Embed Size (px)

Citation preview

1

Brexit: What next?Understanding the implications for businesses

2

Mark Hughes, Group CEOManchester Growth Company

3

4

5

MGC Purpose

Brexit: What next?Understanding the implications for businesses

6

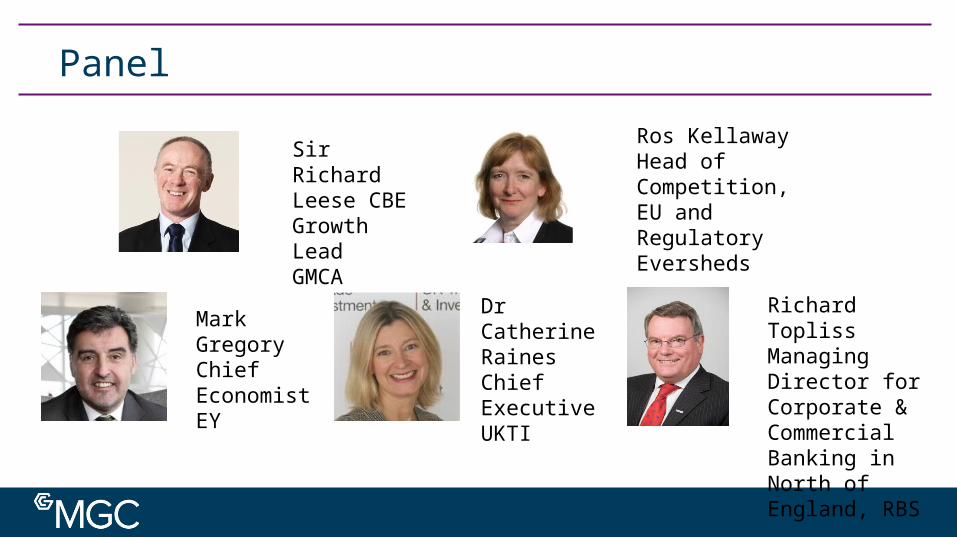

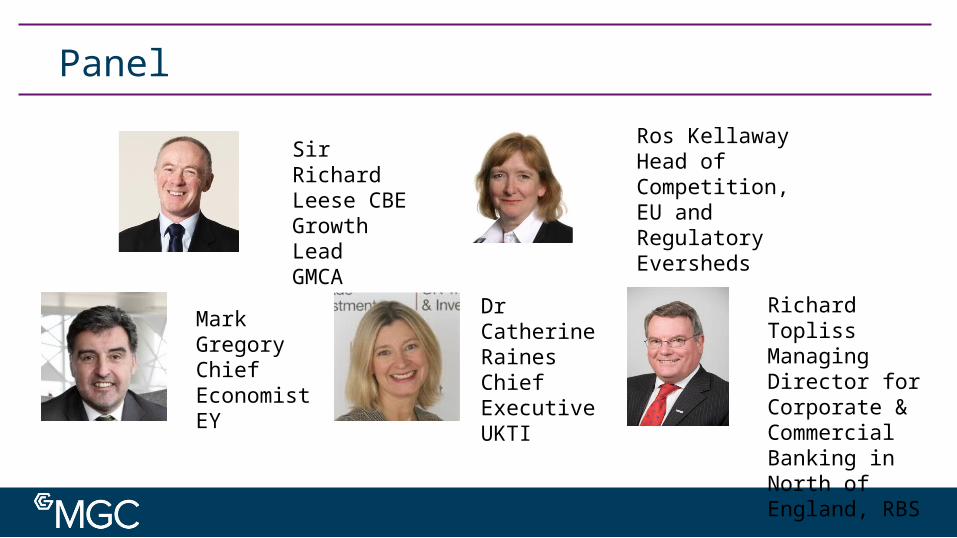

Panel

Sir Richard Leese CBEGrowth LeadGMCA

Ros KellawayHead of Competition, EU and RegulatoryEversheds

Mark GregoryChief EconomistEY

Dr Catherine RainesChief ExecutiveUKTI

Richard Topliss Managing Director for Corporate & Commercial Banking in North of England, RBS

7

MGC Purpose

Sir Richard Leese CBEGrowth Lead, Greater Manchester Combined Authority

8

MGC Purpose

Ros Kellaway Head of Competition, EU and Regulatory, Eversheds

Making Sense of BrexitWhat will it mean to leave the EU?26 July 2016

PartnerRos Kellaway

1. Mechanism for leaving the EU2. EFTA and the EEA3. Five Brexit models4. Trading with the Rest of the World5. How could Brexit impact your business?6. How can Eversheds help?

