Embed Size (px)

DESCRIPTION

This topic is basically related to the econometric analysis and techniques used to develop the model for the calculation of expected stock returns taking into the account various fundamental or accounting variables of the respective stock. The model developed is basically an extension of Fama and French 3-factor model but it is for the calculation of return from individual stocks. The variables considered are all fundamental accounting variables. The technique used for the generating this proposed model is an advanced regression technique known as “panel regression technique”. To select the best model, all the four panel regression techniques i.e. Fixed One-Way, Fixed Two-Way Effect, Random One-Way and Random Two-Way Effect techniques have been used. For the development of the model, two econometrics softwares: SAS Enterprise Guide v3.0 and EVIEWS v7.0 have been used extensively. The factors affecting the return according to the model are supported by the theory also. A total of 6 fundamental factors have found to be significantly affecting the expected stock return along with the 3 factors from the Fama and French 3 factors model.

Citation preview

A REPORT

ON

DEVELOPMENT OF MARKET-WIDE STOCK

VALUATION MODEL (EXTENSION OF FAMA &

FRENCH MODEL) AND AN INDUSTRY

ANALYSIS OF IT AND CONSTRUCTION SECTOR

IN INDIA USING THIS MODEL

By

Saurabh Trivedi

10BSPHH011076

A REPORT

ON

DEVELOPMENT OF MARKET-WIDE STOCK

VALUATION MODEL (EXTENSION OF FAMA &

FRENCH MODEL) AND AN INDUSTRY ANALYSIS OF

IT AND CONSTRUCTION SECTOR IN INDIA USING

THIS MODEL

By

Saurabh Trivedi

10BSPHH011076

A report submitted in partial fulfillment of the requirements of MBA

Program of IBS Hyderabad

Submitted To

Project Guide:

Prof. Rajashekhar Reddy,

Marketing Department

Date of Submission: Friday, May 13th

, 2011

IBS HYDERABAD

CERTIFICATE

This is to certify that the thesis titled “Development Of Market-Wide Stock Valuation Model

(Extension Of Fama & French Model) And An Industry Analysis Of IT And Construction

Sector In India Using This Model” is a bonafide work done by Mr. Saurabh Trivedi,

Enrolment No. 10BSPHH011076, in partial fulfilment of the requirements for the award of any

degree and submitted to the Department of Finance & Economics, IBS Hyderabad.

This work was not submitted earlier at any other University or Institute for the award of the

degree.

Project Guide: Project Coordinator:

Prof. Rajashekhar Reddy Dr. Hilda Amalraj

Department of Marketing Dean of Academics

IBS-Hyderabad IBS-Hyderabad

SUMMER INTERNSHIP REPORT 2011

______________________________________________________________________________

IBS-Hyderabad i

I. Acknowledgement

I would take this opportunity to express my sincere gratitude to all the persons for their valuable

assistance and continuous support during my Summer Internship Program (SIP).

I would like to thank Mr. V. Rajanna, Vice President and General Manager, Tata Consultancy

Services, Hyderabad for giving me an opportunity to work with this department.

I would like to thank Dr. V.P. Gulati, Vice President and Head, TCS Business Domain

Academy, for giving me an opportunity to work with this department.

I am also thankful to Mr. J. Chandrasekhar, Academic Relationships Manager, Tata

Consultancy Services, for his helping hand throughout the internship process.

I am grateful to my company guide, Ms. Vasanta Tadimeti, Domain Consultant, TBDA, TCS

for her guidance and support during development of the project. Her inputs, motivation and

suggestions have played a crucial role at every stage in the development of the project.

I would like to thank the entire TBDA team and all my IBS colleagues at TCS who provided

their valuable inputs throughout the internship, which really helped in successful completion of

my project report.

Prof. Rajashekhar Reddy, Department of Marketing, IBS Hyderabad, my faculty guide,

with his continuous guidance throughout the program helped me to complete this project in a

timely and systematic manner.

SUMMER INTERNSHIP REPORT 2011

______________________________________________________________________________

IBS-Hyderabad ii

II. Declaration

This is to certify that the thesis titled ―Development Of Market-Wide Stock Valuation Model

(Extension Of Fama & French Model) And An Industry Analysis Of It And Construction

Sector In India Using This Model” is a bonafide work done by Mr. Saurabh Trivedi, Enrollment

No. 10BSPHH011076, in partial fulfillment of the requirements of MBA Program and submitted

to IBS Hyderabad.

I also declare that this project is a result of my own efforts and that has not been copied from

anyone and I have taken only citations from the literary resources which are mentioned in the

Bibliography/Reference section.

This work was not submitted earlier at any other university or institute for the award of the

degree.

Saurabh Trivedi,

Hyderabad

SUMMER INTERNSHIP REPORT 2011

______________________________________________________________________________

IBS-Hyderabad iii

III. Abstract

This topic is basically related to the econometric analysis and techniques used to develop the

model for the calculation of expected stock returns taking into the account various fundamental

or accounting variables of the respective stock. The model developed is basically an extension of

Fama and French 3-factor model but it is for the calculation of return from individual stocks. The

variables considered are all fundamental accounting variables. The technique used for the

generating this proposed model is an advanced regression technique known as ―panel regression

technique‖. To select the best model, all the four panel regression techniques i.e. Fixed One-

Way, Fixed Two-Way Effect, Random One-Way and Random Two-Way Effect techniques have

been used. For the development of the model, two econometrics softwares: SAS Enterprise

Guide v3.0 and EVIEWS v7.0 have been used extensively. The data sample taken for the model

development is of 42 Indian companies from various sectors have been considered. The main

finding of the project is that the models developed by all the techniques are in line with the Fama

and French 3 factor model and are consistent with each other also. The finally selected model is a

Fixed Two-Way Effect Model which tells that there can be some more fundamental accounting

variables which can be used to calculate the cost of equity or expected stock return. The factors

affecting the return according to the model are supported by the theory also. A total of 6

fundamental factors have found to be significantly affecting the expected stock return along with

the 3 factors from the Fama and French 3 factors model. The model is developed with the help of

Indian companies as the data sample. It means that it can also work for the similar developing

capital markets of other countries. Various panel data tests have been done to select the most

robust model among the 4 techniques. Then this model is used to do the valuation of 4

companies in IT and Construction Sector and it has been found that the model is working in a

fine manner. In this modeling no macroeconomic factors have been considered which can also be

considered. The industry specific models can also be developed using the Panel Regression

technique which is an advanced technique for regression. The model developed is a bit complex

as far as the calculations and time is considered. Also this model does not work for the financial

institutions and banking firms.

SUMMER INTERNSHIP REPORT 2011

______________________________________________________________________________

IBS-Hyderabad iv

Table of Contents I. Acknowledgement ................................................................................................................ i

II. Declaration ........................................................................................................................... ii

III. Abstract ............................................................................................................................... iii

IV. List of Figures ..................................................................................................................... vi

V. List of Tables ..................................................................................................................... vii

VI. List of Abbreviation .......................................................................................................... viii

VII. Company Profile ................................................................................................................. ix

1. Introduction .......................................................................................................................... 1

2. Asset Review and Learning ................................................................................................. 2

3. Asset Development .............................................................................................................. 3

4. Research Project................................................................................................................... 4

4.1 Project Title ...................................................................................................................... 4

4.2 Introduction ...................................................................................................................... 4

4.3 Literature Review ............................................................................................................. 5

4.4 Objectives of the Project .................................................................................................. 8

4.5 Fundamental Variables Identified .................................................................................... 9

4.6 Steps involved in Financial Modeling ............................................................................ 11

4.7 Data Analysis ................................................................................................................. 12

4.8 Methodology Used for Modeling ................................................................................... 16

4.8.1 Modeling Procedure Used by Fama & French ....................................................... 16

4.8.2 Modeling Procedure Used in this Project ............................................................... 16

4.9 Panel Unit Root Tests ..................................................................................................... 18

4.10 Panel Co-integration Test ............................................................................................... 20

4.11 Developing Fixed One-Way Effect Model for Stock Valuation .................................... 21

4.11.1 Introduction to Fixed One-Way Effect Model ........................................................ 21

4.11.2 Analysis and Modeling Using SAS ........................................................................ 22

4.12 Developing Fixed Two-Way Effect Model for Stock Valuation ................................... 27

SUMMER INTERNSHIP REPORT 2011

______________________________________________________________________________

IBS-Hyderabad v

4.12.1 Introduction to Fixed Two Way Effect Model ....................................................... 27

4.12.2 Analysis and Modeling Using SAS (Fixed 2-Way Effect) ..................................... 28

4.13 Developing Random One-Way Effect Model ................................................................ 35

4.13.1 Introduction to Random One-Way Effect Model ................................................... 35

4.13.2 Analysis and Modeling Using SAS (Random One-Way Effect Model) ................ 36

4.14 Developing Random 2-Way Effect Model..................................................................... 40

5. Important Findings from the Models Developed ............................................................... 42

6. Industrial Analysis ............................................................................................................. 44

