Embed Size (px)

Citation preview

Presented By:Matti UR Rehman

CIIT/FA12-BBA-058/ATD

Outline

• Introduction• Business• Service Design• Performance Management and appraisal• Innovation in HBL• Our Suggestions for betterment of HBL

IntroductionHistory• Habib Bank Limited commonly referred to as "HBL" and head-quartered

in Habib Bank Plaza, Karachi, Pakistan, is the largest bank in Pakistan. • Mohammed Ali Jinnah, Pakistan's founding father, realized the

importance of financial intermediation while he was campaigning for the creation of a separate homeland for the Muslims of India.

• He persuaded the Habib family to establish a commercial bank that could serve the Indian Muslim community. His initiative resulted in the creation of Habib Bank in 1941, with HO in Bombay (now Mumbai), and fixed capital of 25,000 rupees.

• HBL was incorporated on 25th August 1941 and operated in the private sector until its nationalization in 1974.

• The bank has a network of 1425 branches in Pakistan and 55 branches worldwide.

• It has a domestic market share of over 40%. • It has operations in many countries including Australia, Bahrain,

Belgium, Canada, China, France.

Services

• Habib Bank offers the basic range of banking services to its customers, to include Commercial, Corporate, Investment, and Retail Banking, Treasury, and Islamic Banking.

Brand

• HBL is a Banking Company, which is engaged in Commercial & Retail Banking and related services domestically and overseas.

• HBL says – “Our brand identity is the outward expression

of what we stand for as an organization. This is summarized in our vision, mission and is supported by our values.”

Vission & Mission

• Vision– “Enabling people to advance with confidence

and success”

• Mission– “To make our customers prosper, our staff

excel and create value for shareholders”

Values of HBL• Excellence

– The markets in which HBL operates are very competitive, giving their customers an abundance of choice.

– Only through being the very best - in terms of the service HBL offers, its products and premises - can it hope to be successful and grow.

• Integrity– HBL is the leading bank in Pakistan and its success depends upon

• trust.• Its customers• society in general

• Customer focus– HBL understands fully the needs of its customers and adapts its products and

services to meet these. HBL always strives to put the satisfaction of its customers first.

• Meritocracy– HBL believes in giving opportunities and advantages to its employees on the basis of

their ability.• Progressiveness

– HBL believes in the advancement of society through the adoption of enlightened working practices, innovative new products and processes, and a spirit of enterprise.

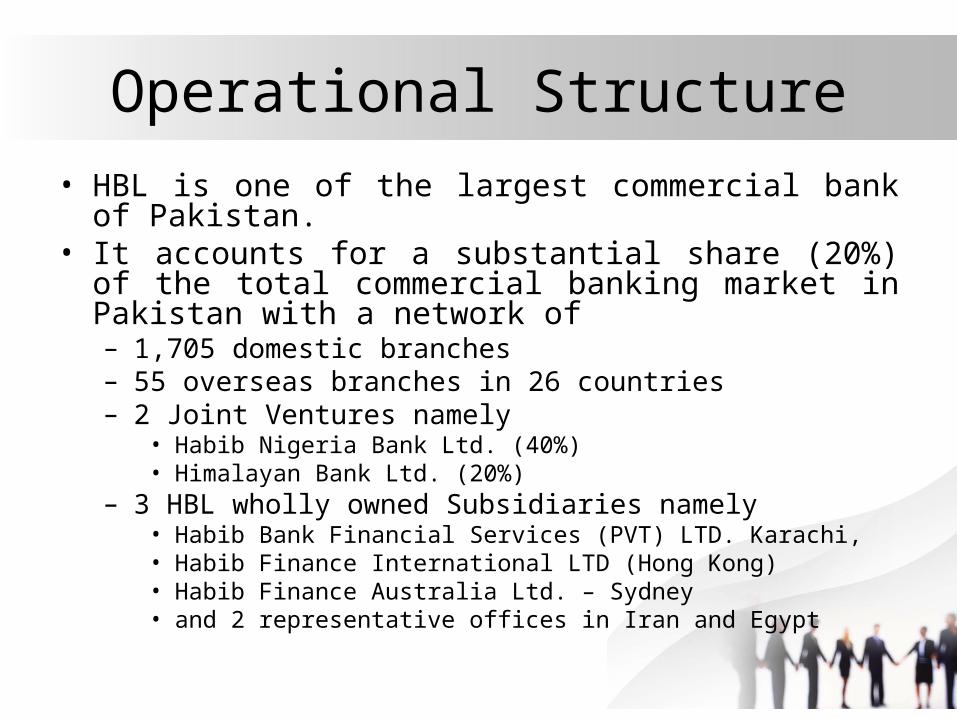

Operational Structure

• HBL is one of the largest commercial bank of Pakistan. • It accounts for a substantial share (20%) of the total

commercial banking market in Pakistan with a network of– 1,705 domestic branches– 55 overseas branches in 26 countries – 2 Joint Ventures namely

