reliance on the prices or other information contained in this publication,

howsoever arising, including but not limited to any direct, indirect, consequential, punitive, incidental, special or similar damage, losses or

expenses.

We are not an investment advisor, a financial advisor or a securities broker. The information published has been prepared solely for

informational and educational purposes and is not intended for trading purposes or to address your particular requirements. The information

provided is not an offer to buy or sell or a solicitation of an offer to buy or sell any security, commodity, financial product, instrument or other

investment or to participate in any particular trading strategy. Such information is intended to be available for your general information and is

not intended to be relied upon by users in making (or refraining from making) any specific investment or other decisions. Your investment

actions should be solely based upon your own decisions and research and appropriate independent advice should be obtained from a suitably

qualified independent advisor before making any such decision.

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 3

Introduction

Latest Developments

Forecasts

Conclusions

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 4

• Introduction

• Latest Developments:

• What are the developments in DRI/HBI production and trade in the rest of the world?

• Forecasts:

• Where are the key growth areas/regions for future production?

• How will growth of DRI/HBI production effect scrap demand in key regions?

• What consequence will this have on scrap & metallics trade as a result?

• What will be the impact on international DRI/HBI and metallics prices?

• Conclusions

• New MBR products:

• MBR Steel Scrap & Metallics Forecaster

• Strategic Outlook to the Global Ferrous Scrap Industry out to 2021

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 5

Introduction

Latest Developments

Forecasts

Conclusions

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 6

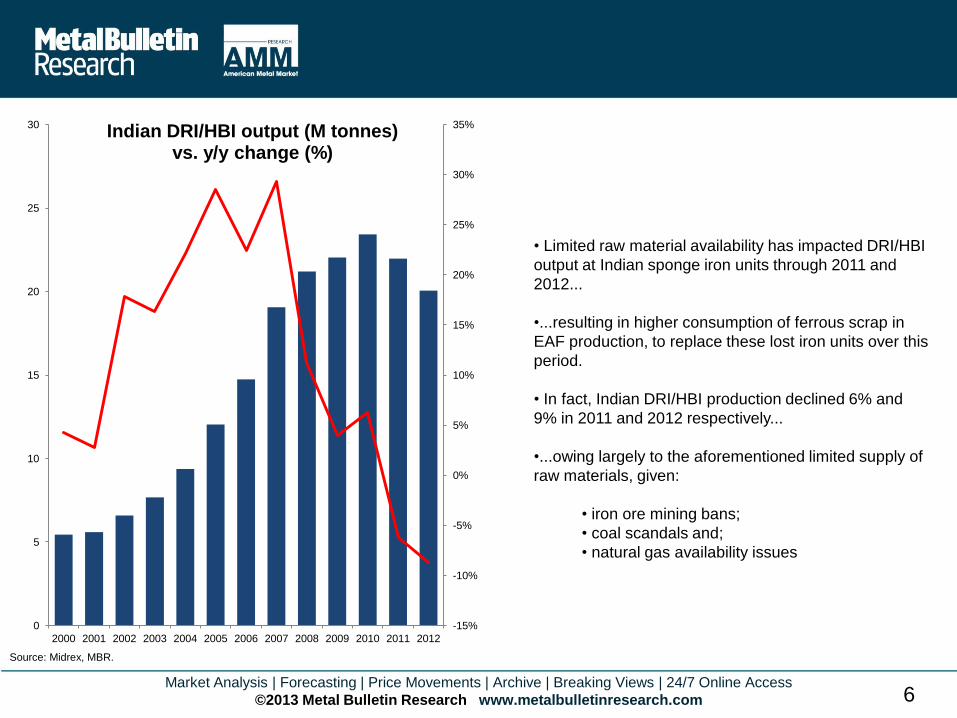

Source: Midrex, MBR.

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0

5

10

15

20

25

30

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Indian DRI/HBI output (M tonnes) vs. y/y change (%)

• Limited raw material availability has impacted DRI/HBI

output at Indian sponge iron units through 2011 and

2012...

•...resulting in higher consumption of ferrous scrap in

EAF production, to replace these lost iron units over this

period.

• In fact, Indian DRI/HBI production declined 6% and

9% in 2011 and 2012 respectively...

