Embed Size (px)

Citation preview

Challenges and opportunities: developing

the Territory’s natural gas resources

Malcolm RobertsChief Executive OfficerAustralian Petroleum Production and Exploration Association

APPEA

• The Australian Petroleum Production & Exploration Association represents the upstream oil and gas industry.

• Our 250 member companies produce 98% of Australia’s oil and gas.

www.appea.com.au

2

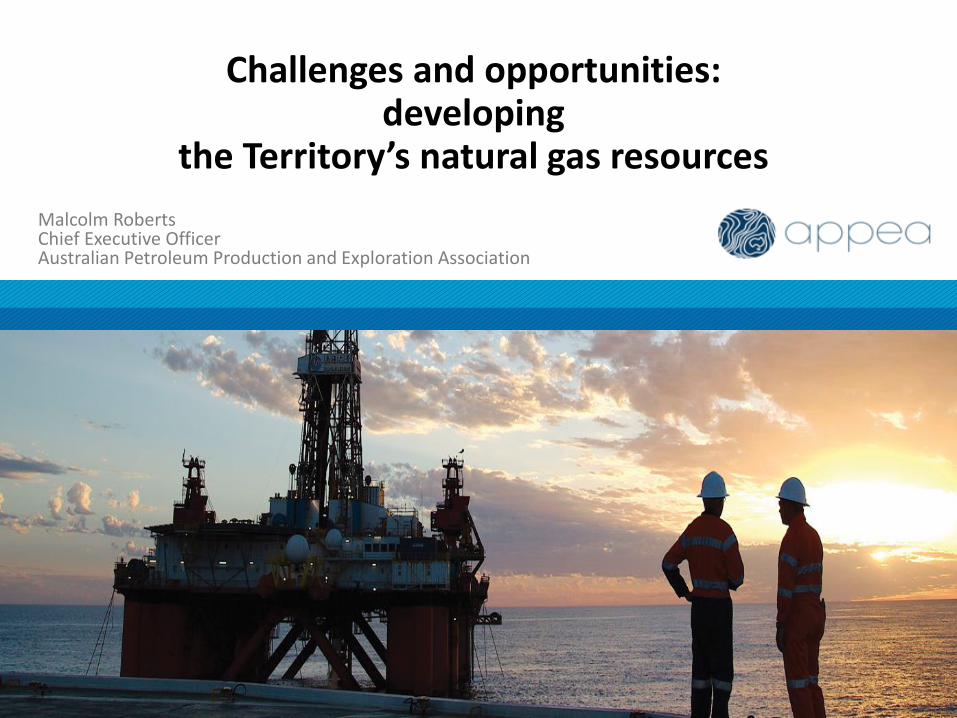

• $30 billion industry.

• Supplies c. two-thirds of our primary energy demand.

• Supports c. 65,000 long-term jobs.

• High wage, high value-add industry.

• $17 billion in exports (forecast $55 billion in 2020).

