Embed Size (px)

Citation preview

Resetting the rules: A New Framework for Affordable Housing?

Bill Randolph, City Futures Research Centre UNSW

Presentation overview

• The ‘affordability crisis’

• What’s driving house prices?

• The problems of the low income renter

• A new Framework for tackling rental unaffordability

• Knowing where and how to intervene calls for accurate analysis of the

problem (see: The Senate Economics References Committee Report 2015)

• ‘Housing unaffordability purely a supply problem’ hard to square with

Sydney’s 2013-2015 coincidence of:

– 27% real terms rise in Sydney prices

– Dwelling approvals and completions at record levels

– Apartment construction boom straining building industry capacity

• Also underlain by claim that real culprit is restrictive planning

• But planning approvals greatly in excess of building completions – 160k

compared with 100k in past 5 years

• Growing inequality in the distribution of housing space in Australia:

– more second homes

– more underutilised homes

– more empty homes (120,000 in Sydney)

A New Framework for Affordable Housing?

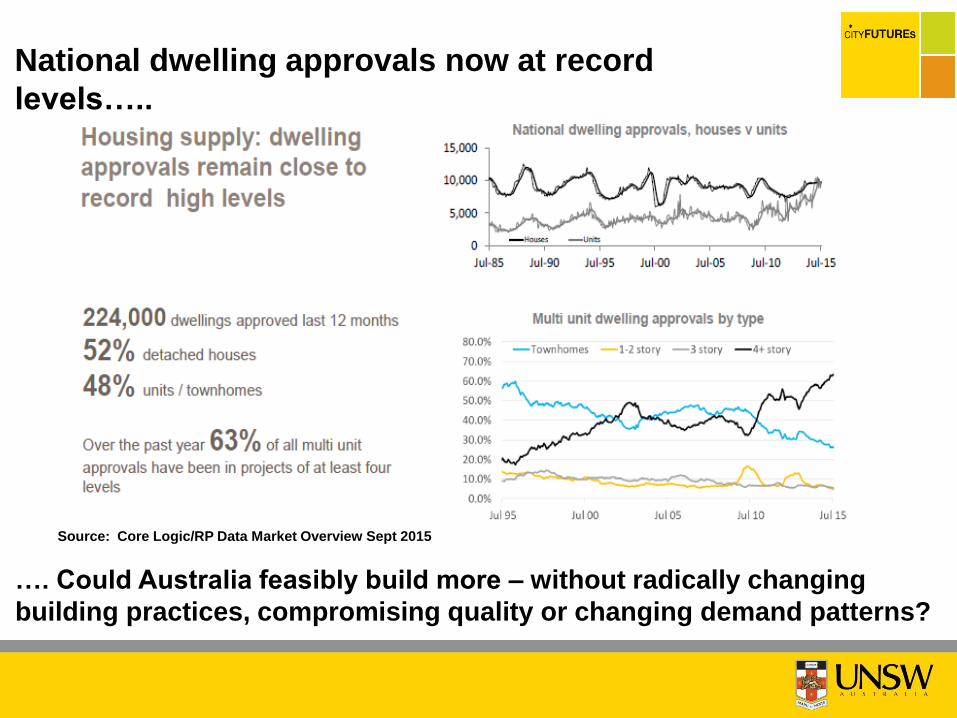

National dwelling approvals now at record

levels…..

…. Could Australia feasibly build more – without radically changing

building practices, compromising quality or changing demand patterns?

Source: Core Logic/RP Data Market Overview Sept 2015

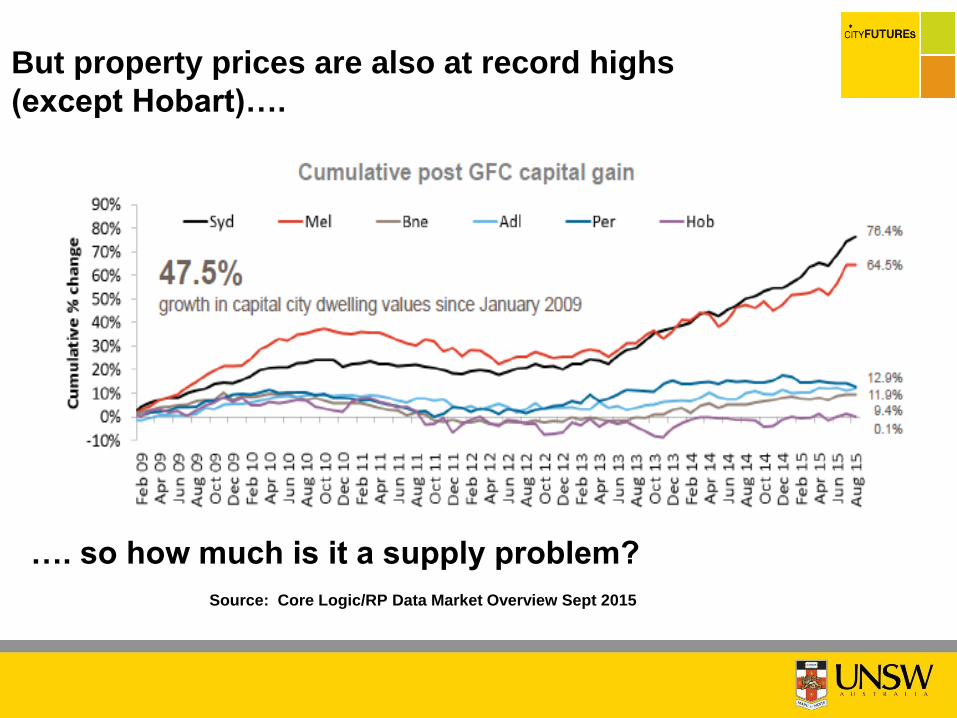

But property prices are also at record highs

(except Hobart)….

…. so how much is it a supply problem?

Source: Core Logic/RP Data Market Overview Sept 2015

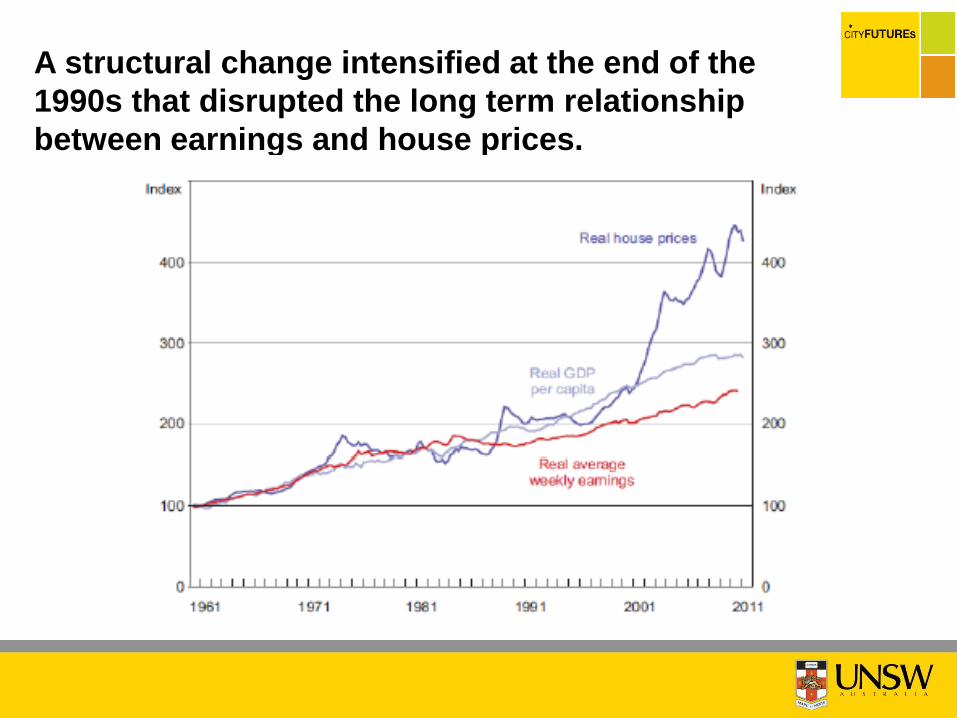

A structural change intensified at the end of the

1990s that disrupted the long term relationship

between earnings and house prices.

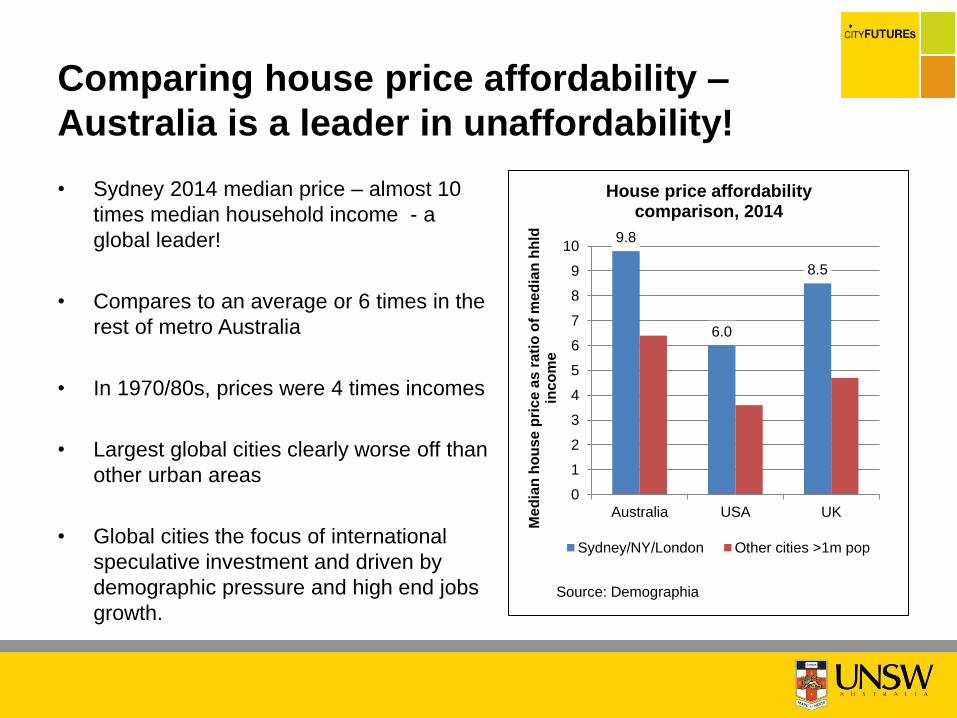

• Sydney 2014 median price – almost 10

times median household income - a

global leader!

