Embed Size (px)

Citation preview

Economy / Internet Trends

December 19, 2008

[email protected] / [email protected]

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision. Customers of Morgan Stanley inthe US can receive independent, third-party research on companies covered in Morgan Stanley Research, at no cost to them, where such research is available. Customers can access this independent research at www.morganstanley.com/equityresearch or can call 1-800-624-2063 to request a copy of this research.For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

2

Outline

• Economy

1. Recession – a long time coming, how long will it last?

2. Advertising Spending – closely tied to GDP growth

• Technology / Internet

1. Digital Consumer – Undermonetized social networks / video / VoIP driving powerful usage growth

2. Mobile – Innovation in wireless products / services accelerating

3. Emerging Markets – Pacing next wave of technology adoption

4. Cloud Computing – Access / storage need / virtualization driving change

• Closing Thoughts

1. Companies with cogent business models that provide consumer value should survive / thrive – consumers need value more than they have needed it in a long time…

Economy

1) Recession – a long time coming, how long will it last?Ten years of inflated growth to be followed by ____?

Hope for 1 tough year but plan for 5?

3

10 Years Ago –I Don’t Want to Miss a Thing, Aerosmith = Billboard Top 5 Song of 1998

Source: YouTube. 4

58%

60%

62%

64%

66%

68%

70%

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

U.S

. Hom

e O

wne

rshi

p R

ate

0%

4%

8%

12%

16%

20%

U.S

. Int

eres

t Rat

e &

Per

sona

l Sav

ings

Rat

e

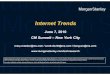

U.S. Home Ownership RateU.S. Interest Rate

January 1993: HUD began promoting broader home ownership. US home ownership = 62MM

June 2004: US home ownership = 73MM

U.S. Home Ownership Rate 30-year (1965-1995) Trendline

U.S. Personal Savings Rate

USA Homeownership Rates vs. Interest Rates vs. Pers onal Savings Rates, 1965-2008

Roots of Economic Challenge?10+ Years of Rising Home Ownership + Declining Interest / Savings Rates

Note: HUD is Department of Housing & Urban Development. Interest rate is the overnight federal funds rate.

Source: Federal Reserve, DOC Bureau of Economic Analysis (BEA), Morgan Stanley Research.5

Market & Regulatory Pressure Made Home Buying More Accessible…1998

In addition to a buoyant economy, the overall housing industry owes its enduring vigor to innovations in mortgage finance that have helped not only expand homeownership opportunities, but also reduce market volatility. Under market and regulatory pressure to makehome buying more accessible to low-income and minority households, financial institutions have revised their underwriting practices to make lending standards more flexible. In the process, they have developed several new products to enable more income-constrained and cash-strapped borrowers at the margin to qualify for mortgage loans.

- 1998 State of the Nation’s Housing Report

6Note: Quoted in Gary Gorton’s NBER Working Paper Series “The Panic of 2007” (Working Paper 14358), p.5.

Source: Harvard University, Joint Center for Housing Studies, 1998.

10 Years of Rising Home Prices – Up ~2x

Note: Real home prices & building costs are adjusted for inflation; Source: Robert Shiller.

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1965 1968 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007

% C

hang

e F

rom

196

5 Le

vel

U.S. Real Home Price Index U.S. Real Building Cost Index

USA Real Home Price & Building Cost Indexes, % Chan ge 1965 - 2007

7

Systemic Leverage Helped Pace ‘Easy Money’Debt at Record Level + Sharp Ramp Up in Foreign Ownership of US Treasuries

Note: Foreign ownership of US treasuries data N/A before 1965.Source: Federal Reserve Board, Ned Davis Research, Bridgewater, Morgan Stanley Research. 8

0%

10%

20%

30%

40%

50%

60%

70%

For

eign

Ow

ners

hip

of U

.S. T

reas

urie

s,%

of T

otal

Mar

ket C

ap

100%

150%

200%

250%

300%

350%

400%

1920 1928 1936 1944 1952 1960 1968 1976 1984 1992 2000 2008

Tot

al D

ebt a

s %

of G

DP

U.S. Total Debt, % of GDP

Foreign Ownership of US Treasuries, % of Total Mark et Capitalization

1931: 2.7x GDP

2008: 3.6x GDPU.S. Total Credit Market Debt as % of GDP& Foreign Ownership % of U.S. Treasuries,

1920 - 2008

Mortgage PoolsMortgage Pools9%9%

ABS IssuersABS Issuers8%8%

Other FinancialOther Financial15%15%

HouseholdHousehold27%27%

CorporateCorporate14%14%

GovernmentGovernment15%15%

OtherOther11%11%

USA Debt Mix Shift –Mortgages / ABS / Financials Up

Note: Other financial debt include those issued by commercial banks, insurance companies, broker-dealers, Government Sponsored Enterprises (GSEs), REITs, Savings & Loans institutions, credit unions, and finance companies, etc. Debt amounts

are nominal, ABS is Asset Backed Security. 2008 data as of CQ3. Source: Federal Reserve, Morgan Stanley Research.9

2008U.S. Total Debt: $52T

Total Financial Debt: $17T

1984U.S. Total Debt: $7T

Total Financial Debt: $1T

Mortgage Pools Mortgage Pools –– 4%4%

ABS Issuers ABS Issuers –– 0%0%Other Other –– 15%15%

Other FinancialOther Financial10%10%

CorporateCorporate19%19%

HouseholdHousehold26%26%GovernmentGovernment

25%25%

USA Mortgage Delinquency @ Record High 6.99%

0%

5%

10%

15%

20%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Del

inqu

ency

Rat

es (

%)

All U.S. Mortgages Prime Mortgages Subprime Mortgages

USA Mortgage Delinquency Rates, CQ1:98 – CQ3:08

Note: National delinquency rate of 6.99% in CQ3:08 is the highest since CQ1:1972, when data first became available;Average national mortgage delinquency rate from 1972-2007 is 4.70%; Source: Mortgage Bankers Association. 10

-0.5% Q/Q USA GDP Growth in CQ3 / Consumer Spending Fell 3.7% Biggest Q/Q Decline Since 1980 – October < September < August < July

U.S. Real GDP vs. Real Personal Consumption Expendi tures (PCE)Q/Q % Change, 2005-2008

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

Q/Q

Gro

wth

Rat

es

U.S. Real GDP Q/Q Growth U.S. Real PCE Q/Q Growth

CQ1:05 CQ3:05 CQ1:06 CQ3:06 CQ1:07 CQ3:07 CQ1:08 CQ3:08

Note, Real GDP and real PCE are inflation- and seasonally adjusted. CQ3:08 data is preliminary, may differ from final reported #s.

Source: BEA, Morgan Stanley Research.11

Discouraging Monthly Trends –Amplified by Internet-Driven Information Transparency?

0%

-2%

-10%

6%

-1%-3%

-7%

-11%

-14%

-20%

-28%-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

Com

para

ble

Sto

re S

ales

Y/Y

% C

hang

e

Abercrombie & Fitch Same-Store SalesY/Y % Change, 1/08 – 11/08

Note: Same-store sales are sales in stores open more than one year. Source: Abercrombie & Fitch, British Retail Consortium. 12

3%2%

-2% -1%

2%

0% -1% -1% -1%-2% -3%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

Com

para

ble

Sto

re S

ales

Y/Y

% C

hang

e

UK Retail Same-Store SalesY/Y % Change, 1/08 – 11/08

13

Global GDP Growth Forecasts =Downward / Decelerating Bias

Country / Region 2006 2007 2008E 2009E 2008E 2009E

USA 2.8% 2.0% 1.4% -0.7% -0.1% -0.8%

Euro zone 2.8 2.6 1.2 -0.5 -0.1 -0.7

UK 2.8 3.0 0.8 -1.3 -0.2 -1.2

China 11.6 11.9 9.7 8.5 -0.1 -0.8

India 9.8 9.3 7.8 6.3 -0.1 -0.6

Russia 7.4 8.1 6.8 3.5 -0.2 -2.0

Brazil 3.8 5.4 5.2 3.0 -- -0.5

Developed Markets(1) 3.0 2.6 1.4 -0.3 -0.1 -0.8

Emerging Markets(2) 7.9 8.0 6.6 5.1 -0.3 -1.0

World 5.1 5.0 3.7 2.2 -0.2 -0.8

Note: (1) IMF equivalent of “advanced economies”; (2) IMF equivalent of “emerging and developing economies”; Source: International Monetary Fund (IMF) World Economic Outlook (WEO) database, 11/08. Morgan Stanley Research.

IMF Forecasts, 11/08Difference from

10/08 IMF Forecasts

USA Manufacturing Contracting Rapidly –Lowest Level (and Declining) Since 1982 for PMI Index

U.S. PMI (Purchasing Mangers Index), 1/48 – 11/08

Note: PMI is a composite index based on five major indicators including: new orders, inventory levels, production, supplier deliveries, and employment environment. A PMI index over 50 indicates that manufacturing is expanding while anything below 50 means that

the industry is contracting. Source: Institute for Supply Management (ISM), Morgan Stanley Research. 14

20

30

40

50

60

70

80

1948

1951

1954

1957

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

ISM

PM

I Ind

ex (

%)

May 1982PMI=35.5

Feb 1991PMI=39.4 Nov 2008

PMI=36.2

Oct 2001PMI=40.8

PMI > 50=

Expansion

PMI < 50=

Contraction

60-year Average= 52.8

Unemployment Rising Rapidly But 110 Basis Points Below Previous PeaksMore Often Than Not, Peak Unemployment = Good Time to Invest

Note: Unemployment rates from 1928–1943 are annual estimates from John Dunlop and Walter Galenson’s Labor in the Twentieth Century (1978); data unavailable between 1943-1948; Post 1948 unemployment data from BLS, peaks are: 9/49 - 7.9%; 9/54 - 6.1%; 7/58 - 7.5%; 5/61 – 7.1%; 8/71 - 6.1%; 5/75 - 9.0%; 11/82 - 10.8%; 6/92 - 7.8%; 7/03 - 6.3%.

