Embed Size (px)

Citation preview

2017 Housing Market Forecast

Connect on the Road Los AngelesOctober 18, 2016

Leslie Appleton-Young Chief Economist & Vice President

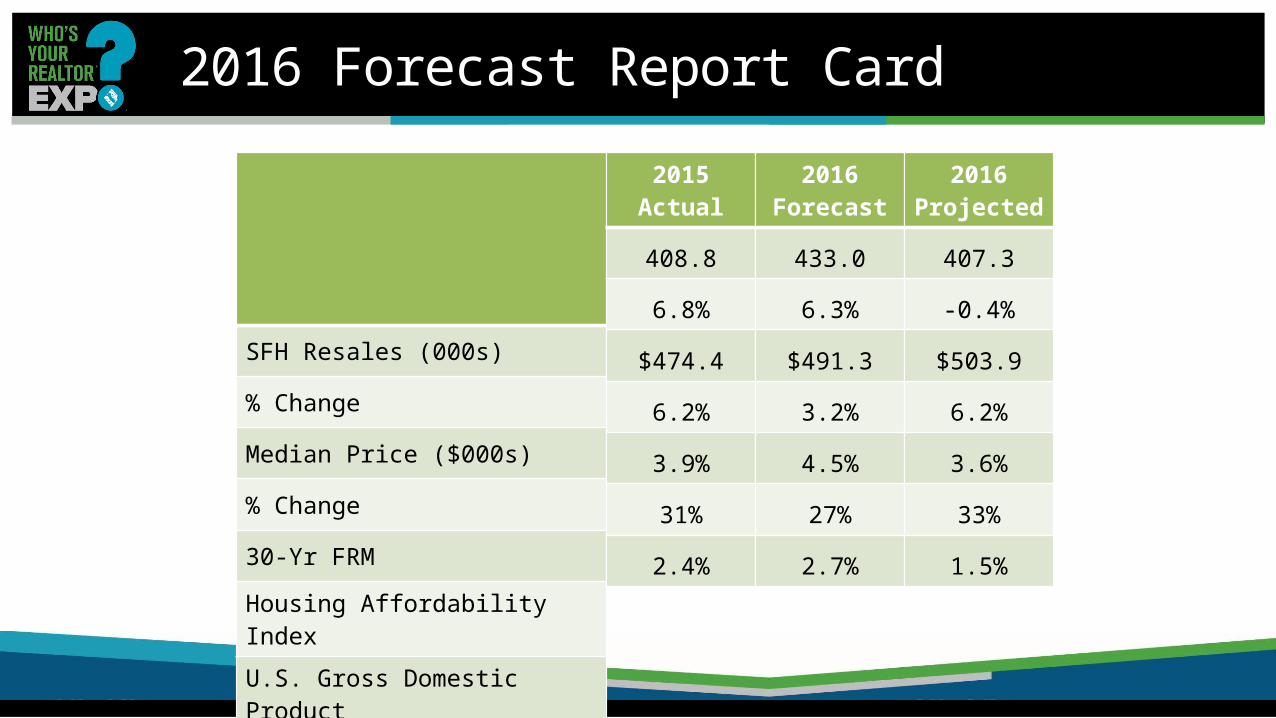

2016 Forecast Report Card SFH Resales (000s)

% Change

Median Price ($000s)

% Change

30-Yr FRM

Housing Affordability Index

U.S. Gross Domestic Product

2015 Actual

408.8

6.8%

$474.4

6.2%

3.9%

31%

2.4%

2016 Forecast

433.0

6.3%

$491.3

3.2%

4.5%

27%

2.7%

2016 Projected

407.3

-0.4%

$503.9

6.2%

3.6%

33%

1.5%

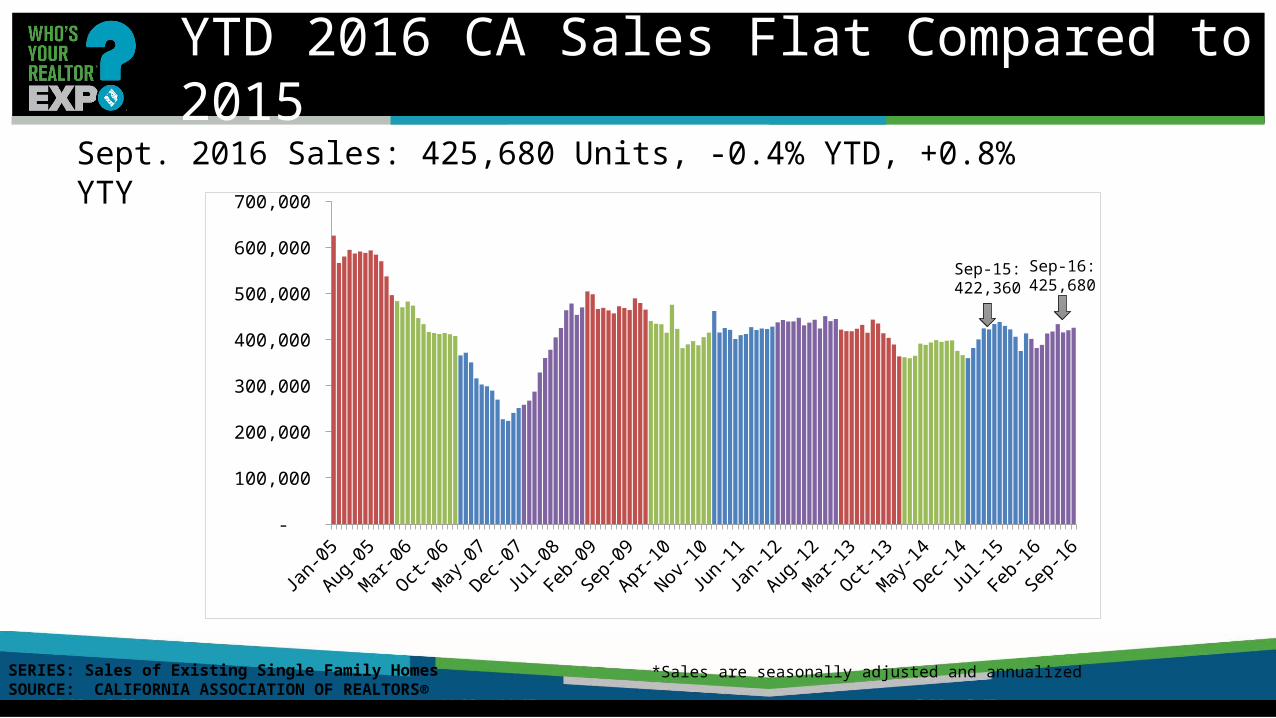

YTD 2016 CA Sales Flat Compared to 2015

Sept. 2016 Sales: 425,680 Units, -0.4% YTD, +0.8% YTY

Jan-05

Sep-0

5

May-06

Jan-07

Sep-0

7

May-08

Jan-09

Sep-0

9

May-10

Jan-11

Sep-1

1

May-12

Jan-13

Sep-1

3

May-14

Jan-15

Sep-1

5

May-16

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

*Sales are seasonally adjusted and annualized SERIES: Sales of Existing Single Family HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Sep-16: 425,680

Sep-15: 422,360

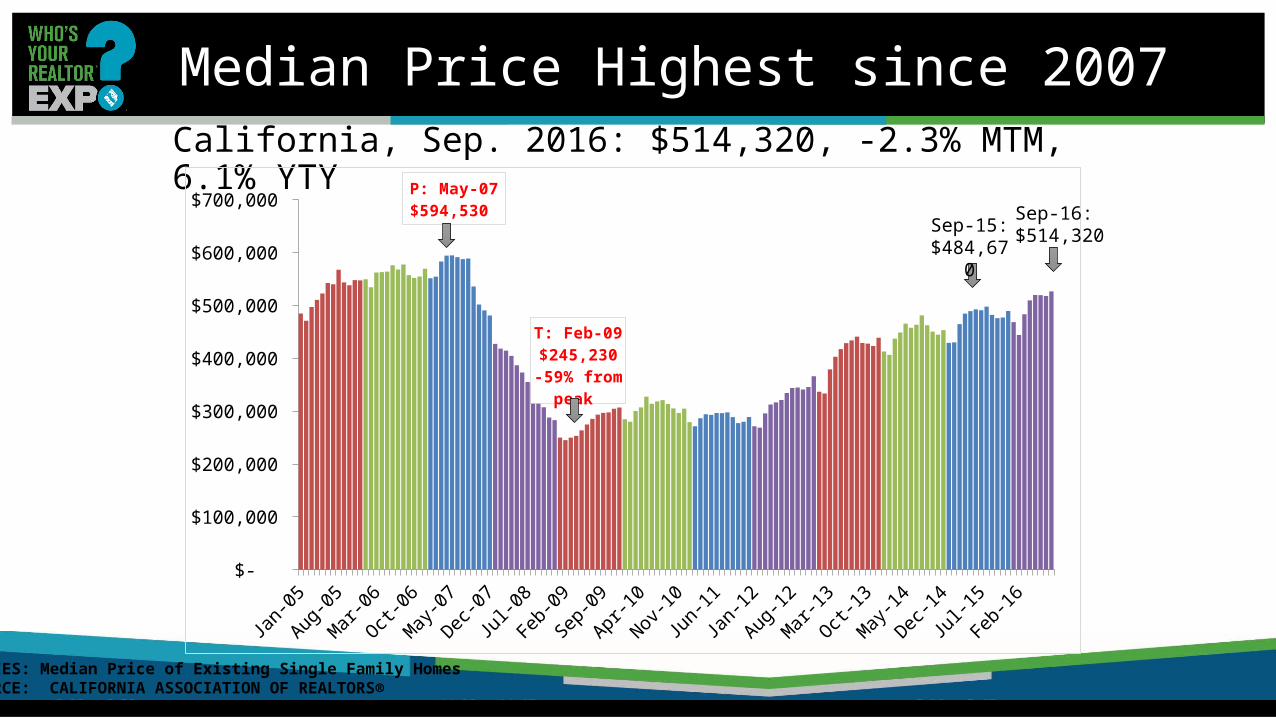

Median Price Highest since 2007California, Sep. 2016: $514,320, -2.3% MTM, 6.1% YTY