• Habib Nigeria Bank Ltd. (40%)• Himalayan Bank Ltd. (20%)

– 3 HBL wholly owned Subsidiaries namely • Habib Bank Financial Services (PVT) LTD. Karachi,• Habib Finance International LTD (Hong Kong) • Habib Finance Australia Ltd. – Sydney• and 2 representative offices in Iran and Egypt

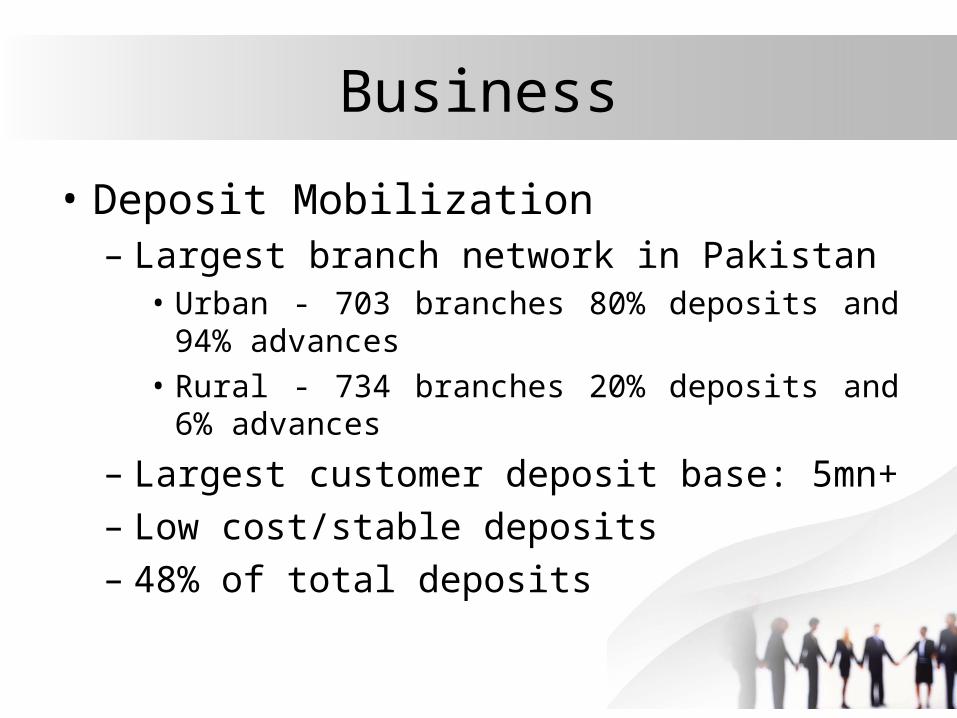

Business

• Deposit Mobilization– Largest branch network in Pakistan

• Urban - 703 branches 80% deposits and 94% advances

• Rural - 734 branches 20% deposits and 6% advances

– Largest customer deposit base: 5mn+– Low cost/stable deposits– 48% of total deposits