Australia’s oil and gas industry

3

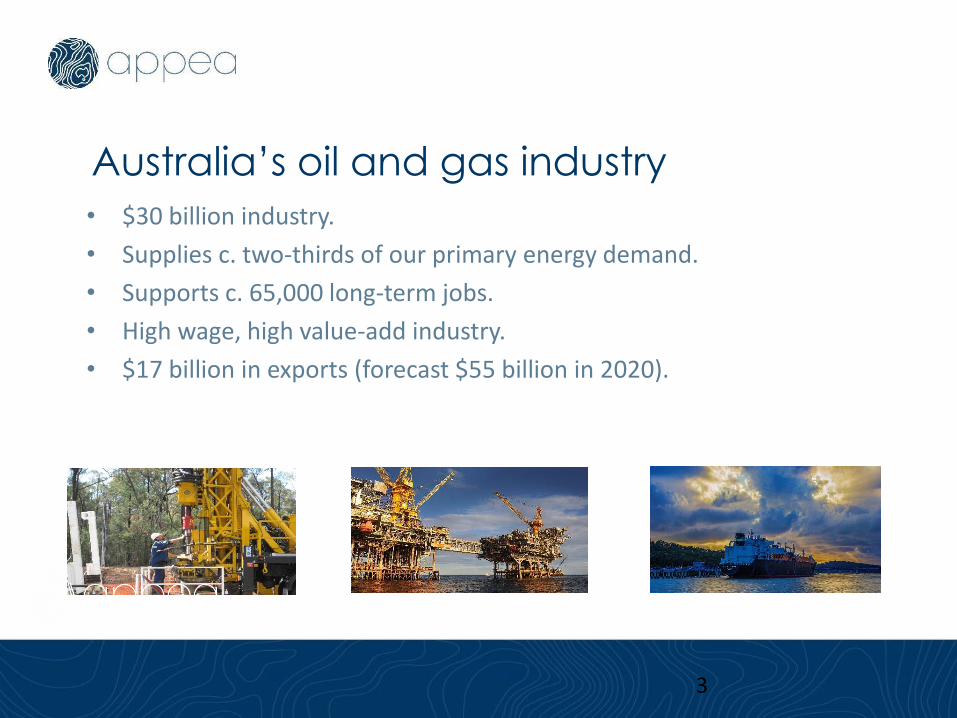

APPEA members in the Territory

• Domestic gas production (Eni, Central, Santos)

• Darwin LNG (ConocoPhillips, Eni, Santos, Inpex, Tokyo EP)

$40bn

• Ichthys LNG (Inpex)

• Offshore exploration & development (MEO, Eni, PTTEP, Woodside, Beach, Santos, Origin, ConocoPhillips, Shell)

• Onshore exploration & development (Central, Origin, Pangaea, Santos, Beach, Armour, Tri-Star, Tamboran)

4

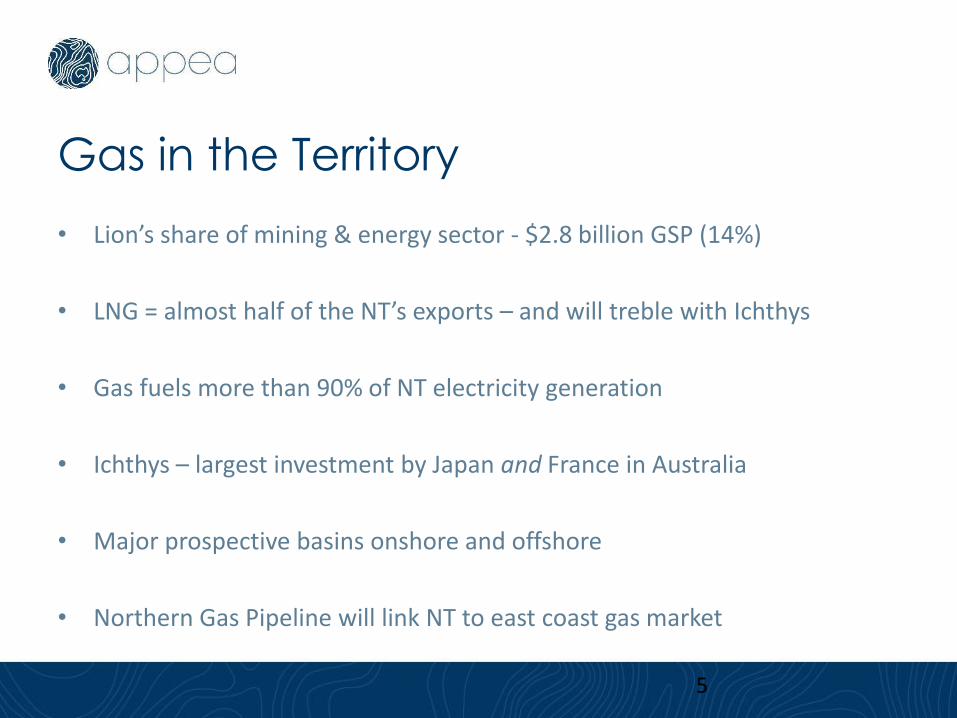

Gas in the Territory

• Lion’s share of mining & energy sector - $2.8 billion GSP (14%)

