Embed Size (px)

Citation preview

Investor Presentation November 2014

2

High corporate governance standards

Novo Mercado (New Market) 1

100% tag along rights 2

Ordinary share only 3

30% of independent board members 4

Special Committee: 5

The custumers accumulate points buying products from our partners & flying with TAM and ONE WORD airline com-panies. They can convert the points in their loyalty programmes to Multiplus

The points are acumulated in the credit card. They can then choose to transfer the points to Multiplus or other loyalty programmes

The points can be redeemed for many products or services at coalition partners

The points are redeemed for an airline tickets

More than 15 million airline

tickets were redeemed during the last five years

Multiplus Business Model / Transaction Flow

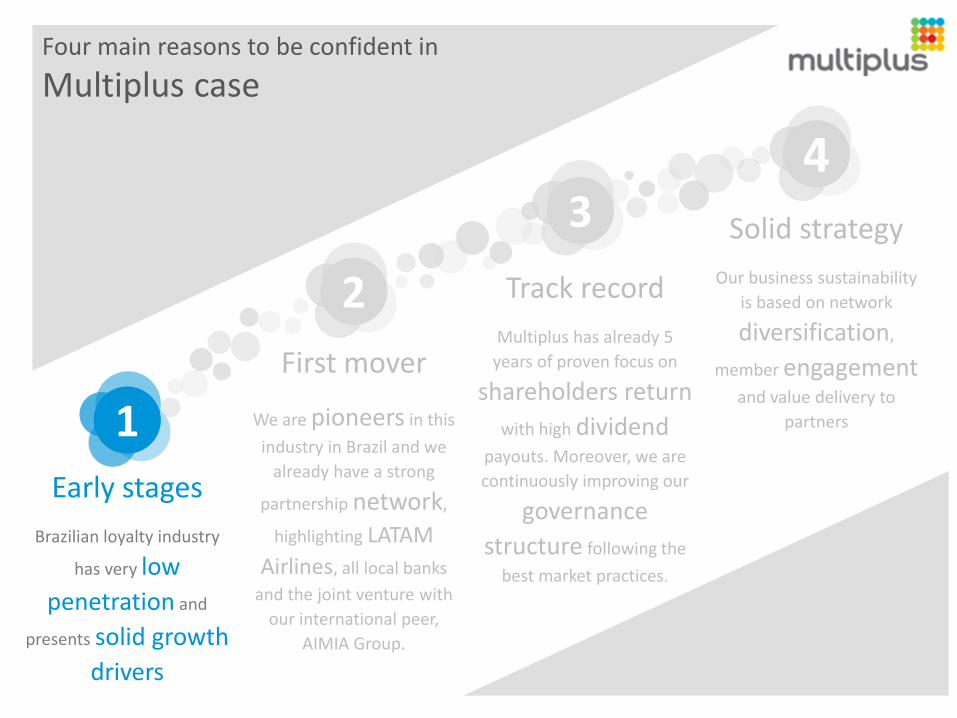

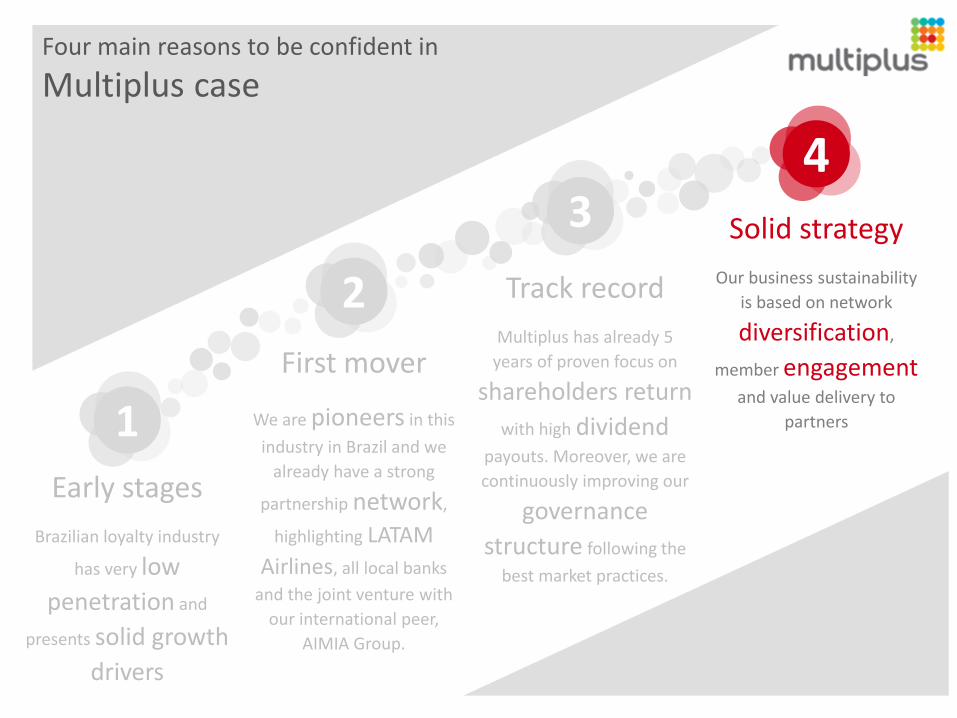

First mover

We are pioneers in this

industry in Brazil and we

already have a strong

partnership network,

highlighting LATAM

Airlines, all local banks

and the joint venture with

our international peer,

AIMIA Group.

2

3

Track record

Multiplus has already 5

years of proven focus on

shareholders return

with high dividend

payouts. Moreover, we are

continuously improving our

governance

structure following the

best market practices.

Early stages

Brazilian loyalty industry

has very low

penetration and

presents solid growth

drivers

1

4

Solid strategy

Our business sustainability

is based on network

diversification,

member engagement

and value delivery to

partners

Four main reasons to be confident in

Multiplus case

Brazilian loyalty industry is still in early stages

53.9%

25.3% 24.2% 20.9% 20.5%

14.4%

7.3% 6.3% 6.1% 4.8% 2.4%

Penetration of loyalty programs in total population (%)

Sources: loyalty programs websites and each country statistic data bureau (Updated in Jan/2014)

High growth potential

Average (ex-Multiplus): 18%

5

Multiple long term growth drivers

Credit Card usage

Expected double digit growth for next 3 years

Only 35% of customers understands that they have

enrolled in a bank loyalty program (vs. 31% in

2011)

Consumption

Possible high single digit growth for next 3 years

Loyalty culture still in the early stages

Air transportation

Latin America is the second fastest growing

region in RPK

Average trips per capita is only 0.5 in

Brazil vs more than 3.0 in mature markets

Wealth distribution

A/B classes expected to reach 15% in 2014 (vs

7% in 2003)

