Embed Size (px)

Citation preview

Serious Illness Cover BoosterEven more help coping with the long-term effects of some serious illnesses

For Advisers

2

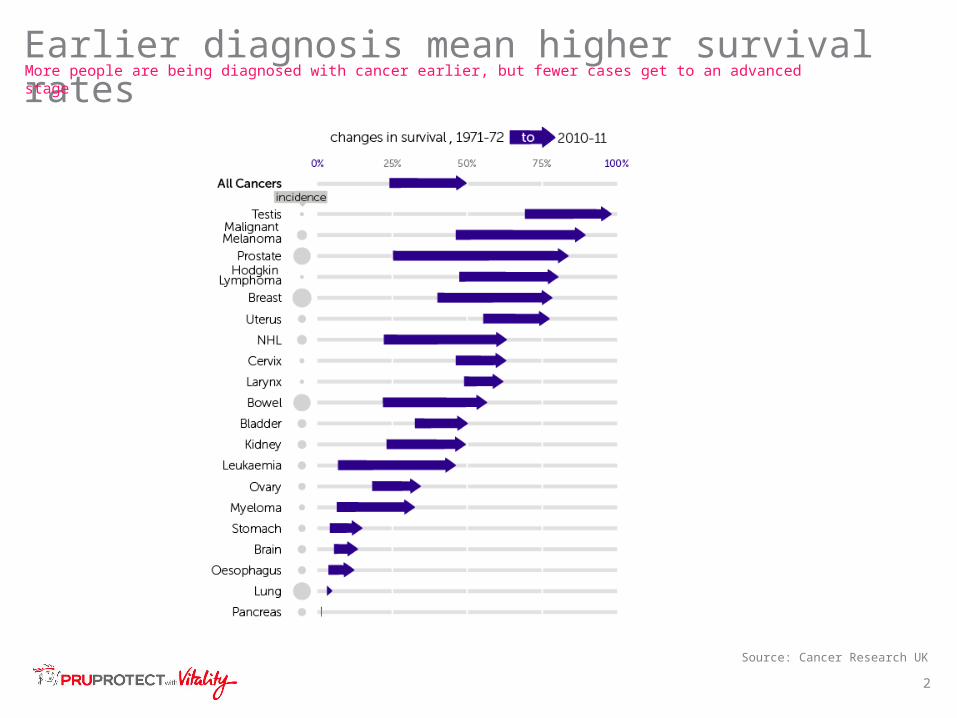

Earlier diagnosis mean higher survival ratesMore people are being diagnosed with cancer earlier, but fewer cases get to an advanced stage

Source: Cancer Research UK

3

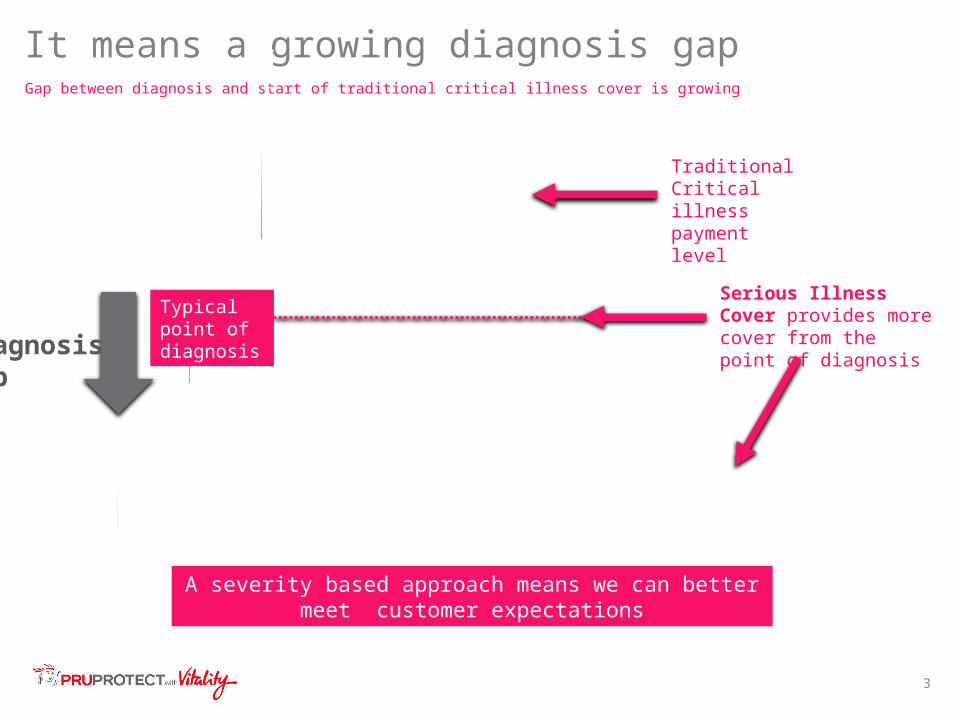

It means a growing diagnosis gapGap between diagnosis and start of traditional critical illness cover is growing

