Embed Size (px)

DESCRIPTION

Ackermans & van Haaren is a diversified group active in 5 key segments: Infrastructure & Marine Engineering (DEME, one of the largest dredging companies in the world - Algemene Aannemingen Van Laere, a leading contractor in Belgium), Private Banking (Delen Private Bank, one of the largest independent private asset managers in Belgium, and asset manager JM Finn in the UK - Bank J. Van Breda & C°, niche bank for entrepreneurs and liberal professions in Belgium), Real Estate, Leisure & Senior Care (Leasinvest Real Estate, a listed real-estate investment trust - Extensa, an important land and real estate developer focused on Belgium, Luxembourg and Central Europe), Energy & Resources (Sipef, an agro-industrial group in tropical agriculture) and Development Capital (Sofinim and GIB). In 2012, through its share in its participations, the AvH group represented a turnover of 3.3 billion euro and employed approximately 18.750 people. The group concentrates on a limited number of strategic participations with significant potential for growth. AvH is quoted on the BEL20 index, the Private Equity NXT index of Euronext Brussels and the European DJ Stoxx 600.

Citation preview

Ackermans & van Haaren

considers the family values of

the founding families to be

of paramount importance. Elements such as

continuity, ethical entrepreneurship, long-

term thinking, work ing with partners and

mutual respect have consequently driven

the group’s policies for many decades and

have created value through growth.

May 15, 2013 Interim statement Q1 2013

May 27, 2013 Ordinary general meeting

August 28, 2013 Half-year results 2013

November 15, 2013 Interim statement Q3 2013

February 28, 2014 Annual results 2013

May 26, 2014 Ordinary general meetingAn

nu

al

rep

ort

20

12

Financial calendar

Ackermans & van Haaren NV

Begijnenvest 113

2000 Antwerp - Belgium

Tel. +32 3 231 87 70

www.avh.be

Annual

report

2012

Ackermans & van Haaren

considers the family values of

the founding families to be

of paramount importance. Elements such as

continuity, ethical entrepreneurship, long-

term thinking, work ing with partners and

mutual respect have consequently driven

the group’s policies for many decades and

have created value through growth.

May 15, 2013 Interim statement Q1 2013

May 27, 2013 Ordinary general meeting

August 28, 2013 Half-year results 2013

November 15, 2013 Interim statement Q3 2013

February 28, 2014 Annual results 2013

May 26, 2014 Ordinary general meetingAn

nu

al

rep

ort

20

12

Financial calendar

Ackermans & van Haaren NV

Begijnenvest 113

2000 Antwerp - Belgium

Tel. +32 3 231 87 70

www.avh.be

Annual

report

2012

Annual report 2012

4

Pursuant to the Royal Decree of 14 November 2007 on the

obligations of issuers of financial instruments admitted to

trading on a Belgian regulated market, Ackermans & van

Haaren is required to publish its annual financial report.

This report contains the combined statutory and consolidat-

ed annual report of the board of directors prepared in accord-

ance with article 119, last paragraph of the Company Code.

The report further contains a condensed version of the

statutory annual accounts prepared in accordance with

article 105 of the Company Code, and the full version of

the consolidated annual accounts. The full version of the

statutory annual accounts has been deposited with the Na-

tional Bank of Belgium, pursuant to articles 98 and 100 of

the Company Code, together with the annual report of the

board of directors and the audit report.

The auditor has approved the statutory and consolidated

annual accounts without qualification. In accordance with

article 12, §2, 3° of the Royal Decree of 14 November 2007,

the members of the executive committee (i.e. Luc Bertrand,

Tom Bamelis, Piet Bevernage, Piet Dejonghe, Koen Janssen

and Jan Suykens) declare that, to their knowledge:

a) the annual accounts contained in this report, which

have been prepared in accordance with the applicable

standards for annual accounts, give a true view of the

assets, financial situation and the results of Ackermans

& van Haaren and the companies included in the con-

solidation;

b) the annual accounts give a true overview of the devel-

opment and the results of the company and of the po-

sition of Ackermans & van Haaren and the companies

included in the consolidation, as well as a description

of the main risks and uncertainties with which they are

confronted.

The annual report, the full versions of the statutory and

consolidated annual accounts, as well as the audit re-

ports regarding said annual accounts are available on

the website (www.avh.be) and may be obtained upon

simple request, without charge, at the following address:

Begijnenvest 113

2000 Antwerp, Belgium

Tel. +32 3 231 87 70

Fax +32 3 225 25 33

E-mail [email protected]