Source: FactSet; Bureau of Labor Statistics. Morgan Stanley Research.15

1

10

100

1000

10000

1928 1933 1938 1943 1948 1953 1958 1963 1968 1973 1978 1983 1988 1993 1998 2003 2008

S&

P 5

00 In

dex

Val

ue (

Log

Sca

le)

0%

5%

10%

15%

20%

25%

30%

Une

mpl

oym

ent R

ate

S&P 500 Index Price Unemployment Rate

S&P 500 Index & U.S. Unemployment Rates, 1928 - 2008

Recessions Unemployment Peak

Note: all indices start at a value of 100 on 12/16/05; data as of 12/18/08; Source: FactSet.

Stock Market = Leading Indicator of Economic Growth Russia off 73% vs. 12-Month Peak, Oil -71% / China -63% / India -52% / Japan -45% / S&P500 -41%

16

0

100

200

300

400

500

600

12/05 3/06 6/06 9/06 12/06 3/07 6/07 9/07 12/07 3/08 6/08 9/08 12/08

Inde

xed

Val

ue (

base

= 1

00)

S&P 500 NASDAQ Composite IndexChina Shanghai SE Composite India SENSEXRussia RTS Light Crude Oil - Continuous ContractGold - Continuous Contract Japan Nikkei 225

2006 20082007

Note: (1) % Change from S&P 500 peak on 10/9/07 to 12/18/08; (2) S&P 500 total market cap and % change, different from S&P 500 index price & % change.

Source: Bloomberg, Morgan Stanley Research.

S&P500 –Key Spending Sectors Have Taken Big Hits

17

Total MktCap ($B) 2008 Peak to

S&P Sector 12/18/08 2006 2007 YTD Current (1) Market Cap Leaders

Financials 1,061 16% -20% -53% -62% JPMorgan, Wells Fargo

Consumer Discretionary 686 9 -18 -38 -49 McDonald's, Walt Disney

Materials 242 10 14 -44 -47 Monsanto, DuPont

Industrials 846 8 7 -42 -47 GE, United Technologies

Information Technology 1,242 11 12 -44 -46 Microsoft, IBM

Telecom Services 293 32 -12 -36 -42 AT&T, Verizon

Energy 1,026 14 36 -39 -36 Exxon, Chevron

Utilities 317 17 6 -31 -34 Exelon, Southern

Health Care 1,153 1 1 -26 -29 Johnson & Johnson, Pfizer

Consumer Staples 1,121 8 10 -21 -20 Wal-Mart, Procter & Gamble

S&P 500 Total (2) 7,987 11% 1% -39% -43%

% Change

2007

2005

1994

1993

1992

1987

1984

1978

1970

1960 2006

1956 2004

1948 1988

1947 1986

1923 1979

1916 1972

1912 1971

2000 1911 1968

1990 1906 1965

1981 1902 1964

1977 1899 1959

1969 1896 1952

1962 1895 1949

1953 1894 1944 2003

1946 1891 1926 1999

1940 1889 1921 1998

1939 1887 1919 1996

1934 1881 1918 1983

1932 1877 1905 1982

2001 1929 1875 1904 1976

1973 1914 1874 1898 1967

1966 1913 1872 1897 1963 1997

1957 1903 1871 1892 1961 1995

1941 1890 1870 1886 1951 1991

1920 1887 1869 1878 1943 1989

1917 1883 1868 1864 1942 1985

1910 1882 1867 1858 1925 1980

1893 1876 1866 1855 1924 1975

1884 1861 1865 1850 1922 1955

1873 1860 1859 1849 1915 1950

2002 1854 1853 1856 1848 1909 1945

1974 1841 1851 1844 1847 1901 1938 1958 1954

1930 1837 1845 1842 1838 1900 1936 1935 1933

1907 1831 1835 1840 1834 1880 1927 1928 1885

1857 1828 1833 1836 1832 1852 1908 1863 1879

1931 1937 1939 1825 1827 1826 1829 1846 1830 1843 1862

-50 to -40% -40 to -30% -30 to -20% -20 to -10% -10 to 0% 0 to 10% 10 to 20% 20 to 30% 30 to 40% 40 to 50% 50 to 60%

2008 YTD-40%

S&P500 Down 40-50% 2x in 183 Year History – 2008 / 1931Bad Years Often Follow Good Years

Note: S&P 500 2008 YTD performance as of 12/18/2008, S&P 500 historical info from 1825 to 2007.Source: Value Square Asset Management, Yale University.

18

GSEs / Washington

Plan

Lehman Bankruptcy

AIG Nationalized

MS / MUFG Investment

JPM Acquires

WaMu

Wells Fargo Acquires Wachovia

Fortis Nationalized

Leading Banks Enter

Preferred Stock

Purchase Program

BofA Acquires ML

GS / Berkshire

Investment$700Bn TARP

B&B Nationalized

Santander / Sovereign

UK Bank Bail Out

September 7 September 14 September 16 September 22 September 25 October 3September 29 October 14

EuropeUnited States

(23%)

5 Weeks in History – Financial Services Restructuring(~$3T in US Aggregate Sector Market Value 1/1/07…now ~$1T)

Dow Jones Industrial Average, 9/8/08 – 10/14/08

Note: Aggregate sector market value is the combined market cap for all companies in the S&P500 financials index,$2.9T as of 1/1/08, $1.2T as of 12/8/08.

Source: Morgan Stanley IBD; Bloomberg.19

8,400

8,600

8,800

9,000

9,200

9,400

9,600

9,800

10,000

10,200

10,400

10,600

10,800

11,000

11,200

11,400

11,600

Dow

Jon

es In

dust

rial A

vera

ge

Consumer Wealth Destruction = ~15% –56%+ of USA Household Assets in Real Estate + Stocks

Real EstateReal Estate38%38%

Equities +Equities +Mutual FundsMutual Funds

18%18%

PensionPensionReservesReserves

22%22%

DepositsDeposits12%12%

Credit MarketCredit MarketInstrumentsInstruments

7%7% OthersOthers3%3%

USA Household Asset Breakdown, C2007A

-40%

-30%

-20%

-10%

0%

10%

CQ1:07 CQ3:07 CQ1:08 CQ3:08

% C

hang

e fr

om C

Q1:

07

S&P/Case-Shiller Home Price IndexS&P 500 Index

Real Estate & Equities Market Performances,% Change from CQ1:07

Note: Median household income in 2007 was $50,233, per U.S. Census Bureau. 56% accounts only real estate + equities / mutual funds; many pension funds also invest in the U.S. equities market, thus actual exposure to these asset classes will likely be higher. Wealth destruction of approx. 15% is calculated

by multiplying the asset allocation of real estate & equities / mutual funds with respective market indices’ declines from CQ1:07 –2008 YTD. Asset allocation % is 2007 average. Source: Federal Reserve; Standard & Poor's; Morgan Stanley Research. 20

Extraordinary Market Volatility = Treacherous Investment EnvironmentGood News = Volatility Has Begun to Decline

0

10

20

30

40

50

60

70

80

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

VIX

Inde

x V

alue

(%

)

Chicago Board Options Exchange (CBOE) Volatility In dex, 1990 - 2008

Note: Data N/A before 1990. VIX is a measure of implied volatility of S&P 500 index options.Source: Morgan Stanley IBD; Bloomberg. 21

Economy

2) Advertising Spending –closely tied to GDP growth…challenges for Internet but likely

not as draconian as 2000-2002?

22

Retail Sales Growth Rates Slowing

0%

10%

20%

30%

40%

CQ3:01 CQ3:02 CQ3:03 CQ3:04 CQ3:05 CQ3:06 CQ3:07 CQ3:08

Y/Y

Gro

wth

US Adjusted Retail E-Commerce Sales US Total Retail Sales

Note: E-Commerce adjusted for eBay by adding eBay US gross merchandise volume and subtracting eBay US transaction revenue; Source: US Dept. of Commerce (CQ3:08), Morgan Stanley Research.

