Embed Size (px)

Citation preview

Complete Guide to Building an Acquisition Strategy and Valuation Methodologies

2

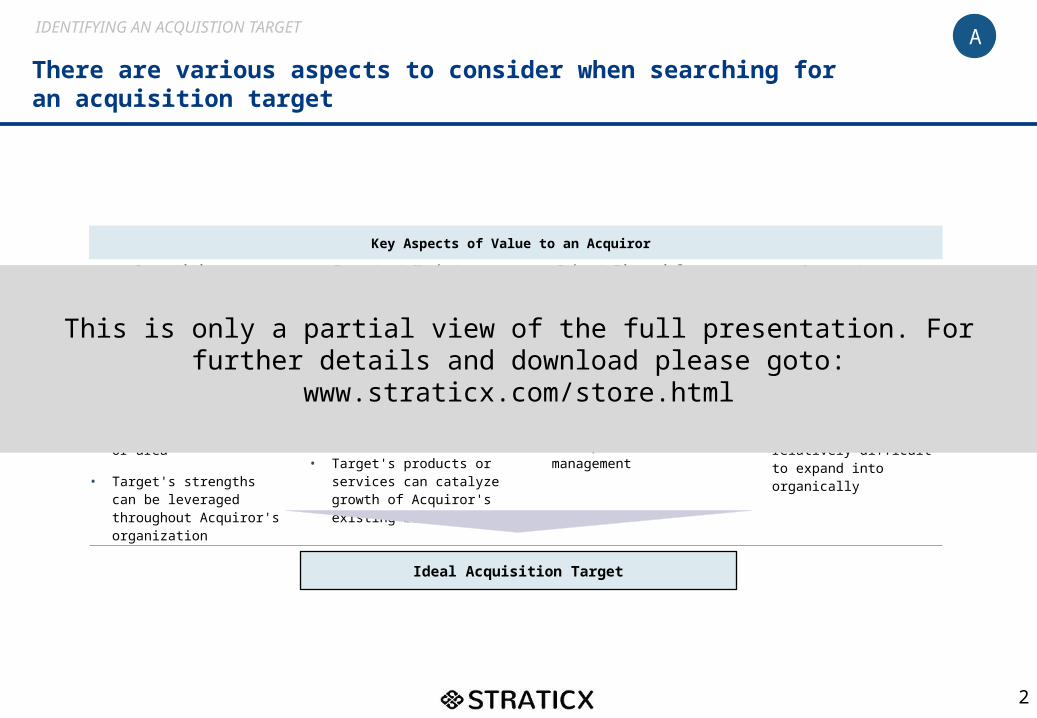

There are various aspects to consider when searching for an acquisition target

IDENTIFYING AN ACQUISTION TARGET

Key Aspects of Value to an Acquiror

Competitive Advantage Important Market

Segment Robust Financial Performance Access to

New Geographies• Strong market position

through large, stable user base or other competitive edge

• Expertise in a particular division or area

• Target's strengths can be leveraged throughout Acquiror's organization

• Operates key commercial platform with potential for strong cash growth

• Market is of key strategic importance in the value chain

• Target's products or services can catalyze growth of Acquiror's existing businesses

• Healthy business with track record of strong cash flows and resilient earnings

• Strong top-line growth trajectory

• Disciplined cost management

• Target has established positions in new or high growth markets where the Acquiror is not present

