Embed Size (px)

Citation preview

Topic 1INTRODUCTION 1.1.0 Background Early Auditing (Vouching Audits) Auditing began as a vouching process and developed from the word audire, which means to hear. In early Audits, an auditor was supposed to conduct vouching audit, which implied checking all transactions so as to detect errors and frauds, which as of then was the main objective of an audit. Under this process the auditor was supposed to prove the true and correct view of company’s financial affairs, which necessitated checking all the transactions, it was possible because transactions were few and could be audited in one single session. Modern Auditing (system based audits)These audits were introduced mainly after 1948. Under these audits, the auditors are expected to rely on the presence and strength of internal control system of the organization. In this case the auditor will apply tests on a sample of entries drawn from population of entries and results of the sample are taken to represent those of the entire population. Such audits were necessitated by the fact that transactions of many organizations increased, making it difficult for an auditor to check for all of them in one session thus the need for sampling. This also meant that the auditor would no longer prove the true and correct view but rather the true and fair view of company’s financial state of affairs.1.2.0 Definition of AuditingAuditing is an independent examination of books of accounts and underlying documents of an enterprise by a qualified auditor so as to ascertain: -

Whether the enterprise has kept proper books of accounts as per requirements of the Company Act

Whether financial statements agree with contents of accounts and Whether such statements portray the true and fair view of company’s state of

affairs as at a given date. Key issues in the above definitions 1. IndependenceAn auditor is an independent person and he should portray an independent attitude during his/her examinations so as to achieve objective reporting.It benefits the owners i.e. shareholders and third parties e.g. government, donors, creditors etc. in that it helps the auditor to form an unbiased opinion hence credible financial statements. The profession for that reason has given auditors guidelines to ensure that such independence is observed both during the practice and outside the practice. For this reason an auditor should not:

a. Give loans to or get from 3rd parties or owners who will use his opinions. b. He shouldn’t have blood relations with parties who will use his report. c. He shouldn’t have any interest in the clients company in form of shares,

etc. 2. Opinion The end product for auditors’ examination is an expression of an opinion by the auditor. The auditors’ opinion might be negative, technically known as a qualified opinion or it may be positive, technically known as unqualified opinion. 3. Financial Statements

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 1

These include balance sheet, Profit and loss account, cash flow statements, etc. These are statements on which the auditor has to form an opinion as to whether they show a true and fair view of the company’s state of affairs. 4. Underlying documents These are documentary evidence in support of transactions in the books of accounts e.g. receipts. From vouchers, the auditors try to ascertain whether;

The transactions are for the current financial period.( cut off test) They are for the particular company in question (Client Company). They are properly authorized. Properly recorded according to generally accepted accounting principles GAAP.

5. True and Fair View True and fair view implies that the company’s financial statements, assets or liabilities profit or loss reflects the exact picture of the company’s financial performance. Objectives of an Audit These are categorized into three;

i. Statutory objectives ii. Professional bodies requirements

iii. Incidental objectives iv. Corporate governance objective

\1. Statutory Objectives i). To prove the true and fair view or otherwise, of the company’s financial state of affairs. This implies that an auditor must certify the company’s financial position at the end of the audit as to whether financial statements portray a true and fair view.ii). The auditor is supposed to ascertain whether the company has kept proper books of accounts which should be in agreement with the financial statements e.g. cashbook, ledgers, Journals, Asset registers, etc.iii). The company Act requires the auditor write a report at the end of his/her audit in which he should communicate his findings out of his examination. 2. Professional Bodies RequirementsThese require the auditor to give advice to the company in the letter of weaknesses or management letter in which the auditor endeavors to highlight problems in the internal control systems; budgetary controls etc. 3. Incidental Objectives An auditor has to detect material errors and frauds so that affect the true and fair view of the company’s state of affairs. However this duty is the role of the company’s management and thus incidental to the auditor. 4. Corporate governance objective There have been an increasing number of companies failing as a result of mismanagement. There is therefore a new call for auditors to report on how companies are managed, controlled and directed by those charged with their governance in any statutory audit. 1.4.0 The Auditors Rights and Duties The auditor has various detailed duties to perform in order to achieve the overall duty to report a True and Fair view of the company’s state of affairs. In order to fulfill these duties various legal rights are given to the auditor. Duties of an Auditor (S. 162)

1. To report on the financial statements to form an opinion as to:-

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 2

o Whether they have obtained all information and explanations necessary for the audit.

o Whether in their opinion, proper books and returns have been kept. o Whether the balance sheet and profit and loss account are in agreement

with the books of accounts of accounts and returns. o Whether the accounts have been prepared in accordance with the Act or

firms constitution. o Whether the director's report is consistent with the accounts. o Whether the financial statements show a true and fair view. 2. To qualify the report if the above in (1) are not satisfied. 3. To consider whether the information in the management report

(management representation) is consistent with the financial statements. 4. To include additional information in the report connected with the director's

remuneration and loan to officers, in case it is not provided in the accounts. Rights of an Auditor (S. 162)The rights given to the auditor under national legislation are designed to ensure that he is able to fulfill his duties and responsibilities to the members. These include:-

1. Access to records, books of accounts, and documents at all times. Never use force or seek court redress when refused access. Simply resign or qualify the report.

2. To get information and explanations from officers necessary for the audit. 3. To attend or get notices of meetings like any shareholder. 4. To speak at the General Meetings as an auditor. 5. To get information from branches or subsidiaries. 6. To get written resolutions proposed. 7. To remuneration if he has completed his work. 8. To sign the audit report. 9. During removal - make representations to shareholders, attend and speak at the

meeting where he is being removal etc. 1.5.0 Parties Who Benefit From Audited Accounts 1. Creditors/Suppliers These use audited accounts to ascertain the company’s ability to meet their short-term obligations as and when they fall due. Also if these are long term suppliers they will use audited accounts to assess the company’s long-term liability. 2. Customers/Debtors These are interested in company’s long term survival to ascertain whether the company can fulfill their long term interests e.g. depositors <->bank. 3. Bankers These use audited accounts to ascertain whether the company can settle their short-term obligations such as bank over drafts and short-term loans, and long-term obligations such long-term loans. 4. Government The government is interested in audited accounts to ascertain tax liability public goods. 5. Competitors These are interested in company’s profitability and market share and how they can compete favorably for the markets. 6. Share holders/investors

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 3

These use audited accounts to check the capability of the organization in paying their dividends fully and on time. 1.6.0 Advantages of Audit

1. An audit gives assurance and credibility to the accounts for the benefit of potential investors. The investors utilize audited accounts to ascertain company’s performance.

2. Audited accounts are used to detect errors and frauds, which could otherwise lead to the failure of the organization.

3. Auditing of accounts enables accounting staff to keep their accounts to date and acts as a source of management information upon which decisions will be made.

4. Audited accounts are used by organizations to raise funds from different financial institutions.

5. Audited accounts are used by income tax authorities to assess or ascertain company’s liability and as such avoids any possible disputes between the company and income tax department/authorities.

6. In case of sale of business, a merger businesses acquisition or take over of business, audited accounts are useful as they indicate the fair value of assets to be acquired.

7. In case of partnerships the audited accounts are used; a). As a basis of sharing profits and thereby minimising disputes between partners.b). As a basis of distributing assets and liabilities amongst partners in the case of dissolution of partnership business.

Disadvantages of an Audit 1. It is usually a very expensive exercise because audit fees and audit

expenses is always too high especially for small companies. 2. If the result of the audit is bad (qualified), this can lead to the failure of the

business. 3. An audit may not be ideal for small business whose transactions are too

few. 4. An audit may not in most cases be in the interest of the owners especially

when these are managers in which case they end up frustrating the entire process etc.

5. Expectation gap- people always believe that the auditors work is detect errors and fraud.

1.7.0 Qualities of an Auditor 1. He should be a master of all fields of Accounting such as Financial

Accounting Cost Accounting, Management Accounting, Income Tax, etc. 2. He must be Honest - a person of unquestionable integrity 3. He must be able to ask intelligent questions in order to extract audit

evidence. 4. He must be independent i.e. he must not have interests in the firm he is

auditing. 5. He should grasp quickly the features of the organisation, e.g.

organisational structure, product line, size of the business etc. 6. He must be tactful so as to gather audited evidence according to his

opinion. 7. He should not reveal the secrets of his clients.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 4

8. The person should be accurate, vigilant and cautious during his course of audit work.

9. He must be able to document his opinion in an audit report .Ability to write a good report, which is concise and clear is a requirement.