• Compares to an average or 6 times in the

rest of metro Australia

• In 1970/80s, prices were 4 times incomes

• Largest global cities clearly worse off than

other urban areas

• Global cities the focus of international

speculative investment and driven by

demographic pressure and high end jobs

growth.

Comparing house price affordability –

Australia is a leader in unaffordability!

9.8

6.0

8.5

0

1

2

3

4

5

6

7

8

9

10

Australia USA UK

Me

dia

n h

ou

se

pri

ce a

s r

ati

o o

f m

ed

ian

hh

ldin

co

me

House price affordability comparison, 2014

Sydney/NY/London Other cities >1m pop

Source: Demographia

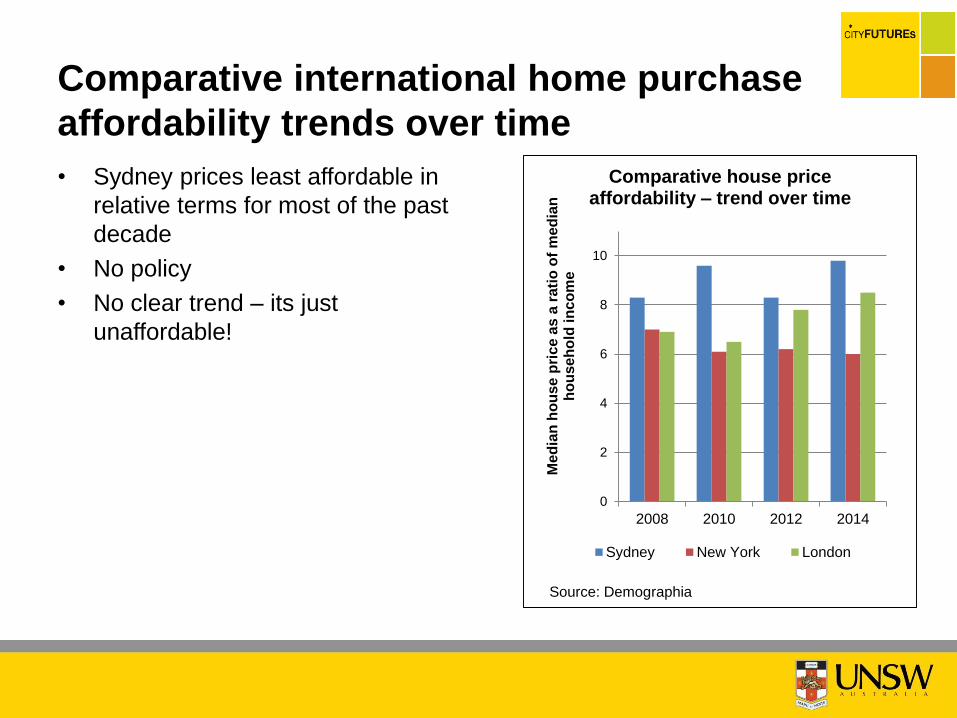

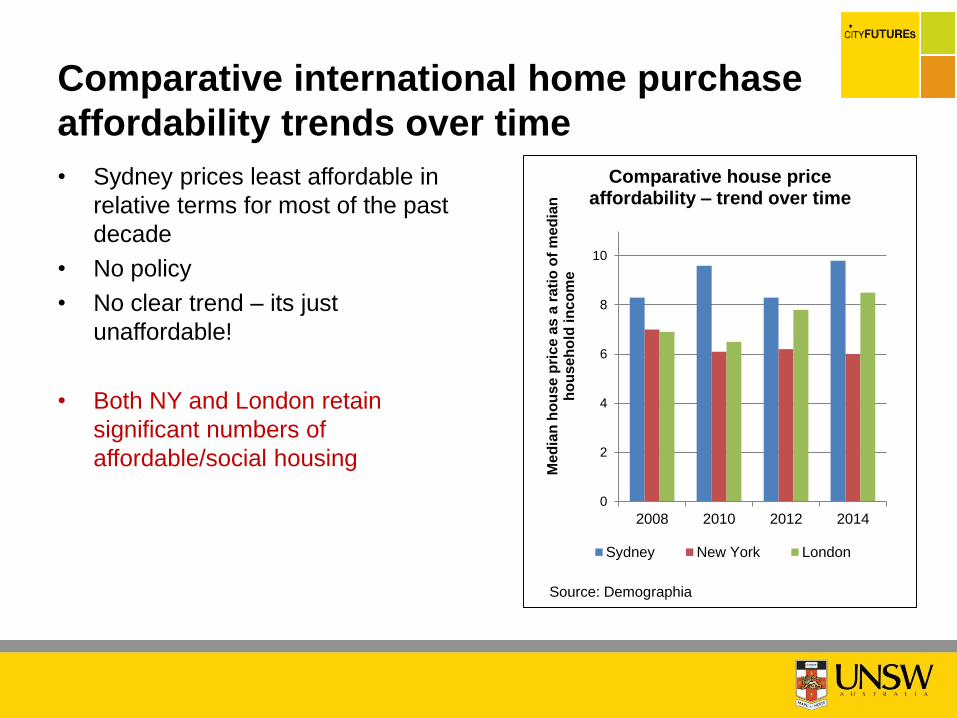

• Sydney prices least affordable in

relative terms for most of the past

decade

• No policy

• No clear trend – its just

unaffordable!

Comparative international home purchase

affordability trends over time

0

2

4

6

8

10

2008 2010 2012 2014

Me

dia

n h

ou

se

pri

ce a

s a

ra

tio

of

me

dia

n

ho

useh

old

in

co

me

Comparative house price affordability – trend over time

Sydney New York London

Source: Demographia

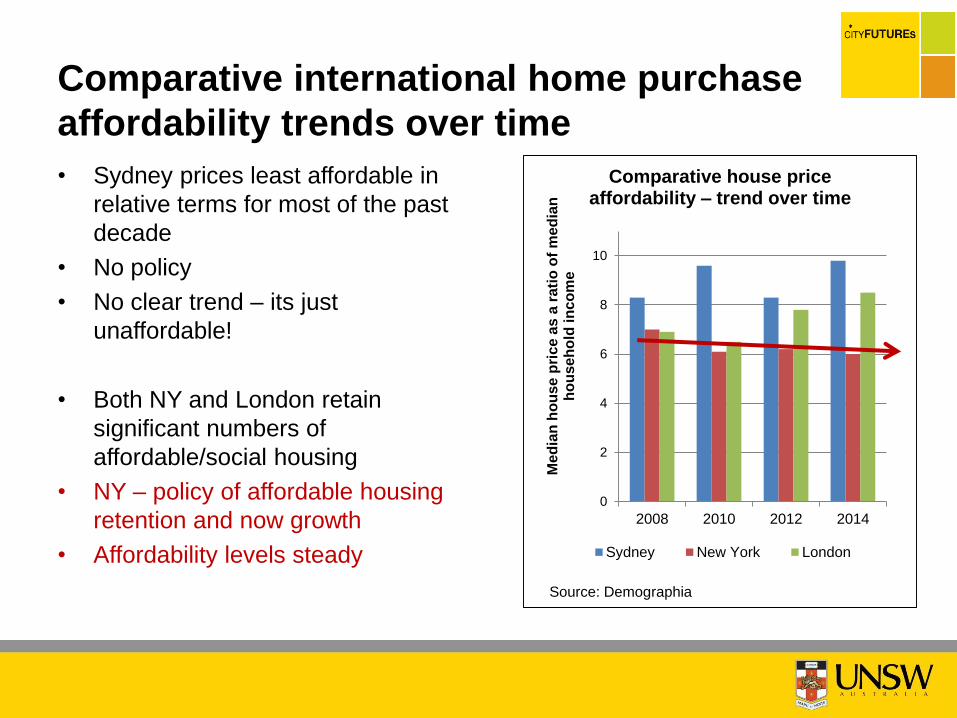

• Sydney prices least affordable in

relative terms for most of the past

decade

• No policy

• No clear trend – its just

unaffordable!

• Both NY and London retain

significant numbers of

affordable/social housing

0

2

4

6

8

10

2008 2010 2012 2014

Me

dia

n h

ou

se

pri

ce a

s a

ra

tio

of

me

dia

n

ho

useh

old

in

co

me

Comparative house price affordability – trend over time

Sydney New York London

Source: Demographia

Comparative international home purchase

affordability trends over time

• Sydney prices least affordable in

relative terms for most of the past

decade

• No policy

• No clear trend – its just

unaffordable!

• Both NY and London retain

significant numbers of

affordable/social housing

• NY – policy of affordable housing

retention and now growth

• Affordability levels steady

0

2

4

6

8

10

2008 2010 2012 2014

Me

dia

n h

ou

se

pri

ce a

s a

ra

tio

of

me

dia

n

ho

useh

old

in

co

me

Comparative house price affordability – trend over time

Sydney New York London

Source: Demographia

Comparative international home purchase

affordability trends over time

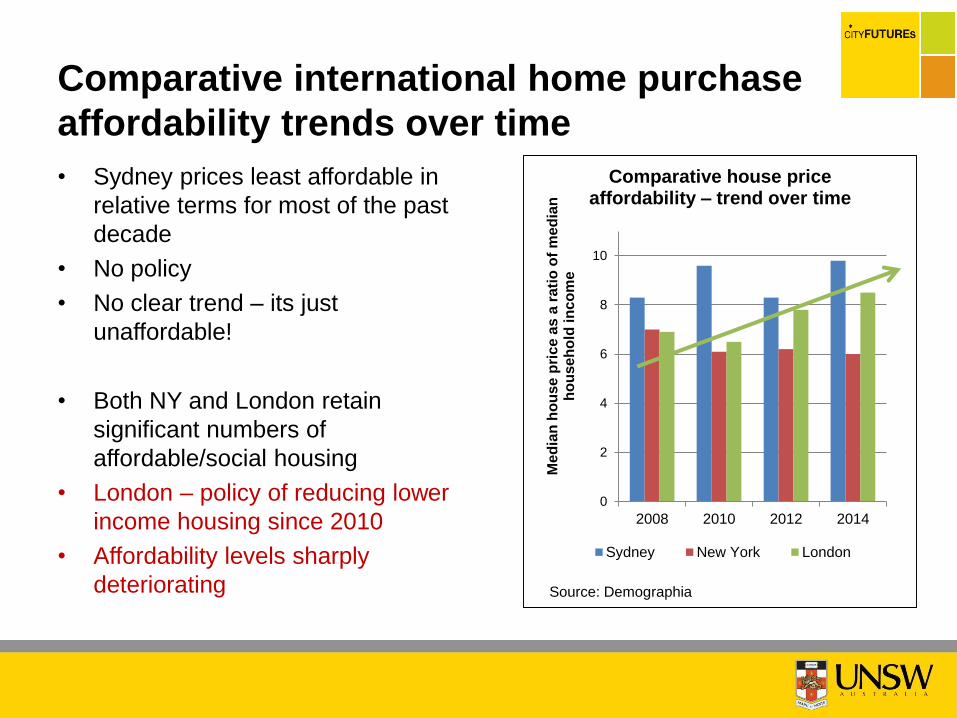

• Sydney prices least affordable in

relative terms for most of the past

decade

• No policy

• No clear trend – its just

unaffordable!

