Embed Size (px)

DESCRIPTION

About V A T

Citation preview

CONTENT

Sr.No.

Topics Covered Page No.

1 Section – I Introduction to Value Added Tax. 1 – 12

2 Section – II Value Added Tax 13

A. Introduction.B. Registration under Value Added Tax.C. Explaining Value Added Tax.D. Calculating Tax Liability.E. Filing of Return and Paying Tax.F. Records and Accounts.G. Business Audit.H. Appeals.I. Tax Payer Service.J. Recovery, Offences and Penalties.

14 – 1617 – 2122 – 2728 – 3637 – 4445 – 4849 – 5152 – 5657 – 6162 – 66

3 Section – III Appendix. 67 – 69

4 Section – IV Conclusion. 70

5 Section – V Bibliography. 71

Value Added Tax

- 1 -

WHAT IS VALUE ADDED TAX?

Value Added Tax is a broad-based commodity tax that is levied at multiplestages of production. The concept is akin to excise duty paid by the

manufacturer who, in turn, claims a credit on input taxes paid. Excise duty is onmanufacture, while VAT is on sale and both work in the same manner,according to the white paper on VAT released by finance minister Chidambaram.

The document was drawn up after all states, barring UP, were prepared toimplement VAT from April. It is usually intended to be a tax on consumption,

hence the provision of a mechanism enabling producers to offset the tax theyhave paid on their inputs against that charged on their sales of goods andservices. Under VAT revenue is collected throughout the production process

without distorting any production decisions.

WHY VAT IS PREFERRED OVER SALES TAX?

While theoretically the amount of revenue collected through VAT is equivalentto sales tax collections at a similar rate, in practice VAT is likely to generate

more revenue for government than sales tax since it is administered on variousstages on the production – distribution chain. With sales tax, if final sales are

not covered by the tax system e.g. due to difficulty of covering all the retailers,particular commodities may not yield any tax. However, with VAT somerevenue would have been collected through taxation of earlier transactions,

even if final retailers evade the tax net.

There is also in-built pressure for compliance and auditing under VAT since it

will be in the interest of all who pay taxes to ensure that their eligibility for taxcredits can be demonstrated. VAT is also a fairer tax than sales tax as it

minimizes or eliminates the problem of tax cascading, which often occurs with

Value Added Tax

- 2 -

sales tax. These are facilitated by the fact that VAT operates through a creditsystem so that tax is only applied on value added at each stage in theproduction – distribution chain. At each intermediate stage credit will be given

for taxes paid on purchases to set against taxes due on sales. Only atconsumption stage where there are no further transactions will there be no taxcredits. Lack of input credit facility in sales tax often results in tax on inputs

becoming a cost to businesses which are often passed on to consumers. Salestax is often applied again to the sales tax element of the cost, thus there is a

problem of tax on tax. This is not the case with VAT, which makes it a neutraltax as it provides the least disturbance to patterns of production and thegeneration and use of income.

In addition, the audit trail that exists under the VAT system makes it a moreeffective tax in administration terms than sales tax as it helps with the

verification of VAT amounts declared as due. This is made possible by the factthat one person’s output is another’s input. As with sales tax imports are

treated the same way as local goods while exports are zero- rated to avoidanti-export bias.

Notwithstanding the advantages mentioned above, it is worth noting that VAT isa considerably complex tax to administer compared with sales tax. It may bedifficult to apply to small companies due to difficulties of record keeping and

its coverage in agriculture and the services sector may be limited. To cover thehigh administration costs, VAT rates of 10-20 per cent are generally

recommended. The equity impact of the relatively high rates have been a causefor concern as it is possible that the poor spend relatively high proportions oftheir incomes on goods subject to VAT. Thus the concept of zero VAT rate on

some items has been introduced.

Value Added Tax

- 3 -

DIFFERENCE BETWEEN VAT AND CST

Under the CST Act, the tax is collected at one stage of purchase or sale of

goods. Therefore, the burden of the full tax bond is borne by only one dealer,either the first or the last dealer. However, under the VAT system, the tax

burden would be shared by all the dealers from first to last. Then, such taxwould be passed upon the final consumers.Under the CST Act, the tax is levied at a single point. Under the VAT system, the

retailers are not subject to tax except for the retail tax.

Under the CST Act, general and specific exemptions are granted on certain

goods while VAT does not permit such exemptions. Under the CST law,concessional rates are provided on certain taxes. The VAT regime will do away

with such concessions as it would provide the full credit on the tax that hasbeen paid earlier.

Under VAT law, first, the dealer pays tax on the sale or purchase of goods. Thesubsequent dealer pays tax on the portion of the value added upon such goods.Thus, the tax burden is shared equally by the last dealer. To illustrate the whole

procedure of VAT, an example is as follows:

At the first point of sale, the value of goods is Rs.100. The tax on this is 12.5%.Therefore, the net VAT would be 12.5%. At the second change of sale, the salevalue is Rs.120 and the tax thereon is 15%. The tax that is to be paid at every

point is 15%. The input tax is 15%. The dealer will get a credit for first change insale of 2.5%-- i.e. 15% -12.5%. Therefore, 2.5% will be the net rate. At the thirdchange of sale, the sale value is Rs.150 and the tax on this is 18.75%. At the

last stage, the tax paid is 18.75%. The Input Tax is 18.75%. Dealer’s get a creditfor second change in sale? i.e. 18.75% -15% = 3.75%. Therefore, 3.75% would

Value Added Tax

- 4 -

be the net VAT. This means that VAT is paid in the last point tax under the saletax regime.

Value Added Tax

- 5 -

WHO GAINS?

State and Central governments gain in terms of revenue. VAT has in-builtincentives for tax compliance — only by collecting taxes and remitting them to

the government can a seller claim the offset that is due to him on his purchases.Everyone has an incentive to buy only from registered dealers — purchasesfrom others will not provide the benefit of credit for the taxes paid at the time

of purchase. This transparency and in-built incentive for compliance wouldincrease revenues. Industry and trade gain from transparency and reduced need

to interact with the tax personnel. For those who have been complying withtaxes, VAT would be a boon that reduces the cost of the product to theconsumer and boosts competitiveness. VAT would be major blow for tax

evaders, both manufacturers who evade excise duty payments and traders whoevade sales-tax.

WHAT’LL BE THE TAX BURDEN?

The overall tax burden will be rationalized as it’ll be shared by all dealers, andprices, in general, will fall. Moreover, VAT will replace the existing system of

inspection by a system of built-in self-assessment by traders andmanufacturers. The tax structure will become simple and more transparent and

tax compliance will improve significantly. It will also be simpler and offer easycomputation and easy compliance. VAT will prevent cascading effect throughinput rebate and help avoid distortions in trade and economy by ensuring

uniform tax rates.

WHO PAYS?

Value Added Tax

- 6 -

All dealers registered under VAT and all dealers with an annual turnover ofmore than Rs 5 lakh will have to register. Dealers with turnovers less than Rs 5lakh may register voluntarily.

Value Added Tax

- 7 -

HOW TO PAY?

VAT will be paid along with monthly returns. Credit will be given within thesame month for entire VAT paid within the state on purchase of inputs and

goods. Credit thus accumulated over any month will be utilized to deduct fromthe tax collected by the dealer during that month. If the tax credit exceeds thetax collected during a month on sale within the state, the excess credit will be

carried forward to the next month.

WHICH GOODS WILL BE TAXABLE UNDER VAT?

All goods except those specifically exempt. In fact, over 550 items will becovered under the new tax regime, of which 46 natural and unprocessed local

products would be exempt from VAT. About 270 items, including drugs andmedicines, all agricultural and industrial inputs, capital goods and declaredgoods would attract 4% VAT. But, following opposition from some states, it was

decided that states would have option to either levy 4% or totally exempt foodgrains from VAT but it would be reviewed after one year. Three items — sugar,textile, tobacco — under additional excise duties will not be under VAT regime

for one year but existing arrangement would continue.

OTHER CONSIDERATIONS

It is imperative that policy makers in considering adoption of VAT should beinterested in the economy wide impact of this tax. Special emphasis is often

placed on its effect on equity, prices and economic growth. This is particularlyimportant because of the potential effects on consumption of certaincommodities that have a direct or indirect effect on labour productivity.

Value Added Tax

- 8 -

VAT EFFECT ON INFLATION

In considering the introduction of VAT, countries are often concerned that itwould cause an inflationary spiral. However there is no evidence to suggest that

this is true. A survey of OECD countries that introduced VAT indicated that VAThad little or no effect on prices. In cases where there was an effect it was a onetime effect that simply shifted the trend line of the consumer price index (CPI).

To guard against any unforeseen price effects the authorities may consider atighter monetary policy stance at the introduction of VAT.

DISTRIBUTION EFFECTS OF VAT

Value added tax is widely criticized as being regressive with respect to income

that is its burden falls heavily on the poor than on the rich. This emanates fromthe fact that consumption as a share of income falls as income rises. Hence auniform VAT rate falls heavily on the poor than the rich. This criticism is valid

when VAT payments are expressed as a proportion of current income. Howeverif, following the premise that welfare is demonstrated by the level ofconsumption rather than income, consumption is used as the denominator the

impact of VAT would be proportional. A proportional burden would also bedemonstrated if lifetime income rather than current income is used. A lifetime

income concept considers the fact that many income recipients are onlytemporarily at lower income brackets as their earnings increase. In order toaddress the regressivity of VAT the following measures can be taken:

♦ The VAT itself can be used to differentiate taxation of consumer itemsthat are consumed primarily by the poor such that they pay less or at zero rate

or to tax luxury goods at a higher than standard rate.

