Embed Size (px)

Citation preview

Revenue from Contracts with

Customers

BFRS 15

Membership and Association: Member of Council of ICAB (Highest Governing Body) Ex Member of Dhaka Regional Committee of ICAB Member of Institute of Internal Auditors - Bangladesh Life member of Gulshan North Club Life member of Banani Society Member Gulshan Health Club Active Rotarian.

As part of professional development programmers, Mr. Mahamud participated in large number of

training programs, seminars and workshops in the area of Financial Planning, Business

Integration, Merger & Takeover and Leadership & Change Management & IFRS in Singapore,

Thailand, India, Sri Lanka, Malaysia, UK and Indonesia etc.

Mr. Mahamud conducted a number oftraining programs on IFRS, ContemporaryAssurances & Corporate Reporting issues,Leadership & Business PerformanceEvaluation for participant from variousleading MNCs and local conglomerates,Bangladesh Bank, National Board of Revenue& University Teachers. As a visiting resourceperson, he also taught in some of the leadingbusiness schools/Institute (ICAB/NationalUniversity).

Mahamud Hosain FCA is business graduate, fellow member of the Institute ofChartered Accountants of Bangladesh [ICAB] and has diversified experience ofabove 13 years in financial planning, financial system & control design, advisoryservices in business integration & transition and project management

Paper Presenter

Revenue recognition and measurement is crucial to reporting financial

performance.

An effective and credible accounting standard on revenue is essential to ensure capital market confidence

Convergence between GAAP & IFRS

BFRS 15 ….. Business Context & background

Mahamud Hosain FCA

BFRS 15 …..replace/supersedes

BFRS 15 replaces/supersedes the following

standards and interpretations:

BAS 11 Construction Contracts [1979]

BAS 18 Revenue [1982]

IFRIC 13 Customer Loyalty Programmes

IFRIC 15 Agreements for the Construction of Real Estate

IFRIC 18 Transfers of Assets from Customers

SIC 31 Revenue - Barter Transactions Involving Advertising Services,

Mahamud Hosain FCA

Major Changes from Earlier Standards

Current Requirements New Requirements

BAS 11: Construction ContractsBAS 18: Sales of GoodsBAS 18: Sales of ServicesIFRIC 15 : Real Estate Sales

BFRS 15: Revenue from Customer Contracts

Over time or at a point in time

BAS 18: RoyaltiesBFRS 15: New guidelines on royalties revenue

IFRIC 13: Customer Loyalties Program BFRS 15 New guidelines with option of additional goods/services & breakageIFRIC 18 : Transfer of Assets from

CustomerSIC 31 : Advertising Barter Transactions

BFRS 15: Guidance on non cash considerations

Previously less guidelines on cost of obtaining and fulfilling a contract

BFRS 15: New guidance on cost of obtaining and fulfilling a contract

BAS 18: InterestBAS 18: Dividend

BAS 39: InterestBFRS 9: Dividend

Mahamud Hosain FCA

to

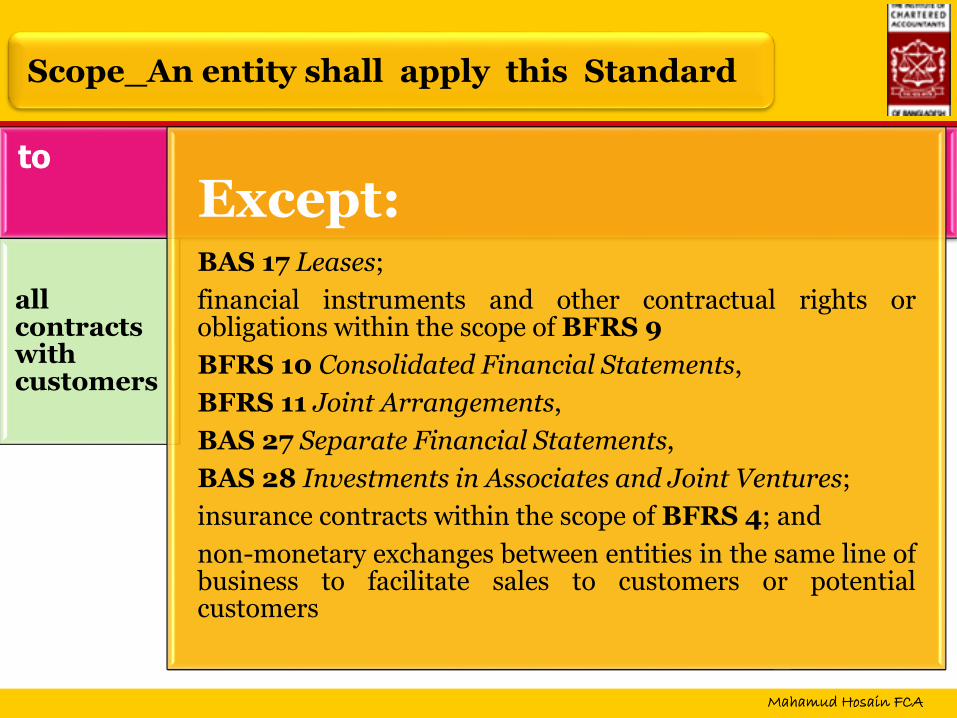

all contracts with customers

Except:BAS 17 Leases;

financial instruments and other contractual rights orobligations within the scope of BFRS 9