Agenda

Eversheds LLP | 01/05/2023 | Eversheds LLP | 01/05/2023 |

• Article 50 sets out the formal mechanism to leave the EU• UK must take a decision to leave the EU “in accordance with its

own constitutional requirements”• Outcome of Referendum advisory to the Government - result

does not trigger Article 50 • Government must formally trigger Article 50 process by giving

notice to the European Council• Will an Act of Parliament be needed or can the Government use

its Royal Prerogative powers? • At least 7 private actions arguing that an Act of Parliament is needed –

case will be heard in October 2016

Article 50 Treaty on the European UnionMechanism for Leaving the EU (1)

Eversheds LLP | 01/05/2023 | Eversheds LLP | 01/05/2023 |

• When will Article 50 notice be given?• Not in 2016 – expected early 2017

• When will the UK leave the EU?• Date the withdrawal agreement comes into force; or• Two years after the notification unless unanimously

extended by the European Council and the UK

TimingMechanism for Leaving the EU (2)

Eversheds LLP | 01/05/2023 | Eversheds LLP | 01/05/2023 |

• UK/EU negotiate and conclude an agreement setting out the withdrawal arrangements taking account the framework for future relationship together

• Two agreements?• Withdrawal agreement – needs to be agreed by European Parliament and Council

• Trade agreement – will need:• European Parliament approval• Unanimous consent and ratification of all Member States

Article 50 Treaty on the European UnionMechanism for Leaving the EU (3)

Eversheds LLP | 01/05/2023 | Eversheds LLP | 01/05/2023 |

• Free trade arrangement founded in 1960 by Austria, Denmark, Norway, Portugal, Sweden, Switzerland and the UK

• EFTA has said it would welcome an application from the UK to re-join EFTA

• Current members: Iceland, Lichtenstein, Norway and Switzerland• EFTA has free trade agreements with 37 countries and is negotiating

others• EFTA States free to negotiate their own free trade agreements e.g.

Switzerland with China and Japan• Being a member of EFTA does not give access to the Internal Market

European Free Trade Area (“EFTA”)

Eversheds LLP | 01/05/2023 | Eversheds LLP | 01/05/2023 |

• Founded in 1992 and effective in 1994• Intended to create closer cooperation between EU and EFTA, pending EFTA States accession to the EU

• EU Member States and three EFTA States (Iceland, Lichtenstein and Norway)

• Access to the Internal Market governed by EEA Agreement – all four freedoms but outside Common Agricultural Policy and Common Fisheries Policy

• EEA minus free movement of people?

European Economic Area (“EEA”)

Eversheds LLP | 01/05/2023 |

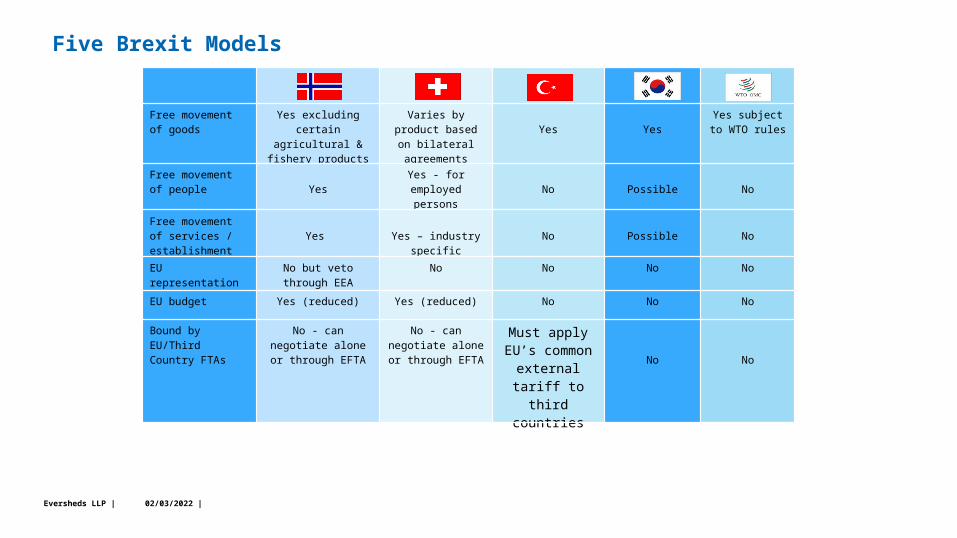

Free movement of goods

Yes excluding certain agricultural & fishery products

Varies by product based on bilateral

agreementsYes Yes

Yes subject to WTO rules

Free movement of people Yes

Yes - for employed persons

No Possible No

Free movement of services / establishment

Yes Yes – industry specific

No Possible No

EU representation No but veto through EEA

No No No No

EU budget Yes (reduced) Yes (reduced) No No No

Bound by EU/Third Country FTAs

No - can negotiate alone or through

EFTA

No - can negotiate alone or

through EFTAMust apply

EU’s common external tariff

to third countries

No No

Five Brexit Models

Eversheds LLP | 01/05/2023 | Eversheds LLP | 01/05/2023 |

• On Brexit, UK will lose benefit of EU’s free trade agreements but will be able to negotiate its own free trade agreements

• Already interest from a number of countries – Australia, Canada, China, Ghana, India, Mexico, New Zealand, South Korea, US

• Preliminary talks with India• UK can negotiate terms of free trade agreements but cannot conclude them before Brexit – exclusive EU competence

Trading with the Rest of the World

Eversheds LLP | 01/05/2023 | Eversheds LLP | 01/05/2023 |

• Supply chains – do they cross the UK and other EU Member States?