Value Added Tax

- 9 -

♦ VAT exemptions may also be granted on goods and services that areconsumed mostly by the poor.

♦ Equity concerns may also be addressed through other ways, outside theVAT system, such as other tax and spending instruments of government. Thiscould be in the form of lower basic income tax rates on the poor or some

pro-poor expenditures of government. The use of multiple rates of VAT hashowever been widely discouraged for various reasons. These include:

♦ The fact that sometimes it is almost impossible to differentiatebetween higher quality expensive products – e.g. food, consumed by the rich

and ordinary products consumed by the poor. Thus any concessions extendedmay tend to benefit the rich much more than the poor.

♦ Increased costs of VAT administration as a differentiated ratestructure brings with it problems of delineating products and interpreting

the rules on which rate to use.

♦ significantly increased costs of tax compliance for small firms, which are

usually unable to keep separate records/accounts for sales of differently taxeditems. This results in the use of presumptive methods of determiningthe tax liability, which leads to more difficulties in monitoring the

compliance. The higher compliance cost resultant from differentiation of VATrates may also be regressive with respect to income since smaller firms with

lower income tend to bear proportionately more of the burden than do largerfirms.

Exemptions refer to situations where output is not taxed but taxes paid oninputs are not recoverable. The rationale behind exemptions is to reducenegative distributional effects of tax through the effect on incomes. The effects

of exemption may be as follows:

Value Added Tax

- 10 -

♦ falling of revenues – exemptions break the VAT chain. If exemptions aregranted at prior to the final sale, it results in a loss of revenue since value

added at the final stage escapes tax.

♦ Un-recovered taxation of some intermediate goods may lead to

producers substituting away from such inputs thus distorting the input choicesof the said producers.

♦ Exemptions may create incentives to “self supply” i.e. tax avoidance byvertical integration.

♦ Exemptions tend to feed on each other giving rise to a phenomenoncalled “exemption creep”. This arises from the fact that each exemption gives

rise to pressures on further exemption. For example creating an exemption toreduce the tax burden on a particular commodity or goods may lead to

increased pressure for exemption or zero rating of inputs used for theproduction of such a commodity.

Based on the above, it is important that care is taken when introducingexemptions in order to avoid distortions in the production process as well as tominimize revenue loss resulting from such distortions.

Given the fact that the primary purpose of VAT is to raise government revenue

in an efficient manner and with as little distortions of economic activity aspossible, distribution effects are perhaps better addressed by other forms oftax and government expenditure policies which can often be better targeted at

these aims.

Value Added Tax

- 11 -

VAT EFFECT ON ECONOMIC GROWTH

Economic growth can be facilitated through investment by both governmentand the private sector. Savings by both parties are required in order to finance

investment in a non-inflationary manner. Compared to other broadly basedtaxes such as income tax VAT is neutral with respect to choices on whetherto consume now or save for future consumption. Although VAT reduces the

absolute return on saving it does not reduce the net rate of return on saving.Income tax reduces the net rate of return as both the amount saved as well as

the return on that saving are subject to tax. In this regard VAT may be said tobe a superior tax in promoting economic growth than income tax. Since VATdoes not influence investment decisions on firms, by increasing their costs, its

effects on investment can be said to be neutral.

FEATURES OF VAT

1. Rate of Tax VAT proposes to impose two types of rate of tax mainly:

a. 4% on declared goods or the goods commonly used.b. 10-12% on goods called Revenue Neutral Rates (RNR). There wouldbe no fall in such remaining goods.

c. Two special rates will be imposed-- 1% on silver or gold and 20%on liquor. Tax on petrol, diesel or aviation turbine fuel are

proposed to be kept out from the VAT system as they would becontinued to be taxed, as presently applicable by the CST Act.

2. Uniform Rates in the VAT system, certain commodities are exempted

from tax. The taxable commodities are listed in the respective schedulewith the rates. VAT proposes to keep these rates uniform in all the statesso the goods sold or purchased across the country would suffer the same

tax rate. Discretion has been given to the states when it comes tofinalizing the RNR along with the restrictions. This rate must not be less

Value Added Tax

- 12 -

than 10%. This will ensure By doing this that there will be level playingfields to avoid the trade diversion in connection with the different states,particularly in neighboring states

3. No concession to new industries Tax Concessions to new industries isdone away with in the new VAT system. This was done as it createsdiscrepancy in investment decision. Under the new VAT system, the tax

would be fair and equitable to all.4. Adjustment of the tax paid on the goods purchased from the tax payable

on the goods of sale All the tax, paid on the goods purchased within thestate, would be adjusted against the tax, payable on the sale, whetherwithin the state or in the course of interstate. In case of export, the tax,

paid on purchase outside India, would be refunded. In case of the branchtransfer or consignment of sale outside the state, no refund would beprovided.

5. Collection of tax by seller/dealer at each stage. The seller/dealer wouldcollect the tax on the full price of the goods sold and shows separately in

the sell invoice issued by him6. VAT is not cascading or additive though the tax on the goods sold iscollected at each stage, it is not cascading or additive because the net

effect would be as follows: - the tax, previously paid on the sale of goods,would be fully adjusted. It will be like levying tax on goods, sold in thelast state or at retail stage.

Value Added Tax

- 13 -

WHAT’S THE BIGGEST ADVANTAGE?

The biggest benefit of VAT is that it could unite India into a large commonmarket. This will translate to better business policy. Companies can start

optimizing purely on logistics of their operations, and not on based ontax-minimization. Lorries need not wait at check-points for days; they canzoom down the highways to their destinations. Reduced transit times and lower

inventory levels will boost corporate earnings. Following are the some moreadvantage of VAT: -

1. Simplification Under the CST Act, there are 8 types of tax rates- 1%, 2%,4%, 8%, 10%, 12%, 20% and 25%. However, under the present VAT system,

there would only be 2 types of taxes 4% on declared goods and 10-12%on RNR. This will eliminate any disputes that relate to rates of tax andclassification of goods as this is the most usual cause of litigation. It also

helps to determine the relevant stage of the tax. This is necessary as theCST Act stipulates that the tax levies at the first stage or the last stagediffer. Consequently, the question of which stage of tax it falls under

becomes another reason for litigation. Under the VAT system, tax wouldbe levied at each stage of the goods of sale or purchase.

2. Adjustment of tax paid on purchased goods Under the present system,the tax paid on the manufactured goods would be adjusted against thetax payable on the manufactured goods. Such adjustment is conditional

as such goods must either be manufactured or sold. VAT is free fromsuch conditions.

3. Further such adjustment of the purchased goods would depend on the

amount of tax that is payable. VAT would not have such restrictions. CSTwould not have the provisions on refund or carry over upon such goods

except in case of export goods or goods, manufactured out of thecountry or sale to registered dealer. Similarly, on interstate sale ontax-paid goods, no refund would be admissible.

Value Added Tax

- 14 -

4. Transparency The tax that is levied at the first stage on the goods or saleor purchase is not transparent. This is because the amount of tax, whichthe goods have suffered, is not known at the subsequent stage. In the

VAT system, the amount of tax would be known at each and every stageof goods of sale or purchase.

5. Fair and Equitable VAT introduces the uniform tax rates across the state

so that unfair advantages cannot be taken while levying the tax.6. Procedure of simplification Procedures, relating to filing of returns,

payment of tax, furnishing declaration and assessment are simplifiedunder the VAT system so as to minimize any interface between the taxpayer and the tax collector.

7. Minimize the Discretion the VAT system proposes to minimize thediscretion with the assessing officer so that every person is treated alike.For example, there would be no discretion involved in the imposition of

penalty, late filing of returns, non-filing of returns, late payment of tax ornon payment of tax or in case of tax evasion. Such system would be free

from all these harassment8. Computerization the VAT proposes computerization which would focuson the tax evaders by generating Exception Report. In a large number of

cases, no processing or scrutiny of returns would be required as it wouldfree the tax compliant dealers from all the harassment which is so mucha part of assessment. The management information system, which would

form a part of integral computerization, would make the tax departmentmore efficient and responsive.

Value Added Tax

- 15 -

VALUE ADDED TAX IN MAHARASHTRA

Quick Flash Back

Sales tax was first introduced in India in the then Bombay Province as early as

March 1938 where a tax was imposed on sale of tobacco within certain urbanand suburban areas. In the year 1946, a general sales tax was introduced

levying sales tax at the last stage of sale of goods.The Bombay Sales Tax Act, 1959 introduced in 1959 underwent many changesthereafter and in July 1981, first point tax was introduced wherein goods were

classified into three main schedules, broadly covering tax free goods,intermediate products and finished goods. The BST Act was repealed and

Maharashtra Value Added Tax Act, 2002 came into force w.e.f. 1st April, 2005 tousher in the progressive value added tax system in place of the old sales taxsystem.

VAT is a progressive and transparent system of taxation which eliminates thecascading impact of multiple taxation through a multipoint taxation and set-offprinciple. It promotes transparency, compliance and equity and therefore, is

both dealer friendly and consumer friendly.VAT being a multi point tax, envisages an increase in the number of dealers and

is based on the concept of self-assessment and self-compliance. It is therefore,inevitable that the Sales Tax Department transforms itself into a dealer friendly,focused and dynamic department to cater to the ever increasing expectations of

both the Government and the Trade & Industry.Sales Tax Department has taken up the challenge to transform their selves andbe available for assisting the dealers in complying with the provisions of the law.

