Embed Size (px)

Citation preview

Topics

Ocean Transport

Supply Chain Management

Ocean Transport

State of the Industry

• Too many ships

• Slow growth of global trade

with recession

• Losses (especially Asia-

Europe)

The Times – They Are A Changing

Global Trade / Global Logistics

Top 10 Container Carriers

1996

1. APM-Maersk

2. Evergreen

3. P&O Nedlloyd

4. Sea-Land

5. COSCO

6. Hanjin

7. MSC

8. NYK

9. Mitsui

10. Hyundai

2010

1. APM-Maersk

2. MSC

3. CMA-CGM

4. APL

5. Evergreen

6. Hapag-Lloyd

7. COSCO

8. CSAV

9. CSCL

10. Hanjin

Top 10 Container Ports

1980

1. New York/New Jersey

2. Rotterdam

3. Hong Kong

4. Kaohsiung

5. Singapore

6. Hamburg

7. Oakland

8. Seattle

9. Kobe

10. Antwerp

2011

1. Shanghai

2. Singapore

3. Hong Kong

4. Shenzhen

5. Busan

6. Ningbo

7. Guangzhou

8. Qingdao

9. Dubai

10. Rotterdam

Top 10 North American Ports

2000

1. Long Beach

2. Los Angeles

3. New York/New Jersey

4. Charleston

5. Oakland

6. Seattle

7. Norfolk

8. Houston

9. Savannah

10. Tacoma

2011

1. Los Angeles

2. Long Beach

3. New York/New Jersey

4. Savannah

5. Vancouver

6. Oakland

7. Seattle

8. Virginia

9. Houston

10. Manzanillo

Ocean Transport

Mega Ships

Mega Ships

Mega Ship Aircraft Carrier

Issues They Face• Megas (Triple E) – 18,000+ TEU (vs.

1,000 TEU in 1970’s)

• Lower Operating Costs

• How Will Ships be Filled?

• Which Ports Will Handle Them?

• How Will Ports Handle Them?

• What’s the Investment?

• Bottlenecks!

The P3 Network and More

The P3 Network• Maersk, MSC, CMA-CGM – The 3 Largest

Carriers

• Formed an operating alliance

• FMC, EU, & China reviewed

• Three Issues –

• Market Share

• Big Ships

• Hubs/Ports Used

P3 Market Share• 44% Asia-to-Europe

• 24% in the Trans-Pacific

• 42% in the Trans-Atlantic

Trade

P3 Vessel Size

• Average vessel for Asia-

Europe – increasing from

9,300 TEU to 14,200 by end

of 2015

• Maersk’s Largest Vessels –

surpass MSC and CMA CGM

when all Megas delivered

• Creates a Domino Effect

The G6 Alliance

The G6 Alliance• From New World & Grand Alliances

APL (#4)

Hapag-Lloyd (#6)

NYK

OOCL

Hyundai

Mitsui

COSCO (#7)

Hanjin (#10)

K Line

Yang Ming

Evergreen (#5) – May Join

The CKYH Alliance

Canals

Panama Canal – 2015 or 2016 Expansion

Updates on East Coast ports with bigger ships &

widening

$1.6 Billion Overrun

Construction was slowed during dispute

Suez Canal - Congestion

Pending Chaos!?

Issues

• Supply (of ships/container

space) exceeds demand

• Pricing/Rates – flat and

somewhat low

• Will “Money People” sit still?

• Last time – carriers laid up

significant tonnage

“coincidentally” at same time

Singapore 2009

Shake Out Ahead?

Financial

Much red ink for last 5 years

Hanjin – operating loss $225 Million / net loss

$631 Million for 2013

M&A

CSAV / Hapag-Lloyd (could this new carrier join

the P3?)

The Next Few Years

As big ships are spread around globally

More rate volatility in more trade lanes

Schedule/Service Vagaries

Dropped weekly sailings

Fewer Carriers

Ocean Carriers &

Global Supply Chain Erosion

What Carriers Are Doing

Fewer carriers in business

Alliances, slot exchanges, and vessel sharing –

created and changed

Shipping Routes – added and revised

Sailing Schedules – made and reworked

“Slow Steaming” – ongoing practice

What It All Means

Irregular Performance

Lack of service reliability

Potential changes as to ports to handle ships

Which Means

Increased uncertainty for planning

Undermine inventory yield maximization

More inventories and more capital tied up

Impact

TOTAL GLOBAL INVENTORIES

REQUIRED INVENTORY TO

MEET REQUIRED TO MEET SALES

SAFETY STOCK

ADDITIONAL BUFFER TO

COMPENSATE FOR

UNRELIABILTY

By The Way…• How does all this factor into

your importing and carrier

selection (even if you use a

NVO)?