• Risks of and opportunities from ceasing to be in the Customs Union

• Loss of EU trade deals• New trade deals• Recruitment of people from the UK for your EU operations and

vice-versa• Effect on contracts

How could Brexit impact your business?

Eversheds LLP | 01/05/2023 | Eversheds LLP | 01/05/2023 |

• Brexit will not impact all sectors equally – each business needs to consider what it will mean for them

• Eversheds has a team of experts that can advise you on the potential impact Brexit will have on your business

• We can help you identify the specific risks, challenges and opportunities for your business to manage your exposure and help you prepare a “Brexit ready” plan

• We can help you lobby for Brexit arrangements for your sector• Further information is available on Eversheds’ Brexit webpage -

www.eversheds.com/brexit

How can Eversheds help?

eversheds.com©2015 Eversheds LLPEversheds LLP is a limited liability partnership

PartnerCompetition, EU and Regulatory+44 20 7919 [email protected]

Ros Kellaway

21

MGC Purpose

Mark Gregory Chief Economist, EY (Item Club)

What does Brexit mean for business?

Mark Gregory27th July 2016

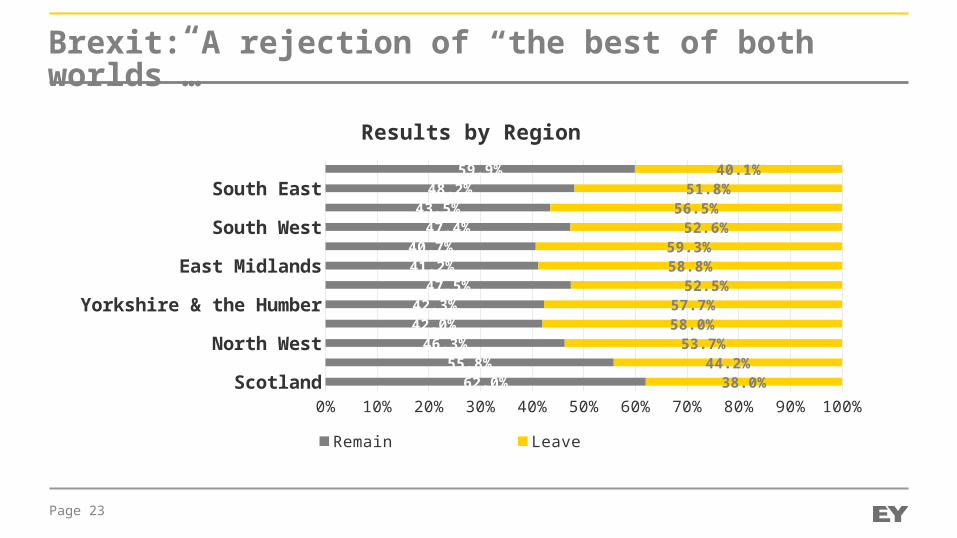

Brexit: A rejection of “the best of both worlds”…

Scotland

North West

Yorkshire & the Humber

East Midlands

South West

South East

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%62.0%

55.8%46.3%

42.0%42.3%

47.5%41.2%40.7%

47.4%43.5%

48.2%59.9%

38.0%44.2%

53.7%58.0%57.7%

52.5%58.8%59.3%

52.6%56.5%

51.8%40.1%

Results by Region

Remain Leave

Page 23

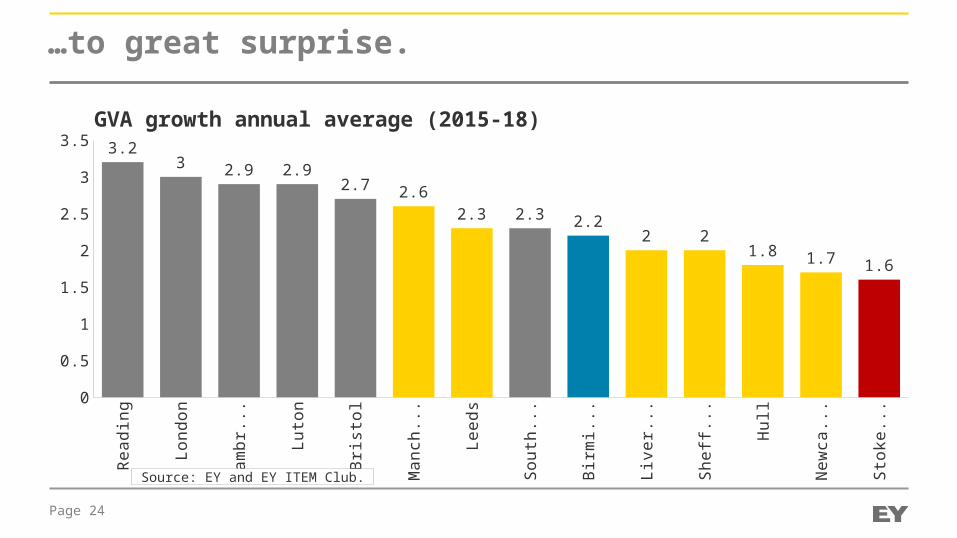

…to great surprise.

Page 24

Rea

ding

Lond

on

Cam

br...