• These new markets are relatively difficult to expand into organically

Ideal Acquisition Target

A

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

3

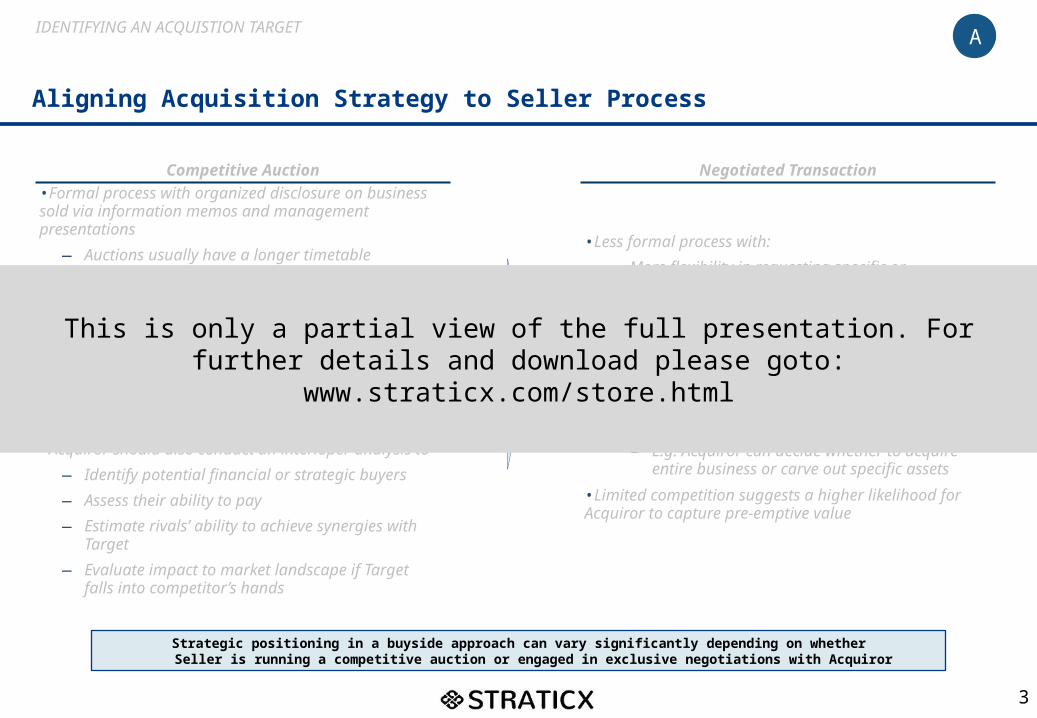

Aligning Acquisition Strategy to Seller Process

IDENTIFYING AN ACQUISTION TARGET

Competitive Auction•Formal process with organized disclosure on business sold via information memos and management presentations

— Auctions usually have a longer timetable— Higher chance that Acquiror’s interest may be

leaked to public•When drawn into a competitive auction, Acquiror can avoid a bidding war by positioning each bid strategically in two-tiered processes

— E.g. bid conservatively in first round to learn more about other bidders and preserve valuation flexibility

•Acquiror should also conduct an interloper analysis to— Identify potential financial or strategic buyers— Assess their ability to pay— Estimate rivals’ ability to achieve synergies with

Target— Evaluate impact to market landscape if Target

falls into competitor’s hands

Negotiated Transaction

•Less formal process with:— More flexibility in requesting specific or

customized information•Greater access to Target’s management team•In a limited negotiation, Acquiror can:

— Push for exclusivity to remove concerns over interloper intervention

— Enjoy more room to structure transaction creatively– E.g. Acquiror can decide whether to acquire

entire business or carve out specific assets•Limited competition suggests a higher likelihood for Acquiror to capture pre-emptive value

Strategic positioning in a buyside approach can vary significantly depending on whether Seller is running a competitive auction or engaged in exclusive negotiations with Acquiror

A

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

4

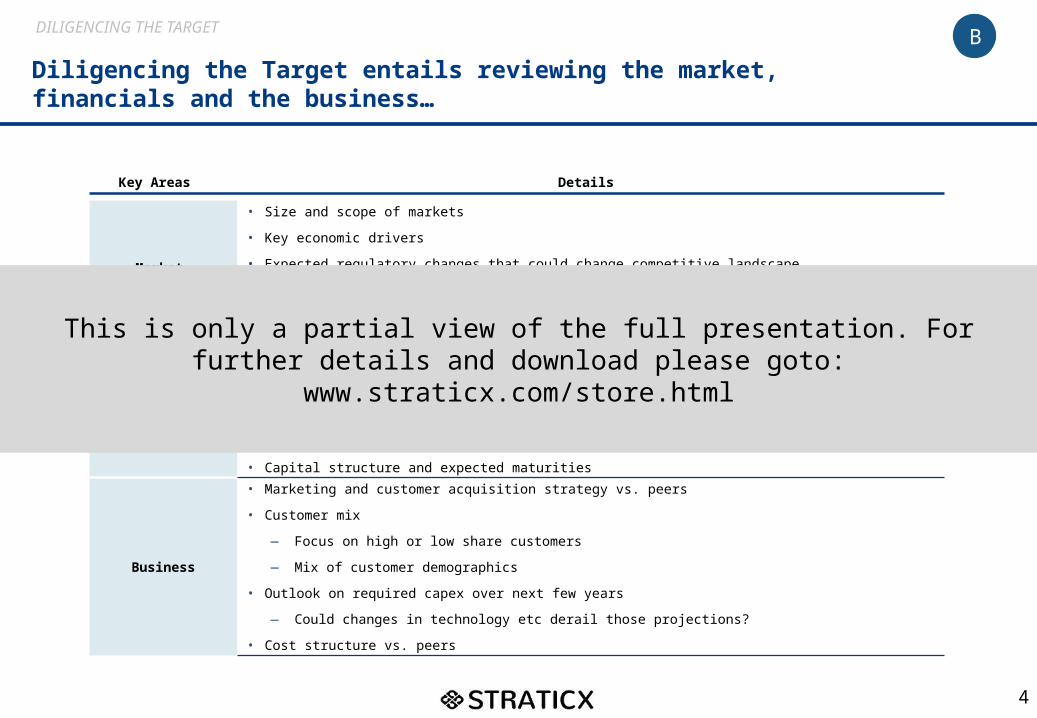

Diligencing the Target entails reviewing the market, financials and the business…