•...owing largely to the aforementioned limited supply of

raw materials, given:

• iron ore mining bans;

• coal scandals and;

• natural gas availability issues

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 7

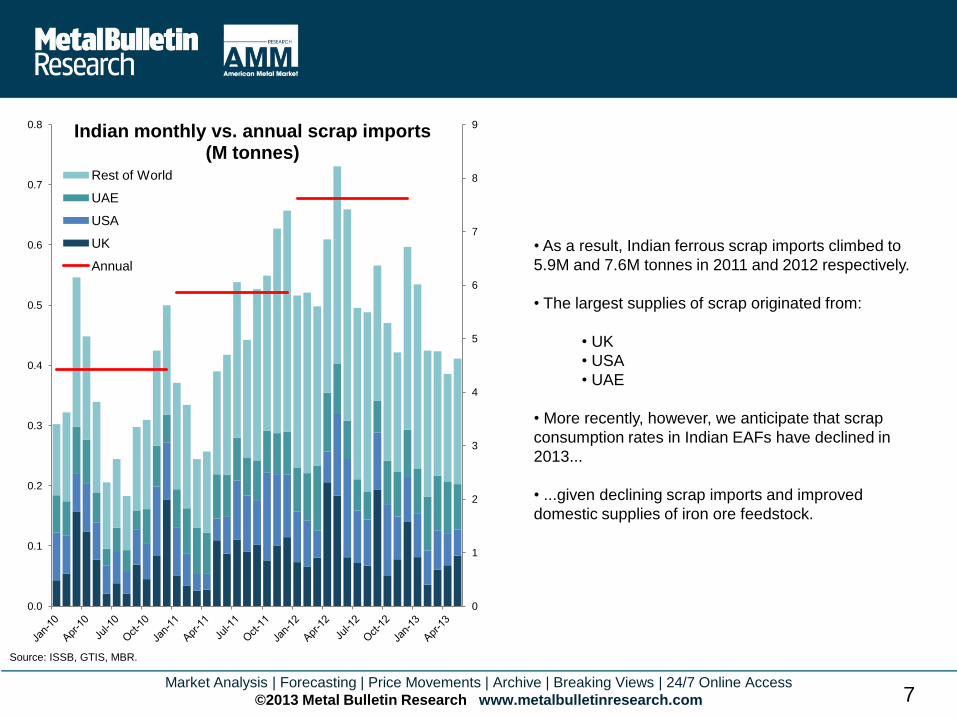

Source: ISSB, GTIS, MBR.

• As a result, Indian ferrous scrap imports climbed to

5.9M and 7.6M tonnes in 2011 and 2012 respectively.

• The largest supplies of scrap originated from:

• UK

• USA

• UAE

• More recently, however, we anticipate that scrap

consumption rates in Indian EAFs have declined in

2013...

• ...given declining scrap imports and improved

domestic supplies of iron ore feedstock.

0

1

2

3

4

5

6

7

8

9

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8 Indian monthly vs. annual scrap imports

(M tonnes) Rest of World

UAE

USA

UK

Annual

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 8

Source: Bloomberg.

