Embed Size (px)

Citation preview

Facilitating Trade Across Africa with Ports Infrastructure Development

Presented by: Derrick Chikanga

Infrastructure Research Analyst

Frost & Sullivan

Agenda…

OverviewCurrent SituationFuture DevelopmentsImplications and Conclusions

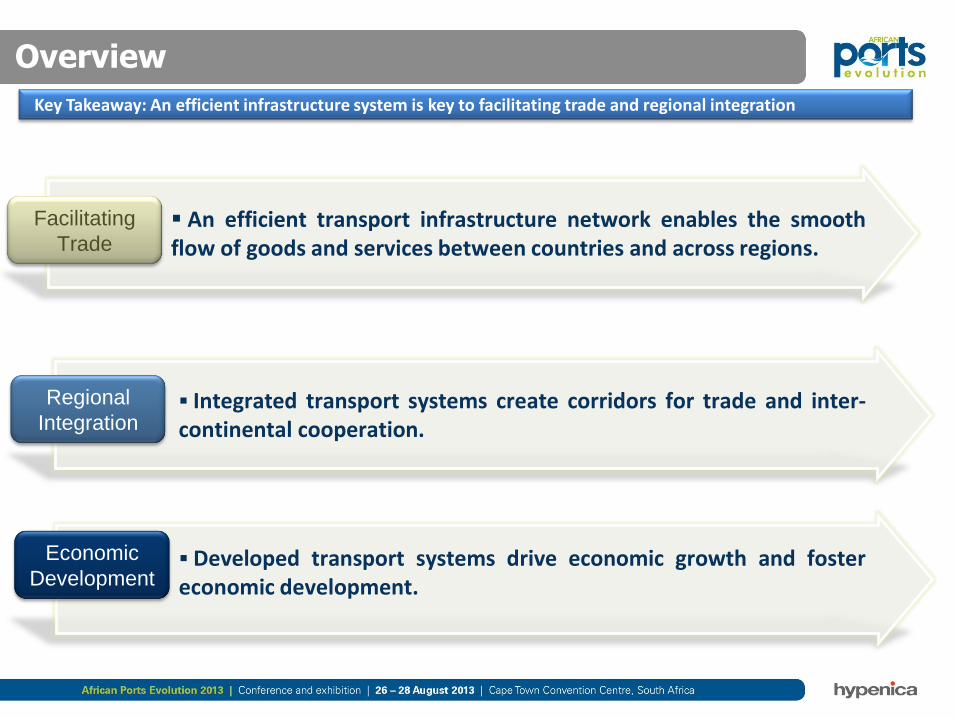

Overview

WHY DOES The Future Hold?Key Takeaway: An efficient infrastructure system is key to facilitating trade and regional integration

An efficient transport infrastructure network enables the smoothflow of goods and services between countries and across regions.

Developed transport systems drive economic growth and fostereconomic development.

Integrated transport systems create corridors for trade and inter-continental cooperation.

Regional

Integration

Economic

Development

Facilitating

Trade

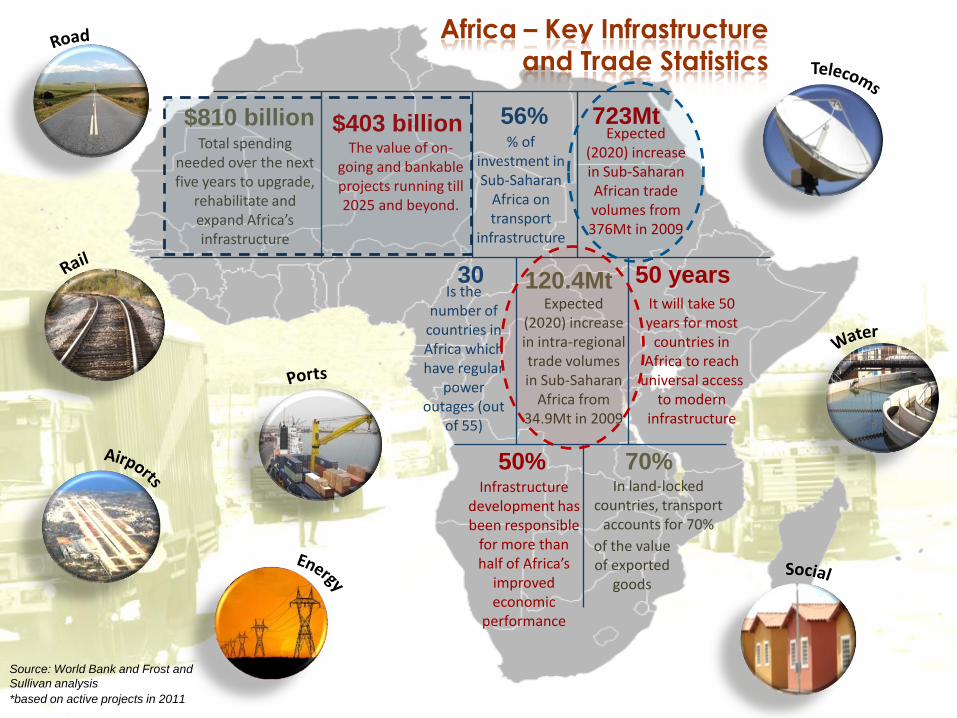

Africa – Key Infrastructure and Trade Statistics

$403 billionThe value of on-

going and bankable projects running till 2025 and beyond.