• Do you form an IGA shippers

association to leverage buying

power for import freight?

• Have you considered how

much is big and big – big

carriers and big shippers?

Questions???

Supply Chain Management

Is This Your Supply Chain?

What do you know about your SC Performance?

Are you doing much “fire-fighting” (reactive vs.

proactive)?

Do you have little/no metrics, beyond complaints,

charge backs or costs?

Yours?

Do you have a monolithic supply chain operation?

Little/no service differentiation beyond customer

order requirements?

Is it defined by costs, tasks, and/or functions?

Is This Your Supply Chain?

Perfect Order

Delivered / Complete / Accurate / On-Time

How well do you do with customer orders?

How well do your suppliers do with your PO’s?

Benefits of Real SCM

Customer Advantage –

IT’S ABOUT THE CUSTOMER!!!

Competitive differentiation

Translates into better revenue and margins

Are You Happy

with the Supply

Chain That YOU

Built?

How Do You View Global Logistics?

SCM - Hot Topics

Time Compression

Omni-Channel / Multi-Channel

Segmentation

Risk Mitigation

Cycle Time Compression

Cycle Time

Cycle Time – time from recognition of need (before PO

is issued) until product delivered to you – and sold,

and paid by customer (funds availability affects

procurement)

Not just length, includes variance

Time – important for business

Cycle Time

Inventory-factor of uncertainty (buffer) – longer

than cycle time, more the uncertainty, more the

inventory

Key factor for responsiveness and agility

In Lean, extra time is waste

Cycle Time Compression

Identify and assess each sub-cycle

Look for gaps, redundancies, and meaningless

items

External and internal (especially)

Streamline practices and operations

SC Omni-Channel / Multi-Channel

What It Is

Selling through multiple channels

For B2C and B2B

Sell 24/7 from anywhere in the world

From any device (e-commerce and m-commerce)

Omni-Channel Examples

Think Amazon and more

Home Depot

Building 3 e-commerce fulfillment centers

100,000 products (vs. 35,000 for stores)

SCM Omni-Channel Issues

Speed and accuracy of order shipment

How to position inventory

Where to position inventory

What inventory to position

Technology – integrated visibility for inventory and

orders in all channels

Multi/Omni-ChannelDirect shipping of gloves “from/for” other party’s ecommerce site

• E-tailer does not have to hold inventory

• Can your suppliers ship to customers elsewhere in the world for you?

Supply Chain Segmentation

What Segmentation Is

Superior best practice

Dividing business into discrete groups (not

based on business units) based on similar

characteristics

Address important company issues

Serve strategic purpose

Key Issues for

Segmenting

• Differing markets

• Product portfolios

• Customer portfolios

• Inventory yields

• Omni-Channel sales

More Issues for

Segmenting

• Global operations

• Channel partners

• Customer attrition

• Suppliers

• Supply chain risk

Why Segment???

Stop one-size-fits-all “service” approach

Reduce internal and external noise that

crates chaos and diverts resources

Design and align operations for different

sectors

Build competitive differentiation

How To Segment

1. Identify segments

2. Profile sectors – and customers in them

3. Determine how customers in each

segment differ for SC services

4. Evaluate supply chain services, including

ones not met, and performance for each

segment

Segment Approaches

Cost – good concept – allocating and

assigning costs - no direct costs

Value – economic – not good to identify

segment characteristics

Need – drivers that segments have for

specific service(s)