Retail Sales vs. Adjusted E-Commerce SalesY/Y Growth, CQ3:01 – CQ3:08

23

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08

Y/Y

Gro

wth

Rat

e

Overall Cable+Broadcast TV MagazinesNewspapers Internet* OutdoorRadio

Advertising Growth Rates Slowing

U.S. Advertising Spending by Medium, Y/Y % Change

*Note: Internet is adjusted to include search ad spending - TNS excludes search revenue from Internet ad spending, thus unadjusted data may under-report online ad spending / growth. Source: TNS, IAB, Morgan Stanley Research. 24

-10%

-5%

0%

5%

10%

15%

20%19

86

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

U.S

. Ad

Spe

nd v

s. G

DP

, Y/Y

Gro

wth

U.S. Real GDP Y/Y Growth U.S. Ad Spend Y/Y Growth

U.S. Advertising Spending Y/Y Growth vs. Real GDP Y /Y Growth, 1986 – 2007

1991 Ad Growth = -2%

Median Y/Y Ad Spend Growth Rate = 5%

2001 Ad Growth = -12%

Source: Zenith Optimedia, IMF, Morgan Stanley Research. 25

Advertising Spending & GDP Growth =High Correlation of 81%

Simple Regression Analysis:1) Ad spend growth 3x sensitivity of real GDP growth

2) If GDP flat in 2009E, ad spend could decline ~4% Y/Y

Note: R2 of 0.655 indicates that correlation is not perfect (n=22), and correlation does not equal causation.Source: Zenith Optimedia, IMF, Morgan Stanley Research. 26

U.S. Advertising Spending vs. Real GDP1986 – 2007

y = 3.0263x – 0.0394R2 = 0.6553

y – ad spend growthx – real GDP growth

-10%

-5%

0%

5%

10%

15%

20%

-1% 0% 1% 2% 3% 4% 5%

Real GDP Y/Y Growth

Ad

Spe

nd Y

/Y G

row

th

U.S. Ad Spend vs. Real GDP Y/Y GrowthLinear Regression Line (y = 3.0263x - 0.0394 R^2 = 0.6553)

If real GDP Ad spendY/Y growth Y/Y growth

is… could be…

5% 11%4 83 52 21 -10 -4

-1 -7-2 -10-3 -13-4 -16-5 -19

$267$907

$1,921

$4,621

$8,225$7,134

$6,009

$7,267

$9,475

$12,542

$16,879

$21,206

$0

$5,000

$10,000

$15,000

$20,000

$25,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

U.S

. Onl

ine

Ad

Spe

ndin

g ($

MM

)

-50%

0%

50%

100%

150%

200%

250%

Y/Y

Gro

wth

Rat

e

U.S. Internet Ad Spending Y/Y Growth Rate

Source: IAB, Morgan Stanley Research. 27

U.S. Online Advertising Spending & Y/Y Growth Rates , 1996-2007

Online Ad Spending Bad News =From 2000 to 2002, USA Spending Fell 27%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

3/96 3/97 3/98 3/99 3/00 3/01 3/02 3/03 3/04 3/05 3/06 3/07 3/08

U.S

. Onl

ine

Spe

ndin

g &

Sea

rch

Rev

enue

($M

M)

-50%

0%

50%

100%

150%

200%

250%

300%

Tot

al U

.S. O

nlin

e S

pend

Y/Y

Gro

wth

U.S. Online Ad Spending Spending on SearchY/Y Growth Online Ad Spend Polynomial Trendline

Online Ad Spending Good News = Now, Less Ad ‘Over Spending’ vs.Trend Line However, Q/Q Pattern Looks a Bit Like Early 2001

U.S. Online Advertising Spending & Y/Y Growth Rates , CQ1:96-CQ3:08

Note: CQ3:08 search spending data not available. Source: IAB, Morgan Stanley Research. 28

Intel – Technology Spending ProxyRevised CQ4E Guidance Implies -16% Y/Y, Worst Since CQ4:01

-12% Q/Q in Seasonally Strong CQ4, Worst in History?

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000C

Q1:

97

CQ

3:97

CQ

1:98

CQ

3:98

CQ

1:99

CQ

3:99

CQ

1:00

CQ

3:00

CQ

1:01

CQ

3:01

CQ

1:02

CQ

3:02

CQ

1:03

CQ

3:03

CQ

1:04

CQ

3:04

CQ

1:05

CQ

3:05

CQ

1:06

CQ

3:06

CQ

1:07

CQ

3:07

CQ

1:08

CQ

3:08

Rev

enue

($M

M)

-30%

-20%

-10%

0%

10%

20%

30%

40%

Y/Y

Gro

wth

Revenue Y/Y Growth

CQ

4:08

E

Note: CQ4:08E based on the midpoint of company’s revised guidance on 11/12/08. Source: Intel, FactSet. 29

Average Y/Y Growth = 6%

Intel Revenue & Y/Y Growth Rate, CQ1:97 – CQ4:08E

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,0001Q

87

1Q88

1Q89

1Q90

1Q91

1Q92

1Q93

1Q94

1Q95

1Q96

1Q97

1Q98

1Q99

1Q00

1Q01

1Q02

1Q03

1Q04

1Q05

1Q06

1Q07

1Q08

Rev

enue

($M

M)

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Y/Y

Gro

wth

Revenue Y/Y Growth

20-yr Average Y/Y Growth =

7%

Note: S&P500 has 84 financial services companies as of 12/9/08. CQ3:08E are FactSet mean estimates. Source: FactSet.

Financial Services – Revenue Back to 10 Year Ago LevelsFor Now, CQ3E of -13% Y/Y Well Below +7% 20-yr Average

Revenue & Y/Y Growth Rate for S&P500 Financial Serv ices Companies

30

31

USA Corporate Sales Quickly Falling Behind Forecasts

0%

10%

20%

30%

40%

50%

60%

CQ1:01 CQ4:01 CQ3:02 CQ2:03 CQ1:04 CQ4:04 CQ3:05 CQ2:06 CQ1 :07 CQ4:07 CQ3:08

Above Plan Below Plan

Overall Corporate Sales Survey Results, CQ1:01 – CQ4 :08

How is your company doing with regard to meeting its sales plan revenue objectives for the current quarter? Are you coming in above plan, even, or below plan?

Note: Survey based on responses of 3,029 U.S. respondents. Source: Changewave, 12/5/08

CQ4:0851%

CQ3:0150%

32

Consumer Spending Trending Lower

0%

10%

20%

30%

40%

50%

60%

Jun-06

Aug-06

Nov-06

Jan-07

Mar-07

May-07

Jun-07

Aug-07

Sep-07

Nov-07

Jan-08

Feb-08

Apr-08

May-08

Jul-08

Aug-08

Sep-08

Nov-08

Dec-08

Spending More Spending Less

Overall Consumer Spending Results – 6/06 - 12/08

Would you say your overall spending over the next 90 days will be more than last year, less than last year, or the same as last year?

Note: Survey based on responses of 2,715 U.S. consumers. Source: Changewave, 12/11/08.

12/0860%

Obama Presidency – USA in Need of a Forced Upgrade,There’s No Time Like a Crisis to Make Changes

• Transportation / Infrastructure (~$225B) – Create millions of jobs via single largest new investment in our national infrastructure since creation of federal highway system in 1950s.

• Technology / Internet (~$100B) – Renew America’s information superhighway. It is unacceptable that the United States ranks 15th in the world in broadband adoption. Here, in the country that invented the Internet, every child should have the chance to get online, and they’ll get that chance when I’m President – because that’s how we’ll strengthen America’s competitiveness in the world.

• Manufacturing / Clean Tech (~$100B) – Extend funding to manufacturing innovators; Advance next generation of bio-fuels & infrastructure / accelerate commercialization of plug-in hybrids, etc.

• Hospital / Health Care (~$10B) – Ensure hospitals are connected to each other through Internet / make sure every doctor’s office and hospital is using cutting edge technology and electronic medical records.

• Public / School Buildings (~$70B) – Make public and school buildings more energy-efficient by replacing old heating systems and installing efficient light bulbs / put new computers in classrooms.

Source: Change.gov, WSJ.com. 33

Economic Recovery Policy Proposals

34

1) Digital Consumer –Our bet = At margin, consumers spend more – not less – time on

Internet in difficult times – it’s a cheap / efficient / transparent thrill! Undermonetized social networks / video / VoIP

driving powerful usage growth – opportunity for innovative marketers to capitalize on low CPMs

Technology / Internet

Discretionary Spending –Broadband Internet Among Last Things to Go

7.2 7.2 6.8 6.6 6.6 6.5 6.4 6.2 5.9 5.6 5.54.7

3.9 3.5

0123456789

10

New fu

rnit u

re o

r flo

or co

verin

gsGam

bling

Going o

ut to

rest

aura

nts,

clu bs

or p

ubsElec

tronic

s

Mus

i c, D

VDs, book

s & g

ames

Mak

ing im

prov

emen

ts to

your

hom

e

Health

club

mem

bersh

ip, go

lf or o

ther s

ports

Going

away

on ho

li day

s or w

eeke

nd br

eaks

Prem

ium or

orga

nice

groc

eries

Cloth

ing, a

c cess

ories

or fo

otw

ear

Mob

il e P

hone

Personal

Care, t

oileter

ies a

nd co

smet

ics

Fixed-

li ne

telep

hon

e ca

ll s

Broad

band In

tern et

Eco

nom

ic V

ulne

rabi

lity

Sco

re

Economic Vulnerability Scores for Items of Discreti onary Expenditure10 = Most Vulnerable / 0 = Least Vulnerable

Note: In 9/08, 8,000 consumers in the UK, France, Germany and Spain were asked to provide a score to assess the likelihood that they would cut back on a particular area of expenditure. 10 = extremely likely to cut back; 0 = not at all likely to cut back. Source: Execution Primary Research, quoted in UK Ofcom’s “The International Communications Market 2008” report, p. 39. 35

36

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

2005E 2006E 2007E 2008E 2009E 2010E 2011E

IP T

raffi

c (T

B /

mon

th)

Total Consumer Business

Global IP Traffic

Consumer Surpassed Business IP Traffic in 2008E –58% IP Traffic CAGR, 2005-2011E

Source: Cisco Systems, Global IP Traffic Forecast and Methodology; Mobility segment (0.1% of traffic in 2007) not displayed

Consumer IP traffic surpasses Business

YouTube + Facebook Gained ~600 Basis Points of Relative Share in Past 2+ Years While Yahoo! + MSN Lost Share

Global Minute Share, 6/06 – 10/08

Source: ComScore Global 10/08, Morgan Stanley Research. 37

0%

2%

4%

6%

8%

10%

12%

14%

6/06 9/06 12/06 3/07 6/07 9/07 12/07 3/08 6/08 9/08

% S

hare

of G

loba

l Min

utes

Yahoo.com Msn.com Google.com YouTube.com Facebook.com

38

Users Y/Y Growth Comments

344MM(1) +50%

#3 site in global minutes; 5B views of online video in the US (Americans watched a total of 12.6B videos / 591MM hours online in 9/08); #2 global search engine – search queries on YouTube reached 9.2B in 8/08 (+123% Y/Y), surpassing Yahoo! sites with 8.5B searches (+2% Y/Y).(1,2,3,6)

182MM(1) +112%

#5 site in global minutes; 140MM+ active users; 50%+ users outside of college; 52K+ applications + 95% of Facebook members have used at least one(1,4)

370MM(5) +51%

If ‘carrier’ then #2 behind China Mobile; $1.55 annualized revenue per registered user (-3% Y/Y); 2.2B Skype Out minutes (+54% Y/Y); 16.0B Skype-to-Skype minutes (+63% Y/Y)(5)

65MM(5) +19%

$15B total payment volume (TPV), +28% Y/Y, higher than eBay’s global gross merchandise volume; Off-eBay payment volume +49% Y/Yto 51% of TPV(5)

Source: (1) comScore global 10/08; (2) comScore Video Metrix 8/08; (3) YouTube; (4) Facebook; (5) eBay CQ3, (6) comScore qSearch, 8/08. Morgan Stanley Research.

