Embed Size (px)

Citation preview

sewellsgroup.com

Quarter ending Jun 2014

sewellsgroup.comPage 1

About Sewells GroupAutomotive Dealer ConfidenceIndex

ADCI Survey Methodology Summary of Respondents

GAUTOMOTIVEDEALERCONFIDENCE

SEWELLS GROUP

INDEXGlobally, confidence indices are viewed as reliable precursors to business performance. Such indices aim to capture and quantify the sentiment of various industry stakeholders – be it CXOs, suppliers, vendors or distribution partners who usually are in the middle of the action. People within the industry, typically use these indices to get a sense of stakeholder sentiment and optimize their actions in line with the sentiment. Market analysts, on the other hand, interpret theses indices as a ‘lead indicators’ of the performance of a particular industry or sector. An accurate, representative index may demonstrates a high level of correlation with actual business performance.

The automotive industry in India has been a sunrise sector contributing a significant share to country’s GDP. A healthy and growing domestic market, an active and constructive involvement from the government, growth of domestic auto manufacturers to become true global players and presence of multiple global brands in the country have made sure that this industry has come of its age. With everything else being executed at a global scale and with global vision, we believe that the time has come for Indian auto industry to have a dealer confidence index.

The important role played by auto dealers in this industry is already known. With their unique position at the market place, auto dealers are usually in touch with ground realities. And therefore such an indicator should be able position itself as useful signalling device for various stakeholders within the automotive industry eco-system.

Ssewellsgroup.comPage 2

About Sewells GroupAutomotive Dealer ConfidenceIndex

ADCI Survey Methodology Summary of Respondents

Sewells Group Automotive Dealer Confidence Index (ADCI) is a measure of dealer sentiment about their business over next six months from the time it is being captured. It will be published on a quarterly basis.

Within the automotive industry, dealers enjoy a unique position close to the ‘action on the ground’. They are in constant touch with prospects, customers, factory staff, competition dealers, financiers and other market intermediaries. Consequently, each dealer gets exposed to a plethora of information that in turn shapes his / her sentiment about the future of markets and businesses. The Sewells Group Automotive Dealer Confidence Index (ADCI) is an attempt to capture and quantify this well informed sentiment of the auto dealers from across the length and breadth of the country, representing multiple brands and product categories. We aim to be able to represent this collective sentiment in the form of an index, whose movement over time will reliably predict the direction of the wholesale and the retail sales within the industry.

We believe publication of such an index will allow industry stakeholders to have meaningful conversations in time, which in turn will help them put together better strategies to perform at the market place.

sewellsgroup.comPage 3

About Sewells GroupAutomotive Dealer ConfidenceIndex

ADCI Survey Methodology Summary of Respondents

TThe Sewells Group ADCI is designed to be a quarterly index that will be computed on the basis of responses received to a structured questionnaire from the automotive dealer fraternity in Indian market. The questionnaire attempts to capture their sentiment about economy in general and their business in particular on a six month forward horizon.

Sewells Group proposes to track the trend of the index which will offer an insight into the future direction of the market. We believe that it is the movement of the index which will offer greater insights than the absolute value of the index in a particular quarter.

In this second edition of the ADCI, we attempt to capture the sentiment of the dealer fraternity at the end of Apr-Jun quarter of 2014. The findings of this survey are compared with the findings of the inaugural survey which captured the sentiments of the dealer fraternity at the end of Jan-Mar quarter of 2014, to map the trend. We propose to repeat the survey at the end of each following quarter. Sewells Group proposes to increase the sample size of the survey in future.

For this edition, a questionnaire was distributed electronically (by email) to the dealer fraternity in India. A total of 126 responses received, from dealers, representing 21 brands were used to compute the index. Every effort has been made to ensure that the index is statistically meaningful and representative of dealer sentiment. However, we advise reader discretion while considering the statistical significance. At this stage, ADCI is designed only for “exploratory” and “indicative” purposes.