Luto

n

Bris

tol

Man

che.

..

Leed

s

Sou

tha.

..

Birm

in...

Live

rpoo

l

She

ffiel

d

Hul

l

New

cast

le

Sto

ke-o

n...0

0.5

1

1.5

2

2.5

3

3.5 3.23 2.9 2.9

2.7 2.62.3 2.3 2.2

2 21.8 1.7 1.6

GVA growth annual average (2015-18)

Source: EY and EY ITEM Club.

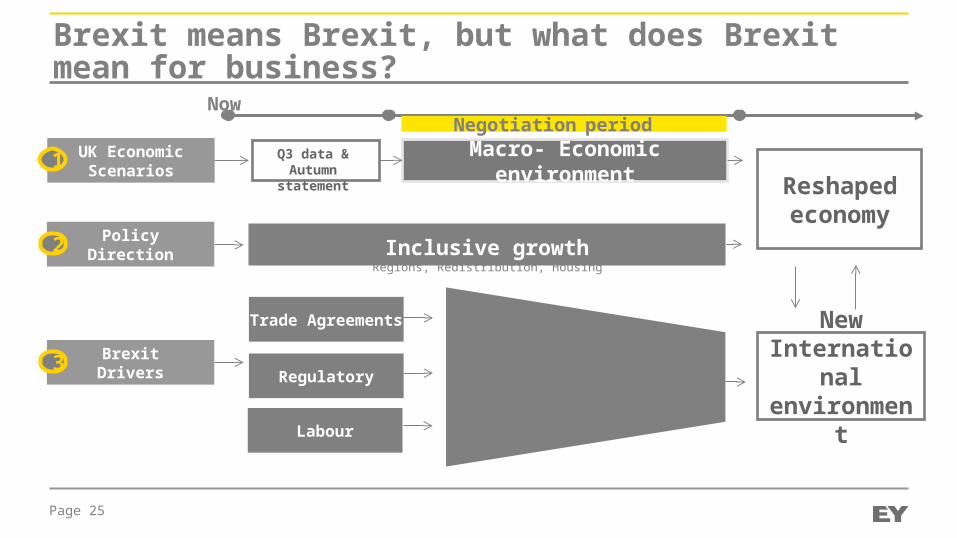

Brexit means Brexit, but what does Brexit mean for business?

Regulatory

Trade Agreements

Labour

UK EconomicScenarios1

PolicyDirection2

BrexitDrivers3

Now

Infrastructure, Inclusive growth, Skills, Regions, Redistribution,

Housing

Macro- Economic environment

Negotiation period

Reshaped economy

New International environment

Page 25

Q3 data & Autumn statement

26

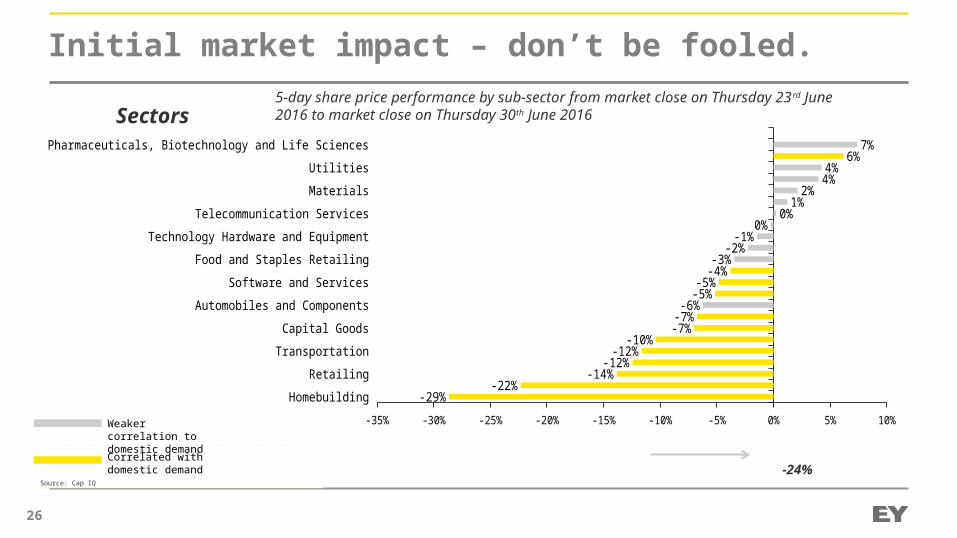

HomebuildingRetailing

TransportationCapital Goods

Automobiles and ComponentsSoftware and Services

Food and Staples RetailingTechnology Hardware and Equipment

Telecommunication ServicesMaterials

UtilitiesPharmaceuticals, Biotechnology and Life Sciences

-35% -30% -25% -20% -15% -10% -5% 0% 5% 10%-29%

-22%-14%

-12%-12%

-10%-7%-7%-6%

-5%-5%

-4%-3%

-2%-1%

0%0%

1%2%

4%4%

6%7%

5-day share price performance by sub-sector from market close on Thursday 23rd June 2016 to market close on Thursday 30th June 2016

Source: Cap IQ

Weaker correlation to domestic demandCorrelated with domestic demand -24%

Initial market impact – don’t be fooled.

