Embed Size (px)

Citation preview

Mogul Ventures Corp. OORTSOG OVOO TIN PROJECT

Q2, 2014

2

THE FOLLOWING INFORMATION may contain forward–looking statements. Forward

looking statements address future events and conditions and therefore involve

inherent risks and uncertainties. Actual results may differ materially from those

currently anticipated in such statement. Forward-looking information is subject to

known and unknown risks, uncertainties and other factors that may cause Mogul

Venture Corp’s actual results, level of activity, performance or achievements to be

materially from those expressed or implied by such forward-looking information.

Such factors include, but are not limited to: uncertainties related to the historical

resource estimates, the work expenditure commitments; the ability to raise

sufficient capital to fund future exploration or development programs; changes in

economic condition or financial markets, regulatory, political and competitive

developments; technological or operational difficulties or an inability to obtain

permits required in connection with maintaining, or advancing projects; and labour

relation matters *All historical resource estimates quoted herein date from the 1960s and 1970s and are based on prior

data and reports obtained and prepared by previous operators and information provided by the State, using

a Russian classification system not compatible with 43-101. Insufficient data exists to compare Russian

categories to current C.I.M. categories. A qualified person has not completed sufficient work to verify the

classification of the historic mineral resources and as such they should not be considered as current

resources and they should not be relied upon. Mogul Ventures believes these historical results provide an

indication of the potential of the property and are relevant to ongoing exploration. It should also be noted

that mineral resources which are not mineral reserves do not have demonstrated economic viability as

defined by NI 43-101 guidelines.

www.mogulvc.com

3

COMPANY OVERVIEW

• Mogul Ventures Corp. focuses on

exploration, development and

production of metals and coal in

Mongolia

• The Khar Tolgoi property is a 34,055 ha

Mining License located in Dundgovi

Province

www.mogulvc.com

• The Oortsog Ovoo (OO) tin + polymetallic

project has a historic resource of 39,000 t of

contained tin with additional credits for

accompanying metals and a significant upside

potential. A substantial body of historic work exists,

augmented by Mogul’s modern exploration program

• OO appears to be one of the largest and highest

grade open-pitable tin deposits in the world. Given

sufficient financing, portions of the project can be

rapidly moved in to production within 12-18

months

Shares Outstanding 112,499,907

Warrants Outstanding 554,195

Fully Diluted 113,054,102

Options 0

Insider Ownership ~70%

Capital Structure (01.04.2014)

4

MOGUL VENTURES TEAM

STEVEN KHAN, MBA, CFA Executive Chairman & Director

Previous 20+ years of experience in all aspects of the investment industry including executive positions with regional and

national full-service Canadian investment brokerage houses. Focused on strategic corporate and business development as

well as resource and venture capital financing during the last decade. Holds Director and Executive Officer roles in a

number of public and private resource companies. Successfully completed major corporate development initiatives both

domestically and internationally including in Japan, Korea and China

www.mogulvc.com

JAMUL JADAMBA , MBA CEO, President & Director

Formerly a natural resource and mining-focused investment banker with an extensive capital raising background,

servicing worldwide companies, especially in Mongolia. Former Director and co-founder of the Metals & Mining Group at

Rodman & Renshaw LLC. Native Mongolian with well-established relationships with influential business and government

leaders in Mongolia. Extensively writes and speaks on topics of Mongolian economy, development and politics for

organizations such as Oxford Analytica, Institutional Investor and Business New Europe. He holds a B.S. in Business

Administration from Northeastern University and M.B.A from N.Y.U.-Stern School of Business

5

MOGUL VENTURES TEAM

DAVID A. TERRY, Ph.D., P.Geo. Senior Technical Advisor

Over 20 years of business experience in the natural resource sector, focused primarily on exploration of precious

and base metal deposits in North and South America. Director of and advisor to several publicly-listed mineral

exploration companies. Specializes in public company management, strategic planning, finance, advanced project

evaluation, identification and acquisition of opportunities, design and implementation of effective and cost-efficient

exploration programs. Held positions with a number of senior mining companies including Boliden Limited, Westmin

Resources Limited, Hemlo Gold Mines Inc., Cominco Limited and Gold Fields Mining Corporation.

www.mogulvc.com

PUJI JADAMBA Country Manager

Over twenty years of experience running various entrepreneurial ventures in Mongolia including natural resources, real estate, cashmere, agriculture and import/export. Was a key principal at the first commercial gold mining company in Mongolia. Extensive local network of business and government contacts and unsurpassed ability to execute locally.