The second edition of the survey represents an interesting point in over last two decades when, the country has a majority government. The business fraternity expect a jump start to the economy. Automotive dealers-an important part of country's business fraternity, expect that, an improved economic environment will translate into improved performance for them.

sewellsgroup.comPage 4

About Sewells GroupAutomotive Dealer ConfidenceIndex

ADCI Survey Methodology Summary of Respondents

71 57%33%

10%

42

13

126

PASSENGER CARS TWO-WHEELERS COMMERCIAL VEHICLES

TOTAL NUMBER OF RESPONDENTS48

3413

10

66

PASSENGER CARS PASSENGER CARSTWO-WHEELERS TWO-WHEELERSCOMMERCIAL VEHICLES COMMERCIAL VEHICLES

PASSENGER CARS TWO-WHEELERS COMMERCIAL VEHICLES OVERALL

38%

43%

19%

0%

46%

23%

8%

23%

54%

30%

13%

3%

65%

24%

10%1%

BEFORE 1975

1975 - 1990

1990 - 2005

AFTER 2005AG

E O

F D

EALE

RSH

IPS

LOC

ATI

ON

OF

RES

PO

ND

ENTS

BR

AN

DS

REP

RES

ENTE

D

21 BRANDS75 CITIES

sewellsgroup.comPage 5

AUTOMOTIVEDEALERCONFIDENCE

END OF APR-JUN 14 QUARTERINDIA

INDEX

SEWELLS GROUP

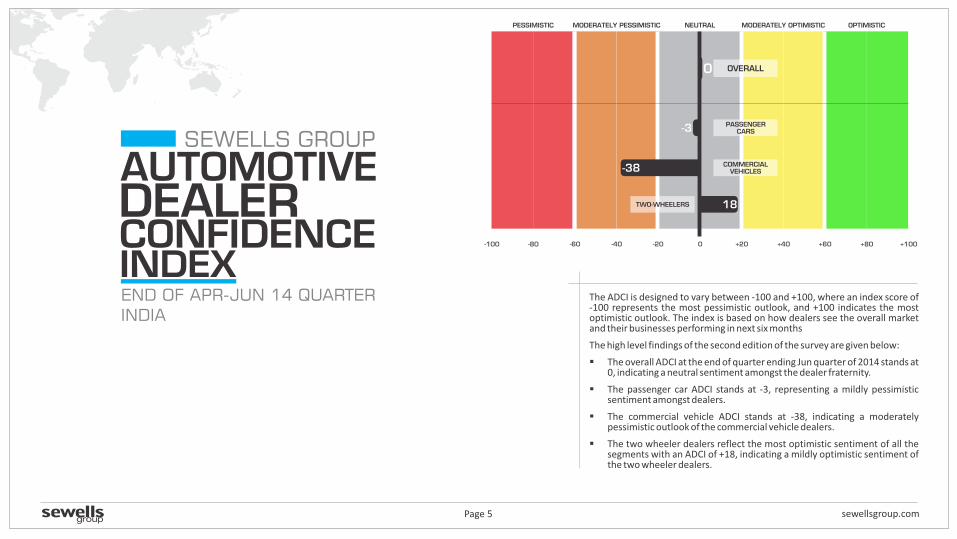

0-80-100 -40-60 -20 +80 +100+40 +60+20

PESSIMISTIC NEUTRAL MODERATELY PESSIMISTIC MODERATELY OPTIMISTIC OPTIMISTIC

0 OVERALL

PASSENGERCARS-3

COMMERCIALVEHICLES-38

TWO-WHEELERS 18

The ADCI is designed to vary between -100 and +100, where an index score of -100 represents the most pessimistic outlook, and +100 indicates the most optimistic outlook. The index is based on how dealers see the overall market and their businesses performing in next six months

The high level findings of the second edition of the survey are given below:

§ The overall ADCI at the end of quarter ending Jun quarter of 2014 stands at 0, indicating a neutral sentiment amongst the dealer fraternity.

§ The passenger car ADCI stands at -3, representing a mildly pessimistic sentiment amongst dealers.