BFRS 10 Consolidated Financial Statements,

BFRS 11 Joint Arrangements,

BAS 27 Separate Financial Statements,

BAS 28 Investments in Associates and Joint Ventures;

insurance contracts within the scope of BFRS 4; and

non-monetary exchanges between entities in the same line ofbusiness to facilitate sales to customers or potentialcustomers

Scope_An entity shall apply this Standard

Mahamud Hosain FCA

- provides a single, principles based five-step model ;

Specific & improved guidelines of BFRS 15

- guide how and when an entity shall recognise revenue;

- require more informative, relevant disclosures.

- Methodical approach (similar to FASB Guidelines)

Mahamud Hosain FCA

However, Application of this guidance will depend on the facts

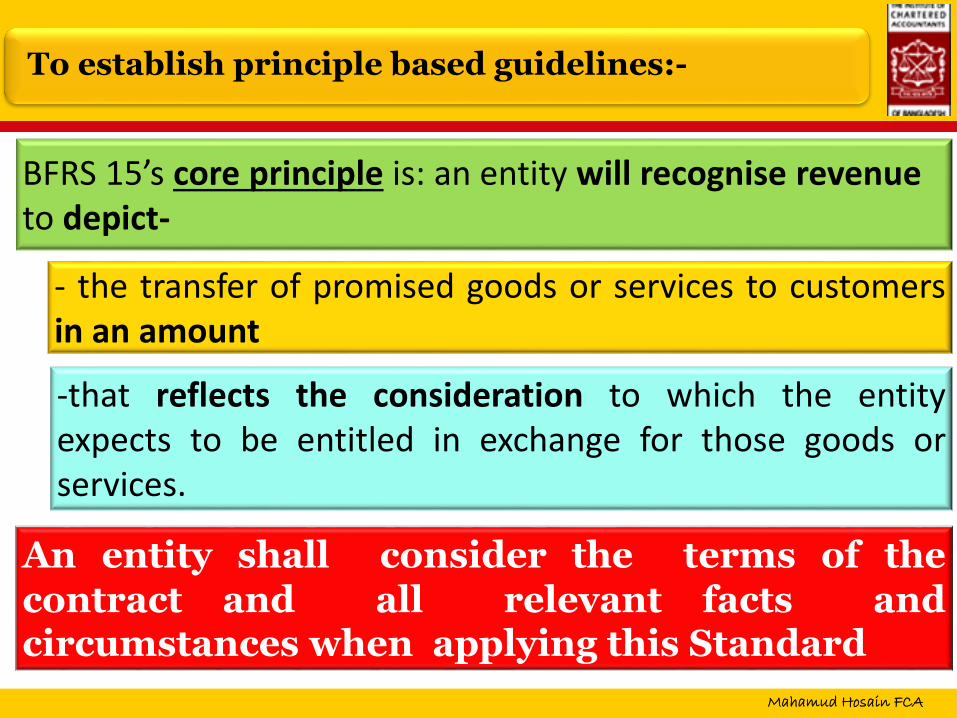

and circumstances present in a contract with a customer and

will require the exercise of judgment.

BFRS 15’s core principle is: an entity will recognise revenueto depict-

To establish principle based guidelines:-

- the transfer of promised goods or services to customersin an amount

-that reflects the consideration to which the entityexpects to be entitled in exchange for those goods orservices.

An entity shall consider the terms of thecontract and all relevant facts andcircumstances when applying this Standard

Mahamud Hosain FCA

the nature;

the amount;

uncertainty of revenue; and

cash flows arising from a contract with a customer.[employs significant emphasis on cash flow]

Value addition of BFRS 15 for disclosures..