HENRY PARK, MBA Director

A highly experienced commodity strategist and investor with a background among some of the world’s most elite

investment firms, Henry brings a depth of knowledge and an impressive network of contacts within the resource

sector. Henry was most recently the Managing Director and Commodity Strategist at Electrum Group, a US based

mining private equity firm. Prior to Electrum, he held the same position at Soros Fund Management where he

oversaw commodity investing in equities and futures. Henry started his career at GE Capital where he was Assistant

Vice President in the distressed debt business, followed by Long/Short equity analyst in basic materials sector for

Wingspan platform of Ospraie Fund Management. He holds a B.A. in Economics from University of Chicago and

M.B.A. from Columbia University.

6

MONGOLIA OVERVIEW

• Recognized as the home of some of the world’s largest natural resource deposits

including coal, gold and copper

• Strategic location

• Next door to the biggest consumer of commodities in the world – China

• Friendly relations and no border disputes with both of its neighbors – Russia and

China

• Mining is the most important sector:

• “Contributes 30% of GDP and 70% of exports”(1)

• Favorable political environment:

• Mongolian Government focused on the long-term development of resource-related

sectors and favorable policies towards business and foreign investments

• Stable business-friendly democracy:

• 20+ year history of uninterrupted peaceful and democratic government

• Homogenous country with minimal risk of ethnic or religious conflict

www.mogulvc.com

Source: (1) the Ministry of Mineral Resources & Energy of Mongolia

7

MONGOLIA: MINING INDUSTRY OVERVIEW

• Investment Capacity of Mongolia’s

mining industry (5 years): $25 - $30B(1)

• 6,000 known mineral occurrences(2)

• 80+mineral deposits found recognized

as economic by the Mineral Resources

Authority of Mongolia(3)

www.mogulvc.com

Mongolia is poised to become one of the fastest growing

economies in the world in the next two decades

Sources:

(1) How much capex the country can absorb given known development projects. Statement made by the former Prime Minister Bayar

(2), (3) The World Bank report on “Mongolian Mining Sector: Managing the Future”

8

TIN MARKET OVERVIEW

• As growth in electronics manufacturing shifted from the West to the East, Asia has emerged

as the leading consumer of Tin

• Not surprisingly, China is both its biggest producer and consumer

www.mogulvc.com

According to LME, Tin (Sn) is the only industrial metal with ongoing

physical supply deficits for 2014

9

TIN USAGE

• Over 50% of Tin is used as a solder.

Emergence of lead-free solders has

boosted demand

• Tinplate’s share (tin coated steel, such as

in cans and containers) has come down

significantly

• There is an increasing trend of tin usage

for various chemical and industrial

applications such as:

• Stabilizer for PVC plastics

• Lithium-ion batteries

• Cutting-edge technologies such as

carbon nanotubes and graphene

• Solar cells, acid batteries and electric

car batteries

• Various chemical catalysts

www.mogulvc.com

Tin Usage

Source: ITRI

10

TIN PRODUCTION

• Most of Tin production is from underground mines. Estimated cash costs for a typical underground mine with 1% grade is ~$20,000/t1

• Open pit production is in a small minority, but has advantage as estimated cash costs at 1% grade are under $10,000/t1

• 10% of world mine production comes from the San Rafael underground mine in Peru (owned by Minsur) which is slated to run out of ore within 3 years2. Small and artisanal mines, which account for ~100ktpa of global mine supply, are being closed as well

• Top ten producers have experienced production volume declines in 2012 and 20133

• Indonesia, which supplies 40% of globally mined tin, has tightened regulations requiring tin ingots to trade on ICDX and introducing a floor price4

www.mogulvc.com

Top Ten Producers in 2012 and 2013

Source: (1) Greenfields Research (2) Minsur (3) ITRI (4) Indonesian Tin Association