They are in the process of installing a state-wide networked IT system tocomputerise entire tax administration and hope to provide online service to the

dealers in due course. They are also realigning their organisational structure tomeet the challenges of the new system and stakeholders' expectations.

Value Added Tax

- 16 -

Part1 - Introduction

Background

Maharashtra is one of the 21 States which have introduced the Value Added Tax(VAT) system of taxation from 1st April 2005. With the introduction of VAT, theSales Tax Department has moved to a globally recognized sales taxation system

that has been adopted by more than 130 countries.

The design of Maharashtra State VAT is generally guided by the bestinternational practices with regard to legal framework, as well as operatingprocedures. Another key factor in preparation of the design of State level VAT is

the national consensus on certain issues. The consensus has been arrived atthrough the discussions in the Empowered Committee of State FinanceMinisters on implementation of State level VAT.

On 1st April 2005, VAT replaced the single point sales tax. Single point sales

tax had a number of disadvantages, primarily that of double taxation. VAT is amodern and progressive taxation system that avoids double taxation. Inaddition to offering the possibility of a set-off of tax paid on purchases, VAT

has other advantages for both business and government.

It eliminates cascading impact of double taxation and promotes economic

efficiency.

It is primarily a self-policing, self-assessment system with more trust put

on dealers.

It provides the potential for a stronger manufacturing base and morecompetitive export pricing.

It is invoice based, and as a result it offers a better financial system withless scope for error.

Value Added Tax

- 17 -

It has an improved control, mechanism resulting in better compliance.

It widens the, tax base and promotes equity.

VAT in Maharashtra is levied under a legislation known as the MaharashtraValue Added Tax Act (MVAT Act), supported by Maharashtra Value Added Tax

Rules (MVAT Rules). VAT is levied on sale of goods including intangible goods.

The meaning of “goods” for VAT purposes

“Goods” means every kind of moveable property including goods of incorporealand intangible nature but there are some exclusion, such as newspapers,

actionable claims, money, shares and securities and lottery tickets.

Businesses engaged in. the buying and selling of goods within the scope of theVAT law are referred to as dealers.

The meaning of 'sale' for VAT purposes

A transaction of sale can be a:

normal sale of goods;

sale of goods under hire-purchase system;

deemed sale of goods used I supplied in the course of execution of works

contract;

deemed sale of goods given on lease.

The rate of tax applicable to the goods sold under various classes of sales is

uniform. However, in respect of normal sales of goods and deemed sales ofgoods under works contract and specified deemed sale of goods given on lease,the Act provides for an optional method for discharging tax liability by way of

composition. Being so, the tax liability has to be determined with reference tothe option exercised by the dealer for discharging tax liability.

Value Added Tax

- 18 -

Businesses covered by VAT

The VAT system embraces all businesses in the production and supply chain,from manufacture through to retail. VAT is collected at each stage in the chainwhen value is added to goods. 1t applies to al1 businesses, including importers,

exporters, manufacturers, distributors, wholesalers, retailers, works contractorsand lessors.

Value Added Tax

- 19 -

Part 2 - Registration under VAT

Rules for registration

If a dealer’s annual turnover exceeds the below mentioned threshold, then itmust register with the local office of the Sales Tax Department.

All Figures in Rs.

Category Annual Turnoverof Sales

Turnover of salesor purchase of

taxable goods notless than

Fees payable onregistration

Importer 1,00,000 10,000 100

Others 5,00,000 10,000 100

If the dealer’s turnover is less than the above threshold, then they are not liableto collect and pay VAT. However, if a dealer wishes to avail the benefits of beinga registered dealer, then they may apply for voluntary registration by paying a

fee of Rs.5,000/ -.

Benefits of being a registered dealer

As a registered dealer, they are entitled to:

collect VAT on the sales;

claim set-off of tax (input tax credit) paid on purchases;

Issue tax invoices and, be competitive.

Value Added Tax

- 20 -

Effective date of registration

The effective date of registration, that is, the date front which a dealer may

charge VAT on sales; will depend on the date they first become liable to payVAT. This date will be determined as follows:a) New businesses:

If a dealer is not registered because their annual turnover is less than thethreshold; their liability to account for VAT starts from the date they cross the

threshold.b) Existing businesses:If a dealer took over an existing business that is registered for VAT, then they

will be liable to pay tax on sales from the date they took over the business.c) Voluntary registration:If a dealer is registered on a voluntary basis, then he will be liable to account

for VAT from the date shown on the certificate of registration.d) Late registration:

If a dealer’s turnover has exceeded the appropriate threshold but they haveapplied late for registration, then he can charge VAT on his sales only after theyare registered, i.e., from the date shown on the certificate of registration.

Further, having crossed the threshold, it is an offence to be engaged inbusiness as a dealer without a certificate of registration

Certificate of registration

A dealer should prominently display the certificate and hologram, or a copy ofthe certificate and hologram, at each place where they carry can on their

business.

Value Added Tax

- 21 -

If a dealer has more than one place of business, then Sales Tax Office willprovide them, upon their request, one copy of the certificate of registration andhologram for each additional place of business.

If a dealer loses his / her certificate of registration or hologram, or it isaccidentally destroyed or defaced, then they may obtain a duplicate copy of the

certificate of hologram from their sales tax office.

The certificate of registration and hologram is personal to the dealer to whom itis issued and is non-transferable.

Changes to business circumstances

If, following dealer register, there are any amendments to the details they can

be reported while applying for registration, it must done within 60 days of thechange, inform us in writing.

Where the amendment involves a:

change in the name of the business;

change in the constitution of the business without dissolution of the

firm;

change in the trustees of a Trust;

change in the guardianship of a ward;

change in the Karta of a Hindu Undivided Family;

conversion of Private limited Company to a Public limited Company;

change in the place of business;

addition of new place of business;

formation of a partnership with regard to the business,

an application made by a dealer for insolvency or liquidation of their

business;

Value Added Tax

- 22 -

an application made against dealer’s business for insolvency or

liquidation;

opening or closing of a bank account;

A dealer will not need to make a fresh application for registration. However, the

communication to the Registering Authority concerned should be made withinsixty days of the change or occurrence of the event.

Cancellation of registration

A dealer will be liable to pay VAT while their registration is effective. If however,

their turnover falls below the threshold, he may choose to apply for cancellationof his registration. However, he should continue to collect and pay VAT in the

normal way until his registration is formally cancelled. Alternatively, they maybe allowed the registration to continue.

If a dealer:

discontinue the business;

dispose of or sell or transfer the business;

A dealer must inform the Sales Tax Department within 30 days of the event. In

case of disposal or sale of business, their successor will need to apply for afresh registration certificate.

For cancellation of registration a dealer should submit form 103 which isavailable with the local sales tax office. It can also be downloaded from the

website www.vat.maharashtra.gov.in

If the Sales Tax Department cancels the dealer’s registration, they must return

the Certificate of Registration

Value Added Tax

- 23 -

The cancellation of their certificate does not affect their liability to pay any tax,interest or penalties in respect of any period prior to the date of cancellation oftheir registration.

Value Added Tax

- 24 -

The obligations of a registered dealer

Following are the registration, which dealer’s are obliged to:

display prominently their certificate of registration and hologram in their

place of business, and a copy of the certificate and hologram in each ofthe other places where they carry on their business;

inform their sales tax office of any changes in the details previouslyreported to the sales tax office;

collect VAT on all sales at appropriate rates;

calculate the tax due and submit correct, complete and self¬ consistent

returns and pay the amount of tax due on or before the due dates;

issue tax invoice / bill or cash memorandum to all customers;

maintain adequate records and retain them for a period of five years from

the end of the tax year to which they relate;

extend co-operation to the officers of the Sales Tax Department at

dealer’s business premises and provide all assistance to them todischarge their duties.

Value Added Tax

- 25 -

Part 3 - Explaining VAT

How VAT works

When a dealer sell goods, the sale price is made up of two elements; the sellingprice of the goods and the tax on the sale. The tax is payable to the StateGovernment.

The tax payable on sales is to be calculated on the selling price. The tax paid

on purchases supported by a, valid tax invoice is generally available as set-off(input, tax credit) while discharging the tax liability on sales.

Example

The following example shows how the VAT works through the chain from

manufacturer to retailer.

Company A buys iron ore and other consumables and manufactures stainlesssteel utensils; Partnership firm B buys the utensils in bulk from Company Aand polishes them; shopkeeper C buys some of the utensils and purchases

packing, material from vendor D, packages them and sells the packed utensilsfor the public.

Value Added Tax

- 26 -

(The sale and purchase figures shown in the example are excluding tax)

Particulars Amount(Rs.)

VAT @4% (Rs.)