Undermonetized Internet Usage Growth Drivers –Video + Social Networking + VoIP + Payments

Next Generation Platforms =Easy-to-Use + Applications + Users

Note: Kindle’s 200k+ apps refer to book titles available, ~12% of sales of these books were on Kindle. iPhone user estimates exclude channel inventory + duplicates from iPhone 2.5 G users who upgraded to 3G, Y/Y growth from CQ4:07 to CQ4:08E; YouTube, Facebook users per comScore global 10/08, Y/Y growth from 10/07 – 10/08. Facebook application downloads are

cumulative monthly active users for the 200 most-used applications, per AppData (as of 12/18/08).Source: Amazon, Apple, AppData, Facebook, Youtube, Morgan Stanley Research. 39

Time Since Y/Y Applications ApplicationsPlatform Inception Users Growth Available Downloaded

Facebook 4.8 Yrs 182MM 112% 48K+ 308MM+

Apple Wireless Devices 1.5 Yrs 30MM 244% 100K+ 300MM+

iPhone (2.5G + 3G) 1.5 Yrs 14MM 291% 100K+ --

iPod Touch (Wi-Fi) 1 Yr 16MM 210% 100K+ --

YouTube 3.8 Yrs 344MM 50% -- --

Amazon Kindle 1 Yr -- -- 200K+ --

Younger Generations Drive Online Usage Changes

Note: Selection based on (1) comScore’s reported global unique visitors for each website in 9/08;excluding sites with negative Y/Y growth, and (2) Alexa global traffic ranking.

Source: ComScore Global, 9/08, Alexa, Morgan Stanley Research. 40

Social NetworkingBlogs

(Sina Blog)

Video / Music Online Gaming

Knowledge Sharing

Social Bookmarking

41

• YouTube - 344MM unique global visitors, +50% Y/Y, 43B minutes, +99% Y/Y(1)

; other video distribution models: Hulu, Fancast, veoh, Joost, Sling Media, VUDU…

• YouTube = 63% of unique US video viewers + 39% of videos watched online + 34% of total minutes

(2)

0

50

100

150

200

250

300

350

Aug-07 Oct-07 Dec-07 Feb-08 Apr-08 Jun-08 Aug-08 Oct-08

Tot

al U

niqu

e V

isito

rs (

MM

)

0

5

10

15

20

25

30

35

40

45

Tot

al M

inut

es (

B)

Total Unique Visitors (MM) Total Minutes (B)

YouTube Global Traffic

Source: (1) comScore global 10/08; (2) comScore Video Metrix (US) 9/08, Morgan Stanley Research

Online Video –Traction High + Increasing

Hulu –Quickly up to 2% of YouTube’s Global Visitors(1)

• Hulu – 6.1MM global unique visitors (+74% M/M), 111MM minutes (+95% M/M) in 10/08.

• 11.6 minutes of average duration of videos viewed at Hulu, ~4x USA average

• Content support from major networks (NBC, Fox, USA, Bravo, FX, SciFi, E!...) + film studios (Universal, 20th Century Fox, MGM, Sony, Lionsgate)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Oct-07 Dec-07 Feb-08 Apr-08 Jun-08 Aug-08 Oct-08

Tot

al U

niqu

e V

isito

rs (

000)

0

20

40

60

80

100

120

Tot

al M

inut

es (

MM

)

Total Unique Visitors (000) Total Minutes (MM)

Hulu Global Traffic

Note: (1) comScore Video Metrix (US only) utilizes a different methodology and reports that Hulu has 24% of YouTube’s US unique viewers & 22% of YouTube’s US minutes in 10/08. US average duration of online video was 3.0 minutes in 10/08. Global unique

visitors & minutes per comScore global, 10/08. 42

43

YouTube –New Portal(s) = Video Distribution Channel + Social Network

Source: Google, YouTube 11/08

News & Politics - Most Viewed

• ‘Organize the world’s information and make it universally accessible and useful’ – in the most effective way for high customer satisfaction – sort by most active / discussed / recent / responded / viewed / etc.. More / more content providers should get on board, after all, users are voting it’s what they want.

• Monetize away litigation - with new ad formats + finger printing advances + revenue shares?

Sports - Most Viewed

• Digg - 16MM unique visitors, +31% Y/Y, 28MM minutes, +13% Y/Y in 10/08

• User-driven editorial / selection of content (news, videos, images, etc.) through sharing / discovery / democratization – vs. traditional media determining front-page / lead stories

• Users in control – search for preferred content + find what others deem relevant / interesting

Consumers Expect –Wisdom of Crowds / Rankings / Searchability

44Source: comScore global 10/08, Digg.com.

Consumers Expect –Fun / Images / Insight from Others

Find friends who share the visual DNA Find hotels vi a Hotels.com Visualiser

• Youniverse.com – 670K unique visitors, +182% Y/Y, 7MM minutes, +134% Y/Y in 10/08.

• Finds one’s visual DNA by asking users to select pictures in response to a series of questions.

• Social networking – ability to find other people who share your visual DNA.

• Market Research – enables advertisers to mine user preference data;

• In 9/08, Hotels.com launched a Youniverse Visualiser to find out customers’ preference of the trip to provide hotel recommendations.

Source: comScore global 10/08, Youniverse.com, Hotels.com, Morgan Stanley Research. 45

46

Consumers Expect –Personalization

Nike.com – NikeiD

Footjoy.com – Myjoys Picturedoor.co.uk

Source: footjoy.com, nike.com, picturedoor.co.uk, mymms.com

MMs.com – MyM&M’s

Consumers Expect –Citizen Journalism

• User-generated content (news, videos, images, etc.) uploaded directly to UReport site

• Fox News selectively airs popular stories that have been vetted

• Competitors: CNN’s iReport; MSNBC’s First Person

Source: Foxnews.com. 47

Searchability

User rating / popularity

Upload from anywhere –UReport iPhone app

Online Content Consumption Mix in 5 Years?

• Consumer or professional generated?− 40% of USA consumers create entertainment (edit movies / music / photos...)

• Consumer enhanced professional content?

48Note: Based on a survey of 2,200 U.S. consumers in Deloitte’s 2007 State of the Media Democracy report. Source: Deloitte.

Video Monetization – YouTube = <$1 Per User(1) –Paid Search / Click-to-Buy / Pre-Post-In Video Roll / Interactive

Note: (1) per year in 2007; average users per comScore global, revenue per our estimates. Source: YouTube 10/08. 49

Search for ‘iPhone 3G’…

…ads for ‘invisible shield’

Like the music?...

…click to buy from iTunes / Amazon mp3

Creative / Interactive...

‘Wario Land: Shake It’ video breaks YouTube’s UI

50

Social Networking –Significant Share Gains of Internet Traffic

Rank Web site2005 (1)

12345678910

yahoo.commsn.com

google.comebay.com

amazon.commicrosoft.commyspace.comgoogle.co.uk

aol.comgo.com

Traffic rank is based on three months of aggregated historical traffic data from Alexa Toolbar users and is a combined measure of page views / users (geometric mean of the two quantities averaged over time).

Rank Web site2008 (2)

12345678910

yahoo.comgoogle.com

youtube.comlive.com

facebook.commsn.com

myspace.comwikipedia.orgblogger.comyahoo.co.jp

Alexa Global Traffic Rankings

(1) Rankings as of 12/31/05, excludes Microsoft Passport; (2) Rankings as of 12/18/08Source: Alexa Global Traffic Rankings, Morgan Stanley Research.

0%

20%

40%

60%

80%

100%

0% 10% 20% 30% 40% 50% 60%

Unique Visitors Y/Y Growth

Pen

etra

tion

(% o

f Onl

ine

Use

rs)

SocialNetworks

Photos

Online Gaming

Reference

Sports

Auto

Travel

InstantMessengersGeneral

News

Business /Finance

Multimedia

E-mailRetail

Entertainment

Search

Portals

World Wide Visitor Growth = 10.4%

Social Networking –Fast Growth + Low Penetration

Source: comScore ‘Digital World – State of the Internet’ 6/08, data from 1/08. 51

Global Internet Category Visitors Y/Y Growth & Pene tration

52Source: USC Annenberg School: Digital Future Report 2007.

