Embed Size (px)

Citation preview

“There are hundreds of startups with a lot of brains and money working on various alterna3ves to tradi3onal banking” Jamie Dimon Chairman and CEO JPMorgan Chase & Co. April 8, 2015

Banking Is (SDll) Under AGack

Kevin Weeks

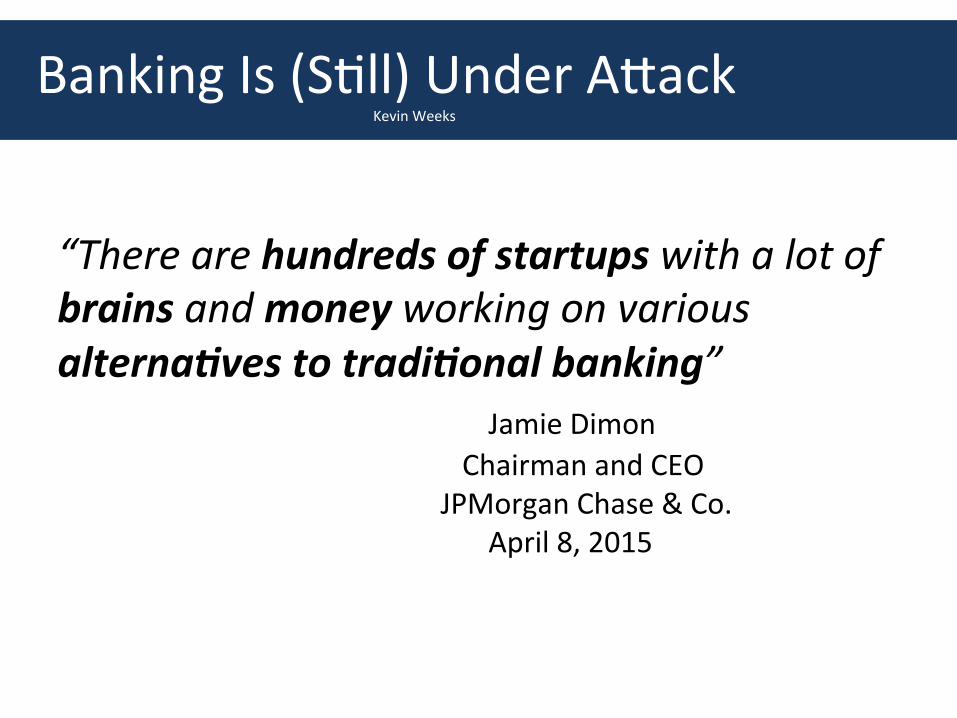

Tom’s post in white/red, Kevin’s annota<ons in grey/blue

Summary: Tom Loverro’s Post (2.0)