• LNG = almost half of the NT’s exports – and will treble with Ichthys

• Gas fuels more than 90% of NT electricity generation

• Ichthys – largest investment by Japan and France in Australia

• Major prospective basins onshore and offshore

• Northern Gas Pipeline will link NT to east coast gas market

5

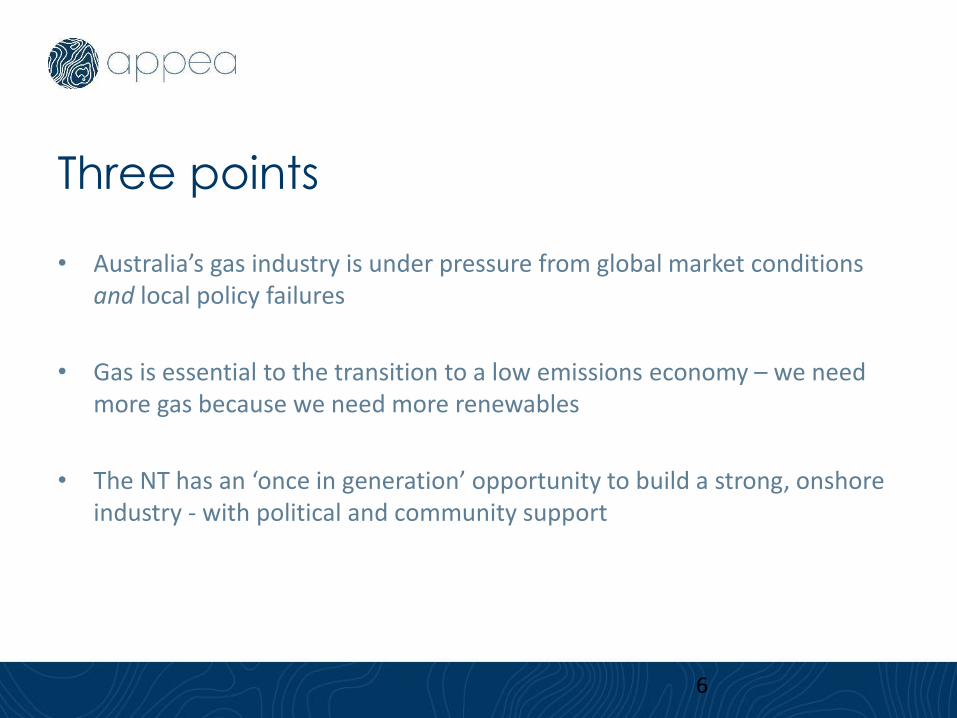

Three points

• Australia’s gas industry is under pressure from global market conditions and local policy failures

• Gas is essential to the transition to a low emissions economy – we need more gas because we need more renewables

• The NT has an ‘once in generation’ opportunity to build a strong, onshore industry - with political and community support