DILIGENCING THE TARGET

Key Areas Details

Market Overview

• Size and scope of markets

• Key economic drivers

• Expected regulatory changes that could change competitive landscape

• Key competitors

— Historical, current and anticipated

— Strengths/weaknesses vs. peers

Financials

• Key performance indicators and expected trends

• Historical audited financials

• Projected financials and near-term

• Variance between historical budgets and actual performance

• Capital structure and expected maturities

Business

• Marketing and customer acquisition strategy vs. peers

• Customer mix

— Focus on high or low share customers

— Mix of customer demographics

• Outlook on required capex over next few years

— Could changes in technology etc derail those projections?

• Cost structure vs. peers

B

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

5

CONTENTS

There are several critical aspects to a well thought-out acquisition strategy for enterprise assets

1. Formulating an Acquisition Strategy

A. Identifying the Acquisition Target and Process

B. Diligencing the Target

C. Evaluating Other Strategic Considerations

2. Overview of Valuation Methodologies

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

6

CONTENTS

There are several critical aspects to a well thought-out acquisition strategy for enterprise assets

1. Formulating an Acquisition Strategy

A. Identifying the Acquisition Target and Process

B. Diligencing the Target

C. Evaluating Other Strategic Considerations

2. Overview of Valuation Methodologies

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

7

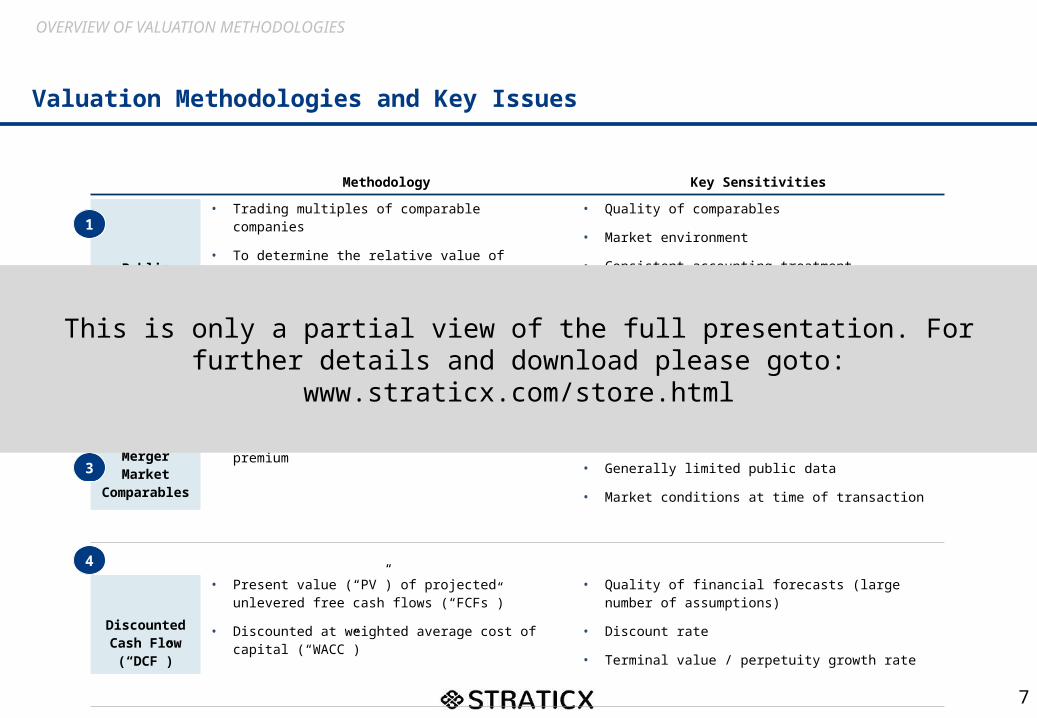

Valuation Methodologies and Key Issues

OVERVIEW OF VALUATION METHODOLOGIES

Methodology Key Sensitivities

Public MarketComparables

• Trading multiples of comparable companies

• To determine the relative value of companies within the sector

• Quality of comparables

• Market environment

• Consistent accounting treatment

• Forward-looking multiples

• Public data

Merger MarketComparables

• Market of comparable transactions

• Takes into consideration acquisition premium

• Quality of comparable transactions

• Historical multiples

• Generally limited public data

• Market conditions at time of transaction

Discounted Cash Flow

(“DCF”)

• Present value (“PV”) of projected unlevered free cash flows (“FCFs”)

• Discounted at weighted average cost of capital (“WACC”)

• Quality of financial forecasts (large number of assumptions)

• Discount rate

• Terminal value / perpetuity growth rate

Pro FormaAnalysis

• Impact of a transaction (growth, margins, credit rating, etc.)