5

ContentsA n n u a l r e p o r t 2 0 1 2

Mission statement 7

2012 at a glance 8

Key events 2012 10

12 Annual report Message of the chairmen 15

Annual report on the statutory annual accounts 18

Annual report on the consolidated annual accounts 22

Corporate governance statement 30

Remuneration report 38

Corporate social responsibility 42

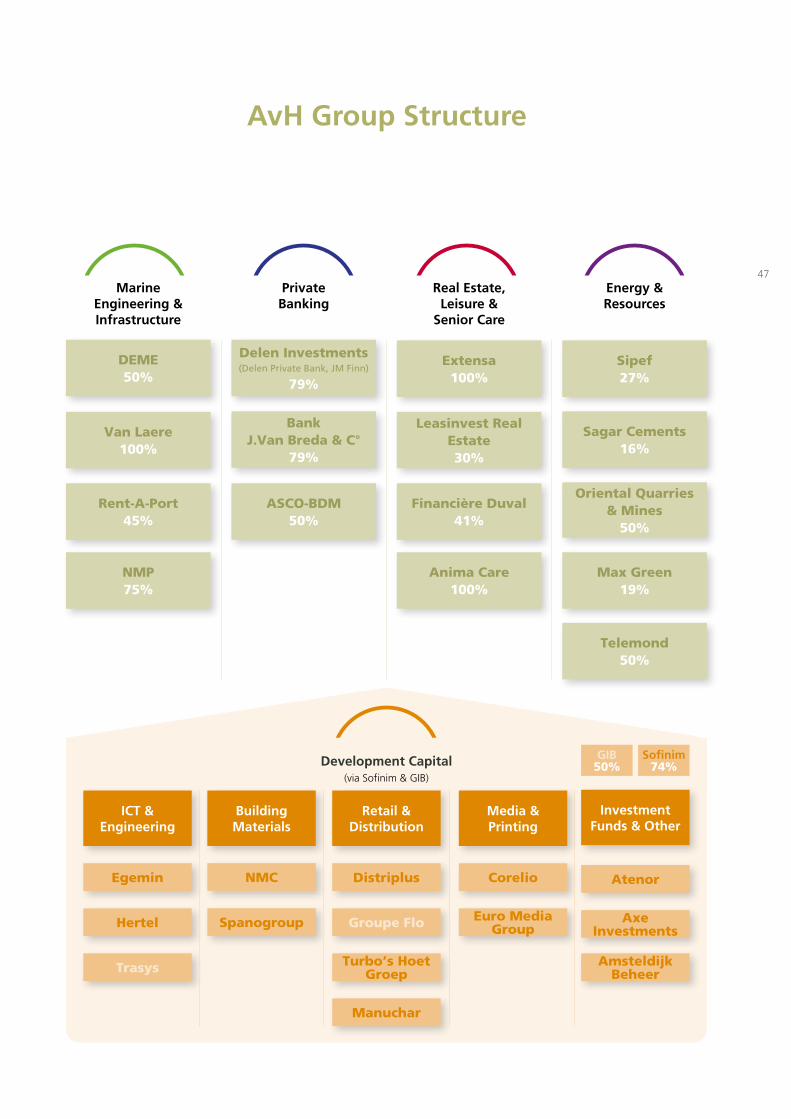

46 Activity report Group structure 47

48 Marine Engineering & Infrastructure

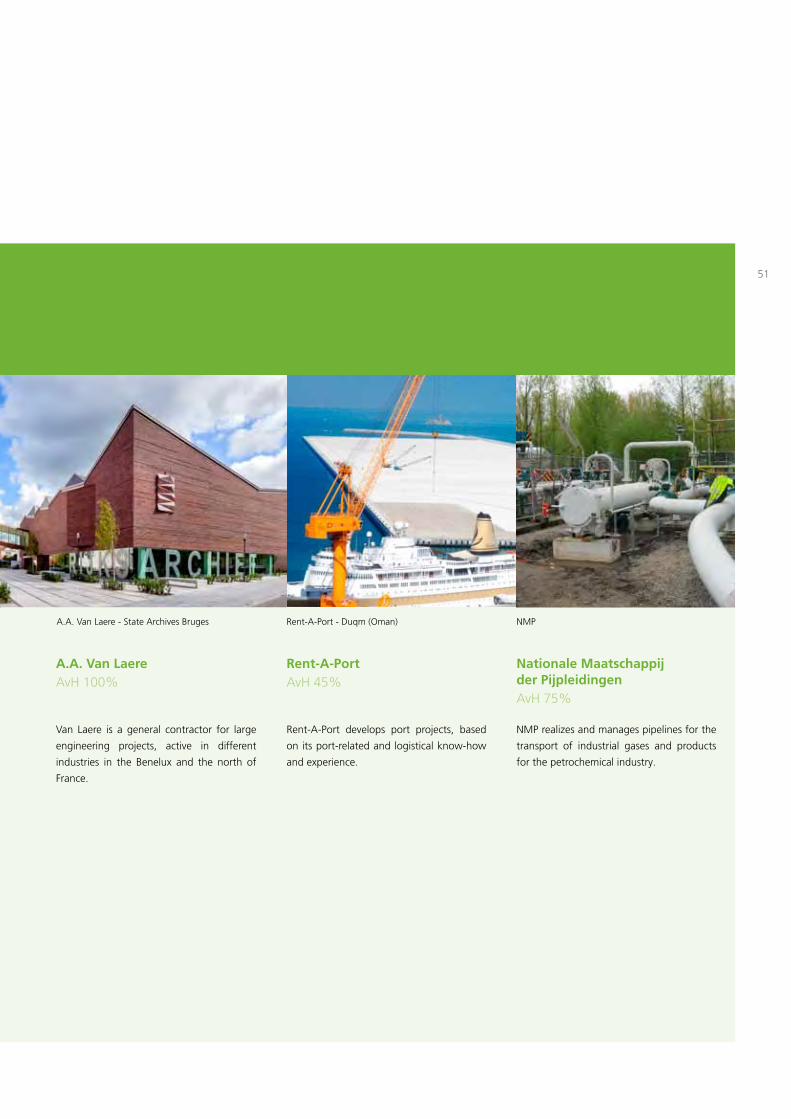

DEME 52

Algemene Aannemingen Van Laere 56

Rent-A-Port 58

NMP 59

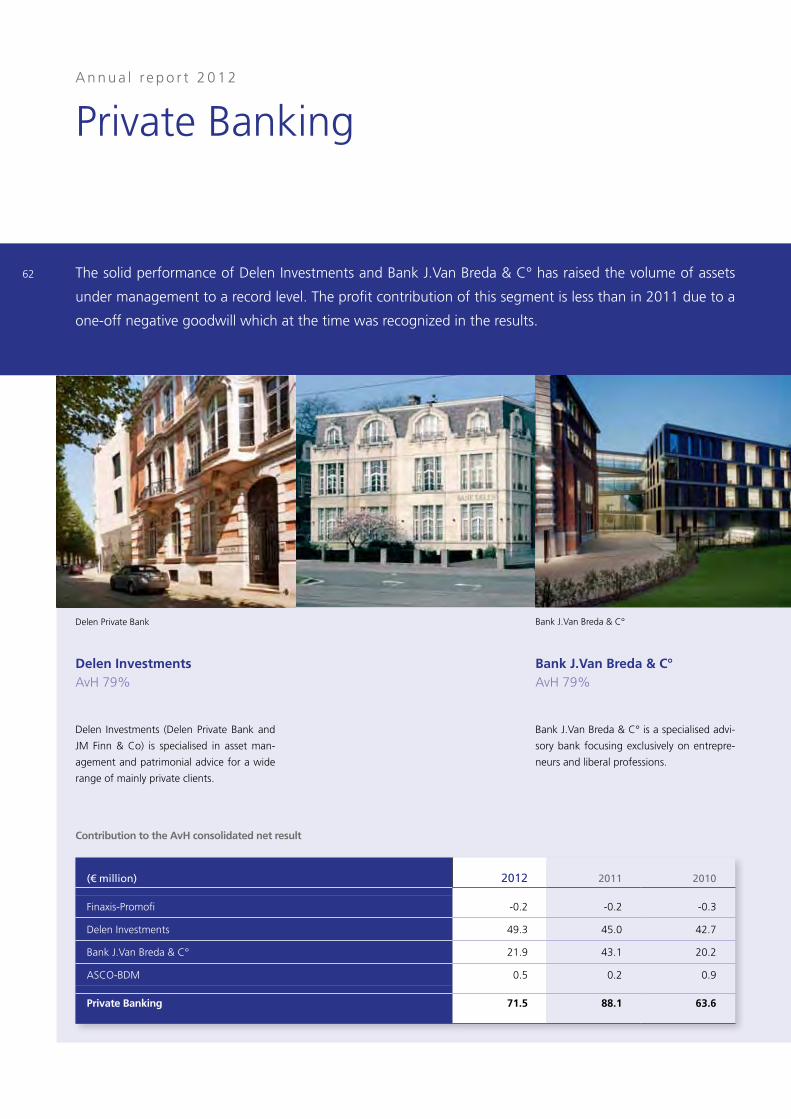

60 Private Banking Delen Investments 64

Bank J.Van Breda & C° 68

ASCO-BDM 71

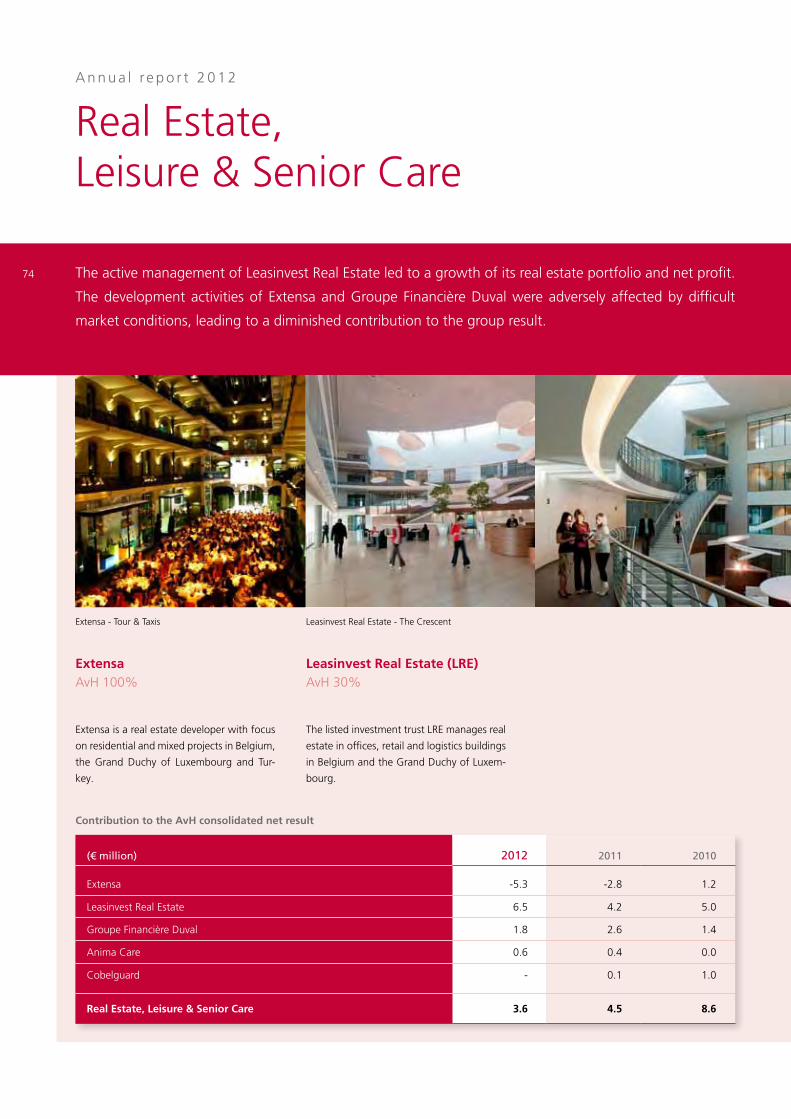

72 Real Estate,Leisure &Senior Care

Extensa 76

Leasinvest Real Estate 79

Financière Duval 82

Anima Care 84

86 Energy& Resources

Sipef 90

Sagar Cements 92

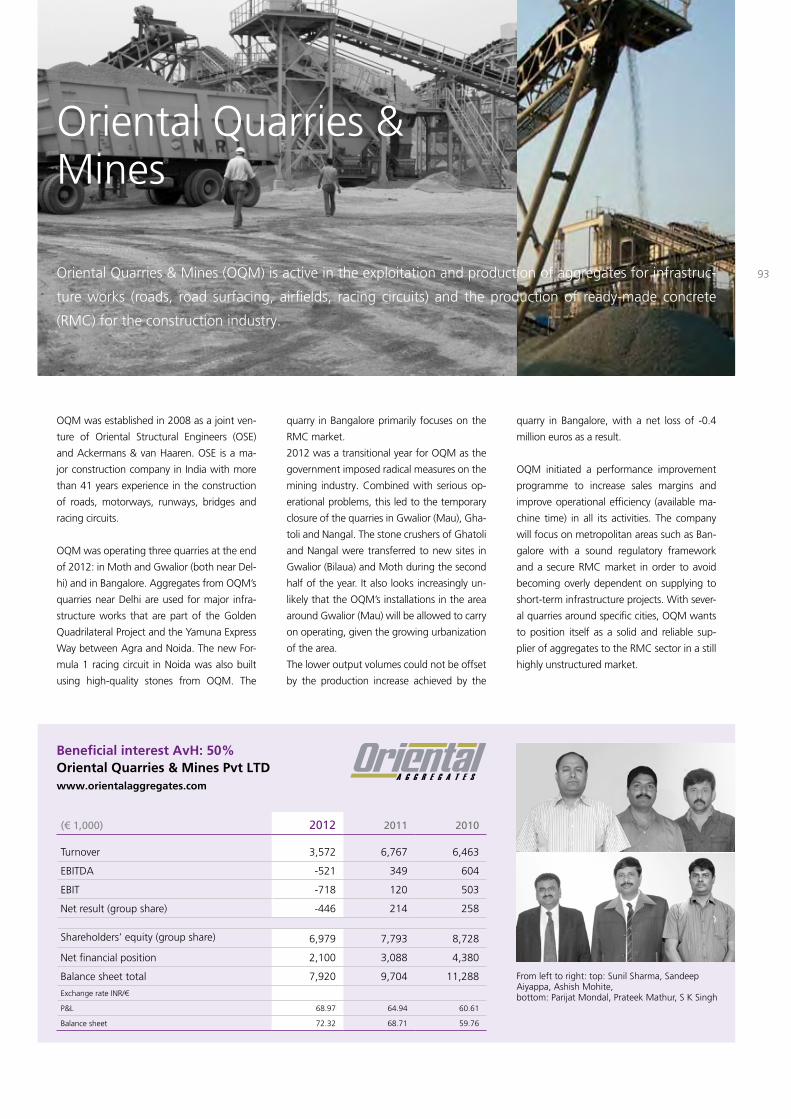

Oriental Quarries & Mines 93

Max Green 94

Telemond Group 95

96 Development Capital

114 Financial statements

General information regarding the company and the capital 174

Annual information 176

Appendix Key figures 2012

6

7

Positioning of Ackermans & van Haaren

• an independent and diversified group

• led by an experienced, multidisciplinary

management team

• based upon a healthy financial structure

to support the growth ambitions of the

participations

Mission statementA n n u a l r e p o r t 2 0 1 2

Our mission is to create shareholder value through long-term investments in a limited number of strategic participations with growth potential on an international level.

Long term perspective

• clear objectives agreed upon with the par-

ticipations

• responsibility of the participations for

their own financial position

• strive for annual growth in the profits of

each participation and in the group as a

whole

• focus on growth sectors in an interna-

tional context

Proactive shareholder

• involvement in selecting senior manage-

ment and defining long-term strategy

• permanent dialogue with management

• monitoring and control of strategic fo-

cus, operational and financial discipline

• active support to management for spe-

cific operational and strategic projects

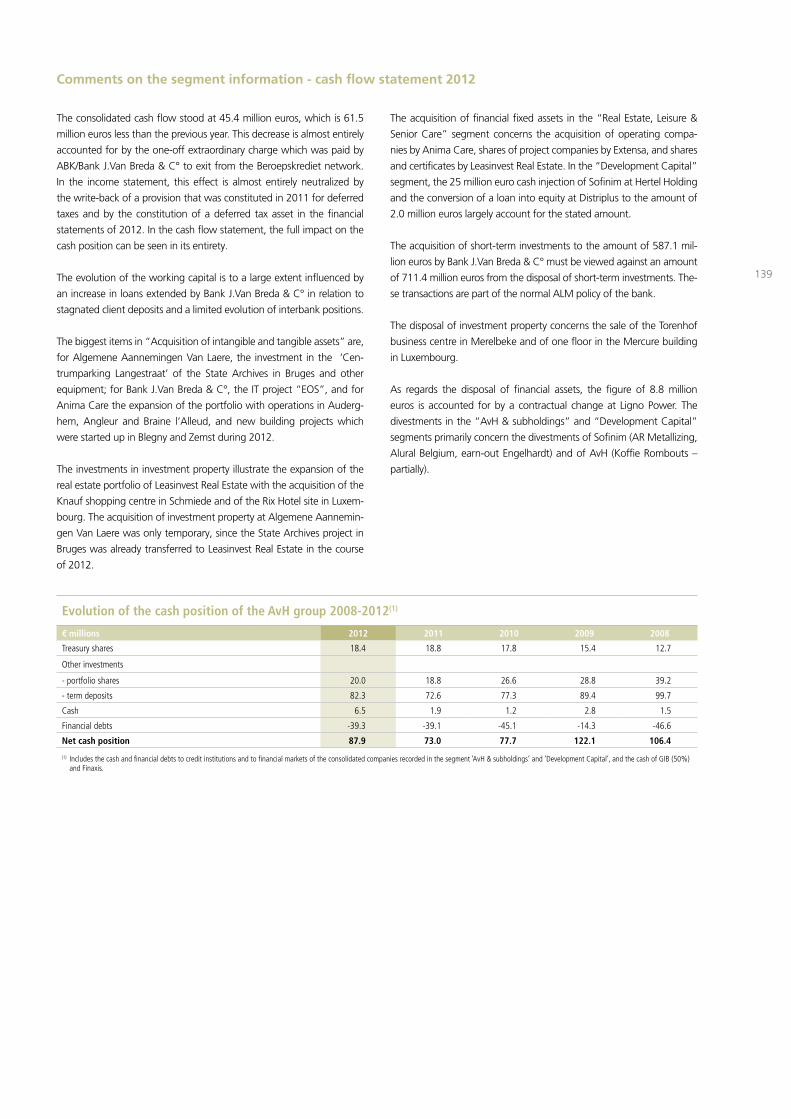

8 The consolidated net result (group share) of Ackermans & van Haaren NV amounts to 167.5 million euros

for the year 2012.

• Delen Investments recorded an out-

standing result, stimulated by assets un-

der management that grew to a record

level of 25.9 billion euros at the end

of 2012. Bank J.Van Breda & C° also

showed a strong performance with a 7%

growth in volume of client assets. Since its

result was positively influenced on a one-

off basis by negative goodwill in 2011,

the net profit contribution is less than in

that year. At the end of 2012, ABK made

use of the possibility offered by the new

legislation to exit from the Beroepskrediet

statute, with only a limited impact on its

equity position.

• DEME ended the transitional year 2012

with a net profit of 89.4 million euros.

The results of the second half of the year

showed a firm recovery. By winning some

major new contracts in Australia, Africa,

the Middle East and in offshore wind,

DEME’s order book closed at 3,317 million

euros. Within the Marine Engineering &

Infrastructure segment, Rent-A-Port con-

tributed positively thanks to the strong

performance of its Vietnamese opera-

tions.

• The active management of Leasinvest

Real Estate allowed its real estate port-

folio to grow to 618 million euros at the

end of 2012. Increased rental income and

the absence of negative value adjust-

ments on the portfolio are reflected in a

63% increase in net profit to 20.5 mil-

lion euros. The development activities of

Extensa and Groupe Financière Duval

were adversely affected by difficult mar-

ket conditions, leading to a diminished

contribution to the group result.