1.8.0 Differences between Auditing and Investigation1. Auditing is carried out by Certified Public Accountants where as

investigation carried out by competent accountants. 2. Auditing is the examination of books of accounts to prove the true and fair

view where as an investigation is searching inquiry into the affairs of the organisation.

3. Auditing covers only one financial period where as investigations could cover more than one financial period.

4. Auditing is guided by professional ethics and guidelines where as investigations are not guided by any standard guidelines.

5. Auditing is conducted for stakeholders where as investigations are conducted for the owners of the organisation (investigation is conducted for particular people and for particular purpose while Auditing is done generally and carried for benefits of all stake holders).

1.9.0 Differences between Auditing and Accounting1. Auditing is an examination to firm’s financial statements with the view of

expressing true and fair view of the statements. On the other hand, accounting is simply the preparation of the books of accounts in order to aid the management in their decision making process.

2. Auditing is usually conducted at the end of the financial year while accounting is conducted through out the year i.e. it is a continuous process.

3. Auditing is guided by auditing standards and guidelines (ISAs) and supervised by professional bodies (ACCA). As for accounting, it is guided by accounting standards (IASs or IFRSs) and guidelines and supervised by management.

4. Auditing is performed by a qualified accountant where as accounting is conducted by any competent accountant.

5. Auditing is conducted not only for the owners but also other stake holders where as accounting is concluded by management.

6. Auditing is conducted using tests as an aid to the process of auditing where as accounting is conducted using vouchers, various books of accounts e.g. Journals, ledgers etc.

7. Auditing is based on accounting information which implies that accounting has to be done first and auditing follows.

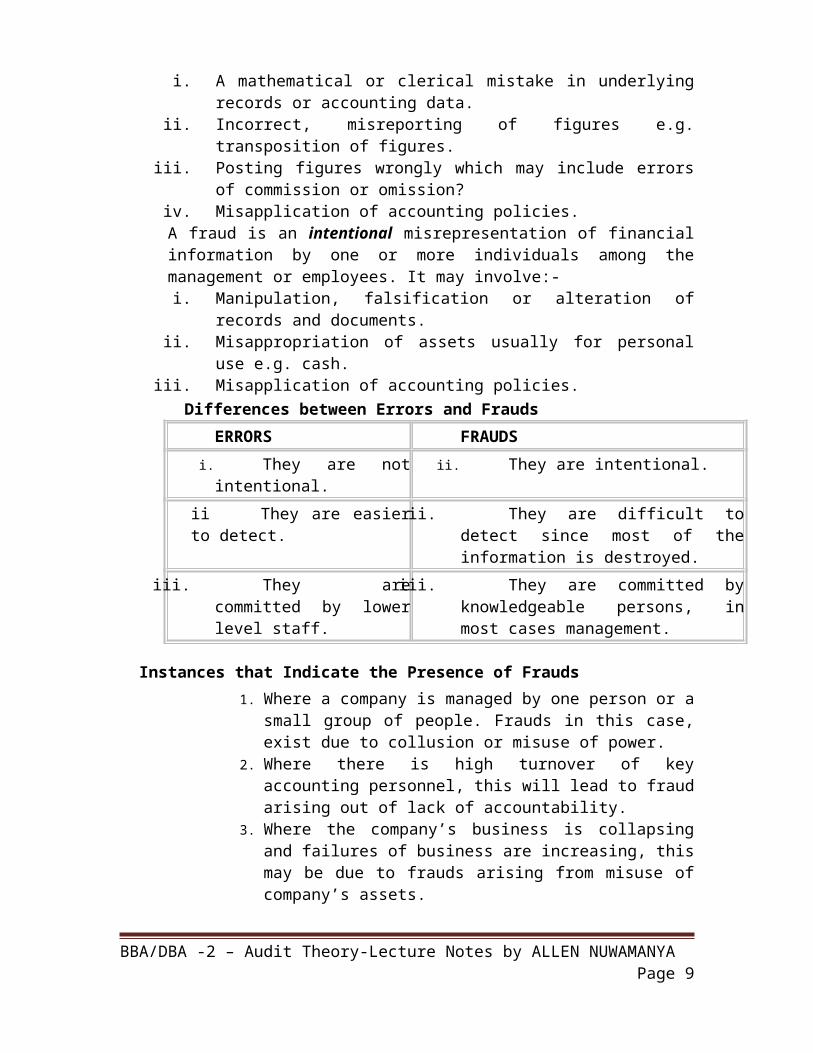

1.10.0 ERRORS AND FRAUDS ISA 240 Frauds and errors states that: An error is an unintentional mistake in financial information such as:-

i. A mathematical or clerical mistake in underlying records or accounting data.

ii. Incorrect, misreporting of figures e.g. transposition of figures. iii. Posting figures wrongly which may include errors of commission or

omission?

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 5

iv. Misapplication of accounting policies. A fraud is an intentional misrepresentation of financial information by one or more individuals among the management or employees. It may involve:-

i. Manipulation, falsification or alteration of records and documents. ii. Misappropriation of assets usually for personal use e.g. cash.

iii. Misapplication of accounting policies. Differences between Errors and Frauds

ERRORS FRAUDSi. They are not

intentional. ii. They are intentional.

ii They are easier to detect. ii. They are difficult to detect since most of the information is destroyed.

iii. They are committed by lower level staff.

iii. They are committed by knowledgeable persons, in most cases management.

Instances that Indicate the Presence of Frauds 1. Where a company is managed by one person or a small group of

people. Frauds in this case, exist due to collusion or misuse of power.

2. Where there is high turnover of key accounting personnel, this will lead to fraud arising out of lack of accountability.

3. Where the company’s business is collapsing and failures of business are increasing, this may be due to frauds arising from misuse of company’s assets.

4. The evasive or unreasonable response of management to audit questions may be due to cover up of fraud.

5. Transactions between related parties whether they are related by blood, financial relations or by associations. These collude to cover up frauds.

6. Where there is inadequate working capital to support the companies capital requirement e.g. cash.

Detection of FraudsIt’s not the duty of the auditor to detect frauds as per ISA (International Standards of Auditing) It is the duty of management which must institute a strong internal control system. However auditors must be aware of the risks of frauds if they are to prove true and fair view of company’s financial statements. Therefore the detection of frauds is an incidental duty of auditors. This may be done by the use of following; 1). Analytical reviews These are reviews, which involve the computation of key ratios, percentages, average and investigation of any unfavourable variances or differences.

2). Surprise checks The auditor may use surprise checks on items such as petty cash, stock etc.

3). Third party confirmation (Circularisation)

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 6

This is where circulars are given to creditors and debtors to fill. The replies from these parties are then compared to company’s own record and the differences investigated.

4). Searching inquiry This is an investigation carried out in areas suspected to have frauds e.g. cash, wages payments etc.

5). In depth Auditing (vouching)This is an initial examination of selected transactions, which are checked from initial stages to final stages.Prevention of Frauds This can be done through the following ways:

1. Through routine checking and balancing of accounts. 2. Institute strong division (Segregation) of duties in preparation and

interpretation of accounting information. 3. To give reasonable salaries and benefits to employees according to their

qualification experience and sensitivity of their jobs. 4. Employment of qualified staff to handle technical areas or sensitive area

of an organisation. 5. Institute periodical comparisons of the budgeted and actual situations. 6. To use where possible computerized accounting systems so as have

accounts that are computerised. 7. Clear job descriptions which involves allocation of jobs and functions

such that personnel responsibility is clearly defined.

Detection of Errors

This can be done through the following ways: 1. Use of comparative figures e.g. current years figures against previous

figures and investigation carried out, in case of unfavourable variances. 2. The auditor should trace the names of accounts from various ledgers to the

Trial balance and ensure that no account was left out in the positing process.

3. He should count accounts or items in the current trial balance and compare them with those of previous year’s trial balance and then investigate the differences.