• Assess whether a transaction is accretive / dilutive to EPS

• Near-term vs. long-term impact

• Affected by financing capital structure

• Affected by accounting (purchase price allocation)

• Not indicator of fundamental value

1

2

3

4

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

8

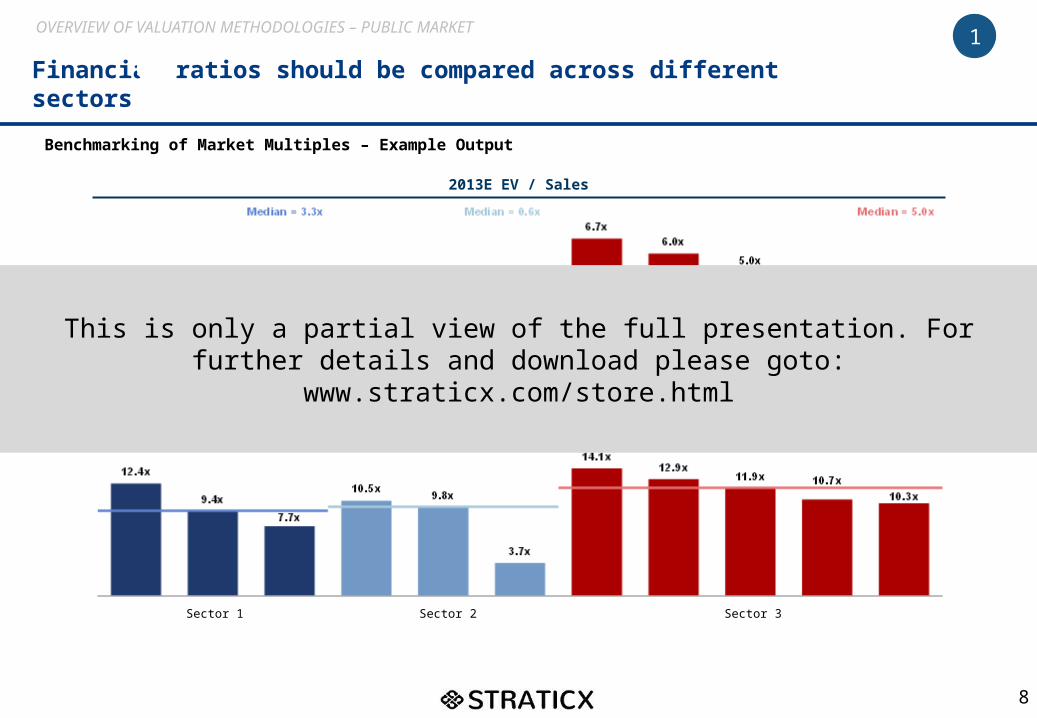

Financial ratios should be compared across different sectors1

2013E EV / Sales

2013E EV / EBITDA

Sector 1 Sector 2 Sector 3

1

Benchmarking of Market Multiples – Example Output

OVERVIEW OF VALUATION METHODOLOGIES – PUBLIC MARKET

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

9

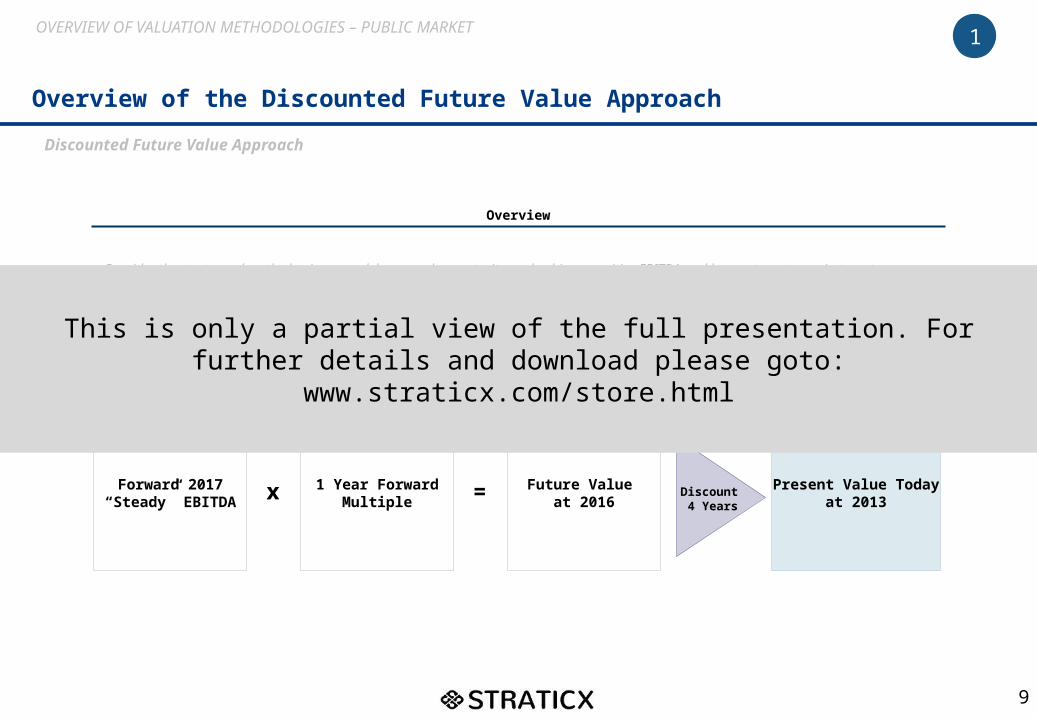

Overview of the Discounted Future Value Approach

Discounted Future Value Approach

•Consider the start-up when the business model approaches maturity, and achieves positive EBITDA and longer-target margin targets•The start-up can be valued with a 1-year forward multiple on future financial metrics based on projected future forward multiples•The resulting valuation is subsequently to today to find the present value of the start-up business