Rs40

Rs45

Rs50

Rs55

Rs60

Rs65

Rs70

Rs75

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13

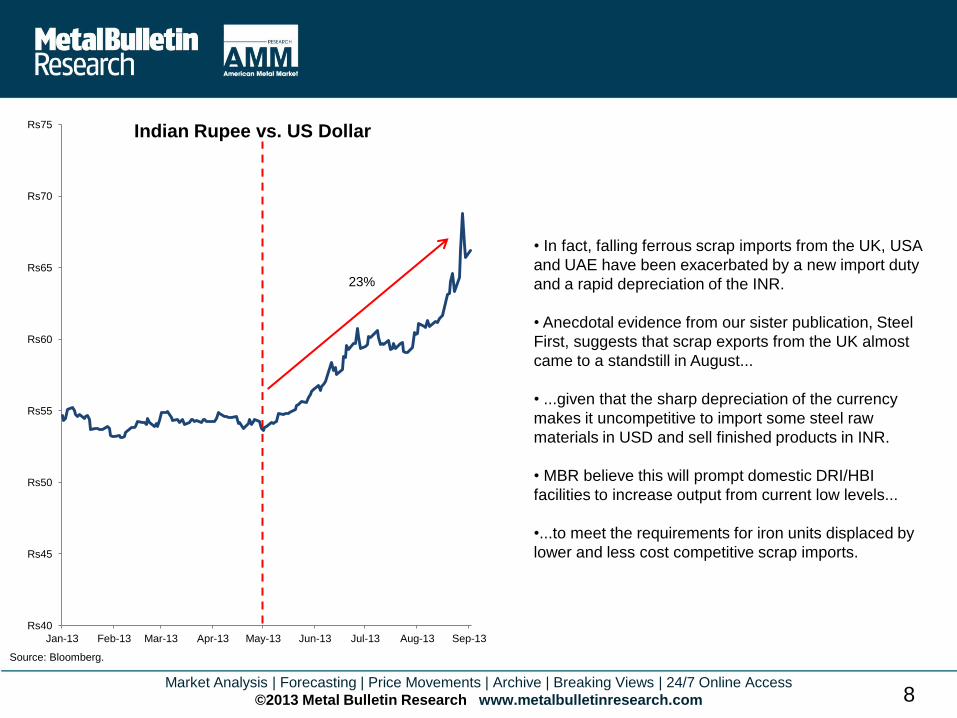

Indian Rupee vs. US Dollar

23%

• In fact, falling ferrous scrap imports from the UK, USA

and UAE have been exacerbated by a new import duty

and a rapid depreciation of the INR.

• Anecdotal evidence from our sister publication, Steel

First, suggests that scrap exports from the UK almost

came to a standstill in August...

• ...given that the sharp depreciation of the currency

makes it uncompetitive to import some steel raw

materials in USD and sell finished products in INR.

• MBR believe this will prompt domestic DRI/HBI

facilities to increase output from current low levels...

•...to meet the requirements for iron units displaced by

lower and less cost competitive scrap imports.

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 9

Source: MBR, GTIS, ISSB.

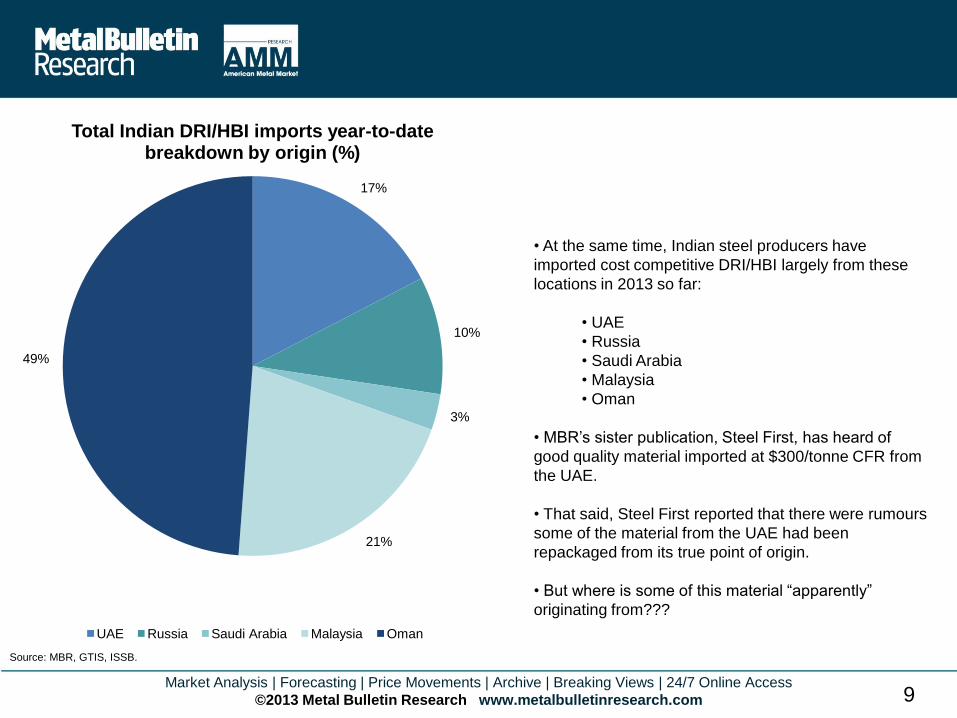

• At the same time, Indian steel producers have

imported cost competitive DRI/HBI largely from these

locations in 2013 so far:

• UAE

• Russia

• Saudi Arabia

• Malaysia

• Oman

• MBR’s sister publication, Steel First, has heard of

good quality material imported at $300/tonne CFR from

the UAE.

• That said, Steel First reported that there were rumours

some of the material from the UAE had been

repackaged from its true point of origin.

• But where is some of this material “apparently”

originating from???