Jan-05

Sep-0

5

May-06

Jan-07

Sep-0

7

May-08

Jan-09

Sep-0

9

May-10

Jan-11

Sep-1

1

May-12

Jan-13

Sep-1

3

May-14

Jan-15

Sep-1

5

May-16

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000 P: May-07$594,530

T: Feb-09$245,230-59% from

peak

SERIES: Median Price of Existing Single Family HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Sep-16: $514,320Sep-15:

$484,670

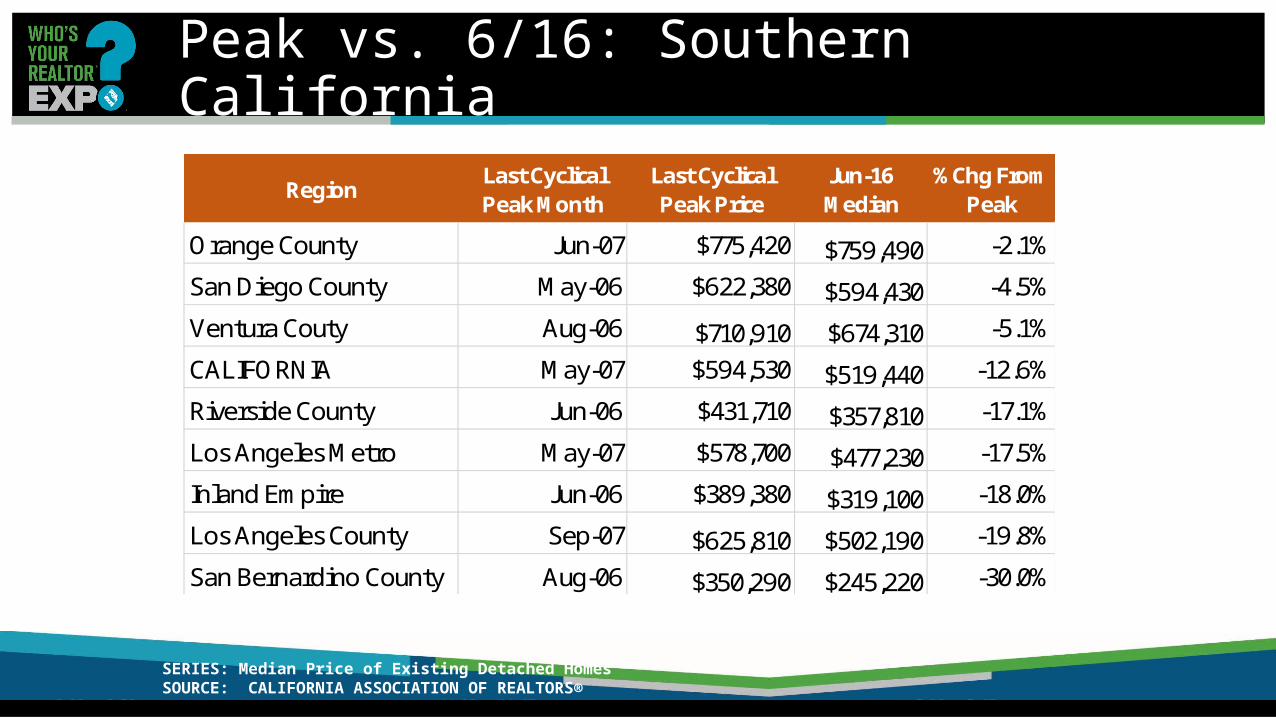

Peak vs. 6/16: Southern California

SERIES: Median Price of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Region Last Cyclical Peak Month

Last Cyclical Peak Price

Jun-16 Median

%Chg From Peak

Orange County Jun-07 $775,420 $759,490 -2.1%San Diego County May-06 $622,380 $594,430 -4.5%Ventura Couty Aug-06 $710,910 $674,310 -5.1%CALIFORNIA May-07 $594,530 $519,440 -12.6%Riverside County Jun-06 $431,710 $357,810 -17.1%Los Angeles Metro May-07 $578,700 $477,230 -17.5%Inland Empire Jun-06 $389,380 $319,100 -18.0%Los Angeles County Sep-07 $625,810 $502,190 -19.8%San Bernardino County Aug-06 $350,290 $245,220 -30.0%

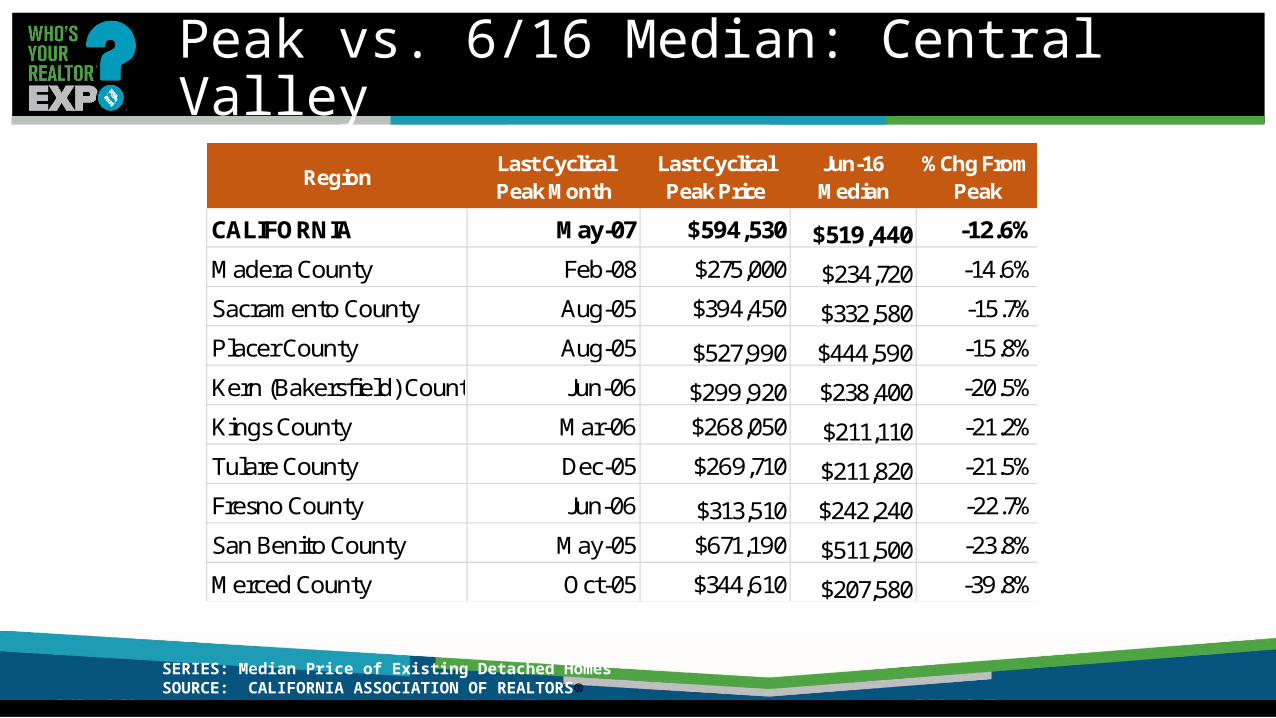

Peak vs. 6/16 Median: Central Valley

SERIES: Median Price of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Region Last Cyclical Peak Month

Last Cyclical Peak Price

Jun-16 Median

%Chg From Peak

CALIFORNIA May-07 $594,530 $519,440 -12.6%Madera County Feb-08 $275,000 $234,720 -14.6%Sacramento County Aug-05 $394,450 $332,580 -15.7%Placer County Aug-05 $527,990 $444,590 -15.8%Kern (Bakersfield) County Jun-06 $299,920 $238,400 -20.5%Kings County Mar-06 $268,050 $211,110 -21.2%Tulare County Dec-05 $269,710 $211,820 -21.5%Fresno County Jun-06 $313,510 $242,240 -22.7%San Benito County May-05 $671,190 $511,500 -23.8%Merced County Oct-05 $344,610 $207,580 -39.8%