% of investment in Sub-Saharan

Africa on transport

infrastructure

56%

70%In land-locked

countries, transport accounts for 70%

Is the number of

countries in Africa which have regular

power outages (out

of 55)

30Expected

(2020) increase in intra-regional trade volumes in Sub-Saharan

Africa from 34.9Mt in 2009

120.4Mt 50 years It will take 50 years for most

countries in Africa to reach

universal access to modern

infrastructure

50%Infrastructure

development has been responsible

for more than half of Africa’s

improved economic

performance

723MtExpected

(2020) increase in Sub-Saharan African trade volumes from 376Mt in 2009

of the value of exported

goods

*based on active projects in 2011

Source: World Bank and Frost and

Sullivan analysis

$810 billionTotal spending

needed over the next five years to upgrade,

rehabilitate and expand Africa’s infrastructure

Current Situation

WHY DOES The Future Hold?

Current Situation

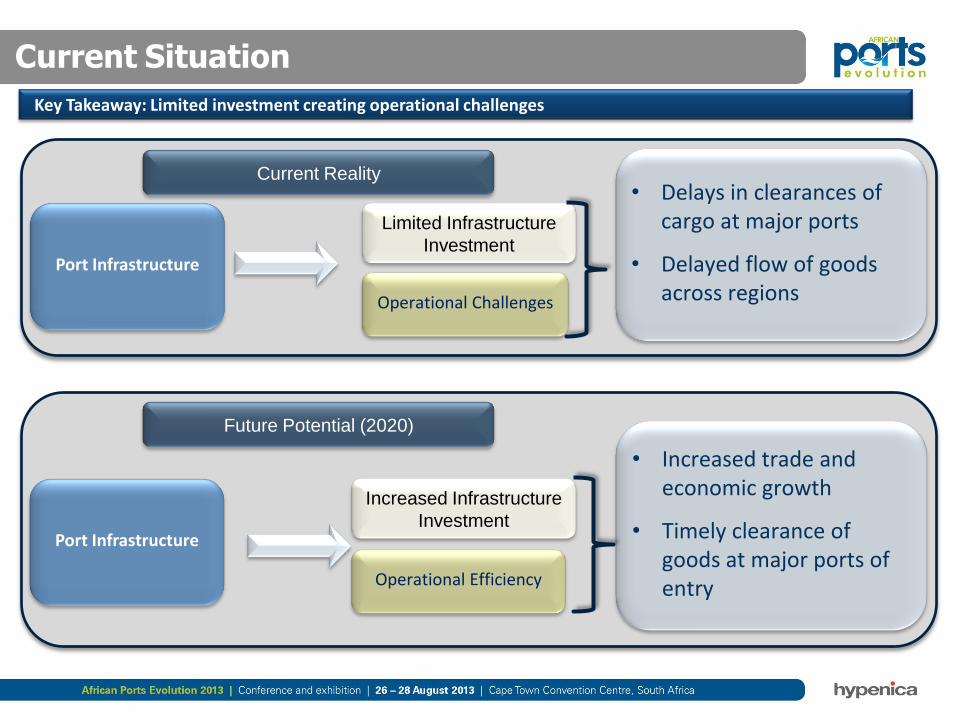

WHY DOES The Future Hold?Key Takeaway: Limited investment creating operational challenges

Current Reality

Future Potential (2020)

Port Infrastructure

Limited Infrastructure

Investment

Operational Challenges

• Increased trade and economic growth

• Timely clearance of goods at major ports of entry

• Delays in clearances of cargo at major ports

• Delayed flow of goods across regions

Port Infrastructure

Increased Infrastructure

Investment

Operational Efficiency

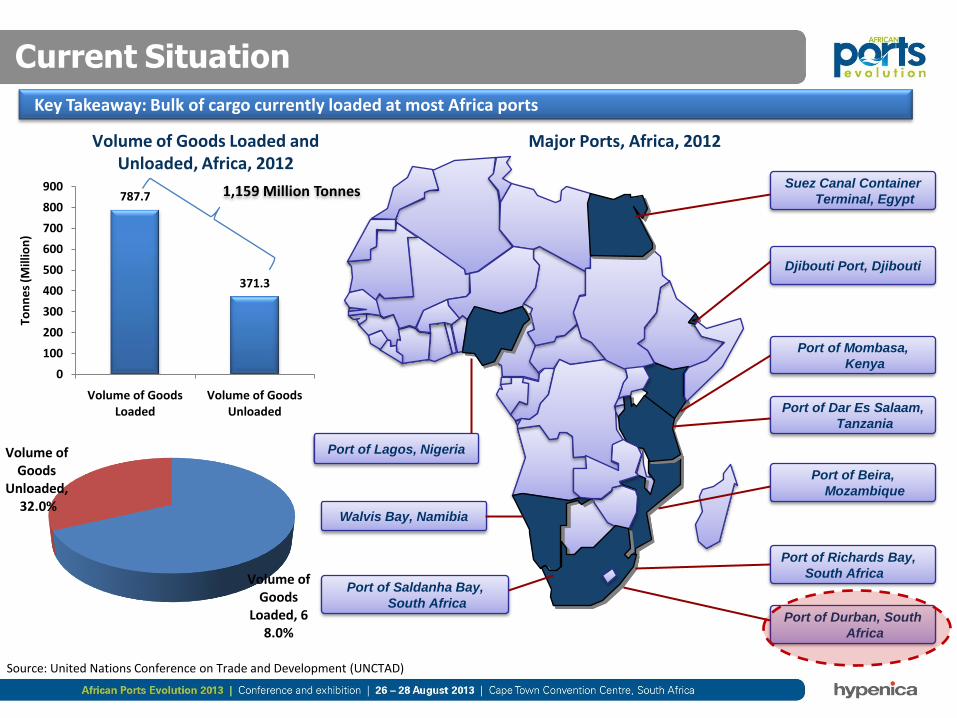

Port of Durban, South

Africa

Port of Richards Bay,

South Africa

Port of Mombasa,

Kenya

Port of Dar Es Salaam,

Tanzania

Port of Beira,

Mozambique

Djibouti Port, Djibouti

Suez Canal Container

Terminal, Egypt

Port of Lagos, Nigeria

Walvis Bay, Namibia

Port of Saldanha Bay,

South Africa

Key Takeaway: Bulk of cargo currently loaded at most Africa ports

787.7

371.3

0

100

200

300

400

500

600

700

800

900

Volume of Goods Loaded

Volume of Goods Unloaded

Ton

ne

s (M

illio

n)