What To Do With Results

1. Prioritize segments

2. Be specific

3. Evaluate the quality of service

4. Implement services for each segment

5. Develop metrics for each segment’s

service and measure

• Have Actionable Info

ExampleOrder Size and Annual Volume

Small Orders Direct to Store

Delivery

Large Orders with Demanding

Delivery

Small Orders and No Real Volume

Medium Size Orders with

Special Preparation for Select Products

Order Requirements

Large Order Segment

3rd Cut2nd Cut1st Cut

Large Orders

Rapid Order Preparation &

Delivery

Same Day Delivery

Nationwide

To Warehouses Prepared for Cross Docking

Regular Delivery

Export

Special Preparation Segment

3rd Cut2nd Cut1st Cut

Mid-Size Orders

Time for Picking Two

Products and Making New

SKU

To Warehouses

To Stores to Support Ads

Standard Orders To Warehouses

Direct to Store Segment

3rd Cut2nd Cut1st Cut

Small Orders

Picking and Special

Packaging

Product Placement in

DCs

Outside Packager

Redesigned Supply Chain

Special Handling---Make New

SKUs & Small Orders

New Approach for Positioning Inventory --Location and

In DCs

Geography/ Location--For Demanding Delivery &

Store Direct

Supply Chain Risk Mitigation

What Risk Is

About business opportunity

Concept traction - Fukushima

Insurance focus - assets

Plus contingency planning

Supply Chain Risk

Complexity

Geographic Scope

Offshoring/sourcing

Outsourcing

Low inventory

Lean manufacturing

JIT manufacturing

Supply Chain Risk

Deloitte Global Survey

45% say SC risk program only somewhat

effective or not effective

53% say SC disruptions have become more

costly

48% say frequency of risk disruptions with

negative outcomes have increased

More From Deloitte

Technology, industrial products, diversified

manufacturing most likely to say SC

disruptions have become more costly

Most costly outcome – margin erosion

71% say SC risk is important in strategic

decision-making

More

Top challenges to risk management (RM)

Lack of cross-functional collaboration (32%)

Cost of implementing RM strategies (26%)

SC RM is organized around silos (75%)

Leads to lack of visibility and collaboration

Makes difficult to assess and manage risk on

holistic basis

Threat Sources

• Natural disasters

• Geopolitical

• Pandemics

• Technological

• Terrorists

• Commodity prices

Sources• Labor costs

• Currency

• Ports

• Markets

• Suppliers

• Execution

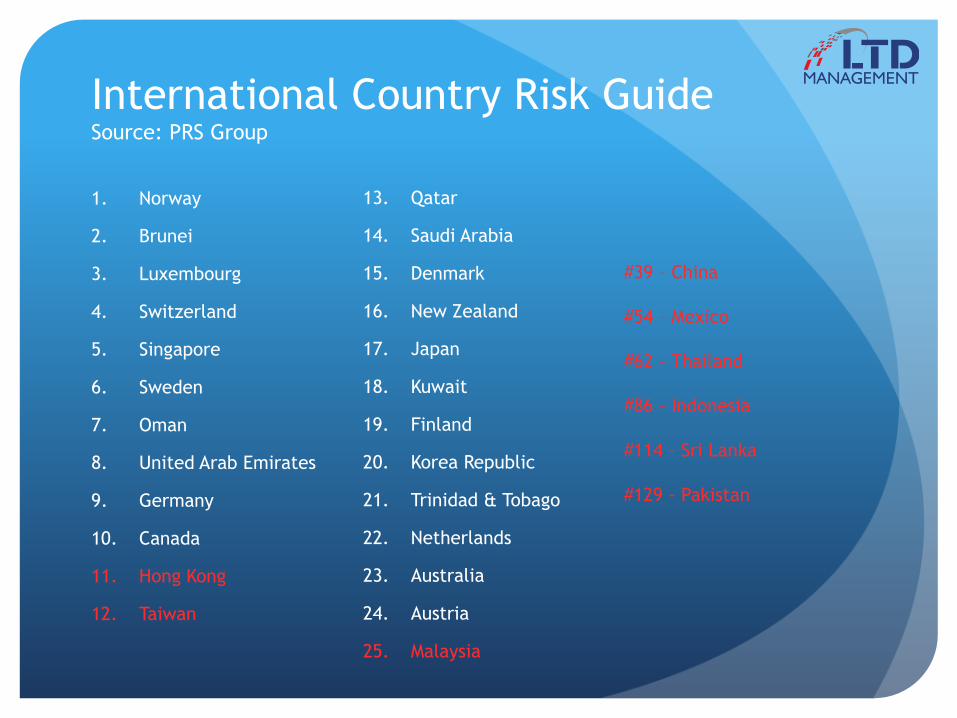

International Country Risk GuideSource: PRS Group

1. Norway

2. Brunei

3. Luxembourg

4. Switzerland

5. Singapore

6. Sweden

7. Oman

8. United Arab Emirates

9. Germany

10. Canada

11. Hong Kong

12. Taiwan

#39 – China

#54 – Mexico

#62 - Thailand

#86 – Indonesia

#114 – Sri Lanka

#129 - Pakistan

13. Qatar

14. Saudi Arabia

15. Denmark

16. New Zealand

17. Japan

18. Kuwait

19. Finland

20. Korea Republic

21. Trinidad & Tobago

22. Netherlands

23. Australia

24. Austria

25. Malaysia

SuppliersTier 1 Suppliers and More

Risk

Measure risk

Financial impact

Time to recover

Identification and mitigation – not just for MNC’s

Cannot mitigate what you do not identify

For IGA?

Where Will Your

Supply Chain

Take You?