§ The commercial vehicle ADCI stands at -38, indicating a moderately pessimistic outlook of the commercial vehicle dealers.

§ The two wheeler dealers reflect the most optimistic sentiment of all the segments with an ADCI of +18, indicating a mildly optimistic sentiment of the two wheeler dealers.

sewellsgroup.comPage 6

AUTOMOTIVEDEALERCONFIDENCE

END OF APR-JUN 14 QUARTER

INDEX-TREND

SEWELLS GROUP

0

+80

+100

+40

+60

+20

-80

-100

-40

-60

-20

MO

DER

ATELY

PESSIM

ISTIC

MO

DER

ATELY

OPTIM

ISTIC

PESSIM

ISTIC

NEU

TR

AL

OPTIM

ISTIC

End of Q1-2014 End of Q2-2014 End of Q3-2014 End of Q4-2014

-40 -3

-20 0

+13

-32

+18

-38

SEGMENT

PASSENGER CARS

OVERALL

TWO-WHEELERS

COMMERCIAL VEHICLES

End of Q1-2014 End of Q2-2014 End of Q3-2014 End of Q4-2014

There is an upward swing in the overall ADCI. The trends observed during the second edition of the survey are given below:

§ The index for passenger cars moved from -40 at the end of quarter ending Mar 2014, to -3 during the current survey. This reflects a highly positive movement of dealer sentiment.

§ The index for two-wheeler dealers moved from +13 at the end of quarter ending Mar 2014, to +18 during the current survey. The movement of the index indicates a slight positive movement of sentiment.

§ Commercial vehicle dealers continue to remain pessimistic about business prospects. The index for commercial vehicles falls from -32 at the end of quarter ending Mar 2014, to-38 during the current survey.

§ The overall index at the end of quarter ending Jun 2014 stands at 0, up from -20 at the end of previous quarter, reflecting a significant positive movement of dealer sentiments. About 60% of respondents expect their business to be profitable in the next 6 months.

OVERALLPASSENGER

CARSTWO-

WHEELERSCOMMERCIAL

VEHICLES

sewellsgroup.com

The following pages carry details of responses received during the second edition of the survey for questions covering the above areas. Sewells Group intends to administer the ADCI survey every quarter, and intends to track the movement of question-level distribution on a quarterly basis.

The findings of this survey are compared with the findings of the inaugural survey which captured the sentiments of the dealer fraternity at the end of Jan-Mar quarter of 2014 to map the trend.

This section of analysis presents the distribution of responses across multiple questions that were asked in the survey and compared with the findings of the previous survey .

Future view of manpower strength of the business

Expected performance of the market as well as the

dealership over the next six months

Expected levels of sales, inventory and profits over the

next six months

View on the current situation of sales, inventory and profits vis-à-vis same period last year

Impact of the current economic scenario on the

market, as well as the dealership business

View on the current situation of sales, inventory and profits

vis-à-vis previous quarter

06

08

02

04

Page 7

07

05

03

01Impact of the Current Economic Scenario on the Market

Expected Market Performance Over Next Six Months

Dealership Performance vis-a-vis Same Period Previous Year

Expected Dealership Performance Over Next Six Months

Impact of the Current Economic Scenario on the Dealership

Expected Dealership Performance Over Next Six Months

Dealership Performance vis-a-vis Previous Quarter

Expected Manpower Strength Over Next Six Months

page 8 page 9

page 10 page 11

page 12 page 15

page 18 page 21

ANALYSIS OF SURVEY FINDINGS

The ADCI survey delves into the following areas:

AUTOMOTIVEDEALERCONFIDENCEINDEX

SEWELLS GROUP

§ Overall, the dealers are more positive about the impact of current economic scenario on the market than what they were in the quarter ending Mar 2014 (up to 41% from 15% at the end of previous quarter). This could be attributed to the positive sentiments of dealers across all segments.

§ Passenger car dealers who were extremely pessimistic during previous survey have shown marked improvement in sentiments about the impact of economic scenario on the market during current survey (up from 1% to 34%).

