Embed Size (px)

Citation preview

How OEMs Can Benefit from Multimodal HMI and Workload Managers

Apps are now common, focus is more on averting driver Apps are now common, focus is more on averting driver distraction with intelligent HMI solutionsdistraction with intelligent HMI solutions

N Praveen ChandrasekarN Praveen Chandrasekar

Program Manager – Telematics & Infotainment

5th April 2012

© 2012 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of

Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

Today’s Presenter

Experience base covers a wide range of industry sectors, forming long standing relationships with

Praveen Chandrasekar

Program Manager–Telematics & Infotainment Research

Frost & Sullivan

2

Experience base covers a wide range of industry sectors, forming long standing relationships with

senior executives in the

• Automotive Telematics and Infotainment

• Automotive Advanced Driver Assistance Systems

• IT and Telecoms

• Electric Vehicles

Focus Points

Today’s Agenda

• Gain top level technology and market trends impacting the infotainment market

• Provide a comparative overview of what different OEMs are doing with respect to

apps, HMI and connectivity in terms of offerings and business models

• Understand more in depth OEM and specially supplier activities in the areas of apps

3

and HMI

• Analyze what consumers are willing to pay for in terms of apps and HMI

• Conclusions and Strategic Recommendations

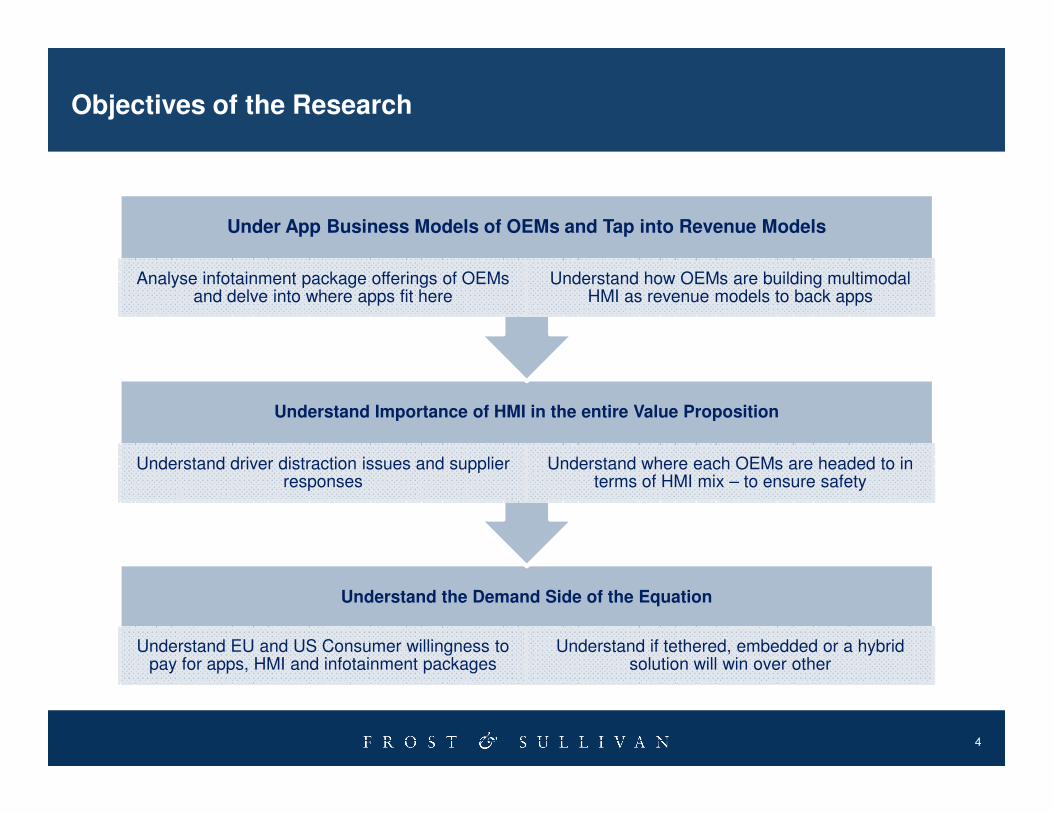

Objectives of the Research

Understand Importance of HMI in the entire Value Proposition

Under App Business Models of OEMs and Tap into Revenue Models

Analyse infotainment package offerings of OEMs and delve into where apps fit here

Understand how OEMs are building multimodal HMI as revenue models to back apps

4

Understand the Demand Side of the Equation

Understand EU and US Consumer willingness to pay for apps, HMI and infotainment packages

Understand if tethered, embedded or a hybrid solution will win over other

Understand Importance of HMI in the entire Value Proposition

Understand driver distraction issues and supplier responses

Understand where each OEMs are headed to in terms of HMI mix – to ensure safety

App Stores

Several OEMs have joined this bandwagon

such as BMW (Connected App), Mercedes Benz

(App Shop), Renault R-Link with dedicated app

store

Driver NHTSA guidelines to

avoid accessing

Major Market TrendsOEM business models for apps are built all around HMI value proposition

