Embed Size (px)

Citation preview

Improving mobile coverage

and choice

Dan Lloyd

Director of Strategy & Corporate Affairs

• 21 April 2015

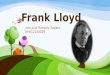

The new Vodafone

• +$3bn investment has delivered a new world class network.

• 40% larger regional footprint since 2010.

• More than two million 4G customers.

• TIO complaints down 50% in 12 months.

• Return to customer and revenue growth

Vodafone driving innovation & competition

wherever possible

3

• Worry free plans: Infinite calling,

international minutes, data workout,

$5/day international roaming.

• Content: Stan, Fairfax and Spotify.

• Local care: $12m Hobart Centre

make us one of the largest private

employers in Tasmania.

• Retail expansion: 30 new stores in

Q4 2014 - one of the largest retail

expansions in Australian history.

• Delivering value: Expanding into

business.

Imitation is the best form of flattery

July, 2013 – Vodafone launches $5-a-day

international roaming

August 2013 – Optus introduces

$10 flat-price travel pack (limited data)

September 2013 – Telstra cuts the cost of

roaming

December, 2014 – Telstra launches

International Travel Pass

Vodafone still the market leader

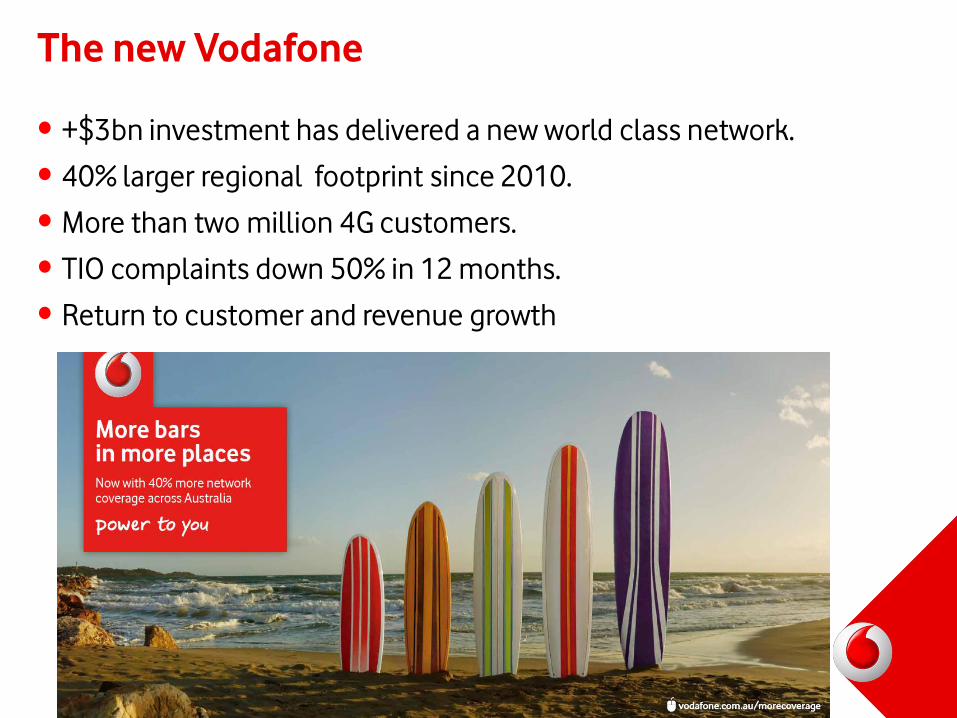

The mobile revolution has just begun…

Source: Google Our Mobile Planet 2014

Great competition and choice for

metropolitan mobile customers:

•Mobiles delivering $33bn to

the Australian economy.

•Very high smartphone

penetration.

•Three large high quality 4G

networks.

•Good price levels.

•Game changing opportunities:

•Machine to Machine

•M-Commerce via NFC.

