Embed Size (px)

Citation preview

IR35

Legislation & Impact

January 2013

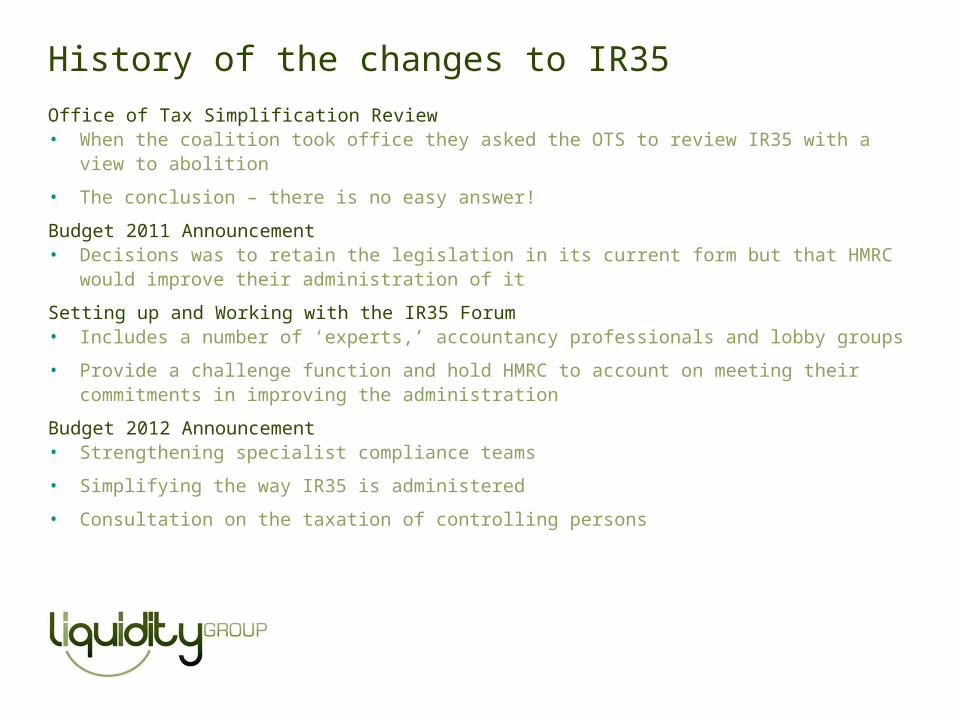

History of the changes to IR35

Office of Tax Simplification Review• When the coalition took office they asked the OTS to review IR35 with a view to

abolition

• The conclusion – there is no easy answer!

Budget 2011 Announcement• Decisions was to retain the legislation in its current form but that HMRC would

improve their administration of it

Setting up and Working with the IR35 Forum• Includes a number of ‘experts,’ accountancy professionals and lobby groups

• Provide a challenge function and hold HMRC to account on meeting their commitments in improving the administration

Budget 2012 Announcement• Strengthening specialist compliance teams

• Simplifying the way IR35 is administered

• Consultation on the taxation of controlling persons

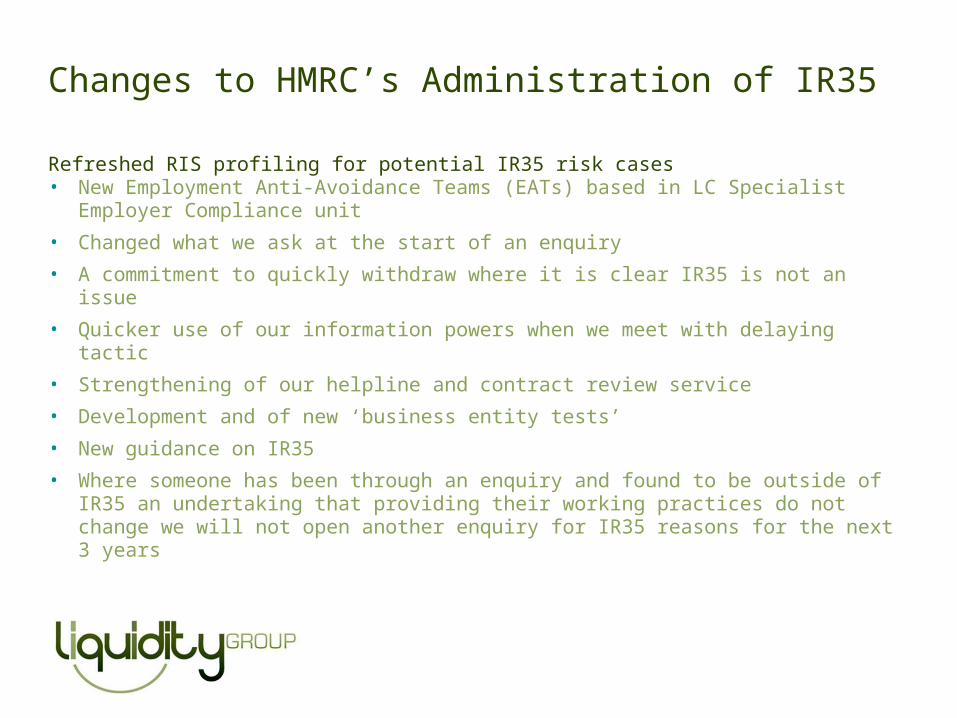

Changes to HMRC’s Administration of IR35

Refreshed RIS profiling for potential IR35 risk cases• New Employment Anti-Avoidance Teams (EATs) based in LC Specialist