17%

10%

3%

21%

49%

Total Indian DRI/HBI imports year-to-date breakdown by origin (%)

UAE Russia Saudi Arabia Malaysia Oman

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 10

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 11

Source: ISSB, MBR.

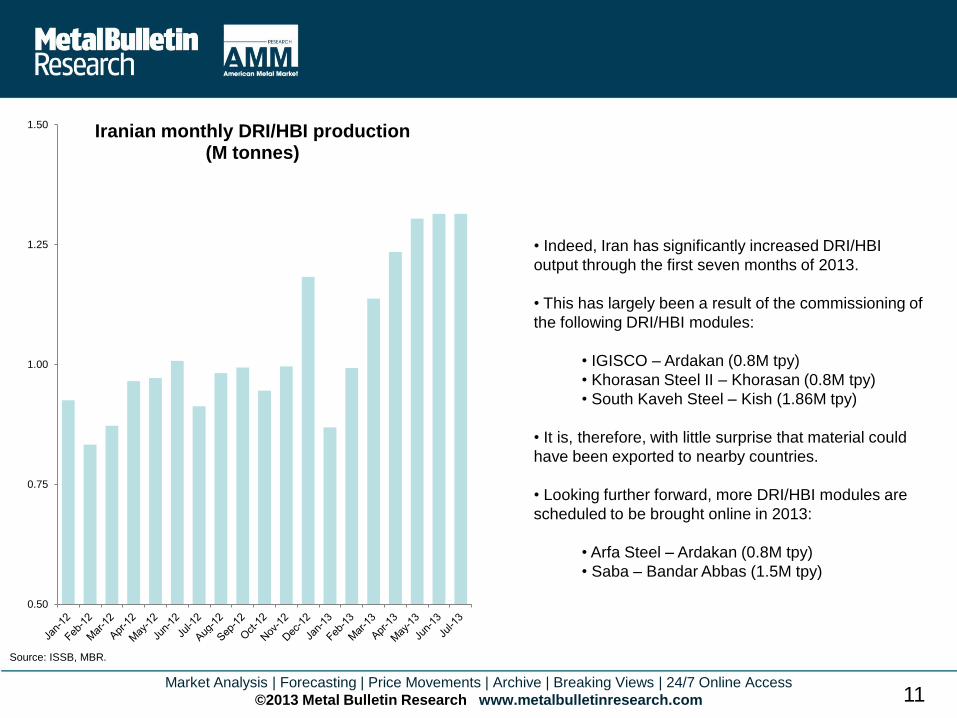

• Indeed, Iran has significantly increased DRI/HBI

output through the first seven months of 2013.

• This has largely been a result of the commissioning of

the following DRI/HBI modules:

• IGISCO – Ardakan (0.8M tpy)

• Khorasan Steel II – Khorasan (0.8M tpy)

• South Kaveh Steel – Kish (1.86M tpy)

• It is, therefore, with little surprise that material could

have been exported to nearby countries.

• Looking further forward, more DRI/HBI modules are

scheduled to be brought online in 2013:

• Arfa Steel – Ardakan (0.8M tpy)

• Saba – Bandar Abbas (1.5M tpy)

0.50

0.75

1.00

1.25

1.50 Iranian monthly DRI/HBI production

(M tonnes)

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 12

Source: ISSB, MBR (deduced).

0.00

0.05

0.10

0.15

0.20

0.25

0.30 Venezuelan monthly DRI/HBI exports

(M tonnes)