Critical

Severe

Chronic

Dia

gn

os

is g

ap

A severity based approach means we can better meet customer expectations

Traditional Critical illness payment level

Typical point of diagnosis

Serious Illness Cover provides more cover from the point of diagnosis

4

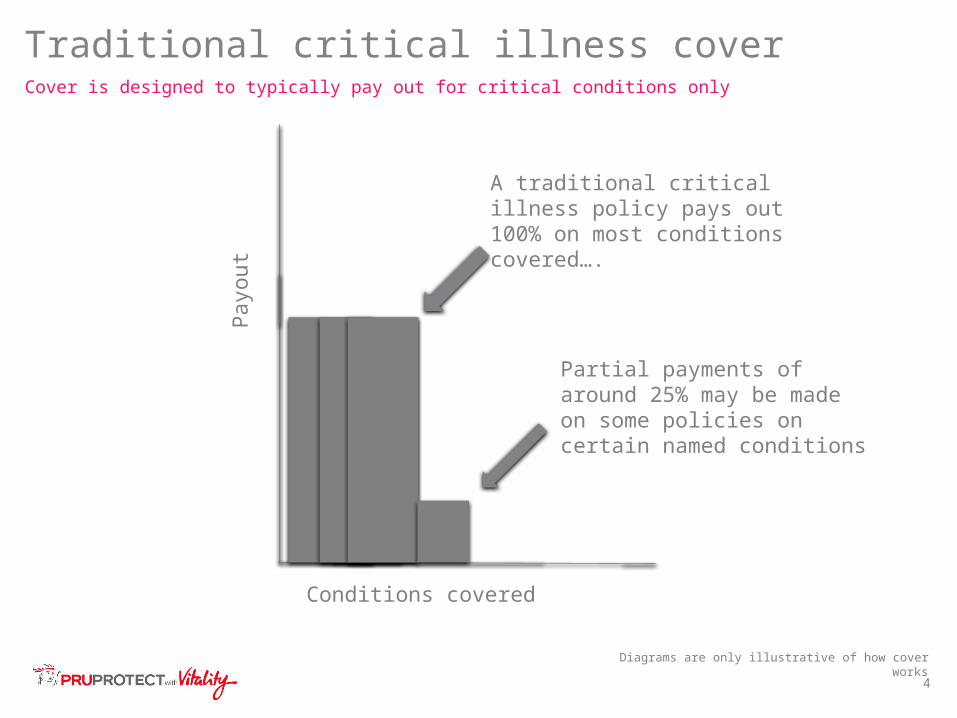

Traditional critical illness coverCover is designed to typically pay out for critical conditions only

Pay

out

Conditions covered

A traditional critical illness policy pays out 100% on most conditions covered….

Diagrams are only illustrative of how cover works

Partial payments of around 25% may be made on some policies on certain named conditions

5

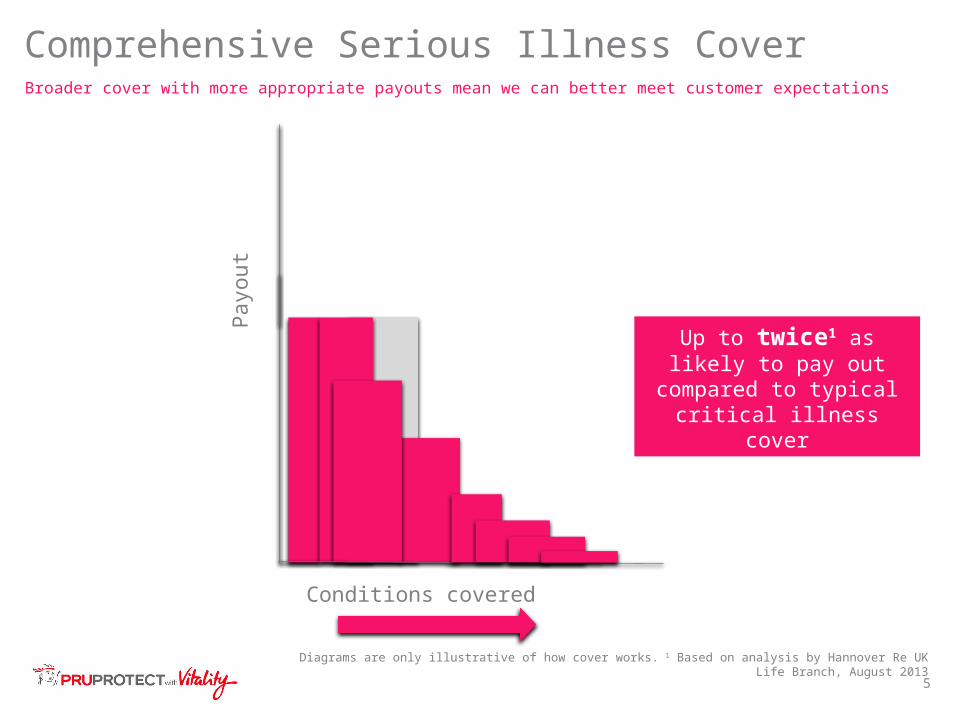

Comprehensive Serious Illness CoverBroader cover with more appropriate payouts mean we can better meet customer expectations

Pay

out

Conditions covered

Up to twice1 as likely to pay out compared to typical

critical illness cover

Diagrams are only illustrative of how cover works. 1 Based on analysis by Hannover Re UK Life Branch, August 2013