6

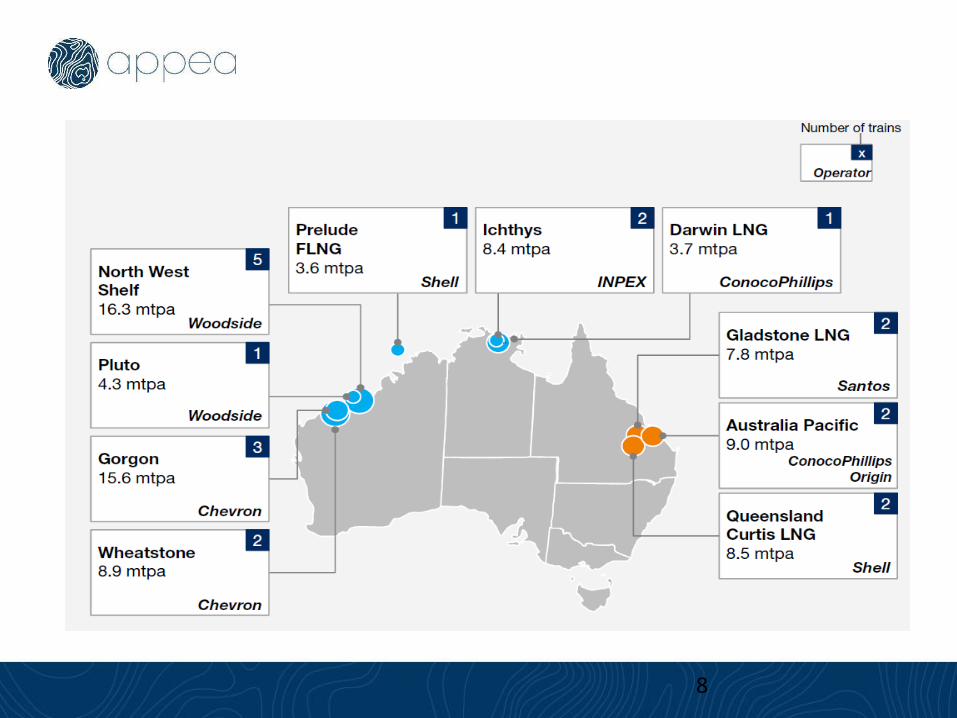

Best of times

• Australia poised to become the world’s leading LNG exporter

– exports worth $16.6 billion (2015-16)