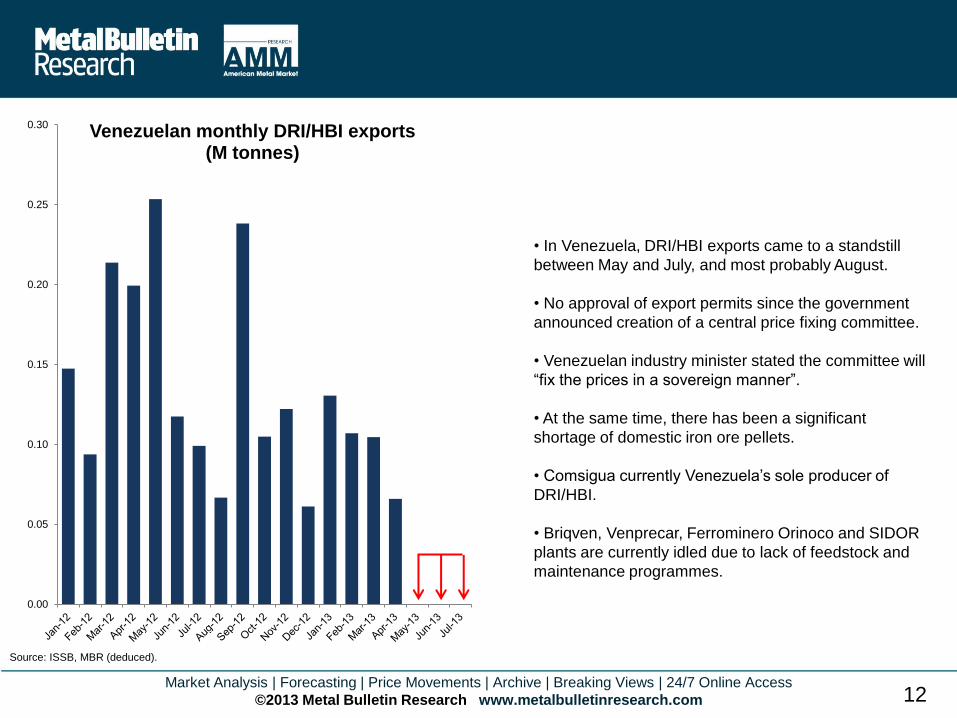

• In Venezuela, DRI/HBI exports came to a standstill

between May and July, and most probably August.

• No approval of export permits since the government

announced creation of a central price fixing committee.

• Venezuelan industry minister stated the committee will

“fix the prices in a sovereign manner”.

• At the same time, there has been a significant

shortage of domestic iron ore pellets.

• Comsigua currently Venezuela’s sole producer of

DRI/HBI.

• Briqven, Venprecar, Ferrominero Orinoco and SIDOR

plants are currently idled due to lack of feedstock and

maintenance programmes.

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 13

Source: World Steel Association, MBR.

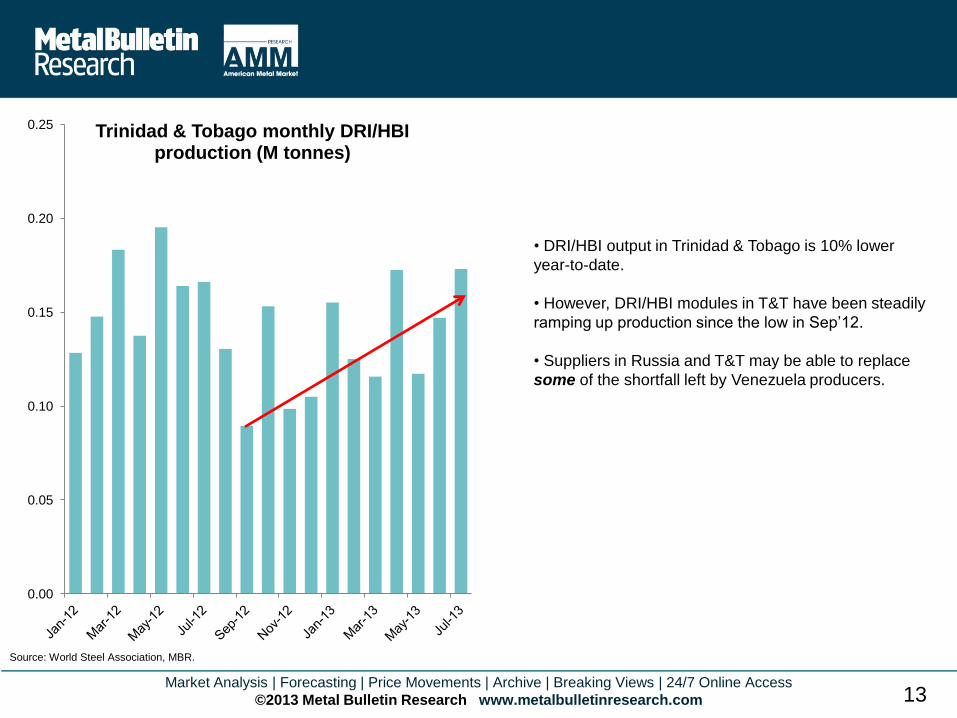

• DRI/HBI output in Trinidad & Tobago is 10% lower

year-to-date.

• However, DRI/HBI modules in T&T have been steadily

ramping up production since the low in Sep’12.