Company A

Cost of iron are and consumables 50,000 2000

Sales of unpolished stainless steel utensils 1,50,000

Value added 1,00,000

Company A is liable to pay VAT on Rs.1,50,000/- @

4%

6000

Less Set Off (2000)

Net VAT amount to pay with the Return (Note: Tax

invoice issued by Company A will show sale price asRs.1,50,000/- tax as Rs.6,000/-. Therefore, the

total invoice value will be Rs.1,56,000/-)

4000

Partnership B

Purchases unpolished stainless steel utensils. 1,50,000

Sales polished stainless steel utensils 1,80,000

Value added 30,000

Partnership B is liable to pay V AT on Rs.1,80,000 at4%

7,200

But can claim set off of tax paid on purchases (6,000)

Net VAT amount to pay with the Return 1200

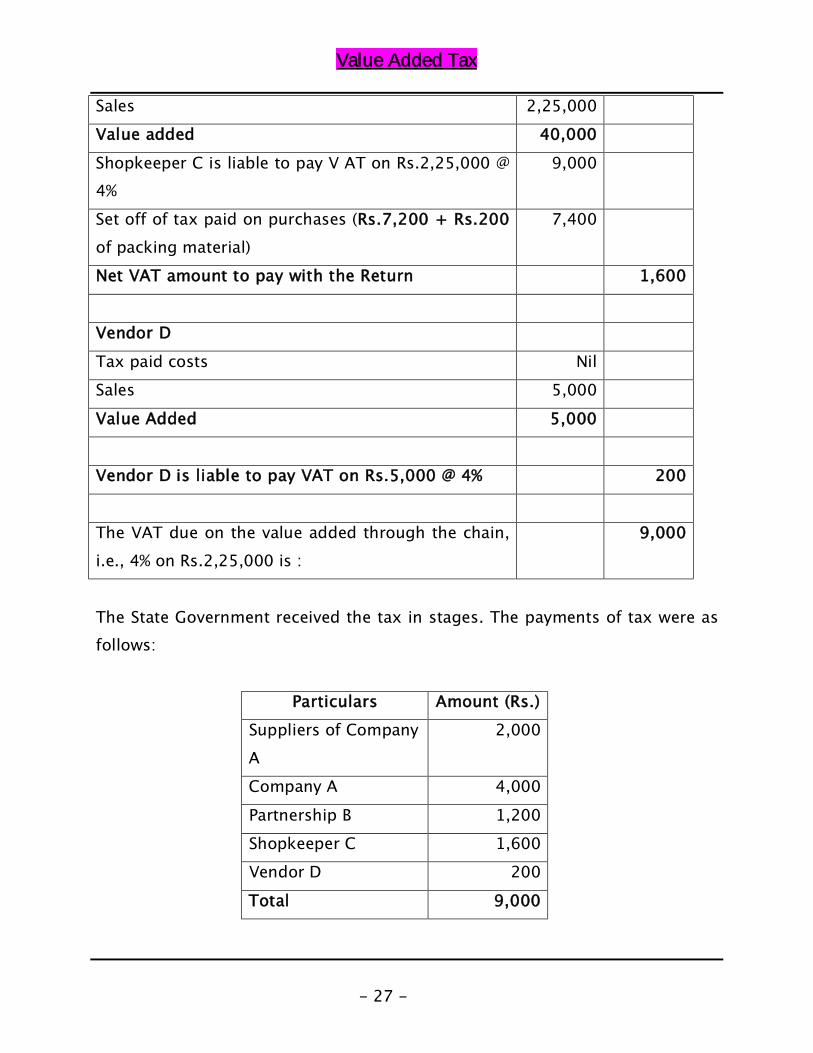

Shopkeeper C

Purchases polished stainless steel utensils 1,80,000

Packing material 5,000

Total Purchases 1,85,000

Value Added Tax

- 27 -

Sales 2,25,000

Value added 40,000

Shopkeeper C is liable to pay V AT on Rs.2,25,000 @4%

9,000

Set off of tax paid on purchases (Rs.7,200 + Rs.200

of packing material)

7,400

Net VAT amount to pay with the Return 1,600

Vendor D

Tax paid costs Nil

Sales 5,000

Value Added 5,000

Vendor D is liable to pay VAT on Rs.5,000 @ 4% 200

The VAT due on the value added through the chain,

i.e., 4% on Rs.2,25,000 is :

9,000

The State Government received the tax in stages. The payments of tax were asfollows:

Particulars Amount (Rs.)

Suppliers of Company

A

2,000

Company A 4,000

Partnership B 1,200

Shopkeeper C 1,600

Vendor D 200

Total 9,000

Value Added Tax

- 28 -

Thus, through a chain of tax on sale price and set off on purchase price, thecascading impact of tax is totally eliminated.

Value Added Tax

- 29 -

Since set-off of tax on purchases is given only on purchases from registereddealers where tax is collected separately, dealer’s purchases from unregistereddealers, imports, inter-state purchases and purchases from registered dealers

without separate tax collection are not entitled to set-off.

In practice, the tax is finally borne by the ultimate consumer, who is not a

registered dealer, in this case, people who buy utensils from the shopkeeper C.

Rates of value added tax

There are two main rates of VAT 4% and 12.5%. The goods are grouped into five

schedules as under:

Schedule Rate oftax

Illustrative Items

A 0% Vegetables, milk, eggs, bread

B 1% Precious metals and precious stones and their jewellery

C 4% Raw materials, notified industrial inputs, notified

information technology products and a few essentialitems

D 20% and

above

Liquor, petrol, diesel etc

E 12.5% Other than items specified in schedules A, B, C & D.

(The list is illustrative and not exhaustive. Please refer to the schedules for

details)

Value Added Tax

- 30 -

Difference between tax free goods and exempt sales

It is sometimes confusing to have goods that are tax free and sales that are

exempt. Both result in no VAT being charged, so what is the difference?

Tax free goods do not attract tax at any stage of sale or in any type of

transaction, whereas, exempted sales are certain types of transactions, viz.,export sales which are exempt from tax.

Composition schemes

Certain dealers may find it difficult to keep detailed records for claiming set-off.For such dealers, a simpler and optional method of accounting for VAT hasbeen introduced. This method is the composition scheme. It may be noted that

composition scheme is not meant to be a tax concession scheme but only asimplification of tax calculation and payment system.

Tax payable by dealers opting for composition in lieu of VAT

The following classes of dealers are eligible for option to pay tax undercomposition:

Resellers selling at retail, i.e., to consumers,

Restaurants, eating houses, hotel (excluding hotels having gradation of'Four Star’ and above), refreshment rooms, boarding establishments,

clubs and caterers,

Bakers,

Dealers in second-hand passenger motor vehicles and

Works contractors

Dealers engaged in the business of providing mandap, pandal, shamiana.

Value Added Tax

- 31 -

Accordingly, if the dealer has opted for payment of tax liability undercomposition, the tax liability has to be determined in terms of the guidelinesgiven in the relevant Notification in this regard. Apart from the terms and

conditions governing each of the composition schemes, the Notificationexplains the methodology for computation of turnover liable to tax and the rateof composition payable.

A dealer can opt for the composition option at the beginning of the financial

year and has to continue to be a composition dealer at least till the end of thatfinancial year. If dealer wishes to switch, over to normal VAT, he can do so onlyat the beginning of the next financial year. However, a new dealer can opt for

composition at the time of registration.

In respect of works contract, the contractor can choose to discharge tax liability

under composition option. Moreover, such an option can be exercised by thecontractor on contract to contract basis.

Value Added Tax

- 32 -

Part 4 - Calculating tax liability

In, order to calculate how much tax a dealer has to pay, he must, first

determine his turnover of sales and turnover of purchases. The second stage isto ascertain the amount of tax due for payment.

Calculating turnover of sales and purchases

The turnover of sales is the total of the amounts received or receivable(excluding VAT charged separately) in respect, of the sale of goods, less theamount refunded to a purchaser in respect of goods returned, within six

months of the date of the sale.

Similarly, the turnover of purchases is the total of the amounts paid or payable(excluding VAT charged separately) in respect of the purchase of goods less(the amounts repaid to dealer in respect of goods they return, within six

months of the date of purchase.

Credit notes and debit notes.

If the sale price, or the purchase price, of any goods is varied and either a credit

note or a debit note is issued, then the credit note or the debit note, as the casemay be, should

show separately, the tax and the price.

be accounted for in the period in which the appropriate entries are made intheir books of accounts.

Value Added Tax

- 33 -

Special cases

Auctioneers

If dealer is an auctioneer, then they must include in their turnover, the price ofthe goods they auction for their principalHotels

There are special rules for hotels and other establishments that provideboarding and lodging for an inclusive amount.

The rules provide a formula to enable them to calculate their turnover of salesfor meals (food and beverages) which they provide.The supply of food in a restaurant also includes an element of service. But the

full amount charged is the sale price for the purposes of calculating turnoverand tax.Works contracts

VAT applies only to the sale of goods. Supply of services is not liable to VAT.Works contracts are deemed sales where both, goods and services are provided

in a transaction and cannot be separated.A works contract may involve the creation of immoveable property, e.g. a house,a factory or a bridge. Some other examples of works contracts are photography,

repairs & maintenance etc.To calculate the amount a dealer should include it in their turnover of sales, sothat they may deduct it from the total contract price, the

costs of labour and service charges.

amount paid to sub-contractors.

charges for planning and designing, and any architect's fees.

hiring charges for machinery and tools.

cost of consumables, such as, water, gas and electricity.

Dealer’s administrative costs relating to labour and services and anyother similar expenses.

any profit element that relates to the supply of labour and services.

Value Added Tax

- 34 -

Alternatively, in lieu of the deductions as above, a dealer may choose todischarge the liability arising on works contracts by referring to the table

prescribed in the rules.If the dealer finds that it is too complicated to calculate the deductions, thenthey may opt for a composition scheme for any works contract.

Sales and purchases not liable to tax under VAT

The VAT law specifically excludes from value added tax all imports, exports andinter-state transactions. These transactions are covered by the CST Act.

Similarly, transactions that take place outside Maharashtra are not within thescope of MVAT Act.