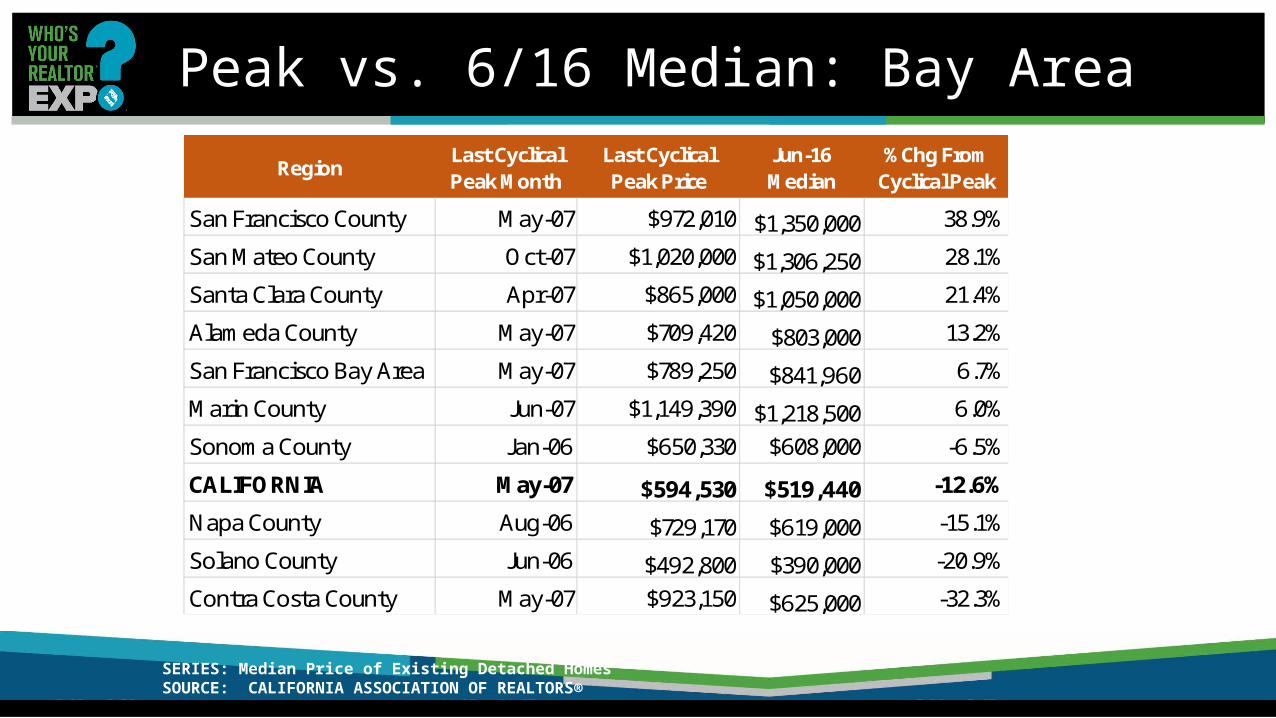

Peak vs. 6/16 Median: Bay Area

SERIES: Median Price of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Region Last Cyclical Peak Month

Last Cyclical Peak Price

Jun-16 Median

%Chg From Cyclical Peak

San Francisco County May-07 $972,010 $1,350,000 38.9%San Mateo County Oct-07 $1,020,000 $1,306,250 28.1%Santa Clara County Apr-07 $865,000 $1,050,000 21.4%Alameda County May-07 $709,420 $803,000 13.2%San Francisco Bay Area May-07 $789,250 $841,960 6.7%Marin County Jun-07 $1,149,390 $1,218,500 6.0%Sonoma County Jan-06 $650,330 $608,000 -6.5%CALIFORNIA May-07 $594,530 $519,440 -12.6%Napa County Aug-06 $729,170 $619,000 -15.1%Solano County Jun-06 $492,800 $390,000 -20.9%Contra Costa County May-07 $923,150 $625,000 -32.3%