5

Driver Distraction Regulations

avoid accessing email/SMS on move and

to reduce levels to access and use voice

Emergence of New

Suppliers and

EcoSystem Partners

E.g. TomTom has risen to top tier player in the

European market also entering infotainment with

the R-Link on Renault Zoe

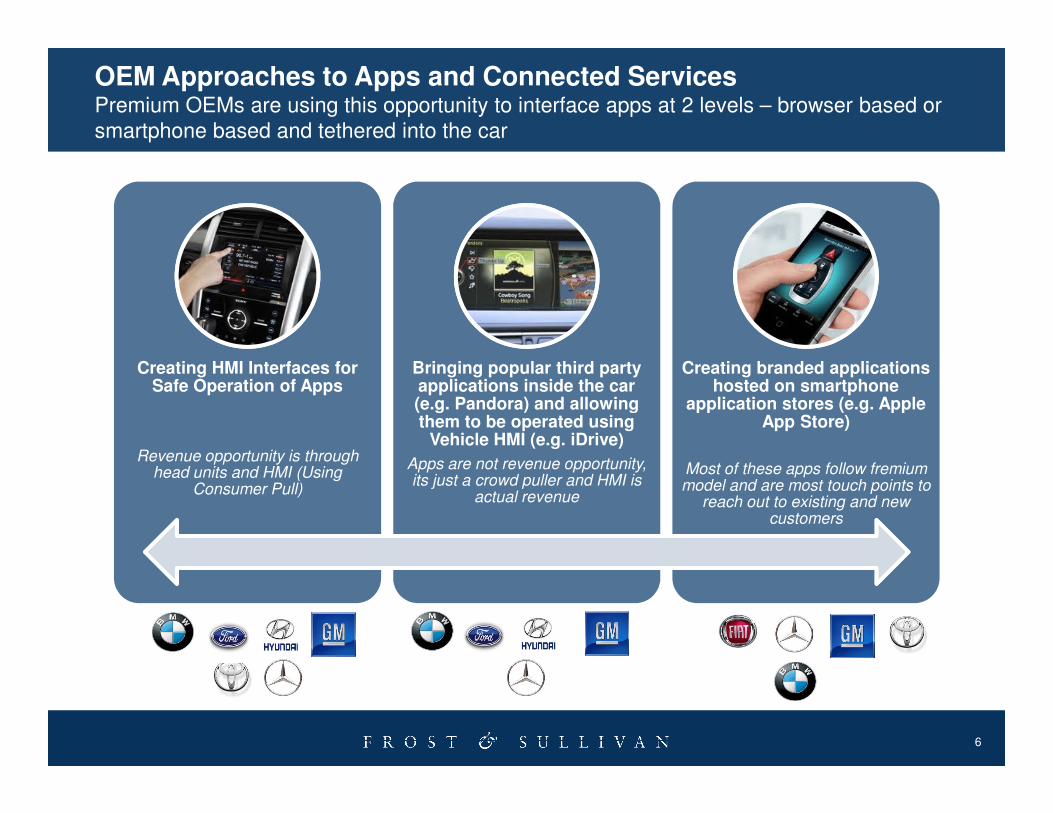

Creating HMI Interfaces for Safe Operation of Apps

Bringing popular third party applications inside the car (e.g. Pandora) and allowing

Creating branded applications hosted on smartphone

application stores (e.g. Apple

OEM Approaches to Apps and Connected ServicesPremium OEMs are using this opportunity to interface apps at 2 levels – browser based or smartphone based and tethered into the car

6

Revenue opportunity is through head units and HMI (Using

Consumer Pull)

(e.g. Pandora) and allowing them to be operated using

Vehicle HMI (e.g. iDrive)

Apps are not revenue opportunity, its just a crowd puller and HMI is

actual revenue

application stores (e.g. Apple App Store)

Most of these apps follow fremium model and are most touch points to

reach out to existing and new customers

• Awarded contract to Bouygues Telecom to develop app store to be launched in 208 model later 2012 – ten different apps powered by USB key (25/35). Some apps- MyPeugeot, Michelin Traffic. Available at annual subscription of 350 Euros

Peugeot Connect Apps

• Harman’s Aha radio platform is rapidly emerging as entertainment hub – assuring safety by voice operation wit h customers including – Subaru, Pioneer, Kenwood and 6 other premium OEMs. EU launch soon with Inrix traffic

Harman Aha Radio Platform

• Integrating dedicated app store called Mercedes Benz App Shop with first apps being park finder and morning star news for stocks and financial information. Available with the ComandOnline system and to be launched by March end 2012

Mercedes Benz App Shop

Recent Announcements and InnovationsHarman’s Aha Radio Platform has had tremendous traction in the last 6 months

7

• Showcased at CES 2012 a concept developed by Kia engineers over 4 months spending almost $500,000 a concept on IVI and user centred driving - with widgets, augmented reality navigation and dedicated app store

Kia Infotainment Concept

• Entune for US and Touch and GO for Europe developed by Harman. In Europe Touch & Go has MirrorLink access. Harman recently announced app interface for Touch & Go where users can access apps through dedicated Toyota portal

Toyota Entune & Touch & Go

• Fully integrated multimedia system with voice and steering mounted controls on a touch screen (unit supplied by TomTom) with dedicated apps powered by different players-e.g. Coyote Speed camera zone warning app

Renault R-Link

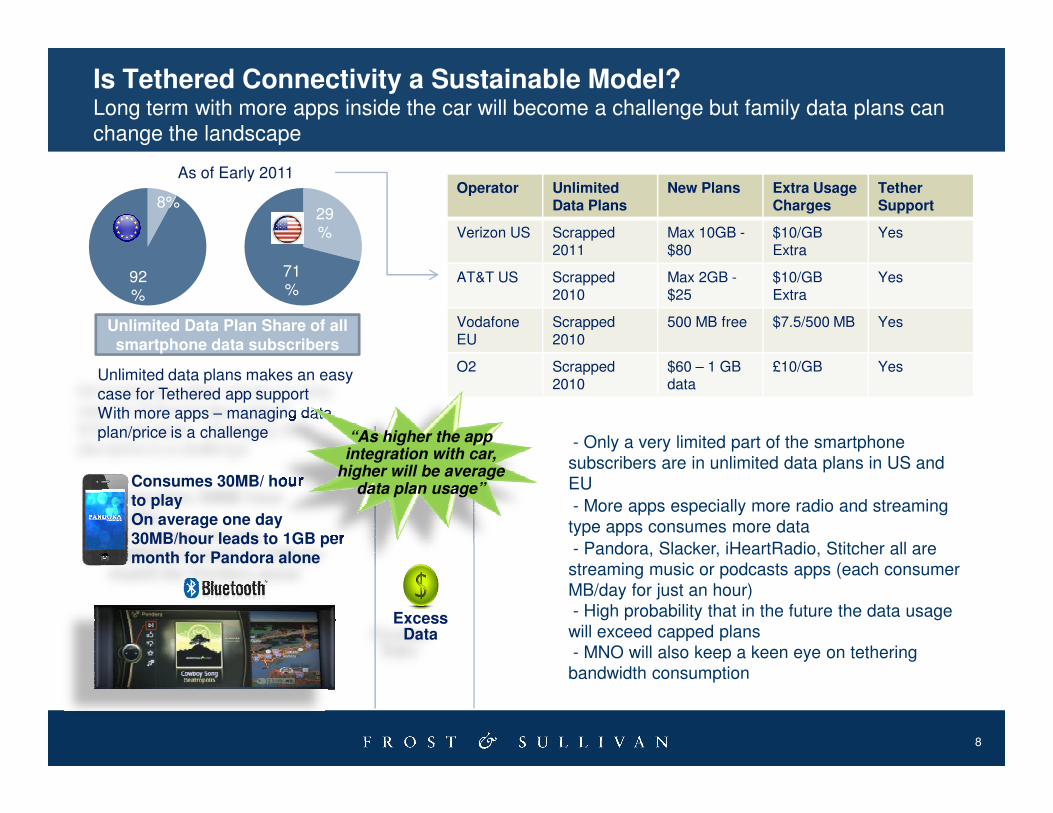

8%

92%

29%

71%

Unlimited Data Plan Share of all smartphone data subscribers

As of Early 2011Operator Unlimited

Data PlansNew Plans Extra Usage

ChargesTetherSupport

Verizon US Scrapped2011

Max 10GB -$80

$10/GBExtra

Yes

AT&T US Scrapped 2010

Max 2GB -$25

$10/GB Extra

Yes

VodafoneEU

Scrapped 2010

500 MB free $7.5/500 MB Yes

O2 Scrapped 2010

$60 – 1 GB data

£10/GB YesUnlimited data plans makes an easy case for Tethered app supportWith more apps – managing data

Is Tethered Connectivity a Sustainable Model?Long term with more apps inside the car will become a challenge but family data plans can change the landscape

8

Consumes 30MB/ hour to playOn average one day 30MB/hour leads to 1GB per month for Pandora alone

Excess Data

- Only a very limited part of the smartphone subscribers are in unlimited data plans in US and EU

- More apps especially more radio and streaming type apps consumes more data

- Pandora, Slacker, iHeartRadio, Stitcher all are streaming music or podcasts apps (each consumer MB/day for just an hour)- High probability that in the future the data usage will exceed capped plans- MNO will also keep a keen eye on tethering bandwidth consumption

With more apps – managing data plan/price is a challenge “As higher the app

integration with car, higher will be average

data plan usage”

Terminal Mode

Display of smartphone screen could distract driver

• Separate cost for HMI tooling software• Smartphone screen and application is replicated

to head unit as it is

HTML 5

Apps

OEM designed menu structures

and user interfaces suitable for

automotive environment

Display of applications in a less distractive interface

HTML 5 OpportunitiesQNX Actively Pushing it. HTML 5 allows OEMs to bring the focus back on the car

9

to head unit as it is automotive environment

• Phone with a web server is connected to head unit with

HTML5 engine.