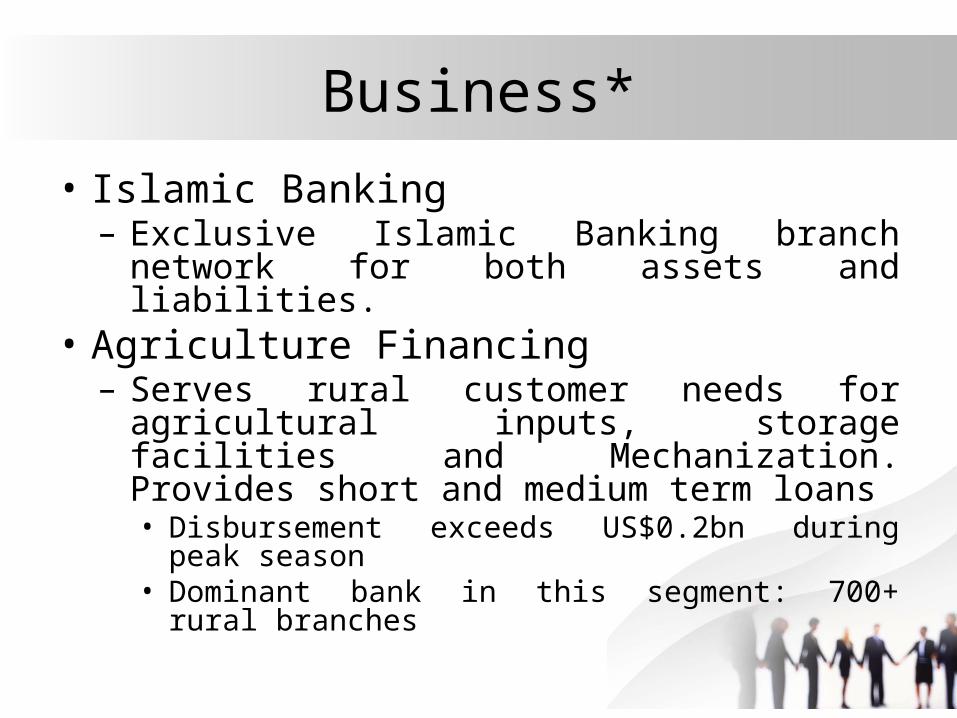

Business*

• Islamic Banking– Exclusive Islamic Banking branch network for

both assets and liabilities.• Agriculture Financing

– Serves rural customer needs for agricultural inputs, storage facilities and Mechanization. Provides short and medium term loans

• Disbursement exceeds US$0.2bn during peak season

• Dominant bank in this segment: 700+ rural branches

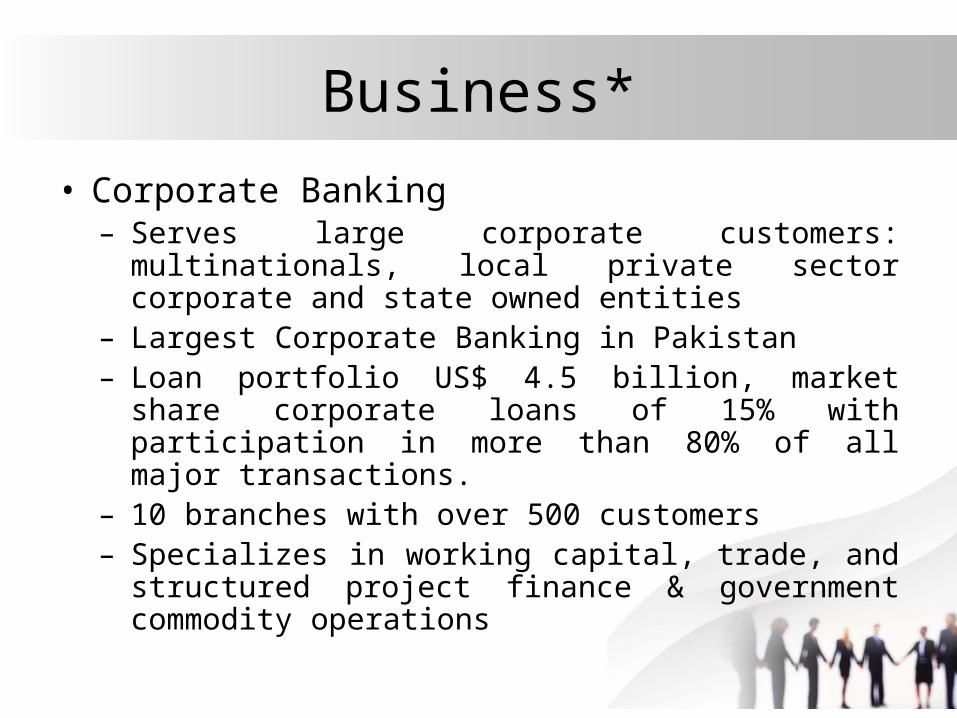

Business*

• Corporate Banking– Serves large corporate customers: multinationals,

local private sector corporate and state owned entities– Largest Corporate Banking in Pakistan– Loan portfolio US$ 4.5 billion, market share corporate

loans of 15% with participation in more than 80% of all major transactions.