0%

20%

40%

60%

80%

100%

Internet Television Radio Newspaper PersonalSource

% o

f Use

rs A

ge 1

7+ R

espo

ndin

g Im

porta

nt /

Ver

y Im

porta

nt

Importance as Source of Information

73%80%

68%63% 63%

The New Social Network =Personal Sources on Internet

Messaging by Generation –Text…Facebook Wall…Email…Phone…US Postal Service

53

Brother (Rob - College)Wrote on my Facebook Wall

Brother (Rob - College)Wrote on my Facebook Wall Wife (Melissa)

Funny emailWife (Melissa)Funny email

Brother (James - High School)Text Message via Mobile

Brother (James - High School)Text Message via Mobile Mom (Victoria)

Phone call (45 minutes!!!)Mom (Victoria)

Phone call (45 minutes!!!)

Grandparents (Dom & Ida)Birthday card with $25

Grandparents (Dom & Ida)Birthday card with $25

Kids (Zach 5 & Jackson 3 yrs.)Hugs and Kisses

Kids (Zach 5 & Jackson 3 yrs.)Hugs and Kisses

Birthday Boy (Tom Zawacki)Happy Birthday from my Family

Birthday Boy (Tom Zawacki)Happy Birthday from my Family

Source: Tom Zawacki – CEO of Lemonade.

54

6%14%

8%

22%

35%

16%

All OtherCommunicationsSocial ConnectionsShopping & TravelEntertainment & LeisureWork, Business & Education

Worldwide Share of Online Time (1)

Category didn’t exist 3

years ago14%

35%38%

22%

0%

10%

20%

30%

40%

Yahoo! Mail Facebook%

of T

otal

Min

utes

Age 15-24 Age 45+

Connecting – Younger Users Via Social Networks + Older Users Via E-Mail? (2)

Social Networking –Connectivity Changing…Is E-Mail Archaic?

Source: (1) comScore ‘Digital World – State of the Internet’ 6/08; (2) comScore global 8/08.

55

Facebook –Rapid User / Usage Growth

0

20

40

60

80

100

120

140

160

180

200

Jul-07 Sep-07 Nov-07 Jan-08 Mar-08 May-08 Jul-08 Sep-08

Tot

al U

niqu

e V

isito

rs (M

M)

0

5

10

15

20

25

30

35

40

Tot

al M

inut

es (B

)

Total Unique Visitors (MM) Total Minutes (B)

Facebook Global Traffic

Source: comScore global 10/08, Facebook 11/08, Morgan Stanley Research.

• 182MM visitors, +112% Y/Y (140MM+ active users), 34B minutes (#4 globally behind Yahoo!, Live and YouTube), +79% Y/Y

• Avg user has 100 facebook friends; 13MM+ users update their status daily; 2.6B minutes spent on Facebook every day (worldwide)

• 10B+ photos uploaded to the site; 700MM+ photos / 4MM+ videos uploaded each month;

• 660K+ developers / entrepreneurs; 52K+ applications built to date; 140 new apps added per day; 95%+ members have used at least one app.

56

Facebook -Connecting is Key

Note: Genre breakdown per O’Reilly Media’s analysis of the primary user goals of 261 of the most-used Facebook application.Source: O’Reilly Media, Inc (March 2008 report), Morgan Stanley Research.

Genres of Facebook’s 261 Most Used Applications

9%

3%

3%

5%

5%

7%

10%

10%

11%

12%

26%

Other

Playing games

Playing with digital pet

Self expression

Media sharing

Sending gifts

Categorizing friends

Profile enhancement

Playing social games

Comparing yourself with others

Enhanced communication

Top 40 Apps' # of Apps# of Monthly Active w/ 1MM+

Category Applications % of Total Users (MM) MAUs

Just For Fun 15,005 31% 137 37Games 4,496 9 78 25Sports 4,020 8 4 0Education 2,424 5 37 5Utility 2,287 5 20 2Music 1,918 4 11 13Chat 1,865 4 16 3Dating 1,840 4 52 13Messaging 1,716 4 30 8Photo 1,571 3 36 3Video 1,532 3 47 4Business 1,520 3 1 0Events 1,493 3 23 5alerts 1,313 3 27 7Fashion 1,155 2 5 1Food & Drink 1,056 2 8 1Politics 976 2 22 7Travel 873 2 7 2Money 553 1 1 0Mobile 482 1 7 1Classified 468 1 0 0File Sharing 303 1 1 0

Overall* 48,549 204 66

Facebook –48K+ Applications – 48% = Fun / Games / Sports

Note: Category breakdown per Facebook, one application can belong to multiple categories; Overall* statistics eliminate these duplications; Facebook reports 52,000+ apps “built to date” while AppData reports 48,549 available as of 12/18/08.

Source: Facebook, AppData, Morgan Stanley Research. 57

Facebook –Home Page for Next Generation – Customized / Current

• Facebook rolled out cleaner / simpler design 7/20/08 aiming to provide easier navigation with separate tabs for Wall (updates), Info (background), Photo, and Boxes (applications).

• Biggest change: Wall is now default tab, with full multimedia feeds integration – showing most recent and relevant info both about the user and by the user.

Tabbed Browsing

Integrating Feeds into

the Wall

Picture / Video Updates on the

Multimedia Wall

Third-party Applications

Now on Toolbar

Online Chatting Function

Source: Facebook 58

‘Engagement Ads’ – Thump Up to Recommend

to Friends

59Note: (1) per year in 2007, average unique visitors per comScore global, revenue per our estimates.

Source: Facebook.

Social Networking – Facebook = $2 Per User(1)

Opportunity to Get in Middle of Conversations

Virtual Gift – $1 = One Wish

…Friends Notified via News Feeds

Become a Fan of …

Source: Company Reports, Morgan Stanley Telecom Research. Note: (1) Subscriber data based on CQ2:08; (2) Subscribers given as access lines, excluding DSL. (3) China Netcom officially

merged into China Unicom on 10/15/08, China Unicom wireless sold all CDMA business to China Telecom; (4) Market Cap data as of 10/14/08; (5) Subscriber figure for Skype is registered user amount as of CQ3:08.

Company

China Mobile (1)

Vodafone (2)

China Telecom (1)

Telefonica MovilesAmerica Movil China Unicom (3)

T-MobileOrangeChina Unicom (3)

AT&T WirelessTelecom Italia MobileVerizon WirelessBharti AirtelAT&TNTT DoCoMoNTTSprint / Nextel Verizon

RegionSubscribers

(MM)Market Cap (4)

($B)

ChinaEurope / Japan

ChinaEurope / LatAm

LatAmChina

Europe / USAEuropeChinaUSA

Europe / LatAmUSAIndiaUSA

JapanJapanUSAUSA

415269215183165 128125 11410973706969 5954454338

$199 11034986837606713

155188230

15563541282

Y/YGrowth

25%16(4)542

134

11(6)15111162(8)1

(9)(6)10

Type

WirelessWirelessWirelineWirelessWirelessWirelessWirelessWirelessWirelineWirelessWirelessWirelessWirelessWirelineWirelessWirelineWirelessWireline

Skype (5)

370MM Registered Users(+51% Y/Y)

Average Growth: 11%

VoIP –Skype = #2 Global Wireless / Wireline Carrier

60

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

CQ3:05 CQ4:05 CQ1:06 CQ2:06 CQ3:06 CQ4:06 CQ1:07 CQ2:07 CQ3 :07 CQ4:07 CQ1:08 CQ2:08 CQ3:08

Glo

bal O

nlin

e A

dver

tisin

g R

even

ue ($

MM

)

Google Yahoo! Microsoft AOL

Online Advertising –Google Share = 67% in CQ3:08 vs. 46% in CQ3:05

Global Online Advertising Revenue (1)

(1) Google and Yahoo! include TAC; Source: Company Reports, Morgan Stanley Research 61

46%46%

34%34%

10%10%

7%7%

20%20%

67%67%

6%6%

10%10%

62

Source: (1) Google, Morgan Stanley Research (calculated as reported gross ad revenue multiplied by US % share of gross revenue)(2) Yahoo!, Morgan Stanley Research (calculated as gross Marketing Services revenue multiplied by US % share of gross revenue);

(3) Internet Advertising Bureau (IAB) / PriceWaterhouseCoopers (PWC) Internet Advertising Revenue Reports (calculated as difference between total IAB US ad revenue and sum of Google, Yahoo! gross ad revenue), Morgan Stanley Research. Assuming

that TAC of Google and Yahoo! was included in others total, this segment would have been up ~10% Y/Y

0

500

1,000

1,500

2,000

2,500

3,000

CQ3:07 CQ3:08

US

Ad

Rev

enue

($M

M)

Google, US Gross Ad Revenue (1) Yahoo!, US Gross Ad Revenue (2) Others (3)

42%

20%

44%

19%

US Online Ad Revenue Mix

37%38%

Google + Yahoo! = ~63% of US Online Ad Revenue -‘Others’ Grew ~10% (vs. ~6%) Owing to Google / Yahoo! Affiliate Assist, CQ3:08

63

• Google generated $5.5B in gross ad revenue in CQ3:08; it PAID OUT $1.5B (28%) to thousands of partners like AOL, Ask Jeeves, EarthLink, + HowStuffWorks(1)

• Yahoo! generated $1.6B in gross ad revenue in CQ3:08; it PAID OUT $461MM (30%) to partners like CNN, ESPN, + The Wall Street Journal (2)

Google + Yahoo! Share Significant Portion of Revenue with Partners + Affiliates

Source: (1) Google gross Advertising revenue, Morgan Stanley Research; (2) Yahoo! gross Marketing Servicesrevenue, Morgan Stanley Research.

64Source: The State of Retailing Online 2007 / 2008 (Forrester Research), comScore global 9/08, Morgan Stanley Research.