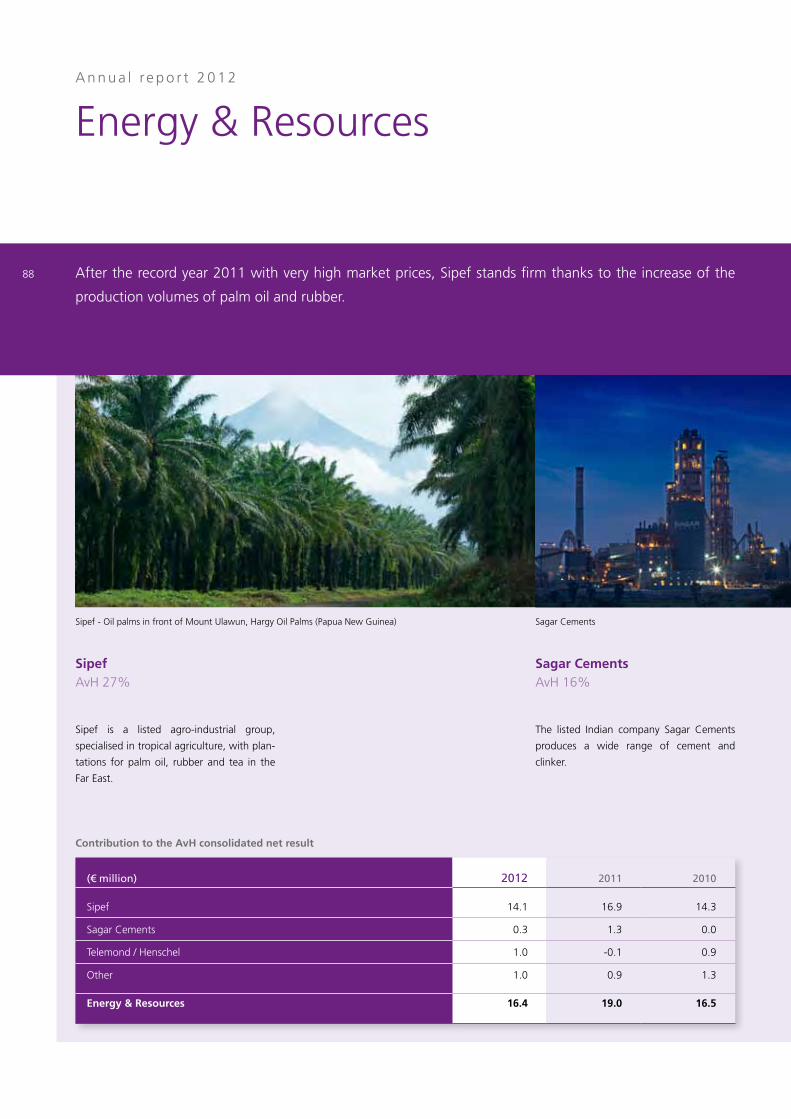

• After the record year 2011 with very high

market prices, Sipef stands firm thanks to

the increase of the production volumes of

palm oil and rubber.

• The contribution from the Development

Capital segment was encumbered in

2012 by the non-recurring results of Her-

tel. The sale in the second half of 2012 of

the participation in AR Metallizing con-

tributed to the 22.7 million euros capital

gains that were realized in this segment.

Breakdown of the consolidated net result (part of the group) - IFRS

(€ mio) 2012 2011 2010

Marine Engineering & Infrastructure 51.7 54.6 58.7

Private Banking 71.5 88.1 63.6

Real Estate, Leisure & Senior Care 3.6 4.5 8.6

Energy & Resources 16.4 19.0 16.5

Development Capital 6.1 8.6 13.3

Result of the participations 149.3 174.8 160.7

Capital gains Development Capital 22.7 -0.9 -0.3

Result of the participations (incl. capital gains) 172.0 173.9 160.4

AvH & subholdings -3.9 -0.9 -0.1

Other non-recurrent results -0.6 4.5 0.5

Consolidated net result 167.5 177.5 160.8

2012 at a glance

A n n u a l r e p o r t 2 0 1 2

The board of directors of Ackermans & van

Haaren proposes to the general meeting of

shareholders of 27 May to increase the divi-

dend to 1.67 euros per share.

9

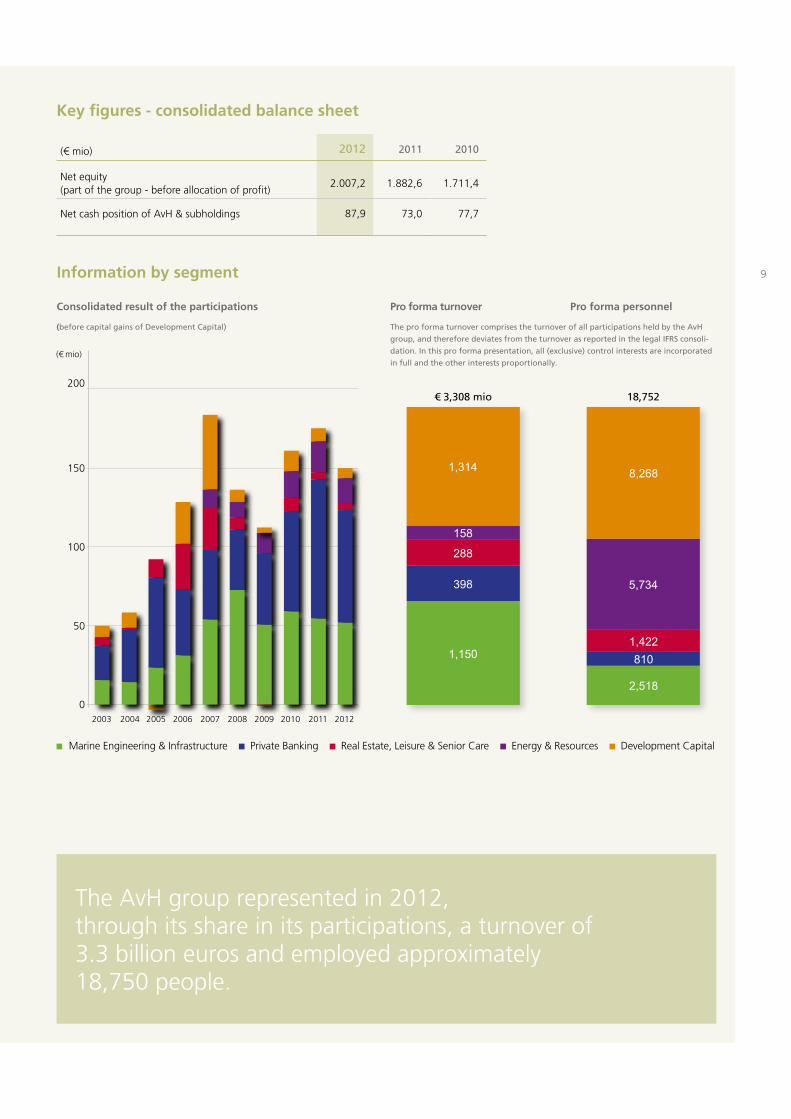

Key figures - consolidated balance sheet

(€ mio) 2012 2011 2010

Net equity (part of the group - before allocation of profit)

2.007,2 1.882,6 1.711,4

Net cash position of AvH & subholdings 87,9 73,0 77,7

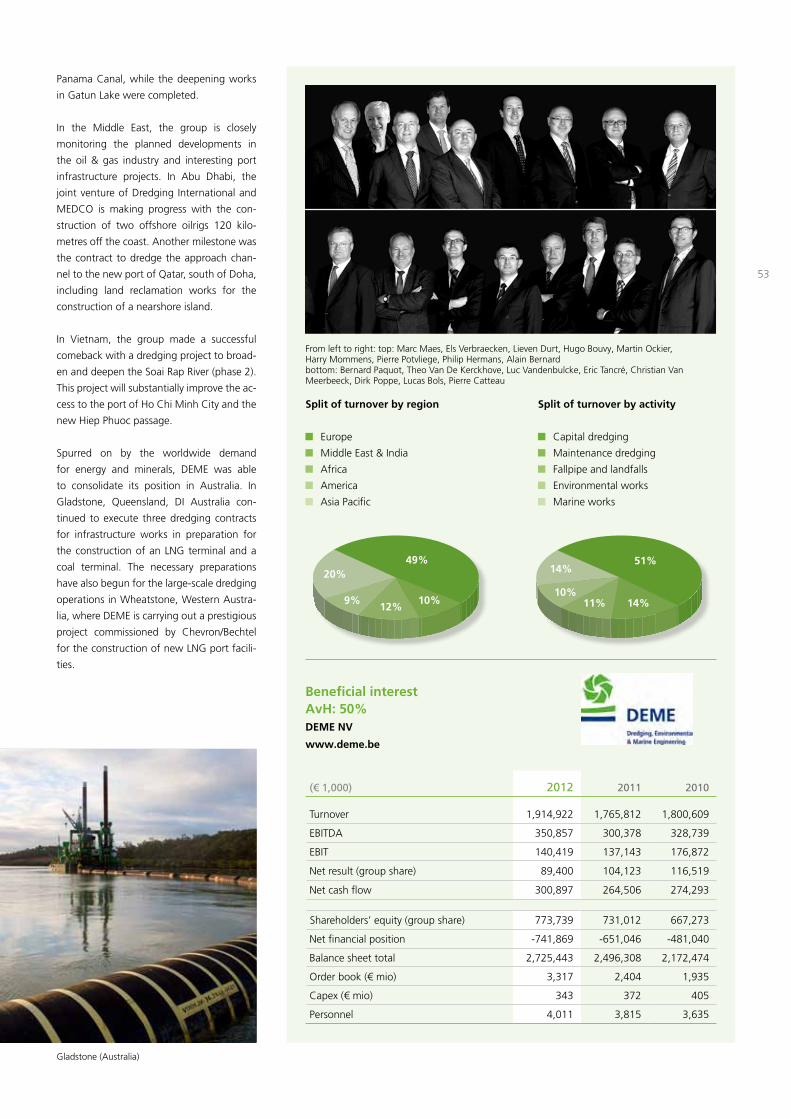

Marine Engineering & Infrastructure Private Banking Real Estate, Leisure & Senior Care Energy & Resources Development Capital

Consolidated result of the participations (before capital gains of Development Capital)

Pro forma turnover

The pro forma turnover comprises the turnover of all participations held by the AvH

group, and therefore deviates from the turnover as reported in the legal IFRS consoli-

dation. In this pro forma presentation, all (exclusive) control interests are incorporated

in full and the other interests proportionally.

Pro forma personnel

The AvH group represented in 2012, through its share in its participations, a turnover of 3.3 billion euros and employed approximately 18,750 people.

Information by segment

€ 3,308 mio 18,752

1,150

398

288

158

1,314

2,518

810 1,422

5,734

8,268

10

January

• Anima Care acquires the residential care

centre ‘Résidence Parc des Princes’ in

Auderghem.

February

• DEME secures a contract for the Wheat-

stone project in Australia, worth 916

million euros.

March

• MEDCO (DEME 44%) wins a contract for

the New Port Project in Qatar, worth 941

million euros.

• Sofinim sells its 60% stake in Alural

Belgium.

May

• DEME launches the self-propelled rock

cutter dredger ‘Ambiorix’.

Financière Duval (Residalya) - Le Clos Saint-Vincent DEME - Ambiorix

Key events 2012A n n u a l r e p o r t 2 0 1 2

June

• GeoSea (DEME) is awarded a contract

for the Northwind offshore wind turbine

project off the Belgian coast, worth more

than 230 million euros.

• Anima Care acquires ‘Azur Soins et

Santé’ in Braine-L’Alleud.

• AvH increases its stake in Groupe Finan-

cière Duval to 41.14%.

July

• Extensa secures planning permission for

the building for the Brussels Department

of Environment on the Tour & Taxis site

in Brussels.

11

September

• DEME launches the powerful high-tech

jack-up vessel ‘Innovation’.

• Sofinim sells its 63% (fully diluted) inter-

est in AR Metallizing.

• Leasinvest Real Estate subscribes the real

estate certificate for the Knauf shopping

centre in Luxembourg.

November

• DEME launches the first maintenance

vessels of OWA and the cutter dredger

‘Amazone’.

• NMC acquires the operations in the area

of EPS subfloor foils and thin wall insula-

tion of Isomo.

January

• DEME issues a retail bond, which is

closed early.

• Sofinim announces the sale of its

participation in Spano Invest.

• Sofinim and NPM Capital contribute

to a substantial refinancing of Hertel

by way of a cash injection.

Sipef - Oil palm nursery (North Sumatra)

Leasinvest Real Estate - Knauf shopping centre DEME - Innovation

December

• Leasinvest Real Estate acquires a prime

location in the centre of Luxembourg City.

• Anima Care acquires ‘Résidence Kinkem-

pois’ in Angleur.

• After obtaining two licences for a potential

expansion of 19,500 hectares in South

Sumatra, Sipef has already compensated

more than 2,000 hectares and planted an

extra 1,790 hectares in 2012.

• ABK (Bank J.Van Breda & Co) exists the

Beroepskrediet statute.

Key events 2013

1212

Annual report 2012

Message of the chairmen

Annual report of the board of directors

Corporate social responsibility

Ackermans & van Haaren considers the

family values of the founding families to

be of paramount importance. Elements

such as continuity, ethical entrepreneur-

ship, long-term thinking, work ing with

partners and mutual respect have

consequently driven the group’s policies

for many decades and have created value

through growth.

14

From left to right: Luc Bertrand, Jacques Delen

15Ladies and gentlemen,

Although the actual situation today in Western Europe, the United States and Japan suggests otherwise, the world economy is probably

developing faster during this decade than in the previous three decades. A 4.1% growth (Goldman Sachs) is projected for the period from

2011 to 2020. In the previous three decades, this growth figure never exceeded 3.5%.

What is clearly different is where this growth originates. The share of the BRIC countries in the world economy is expanding. In 2012, the

companies of our group derived roughly 1/3 of their turnover (3.3 billion euros in total) outside Western Europe. The international activities

of Ackermans & van Haaren allow our companies to participate in the expansion of international trade outside the traditional industrialized

countries. The success of this strategy should sustain the long-term growth of our group.

In the fifth year of the financial crisis, AvH stood its ground very well with a stable result for our participations of 172 million euros in 2012

compared to 173.9 million euros in 2011. Although this result was influenced by a number of positive and negative one-off elements, it

provides a solid basis for the anticipated growth during the current financial year. This result also led to an increase in the group’s equity to

more than two billion euros, which is an all-time high. The goal of a strong equity without any debt should bolster the group’s credibility

in today’s difficult economic environment.