– produced 37.5 MT (2015-16), forecast to rise to 86 MT

• New production

– All six Qld trains will be producing by end of 2016

– Gorgon’s first cargo March 2016

– Wheatstone first cargomid-2017

– Ichthys late 2017

– Prelude 2018+

7

8

Challenging times

• Australia’s expansion coincides with global glut and soft demand

• Major buyers over-contracted – demand flat or lower in key markets

• New supply entering market

– first US shipment to China in March

• Inevitable result depressed prices

9

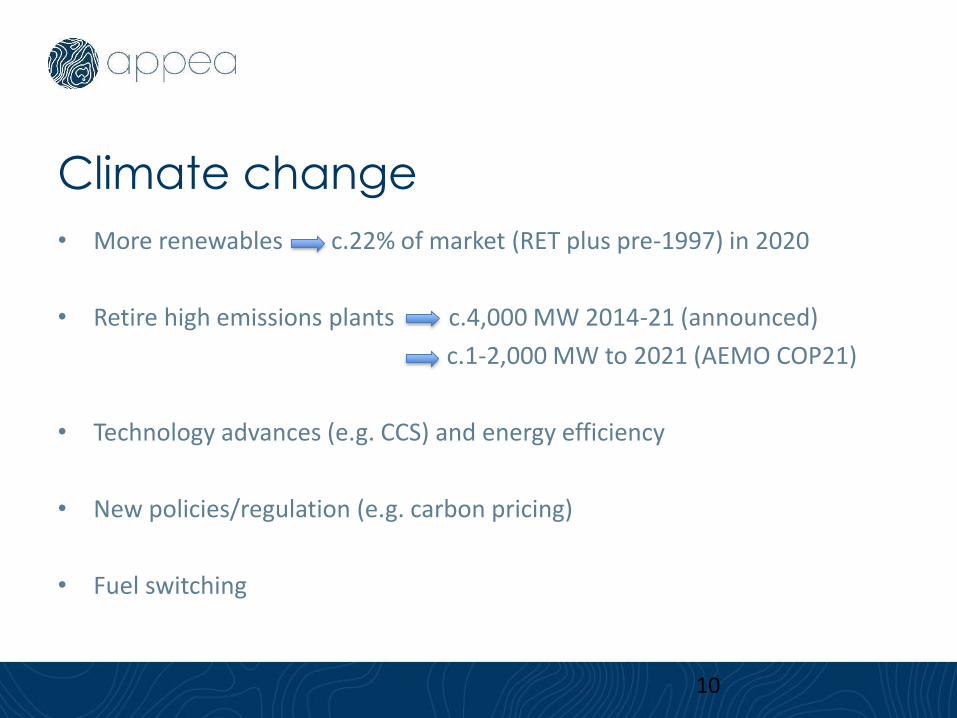

Climate change

• More renewables c.22% of market (RET plus pre-1997) in 2020

• Retire high emissions plants c.4,000 MW 2014-21 (announced)

c.1-2,000 MW to 2021 (AEMO COP21)

• Technology advances (e.g. CCS) and energy efficiency

• New policies/regulation (e.g. carbon pricing)

• Fuel switching

10

The zero sum fallacy

11

• Gas complements as well as competes with renewables

• Gas-fired generation only technology to combine reliability with flexibility

– SA and Tasmania return to service of retired gas-fired plant

• Fuel switching is a major abatement opportunity NOW

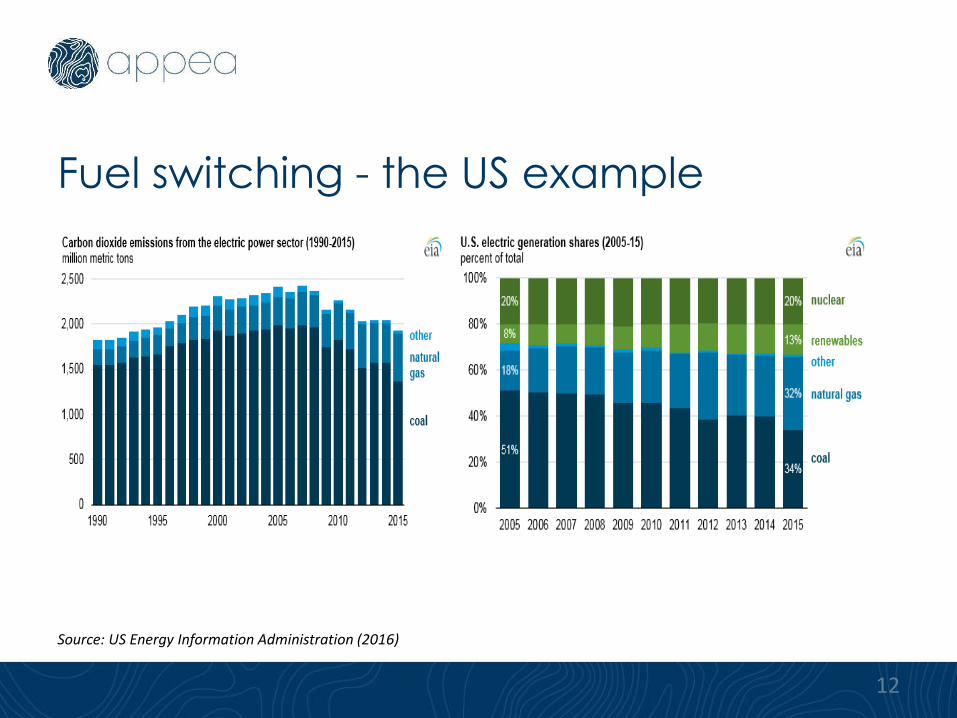

Fuel switching - the US example

12

Source: US Energy Information Administration (2016)