Volume of Goods

Loaded, 68.0%

Volume of Goods

Unloaded,32.0%

Major Ports, Africa, 2012Volume of Goods Loaded and Unloaded, Africa, 2012

Current Situation

Source: United Nations Conference on Trade and Development (UNCTAD)

1,159 Million Tonnes

Current Situation

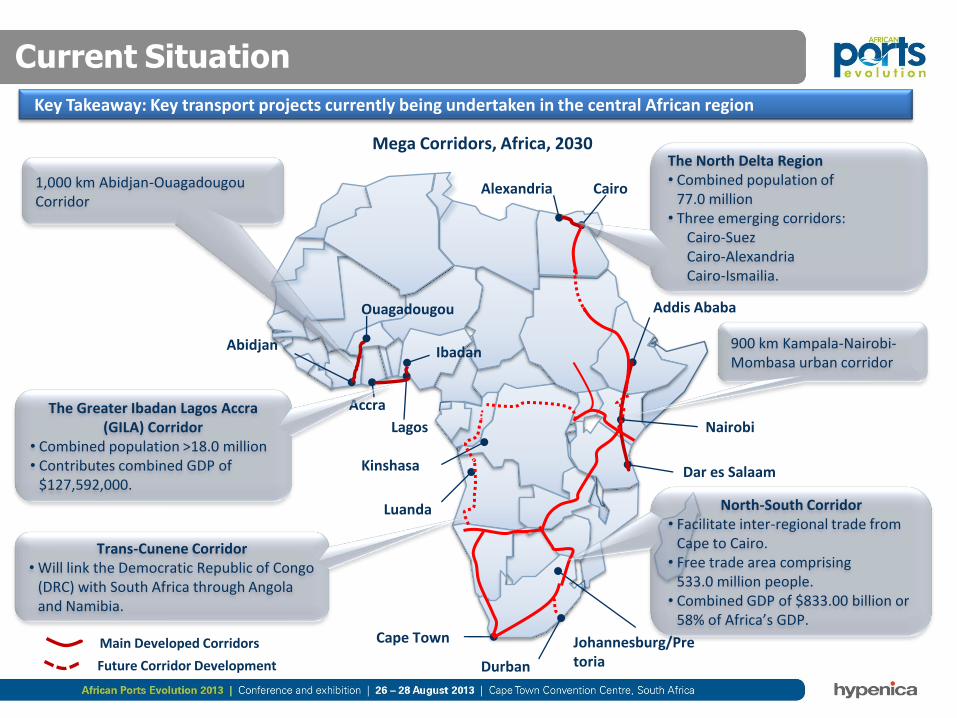

Key Takeaway: Key transport projects currently being undertaken in the central African region

Lagos

Luanda

Johannesburg/Pretoria

Cairo

Dar es Salaam

Alexandria

Nairobi

Accra

Abidjan

Kinshasa

Addis Ababa

Main Developed Corridors Cape Town

Durban

The Greater Ibadan Lagos Accra (GILA) Corridor

• Combined population >18.0 million• Contributes combined GDP of

$127,592,000.

The North Delta Region• Combined population of

77.0 million• Three emerging corridors:

Cairo-SuezCairo-AlexandriaCairo-Ismailia.

900 km Kampala-Nairobi-Mombasa urban corridor

1,000 km Abidjan-Ouagadougou Corridor

North-South Corridor• Facilitate inter-regional trade from

Cape to Cairo. • Free trade area comprising

533.0 million people. • Combined GDP of $833.00 billion or

58% of Africa’s GDP.

Trans-Cunene Corridor• Will link the Democratic Republic of Congo

(DRC) with South Africa through Angola and Namibia.