§ Two wheeler dealers are the most optimistic amongst all the segments, with 62% of dealers feeling that the current market scenario has a positive impact on the market.

§ Commercial vehicle dealers are the least optimistic amongst the three segments with only 16% of dealers being optimistic about the impact of current economic scenario on market.

sewellsgroup.com

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

EXCITING POSITIVE NOT SO POSITIVE WORRISOME

1CURRENT ECONOMICSCENARIO

IMPACT OF THE

ON THE MARKET 0%

20%

40%

60%

80%

100%

4%

11%

58%

27%

% O

F R

ESP

ON

DEN

TS

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

7%

34%

41%

18%

Page 8

6%

28%

48%

18% 10%

52%

29%

10% 8%8%

38%

46%

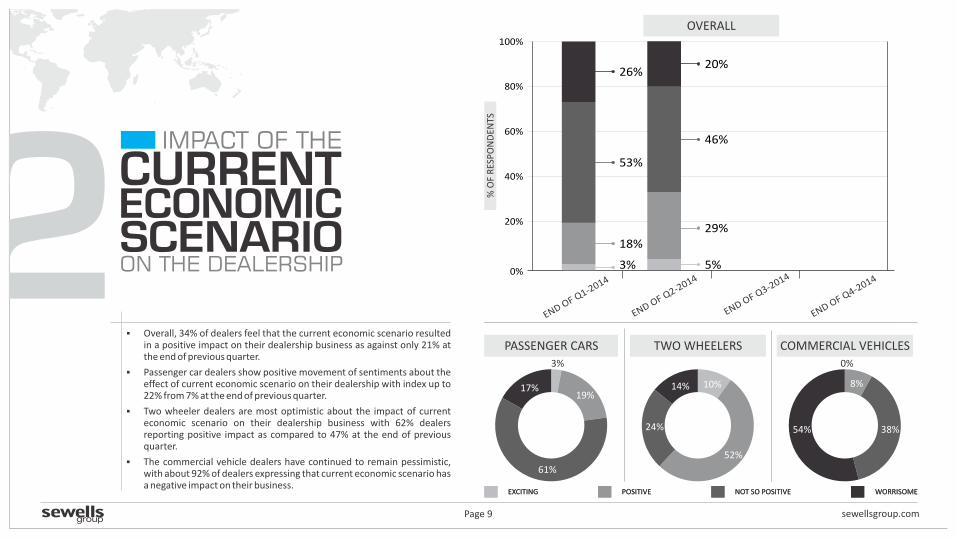

§ Overall, 34% of dealers feel that the current economic scenario resulted in a positive impact on their dealership business as against only 21% at the end of previous quarter.

§ Passenger car dealers show positive movement of sentiments about the effect of current economic scenario on their dealership with index up to 22% from 7% at the end of previous quarter.

§ Two wheeler dealers are most optimistic about the impact of current economic scenario on their dealership business with 62% dealers reporting positive impact as compared to 47% at the end of previous quarter.

§ The commercial vehicle dealers have continued to remain pessimistic, with about 92% of dealers expressing that current economic scenario has a negative impact on their business.

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

EXCITING POSITIVE NOT SO POSITIVE WORRISOME

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

EXCITING POSITIVE NOT SO POSITIVE WORRISOME

sewellsgroup.comPage 9

2CURRENT ECONOMICSCENARIOON THE DEALERSHIP

IMPACT OF THE

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

3%

18%

53%

26%

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

5%

29%

46%

20%

3%

19%

61%

17% 10%

52%

24%

14%

0%

8%

38%54%

§ Overall, the dealers are more optimistic about the expected market performance over the next 6 months than the previous quarter with 67% expecting positive sentiments as compared to 51% at the end of previous quarter.

§ There is a significant swing in the sentiment of the passenger car dealers in the positive direction. 72% of passenger car dealers feel that the market is going to perform well in the next six months as against only 35% at the end of previous quarter.