• Both NY and London retain

significant numbers of

affordable/social housing

• London – policy of reducing lower

income housing since 2010

• Affordability levels sharply

deteriorating

0

2

4

6

8

10

2008 2010 2012 2014

Me

dia

n h

ou

se

pri

ce a

s a

ra

tio

of

me

dia

n

ho

useh

old

in

co

me

Comparative house price affordability – trend over time

Sydney New York London

Source: Demographia

Comparative international home purchase

affordability trends over time

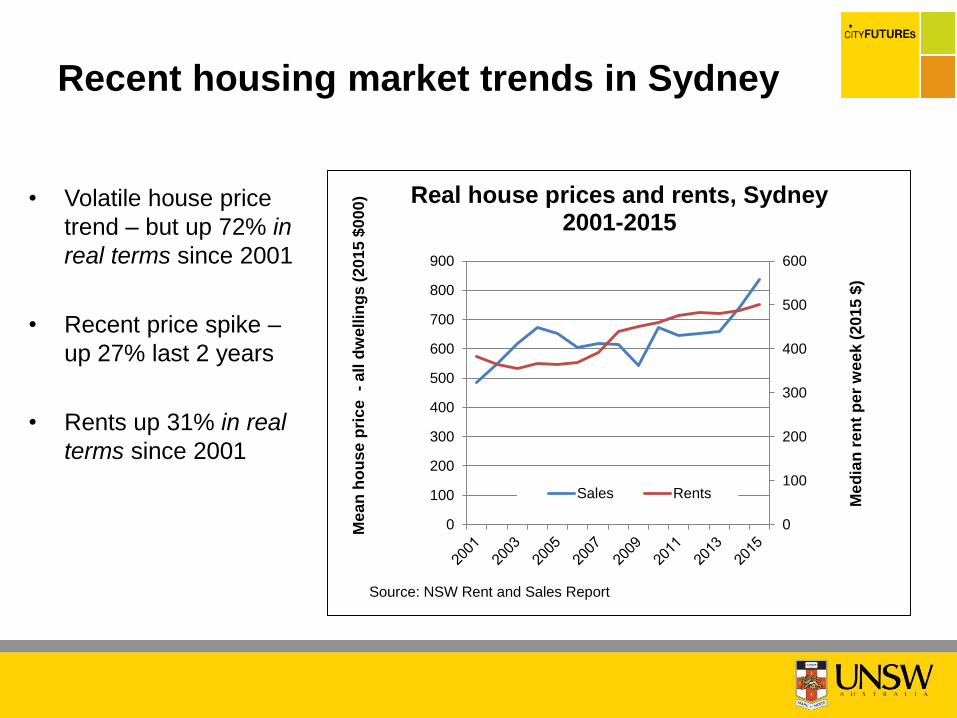

• Volatile house price

trend – but up 72% in

real terms since 2001

• Recent price spike –

up 27% last 2 years

• Rents up 31% in real

terms since 2001

Recent housing market trends in Sydney

0

100

200

300

400

500

600

0

100

200

300

400

500

600

700

800

900

Me

dia

n r

en

t p

er

we

ek

(20

15

$)

Me

an

ho

use

pri

ce

-

all

dw

ell

ing

s (

20

15

$0

00

) Real house prices and rents, Sydney 2001-2015

Sales Rents

Source: NSW Rent and Sales Report

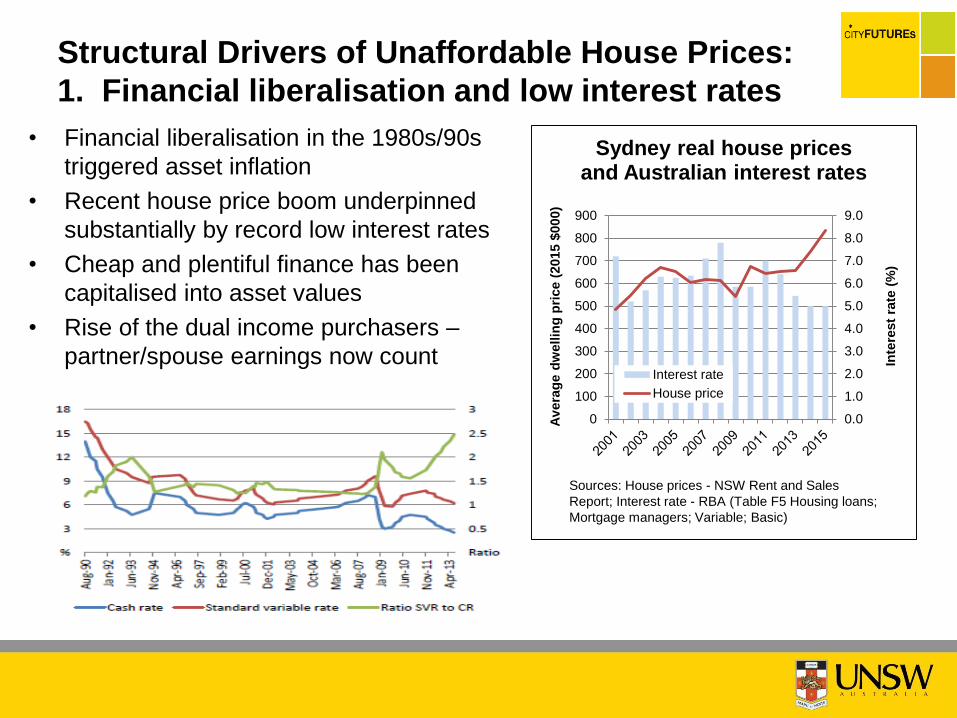

• Financial liberalisation in the 1980s/90s

triggered asset inflation

• Recent house price boom underpinned

substantially by record low interest rates

• Cheap and plentiful finance has been

capitalised into asset values

• Rise of the dual income purchasers –

partner/spouse earnings now count

Structural Drivers of Unaffordable House Prices:

1. Financial liberalisation and low interest rates

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

0

100

200

300

400

500

600

700

800

900

Inte

rest

rate

(%

)

Av

era

ge d

wellin

g p

rice (

2015 $

000)

Sydney real house prices and Australian interest rates

Interest rate

House price

Sources: House prices - NSW Rent and Sales

Report; Interest rate - RBA (Table F5 Housing loans;

Mortgage managers; Variable; Basic)

Structural Drivers of Unaffordable House Prices:

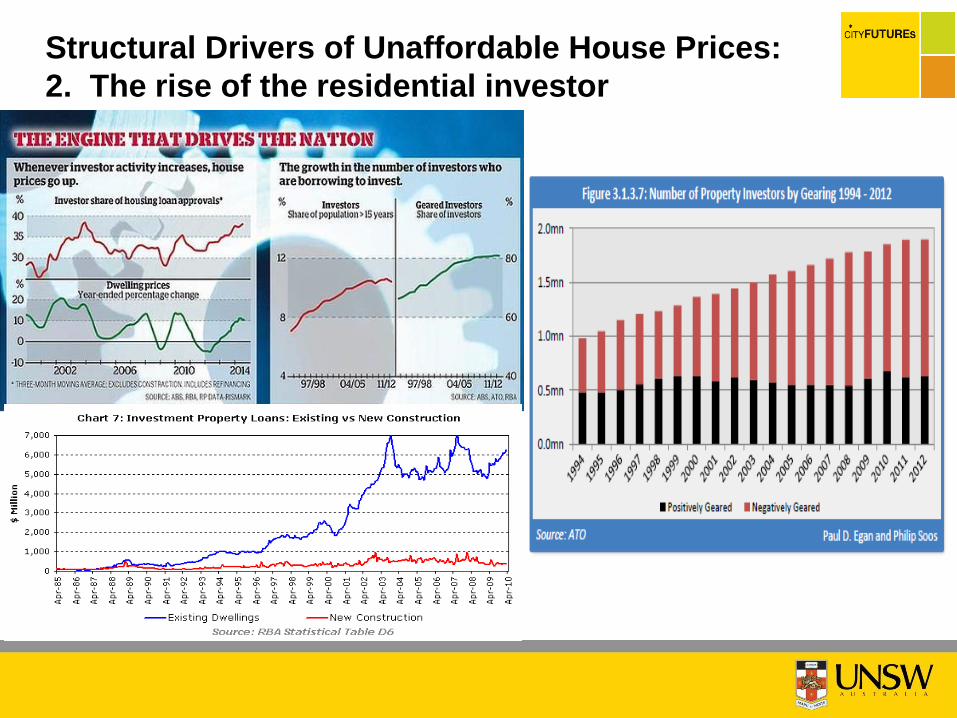

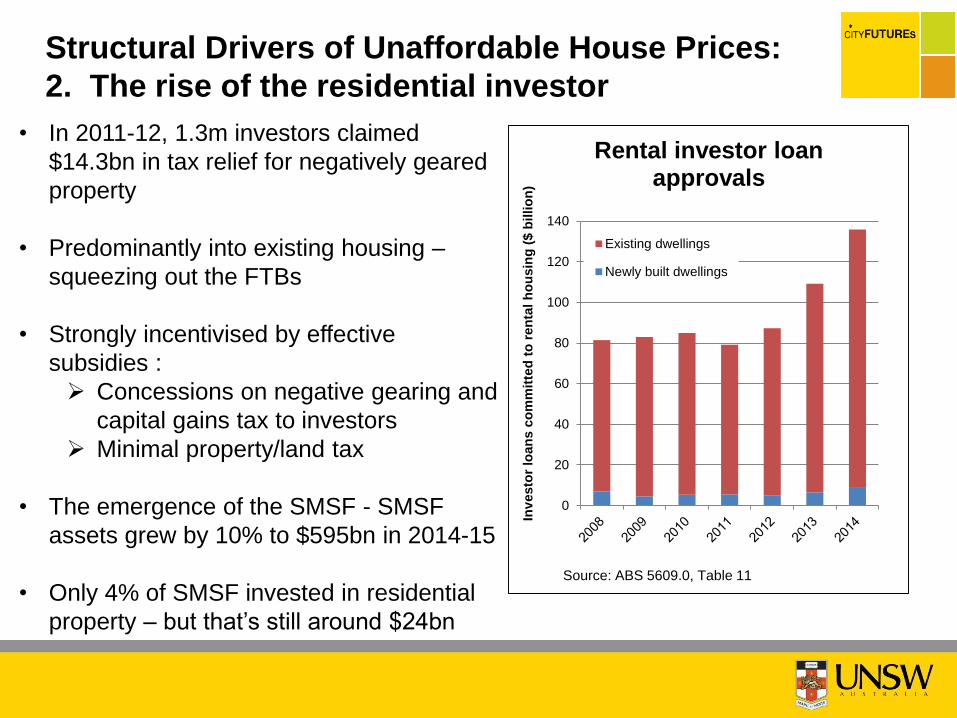

2. The rise of the residential investor

Structural Drivers of Unaffordable House Prices:

2. The rise of the residential investor

• In 2011-12, 1.3m investors claimed

$14.3bn in tax relief for negatively geared

property

• Predominantly into existing housing –

squeezing out the FTBs

• Strongly incentivised by effective

subsidies :

Concessions on negative gearing and

capital gains tax to investors

Minimal property/land tax

• The emergence of the SMSF - SMSF

assets grew by 10% to $595bn in 2014-15

• Only 4% of SMSF invested in residential

property – but that’s still around $24bn

0

20

40

60

80

100

120

140

Inv

esto

r lo

an

s c

om

mit

ted

to

ren

tal

ho

usin

g (

$ b

illio

n)

Rental investor loan approvals

Existing dwellings

Newly built dwellings

Source: ABS 5609.0, Table 11

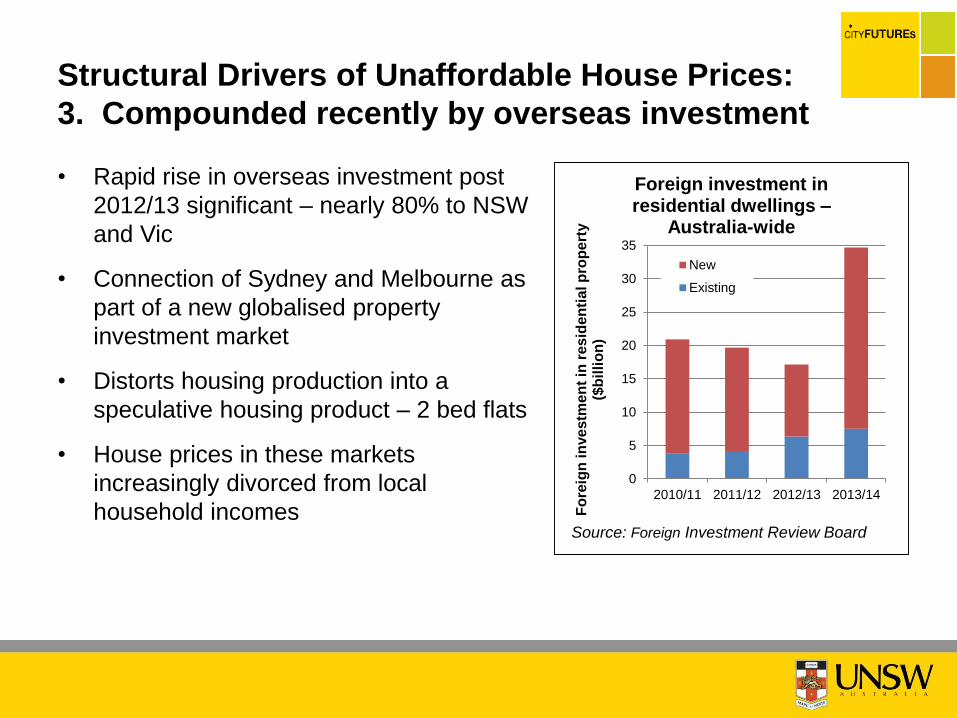

• Rapid rise in overseas investment post

2012/13 significant – nearly 80% to NSW

and Vic

• Connection of Sydney and Melbourne as

part of a new globalised property

investment market

• Distorts housing production into a

speculative housing product – 2 bed flats

• House prices in these markets

increasingly divorced from local

household incomes

Structural Drivers of Unaffordable House Prices:

3. Compounded recently by overseas investment

0

5

10

15

20

25

30

35

2010/11 2011/12 2012/13 2013/14

Fo

reig

n in

ve

stm

en

t in

re

sid

en

tia

l p

rop

ert

y

($b

illi

on

)

Foreign investment in residential dwellings –

Australia-wide

New

Existing

Source: Foreign Investment Review Board

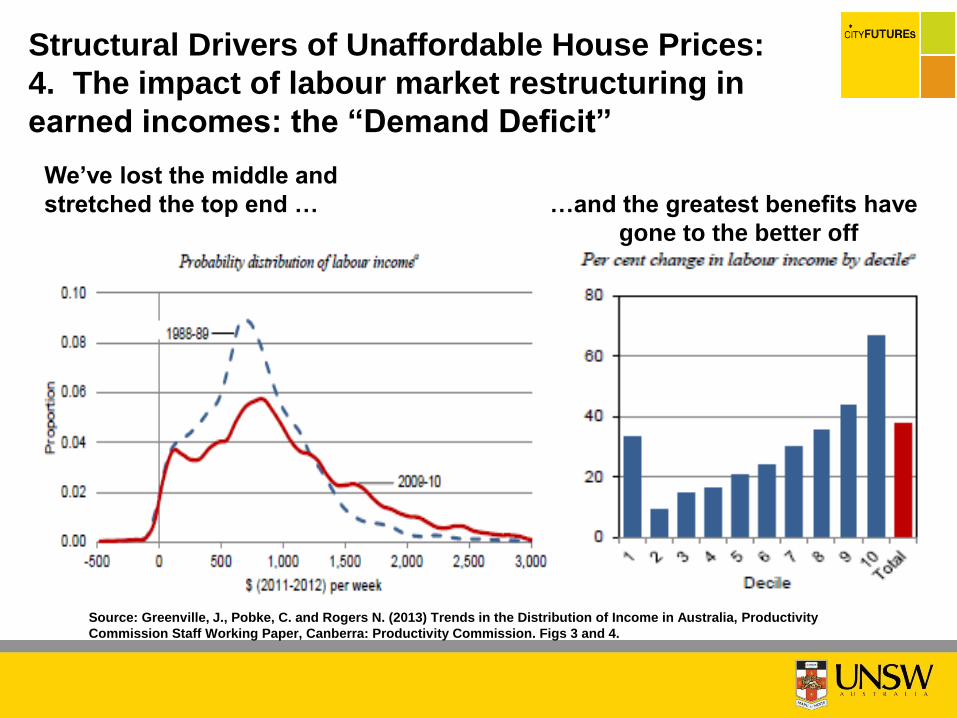

Structural Drivers of Unaffordable House Prices:

4. The impact of labour market restructuring in

earned incomes: the “Demand Deficit”

Source: Greenville, J., Pobke, C. and Rogers N. (2013) Trends in the Distribution of Income in Australia, Productivity

Commission Staff Working Paper, Canberra: Productivity Commission. Figs 3 and 4.

We’ve lost the middle and

stretched the top end … …and the greatest benefits have

gone to the better off

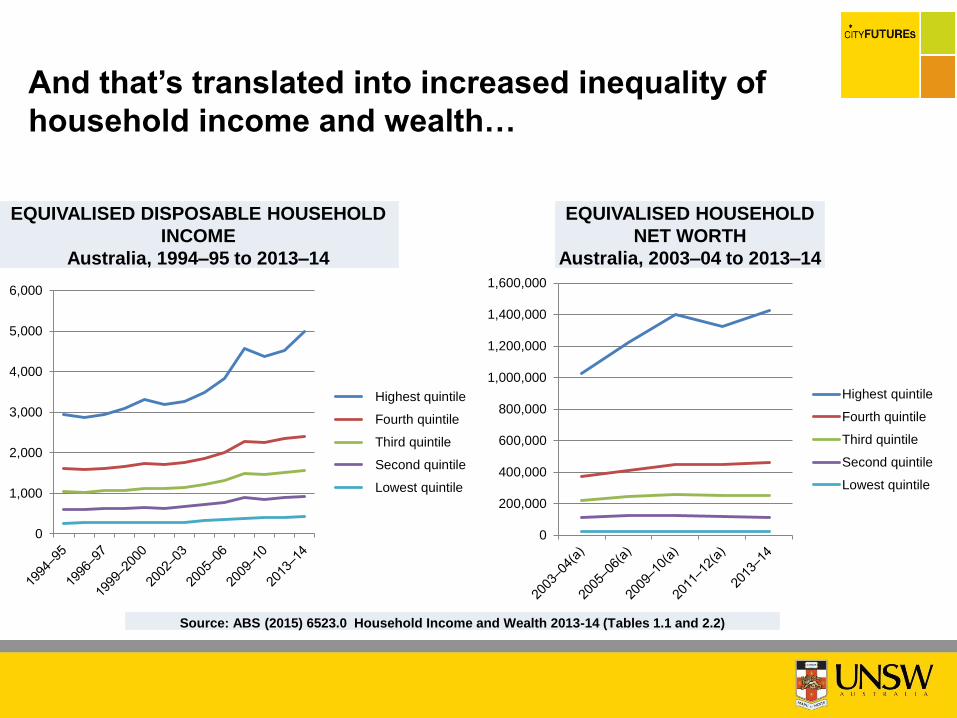

And that’s translated into increased inequality of

household income and wealth…

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Highest quintile

Fourth quintile

Third quintile

Second quintile

Lowest quintile

0

1,000

2,000

3,000

4,000

5,000

6,000

Highest quintile

Fourth quintile

Third quintile

Second quintile

Lowest quintile

EQUIVALISED HOUSEHOLD

NET WORTH

Australia, 2003–04 to 2013–14

EQUIVALISED DISPOSABLE HOUSEHOLD

INCOME

Australia, 1994–95 to 2013–14

Source: ABS (2015) 6523.0 Household Income and Wealth 2013-14 (Tables 1.1 and 2.2)