• Allows two way interaction, if the head unit also has a

web server, allows hosting web pages on the phone.

• Allows OEMs to create a separate module where

graphics for individual functionality can be made and

addition of more features.

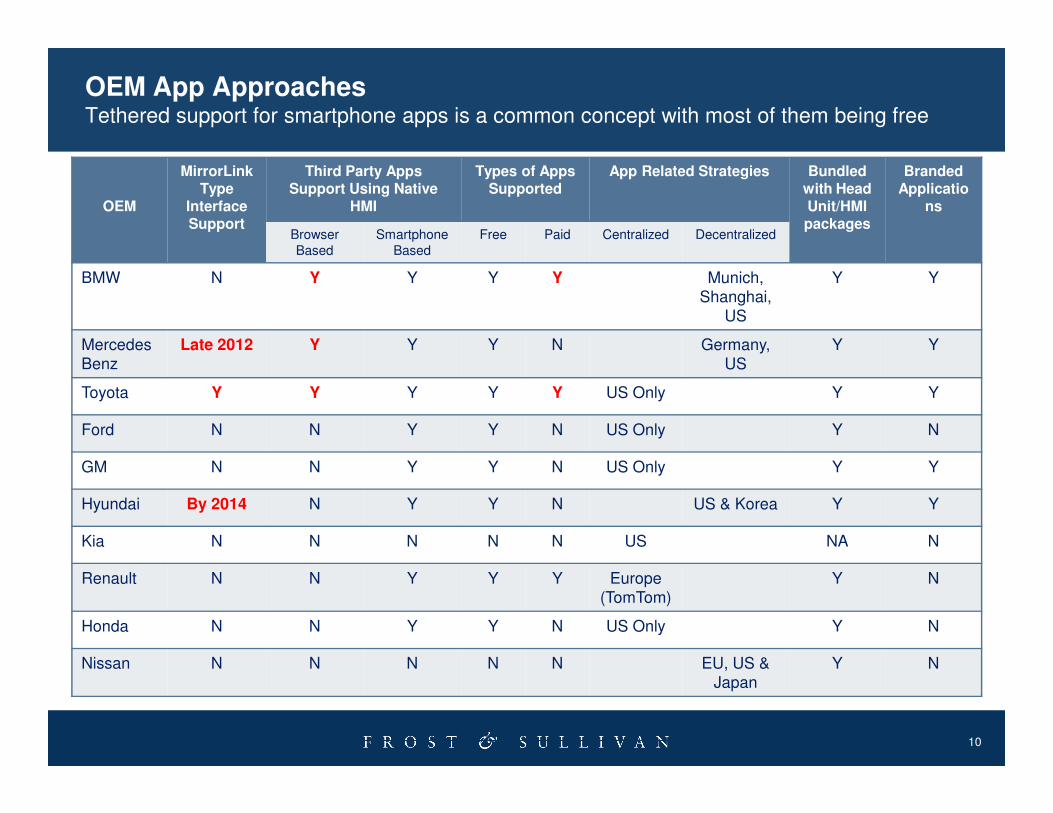

OEM App ApproachesTethered support for smartphone apps is a common concept with most of them being free

OEM

MirrorLink Type

Interface Support

Third Party Apps Support Using Native

HMI

Types of Apps Supported

App Related Strategies Bundledwith Head Unit/HMI packages

BrandedApplicatio

ns

Browser Based

SmartphoneBased

Free Paid Centralized Decentralized

BMW N Y Y Y Y Munich, Shanghai,

US

Y Y

Mercedes Benz

Late 2012 Y Y Y N Germany, US

Y Y

Toyota Y Y Y Y Y US Only Y Y

10

Ford N N Y Y N US Only Y N

GM N N Y Y N US Only Y Y

Hyundai By 2014 N Y Y N US & Korea Y Y

Kia N N N N N US NA N

Renault N N Y Y Y Europe (TomTom)

Y N

Honda N N Y Y N US Only Y N

Nissan N N N N N EU, US & Japan

Y N

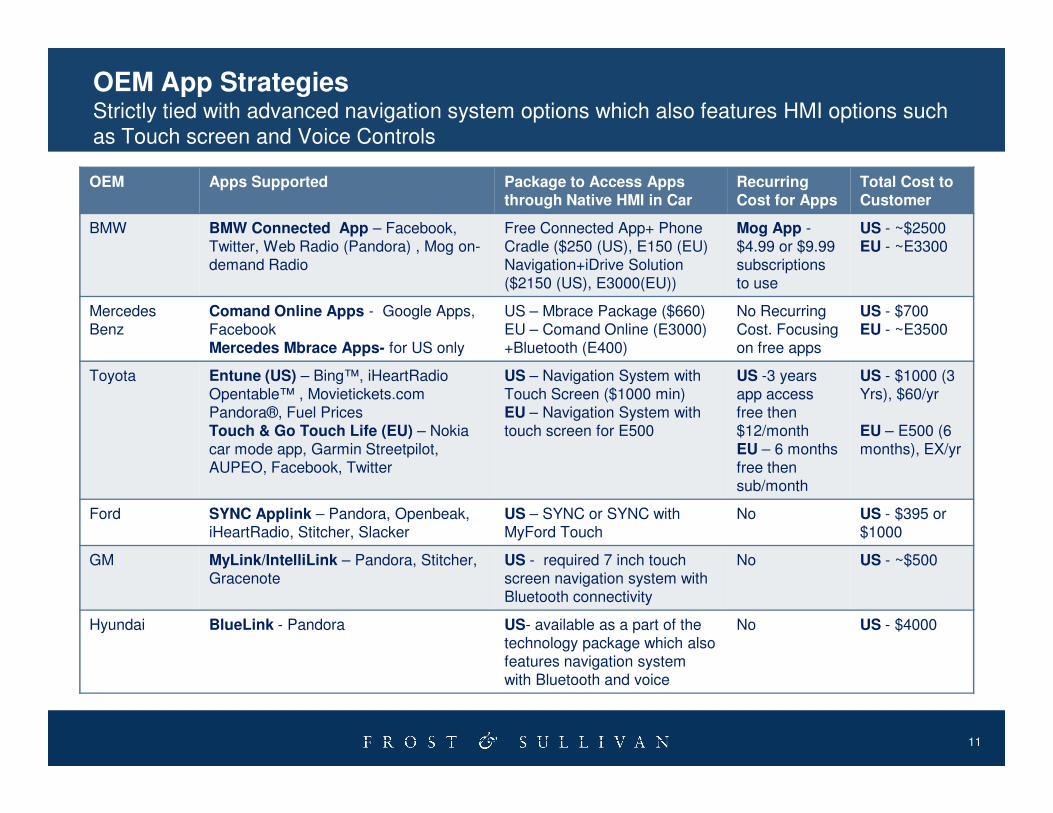

OEM App StrategiesStrictly tied with advanced navigation system options which also features HMI options such as Touch screen and Voice Controls