In the Marine Engineering & Infrastructure segment, the turnover and EBITDA of DEME increased by 8.5% and 17% to 1,915 million euros

(1,766 million euros in 2011) and 351 million euros (300 million euros in 2011) respectively. On the other hand, the net profit decreased

to 89.4 million euros (104.1 million euros in 2011), due partially to increased depreciation and financial charges. The record order book of

DEME (3,317 million euros at year-end 2012 compared to 2,404 million euros in 2011) constitutes a solid basis for the current year. The

shift of activities to Australia and the Middle East continues. The Western European operations remain stable. Following the expansion of

the fleet with 7 vessels in 2012, DEME now has the necessary state-of-the-art and appropriate capacity to execute its order book in the

most productive way. The diversification into wind farms, offshore and jack-up vessels, oil and gas, environment, services and concessions

underscores the company’s potential for continuing future growth.

Despite the turbulent financial markets, the Private Banking segment of the group experienced a vigorous growth in 2012. JM Finn & Co

included, the assets under management of Delen Investments grew by 14.6% to 25,855 million euros (22,570 million euros in 2011).

The cost-income ratio is highly competitive at 55.2% (38.8% for Delen Private Bank), but increased as expected in relation to the previ-

ous year (44.2%) as a result of the consolidation of JM Finn & Co for a full financial year. The group is more than adequately capitalized

and amply satisfies the Basel II and Basel III requirements with respect to equity, with a Core Tier1 capital ratio of 23.1%. The net result of

Delen Investments grew by 9.5% to 62.6 million euros (57.2 million euros in 2011). The financial return for the clients was supported by

the bank’s prudent management in a more favourable environment. The steady improvement of the results of JM Finn & Co bodes well for

this investment in a new market.

Bank J.Van Breda & Co again showed a strong financial performance in 2012. As a result of the constant inflow of new funds, the client assets

grew by 7% to 8.0 billion euros (7.5 billion euros in 2011). With the bank’s targeted policy of focusing on a known clientele of liberal professionals

and entrepreneurs, provisions for loan losses were kept very low (0.08%). The consolidated profit amounted to 27.7 million euros (26.4 million

euros normalized in 2011). The growth in equity to 427 million euros (395 million euros in 2011) allows the bank to continue its expansion. With

a Core Tier1 capital ratio of 14.2%, Bank J.Van Breda & Co already satisfies the solvency criteria of Basel III. At year-end 2012, ABK decided to exit

from Beroepskrediet, which allows it to organize its partnership with Bank J.Van Breda & Co as efficiently as possible.

Message of the chairmen

A n n u a l r e p o r t 2 0 1 2

16

The Real Estate, Leisure & Senior Care segment again made a diminished contribution of 3.6 million euros to the group’s profit, compared

to 4.5 million euros in 2011. This is due to limited project results and delays in land development projects at Extensa. We firmly believe

that this is a cyclical rather than structural phenomenon. Leasinvest Real Estate continues to develop its operations on a profitable foot-

ing. The management was able to boost the net profit by 63% to 20.5 million euros through a higher rental income and the absence of

negative value adjustments on the portfolio. Financière Duval and Anima Care are currently bearing the cost of their future growth in

the sector of retirement homes and holiday residences. The group’s real estate strategy is focused on realizing a sustainable profit on real

estate related service activities of a recurrent nature.

The Energy & Resources segment contributed 16.4 million euros to the group result in 2012 (compared to 19 million euros in 2011). The

turnover of Sipef stood at USD 333 million (USD 368 million in 2011), while the net result decreased by 28% to USD 68.4 million com-

pared to the record year 2011 (USD 95.1 million). The shrinking demand from China had an adverse impact on the average price of palm

oil and rubber (USD 999 and USD 3,377 compared to USD 1,125 and USD 4,823 in 2011). Along with increased production costs, this has

contributed to a decrease in profit in 2012. With an EBITDA of USD 103 million (USD 130 million in 2011), Sipef has the necessary means

to further expand its plantations. The total planted acreage is approximately 65,000 hectares, of which more than 20% has not yet reached

the production stage. The skills of a highly professional management to develop new plantations at a cost of less than the current market

price confirm our belief in the continued growth of the added value of this company for our group.

Sagar Cements and Oriental Quarries & Mines suffered from the difficult economic situation in India, but the big infrastructure

budgets of the Indian government should shore up our operations in the future. Today, their contribution to the group is not yet mean-

ingful. Changes in the Flemish regulations in the area of renewable energy have a substantial impact on the results of Max Green and

markedly increase the risks in new projects. At Telemond Group, which specializes in welded steel structures in Poland, the turnover and

EBITDA increased further to 74.3 million euros (64.4 million euros in 2011) and 7.4 million euros (3.4 million euros in 2011) respectively.

Further growth is expected for 2013.

As far as Development Capital is concerned, a result – including capital gains – of 28.8 million euros was recorded. The recurring result

(AvH share) of the portfolio companies amounted to 6.1 million euros, including a negative contribution of 11 million euros at Hertel.

Hertel’s result was once again affected by certain heavy loss-making activities in Kazakhstan, France and Australia. The accompanying

restructuring operations and impairments led to a highly negative result of 33 million euros at Hertel (-21.8 million euros in 2011). A new

management team has taken over and the balance sheet was recapitalized at the beginning of 2013 with 75 million euros (37.5 million eu-

ros Sofinim). We are confident that this has helped to restore the balance sheet ratios and that it will also lead to a recovery in profitability.

The importance of a professional management team was highlighted once more by the turnaround at AR Metallizing, which enabled

the sale in 2012 with a capital gain of 20.6 million euros. In line with the strategy of this segment in terms of focus on bigger portfolio

companies, the interest in Alural Belgium was also sold at a slight profit. An earn-out was realized on the sale of Engelhardt Druck. The

agreement for the sale of Spanogroup was recently (March 2013) confirmed and, if approved by the competition authorities, is expected

to yield a substantial capital gain in 2013.

The strategy of the group in the direction of a further growth of the larger companies in the Development Capital segment continues. In

2012, the adjusted net asset value of this segment increased further to 481 million euros (452 million euros at year-end 2011).

A n n u a l r e p o r t 2 0 1 2

17

In the course of 2012, the net cash position of the group increased slightly from 73.0 million euros to 87.9 million euros. The growth of the

group’s equity from 1.883 million euros to 2.007 million euros and the favourable outlook for the current financial year of Ackermans &

van Haaren inspired the board of directors to propose an increase in the gross dividend from 1.64 euros per share to 1.67 euros per share.

We would like to thank all the staff members of the group for their efforts and resilience in a difficult economic environment.