4. The auditor should check the total of balances and find out if there are any differences.

Prevention of Errors Errors may be prevented as follows:

1. The organization or the company should employ qualified staff within the technical field.

2. Use of mechanized accounting systems. 3. Use of closer supervision of staff over managing sensitive jobs. 4. Use of surprise checks of items subject to errors such as cash and ledger accounts. 5. Use of automatic transfers or rotation of duties in order to cut continuity of errors

perpetrated.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 7

TOPIC 22.0.0 TYPES OF AUDITSAudits can be classified in two ways, i.e.

a. According to the nature of work done. b. According to the approach to the work to be done.

2.1 0 According to the nature of work done.By this classification, the nature of work may be statutory or private, hence resulting to statutory audit or private audit 2.1.1 Statutory AuditThese are audits that are conducted as per the requirements of the Company Act and hence they are mandatory. This type of audit is carried out for limited companies. I.e. public or private ltd. It is conducted by an auditor appointed as per the Company Act.The objective of such an audit is to prove the true and fair view of the organization. Statutory audits are done at the end of a financial year and the report produced is addressed to the shareholders.In this case, the duties and rights of an auditor are defined by the Company Act. The auditor performs pure audit work. 2.1.2 Private AuditThese are audits that are carried out as per the wishes of the directors or owners of the business hence they are not mandatory. Private audits are carried out for organisations such as partnerships, clubs, NGOs, sole traders etc, however; the owner of the business does the appointment of auditors. The objective of such an audit is to detect errors and frauds, and to ascertain profits for tax purposes. These audits can be done anytime during the financial period, and the report produced is addressed to the stakeholder. The owners of the business define the duties and rights. The auditor may perform both auditing and accountancy.Similarities between statutory and private audits

o Both are carried out by Certified Public Accountants. o Both are carried out using auditing guidelines and standards. o In both cases, the auditors may provide management advisory services to

the clients. o In both cases, reports are used as bases for decision-making o In both cases, reports are used by income tax authorities and financiers in

determining performance. o In both cases, the audits will boost the morale of the accounting staff to

keep their accounts up to date. 2.2.0 According to the approach of work to be done. These include: -

a. Continuous audit b. Interim audit c. Procedural audit d. Management audit e. Final audit/complete/detailed

2.2.1 Continuous Audit

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 8

These are audits, which involve detailed examination of books of accounts at regular intervals of say three to four months. Such audits are ideal for:-

i. Banking businesses where by virtue of their transactions, the auditor has to conduct continuous audits to detect and prevent errors and frauds at their earliest stages.

ii. Companies whose volume of transactions is large and cannot be audited in one session e.g. manufacturing companies.

iii. Organisations whose internal control systems are weak. iv. Where the statement of accounts is required to be presented to the

management after every three or four months. Advantages of Continuous Audit.

1. Errors and frauds can be detected and prevented at their earliest stages before they have reached advanced proportions.

2. This audit will enable the auditor to have a sound technical knowledge of the business, which will help him in performing efficient audits.

3. This audit may boost the morale of accounting staff, who will keep their accounts up to date, lessen the possibility of committing frauds and hence facilitate the auditors’ work.

4. It enables the auditor to conduct his final audit efficiently because much of the audit work will have been tackled during the continuous audit and less will be left for the final audits.

5. This audit will facilitate the preparation of the management letter, since by virtue of his constant presence in the business he is able to understand it and give advice on the situation pertaining to the company.

Disadvantages of Continuous Audit1. The accounts figures audited may be altered by dishonest clerks in a bid to

perpetrate frauds. 2. It is time consuming and hence a tedious exercise on the part of the auditor. 3. It is an expensive audit because of the time used for a given audit assignment. 4. By virtue of his constant presence in the business, the client’s staff may get used

to the audit staff and this may affect the independence and objectivity of the audit staff leading to a biased opinion.

5. This type of audit will disorganise the clients’ work in so far as books of accounts will be used for audit purposes.

2.2.2 Interim AuditsThese are audits conducted to a particular date within the accounting period e.g. per quarter or half year, and hence form part of the final audit. These audits help to ascertain the company interim performance for the purpose of paying interim dividends. The conditions where these audits are ideal include:-

o Where a company is allowed by its Articles of Association. o Where a company by law is required to publish its interim performance for

the interests of the various parties. Advantages of Interim Audits

1. These audits are useful in the determination of the interim condition of the company. Therefore, the client will know the financial position of the company for the half-year and plan accordingly.

2. It enables the auditor to detect and prevent errors and frauds perpetrated in the interim period (at earlier stages).

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 9

3. This audit may boost the morale of accounting staff hence enabling them keep their work up to date, as accounts are checked at regular intervals.

4. It enables the auditor to assess the strengths and weaknesses of an internal control system, which is necessary for the final audit.

5. It entails less disruptions in the clients work as it is conducted mid financial period when the company accounts are mid way prepared.

6. Interim audit help to speed up the completion of final audit at the end of the financial period.

7. This audit is essential for the preparation of interim reports which are necessary for managerial decision making process in areas like:-

o -Raising additional funds for investment purpose. o -Ensuring that a company is operating within the laid down policies, etc

Disadvantages of interim audits1. Dishonest clerks with the intention to commit fraud may alter accounting figures

audited. 2. Errors and frauds detected at this time of the financial period may have reached

advanced stages, hence exposing the organization to serious losses. 3. This audit entails a lot of note taking. In other words, it will mean that the audit

staff will have to prepare notes after the interim audit e.g. interim balance sheet, records of forecasts, budgeted performance figures etc.

2.2.3 Procedural AuditsThese involve the examination and review of a company’s procedures and records so as to ascertain whether these are accurate, genuine and reliable for decision making purposes. These audits are ideal for the following conditions.

i. Businesses operating in dynamic situations and environment such as banks, hotels etc.

ii. Companies whose operations are so technical and need to be updated overtime e.g. motor vehicle industry.

iii. Companies with several procedures, which affect each other such that if one were inefficient, it would disrupt others.

Advantages of Procedural Audits1. This audit may reveal the procedures, which are not working as per laid down

policies and hence may be rectified. 2. This audit will identify procedures, which are not up to date, and this may be

scrapped off or be updated for the benefit of the organisation. 3. It will facilitate the reorganisation of procedures, which will enable the company

to alleviate procedures that lead to duplication of efforts and unnecessary high costs.

4. This audit will reveal procedures which do not have strong controls and these will be strengthened to enable the company to operate efficiently.

5. This audit will reveal procedures, which tend to be bureaucratic and measures then can be taken to rectify the situation. Usually, bureaucratic procedures lead to delay in operations hence inefficiency.

Disadvantages of procedural audits1. This audit is time-consuming and tedious in which case it may frustrate or delay

other audit assignments or engagements. 2. It is an expensive audit to conduct because the auditor will spend a lot of time to

ascertain failure of procedures.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 10

3. This audit may frustrate the top management because the failure of procedures is due to inefficiencies among the top management.

2.2.4 Management AuditThese are audits which involve investigations of the entire management aspects of a business e.g. decision making process, internal control systems, personal relationships with employees etc. The main purpose for this audit is to prepare a report on the effectiveness of the management from the point of view of the profitability and efficient running of the business.Advantages of Management Audits

1. It improves the quality of top management in terms of efficient management of resources, achievement of budgeted goals, effective management of time etc.

2. It reveals the weaknesses in the internal control systems, which is due to management failure to sustain such strong controls. This will also boost managerial supervision and motivation.

3. This audit minimizes bureaucracy in a company hence leading to efficient operations achieved through proper planning, faster implementations etc.

4. It will reveal the management’s weakness to operate a viable company e.g. failure in credit control policies, financial controls etc.

5. It does not disrupt the client’s work as it deals with human attributes for organisation, controlling and directing of human resources of the company.

Disadvantages of Management Audits1. It may lower the morale of the top management. 2. It may lead to biased reports because the attributes of efficiency are difficult to

measure. 3. The audit is time consuming if conducted for large company whose managerial

tasks demand constant reviews. 4. In case of organisation with many subsidiaries (branches) this audit may be

expensive as the auditor will have to visit each of the subsidiaries/branches to assess the efficiency of each manager in the light of the company’s total performance.

2.2.5 Final/ Complete/ Periodic AuditsThese are audits conducted at the end of the financial period, usually in one session and it is ideal for businesses which are small and whose transactions can be audited in one session. Advantages of Final Audits

1. It is easier to programme, plan and execute as it takes place in one single session at the end of the year.

2. It eliminates the possibility of alterations of figures, since it is the last audit. 3. It is a less expensive audit as compared to continuous audit because it demands

less time on the part of the auditor. 4. In final audits the auditor is able to give his client a balanced opinion and advice

based on the final circumstances. Disadvantages of Final Audits

1. If any fraud is committed and detected at the end of the financial period, it will have reached advanced stages, hence resulting to losses for the company.