(t) % change (t) % change

1 Yunnan Tin (China) 56,174 69,760 24% 70,383 0.89%

2 Malaysia Smelting Corporation 40,267 37,792 -6% 32,668 -13.56%

3 Minsur (Peru) 30,162 24,822 -18% 24,397 -1.71%

4 PT Timah (Indonesia) 38,132 29,512 -23% 23,718 -19.63%

5 Thaisarco (Thailand) 23,864 22,847 -4% 22,986 0.61%

6 Yunnan Chengfeng (China) 15,430 16,600 8% 18,300 10.24%

7 Guangxi China Tin (China) 15,517 14,034 -10% 11,870 -15.42%

8 EM Vinto (Bolivia) 10,960 11,241 3% 11,253 0.11%

9 Metallo Chimique (Belgium) 10,007 11,350 13% 10,344 -8.86%

10 Gejiu Zi-Li (China) 8,600 7,000 -19% 6,000 -14.29%

Total 249,113 244,958 -2% 231,919 -5.32%

2013

RankingCompany

2011

(t)

2012 2013

11

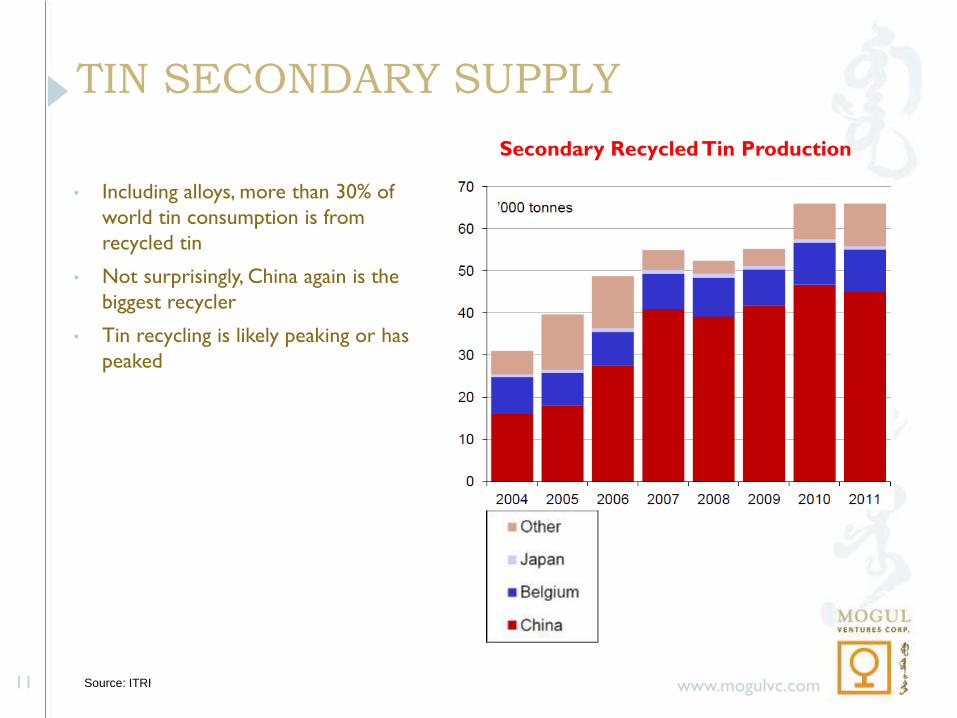

TIN SECONDARY SUPPLY

• Including alloys, more than 30% of

world tin consumption is from

recycled tin

• Not surprisingly, China again is the

biggest recycler

• Tin recycling is likely peaking or has

peaked

www.mogulvc.com

Secondary Recycled Tin Production

Source: ITRI

12

TIN MARKET

• In early 2011, Tin prices hit a high of over $32,000/t

• For new mine supplies to materialize, prices are likely to hold or stay above current levels of

about $23,000/t

www.mogulvc.com

Actual and Inflation-Adjusted Prices Historic and Forecasted Demand

Source: ITRI

13

LARGEST UNDEVELOPED TIN DEPOSITS

www.mogulvc.com

Source: SNL Metals Economics Group, Company websites, Mogul Ventures Corp.

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Co

nta

ined

Sn

(m

t)

Gra

de

(%

)

1.2

1.0

0.8

0.6

0.4

0.2

Xit

ian

Pra

vou

rmiis

koye

Cat

avi T

ailin

gs

Ach

mm

ach

Mo

un

t Li

nd

say

Ko

khsh

etau

Ren

tails

Hee

msk

irk

Ton

gkah

Mo

un

t G

arn

et

Mo

un

t P

leas

ant

Oro

pes

a

Nar

siin

Kh

un

dle

n

Oo

rtso

g O

voo

Blu

e Ti

er

Jean

nie

Riv

er

Open Pit UG Tailings Dredge Placer

14

PUBLIC COMPARABLES

• Mogul’s Oortsog Ovoo is one of the top near-development tin projects in the world