27 March 2013

Luc Bertrand

President of the executive committee

Jacques Delen

President of the board of directors

18

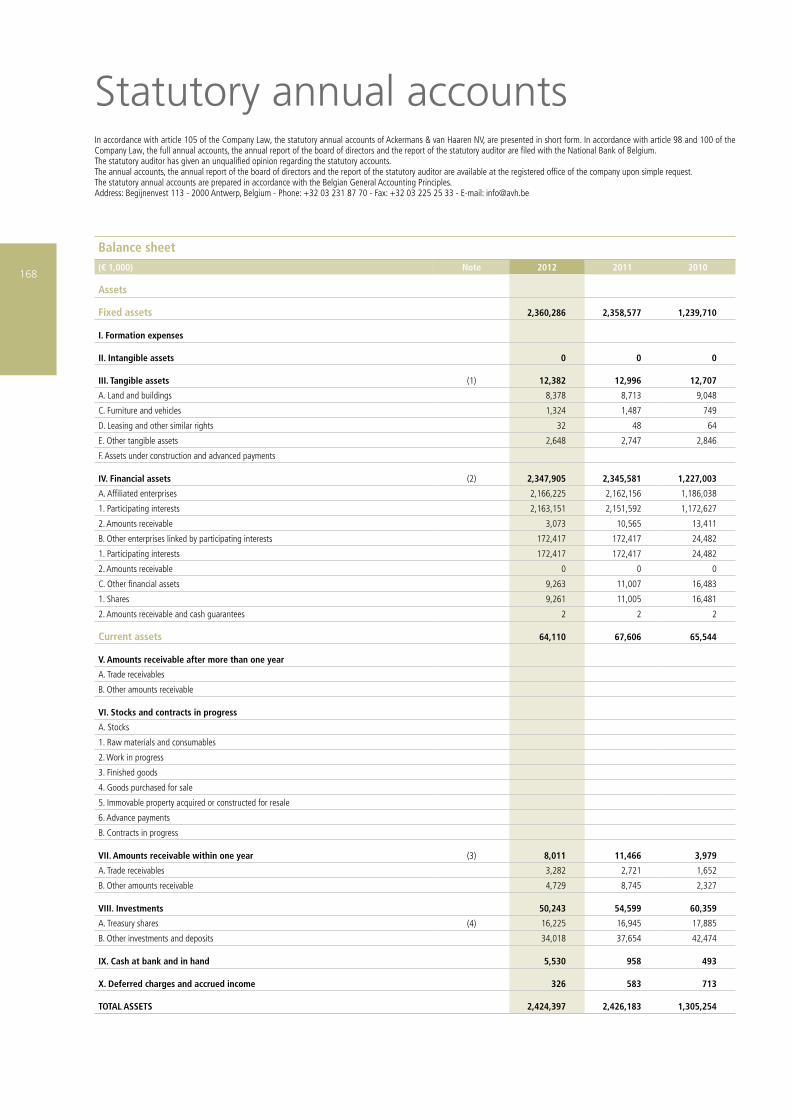

I Statutory annual accounts

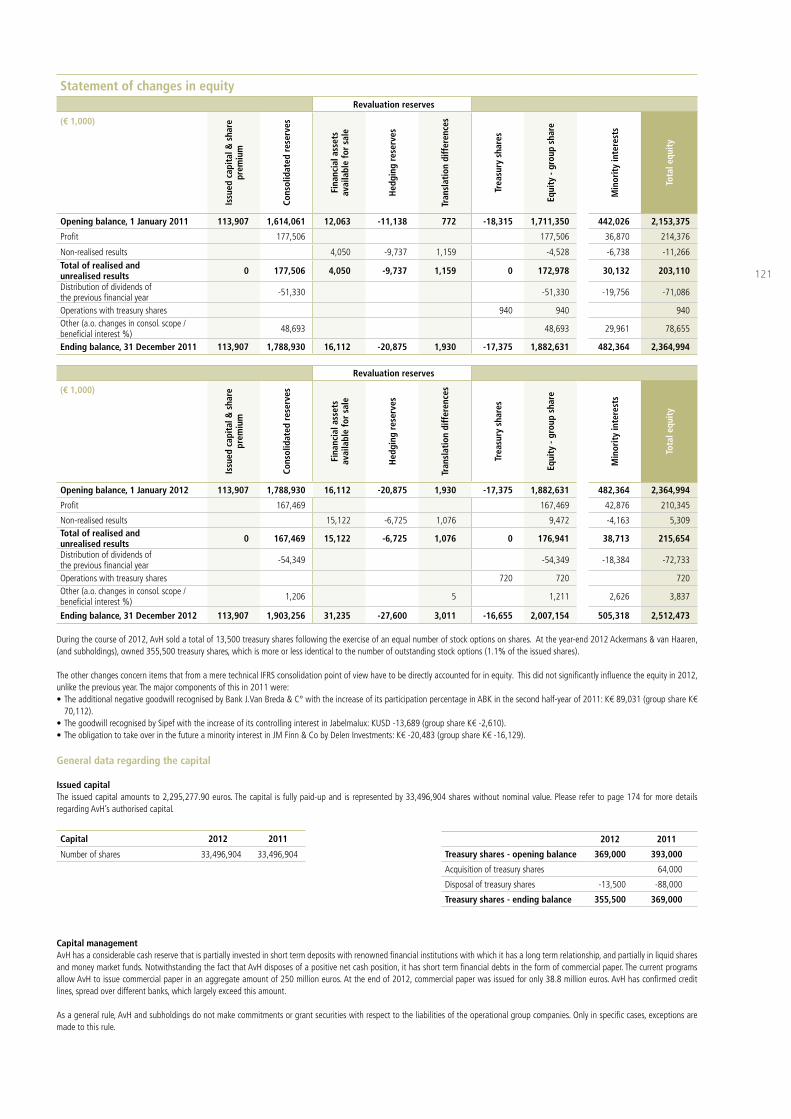

1. Share capital and shareholding structureNo changes were made to the company’s

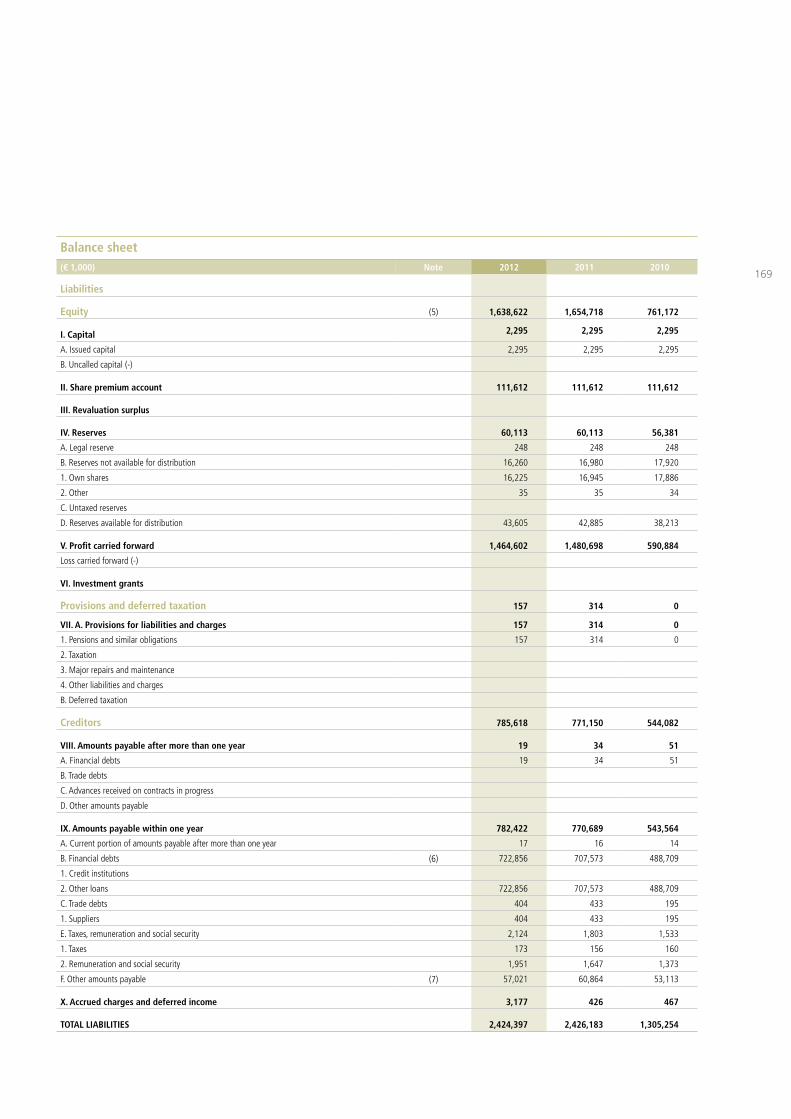

share capital during the last financial year.

The share capital amounts to 2,295,278

euros and is represented by 33,496,904

no-nominal-value shares. All shares have

been paid up in full.

In 2012, 47,000 new options were granted

under the stock option plan. As at 31 De-

cember 2012, the options granted and not

yet exercised entitled their holders to acquire

an aggregate of 353,000 Ackermans & van

Haaren shares (1.05%).

The company received a transparency no-

tice on 31 October 2008 under the tran-

sitional regulations of the Act of 2 May

2007, whereby Scaldis Invest NV - together

with “Stichting Administratiekantoor Het

Torentje” - communicated its holding per-

centage. The relevant details of this trans-

parency notice can be found on the website

of the company (www.avh.be).

2. ActivitiesFor an overview of the group’s main activi-

ties during the 2012 financial year, please

refer to the Message of the chairmen (p. 15).

3. Comments on the statutory annual accounts

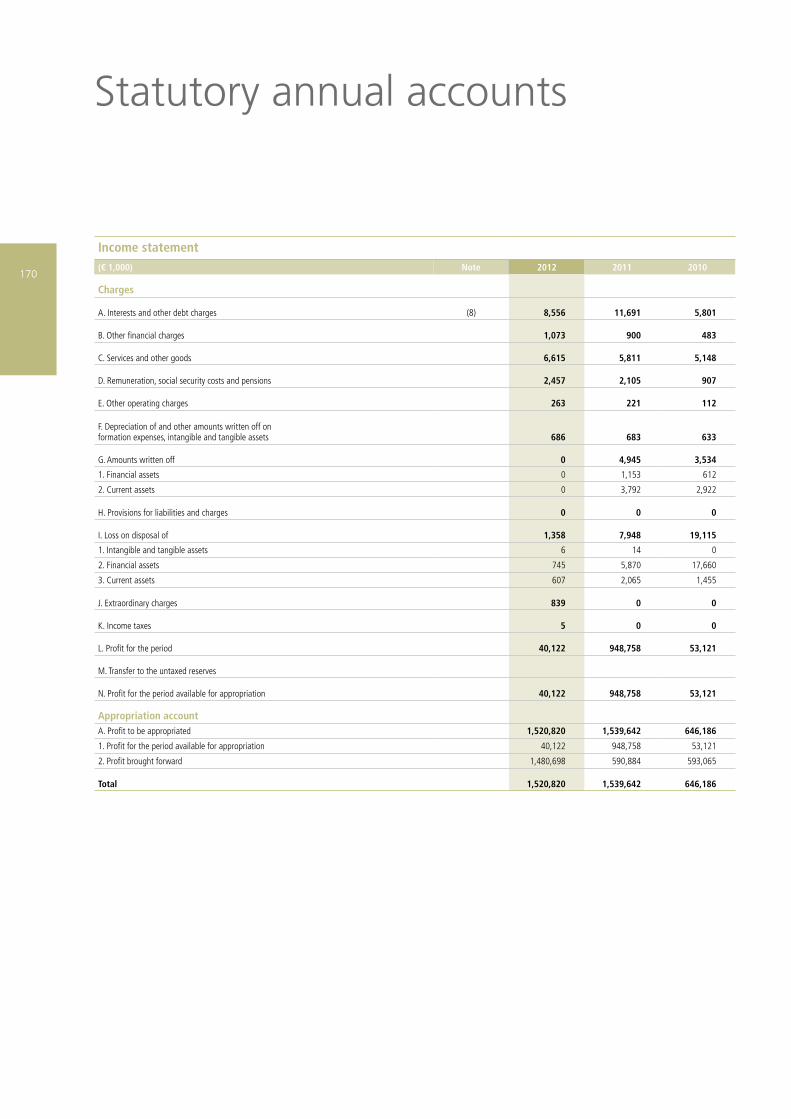

3.1 Financial situation as at 31 December 2012The statutory annual accounts have been

prepared in accordance with Belgian ac-

counting principles.

The balance sheet total at year-end 2012

amounted to 2,424 million euros, which is

virtually the same as the previous year (2011:

2,426 million euros). Besides the 12 million

euros in tangible fixed assets on the balance

sheet (primarily the office building located

on Begijnenvest and Schermersstraat in Ant-

werp), the assets consist of 50 million euros

in investments and 2,348 million euros in

financial fixed assets.

Unlike in 2011, which was characterized

by a substantial portfolio growth following

the liquidation of the subsidiary Nationale

Investeringsmaatschappij, the portfolio un-

derwent only minor changes in 2012. The

largest investments in 2012 were the ad-

ditional investments by Ackermans & van

Haaren in Anima Care and Holding Groupe

Duval. Since Ackermans & van Haaren sold

no participations to speak of in 2012, virtu-

ally no capital gains were realized. The very

substantial capital gain that was reported in

2011 originated from the liquidation of the

Nationale Investeringsmaatschappij and was

not in the least recurrent.

On the liabilities side of the balance sheet,

the dividend payment of 56 million euros

Annual report of the board of directors

A n n u a l r e p o r t 2 0 1 2

Dear shareholder,

It is our privilege to report to you on the activities of our company during the past financial year and to sub-

mit to you for approval both the statutory and consolidated annual accounts closed on 31 December 2012.

In accordance with Article 119 of the Companies Code, the annual reports on the statutory and consoli-

dated annual accounts have been combined.

19

and the profit for the financial year of 40

million euros caused the shareholders’ equi-

ty to decrease to 1,639 million euros (2011:

1,655 million euros). In 2012, too, the short-

term financial debts consisted for the most

part of financial liabilities incurred by AvH

Coordination Center, a company that is an

integral part of the group and which fulfils

the role of internal bank for the group. The

other liabilities already include the profit

distribution for the 2012 financial year that

is being proposed to the ordinary general

meeting. As a result of the dividends re-

ceived, the financial year closed with a profit

amounting to 40 million euros.

Including the profit distribution proposal

submitted to the annual general meeting

on 27 May 2013, the statutory sharehold-

ers’ equity of Ackermans & van Haaren at

the end of 2012 stood at 1,639 million euros

as compared to 1,655 million euros at the

end of 2011. This amount does not include

unrealised capital gains present in the port-

folio of Ackermans & van Haaren and group

companies.

In the course of 2012, Ackermans & van

Haaren did not purchase own shares and

sold 13,500. These transactions are purely

related to the implementation of the stock

option plan.

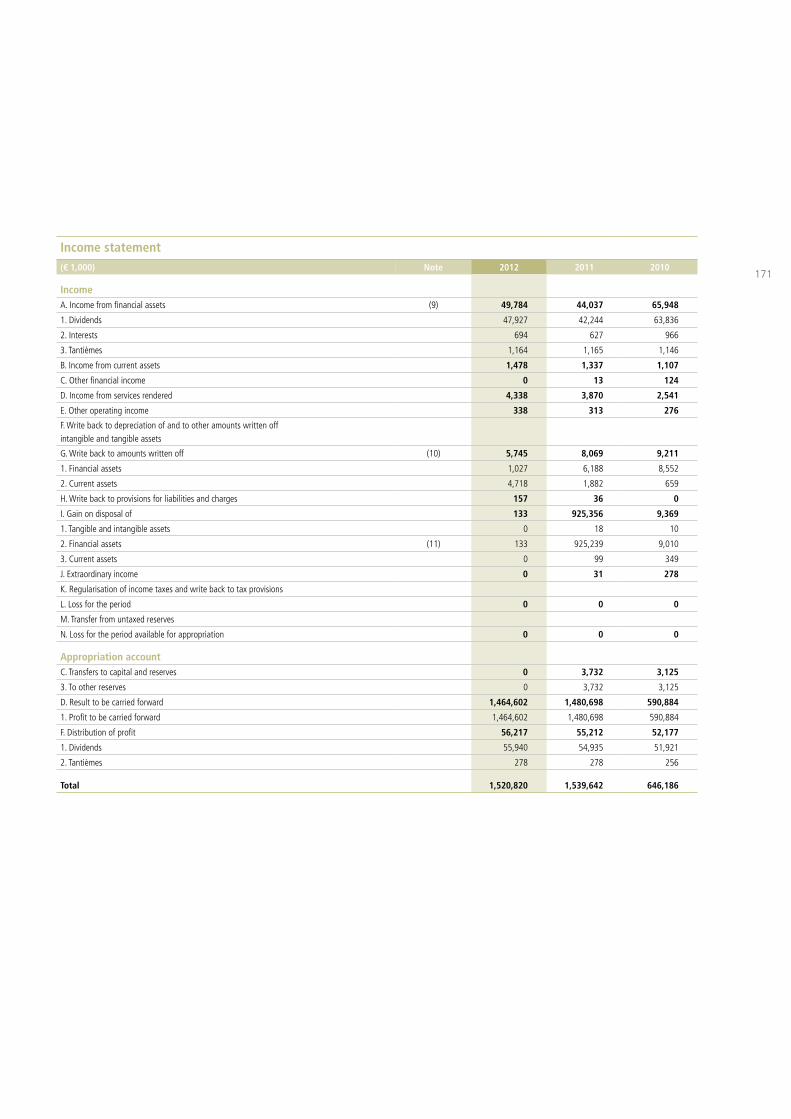

3.2 Appropriation of the resultsThe board of directors proposes to appropri-

ate the result (in euros) as follows:

Profit from the previous financial year carried forward

1,480,698,020

Profit of the financial year 40,121,506

Total for appropriation 1,520,819,526

Allocation to the legal reserve

0

Allocation to the non-distributable reserves

0

Allocation to the distributable reserves

0

Dividends 55,939,830

Directors’ fees 277,500

Profit to be carried forward

1,464,602,196

The board of directors proposes to distrib-

ute a gross dividend of 1.67 euros per share.

After deduction of withholding tax, the net

dividend will amount to 1.2525 euros per

share.

If the annual general meeting approves this

proposal, the dividend will be payable from

3 June 2013. From that day onwards, hold-

ers of bearer shares can present themselves

to Bank Delen, Bank J.Van Breda & C°, Bank

Degroof, BNP Paribas Fortis, KBC Bank, ING

Belgium, Belfius Bank and Petercam and will

receive the dividend against presentation of

coupon no. 14.

Following this distribution, shareholders’ eq-

uity will stand at 1,638,622,063 euros and

will be composed as follows:

Capital

- Subscribed capital 2,295,278

- Issue premium 111,612,041

Reserves

- Legal reserve 248,081

- Non-distributable reserves 16,259,805

- Tax-exempt reserves 0

- Distributable reserves 43,604,663

Profit carried forward 1,464,602,196

Total 1,638,622,063

3.3 OutlookAs in previous years, the results for the cur-

rent financial year will to a large extent de-

pend on the dividends paid by the compa-

nies within the group and on the realization

of any capital gains or losses.