Ouagadougou

Ibadan

Future Corridor Development

Mega Corridors, Africa, 2030

Current Situation

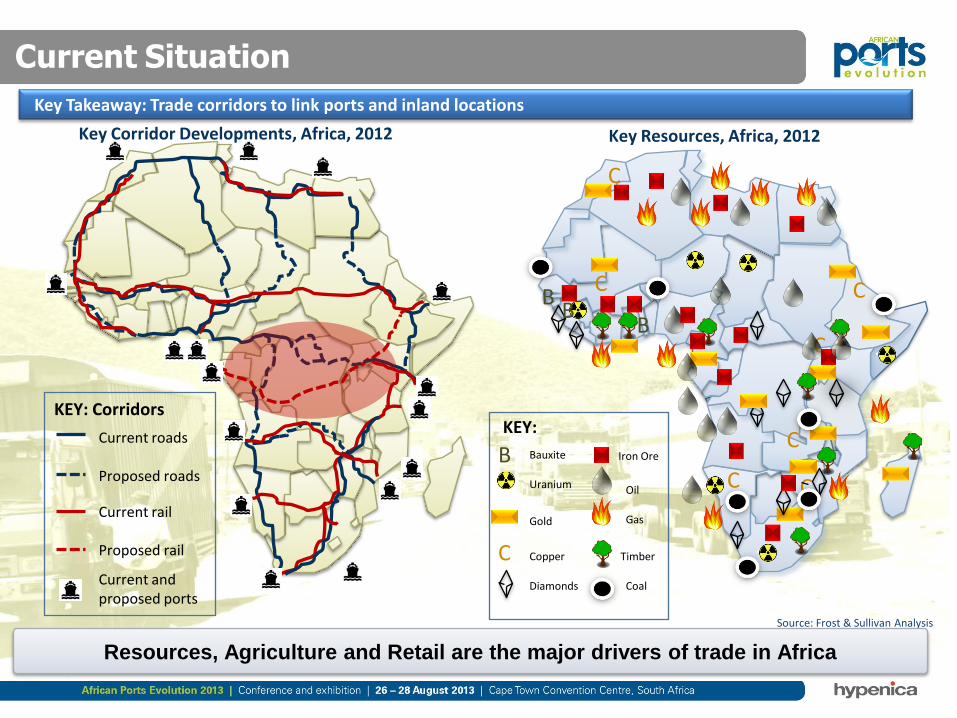

Key Takeaway: Trade corridors to link ports and inland locations

C

B Bauxite

Uranium

Gold

Copper

Diamonds

Oil

Gas

Timber

KEY:

Iron Ore

Coal

C

CC

CC

C

C

BB

B

Source: Frost & Sullivan Analysis

KEY: Corridors

Current roads

Proposed roads

Current rail

Proposed rail

Current and proposed ports

Resources, Agriculture and Retail are the major drivers of trade in Africa

Key Resources, Africa, 2012Key Corridor Developments, Africa, 2012

Current Situation

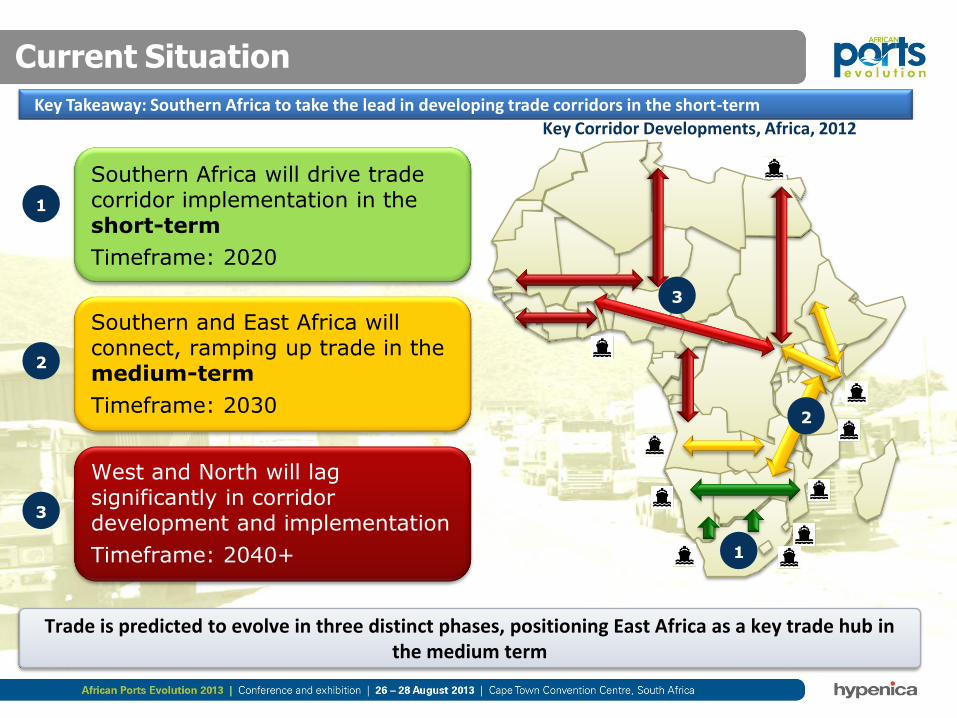

Key Takeaway: Southern Africa to take the lead in developing trade corridors in the short-term

1

Southern Africa will drive trade corridor implementation in the short-term

Timeframe: 2020

Southern and East Africa will connect, ramping up trade in the medium-term

Timeframe: 2030

West and North will lag significantly in corridor development and implementation

Timeframe: 2040+

2

3

Trade is predicted to evolve in three distinct phases, positioning East Africa as a key trade hub in the medium term