OEM Apps Supported Package to Access Apps through Native HMI in Car

RecurringCost for Apps

Total Cost to Customer

BMW BMW Connected App – Facebook, Twitter, Web Radio (Pandora) , Mog on-demand Radio

Free Connected App+ PhoneCradle ($250 (US), E150 (EU)Navigation+iDrive Solution ($2150 (US), E3000(EU))

Mog App -$4.99 or $9.99 subscriptions to use

US - ~$2500EU - ~E3300

Mercedes Benz

Comand Online Apps - Google Apps, FacebookMercedes Mbrace Apps- for US only

US – Mbrace Package ($660)EU – Comand Online (E3000) +Bluetooth (E400)

No RecurringCost. Focusing on free apps

US - $700EU - ~E3500

Toyota Entune (US) – Bing™, iHeartRadio Opentable™ , Movietickets.com Pandora®, Fuel Prices

US – Navigation System with Touch Screen ($1000 min) EU – Navigation System with

US -3 years app access free then

US - $1000 (3 Yrs), $60/yr

11

Pandora®, Fuel PricesTouch & Go Touch Life (EU) – Nokia car mode app, Garmin Streetpilot, AUPEO, Facebook, Twitter

EU – Navigation System with touch screen for E500

free then $12/monthEU – 6 months free then sub/month

EU – E500 (6 months), EX/yr

Ford SYNC Applink – Pandora, Openbeak, iHeartRadio, Stitcher, Slacker

US – SYNC or SYNC with MyFord Touch

No US - $395 or$1000

GM MyLink/IntelliLink – Pandora, Stitcher, Gracenote

US - required 7 inch touch screen navigation system with Bluetooth connectivity

No US - ~$500

Hyundai BlueLink - Pandora US- available as a part of the technology package which also features navigation system with Bluetooth and voice

No US - $4000

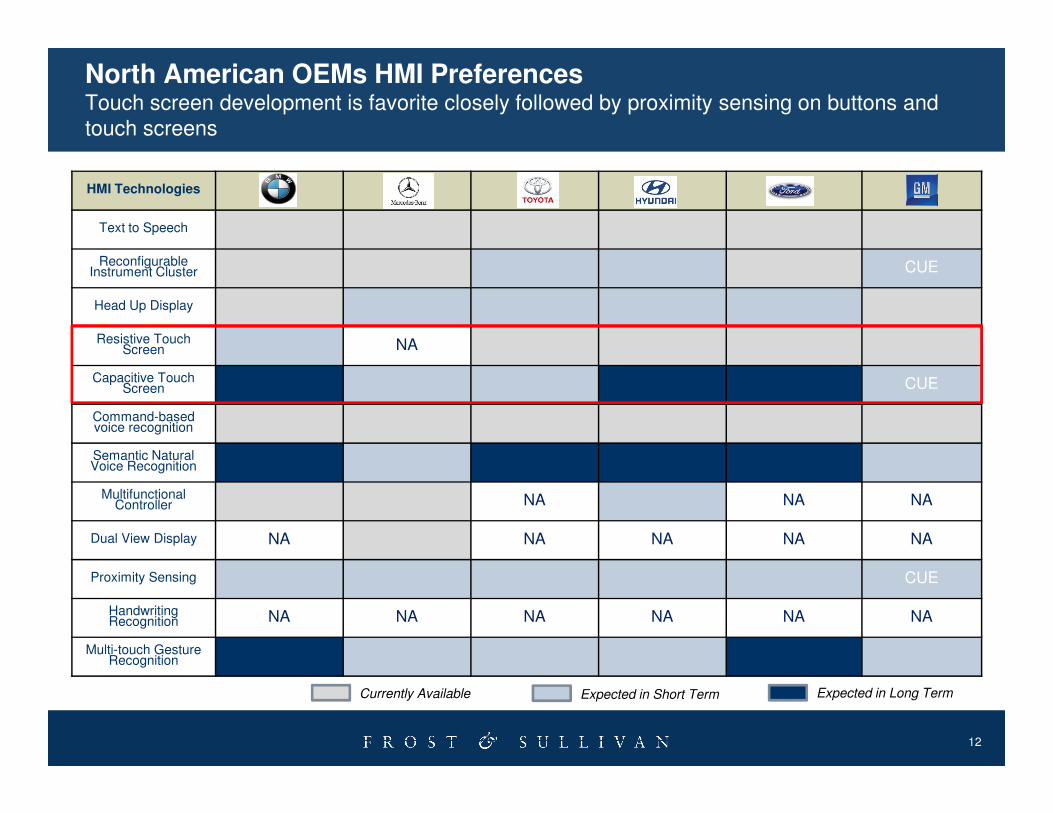

North American OEMs HMI PreferencesTouch screen development is favorite closely followed by proximity sensing on buttons and touch screens