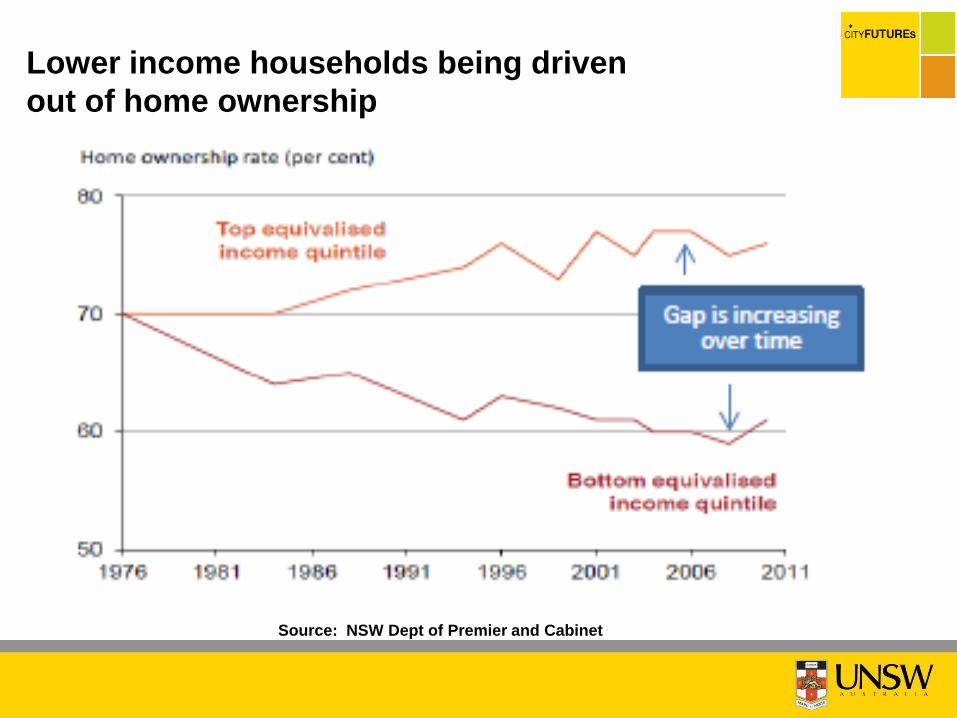

Lower income households being driven

out of home ownership

Source: NSW Dept of Premier and Cabinet

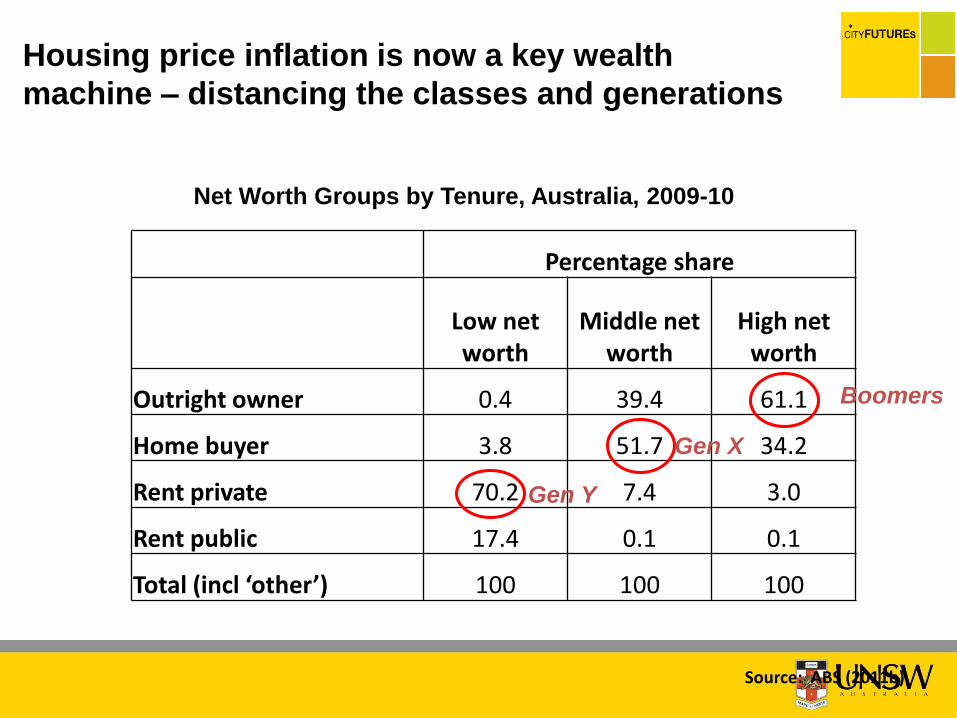

Percentage share

Low net worth

Middle net worth

High net worth

Outright owner 0.4 39.4 61.1

Home buyer 3.8 51.7 34.2

Rent private 70.2 7.4 3.0

Rent public 17.4 0.1 0.1

Total (incl ‘other’) 100 100 100

Net Worth Groups by Tenure, Australia, 2009-10

Source: ABS (2011b)