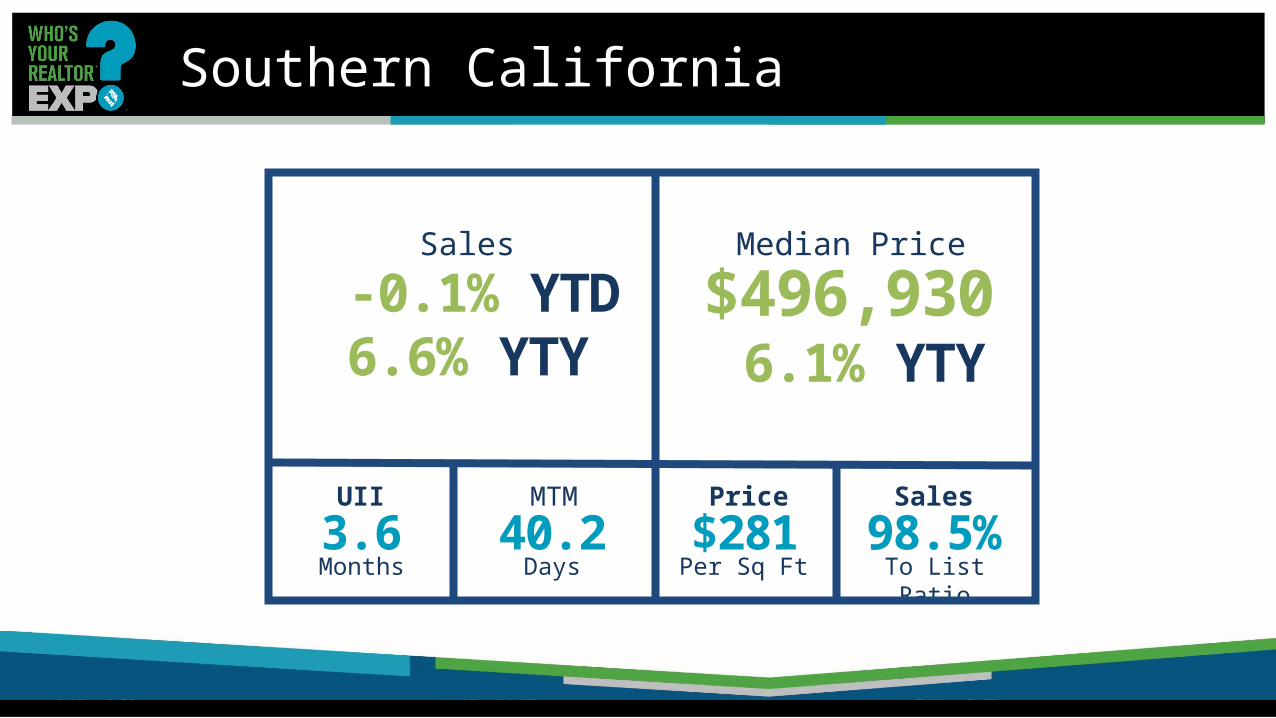

Southern CA Regional Housing Markets

$496,930 6.1% YTY

-0.1% YTD6.6% YTY

3.6 40.2 98.5%$281UII

Months Days

MTM Price

Per Sq Ft

Sales

To List Ratio

Median PriceSales

Southern California

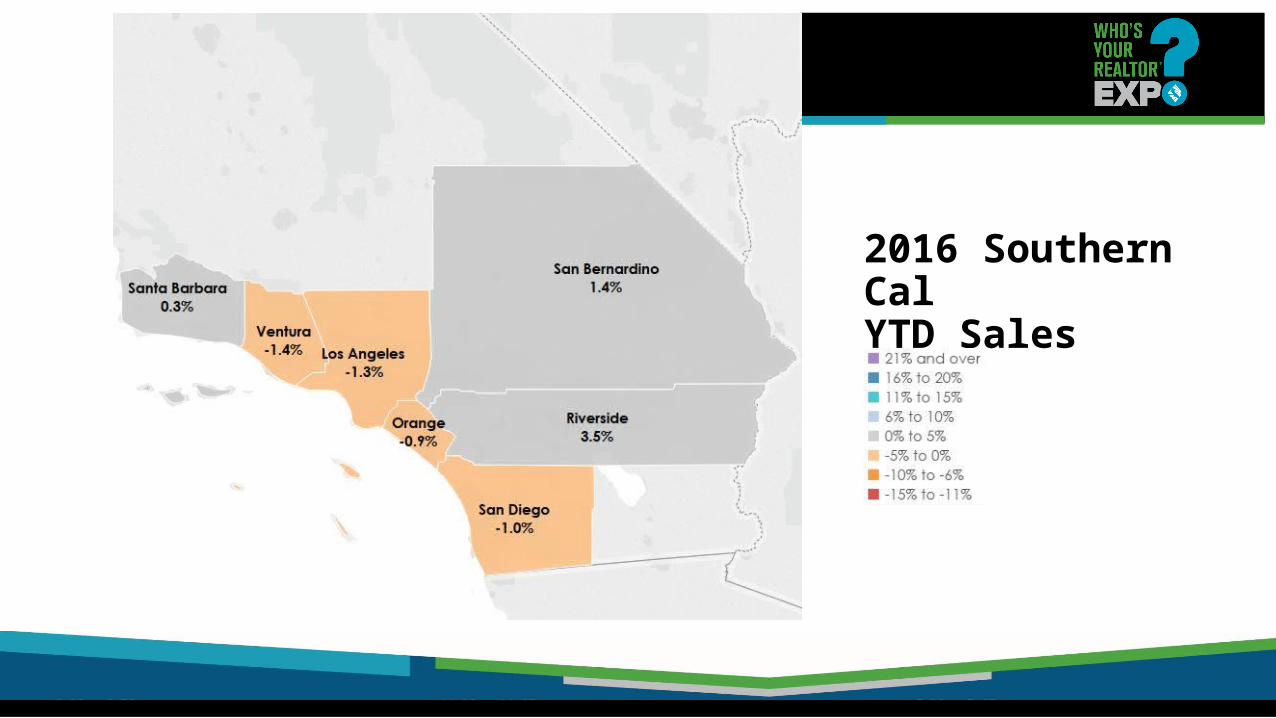

2016 Southern CalYTD Sales

2016 Southern CalMedian Prices YTY

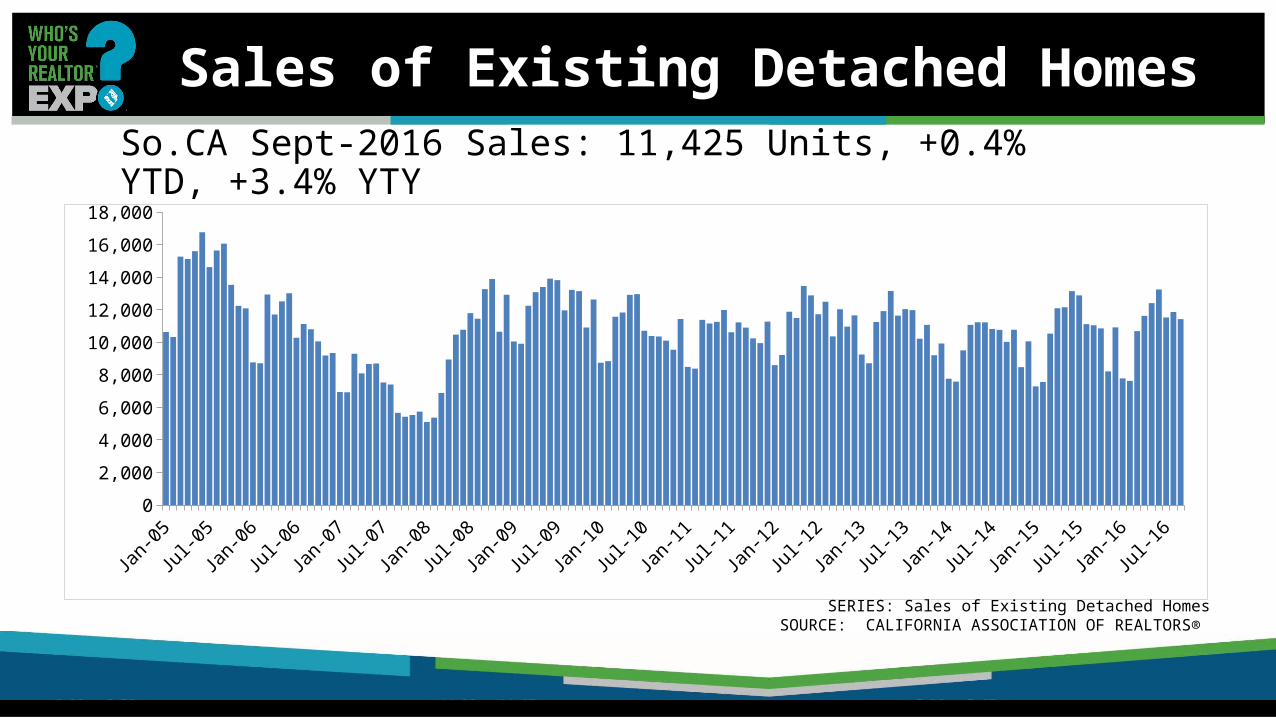

Sales of Existing Detached HomesSo.CA Sept-2016 Sales: 11,425 Units, +0.4% YTD, +3.4% YTY