It establishes the principles that an entity shall apply to report useful information to users of financial statements about :-

IASB has made clear cut guidelines in respect ofcoverage by another standards

Timing;

Mahamud Hosain FCA

Definition…

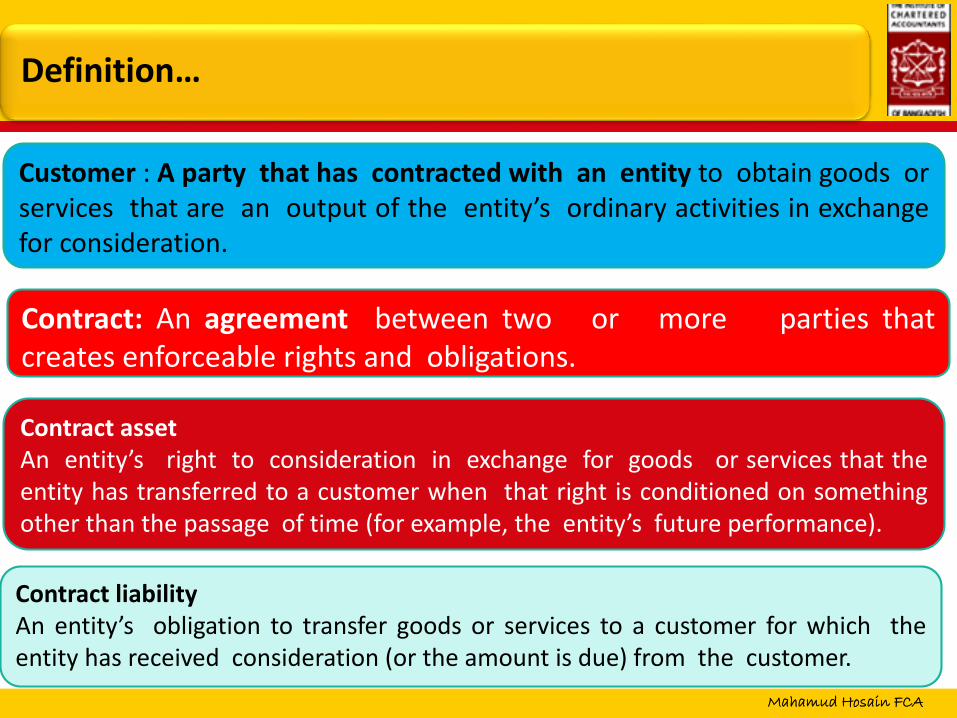

Contract liabilityAn entity’s obligation to transfer goods or services to a customer for which theentity has received consideration (or the amount is due) from the customer.

Contract assetAn entity’s right to consideration in exchange for goods or services that theentity has transferred to a customer when that right is conditioned on somethingother than the passage of time (for example, the entity’s future performance).

Customer : A party that has contracted with an entity to obtain goods orservices that are an output of the entity’s ordinary activities in exchangefor consideration.

Contract: An agreement between two or more parties thatcreates enforceable rights and obligations.

Mahamud Hosain FCA

Definition…

Stand-alone selling price (of a good or service)The price at which an entity would sell a promised good or service separately to a customer

Transaction priceThe amount of consideration to which an entity expects to be entitled in exchange fortransferring promised goods or services to a customer, excluding amounts collected on behalfof third parties.

Performance obligationA promise in a contract with a customer to transfer to the customer either:• a good or service (or a bundle of goods or services) that is distinct; or• a series of distinct goods or services that are substantially the same and that have the

same pattern of transfer to the customer.

Mahamud Hosain FCA

Identify the contract(s) with a customer

Identify the performance obligations in the contract

Determine the transaction price (Amount)

Allocate the transaction price to the performance obligations in the contract (How much)

Recognise revenue when (or as) the entity satisfies a performance obligation

Five steps model….

Step 1

Step 2

Step 3

Step 4

Step 5

Mahamud Hosain FCA

the contract has been approved by the parties to the contract

the contract has commercial substance [(ie the risk, timing]

it is probable that consideration is collectible

Step 1

the payment terms for the goods or services to betransferred can be identified :Definite

Identify the contract with the customer

An entity shall account for a contract with a customer only whenall of the following criteria are met:-

each party’s rights in relation to the goods or services whichto be transferred can be identified: Definite

Mahamud Hosain FCA

a good or service (or a bundle of goods or services)that is distinct; or

Step 2

a series of distinct goods or services that aresubstantially the same and that have the samepattern of transfer to the customer

Identifying performance obligations

At contract inception, an entity shall :-(i) assess the goods or services promised in a contract with a

customer; &

(ii) identify as a performance obligation each promise to transfer tothe customer either

Mahamud Hosain FCA

The transaction price is the amount to which an entity expects to beentitled in exchange for the transfer of goods and services. When makingthis determination, an entity will consider past customary businesspractices

Step 3

Where a contract contains elements of variable consideration, theentity will estimate the amount of variable consideration to whichit will be entitled under the contract.