6%4%

35%

1% 1% 1%

27%30%

9%6%

13%

4%

11%

4%2%

7% 7%

18%

4%5%2%

3%2%

0%

10%

20%

30%

40%

Searc

h en

gine

mar

ketin

gOrg

anic

traffic

Affiliat

e pr

ogra

ms

to p

rosp

ectin

g lis

ts

Shopp

ing

com

paris

on en

gines

Catalo

gsNew

por

tal d

eals

Offline

adv

ertis

ingBan

ner a

ds

Tradit

ional

por

tal d

eals

Sweeps

take

s

Social

net

workin

g sit

es

Co-re

gistra

tion

on o

ther

Web

site

s

2006 2007

% of New Online Customers for Online Retailers / Ma rketing Spend Mix

N/AN/A

% C

usto

mer

s ac

quire

d fr

om s

ourc

e

N/A

Search Should Continue to Become More Important –34% Y/Y Google Query Growth (CQ3:08)

U.S. Internet Ad Revenue Share by Pricing Model, 20 00 - 2007

Note: Performance based advertising includes search, lead-generation, among others; Hybrid pricing model includes a mix of impression-based pricing plus cost-per-click, sale, lead / straight revenue share;

Source: IAB, Morgan Stanley Research 65

Performance-Based Advertising Gaining Share+20% Y/Y in CH1:08 vs. +12% for CPM-Based Revenue

10%12%

21%

37%41% 41%

47%51%

0%

15%

30%

45%

60%

2000 2001 2002 2003 2004 2005 2006 2007

% S

hare

of T

otal

Rev

enue

Performance CPM HybridSearch Revenue Share

0%

20%

40%

60%

80%

100%

2002 2003 2004 2005 2006 2007

U.S

. In

tern

et A

d S

pend

% M

ix

Search Advertising Banner Ads Rich MediaClassified Advertising E-mail and Other

Search =Dramatic Share Gains of Online Ad Spending

Source: IAB, search spending adjusted by our estimates, Morgan Stanley Research 66

U.S. Internet Advertising Mix

52%52%

20%20%

10%10%

12%12%

7%7%

15%15%

14%14%

15%15%

9%9%

47%47%

Search =Still Lots of Share to Grab

U.S. Internet Search Spendingvs.

Ad Spending on Classified, Yellow Pages & Newspaper , 2000-2007

$122 $299 $889 $2,133$4,113

$6,910$9,430

$12,282

$68,402

$61,224 $60,890$63,265

$67,115$69,923

$65,146

$70,348

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

2000 2001 2002 2003 2004 2005 2006 2007

Ad

Spe

nd (

$MM

)

Internet Search Combined Classified, Yellow Pages & Newspaper

Source: IAB, search spending adjusted by our estimates;Classified, Yellow Pages & Newspaper spending per MS Media team.

Morgan Stanley Research. 67

68

$30

$25

$31$28

$2$3$2 $1

$26

$34

$22

$18

$0

$10

$20

$30

$40

2005 2006 2007 2008E

Sea

rch

vs. D

ispl

ay E

ffect

ive

CP

M

Search Banner Ads Rich Media

Note: (1) Search effectiveness here measured by dividing the total search advertising revenue by total search ads impressions (000);(2) Banner Ad / Rich Media CPM calculated as total banner / rich media advertising revenue divided by total impressions (000).

Source: Morgan Stanley Research.

CPMs –Search vs. Banner vs. Rich Media

2005-2008ECAGR

8%

-19%

-19%

69

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

3/05

9/05

3/06

9/06

3/07

9/07

Impr

essi

ons

(MM

)

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

CP

M

Banner Ads Impressions Banner Ads CPM

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

3/05

9/05

3/06

9/06

3/07

9/07

Impr

essi

ons

(MM

)

$0

$5

$10

$15

$20

$25

$30

$35

$40

CP

M

Rich Media Impressions Rich Media CPM

Near term: Ad Supply > Ad Demand –Ad Impressions Growing Rapidly…CPMs Declining

Source: Internet Advertising Bureau (IAB), Nielsen NetRatings, Morgan Stanley Research.

U.S. Banner Ad Impressions & CPM,2005-2007

U.S. Rich Media Impressions & CPM,2005-2007

$0.40 $0.41

$0.44 $0.43 $0.42$0.44

$0.46$0.44 $0.45

$0.48 $0.49$0.51

$0.53 $0.54 $0.53

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

1Q05 3Q05 1Q06 3Q06 1Q07 3Q07 1Q08 3Q08

Search Cost Per Click

Search =CPC Trend - Up / Down / Sideways?

Google Cost Per Click, 2005 - 2008

Source: Google, Morgan Stanley Research 70

71

E-Commerce -USA Online Penetration = 4-6% and Rising

Note: (1) Our proprietary adjusted e-Commerce sales & Census Bureau’s quarterly total retail sales data suggest ~4% penetration, Forrester claims 6%.

Source: The State of Retailing Online 2008 (Forrester Research).

Categories’ Online Penetration of US Retail Market, 2007

1%Food / beverage / grocery10%Movie tickets

2%Auto / auto parts10%Apparel / footwear

4%Pet supplies11%Jewelry

5%Appliances / tools12%Flowers / cards21%Gift cards / certificates

6%OTC meds / personal care13%Office supplies24%Music / video

8%Sporting goods / apparel18%Consumer electronics24%Books

9%Cosmetics / fragrances19%Baby products27%Other event tickets

9%Home furnishings19%Toys / video games45%Computer products

>20% 10 - 20% <10%

72

Amazon.com’s Recommendation Engine =Web’s Most Search Engine + Advertiser?

Source: Amazon.com, Google

Amazon.com search + recommendation engine: Leveraging data

What other customers are

thinking

What other customersare saying

What other customersare buying

New formats: Kindle

What Amazonrecommends

73

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

CQ3:02 CQ3:03 CQ3:04 CQ3:05 CQ3:06 CQ3:07 CQ3:08

Y/Y

Gro

wth

US Adjusted Retail E-Commerce Sales Amazon.com North America RevenueUS Total Retail Sales

Amazon.com vs. US Retail E-Commerce Sales (1)

~24ppts

(1) Adjusted for eBay by adding eBay US gross merchandise volume and subtracting eBay US transaction revenue; Source: Amazon.com (CQ3:08), US Dept. of Commerce (CQ3:08), Morgan Stanley Research.

Amazon.comKey Operating Metrics

CQ4:07 CQ1:08 CQ2:08 CQ3:08

Revenue $5,673 $4,135 $4,063 $4,264

Y/Y Growth 42% 37% 41% 31%

Active Customers 76 79 82 85

Y/Y Growth 19% 19% 18% 17%

TTM Revenue per Active Customer

$195 $202 $210 $215

Y/Y Growth 17% 17% 19% 18%

Total Units 241 196 190 203

Y/Y Growth 33% 31% 32% 30%

(All metrics in MMs, except for TTM Revenue per Active Customer)

Amazon.com Should Continue to Gain ShareHigh Customer Satisfaction / Recommendation Engine / Impressive Metrics

74

Amazon.com –Following Its Customers By Leading With Technology

* Note: Amazon.com utilizes its Mechanical Turk to try to match the product with the picture you sent. These “Mechanical Turks”are not Amazon employees or any artificial intelligence, but ordinary folks around the world. Once product is matched, you can

access the findings on both your iPhone and Amazon.com. Source: Amazon.com.

• Search on any keyword (e.g. item name, author, artist, etc.) or ISBN / UPC code

Amazon TextBuyIt

1 2

Text search keywords to ‘AMAZON’(262966)

Reply with 1 or 2 to buy an

item from search results

3

Answer call to hear details + confirm order

Amazon iPhone Application - Amazon Remembers*

75

2) Mobile –Innovation in wireless products / services accelerating – changes

should create + destroy significant wealth

Technology / Internet

76

Nintendo Wii

30MM consoles since 11/06 launch – raised bar with motion sensors + playability

Apple iPhone 3G

1MM units sold in three days; 300MM apps downloaded since 7/11/08 launch; mobile browser market share already 50% > Windows Mobile –raised bar with ease-of-use + functionality

Microsoft Xbox 360

12MM Xbox Live members (+100% Y/Y) since 11/02 launch – raised bar with online playability

3 Skype Phone

500K+ units in < 200 days. Leverage large Skype / Facebook user base of 370MM (+51%Y/Y) / 161MM (+119%Y/Y) + create a low-cost web-enabled VoIP, social networking, digital presence phone. Now INQ1…

Amazon.com Kindle

With free EV-DO + 200K titles + newspaper / magazine / blog subscriptions. Amazon may do with books what Apple did with tunes. Kindle accounts for 12% of AMZN’s sales for titles available on Kindle

Netbooks (Asus Eee PC)

Estimated 5.2MM units will be shipped in 2008; as much as 50MM could be shipped in 2012, per Gartner – low price points + high mobility + wireless / 3G access pioneering ‘Cloud Computing’ usage model.

Source: Nintendo (CQ2:08), Microsoft, Amazon.com, Apple, TechCrunch estimates, eBay (CQ3), Gartner, Morgan Stanley Research.

Mobile –A New Computing Cycle With Game Changer Products with

Extraordinary Ease-of-Use

77

Notebooks Retrofitting to Cloud Via 3G –PCs Retrofitted to Internet Via Dial-Up ~1995 Deja Vu?!

• 64% of new Austrian broadband subs used cellular modems, CQ2:07

• Global cellular modem to rise from 5MM in 2006E to 68MM+ shipments in 2012E (53% CAGR) – ABI Research, 5/07

• 13MM cellular modem users in USA, CQ2:08E – Nielsen Mobile

• 66MM global WiFi unit shipments, C2007E - Synergy Research

Note: Cellular modem shipments includes PC Cards / ExpressCards, USB modems, internal modems + 3G/Wi-Fi routers); Source: ABI Research, Informa, Nielsen Mobile, Synergy Research.