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

Jul-10

Jan-11

Jul-11

Jan-12

Jul-12

Jan-13

Jul-13

Jan-14

Jul-14

Jan-15

Jul-15

Jan-16

Jul-16

02,0004,0006,0008,000

10,00012,00014,00016,00018,000

SERIES: Sales of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

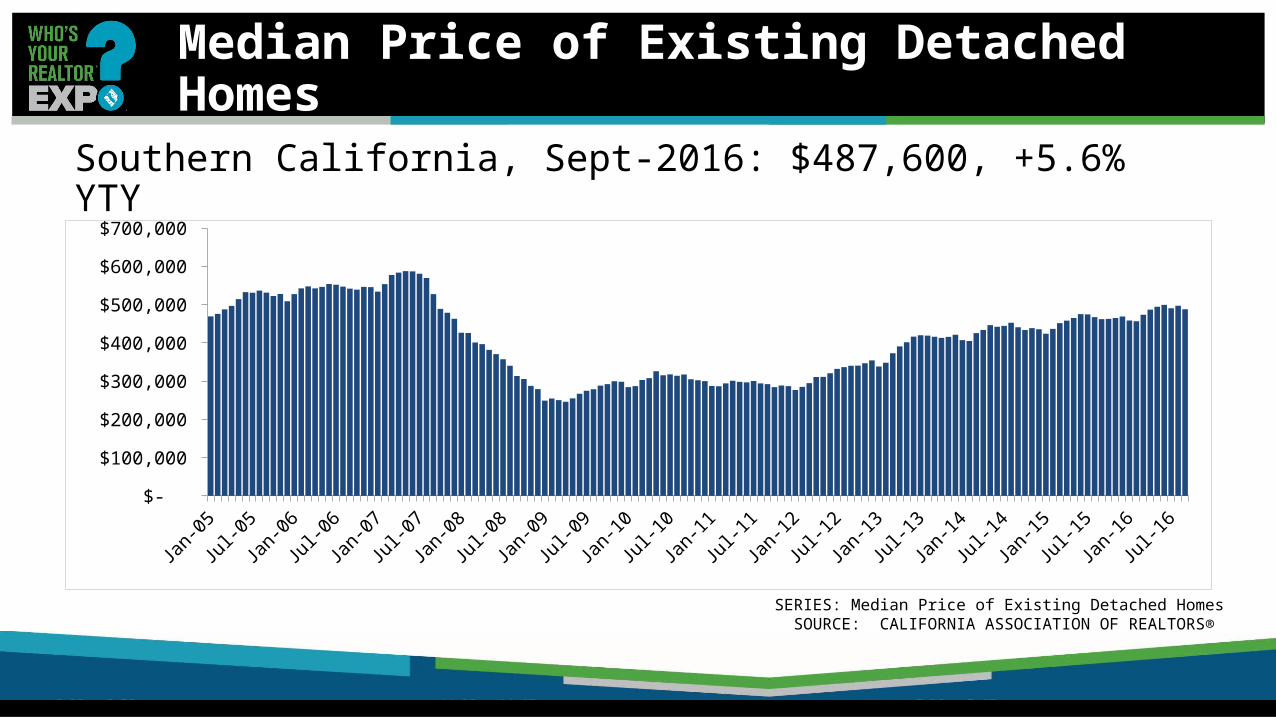

Median Price of Existing Detached Homes

Southern California, Sept-2016: $487,600, +5.6% YTY

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

Jul-10

Jan-11

Jul-11

Jan-12

Jul-12

Jan-13

Jul-13

Jan-14

Jul-14

Jan-15

Jul-15

Jan-16

Jul-16

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

SERIES: Median Price of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

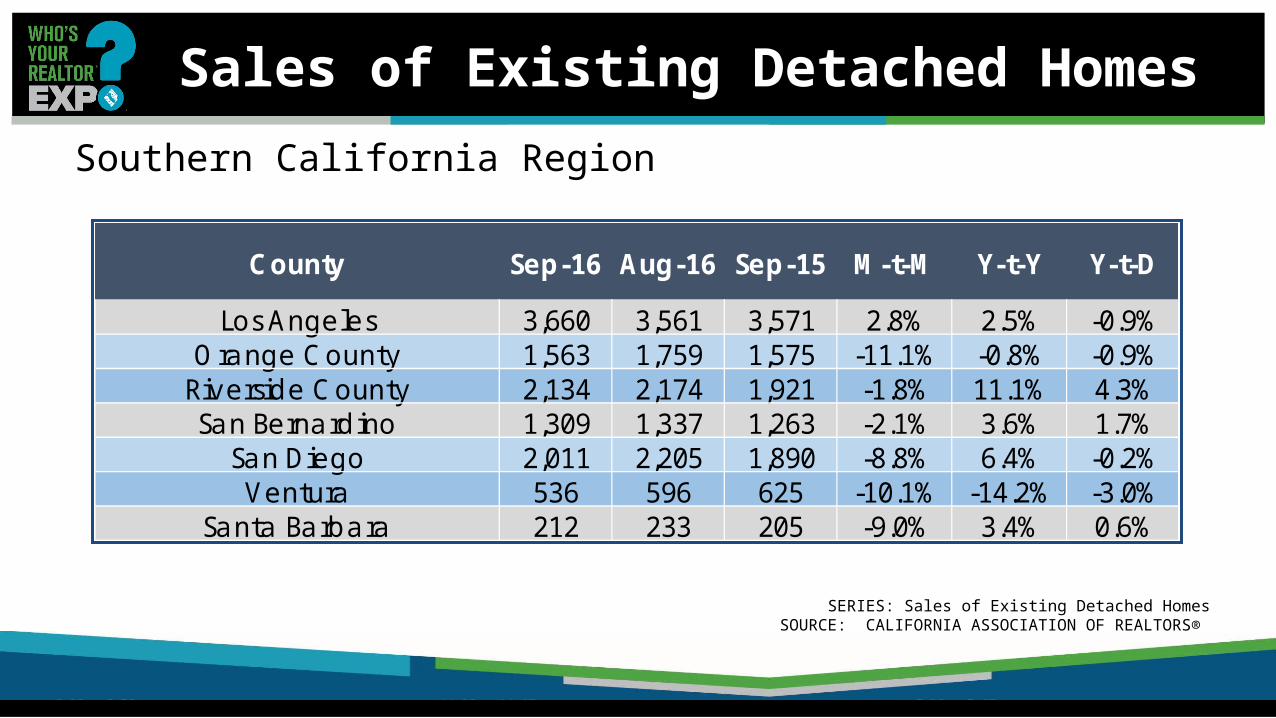

Sales of Existing Detached HomesSouthern California Region

Los Angeles 3,660 3,561 3,571 2.8% 2.5% -0.9%Orange County 1,563 1,759 1,575 -11.1% -0.8% -0.9%

Riverside County 2,134 2,174 1,921 -1.8% 11.1% 4.3%San Bernardino 1,309 1,337 1,263 -2.1% 3.6% 1.7%

San Diego 2,011 2,205 1,890 -8.8% 6.4% -0.2%Ventura 536 596 625 -10.1% -14.2% -3.0%

Santa Barbara 212 233 205 -9.0% 3.4% 0.6%

Y-t-YCounty Sep-16 Aug-16 Sep-15 M-t-M Y-t-D

SERIES: Sales of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

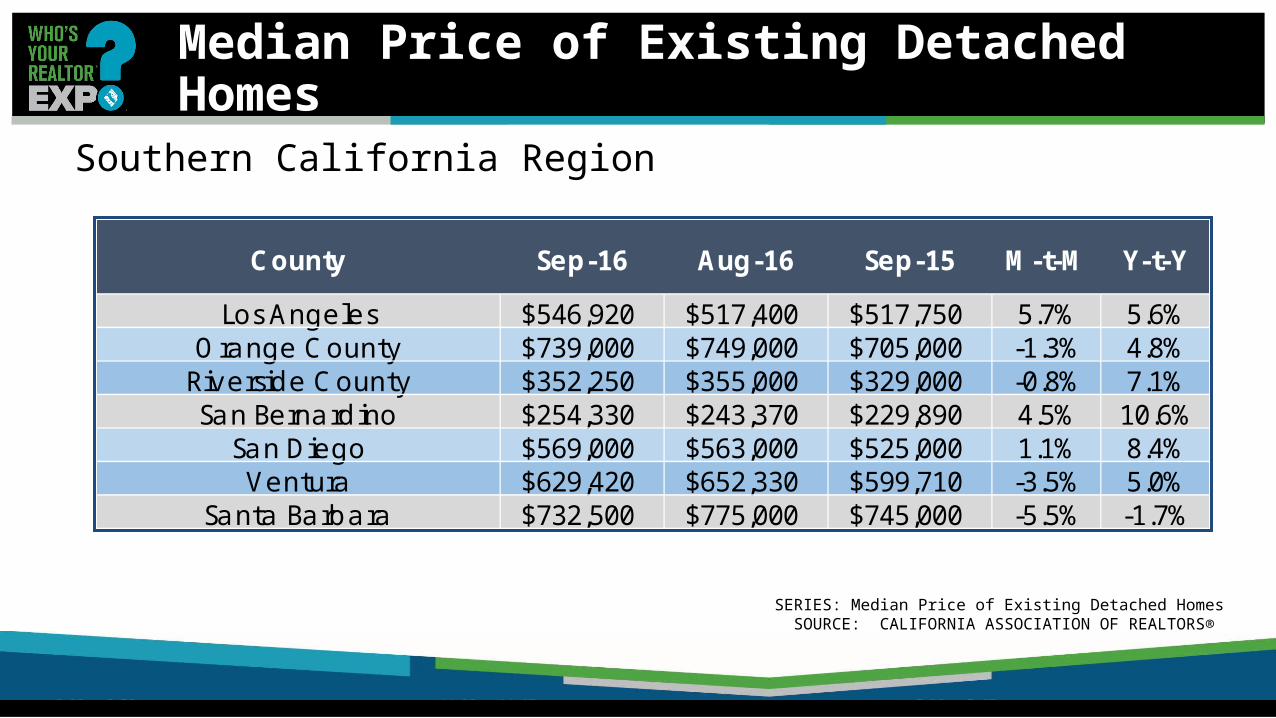

Median Price of Existing Detached Homes

Southern California Region

Los Angeles $546,920 $517,400 $517,750 5.7% 5.6%Orange County $739,000 $749,000 $705,000 -1.3% 4.8%

Riverside County $352,250 $355,000 $329,000 -0.8% 7.1%San Bernardino $254,330 $243,370 $229,890 4.5% 10.6%

San Diego $569,000 $563,000 $525,000 1.1% 8.4%Ventura $629,420 $652,330 $599,710 -3.5% 5.0%

Santa Barbara $732,500 $775,000 $745,000 -5.5% -1.7%

Y-t-YCounty Sep-16 Aug-16 Sep-15 M-t-M

SERIES: Median Price of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

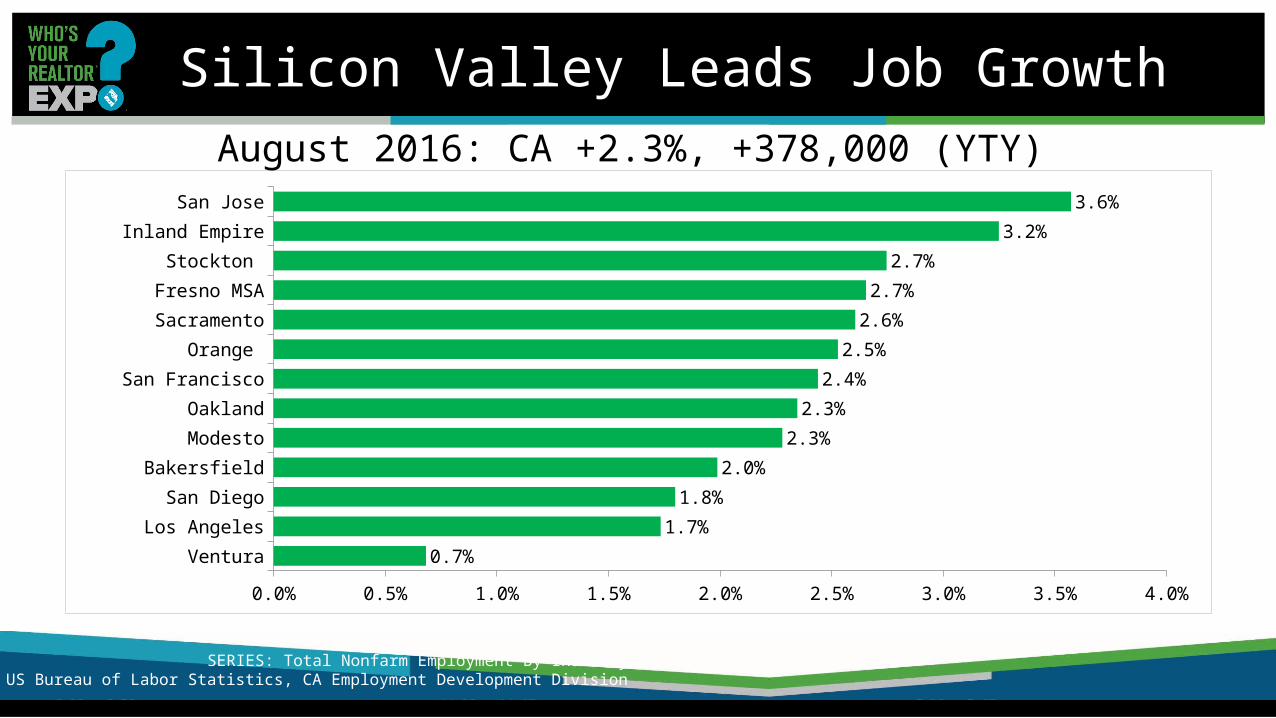

Silicon Valley Leads Job Growth

VenturaLos Angeles

San DiegoBakersfield

ModestoOakland

San FranciscoOrange

SacramentoFresno MSA

Stockton Inland Empire

San Jose

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0%0.7%

1.7%1.8%

2.0%2.3%

2.3%2.4%

2.5%2.6%2.7%

2.7%3.2%

3.6%

August 2016: CA +2.3%, +378,000 (YTY)