2. It may be difficulty to conduct for large company.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 11

3. Due to time constraints, such audits may not be exhaustive so as to enable the auditor give a balanced opinion.

Revision Questions 1. Write short notes on the following:

i. Continuous audit ii. Interim audit

iii. Procedure audit iv. Management audits v. Final audits

2. Distinguish between statutory and private audits

TOPIC 33.0.0 AUDITORS APPOINTMENT AND REMOVAL

Most audit work is conducted for companies and is governed by the rules of the Company Act 1985 as amended by the Company Act 1989. Cap 110

3.1.0 Appointment of Auditors This can be done in the following ways:- a) Appointment by the Annual General Meeting (AGM) s.159

The Co Act requires that the auditors should be appointed by and therefore answerable to the shareholders. The general rule is that auditors are appointed by shareholders at the AGM and once appointed holds office till the next AGM.

b) Automatic AppointmentIn this case, a retiring auditor is deemed re-appointed without any resolution passed unless:-

o He is not qualified for reappointment. o It is stated that he shall not be reappointed. o He has given a notice in writing that he is unwilling to be re appointed.

c) Appointment by DirectorsThe directors may appoint the first auditors of a company before the AGM. They hold office till the first AGM. Shareholders may appoint the first auditors if the directors do not appoint one before the first AGM. The appointment by the directors is done under the following circumstances

o When delegated by shareholders o Before the first AGM o To fill the casual vacancy .

Casual vacancies may be created by death or incapacitation of the auditor. In such situations, the directors may fill any vacancies in the office of the auditor, however if such a vacancy is created by the resignation of the auditor, then such can only be filled by shareholders at a general meeting.

d) Appointment by the Registrar of CompaniesWhen no auditor has been appointed at the AGM, or in case the directors do not appoint the first auditor, the Co Act requires the company to inform the registrar within one week. The registrar may then make an appointment.

3.2.0 Remuneration of auditors s.159 The remuneration of auditors is fixed either by: - a) Whoever made the appointment, which could be: -

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 12

o The shareholder o The directors o The registrar of companies.

b) The company in a general meeting or in such a manner determined by the GM.Note: the auditors’ remuneration is fixed and it must be disclosed in the annual accounts of the company.

Removal of an auditor s. 160An auditor can only be dismissed by shareholders in a properly convened G.M. This safeguards his independence. An auditor can be dismissed at any time at the end of his term of office. This removal is by ordinary resolution at the meeting with special notice (28 days) having been served.

Removal Procedure. i. Special notice is needed for a resolution at the GM appointing another

auditor or expressly stating that the retiring one shall not be reappointed. ii. A copy of the notice must be sent to the retiring auditor.

iii. Where a retiring auditor makes written representations regarding the resolution, the shareholders should be sent copies of representations.

iv. If the representations are not sent, they should be read out in the meeting, unless the court has ruled it out.

v. The auditor has a right to defend himself at the meeting. N.B. Removal procedures allow members to appoint auditors of choice and it safeguards the auditors’ independence by not allowing directors to remove auditors. These procedures ensure that the auditor is not removed for improper reasons without the knowledge of the shareholders.

Reasons for removali. Disagreements on accounting policies, audit findings. Where

directors feel the auditor is taking unreasonable stance. ii. Rationalization – subsidiaries having one firm with the holding

company. iii. Incompatibility between management and auditor. iv. Threat to expose management fraud. Auditor threatens to expose

management fraud or curb management’s unrestricted use corporate resources (via additional disclosures for instance).

v. Incompetence of the auditor. vi. Change of ownership of the business.

vii. Change of requirements of the client firm e.g. after expansion.

Resignation of auditors An auditor may resign due to:

o Ill health o Expansion of the client firm o Inadequate fees o Management fraud etc.

Revision Questions1. Kent ltd was formed on 1st February 2000 in order to export roses to European markets. The directors are unsure as to their responsibilities, and the nature of

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 13

their relationship with the external auditors. The audit partner has asked you to visit the client and explain to the directors the more fundamental aspects of the accountability of the company and their relationship with the auditor.

Explain to the directors; a) Why there is need for an audit b) How the auditor of a public co. may be appointed under the Co. Act. c) What are the auditors’ rights?d) The responsibilities of the directors to the accounting function of the company. e) What are the statutory responsibilities of auditors?

2. An auditor must always approach his work with integrity and objectivity. The approach must be in a spirit of independence of mind.

Briefly explain the matters that may threaten or appear to threaten the independence of an auditor.

TOPIC 4 4.0.0 INTERNAL CONTROL SYSTEMS (ICS)Internal ControlsThese are processes affected by the entity’s board of directors, management and other personnel designed to provide reasonable assurance regarding the objectives of an organization. ISA 315; “Understanding the Entity and its Environment and Assessing the risk of material misstatements “, requires the auditor to perform risk assessment procedures to obtain an understanding of the entity its environment, including its internal controls. This standard defines Internal Control System as comprising of control environment and control procedures.It includes all the policies and procedures adopted by management to assist in the objective of achieving as far as practicable; the orderly and efficient conduct of the business. Control EnvironmentThis means the overall attitude, awareness and actions of directors and management regarding ICS and its importance to the entity. It encompasses personnel policies and procedures, organization structure etc.Control Procedures These are procedure established to achieve the entity’s objectives. These objectives may include proper authorization, timely and accurate recording of transaction in the correct period, safeguarding of assets etc. These procedures differ from entity of entity and depend on the size of the firm. Internal Control Systems may also be defined as:-“The whole system of controls, financial and otherwise established by the management in order to carry on business of the entity in an orderly and efficient manner, safeguard the assets and secure as far as possible the completeness and accuracy of the records.”4.1.0 Types of Internal Controls The types of Internal Controls can be categorized as; 1. Plan of the Organization / Organisation chart An organisation should have a preplanned organisation chart that should define;

a) Duties and responsibilities of each individual in the organisation. b) Responsibilities such that it defines lines of reporting for all operations within the

organisation.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 14

c) The flow of authority and responsibility, which should be clearly defined to avoid conflict in duties, authority and power.

d) How duties should be delegated in particular financial and accounting duties or assignments.

2. Segregation /Division of DutiesThis control means separation/division of duties and all responsibilities which if combined (i.e. not separated) will enable one single person to process and record the transactions from the beginning to the end hence exposing such persons to committing fraud. The main aim is to ensure that no one is responsible for the recording and processing of a complete transaction. 3. Physical Controls / Safeguarding of assetsThese aim at limiting accessibility of companies assets to authorized persons at authorized times. This control will take the form of physical measures which are also aimed at limiting direct access to assets using physical barriers e.g. being able to enter the warehouse. Or indirect limitations using documentation to company assets. 4. Authorisation and Approval ControlsThis is a control aimed at ensuring that all the company’s transactions are authorized by responsible officials whose limits of authority are defined such that they match transactions they authorise. Approvals should be segregated from authorisation e.g. all credit sales must be approved by the credit control department, all overtime must be approved by the works manager. 5. Arithmetic and Accounting ControlsThis is used to check the recording function in the organisation and to ensure that figures in the financial statements are not only genuine but also correct for accounting purposes. It requires the following measures:

a) Periodic reconciliation. b) Drawing the trial balance. c) Periodic balancing of accounts d) Control accounts, etc.

6. Personnel Controls/ competence of staff An ICS regardless of its application should be operated by personnel of integrity, competent and qualified to understand essence of the controls. Such people should have capabilities to carry out responsibilities assigned to them. It is normally achieved from the point of recruitment and retraining of staff. 7. Supervision. This has three levels. I.e.

a) Low level supervision. Such supervision should be manned by trained and competent supervisor who should supervise the company’s day-to-day operations such that they are carried out smoothly.

b) Middle level supervision. This is done by line managers who should ensure policies and procedures are adhered to and are in line with the company’s objectives and goals.

c) Managerial supervision and review. This is a management control done by the top management using such tools like budgets, standard costing statements, internal audit feed back, etc. All these aim at checking daily running of the organisation. It also involves reviews to ensure that all controls are working in harmony to achieve predetermined goals.

