Embed Size (px)

Citation preview

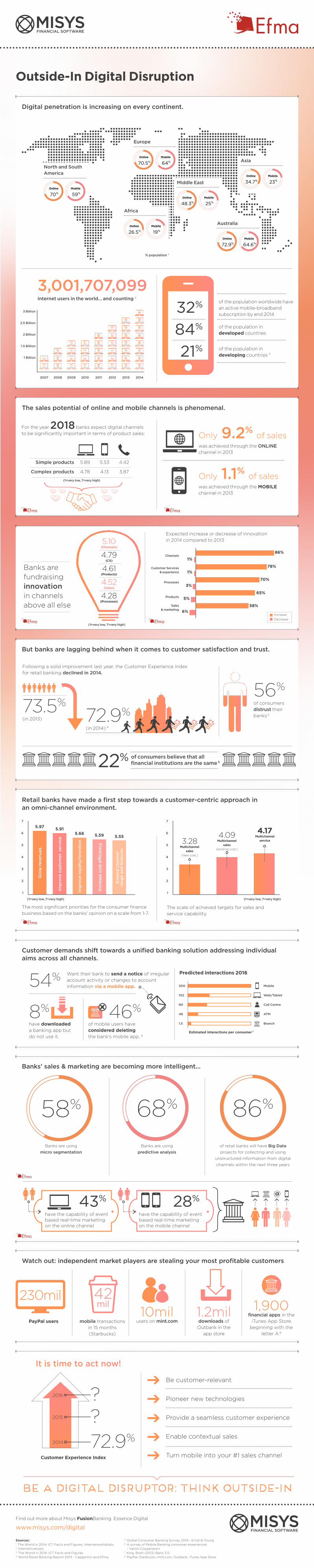

Outside-In Digital Disruption

Digital penetration is increasing on every continent.

The sales potential of online and mobile channels is phenomenal.

Retail banks have made a first step towards a customer-centric approach in an omni-channel environment.

The most significant priorities for the consumer finance business based on the banks’ opinion on a scale from 1-7.

The scale of achieved targets for sales and service capability.

It is time to act now!

Be a Digital Disruptor: Think Outside-In

But banks are lagging behind when it comes to customer satisfaction and trust.

Customer demands shift towards a unified banking solution addressing individual aims across all channels.

Banks’ sales & marketing are becoming more intelligent...

Watch out: independent market players are stealing your most profitable customers

3,001,707,09932%

84%

21%

73.5% (in 2013) 72.9%

(in 2014) 4

54%

72.9%

??

8% 46%

56% of consumers distrust their banks 5

22%

North and South America

% population 1

Africa

Middle East

Asia

Australia

Europe

70%

Online

59%

Mobile

26.5%

Online

19%

Mobile

48.3%

Online

25%

Mobile

70.5%

Online

64%

Mobile

34.7%

Online

23%

Mobile

72.9%

Online

64.6%

Mobile

20142010 20132009 2012201120082007

3 Billion

2.5 Billion

2 Billion

1.5 Billion

1 Billion

Internet users in the world... and counting 2

was achieved through the ONLINE channel in 2013

was achieved through the MOBILE channel in 2013

For the year 2018 banks expect digital channels to be significantly important in terms of product sales:

Banks are fundraising innovation in channels above all else

Expected increase or decrease of innovation in 2014 compared to 2013

of the population worldwide have an active mobile-broadband subscription by end 2014

of the population in developed countries

of the population in developing countries 3

Following a solid improvement last year, the Customer Experience Indexfor retail banking declined in 2014.

of consumers believe that all financial institutions are the same 5

of mobile users have considered deleting the bank’s mobile app. 6

Mobile300

Web/Tablet102

Call Centre90

ATM48

Branch1.5

Predicted interactions 2016Want their bank to send a notice of irregular account activity or changes to account information via a mobile app.

have downloaded a banking app but do not use it.

Banks are using micro segmentation

Banks are using predictive analysis

have the capability of event based real-time marketing on the online channel

have the capability of event based real-time marketing on the mobile channel

of retail banks will have Big Data projects for collecting and using

unstructured information from digital channels within the next three years

230mil 42mil

PayPal users

Customer Experience Index

mobile transactions in 15 months (Starbucks)

10mil users on mint.com

1.2mil downloads of Outbank in the

app store

1,900 financial apps in the

iTunes App Store beginning with the

letter A 8

2014

2015

2016

Be customer-relevant

Pioneer new technologies

Provide a seamless customer experience

Enable contextual sales

Turn mobile into your #1 sales channel

Sources: 1. The World in 2014: ICT Facts and Figures, Internetworldstats 2. Internetlivestats3. The World in 2014: ICT Facts and Figures4. World Retail Banking Report 2014 - Capgemini and Efma

5. Global Consumer Banking Survey 2014 - Ernst & Young6. A survey of Mobile Banking consumer experiences - Varolii Cooperation7. King, Brett (2013) Bank 3.08. PayPal, Starbucks, mint.com, Outbank, iTunes App Store

7 7

5.97 5.915.66 5.59 5.55

6 6

3 3

5 5

2 2

4 4

1 1

Gro

w re

venu

es

Imp

rove

cus

tom

er s

ervi

ce

Imp

rove

loya

lty/

rete

ntio

n

Incr

ease

co

st e

ffici

ency

Ext

end

cha

nnel

ra

nge

and

feat

ures

4.17Multichannel

service4.09

Multichannel sales

(existing cust.)

3.28Multichannel

sales(new cust.)

Simple products

Complex products

5.89

4.78

5.53

4.13

4.42

3.87

5.10(Channels)

4.79(CX)

4.61(Products)

4.52(Sales)

4.28(Processes)

IncreaseDecrease

65%5%

58%6%

86%1%

78%1%

70%3%

58%

43% 28%

68% 86%

(1=very low, 7=very high)

(1=very low, 7=very high)

(1=very low, 7=very high)

(1=very low, 7=very high)

Estimated interactions per consumer 7

Only 9.2% of sales

Only 1.1% of sales

Find out more about Misys FusionBanking Essence Digital

www.misys.com/digital

![Tips for Creating the Perfect Infographic [Infographic]](https://img.pdfslide.net/doc/110x75/58a64df11a28ab6e368b61e7/tips-for-creating-the-perfect-infographic-infographic.jpg)