Embed Size (px)

DESCRIPTION

Alpha Investment Management Alpha Portfolio Constructor Alpha uses a pragmatic not idiosyncratic approach to portfolio construction. It is robust and built around the realities of the benchmark. It is disciplined and ensures that each stock is held at a sensible weight within the portfolio. Topics: Understanding the shape of the market. Big Cog / Little Cog From Research to Portfolio - "Which stocks", "When" and "What weight" Risk overlays

Citation preview

Alpha Investment Management

Alpha Portfolio Constructor

October 1999

Alpha Investment Management 2

Table of Contents

Summary ............................................................................................................................................................................ 3

Understanding the shape of the market. ......................................................................................................................... 3

Big Cog / Little Cog ........................................................................................................................................................... 4

From Research to Portfolio - "Which stocks", "When" and "What weight" ................................................................. 4

"What weight" - The language of the Alpha Portfolio Constructor ............................................................................... 5

Risk overlays ..................................................................................................................................................................... 5

Alpha Investment Management 3

Summary

Alpha uses a pragmatic not idiosyncratic approach to portfolio construction. It is robust and built around the

realities of the benchmark. It is disciplined and ensures that each stock is held at a sensible weight within the

portfolio.

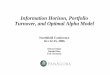

Understanding the shape of the market.

The Australian market is concentrated

Cumulative All Ords Weight

11 Stocks equals 52% of the market

69 Stocks equals 90% of the market

40 Stocks equals 80% of the

market

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

0 10 20 30 40 50 60 70 80 90 100 110Number of stocks

Pe

rce

nta

ge

of

All O

rdin

ari

es

(%

)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

All O

rdin

ari

es

we

igh

t (%

)

All Ords weight Cumulative All Ords weight

One of the key realities that feed into portfolio construction is the shape of the

market. No portfolio construction model is complete without reference to the

"Big Cogs" in the market. This does not mean they need to be in the portfolio,

but the benchmark risk of excluding "Big Cogs" must be understood. The

diagram above shows that 11 companies represent 52% of the market by

capitalisation, but only 4% by number of the 272 companies that compose the

ASX All Ordinaries benchmark.

Alpha Investment Management 4

Big Cog / Little Cog

Alpha uses the terms "Big Cog" and "Little Cog" to classify stocks within

the benchmark. As can be seen from the diagram below, the Telstra

Corporation Limited share price moved from $9.15 and $7.36 between

the 1st February 1999 and the 5th May 1999. This is the equivalent of

the entire market capitalisation of Woolworths Limited. A 30 cent move

in the Telstra share price has the same benchmark impact as a 100%

move in Seven Network Limited.

Why the big stocks are so important

Telstra Corporation Ltd Price move from $9.15 down to $7.36

(1-Feb-1999 to 5-May-1999)

2nd

Southcorp30th Largest Company

73rd

63rd57th

39th

18th

7.15

7.35

7.55

7.75

7.95

8.15

8.35

8.55

8.75

8.95

9.15

Te

lstr

a (

$9

.15

to

$7

.36

)

Wo

olw

ort

hs -

$6

,37

5 B

ill

Qa

nta

s -

$5

,85

8 B

ill

Am

co

r -

$5

,32

8 B

ill

Co

lon

ial -

$5

,13

4 B

ill

St G

eo

rge

Ba

nk -

$5

,06

0 B

ill

Co

ca

-co

la -

$5

,02

7 B

ill

CS

R L

td -

$4

,92

0 B

ill

We

stfie

ld H

ldg

s -

$4

,89

7 B

ill

We

stfie

ld T

rust -

$4

,84

6 B

ill

Co

ma

lco

- $

4,3

17

Bill

Na

tion

al M

utu

al -

$4

,14

2 B

ill

Ge

n P

rop

Tru

st -

$3

,74

7 B

ill

So

uth

co

rp -

$3

,63

0 B

ill

We

sfa

rme

rs -

$3

,58

9 B

ill

Pio

ne

er

- $

3,5

60

Bill

Fa

irfa

x -

$3

,41

2 B

ill

Ta

bco

rp -

$3

,34

0 B

ill

Sa

nto

s -

$3

,28

9 B

ill

Ma

cq

ua

rie

Ba

nk -

$3

,26

0 B

ill

AG

L L

td -

$3

,09

7 B

ill

Bo

ral -

$3

,01

2 B

ill

Ha

rve

y N

orm

an

- $

2,8

25

Bill

Ja

me

s H

ard

ie -

$1

,78

0 B

ill

Le

igh

ton

- $

1,5

18

Bill

Se

ve

n -

$1

,10

0 B

ill

Te

lstr

a p

ric

e r

an

ge

From Research to Portfolio - "Which stocks", "When" and "What weight"

The path to portfolio construction becomes a question of "which stocks"

are suitable for the portfolio, "When" does a stock enter or leave a

portfolio, and at "What weight" should that stock be held. The answer to

these questions occurs as part of the research process. Here

quantitative and qualitative information is bought together after extensive

research and rigorous valuation. A combination of a "Risk Adjusted Rate

of Return" (RARR) coupled with the reality of the benchmark leads to a

language which feeds into the Alpha Portfolio Constructor.

Alpha Investment Management 5

"What weight" - The language of the Alpha Portfolio Constructor

♦ "not included"

Do not like the stock, hold at zero weight. Applies to "Big Cogs" and "Little

Cogs".

♦ "included less"

Not as good as other stocks in the portfolio. Hence underweight a "Big Cog"

and do not have to be invested in a "Little Cog" as no market impact.

♦ "included"

If we like all stocks in the portfolio equally, then logical mechanism for

spreading excess above portfolio market weight.

♦ "more"

We like the stock more than other stocks in the portfolio.

♦ "much more"

We like the stock much more than other stocks in the portfolio.

Other overrides

♦ "index"

This is used rarely for "Big Cogs" which have no clear direction or valuation.

This is not a core component of the Alpha Portfolio Constructor language,

but is a necessary evil required when a "Big Cog" is subject to large event

risk.

♦ Short-term tactical overrides

Tactical overrides occur during entry and exit of a stock or when taking large

short-term conscious bets outside the standard model.

Risk overlays

Alpha Investment Management has a series of risk overlay tools. These

include a sector view of the decision making by the Alpha Portfolio

Constructor. This is to ensure no unconscious sector bets are taken.

Sectors of particular interest are Banks, Resources, Insurance, and

Property Trusts.

Another tool that Alpha uses is the Advantage research database, which

gives amongst other things details on sensitivity of valuations to bond

yield direction and change.

The Alpha Risk Analyser allows Alpha to apply different paradigms to

the portfolio in both traditional "tracking error" breakdown and weight

exposure. Paradigms may include ASX Sectors, Large stocks versus

Small stocks, Growth versus Value, Industrial/Resources split, Alpha

defined sector exposure, or potentially financial factors based on the

extensive Advantage database.