4. Major events after the closing of the financial yearSince the closing of the 2012 financial year,

there have been no major events which

could have a significant impact on the de-

velopment of the company, except those

referred to under II.3 below.

5. Research and developmentThe company did not undertake any activi-

ties in the area of research and development.

20

6. Financial instrumentsCompanies within the group may use fi-

nancial instruments for risk management

purposes. Specifically, these are instruments

principally intended to manage the risks

associated with fluctuating interest and ex-

change rates. The counterparties in the re-

lated transactions are exclusively first-ranked

banks. As at the end of 2012, neither Acker-

mans & van Haaren nor any other fully con-

solidated group company within the ‘AvH &

sub-holdings’ segment had any such instru-

ments outstanding.

7. Notices

7.1 Application of Article 523 of the Companies CodeExtract from the minutes of the meeting of

the board of directors of Ackermans & van

Haaren held on 13 November 2012:

“Mandate for granting stock options

Before the board of directors starts delibera-

tions on the granting of stock options, Luc

Bertrand declares that he, as a beneficiary of

the stock option plan, has a direct interest of

a proprietary nature which conflicts with the

proposed resolution within the meaning of

Article 523 of the Companies Code.

Pursuant to Article 523 of the Companies

Code, Luc Bertrand states that he will inform

the company auditor of the conflict of inter-

est after this meeting. Luc Bertrand leaves

the meeting and does not take part in the

deliberations or decision-making concerning

this item.

Based on the recommendations of the re-

muneration committee, the board of di-

rectors decides to grant, under the current

stock option plan, Jacques Delen and Luc

Bertrand, each acting separately, special au-

thorization to offer a maximum of 50,000

options on Ackermans & van Haaren shares

to the members of the executive committee

and certain members of staff and independ-

ent service providers of Ackermans & van

Haaren and Sofinim.

The offering of the options is to take place

on 2 January 2013 and, as in previous years,

the exercise price will be determined based

on the average price of the share during the

30 days preceding the offer.

As it is the policy of the company to hedge

the stock options through the purchase of

own shares, the proprietary consequences

for the company are in principle limited to (i)

the interest borne or lost during the period

running from the purchase of the shares to

their resale to the option holders, (ii) any dif-

ference between the purchase price of own

shares and the exercise price of the options

granted, and (iii) the accounting cost which

in pursuance of IFRS 2 must be shown in the

income statement and which has an impact

on the result per share.

Luc Bertrand rejoins the meeting.”

7.2 Additional remuneration for the auditorPursuant to Article 134, §§2 and 4 of the

Companies Code, we inform you that an ad-

ditional fee of 17,980 euros (excluding VAT)

was paid to Ernst & Young Tax Consultants

for tax advice and 5,750 euros (excluding

VAT) to Ernst & Young Bedrijfsrevisoren for

diverse activities.

7.3 Acquisition and transfer of own sharesOn 25 November 2011, the extraordinary

general meeting authorized the board of

directors of Ackermans & van Haaren to ac-

quire own shares within a well-defined price

range during a period of 5 years.

In the course of the 2012 financial year,

Ackermans & van Haaren did not acquire ad-

ditional own shares to cover its obligations

under the stock option plan.

A n n u a l r e p o r t 2 0 1 2

21

Taking into account the sale of 13,500

shares pursuant to the exercising of options,

the situation as at 31 December 2012 was

as follows:

Number of treasury shares

304,200 (0.91%)

Par value per share 0.07 euros

Average price per share

53.34 euros

Total investment value

16,225,052 euros

In addition, Brinvest, a direct subsidiary of

Ackermans & van Haaren, holds another

51,300 shares of Ackermans & van Haaren.

7.4 Notice pursuant to the law on takeover bidsIn a letter dated 18 February 2008, Scaldis

Invest sent a notice to the company in ac-

cordance with Article 74, §7 of the Act of

1 April 2007 on takeover bids. From this

notice, it appeared that Scaldis Invest owns

over 30% of the securities with voting rights

in Ackermans & van Haaren and that Sticht-

ing Administratiekantoor “Het Torentje” ex-

ercises ultimate control over Scaldis Invest.

7.5 Protection schemes (i) Powers of the management body

On 25 November 2011, the extraordinary

general meeting renewed the authorization

of the board of directors to proceed, in case

of a takeover bid for the securities of Acker-

mans & van Haaren, to a capital increase in

accordance with the provisions and within

the limits of Article 607 of the Companies

Code.

The board of directors is allowed to use

these powers if the notice of a takeover bid

is given by the Financial Services and Mar-

kets Authority ('FSMA') to the company

not later than three years after the date of

the abovementioned extraordinary general

meeting. The board of directors is also au-

thorised for a period of three years expiring

on 14 December 2014 to acquire or transfer

shares of the company in the event that such

action is required in order to safeguard the

company from serious and imminent harm.

(ii) Important agreements

The shareholders’ agreement with respect

to DEME NV which the company conclud-

ed on 22 March 2007 with Aannemings-

maatschappij CFE NV ('CFE') grants specific

rights to the latter in the case of a change or

acquisition of direct control over Ackermans

& van Haaren. These rights essentially mean

that in such case CFE has the option of ter-

minating the shareholders’ agreement.

22

II Consolidated annual accounts

1. Risks and uncertaintiesThis section describes, in general terms, the

risks facing Ackermans & van Haaren NV

(“AvH”) as an international investment com-

pany, and the operational and financial risks

associated with the different segments in

which it is active (either directly or indirectly

through its subsidiaries).

The executive committee of AvH is respon-

sible for the preparation of a framework for

internal control and risk management which

is submitted for approval to the board of di-

rectors. The board of directors is responsible

for the evaluation of the implementation

of this framework, taking into account the

evaluation carried out by the audit commit-

tee. At least once a year the audit committee

evaluates the internal control systems which

the executive committee has set up in order

to ascertain that the main risks have been

properly identified, reported and managed.

The subsidiaries of AvH are responsible for

the management of their own operational

and financial risks. Those risks, which vary

according to the sector, are not centrally

managed by AvH. The management teams

of the subsidiaries in question report to their

board of directors or audit committee on

their risk management.

Risks at the level of Ackermans & van Haaren

Strategic riskThe objective of AvH is to create shareholder

value by long-term investment in a limited

number of strategic participations. The avail-

ability of opportunities for investment and

divestment, however, is subject to macro-

economic, political, social and market condi-

tions. The achievement of the objective can

be adversely affected by difficulties encoun-

tered in identifying or financing transactions

or in the acquisition, integration or sale of

participations.

The definition and implementation of the

strategy of the group companies is also de-

pendent on this macroeconomic, political,

social and market context. By focusing as

a proactive shareholder on long-term value

creation and on the maintenance of opera-

tional and financial discipline, AvH endeav-

ours to limit those risks as much as possible.

In several group companies, AvH works

together with partners. In certain group

companies, AvH has a minority stake. The

diminished control which may result from

that situation could lead to relatively greater

risks; however, this is counterbalanced by a

close cooperation and by an active represen-

tation on the board of directors of the com-

panies concerned.

Risk related to the stock market listingAs a result of its listing on NYSE Euronext

Brussels, AvH is subject to a whole series of

regulations regarding information require-

ments, transparency reporting, takeover

bids, corporate governance and insider

trading. AvH pays the necessary attention

to keeping up and complying with the con-

stantly changing laws and regulations in this

area.

The volatility of the financial markets has an

impact on the value of the share of AvH (and

of some of its listed group companies). As

was mentioned earlier, AvH seeks to system-

atically create longterm shareholder value.

Short-term share price fluctuations and the

speculation associated with this can produce

a momentarily different risk profile.

A n n u a l r e p o r t 2 0 1 2

23

Liquidity riskAvH has sufficient resources at its disposal

to implement its strategy and has no net

financial debts. The subsidiaries are respon-

sible for their own debt financing, it being

understood that, in principle, AvH does not

extend credit lines or securities to or for the

benefit of its participations.

The external financial debts of ‘AvH & sub-

holdings’ virtually correspond to the treas-

ury bonds issued by AvH (commercial paper

programme). AvH has confirmed credit lines

from different banks with which it has a

long-term relationship, such credit lines am-

ply exceeding the outstanding commercial

paper obligations.

The board of directors believes that the li-

quidity risk is fairly limited.

Risks at group company level

Marine Engineering & Infrastructure The operational risks of this segment are

essentially associated with the execution

of often complex projects and are, among

other things, related to the technical design

of the projects and the integration of new

technologies; the setting of prices for ten-

ders and, in case of deviation, the possibil-

ity or impossibility of hedging against extra

costs and price increases; performance obli-

gations (in terms of cost, conformity, quality,

turnaround time) with the direct and indirect

consequences associated therewith, and the

time frame between quotation and actual

execution. In order to cope with those risks,

the different group companies work with

qualified and experienced staff. In principle,

AvH is only involved in strategic decisions

at the level of the board of directors and in

the selection of the top management of the

DEME group rather than in the management

of the operational risks mentioned above.

The construction and dredging sector is typi-

cally subject to economic fluctuations. The

market of large traditional infrastructural

dredging works is subject to strong cyclical

fluctuations on both the domestic and inter-

national markets. This has an impact on the

investment policy of private sector custom-

ers (e.g. oil companies or mining groups)

and of local and national authorities. DEME

is to a significant degree active outside the

euro zone. Consequently, it runs not only a

currency exchange risk, but in some cases

also a political risk. DEME hedges against

exchange rate fluctuations or sells foreign

currency futures. Certain commodities or

raw materials, such as fuel, are hedged as

well.

Given the size of the contracts in this

segment, the credit risk is closely moni-

tored too. For the purposes of large foreign

contracts, for instance, DEME regularly uses

the services of the Office national du du-

croire/Nationale Delcrederedienst (ONDD

- Belgium’s national delcredere office) in-

sofar as the country concerned qualifies

for this service and the risk can be cov-

ered by credit insurance. For largescale

infrastructural dredging contracts, DEME

is dependent on the ability of custom-

ers to obtain financing and can, if neces-

sary, organize its own project financing.

Van Laere bills and is paid as the works pro-

gress. As far as NMP is concerned, the risk

of discontinuity of income is estimated to be

fairly limited, since it has long-term transport

contracts with large national and interna-

tional petrochemical firms.

The liquidity risk is limited by spreading

the financing over several banks and by

consolidating this financing to a significant

extent over the long term. DEME continu-

ously monitors its balance sheet structure

and pursues a balance between a consoli-

dated shareholders’ equity position and con-

solidated net debts. DEME has major credit

and guarantee commitments with a whole

string of international banks. In a number of

cases, certain ratios (covenants) were agreed

in the loan agreements with the relevant

banks which DEME must observe. In addi-

tion, it has a commercial paper programme

to cover short-term financial needs. DEME

predominantly invests in equipment with

a long life which is written off over several

years. For that reason, DEME seeks to sched-

ule a substantial part of its debts over a long

term. Om bovendien In order to diversify the

funding over several sources, DEME issued

a retail bond of 200 million euros in Janu-

ary 2013. This was placed with a diversified

DEME

24

group of (mainly private) investors. Accor-

ding to the terms of issue, DEME will not

make any interim redemptions of the princi-

pal, but will instead repay everything on the

maturity date in 2019.

Private BankingThe credit risk and risk profile of the invest-

ment portfolio have for many years now

been deliberately kept very low by Delen

Private Bank and Bank J.Van Breda & C°.

The banks invest in a conservative manner.

In the case of Delen Private Bank, lending

to customers is limited and is guaranteed by

pledges on securities. The credit portfolio of

Bank J.Van Breda & C° is very widely spread

among a client base of local entrepreneurs

and professionals, and credit is granted to

this target group of clients. The bank applies

concentration limits per sector and maxi-

mum credit amounts per client.

Bank J.Van Breda & C° adopts a cautious

policy with regard to interest rate risk,

well within the standards set by the NBB.

Where the terms of assets and liabilities do

not match sufficiently, the bank deploys

hedging instruments (a combination of in-

terest rate swaps and options) to correct

the balance. The interest rate risk at Delen

Private Bank is limited, due to the fact that

it primarily focuses on asset management,

with very limited lending and without taking

positions.

The exchange rate risk at Delen Invest-

ments is limited to the holdings in foreign

currency (Delen Suisse & JM Finn & Co). At

present, the net exposure in pound sterling

is limited since the impact of exchange rate

fluctuations on the equity of JM Finn & Co is

neutralized by an opposite impact on the li-

quidity obligation on the remaining 26.51%

in JM Finn & Co.

The liquidity and solvency risk of the

banks is continuously monitored by a proac-

tive risk management. Furthermore, the two

groups have more than sufficient liquid as-

sets to meet their commitments, as well as

sound Core Tier1 equity ratios.

Both banks are adequately protected against

business risk or income volatility risk. The

operating charges of Delen Private Bank are

amply covered by the regular income, while

in the case of Bank J.Van Breda & C° the

income from relationship banking is highly

diversified in terms of clients as well as of

products.