3

2

1

Key Corridor Developments, Africa, 2012

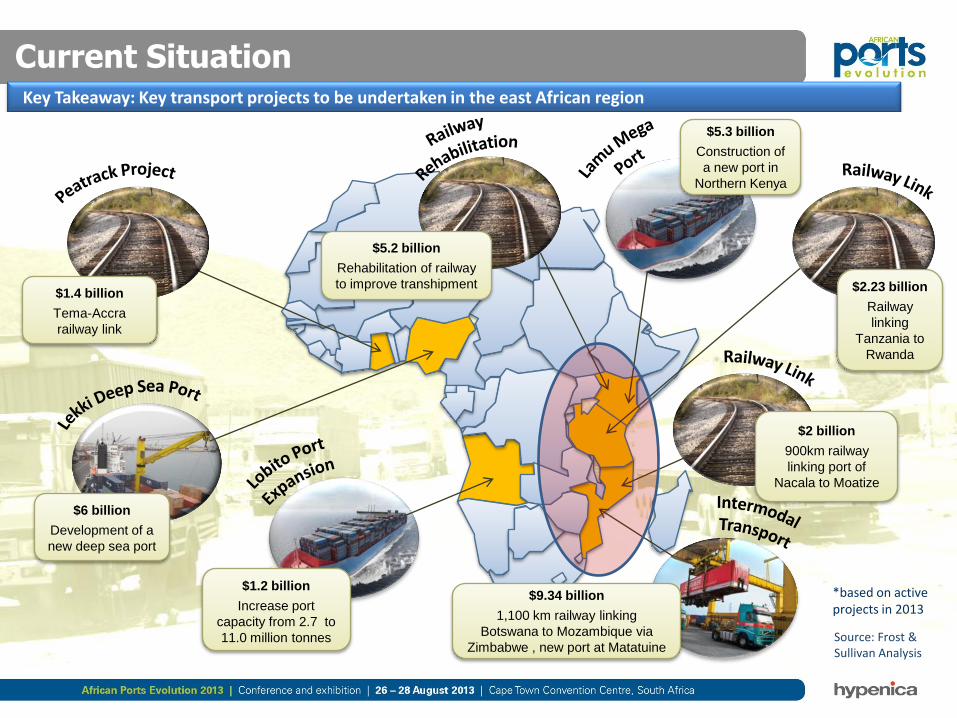

Current SituationKey Takeaway: Key transport projects to be undertaken in the east African region

$2 billion

900km railway

linking port of

Nacala to Moatize

$5.2 billion

Rehabilitation of railway

to improve transhipment

$5.3 billion

Construction of

a new port in

Northern Kenya

$2.23 billion

Railway

linking

Tanzania to

Rwanda

$1.4 billion

Tema-Accra

railway link

$1.2 billion

Increase port

capacity from 2.7 to

11.0 million tonnes

$6 billion

Development of a

new deep sea port

*based on active projects in 2013

Source: Frost & Sullivan Analysis

$9.34 billion

1,100 km railway linking

Botswana to Mozambique via

Zimbabwe , new port at Matatuine

Future Developments

WHAT DOES THE FUTURE HOLD?

Future Developments

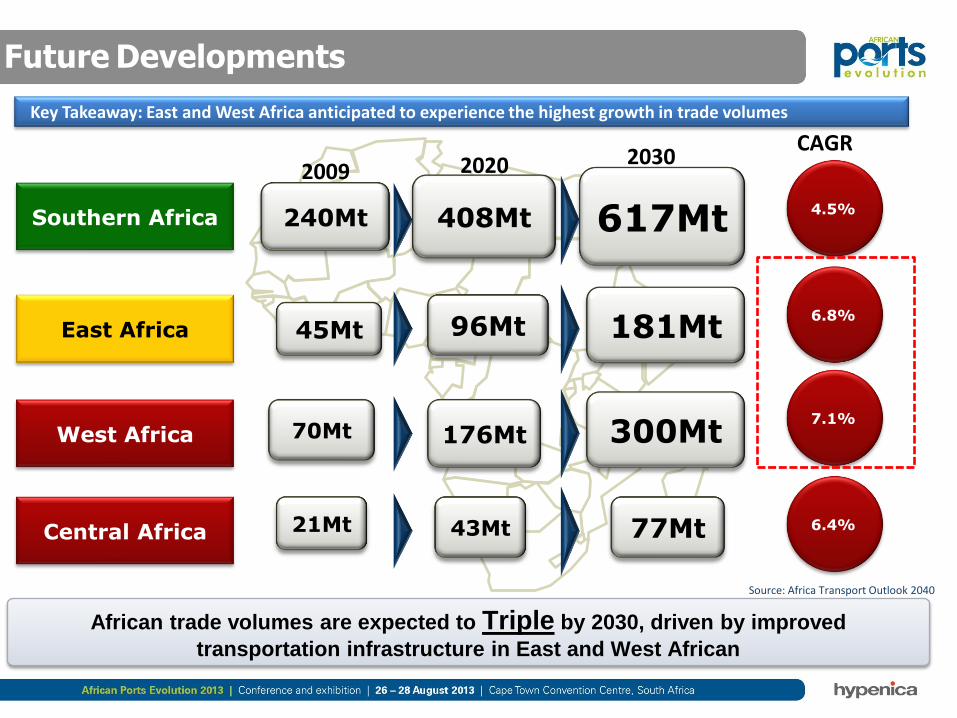

Key Takeaway: East and West Africa anticipated to experience the highest growth in trade volumes