Employer Compliance unit

• Changed what we ask at the start of an enquiry

• A commitment to quickly withdraw where it is clear IR35 is not an issue

• Quicker use of our information powers when we meet with delaying tactic

• Strengthening of our helpline and contract review service

• Development and of new ‘business entity tests’

• New guidance on IR35

• Where someone has been through an enquiry and found to be outside of IR35 an undertaking that providing their working practices do not change we will not open another enquiry for IR35 reasons for the next 3 years

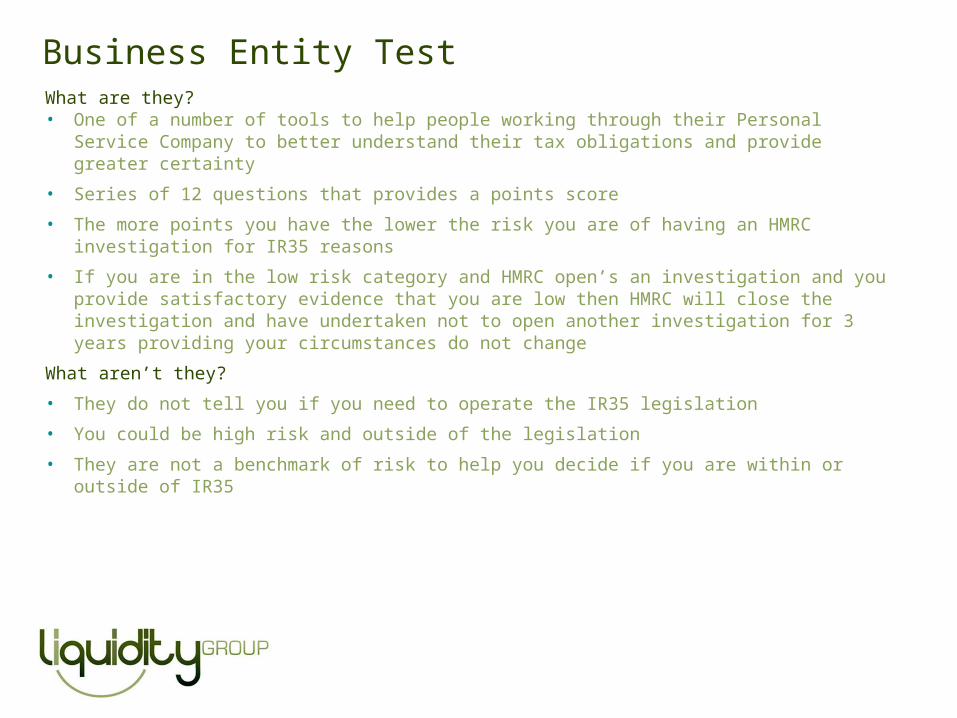

Business Entity TestWhat are they?• One of a number of tools to help people working through their Personal Service

Company to better understand their tax obligations and provide greater certainty

• Series of 12 questions that provides a points score

• The more points you have the lower the risk you are of having an HMRC investigation for IR35 reasons

• If you are in the low risk category and HMRC open’s an investigation and you provide satisfactory evidence that you are low then HMRC will close the investigation and have undertaken not to open another investigation for 3 years providing your circumstances do not change

What aren’t they?

• They do not tell you if you need to operate the IR35 legislation

• You could be high risk and outside of the legislation

• They are not a benchmark of risk to help you decide if you are within or outside of IR35