Multiplus network focus on A, B and C+

6

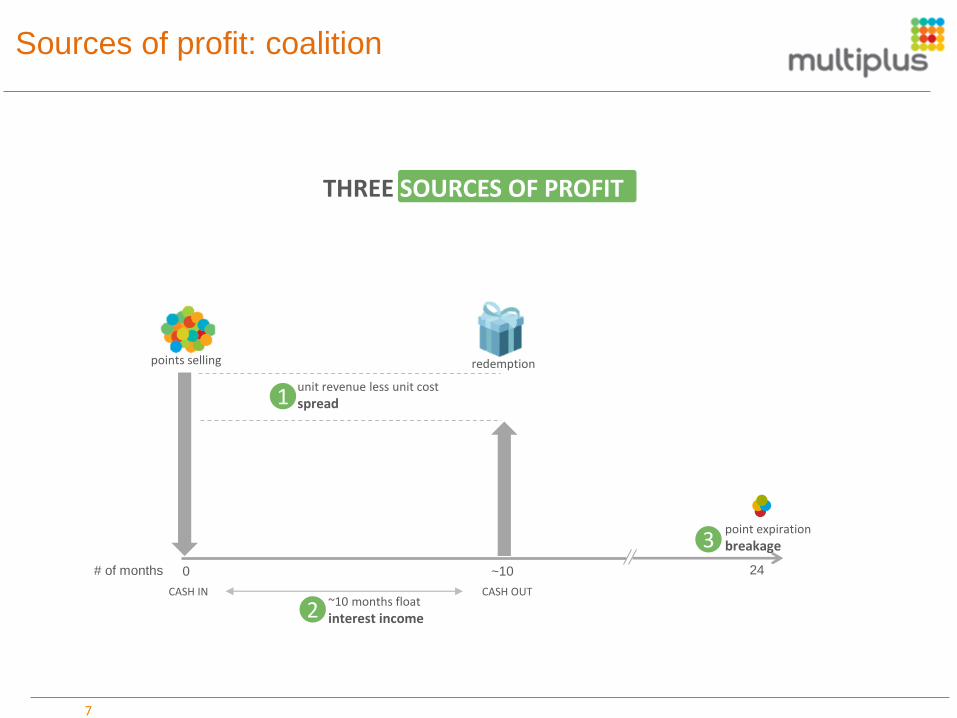

THREE SOURCES OF PROFIT

Sources of profit: coalition

# of months ~10 0 24

3

2

points selling redemption

unit revenue less unit cost

spread 1

CASH IN CASH OUT ~10 months float

interest income

point expiration

breakage

7

First mover

We are pioneers in this

industry in Brazil and we

already have a strong

partnership network,

highlighting LATAM

Airlines, all local banks

and the joint venture with

our international peer,

AIMIA Group.

2

3

Track record

Multiplus has already 5

years of proven focus on

shareholders return

with high dividend

payouts. Moreover, we are

continuously improving our

governance

structure following the

best market practices.

Early stages

Brazilian loyalty industry

has very low

penetration and

presents solid growth

drivers

1

4

Solid strategy

Our business sustainability

is based on network

diversification,

member engagement

and value delivery to

partners

Four main reasons to be confident in

Multiplus case

9

1993 Creation of TAM Fidelidade

2009 Spin-off from TAM Fidelidade

Feb/2010 Multiplus’ IPO

Oct/2011 Multiplus presents its new brand

Dec/2011 Multiplus becomes one of TOP 100 most liquid stocks in Bovespa

Aug/2010 New headquarters and IT loyalty platform

Mar/2012 Multiplus reaches 200 partners

Apr/2012 Multiplus reaches 10 mn members

May/2013 launched the new‖ campaign on several media vehicles

Jun/2013 Non-air redemptions reached 8% for the first time in a quarter

Oct/2013 Improved corporate governance structure

Created from TAM Fidelidade, Multiplus has already

five years of track record

Mar/2014 Multiplus mobile app for IOS and Android

Sept/2014 Multiplus launches "Points + Money“ and Multiplus Challenge (gamification)

9.4

10.9

12.2 11.9

12.9 13.3

2011 2012 2013 3Q13 2Q14 3Q14

10

Consistent network growth

Partners

13.3mn members can gather points

from several programs in one single

account

465 partners gain a powerful

support acquiring and retaining

clients

Members (mn)

190

369

472 466 477 465

2011 2012 2013 3Q13 2Q14 3Q14

Note: based 3Q14

Member base growth and profile

15%

56%

29%

14%

24%

Source: Social Policies Center of FGV-Rio

24%

61%

´

Coalition TAM

Coalition represents more than 80% of points accumulated

13

Strategic long-term agreement with TAM Airlines

15 years agreement automatically renewable for additional 5-year periods

Exclusive relationship

Points per seat vary according to flight fare with 100% availability,

improving Multiplus competitive advantage

up to 360 days before flight date

fee exemptions, lowered points requirement, complimentary

upgrades and up to 100% bonus points

High recognition to premium clients

High flexibility

Superior frequent flyer program

lower earn-to-burn ratios redemptions via TAM, LAN and their airline partners

Wide redemption window

Pricing model methodology with TAM Airlines U

nit

co

st (

R$

)