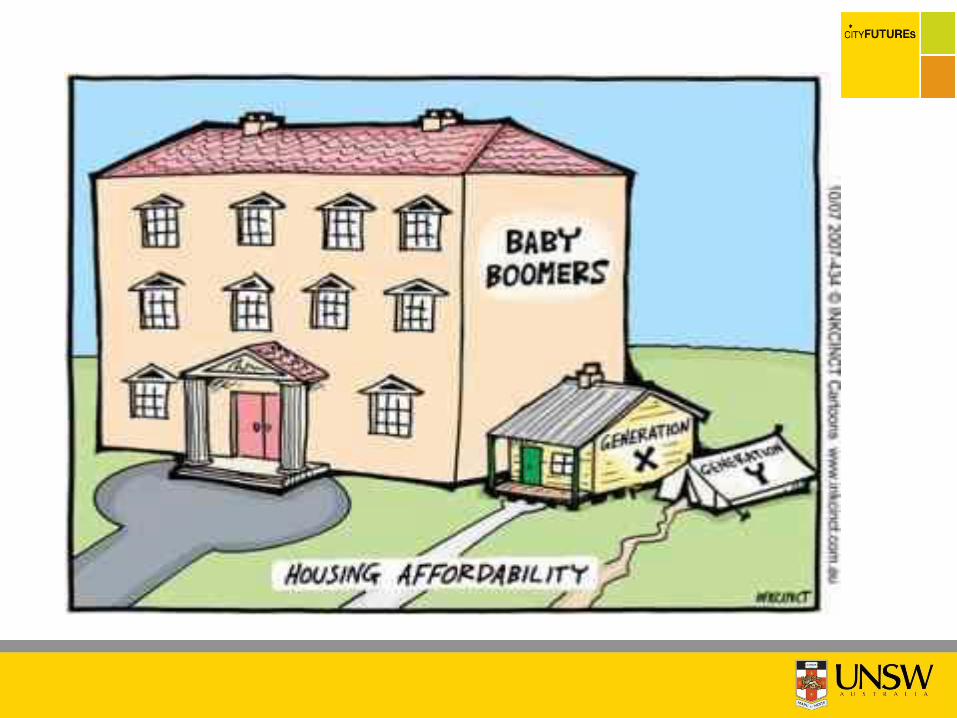

Housing price inflation is now a key wealth

machine – distancing the classes and generations

Boomers

Gen Y

Gen X

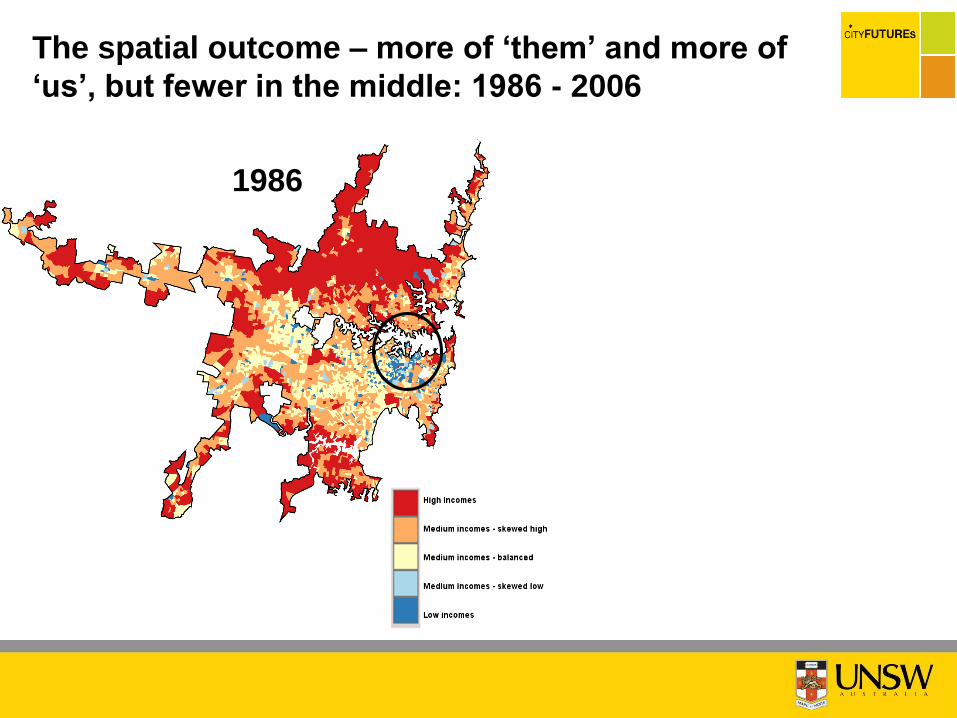

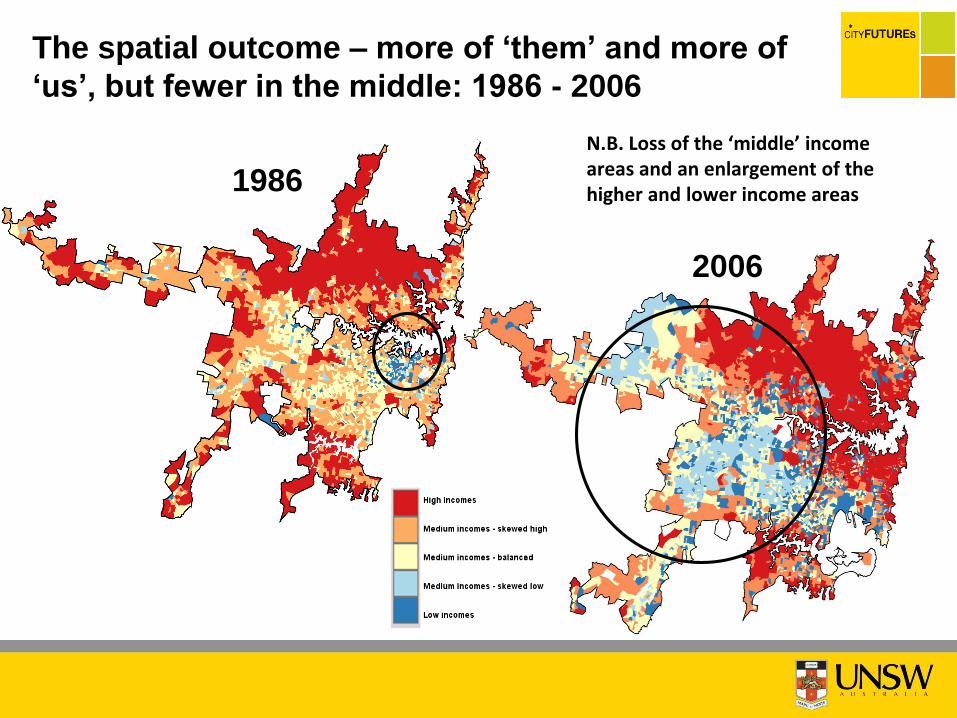

The spatial outcome – more of ‘them’ and more of

‘us’, but fewer in the middle: 1986 - 2006

20011986

2001

2006

1986

N.B. Loss of the ‘middle’ income areas and an enlargement of the higher and lower income areas

The spatial outcome – more of ‘them’ and more of

‘us’, but fewer in the middle: 1986 - 2006

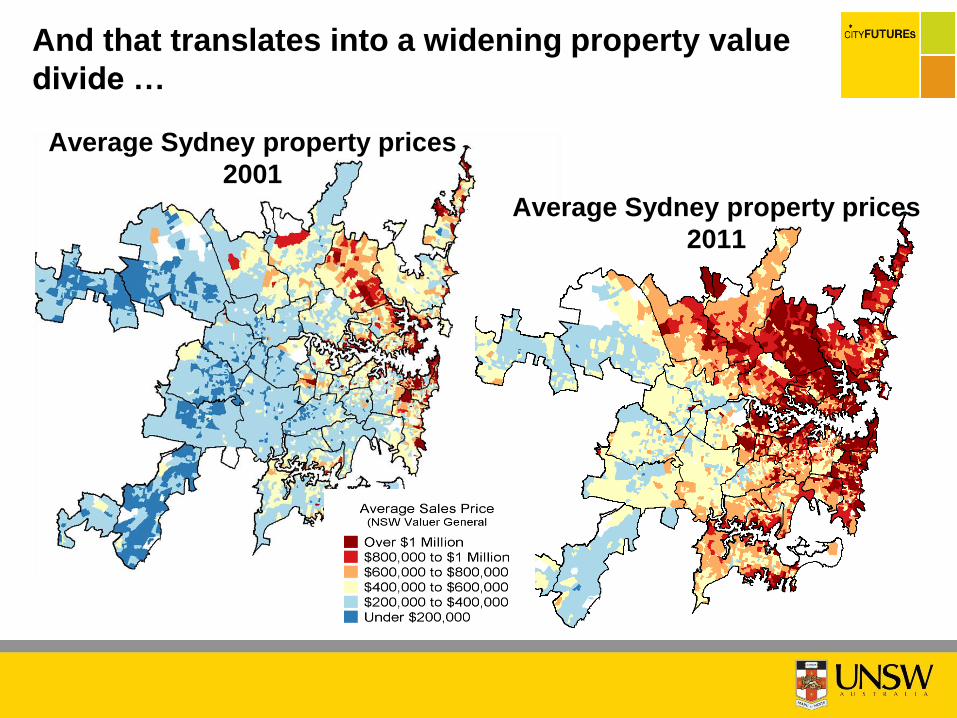

And that translates into a widening property value

divide …

Average Sydney property prices

2011

Average Sydney property prices

2001

0

20

40

60

80

100

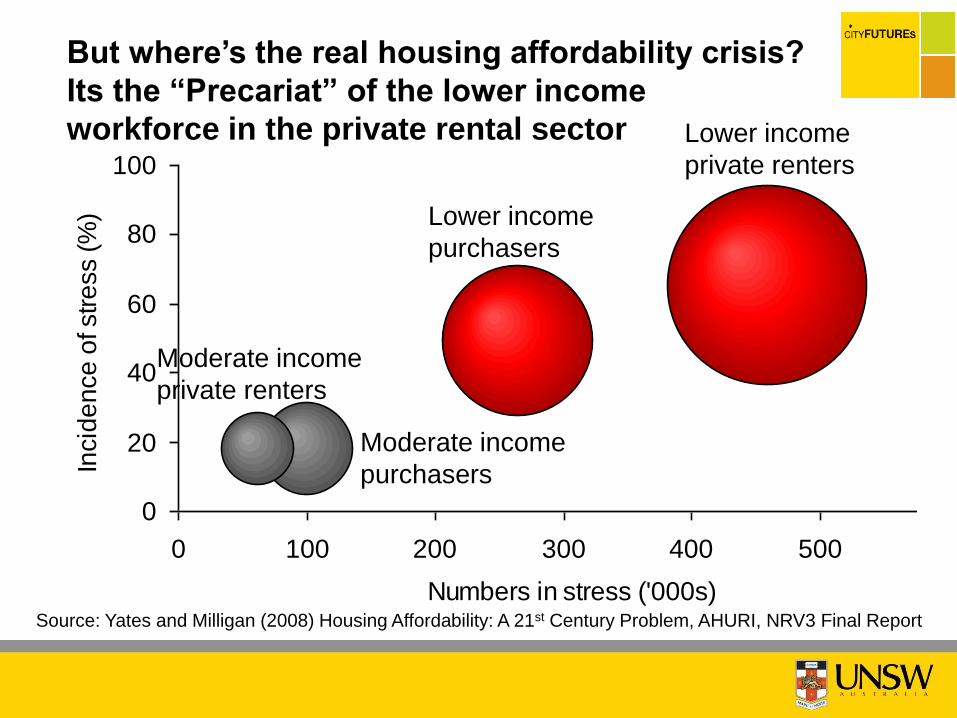

0 100 200 300 400 500 600

Numbers in stress ('000s)

Incid

en

ce

of str

ess (

%)

Lower income

private renters

Lower income

purchasers

Moderate income

purchasers

Moderate income

private renters

Source: Yates and Milligan (2008) Housing Affordability: A 21st Century Problem, AHURI, NRV3 Final Report

But where’s the real housing affordability crisis?

Its the “Precariat” of the lower income

workforce in the private rental sector

• Rents rising faster than

incomes so rental affordability

declining

• Nationally, 54% of lower

income renter households

facing unaffordable rents in

201153

46

3840

10 14

0%

20%

40%

60%

80%

100%

2006 2011

% o

f a

ll lo

we

r in

co

me

pri

va

te r

en

ters

Private renters in lowest 40% of income distribution, 2006 and 2011

Paying severely unaffordable rent

Paying unaffordable rent

Paying affordable rent

Source: Hulse et al (2015)

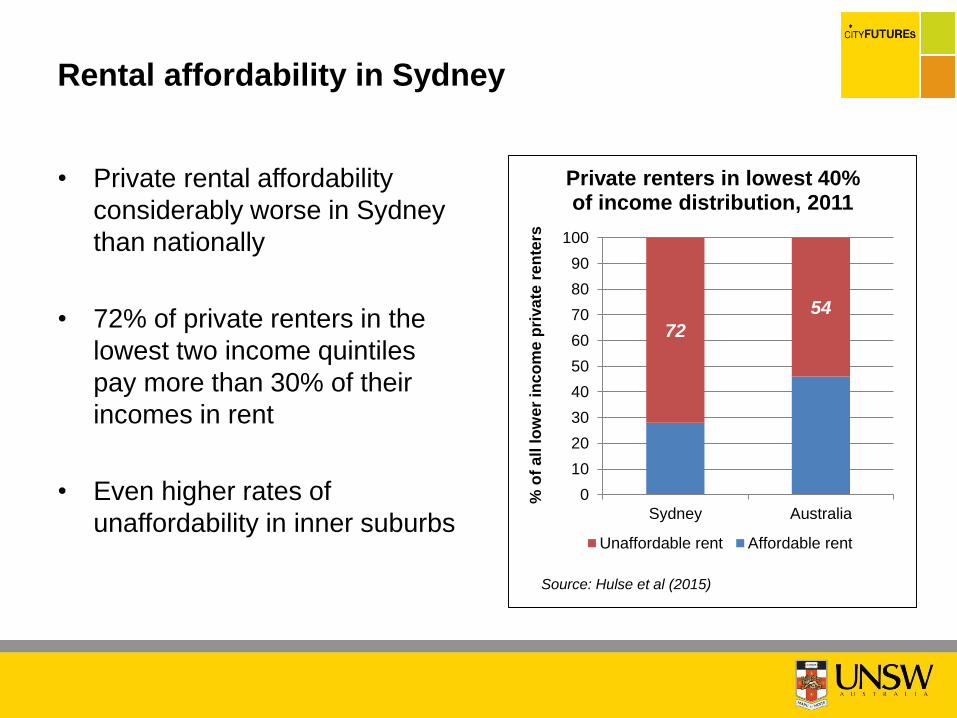

Private rental affordability – Australia-wide

• Private rental affordability

considerably worse in Sydney

than nationally

• 72% of private renters in the

lowest two income quintiles

pay more than 30% of their

incomes in rent

• Even higher rates of

unaffordability in inner suburbs

72

54

0

10

20

30

40

50

60

70

80

90

100

Sydney Australia

% o

f a

ll lo

we

r in

co

me

pri

va

te r

en

ters

Private renters in lowest 40% of income distribution, 2011

Unaffordable rent Affordable rent

Source: Hulse et al (2015)