50.00%

55.00%

60.00%

65.00%

70.00%

75.00%

Smartphone Penetration

4

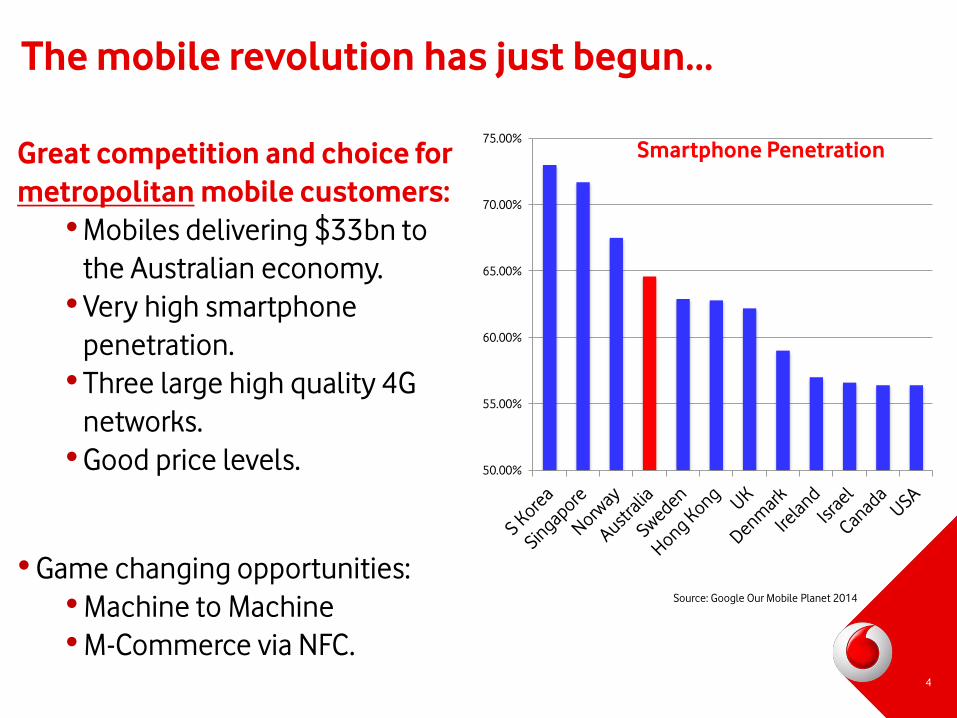

Regional Australia: Not just about

coverage, its about choice

6

•Australia has one of the most

distorted regional mobile markets

in the world. Very high market shares

for the incumbent in the 70-98.5%

marginal areas.

•Monopoly for 1 million km2.