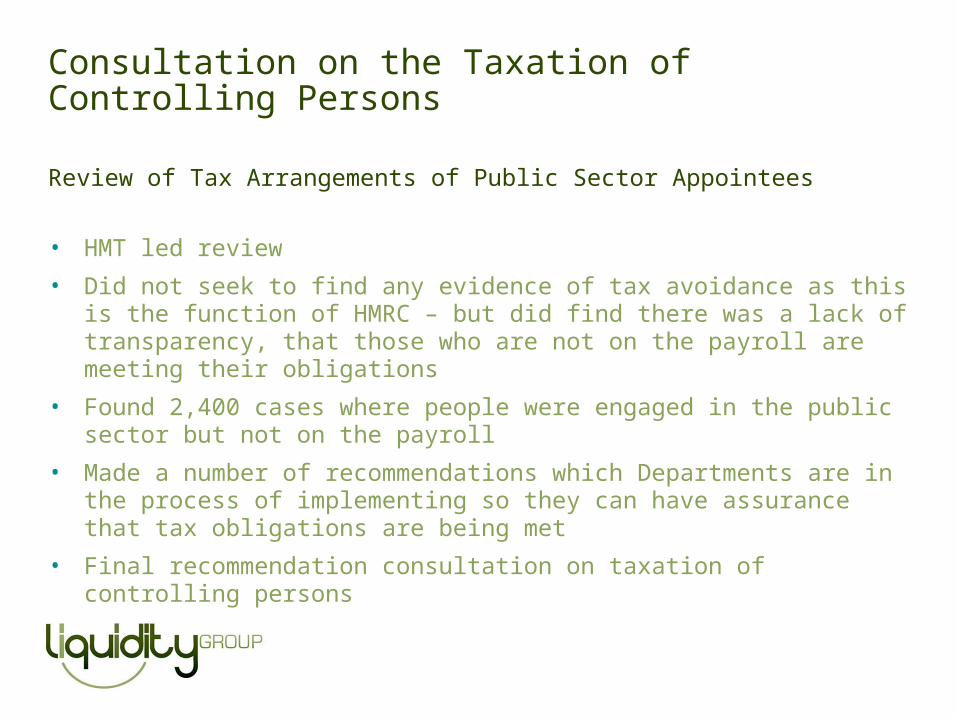

Consultation on the Taxation of Controlling Persons

Review of Tax Arrangements of Public Sector Appointees

• HMT led review

• Did not seek to find any evidence of tax avoidance as this is the function of HMRC – but did find there was a lack of transparency, that those who are not on the payroll are meeting their obligations

• Found 2,400 cases where people were engaged in the public sector but not on the payroll

• Made a number of recommendations which Departments are in the process of implementing so they can have assurance that tax obligations are being met

• Final recommendation consultation on taxation of controlling persons

Changes to IR35

Consultation on the Taxation of Controlling Persons

• Suggestion that all the most senior ‘controlling persons’ should be placed on the payroll of the engaging organisation

• This proposal was consulted on over the Summer with the response document issued alongside the draft legislation in December

Changes to IR35

• Following the consultation the Government decided that they would not legislate for controlling persons at the current time but instead would strengthen the existing IR35 legislation to put beyond doubt that it applies to office holders for tax purposes.

• What these changes mean in reality

Any Questions?

Employment Intermediaries

Presentation

January 2013

What’s in a name

• Many generic labels are given to intermediaries

• Umbrella

• Pay day by pay day model

• None of the names given have been statutorily defined

• They mean different things to different people

• What is important are the facts of the arrangement

• HMRC will always consider the actual facts of the arrangements NOT the model/scheme the company says it is operating

• Always need to consider precisely how the arrangements are structured

Buyer Beware!

HMRC does NOT kite-mark schemes and does NOT provide generic advice that a ‘scheme’ or ‘model’ is compliant

• You will often see:

• We have leading counsel’s opinion

• HMRC has agreed our model is compliant

• HMRC will not pursue you or your end client for arrears should they arise

• Bold statements by the promoters are no guarantee

• HMRC will always determine the facts of each individual case

Dispensations

What are they?• A dispensation dispenses an employer’s statutory obligation to report

taxable expenses to HMRC at the end of the year – where HMRC is satisfied that those expenses qualify for a relief

What aren’t they?

• They are not an HMRC kite mark

• They do not allow an employer to do what they like with expenses once they have attained a dispensation

HMRC action• HMRC will check that an employer is using a dispensation in

accordance with the terms under which it was issued

• If the employer is not acting in accordance with the terms then HMRC may hold the employer responsible for any tax and National Insurance underpaid and may revoke the dispensation

Offshore Intermediaries

What is an offshore intermediary?• I would characterise this a company which is the employer of a UK worker but

who bases themselves outside of the UK and the EEA

They promise….

• Many of these companies claim that there is no liability for them to pay employer National Insurance – if they have no place of business, presence or residence in the UK there is no obligation on the offshore employer to operate PAYE or pay employers National Insurance Contributions

• These companies also claim that no PAYE/ NICs liability will arise on any of the UK companies in the contractual chain

The reality….

• Where the employer is truly offshore HMRC can use the host regulations together with the agency legislation to place this PAYE/NICs charge on the UK employment business

• Alternatively we can use the host regulations to place the charge on the UK end client.

Any Questions?

Thank you

Liquidity GroupBaskerville HouseCentenary SquareBirmingham B1 2ND