HMI Technologies

Text to Speech

Reconfigurable Instrument Cluster CUE

Head Up Display

Resistive Touch Screen NA

Capacitive Touch Screen CUE

12

Command-based voice recognition

Semantic Natural Voice Recognition

Multifunctional Controller NA NA NA

Dual View Display NA NA NA NA NA

Proximity Sensing CUE

Handwriting Recognition NA NA NA NA NA NA

Multi-touch Gesture Recognition

Expected in Long TermExpected in Short TermCurrently Available

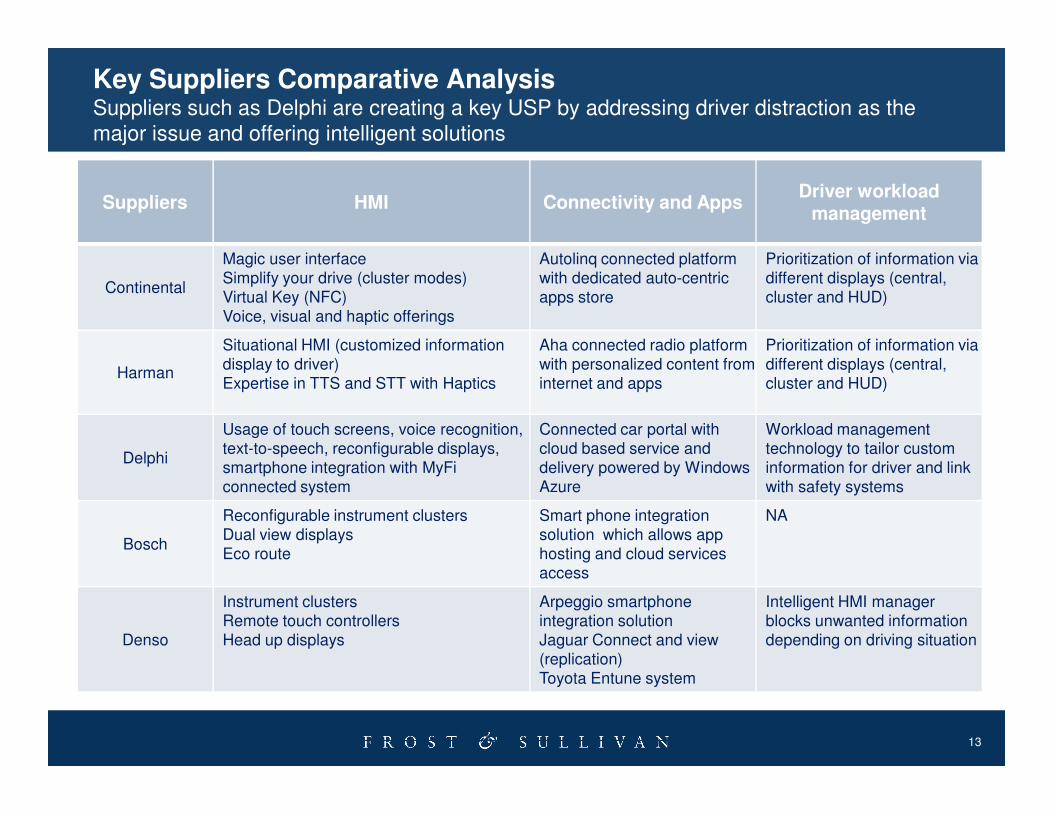

Suppliers HMI Connectivity and AppsDriver workload

management

Continental

Magic user interfaceSimplify your drive (cluster modes)Virtual Key (NFC)Voice, visual and haptic offerings

Autolinq connected platform with dedicated auto-centric apps store

Prioritization of information via different displays (central, cluster and HUD)

Harman

Situational HMI (customized information display to driver)Expertise in TTS and STT with Haptics

Aha connected radio platform with personalized content from internet and apps

Prioritization of information via different displays (central, cluster and HUD)

Key Suppliers Comparative AnalysisSuppliers such as Delphi are creating a key USP by addressing driver distraction as the major issue and offering intelligent solutions

13

Delphi

Usage of touch screens, voice recognition, text-to-speech, reconfigurable displays,smartphone integration with MyFi connected system

Connected car portal with cloud based service and delivery powered by Windows Azure

Workload management technology to tailor custom information for driver and linkwith safety systems

Bosch

Reconfigurable instrument clustersDual view displaysEco route

Smart phone integration solution which allows app hosting and cloud services access

NA

Denso

Instrument clustersRemote touch controllersHead up displays

Arpeggio smartphone integration solutionJaguar Connect and view (replication)Toyota Entune system

Intelligent HMI manager blocks unwanted informationdepending on driving situation

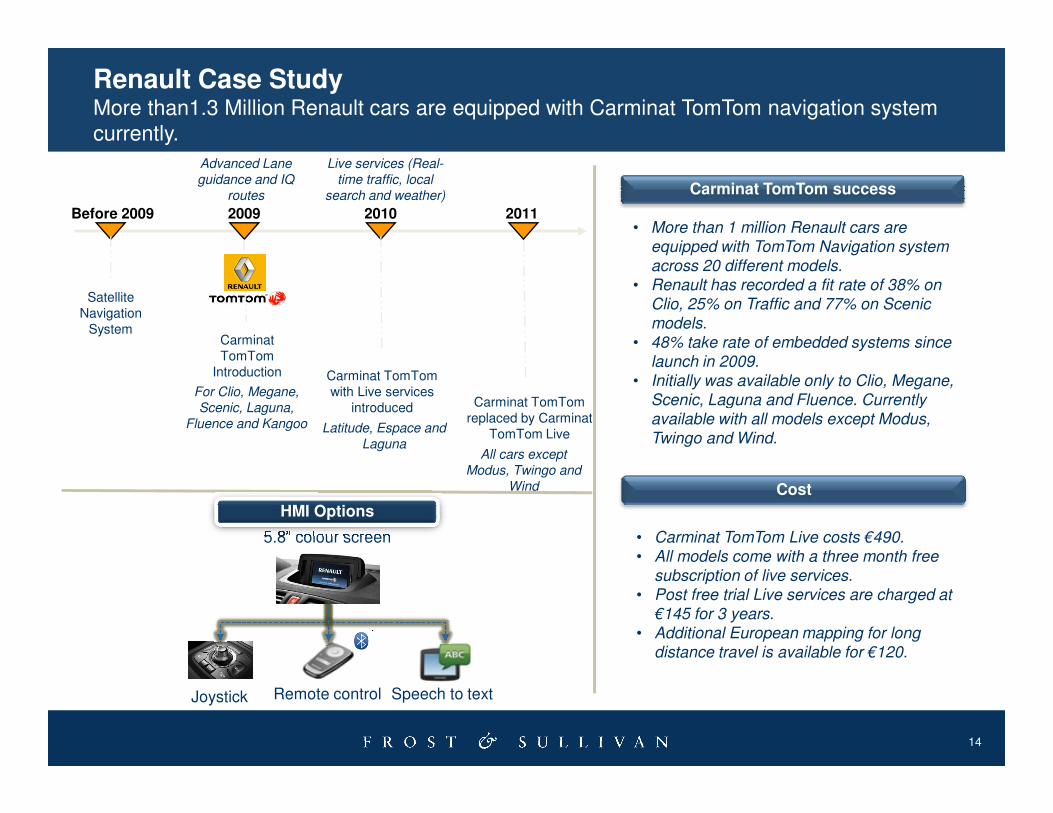

Before 2009 2009 2010

Satellite Navigation

SystemCarminat TomTom

Introduction Carminat TomTom with Live services

introduced Carminat TomTom

2011

For Clio, Megane,

Scenic, Laguna,

Advanced Lane

guidance and IQ

routes

Live services (Real-

time traffic, local

search and weather) Carminat TomTom success

• More than 1 million Renault cars are equipped with TomTom Navigation system across 20 different models.

• Renault has recorded a fit rate of 38% on Clio, 25% on Traffic and 77% on Scenic models.

• 48% take rate of embedded systems since launch in 2009.

• Initially was available only to Clio, Megane,

Scenic, Laguna and Fluence. Currently

Renault Case StudyMore than1.3 Million Renault cars are equipped with Carminat TomTom navigation system currently.

14

introduced Carminat TomTom replaced by Carminat

TomTom Live

Scenic, Laguna,

Fluence and Kangoo Latitude, Espace and

LagunaAll cars except

Modus, Twingo and

Wind

Scenic, Laguna and Fluence. Currently available with all models except Modus, Twingo and Wind.

Cost

• Carminat TomTom Live costs €490. • All models come with a three month free

subscription of live services. • Post free trial Live services are charged at

€145 for 3 years. • Additional European mapping for long

distance travel is available for €120.