Jun/2013 ~Oct/2014

Cap

Floor

Previous model Setup period New pricing model

• Multiplus pays discounted

market price per seat

• 5% cap and floor protect margin

and guarantee business

sustainability

• Data gathering of

fares available

at redemption

moment

• Discount

measurement

• Unit cost set according to a

combination of TAM’s

marginal cost and revenue

displacement

• Short term fluctuations due to

TAM’s promotional activity

Average

Air tickets market price

Discounted market price

Long haul and South America flights priced in USD

12 months data gathering

Multiplus` implicit discount

ILLUSTRATIVE

14

16

Strong partnership network

Accrual partners Coalition partners Redemption partners

17

Non-air redemptions

12% of

the total redemption in 3Q14

• More affordable redemption options • More competitive portfolio of products and services • Improved members´ experience • Additional liquidity • Better profitability

% o

f t

ota

l red

emp

tio

n

2010 2011 2012 2013 2014

0.4%

2.1%

5.4%

9.2%

18

Innovative partnership

23

•

•

•

•

•

•

25

More than 80% of the costumers prefer to shop in Loyalty Programs

Source: Research made by Technology Advice, in EUA

82.4%

17.6%

Don’t consider relevant

Adding value to partners: sales increase

26

Solid relationship with banks

bonus points per each new credit card activated

Targeted redemption offers

1 Activation

bonus points according to the volume of points transferred

segmented offers to engage an specific member group

2 Spending

3 Targeting

First mover

We are pioneers in this

industry in Brazil and we

already have a strong

partnership network,

highlighting LATAM

Airlines, all local banks

and the joint venture with

our international peer,

AIMIA Group.

2

3

Track record

Multiplus has already 5

years of proven focus on

shareholders return

with high dividend

payouts. Moreover, we are

continuously improving our

governance

structure following the

best market practices.

Early stages

Brazilian loyalty industry

has very low

penetration and

presents solid growth

drivers

1

4

Solid strategy

Our business sustainability

is based on network

diversification,

member engagement

and value delivery to

partners

Four main reasons to be confident in

Multiplus case

1,119

1,525

1,871 2,009

1,529 1,560

536 472

550

2010 2011 2012 2013 9M13 9M14 3Q13 2Q14 3Q14

28

Gross Billings (BRL mn) Points issued (bn)

53.2

76.3

85.2 85.3

65.2 65.4

22.6 20.1 23.2

2010 2011 2012 2013 9M13 9M14 3Q13 2Q14 3Q14

Sales growth: consistent track record

*Includes bonus points

29

Net Revenue (BRL mm) Net income (BRL mm)

Financial Results

470

1,247

1,476

1,651

1,243 1,343

471 417

485

2010 2011 2012 2013 9M13 9M14 3Q13 2Q14 3Q14

118.4

274.2

224.3 232.1

166.3

241.4

62.2 80.1 86.7

2010 2011 2012 2013 9M13 9M14 3Q13 2Q14 3Q14

41.6% 32.5% 25.8% 25.7%

Gross margin Net margin

25.2% 22.0% 15.2% 14.1% 13.4% 13.2% 25.6% 29.3% 23.8% 31.2% 29.1% 18.2% 18.4% 19.2%