2030CAGR

240Mt 408Mt

2009

617Mt

2020

70Mt 176Mt 300Mt

Southern Africa

East Africa

West Africa

Central Africa

45Mt 96Mt 181Mt

21Mt 43Mt 77Mt

4.5%

6.8%

7.1%

6.4%

Source: Africa Transport Outlook 2040

African trade volumes are expected to Triple by 2030, driven by improved

transportation infrastructure in East and West African

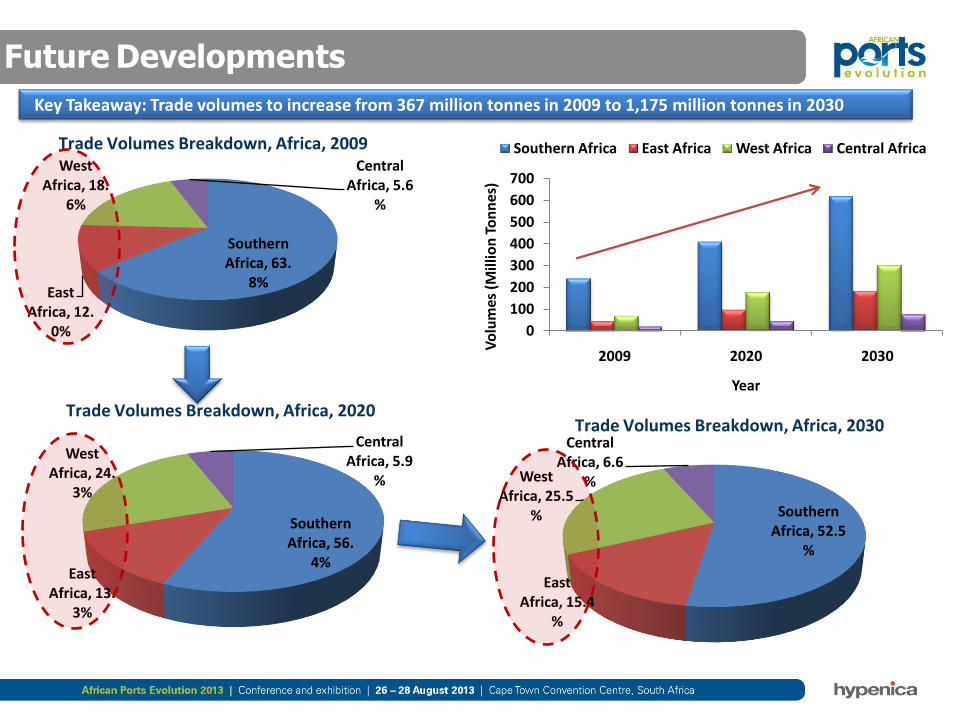

WHY DOES The Future Hold?Key Takeaway: Trade volumes to increase from 367 million tonnes in 2009 to 1,175 million tonnes in 2030

0

100

200

300

400

500

600

700

2009 2020 2030

Vo

lum

es (

Mill

ion

To

nn

es)

Year

Southern Africa East Africa West Africa Central Africa

Southern Africa, 63.

8%East

Africa, 12.0%

West Africa, 18.

6%

Central Africa, 5.6

%

Southern Africa, 56.

4%East

Africa, 13.3%

West Africa, 24.

3%

Central Africa, 5.9

%

Southern Africa, 52.5

%

East Africa, 15.4

%

West Africa, 25.5

%

Central Africa, 6.6

%

Trade Volumes Breakdown, Africa, 2009

Trade Volumes Breakdown, Africa, 2020Trade Volumes Breakdown, Africa, 2030

Future Developments

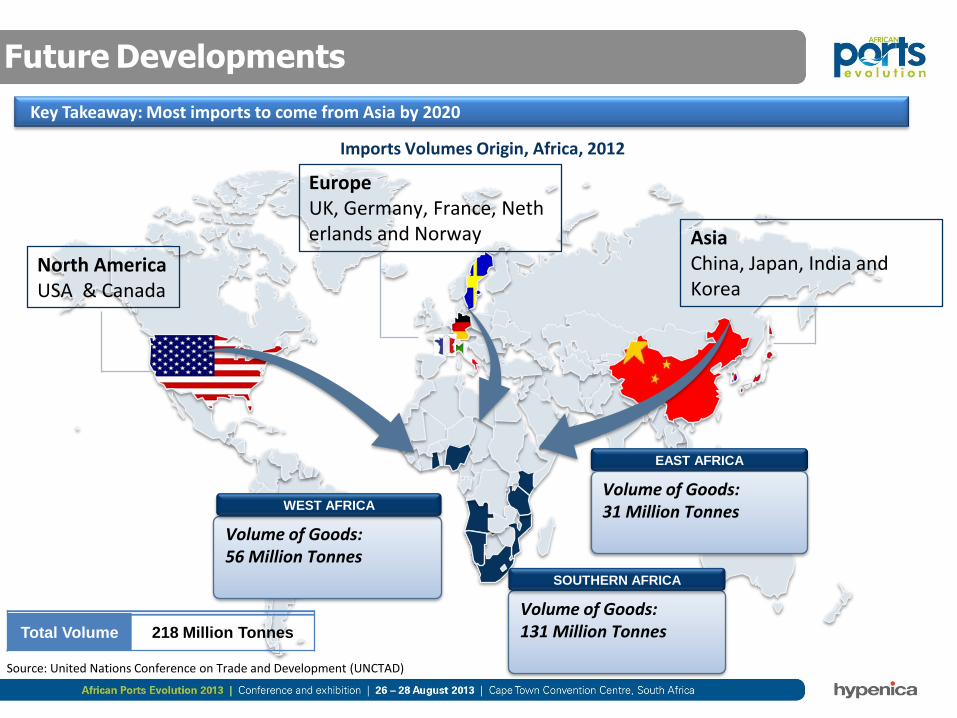

Key Takeaway: Most imports to come from Asia by 2020

North AmericaUSA & Canada

Europe UK, Germany, France, Netherlands and Norway

Source: United Nations Conference on Trade and Development (UNCTAD)