• Suppliers in Russia and T&T may be able to replace

some of the shortfall left by Venezuela producers.

0.00

0.05

0.10

0.15

0.20

0.25 Trinidad & Tobago monthly DRI/HBI production (M tonnes)

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 14

Introduction

Latest Developments

Forecasts

Conclusions

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 15

Source: ISSB, GTIS, MBR.

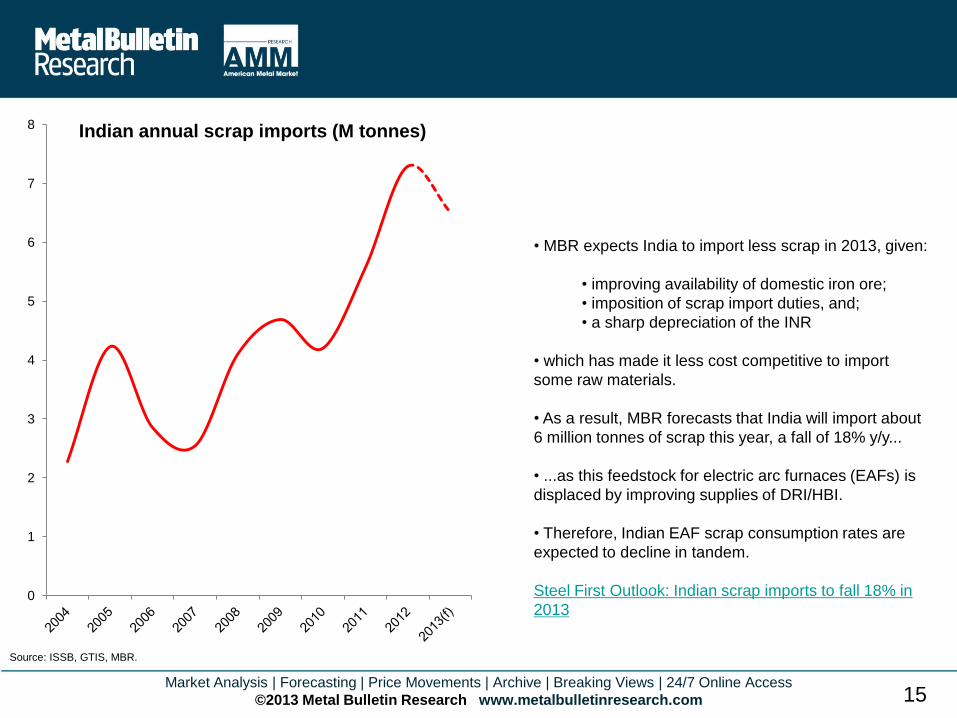

• MBR expects India to import less scrap in 2013, given:

• improving availability of domestic iron ore;

• imposition of scrap import duties, and;

• a sharp depreciation of the INR

• which has made it less cost competitive to import

some raw materials.

• As a result, MBR forecasts that India will import about

6 million tonnes of scrap this year, a fall of 18% y/y...

• ...as this feedstock for electric arc furnaces (EAFs) is

displaced by improving supplies of DRI/HBI.

• Therefore, Indian EAF scrap consumption rates are

expected to decline in tandem.

Steel First Outlook: Indian scrap imports to fall 18% in

2013 0

1

2

3

4

5

6

7

8 Indian annual scrap imports (M tonnes)

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 16

Source: Midrex, MBR.