of regional

consumers agree that

a choice of mobile

provider is important

83%

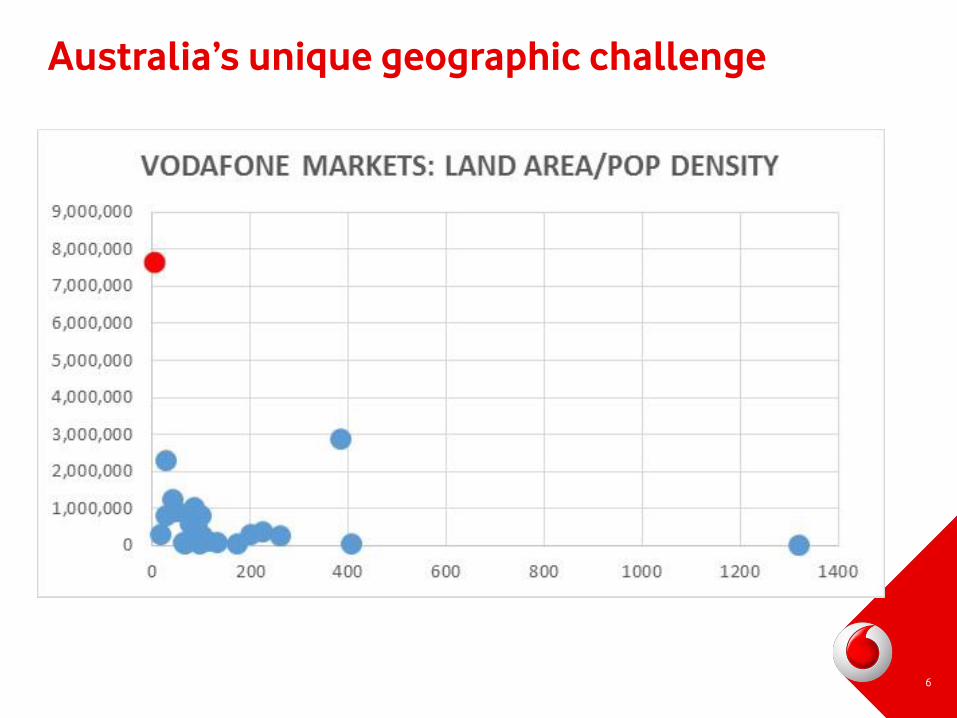

Australia’s unique geographic challenge

6

7

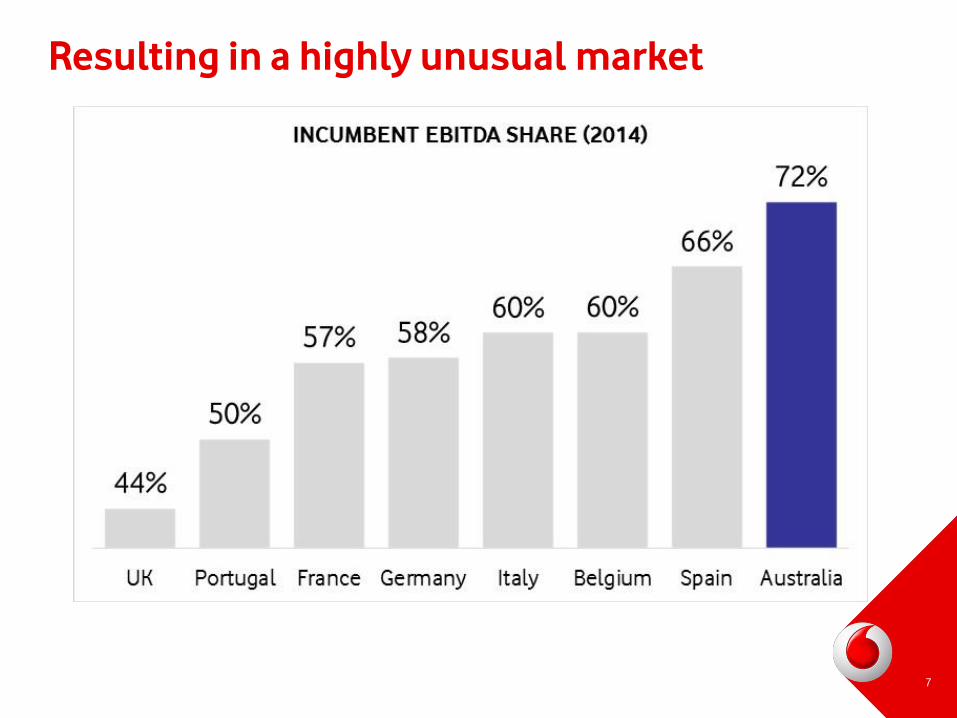

Resulting in a highly unusual market

8