– 10 branches with over 500 customers– Specializes in working capital, trade, and structured

project finance & government commodity operations

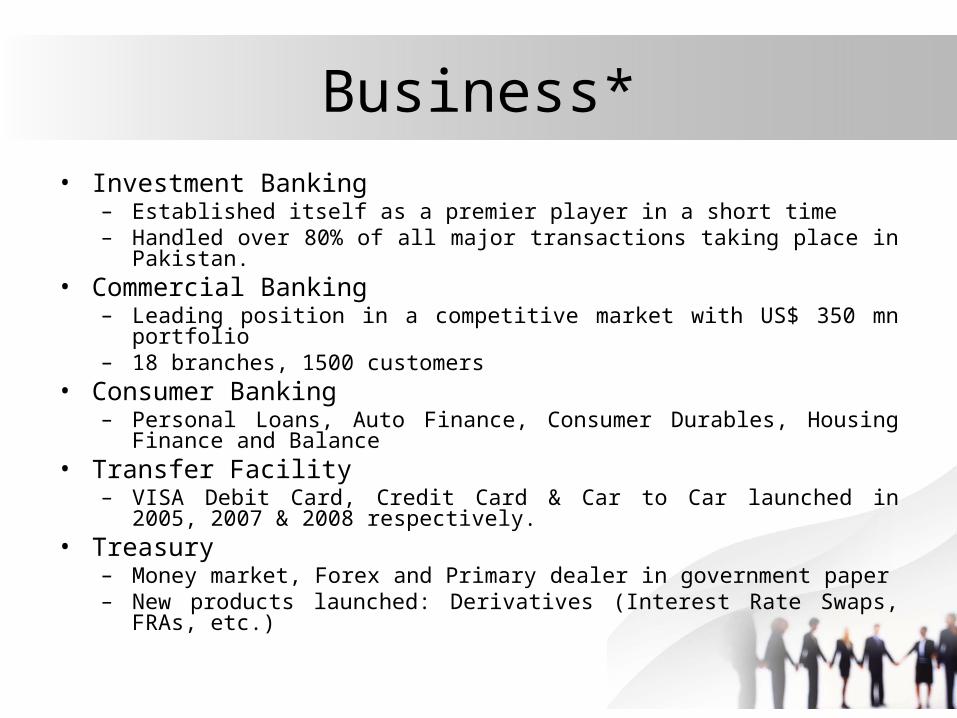

Business*• Investment Banking

– Established itself as a premier player in a short time– Handled over 80% of all major transactions taking place in Pakistan.

• Commercial Banking– Leading position in a competitive market with US$ 350 mn portfolio– 18 branches, 1500 customers

• Consumer Banking– Personal Loans, Auto Finance, Consumer Durables, Housing Finance and

Balance• Transfer Facility

– VISA Debit Card, Credit Card & Car to Car launched in 2005, 2007 & 2008 respectively.

• Treasury– Money market, Forex and Primary dealer in government paper– New products launched: Derivatives (Interest Rate Swaps, FRAs, etc.)