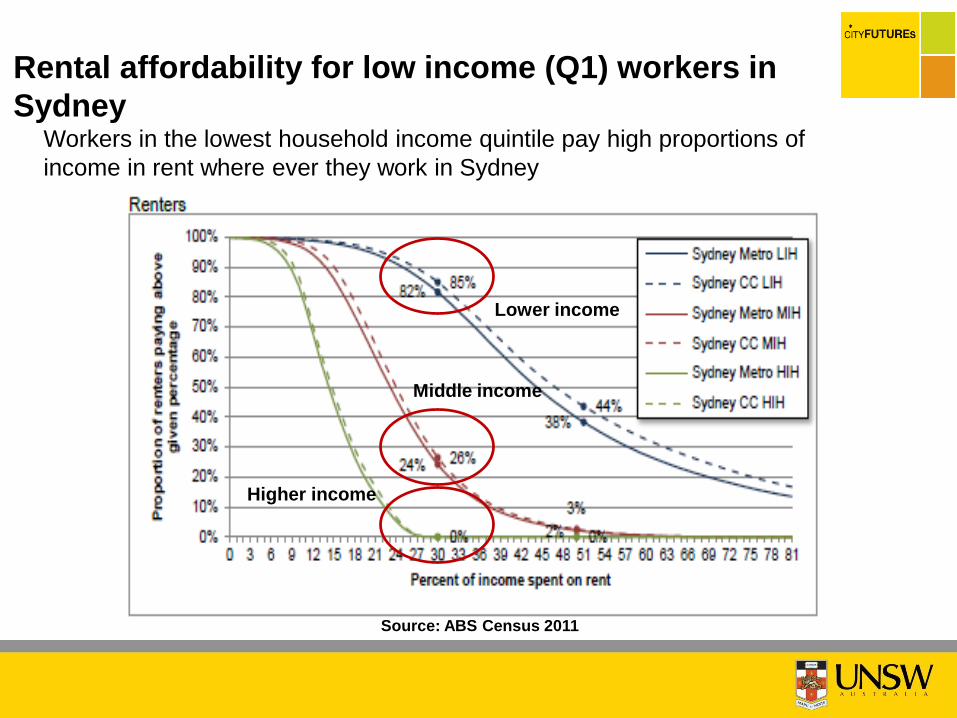

Rental affordability in Sydney

Workers in the lowest household income quintile pay high proportions of

income in rent where ever they work in Sydney

Rental affordability for low income (Q1) workers in

Sydney

Lower income

Middle income

Higher income

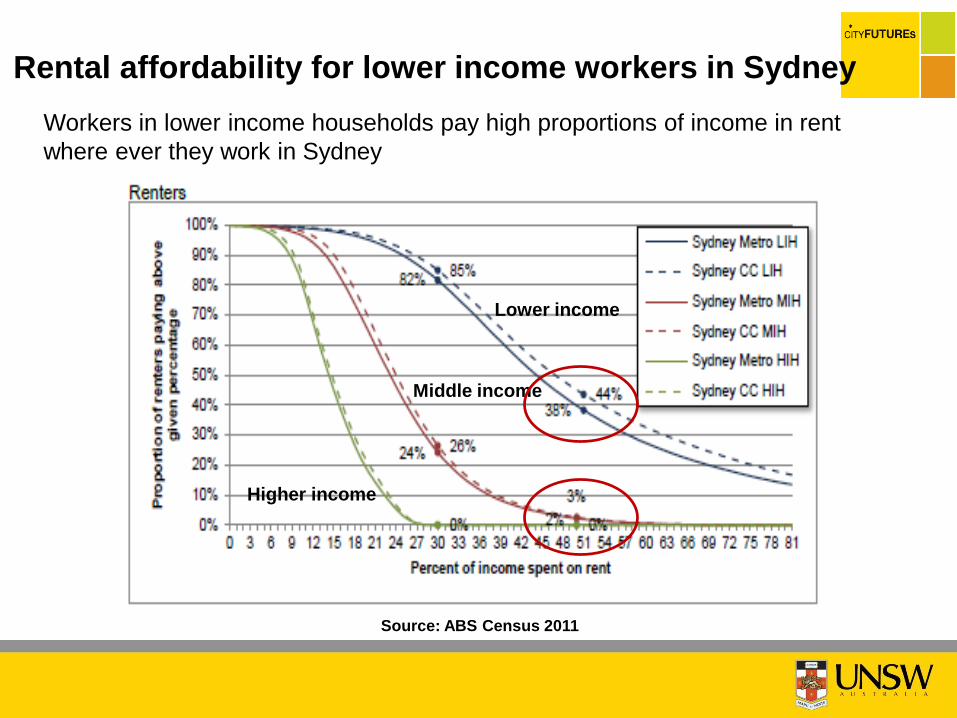

Source: ABS Census 2011

Workers in lower income households pay high proportions of income in rent

where ever they work in Sydney

Lower income

Middle income

Higher income

Source: ABS Census 2011

Rental affordability for lower income workers in Sydney

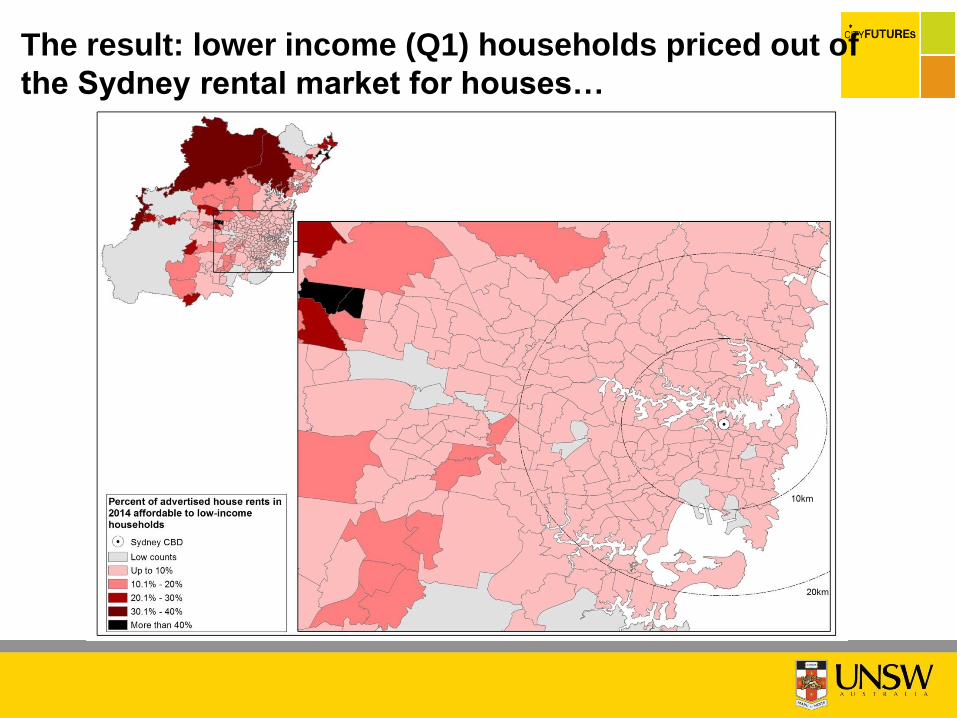

The result: lower income (Q1) households priced out of

the Sydney rental market for houses…

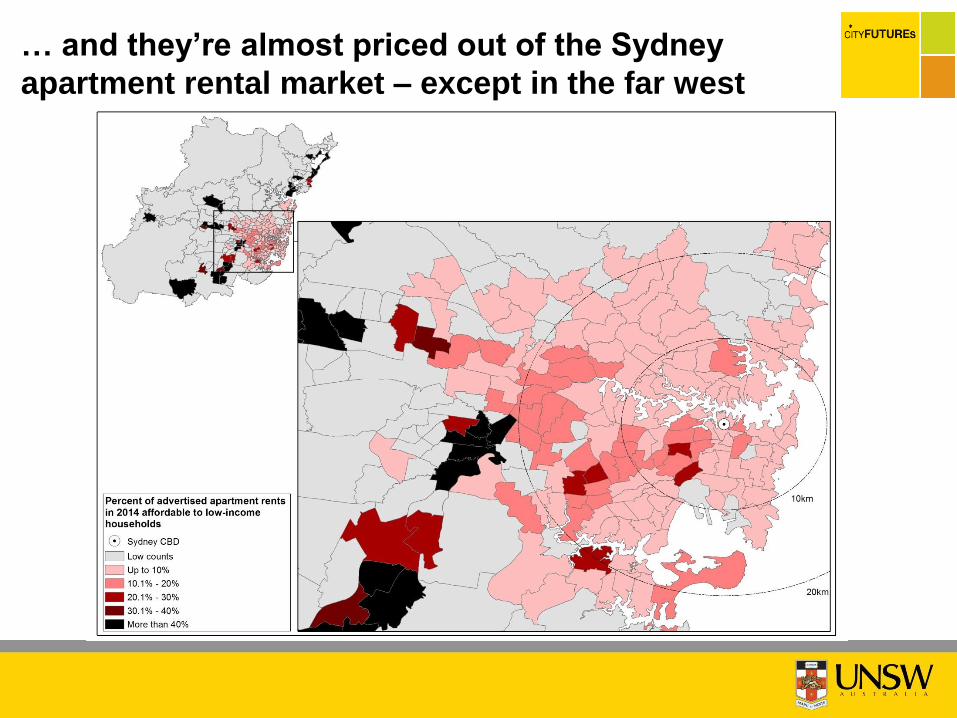

… and they’re almost priced out of the Sydney

apartment rental market – except in the far west

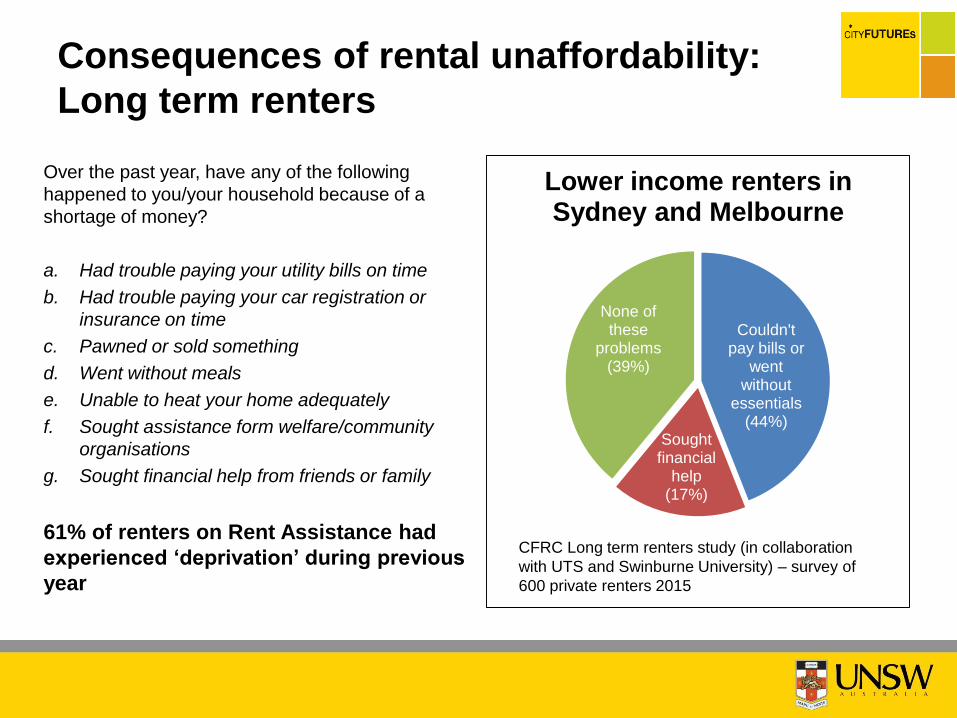

Over the past year, have any of the following

happened to you/your household because of a

shortage of money?

a. Had trouble paying your utility bills on time

b. Had trouble paying your car registration or

insurance on time

c. Pawned or sold something

d. Went without meals

e. Unable to heat your home adequately

f. Sought assistance form welfare/community

organisations

g. Sought financial help from friends or family

61% of renters on Rent Assistance had

experienced ‘deprivation’ during previous

year

Couldn't pay bills or

went without

essentials (44%)

Sought financial

help (17%)

None of these

problems (39%)

Lower income renters in Sydney and Melbourne

CFRC Long term renters study (in collaboration

with UTS and Swinburne University) – survey of

600 private renters 2015

Consequences of rental unaffordability:

Long term renters

• 10-point plan highlights need for actions to:– Cool overpriced market by correcting tax system distortions to

moderate price rises over the longer term

– Redirect effective rental housing subsidies to new affordable

rental through institutional investment

– Direct intervention to expand affordable housing in high demand

locations – inclusionary zoning backed by targeted support for

affordable housing ($1bn NSW Poles and Wires?)

• For State Govts, more scope for actions of third type

– esp. through planning powers

• Compared with NY and London, little Sydney action

to preserve and expand AH since 1990s