8. Rotation of duties and vacations.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 15

Duties of routine nature should be rotated to avoid continuity of errors and fraud and also as a means of avoiding routine boredom, which may lead to innocent errors. Employees should also be encouraged to take leave when it falls due. 9. Routine and automatic checks.Controls conducted on routine duties and operations are important in that they ensure that these operations are carried on efficiently and such controls are operated at a surprise basis to minimize errors and frauds. 10. Recording and record keepingThe system of recording the business transactions at all stages should be complete and reliable. The records should be kept properly to avoid any losses or alterations.NB. Any ICS should be operated at such a reasonable cost so as to enable the company derive maximum benefits which should out weigh the cost of installation and maintaining such system.Objectives of an Internal Control SystemThe main objectives of Internal Controls are to ensure that:-

1. The business is carried in an orderly and efficient way. 2. All business transactions take place according to set procedures. It means that the

management policies are followed strictly. 3. The assets are safeguarded properly. The acquisition usage, and disposal of assets

must be duly authorised and in accordance with the company policies. 4. The records are complete and accurate. It means that all incomes and expenses are

recorded adequately and correctly. These are maintained in such a way that the possibilities of errors and frauds are minimised.

5. The records provide adequate and reliable information for the preparation of financial statements.

Advantages of Internal Control Systems 1. It boosts the confidence and gives assurance to third parties or stakeholders in

running the organisations preparations smoothly. 2. It helps the auditor to obtain reliable evidence. 3. It strengthens the financial controls and prevents errors and fraud within the

organisation. 4. It boosts efficiency of staff by segregation of duties, use of qualified staff and

proper use of the organisation chart. 5. It helps the company to have accurate and correct records. 6. It minimizes the cost of an audit as it facilitates an audit through minimization of

errors and fraud. 7. It facilitates accurate decision-making processes with accurate information from

controls, which will lead to the growth of the company. 8. It enables the auditor to avail management with quality advice through the

management letter, which will facilitate the company’s operations. Disadvantages of Internal Control Systems

1. It is expensive to install and maintain especially in small organisations. 2. It may lead to over reliance on ICS by management team and thus reduce its

supervision and give room to perpetrators and frauds. 3. The integrity, competence and quality of management changes and this will lead

to changes in control.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 16

4. There is possibility that procedures may become inadequate due to changes in conditions and compliance procedures.

5. There is a possibility that a person responsible for exercising internal control could abuse that responsibility.

6. Most internal controls tend to be directed at routine transactions rather than non-routine transactions.

4.3.0 How the Internal Control Systems assist in detecting errors and frauds 1. Plan or the organisation chart.

o In defining the duties effectively, perpetration of frauds can easily be detected.

o Where powers conflict (duplication of efforts) such an area is grounds for errors and frauds.

2. Segregation of dutieso Segregation entails interchecking by superior colleagues thus errors and

frauds are identified with ease. o A person authorizing a transaction may want to perpetrate the fraud but

the executor may block the fraud. o A person keeping assets (storekeeper) can’t keep a fraudulent asset, which

has either been perpetrated by the executor or authorizer, as it is not a genuine business transaction. This is important because it prevents collusion between the authorizers, executors’ custodians and the recording parties.

3. Physical Control i.e. direct and indirect controls. o Indirect limitations (use of documentation) will give an idea of the

perpetration of frauds. This is achieved via the serialization of documents. o Physical barriers such as locked areas, strong rooms, safes etc. will show

actual frauds where there are shortfalls such as shortages and breakages. 4. Authorisation and approval controls

o Exceeding limits of authorisation will serve as a good indication of fraud. o Unauthorized transactions could be a sign of frauds.

5. Arithmetic and Accounting controls Trial balances not balancing should reveal

o Frauds and errors, o Excessive changes of accounting figures. o Out of balance account is an indication of frauds.

6. Supervisiono Supervisors are people of integrity thus will reveal frauds perpetrated to

avoid being victimized. o Managerial reviews, out of balance budget/ balance forecasts will give a

clue to frauds. o Where procedures are not adhered to due to relaxation of supervisor will

give room to frauds. 7. Personnel

o Qualified people will not normally allow frauds to pass their way. o Properly remunerated personnel will reveal frauds committed by lower

level employees under them. o High turnover of qualified personnel will serve as an indication of frauds.

8. Rotation of duties and vacations

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 17

o Once a person has been rotated, the incoming person will be able to detect any fraud if any. This also applies for a person gone for leave.

o Reluctance to be rotated or go for leave may indicate presence of frauds. 9. Routine and automatic checks

o Perpetrators of fraud are normally caught unaware with surprise checks. o Periodic, routine and automatic checks will detect errors and frauds

perpetrated. 10. Control over documents

o Missing pre numbered and serialized documents will reveal frauds. o Unauthorized documents or forged documents will also reveal frauds.

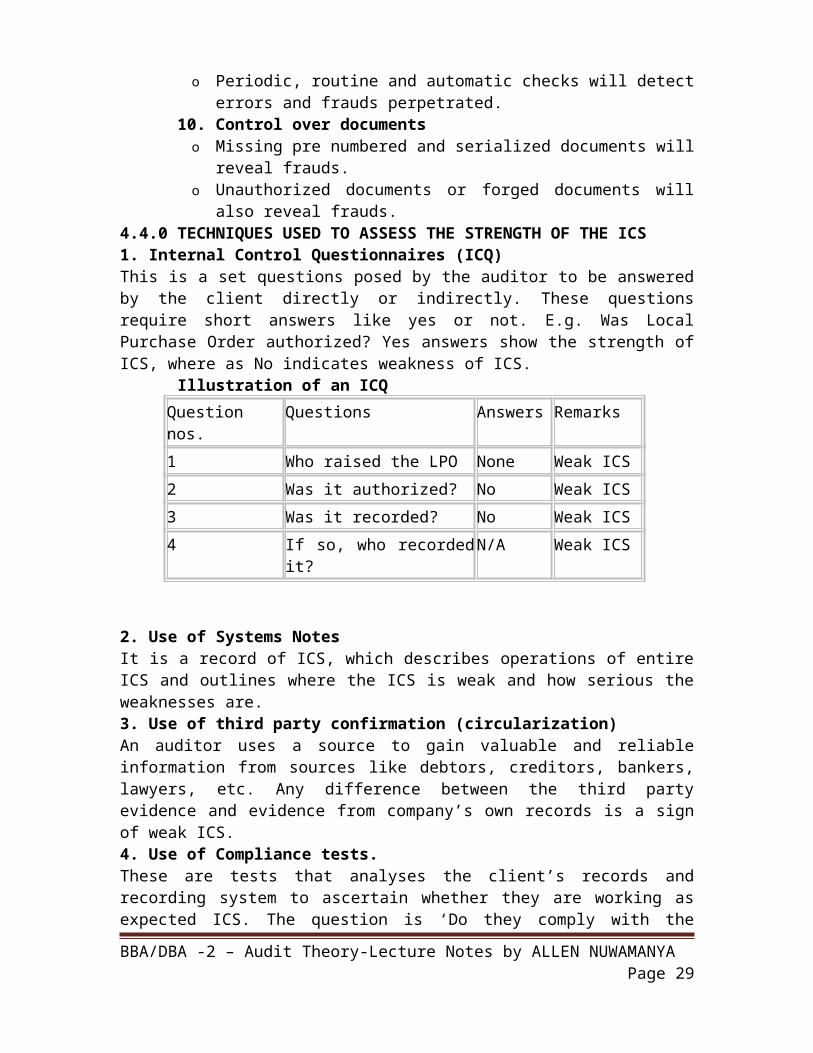

4.4.0 TECHNIQUES USED TO ASSESS THE STRENGTH OF THE ICS 1. Internal Control Questionnaires (ICQ)This is a set questions posed by the auditor to be answered by the client directly or indirectly. These questions require short answers like yes or not. E.g. Was Local Purchase Order authorized? Yes answers show the strength of ICS, where as No indicates weakness of ICS. Illustration of an ICQ

Question nos. Questions Answers Remarks1 Who raised the LPO None Weak ICS2 Was it authorized? No Weak ICS3 Was it recorded? No Weak ICS4 If so, who recorded it? N/A Weak ICS