Overview

Illustrative Calculation Methodology

Forward 2017 “Steady” EBITDA

1 Year Forward Multiple

Future Value at 2016

Present Value Today at 2013x = Discount

4 Years

1

1OVERVIEW OF VALUATION METHODOLOGIES – PUBLIC MARKET

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

10

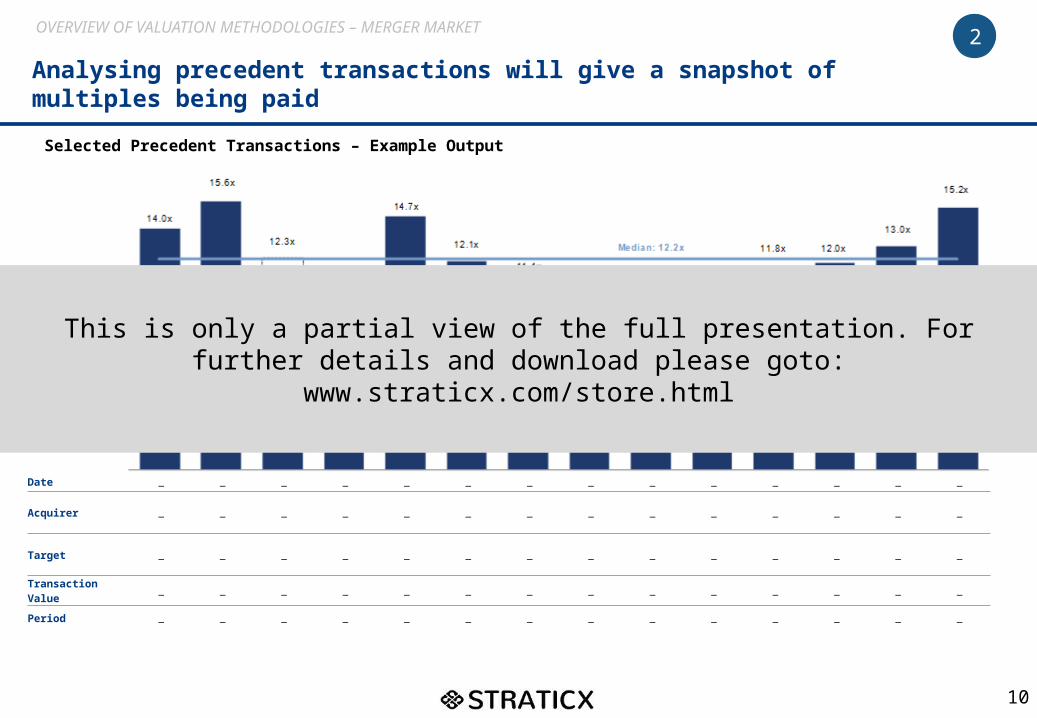

Analysing precedent transactions will give a snapshot of multiples being paid

Date _ _ _ _ _ _ _ _ _ _ _ _ _ _

Acquirer _ _ _ _ _ _ _ _ _ _ _ _ _ _

Target _ _ _ _ _ _ _ _ _ _ _ _ _ _

Transaction Value _ _ _ _ _ _ _ _ _ _ _ _ _ _

Period _ _ _ _ _ _ _ _ _ _ _ _ _ _

2

Selected Precedent Transactions – Example Output

OVERVIEW OF VALUATION METHODOLOGIES – MERGER MARKET

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

11

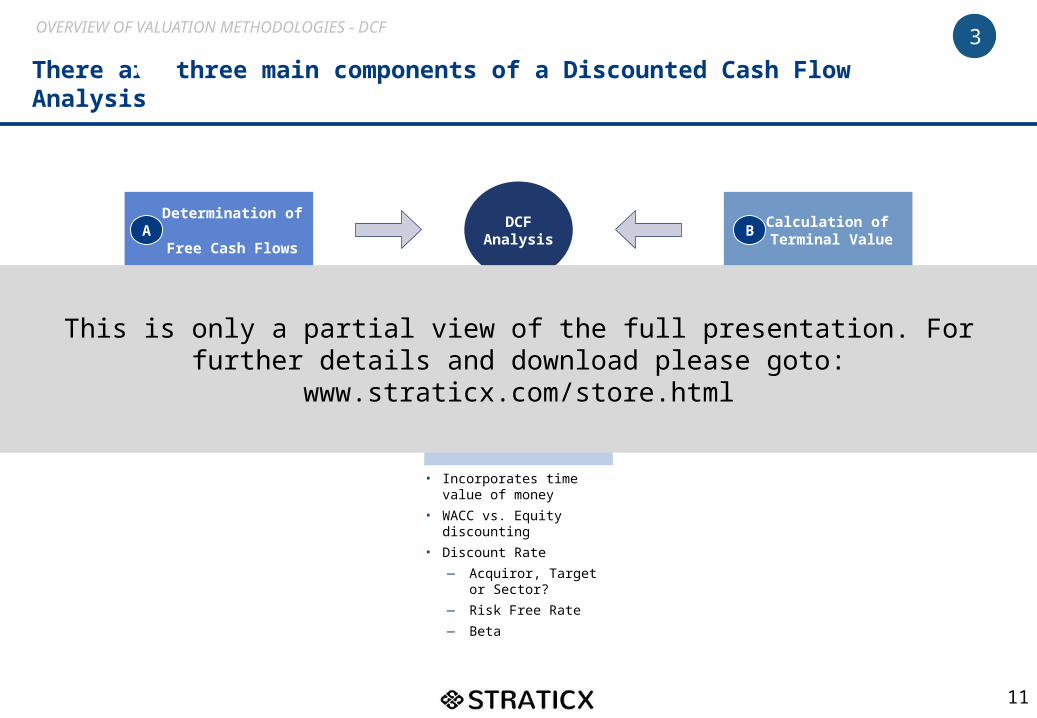

