Embed Size (px)

Citation preview

www.pwc.com

Matthew PottleManaging Partner, PwC

Impact of regional developments on Mongolia’s coal market

PwC

Agenda

• Mine 2013

• Is demand still there?

• China – drivers of growth

• The future for coal

• Shifts in global manufacturing – automotive

• Summary

2

PwC

PwC: Mine 2013

“Over the past decade the mining industry has outperformed the broader equity markets, but this trend has recently changed. While mining stocks fell slightly in 2012, during the first four months of 2013 mining stocks were hammered, falling nearly 20%. The mining industry is facing a confidence crisis.”

However …..

• China will still grow

• Brazil, India and Indonesia will continue

to emerge

So:

The future demand for commodities still looks

healthy

3

PwC

Is demand still there?

• Long-term global demand fundamentals remain intact….

- Over the year, the global economy grew by just over 3%.

- Higher growth prospects will return from 2014.

• …but it won’t come from advanced economies…

- The US has projected real GDP growth of 2% in 2013, increasing to 3% by 2014.

- Europe will have real GDP growth of less than 2% for 5 years.

4

PwC

Is demand still there?

• …as global growth prospects depend on emerging and developing economies.

- Emerging and developing markets have become the world’s growth engine. Emerging economies will grow at around 6%.

- However, for mining the one that really counts is China. The Chinese economy will grow at 8%.

- Mining companies should not ignore the potential for further declines in real growth rates in China

5

PwC 6

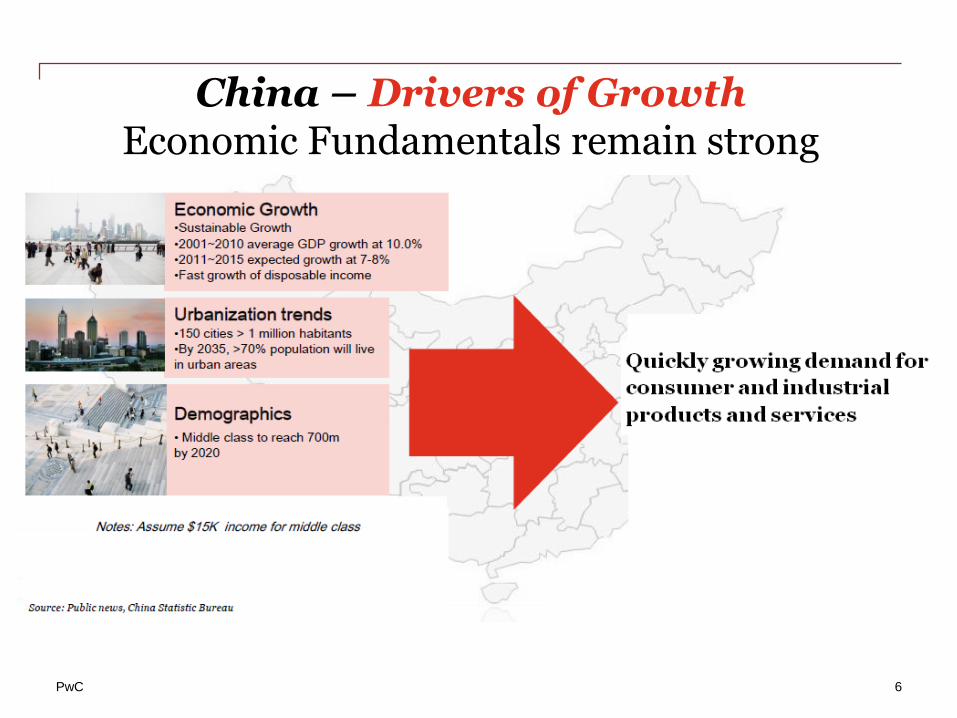

China – Drivers of GrowthEconomic Fundamentals remain strong

PwC 7

China – Drivers of Growth Urbanization drives growth

PwC

The future for coal…..

• The share of coal in world energy consumption is expected to remain fairly constant at 27% through to 2035.

• The global consumption of coal is expected to increase by 30% to 2035 (50% outside the OECD).

• The share of internationally traded coal remains at around 17% as China and India expand domestic production.

• Internationally traded coal will similarly increase by 50% outside the OECD.

• In China the amount of coal used in electricity generation will increase by 3% per year despite increased use of nuclear and other sources.