6

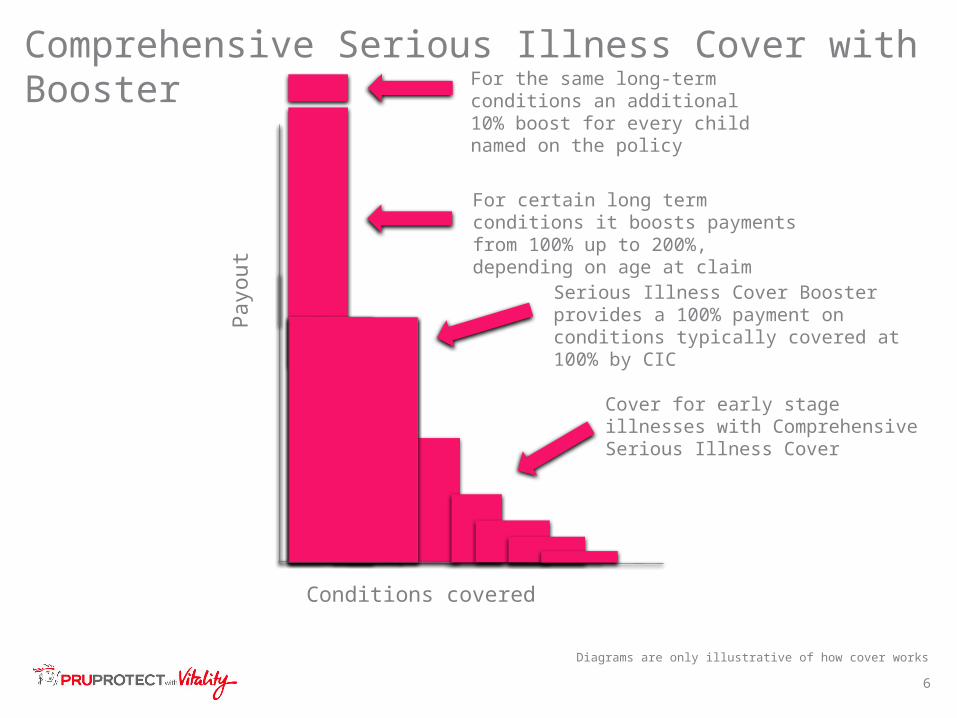

Comprehensive Serious Illness Cover with Booster

Pay

out

Conditions covered

Serious Illness Cover Booster provides a 100% payment on conditions typically covered at 100% by CIC

For certain long term conditions it boosts payments from 100% up to 200%, depending on age at claim

For the same long-term conditions an additional 10% boost for every child named on the policy

Cover for early stage illnesses with Comprehensive Serious Illness Cover

Diagrams are only illustrative of how cover works

7

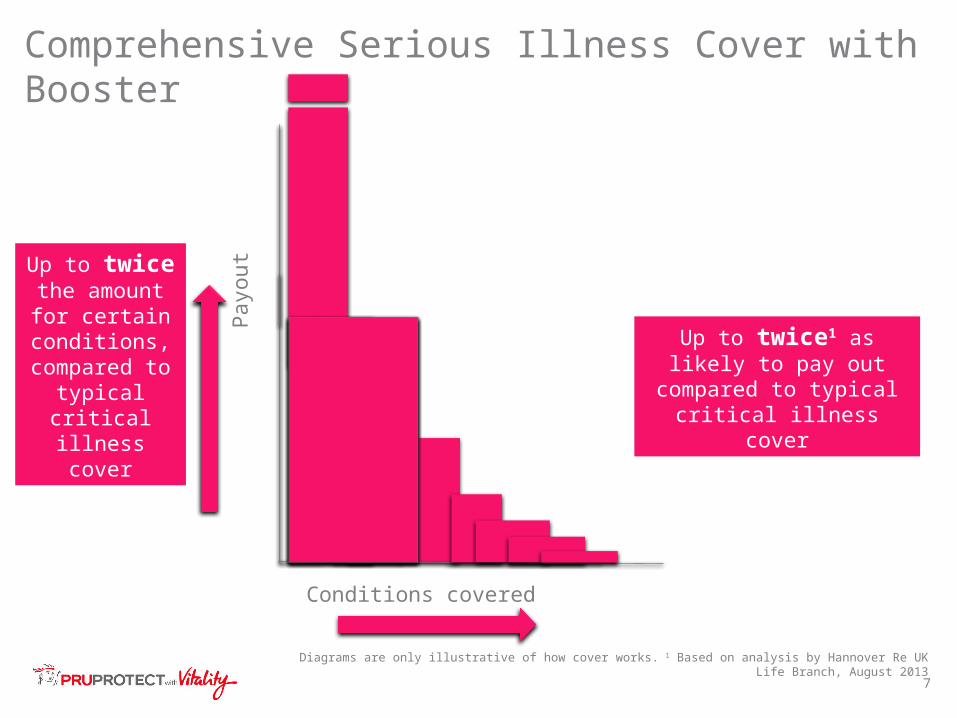

Comprehensive Serious Illness Cover with Booster

Pay

out

Conditions covered

Up to twice the amount for

certain conditions,

compared to typical critical illness cover

Diagrams are only illustrative of how cover works. 1 Based on analysis by Hannover Re UK Life Branch, August 2013