Sectors

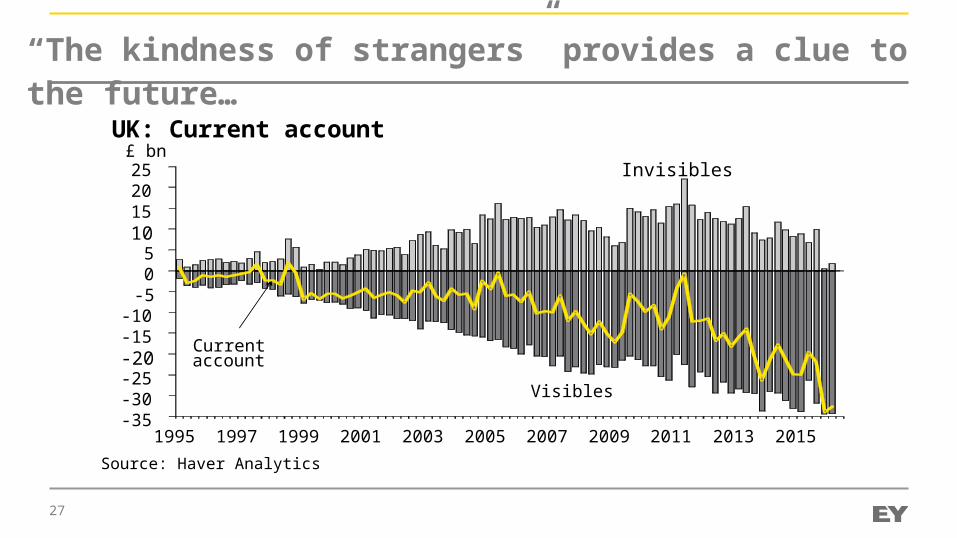

“The kindness of strangers” provides a clue to the future…

27

-35-30-25-20-15-10

-505

10152025

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015Source: Haver Analytics

£ bn

Currentaccount

UK: Current accountInvisibles

Visibles

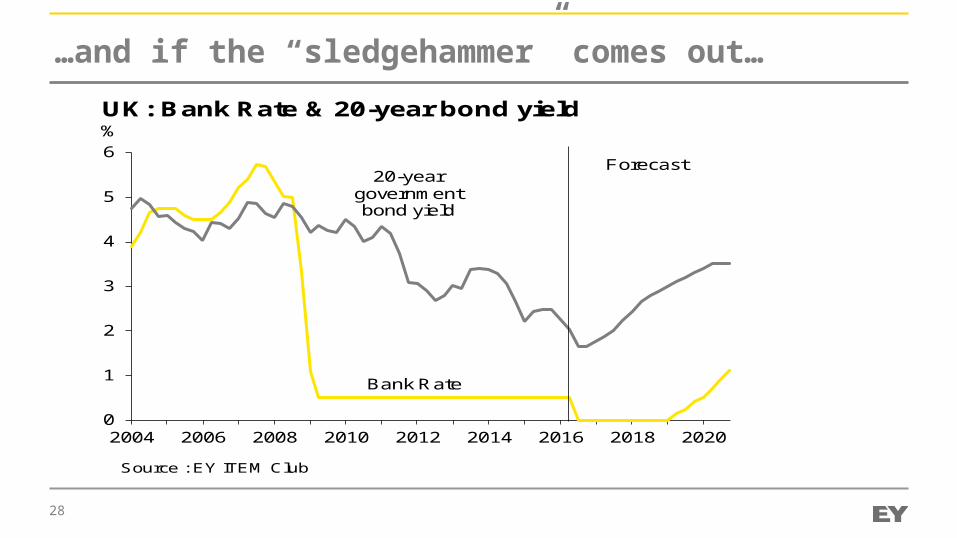

…and if the “sledgehammer” comes out…

0

1

2

3

4

5

6

2004 2006 2008 2010 2012 2014 2016 2018 2020

UK: Bank Rate & 20-year bond yield%

Source : EY ITEM Club

Bank Rate

20-year government bond yield

Forecast

28

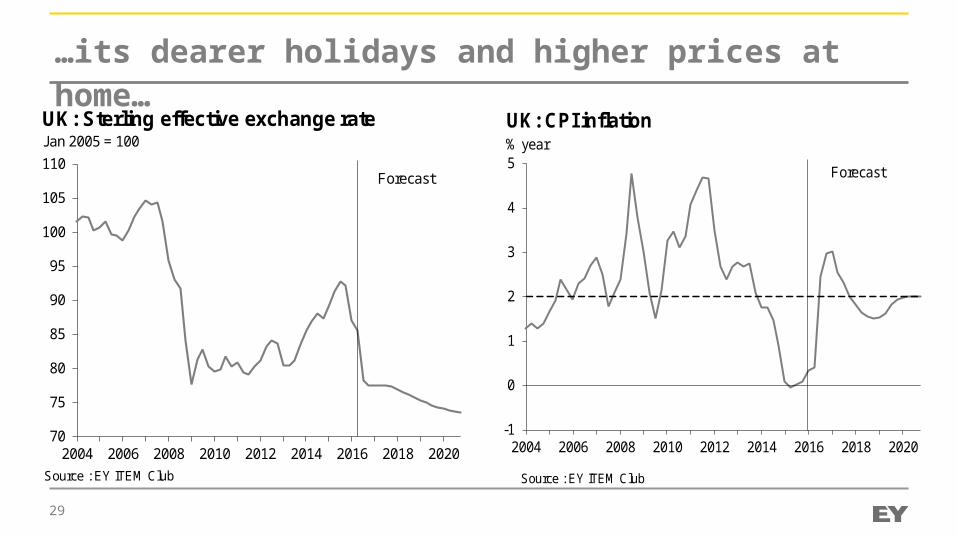

…its dearer holidays and higher prices at home…

70

75

80

85

90

95