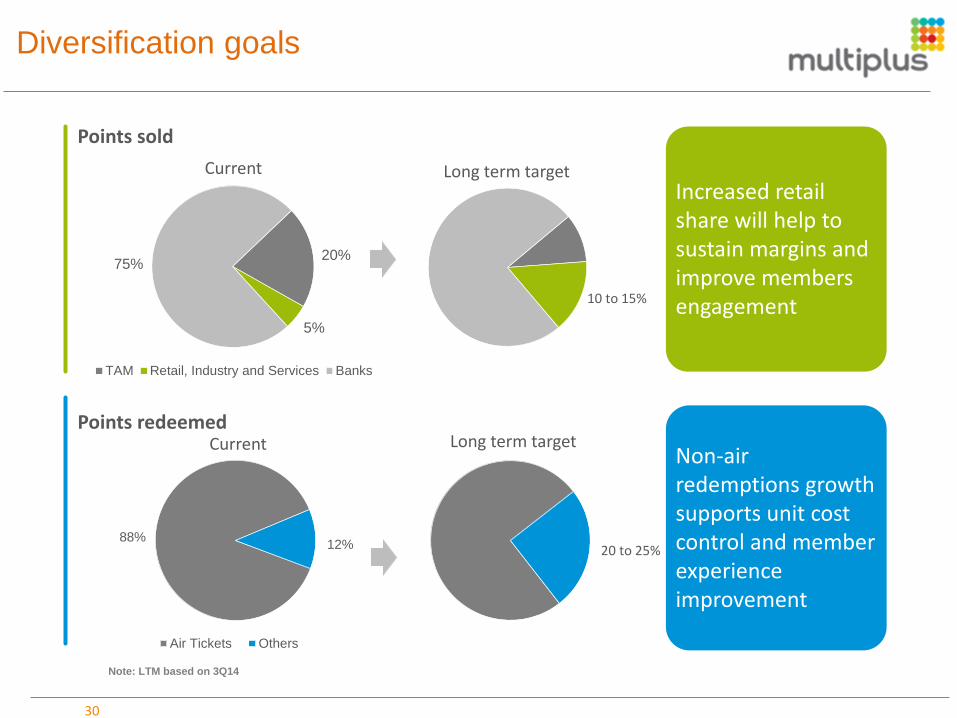

30

Diversification goals

88% 12%

Current

Air Tickets Others

20%

5%

75%

Current

TAM Retail, Industry and Services Banks

Note: LTM based on 3Q14

Long term target

Long term target

10 to 15%

20 to 25%

Points redeemed

Points sold

Increased retail share will help to sustain margins and improve members engagement

Non-air redemptions growth supports unit cost control and member experience improvement

31

Breakage rate (%)

22.6% 24.1%

21.0%

18.5% 17.7% 17.9% 17.7%

2010 2011 2012 2013 3Q13 2Q14 3Q14

Non-air redemptions (%)

Breakage rate: gradual decline as expected while

non-air redemptions becomes robust

0.4%

2.1%

5.4%

9.2% 9.2%

10.2%

13.9%

10.7%

12.2%

2010 2011 2012 2013 9M13 9M14 3Q13 2Q14 3Q14

32

Cash generation and shareholders’ return

FCF* (BRL mn)

589.0

460.6 418.1

452.6

379.9

263.0

135.9

71.9 91.4

2010 2011 2012 2013 9M13 9M14 3Q13 2Q14 3Q14

*Excluding Dividends, Interest on Capital and variations of Prepaid Expenses and Capital (2012 and 2013 are adjusted with R$ 71.3 of anticipated settlement in Accounts Payable)

First mover

We are pioneers in this

industry in Brazil and we

already have a strong

partnership network,

highlighting LATAM

Airlines, all local banks

and the joint venture with

our international peer,

AIMIA Group.

2

3

Track record

Multiplus has already 5

years of proven focus on

shareholders return

with high dividend

payouts. Moreover, we are

continuously improving our

governance

structure following the

best market practices.