Since Delen Investments does not manage a

share portfolio of its own, the direct market

risk is limited to open overnight positions

for securities purchased or sold for clients

and not yet settled. The (indirect) risk that a

prolonged stock market decline impairs the

bank’s assets under management is counter-

balanced by a solid cost/income ratio for De-

len Investments, so that the group continues

to be profitable even in the event of a sharp

stock market decline.

Real Estate, Leisure & Senior CareThe operational risks in the real estate

sector can be classified according to the

different stages in the process. A first cru-

cial element is the quality of the offering of

the right buildings and services. In addition,

long-term lease contracts with solvent ten-

ants are expected to guarantee the highest

possible occupancy rate of both buildings

and services and a recurrent flow of income,

and should limit the risk of non-payment. Fi-

nally, the renovation and maintenance risk is

also continuously monitored.

The real estate development activity is sub-

ject to strong cyclical fluctuations (cyclical

risk). Development activities for office build-

ings tend to follow the conventional eco-

nomic cycle, whereas residential activities

respond more directly to the economic situa-

tion, consumer confidence and interest rate

levels. Extensa Group is active in Belgium

and Luxembourg (where the main focus of

its activity lies) as well as in Turkey, Romania

and Slovakia, and is therefore subject to the

local market situation. However, the spread

of its real estate operations over different

segments (e.g. residential, logistics, offices,

retail) limits this risk.

The exchange risk is very limited because

most operations are situated in Belgium and

Luxembourg, with the exception of Extensa’s

operations in Turkey (risk linked to the USD

and the Turkish lira) and in Romania (risk

linked to the RON). Leasinvest Real Estate

A n n u a l r e p o r t 2 0 1 2

Bank J.Van Breda & C° - Sint Niklaas Delen Private Bank

25

and Extensa Group possess the necessary

long-term credit facilities and backup lines

for their commercial paper programme to

cover present and future investment needs.

Those credit facilities and backup lines serve

to hedge the financing risk. The liquidity

risk is limited by having the financing spread

over several banks and by diversifying the

expiration dates of the credit facilities over

the long term.

The hedging policy for the real estate opera-

tions is aimed at confining the interest rate

risk as much as possible. To this end, various

financial instruments such as spot & forward

interest rate collars, interest rate swaps and

CAPs are employed.

Energy & ResourcesThe focus of this segment is on businesses

in growth markets, such as India, Indonesia

and Poland. Since the companies concerned

are to a great extent active outside the euro

zone (Sagar Cements and Oriental Quar-

ries & Mines in India, Sipef in Indonesia and

Papua New Guinea among others), the cur-

rency exchange rate risk (on the balance

sheet and in the income statement) is more

relevant here than in the other segments.

The risk of fluctuations in the local economic

and political situation must be taken into

account as well.

The output volumes and therefore the

turnover and margins realized by Sipef are to

some extent influenced by climatic conditi-

ons such as rainfall, sunshine, temperature

and humidity.

Finally, the group is in this segment also ex-

posed to fluctuations in raw material prices

(e.g. Sipef: palm oil, rubber and tea; Sagar

Cements: coal).

Development CapitalAvH makes venture capital available to a lim-

ited number of companies with international

growth potential. The investment horizon is

on average longer than that of the tradition-

al players on the development capital mar-

ket. The investments are usually made with

conservative debt ratios, with in principle no

advances or securities being granted to or

for the benefit of the group companies con-

cerned. In addition, the diversified nature of

these investments contributes to a balanced

spread of the economic and financial risks.

As a rule, AvH will finance those investments

with shareholders’ equity.

The economic situation has a direct impact

on the results of the group’s companies, par-

ticularly in the case of the more cyclical or

consumer-driven companies. The fact that

the activities of the group companies are

spread over different segments affords a

partial protection against the risk.

Each group company is subject to specific

operational risks such as price fluctuations

of services and raw materials, the ability to

adjust sales prices, competitive risks, etc. The

companies monitor those risks themselves

and can try to limit them by operational and

financial discipline and by strategic focus.

Monitoring and control by AvH as a proac-

tive shareholder also play an important part

in that respect.

Several of the group’s companies (e.g.

Hertel, Manuchar) are to a significant extent

active outside the euro zone. The exchange

rate risk in each of these cases is monitored

and controlled by the group company itself.

Extensa - Tour & Taxis Sipef

26

2. Comments on the consolidated annual accountsThe consolidated annual accounts were

prepared in accordance with International

Financial Reporting Standards (IFRS).

The group’s consolidated balance sheet total

as at 31 December 2012 amounted to 6,759

million euros, which is an increase of 4%

compared to the figure for the end of 2011

(6,517 million euros). This balance sheet to-

tal is obviously impacted by the manner in

which certain group companies are included

in the consolidation.

The accounting principles used remained un-

changed from those applied to the accounts

for 2011. Shareholders’ equity (group share)

at the end of 2012 was 2,007 million euros,

which represents an increase of 125 million

euros compared to the figure for the end of

2011. In June 2012, AvH paid out a gross

dividend of 1.64 euros per share, resulting

in a decrease in equity by 54.3 million euros.

In the course of 2012, investments amount-

ed to 51 million euros, while divestments

reached 65 million euros. Apart from some

smaller investments, an additional 26.1 mil-

lion euros was invested in Hertel; the capi-

tal of Anima Care was further paid up, in

an amount of 8.4 million euros, in order

to finance the expansion of the retirement

home portfolio, and AvH increased its stake

in Groupe Financière Duval by 1.96% to

41.14%. AvH further streamlined its portfo-

lio with the sale of its interests in Alural Bel-

gium (60% through Sofinim), AR Metallizing

(63% through Sofinim), Gulf Lime (35%),

and the sale of 2% of its interest in Koffie F.

Rombouts (remaining interest 12%).

The net cash position of Ackermans & van

Haaren stood at 87.9 million euros at the

end of 2012, compared with 73.0 million

euros at the end of 2011.

An (economic) breakdown of the results for

the group’s various activity segments is set

out in the ‘Key Figures’ appendix to the an-

nual report.

Marine Engineering & Infrastructure.

DEME’s profit contribution decreased in

2012 despite an increase in turnover and a

very solid order book. Rent-A-Port contrib-

uted positively thanks to the strong perfor-

mance of its Vietnamese operations.

Despite the persistent economic slowdown

in large parts of the world, DEME (AvH

50%) managed to increase its turnover in

2012 to 1,915 million euros (compared to

1,766 million euros in 2011) thanks to a

well-filled order book (3,317 million euros

compared to 2,404 million euros at the end

of 2011) and a strategy that is resolutely fo-

cused on a balanced spread of its activities,

coupled with a multidisciplinary approach to

markets and customers.

The traditional dredging activities in 2012

represented 65% of DEME’s turnover. The

ancillary activities, such as environmental

works, services to the oil, gas and mining

industry, extraction of construction aggre-

gates at sea, and the construction of off-

shore wind farms, together accounted for

the remaining 35% of turnover. GeoSea and

Tideway in particular, which specialize in

maritime and offshore construction works,

witnessed a spectacular growth as a result

of the rapidly growing renewable energy

market and developments in the oil and gas

industry.

The EBITDA increased from 300 million eu-

ros in 2011 to 351 million euros, whereas

the net result decreased to 89.4 million

euros due to higher depreciation expenses

resulting from the expansion of the fleet, as

well as increased financial costs.

The order book contains a fair number of

new orders from across all continents. These

include some strategic contracts which the

group won for the construction of port and

oil & gas infrastructures in Australia and the

Persian Gulf. MEDCO (DEME 44%) signed

the New Port Project in Qatar (total value

941 million euros), and the Wheatstone LNG

project of Chevron in Australia (total value

916 million euros) was approved. In addi-

tion, GeoSea was awarded a contract for the

construction and installation of the founda-

tions for the Northwind offshore wind tur-

bine project off the Belgian coast (turnover

in excess of 230 million euros).

In 2012, DEME concluded its ambitious in-

vestment programme for the period 2008-

A n n u a l r e p o r t 2 0 1 2

DEME - Thornton Bank

27

2012, and seven new vessels were launched

and put into service: the backhoe dredger

‘Peter the Great’, the DP2 jack-up vessel

‘Neptune’, the rock cutter dredger ‘Am-

biorix’ (28,000 kW), the state-of-the art

high-tech jack-up vessel ‘Innovation’, two

maintenance vessels ‘Arista’ and ‘Aquata’,

and finally the seagoing cutter dredger

‘Amazone’ (12,860 kW). With these vessels,

the group has one of the most advanced, ef-

ficient and versatile fleets in the world.

Targeted commercial efforts enabled

Algemene Aannemingen Van Laere

(AvH 100%) to realize in 2012 another

significant increase in turnover (161 million

euros, +17% compared to 2011). Several

projects were successfully implemented,

such as the State Archives in Bruges, the

Jetair-Tui hangar at Brussels Airport, and

the Genzyme project in Geel. The net re-

sult, however, decreased (1.2 million euros

compared to 1.7 million euros in 2011)

due to the extremely competitive market,

some difficult sites and the start-up costs

of the parking company Alfa Park. The or-

der book amounted to 131 million euros

at the end of the year, which bodes well

for 2013.

Bank (17,884 million euros) and JM Finn

(7,971 million euros) contributed to this

growth of 14.6% compared to the end of

2011 (22,570 million euros). The group pri-

marily benefited from a major organic net

growth, with an inflow of new assets from

both existing and new private clients, as well

as from the impact of recovering financial

markets on its client portfolio. The gross

operating income of Delen Investments in-

creased to 214.8 million euros (2011: 162.5

million euros), primarily thanks to the higher

level of assets under management and

the recognition of JM Finn & Co for a full

year (2011: three months). The cost - in-

come ratio remained highly competitive at

55.2% (38.8% for Delen Private Bank), but

increased substantially as expected in com-

parison to the previous year (44.2%), as a

result of the consolidation of JM Finn for a

full financial year. The net profit amounted

to 62.6 million euros (57.2 million euros in

2011). The consolidated equity of Delen In-

vestments (group share) at the end of 2012

stood at 414.5 million euros (364.3 million

euros at the end of 2011). The group is

more than adequately capitalized and am-

ply satisfies the Basel II and Basel III criteria

with respect to equity. The Core Tier I capi-

2012 was a breakthrough year for Rent-

A-Port (AvH 45%) in several respects,

particularly in Vietnam, Oman and Qatar.

The project in the industrial zone of Dinh

Vu (Vietnam) is a success and will probably

be extended to 1,500 ha of industrial land.

Negotiations for this project are expected

to be completed in the course of 2013. In

December, a key contract was signed in

Oman between the Omani government

and ‘Consortium Antwerp Port’ for the

concession of the port and industrial es-

tates of Duqm for a 30-year period. Rent-

A-Port realized a net profit in 2012 of 12.3

million euros.

Private Banking. The solid performance

of Delen Investments and Bank J.Van Breda

& C° has raised the volume of assets under

management to a record level. The profit

contribution of this segment is less than in

2011 due to a one-off negative goodwill

which at the time was recognized in the re-

sults.

The assets under management of the

Delen Investments (AvH 78.75%) group

attained a record high of 25,855 million eu-

ros at the end of 2012. Both Delen Private

DEME - Aquata Van Laere - Leopold III tunnel (Brussels)

28

tal ratio stood at 23.1% and remained well

above the industry average, taking into ac-

count the acquisition of the stake in JM Finn

and the long-term commitment to buy out

minority shareholders in JM Finn.

Bank J.Van Breda & C° (AvH 78.75%)

again showed a strong financial performance

in 2012. As a result of a constant inflow

of funds, the total client assets (incl. ABK)

grew by 7% to 8.0 billion euros (2011: 7.5

billion euros, 7 months ABK), of which 3.4

billion euros client deposits and 4.6 billion

euros entrusted funds. After a 20% volume

growth in 2011, client deposits stagnated in

2012. The 14% increase in entrusted funds

is due to the inflow of additional funds and

the excellent financial performance of the

assets under management. Of these, 2.5 bil-

lion euros is managed by Delen Private Bank.

Aslo the loan volume from the banking core

clients increased further to 2.9 billion euros,

while provisions for loan losses remained

very low (0.08%).

The consolidated net profit for 2012

amounted to 27.7 million euros, compared

to the normalized net result of 26.4 million

euros in 2011. The cost - income ratio stood

at 58% (61% in 2011). The consolidated

equity (group share) increased from 395.0

million euros to 427.3 million euros. This

equity solidifies the bank’s position to sus-

tain its steady growth on a sound financial

footing. Furthermore, the bank already sat-

isfies the solvency criteria which the Basel III

agreement will implement, with a financial

leverage (assets-to-equity ratio) of 9 and a

Core Tier 1 capital ratio of 14.2%.

At the end of 2012, ABK took the opportu-

nity to exit from the Beroepskrediet statute,

subject to payment of an extraordinary con-

tribution of 60.1 million euros, with only a

limited impact on its equity position. This en-

ables it to roll out the strategy of asset man-

ager in a more flexible way and to organ-

ize the partnership between ABK and Bank

J.Van Breda & C° as efficiently as possible.

Real Estate, Leisure & Senior Care. The

active management of Leasinvest Real Estate

led to a growth of its real estate portfolio

and net profit. The development activities of

Extensa and Groupe Financière Duval, how-

ever, had a negative impact on the contribu-

tion to the group results.