100

105

110

2004 2006 2008 2010 2012 2014 2016 2018 2020

UK: Sterling effective exchange rateJan 2005 = 100

Source : EY ITEM Club

Forecast

29

-1

0

1

2

3

4

5

2004 2006 2008 2010 2012 2014 2016 2018 2020

UK: CPI inflation% year

Source : EY ITEM Club

Forecast

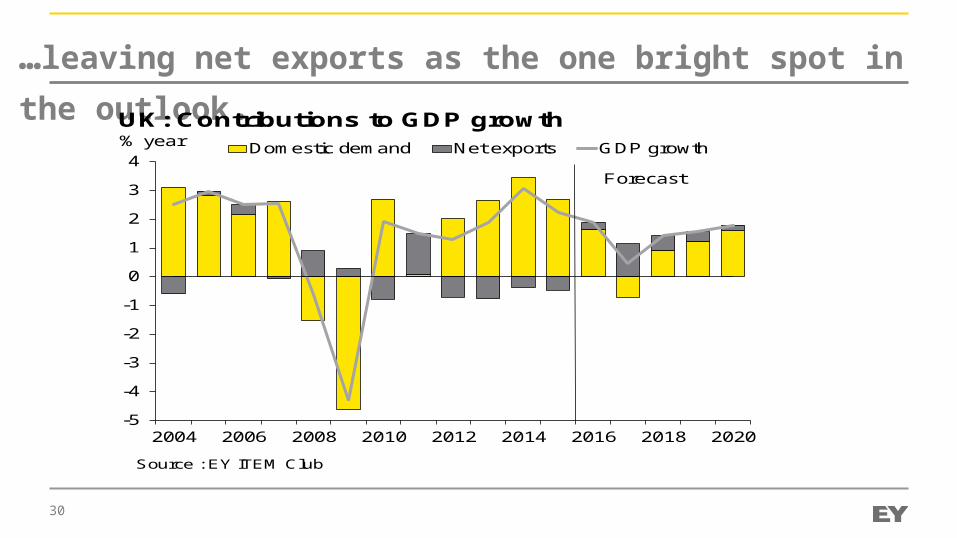

…leaving net exports as the one bright spot in the outlook.

-5

-4

-3

-2

-1

0

1

2

3

4

2004 2006 2008 2010 2012 2014 2016 2018 2020

Domestic demand Net exports GDP growth

UK: Contributions to GDP growth% year

Source : EY ITEM Club

Forecast

30

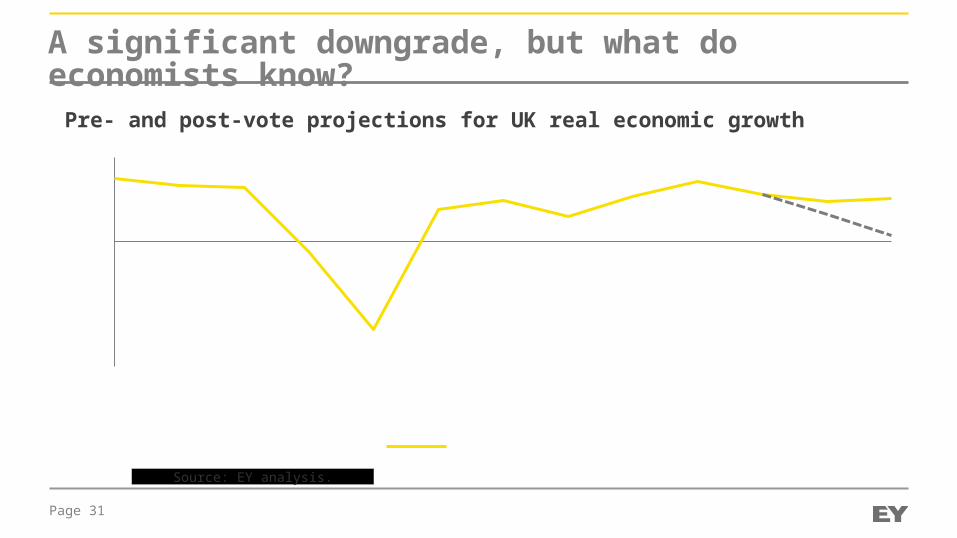

A significant downgrade, but what do economists know?