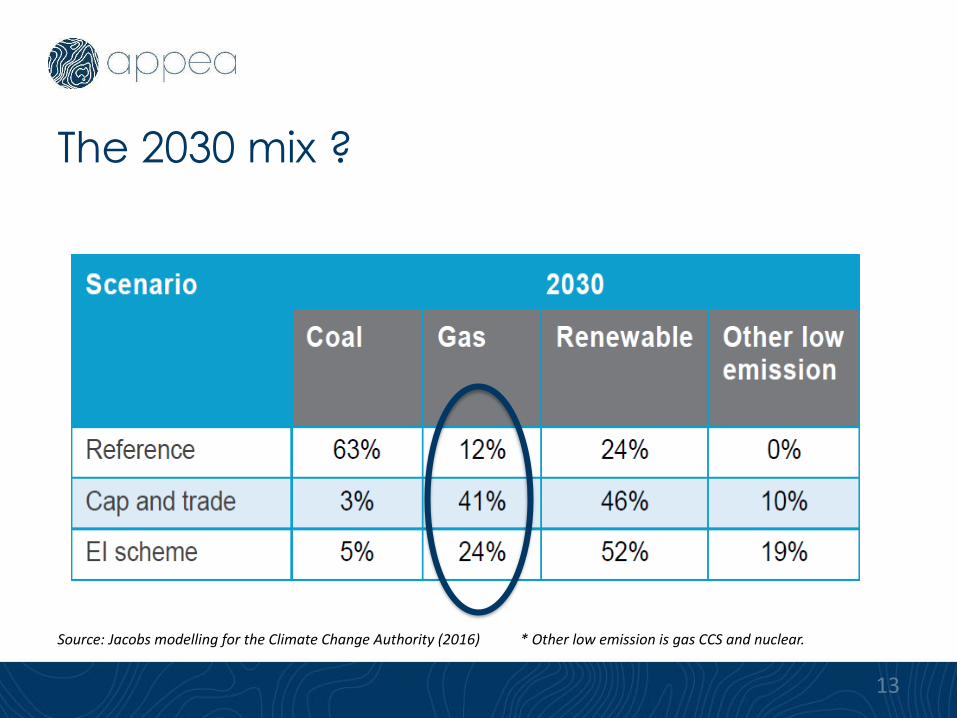

The 2030 mix ?

13

Source: Jacobs modelling for the Climate Change Authority (2016) * Other low emission is gas CCS and nuclear.