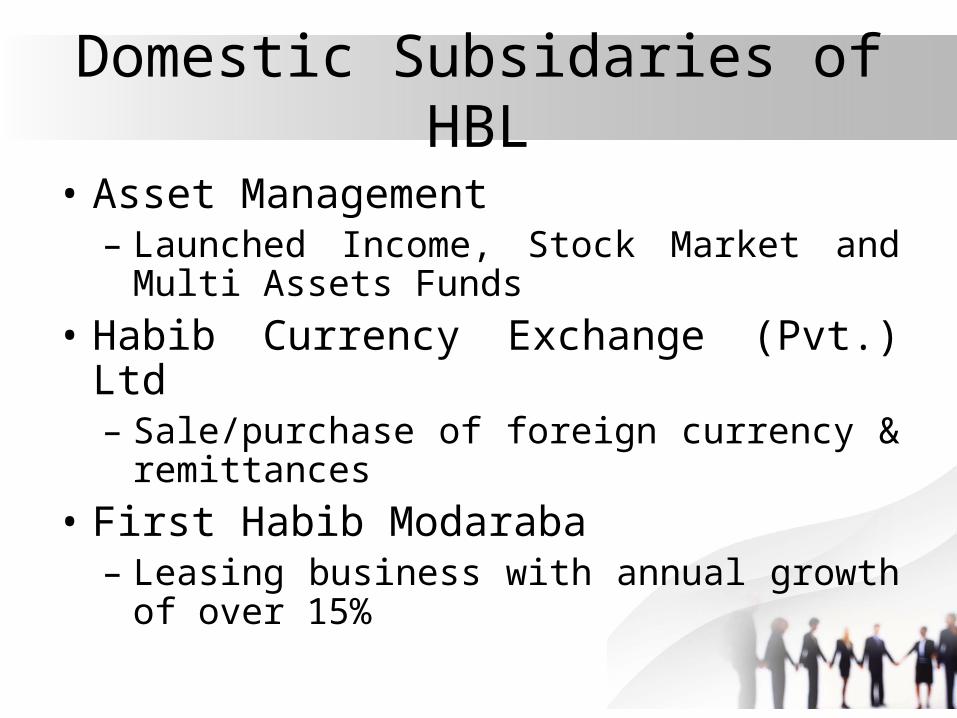

Domestic Subsidaries of HBL

• Asset Management– Launched Income, Stock Market and Multi

Assets Funds

• Habib Currency Exchange (Pvt.) Ltd– Sale/purchase of foreign currency &

remittances

• First Habib Modaraba– Leasing business with annual growth of over

15%

Service Design

• The Main services of banks are account opening and the steps involved in opening an account are: – Customer (who submit money in bank)– Bank staff (they deliver their services ) – Bank offered (interest rate, free check

book, ATM card, free SMS alert)• These 3 are further divided in 8 which are

discussed as under:

Service Design*

• Step 1– Customer has some money he wants to deposit it in bank locker

to secure money from theft or any other risk

• Step2– After entering in bank he get information from info cell or read

charts which are placed in wall of bank or get information from internet official website of HBL

• Step 3– After getting information ha directly met account officer for

opening account the account officer asked him for type of account

• HBL value account• HBL saving Account• HBL Student Account

Service Design*

• Step 4– After giving information to customer the choice of him/her which

type of account he/she is opening for• Step 5

– Selecting a/c account officer gives him bank opening account form. Customer has to fill it and give basic information e.g.

• name • Father name• Postal address • Mobile number• Signature

• Step 6– After completing form he submitted to account officer. Checking from

officered asked him to submit 500 rupees to get dummy account number after 3 days you get original account number and you become regular customer of bank

Service Design*

• Step7– A/c officer sends hos form to head office Islamabad, – they verify person from NADRA, – after 3 days they issued account number to customer,

check book and enter person name and account number in bank.

– After this task customer become account holder of HBL

• Step 8– Account no issued manager calls customer to get

ATM card check book from branch

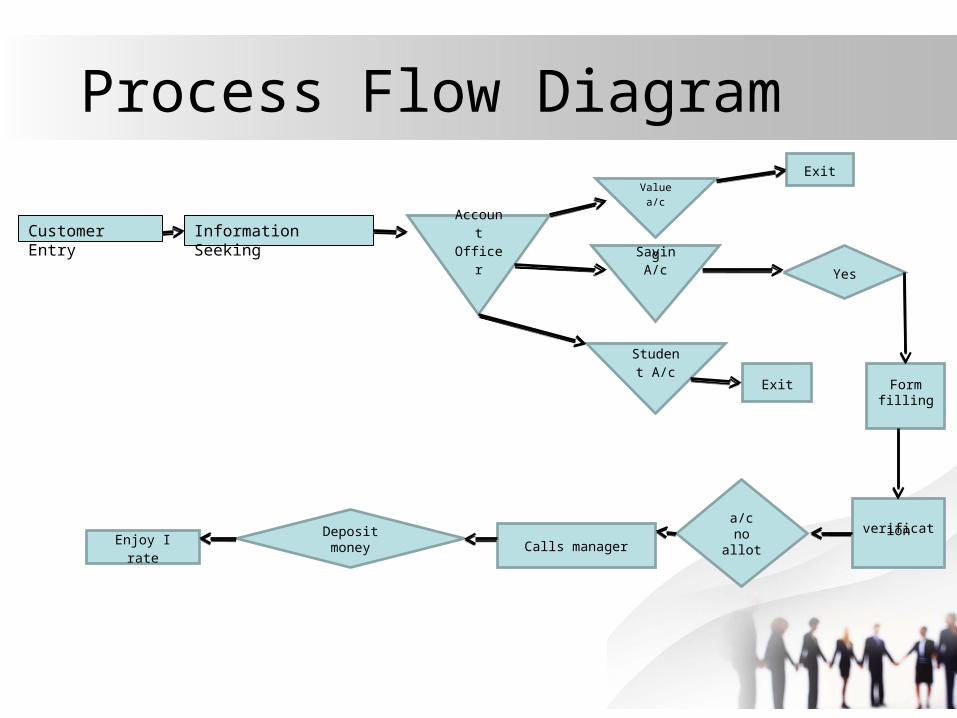

Process Flow Diagram

Customer Entry Information Seeking Account Officer

Value a/c

SavingA/c

Student A/c

Exit

Yes

Exit Formfilling

verificationa/c no allotCalls managerDeposit money

Enjoy I rate

Performance MGT & Appraisal

• Evaluating an employee’s current and past performance relative to its performance standards is called performance appraisal.