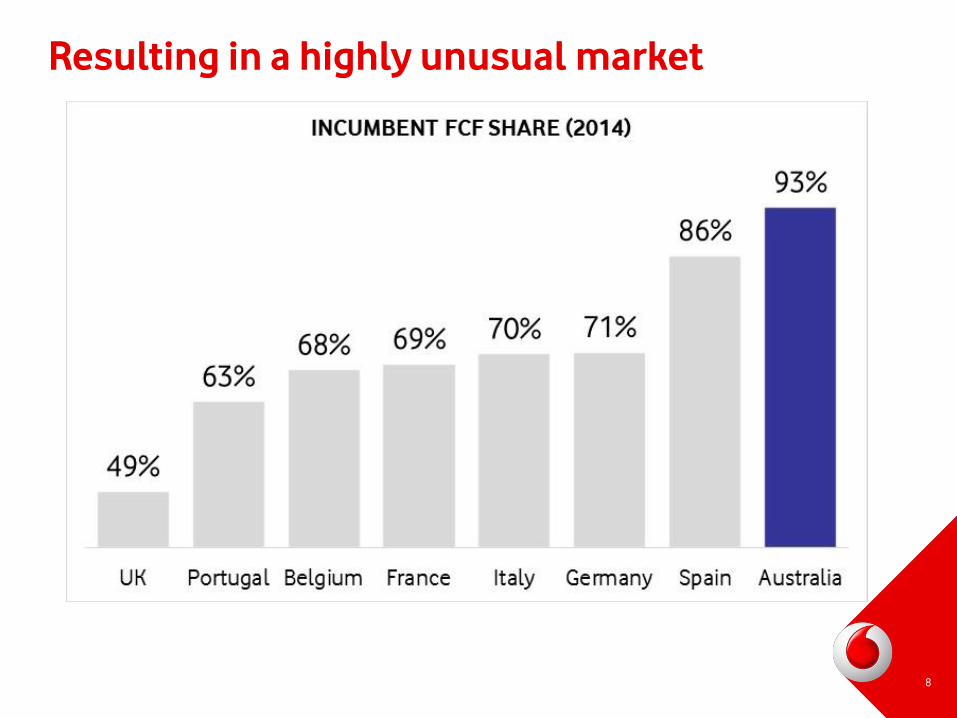

Resulting in a highly unusual market

Resulting in a highly unusual market

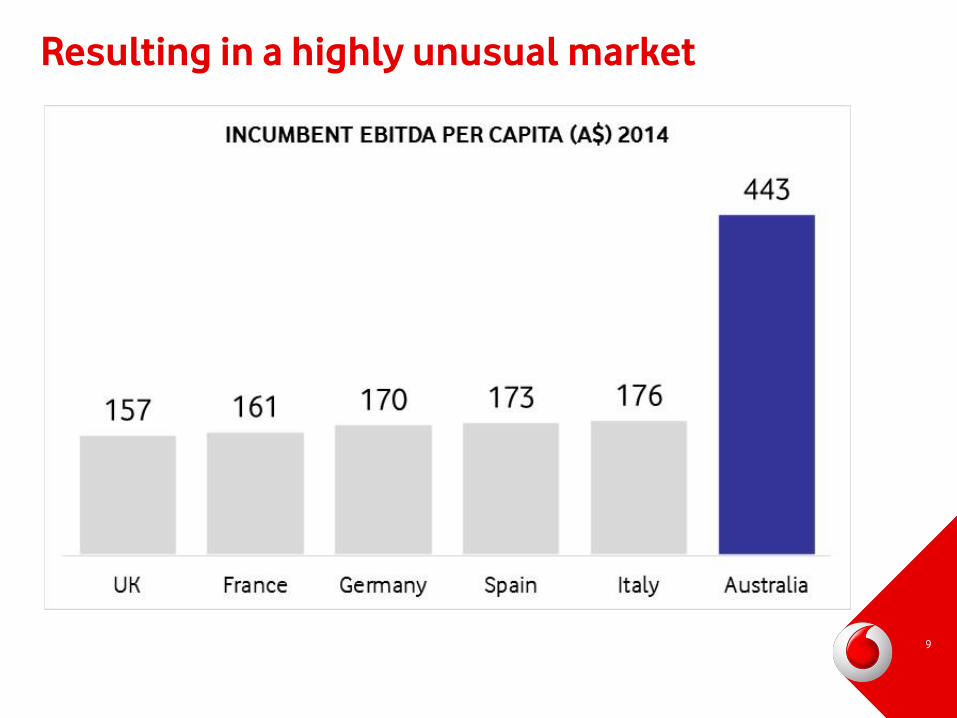

9

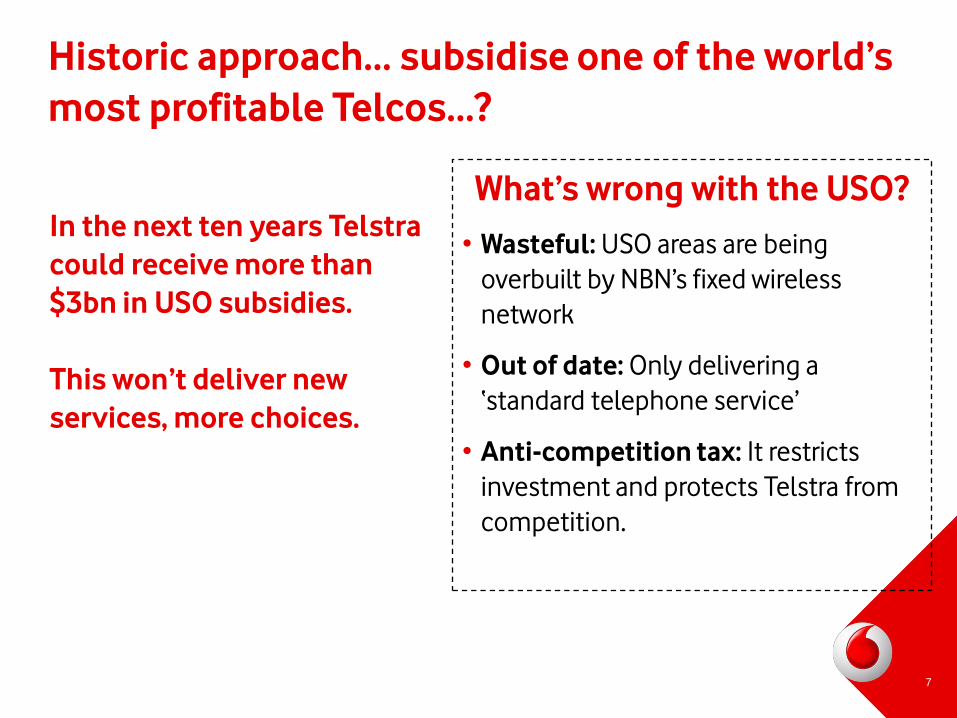

In the next ten years Telstra

could receive more than

$3bn in USO subsidies.