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

-5%-4%-3%-2%-1%0%1%2%3%4%

Actual / Pre-vote

Pre- and post-vote projections for UK real economic growth

Page 31

Source: EY analysis.

The three legs of Brexit

Trade Migration Regulation

Page 32

The key drivers of the future state.

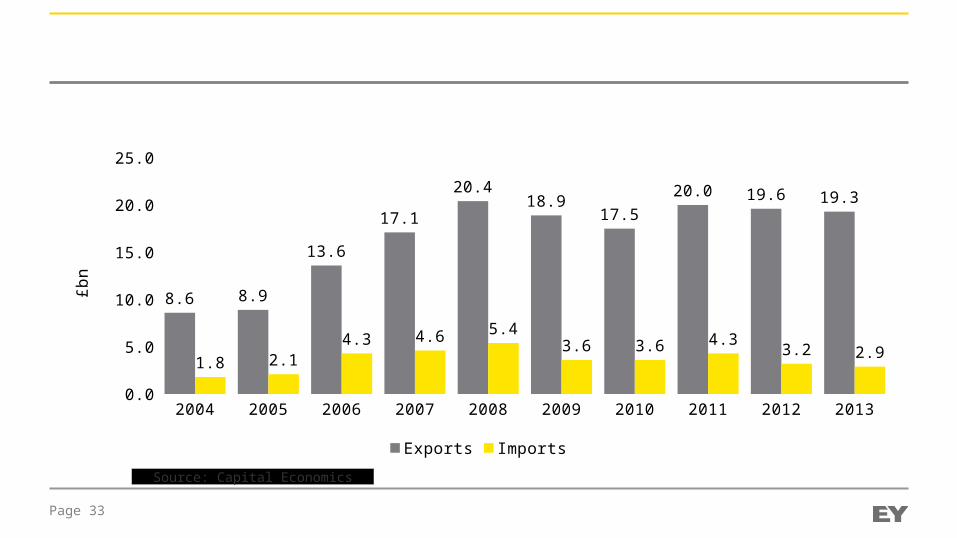

Financial services in the firing line.

Page 33

UK FS trade with EU

2004 2005 2006 2007 2008 2009 2010 2011 2012 20130.0

5.0

10.0

15.0

20.0

25.0

8.6 8.9

13.6

17.1

20.418.9

17.520.0 19.6 19.3

1.8 2.14.3 4.6 5.4

3.6 3.6 4.33.2 2.9

Exports Imports

£bn

Source: Capital Economics

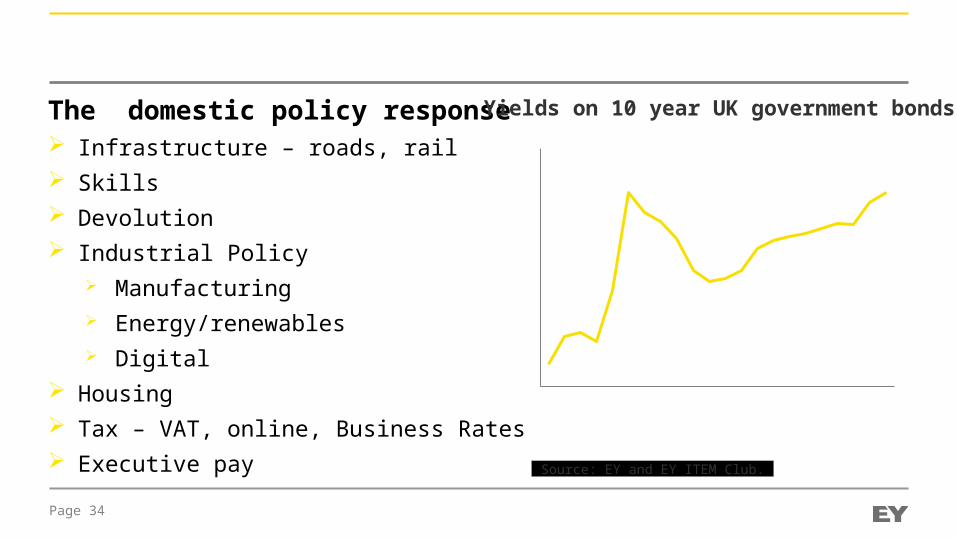

The end of Thatcherism?

The domestic policy response Infrastructure – roads, rail Skills Devolution Industrial Policy

Manufacturing Energy/renewables Digital

Housing Tax – VAT, online, Business Rates Executive pay

2-Ju

n-16

3-Ju

n-16

4-Ju

n-16

5-Ju

n-16

6-Ju

n-16

7-Ju

n-16

8-Ju

n-16

9-Ju

n-16

10-J

un-1

611

-Jun

-16

12-J

un-1

613

-Jun

-16

14-J

un-1

615

-Jun

-16

16-J

un-1

617

-Jun

-16

18-J

un-1

619

-Jun

-16

20-J

un-1

621

-Jun

-16

22-J

un-1

623

-Jun

-16

24-J

un-1

625

-Jun

-16

26-J

un-1

627

-Jun

-16

28-J

un-1

629

-Jun

-16

30-J

un-1

60.8

0.9

1

1.1

1.2

1.3

1.4

1.5

Yields on 10 year UK government bonds

Page 34

Source: EY and EY ITEM Club.