Early stages

Brazilian loyalty industry

has very low

penetration and

presents solid growth

drivers

1

4

Solid strategy

Our business sustainability

is based on network

diversification,

member engagement

and value delivery to

partners

Four main reasons to be confident in

Multiplus case

Clear prioritization of segments

Network diversification

Anticipate members behaviour

(CRM, analysis of customer

profiles)

Better experience and more members´

engagement

Focus on adding value to comercial

partners

Redemptions diversification,

leading to higher

margins

Solid strategy in force

35

Disclaimer

This notice may contain estimates for future events. These estimates merely reflect the expectations of the Company’s management, and involve risks and uncertainties. The Company is not responsible for investment operations or decisions taken based on information contained in this communication. These estimates are subject to changes without prior notice. This material has been prepared by Multiplus S.A. (“Multiplus“ or the “Company”) includes certain forward-looking statements that are based principally on Multiplus’ current expectations and on projections of future events and financial trends that currently affect or might affect Multiplus’ business, and are not guarantees of future performance. They are based on management’s expectations that involve a number of business risks and uncertainties, any of each could cause actual financial condition and results of operations to differ materially from those set out in Multiplus’ forward-looking statements. Multiplus undertakes no obligation to publicly update or revise any forward looking statements. This material is published solely for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Likewise it does not give and should not be treated as giving investment advice. It has no regard to the specific investment objectives, financial situation or particular needs of any recipient. No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein. It should not be regarded by recipients as a substitute for the exercise of their own judgment.

Appendix

37

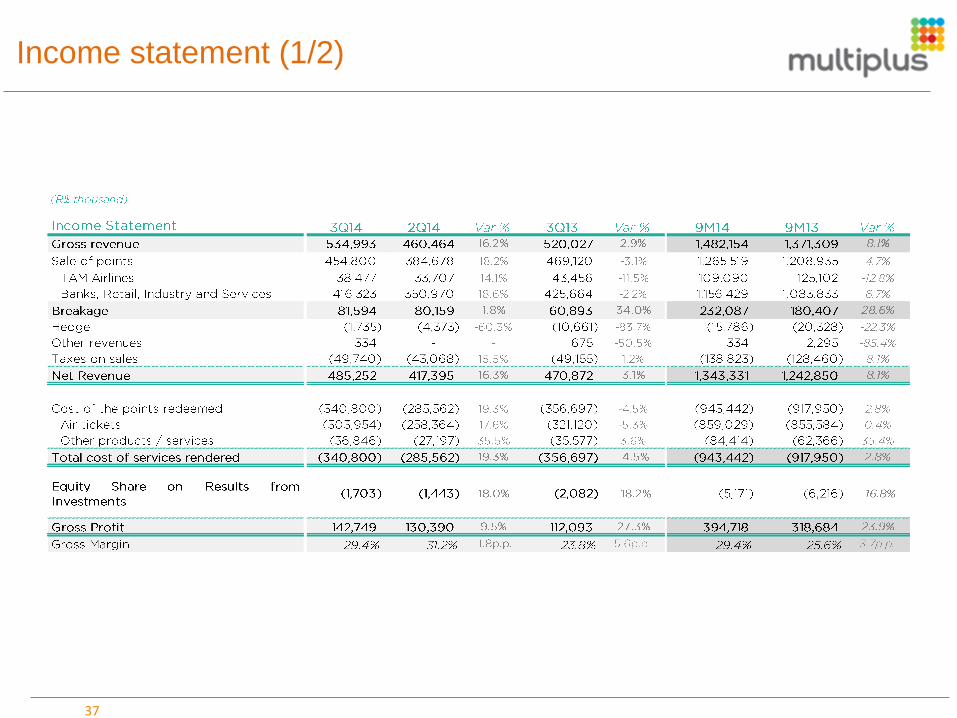

Income statement (1/2)

38

Income statement (2/2)

39

Balance sheet: assets

40

Balance sheet: liabilities and shareholders' equity

Thank you! Contact IR Team +55 11 5105-1847 [email protected] www.pontosmultiplus.com.br/ir