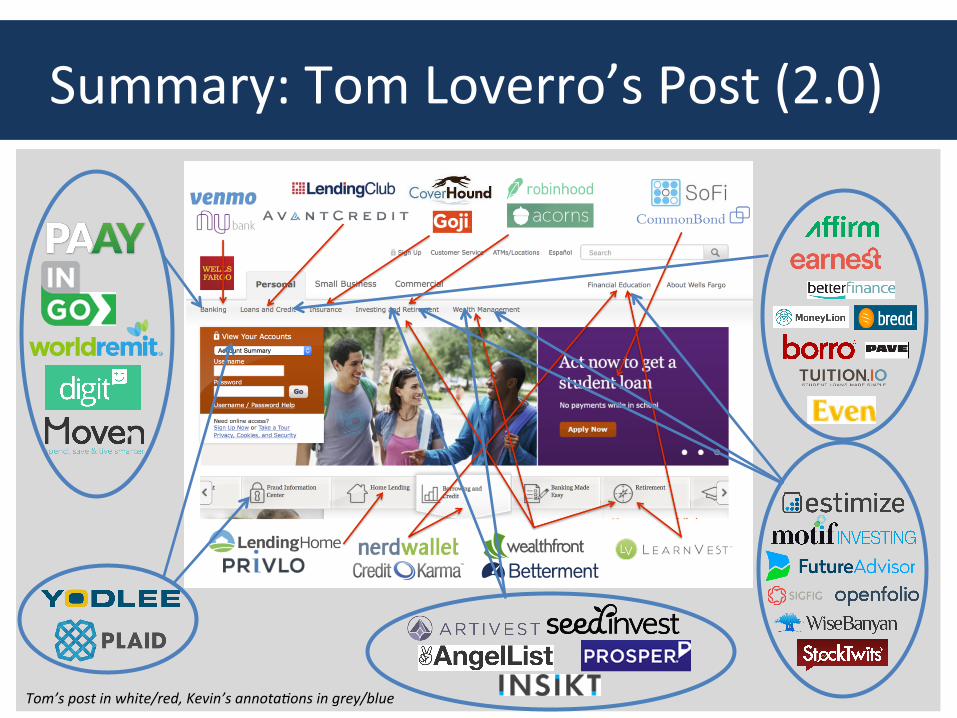

Basic Personal Banking • Checking, savings, debit and prepaid cards, transfers • Ultra low margins so massive success requires massive scale How can a company be disrupDve in

this space? Who’s gunning for it Commentary

Deliver a be*er customer experience: Mobile first or mobile only. Avoid piZalls of compeDng with a huge retail footprint

Big: Small:

• May beat brick and mortar incumbents but hard to differenDate from other startups

• Online-‐only banking is crowded (Ally) Be*er asset gathering: Technology-‐enabled or other creaDve asset gathering techniques can win customers

Big: Small:

• Collect interest on lots of small bases • New customers demand convenience through technology

• B&M model is a poor use of assets

Create a way to earn be*er net interest margin: Net interest margin is bank’s biggest compeDDve advantage but it’s not unbeatable

Big: Small:

• Two ways to do this: find cheaper money or charge higher rates

• Customers may not expect interest income now, but when rates rise…

Sell shovels and pick axes: Build ancillary services that leverage bank infrastructure and help startups gather deposits

Big:

Small:

• APIs “export” bank trust • Blockchain could kill this

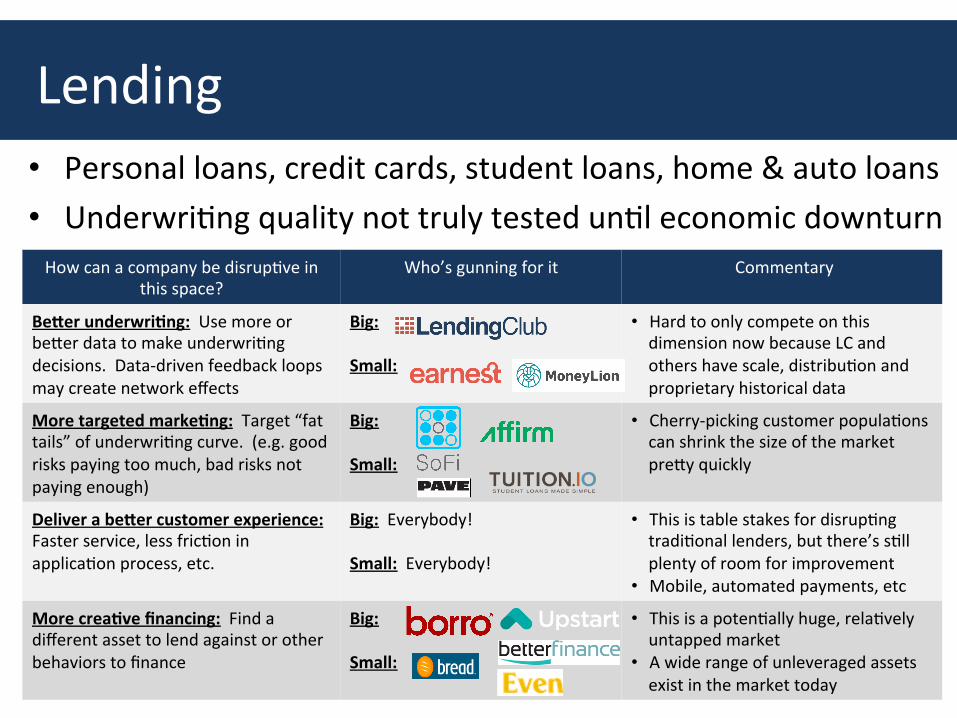

Lending • Personal loans, credit cards, student loans, home & auto loans • UnderwriDng quality not truly tested unDl economic downturn How can a company be disrupDve in

this space? Who’s gunning for it Commentary

Be*er underwri>ng: Use more or beGer data to make underwriDng decisions. Data-‐driven feedback loops may create network effects

Big: Small:

• Hard to only compete on this dimension now because LC and others have scale, distribuDon and proprietary historical data

More targeted marke>ng: Target “fat tails” of underwriDng curve. (e.g. good risks paying too much, bad risks not paying enough)

Big: Small:

• Cherry-‐picking customer populaDons can shrink the size of the market preGy quickly

Deliver a be*er customer experience: Faster service, less fricDon in applicaDon process, etc.