• A process that consolidates goal settings, performance appraisal, and development into a single common system to ensure that employee’s performance is according to company’s aims is called performance management

Performance MGT & Appraisal*

• HBL’s performance management and reward systems ensure that goals are met in an effective and efficient manner.

• HBL defines a clear path for you to contribute to the organization’s overall goals, peppered with regular reviews and feedback to help you gauge your progress.

• At HBL growth is not a function of time but rather of performance.

• As your performance improves, the role that you play within the organization will accelerate to reflect your input.

• HBL generally uses BARS (Behaviorally anchored rating scale) it is an appraisal method that uses quantified scale with specific narrative examples of good and poor performance

Performance MGT & Appraisal*

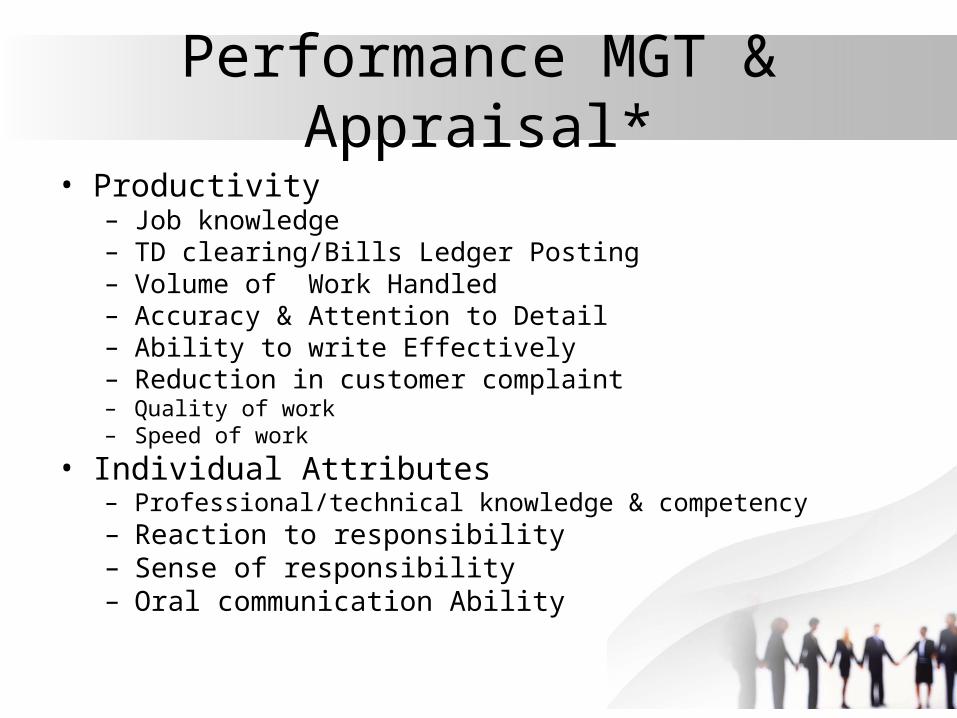

• HBL’s performance appraisal form contains two sheets, one is FORM B2 and other is FORM B3.

• FORM B2 contains appraisal for Clerical staff at branch or Field Offices there are two main headings Area/factors and level of achievement points. Level of achievement point contains five points’ ratings A (4), B (3), C (2), D (0-1) and N/A.