Determine the transaction price

When (or as) a performance obligation is satisfied, an entity shalldetermine the attributable portion of transaction price to recogniserevenue

uncertainty relating to variable consideration shall be taken underconsideration by limiting the amount of variable consideration that can berecognised.

Mahamud Hosain FCA

To meet the allocation objective, an entity shall allocate the transaction price toeach performance obligation identified in the contract on a relative stand-aloneselling price

Step 4

Allocating the transaction price to performance obligations

when allocating the transaction price it shall be allocated to each performance obligation (ordistinct good or service) in an amount that depicts the amount of consideration to which theentity expects to be entitled in exchange for transferring the promised goods or services to thecustomer

Where consideration is paid in advance or in arrears, the entity will need to considerwhether the contract includes a significant financing arrangement and, if so, adjustfor the time value of money

Mahamud Hosain FCA

Control of an asset is defined as the ability to direct the use of and obtainsubstantially all of the remaining benefits from the asset. This includes the ability toprevent others from directing the use of and obtaining the benefits from the asset.

Step 5

Recognise revenue when (or as) the entity satisfies a performance obligation

Revenue is recognised as control is passed, either over time or at apoint in time.

using the asset to produce goods or provide services;

The benefits related to the asset are the potential cash flows that may be obtaineddirectly or indirectly. These include, but are not limited to:

using the asset to enhance the value of other assets;

using the asset to settle liabilities or to reduce expenses

selling or exchanging the asset

pledging the asset to secure a loan; and

holding the asset.

Mahamud Hosain FCA

Presentation

An entity shall present the contract in the statement of financialposition as a contract asset or a contract liability

the entity shall present the contract as a contract liabilitywhen the payment is made or the payment is due (whichever isearlier).

the entity shall present the contract as a contract asset, Ifan entity performs its obligation before the customer paysconsideration or before payment is due

Disclosure of impairment

Any difference between the initial recognition of a receivable andthe corresponding amount of revenue recognised should also bepresented as an expense, for example, an impairment loss

Mahamud Hosain FCA

Disclosure

Contracts with customers:An entity shall disclose all of the following amounts for the reporting period unless those amounts are presented separately in the statement of comprehensive income in accordance with other Standards:

revenue recognised from contracts with customers, which the entity shall disclose separately from its other sources of revenue; and

any impairment losses recognised (in accordance with BFRS 9) on any receivables or contract assets arising from an entity’s contracts with customers, which the entity shall disclose separately from impairment losses from other contracts.

Mahamud Hosain FCA

Presentation

When either party to a contract has performed, an entity shall present the contract in the statement of financial position as a contract asset or a contract liability

If a customer pays consideration, or an entity has a right to an amount of consideration that is unconditional (ie a receivable), before the entity transfers a good or service to the customer, the entity shall present the contract as a contract liability when the payment is made or the payment is due (whichever is earlier).

If an entity performs by transferring goods or services to a customer before the customer pays consideration or before payment is due, the entity shall present the contract as a contract asset, excluding any amounts presented as a receivable.

This Standard uses the terms ‘contract asset’ and ‘contract liability’ but does not prohibit an entity from using alternative descriptions in the statement of financial position. If an entity uses an alternative description for a contract asset, the entity shall provide sufficient information for a user of the financial statements to distinguish between receivables and contract assets.

Mahamud Hosain FCA

Contract balances; opening, closing & movements

Other major Disclosure…

An entity shall disclose all of the following:

Performance obligations;

Transaction price allocated to the remaining performance obligations

Determining the transaction price and the amounts allocated to performance obligations

Assets recognised from the costs to obtain or fulfil a contract with a customer

Determining the timing of satisfaction of performance obligations

Practical expedients/Measure: If an entity elects to use the practical expedient the entity shall disclose that fact.

Mahamud Hosain FCAMahamud Hosain FCA

Questions

Answers

&Mahamud Hosain FCA

Thank You!

Thank You!

Mahamud Hosain FCA

![download.microsoft.comdownload.microsoft.com/.../Files/4000008234/Sagacent_Windows… · Web viewPlastic parts contain < 1000 ppm (0.1%) of bromine [if the Br source is from BFRs]](https://img.pdfslide.net/doc/110x75/5e7b398299493e4508306f5c/web-view-plastic-parts-contain-1000-ppm-01-of-bromine-if-the-br-source.jpg)

![$ EDUCATIONAL FACILITIES REVENUE [AND REVENUE REFUNDING… · EDUCATIONAL FACILITIES REVENUE [AND REVENUE REFUNDING] ... Educational Facilities Revenue [and Revenue ... Aeronautical](https://img.pdfslide.net/doc/110x75/5b16e1207f8b9a686d8e7aa7/-educational-facilities-revenue-and-revenue-refunding-educational-facilities.jpg)