Point of levy in certain casesHire purchase

Where there is a hire purchase agreement or an agreement for sale byinstallments, the date of the sale is deemed to be the date of the delivery ofgoods. This is despite the fact that legal ownership of the goods only passes to

the buyer after payment of the final installment.If the hire-purchase agreement specifies the interest component then incalculating the sales price, dealer should disregard the interest component

included in the agreement.Calculating the amount of VAT due on sales

Dealer should also make some adjustments to the total turnover of sales toarrive at the amount on which tax is due.From the total sales one should deduct

the total of exports and inter-State sales.

the total of sales of goods that are tax free, and

branch / consignment transfers to locations in Maharashtra as well as

other States.

Value Added Tax

- 35 -

the tax collected.

To calculate the tax due, dealer should start allocating their turnover of sales inthe return period (net of the above deductions) to the rates of tax they have

been charged. They should also ensure that the correct tax rates are applied.The information should be readily available from their records. This gives thetotal of sales tax due.

Calculating the turnover of purchasesRecords will provide the total figure, but they may not have paid VAT on all

their purchases. They must now deduct the total value of

imports from out of India.

inter-State purchases.

purchases of tax free goods.

direct purchases from exempted units under the Package Scheme of

Incentives.

consignment transfers, and

local purchased from unregistered dealers.

local purchases from registered dealers not supported by tax invoice.The resulting figure represents purchases against tax invoices from registered

dealers.Calculating the amount of set off due (VAT paid on purchases)This is the next stage of tax calculation. At this stage VAT is charged on total

purchases. Dealer must, however, make some adjustments to this amount for,in certain cases, the full set off of the VAT paid on purchases is not available.

Adjustments to tax available for set off

If dealer’s purchases include goods, used

o as fuel, oro for the manufacture of any tax-free goods, or

o as packaging for tax-free goods, this goods should be sold.

Value Added Tax

- 36 -

Then a dealer must calculate the value of those items and deduct tax @ 4% ofthe corresponding purchase price from the amount otherwise available for setoff. (Not applicable to PSI dealers other than the New Package Scheme of

Incentives for Tourism Projects, 1999 and also to manufacturers of tax-freesugar or fabrics covered by Entry A 45 and where such goods are sold in thecourse of export falling under section 5 of the CST Act, 1956).

Similarly, if the goods are stock transferred by way of branch / consignment

transfer to a place outside the State, deduct tax @ 4% (1 % in respect of goodscovered by Schedule B) of the corresponding purchase price from the amountotherwise available for set off.

Dealer must also make further adjustments as follows: -

If they have been used any goods (other than capital assets) as part of a

works contract for which they have been opted for payment composition@ 8% on the total contract value, they must also deduct 36% of the

amount from the set off otherwise available (4% of purchase price inrespect of construction contracts for which they have been opted forpayment of composition @ 5% on total contract value).

Where a dealer’s sales are less than 50 % of their gross receipts, then theycan claim set off only on those purchases of goods or packing materials

effected in that year where the corresponding goods are sold within sixmonths of the date of purchase or consigned within the said period toanother State by way of stock transfers.

In respect of office equipment, furniture or fixtures which have been

treated as capital assets, a dealer should reduce set-off otherwiseentitled by an amount equal to 4% of the purchase price.

If a dealer is the retailer of liquor vendor and its actual sale prices are lessthan the Maximum Retail Price, there is a special formula for calculating

the amount of the adjustment. Effectively this means that, if a dealer sells

Value Added Tax

- 37 -

at 75% of the MRP then they can claim set off only to the extent of 75% ofthe tax paid.

A dealer can not claim any set off for the tax paid on any purchases that

remain unsold on the date when business discontinues.

All this information should be available from their records, including tax

invoices and bills or cash memorandum they have issued, and the tax invoicesthey have received.

Value Added Tax

- 38 -

Set off not available

There are various items on which set-off is not available such as, goods of

incorporeal or intangible character other than those specified, passenger motorvehicles, motor spirits, crude oil, building material used for construction etc.

Conditions for claiming set off

A dealer can claim set off only for VAT paid on purchase if they have a valid taxinvoice for that transaction and they had maintain account of purchasesshowing the specified details.

Tax payable

The amount of set-off admissible can be adjusted against tax payable. Theamount of net tax payable is the total of sales tax collected on sales less the

set-off available.

Refund cases

If the amount of set-off admissible during the period is more than the amountof tax payable, then dealer’s return would reflect a balance refundable to the

dealer. The amount of set-off can be more than the tax payable for a variety ofreasons, such as

¬

Inputs are taxable at higher rate as compared with the rate of tax onoutput.

Outputs are tax-free goods while inputs carry tax.

Outputs are export sales.

Outputs are CST sales which are taxable at the concessional rate of CST.

Value Added Tax

- 39 -

Manufactured goods or trading goods are transferred to branches outside

the State or are sent on consignment transfers.

Apart from part of the admissible set-off which can remain unutilized, excesscredit can be on account of:

unutilised portion of tax deducted at source or

refund payment order or

ad-hoc payment made is more than tax payable.

Whatever may be the reason for credit in excess of tax due and payable during

a tax period, dealers are eligible to claim refund of such excess credit. For thepurpose of granting refund, dealers have been classified under two categoriesviz. a) specified class of dealers and b) other dealers

Refund to specified class of dealers

Specified classes of dealers are ¬: -

Exporters exporting out of the country or dealers selling to an exporter

against form H.

A unit set-up in SEZ or STP or EHTP or a 100% EOU unit. These units haveto be certified by the Commissioner of Sales Tax.

An Entitlement Certificate holder availing of the benefit of incentivesunder the Package Scheme of Incentives (PSI).

Specified class of dealers and the dealers who have made a sale in the course ofinter-State trade or commerce and in the return he has shown any amount to

be refundable are eligible to claim refund in each of the returns filed by them.Full amount of excess credit can be claimed as refund due for the return period.

Value Added Tax

- 40 -

The dealer eligible to claim refund has to file refund application in Form 501.The application has to be filed with the Refund Branch. The Refund Branch mayask for Bank Guarantee and any relevant information for checking correctness

of refund claimed. Normally, refund would be granted within one month fromthe receipt of Bank Guarantee or within three months from the date of receiptof refund application in Form 501, or as the case may be, the date of receipt of

the additional information, whichever is later.

Refund to other dealers

Other dealers are not eligible to get refund in each of the return filed. They are

required to carry forward excess credit to the next return within the samefinancial year and claim refund of excess credit in the return for the periodending March.

The dealer claiming refund in March return has to make refund application in

Form 501. The application has to be filed with the Refund Section. Normally,refund would be granted within six months of the end of the year to which thereturn relates. However, refund would be granted within six months to the new

dealer’s at the end of the year succeeding the said year.

Audit of refund claims

The refund granted to dealer would be subject to audit by the Refund Audit

Section. The audit may be taken up before granting the refund or after therefund is granted. Normally, refunds made against Bank Guarantee would betaken up for audit after the refund has been granted. During the course of the

audit, the audit team will check dealer’s eligibility to claim refund and thecorrectness of the amount of refund claimed by them.

Interest on delayed refund

Value Added Tax

- 41 -

No interest is payable on the refund due to a dealer as per returns filed by adealer. However, if granting of refund is delayed beyond the above mentioned

periods, dealer is eligible for interest for delayed payment. Simple interest atthe rate of 6% per year would be payable for the period from the due date to thedate of refund.

Some tips for getting timely refund

Dealer’s claim of refund would be processed faster if: -

They had filed the return with the Returns branch as per the prescribedtime schedule.

The return filed by the dealer’s should be correct, complete and

self-consistent.

They should have claimed refund as per the appropriate periodicity.

The amount of refund due to them should be computed correctly.

Refund application in Form 501 is filed with the Refunds branch in time.

They should have promptly furnished Bank Guarantee and other detailswhen called for.

They should keep ready all the documents and records for audit.

They should file the return for a period for which they are required to file.

Thus, if they are required to file a quarterly return, but they file a monthlyreturn, then the refund would not be granted for the monthly return. In order to

be eligible for refund, they would have to file a quarterly return.

Value Added Tax

- 42 -

Part 5 - Filing a return and paying the tax

VAT is a self-assessment system and dealer’s are expected to make self ¬assessment for a given tax period and declare their VAT liability by filing

returns. The returns have to be filed in the prescribed form and by the specifieddates. Further, they are also required to pay the tax due as per the return filed.

In Maharashtra, return form is return-cum-chalan. As such, filing of returnsalong-with payment of tax on or before the due date at the notified bank would

be considered as sufficient compliance. However, where any amount of taxincluding interest or penalty is due as per a fresh or revised return, then theyshould first pay such amount in Government Treasury and file the return in the

local office of Sales Tax Department along with a self attested copy of thechalan. If no payment is due or a refund is claimed as per the return, they arealso required to file the return in the local office of the Sales Tax Department.

Return forms

The return forms prescribed are as follows.

Form

No.

To Be Used By

221 All VAT dealers other than dealers executing works contract,

dealers engaged in leasing business, composition dealers(including dealers opting for composition only for part of theactivity of the business), PSI dealers and notified Oil

Companies.

222 All composition dealers whose entire turnover is under

composition(excluding works contractors opting for composition anddealers opting for composition only for part of the activity of

Value Added Tax

- 43 -

the business).

223 VA T dealers who are also in the business of executing workscontracts, leasing and dealers opting for composition only for

part of the activity of the business.