6.1 Information Technology Sector ..................................................................................... 44

6.1.1 Overview of IT/Service Sector ............................................................................... 44

6.1.2 Porter‘s Five-Force Analysis for IT Sector ............................................................. 44

6.1.3 Contribution of IT Sector to GDP ........................................................................... 46

6.2 Construction Sector ........................................................................................................ 46

6.2.1 Overview of Construction Sector ............................................................................ 46

6.2.2 Porter‘s 5-Force Analysis for Construction Sector ................................................. 47

6.2.3 Contribution of Construction Sector towards GDP ................................................ 48

7. Valuation of Stocks Using the Proposed Model ................................................................ 49

8. Limitations of the Study..................................................................................................... 51

9. Conclusion and Recommendations .................................................................................... 52

10. References and Sources of Data ........................................................................................ 53

SUMMER INTERNSHIP REPORT 2011

______________________________________________________________________________

IBS-Hyderabad vi

IV. List of Figures

Figure 4-1: CAPM Regression Line ............................................................................................... 6

Figure 4-2: Steps Involved in forming an Econometric Model .................................................... 11

Figure 4-3: SAS Data Screenshot ................................................................................................. 14

Figure 4-4: Histogram Normality Test for the Residuals (Fixed 2 Way Effect) .......................... 35

Figure 6-1: IT Service Revenue Growth ....................................................................................... 45

Figure 6-2: Service Sector Growth Rate Graph ............................................................................ 46

Figure 6-3: Revenue Growth of Construction Sector ................................................................... 48

SUMMER INTERNSHIP REPORT 2011

______________________________________________________________________________

IBS-Hyderabad vii

V. List of Tables

Table 4-1: List of Sample Companies .......................................................................................... 13

Table 4-2: Data Summary Statistics ............................................................................................. 15

Table 4-3: Levin, Lin and Chu Unit Root Test ............................................................................. 20

Table 4-4: KAO Cointegration Test ............................................................................................. 21

Table 4-5: Fit Statistics for Fixed One-Way Effect Model ........................................................... 22

Table 4-6: Parameter Estimates for Fixed One Way Effect ......................................................... 25

Table 4-7: Chow Test (F-Test) for Fixed One Effect Model ........................................................ 27

Table 4-8: Redundant Fixed Effect Test ....................................................................................... 28

Table 4-9: Fit Statistics for Fixed 2-Way Effect Model ............................................................... 29

Table 4-10: Parameter Estimates for Fixed One Way Effect ....................................................... 32

Table 4-11: F-test for Fixed 2 Way Effect Model ........................................................................ 34

Table 4-12: Fit Statistics for Random 1-Way ............................................................................... 37

Table 4-13: Variance Component Estimates ................................................................................ 37

Table 4-14: Parameter Estimates for Random One Way Effect Model ........................................ 37

Table 4-15: Hausman Test for Correlated Random Effects .......................................................... 40

Table 4-16: Fit Statistics for Random 2 Way Effect Model ......................................................... 40

Table 4-17: Parameter Estimates for Random 2-Way Effect Model ............................................ 41

Table 4-18: Hausman Test for Random 2 Way Effect ................................................................. 41

SUMMER INTERNSHIP REPORT 2011

______________________________________________________________________________

IBS-Hyderabad viii

VI. List of Abbreviation

ADM Application Development and Maintenance

CAPM Capital Asset Pricing Model

FDI Foreign Direct Investment

GDP Gross Domestic Product

GLS Generalized Least Squares

LLC Levin, Lin and Chu (Test)

LSDV Least Square Dummy Variable

Mkt Market Capitalization

NSE National Stock Exchange

P/E Price to Earnings Ratio

OLS Ordinary Least Squares

SUMMER INTERNSHIP REPORT 2011

______________________________________________________________________________

IBS-Hyderabad ix

VII. Company Profile

Tata Consultancy services (TCS) is one of the leading IT Consultancy companies in the world.

TCS is providing its expertise to many of the world‘s largest companies in the areas of IT

Services, Business Solutions, Outsourcing and Consultancy. TCS provides a comprehensive

range of services & solutions for the clients to focus on their core businesses. Such engagements

require extensive and updated knowledge of client business domain.

TCS has the lineage of Tata Group, one of India‘s largest industrial conglomerates and most

respected brands. TCS offers a consulting-led, integrated portfolio of IT and IT-enabled services

delivered through its unique Global Network Delivery Model™, recognized as the benchmark of

excellence in software development. TCS has over 170,000 of the world's best trained IT

consultants in more than 50 countries. Financial Information: Revenue of over $8.2 billion (fiscal

year 2010-11).

TCS is headquartered in Mumbai, and operates in more than 50 countries and has more than 170

offices across the world. Mr. Natarajan Chandrasekaran is the Chief Executive Officer (CEO)

and Managing Director of the company. TCS is the world‘s first organization to achieve an

enterprise-wide Maturity Level 5 on CMMI® and P-CMM® based on SCAMPISM, the most

rigorous assessment methodology. TCS helps clients optimize business processes for maximum

efficiency and galvanize their IT infrastructure to be both resilient and robust. TCS offers variety

of solutions like IT Services, IT infrastructure services, Enterprise solutions, Consulting,

Business process outsourcing and Business process outsourcing.

TCS‘ global alliance mission in partnering with organizations is to ensure that TCS and the

Partner Organization derive the maximum benefit of our relationship, in terms of services and

products growth. TCS has the depth and breadth of experience and expertise that businesses need

to achieve business goals and succeed amidst fierce competition. TCS helps clients from various

industries solve complex problems, mitigate risks, and become operationally excellent. Some of

the industries it serves includes Banking and financial services, Insurance, Telecom,

Government, Media and information services.

SUMMER INTERNSHIP REPORT 2011

______________________________________________________________________________

IBS-Hyderabad x

Above 40% of the revenue generated by the gamut of services provided by TCS is contributed by

the Banking, Financial Services and Insurance (BFSI) vertical. More than 33% of the total

employees of TCS are working on the BFSI projects. Hence in view of the role of BFSI and the

employees working on such projects, Financial Technology Centre (FTC) was formed.

To build such domain knowledge, TCS piloted FTC in July 2005 focusing on Banking and

Financial Services (BFS). The success of FTC prompted expansion into other industries in mid-

2007, including Insurance, e-governance, and Telecom, Life sciences & Healthcare, Energy

resources & utilities, Retail, Manufacturing, Hi-tech, and Travel Transportation & Hospitality.

FTC got re-christened as TCS Business Domain Academy (TBDA) during April 2009 and is

now creating assets for other industry.

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 1

1. Introduction

This report is an analysis for all the work done at the TCS TBDA department, under the SIP

program of IBS College, Hyderabad. The report starts with discussing the working of TBDA

asset development processes. It critically highlights the important drivers of the process. The

project consists of the following three tasks:

Asset Review and Learning

Asset Development

Research Project

For doing the asset review and development stringent TCS Quality norms were followed and

there was a strict adherence to the Integrated Quality Management System (iQMS TM

). These

tasks have been carried out as per schedule.

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 2

2. Asset Review and Learning

In this first phase, the review of the existing Assets is done for further additions and error

rectifications, if any. Asset review requires understanding the asset in a comprehensive way.

Asset learning and related background reading is a prerequisite to asset review. The major

objective of the asset review is to check for the consistency of subject in terms of concept and

matter. Based on asset learning, further additions to the existing asset are done if any

drawback in the conceptual understanding of asset is found.

The course assigned for review is ―Program in Equity Research and Trading‖. It has been

restructured after the merger of 2 previous certification courses for the new Business

Analysis Certification Program. This course gives the basic details about the various aspects

of the Equity Research and Electronic Trading like Technical and Fundamental Analysis,

Equity Risk Management, Electronic Trading, Algorithm Trading, Accounting of Stocks,

Direct Market Access, NASDAQ and NYSE Trading, Custody and Asset Servicing,

Commodity Online Trading. A total of 17 chapters had been assigned along with their

corresponding PowerPoint Presentations for review. The list of tasks done during the Asset

Review is mentioned as below:

In most of the chapters, some modification (addition of more points) was done as per the

requirements.

The change in the sequence of the chapters in the above assigned course has been done.

A great care has been taken to remove the plagiarism. All that have been removed and

rewritten freshly to remove the plagiarism almost completely.

All the 17 Power Point Presentations for the above chapters have been reviewed.