5.8” colour screen

Joystick Remote control Speech to text

HMI Options

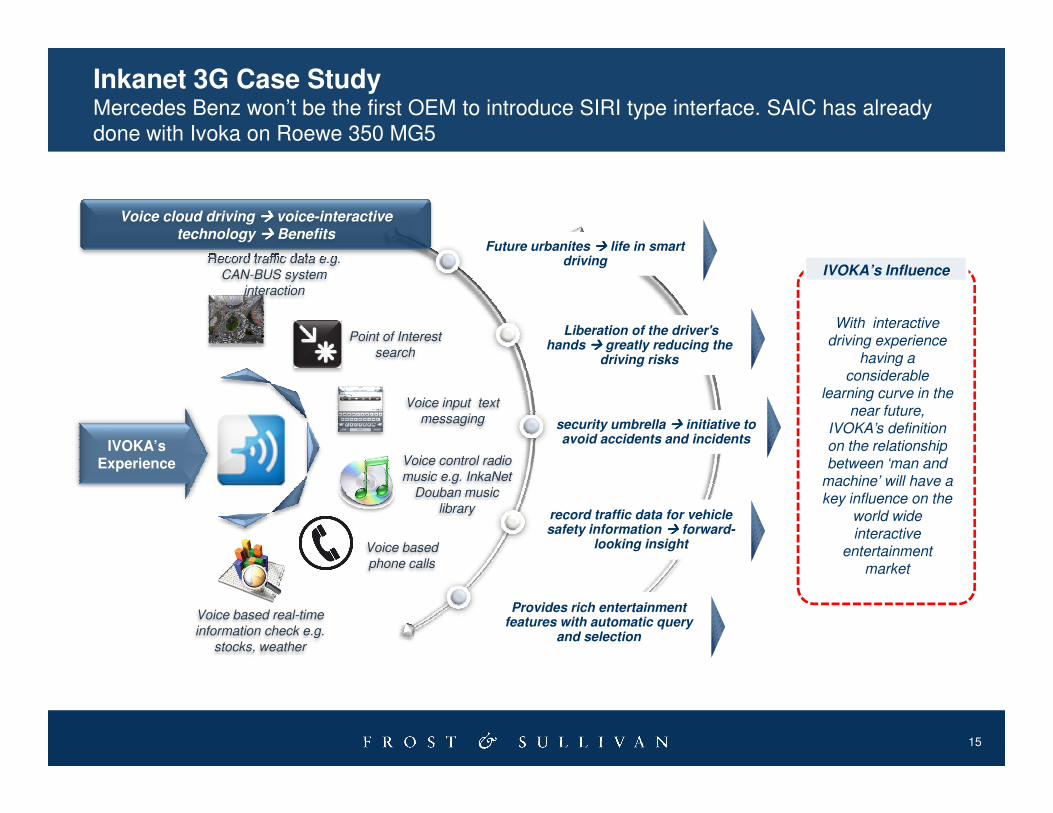

Inkanet 3G Case StudyMercedes Benz won’t be the first OEM to introduce SIRI type interface. SAIC has already done with Ivoka on Roewe 350 MG5

Point of Interest

search

Voice input text

Liberation of the driver's hands ���� greatly reducing the

driving risks

Future urbanites ���� life in smart drivingRecord traffic data e.g.

CAN-BUS system

interaction

With interactive driving experience

having a considerable

learning curve in the near future,

IVOKA’s Influence

Voice cloud driving ���� voice-interactive technology ���� Benefits

15

Voice input text

messaging

Voice control radio

music e.g. InkaNet

Douban music

library

Voice based

phone calls

IVOKA’s Experience

Voice based real-time

information check e.g.

stocks, weather

security umbrella ���� initiative to avoid accidents and incidents

record traffic data for vehicle safety information ���� forward-

looking insight

Provides rich entertainment features with automatic query

and selection

near future, IVOKA’s definition on the relationship between ‘man and

machine’ will have a key influence on the

world wide interactive

entertainment market

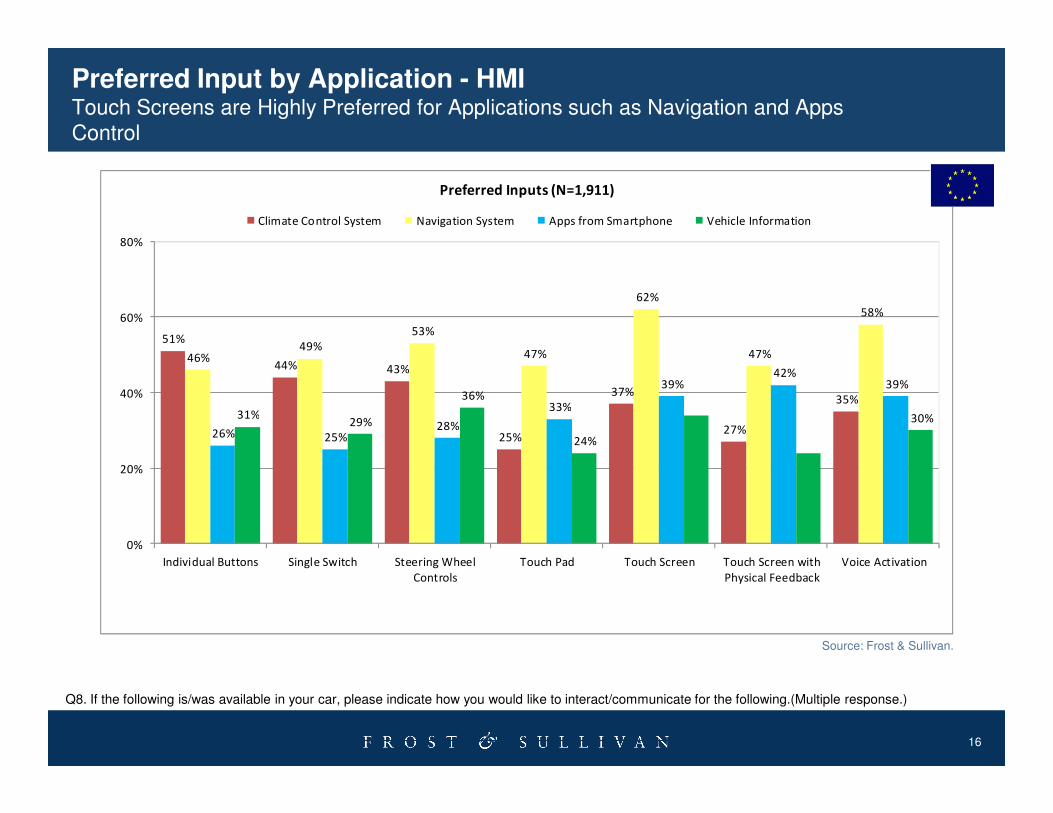

51%

44% 43%

37%35%

46%49%

53%

47%

62%

47%

58%

33%

39%42%

39%

31%

36%40%

60%

80%

Preferred Inputs (N=1,911)

Climate Control System Navigation System Apps from Smartphone Vehicle Information

Preferred Input by Application - HMITouch Screens are Highly Preferred for Applications such as Navigation and Apps Control

16

25%27%26% 25%

28%

33%31%

29%

24%

30%

0%

20%

Individual Buttons Single Switch Steering Wheel

Controls

Touch Pad Touch Screen Touch Screen with

Physical Feedback

Voice Activation

Q8. If the following is/was available in your car, please indicate how you would like to interact/communicate for the following.(Multiple response.)