224 PSI dealers holding Entitlement Certificate (Transactions by PSI

dealers relating to the business of execution of workscontracts, leasing, frading and composition only for part of theactivity of the business to be included in a separate return in

Form 223).

225 Notified Oil Companies (Transactions by OIL Companies

relating to the business of execution of works contracts,leasing and composition only for part of the activity of thebusiness to be included in a separate return in Form 223).

A dealer can refer to the instructions given in the form before filling the return.

Please ensure that the return for a tax period covers all the transactions of sales,purchases, branch transfers received, branch transfers made etc. Further, they

must ensure that all the columns of the return are duly filled in and are clearlylegible. If a particular column is not relevant, please do not leave it blank butmention" not applicable". The return filed by them must be correct, complete

and self-consistent.

Time schedule for filing returns

Periodicity of filing returns is as follows: -¬

Retailers who have opted for composition should file six-monthly returns.

Newly registered dealers should file quarterly returns until the end of the

year in which they first register.

All package scheme dealers should file quarterly returns.

Value Added Tax

- 44 -

All other dealers should file returns as given below :-¬

o Dealers whose tax liability in the previous year was less thanRs.1,OO,OOOj- (Rs.1lakh) or whose entitlement for refund was less

than Rs.10,OO,OOOj- (Rs.10lakh) should file six-monthly returns.o Dealers whose tax liability in the previous year was more. thanRs.10,00,000- (Rs.10lakh) or whose entitlement for refund was

more than Rs.l,00,00,000- (Rs1crore) should file monthly returns.o All other dealers should file quarterly returns.

Filing and payment dates for return-cum-chalan are as follows:

ReturnFrequency

Filing / Payment date

Monthly 21 days from the end of the return period

Quarterly 21 days from the end of the return period

Six Monthly 21 days from the end of the return period

Scrutiny of returns filed

The return filed by the dealer should be correct, complete, and self-consistent

in every respect. The Sales Tax Office will check the return to ensure that thereare no obvious errors in consistencies or contradictions in calculations. If thischeck reveals discrepancies, then the dealer’s will be advised and invited to

submit a fresh return. The department will issue this defect notice within fourmonths of receiving their return. Then they should file their fresh return within30 days of the notice. If they fail to do so, it will be deemed not to have filed

the return within the time allowed, and will so liable to a penalty charge.

At the same time, as the department issues the defect notice, dealers will besent a 'show cause' notice, explaining that a penalty may be imposed.

Value Added Tax

- 45 -

Value Added Tax

- 46 -

Offences relating to filing of returns and payment of tax

The following are the offences liable for interest / penalty / prosecution etc.

Short- payment / non- payment of tax due

Failure to file returns

Delay in filing returns

Knowingly furnishing false returns

Filing of incorrect or incomplete or inconsistent returns

Consequences for filing a return, which is not correct, complete and

self-consistent

Each of the returns filed by them is checked to confirm that the same is correct,

complete and self-consistent. In case the return is defective, a defect notice isissued by the Returns Branch pointing out the error or the omission. On receiptof the notice, it is required to file fresh return which is correct, complete and

self-¬consistent and should also pay differential tax due, if any.

The return filed by them in response to defect notice is termed as Fresh Returnand the dealer should indicate so on the return in the space provided for thesame.

Fresh return rectifying the defects has to be filed within the time limit specifiedin the defect notice. Failure to comply with the notice would be construed as

non-filing of return and consequently, a unilateral (ex-parte) assessmentorder would be passed.

Value Added Tax

- 47 -

Failure to file a return

If dealer’s fails to file a return within the time allowed, then they are committing

an offence and, in addition to any tax and interest that may be due, which isliable to a penalty.

As no return has been filed by them, a unilateral assessment without givingthem a notice will be made. This unilateral assessment order is non-appealable.

However, they can get this assessment order cancelled only by filing the returnand paying the tax and interest due as per the return. For this purpose theyshould file application in Form 304 and submit to Returns Branch.

Paying the tax due

All the dealer’s or the person must file their return and should pay the tax due,in a bank that is authorized to accept the return. If they are required to file a

revised return, and the tax due exceeds the amount which they had paid whensubmitted earlier form, then they should pay the balance amount which is duenow.

The bank will give them an acknowledgement of the receipt of their return andpayment. If there is any doubt that where to file the return and pay the tax due,

then can ask to their local sales tax office.

Revised return

Subsequent to filing the return, in case dealer notices any error or omission,

then they can file a revised return before expiry of eight months from the endof the financial year to which the return relates or before a notice forassessment is served, whichever is earlier. Such return should be accompanied

by payment of tax and interest, if any. In case the return filed by them is a

Value Added Tax

- 48 -

revised return, then they should indicate it on the return form in the spaceprovided for the same.

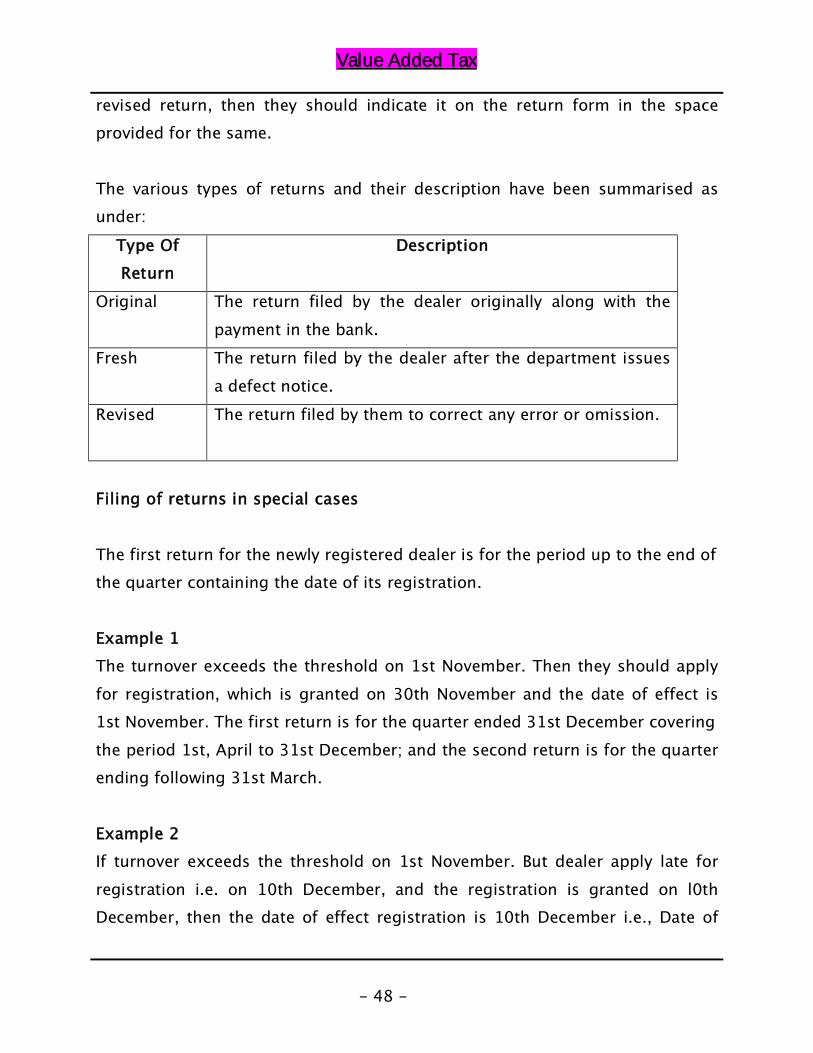

The various types of returns and their description have been summarised asunder:

Type OfReturn

Description

Original The return filed by the dealer originally along with the

payment in the bank.

Fresh The return filed by the dealer after the department issues

a defect notice.

Revised The return filed by them to correct any error or omission.

Filing of returns in special cases

The first return for the newly registered dealer is for the period up to the end ofthe quarter containing the date of its registration.

Example 1The turnover exceeds the threshold on 1st November. Then they should apply

for registration, which is granted on 30th November and the date of effect is1st November. The first return is for the quarter ended 31st December covering

the period 1st, April to 31st December; and the second return is for the quarterending following 31st March.

Example 2If turnover exceeds the threshold on 1st November. But dealer apply late for

registration i.e. on 10th December, and the registration is granted on l0thDecember, then the date of effect registration is 10th December i.e., Date of

Value Added Tax

- 49 -

application. The first return is due for the quarter ending on 31st December(covering. the period 10th December to 31st December). .

Value Added Tax

- 50 -

Filing of return in case of cancellation of registration

Dealer’s registration may be cancelled if they discontinue, transfer or sell the

business. They may also choose to cancel their registration if their turnoverfalls below the threshold limit¬.

ExampleIf dealer’s file the returns quarterly and their, last return was for the quarter

ending 30th September. If a dealer closes the business on 15th November, thentheir final return will be for, the period 1st October to 15th November. Thereturn should be filed within one month, that is, before 15th December.

Dealer under the Package Scheme of Incentives

If dealer’s hold a Certificate of Entitlement granting an exemption frompayment of tax or deferment of payment of tax, it should be for the unit which

is eligible for the incentives, file a quarterly return, in Form 224. They mustcontinue to file quarterly return till the Certificate of Entitlement remains valid.

When the validity of the Certificate of Entitlement ends, then dealer must file:- ¬

a quarterly return, in form 224, for the period from the first day of the

quarter in which the event occurs to the date the Certificate ofEntitlement ceases, and

a quarterly return, in form 221 or 222 or 223 as the case may be, for

the remainder of that financial year. For succeeding years, the periodand frequency of the returns will be determined on the basis of the tax

liability or entitlement for refund of the preceding financial year.

