Embed Size (px)

Citation preview

COMPETITION AUTHORITIES AND FINANCIAL REGULATORS: SOME ISSUES AND VIEW FROM BRAZIL MÁRCIO ISSAO NAKANE ECONOMICS DEPARTMENT, UNIVERSITY OF SÃO PAULO

PRESENTATION GIVEN AT THE FIFTEENTH ANNUAL MEETING OF THE LATIN AMERICAN AND CARIBBEAN COMPETITION FORUM (LACCF) – SESSION III – ‘ADDRESSING COMPETITION CHALLENGES IN FINANCIAL MARKETS’

MANAGUA – 5 APRIL, 2017

THIS TALK

• A case for effective cooperation between competition authorities and financial regulators

• Two examples from Brazil: • Lack of cooperation: merger reviews • Effective cooperation: payment cards

WHY EFFECTIVE COOPERATION IS SO RELEVANT • Robert Mundell, the 1999 Economics Nobel Prize winner, introduced the principle of

effective market classification in 1960. According to this principle, the economic system works better if each policy instrument is allocated to the variables upon which they have more influence. His analysis was in the context of comparing different exchange rate arrangements (fixed vs. flexible). But his framework is also useful in the present context.

• Competition authorities have expertise in reviewing mergers and in dealing with anticompetitive behavior applied to different markets, sectors, and circumstances. They have knowledge of the best practice cutting edge methodologies and techniques available to undertake their tasks.

• Financial regulators have deep knowledge on the workings and intricacies of financial markets and financial products and services. Access to detailed data is usually subject to confidentiality issues.

• Comparative advantages of competition authorities and financial regulators have to be maximized: gains of specialization (Mundell’s argument).

WHY EFFECTIVE COOPERATION IS SO RELEVANT

• Financial industry is a complex one and changing all the time (very dynamic). It is heavily regulated and competition issues in such markets are far from trivial.

• Landscape of competition in financial markets: • Financial innovations, role of information technology • Internet banking, mobile banking, big data • Peer-to-peer, crowdfunding • Platforms, network externalities (e.g. payments) • Systemic risk, financial stabilization, too big to fail, contagion

• In such complex environment, cooperation allows for sharing the benefits of the comparative advantages of each agency: economies of scope.

LACK OF COOPERATION: FINANCIAL SECTOR MERGER REVIEWS IN BRAZIL

• Origin of the problem is an apparent conflict between the banking law from 1964 and the competition law from 1994 and 2011 (new law).

• Banking law asserts the Central Bank authority on issues related to M&As in the financial sector. Moreover, it gives the Central Bank the mandate to “regulate the conditions of competition between financial institutions”.

• Competition law, on the other hand, assigns to CADE the function of analyzing M&As and care for competition issues, without distinction as to their nature.

• A compromise was agreed giving the Central Bank the authority to review mergers when systemic risk is an issue.

• Final position from the Supreme Court is still pending.

LACK OF COOPERATION: FINANCIAL SECTOR MERGER REVIEWS IN BRAZIL

• This situation is far from ideal, creating legal uncertainty for the concerned players: • Bradesco-BCN merger in 2001 was not submitted to CADE. Bradesco was fined as a result. • Itau-Unibanco merger in 2008: only non-financial operations (securities brokerage,

insurance, credit cards) were submitted to CADE. • More recent M&As (Banco do Brasil-Nossa Caixa; Bradesco-HSBC) were submitted to

CADE.

LACK OF COOPERATION: FINANCIAL SECTOR MERGER REVIEWS IN BRAZIL • Bradesco-HSBC illustrates why lack of cooperation may be an issue in the analysis:

• Merger between the 4th and 6th largest commercial banks in Brazil. • CADE’s General Superintendence analysis of the case: very detailed account of the banking

sector and of the proposed merger. • Public available version:

http://sei.cade.gov.br/sei/institucional/pesquisa/documento_consulta_externa.php?8b7ordf_KdjqNE7xXQyIT8ywVE20IstN0KvraVhk2Pdu0JmyScJG7yscsiknowgJxvnI3g2qMrUOm3H4HELqKw,,

• But the lack of specific knowledge about the workings of the financial sector left some important gaps in the report. Two examples:

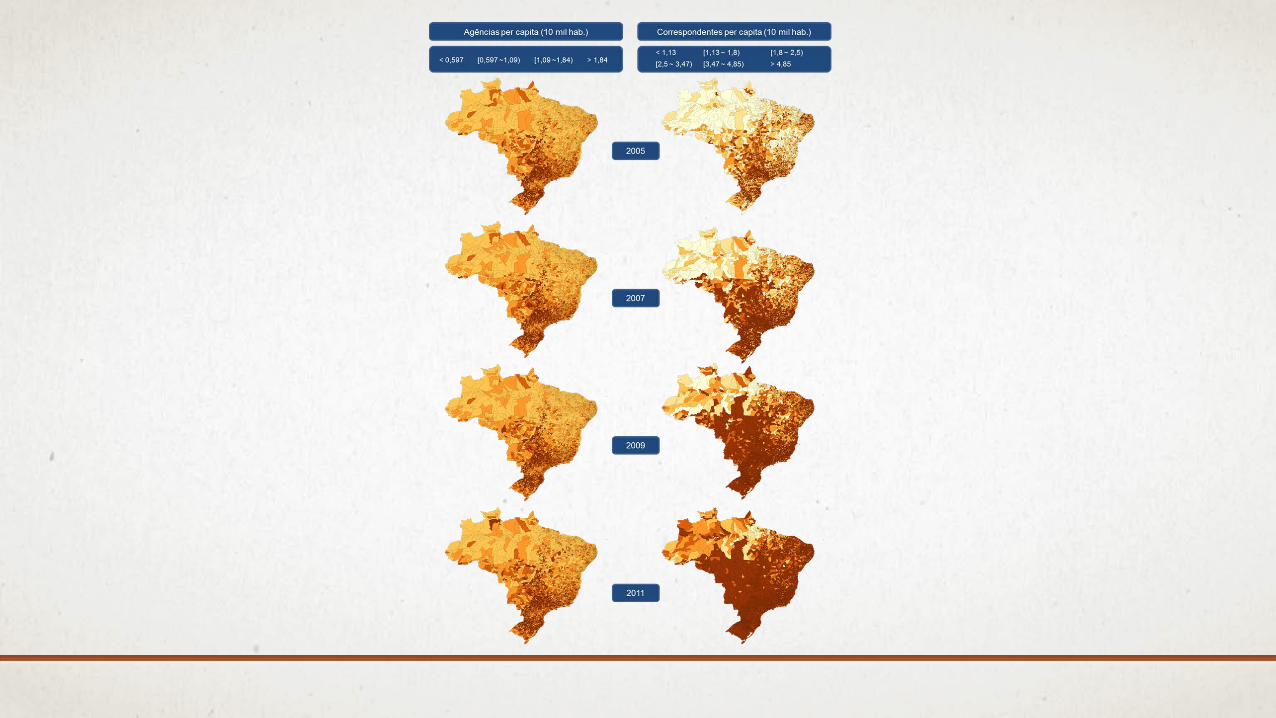

• Example 1: Importance of a network of branches is pointed out as one of the main entry barriers in the sector. Moreover, market concentration in local markets (municipal level) was evaluated through the presence of branches.

• This analysis completely ignores the competitive impact of bank correspondents. Bank correspondents are nonfinancial or financial firms hired by financial institutions to offer some financial services. E.g., lottery houses, post offices.

• Number of bank correspondents grew from 63,509 in 2000 to 346,502 in 2014, a staggering 446% increase. For reference, in the same period, bank branches grew from 16,396 to 23,126, an increase of 41%.

BANK CORRESPONDENTS IN BRAZIL

LACK OF COOPERATION: FINANCIAL SECTOR MERGER REVIEWS IN BRAZIL • Bradesco-HSBC : Example 2:

• Unilateral effects of the merger are assessed through the application of UPP (Upward Pricing Pressure) and GUPPI (Gross Upward Price Pressure Index) tests. Coordinated effects are assessed through the application of the CPPI (Coordinated Price Pressure Index) test.

• Such tests are at the frontier of the techniques available to the competition authorities for the evaluation of mergers.

• The application of these tests requires the definition of the relevant products or basket of products/services. For the Bradesco-HSBC case, tests were separately applied to the following baskets of financial services : • C1: Demand Deposits + Savings Accounts • C2: Demand Deposits + Free Loans • C3: Demand Deposits + Savings Accounts + Free Loans • C4: Demand Deposits + Savings Accounts + Free Loans +Credit Card • C5: Demand Deposits + Savings Accounts + Free Loans + Credit Card + Personal Insurance • C6: Demand Deposits + Free Loans + Credit Card • C7: Demand Deposits + Savings Accounts + Credit Card

LACK OF COOPERATION: FINANCIAL SECTOR MERGER REVIEWS IN BRAZIL

• Bradesco-HSBC : • Problem is that these tests assume that firms compete in prices (Bertrand competition)

and demand deposits pay no interest. Also, savings accounts interest rates are not set by the bank but by law. So, none of the reported tests can convey any information on unilateral or coordinated effects for the case.

• Again, lack of simple knowledge of the workings of the banking industry just jeopardized the whole analysis.

• Cooperation would definitely improve the analysis.

EFFECTIVE COOPERATION: RETAIL PAYMENT CARDS

• In July 2006, the Central Bank of Brazil and the country’s competition authorities signed a cooperation agreement to study the local payment card industry.

• Special database was assembled as part of the agreement.

• Detailed market study was published in 2010. This study pointed out some competitive concerns. For example, in the acquiring activity.

• Legislation and regulation were put in place to deal with such competitive issues.

• Main statistics of the sector are continuously updated by the Central Bank.

EFFECTIVE COOPERATION: RETAIL PAYMENT CARDS • Ex post evaluation: Gabriel Garber and Márcio I. Nakane, The break of brand

exclusivity in Brazilian credit card acquiring: effects and markup-cost decomposition in a price dispersion setting, Central Bank of Brazil Working Paper 390, July 2015 (http://www.bcb.gov.br/pec/wps/ingl/wps390.pdf)

• The gathering of detailed data allowed us to study the effect of a change in policy undertaken in 2010 ending the exclusivity in the acquiring activity. Prior to the change, the acquiring activity was dominated by only two firms: Cielo , that had an exclusivity contract to acquire merchants for the Visa scheme, and Redecard, that although lacking a similar contractual position, in fact monopolized MasterCard acquiring.

• We document that the intervention produced a price reduction mainly explained by a markup decrease, which we interpret as an increase in competition. We find a reduction of 14.2 percent points on an average margin of 62% over marginal cost, representing a reduction of almost 23% of that measure.

PAYMENT CARDS

Merchant

Brand

Issuer Acquirer

P

P - IF

P-DR

Cardholder

Goods

Annual fee

Rent/ connectivity

fees fees

AVERAGE MERCHANT DISCOUNT RATE IN THE BRAZILIAN CREDIT CARD INDUSTRY

2.50

2.55

2.60

2.65

2.70

2.75

2.80

2.85

2.90

2.95

3.00

3.05

3.10

2006/1 2006/4 2007/3 2008/2 2009/1 2009/4 2010/3 2011/2 2012/1 2012/4

%