8

PwC

China’s ability to satisfy its own demand

• China is the world’s largest miner and by volume, in 2011 China produced almost 50% of the world’s coal.

• The Chinese mining industry is dominated by domestic players, but China lacks true domestic champions.

• While China Shenhua is the nation’s largest coal miner, it mines less than 10% of total Chinese coal.

• China is depleting its coal reserves at 1.9% annually.

9

PwC

Automotive – an example of the shift

• Cars are complex and expensive consumer products.

• Automotive is one of the most capital intensive and resource hungry manufacturing industries – steel, aluminum, copper.

• The automotive supply chain is complex – where car companies go others follow.

• What do the car companies think of China…..?

10

PwC

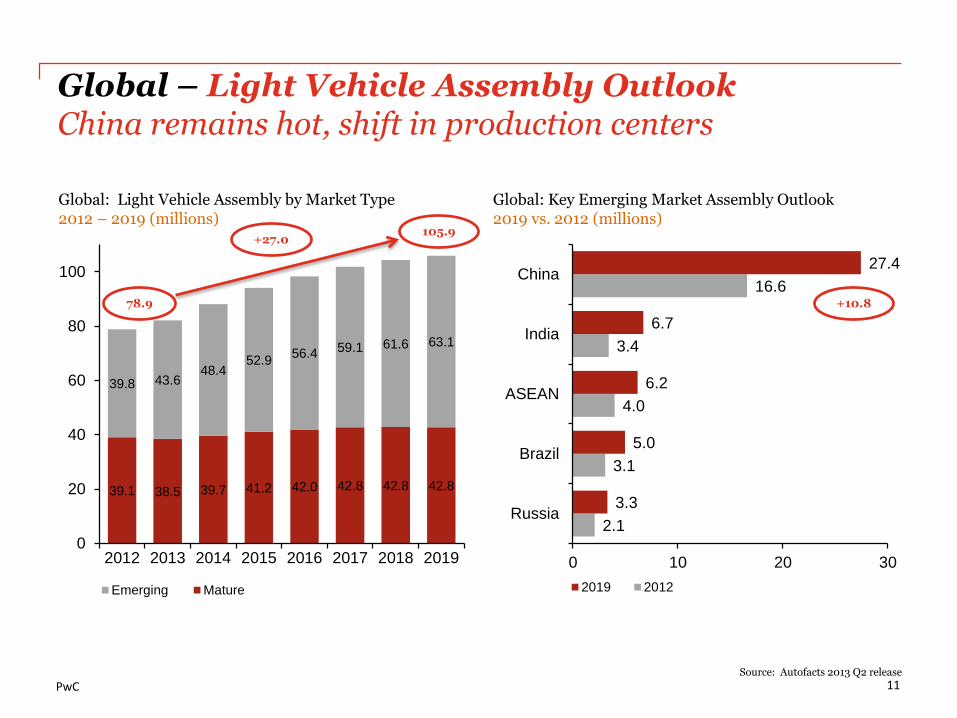

39.1 38.5 39.7 41.2 42.0 42.8 42.8 42.8

39.8 43.648.4

52.956.4 59.1 61.6 63.1

0

20

40

60

80

100

2012 2013 2014 2015 2016 2017 2018 2019

Emerging Mature

Global – Light Vehicle Assembly OutlookChina remains hot, shift in production centers

11

Global: Light Vehicle Assembly by Market Type2012 – 2019 (millions)

Global: Key Emerging Market Assembly Outlook2019 vs. 2012 (millions)

2.1

3.1

4.0

3.4

16.6

3.3

5.0

6.2

6.7

27.4

0 10 20 30

Russia

Brazil

ASEAN

India

China

2019 2012

Source: Autofacts 2013 Q2 release

78.9

+27.0105.9

+10.8

PwC

Global – China counts From west to east, north to south

12

There are plans to build or extend over additional 30 car factories in China in the next 5 Years.

The additional capacity is the equivalent of theentire car production of Western Europe.

PwC

In summary – good news for Mongolia

• The continued shift of industrial capacity and consumer spending to Asia and ……

• Further population movements to cities….

….. will underpin the future demand for energy and in particular coal

….. which cannot be satisfied by domestic production

• Mongolia’s geographical position will increasingly come into play as the global economy centres around China.

13