There are three main components of a Discounted Cash Flow Analysis3

Calculation of Discount Rate

Determination of Free Cash Flows

Calculation of Terminal Value

DCF Analysis

• Value of business in projection period

• Projections (5 – 10 years)— Sales growth— Margins— Capex— Change in Working

Capital

• Incorporates time value of money

• WACC vs. Equity discounting

• Discount Rate— Acquiror, Target or

Sector?— Risk Free Rate— Beta

• Value of business / cashflows post projection period

• Exit multiple method• Perpetuity growth method

(steady state)

A B

C

3OVERVIEW OF VALUATION METHODOLOGIES - DCF

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

12

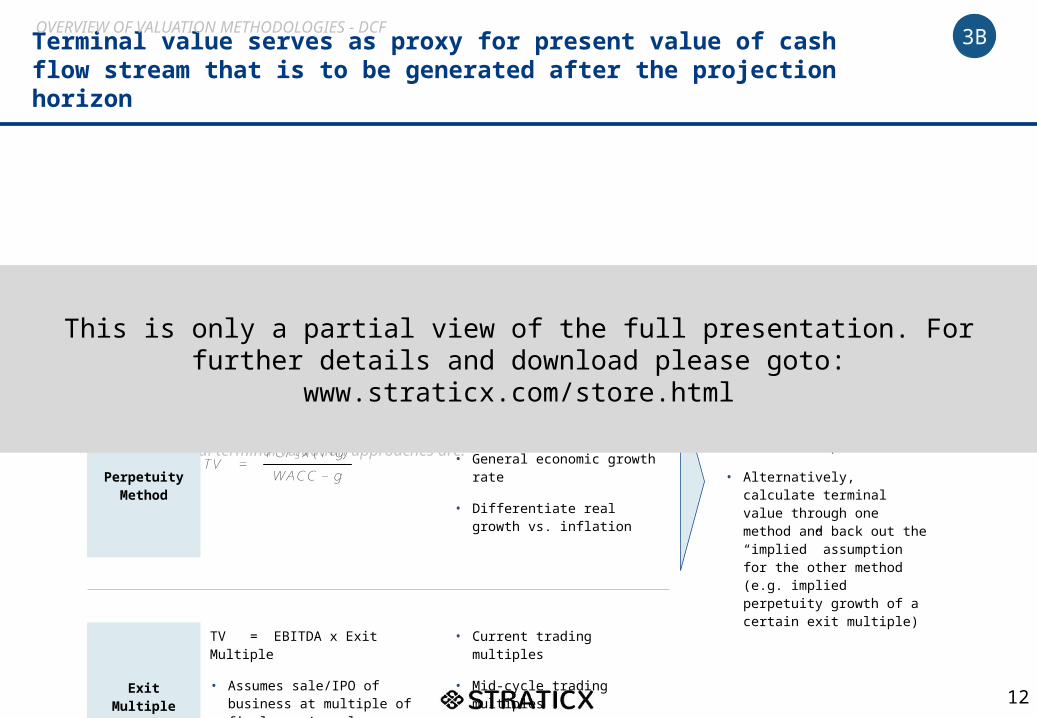

Terminal value serves as proxy for present value of cash flow stream that is to be generated after the projection horizon