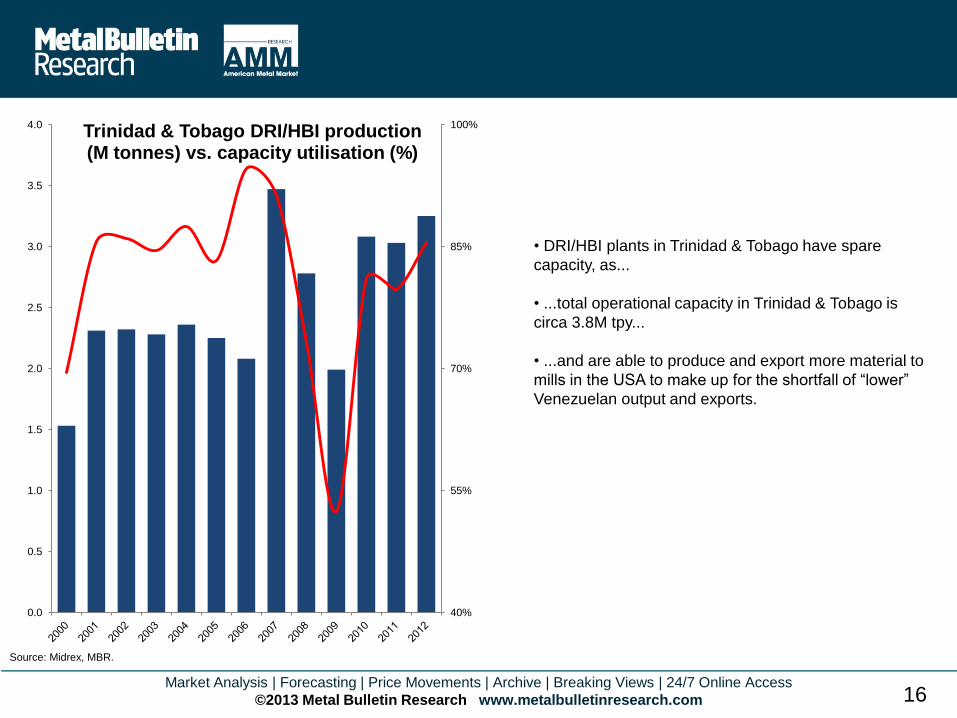

• DRI/HBI plants in Trinidad & Tobago have spare

capacity, as...

• ...total operational capacity in Trinidad & Tobago is

circa 3.8M tpy...

• ...and are able to produce and export more material to

mills in the USA to make up for the shortfall of “lower”

Venezuelan output and exports.

40%

55%

70%

85%

100%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0 Trinidad & Tobago DRI/HBI production (M tonnes) vs. capacity utilisation (%)

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 17

Source: ISSB, GTIS, MBR.

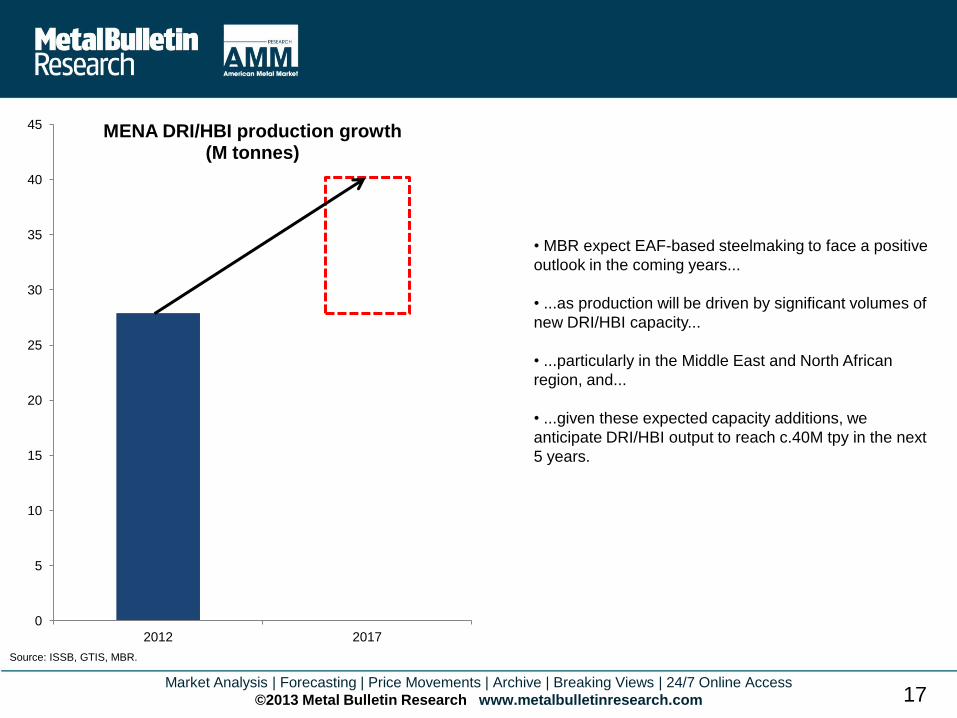

• MBR expect EAF-based steelmaking to face a positive

outlook in the coming years...

• ...as production will be driven by significant volumes of

new DRI/HBI capacity...

• ...particularly in the Middle East and North African

region, and...

• ...given these expected capacity additions, we

anticipate DRI/HBI output to reach c.40M tpy in the next

5 years.