78Source: Opera Software, Morgan Stanley Research.

A full web experience + 50% faster Pages transcoded p er month (Bn)

− Remote Server first pre-processes requested web pages

− Web content is then compressed to reduce the size of data transfer

− Fully-rendered web pages sent to your phone

− Advantage: full web rendering and faster browsing on simpler phones

2006 2007 2008

Opera Mobile Web Browser Shows Mobile Internet Growth -~21MM Users (+311% Y/Y), 5B+ Page Views (+326% Y/Y), 10/08

Mar JunSep Mar Oct

5

4

3

2

1

17.121.1

25.6

32.4

43.3

52.1

58.3

0

10

20

30

40

50

60

70

CQ1:07 CQ2:07 CQ3:07 CQ4:07 CQ1:08 CQ2:08 CQ3:08

Mes

sage

s D

eliv

ered

by

Ver

iSig

n (B

n)

VeriSign Mobile Message Shows Mobile Internet Growth –~58B Messages (+142% Y/Y), CQ3:08

Global Mobile Messages Delivered by VeriSign, CQ1:0 7 – CQ3:08

Note: Mobile messages include both text and multimedia messages. Source: VeriSign Mobile Messaging Index Report. 79

Mobile Internet Evolving at Uniquely Fast Clip

Source: Nokia, AT&T, Apple, Motorola, Google, T-Mobile, RIM, 3 UK, as of 12/12/08. Morgan Stanley Research. 80

Date Important Announcements in the Mobile Industry

12/05/08 3 UK launches INQ1, the world's first social networking phone, with 50,000 pre-registration

10/01/08 AT&T announces reorganization to better align broadband, TV and mobile services for consumers.

10/01/08 Apple drops the non-disclosure agreement (NDA) for iPhone application developers.

9/30/08 Nokia to acquire leading consumer email and instant messaging provider OZ Communications.

9/29/08 Nokia’s Chief Technology Officer Bob Iannucci resigns.

9/28/08 Motorola to build a 350-person Android team.

9/24/08 Google, T-Mobile and HTC launch G1, the first phone based on Google’s Android open mobile platform.

8/04/08 Motorola hires Qualcomm’s Sanjay Jha as co-chief executive to oversee the mobile devices division.

7/23/08 Nokia, Qualcomm settle patent dispute.

7/11/08 Apple and AT&T launch iPhone 3G in the U.S.

6/24/08 Nokia acquires Symbian Limited and establishes the Symbian Foundation.

5/12/08 RIM introduces the BlackBerry Bold smartphone.

5/12/08 RIM, RBC and Thomson Reuters to anchor a $150MM BlackBerry Partner Fund focused on developing mobile applications.

5/08/08 Apple, KPCB launches $100MM iFund venture capital pool to support iPhone / iPod Touch application development.

81

Still Early in 3G+ Ramp But…2010 Should Be Inflection Point @ ~22% of Subscribers

0

1

2

3

4

5

2007E 2008E 2009E 2010E 2011E 2012E 2013E

Sub

scrib

ers

(B)

0%

10%

20%

30%

40%

50%

% o

f Tot

al W

irele

ss S

ubsc

ribe

rs

2.5G and Below Subscriptions 3G and Above Subscriptions % 3G and Above Penetration

Global 3G+ Penetration

Note: 2.5G can be compared to ‘narrowband’ Internet access, while 3G can be compared to ‘broadband ’ Internet access.Source: Ovum, Morgan Stanley Research.

Japan Internet Users by Access Device

40%

58%

73%

81% 81% 83%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2002 2003 2004 2005 2006 2007

% o

f Jap

an In

tern

et U

sers

% using PC % using Mobile

Source: Japan Ministry of Internal Affairs and Communication. 82

Japan Shows Way in Mobile Internet Usage –Mobile Nearly Matches PC

83

Apple Changed Mobile Game…With Impressive UI + 2.5G!i – NOT – A - Phone

Source: Apple

Apple iPhone 3G –Winning Consumers Via Simple + Useful Applications

Speak Mandarin?

Lonely Planet Mandarin

Phrasebook will say it for you.

Catchy Tunes?

Shazam will listen and find the song

for you.

Source: Apple. 84

Apple iPhone –Data Usage 6-10x Higher than Average USA Mobile UsersApp Downloads per iPhone 100x Higher than non-iPhones

13%7% 9%

6% 4% 5%

85%

74%70%

59%

50%

31%

0%

20%

40%

60%

80%

100%

BrowsingNews

Music Games Web Search SocialNetworking

MobileVideo

% o

f U.S

. Mob

ile S

ubsc

riber

s

Average U.S. Mobile Users iPhone Users

Note: KPCB iFund estimates 14MM total weekly app downloads for 12MM iPhone users, and 3MM weekly mobile app downloads on 250MM non-iPhones, thus translating into mobile application downloads 100x higher on iPhone. Source:

M:Metrics, 1/08 Survey of U.S. mobile subscribers, n= 31,389, Games category per KPCB estimates. 85

Mobile Content Consumption

Stunning Growth in iPhone Applications Since 7/08 Launch –~10K Apps, 34% = Games / Entertainment, 300MM Downloads (~10 per User)

Note: Data as of 11/30/08. ~10 downloads per user include iPod Touch users. Source: Apple iTunes, Morgan Stanley Research. 86

# of Apps % of Total# of Paid

Apps

Paid as % of Category

Total

Average Price of Paid

Apps

Games 2224 23% 1756 79% $2.24Entertainment 1054 11 784 74 1.64Utilities 974 10 708 73 3.08Education 716 7 654 91 5.59Book 499 5 459 92 2.11Productivity 491 5 374 76 3.92Lifestyle 490 5 362 74 3.05Reference 429 4 360 84 7.27Travel 408 4 310 76 7.88Healthcare & Fitness 342 4 284 83 3.14Music 316 3 233 74 5.13Sports 298 3 185 62 4.65Navigation 269 3 209 78 5.88Business 261 3 191 73 11.07Finance 248 3 187 75 7.99Photography 189 2 136 72 2.67Social Networking 170 2 59 35 3.07News 136 1 60 44 2.06Medical 83 1 71 86 35.40Weather 48 0 33 69 5.02

Total 9645 7415 77% $4.15

Category

INQ1 –World’s First Social Phone + 50K Registered Potential Users Before Launch

• Full Facebook integration with phone’s contacts / messages / notification system

• Seamless Skype integration (free Skype-to-Skype calls over 3’s network) + full web browser based on WebKit (the rendering engine behind iPhone and Android’s browser) + doubles as a 3G modem

• Preloaded with Google apps / YouTube link / eBay tracker / MySpace / 3Music Store, etc.

• Free on contract (from £15 / month) / £79.99 on Pay-As-You-Go.

Note: 50K people registered an interest in the INQ1 phone prior to official launch in 11/08, these are not pre-orders.Source: Three, Morgan Stanley Research. 87

FacebookWindows Live

MessengerSkype ‘Live Contacts Book’

USA Mobile Carriers –Data ARPU Growth Offsetting Declining Voice ARPU

$50 $50 $49$47 $46 $45 $46

$44 $43 $43 $43$41 $40 $40 $39

$3 $4 $5 $5 $6 $6 $7 $8 $8 $9 $10 $10 $11 $12 $12

$0

$10

$20

$30

$40

$50

$60

$70

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08

Voice ARPU Data ARPU Total Average ARPU

Source: Simon Flannery, Morgan Stanley Research.

Average U.S. Wireless Carrier ARPU (Average Revenue Per User) Breakdown, CQ1:05 – CQ3:08

88

Global Wireless Data ARPU –Japan in Clear Lead, USA Catching Up Faster Than Others

Data ARPU as Percentage of Total, CQ1:05 – CQ3:08

Note: Western Europe is the weighted average of UK, Germany, Spain, Italy & France; Asia (ex. Japan) is the weighted avg of China, India, Indonesia, S. Korea, Thailand, Philippines, Malaysia and Singapore. Blended ARPU includes both pre-paid and contract plans.

Asia (ex. Japan)’s blended ARPU ranges from $5 (Philippines), $10 (China), to $18 (Malaysia) and $37 (S. Korea). USA (iPhone) ARPU is contract only, per AT&T. Latin America data ARPU is ~13% of total in CQ3:08. Source: Morgan Stanley Research. 89

26% 26% 26% 26%28% 28% 29% 29%

31% 32%33%

35%

37%39% 39%

6% 7%9%

10%11%

12% 13%15%

16%18%

18%20%

21%22%

24%

0%

10%

20%

30%

40%

CQ1:05 CQ3:05 CQ1:06 CQ3:06 CQ1:07 CQ3:07 CQ1:08 CQ3:08

Dat

a A

RP

U a

s %

of T

otal

Japan Western Europe Asia (ex. Japan) USA

$54CQ3:08 Blended

ARPU (US$) : $5 - $37$37 $51 ($95)

(iPhone)

Quarterly Worldwide Smartphone Sales by Operating S ystem

0

5

10

15

20

25

30

35

40

CQ1:06 CQ2:06 CQ3:06 CQ4:06 CQ1:07 CQ2:07 CQ3:07 CQ4:07 CQ1 :08 CQ2:08 CQ3:08

Uni

ts S

hipp

ed (M

M)

Symbian RIM Microsoft Apple Linux Palm Others

Source: Gartner. 90

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

EMEA North America APAC ex. Japan Japan Latin AmericaCQ

3:08

Dis

t.of S

mar

tpho

ne S

ales

Symbian Dominates Smartphones But Losing Share –USA Could Gain Lead in Mobile Internet Innovation?