Source: Frost & Sullivan.

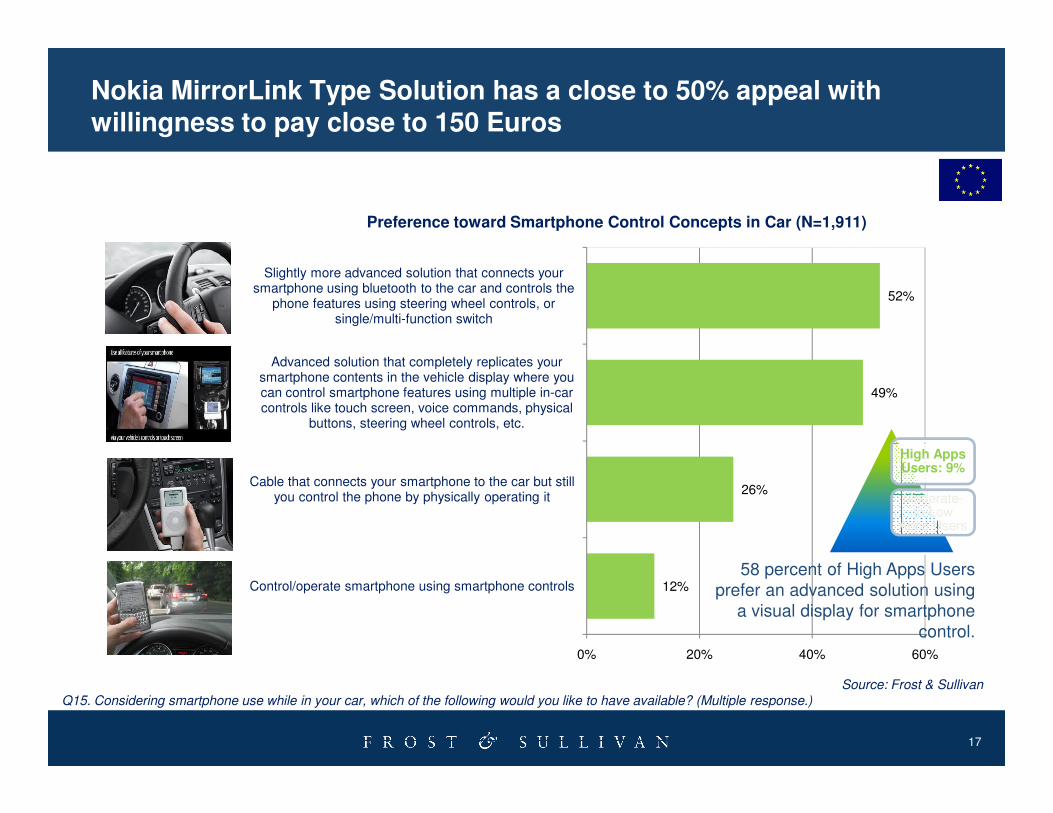

Nokia MirrorLink Type Solution has a close to 50% appeal with willingness to pay close to 150 Euros

49%

52%

Advanced solution that completely replicates your smartphone contents in the vehicle display where you can control smartphone features using multiple in-car controls like touch screen, voice commands, physical

Slightly more advanced solution that connects your smartphone using bluetooth to the car and controls the

phone features using steering wheel controls, or single/multi-function switch

Preference toward Smartphone Control Concepts in Car (N=1,911)

17

12%

26%

0% 20% 40% 60%

Control/operate smartphone using smartphone controls

Cable that connects your smartphone to the car but still you control the phone by physically operating it

controls like touch screen, voice commands, physical buttons, steering wheel controls, etc.

Source: Frost & Sullivan

Q15. Considering smartphone use while in your car, which of the following would you like to have available? (Multiple response.)

High Apps Users: 9%

Moderate-to-Low

Apps Users

58 percent of High Apps Users prefer an advanced solution using

a visual display for smartphone control.

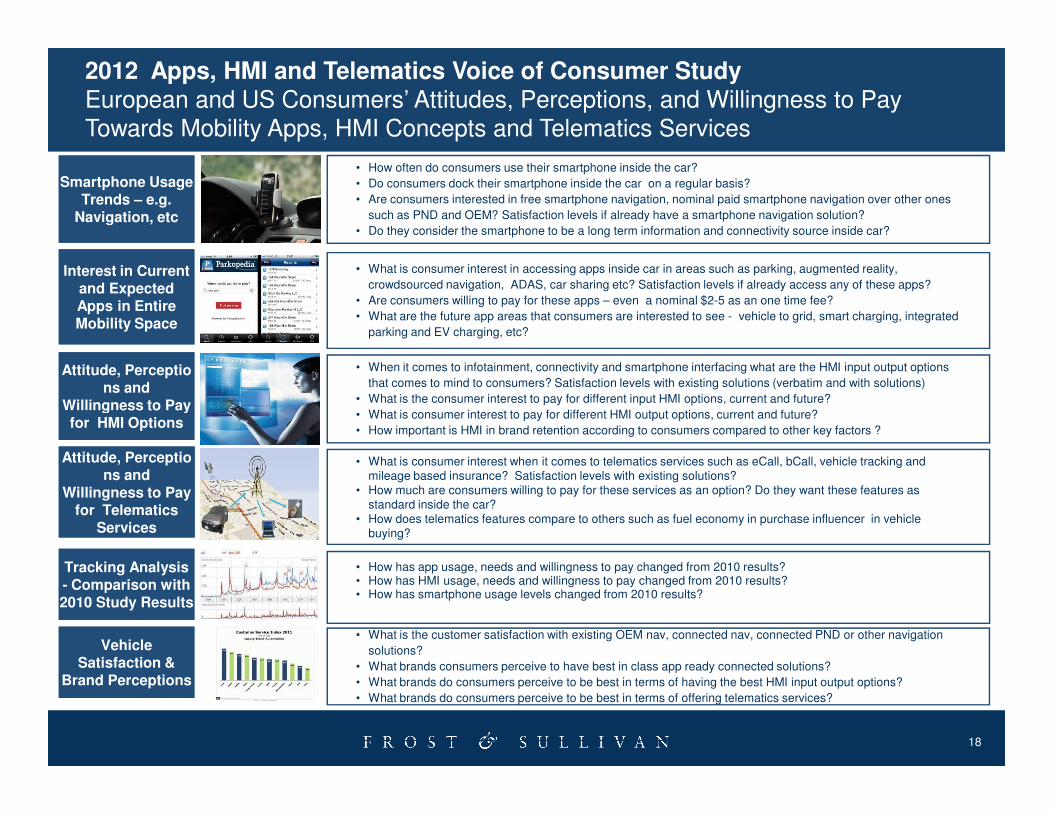

• How often do consumers use their smartphone inside the car?

• Do consumers dock their smartphone inside the car on a regular basis?

• Are consumers interested in free smartphone navigation, nominal paid smartphone navigation over other ones

such as PND and OEM? Satisfaction levels if already have a smartphone navigation solution?

• Do they consider the smartphone to be a long term information and connectivity source inside car?