• One result: decisive & damaging outward shift in low

income population – remote from job growth zones

• Current NSW Govt may be facing up to problem

• Chance to embed affordable housing in new wave of

major Urban Renewal projects must not be missed

Intervening to tackle Australia’s housing

unaffordability – a 10-point plan for affordable rental

Hal Pawson,

UNSW

Viv Milligan,

UNSW

Peter Phibbs,

Univ of SydneyJudy Yates,

Univ of Sydney

Nicole Gurran,

Univ of Sydney

Michael Darcy,

UWS

10-point plan co-authors

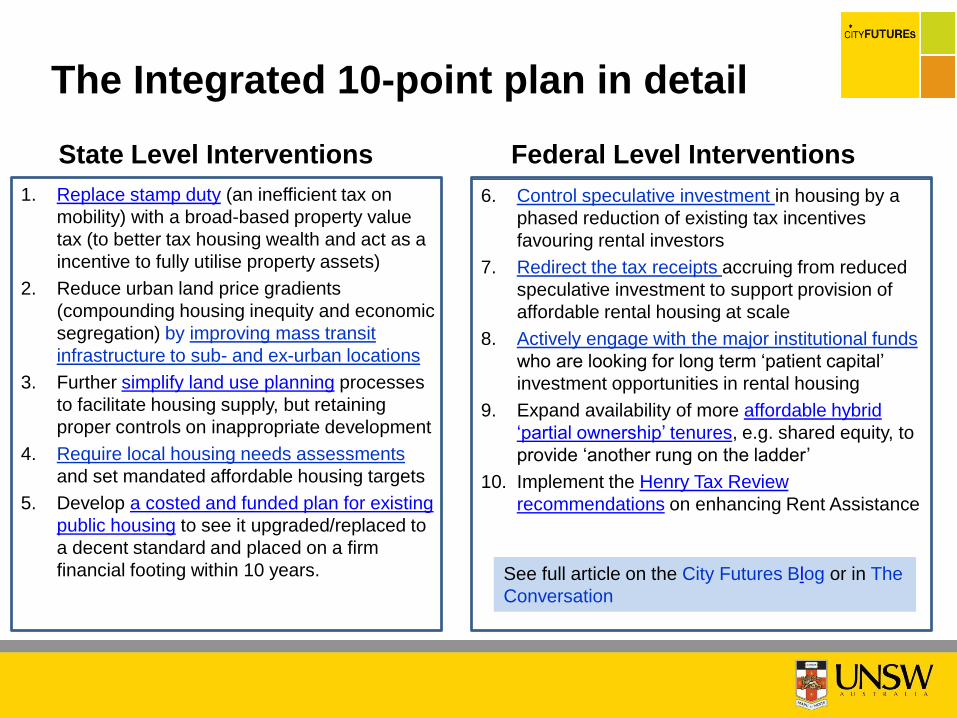

The Integrated 10-point plan in detail

6. Control speculative investment in housing by a

phased reduction of existing tax incentives

favouring rental investors

7. Redirect the tax receipts accruing from reduced

speculative investment to support provision of

affordable rental housing at scale

8. Actively engage with the major institutional funds

who are looking for long term ‘patient capital’

investment opportunities in rental housing

9. Expand availability of more affordable hybrid

‘partial ownership’ tenures, e.g. shared equity, to

provide ‘another rung on the ladder’

10. Implement the Henry Tax Review

recommendations on enhancing Rent Assistance

1. Replace stamp duty (an inefficient tax on

mobility) with a broad-based property value

tax (to better tax housing wealth and act as a

incentive to fully utilise property assets)

2. Reduce urban land price gradients

(compounding housing inequity and economic

segregation) by improving mass transit

infrastructure to sub- and ex-urban locations

3. Further simplify land use planning processes

to facilitate housing supply, but retaining

proper controls on inappropriate development

4. Require local housing needs assessments

and set mandated affordable housing targets

5. Develop a costed and funded plan for existing

public housing to see it upgraded/replaced to

a decent standard and placed on a firm

financial footing within 10 years. See full article on the City Futures Blog or in The

Conversation

State Level Interventions Federal Level Interventions

Resetting the rules: A New Framework for Affordable Housing?

www.cityfutures.net.au

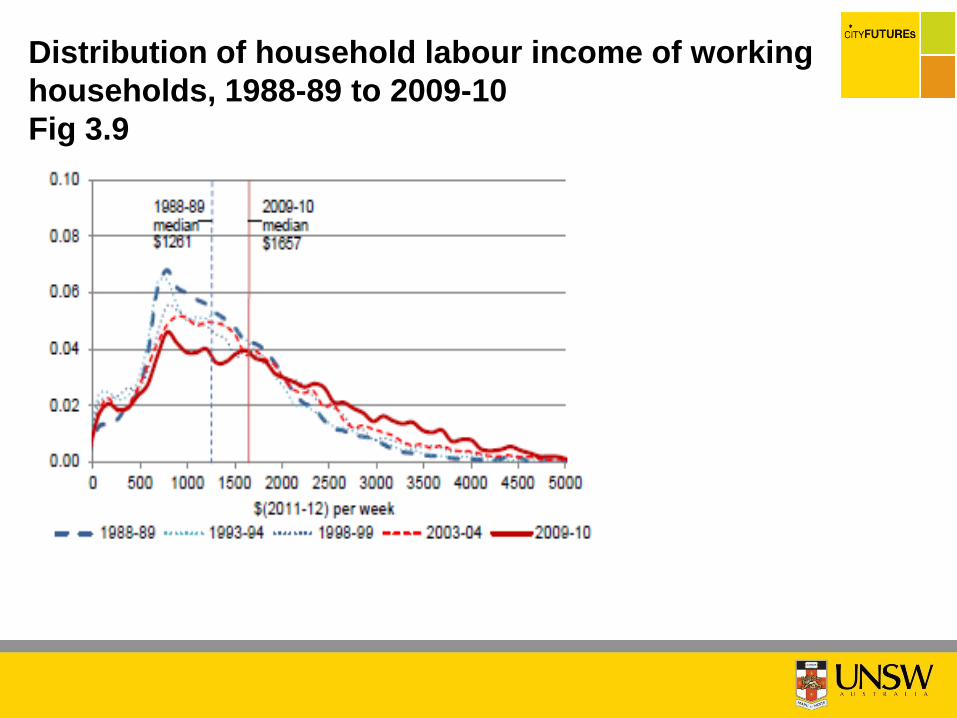

Distribution of household labour income of working

households, 1988-89 to 2009-10

Fig 3.9

Like what you see?Be part of our conversation.

informa.com.au

Join our e-newsletter