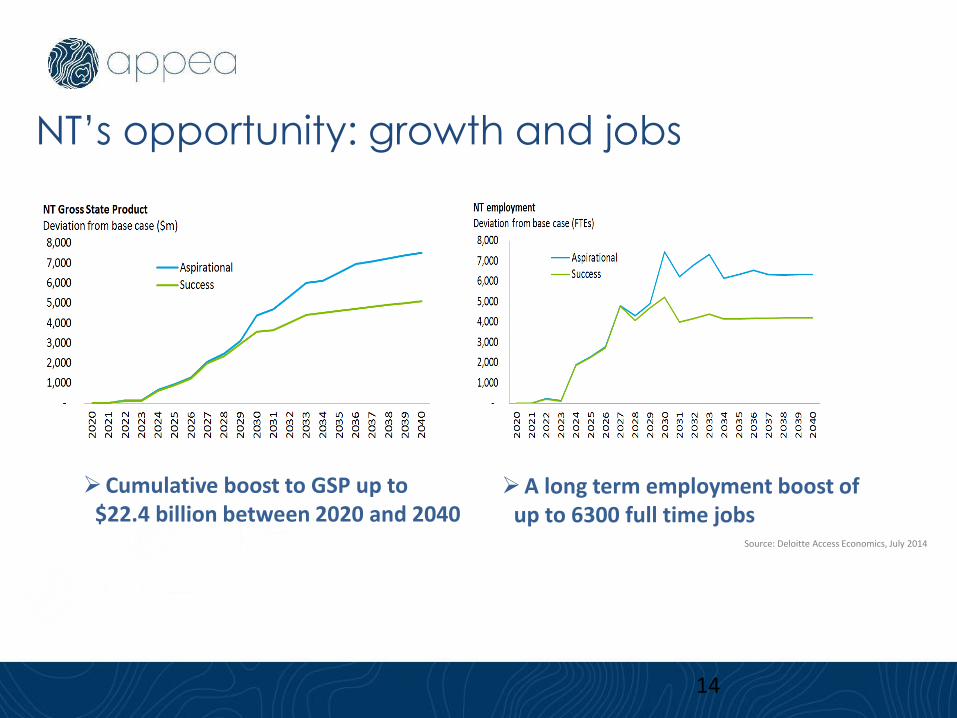

NT’s opportunity: growth and jobs

Cumulative boost to GSP up to$22.4 billion between 2020 and 2040

A long term employment boost of up to 6300 full time jobs

Source: Deloitte Access Economics, July 2014

14

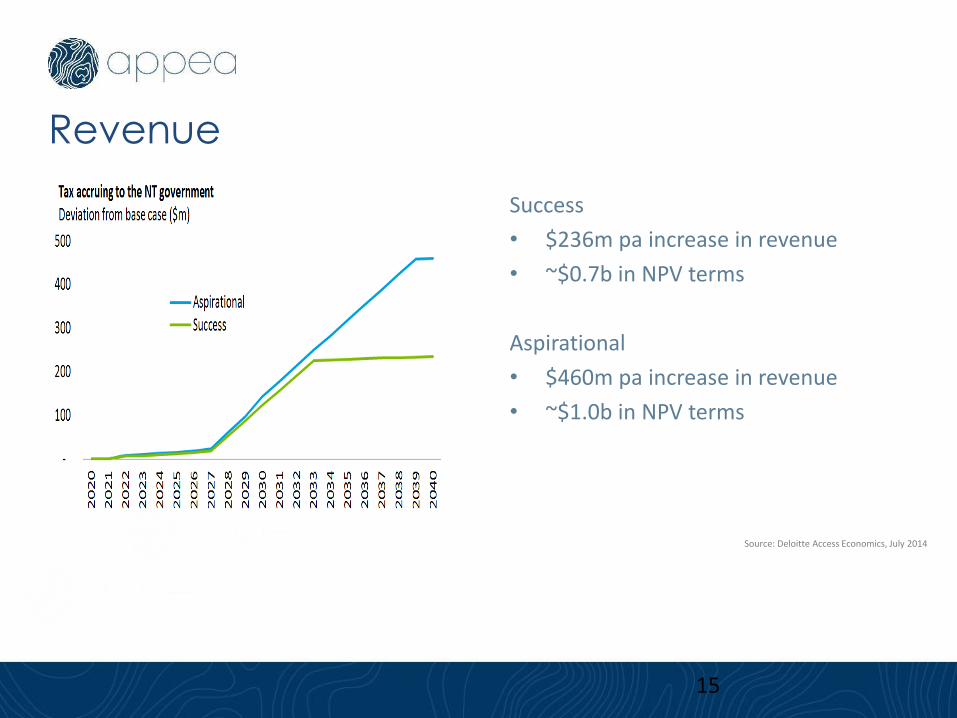

Success

• $236m pa increase in revenue

• ~$0.7b in NPV terms

Aspirational

• $460m pa increase in revenue

• ~$1.0b in NPV terms

Revenue

Source: Deloitte Access Economics, July 2014

15

Fear sells

• Fear campaigns don’t have to be accurate or honest to be effective

• Industry must always be accountable for its statements and its actions

• Industry alone cannot secure community confidence

– independent science vital to inform debate

– political support for an honest debate

– effective regulation which manages risk and promotes co-existence

16

The path forward

17

Early communication and community engagement

Treating everyone with respect Committing to our words with actions Understanding the impacts of our activities

on agriculture Delivering lasting benefits and

opportunities to the wider community Protecting valuable water resources and

long-term land use