• Oortsog Ovoo has one of the best grades among known potential open pit mines, further

improved by likely credits for accompanying metals

www.mogulvc.com

Source: Company websites

Company Project Location Main Mineral Resources Grade

Mkt Cap

(4/15/14)

Proposed

Mining Method

Economic

Interest

Kasbah Resources Kasbah Morocco Tin 135,000 t1 0.90% $44M UG 100%

Gillian 23,393 0.65%

Pinnacles 21,105 0.30%

Deadmans Gully 1,510 0.34%

Windermere 5,508 0.27%

TOTAL 2 51,516 0.46%

Stellar Resources Heemskirk Australia Tin 71,500 t3 1.14% $11M UG 100%

Mogul Ventures Oortsog Ovoo Mongolia Tin 39,200 t4 0.65%5 N/A Open Pit 100%

Venture Minerals Mt. Lindsay Australia Tin/Tungsten 81,000 t6 0.20%6 $26M Open Pit 100%

1 JORC compliant resources: Inferred 93,000 t, Indicated 42,000 t

2 JORC compliant resource, included Indicated and Inferred

3 JORC compliant resource, included Indicated and Inferred

4 Historic resource based on 41 drill holes and 207 trenches. Does not include credits for other metals present such as Cu, Pb, Zn, Ag, Au, Bi, Ca and Fe

5 Grade doesn't account for other metals credit

6 JORC compliant resource, only credits Sn, Sn-equivalent average grade would be 0.40%

Consolidated Tin Mines Australia Tin $17M Open Pit 50%

15

OORTSOG OVOO DEPOSIT

• Cassiterite (Sn) skarn system with Zn-Pb-Cu-Fe-

W-Ag-In

• Twenty four ore bodies have been identified and

studied to varying extents

• A NI 43-101 Technical Report by APEX

Geoscience Ltd. under way

• Historic exploration focused on Sn provided

following results:

• Historic Resources totalling 39,237 t Sn

Metal reported*, making Oortsog Ovoo an

overall top 20 deposit in the world1

• ~6.7 Mt @ an average grade of 0.65% Sn, with

no credits for other metals present

• The deposit was proposed to be mined via 5

open pits to a maximum depth of 150m, with

average stripping ratio of 4:1

• Low Sulphide Sn-dominant (0.25 to 1.13% Sn)

and High Sulphide Zn-Pb-Cu-Fe-Ag-In zones

delineated

*Historical resources - see note on Page 2 of Presentation (1) Based on resource size ranking by ITRI

Photo: Crystalline Cassiterite from Oortsog Ovoo

16

OORTSOG OVOO DEPOSIT

• A significant historical body of exploration

work exists on Oortsog Ovoo

• 41 holes were drilled on the three zones

depicted

• A significant trenching program of 207

trenches was also conducted

• Rock chip samples taken by Mogul also had

high grades of copper ranging as high as

1.5%, 3% and over 6%

• A total of eight mineralized zones have

been identified, three of which have had a

significant amount of exploration work

• There is excellent potential for expanding

resources through exploring the zones

that have not seen limited work to date as

well as areas in between zones

17

GROUND MAGNETICS PROGRAM

1km

1km

North Zone

Middle Zone

Central Zone

Eastern Zone

South-Eastern

Zone

Magnetic

Intrusive? • The Vertical Gradient image above shows a

strong linear dipole anomaly is associated with

the three main segments which comprise the

Northern Zone, which has been delineated to

date by trenching and drilling over 1.2km of

strike length.

0.5km

• The Company contracted a detailed ground magnetic survey in June, 2013 covering a 3.5km

by 4km area.

• The RTP results (above) shows a significant number of magnetic anomalies were detected;

many anomalies correlate with known zones while some require follow-up.