This won’t deliver new

services, more choices.

Historic approach… subsidise one of the world’s

most profitable Telcos…?

What’s wrong with the USO?

• Wasteful: USO areas are being

overbuilt by NBN’s fixed wireless

network

• Out of date: Only delivering a

‘standard telephone service’

• Anti-competition tax: It restricts

investment and protects Telstra from

competition.

7

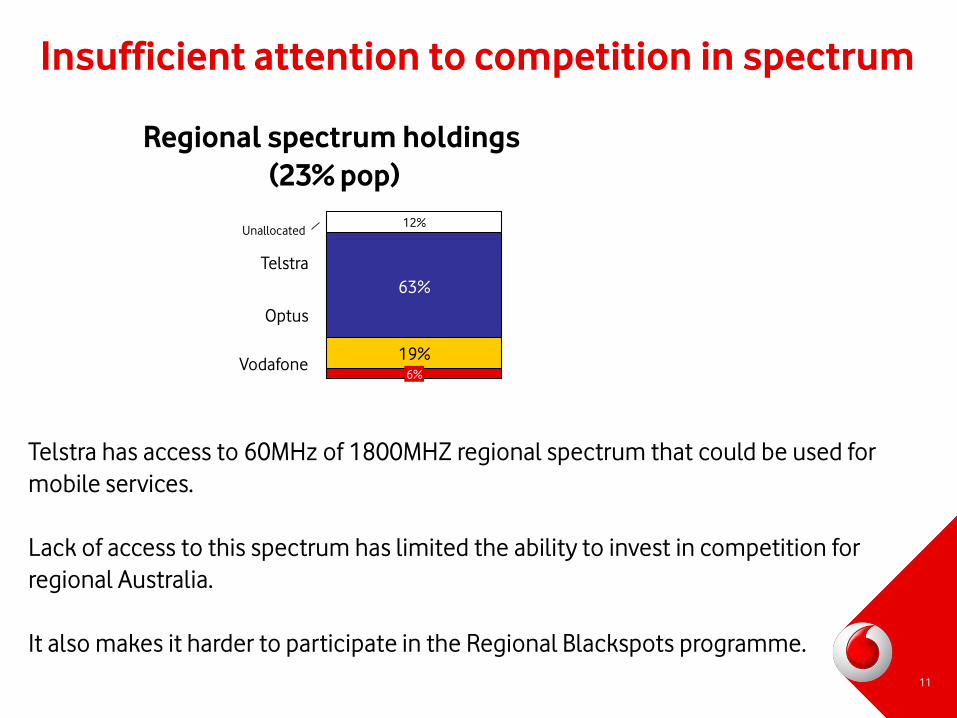

Insufficient attention to competition in spectrum

11

Telstra has access to 60MHz of 1800MHZ regional spectrum that could be used for

mobile services.

Lack of access to this spectrum has limited the ability to invest in competition for

regional Australia.

It also makes it harder to participate in the Regional Blackspots programme.

Telstra

63%

Unallocated

Optus

Regional spectrum holdings

(23% pop)