Re-formatting of all the Chapters and the corresponding PPTs have been finished for the

above mentioned Certificate Program as per the new template of TCS Business Domain

Academy.

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 3

3. Asset Development

Asset development deals with developing the new certification course for the TCS

employees. A course outline for the subject is prepared and then chapters are prepared

following the course outline. The work done in this phase is the main contribution to the TCS

Business Domain Academy. Through this phase, new Assets or the certification courses are

being added in the Organization‘s already existing assets.

Following is the list of tasks performed during Asset Development Phase:

One Complete Chapter on Credit Management has been re-written completely.

The task of preparing questions for the US Mortgage Course has been completed. Four

chapters were assigned for the course. A total of 85 questions have been developed for

these chapters.

The course assigned for the Asset Development is United Kingdom Mortgage Industry. A

total of five chapters have been developed for this course.

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 4

4. Research Project

4.1 Project Title

Development of Market-Wide Stock Valuation Model (Extension of Fama & French Model)

and an Industry Analysis of IT and Construction Sector in India Using the Proposed Model.

4.2 Introduction

The Domain of this project is Financial Econometrics. Market Anomalies have always been

the subject of great interest of financial research scholars as these create huge opportunities

for high gains that can be earned by profitable investment decisions based on historical

information. This project also serves the same purpose and interest. The project focuses on

developing a Market-Wide Stock Valuation Model to calculate the expected return from a

stock. This project is basically an extension of Fama and French 3-factor model which itself

is an extension of Capital Asset Pricing Model (CAPM). In 2004, Fama and French suggested

that there can be various other factors which can affect the stock returns. In this project, the

focus will be to find and study the various other fundamental factors which affect the

expected return from a stock which were not taken into consideration in 3-factor model.

Financial econometrics in stock valuation is focused mainly on developing models that can

be used with same effect for all potential firms under normal financial circumstances. These

models are used to determine the stock return of a company with greater accuracy. The

approach used for the generation of model is an advanced technique used in the field of

econometrics. This approach is of panel regression technique which is used for panel data.

The panel regression technique is one of the most advanced regression technique which is

used very extensively if data allows doing so. It is still in evolving stage. In simplest terms,

―panel data‖ refers to the pooling of observations on a cross-section of households or

individuals, countries, firms over several time-periods. Panel data has lots of advantages of

simple cross-sectional data or the time-series data.

In this modeling procedure, the main objective is to develop a market-wide stock valuation

model which can calculate the expected stock return of an individual stock with the help of

various fundamental variables which will be discussed in details in the following sections.

This model will basically tell how these fundamental accounting variables of a company are

related to its expected return.

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 5

The model that will be developed will be actually a ―Risk-Based‖ model just like the CAPM

or Fama French 3-factor model. The coefficient or the slope attached to the independent

fundamental variables considered actually indicates about the risk involved with that variable

when an investor consider that fundamental variable for his investment decision for a

particular stock. The another category of general stock valuation model is discounted cash

flow models like dividend discount model, FCFE model, which do not consider the risk

factor.

After the development and the statistical testing of the model, the second phase of the project

is the practical implementation of the model developed. In the second part, the main objective

will be to check for the practical implementation of the proposed model. The valuation of 2

companies in 2 main Indian Sector: Information Technology and Civil Engineering

(Construction) will be done by both the models after the complete Industrial Analysis of the 2

concerned Sectors.

4.3 Literature Review

Stock valuation has primarily been focused on the use of CAPM which was developed by

William Sharpe (1964), John Lintern (1965) and others. This model used the systematic risk

i.e. variation to the market and the risk free rate to develop a simple linear model for expected

stock return.

The CAPM equation for expected stock returns is shown as below:

E (Ra) = R+ βim (E (Rm) - Rf) (Eq-4.1)

Where,

Rf = Risk Free Rate

βim = Beta of Security

E (Rm) = Expected Market Return

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 6

The regression function of CAPM equation is shown in following Figure 4-11:

Figure 4-1: CAPM Regression Line

Miller (1999) stated that CAPM has not only emphatically explained new and powerful

insight into the nature of the risk involved, but also through its empirical investigation

contributed to the development of the finance and to major innovation in the field of financial

econometrics.

Following the study of CAPM, there have been various empirical studies that tested this

model and in later years it has been found that there are influences beyond the market which

affect the stock returns. These studies suggested that single factor model is not that capable to

calculate and predict the expected return of an asset.

Fama and French (Journal of Finance, Vol.XLVII, No.2, June 1992) developed a 3-Factor

model in their landmark paper published in 1992. In their study, they empirically examined

the joint role of market return, firm‘s size (market capitalization), firm‘s book-to-market

equity (BE/ME) ratio, in the cross-section of average stock returns using a multifactor

approach.

Fama and French, through their Research, concluded that the systematic risk represented by

security beta (β) does not have any significant effect on the expected stock return. They

actually found in their observations and analysis that there was a simple linear relation

1 Source: www.images.google.com

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 7

between the average stock returns and the market β during the early periods of 1926-1968 but

this relation became very weak in the later periods of 1963-1990.

Fama and French took three main factors in their analysis. These were relative size of the

firm (market capitalization), relative book-to-market value ratio and beta of the assets. In this

paper, they showed that the relative size of the firm and the book to market ratio were highly

correlated with the expected stock returns in their considered time frame 1963-1990.

The Fama and French 3-factors model is shown as below:

E (Ra) = α+ β1 (MKT) +β2 (SMB) +β3 (HML) (Eq-4.2)

Where,

MKT =Excess Return on Market Portfolio

SMB=the difference in returns between small-capitalization stocks and large-

capitalization stocks (size)

HML=the difference between the return from High Book-to-Market Value Firms

and that from Low Book-to-Market Value Firms

Following is the brief description of SMB and HML factors:

The SMB Factor: SMB is designed to measure the additional return investors have

historically received by investing in stocks of companies with relatively small market

capitalization. This additional return is often referred to as the ―size premium.‖

The HML Factor: HML has been constructed to measure the ―value premium‖ provided

to investors for investing in companies with high book-to-market values (essentially, the

value placed on the company by accountants as a ratio relative to the value the public

markets placed on the company, commonly expressed as B/M).

At present, there is considerable evidence from other world markets in support of Fama and

French 3-Factor model. However, much of the study has been limited to developed capital

markets. Kothari, Shanken and Sloan asserted that any robust multi-factor model must be

tested to work under a variety of conditions. Hence, there is a need for sample tests,

especially for emerging capital markets like that of India. Indian capital market is grossly

under-researched as far as the applicability of these CAPM or multi-factor models are

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 8

concerned. There have been some empirical studies based on Fama and French model in

Indian markets. Some of these studies have suggested that Fama and French have worked

successfully in Indian context (Vaidyanathan and Chava, 1997; Marisetty and Vedpurishwar

2002; Mohanty, 1998, 2002; Sehgal, 2003; Connor and Sehgal, 2003). On the other hand, a

recent study carried by Manjunatha and Mallikakarjunappa (2006) reveal confounding

relationship among factors viz., market, size, and book-to-market (BE/ME) ratio and

portfolio return (dependent variable).

Fama and French (2004) suggest that there are multiple factors besides beta that impact stock

valuation and that are anomalous with the efficient market hypothesis.

There have been various attempts to develop a model which can be more robust and can be

used in more general sense. The more the complicate is the stock valuation model; the more

is it able to explain the complex business situations and its anomalies. A similar attempt was

made in paper named ―An Investigation of Stock Valuation Models: Market-wide & Industry

Factors” (Gary Mingle et. al, Golden Gate University, 2005).” The techniques used in this

paper were not adequate to develop a statistically justified and a more robust model.

The methodology used by Fama and French was more useful for the valuation of portfolios.

The CAPM is used extensively for individual stocks to calculate the expected stock return.

There has always been a need to develop a model which is capable of calculating the

expected stock returns from an individual stock. In a working paper on Estimation of

Expected Return: CAPM vs. Fama and French- Jan Bartholdy and Paula Peare—CAF,

2004(WP Series No.176), an attempt was made to modify the Fama and French 3-factor

model so that it can be used for individual stocks successfully.

The research on analyst forecast changes (Stickel 1991) and accruals (Sloan 1996) suggests

that there are many other factors which can act as an indication of earnings quality and are

not fully understood or factored into the valuation models as yet. These studies act as the

motivation for the base of this research project.

4.4 Objectives of the Project

The main objectives of the research project are mentioned below:

To study and identify the various fundamental variables which can or affect the expected

return of a stock.

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 9

To develop a quantitative panel regression model using all the 4 techniques of panel

regression.

To identify which of these factors have the most predictive and explanatory power.

To do a brief industry analysis of information technology and construction industries

taking into consideration their role in Indian economy.