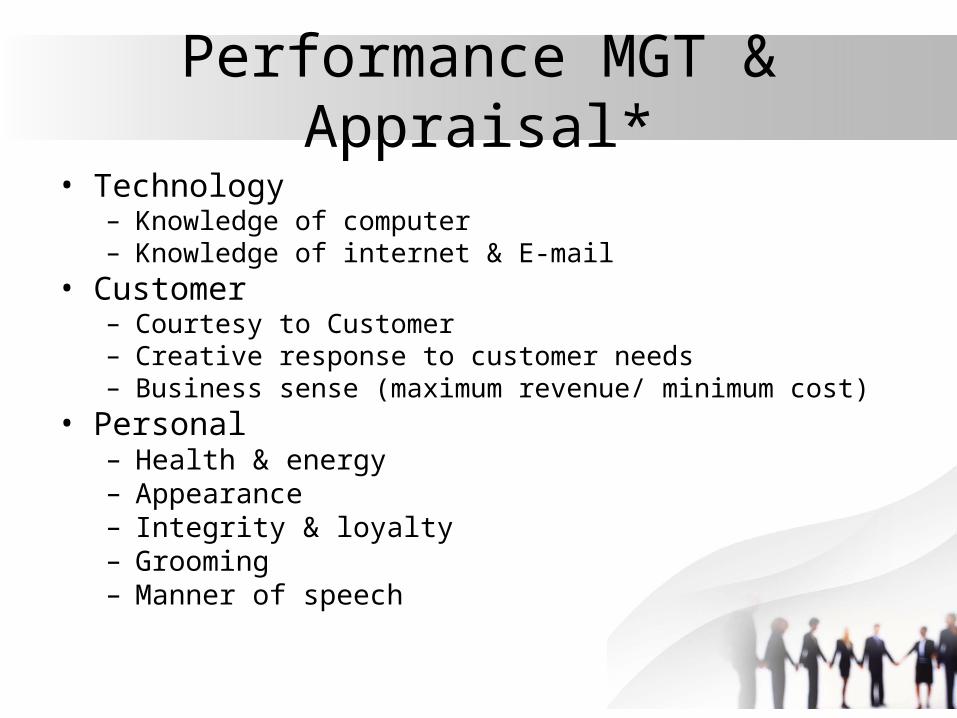

• AREA/factors contains five kinds of factors which are discussed as under:

Performance MGT & Appraisal*

• Productivity– Job knowledge– TD clearing/Bills Ledger Posting– Volume of Work Handled– Accuracy & Attention to Detail– Ability to write Effectively– Reduction in customer complaint– Quality of work – Speed of work

• Individual Attributes– Professional/technical knowledge & competency– Reaction to responsibility– Sense of responsibility– Oral communication Ability

Performance MGT & Appraisal*

• Technology– Knowledge of computer– Knowledge of internet & E-mail

• Customer– Courtesy to Customer– Creative response to customer needs– Business sense (maximum revenue/ minimum cost)

• Personal– Health & energy– Appearance– Integrity & loyalty– Grooming– Manner of speech

Innovation in HBL

• HBL believes in the advancement of society through the adoption of enlightened working practices, innovative new products and processes, and a spirit of enterprise.

• HBL launches new finance product to aid SME growth in UAE

– To play a pivotal role in the economic development of the UAE, HBL has launched yet another product, this time to finance the needs of SMEs.

– A flexible business finance solution, HBL Irtiqa'a is specifically for SMEs who have been operational for three years or more and want to develop and expand their business. With a loan tenure of up to three years available, the new offering enables investment in essential growth elements such as new premises, equipment and inventory.

Innovation in HBL*

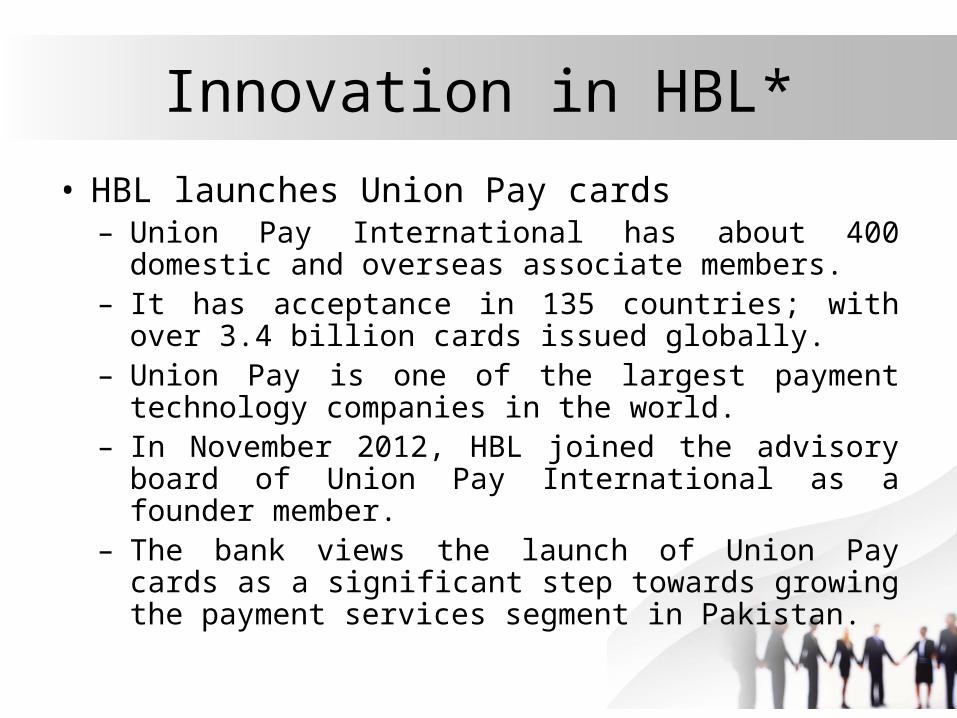

• HBL launches Union Pay cards– Union Pay International has about 400 domestic and