Up to twice1 as likely to pay out compared to typical

critical illness cover

8

Drag picture to placeholder or click icon to add

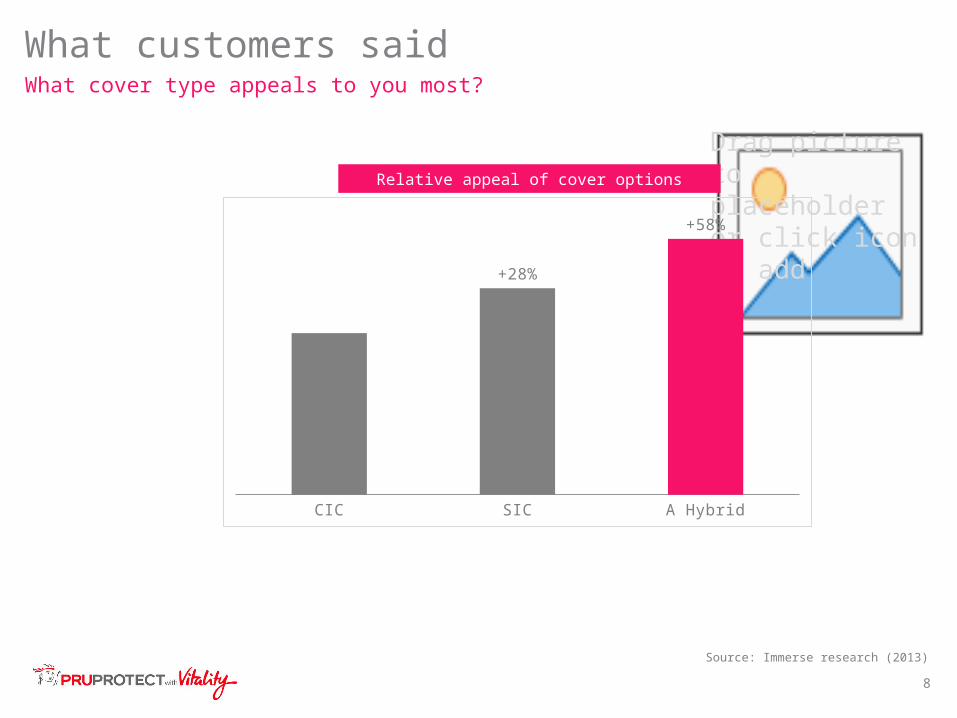

What customers saidWhat cover type appeals to you most?

CIC SIC A Hybrid

+28%

+58%

Relative appeal of cover options

Source: Immerse research (2013)

9

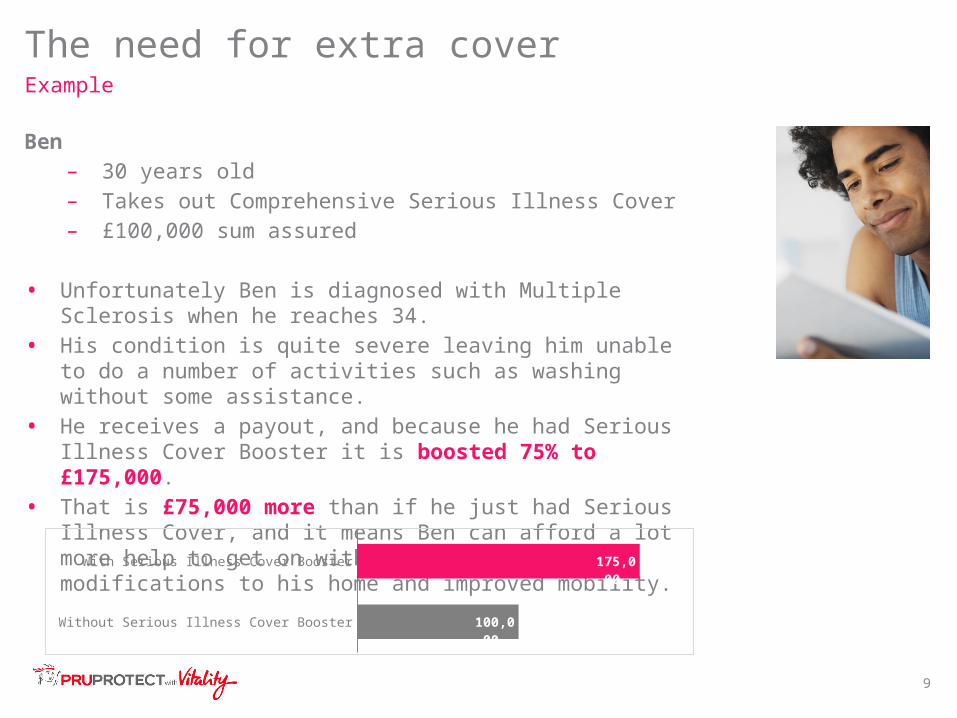

Ben– 30 years old – Takes out Comprehensive Serious Illness Cover – £100,000 sum assured

• Unfortunately Ben is diagnosed with Multiple Sclerosis when he reaches 34.

• His condition is quite severe leaving him unable to do a number of activities such as washing without some assistance.