To find the intrinsic value of the stock using the above developed model.

4.5 Fundamental Variables Identified

The first objective has been completed by going through the various research papers, Journals

of finance, and fundamental analyst‘s reports. Through these sources and other analytical

studies, finally eight fundamental accounting variables have been identified, which can have

some effect on the expected stock returns that will be analyzed in modeling procedure. Three

of these variables are same as that in CAPM and Fama & French 3-factor model.

The rationale behind selecting the fundamental accounting variables is that these are the

numbers which may have the direct effect on an investor‘s investment decision. These

variables actually reflect the risk involved in investing in a particular firm, though it is not

always quite obvious. The fundamental analysis is always based on these accounting

variables only.

A brief description of all these variables along with their source has been discussed below:

Size: Market Equity (ME) stands as the proxy for the size of a firm. It is also termed as

the market capitalization which is equal to the product of market price per share and

number of shares outstanding. This factor has already been researched and analyzed by

many financial researchers especially, by Fama and French in 1992. Fama and French

concluded in their studies that there is a strong negative correlation between the size of a

firm and average expected stock returns. The results of their model supported the theory

that small cap companies outperform the big cap companies as far as the average

expected return is concerned. It means that there is a negative relation between market

capitalization (size) of a firm and the average stock return from that particular stock.

Book-to-Market Ratio: The book-to-market ratio attempts to identify undervalued or

overvalued securities by taking the book value and dividing it by market value. In general

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 10

term, if this ratio is greater than one, then the stock is undervalued otherwise it would be

overvalued. Fama and French in their analysis showed that there seemed to be a strong

positive correlation between the average stock return and the BE/ME ratio in their

considered time-frame for the sample. This clearly supported the theory that an investor

higher returns from the value stocks (high BE/ME ratio) and this expectation is lower in

case of growth stocks (low BE/ME ratio).

Net Sales: This factor has been taken as a proxy for the prediction of average expected

stock returns by going through two or three different research papers. (i. Revenue and

Stock Returns- Narasimhan Jegadeesh & Joshua Livnat, 2004; ii. The Impact of Sales

and Income Growth on Profitability and Market Value Measures in Actual and Simulated

Industries- William C. House, University of Arkansas Michael E. Benefield, University of

Arkansas,1995). Apart from these sources, many fundamental analysts consider that the

sales growth of a company tends provide a positive impact on the expectation of an

investor from that particular stock.

P/E Ratio: When it comes to valuing a stock, the price/earnings ratio is one of the oldest

and most frequently used metrics. Although, it is a simple indicator to measure but it is

actually quite difficult to interpret. It is extremely informative in certain situations, while

it is next to meaningless other times. Fama and French suggested in their original paper

(1992) that, it can be an important accounting variable which can impact an investor‘s

expectations of return from a particular stock. There has been various research and studies

to justify it as a factor for the stock valuation.

Dividend Payout Ratio: There have been various arguments by different research

scholars regarding the effect of dividends on the stock prices. Dividend-discount models

supports the theory that the stock prices are determined by the amount of dividend paid

by a company. It is always expected by an investor that the stock of a company which is

giving high dividends must be available at discount price. A study has been conducted by

Fischer Black and Myron Scholes, Massachusetts Institute of Technology (MIT) to

develop a model which can show the effect of dividends paid by the company on its stock

price. In this project, the factor taken is dividend payout ratio rather than dividends as

dividends are absolute figures and are not comparable whereas, payout ratio can show the

relative effect and thus it is more interpretable. Lamont (1998) suggests that the dividend

payout ratio, defined as the ratio of dividends per share to earnings per share, has

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 11

predictive power for future stock market returns. In particular, he argues that the dividend

payout ratio should be positively correlated with future returns, since high dividends

typically forecast high returns whereas high earnings typically forecast low returns.

Leverage Effect (Debt-to-Equity Ratio): A levered company is always considered as a

risky investment by any rational investor. More the leverage of a company is, more risk is

associated with that particular stock. Due to this higher risk involved in that stock, the

investor expects higher return from the stock.

Operating Profit to Book Value: The earnings ratios have also been an indication about

the performance and financial condition of any firm. EBIT or the operating profit can be

an important factor for stock valuation. Fundamental analysts of various equity research

firms emphasize seriously on this number for any company. To make it more

interpretable, in this analysis, the ratio operating profit to book value will be considered.

Excess Return on Market: It is already a much researched variable. In CAPM model, it

was the only factor considered for calculating the expected stock return. Later, Fama and

French also included it in their 3-factors model. It is equal to the difference between the

market return and the annual risk free rate of return.

4.6 Steps involved in Financial Modeling

Although there can be various different ways to go about the process of model building, a

logical and valid approach would be to follow the steps described in Figure 4-22:

Figure 4-2: Steps Involved in forming an Econometric Model

Throughout the whole modeling, a great care has been taken to follow all these steps. As far

as the first 2 steps are considered, these have been already discussed in ‗literature review‘ and

2 Chris Brook, 2

nd e, Introductory Econometrics for Finance, 2008

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 12

‗fundamental variables identified‘ sub-sections. Rest of the steps will be discussed in detail in

following sections.

4.7 Data Analysis

Initially, the data for around 80-90 companies was collected from the Capitaline Database

and CMIE‘s Prowess database. The data of all the 3 financial statements (balance sheet,

income statement, and cash flows) of a company was collected for the time-frame of 10 years

from 2001-2010. The monthly data of stock prices of all these firms was also collected to

calculate the average return of that stock. The source taken for the collection of stock prices

was BSE and the yahoo finance online data.

Some of these firms whose book values were negative in any year in the considered time

frame were removed from the sample for the sake of data smoothening and better analysis.

The main reason to remove the companies with negative book value was that this model is to

be developed for normal financial situations. The firms with negative book value suggest that

their financial condition is pretty critical. Such firms could have involved the extreme values

in data points due to which these firms have not been included in final data sample. The firms

whose data was inconsistent and large number of extreme values were there have also been

removed from the final sample. The banking firms and the financial firms are also excluded

from the final sample because their fundamental variables have totally different

interpretations.

All the data used in this project is of secondary in nature and taken from public domain

sources mentioned above.

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 13

Following are the main points of Data Analysis:

The final Sample considered for the modeling procedure is of 42 firms and time frame of

10 years. The name of the companies is listed in following Table 4-1:

1.ACC

2.Apollo Tires

3.Ashok Leyland

4.Asian Paints

5.BEL

6.Bharti Airtel

7.BHEL

8.BPCL

9.Castrol India

10.Cipla Ltd

11.GAIL

12.Gammon India

13.GlaxoSmithKline

14.Grasim Industries

15.HCL Technologies

16.HimachalFuturistic Communications Ltd

17.Hindalco

18.HPCL

19.HUL

20.Infosys Technology

21.IOCL

22.ITC Ltd

23.Jindal Steel & Power ltd

24.Mahindra & Mahindra Ltd

25.Maruti Udyog Ltd

26.NIIT Ltd

27.NTPC Ltd

28.ONGC Ltd

29.Polaris Software Ltd

30.Ranbaxy Labs Ltd

31.RIL

32.SAIL

33.Sterlite Industries Ltd

34.Sun Pharma Ltd

35.Tata Motors

36.Tata Steel

37.TATA Teleservices

38.TCS

39.TITAN Industries Ltd

40.UNITECH Ltd

41.Wipro Ltd

42.Zee Enterprises Ltd

Table 4-1: List of Sample Companies

The calculations of all the variables as mentioned above has been done for all the

companies for each year from Jan‘01 to Dec‘10 with the help of financial statements of

these companies. The calculations of the monthly Stock Returns has also been done for

each company and then the average has been taken for each year. This Historical return is

the ―dependent variable.‖

The data that has been considered will be arranged in panel form in both the econometric

software: SAS enterprise guide v3.0 and EVIEWS v7.0.

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 14

The screenshot of the SAS for the data used for the analysis is shown in the following

Figure 4-3:

Figure 4-3: SAS Data Screenshot

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 15

Following Table 4-2 shows the Statistic summary of the data sample taken in Eviews:

Workfile Statistics

Date: 02/04/09 Time: 03:45

Name: WORKED EVIEWS FILE

Number of pages: 1

Page: Untitled

Workfile structure: Panel - Annual

Indices: CROSSID x DATEID

Panel dimension: 42 x 10

Range: 2001 2010 x 42 -- 420 obs

Object Count Data Points

Series 12 5040

Coef 1 750

Total 13 5790

Table 4-2: Data Summary Statistics

Hence, the total number of panel observations is 42*10=420 and the total data points are

420*11=4620 (including the time-series id and cross-sectional ids).

The sample size taken for the modeling is quite sufficient to run regression. The

necessary condition of Normality has been taken care in the considered sample.