91

Technology / Internet

3) Emerging Markets –Pacing next wave of technology adoption – leading players in

many emerging markets aren’t the usual suspects…

Broadband + Mobile + Internet =Especially High Global Growers

2002 Y/Y 2007 Y/Y Global 2007 NetCategory Growth Rate Growth Rate Market Size Additions

Broadband Subscribers 78% 23% 349MM 64MM

Mobile Subscribers 20 20 3,319MM 563MM

Internet Users(1) 26 16 1,352MM 182MM

Financial Cards(2) 12 11 8,016MM 804MM

Installed PCs 12 8 900MM 66MM

Cable / Satellite TV Subscriptions 8 6 761MM 40MM

GDP per Capita 2 3 22K 1K

Population 2 1 6,501MM 77MM

Telephone Lines 5 -0 1,277MM -4MM

Note: (1) Include mobile Internet users, based on ITU’s compilation of country reports, surveys and estimates; (2) Includes credit / debit / ATM / charge cards in circulation; Source: Morgan Stanley Research. 92

Top 10 Emerging Markets to Surpass Top 10 Developed Markets in Internet Users in 2008

Top 10 Emerging Markets vs. Top 10 Developed Market s – Internet Users

Note: Emerging / developed markets as defined by IMF; Top 10 chosen based on largest GDP.Top 10 emerging markets: China, India, Russia, Brazil, Mexico, Turkey, Indonesia, Iran, Poland, and Saudi Arabia;Top 10 developed markets: U.S., Japan, Germany, U.K., France, Italy, Spain, Canada, South Korea, and Australia;

Source: IMF, ITU, Morgan Stanley Research. 93

0

100

200

300

400

500

600

700

2001 2002 2003 2004 2005 2006 2007 2008E

Inte

rnet

Use

rs (

MM

)

0%

10%

20%

30%

40%

50%

60%

70%

80%

Y/Y

Gro

wth

Top 10 Emerging Markets Top 10 Developed Markets

Top 10 EM Y/Y Growth Top 10 DM Y/Y Growth

94

Rank CountryRelative

Weighting

2004

Rank CountryRelative

Weighting

12345678910

12345678910

USAChinaJapan

GermanyUK

IndiaFranceItaly

S. KoreaCanada

9.08.26.55.75.55.35.25.25.15.1

ChinaUSA

JapanGermany

IndiaUK

FranceRussia

S. KoreaBrazil

2007

Note: Red indicates countries moving out of the top 10 TMT countries;Green indicates countries moving into the top 10 and highlights China / India

Source: Morgan Stanley Research

TMT (Technology / Media / Telecom) Update =China #1 + Rest of BRIC Gaining Ground

8.98.86.15.65.65.35.35.25.25.2

From our database on market sizing of global TMT (Technology, Media & Telecommunications) products and services. We measure market sizes and growth rates for core TMT metrics: GDP per capita (PPP), telephone lines, cable / satellite TV households, installed PCs, mobile subscribers, internet users, financial cards(1), and broadband subscribers. We do this for the 52 most important economies based on purchasing power / economic strength, as measured in terms of population / GDP per capita. We standardized each country’s position in the global market in each category and adjusted values to reflect a positive scale. The relative ratings and ranks were then determined by calculating an average of Z-scores across categories. For example, in the United States in 2007, standardized and adjusted values of 6.58 in GDP per capita, 7.57 in telephone lines, 10.79 in installed PCs, 7.30 in mobile subscribers, 8.55 in cable subscribers, 9.60 in Internet users, 10.91 in financial cards, and 9.45 in broadband subscribers, produces a relative weighting of 8.84.

Internet User Net Additions –China, Brazil, Pakistan, Columbia, India, Iran, Russia Impressive

Note: Penetration is per person. Source: ITU, Morgan Stanley Research. 95

2007Net Internet

Users Added 2007 PenetrationRank Country (000's) Y/Y Growth Level

1 China 73,000 53% 16% 2 United States 9,800 5 73 3 Brazil 7,400 17 26 4 Pakistan 5,500 46 11 5 Colombia 5,395 80 25 6 India 5,000 7 7 7 Iran 5,000 28 32 8 Russia 4,311 17 21 9 Germany 3,900 10 52

10 France 3,553 12 55 11 Vietnam 3,188 22 21 12 Canada 3,000 12 85 13 Egypt 2,620 44 12 14 Indonesia 2,424 23 6 15 United Kingdom 2,400 6 66 16 Mexico 2,248 11 22 17 Thailand 2,003 18 20 18 Nigeria 2,000 25 7 19 Poland 1,915 14 42 20 Venezuela 1,580 38 21

Note: (1) Penetration is per person; mobile subscribers include all active SIM card subscriptions; people in many countries outside of the US use more than one SIM cards on a regular basis, which may results in greater than 100% penetration levels.

Source: Morgan Stanley Research.96

Mobile Subscriber Net Additions –Pakistan = 226% more than USA, Indonesia = 33% more than USA, Iran just 5% less than USA

2007 NetMobile Subs 2007 Penetration

Rank Country Added (000's) Y/Y Growth Level (1)

1 China 86,228 19% 41% 2 India 67,570 41 21 3 Pakistan 44,346 129 50 4 Brazil 21,062 21 64 5 Russia 19,326 13 120 6 Indonesia 18,032 28 36 7 United States 13,596 6 85 8 Iran 12,910 77 42 9 Egypt 12,046 67 41

10 Germany 11,499 13 118 11 Mexico 11,237 20 65 12 Thailand 10,654 26 78 13 Turkey 9,313 18 90 14 Argentina 8,891 28 103 15 Saudi Arabia 8,718 44 117 16 Vietnam 8,225 53 28 17 Nigeria 8,073 25 28 18 Philippines 7,306 17 57 19 Peru 6,645 76 55 20 Algeria 6,565 31 80

Non-US Markets Lead Usage Penetration in Many Categories

Source: Morgan Stanley Research

Social Networking: Brazil / S. Korea

E-commerce: Germany

Mobile Payments + TV: Japan

Broadband:S. Korea

Online Gaming: China

Microtransactions via SMS: Philippines

Online Advertising: UK

97

A Scary Thing Happened on the Way to the Forum –Rampant Piracy in Most Emerging Markets

21%

33%

59%

60%

65%

68%

0% 10% 20% 30% 40% 50% 60% 70% 80%

North America

Western Europe

Asia-Pacific

Middle East / Africa

Latin America

Central / Eastern Europe

Piracy Rate

Note: per BSA (Business Software Alliance) and IDC Global Software Piracy Study, which covers piracy of all packaged software that runs on personal computers, the study excludes types of software that run on servers or mainframes or software sold as a service.

Source: BSA.

Packaged Software - Piracy Rate by Region, 2007

Russia Russia –– 73%73%

China China –– 82% / India 82% / India –– 69%69%

98

Brazil Brazil –– 59%59%

99

4) Cloud Computing –Access + storage need + virtualization driving change

Technology / Internet

100

Storage Growth +62% in 2007E –Consumer > Professional Demand

Source: Seagate, Katy Huberty, Morgan Stanley Research

0

20,000

40,000

60,000

80,000

100,000

120,000

2003E 2004E 2005E 2006E 2007E 2008E 2009E 2010E

Pet

abyt

es

Home Professional

Global Storage Sold Annually

Cloud Computing –Consumer + Enterprise Adopt ‘Software-as-a-Service’ Model

Amazon.com Salesforce.com

101Source: Amazon.com, Salesforce.com, Morgan Stanley Research

102102Source: Getty Images

Google Data Center – The Dalles, Oregon

‘A Giant Supercomputer’ –Datacenter Behind the Cloud

103

1. sarah palin

2. beijing 2008

3. facebook login

4. tuenti

5. heath ledger

6. obama

7. nasza klasa

8. wer kennt wen

9. euro 2008

10. jonas brothers

Google Zeitgeist –Predictive Power of Data Underutilized

Trendsetters 2008 – Going Green

Source: Google Year-End Zeitgeist, 2008.

Fastest Rising (global)1. obama

2. facebook

3. att

4. iphone

5. youtube

6. fox news

7. palin

8. beijing 2008

9. david cook

10. surf the channel

Fastest Rising (US)

Economy – Layaway Makes a Comeback Politics – U.S. Presidential Election

104

Amazon Web Services –Providing Cheap / Reliable Storage in Cloud

0

50

100

150

200

250

300

350

400

450

CQ2:05 CQ3:05 CQ4:05 CQ1:06 CQ2:06 CQ3:06 CQ4:06 CQ1:07 CQ2 :07 CQ3:07 CQ4:07 CQ1:08 CQ2:08

Tot

al R

egis

tere

d D

evel

oper

s (0

00)

0%

2%

4%

6%

8%

10%

12%

14%

16%

Q/Q

Gro

wth

Total Registered Developers (000) Q/Q Growth

Amazon Web Services

• Simple Storage Service (S3) – Provides a simple web services interface that can be used to store (for as low as $0.12 per GB per mo.) / retrieve any amount of data, at any time, from anywhere. 29B+ objects stored by the end of CQ3, +32% Q/Q.

• Elastic Compute Cloud (EC2) – Provides resizable compute capacity in the cloud, with users paying only for capacity they actually use (starting $0.10 / instance-hour).

Source: Amazon.

105

Closing Thoughts

1) Companies with cogent business models that provide consumer value should survive / thrive – consumers need

value more than they have needed it in a long time

HugeMarket

Simple, FocusedMission

Active, MissionaryFounders

GreatManagement

Team,Culture

ConstantImprovement

InsaneCustomer

Focus

BigGross

Margin (1)

Annuity-Like

ModelStrongBoard

X

X

X

X

XX

X