• He receives a payout, and because he had Serious Illness Cover Booster it is boosted 75% to £175,000.

• That is £75,000 more than if he just had Serious Illness Cover, and it means Ben can afford a lot more help to get on with life including modifications to his home and improved mobility.

The need for extra coverExample

Without Serious Illness Cover Booster

With Serious Illness Cover Booster

100,00

0

175,00

0

10

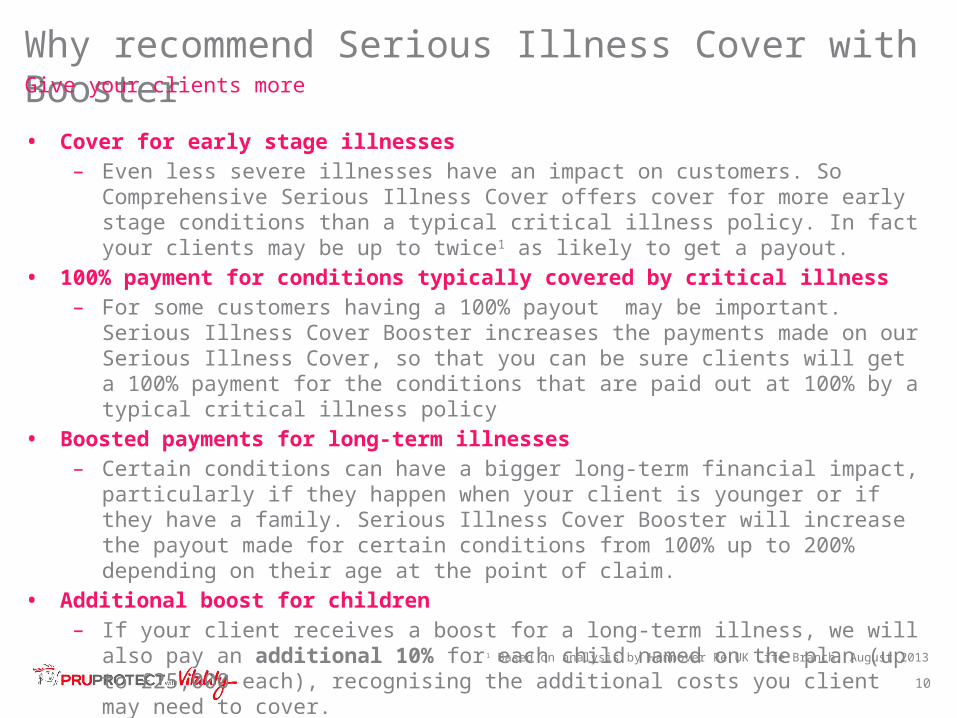

Why recommend Serious Illness Cover with BoosterGive your clients more

• Cover for early stage illnesses– Even less severe illnesses have an impact on customers. So Comprehensive Serious

Illness Cover offers cover for more early stage conditions than a typical critical illness policy. In fact your clients may be up to twice1 as likely to get a payout.

• 100% payment for conditions typically covered by critical illness – For some customers having a 100% payout may be important. Serious Illness Cover

Booster increases the payments made on our Serious Illness Cover, so that you can be sure clients will get a 100% payment for the conditions that are paid out at 100% by a typical critical illness policy

• Boosted payments for long-term illnesses– Certain conditions can have a bigger long-term financial impact, particularly if they

happen when your client is younger or if they have a family. Serious Illness Cover Booster will increase the payout made for certain conditions from 100% up to 200% depending on their age at the point of claim.

• Additional boost for children– If your client receives a boost for a long-term illness, we will also pay an additional

10% for each child named on the plan (up to £25,000 each), recognising the additional costs you client may need to cover.