§ Surprisingly, both the the two wheeler dealers (down to 70% from 75%) and the commercial vehicle dealers (down to 39% from 50%) are not as optimistic as they were in the previous quarter about expected market performance over next six months.

3MARKET OVER NEXT SIX MONTHS

EXPECTED

PERFORMANCE

sewellsgroup.comPage 10

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

-40

38%

46%

5%

11%

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

7%

60%

26%

7%

6%

66%

22%

6% 8%

31%

46%

15%

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

EXCITING POSITIVE NOT SO POSITIVE WORRISOME

10%

60%

27%

5%

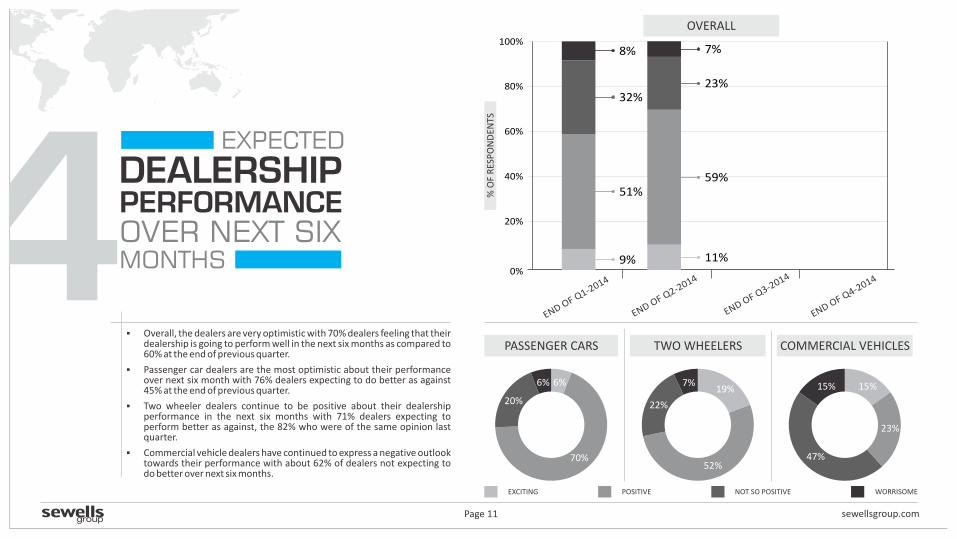

§ Overall, the dealers are very optimistic with 70% dealers feeling that their dealership is going to perform well in the next six months as compared to 60% at the end of previous quarter.

§ Passenger car dealers are the most optimistic about their performance over next six month with 76% dealers expecting to do better as against 45% at the end of previous quarter.

§ Two wheeler dealers continue to be positive about their dealership performance in the next six months with 71% dealers expecting to perform better as against, the 82% who were of the same opinion last quarter.

§ Commercial vehicle dealers have continued to express a negative outlook towards their performance with about 62% of dealers not expecting to do better over next six months.

EXCITING POSITIVE NOT SO POSITIVE WORRISOME

0%

20%

40%

60%

80%

100%

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

% O

F R

ESP

ON

DEN

TS

9%

51%

32%

8%

4DEALERSHIP

OVER NEXT SIX MONTHS

EXPECTED

PERFORMANCE

sewellsgroup.comPage 11

OVERALL

11%

59%

23%

7%

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

6%

70%

20%

6%19%

52%

22%

7% 15%

23%

47%

15%

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

sewellsgroup.comPage 12

5PERFORMANCE

YEAR

DEALERSHIP

VIS-À-VIS SAME PERIOD

PREVIOUS

DEFINITELY HIGHER HIGHER OR SAME SAME OR LOWER DEFINITELY LOWER

SALES INVENTORY PROFITS 0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

29%

24%

27%

20%

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

20%

23%

37%

20%

14%

22%

44%

20%33%

31%

17%

19%8%

8%

62%

24%

§ Current economic scenario continues to affect dealer sales negatively. Overall, only 43% of the dealers reported doing better on sales, than the previous year, as compared to 47% at the end of previous quarter.