The panel data that will be used for the modeling is a balanced panel data. A balanced

panel is one which has same number of time-series observations for each cross-sectional

unit.

The data was first arranged in an excel file and then it was transferred in SAS Enterprise

Guide v3.0 for the analysis. For the panel data arrangement, the time-series code and the

cross-sectional codes have also been assigned. For the time-series for the year 2001 to

2010, the time-series id assigned is from 101 to 110 respectively. For the companies, the

cross-sectional ids taken are from 1 to 42.

For some of the variables, natural log transformation has been done just to normalize the

data for all the variables. It helps in increasing the normality of data if there is lot of non-

normality amongst the variables. The variables which are transformed into their natural

log are market capitalization, net sales, book-to-market ratio and P/E ratio. Even in Fama

and French, they took the log for market capitalization and BE/ME Ratio. The variables

selected for the log transformation are being finalized by running several regressions

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 16

using different combination of log transformation. The better combination is finally

selected.

4.8 Methodology Used for Modeling

The technique that will be used for modeling is a bit complicated regression technique known

as panel regression technique. For generating and the testing of the model, 2 advanced

econometric software are used extensively. These are SAS Enterprise Guide v3.0 and

EVIEWS v7.0.

4.8.1 Modeling Procedure Used by Fama & French

Fama and French test involved a 2-step estimation procedure: First, they estimated the betas

(slopes or coefficients) in separate time series regressions for each firm (around 4000 firms)

and then, for each separate point in time, a cross-sectional regression of the excess returns on

the betas was conducted by them which then looked like as shown in following equation:

E (Rit) =E (R0t)+λMKTi*βMKT+λSMBi*βSMB+λHMLi*βHML (Eq-4.3)

Actually, Fama and French proposed estimating this second stage (cross-sectional) regression

separately for each time-period, and then taking the average of the parameters estimates to

conduct the hypothesis testing. It was a very cumbersome approach. The regression technique

used in their whole analysis was Ordinary Least Square (OLS) technique which is the most

basic technique of regression analysis. Though OLS is one of the most unbiased regression

techniques, there are several disadvantages when its application to panel data is concerned.

4.8.2 Modeling Procedure Used in this Project

The major and a very important part of the analysis of Fama and French 3-factor model tests

was that the betas that they used in the second stage was not the beta of the individual firms

rather it was the average beta of the portfolios that they made according to market

capitalization and book-to-market ratio. There were 6 portfolios in their analysis. Many

academicians use CAPM for calculating the returns for individual stock returns whereas for

portfolios‘ return calculation the Fama and French Model are preferred. In this paper, the

technique of panel regression will be used for modeling of Stock Valuation Equation for

Individual Stock Returns. Though, there are its own advantage of a valuation model used for

portfolios but it is always preferred that the model must be able to calculate the expected

stock return of an individual stock. There have already been some research by many scholars

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 17

in which they have tried to modify or interpret the Fama and French model for individual

stocks (working paper on Estimation of Expected Return: CAPM vs. Fama and French- Jan

Bartholdy and Paula Peare—CAF, 2004).

The situation often arises in financial modeling where one has data comprising both time

series and cross-sectional elements, and such a dataset would be known as a panel of data or

longitudinal data. A panel of data embodies the information across both time and space

(cross-sections).

Econometrically, the setup of panel data regression model can be represented as below:

Yit = α+∑Nk=1 βk*Xit+uit (Eq-4.4)

Where,

Yit is the dependent variable, α is the intercept term, β is a (k * 1) vector of parameters

to be estimated on the exploratory variables, and Xit is a (1 * k) vector of observations

on the explanatory variables, t= 1,…..,T; i=1,2,…….,N.

The simplest way to deal with such data would be to estimate a pooled regression, which

would involve estimating a single equation on all the data together, so that the dataset for y is

stacked up into a single column containing all the cross-sectional and time-series

observations, and similarly all of the observations on each explanatory variable would be

stacked up into single columns in the X matrix. Then this equation would be estimated in the

usual fashion using OLS.

While it is indeed a simple way to proceed, and requires the estimation of few parameters

possible, it has some severe limitations. Pooling the data in such a way implicitly assumes

that the average values of the variables and the relationships between them are constant over

time and across all of the cross-sectional units in the sample.

The approach used by the Fama and French was a 2 step process in which they separately

estimated the time-series effects for each cross-sections (firms) and then the estimated

parameters were used as the independent variables and were regressed with the same

dependent variable i.e., the historical stock returns. But it is a very tedious approach and also

the technique is OLS which is bit sub-optimal for such type of analysis. If one is fortunate

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 18

enough to have a panel of data at the disposal; there are important advantages to making full

use of this rich structure which are shown as below:

First, and perhaps most importantly, one can address a broader range of issues and tackle

more complex problems with panel data than would be possible with pure time-series or

pure cross-sectional data alone.

Panel data give more informative data, more variability, less collinearity among the

variables, more degrees of freedom and more efficiency.

Third, by structuring the model in an appropriate way, one can remove the impact of

certain forms of omitted variables bias in regression results.

Controlling of Individual Heterogeneity is achieved in Panel Data. Panel data suggests

that individuals, firms, states or countries are heterogeneous. Time-series and cross-

section studies not controlling this heterogeneity run the risk of obtaining biased results.

Panel data are better able to study the dynamics of adjustment. Cross-sectional

distributions that look relatively stable hide a multitude of changes. This drawback is

overcome in panel data.

Before applying any of the panel techniques, at first the data will be tested by some available

panel data test procedures which are discussed in following sections.

4.9 Panel Unit Root Tests

It is very important for any time-series data to pass this test. A unit root test tests whether a

time-series variable is non-stationary. Recent literature suggests that the panel-based unit root

tests have higher power than those based on individual time series. For the testing of the unit

root in a panel data, Levin, Lin and Chu (LLC3) Test will be used using the EVIEWS v7.0.

The null hypothesis is that each individual time series contains a unit root against the

alternative that each time series is stationary.

LLC consider the following basic Augmented Dickey-Fuller (ADF) specification:

∆yit = αyit-1+∑Pj=1 βij∆yit-j+Xit

’δ+εit (Eq-4.5)

Where the assumption is that α=ρ-1 (ρ are the autoregressive coefficients). So, the null

hypothesis of the test is written as:

3 For details, please see Baltagi, Econometric Analysis of Panel Data 3e,Willey & Sons, 2005, pp. 240

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 19

H0: α = 0

H1: α < 0

The LLC test is performed for each of the 9 variables (both dependent and independent).

Following Table 4-3 shows the LLC Unit Root Test Results for each of those variables:

Null Hypothesis: Unit root (common unit root process) is present.

Date: 04/29/2011 Time: 16:04

Sample: 2001 2010

Exogenous variables: Individual effects

User-specified lags: 1

Newey-West automatic bandwidth selection and Bartlett kernel

Total (balanced) observations: 336 Cross-sections included: 42

Series: RETURN Method Statistic Prob.**

Levin, Lin & Chu t* -

6.45613 0.0000

Series: ln (Book to Market value)

Method Statistic Prob.**

Levin, Lin & Chu t* -13.2298 0.0000 Series: Dividend Payout Ratio

Method Statistic Prob.**

Levin, Lin & Chu t* -

15.3991 0.0000

Series: Leverage Ratio

Method Statistic Prob.**

Levin, Lin & Chu t* -

12.4196 0.0000

Series: ln (Market Capitalization)

Method Statistic Prob.**

Levin, Lin & Chu t* -

3.95747 0.0000

Series: Operating Profit to Book Value

Method Statistic Prob.**

Levin, Lin & Chu t* -

4.37614 0.0000

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 20

Series: Ln (P/E Ratio)

Method Statistic Prob.**

Levin, Lin & Chu t* -

20.1611 0.0000

Series: Premium

Method Statistic Prob.**

Levin, Lin & Chu t* -

7.52612 0.0000

Series: Ln (Sales)

Method Statistic Prob.**

Levin, Lin & Chu t* -

7.83774 0.0000 ** Probabilities are computed assuming asymptotic normality

Table 4-3: Levin, Lin and Chu Unit Root Test

The above Table for the unit root test tells that No Unit Root is present in any of the variable.

It means that the data for all the 9 variables are stationary.