• What is consumer interest in accessing apps inside car in areas such as parking, augmented reality,

crowdsourced navigation, ADAS, car sharing etc? Satisfaction levels if already access any of these apps?

• Are consumers willing to pay for these apps – even a nominal $2-5 as an one time fee?

• What are the future app areas that consumers are interested to see - vehicle to grid, smart charging, integrated

parking and EV charging, etc?

• When it comes to infotainment, connectivity and smartphone interfacing what are the HMI input output options

that comes to mind to consumers? Satisfaction levels with existing solutions (verbatim and with solutions)

• What is the consumer interest to pay for different input HMI options, current and future?

Smartphone Usage Trends – e.g.

Navigation, etc

Interest in Current and Expected Apps in Entire Mobility Space

Attitude, Perceptions and

Willingness to Pay

2012 Apps, HMI and Telematics Voice of Consumer StudyEuropean and US Consumers’ Attitudes, Perceptions, and Willingness to Pay Towards Mobility Apps, HMI Concepts and Telematics Services

18

• What is consumer interest to pay for different HMI output options, current and future?

• How important is HMI in brand retention according to consumers compared to other key factors ?

• What is the customer satisfaction with existing OEM nav, connected nav, connected PND or other navigation

solutions?

• What brands consumers perceive to have best in class app ready connected solutions?

• What brands do consumers perceive to be best in terms of having the best HMI input output options?

• What brands do consumers perceive to be best in terms of offering telematics services?

• How has app usage, needs and willingness to pay changed from 2010 results? • How has HMI usage, needs and willingness to pay changed from 2010 results?• How has smartphone usage levels changed from 2010 results?

Vehicle Satisfaction &

Brand Perceptions

Tracking Analysis - Comparison with 2010 Study Results

• What is consumer interest when it comes to telematics services such as eCall, bCall, vehicle tracking and mileage based insurance? Satisfaction levels with existing solutions?

• How much are consumers willing to pay for these services as an option? Do they want these features as standard inside the car?

• How does telematics features compare to others such as fuel economy in purchase influencer in vehicle buying?

Attitude, Perceptions and

Willingness to Pay for Telematics

Services

Willingness to Pay for HMI Options

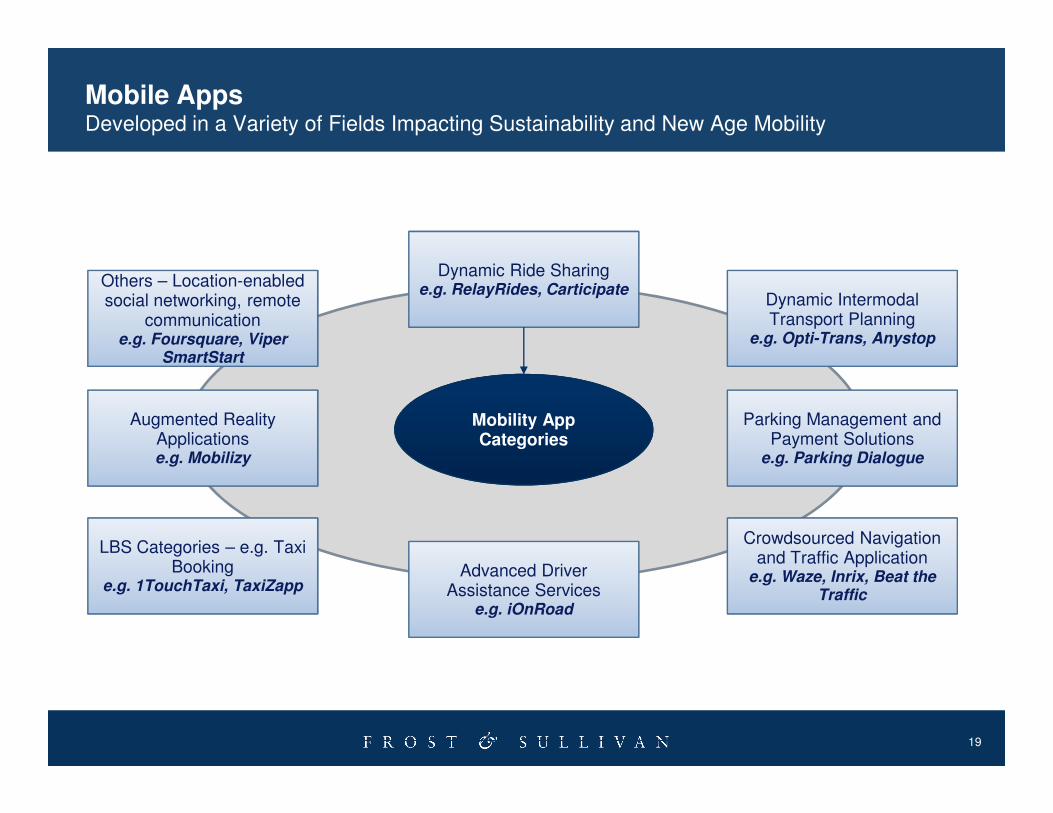

Dynamic Intermodal Transport Planning

e.g. Opti-Trans, Anystop

Dynamic Ride Sharinge.g. RelayRides, Carticipate

Others – Location-enabled social networking, remote

communicatione.g. Foursquare, Viper

SmartStart

Mobile Apps Developed in a Variety of Fields Impacting Sustainability and New Age Mobility

19

Mobility App Categories

Advanced Driver Assistance Services

e.g. iOnRoad

Parking Management and Payment Solutions

e.g. Parking Dialogue

LBS Categories – e.g. Taxi Booking

e.g. 1TouchTaxi, TaxiZapp

Crowdsourced Navigation and Traffic Application

e.g. Waze, Inrix, Beat the Traffic

Augmented Reality Applicationse.g. Mobilizy

No clear importance for MirrorLink type interface for

smartphone app access inside car (focus on voice

control)

Short to medium term focus is on music and social networking related app

control through vehicle HMI (Multimodal Mix). Largely US

driven trend

Conclusions and Strategic RecommendationsNorth American market is an ideal launch pad for mobile apps. Bundling apps with cool hardware is critical for OEMs to create a revenue stream.

Q&A!!!!!!!!!!!

20

Tethered connectivity for smartphone apps is a weak model and at the same time users willingness to pay for

dedicated data plan is unclear

Several OEMs have launched branded applications in line with

their connected services package – e.g. Mbrace, BlueLink. This is a

good free convenience add on (GM app downloaded over 400,000

times)

OEM strategies to allow apps access inside the

vehicle ties in with package options which make sure

revenue add-on are healthy (e.g. Ford SYNC applink)

Q&A!!!!!!!!!!!

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

21

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

22

http://twitter.com/frost_sullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

For Additional Information

Katja FeickCorporate Communications

Automotive & Transportation

+49 (0) 69 [email protected]

Cyril Cromier

Sales Director

Europe

+33 1 42 81 22 44

23

N Praveen Chandrasekar

Program Manager, Telematics and Infotainment

Automotive & Transportation

(9144) 6681.4129

Sarwant Singh

Partner

Automotive & Transportation

+44 207 915 7843