Volume of Goods:131 Million Tonnes

SOUTHERN AFRICA

Volume of Goods:56 Million Tonnes

WEST AFRICA

EAST AFRICA

Volume of Goods:31 Million Tonnes

Imports Volumes Origin, Africa, 2012

AsiaChina, Japan, India and Korea

Total Volume 218 Million Tonnes

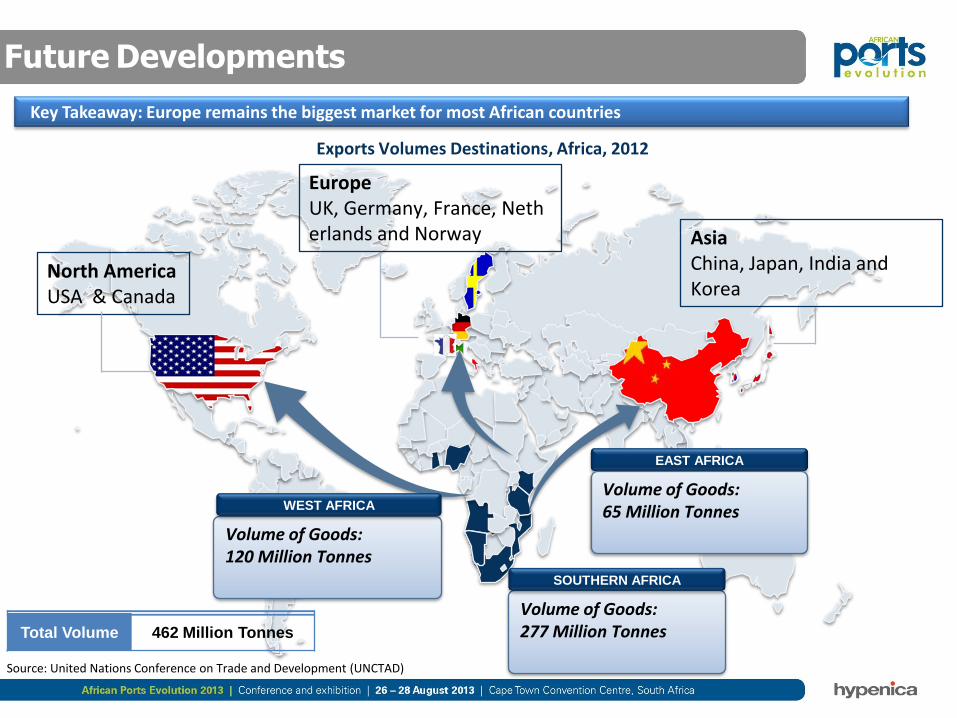

Future Developments

Key Takeaway: Europe remains the biggest market for most African countries

Volume of Goods:277 Million Tonnes

SOUTHERN AFRICA

Volume of Goods:120 Million Tonnes

WEST AFRICA

EAST AFRICA

Volume of Goods:65 Million Tonnes

Exports Volumes Destinations, Africa, 2012

North AmericaUSA & Canada

Europe UK, Germany, France, Netherlands and Norway Asia

China, Japan, India and Korea

Source: United Nations Conference on Trade and Development (UNCTAD)

Total Volume 462 Million Tonnes

Future Developments

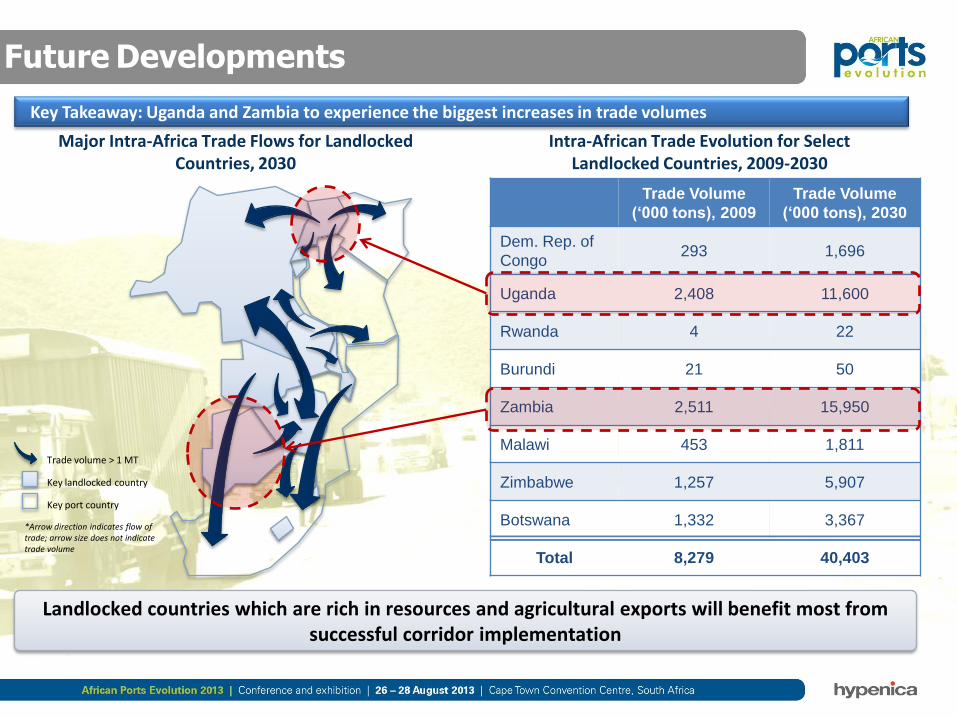

WHY DOES The Future Hold?

Trade Volume

(‘000 tons), 2009

Trade Volume

(‘000 tons), 2030

Dem. Rep. of

Congo293 1,696

Uganda 2,408 11,600

Rwanda 4 22

Burundi 21 50

Zambia 2,511 15,950

Malawi 453 1,811

Zimbabwe 1,257 5,907

Botswana 1,332 3,367

Total 8,279 40,403

Trade volume > 1 MT

Key landlocked country

Key port country

*Arrow direction indicates flow of trade; arrow size does not indicate trade volume

Landlocked countries which are rich in resources and agricultural exports will benefit most from successful corridor implementation

Major Intra-Africa Trade Flows for Landlocked Countries, 2030

Intra-African Trade Evolution for Select Landlocked Countries, 2009-2030

Key Takeaway: Uganda and Zambia to experience the biggest increases in trade volumes