The return of Empire?

Time to re-invent trade The UK is a key part of the global

trade jigsaw How hard can it be to negotiate a

trade deal? Domestic policy has to support trade

activity Devolution Skills Industrial policy and procurement

UK trade strategy has to be more integrated FDI Exports ODI Migration/Education Education

Page 35

37

MGC Purpose

Dr Catherine Raines Chief Executive, UKTI

Dr Catherine RainesCEO UKTI

Building trade and investment prospects for the UK and supporting the Northern Powerhouse

Our new Ministerial team

Liam Fox MPSecretary of State for International Trade and President of the Board of Trade

Greg Hands MPMinister of State

Lord PriceMinister of State

for Trade and Investment

Mark Garnier MPParliamentary Under

Secretary of State

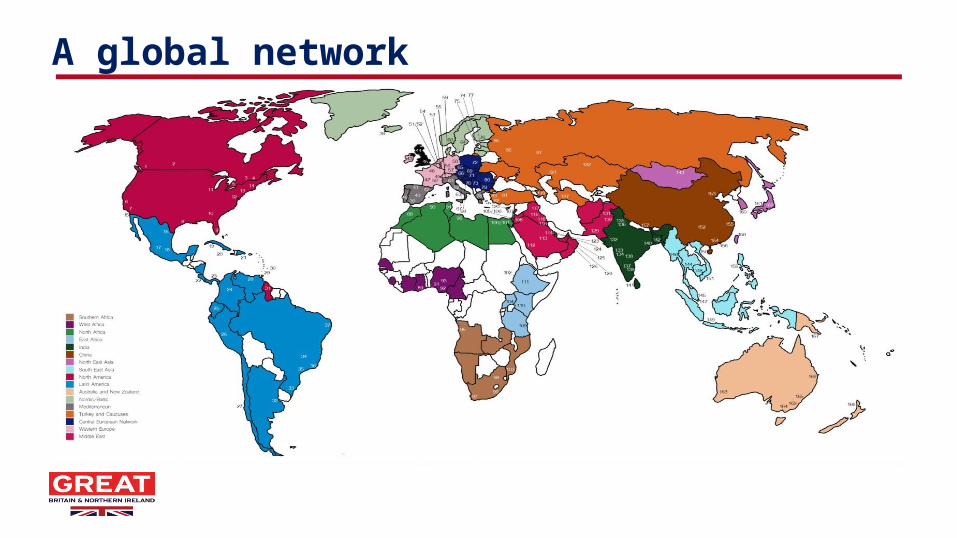

A global network

41

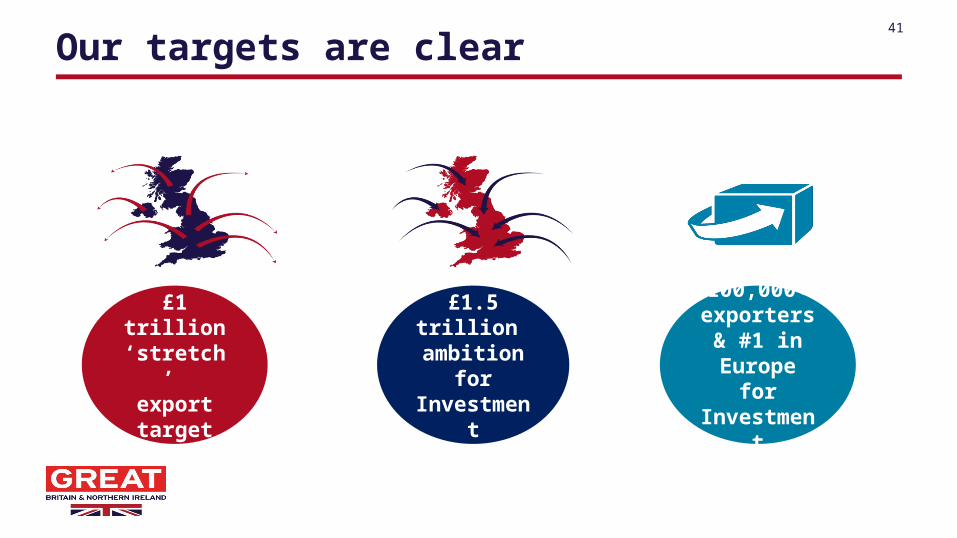

Our targets are clear

£1 trillion ‘stretch’ export target

£1.5 trillion

ambition for

Investment

100,000+exporters &

#1 in Europe for Investment

International Expo – Astana

Driving the Northern Powerhouse

Get involved

www.exportingisgreat.gov.uk

46

Brexit: What next? – panel session

47

Panel

Sir Richard Leese CBEGrowth LeadGMCA

Ros KellawayHead of Competition, EU and RegulatoryEversheds

Mark GregoryChief EconomistEY

Dr Catherine RainesChief ExecutiveUKTI

Richard Topliss Managing Director for Corporate & Commercial Banking in North of England, RBS

48

Brexit: What next?