4.10 Panel Co-integration Test4

Though it is not much required now to check for the co-integration test as the whole data is

stationary, to be on the safe side this test has also been applied for the panel data. For panel

cointegrated regression models, the asymptotic properties of the estimators of the regression

coefficients and the associated statistical tests are different from those of the time series

cointegration regression models. Following Table 4-4 shows the panel cointegration test

using the KAO (Engle-Granger based) cointegration Tests in EVIEWS:

Kao Residual Cointegration Test

Series: RETURN PREMIUM OPBV LNSALES LNPE LNMKT LNBTM DPO

DER

Date: 29/04/2011 Time: 01:42

Sample: 2001 2010

Included observations: 420

Null Hypothesis: No cointegration

Trend assumption: No deterministic trend

User-specified lag length: 1

Newey-West automatic bandwidth selection and Bartlett kernel

t-Statistic Prob.

4 For details, please see Baltagi, Econometric Analysis of Panel Data 3e, Willey & Sons, 2005, pp. 257

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 21

ADF -6.532121 0.0000

Residual variance 40.79466

HAC variance 16.48424

Table 4-4: KAO Cointegration Test

It is clear from the above output Table that the null hypothesis of no cointegration is rejected.

It means that all the variables are cointegrated (alternate hypothesis accepted) and therefore,

the regression of return on the other 8 independent variables is meaningful i.e., not spurious.

There are broadly 2 types of panel estimation techniques for the financial modeling. These

are fixed-effect and random-effect technique. In this paper, both these techniques will be used

extensively for the development of required model. The better and the statistically more

significant model will be used as the final model for the calculation of expected stock return.

4.11 Developing Fixed One-Way Effect Model for Stock Valuation

4.11.1 Introduction to Fixed One-Way Effect Model5

If the specification is dependent only on the cross section to which the observation belongs,

such a model is referred to as a model with one-way effects. The term ―fixed effect‖ is due to

the fact that, although the intercept may differ across the cross-section (here 42 companies),

each cross-section‘s intercept does not vary over time i.e. it is time-invariant. It should be

noted that the Fixed-Effect model given below assumes that the (slope) coefficients of the

regressors do not vary across individuals or over time. In equation (4.4), for fixed one-way

effect model, the specifications are given as below:

uit = μi + vit (Eq-4.6)

μi is used to encapsulate all the variables that affect Yit cross-sectionally but do not vary over

time. To allow for the (fixed effect) intercept to vary between companies, differential

intercept dummies technique is used. It is also termed as the Least Square Dummy Variable

(LSDV) approach. Then the model will look like as below:

Yi t = βxit + μ1D1i + μ2D2i + μ3D3i +· · · +μNDNi + vit (Eq-4.7)

5 Chris Brook, Introductory Econometric for Finance,2

nd e, 2008

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 22

Where, D1i is a dummy variable that takes the value 1 for all observations on the first entity

(e.g. Company ACC) in the sample and zero otherwise and similarly for other dummies.

4.11.2 Analysis and Modeling Using SAS

For generating the Fixed-One Way Model, SAS enterprise guide v3.0 has been used. During

the process of generating the model, the intercept term has been removed. The intercept term

(α) has not been included in the analysis so as to avoid the ‘dummy-variable trap’.

The regression analysis of the panel data generated by the SAS is shown one by one as below

in the following tables. Following Table 4-5 represents the fit-statistics of fixed One-way

effect model:

Fit Statistics

SSE 9078.1349 DFE 370

MSE 24.5355 Root MSE 4.9533

R-Square 0.3671

Table 4-5: Fit Statistics for Fixed One-Way Effect Model

The correlation (R2) is 36.71% which is quite satisfactory.

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 23

The cross-sectional parameter estimates have also been shown in the following output Table

4-6:

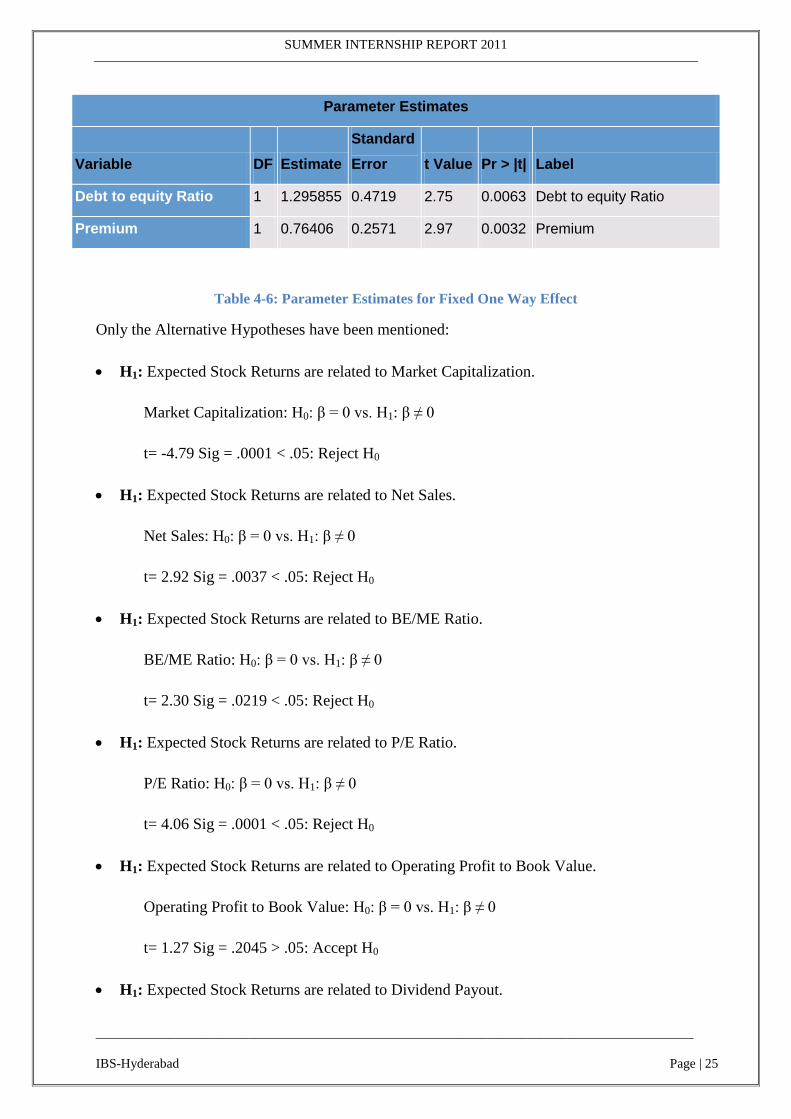

Parameter Estimates

Variable DF Estimate

Standard

Error t Value Pr > |t| Label

CS1 1 -2.81729 18.9348 -0.15 0.8818 Cross Sectional Effect 1

CS2 1 -3.88115 18.3950 -0.21 0.8330 Cross Sectional Effect 2

CS3 1 1.637425 18.4094 0.09 0.9292 Cross Sectional Effect 3

CS4 1 -0.89955 19.1368 -0.05 0.9625 Cross Sectional Effect 4

CS5 1 -0.60989 18.7645 -0.03 0.9741 Cross Sectional Effect 5

CS6 1 0.204929 19.9113 0.01 0.9918 Cross Sectional Effect 6

CS7 1 -0.55332 19.8478 -0.03 0.9778 Cross Sectional Effect 7

CS8 1 -6.83975 20.8407 -0.33 0.7430 Cross Sectional Effect 8

CS9 1 -2.08924 18.6880 -0.11 0.9110 Cross Sectional Effect 9

CS10 1 -0.7814 18.8049 -0.04 0.9669 Cross Sectional Effect 10

CS11 1 -0.93704 19.8118 -0.05 0.9623 Cross Sectional Effect 11

CS12 1 -8.82817 18.4380 -0.48 0.6324 Cross Sectional Effect 12

CS13 1 1.532418 18.4531 0.08 0.9339 Cross Sectional Effect 13

CS14 1 -1.28167 19.2522 -0.07 0.9470 Cross Sectional Effect 14

CS15 1 1.878681 18.6177 0.10 0.9197 Cross Sectional Effect 15

CS16 1 -0.22525 19.3104 -0.01 0.9907 Cross Sectional Effect 16

CS17 1 3.431067 17.8516 0.19 0.8477 Cross Sectional Effect 17

CS18 1 -7.28189 20.7974 -0.35 0.7264 Cross Sectional Effect 18

CS19 1 -1.85599 20.2124 -0.09 0.9269 Cross Sectional Effect 19

CS20 1 -0.39245 19.7328 -0.02 0.9841 Cross Sectional Effect 20

CS21 1 -6.45574 21.4552 -0.30 0.7637 Cross Sectional Effect 21

CS22 1 0.471677 19.6837 0.02 0.9809 Cross Sectional Effect 22

CS23 1 3.594788 18.3705 0.20 0.8450 Cross Sectional Effect 23

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 24

Parameter Estimates

Variable DF Estimate

Standard

Error t Value Pr > |t| Label

CS24 1 -2.29546 19.3149 -0.12 0.9055 Cross Sectional Effect 24

CS25 1 -0.24741 19.8403 -0.01 0.9901 Cross Sectional Effect 25

CS26 1 -1.93674 17.2675 -0.11 0.9108 Cross Sectional Effect 26

CS27 1 1.735368 20.3114 0.09 0.9320 Cross Sectional Effect 27

CS28 1 -3.82409 20.7133 -0.18 0.8536 Cross Sectional Effect 28

CS29 1 -0.72479 17.6037 -0.04 0.9672 Cross Sectional Effect 29

CS30 1 -1.7701 19.1224 -0.09 0.9263 Cross Sectional Effect 30

CS31 1 -2.57113 21.0311 -0.12 0.9028 Cross Sectional Effect 31

CS32 1 -2.97284 20.1641 -0.15 0.8829 Cross Sectional Effect 32

CS33 1 -0.87976 19.0755 -0.05 0.9632 Cross Sectional Effect 33

CS34 1 2.584431 18.4323 0.14 0.8886 Cross Sectional Effect 34

CS35 1 -2.62864 19.9215 -0.13 0.8951 Cross Sectional Effect 35

CS36 1 -1.25292 19.7015 -0.06 0.9493 Cross Sectional Effect 36

CS37 1 -1.25292 19.7015 -0.06 0.9493 Cross Sectional Effect 37

CS38 1 0.52898 20.4839 0.03 0.9794 Cross Sectional Effect 38

CS39 1 -1.78398 18.3359 -0.10 0.9225 Cross Sectional Effect 39

CS40 1 1.616614 17.6167 0.09 0.9269 Cross Sectional Effect 40

CS41 1 -0.82733 19.8072 -0.04 0.9667 Cross Sectional Effect 41

CS42 1 1.977371 17.8052 0.11 0.9116 Cross Sectional Effect 42

ln Market Capitalisation 1 -2.07522 0.4337 -4.79 <.0001 ln Market Capitalisation

ln Net Sales 1 2.457405 0.8413 2.92 0.0037 ln Net Sales

ln Book to Market value 1 0.63548 0.2760 2.30 0.0219 ln Book to Market value

ln P E 1 0.779547 0.1920 4.06 <.0001 ln P E

OPBV 1 0.361881 0.2847 1.27 0.2045 OPBV

Dividend Payout 1 -0.01712 0.0144 -1.19 0.2358 Dividend Payout

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 25

Parameter Estimates

Variable DF Estimate

Standard

Error t Value Pr > |t| Label

Debt to equity Ratio 1 1.295855 0.4719 2.75 0.0063 Debt to equity Ratio

Premium 1 0.76406 0.2571 2.97 0.0032 Premium

Table 4-6: Parameter Estimates for Fixed One Way Effect

Only the Alternative Hypotheses have been mentioned:

H1: Expected Stock Returns are related to Market Capitalization.

Market Capitalization: H0: β = 0 vs. H1: β ≠ 0

t= -4.79 Sig = .0001 < .05: Reject H0

H1: Expected Stock Returns are related to Net Sales.

Net Sales: H0: β = 0 vs. H1: β ≠ 0

t= 2.92 Sig = .0037 < .05: Reject H0

H1: Expected Stock Returns are related to BE/ME Ratio.

BE/ME Ratio: H0: β = 0 vs. H1: β ≠ 0

t= 2.30 Sig = .0219 < .05: Reject H0

H1: Expected Stock Returns are related to P/E Ratio.

P/E Ratio: H0: β = 0 vs. H1: β ≠ 0

t= 4.06 Sig = .0001 < .05: Reject H0

H1: Expected Stock Returns are related to Operating Profit to Book Value.

Operating Profit to Book Value: H0: β = 0 vs. H1: β ≠ 0

t= 1.27 Sig = .2045 > .05: Accept H0

H1: Expected Stock Returns are related to Dividend Payout.

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 26

Dividend Payout: H0: β = 0 vs. H1: β ≠ 0

t= -1.19 Sig = .2358 > .05: Accept H0

H1: Expected Stock Returns are related to Debt to Equity Ratio.

Debt to Equity Ratio: H0: β = 0 vs. H1: β ≠ 0

t= 2.75 Sig = .0063 < .05: Reject H0

H1: Expected Stock Returns are related to Premium (E (Rm) - Rf).

Premium: H0: β = 0 vs. H1: β ≠ 0

t= 2.97 Sig = .0032 < .05: Reject H0

The final Fixed-One Way Effect Model for the Stock Returns is shown as below. In this

Regression, the cross-sectional dummy variables for the companies have not been shown

(available in Table 4-6) due to very large number (42 Dummies for Cross Section). So, only

the main factors will be mentioned:

Test Statistics for the Model:

In SAS Enterprise Guide, only F-Statistics (Chow Test) is available for the Fixed One-Way

Effect Model Test. This test checks whether the panel approach is necessary at all. It involves

the restriction that all the dummy variables have the same parameter (i.e. H0: μ1 = μ2 = · ·

· = μN).

E(Rit)=-2.07522*(ln(MKTit))+2.457405*(ln(Net-Salesit))+

0.63548*(ln(BE/MEit))+0.779547*(ln(P/Eit))+1.295855*(D/Eit)+0.

76406*(Premiumit) (A)

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 27

The output result for this test generated by SAS is shown in the following Table 4-7:

F Test for No Fixed Effects and

No Intercept

Num DF Den DF F Value Pr > F

42 370 1.15 0.2459

Table 4-7: Chow Test (F-Test) for Fixed One Effect Model

H0: μ1 = μ2 = · · · = μN

Since, Pr (F-Stats) > 0.05 (p-value)

Therefore, H0 can’t be rejected.

Test results are not very satisfactory. It suggests that the model is not very robust.

This test suggests that simple OLS technique can also be implemented in the place of

Fixed One Way Effect.

Now referring to the steps shown in Figure 4-2, one can see that the step 4 is violated. So,

new estimation technique will be used for the modeling. There are 3 more broad techniques

left which will be used subsequently and the technique which will provide the most robust

and justifiable model will be used as the final model for the expected stock returns.

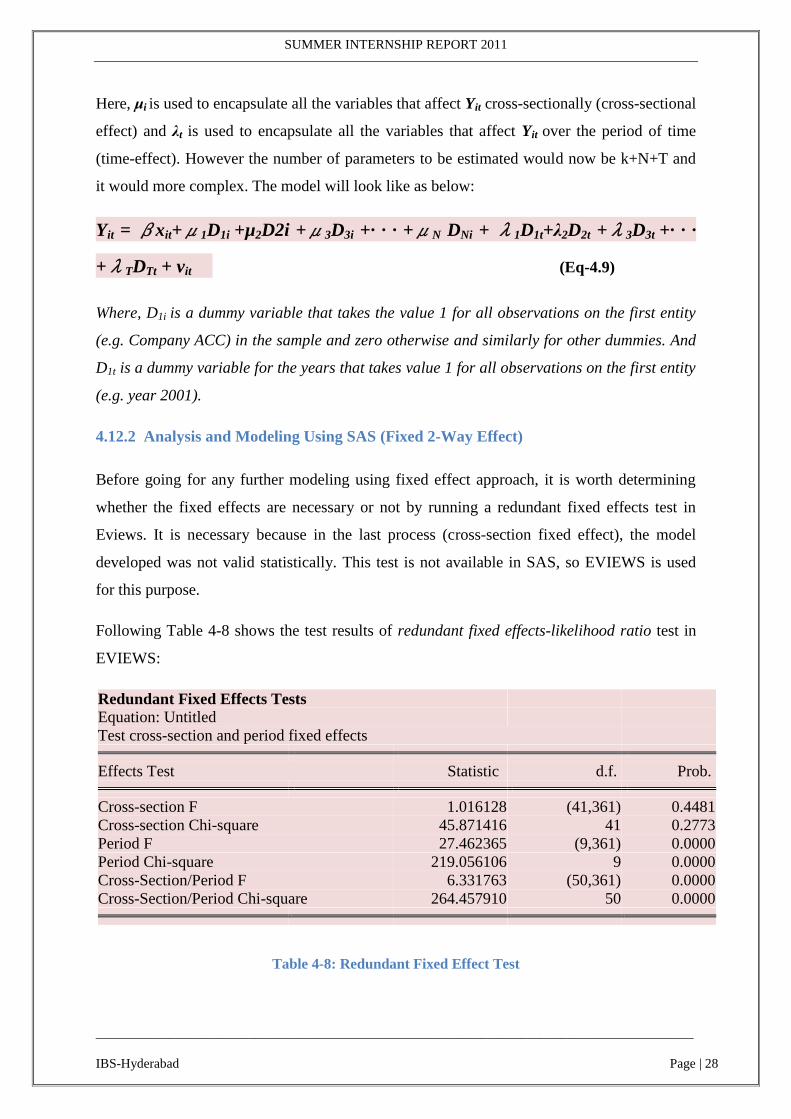

4.12 Developing Fixed Two-Way Effect Model for Stock Valuation

4.12.1 Introduction to Fixed Two Way Effect Model

A 2-way fixed effect model is the one when specification depends on both the cross section

and the time series to which the observation belongs. This technique allows for both entity-

fixed effects and the time-fixed effects within the same model. In this case the LSDV

equivalent model would contain both cross-sectional and time-dummies.