Future Developments

Implications and Conclusions

What are the Implications for Africa’s Development

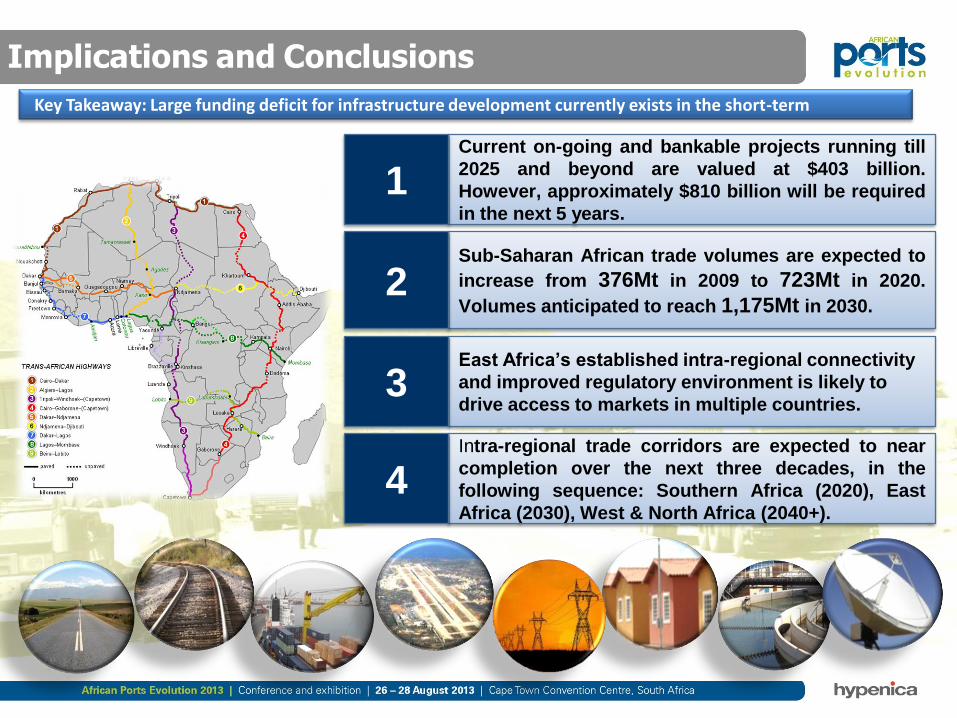

Key Takeaway: Large funding deficit for infrastructure development currently exists in the short-term

Current on-going and bankable projects running till

2025 and beyond are valued at $403 billion.

However, approximately $810 billion will be required

in the next 5 years.

Sub-Saharan African trade volumes are expected to

increase from 376Mt in 2009 to 723Mt in 2020.

Volumes anticipated to reach 1,175Mt in 2030.

Intra-regional trade corridors are expected to near

completion over the next three decades, in the

following sequence: Southern Africa (2020), East

Africa (2030), West & North Africa (2040+).

1

2

4

East Africa’s established intra-regional connectivity

and improved regulatory environment is likely to

drive access to markets in multiple countries.3

Implications and Conclusions

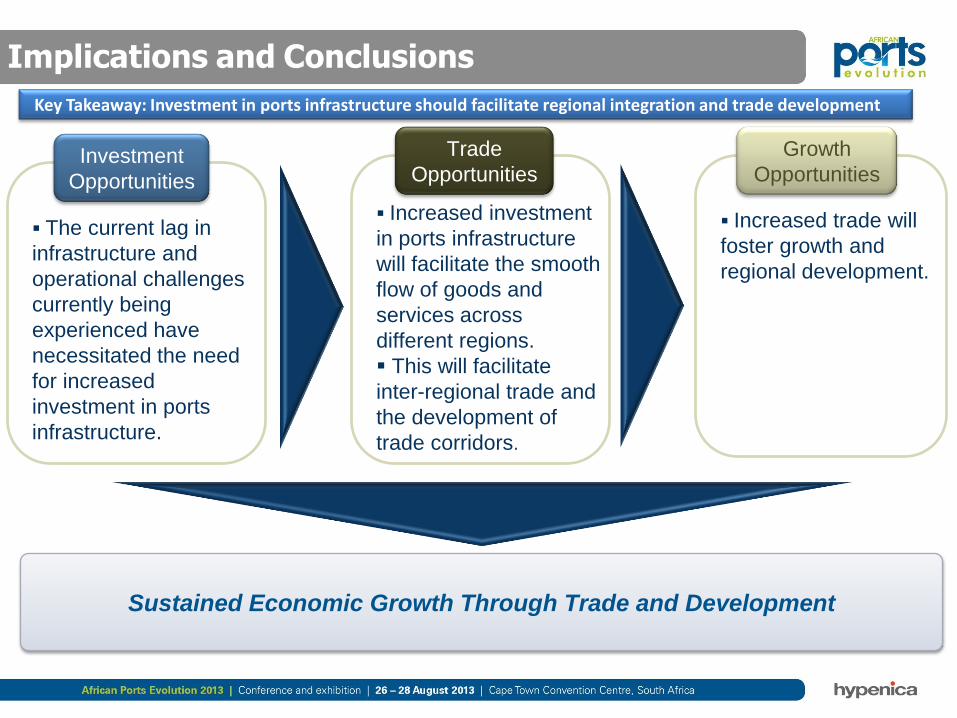

WHY DOES The Future Hold?Key Takeaway: Investment in ports infrastructure should facilitate regional integration and trade development

The current lag in

infrastructure and

operational challenges

currently being

experienced have

necessitated the need

for increased

investment in ports

infrastructure.

Trade

OpportunitiesInvestment

Opportunities

Growth

Opportunities

Sustained Economic Growth Through Trade and Development

Increased investment

in ports infrastructure

will facilitate the smooth

flow of goods and

services across

different regions.

This will facilitate

inter-regional trade and

the development of

trade corridors.

Increased trade will

foster growth and

regional development.

Implications and Conclusions

The End

Your contacts:

Derrick Chikanga

Infrastructure Analyst, Africa

Tel: +27 (0) 21 680 3204

Email: [email protected]

Samantha James

Corporate Communications

Tel: +27 (0) 21 680 3260

Email: [email protected]