Value Added Tax

- 51 -

Filing multiple returns

Dealers are required to file a single return at its principal place of business for

all its businesses or places of business. If they desire to file separate returns forseparate places / divisions, then they must apply for Form 211 for permissionto file multiple returns. Dealer should ensure that correct, complete and

self-consistent returns are filed at all the locations in the State.

Tax deduction at source by an employer in a works contract

The works contractor is obliged to pay the tax on the works contracts executed

by him. However, the employer i.e. the notified person who has engaged theworks contractor is obliged to deduct tax at the specified rate from the amountpayable to the works contractor, excluding the amount of tax, if any, separately

charged or service tax levied by the contractor.. The tax amount so deductedand paid to the Government treasury IS considered as a payment made on

behalf of the works contractor.

The employer is required to deposit this tax and issue a certificate of tax

deduction at source in the prescribed format based on which the workscontractor is allowed to take the credit of the same while discharging his taxliability.

Value Added Tax

- 52 -

Part 6 - Records and accounts

Keeping records

Proper records are an essential part of effective management and control oftheir business. Dealers are required by law to keep a true and accurate accountof the transactions effected by them. This will also help them to correctly

quantify their tax liability or refunds, as the case may be.

They should keep all their accounts, registers and documents relating to theirstocks of goods, purchases, sales and deliveries of goods, at their place ofbusiness. If they wish to keep them at a different location they may do so, but

only if they have the permission of the Commissioner of Sales Tax.

Nature of records

Normally, this department will not expect them to keep any special records for

VAT purposes. However, the records that they do keep should have sufficientdetails to enable them to correctly calculate the amount of VAT due forpayment and file their return.

If Sales Tax Office happens to find that their records are not properlymaintained, then they will issue a notice, informing dealers about what records

they must keep.

A dealer should maintain the following records¬: -

to identify the nature and value of goods purchased and sold;

distinguish between -

o local sales, interstate sales & exports.o local purchases, interstate purchase & imports.

Value Added Tax

- 53 -

indicate value of -

o sale and purchase of tax free goods.o sales exempted from tax.

o purchases from URD.o rate-wise purchases & sales.o local purchases from registered dealer with VAT shown separately.

record payments for the purchases and sale of goods in cash book / bankbook.

include a summary of VAT paid separately on purchases, VAT charged on

sales, VAT paid to the State treasury and VAT refundable / refunded tothe dealers.

contain adequate proof that goods have been exported or imported;

be supported by invoices for all goods purchased, and copies of invoices,

and bills or cash memoranda, issued for goods sold.

Tax invoices and memoranda of sales or purchases

As a registered dealer, they should issue a tax invoice when they sell goods to

another registered dealer and charge VAT. For sales made to consumers andunregistered dealers, they must issue a tax invoice, or a bill or cashmemorandum. However, if a dealer is a composition dealer other than a works

contractor, they must issue a bill or cash memorandum only and not a taxinvoice. Failure to issue a tax invoice or a bill or cash memorandum may resultin a penalty.

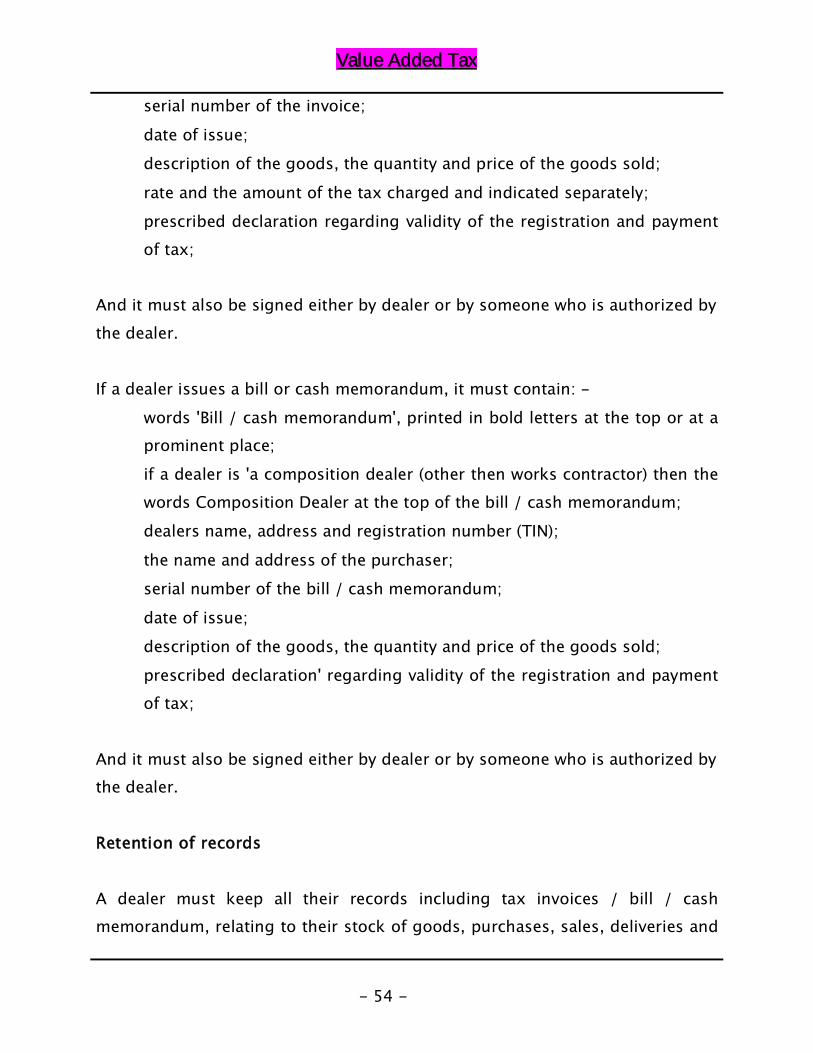

The tax invoice must contain: -

the words 'Tax invoice', printed in bold letters at the top or at a

prominent place;

dealers name, address and registration number (TIN).

the name, address and the registration number of the purchaser;

Value Added Tax

- 54 -

serial number of the invoice;

date of issue;

description of the goods, the quantity and price of the goods sold;

rate and the amount of the tax charged and indicated separately;

prescribed declaration regarding validity of the registration and payment

of tax;

And it must also be signed either by dealer or by someone who is authorized by

the dealer.

If a dealer issues a bill or cash memorandum, it must contain: -

words 'Bill / cash memorandum', printed in bold letters at the top or at aprominent place;

if a dealer is 'a composition dealer (other then works contractor) then the

words Composition Dealer at the top of the bill / cash memorandum;

dealers name, address and registration number (TIN);

the name and address of the purchaser;

serial number of the bill / cash memorandum;

date of issue;

description of the goods, the quantity and price of the goods sold;

prescribed declaration' regarding validity of the registration and payment

of tax;

And it must also be signed either by dealer or by someone who is authorized bythe dealer.

Retention of records

A dealer must keep all their records including tax invoices / bill / cashmemorandum, relating to their stock of goods, purchases, sales, deliveries and

Value Added Tax

- 55 -

payments made or received for the purchase or sale of goods for a minimum offive years from the end of the year to which they relate.

However, in case any legal proceedings are pending; the records pertaining tothat period should be retained till the proceedings reach finality.

Value Added Tax

- 56 -

Independent audit of accounts by a Chartered Accountant

If dealers’ annual turnover of sales exceeds Rs.40lakhs, or if they hold a license

for the manufacture or sale of liquor, then they must have their books ofaccounts audited by a practicing chartered accountant.

The Chartered Accountant's audit report, to be made on Form 704 and it mustbe submitted within 8 months from the end of the financial year. If they fail to

submit the audit report to the Sales Tax Department within the prescribed time,then they may be liable to a penalty.

Production and inspection of accounts and documents

If the concerned sales tax authorities have reason to believe that there may

have been attempts to evade the payment of tax, they may require dealer toproduce all their books of accounts.

If a dealer fails to comply with such a requirement, it may commit an offenceand will be liable to a penalty.