The specifications for Fixed One-Way Effect model are given as below:

uit = μi +λt+ vit (Eq-4.8)

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 28

Here, μi is used to encapsulate all the variables that affect Yit cross-sectionally (cross-sectional

effect) and λt is used to encapsulate all the variables that affect Yit over the period of time

(time-effect). However the number of parameters to be estimated would now be k+N+T and

it would more complex. The model will look like as below:

Yit = βxit+μ1D1i +µ2D2i +μ3D3i +· · · +μN DNi + λ1D1t+λ2D2t +λ3D3t +· · ·

+λTDTt + vit (Eq-4.9)

Where, D1i is a dummy variable that takes the value 1 for all observations on the first entity

(e.g. Company ACC) in the sample and zero otherwise and similarly for other dummies. And

D1t is a dummy variable for the years that takes value 1 for all observations on the first entity

(e.g. year 2001).

4.12.2 Analysis and Modeling Using SAS (Fixed 2-Way Effect)

Before going for any further modeling using fixed effect approach, it is worth determining

whether the fixed effects are necessary or not by running a redundant fixed effects test in

Eviews. It is necessary because in the last process (cross-section fixed effect), the model

developed was not valid statistically. This test is not available in SAS, so EVIEWS is used

for this purpose.

Following Table 4-8 shows the test results of redundant fixed effects-likelihood ratio test in

EVIEWS:

Redundant Fixed Effects Tests

Equation: Untitled

Test cross-section and period fixed effects

Effects Test Statistic d.f. Prob.

Cross-section F 1.016128 (41,361) 0.4481

Cross-section Chi-square 45.871416 41 0.2773

Period F 27.462365 (9,361) 0.0000

Period Chi-square 219.056106 9 0.0000

Cross-Section/Period F 6.331763 (50,361) 0.0000

Cross-Section/Period Chi-square 264.457910 50 0.0000

Table 4-8: Redundant Fixed Effect Test

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 29

From the output shown in above table, it is quite obvious that these are the time fixed-effect

which had a greater impact as compared to the cross-sectional fixed-effect. The output clearly

suggests that fixed effect model (especially time-fixed effect approach in this case) is a valid

approach rather than the pooled estimation approach.

The Table 4-9 shows the SAS outputs for the generated fixed two-way effect model:

Fit Statistics

SSE 5398.0873 DFE 361

MSE 14.9532 Root MSE 3.8669

R-Square 0.6237

Table 4-9: Fit Statistics for Fixed 2-Way Effect Model

The correlation (R2) is 62.37% which is very good if one compare it with the previous

model’s correlation. The main reason of this increased R2

is the introduction of time-effect in

the estimation.

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 30

The cross-sectional and time-series parameter estimates have also been shown in the

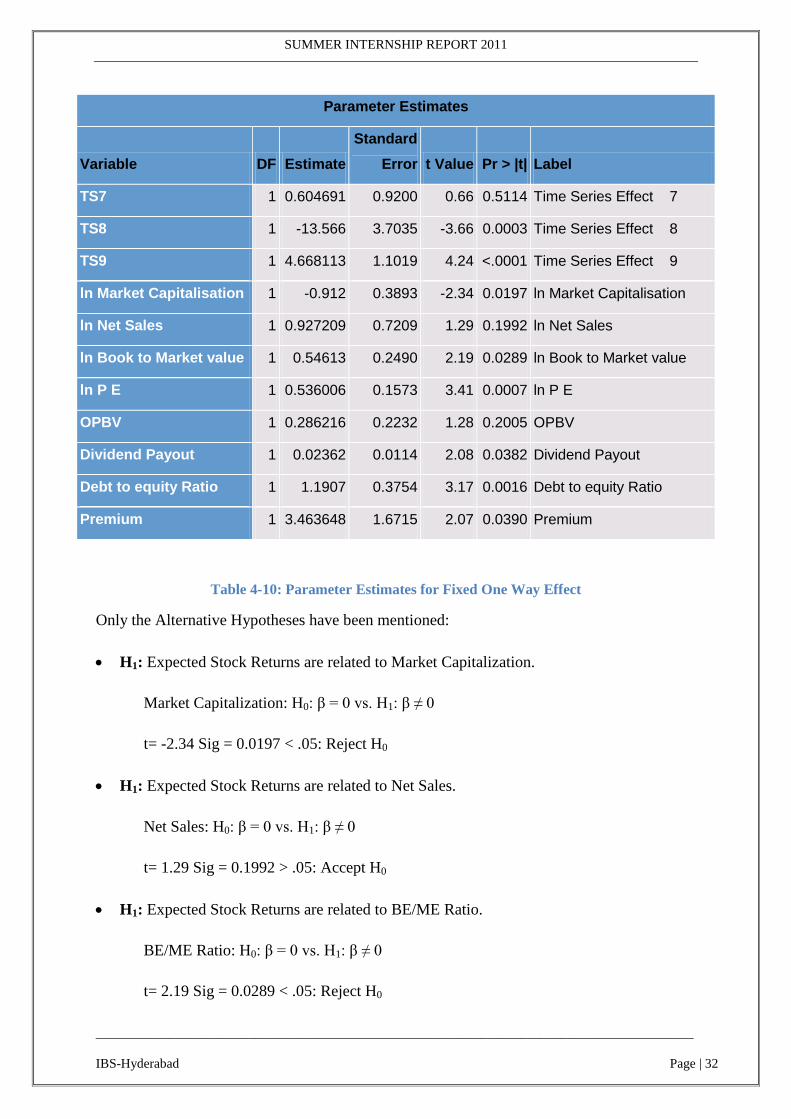

following output Table 4-10:

Parameter Estimates

Variable DF Estimate

Standard

Error t Value Pr > |t| Label

CS1 1 -33.8899 22.8094 -1.49 0.1382 Cross Sectional Effect 1

CS2 1 -34.8837 22.6737 -1.54 0.1248 Cross Sectional Effect 2

CS3 1 -30.0649 22.6489 -1.33 0.1852 Cross Sectional Effect 3

CS4 1 -32.3899 22.6833 -1.43 0.1542 Cross Sectional Effect 4

CS5 1 -32.007 22.5642 -1.42 0.1569 Cross Sectional Effect 5

CS6 1 -32.0588 23.3943 -1.37 0.1714 Cross Sectional Effect 6

CS7 1 -31.8816 23.3305 -1.37 0.1726 Cross Sectional Effect 7

CS8 1 -34.5995 23.9363 -1.45 0.1492 Cross Sectional Effect 8

CS9 1 -33.3161 22.4648 -1.48 0.1389 Cross Sectional Effect 9

CS10 1 -33.5823 22.6132 -1.49 0.1384 Cross Sectional Effect 10

CS11 1 -31.9195 23.3727 -1.37 0.1729 Cross Sectional Effect 11

CS12 1 -38.448 22.3645 -1.72 0.0864 Cross Sectional Effect 12

CS13 1 -31.4672 22.4358 -1.40 0.1616 Cross Sectional Effect 13

CS14 1 -32.6965 22.9564 -1.42 0.1552 Cross Sectional Effect 14

CS15 1 -31.1605 22.5560 -1.38 0.1680 Cross Sectional Effect 15

CS16 1 -31.9454 23.0078 -1.39 0.1659 Cross Sectional Effect 16

CS17 1 -32.2655 22.0575 -1.46 0.1444 Cross Sectional Effect 17

CS18 1 -35.0931 23.9577 -1.46 0.1438 Cross Sectional Effect 18

CS19 1 -33.2456 23.5623 -1.41 0.1591 Cross Sectional Effect 19

CS20 1 -33.3408 23.2575 -1.43 0.1526 Cross Sectional Effect 20

CS21 1 -34.5865 24.4113 -1.42 0.1574 Cross Sectional Effect 21

CS22 1 -32.1752 23.2371 -1.38 0.1670 Cross Sectional Effect 22

CS23 1 -28.9581 22.4042 -1.29 0.1970 Cross Sectional Effect 23

SUMMER INTERNSHIP REPORT 2011

__________________________________________________________________________________________

IBS-Hyderabad Page | 31

Parameter Estimates