2. Use of Systems NotesIt is a record of ICS, which describes operations of entire ICS and outlines where the ICS is weak and how serious the weaknesses are. 3. Use of third party confirmation (circularization)An auditor uses a source to gain valuable and reliable information from sources like debtors, creditors, bankers, lawyers, etc. Any difference between the third party evidence and evidence from company’s own records is a sign of weak ICS. 4. Use of Compliance tests.These are tests that analyses the client’s records and recording system to ascertain whether they are working as expected ICS. The question is ‘Do they comply with the company’s laid down policies?’ If the results of these tests indicate a strong control system then the auditor reduces the volume of substantive tests. 5. ObservationThis technique reveals deviations from usual conduct of operations. These observations are made in areas such as wage payments, stocktaking cash counts etc. Any deviations from laid down policies are an indication of weak ICS. 6. Flow ChartsThese are grammatical representations of the company’s procedures designed to show movement of documents within the organisation. Any destruction in the flow lines or blocked flow line is assumed to be an indication of weak ICS. 7. Analytical Reviews

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 18

These are trend measurements aimed at analyzing company’s performance say by use of ratios to determine normal changes. If the changes of the deviations are not justified, it could indicate weakness in the ICS. 8. Use of Depth TestsThis involves the checking of a transaction through various stages of recording , analyzing each stage to ascertain whether the controls are working through out such stages. 9. Use of Walk through tests.These are limited tests aimed at ascertaining the strength or otherwise of an ICS. In order to follow a particular sequence relating to a single transaction, it may be best to follow through a few typical or similar transactions. 4.5.0 Differences between Internal Control Systems (ICS) and Internal Checks (IC). An Internal Check System is part of Internal Control System where duties or functions of an individual are independently checked by his colleagues. The essence of ICS is to ensure that any given function is counter checked to avoid possibility of frauds and errors. The differences between ICS and IC include the following:

1. An internal control system is a broad spectrum of controls aiming at ensuring that the organisation is run efficiently where as an internal check system is aimed at preventing errors and frauds.

2. The internal control system is necessary for all businesses regardless of their size where as an internal check system is ideal for large companies, which require strong segregation of duties.

3. An internal control system is operated by competent and qualified personnel whereas an internal check can be manned by any person regardless of his qualifications.

4. The weak ICS may lead to a qualified report where as internal check may not lead to a qualified report.

Actions to be taken by the Auditor if the ICS is weak 1. He should bring such weaknesses to the attention of the management immediately

and request for corrective measures to this effect. 2. The auditor should increase substantive tests. The auditor should increase the

volume of tests to ensure that he gathers sufficient audit evidence. 3. The auditor should change his audit approach in areas where the ICS is weak .eg

from system-based audit to vouching audit and auditing in depth. 4. If the weaknesses persist year after year the auditor should bring this to the

attention of the shareholders so as to take appropriate action. 5. If ICS are too weak to allow testing, the auditor should qualify his report on the

strength of the fact that he is unable to get all the information and explanations he considers necessary for the purpose of his opinion.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 19

TOPIC 55.0.0 INTERNAL AUDITING Internal audit can be defined as 'an independent appraisal function established by the management of an organisation for the review of the Internal Control System as a service to the organisation'.Internal audit is an element of the internal control system set up by the management of an enterprise to examine, evaluate and report an accounting and other controls on operations.

Scope and Objectives of IA1. Review of accounting system and related internal controls.

2. Examining the financial and operating information for management. This may include review of the means used to identify measure, classify and report such information.

3. Reviewing the economy efficiency and effectiveness of operations and of the functioning of non-financial controls. This can be done through routine and automatic cheeks, periodic reviews and surprise checks.

Routine and automatic checks - are checks on the procedures and items prone to misuse or misappropriations e.g. stock, petty cash, wages payment etc.

Periodic reviews are conducted on company activities that are subject to abrupt change. The review is to ensure that they conform to laid down procedure policies e.g. budgets.

Surprise checks are checks on sensitive assets that are desirable, portable and viable to prevent their misuse through unauthorized access.

4. Review of the implementation of corporate policies, plans and procedures.

5. Special investigations. 5.1.0 Functions of Internal Auditors An Internal Auditor ensures the following:

1. Detection of errors and fraud. 2. An effective system of internal control in place. 3. Continuous effective operation of such systems 4. Adequate management of information flow 5. Asset safeguarding 6. Adequate accounting system in place. 7. Compliance with statutory and regulatory requirements.

Functions of Internal Auditing1. It acts as a consultant department on matters of controls e.g. financial controls,

personal controls etc. 2. It ensures that the organization has strong ICS, which will enhance efficient and

orderly running of the organization. 3. It serves as a preventive measure against errors and frauds, and as such ensures

safety of the company's resources.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 20

4. IA safeguards the company’s assets through strong controls and as such it ensures that the company assets are used by authorized persons and for the right purpose.

5. This function conducts special investigations in such areas:- a. Where frauds and errors are suspected. b. Where profit margins have fallen for no apparent reasons etc.

6. The department performs routine duties such as verification of assets and liability, surprise checks etc.

7. IA performs executive duties such as designing of policies and execution or supervision of board directors, all of which are aimed at ensuring efficient organization policies.

5.2.0 Limitations to setting up an Internal Auditing function 1. Size of the organization may be too small to warrant the function. 2. The cost of installing and maintaining the internal auditing function may be too

high. 3. If operations are few, the function may not be necessary. 4. The ability of staff (qualified and competent) to operate the function may be

unavailable. 5. Lack of cooperation on the part of management. 6. The company’s technical aspects.

5.3.0 Areas/ ways which in Internal Auditors can assist External Auditors 1. Identify areas in which the ICS’s are weak. This will enable the external auditor

to plan his audit work to concentrate his effort in those areas. 2. The internal auditor will pin point technical matters over which the external

auditor may not have sufficient knowledge e.g. technical assets. 3. The internal auditor will pinpoint areas where there are fundamental changes in

management and ICS. 4. He undertakes routine duties on behalf of the external auditor such as, branch

visits, stocktaking, wage payment etc. all of which will assist the external auditor. 5. The internal auditor may prepare schedules for the external auditor e.g. creditors,

debtors and assets schedules, which are useful for comparison purposes and for final review.

6. He makes inquiries/queries and undertakes observation over operations on behalf of the external auditor.

7. The presence of an IA boosts the moral of the accounts staff thereby keeping their accounts to date.

5.4.0 Factors to consider before the external auditors can rely on the internal auditors work. Before placing reliance on the work of an internal auditor, it is necessary to make assessment of the likely effectiveness and the relevance of the internal audit function. The criteria for making this assessment should include the following:-

1. Degree of independence: The external auditor should evaluate the organisation status and reporting responsibility of the IA and consider any restrictions placed on him. Although an IA is an employee of the organisation, he should be able to organise his work and have access to the highest level of management. An IA should also be free to communicate freely with the external auditor.

2. The scope and objectives of the IA function: The EA should ascertain the scope and objectives of IA assignments. This enables the EA to consider the relevant assignments.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 21

3. Due professional care: To be useful to an external auditor, the internal auditor's work must be done in a professional manner. It must be properly planned, controlled, supervised, recorded and reviewed example of the exercise of due professional care by internal auditor are:- existence of an audit manual, general internal audit plans etc.

4. Technical competence: The EA should ascertain whether the work of the internal audit is performed by persons having adequate training. Indications of technical competence may be membership of an appropriate professional body or the possession of relevant practical esp.

5. Reporting standards: The EA should consider the quality of reports issued by internal audit and ascertain whether management acts upon the reports.

6. Resources available: The EA should consider whether IA has adequate resources e.g. in terms of staff and computer facilities.