6%

19%Vodafone

12%

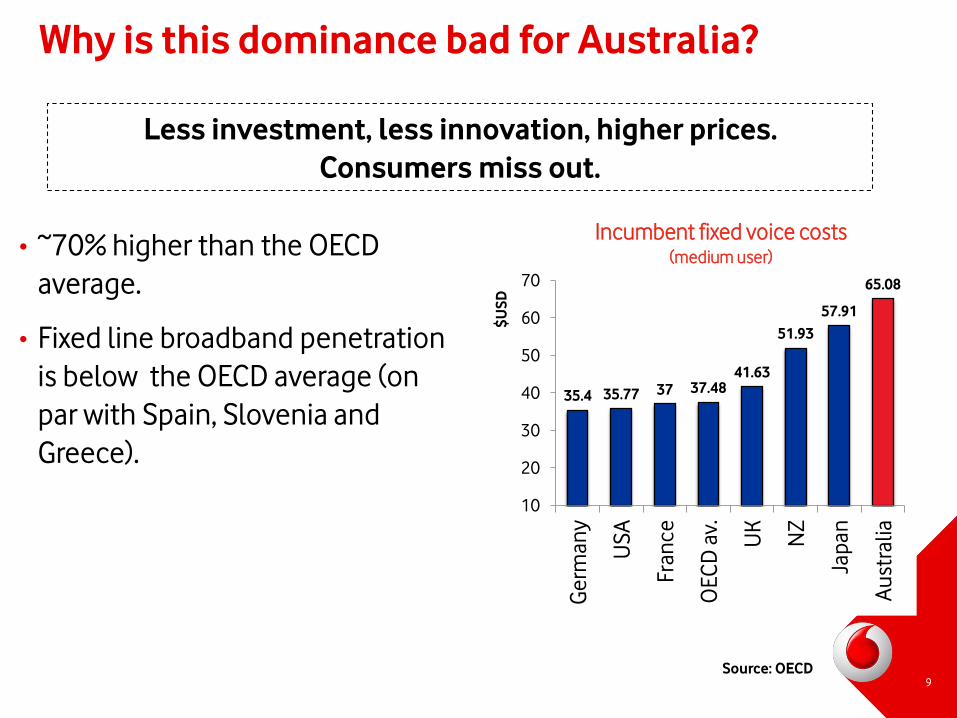

Why is this dominance bad for Australia?

• ~70% higher than the OECD

average.

• Fixed line broadband penetration

is below the OECD average (on

par with Spain, Slovenia and

Greece).

35.4 35.77 37 37.4841.63

51.93

57.91

65.08

10

20

30

40

50

60

70

Ge

rma

ny

US

A

Fra

nc

e

OE

CD

av.

UK

NZ

Jap

an

Au

stra

lia

$U

SD

Incumbent fixed voice costs(medium user)

Source: OECD

Less investment, less innovation, higher prices.

Consumers miss out.

9

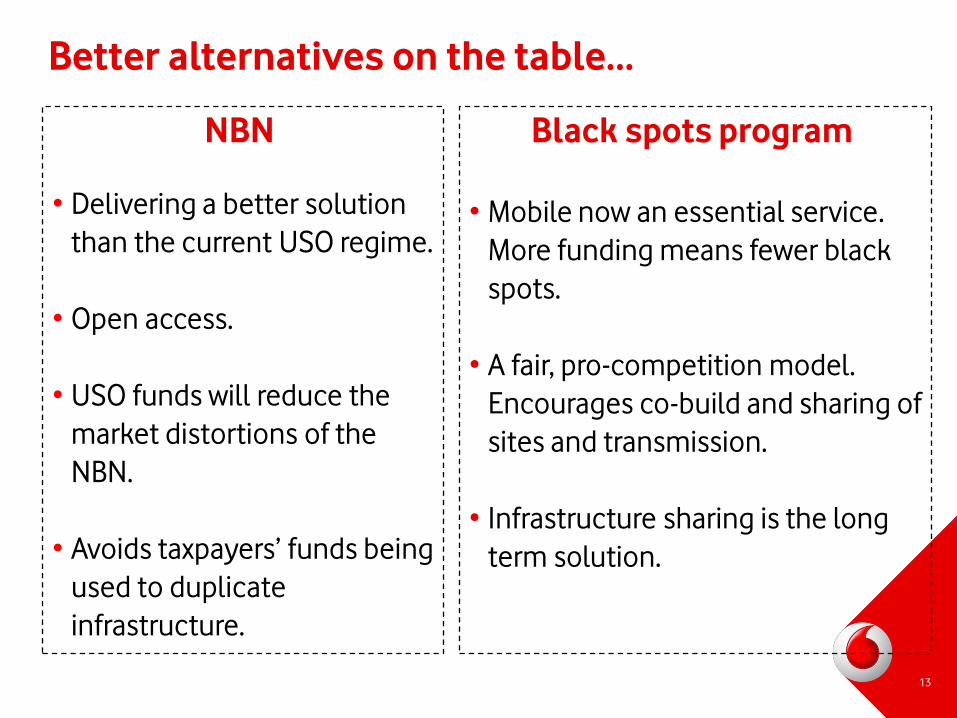

Better alternatives on the table…

NBN

• Delivering a better solution

than the current USO regime.

• Open access.

• USO funds will reduce the

market distortions of the

NBN.

• Avoids taxpayers’ funds being

used to duplicate

infrastructure.

13

Black spots program

• Mobile now an essential service.