§ The slight dip in this sentiment is due to the commercial vehicle dealership performance. Only 16% of the commercial vehicle dealers feel that their sales has improved since the previous year as against the 39% dealers feeling the same at the end of previous quarter.

§ Both passenger car (at 36% in the current and previous survey) and two wheeler dealers (down to 64% from 69% in previous quarter) report no significant change in dealers doing well on sales volume as compared to the dealers doing better on sales in the previous quarter and same period previous year.

SALES INVENTORY PROFITS

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

sewellsgroup.comPage 13

DEFINITELY HIGHER HIGHER OR SAME SAME OR LOWER DEFINITELY LOWER

5PERFORMANCE

YEAR

DEALERSHIP

VIS-À-VIS SAME PERIOD

PREVIOUS0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

8%

21%

36%

35%

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

31%

34%

26%

9%

23%

35%

31%

11%

54%28%

13%5% 8%

46%38%

8%

§ Overall, dealers indicate some inventory correction with only 65% reporting higher inventory as against 71% at the end of previous quarter as compared to same period last year.

§ Inventory levels viz-a-viz same period previous year for both passenger cars and commercial vehicle dealers have reduced as compared to the results of the previous survey. However, 58% passenger car dealers (down from 67% at the end of previous quarter) and 52% commercial vehicle dealers (down from 62% at the end of previous quarter) feel that their inventory levels have gone up viz-a-viz same period previous year.

§ Two wheeler dealers continue to face adverse impact of high inventory. As in the last quarter, around 82% of two wheeler dealers feel that their inventory levels have gone up as compared to the same period previous year.

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

sewellsgroup.comPage 14

DEFINITELY HIGHER HIGHER OR SAME SAME OR LOWER DEFINITELY LOWER

5PERFORMANCE

YEAR

DEALERSHIP

VIS-À-VIS SAME PERIOD

PREVIOUSSALES INVENTORY PROFITS 0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

43%

24%

21%

12%

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

13%

20%

26%

41%

8%

22%

28%

42%

26%

23%20%

31%

0%

8%

23%

69%

§ Overall, the dealers have continued to express a pessimistic sentiment about their profits vis-a-vis same period previous year. Only 33% of dealers feel that their profits have increased as compared to same period last year.

§ The above sentiments are reflected across all the three segments. The two wheeler dealers (at 49% up from 46% at the end of previous quarter) and the passenger car dealer (at 30% up from 25% at the end of previous quarter) reporting higher profits when compared with the same period last year.

§ Commercial vehicle dealers remain pessimistic with only 8% dealers expecting higher profits as compared to 24% at the end of previous quarter when compared with the same period last year.

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

sewellsgroup.comPage 15

6PERFORMANCE

QUARTER

VIS-À-VIS

PREVIOUS

DEALERSHIP

DEFINITELY HIGHER HIGHER OR SAME SAME OR LOWER DEFINITELY LOWER

SALES INVENTORY PROFITS 0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

21%

36%

30%

13%

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

§ 45% of dealers feel that their sales has increased over previous quarter as compared to 43% reporting the same at the end of quarter ending Mar 2014.

§ Passenger car (up at 37% from 27% at the end of previous quarter) and two wheeler (up at 66% from 59% at the end of previous quarter) dealers reported doing better on sales as compared to the previous quarter, showing signs of economic revival.

§ Contrary to the above sales performance of the commercial vehicle dealers remains a cause of worry with only 24% reporting higher sales as compared to 34% reporting higher sales at the end of previous quarter.

17%

28%

40%

15%

14%

23%

53%

10%23%

43%

17%

17% 16%

8%

38%

38%

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

sewellsgroup.comPage 16

DEFINITELY HIGHER HIGHER OR SAME SAME OR LOWER DEFINITELY LOWER

6PERFORMANCE

QUARTER

VIS-À-VIS

PREVIOUS

DEALERSHIP

SALES INVENTORY PROFITS 0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

6%

27%

37%

30%

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

18%

46%

32%

4%

14%

47%

38%

1%

30%

49%

16%5% 8%

31%

46%

15%

§ Overall, the higher inventories continue to be troublesome for dealers. However, there is slight improvement in the situation with only 64% reporting higher inventory as compared to 68% at the end of previous quarter.