1 Based on analysis by Hannover Re UK Life Branch, August 2013

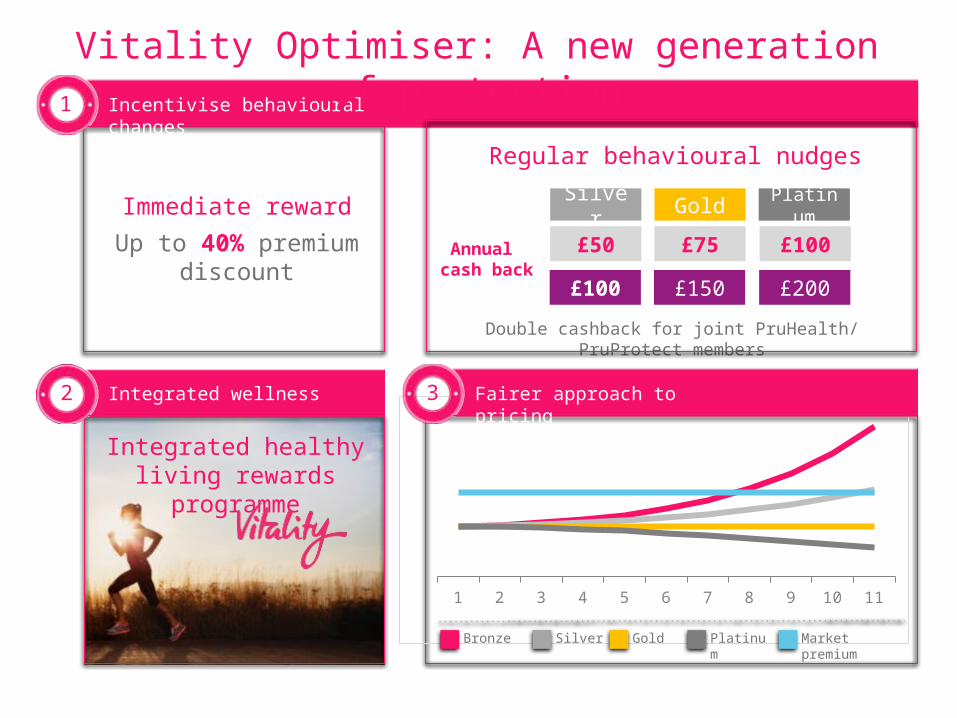

Vitality OptimiserA new generation of protection

1 2 3 4 5 6 7 8 9 10 11

Regular behavioural nudges

Double cashback for joint PruHealth/ PruProtect members

Annual cash back

PlatinumGoldSilver

£50 £75 £100

£100 £150 £200

Incentivise behavioural changes1

Integrated wellness2

Immediate reward

Up to 40% premium discount

Integrated healthy living rewards programme

Fairer approach to pricing3

Bronze Silver Gold Platinum Market premium

Vitality Optimiser: A new generation of protection

13

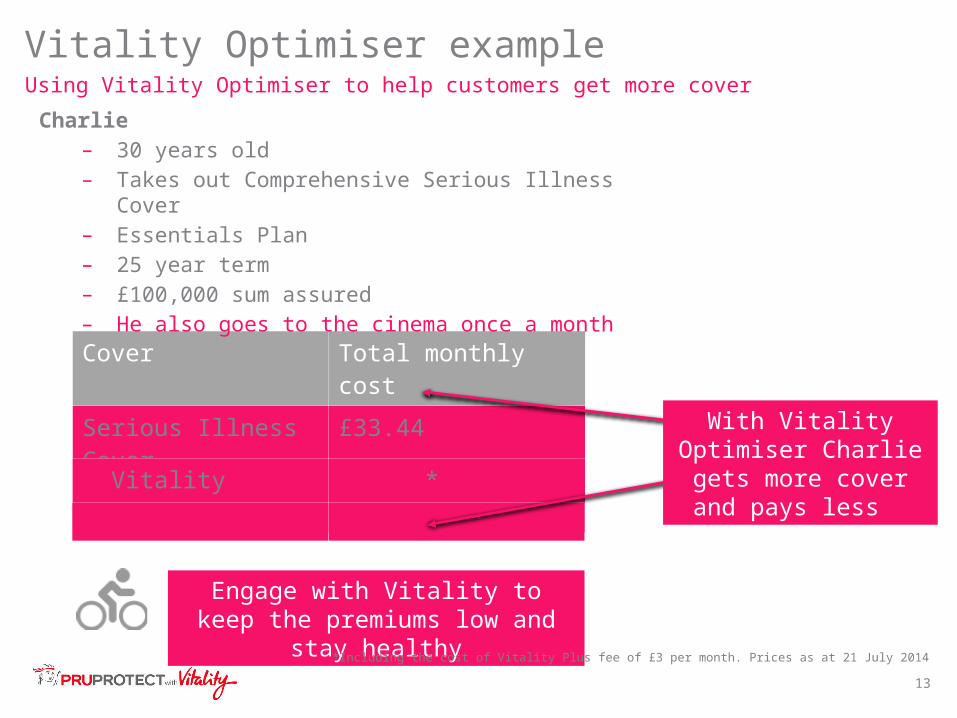

Cover Total monthly cost

Serious Illness Cover £33.44

+ SIC Booster £36.23

Vitality Optimiser exampleUsing Vitality Optimiser to help customers get more cover

+ Vitality Optimiser £33.79*

Engage with Vitality to keep the premiums low and stay healthy

A cinema ticket £23.79

*Including the cost of Vitality Plus fee of £3 per month. Prices as at 21 July 2014

With Vitality Optimiser Charlie gets more cover

and pays less

Charlie– 30 years old – Takes out Comprehensive Serious Illness Cover– Essentials Plan– 25 year term – £100,000 sum assured – He also goes to the cinema once a month