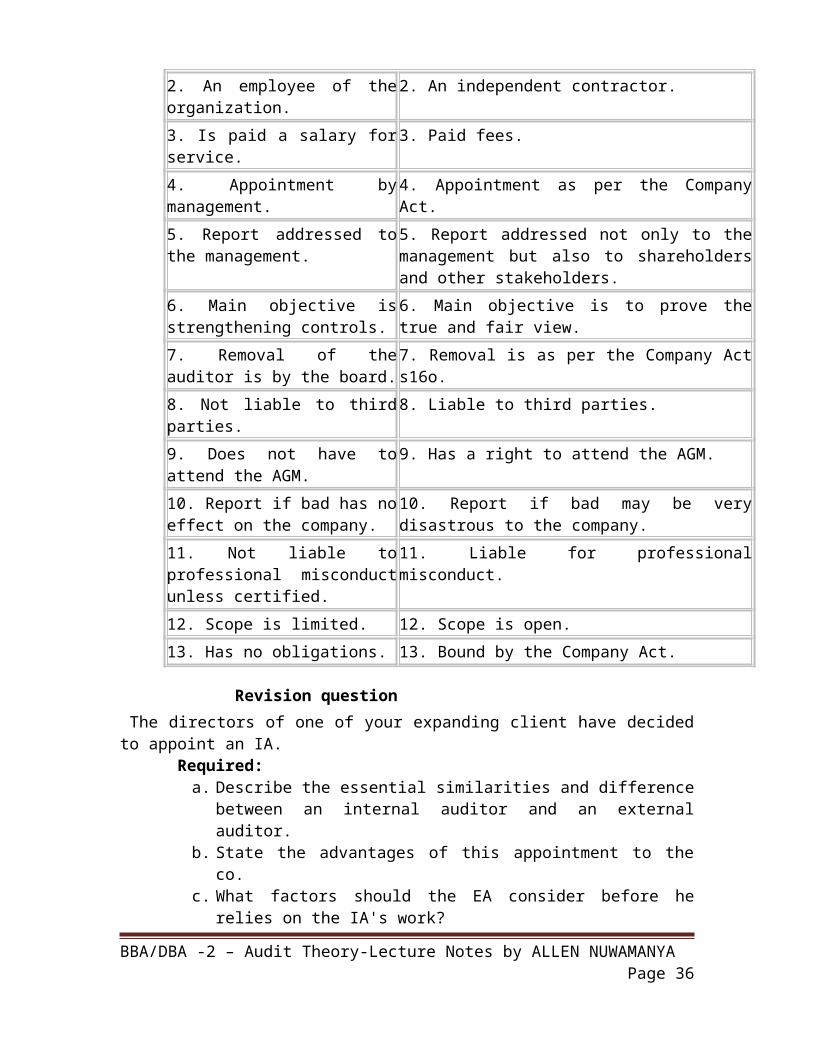

Differences between an Internal Auditor and an External Auditor Internal Auditor External Auditor

1. Does not have to be a certified accountant.

1. Should be a certified accountant.

2. An employee of the organization. 2. An independent contractor.3. Is paid a salary for service. 3. Paid fees.4. Appointment by management. 4. Appointment as per the Company Act.5. Report addressed to the management.

5. Report addressed not only to the management but also to shareholders and other stakeholders.

6. Main objective is strengthening controls.

6. Main objective is to prove the true and fair view.

7. Removal of the auditor is by the board.

7. Removal is as per the Company Act s16o.

8. Not liable to third parties. 8. Liable to third parties.9. Does not have to attend the AGM.

9. Has a right to attend the AGM.

10. Report if bad has no effect on the company.

10. Report if bad may be very disastrous to the company.

11. Not liable to professional misconduct unless certified.

11. Liable for professional misconduct.

12. Scope is limited. 12. Scope is open.13. Has no obligations. 13. Bound by the Company Act.

Revision question The directors of one of your expanding client have decided to appoint an IA. Required:

a. Describe the essential similarities and difference between an internal auditor and an external auditor.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 22

b. State the advantages of this appointment to the co. c. What factors should the EA consider before he relies on the IA's work?

TOPIC 66.0.0 AUDIT MANAGEMENT6.1.0 Audit planning An audit plan:

Is the formulation of the general strategy for the auditor? Which sees the direction for the audit Describes the expected scope and conduct of the audit, and Provides guidance for the development of the audit programme.

Audit planning refers to the arrangement of audit work to be performed in respect to a particular audit assignment.Purpose/advantages of Audit planning

1. Helps to define the objectives and scope of the audit. 2. It increases efficiency, in that, the plan will enable the auditor to concentrate his

audit effort in key areas of an audit and avoid wasting time on routine matters.

3. Audit planning helps the auditor to complete his audit work in time so as to meet such deadlines as:

a. The AGM b. Income tax returns c. Returns to the registrar d. Financial commitments etc.

4. It enables the auditor to make optimal use of audit staff available so as to enable him conduct efficient audits in an exhaustive manner and above all, to avoid any delays in a given part of the audit work.

5. It also enables the auditor to control his audit work, for it is impossible to control an audit that has not been planned.

6. It facilitates the co-operation between the auditor, his assistant and his client. This cooperation:

a. Avoids delays b. Enables the auditor obtain important documents from the client c. Conduct interviews and reviews of the client’s activities.

7. Audit planning takes into consideration the volume of transactions. The size of modern business is such that the volumes of transactions are numerous, and as such, without proper audit planning, an auditor cannot finish his work in time.

8. It ensures that potential problems are identified and given due attention.

Knowledge of the client's businessAudit planning enables the auditor to conduct efficient audits in an effective manner, and to complete his work in time. For this reason he should have a good knowledge of the client's business. Sources of knowledge.

a) Previous experience of the client and its industry. b) Discussion with contacts within the client management and senior operating

personnel.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 23

c) Discussion with internal audit personnel and review of internal audit reports. d) Discussion with other auditors and with legal and other advisors who have

provided services to the client. e) Discussion with knowledgeable people outside the client. f) Publications related to the industry. g) Visits to the client’s premises and plant factories. h) Documents produced by the client.

Audit planning procedures. This includes the following:

a) Consider the background to the clients business, and attempt to ascertain any problem for that sector of industry or commerce, which may affect the audit work. This is more important in case of a new client and is done during the initial visit.

b) Consider an outline plan of the audit including the extent to which he may wish to rely upon internal controls and extent to which work can be allocated to interim or final audit stages where appropriate.

c) Review matters raised in the audit of the previous years, by examining the audit files and discussing points with staff previously involved in the audit to ascertain those facts which may have relevance to the current year.

d) Assess the effect of any changes in legislation or accounting practice on the financial statements of the client.

e) Review any management or interim accounts the client may have prepared as these may indicate areas of concern in his audit.

f) Meet the senior management of the client to identify problem areas e.g. variances between the budgeted and actual results, changes in the accounting system, staffing, management structure etc.

g) Discuss with management the extent to which the client’s employees will assist in the audit work.

h) The auditor will need to determine the number of audit staff required, their experience and special skills they need to possess and the timing of their audit visits.

6.2.0 Audit ProgrammeIt is a detailed approach to an audit showing procedures and relevant items in carrying out an audit. Its formulation is based on the overall audit plan and the nature of the client. The audit programme provides the instructions to the audit team in form of tests or activities to be carried out during the audit. Factors to consider in developing an audit programme

Risk of error; high risk detailed programme low risk, less detailed programme. The necessary audit evidence needed to fulfill the procedure. Some areas of

audits requires more evidence and therefore more instruction are given for such areas compared to those whose audit requires little evidence.

Coordination of audit work with any work on preparing the financial statements. Timing of tests of control and substitute procedures. Coordination of any assistance from the entity. The composition of the audit team.

The involvement of other auditor or experts. NB: The level of detail in the audit programme will depend on the complexity and size of the client and the issues there to.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 24

Objectives of an audit Programme1. It assists in ensuring that the audit work is done efficiently and effectively to meet

the overall audit strategy or plan. 2. It’s intended to provide clear instructions and timing of procedures to audit staff 3. Provides a record of work done and conclusions made and therefore can be used

as a defense against an action for negligence 4. It aids audit control as it forms basis for audit review. (Through cross

examination). Characteristics of good Audit programme.

Should describe the nature of audit procedure in detail. It should indicate the extent of testing; audit checking It should show against each procedure across reference to working papers, initials

of the audit staff, date of completion of the work, exceptions and how they are cleared.

Note: Each area of the audit must have its own audit programme e.g. audit programme for payroll, company consumables, Noncurrent assets, investments of the company etc.

Amendment of Audit ProgrammeThe audit programme is prepared before the audit commences and on some assumptions.On the commencement of the actual audit, these assumptions may have changed and hence a need to change the audit programme. Below are some of the factors that may necessitate a change in the audit programme;

The accounting system or computer software may have been changed by the client. Eg change to specialized self balancing ledges from general journal and ledger.

There may be ground for suspicious of fraud. The amount of audit work might have been under estimated. The client business may have expanded its operations or contracted part of it or

cutting the size down Change in the accounting policies.