§ The above trend is replicated by passenger car dealers with 61% reporting higher inventory as compared to 64% at the end of previous quarter.

§ The two wheeler dealers are the worst effected with 79% of dealers feeling that their inventory levels are higher than the previous quarter, as compared to 77% at the end of previous quarter.

§ Commercial vehicle dealers saw reduction in inventories with only 39% reporting higher inventories as compared 50% at the end of previous quarter.

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

sewellsgroup.comPage 17

DEFINITELY HIGHER HIGHER OR SAME SAME OR LOWER DEFINITELY LOWER

6PERFORMANCE

QUARTER

VIS-À-VIS

PREVIOUS

DEALERSHIP

SALES INVENTORY PROFITS 0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

36%

31%

22%

11%

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

8%

32%

30%

30%

8%

30%

33%

29%

11%

35%

30%

24%

0%

31%

15%

54%

§ Overall, there is a positive movement of sentiment of dealers about profitability with 40% dealers reporting higher profits as compared 33% at the end of previous quarter.

§ Passenger car (at 38% up from 24% at the end of previous quarter) and commercial vehicle (at 31% up from 24% at the end of previous quarter) dealers have reported higher profitability as compared to the previous quarter.

§ There is no change in two wheeler dealers sentiments on profitability, with about 46% reporting higher profits, the same as at the end of previous quarter

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

sewellsgroup.comPage 18

7DEALERSHIP

MONTHS

EXPECTED

PERFORMANCEOVER NEXT SIX

DEFINITELY HIGHER HIGHER OR SAME SAME OR LOWER DEFINITELY LOWER

SALES INVENTORY PROFITS 0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

7%

31%

46%

16%

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

21%

54%

19%

6%

18%

59%

17%

6%

28%

50%

17%

5% 8%

38%

38%

16%

§ Optimism of overall, dealers about their dealership sales in the next six month has improved with 75% expecting higher sales as compared to 70% at the end of previous quarter.

§ Most positive movement of sentiments is of the passenger car dealers with 77% expecting higher sales as compared to only 47% dealers feeling the same at the end of previous quarter.

§ Two wheeler dealers continue to be optimistic with 78% dealers expecting to clock higher sales in the next six months.

§ Commercial vehicle dealers however are concerned about their sales figures in the next six months with only 46% feeling that their sales would be higher as compared to 56% dealers feeling the same at the end of previous quarter.

7DEALERSHIP

MONTHS

EXPECTED

PERFORMANCEOVER NEXT SIX

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

sewellsgroup.comPage 19

DEFINITELY HIGHER HIGHER OR SAME SAME OR LOWER DEFINITELY LOWER

SALES INVENTORY PROFITS 0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

3%

25%

55%

17%

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

19%

53%

26%

2%

9%

59%

30%

2%

41%

41%

18%

0% 0%

54%31%

15%

§ Overall, the dealers expect the inventories to continue to be a concern, with 72% dealers expecting their inventory levels to be higher in the next six months, as against 64% dealers feeling the same in the previous quarter.

§ The above trend is reflected across all the segments.

§ Two wheeler dealers are the most affected with 82% expecting to carry higher inventories in the next six months as compared to 68% of passenger car and 54% of commercial vehicle dealer expecting to carry higher inventories in the next six months.

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

sewellsgroup.comPage 20

DEFINITELY HIGHER HIGHER OR SAME SAME OR LOWER DEFINITELY LOWER

7DEALERSHIP

MONTHS

EXPECTED

PERFORMANCEOVER NEXT SIX

SALES INVENTORY PROFITS 0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

20%

30%

38%

12%

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

13%

46%

25%

16%

12%

49%

28%

11% 18%

49%

20%

13%

0%

23%

23%

54%

§ Overall, the expectations of dealers about profits have shown improvement with 59% dealers expecting higher profits as compared to 50% at the end of last quarter.