More funding means fewer black

spots.

• A fair, pro-competition model.

Encourages co-build and sharing of

sites and transmission.

• Infrastructure sharing is the long

term solution.

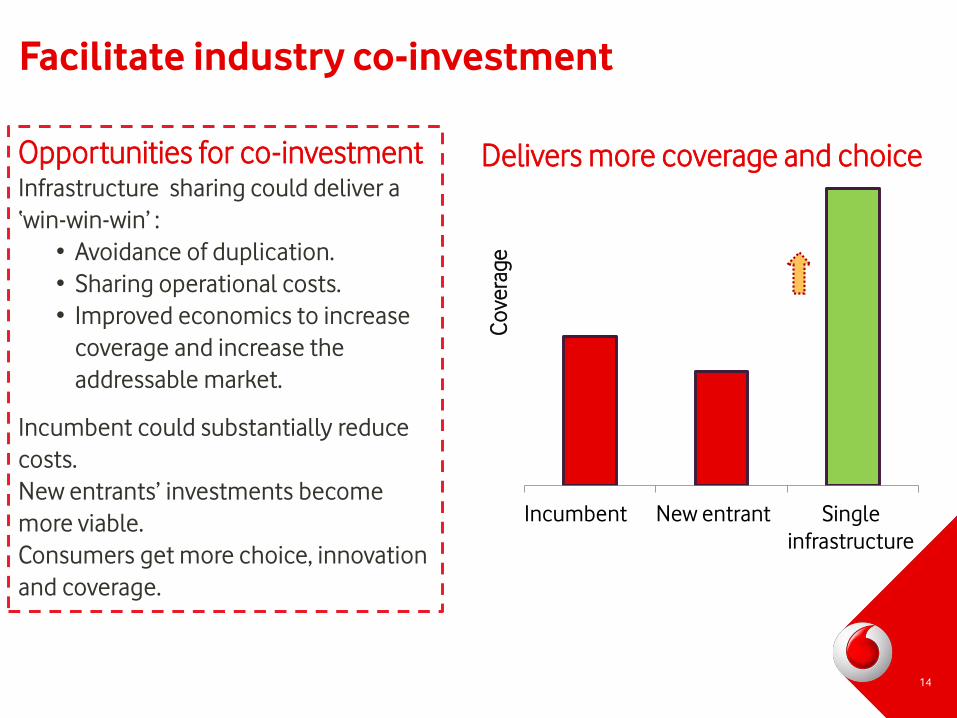

Incumbent New entrant Single

infrastructure

Facilitate industry co-investment

Co

vera

ge

Opportunities for co-investmentInfrastructure sharing could deliver a

‘win-win-win’ :

• Avoidance of duplication.

• Sharing operational costs.

• Improved economics to increase

coverage and increase the

addressable market.

Incumbent could substantially reduce

costs.

New entrants’ investments become

more viable.

Consumers get more choice, innovation

and coverage.