Due to the delay of various permits and the

poor economic climate in Romania, Extensa

(AvH 100%) made a loss in 2012 of 5.3 mil-

lion euros, of which 3.2 million euros in im-

pairments and exchange losses.

The group sold some land at a profit and

successfully continued the sale of its prop-

erty developments in Roeselare, Hasselt and

Istanbul. In Wallonia, Extensa is actively in-

volved in three real estate promotion pro-

jects, which will contribute to the results

within a few years.

The permit for the construction of a pas-

sive office building on the Tour & Taxis site

(Extensa 50%) in Brussels was obtained in

July 2012, and construction works have be-

gun. The building will be completed in 2014

along with a new public car park. Construc-

tion works on the Grossfeld site in Luxem-

bourg (Extensa 50%) couldn't start yet,

which meant that the projected results could

not be realized in 2012.

Strategically, 2012 was a crucial year for

Leasinvest Real Estate (LRE, AvH 30.01%).

Firstly, significant investments made the

Grand Duchy of Luxembourg the main in-

vestment market for LRE (53% of the real

estate portfolio, compared to 47% in Bel-

gium); secondly, the share of retail increased

substantially in the split of the portfolio by

type of building (offices 47%, retail 29%,

and logistics 24%).

The fair value of this real estate portfolio, in-

cluding project developments, stood at 618

million euros at the end of the year (com-

pared to 504 million euros at 31/12/2011).

This 22.5% increase is primarily the result

of the investments in the Knauf shopping

centre, the Rix Hotel (both in Luxembourg),

and the State Archives in Bruges. As a result

of these major investments, rental income in

2012 increased to 38 million euros (36.6 mil-

lion euros at the end of 2011).

As a result of the new (re)lettings and the

fully let investments, the average duration of

the portfolio increased to 4.9 years and the

occupancy rate rose from 92.57% (2011) to

nearly 95%. In June, 100% of the logistical

premises of Canal Logistics (Brussels) were

occupied as a result of new lettings; in De-

cember, a major lease and services agree-

ment was concluded for 2,300 m² in the

building The Crescent (Anderlecht), raising

its occupancy rate to 62.5%.

The rental yield, calculated on the fair value,

was 7.30% at 31/12/2012 (2011: 7.23%),

and the debt ratio increased to 56.19%

(47.29% at 31/12/2011). Leasinvest Real

Estate ended 2012 with a higher net result

of 20.5 million euros (2011: 12.6 million eu-

ros), thanks to increased rental income and

the absence of negative value adjustments

on the portfolio.

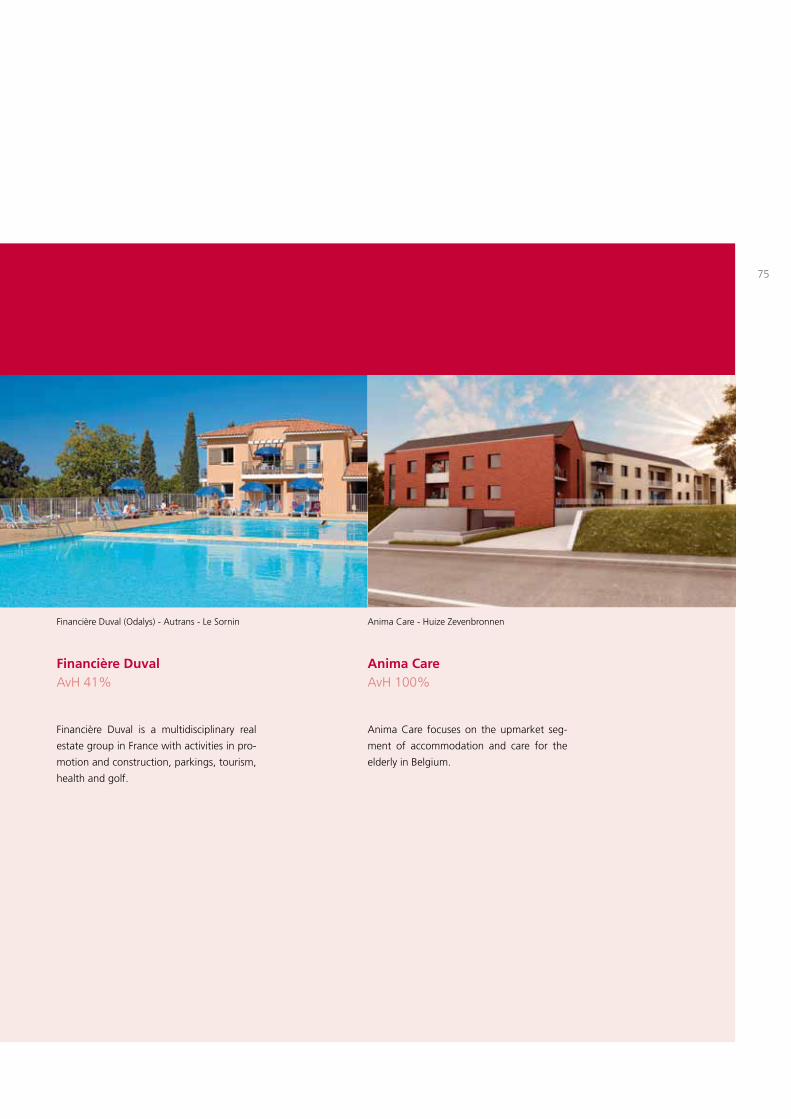

Groupe Financière Duval (AvH 41.14%)

realized a lower net result in 2012 (3.9 mil-

lion euros compared to 6.6 million euros in

2011), despite a substantial increase (+19%)

in turnover to 514 million euros. The pro-

motion activities witnessed a delay in the

permitting procedure for certain projects, as

well as exceptional losses in project manage-

ment. The exploitation activities (Odalys holi-

day parks, Résidalya retirement homes, and

NGF golf) continue to make the biggest and

fairly constant contribution to the operating

results of the Duval group.

Energy & Resources. After the record year

2011 with very high market prices, Sipef

stands firm thanks to the increase of the

production volumes of palm oil and rubber.

Plantation group Sipef (AvH 26.69%) real-

ized rising production volumes in 2012 for

the four basic products palm oil, rubber, tea

and bananas. This growth is attributable to

favourable weather conditions, greater ma-

A n n u a l r e p o r t 2 0 1 2

29

turity of the plantations, and newly devel-

oped acreage.

A lower demand for palm oil from China

and the biofuel industry, combined with

higher production volumes in the main pro-

ducing countries, resulted in higher stocks in

the second half of the year and had an im-

pact on palm oil pricing. Coupled with rising

costs as a result of local inflation and higher

labour costs, this had a negative impact on

operating results.

The turnover stood at 333 million USD (368

million USD in 2011), while the net result

decreased by 28% to 68.4 million USD com-

pared to the record year 2011 (95.1 million

USD).

Despite a delay in the implementation of

the expansion plans in Papua New Guinea

and Indonesia as a result of sustainability

procedures and technical limitations, 1,790

hectares were added to the planted acreage

of the group. This acreage has now topped

65,000 hectares, of which more than 20%

has not yet reached the production stage.

Development Capital. The contribution

from the Development Capital segment was

encumbered by the non-recurring results of

Hertel. Thanks to the capital gains from the

sales of AR Metallizing and Alural Belgium,

this segment had a larger contribution to

the group result. The results of the different

participations in this segment are described

from page 98 onwards.

3. Key events after the closing of the financial yearOn 16 January 2013, Sofinim and NPM Capi-

tal contributed to a substantial refinancing of

Hertel by way of a cash injection of 75 mil-

lion euros (Sofinim 37.5 million euros). This

has laid the foundations for an upturn in the

results, and at the same time served to dras-

tically reduce Hertel’s net financial debt to

27.6 million euros.

On 25 January 2013, AvH announced that

Sofinim has agreed to sell its 72.92% stake

in Spano Invest to the Unilin group. The

transaction, which is subject to the approval

of the competition authorities and to other

customary conditions precedent, is expected

(depending on the timing of the closing) to

result in a capital gain of more than 30 mil-

lion euros.

On 25 January 2013, DEME successfully is-

sued a retail bond of 200 million euros. These

debentures yield a gross interest of 4.145%

and are quoted on Alternext Brussels.

4. Research and developmentThe fully-consolidated group companies of

Ackermans & van Haaren did not engage in

any significant research and development

activities in 2012.

5. Financial instrumentsWithin the group (a.o. Bank J.Van Breda &

C°, Leasinvest Real Estate, DEME, Extensa),

an effort is being made to pursue a cautious

policy in terms of interest rate risk by using

interest swaps and options. A large number

of the group’s companies operate outside

the euro zone (for example DEME, Delen

Investments, Sipef, Hertel, Manuchar, Tele-

mond Group). Hedging activities for ex-

change rate risk are always carried out and

managed at the level of the individual com-

pany.

6. OutlookNotwithstanding a limited view of how the

economy will evolve in 2013, the board of

directors expects an improvement in the net

result.

Leasinvest - Canal Logistics (Neder-over-Heembeek) Sipef - Fresh palm fruit bunches entering the oil mill

30

III Corporate governance statement

1. GeneralAckermans & van Haaren has adopted the

Belgian Corporate Governance Code (the

‘Code’), as published on 12 March 2009, as

its reference code. The Code can be consult-

ed on the website of the Corporate Govern-

ance Committee (http://www.corporategov-

ernancecommittee.be).

On 14 April 2005, the board of directors of

Ackermans & van Haaren adopted the first

Corporate Governance Charter (‘Charter’).

The board of directors has subsequently up-

dated this Charter several times:

• On 18 April 2006, the Charter was aligned

to various Royal Decrees adopted pursuant

to European regulations on market abuse;

• On 15 January 2008, the board of directors

amended article 3.2.2. (b) of the Charter

in order to clarify the procedure regarding

investigations into irregularities;

• On 12 January 2010, the Charter was

modified to reflect the new Code and the

new independence criteria set forth in Arti-

cle 526ter of the Companies Code;

• On 4 October 2011, the board of direc-

tors deliberated on the adaptation of the

Charter to the Act of 6 April 2010 on the

reinforcement of corporate governance in

listed companies and the Act of 20 Decem-

ber 2010 on the exercise of certain share-

holders’ rights in listed companies. On this

occasion, the board of directors also tight-

ened its policy on the prevention of market

abuse (Section 5 of the Charter) with the

introduction of a prohibition on short sell-

ing and speculative share trading.

The Charter is available in three languages

(Dutch, French and English) on the company’s

website (www.avh.be).

This chapter (‘Corporate Governance State-

ment’) contains the information as referred

to in Articles 96, §2 and 119, second para-

graph, 7° of the Companies Code. In accord-

ance with the Code, this chapter specifically

focuses on factual information involving cor-

porate governance matters and explains any

derogations from certain provisions of the

Code during the past financial year in accord-

ance with the principle of ‘comply or explain’.

31

Board of directors - from left to right: Pierre Macharis, Pierre Willaert, Teun Jurgens, Julien Pestiaux, Jacques Delen, Luc Bertrand, Frederic van Haaren, Thierry van Baren

Jacques Delen (born 1949, Belgian) com-

pleted his studies as a stockbroker in 1976.

He is chairman of the executive committee

of Bank Delen and a director with the listed

agro-industrial group Sipef and with Bank

J.Van Breda & C°. Jacques Delen was ap-

pointed director at Ackermans & van Haaren

in 1992 and has been chairman of the board

of directors since 2011.

Luc Bertrand (born 1951, Belgian) is chair-

man of the executive committee of Acker-

mans & van Haaren. He graduated in 1974

as a commercial engineer (KU Leuven) and

began his career at Bankers Trust, where

he held the position of Vice-President and

Regional Sales Manager, Northern Europe.

He has been with Ackermans & van Haaren

since 1986. He holds various mandates as

director within and outside the Ackermans

& van Haaren group. His mandates include

being chairman of the board of directors

of DEME, Dredging International, Finaxis,

Sofinim and Leasinvest Real Estate and he

is a director at Sipef, Atenor Group and

Groupe Flo. Outside the group, Luc Bertrand

holds mandates as director at Schroeders

and ING Belgium. Luc Bertrand is also ac-

tive at the social level and is, among other

things, chairman of Guberna (the Belgian

Governance Institute) and Middelheim Pro-

motors, and sits on the boards of several

other non-profit organizations and public

institutions such as KU Leuven, de Duve

Institute, Institute of Tropical Medicine and

Museum Mayer van den Bergh. Luc Bertrand

was appointed director at Ackermans & van

Haaren in 1985.

Teun Jurgens (born 1948, Dutch) gradu-

ated as an agricultural engineer at the Rijks

Hogere Landbouwschool in Groningen (The

Netherlands). He was a member of the man-

agement team of Banque Paribas Nederland

and founder of Delta Mergers & Acquisi-

tions. Teun Jurgens was appointed director

at Ackermans & van Haaren in 1996.

Pierre Macharis (born 1962, Belgian) com-

pleted a master’s degree in commercial and

financial sciences (1986) and also earned