0

5

10

15

20

25

30

35

40

45

2012 2017

MENA DRI/HBI production growth (M tonnes)

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 18

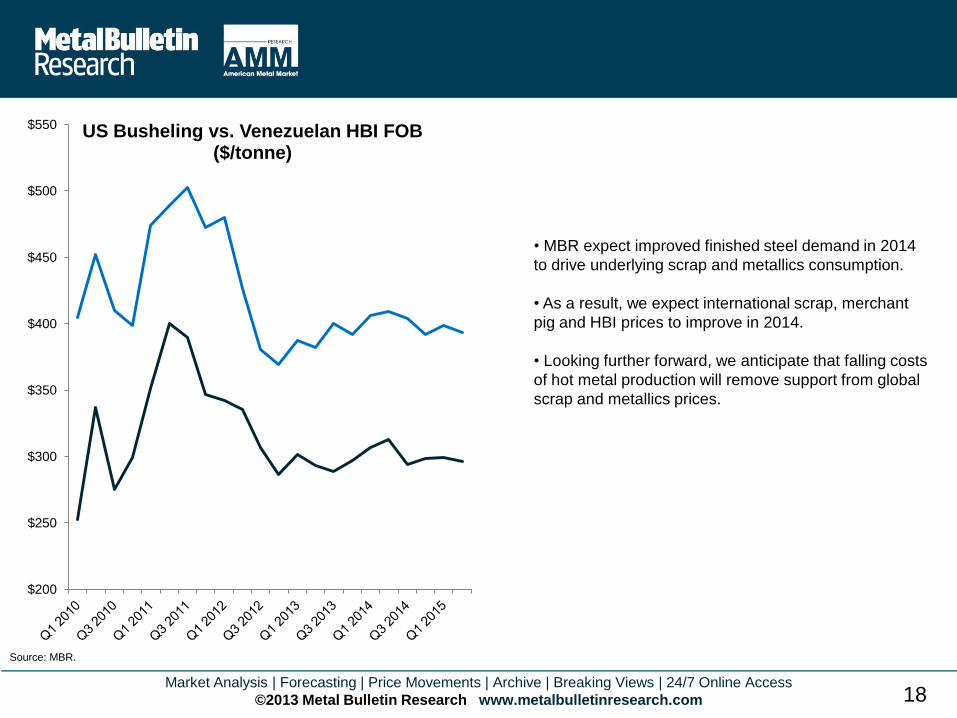

Source: MBR.

• MBR expect improved finished steel demand in 2014

to drive underlying scrap and metallics consumption.

• As a result, we expect international scrap, merchant

pig and HBI prices to improve in 2014.

• Looking further forward, we anticipate that falling costs

of hot metal production will remove support from global

scrap and metallics prices.

$200

$250

$300

$350

$400

$450

$500

$550 US Busheling vs. Venezuelan HBI FOB ($/tonne)

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 19

Introduction

Latest Developments

Forecasts

Conclusions

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 20

• Conclusions:

• Where are the key growth areas/regions for future production?

• Middle East North Africa (Egypt, Iran, Qatar & Saudi Arabia) and India

• How will growth of DRI/HBI production effect scrap demand in key regions?

• Lower scrap consumption rates in EAF steelmaking

• What consequence will this have on scrap & metallics trade as a result?

• Lower scrap and metallics imports in some regions

• What will be the impact on international DRI/HBI and metallics prices?

• DRI/HBI and merchant pig iron prices will continue to track scrap prices

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 21

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 22

• Metal Bulletin Research (MBR) has published a

timely study, A Strategic Outlook to the Global

Ferrous Scrap Industry out to 2021, providing

valuable global information, expert analysis and

forecasting for this important industry.

• The study provides unparalleled industry knowledge

from a team of experts who have a high level of

experience in economics and metallurgy.

• PLUS a dynamic scrap supply/demand model

enabling you to run your own scenarios by country.

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 23

Thank you for your attention

Questions & Answers

Market Analysis | Forecasting | Price Movements | Archive | Breaking Views | 24/7 Online Access

©2013 Metal Bulletin Research www.metalbulletinresearch.com 24

Contact details for further information:

Metal Bulletin Research

Nestor House, Playhouse Yard, London EC4V 5EX

+44 (0)20 7779 7999

Atilla Widnell

Senior Metals Analyst

+44 (0)20 7827 6480