Terminal value serves as proxy for present value of cash flow stream that is to be generated after the projection horizon (usually 5 to 10 years)

— Ideally when business is in steady state

Calculate PV of terminal value and add to PV of projected cash flows to arrive at a total value for the company

The two principal terminal valuation approaches are:

Methodology Benchmarks

PerpetuityMethod

• Industry growth rate

• General economic growth rate

• Differentiate real growth vs. inflation

• Compare results to check assumptions

• Alternatively, calculate terminal value through one method and back out the “implied” assumption for the other method (e.g. implied perpetuity growth of a certain exit multiple)

ExitMultiple

TV = EBITDA x Exit Multiple

• Assumes sale/IPO of business at multiple of final year’s sales, EBITDA, EBIT or other metric

• Current trading multiples

• Mid-cycle trading multiples

• M&A multiples

TV =FCF5 x (1+g)

WACC – g

TV =FCF in Year after Final Year

WACC – Growth Rate

3BOVERVIEW OF VALUATION METHODOLOGIES - DCF

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

13

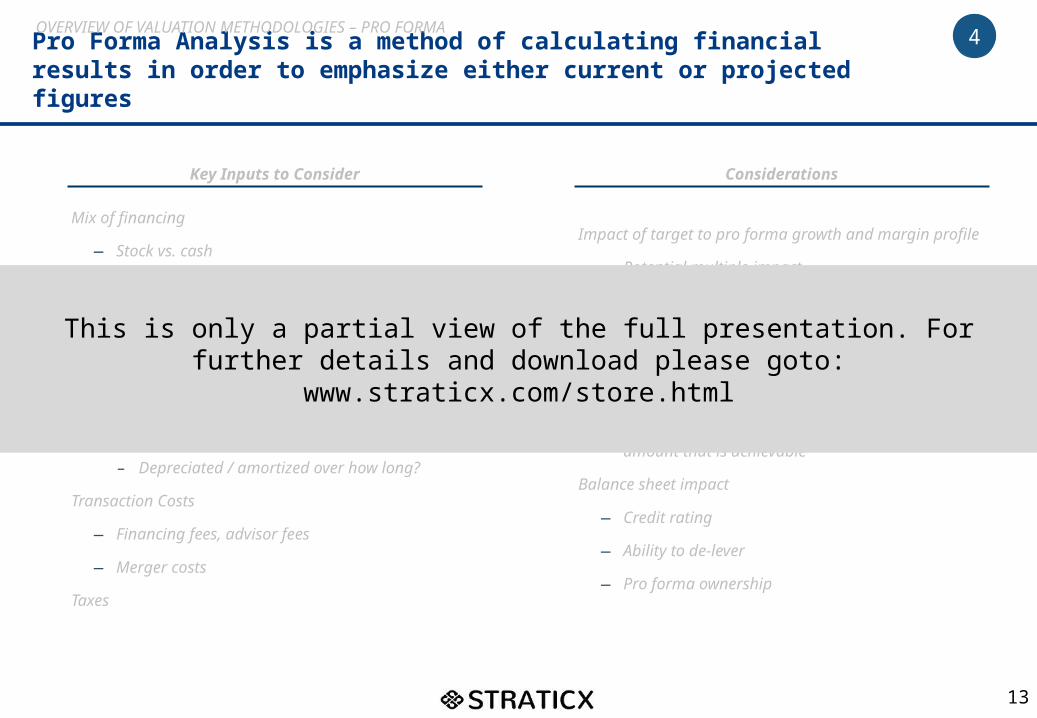

Pro Forma Analysis is a method of calculating financial results in order to emphasize either current or projected figures

OVERVIEW OF VALUATION METHODOLOGIES – PRO FORMA

Key Inputs to Consider

Mix of financing

— Stock vs. cash

Financing Cost (incremental debt to finance the acquisition)

— Interest expense on new debt issued

— Interest income lost on cash used

Accounting Treatment

— Excess purchase price allocated to asset write-up

– Depreciated / amortized over how long?