Delivers more coverage and choice

14

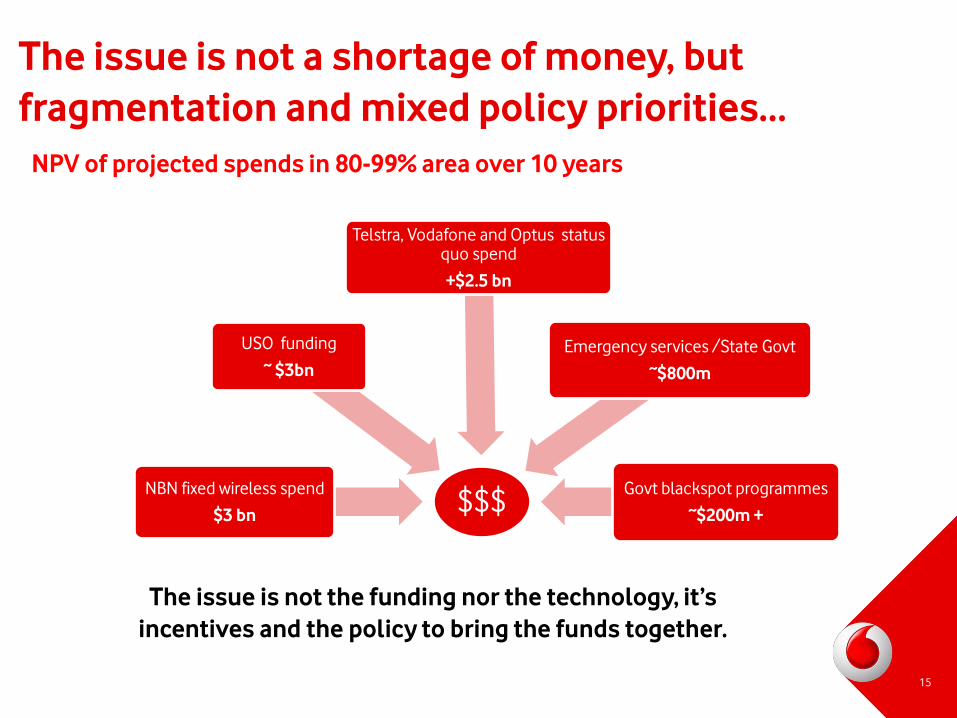

The issue is not a shortage of money, but

fragmentation and mixed policy priorities…

15

$$$NBN fixed wireless spend

$3 bn

USO funding

~ $3bn

Telstra, Vodafone and Optus status quo spend

+$2.5 bn

Emergency services /State Govt

~$800m

Govt blackspot programmes

~$200m +

NPV of projected spends in 80-99% area over 10 years

The issue is not the funding nor the technology, it’s

incentives and the policy to bring the funds together.

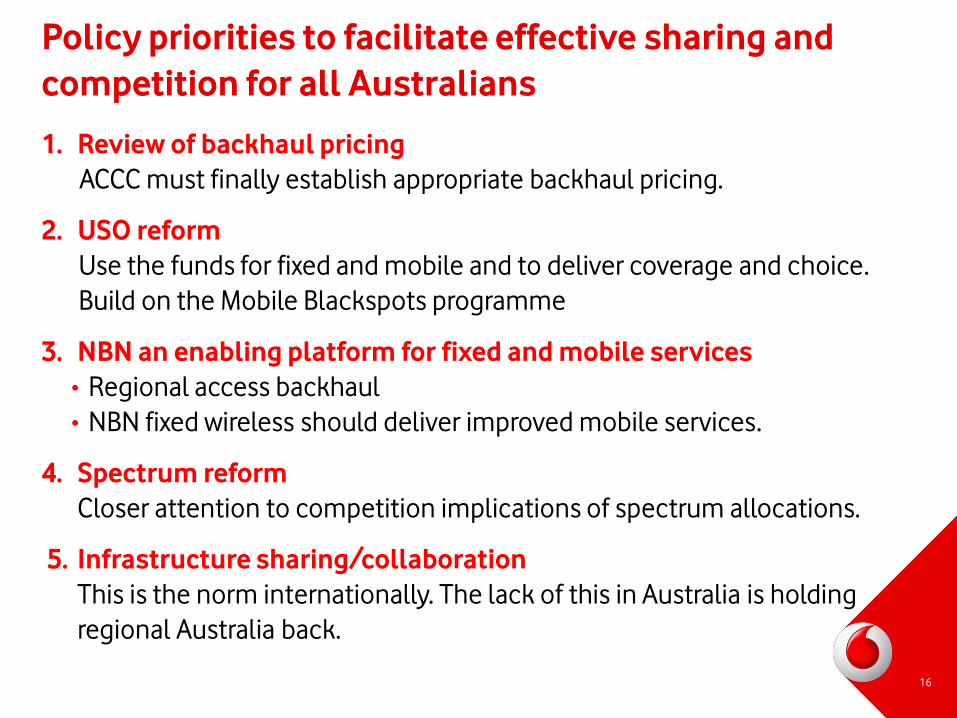

Policy priorities to facilitate effective sharing and

competition for all Australians

1. Review of backhaul pricing

ACCC must finally establish appropriate backhaul pricing.

2. USO reform

Use the funds for fixed and mobile and to deliver coverage and choice.

Build on the Mobile Blackspots programme

3. NBN an enabling platform for fixed and mobile services

• Regional access backhaul

• NBN fixed wireless should deliver improved mobile services.

4. Spectrum reform

Closer attention to competition implications of spectrum allocations.

5. Infrastructure sharing/collaboration

This is the norm internationally. The lack of this in Australia is holding

regional Australia back.

16

![[Leo Jason-Lloyd, Leonard Jason-Lloyd] an Introduc(BookSee.org)](https://img.pdfslide.net/doc/110x75/55cf8e0f550346703b8e1817/leo-jason-lloyd-leonard-jason-lloyd-an-introducbookseeorg.jpg)