Standard audit programme.Is a pre-prepared audit program for use in the audit firm by all audit staff irrespective of the client. Advantages of standard audit programme

It ensures that all work is completed on time without any omissions. Its used to monitor the progress of the audit Enhances uniformity of work for audits across periods It facilitates allocation of audit work and assessment of staff competencies It facilitates the final review as it provides summaries of what is to be checked

(and this done normally by the audit partner). It serves as a record of work done and therefore can be used as evidence for any

action of negligence. Disadvantages of the standard audit programme.

It may be followed mechanically leaving some areas of importance without proper understanding of what is done.

It may destroy the innovativeness of the audit staff and may slow their development in the audit field.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 25

It may leave errors and fraud undetected as it may be followed without due attention and profession skills

Audit clerks may hurriedly try to finish on time leaving some work unchecked Familiarity with the audit program may facilitate fraud by the client staff

Precautions to be taken when the audit programme is standardized

Encourage the audit staff to point out any defects in the programme Encourage the audit staff to use the programme as a guide but to apply

professional judgment Revise the audit programme often Allocating responsibility for each audit staff who are encouraged to keep the

overall perspective in mind. Plan audit checks in such a way as to prevent parts of the programme being

completed in isolation. 6.3.0 Audit riskWhen planning the audit, the auditor should assess the risk of the client he is to handle in order to assess the extent and nature of the work he is to perform. The riskier the client, the more the auditor will plan to perform.

Audit risk is the chance that an auditor may give a wrong opinion on the financial statements i.e. he may issue a qualified report when actually there were no material errors in the financial statements or he may issue an unqualified report when actually there were material errors. The effect of audit risk is damage to the audit firm (e.g. in form compensation to third parties) or loss of reputation with the client or the business community.

Audit risk has three components:a) Inherent risk Refers to the risk of material errors in the financial statements arising from characteristics of the client business and its environment, some of the characteristics include:

o Dominance by a single person o The experience a unqualified staff o Unusual pressures on management e.g. tight reporting deadlines. eve.

b) Control risk. Refers to the risk that the client's controls in place will fail to detect or prevent material errors or frauds in the financial statements.Factors to be considered may include:-

o Quality and effectiveness of management (degree or supervision) o Quality of IC e.g. poor segregation of duties. o Competence of accounts staff o Accounting system etc.

c) Detection risk. Is the risk that audit procedures will fail to detect material errors or fraud e.g.

o Failure to draw proper conclusions in particular audits evidence. o Failure to perform necessary audit work due to limited time or high cost

e.g. missing stock taking, wages payment etc. 6.4.0 Audit control (Quality Control)

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 26

Audit control refers to the steps which are taken by the auditor to ensure that the actual audit carried out is as per the audit plan.Quality control refers to the procedures organised to ensure that audits are performed:-

a. In accordance with approved auditing standards. b. In conformity with statutory and contractual requirements. c. In conformity with any professional standards. d. Economically and to time schedules e. With minimum risk.

Quality control policies and procedures should be implemented both at the level of the audit firm and at the level of individual audits. Quality Control at Individual Audit LevelThe following ways can be adopted to control the audit:-

i. Allocation of work. Work should be allocated to audit staffs that have appropriate skills and competence to carry out the assigned tasks.

ii. Proper briefing. Ensure that audit staffs of all levels clearly understand their responsibilities and the objectives of the procedures, which they are expected to perform.

iii. Audit completion check list. It is a common experience that in the rush to complete an audit on time, matters of importance may be overlooked. So it is necessary to go through the checklist to make sure that everything is covered.

iv. Documentation. All audit work and conclusions reached must be fully recorded in the working papers.

v. Review. The work performed by each member of the audit must reviewed by more senior persons in the audit firm. This is necessary to ensure that the work was adequately performed and to confirm that the results obtained, support the audit conclusions which have been reached.

vi. Acknowledgement. All audit work and review action should be acknowledged in writing by the performer.

vii. Supervision. Personnel with supervisory responsibilities should monitor the progress of the audit to consider whether:-

Assistants have the necessary skills and competence to carry out their tasks.

Assistants understand the audit direction, etc. Quality Control at the Level of the Audit Firm. The procedures include:-

1. Acceptance and retention of clients. This involves screening prospective clients and reviewing existing clients in terms of independence, ability to properly audit the client and the integrity of the client’s management.

2. Professional Ethics. There should be procedures within the firm to ensure that all partners and professional staff adhere to the principles of independence, objectivity, integrity and confidentiality.

3. Skill and Competence. The firm’s partners and staff should have attained the skills and competence required to fulfill their responsibilities. This involves procedures relating to

a. Effective recruitment b. Technical training and up dating c. On the job training and professional development

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 27

4. Assignment. Audit work should be assigned to audit staff who have the technical training and proficiency needed to do the work.

5. Delegation. Sufficient direction, supervision and review of work at all levels. This includes the use of audit programme and standard documents.

6. Consultation. There should be procedures for consultation. Individual members of the firm should not take decisions on problems areas without consultation with others. Problem areas may be technical or a matter of risk.

7. Monitoring the firm’s quality control procedures. Suitable procedures should be introduced to monitor the effectiveness of the application of quality control procedures outlined above.

6.5.0 Audit recording (Audit working papers) Audit recording refers to documentation of audit work in form of working papers (WP). WP are the materials the auditors prepare or obtain and retain in connection with the performance of the audit. WP may be in form of data stored on papers, films, electronic media etc.The auditor should document all materials, which are important in providing evidence to support his/her audit opinion, and should show compliance with audit standards. In other words, WP should:-

o Record auditor's planning, nature, timing and the extent of audit procedures performed and conclusions made from evidence obtained.

o Include matters such as auditor's reasoning, judgment and conclusions. o Acts as evidence of work done to support his conclusion

Importance/ purpose/ advantages of WP1. WP are used as a basis for planning subsequent years’ audits because the starting

point of a given year's audit (especially for existing clients) is a review of the previous year's WP.

2. They provide evidence of work done in case of threat of or action taken against the auditor for negligence. I.e. WP show evidence of appropriate audit procedures carried out and conclusions reached.

3. They assist the manager in reviewing the audit work and the reporting partners in reaching an audit opinion i.e. whether the financial statements portray a true and fair view of the company's performance.

4. They are also used to control audit work, in that the best audit control is effected through the review of documentation.

5. WP enables the auditor to adopt methodical approach to his audit work and by so doing, adhere to laid down professional standards and the audit firm's own standards. This in turn improves quality of audit work.

N.B: Working Papers are the property of the auditor, but at his discretion, he may give the client extracts or portions of such working papers.

Audit files Normally an auditor maintains two files of WP for each client i.e.

o The Current Audit File o The Permanent Audit File

Current Audit File (CAF)This contains information relevant to the current year's audit.

BBA/DBA -2 – Audit Theory-Lecture Notes by ALLEN NUWAMANYA Page 28

Contents:1. A copy of accounts and statements which the auditor is reporting on. 2. An index to the file 3. A description of the internal controls in form of an ICQ, flow charts, etc. 4. An audit programme. 5. A schedule for each item in the balance sheet. 6. A schedule for each item in the profit and loss account. 7. A checklist for compliance with statutory disclosure requirements, accounting

standards and guidelines. 8. A record of questions raised and answers obtained and if not satisfactorily

answered, what course of action to be taken, a qualification of opinion. 9. A schedule of important statistics. 10. A record or abstract from the minutes of the company, directors etc. 11. A copy of the management letter that highlights the weakness of the internal

control system. 12. Letters of representation which are written by the directors or their representatives

to the auditor. Permanent Audit File (PAF) This contains information of a long-term nature or matters of continuing importance to the auditor, which will be used for a period beyond one audit.Contents of PAF

1. Statutory material governing the conduct of accounts and audit of enterprises.e.g company act, accounting and audit standards, etc

2. Rules and regulations of the enterprise e.g. the Memorandum of Association, Articles of Association, Partnership Deed, etc

3. Documents of continuing importance to the auditor. e.g. letters of engagement, trade licenses, debenture deeds, leases etc

4. Address of the registered office. 5. The organization chart showing principle departments and their sub-divisions. 6. A list of books and other records, which are kept, names, positions and specimen

signatures of people keeping such records. 7. A list of accounting matters of long-term use to the auditor e.g. accounting