§ The two wheeler dealers are most optimistic about profits, with 67% dealers expecting higher profits in next six months, as compared to 23% commercial dealers and 61% passenger car dealers expecting higher profits in the next six months.

§ There has been a marked improvement of dealers sentiments on profit in next six months in passenger cars and two wheeler segments. The commercial vehicle dealers sentiments have shown negative trend with only 23% expecting higher profits in next six months as compared to 57% feeling the same at the end of previous quarter.

PASSENGER CARS TWO WHEELERS COMMERCIAL VEHICLES

sewellsgroup.comPage 21

8MANPOWER

MONTHS

EXPECTED

STRENGTHOVER NEXT SIX

DEFINITELY HIGHER HIGHER OR SAME SAME OR LOWER DEFINITELY LOWER

0%

20%

40%

60%

80%

100%

% O

F R

ESP

ON

DEN

TS

6%

26%

47%

21%

OVERALL

END OF Q1-2014

END OF Q2-2014

END OF Q3-2014

END OF Q4-2014

19%

54%

25%

2%

15%

54%

31%

0%

29%

59%

12%

0%

8%

38%

31%

23%

§ Overall, the dealers are positive about their dealership sales performance (73% expecting increase in sales) in the next 6 months, they also expect their man power strength to go up (75% dealers expecting increase in manpower) in the next 6 months.

§ Both the passenger car (69%) and two wheeler (88%) dealers expect their manpower strength to increase in the next six months. This reflects the positive movement of sentiments of the dealers.

§ 46% of the commercial vehicle dealers expect increase in manpower in the next six months as compared to 63% at the end of previous quarter reflecting pessimistic outlook of this segment.

sewellsgroup.comPage 22

SSEWELLSGROUP

ABOUT

Sewells Group is a global consulting and outsourcing firm which specializes in the automotive retail industry. Our very reason for being in the business is to improve the performance of individuals and organizations in the automotive retail industry. We operate across the Asia-Pacific, Africa and Middle East regions.

Our in-depth subject matter expertise in this area and our deep engagements with many leading automotive brands make us a leader in our business. Our Integrated Dealer Performance Management Model has delivered exceptional success to leading OEMs across the world. Through our proven business management model, demonstrated competence solutions and process efficacy initiatives, we contribute meaningfully to our clients’ businesses.

For more information, visit www.sewellsgroup.com

Sewells Group Contacts:

JAYESH JAGASIAManaging Partner & CEO-Sewells Group IndiaE: [email protected]: +91 22 67354915, M: +91 9819765234

POOJA PEWEKARGroup Marketing Manager-Sewells GroupE:[email protected]: +91 22 67354914

sewellsgroup.comPage 23

DISCLAIMER

§ The contents of this report represent the opinion of survey respondents, and not that of Sewells Group, Sewells Group India, any of their subsidiary companies, or employees thereof.

§ The contents of this report and analysis of responses received in response to the quarterly Automotive Dealer Confidence Index (ADCI) survey are to be viewed as broad trends being observed, and not as definite commentary on the state of economy, state of business or policy framework of any automotive manufacturer and/or franchised automotive dealer group.

§ The contents of this report should not be viewed as commentary on the prospects of a particular manufacturer or brand as it is only intended to summarize the perceptions and opinions of respondents.

§ The contents of the report and analysis of responses should not be viewed in isolation, but in conjunction with the number of responses considered in the computation of the index and subsequent analysis.

§ ADCI methodology and this survey may be limited by significance of sample size or other statistical parameters. We advise reader discretion on matters such as these.

§ Sewells Group does not take the responsibility of or does not indemnify any user of the study against the impact of the decisions made taking into accounts the findings of this study.

© 2014 Sewells Group

ASIA PACIFIC - AFRICA - MIDDLE EAST

sewellsgroup.com