Big: Everybody! Small: Everybody!

• This is table stakes for disrupDng tradiDonal lenders, but there’s sDll plenty of room for improvement

• Mobile, automated payments, etc

More crea>ve financing: Find a different asset to lend against or other behaviors to finance

Big: Small:

• This is a potenDally huge, relaDvely untapped market

• A wide range of unleveraged assets exist in the market today

InvesDng and Wealth Management • Historical delineaDon between self-‐directed invesDng and

professionally-‐driven invesDng is becoming less important How can a company be disrupDve in

this space? Who’s gunning for it Commentary

Take more costs out of the system: Remove people, brick & mortar and transacDon costs. Use technology to scale economically

Big: Small:

• DisrupDon has already removed lots of costs-‐ trading margins are historically low and online-‐only exists already (Ameritrade, Etrade, etc)

Gather more assets by providing more personalized service: Use tech to beGer serve customers. Like checking, this is an asset gathering race

Big: Small:

• Algorithmically-‐run “roboadvisors” offer personalized advice based on customer preference or data

Address new markets and/or new customers: Make products that banks don’t want to/can’t make or serve audiences that banks don’t want to/can’t serve

Big: Small:

• Open inaccessible asset classes • DemocraDze previously opaque informaDon

• Growing demand in the market for alternaDves right now, but if the bubble bursts…

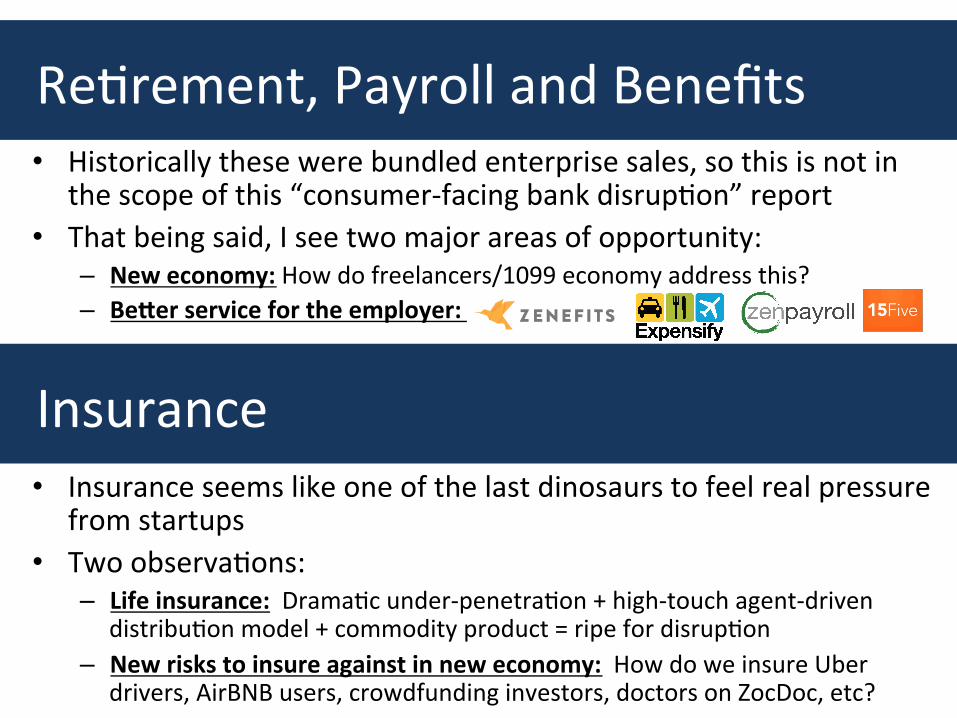

ReDrement, Payroll and Benefits • Historically these were bundled enterprise sales, so this is not in

the scope of this “consumer-‐facing bank disrupDon” report • That being said, I see two major areas of opportunity:

– New economy: How do freelancers/1099 economy address this? – Be*er service for the employer:

Insurance • Insurance seems like one of the last dinosaurs to feel real pressure

from startups • Two observaDons:

– Life insurance: DramaDc under-‐penetraDon + high-‐touch agent-‐driven distribuDon model + commodity product = ripe for disrupDon

– New risks to insure against in new economy: How do we insure Uber drivers, AirBNB users, crowdfunding investors, doctors on ZocDoc, etc?