Transaction Costs

— Financing fees, advisor fees

— Merger costs

Taxes

Considerations

Impact of target to pro forma growth and margin profile

— Potential multiple impact

— Level of diversification vs. product concentration

Synergy Analysis

— Cross-selling opportunity

— Cost savings potential

— Amount required to breakeven (if dilutive) vs. amount that is achievable

Balance sheet impact

— Credit rating

— Ability to de-lever

— Pro forma ownership

4

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

14

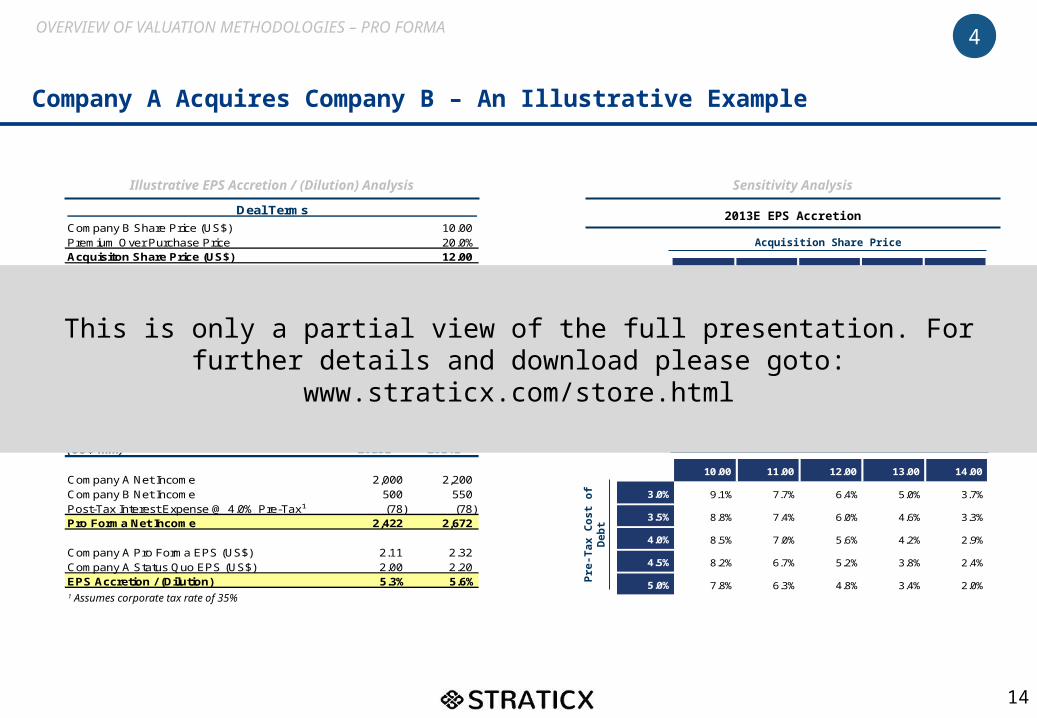

Deal TermsCompany B Share Price (US$) 10.00Premium Over Purchase Price 20.0%Acquisiton Share Price (US$) 12.00Company B Shares Outstanding (mm) 500Implied Takeover Equity Value 6,000

Financing TermsDebt Financing (50%) 3,000Equity Financing (50%) 3,000

Company A Share Price 20.00Company A Pre-Deal Shares Outstanding 1,000Company A Post-Deal Shares Outstanding 1,150

EPS Accretion / (Dilution)(US$ mm) 2013E 2014E

Company A Net Income 2,000 2,200Company B Net Income 500 550Post-Tax Interest Expense @ 4.0% Pre-Tax¹ (78) (78)Pro Forma Net Income 2,422 2,672

Company A Pro Forma EPS (US$) 2.11 2.32Company A Status Quo EPS (US$) 2.00 2.20EPS Accretion / (Dilution) 5.3% 5.6%

Company A Acquires Company B – An Illustrative Example

1 Assumes corporate tax rate of 35%

Illustrative EPS Accretion / (Dilution) Analysis Sensitivity Analysis

2013E EPS Accretion

Acquisition Share Price

Pre-

Tax

Cos

t of D

ebt

2014E EPS Accretion

Acquisition Share Price

Pre-

Tax

Cos

t of D

ebt

4

5.3% 10.00 11.00 12.00 13.00 14.00

3.0% 8.9% 7.5% 6.2% 4.8% 3.5%

3.5% 8.6% 7.1% 5.7% 4.3% 3.0%

4.0% 8.2% 6.7% 5.3% 3.9% 2.5%

4.5% 7.9% 6.4% 4.9% 3.4% 2.0%

5.0% 7.5% 6.0% 4.5% 3.0% 1.5%

5.6% 10.00 11.00 12.00 13.00 14.00

3.0% 9.1% 7.7% 6.4% 5.0% 3.7%

3.5% 8.8% 7.4% 6.0% 4.6% 3.3%

4.0% 8.5% 7.0% 5.6% 4.2% 2.9%

4.5% 8.2% 6.7% 5.2% 3.8% 2.4%

5.0% 7.8% 6.3% 4.8% 3.4% 2.0%

4OVERVIEW OF VALUATION METHODOLOGIES – PRO FORMA

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html

15

This is only a partial view of the full presentation. For further details and download please goto: www.straticx.com/store.html