Value Added Tax

- 57 -

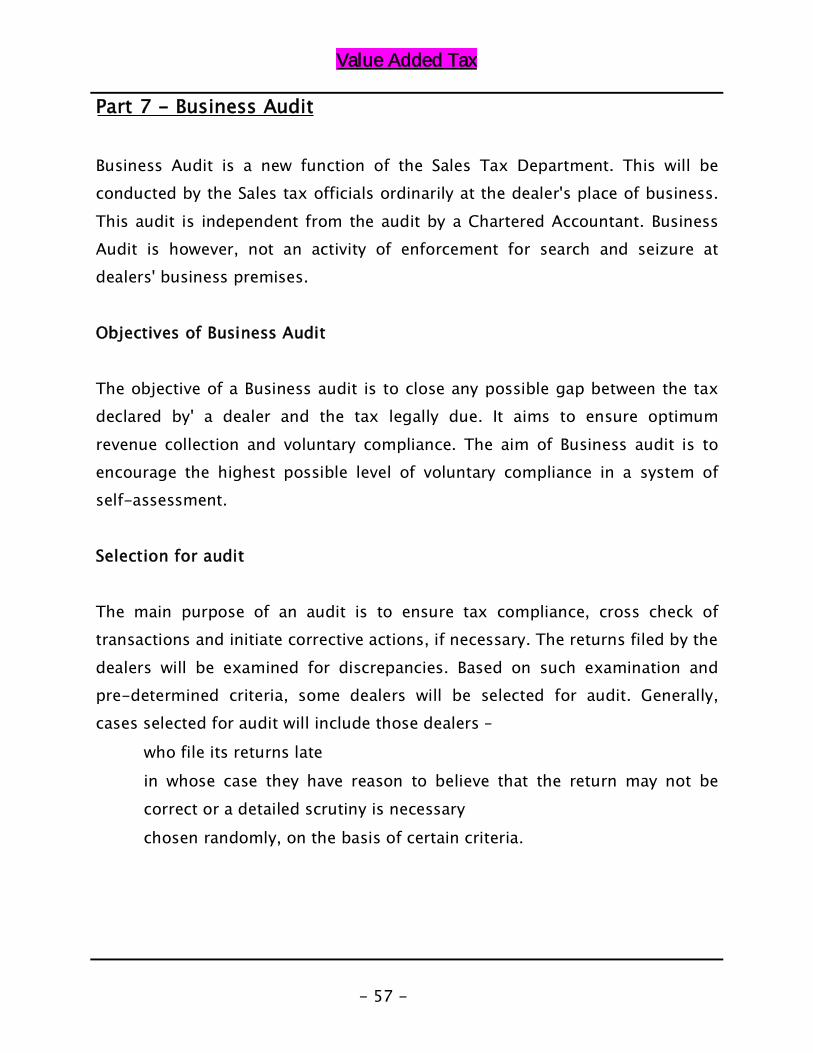

Part 7 - Business Audit

Business Audit is a new function of the Sales Tax Department. This will beconducted by the Sales tax officials ordinarily at the dealer's place of business.

This audit is independent from the audit by a Chartered Accountant. BusinessAudit is however, not an activity of enforcement for search and seizure atdealers' business premises.

Objectives of Business Audit

The objective of a Business audit is to close any possible gap between the taxdeclared by' a dealer and the tax legally due. It aims to ensure optimum

revenue collection and voluntary compliance. The aim of Business audit is toencourage the highest possible level of voluntary compliance in a system ofself-assessment.

Selection for audit

The main purpose of an audit is to ensure tax compliance, cross check oftransactions and initiate corrective actions, if necessary. The returns filed by the

dealers will be examined for discrepancies. Based on such examination andpre-determined criteria, some dealers will be selected for audit. Generally,cases selected for audit will include those dealers –

who file its returns late

in whose case they have reason to believe that the return may not be

correct or a detailed scrutiny is necessary

chosen randomly, on the basis of certain criteria.

Value Added Tax

- 58 -

A dealer who consistently and regularly complies with the VAT law and filescorrect, complete and self consistent returns will normally not be selected foraudit. The selection of audit cases will be by exception rather than as a rule.

The Business Audit Process

If any of the dealers business is selected for an audit, then Sales Tax Office will

inform them and then fix a suitable date.

The audit officer will inspect the books of accounts and supporting documents.

At that time dealer should make available any information or documents that hemay require to enable him to carry out the audit effectively and speedily.

The audit officer may like to understand dealer’s business process and examinetheir stocks of goods. He may also like to interview the person or its employees

for this.

The audit officer cannot remove any books of accounts or documents from their

premises. However, audit officer can request for copies.

Results of the audit

If the audit shows that the returns filed do not reflect the true picture of the

dealers business, then the auditor may discuss the matter with the dealer andwill give guidance to them to prevent recurrence and will also explain themabout what action should be followed. The audit may result in additional tax

demand or a refund.

Value Added Tax

- 59 -

Additional tax demand

If any additional tax is due, the auditor will issue a notice explaining the

additional demand. If the dealer accepts the additional demand shown, thenthey should file a revised return along-with the payment of tax.

However, if the dealer disagrees with the findings of the auditor, then they mayproceed to assess their case and issue an assessment order unless they are able

to provide evidence and convince the audit officer not to assess them foradditional demand. The assessment order will also include interest due fromthe date they should have paid the tax to the date of the assessment. In

addition, they may also impose a penalty. They should pay the dues as per theassessment order or they may prefer an appeal against this order.

Time limit for audit

There is no time limit prescribed for conducting Business Audit. Normally, theymay carry out an audit within two years of filing the return. They may follow thetimelines as prescribed for completion of assessments under the MVAT Act and

MVAT Rules.

Investigation

Normally, the Sales Tax Department will make Business Audit visits by

appointment. However, if the department suspects any tax evasion, it mayconduct investigation of the business including search and seizure operationsat any time without giving notice. Such investigation will be carried out by a

duly authorized investigation officer (not audit officer).

Value Added Tax

- 60 -

Part 8 - Appeals

A dealer may appeal against an assessment order if they do not agree with theamount assessed. They may also appeal against an order for the charging of

interest or the imposition of a penalty. They can also file an appeal against anyother order passed in their case. Appeals cannot be filed against certaininterlocutory proceedings or orders. Also, they can not appeal against an

unilateral assessment order passed as a consequence of non filing of returns.

There are two appeal bodies; the first is the departmental appeal officers andthe second is the Maharashtra Sales Tax Tribunal ('Tribunal').

Appeal bodies

Normally, dealer’s appeal will be, in the first instance, to the departmental

appellate authority. However, where the Commissioner, or a Joint or AdditionalCommissioner issues the order, its appeal is directly to the Tribunal. (The order

will show the designation of the officer.)

If the dealer is not satisfied with the decision of the departmental appellate

authority, then they may make a second appeal to the Tribunal.

The Tribunal

The Tribunal consists of equal number of judicial and technical members. The

latter are ordinarily, senior ex-officers of the Sales Tax Department.

Value Added Tax

- 61 -

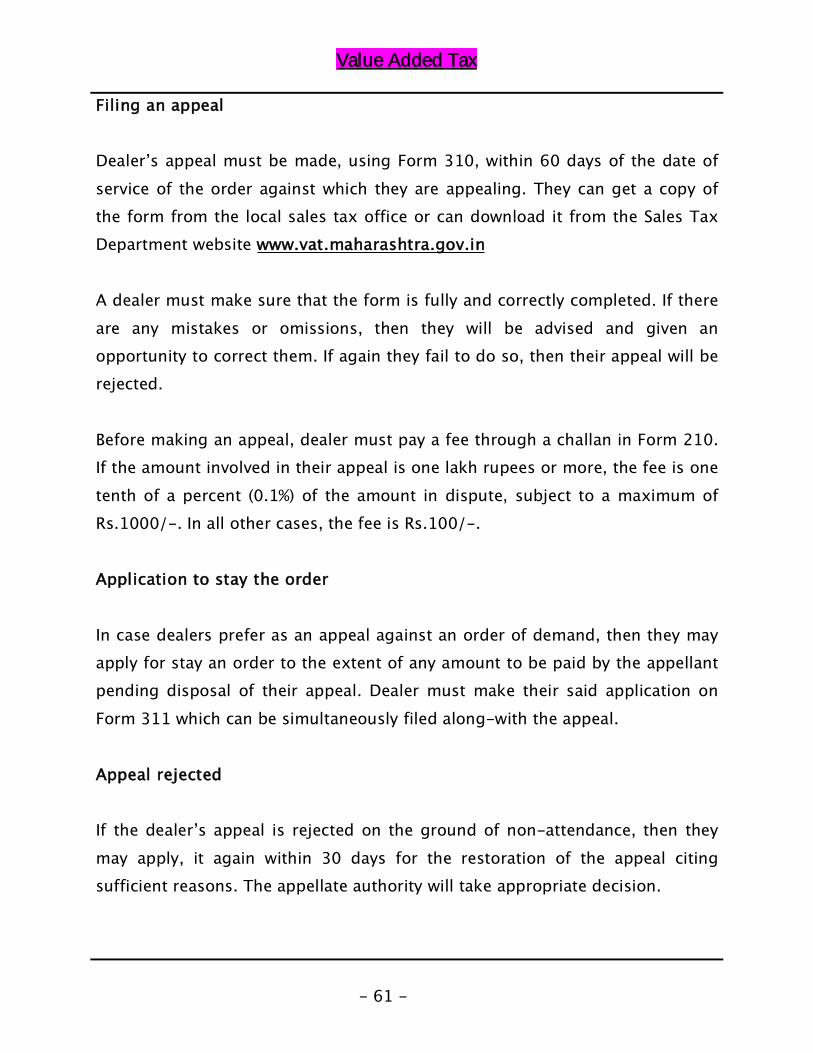

Filing an appeal

Dealer’s appeal must be made, using Form 310, within 60 days of the date of

service of the order against which they are appealing. They can get a copy ofthe form from the local sales tax office or can download it from the Sales TaxDepartment website www.vat.maharashtra.gov.in

A dealer must make sure that the form is fully and correctly completed. If there

are any mistakes or omissions, then they will be advised and given anopportunity to correct them. If again they fail to do so, then their appeal will berejected.

Before making an appeal, dealer must pay a fee through a challan in Form 210.If the amount involved in their appeal is one lakh rupees or more, the fee is one

tenth of a percent (0.1%) of the amount in dispute, subject to a maximum ofRs.1000/-. In all other cases, the fee is Rs.100/-.

Application to stay the order

In case dealers prefer as an appeal against an order of demand, then they mayapply for stay an order to the extent of any amount to be paid by the appellantpending disposal of their appeal. Dealer must make their said application on