SERIES: Total Nonfarm Employment By IndustrySOURCE: US Bureau of Labor Statistics, CA Employment Development Division

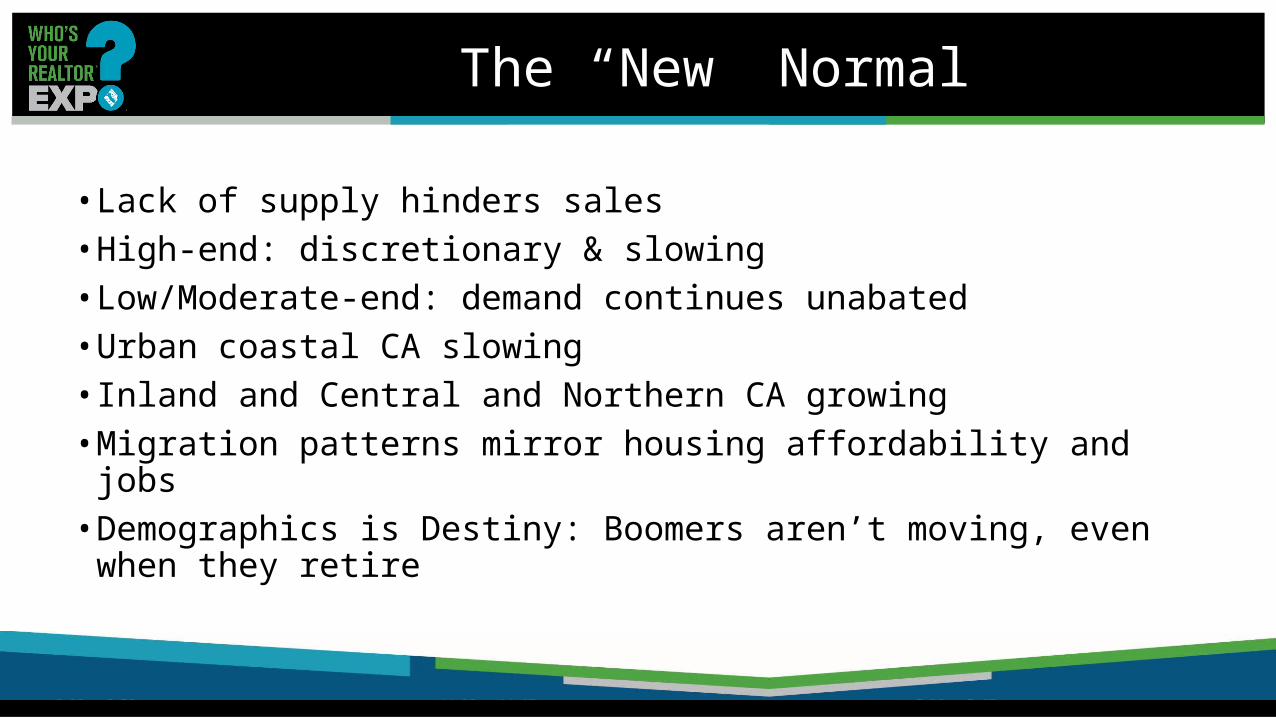

The “New” Normal

• Lack of supply hinders sales• High-end: discretionary & slowing• Low/Moderate-end: demand continues unabated• Urban coastal CA slowing• Inland and Central and Northern CA growing• Migration patterns mirror housing affordability and jobs• Demographics is Destiny: Boomers aren’t moving, even

when they retire

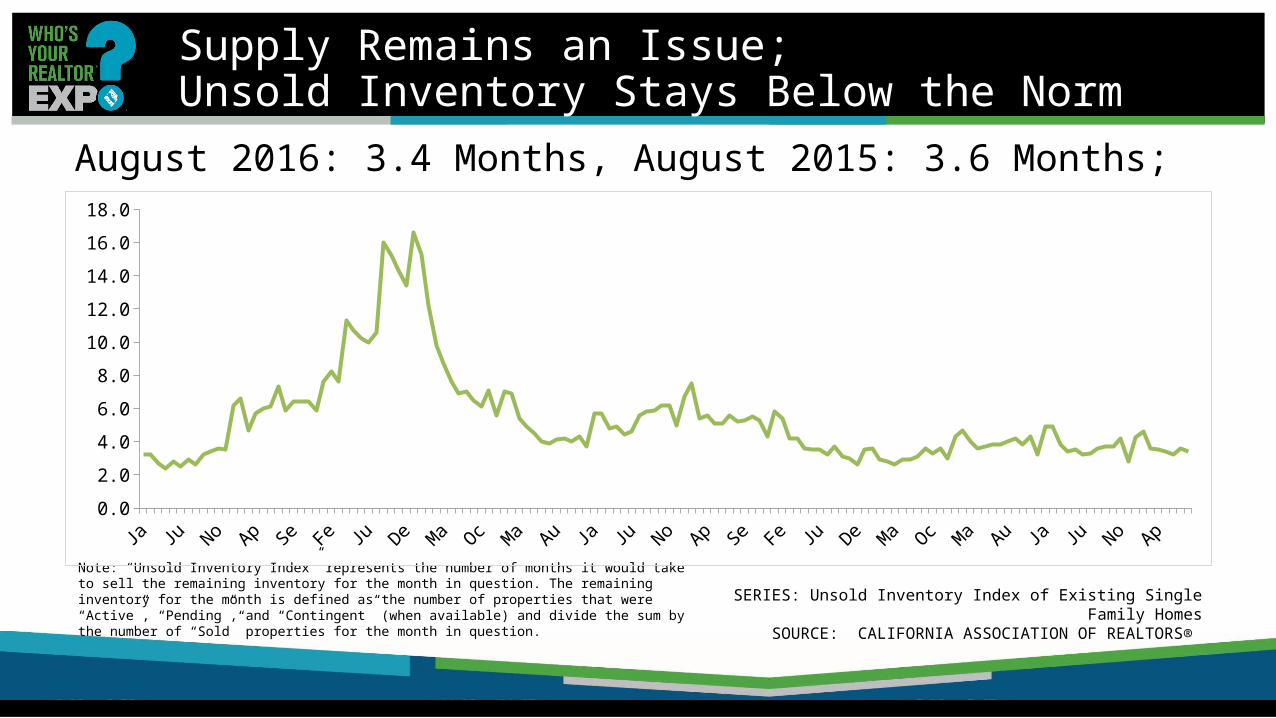

Supply Remains an Issue; Unsold Inventory Stays Below the Norm

August 2016: 3.4 Months, August 2015: 3.6 Months;

Note: “Unsold Inventory Index” represents the number of months it would take to sell the remaining inventory for the month in question. The remaining inventory for the month is defined as the number of properties that were “Active”, “Pending”, and “Contingent” (when available) and divide the sum by the number of “Sold” properties for the month in question.

0.02.04.06.08.0

10.012.014.016.018.0

SERIES: Unsold Inventory Index of Existing Single Family Homes

SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Where is the inventory? Long-Time Homeowners are not moving as in the past

Low rate on current mortgage Low property taxesCapital gains hitWhere can I afford to go?Could not qualify for a mortgage todayRemodel and stay

Are we headed for the “European Model” where children inherit the home of their parents?One more thing…Secular decline in marriage