18

2013 WORK PROGRAMS • Mogul conducted a 1,500 meter confirmation drill program

in October of 2013

• The program focused only on the Eastern zone and a

segment of the Northern zone of the system. These areas

had the most detailed historical exploration with the

resulting potential for rapid resource

confirmation/delineation and near-term development

• The program’s main objectives were:

• Parallel drill (twin) select historic holes to confirm and

correlate accuracy of historic work

• Drill vertical and horizontal step out holes to delineate

mineralized zones in detail

• Conduct modern assays based on a +90% core

recovery rates, which were achieved. This may result in

an upside in tin grades compared to the historically

reported resource average of 0.65% Sn

• Improve the overall geological understanding of the

deposits

• Subsequent to this program, we believe that either the

Northern or Eastern zone can be targeted for rapid

exploration and development

Photo: Drill rigs at the Eastern Zone of Oortsog Ovoo, magnetite core from drilling

19

www.mogulvc.com

2013 WORK PROGRAMS • Drill core logs generally showed a good correlation in

lithology, thickness and depth of orebody intersects

where historical holes were twinned

• Core from two drill holes were assayed so far with the

following results:

• DH# 1W intersected 81.6m averaging 0.63% Sn,

with all samples >0.1%

• DH# 70Q intersected 34.7m averaging 0.55% Sn,

with all samples >0.1%

• DH# 70Q was a twin hole for historic DH# 70 and

compares favorably with the historically reported

56m averaging 0.47% Sn

• The tin mineralization is associated with magnetite

skarn with wide intervals of >20% Fe

• The program generally confirms historical work on the

sections of the deposits drilled in this program

• It served to boost our confidence in historic work and

ability to rely on it for further exploration, resource

delineation and engineering work

Northern Zone

Eastern Zone

20

GOALS AND OBJECTIVES

EXPLORATION AND FEASIBILITY WORK

• Confirm, expand and delineate resources focusing on the Northern and Eastern Zones

• Metallurgical testing

• Resource modelling and engineering work

• Develop a PFS or BFS based on the most advanced mineralized zones by end of Q1 2015

www.mogulvc.com

FAST TRACK DEVELOPMENT AND PRODUCTION

• Mogul already has a Mining License

• Pursuant to feasibility work, a small scale 500 tpd open pit operation can be built by Q4 2015

EXPANSION

• Expand production from 500 tpd to 2,000 tpd within the next 2-3 years

• Conduct additional exploration to increase resources at Oortsog Ovoo with the goal of

making it a +100 kt of contained tin project with additional credits for other metals

• Look at acquisition opportunities aimed at consolidating and growing Mongolia’s tin sector

21

TIMELINE

www.mogulvc.com

Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15

Geochemistry for Drilling Program

Planning for 2014 Work Program

PQ Diamond Drilling for Metallurgy

Blasting and Trenching - Bulk Sample for

Metallurgy

Preliminary Metallurgical Testing

NQ drillilng for Deposit Confirmation

Geophysics

Resource Modelling

Additional Metallurgy and Process Design

Mine and Site Engineering, Economic

Study

Environmental Baseline

Feasibility Study

2014 2015Item

22

COAL PROJECT

• Mogul’s license also contains a large coal system consisting of two deposits: Ovdog Hudag and Ikh Ulaan Nuur

• Ovdog Hudag has a NI 43-101 Resource Estimate and Report by SRK Consulting which found:

• Estimated Inferred Resources - 89.6 Mt* of Thermal Coal

• 8 coal seams recognized – 4 fully mineable, 2 partially

• Average Gross Calorific value – 5,636 to 6,431 kcal/kg (daf)*

• Ovdog Hudag coal deposit historical resources, based on Russian drilling from the ‘60s and ‘70s, using a Russian Classification system and based on >85 drill holes:

• 1968: C1+C2 resources totalling 201.2 Mt*1

• 1970: B+C1+C2 resources totalling 168.2 Mt*1

• Ikh Ulaan-Nuur coal deposit is located 7km NNE of Ovdog Hudag and was defined by Russian drilling in the ‘60s and ‘70s

• 1970: A+B+C1+C2 resources totalling 86.4 Mt*1

• Excellent potential for additional coal resources to be delineated in the undrilled area between Ovdog Hudag and Ikh Ulaan-Nuur

• Open pit accessible coal resources with expected low strip ratio

* Ovdog Hudag Coal Deposit – NI43-101 Report by SRK Consulting, June 30, 2012 *1 SRK Consulting External Technical memo, May 28, 2011; “Technical Report on the Coal Resources of the

Ovdog Hudag Coal Deposit Dundgovi Province, Mongolia” prepared by Flora Tungalag

www.mogulvc.com

Contact Information Jamul Jadamba, CEO & President

+1 416.915.4202 | [email protected]

Suite 5700 – 100 Kings St. West

Toronto, Ontario

M5X 1C7, Canada