overseas associate members. – It has acceptance in 135 countries; with over 3.4

billion cards issued globally.– Union Pay is one of the largest payment technology

companies in the world. – In November 2012, HBL joined the advisory board of

Union Pay International as a founder member. – The bank views the launch of Union Pay cards as a

significant step towards growing the payment services segment in Pakistan.

Innovation in HBL*

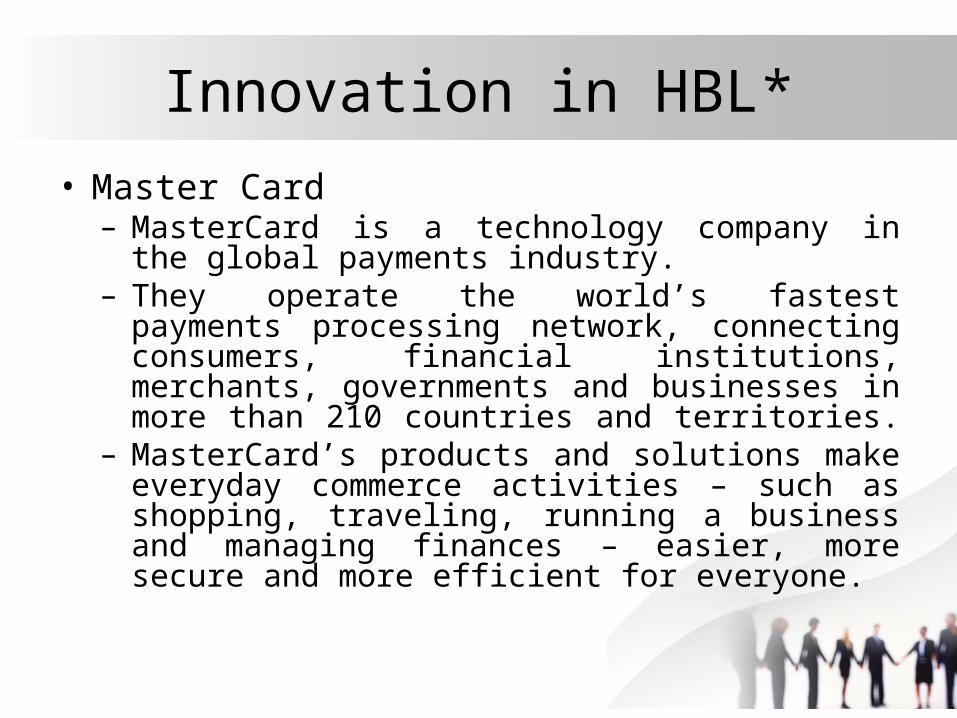

• Master Card– MasterCard is a technology company in the global

payments industry. – They operate the world’s fastest payments

processing network, connecting consumers, financial institutions, merchants, governments and businesses in more than 210 countries and territories.

– MasterCard’s products and solutions make everyday commerce activities – such as shopping, traveling, running a business and managing finances – easier, more secure and more efficient for everyone.

Suggestion to HBL• HBL is Pakistan’s largest bank. It should eliminate the cost of online banking

since they charge cost of online transaction or transfer. • HBL is initiator of Tele-banking service which is unique service in Pakistan.

Through this service we can get information about our personal account on telephone. Most of times customers find the service operator busy. HBL should increase their Tele-banking service center.

• HBL has begun campus recruiting which provides youngsters to come ahead but their campus recruiting process is so slow.

• They should increase their pace of hiring youngsters as other banks are doing successfully.

• They should provide more and more opportunities to fresh graduates and masters.

• The process of promotion at HBL is slow so they should maximize the promotion process which would be source of motivation for their employees.

• At many occasions HBL’s ATM network gets slow and their AT machines don’t allow for transaction they should renew their ATM links in order to make their customers avoiding inconvenience.

![Project_report - Final[1] POM](https://img.pdfslide.net/doc/110x75/577d2dbf1a28ab4e1eae3b28/projectreport-final1-pom.jpg)

![Iffco Pom Final[1]](https://img.pdfslide.net/doc/110x75/55263f3d550346856f8b4c5c/iffco-pom-final1.jpg)