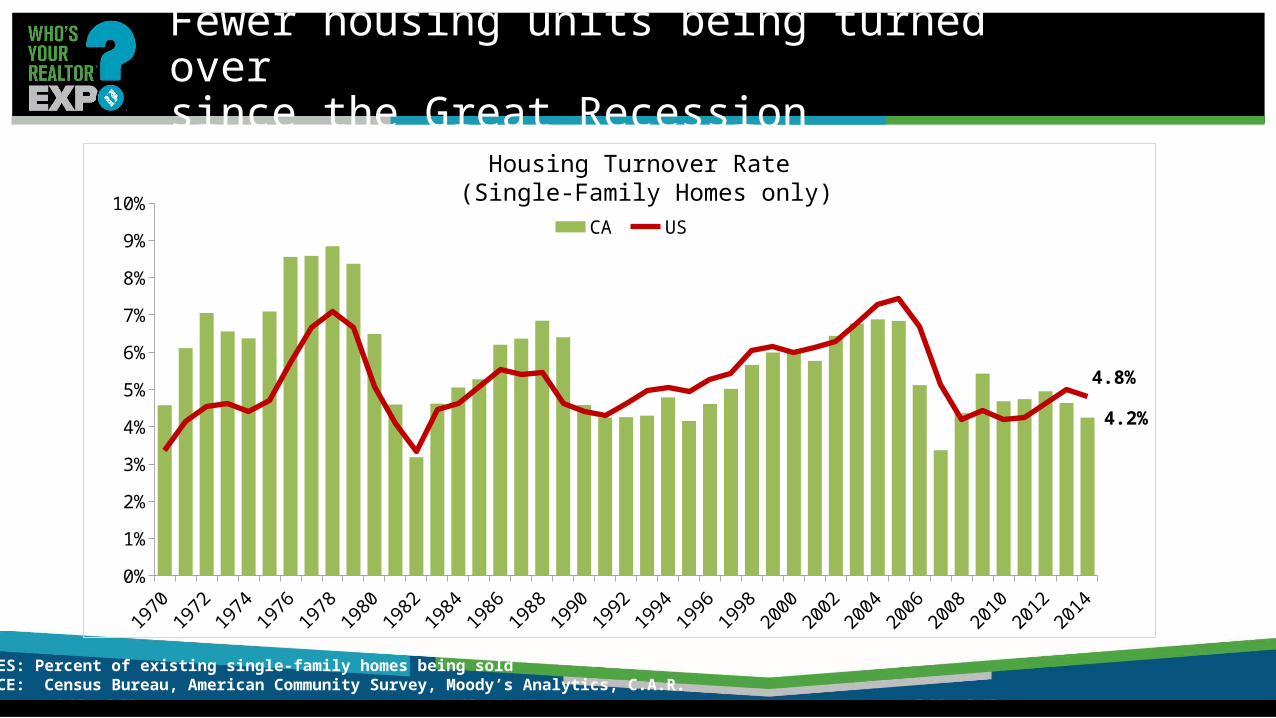

Fewer housing units being turned over since the Great Recession

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

0%1%2%3%4%5%6%7%8%9%

10%

4.2%

4.8%

CA US

SERIES: Percent of existing single-family homes being sold SOURCE: Census Bureau, American Community Survey, Moody’s Analytics, C.A.R.

Housing Turnover Rate (Single-Family Homes only)

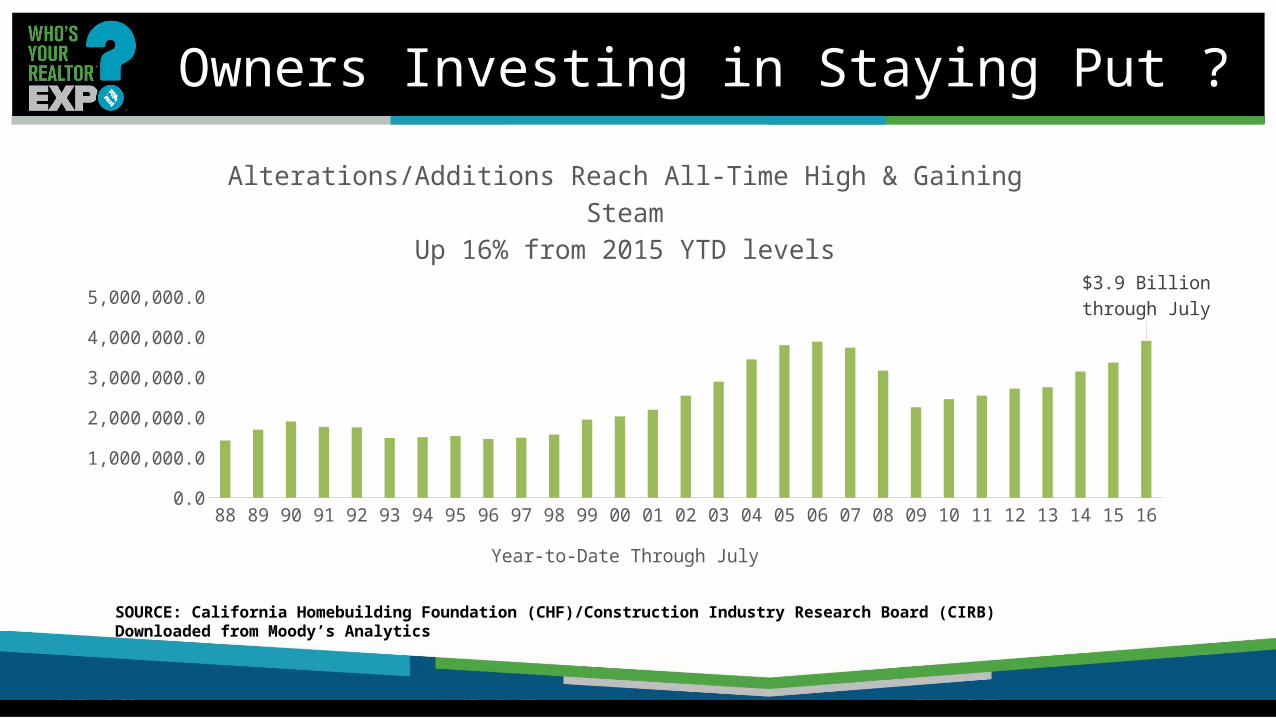

Owners Investing in Staying Put ?

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 160.0500,000.0

1,000,000.01,500,000.02,000,000.02,500,000.03,000,000.03,500,000.04,000,000.04,500,000.0

$3.9 Billionthrough July

Alterations/Additions Reach All-Time High & Gaining SteamUp 16% from 2015 YTD levels

Year-to-Date Through July SOURCE: California Homebuilding Foundation (CHF)/Construction Industry Research Board (CIRB)Downloaded from Moody’s Analytics

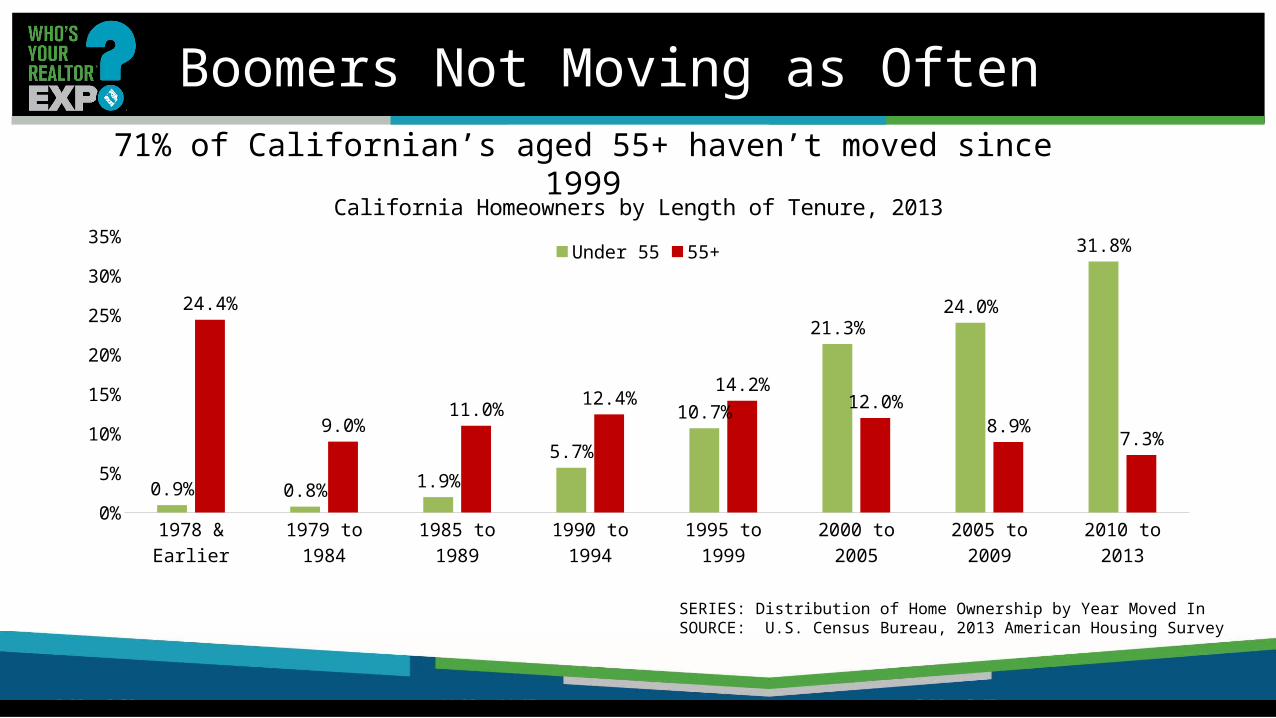

Boomers Not Moving as Often

1978 & Ear-lier

1979 to 1984

1985 to 1989

1990 to 1994

1995 to 1999

2000 to 2005

2005 to 2009

2010 to 2013

0%

5%

10%

15%

20%

25%

30%

35%

0.9% 0.8% 1.9%5.7%

10.7%

21.3%24.0%

31.8%

24.4%

9.0%11.0% 12.4% 14.2%

12.0%8.9% 7.3%

California Homeowners by Length of Tenure, 2013Under 55 55+

SERIES: Distribution of Home Ownership by Year Moved InSOURCE: U.S. Census Bureau, 2013 American Housing Survey

71% of Californian’s aged 55+ haven’t moved since 1999

More Single Family Units Now Rentals

SF Owners SF Renters0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,0006,919,164

1,940,607

6,527,730

2,674,808

2000 2005 2010 2015 SOURCE: U.S. Census Bureau, Annual Social and Economic Supplement (ASEC) to the Current Population Survey (CPS)Downloaded from the National Bureau of Economic Research (NBER)

Potentially between 400,000 and 700,000 SF Rentals that Used to be Owner-Occupied

“Missing” 65,000 New Units Annually

SERIES: California New Housing PermitsSOURCE: Construction Industry Research Board

0

50000

100000

150000

200000

250000

300000

350000

Single Family Multi-Family

Household Growth: 165,000/yr.