Serious Illness Cover Booster - Appendix For Advisers

15

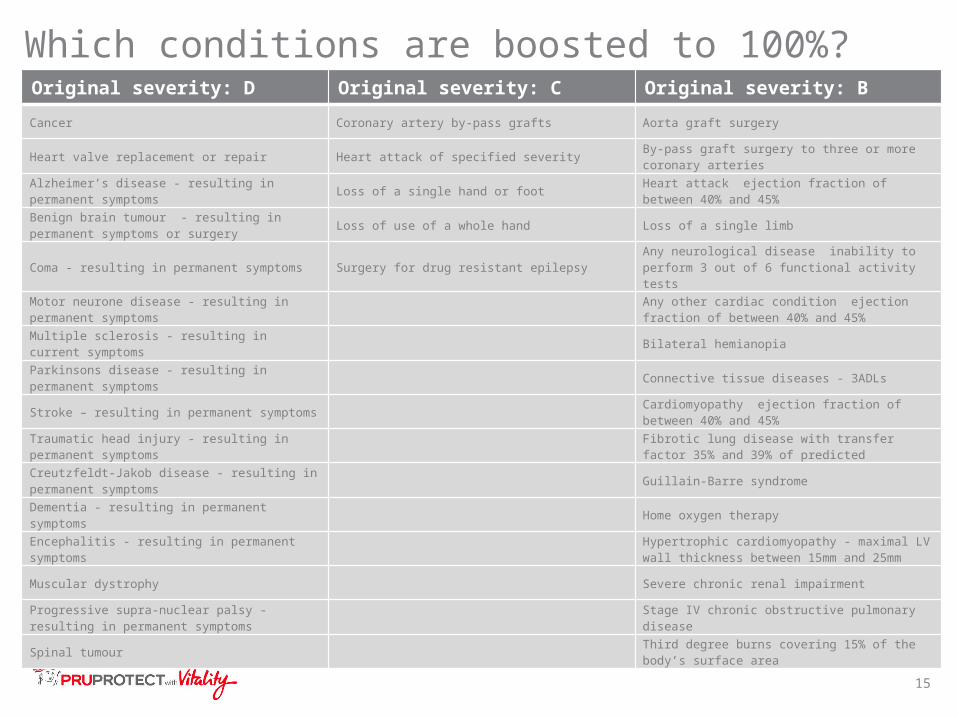

Original severity: D Original severity: C Original severity: B

Cancer Coronary artery by-pass grafts Aorta graft surgery

Heart valve replacement or repair Heart attack of specified severityBy-pass graft surgery to three or more coronary arteries

Alzheimer’s disease - resulting in permanent symptoms

Loss of a single hand or footHeart attack ejection fraction of between 40% and 45%

Benign brain tumour - resulting in permanent symptoms or surgery

Loss of use of a whole hand Loss of a single limb

Coma - resulting in permanent symptoms Surgery for drug resistant epilepsy Any neurological disease inability to perform 3 out of 6 functional activity tests

Motor neurone disease - resulting in permanent symptoms

Any other cardiac condition ejection fraction of between 40% and 45%

Multiple sclerosis - resulting in current symptoms Bilateral hemianopia

Parkinsons disease - resulting in permanent symptoms

Connective tissue diseases - 3ADLs

Stroke – resulting in permanent symptoms Cardiomyopathy ejection fraction of between 40% and 45%

Traumatic head injury - resulting in permanent symptoms

Fibrotic lung disease with transfer factor 35% and 39% of predicted

Creutzfeldt-Jakob disease - resulting in permanent symptoms

Guillain-Barre syndrome

Dementia - resulting in permanent symptoms Home oxygen therapy

Encephalitis - resulting in permanent symptomsHypertrophic cardiomyopathy - maximal LV wall thickness between 15mm and 25mm

Muscular dystrophy Severe chronic renal impairment

Progressive supra-nuclear palsy - resulting in permanent symptoms

Stage IV chronic obstructive pulmonary disease

Spinal tumourThird degree burns covering 15% of the body’s surface area

Which conditions are boosted to 100%?

16

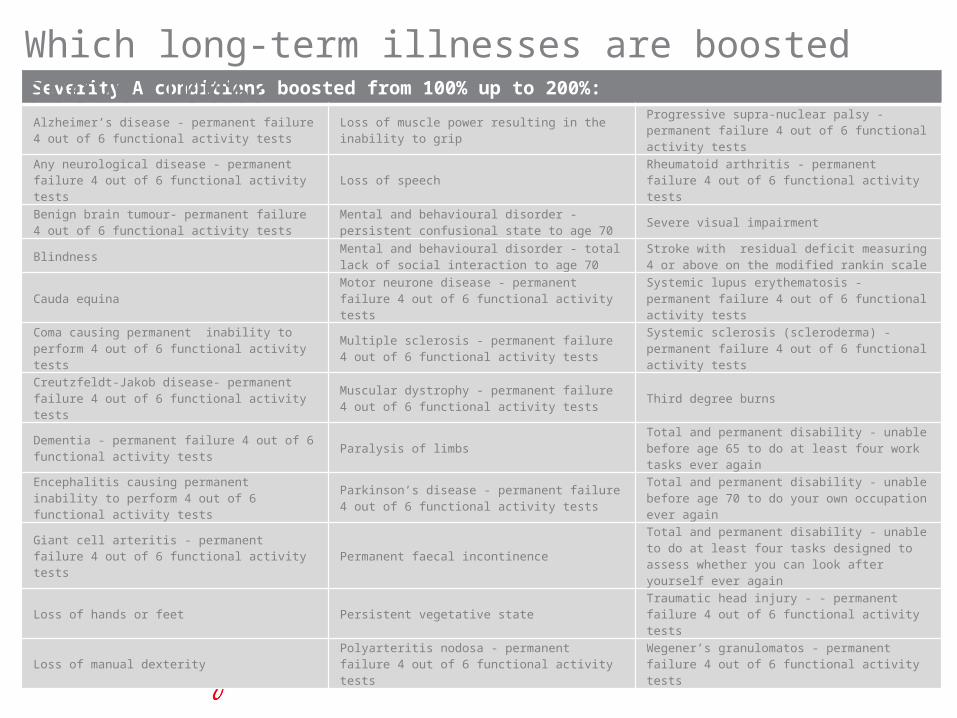

Severity A conditions boosted from 100% up to 200%:

Alzheimer’s disease - permanent failure 4 out of 6 functional activity tests

Loss of muscle power resulting in the inability to gripProgressive supra-nuclear palsy - permanent failure 4 out of 6 functional activity tests

Any neurological disease - permanent failure 4 out of 6 functional activity tests

Loss of speech Rheumatoid arthritis - permanent failure 4 out of 6 functional activity tests

Benign brain tumour- permanent failure 4 out of 6 functional activity tests

Mental and behavioural disorder - persistent confusional state to age 70

Severe visual impairment

BlindnessMental and behavioural disorder - total lack of social interaction to age 70

Stroke with residual deficit measuring 4 or above on the modified rankin scale

Cauda equinaMotor neurone disease - permanent failure 4 out of 6 functional activity tests

Systemic lupus erythematosis - permanent failure 4 out of 6 functional activity tests

Coma causing permanent inability to perform 4 out of 6 functional activity tests

Multiple sclerosis - permanent failure 4 out of 6 functional activity tests

Systemic sclerosis (scleroderma) - permanent failure 4 out of 6 functional activity tests

Creutzfeldt-Jakob disease- permanent failure 4 out of 6 functional activity tests

Muscular dystrophy - permanent failure 4 out of 6 functional activity tests

Third degree burns

Dementia - permanent failure 4 out of 6 functional activity tests

Paralysis of limbs Total and permanent disability - unable before age 65 to do at least four work tasks ever again

Encephalitis causing permanent inability to perform 4 out of 6 functional activity tests

Parkinson’s disease - permanent failure 4 out of 6 functional activity tests

Total and permanent disability - unable before age 70 to do your own occupation ever again

Giant cell arteritis - permanent failure 4 out of 6 functional activity tests

Permanent faecal incontinence Total and permanent disability - unable to do at least four tasks designed to assess whether you can look after yourself ever again

Loss of hands or feet Persistent vegetative stateTraumatic head injury - - permanent failure 4 out of 6 functional activity tests

Loss of manual dexterityPolyarteritis nodosa - permanent failure 4 out of 6 functional activity tests

Wegener’s granulomatos - permanent failure 4 out of 6 functional activity tests

Which long-term illnesses are boosted above 100%?

17

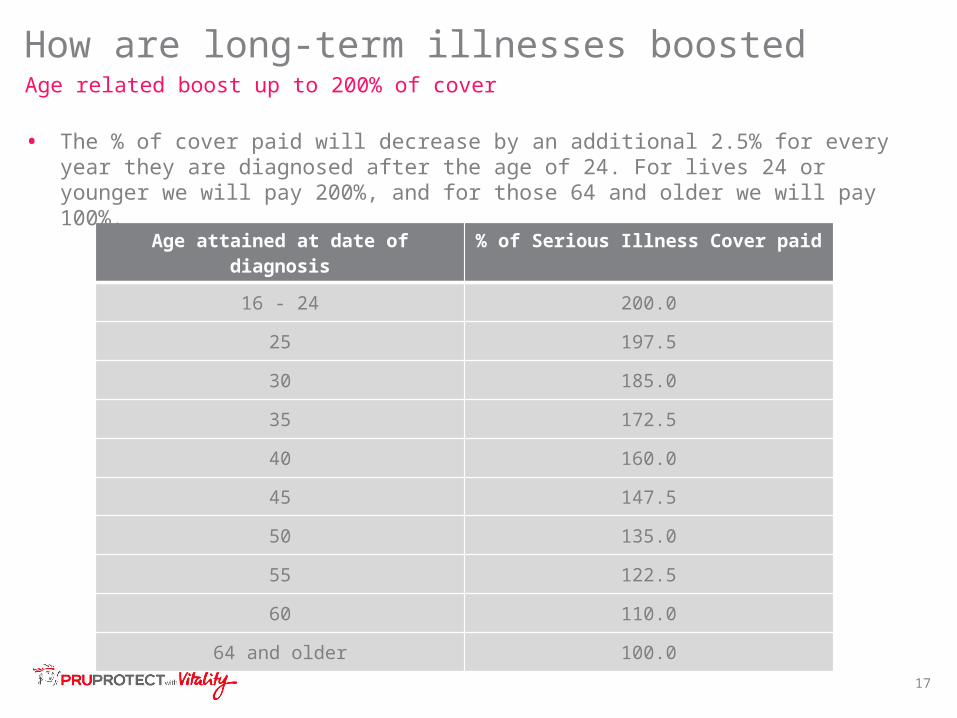

How are long-term illnesses boostedAge related boost up to 200% of cover

Age attained at date of diagnosis % of Serious Illness Cover paid

16 - 24 200.0

25 197.5

30 185.0

35 172.5

40 160.0

45 147.5

50 135.0

55 122.5

60 110.0

64 and older 100.0

• The % of cover paid will decrease by an additional 2.5% for every year they are diagnosed after the age of 24. For lives 24 or younger we will pay 200%, and for those 64 and older we will pay 100%.