2015: 95,822 (42,959 sf, 52,863 mf)2016p: 98,300 total units

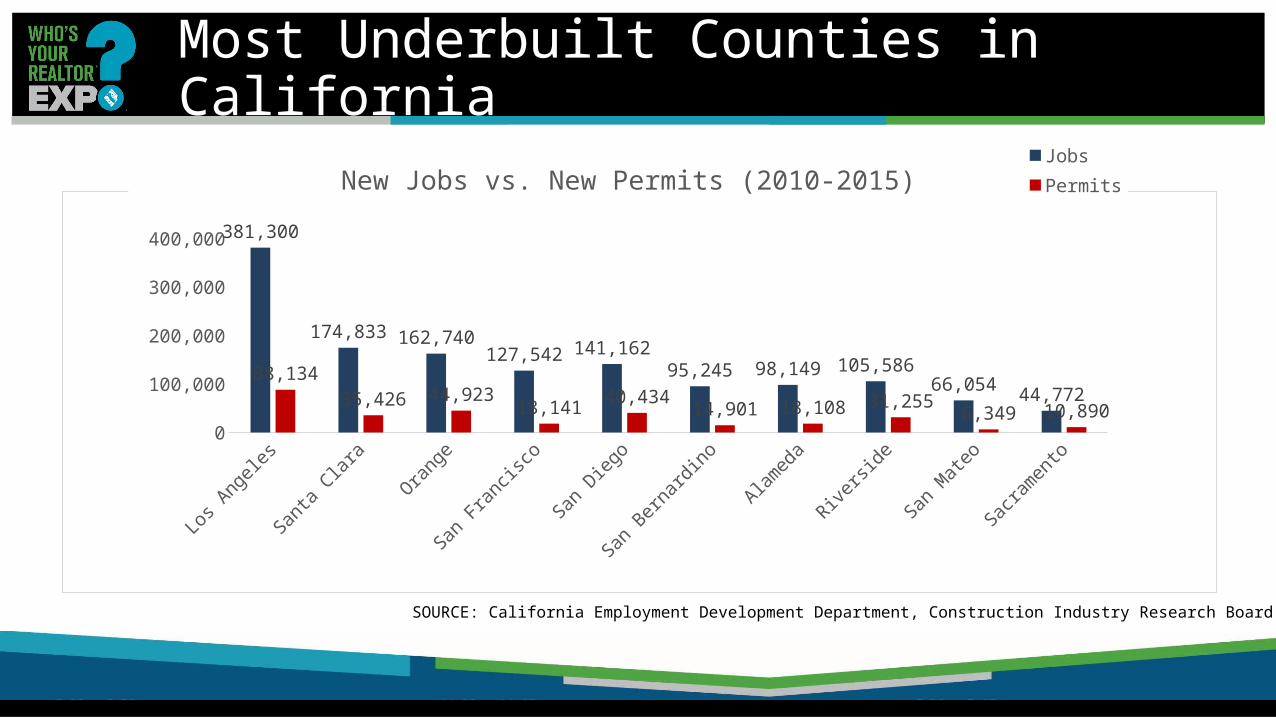

Most Underbuilt Counties in California

Los A

ngele

s

Santa

Clara

Orange

San F

rancis

co

San D

iego

San B

ernard

ino

Alamed

a

Riversi

de

San M

ateo

Sacra

mento

050,000

100,000150,000200,000250,000300,000350,000400,000450,000

381,300

174,833 162,740127,542 141,162

95,245 98,149 105,58666,054 44,772

88,13435,426 44,923 18,141 40,434 14,901 18,108 31,255 6,349 10,890

New Jobs vs. New Permits (2010-2015)JobsPermits

SOURCE: California Employment Development Department, Construction Industry Research Board

2017 Forecast

California Housing Market Outlook

SERIES: CA Housing Market OutlookSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

2011 2012 2013 2014 2015 2016p 2017f

SFH Resa les (000s) 422.6 439.8 414.9 382.7 408.8 407.3 413.0

% C hange 1.4% 4.1% -5.9% -7.8% 6.8% -0.4% 1.4%M edian Price ($000s) $286.0 $319.3 $407.2 $446.9 $474.4 $503.9 $525.6

% C hange -6.2% 11.6% 27.5% 9.8% 6.2% 6.2% 4.3%Housing A ffordability Index 53% 51% 36% 30% 31% 33% 29%

30-Yr FRM 4.5% 3.7% 4.0% 4.2% 3.9% 3.6% 4.0%

2017 Challenges & Opportunities

Lack of af -fordability,

56%Lack of in-

ventory; 28%

Mortagage rate increase; 10%

Recession, 6%

2017 Challenges

Q2 - What will be the biggest challenge for the housing market in 2017?

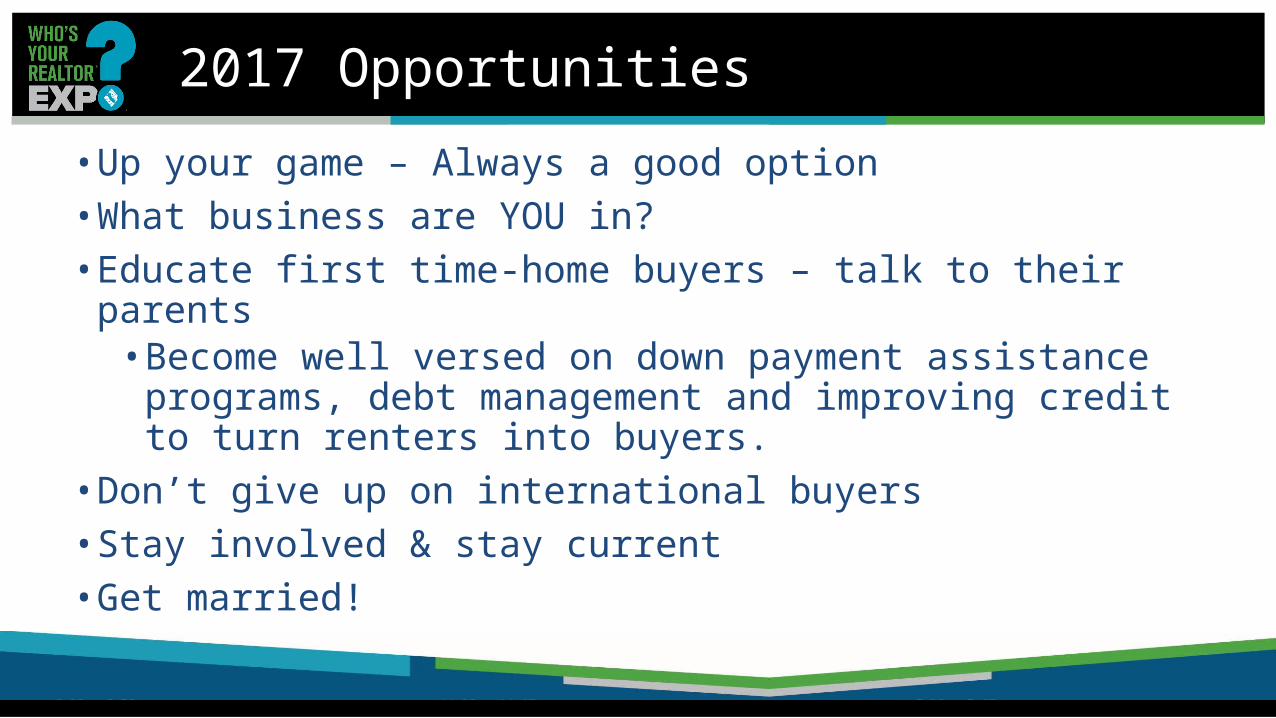

2017 Opportunities • Up your game – Always a good option• What business are YOU in?• Educate first time-home buyers – talk to their parents• Become well versed on down payment assistance

programs, debt management and improving credit to turn renters into buyers.

• Don’t give up on international buyers• Stay involved & stay current• Get married!